Embed Size (px)

Citation preview

04/01/2017

1

1

T R Srinivasan FCAG Sekar Associates, CAs

Agenda

1 Background 1

2 Export Incentive Schemes 5

2.1 Merchandise Exports From India Scheme 6

2.2 Service Exports From India Scheme 10

2.3 Common Provisions 14

2.4 Documentation & Procedures 17

2.5 Case Studies 22

2.6 Export House Status 28

3 Duty Exemption Schemes 30

Page

04/01/2017

2

Background

1

4

Outlook on Exports

04/01/2017

3

5

Governing Authority

Director General of Foreign Trade

Background• Foreign Trade (Development and Regulation) Act, 1992 (‘FTDR’) designed to

develop and regulate foreign trade.• FTDR Act, 1992 announces Foreign Trade Policy (‘FTP’) from time to time to

formulate Export Import Policies. • Generally, FTP is introduced for a period of five years.• FTP 2015 ‐20 ‐ Key Focus

− Trade facilitation (cutting down transaction cost) and enhance the‘ease of doing business’ in India

− Support manufacturing and service sectors− Intensify framework to increase export potential of goods and services− Elevate value addition in country in line with ‘Make in India’ Vision− Effort to move towards paperless processing− Nirayat Bandhu Scheme for new export/import entrepreneurs(http://niryatbandhu.iift.ac.in)

2

Section 1 – Background

04/01/2017

4

FTP ‐ 2015 – 20 – At a Glance !

3

Section 1 – Background

8 piece puzzlediagram

01 Legal Framework & Trade Facilitation

04Duty Exemptions & Remission Schemes

0506Export Promotion Capital g00ds Scheme

EOU/EHTP/STPI/ BTP

07

Deemed Exports

08Quality Complaints and Trade Disputes

03Exports from India schemes

Hand Book of Procedures

Questions?• Whether IEC is Compulsory for all imports /

exports?

• Can exports be denominated only in Forex or in INR also? (Para 2.52)

2Export Incentives – Key Policy/procedural aspects

•

Section 1 – Background

04/01/2017

5

Key Highlights

4

Section 1 – Background

Reduction in mandatory documents for export/ import

MoU with State Governments – Refund of VAT

Creation of Exporter ‐ Importer Profile

EDI Help Desk & Online complaint registration and monitoring system

Message Exchange system with Community Partners

Export Incentive Schemes

5

04/01/2017

6

Merchandise Exports From India Scheme

6

Export of Goods ‐ Incentives

7

Description FTP 2009‐14 FTP 2015‐20

Scheme Focus Product SchemeFocus Market SchemeMarket Linked Focus Product SchemeVishesh Krishi Gram Udyog YojanaScheme

Merchandise Exports from India Scheme

% of Incentives 2% to 5% on FOB value of Exports 2% to 5% on FOB value of Exports

Eligibility Export of Specified ProductsExport to Specified CountriesExport of Specified products to Specified Countries

Export of Specified products to Specified Countries

Exports by SEZ Ineligible for incentives Eligible for incentives

04/01/2017

7

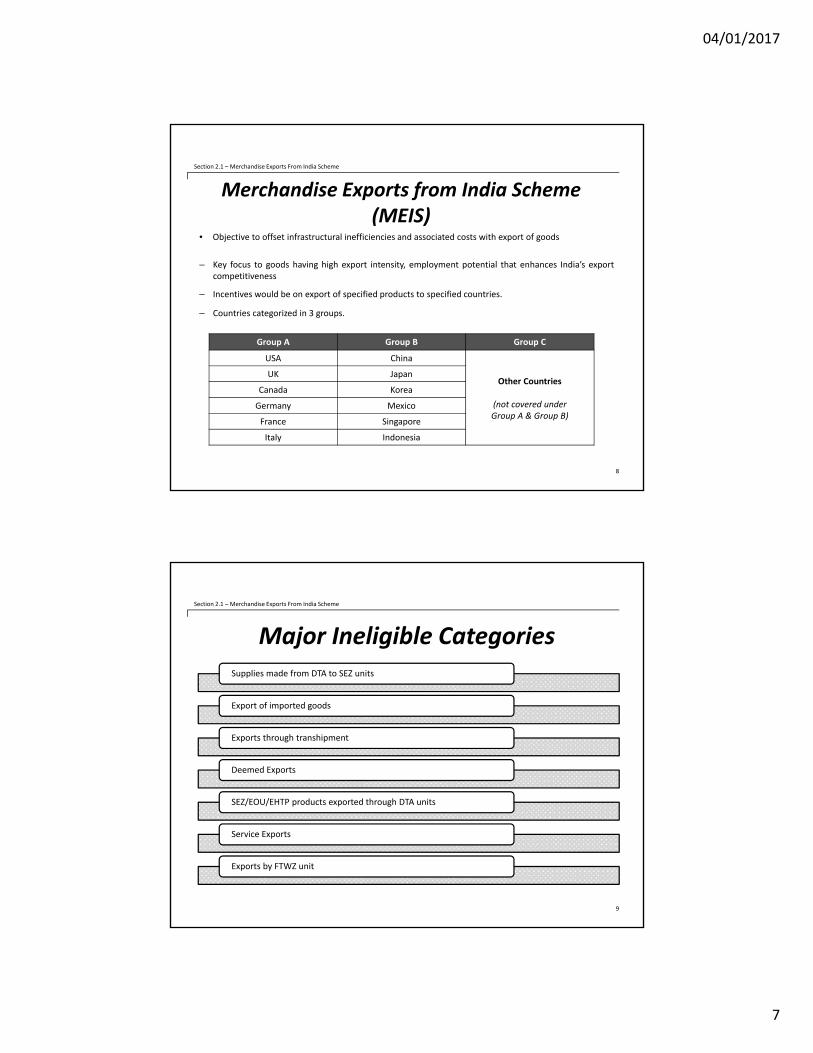

Merchandise Exports from India Scheme (MEIS)

• Objective to offset infrastructural inefficiencies and associated costs with export of goods

– Key focus to goods having high export intensity, employment potential that enhances India’s exportcompetitiveness

– Incentives would be on export of specified products to specified countries.

– Countries categorized in 3 groups.

