Embed Size (px)

Citation preview

Presentation for the panel “Is the euro crisis over?”

EUI-nomics, Florence, 25 April 2014

Simone Manganelli

Head of Financial Research

European Central Bank

ECB-UNRESTRICTED

DRAFT

Rubric

www.ecb.europa.eu ©

Overview

6

1

2

3

Sovereign stress and risks

Financial fragmentation

Systemic stress in the financial system

1.1 The CISS Indicator

Rubric

www.ecb.europa.eu ©

1.1 The CISS Indicator

• Based on the work of Holló, Kremer, and Lo Duca (2012), "CISS - a composite indicator of

systemic stress in the financial system," ECB WP No. 1426.

• The CISS indicator is based on a total of 15 raw indicators of financial stress in 5 different

market segments:

– Money market (MM): realised volatility of 3 month Euribor; spread Euribor/T-bill (3 month maturity);

recourse to the marginal lending facility at the ECB.

– Bond market, sovereign and non-financials (BM): realised volatility of 10y Bund; spread corporate

A-rated versus government bonds; 10y interest rate swap spread.

– Equity market, non-financials (EM): realised volatility of equity returns; CMAX; stock-bond

correlation

– Financial intermediaries (FI): realised volatility of idiosyncratic returns of the banking index; spread

A rated financials/non-financials; CMAX interacted with book-price ratio for the financial sector equity

index.

– Foreign exchange market (FX): realised volatility of US/EUR, JPY/EUR, GBP/EUR.

An indicator of contemporaneous stress in the financial system:

CISS = Composite Indicator of Systemic Stress

Rubric

www.ecb.europa.eu ©

The CISS Indicator transformation

The 15 raw stress indicators are transformed on the basis of order statistics (“probability

integral transform”):

•replace each value of the raw indicator by its empirical quantile;

•yields homogeneous set of standard uniform distributed indicators;

•trades off distributional consistency and likely gains in robustness against loss of cardinal

information;

•the aggregation method takes into account the time-varying cross-correlations between the 5

subindices: situations in which stress prevails in several markets segments are given more

weight, thus capturing the idea that financial stress is more systemic.

4

ECB-PUBLIC

DRAFT

ECB-UNRESTRICTED

DRAFT 1.1 The CISS Indicator

Rubric

www.ecb.europa.eu ©

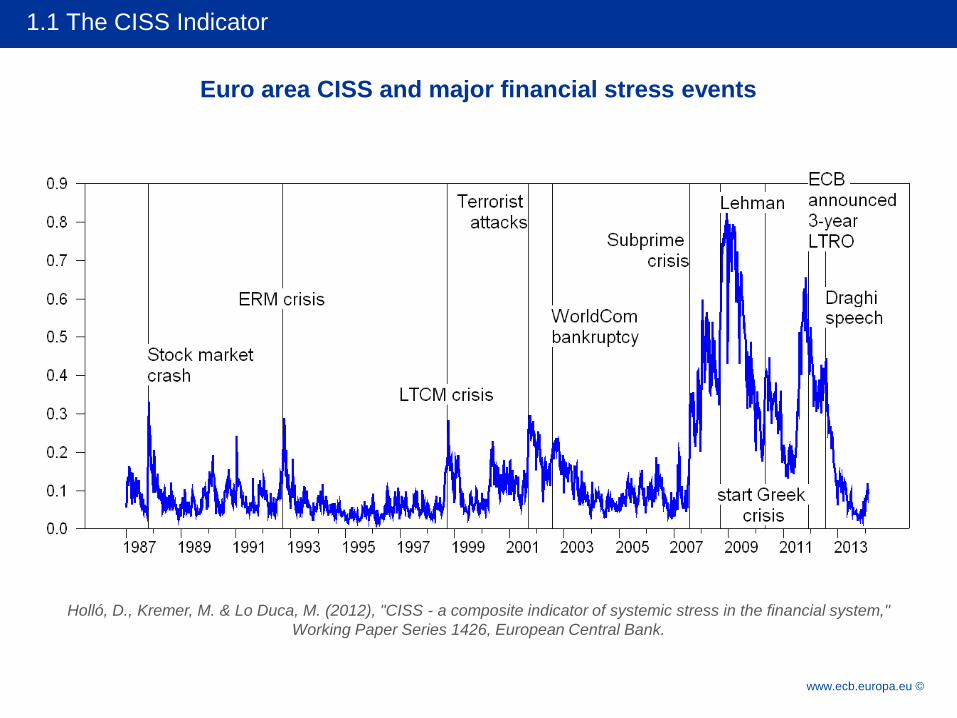

Euro area CISS and major financial stress events

Holló, D., Kremer, M. & Lo Duca, M. (2012), "CISS - a composite indicator of systemic stress in the financial system,"

Working Paper Series 1426, European Central Bank.

