Embed Size (px)

Citation preview

Presentation of Results for the year ended 31st March 2000

8th June 2000

Johnson MattheyJohnson Matthey

Johnson Matthey

OverviewOverview

Continuing businesses’ profits up 17% EMD sold for US$655 million Profit before tax up 10% to £143.8 million Double digit growth in all three divisions Earnings and dividend up 7%

StrategyStrategy

Strategy successfully implemented Investment for growth Fuel Cells Refocusing Colours & Coatings

Johnson Matthey

Summary ResultsSummary Results2000 1999

£m £m %

Turnover – Continuing 3,769 2,963 +27

Op. Profit – Continuing 146.5 125.0 +17

– Discontinued (0.3) 22.1

Interest (2.4) (15.9)

Profit before tax* 143.8 131.2 +10

EPS* 47.5p 44.3p +7

EPS 51.4p 49.3p +4

Dividend 20.3p 19.0p +7

* Excluding exceptionals

Operating Profit ContinuingOperating Profit Continuing

2000 1999 2000 at 1999 rates

£m £m % £m %

Catalysts & Chemicals 84.8 74.2 +14 83.6 +13

Precious Metals 45.4 37.3 +22 44.9 +20

Colours & Coatings 27.9 25.1 +11 29.2 +16

Corporate (11.6) (11.6) (11.5)