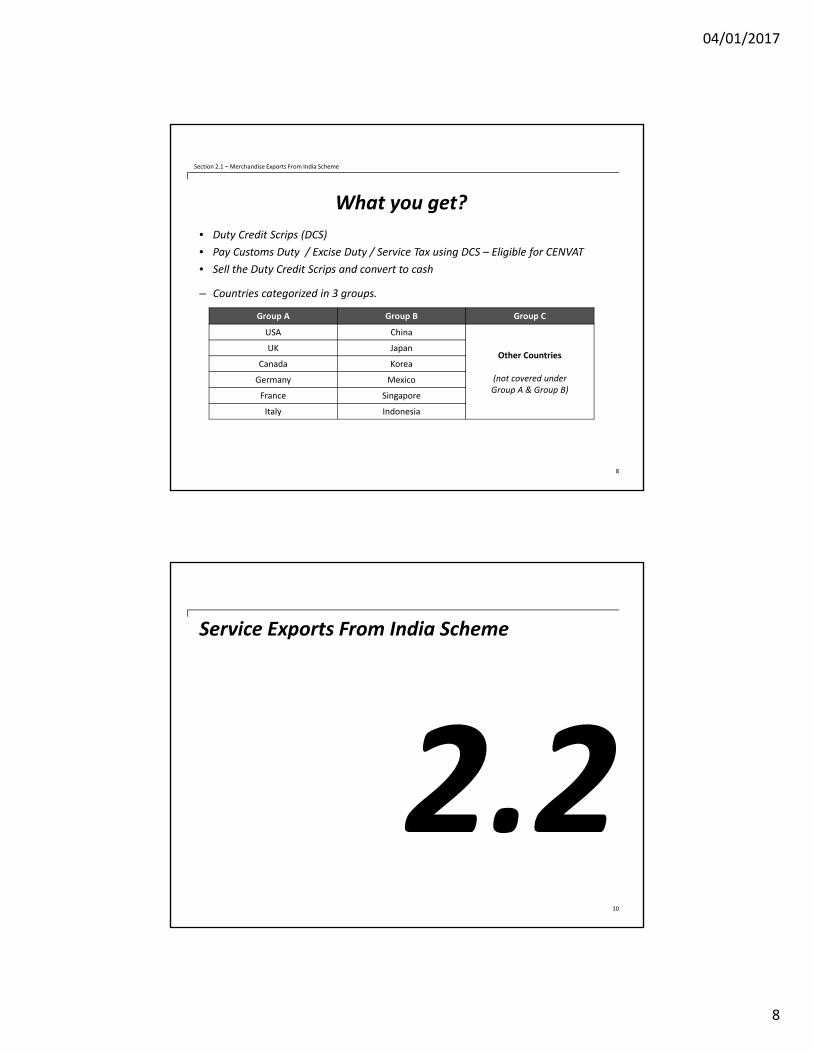

8

Section 2.1 – Merchandise Exports From India Scheme

Group A Group B Group C

USA China

Other Countries

(not covered under Group A & Group B)

UK Japan

Canada Korea

Germany Mexico

France Singapore

Italy Indonesia

Major Ineligible Categories

9

Section 2.1 – Merchandise Exports From India Scheme

Supplies made from DTA to SEZ units

Export of imported goods

Exports through transhipment

Deemed Exports

SEZ/EOU/EHTP products exported through DTA units

Service Exports

Exports by FTWZ unit

04/01/2017

8

What you get?• Duty Credit Scrips (DCS)• Pay Customs Duty / Excise Duty / Service Tax using DCS – Eligible for CENVAT• Sell the Duty Credit Scrips and convert to cash

– Countries categorized in 3 groups.

8

Section 2.1 – Merchandise Exports From India Scheme

Group A Group B Group C

USA China

Other Countries

(not covered under Group A & Group B)

