Embed Size (px)

Citation preview

© 2012 Colt Technology Services Group Limited. All rights reserved

Hybrid cloud

VMware Forum Manchester

23rd May 2012

Agenda

Market perspective 1

2

3

Customer perspective

IT perspective

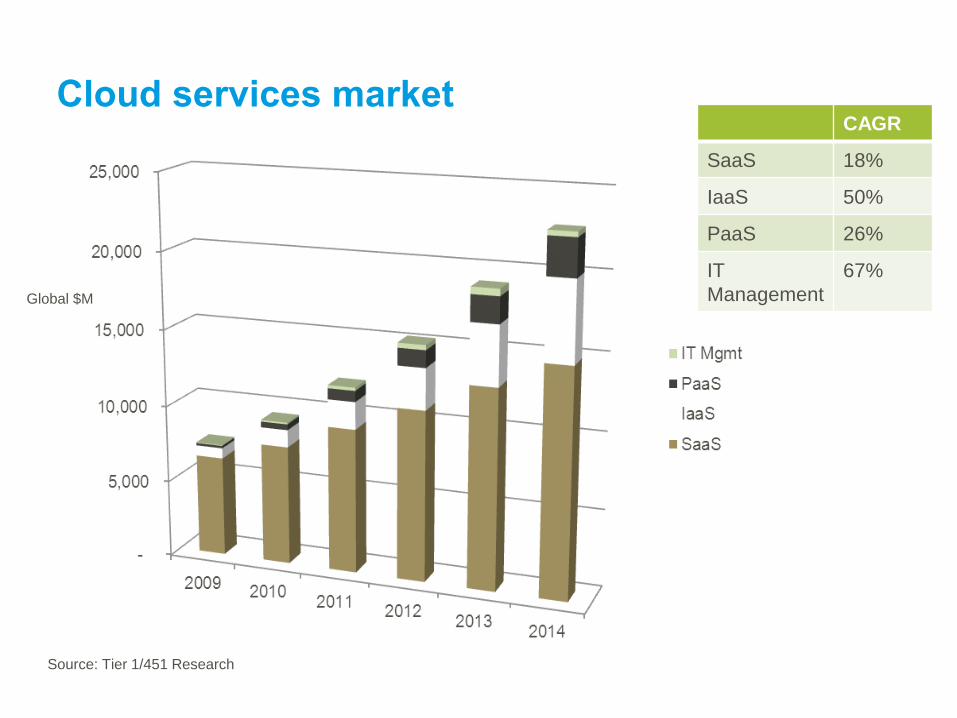

Cloud services market

Global $M

Source: Tier 1/451 Research

CAGR

SaaS 18%

IaaS 50%

PaaS 26%

IT

Management

67%

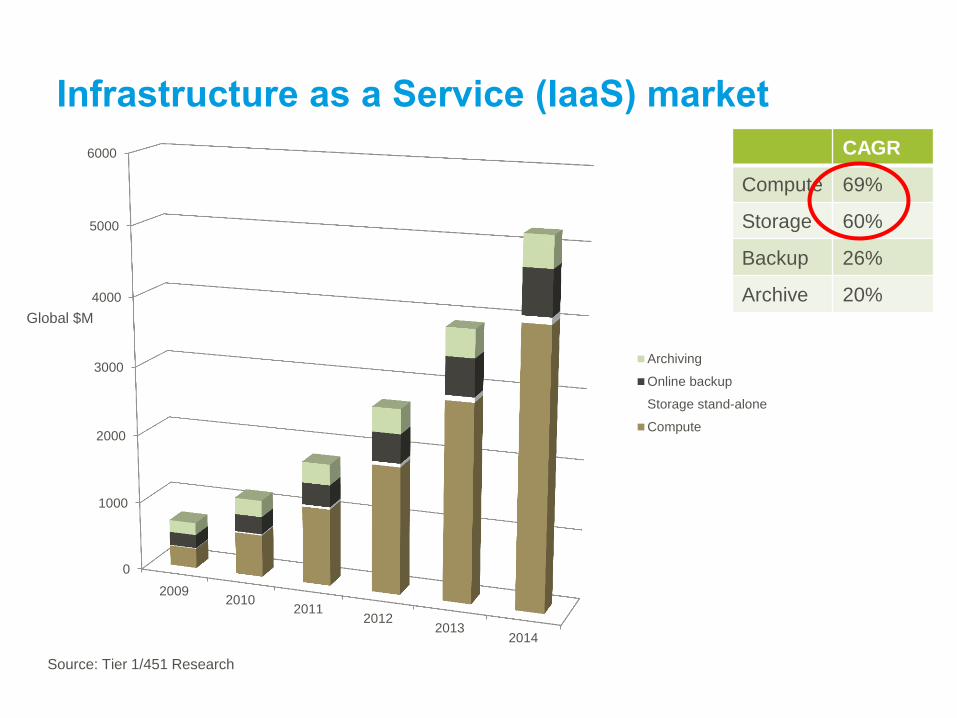