146.5 125.0 +17 146.2 +17

Return on SalesReturn on Sales

Sales ROS

2000 1999 Growth 2000 1999

£m £m % % %

Catalysts & Chemicals 856 677 +26 9.9 11.0

Precious Metals 2,672 2,041 +31 1.7 1.8

Colours & Coatings 241 244 -1 11.6 10.3

3,769 2,963 +27 3.9 4.2

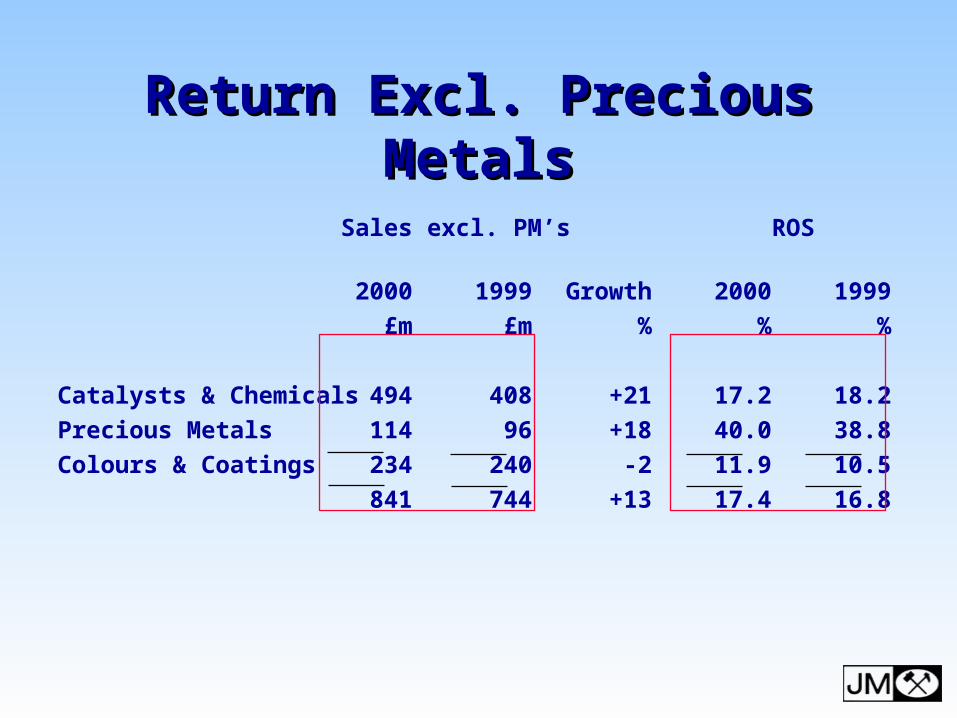

Return Excl. Precious MetalsReturn Excl. Precious Metals

Sales excl. PM’s ROS

2000 1999 Growth 2000 1999

£m £m % % %

Catalysts & Chemicals 494 408 +21 17.2 18.2

Precious Metals 114 96 +18 40.0 38.8

Colours & Coatings 234 240 -2 11.9 10.5

841 744 +13 17.4 16.8

1999£125.0m

58.1

54.1

9.2

3.6

2000£146.5m

52.2

69.3

16.2

8.8

Europe

Rest of World

Asia

North America

Geographical SplitGeographical SplitOperating Profit - Continuing

InterestInterest

2000 2000 2000 1999

1H 2H

£m £m £m £m

Financial (4.1) 3.9 (0.2) (14.6)

Gold & Silver leases (1.1) (1.1) (2.2) (1.3)

(5.2) 2.8 (2.4) (15.9)

Full Year

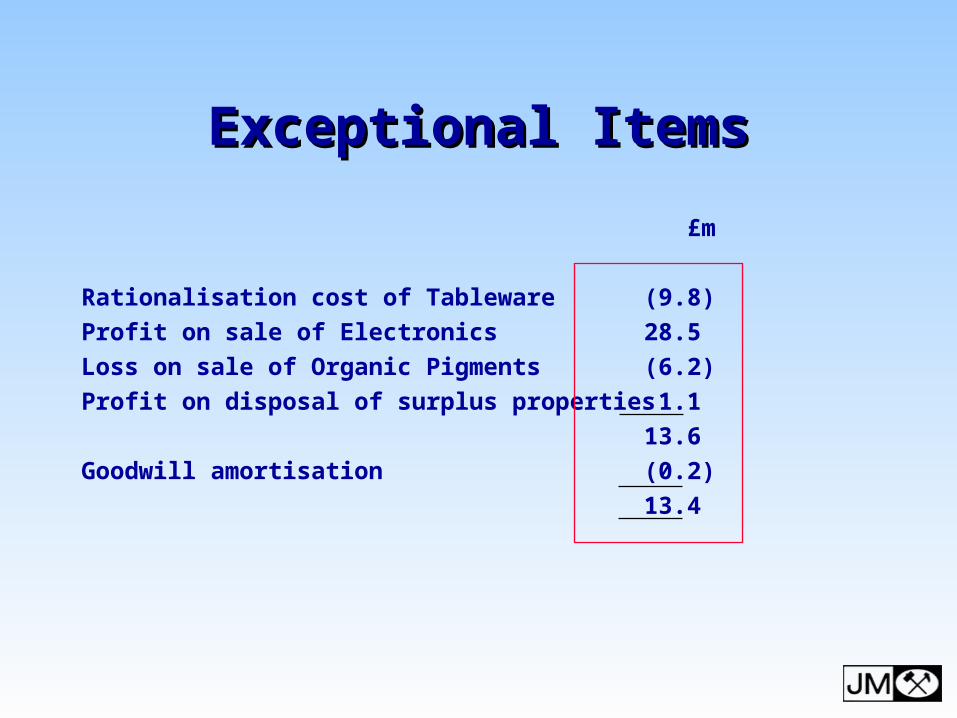

Exceptional ItemsExceptional Items

£m

Rationalisation cost of Tableware (9.8)

Profit on sale of Electronics 28.5

Loss on sale of Organic Pigments (6.2)

Profit on disposal of surplus properties 1.1

13.6

Goodwill amortisation (0.2)