UK Japan

Canada Korea

Germany Mexico

France Singapore

Italy Indonesia

Service Exports From India Scheme

10

04/01/2017

9

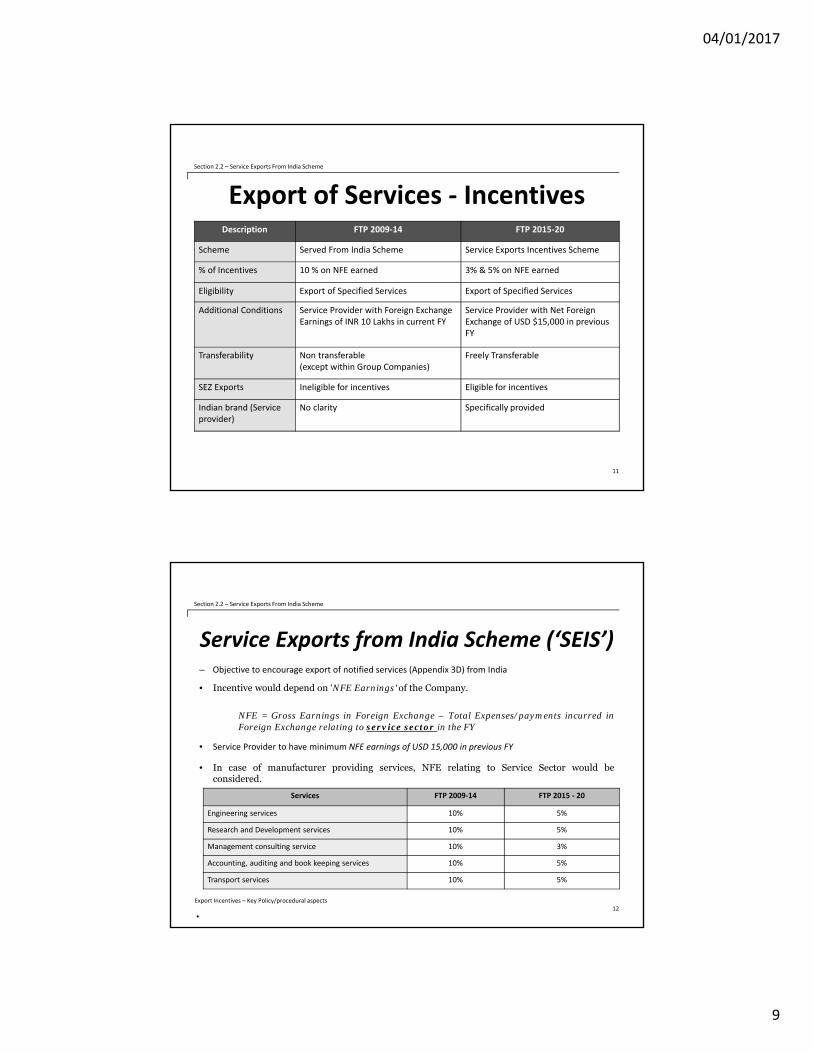

Export of Services ‐ Incentives

11

Section 2.2 – Service Exports From India Scheme

Description FTP 2009‐14 FTP 2015‐20

Scheme Served From India Scheme Service Exports Incentives Scheme

% of Incentives 10 % on NFE earned 3% & 5% on NFE earned

Eligibility Export of Specified Services Export of Specified Services

Additional Conditions Service Provider with Foreign Exchange Earnings of INR 10 Lakhs in current FY

Service Provider with Net Foreign Exchange of USD $15,000 in previous FY

Transferability Non transferable (except within Group Companies)

Freely Transferable

SEZ Exports Ineligible for incentives Eligible for incentives

Indian brand (Service provider)

No clarity Specifically provided

Service Exports from India Scheme (‘SEIS’)– Objective to encourage export of notified services (Appendix 3D) from India

• Incentive would depend on ‘NFE Earnings’ of the Company.

NFE = Gross Earnings in Foreign Exchange – Total Expenses/payments incurred inForeign Exchange relating to service sector in the FY

• Service Provider to have minimum NFE earnings of USD 15,000 in previous FY

• In case of manufacturer providing services, NFE relating to Service Sector would beconsidered.

12Export Incentives – Key Policy/procedural aspects

•

Section 2.2 – Service Exports From India Scheme

Services FTP 2009‐14 FTP 2015 ‐ 20

Engineering services 10% 5%

Research and Development services 10% 5%

Management consulting service 10% 3%

Accounting, auditing and book keeping services 10% 5%

Transport services 10% 5%

04/01/2017

10

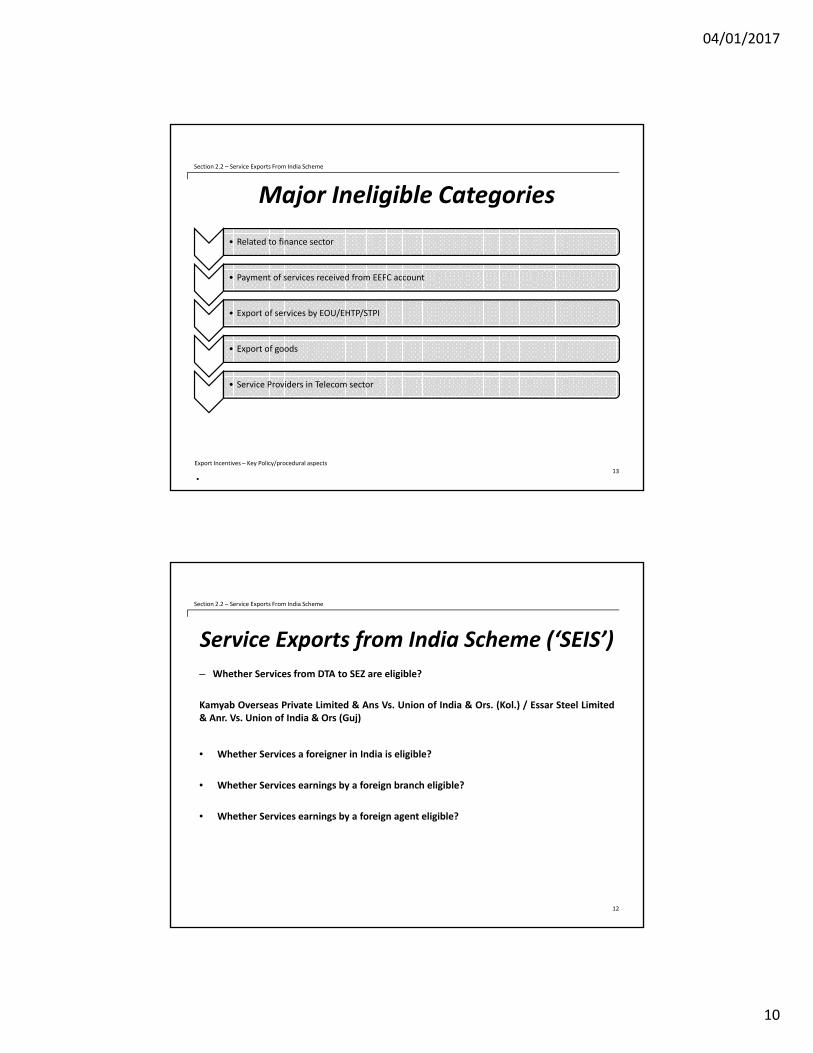

Major Ineligible Categories

• Related to finance sector

• Payment of services received from EEFC account

• Export of services by EOU/EHTP/STPI

• Export of goods

• Service Providers in Telecom sector

13Export Incentives – Key Policy/procedural aspects

•

Section 2.2 – Service Exports From India Scheme

Service Exports from India Scheme (‘SEIS’)– Whether Services from DTA to SEZ are eligible?

Kamyab Overseas Private Limited & Ans Vs. Union of India & Ors. (Kol.) / Essar Steel Limited& Anr. Vs. Union of India & Ors (Guj)

• Whether Services a foreigner in India is eligible?

• Whether Services earnings by a foreign branch eligible?

• Whether Services earnings by a foreign agent eligible?