Infrastructure as a Service (IaaS) market

0

1000

2000

3000

4000

5000

6000

20092010

20112012

20132014

Archiving

Online backup

Storage stand-alone

Compute

Source: Tier 1/451 Research

CAGR

Compute 69%

Storage 60%

Backup 26%

Archive 20% Global $M

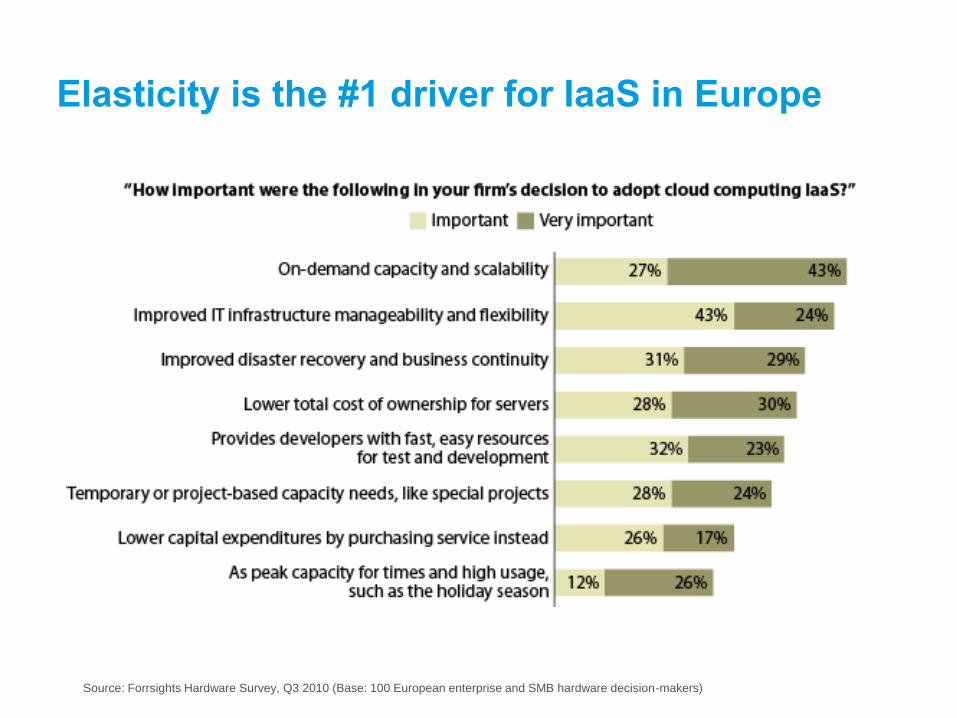

Elasticity is the #1 driver for IaaS in Europe

Source: Forrsights Hardware Survey, Q3 2010 (Base: 100 European enterprise and SMB hardware decision-makers)