13.4

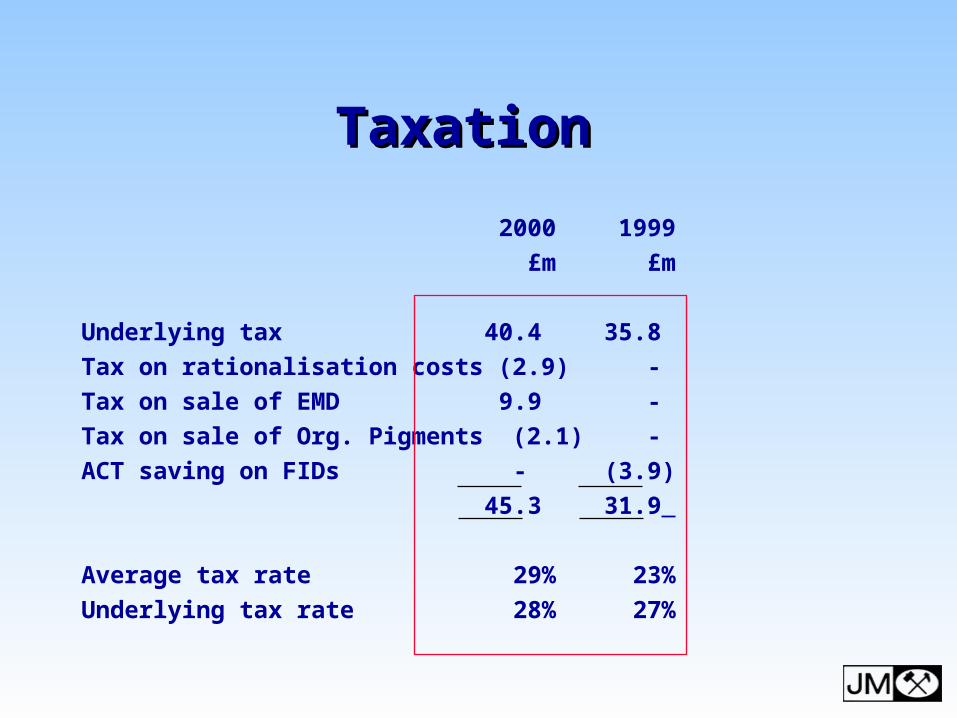

Taxation Taxation

2000 1999

£m £m

Underlying tax 40.4 35.8

Tax on rationalisation costs (2.9) -

Tax on sale of EMD 9.9 -

Tax on sale of Org. Pigments (2.1) -

ACT saving on FIDs - (3.9)

45.3 31.9

Average tax rate 29% 23%

Underlying tax rate 28% 27%

Return on InvestmentReturn on Investment2000 1999

£m £m

Operating profit 146.2 147.1

Average assets:

Equity and minorities 657 521

Cumulative goodwill 109 171

Net (cash) / borrowings 28 223

Total investment 794 915

Pre-tax ROA - continuing 24.2% n/a

- total 18.4% 16.1%

Post-tax ROA 13.2% 11.7%

Economic value added £32m £16m

Free Cash FlowFree Cash Flow

Continuing EMD TOTAL

2000 2000 2000

£m £m £m

Operating profit 136.1 0.1 136.2

Depreciation and amortisation 38.0 8.6 46.6

Working capital / other (54.5) 2.0 (52.5)

Cash flow from operations 119.6 10.7 130.3

Interest / tax / dividends (72.2) (5.9) (78.1)

Capital expenditure (gross) (63.4) (11.4) (74.8)

Sale of fixed assets 8.4 0.7 9.1

Free cash flow (7.6) (5.9) (13.5)