12

Section 2.2 – Service Exports From India Scheme

04/01/2017

11

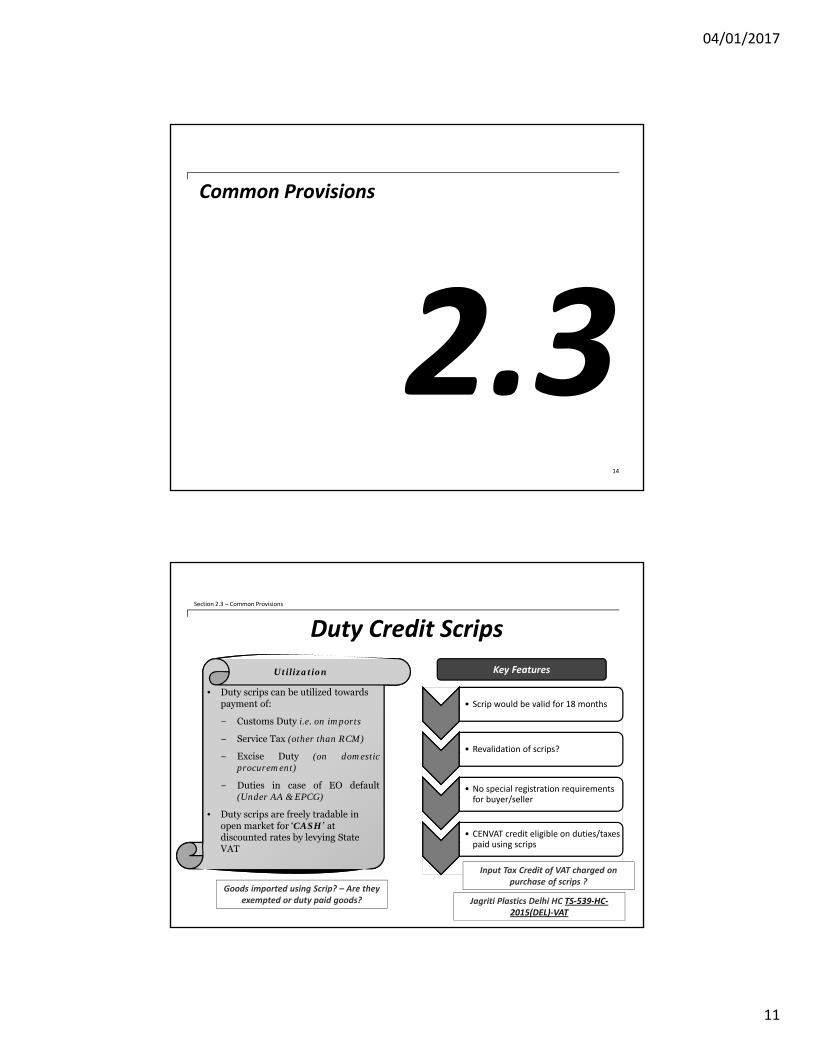

Common Provisions

14

Duty Credit Scrips

15

Section 2.3 – Common Provisions

• Duty scrips can be utilized towards payment of:

− Customs Duty i.e. on imports

− Service Tax (other than RCM)

− Excise Duty (on domesticprocurement)

− Duties in case of EO default(Under AA & EPCG)

• Duty scrips are freely tradable in open market for ‘CASH’ at discounted rates by levying State VAT

• Scrip would be valid for 18 months

• Revalidation of scrips?

• No special registration requirements for buyer/seller

• CENVAT credit eligible on duties/taxes paid using scrips

Key FeaturesUtilization

Input Tax Credit of VAT charged on purchase of scrips ?

Jagriti Plastics Delhi HC TS‐539‐HC‐2015(DEL)‐VAT

Goods imported using Scrip? – Are they exempted or duty paid goods?

04/01/2017

12

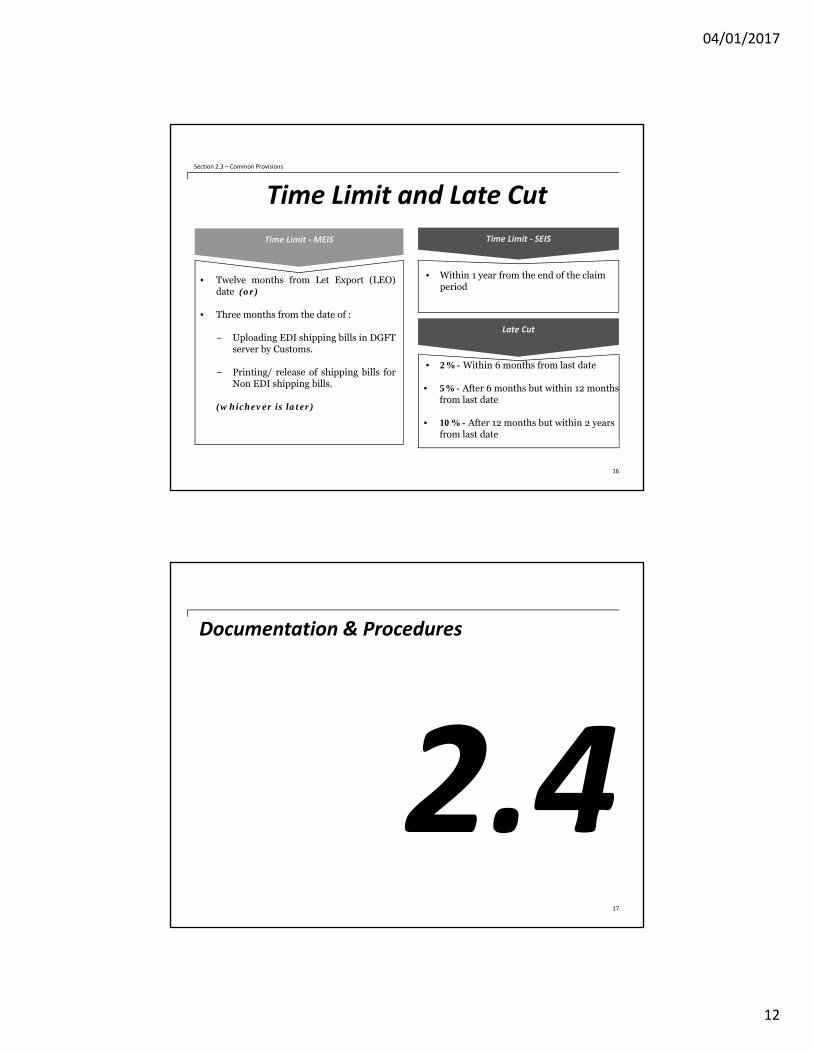

Time Limit and Late Cut

16

Section 2.3 – Common Provisions

• Twelve months from Let Export (LEO)date (or)

• Three months from the date of :

− Uploading EDI shipping bills in DGFTserver by Customs.