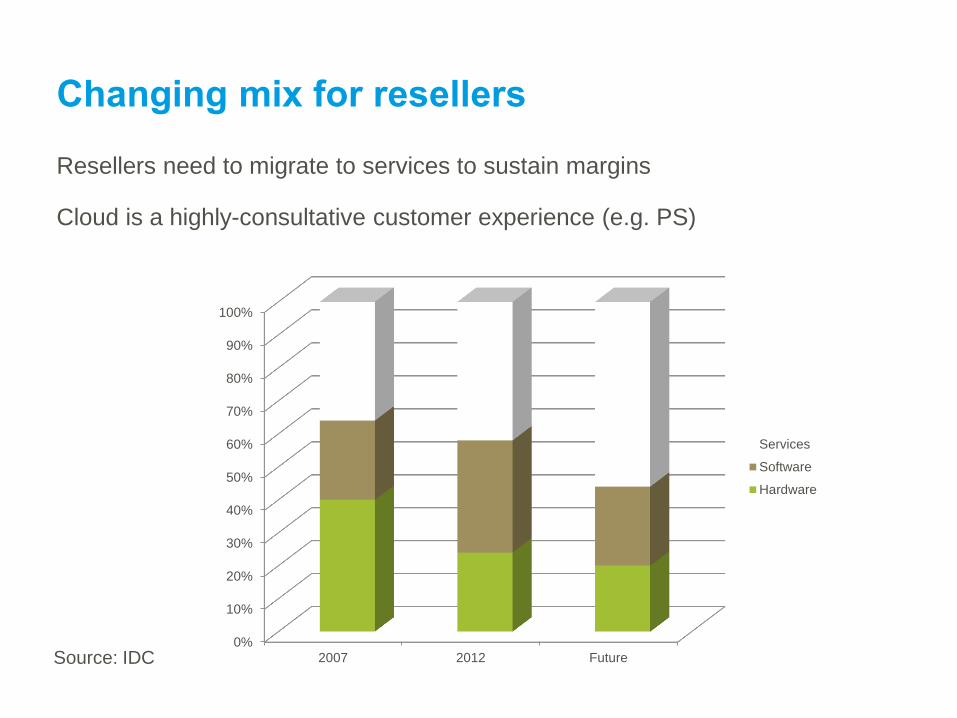

Changing mix for resellers

Resellers need to migrate to services to sustain margins

Cloud is a highly-consultative customer experience (e.g. PS)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2012 Future

Services

Software

Hardware

Source: IDC

Computing capacity as a utility

http://www.nicholasgcarr.com/bigswitch/

“Operating your own IT assets is

becoming akin to running your

own power station”