ECB-UNRESTRICTED

DRAFT 1.1 The CISS Indicator

Rubric

www.ecb.europa.eu ©

6

1

2

3

Sovereign stress and risks

Financial fragmentation

Systemic stress in the financial system

2.1 The Sovereign CISS indicator

2.2 Sovereign default risk

Overview

Rubric

www.ecb.europa.eu ©

A composite indicator monitoring stress in the euro area

sovereign bond markets

• SovCISS aims to measure the level of stress in euro area sovereign bond markets

– Composite stress indicator for the euro area as a whole;

– Decomposition into country-specific indicators

(11 countries: AT, BE, DE, ES, FI, FR, GR, IE, IT, NL, PT);

• Combines data from short- and long-end of the yield curve (2-year and 10-year

maturity bonds):

– 2 spreads b/w sovereign yield and euro swap interest rate (absolute spreads);

– 2 realised yield volatilities (weekly average of absolute daily changes);

– 2 bid/ask bond price spreads (in % of mid-price);

• Aggregation into country-specific and EA-aggregate SovCISS follows Hollo, Kremer

and Lo Duca (2012)

7

ECB-PUBLIC

DRAFT

ECB-UNRESTRICTED

DRAFT 2.1 The Sovereign CISS Indicator

Rubric

www.ecb.europa.eu © 8

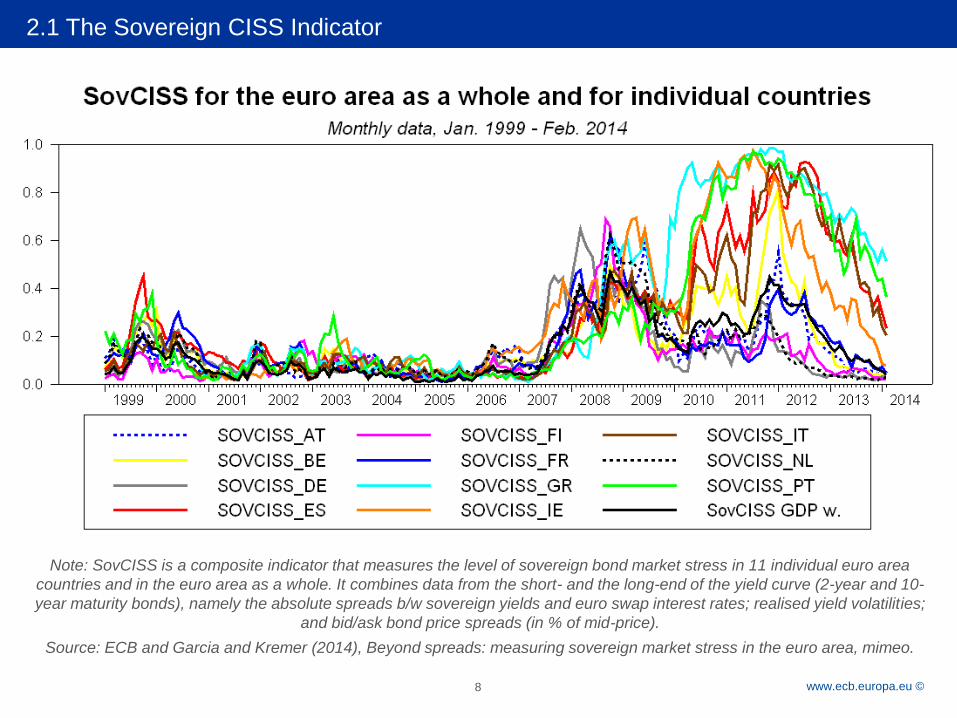

Note: SovCISS is a composite indicator that measures the level of sovereign bond market stress in 11 individual euro area

countries and in the euro area as a whole. It combines data from the short- and the long-end of the yield curve (2-year and 10-

year maturity bonds), namely the absolute spreads b/w sovereign yields and euro swap interest rates; realised yield volatilities;

and bid/ask bond price spreads (in % of mid-price).