− Printing/ release of shipping bills forNon EDI shipping bills.

(whichever is later)

Time Limit ‐MEIS

• Within 1 year from the end of the claim period

Time Limit ‐ SEIS

• 2% - Within 6 months from last date

• 5% - After 6 months but within 12 months from last date

• 10% - After 12 months but within 2 years from last date

Late Cut

Documentation & Procedures

17

04/01/2017

13

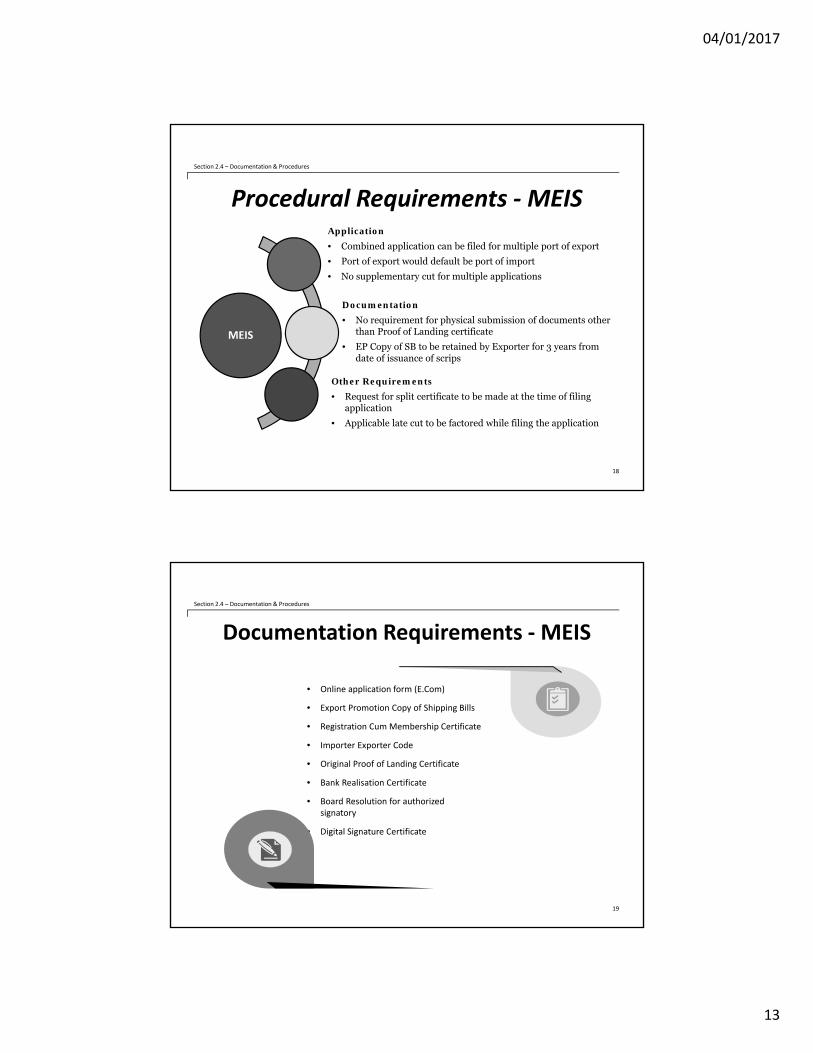

Procedural Requirements ‐MEIS

MEIS

18

Section 2.4 – Documentation & Procedures

Application

• Combined application can be filed for multiple port of export

• Port of export would default be port of import

• No supplementary cut for multiple applications

Documentation

• No requirement for physical submission of documents other than Proof of Landing certificate

• EP Copy of SB to be retained by Exporter for 3 years from date of issuance of scrips

Other Requirements

• Request for split certificate to be made at the time of filing application

• Applicable late cut to be factored while filing the application

Documentation Requirements ‐MEIS

19

Section 2.4 – Documentation & Procedures

• Online application form (E.Com)