• Capex intensive

• Long lead-time

• Specialist skills

• Benefits from scale

• Not core to most businesses

Hybrid Cloud: Win, Win, Win

Customer perspective

Smart Gaming Group

Michael Meaney

9

http://youtu.be/pa0azMA9WHY

Customer perspective

Smart Gaming Group

Michael Meaney

11

• Flexibility

• Consistency

• Utility consumption

• Expertise

• Uptime

• Expansion/growth

• Speed of delivery

Customer perspective

Oxford University / DBaaS

Dr Stuart Lee

12

http://www.youtube.com/watch?v=Cps6XqhUlaU

Customer perspective

Oxford University / DBaaS

Dr Stuart Lee

14

• Reduced need for local hardware

• Concentration of data / improved curation

• Data location is important in public cloud

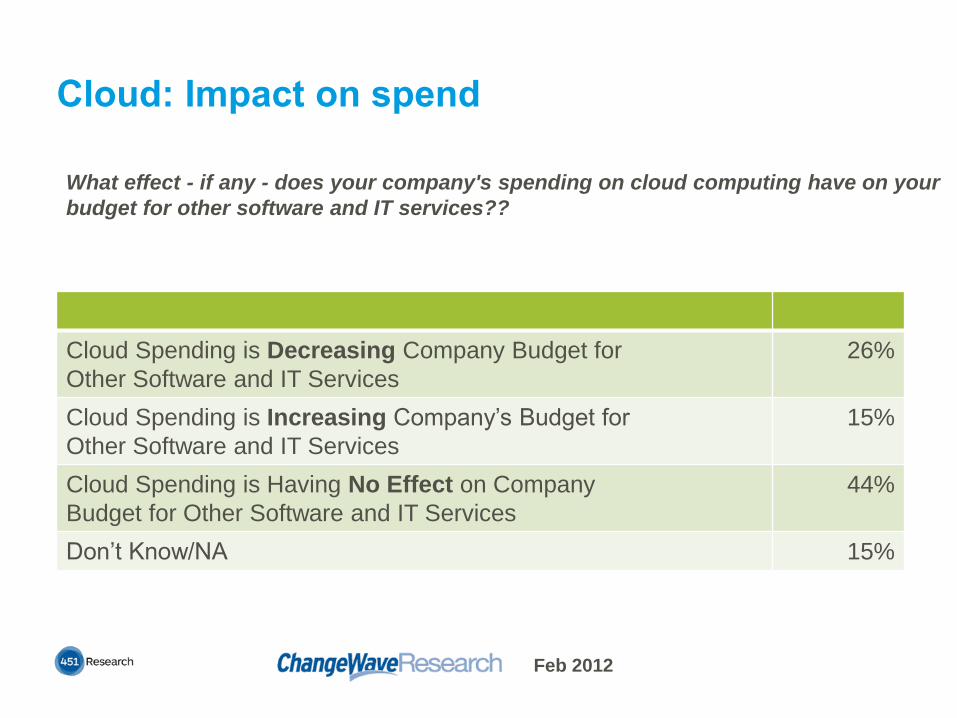

Cloud: Impact on spend

Cloud Spending is Decreasing Company Budget for

Other Software and IT Services

26%

Cloud Spending is Increasing Company’s Budget for

Other Software and IT Services

15%

Cloud Spending is Having No Effect on Company

Budget for Other Software and IT Services

44%

Don’t Know/NA 15%

What effect - if any - does your company's spending on cloud computing have on your

budget for other software and IT services??

Feb 2012

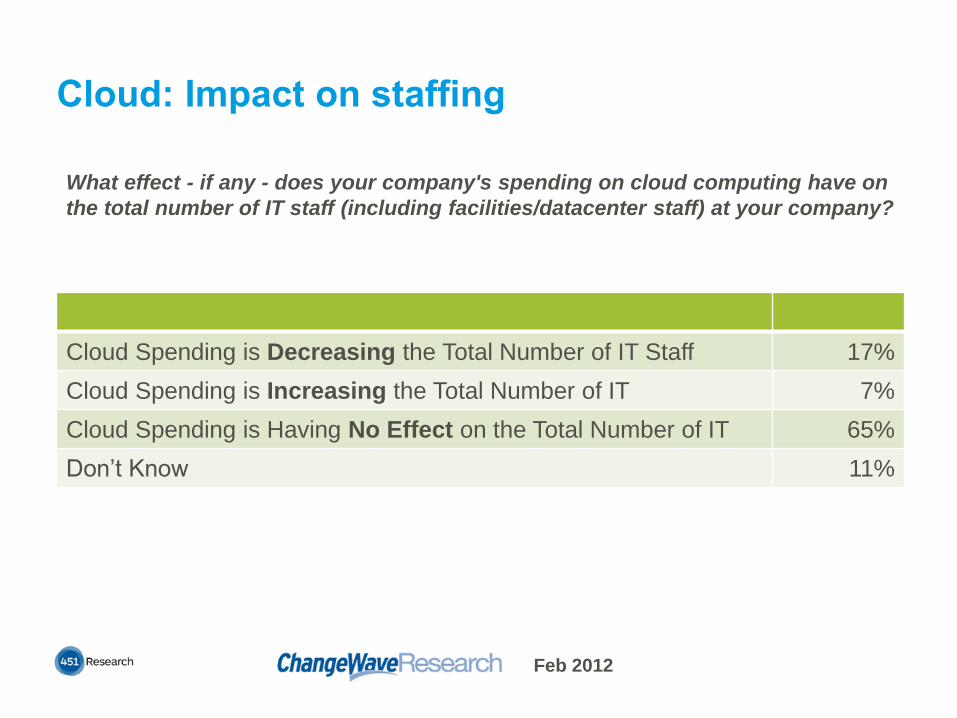

Cloud: Impact on staffing

Cloud Spending is Decreasing the Total Number of IT Staff 17%

Cloud Spending is Increasing the Total Number of IT 7%

Cloud Spending is Having No Effect on the Total Number of IT 65%

Don’t Know 11%

What effect - if any - does your company's spending on cloud computing have on

the total number of IT staff (including facilities/datacenter staff) at your company?

Feb 2012

No knobs & switches

What is your role in the management team?