Source: ECB and Garcia and Kremer (2014), Beyond spreads: measuring sovereign market stress in the euro area, mimeo.

2.1 The Sovereign CISS Indicator

Rubric

www.ecb.europa.eu ©

6

1

2

3

Sovereign stress and risks

Financial fragmentation

Systemic stress in the financial system

2.1 The Sovereign CISS indicator

2.2 Sovereign default risk

Overview

Rubric

www.ecb.europa.eu ©

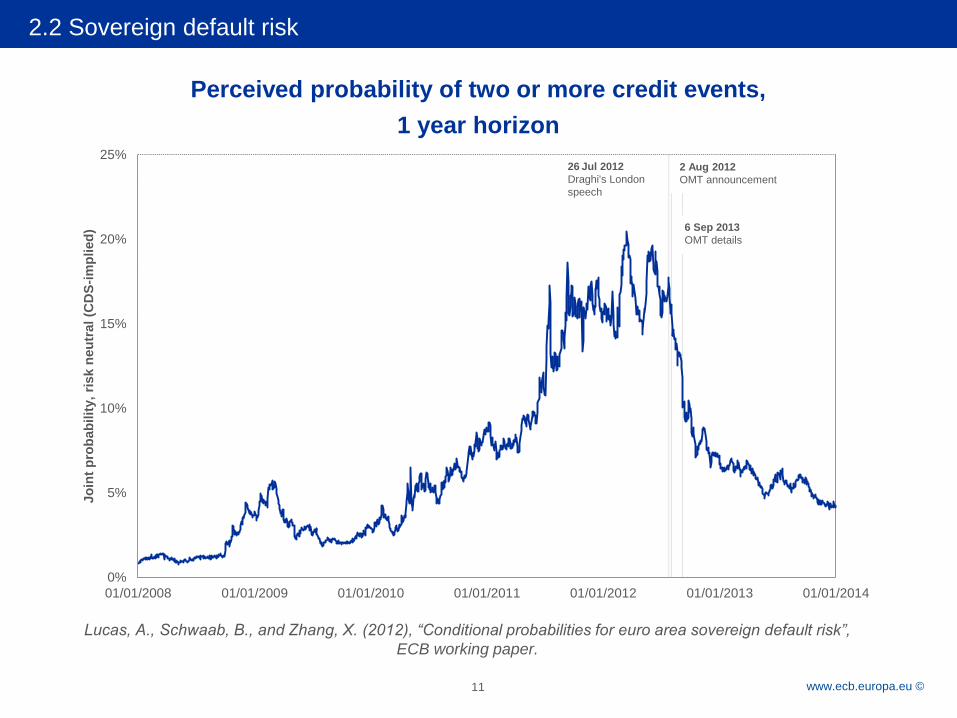

2.2 Sovereign default risk

10

• Lucas, A., Schwaab, B., and X. Zhang (2012) developed an indicator based on

observed prices for credit default swaps on sovereign debt;

• Country-specific risks are estimated from CDS quotes directly, while a time varying

dependence function is inferred from the co-movement in CDS Spreads;

• The euro area is proxied by ten member countries for which liquid CDS quotes are

available, i.e. Austria, Belgium, France, Germany, Greece, Ireland, Italy, the Netherlands,

Portugal, and Spain.

• The joint probability estimate is based on risk neutral probabilities of default, which are

higher than actual or historical probabilities.

A framework to assess the probability of joint and conditional default of

euro area member states

Rubric

www.ecb.europa.eu ©

2.2 Sovereign default risk

11

Lucas, A., Schwaab, B., and Zhang, X. (2012), “Conditional probabilities for euro area sovereign default risk”,

ECB working paper.

0

2

4

6

8

10

12

14

16

18

20

0%

5%

10%

15%

20%

25%

01/01/2008 01/01/2009 01/01/2010 01/01/2011 01/01/2012 01/01/2013 01/01/2014

Jo

int

pro

bab

ilit

y,

risk n

eu

tral

(CD

S-i

mp

lied

)