• Export Promotion Copy of Shipping Bills

• Registration Cum Membership Certificate

• Importer Exporter Code

• Original Proof of Landing Certificate

• Bank Realisation Certificate

• Board Resolution for authorized signatory

• Digital Signature Certificate

04/01/2017

14

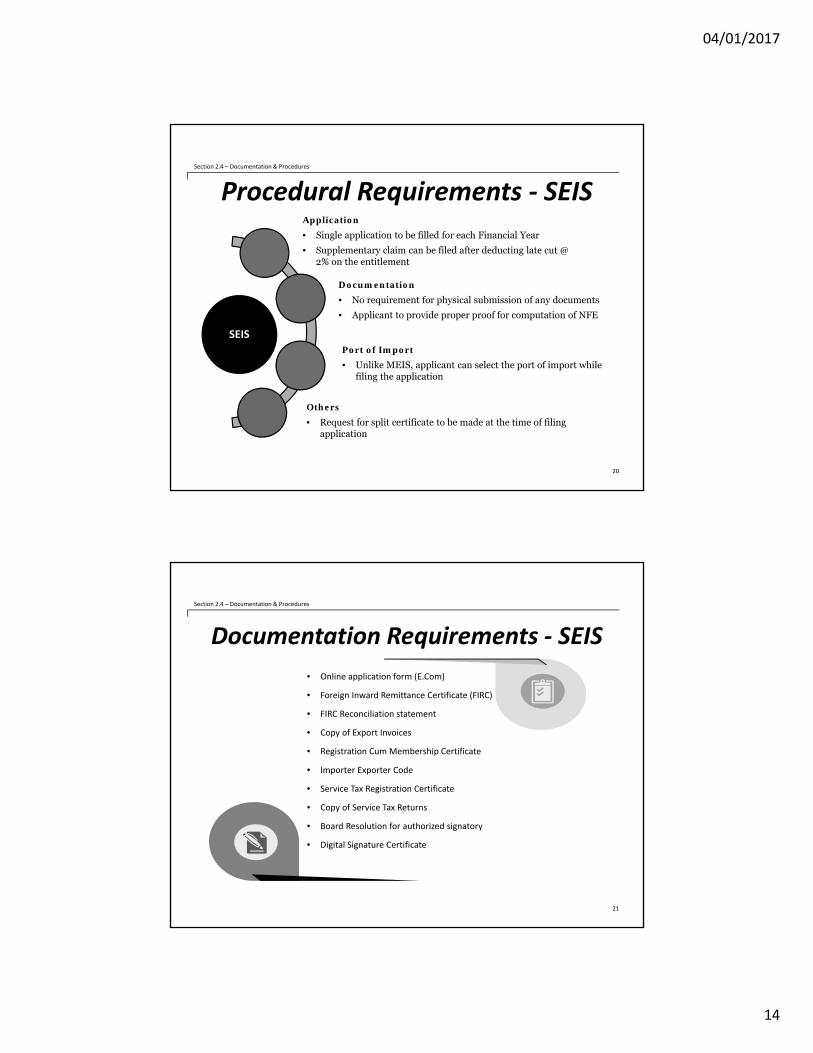

Procedural Requirements ‐ SEIS

SEIS

20

Section 2.4 – Documentation & Procedures

Application

• Single application to be filled for each Financial Year

• Supplementary claim can be filed after deducting late cut @ 2% on the entitlement

Port of Import

• Unlike MEIS, applicant can select the port of import while filing the application

Others

• Request for split certificate to be made at the time of filing application

Documentation

• No requirement for physical submission of any documents

• Applicant to provide proper proof for computation of NFE

Documentation Requirements ‐ SEIS

21

Section 2.4 – Documentation & Procedures

• Online application form (E.Com)

• Foreign Inward Remittance Certificate (FIRC)