Building power-

downs: need

weekend staff

Constant re-

investment in

training for

infrastructure

vendor skills

Adds, moves,

changes,

warranty work

Operating a

physical security

regime

Planning for space,

power, cooling

Constantly striving

to be “right-sized”

19

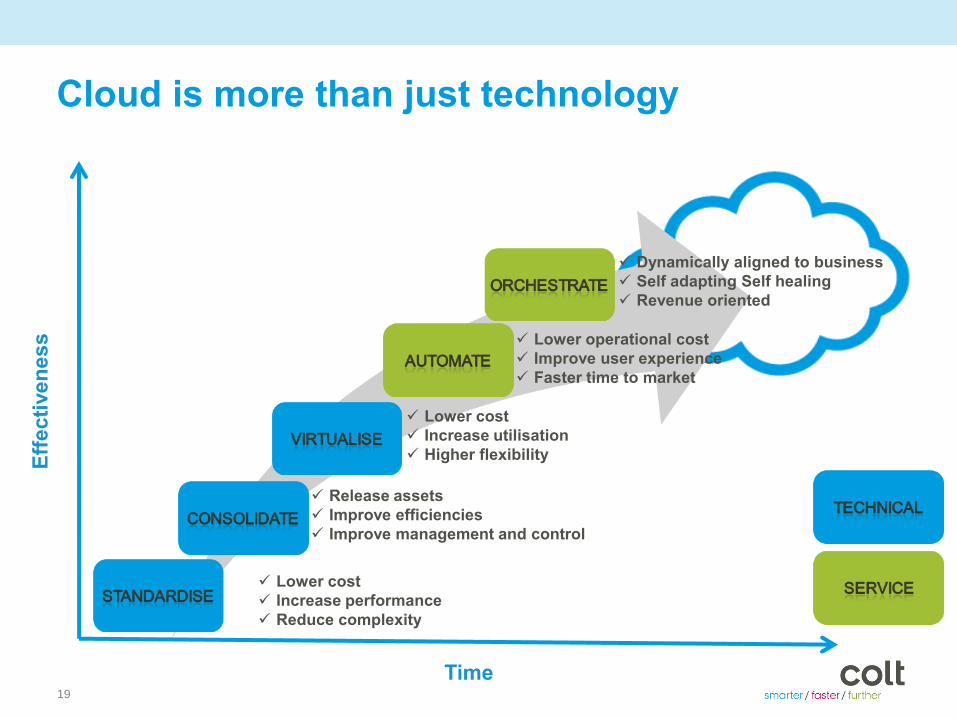

Cloud is more than just technology

Time

Eff

ecti

ven

ess

Lower cost

Increase utilisation

Higher flexibility

Lower operational cost

Improve user experience

Faster time to market

Dynamically aligned to business

Self adapting Self healing

Revenue oriented

Release assets

Improve efficiencies

Improve management and control

Lower cost

Increase performance

Reduce complexity

20

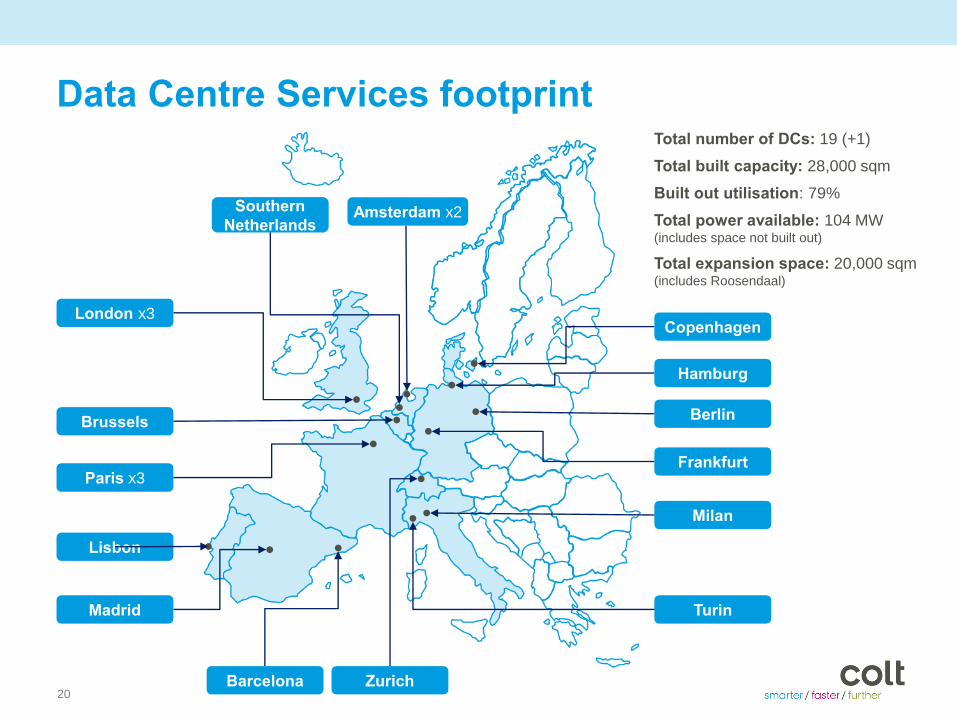

Data Centre Services footprint

Paris x3

London x3