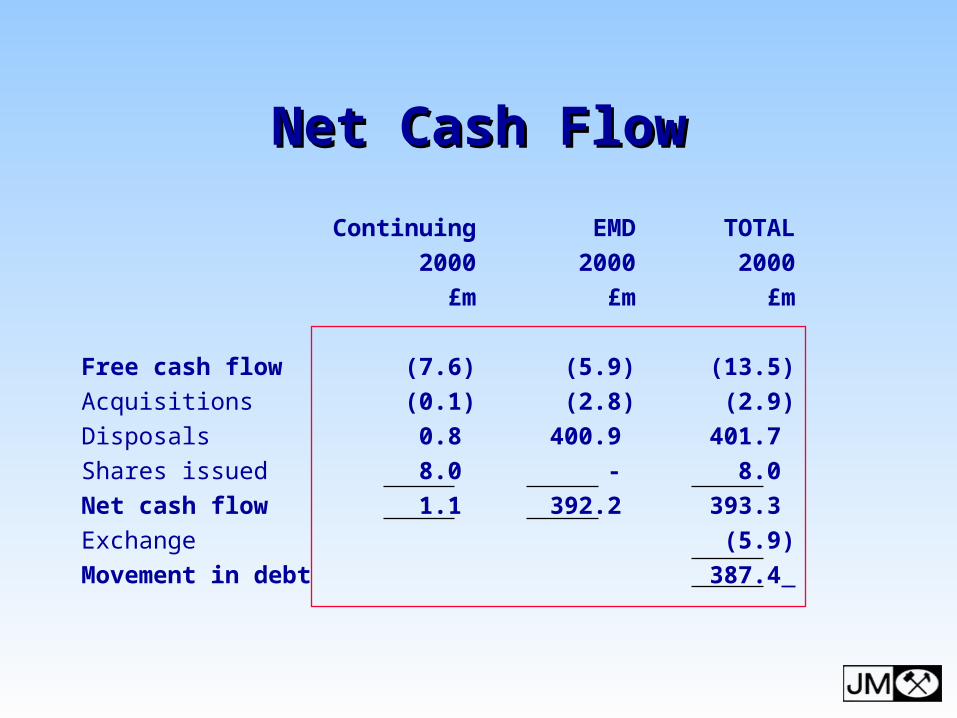

Net Cash FlowNet Cash Flow

Continuing EMD TOTAL

2000 2000 2000

£m £m £m

Free cash flow (7.6) (5.9) (13.5)

Acquisitions (0.1) (2.8) (2.9)

Disposals 0.8 400.9 401.7

Shares issued 8.0 - 8.0

Net cash flow 1.1 392.2 393.3

Exchange (5.9)

Movement in debt 387.4

GearingGearing

Mar 00 Mar 99

£m £m

Net (cash) / debt (166) 222

Equity and minorities 760 559

Capital employed 594 781

Gearing n/a 40%

Interest cover 61x 9x

Catalysts & Chemicals DivisionCatalysts & Chemicals Division

Operating ProfitSales

0

20

40

60

80

100

+14%+26%

1999 20001999 2000

677

856

74.2

84.8

£m £m

0

200

400

600

800

1000

AutocatalystsAutocatalysts

Volumes up 11%

- tighter legislation

- strong car sales Investing in capacity and technology Well placed in developing markets Progress with Heavy Duty Diesel

Major Changes in Emissions LegislationMajor Changes in Emissions Legislation

Europe

USA

Fed 75 and amendments to CAA

Fed 75Fed 75 Tier 1

Euro I

Euro II

Euro III

Euro III(HDD)

Euro IV

Euro “V”(HDD)

Tier 2

LEV I(CAL.)

LEV II(CAL.)

Tier 1

8075 90 009585 051970 2010

Fed 75 USHDD

USHDD

Euro IV(HDD)

CAL.HDDTier 1

“I am very excited about fuel cells. I believe they’re going to be a significant part of our industry a lot sooner than many people think. I think that it’s possible that they could displace the internal combustion engine as the dominant source of power for consumer vehicles within my lifetime.”

William Clay Ford Jr,

Chairman, Ford Motor Company

Fuel CellsFuel Cells

£12 million being invested in development and testing capability

Customer collaborations on plan Securing supply base Fuel Reformer developed for residential

market

Chemicals Chemicals

PGM refining strong on back of higher prices

High throughput screening adding value for customers

Expansion of process catalyst manufacturing

Smoptech acquisition

Pharmaceutical MaterialsPharmaceutical Materials

Methylphenidate prices hit by competition Strong performance from carboplatin and