• FIRC Reconciliation statement

• Copy of Export Invoices

• Registration Cum Membership Certificate

• Importer Exporter Code

• Service Tax Registration Certificate

• Copy of Service Tax Returns

• Board Resolution for authorized signatory

• Digital Signature Certificate

04/01/2017

15

Case Studies

22

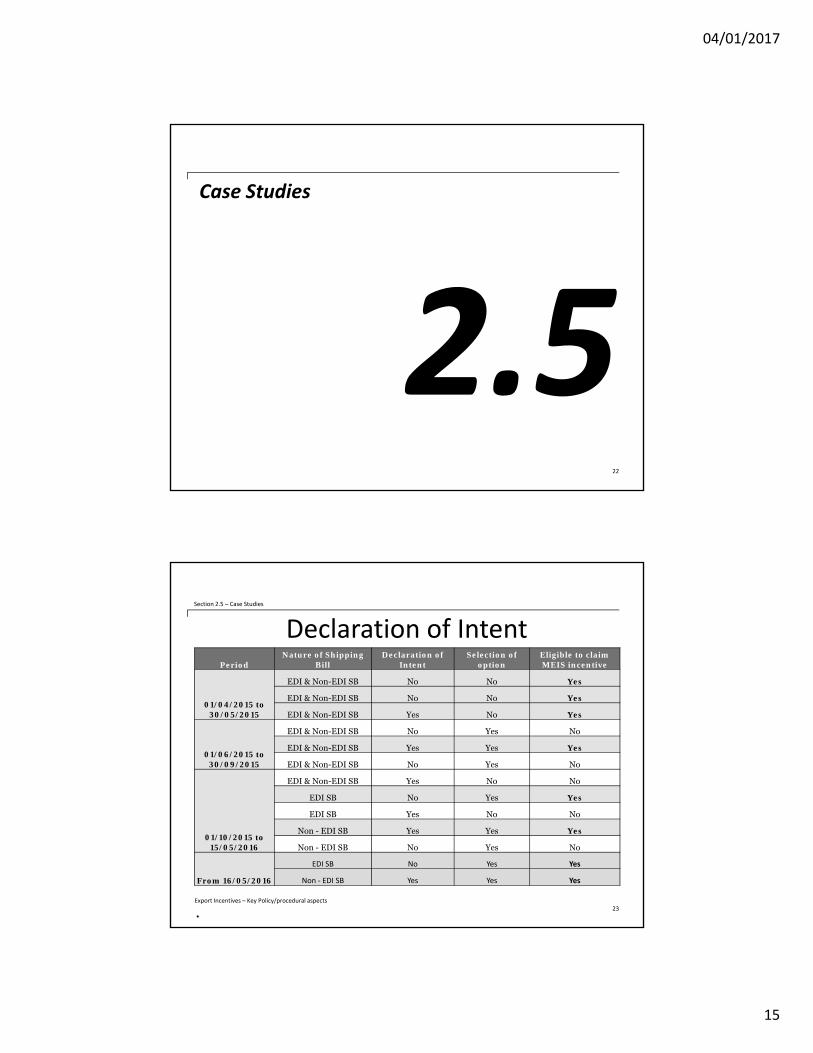

Declaration of Intent

23Export Incentives – Key Policy/procedural aspects

•

Section 2.5 – Case Studies

PeriodNature of Shipping

BillDeclaration of

IntentSelection of

optionEligible to claim MEIS incentive

01/04/2015 to 30/05/2015

EDI & Non-EDI SB No No Yes

EDI & Non-EDI SB No No Yes

EDI & Non-EDI SB Yes No Yes

01/06/2015 to 30/09/2015

EDI & Non-EDI SB No Yes No

EDI & Non-EDI SB Yes Yes Yes

EDI & Non-EDI SB No Yes No

01/10/2015 to 15/05/2016

EDI & Non-EDI SB Yes No No

EDI SB No Yes Yes

EDI SB Yes No No

Non - EDI SB Yes Yes Yes

Non - EDI SB No Yes No

From 16/05/2016

EDI SB No Yes Yes

Non ‐ EDI SB Yes Yes Yes

04/01/2017

16

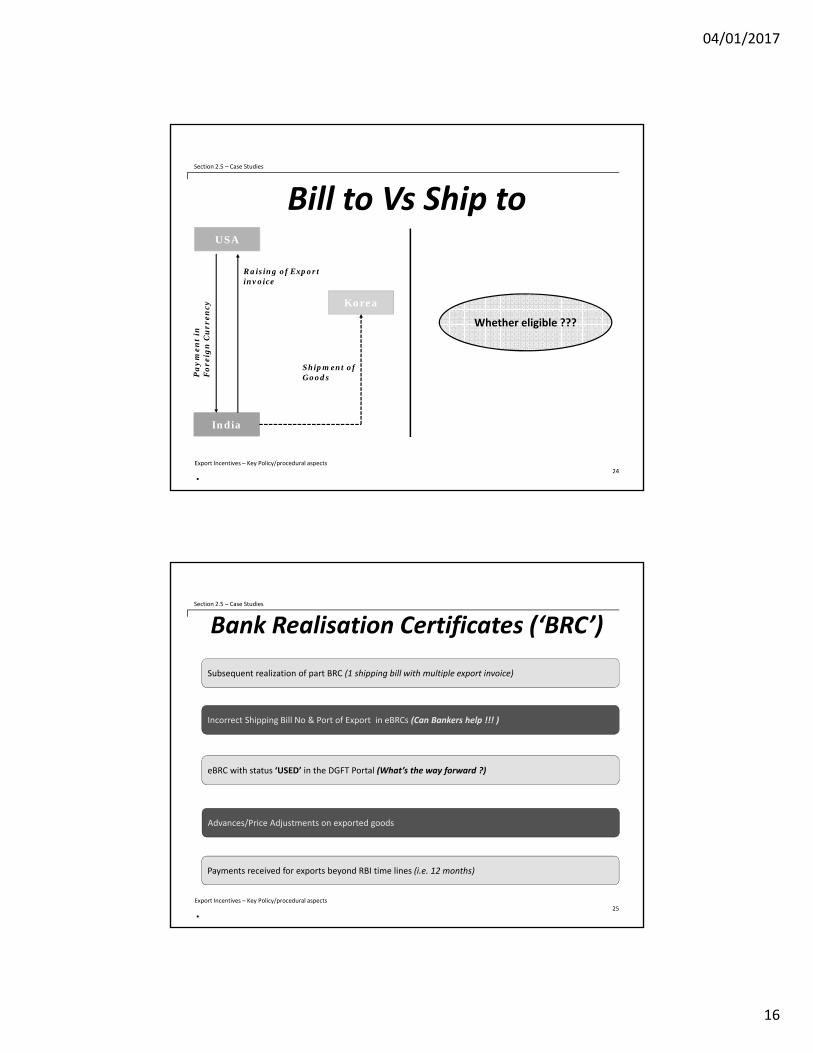

Bill to Vs Ship to

24Export Incentives – Key Policy/procedural aspects

•

Section 2.5 – Case Studies

India

Korea

USA

Pa

ym

ent

in

Fo

reig

n C

urr

ency

Raising of Export invoice

Shipment of Goods

Whether eligible ???

Bank Realisation Certificates (‘BRC’)

25Export Incentives – Key Policy/procedural aspects

•

Section 2.5 – Case Studies

Subsequent realization of part BRC (1 shipping bill with multiple export invoice)

Incorrect Shipping Bill No & Port of Export in eBRCs (Can Bankers help !!! )

eBRC with status ‘USED’ in the DGFT Portal (What’s the way forward ?)

Advances/Price Adjustments on exported goods

Payments received for exports beyond RBI time lines (i.e. 12 months)

04/01/2017

17

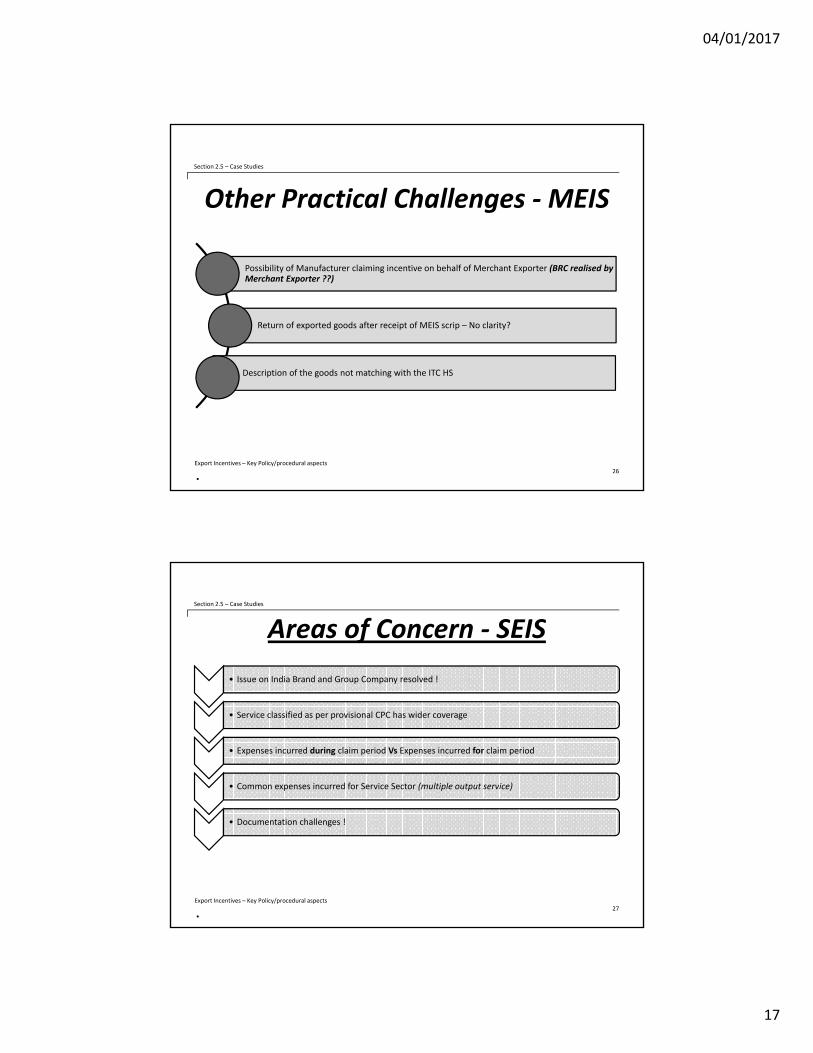

Other Practical Challenges ‐MEIS

Possibility of Manufacturer claiming incentive on behalf of Merchant Exporter (BRC realised by Merchant Exporter ??)