26 Jul 2012

Draghi's London

speech

6 Sep 2013

OMT details

2 Aug 2012

OMT announcement

Perceived probability of two or more credit events,

1 year horizon

Rubric

www.ecb.europa.eu ©

Overview

6

1

2

3

Sovereign stress and risks

Financial fragmentation

Systemic stress in the financial system

3.1 Money markets

3.2 Corporate bond markets

Rubric

www.ecb.europa.eu ©

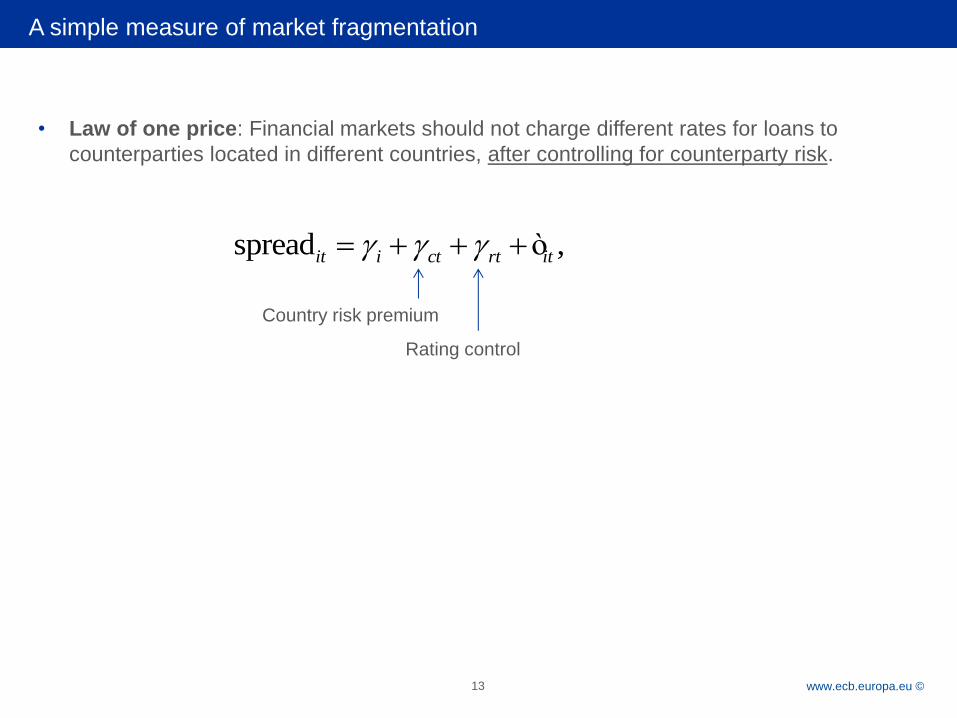

A simple measure of market fragmentation

13

• Law of one price: Financial markets should not charge different rates for loans to

counterparties located in different countries, after controlling for counterparty risk.

,spreadit i ct rt it ò

Country risk premium

Rating control

Rubric

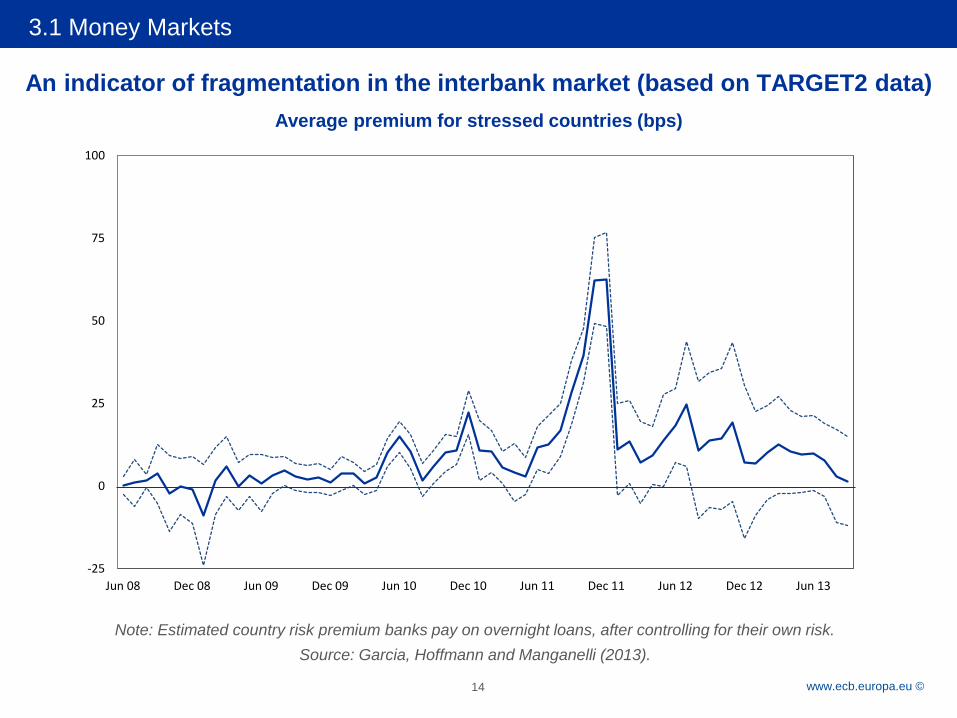

www.ecb.europa.eu © 14

Note: Estimated country risk premium banks pay on overnight loans, after controlling for their own risk.