Madrid

Zurich

Milan

Copenhagen

Berlin

Barcelona

Lisbon

Amsterdam x2

Turin

Brussels

Hamburg

Frankfurt

Southern

Netherlands

Total number of DCs: 19 (+1)

Total built capacity: 28,000 sqm

Built out utilisation: 79%

Total power available: 104 MW (includes space not built out)

Total expansion space: 20,000 sqm (includes Roosendaal)

21

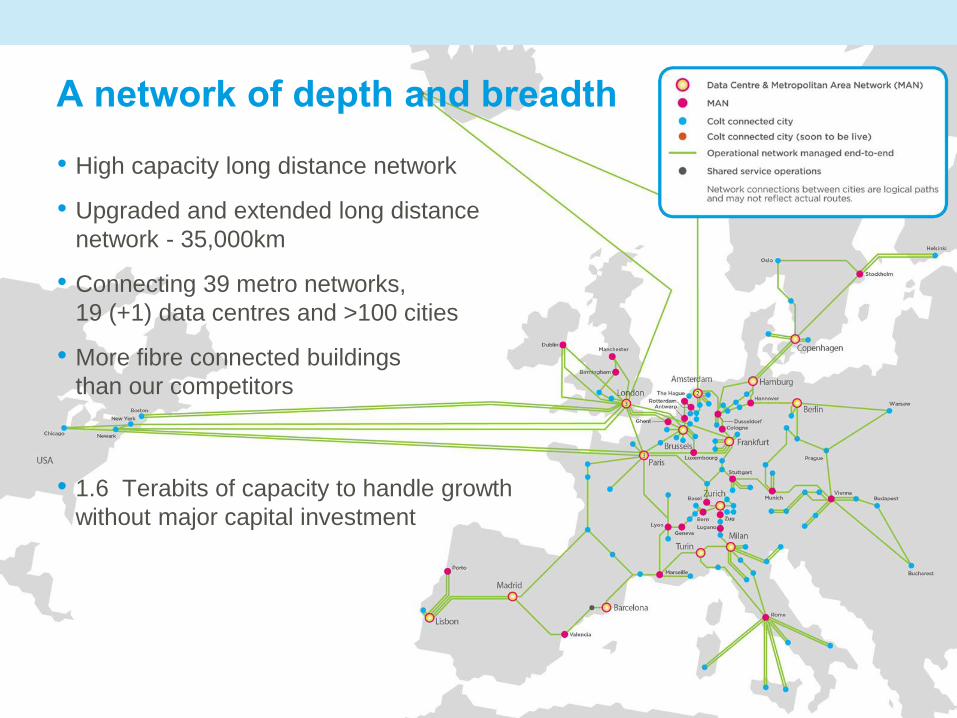

A network of depth and breadth

• High capacity long distance network

• Upgraded and extended long distance

network - 35,000km

• Connecting 39 metro networks,

19 (+1) data centres and >100 cities

• More fibre connected buildings

than our competitors

• 1.6 Terabits of capacity to handle growth

without major capital investment

Disaster Recovery

22

The DR Use Case seems to be a common entry point

23 23