Return of exported goods after receipt of MEIS scrip – No clarity?

Description of the goods not matching with the ITC HS

26Export Incentives – Key Policy/procedural aspects

•

Section 2.5 – Case Studies

Areas of Concern ‐ SEIS

27Export Incentives – Key Policy/procedural aspects

•

Section 2.5 – Case Studies

• Issue on India Brand and Group Company resolved !

• Service classified as per provisional CPC has wider coverage

• Expenses incurred during claim period Vs Expenses incurred for claim period

• Common expenses incurred for Service Sector (multiple output service)

• Documentation challenges !

04/01/2017

18

Export House Status

28

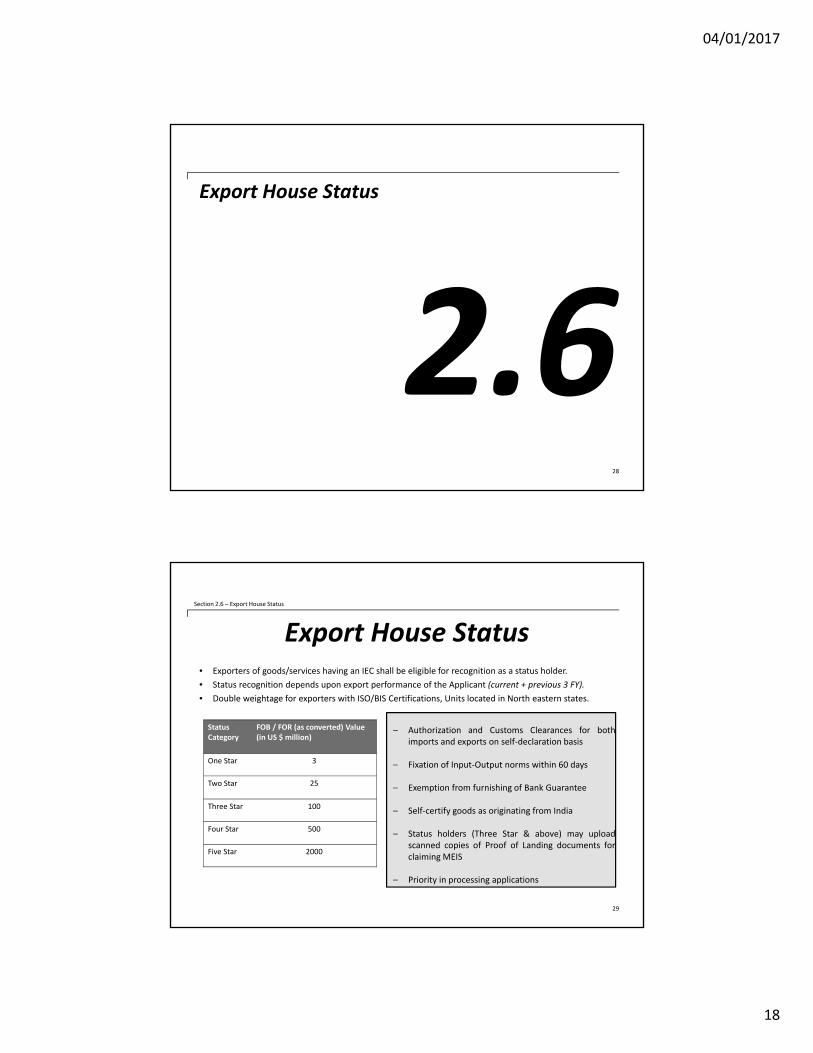

Export House Status• Exporters of goods/services having an IEC shall be eligible for recognition as a status holder.• Status recognition depends upon export performance of the Applicant (current + previous 3 FY).• Double weightage for exporters with ISO/BIS Certifications, Units located in North eastern states.

29

Section 2.6 – Export House Status

Status Category

FOB / FOR (as converted) Value(in US $ million)

One Star 3

Two Star 25

Three Star 100

Four Star 500

Five Star 2000

− Authorization and Customs Clearances for bothimports and exports on self‐declaration basis

− Fixation of Input‐Output norms within 60 days

− Exemption from furnishing of Bank Guarantee

− Self‐certify goods as originating from India

− Status holders (Three Star & above) may uploadscanned copies of Proof of Landing documents forclaiming MEIS

− Priority in processing applications

04/01/2017

19

Duty Exemption Schemes

30

Advance Authorisation (AA) – For Inputs• Duty free procurement of inputs that are physically to be incorporated in the

export product.

• Available for Manufacturer Exporter or Merchant exporter tied up with aSupporting manufacturer.

• Physical exports (including SEZ), Supplies to EOU/EHTP/BTP & IntermediarySupply eligible for AA.

• Inputs are subject to Actual User Condition.

• Minimum value addition should be 15%.

• Authorisation valid for a period of 12 months from the ‘Date of issue’

• EO to be fulfilled within 18 months from the date of issued of authorisation.

31

Section 3 – Duty Exemption Schemes

AA for Annual Procurement !

04/01/2017

20

Export Promotion Capital Goods Scheme (EPCG) –For Capital Goods

• Duty free procurement of capital goods for Pre‐production, Production & Post‐production.

• Available for Manufacturer Exporter, Merchant exporter tied up with a Supporting manufacturer andService Provider.

• Authorisation valid for a period of 18 months from the ‘date of issue’.

• Goods are subject to actual user condition.

• Nexus to be established between capital goods and exports.

• Procurement of goods under EPCG scheme is subject to fulfilment of:

− Export Obligation− Average Export Obligation

• Not available for procurement of second hand capital goods.

• EPCG annual requirement – Not possible!!!

32

Section 3 – Duty Exemption Schemes

Opportunity for CAs

• Cost reduction for the Exporters

• Additional Benefits for the Exporters

• Certification on Forex Earnings

• Certification for the Export House Status

‐‐‐‐ Thank you ‐‐‐‐

TR Srinivasan FCA, Ph No.: 9789976079;

32

Section 3 – Duty Exemption Schemes