organics Good progress on new products New facility under way

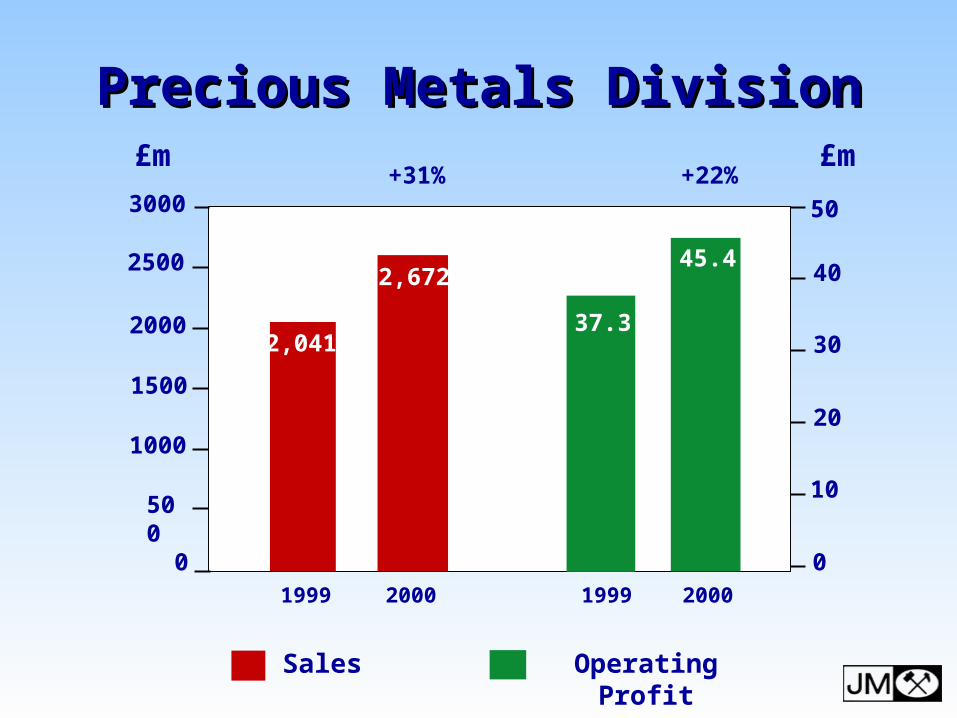

Precious Metals DivisionPrecious Metals Division

Operating ProfitSales

0

10

20

30

40

50

+22%+31%

1999 20001999 2000

2,041

2,672

37.3

45.4

£m£m

0

1000

1500

2000

2500

500

3000

Precious Metals DivisionPrecious Metals Division

Strong demand for pgms 50% growth in China jewellery Robust prices Good growth in fabricated products Outlook strengthening further with

uncertainty over palladium availability Gold satisfactory in difficult markets

Platinum & Palladium PricesPlatinum & Palladium Prices

April1998

$/oz900

800

700

600

500

400

300

200

100

0April2000

April1999

Palladium

Platinum

April1997

Colours & Coatings DivisionColours & Coatings Division

Operating ProfitSales

0

5

10

15

25

30

+11%-1%

1999 20001999 2000

244 241 25.1

27.9

£m £m

0

100

150

200

250

50

300

20

Colours & Coatings DivisionColours & Coatings Division

Underlying sales growth Margins up to 12% Focus on growth businesses Investment in Spain Expansion of facilities at Maastricht Exit from organic pigments complete

Colours & Coatings DivisionColours & Coatings DivisionRationalisation UpdateRationalisation Update

Spent £5.2 million out of £10 million provision Headcount reduced by 113 Singapore and Milan operations closed Closure of Burslem underway Annual savings of £2.8 million already

secured Savings of £4 million in current year and

£7 million p.a. thereafter

e - Commercee - Commerce

Longstanding internet presence Catalogue sales in US Expanding into Europe this year e-Procurement project Developments in car industry

Outlook Outlook

Prospects for growth very encouraging Investing in new technology and new

facilities Acquisition opportunities

Johnson Matthey