Source: Garcia, Hoffmann and Manganelli (2013).

3.1 Money Markets

-25

0

25

50

75

100

Jun 08 Dec 08 Jun 09 Dec 09 Jun 10 Dec 10 Jun 11 Dec 11 Jun 12 Dec 12 Jun 13

An indicator of fragmentation in the interbank market (based on TARGET2 data)

Average premium for stressed countries (bps)

Rubric

www.ecb.europa.eu ©

Overview

6

1

2

3

Sovereign stress and risks

Financial fragmentation

Systemic stress in the financial system

3.2 Corporate bond markets

3.1 Money markets

Rubric

www.ecb.europa.eu © 16

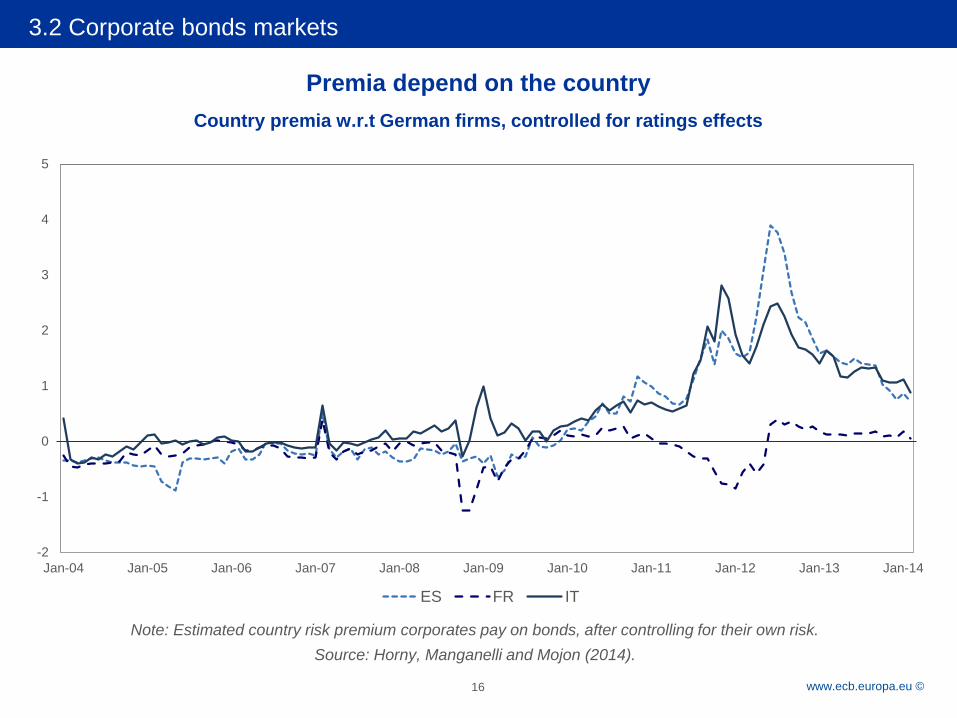

3.2 Corporate bonds markets

-2

-1

0

1

2

3

4

5

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

ES FR IT

Premia depend on the country

Country premia w.r.t German firms, controlled for ratings effects

Note: Estimated country risk premium corporates pay on bonds, after controlling for their own risk.

Source: Horny, Manganelli and Mojon (2014).

Rubric

www.ecb.europa.eu ©

1. Overall level of financial distress in the euro area returned to pre-crisis levels

2. Sovereign risk

a. reached its acute phase in the first half of 2012

b. has been brought under control with the announcement of OMT

c. has not yet returned to pre-crisis levels

3. Financial fragmentation

a. Evidence of acute stress in money markets at end 2011, brought under

control by the 3-year LTRO

b. Corporates continue to pay significant premium due to their geographic

location

17

Conclusion