Embed Size (px)

Citation preview

Cementos ArgosCorporate presentation

December, 2019

Growing multinational, producer of building materials with focus on value creation

Successful track-record deploying

a disciplined expansion strategy

Value generation by

closing efficiency gaps:

BEST program

Healthy financial position

and flexibility to pursue growth

The best footprint

in the Americas

Segmented value proposition

for market differentiation1 2 3

4 5

The best footprint in the Americas

23M MTCement installed capacity

RMC installed capacity

16 M M3

Colombia

USA

Caribbean and Central America

▪ Logistic synergies

▪ Balance between emerging and developed economies

▪ Markets with high growth potential

▪ Negative correlation between economic cycles

Interconnected footprint to maximize value generation

Operating EBITDA by

region*

Revenues by

segment*

Revenues by

region*

*LTM figures, EBITDA without IFRS 16

Cement; 61%

RMC; 39%

74%

22%

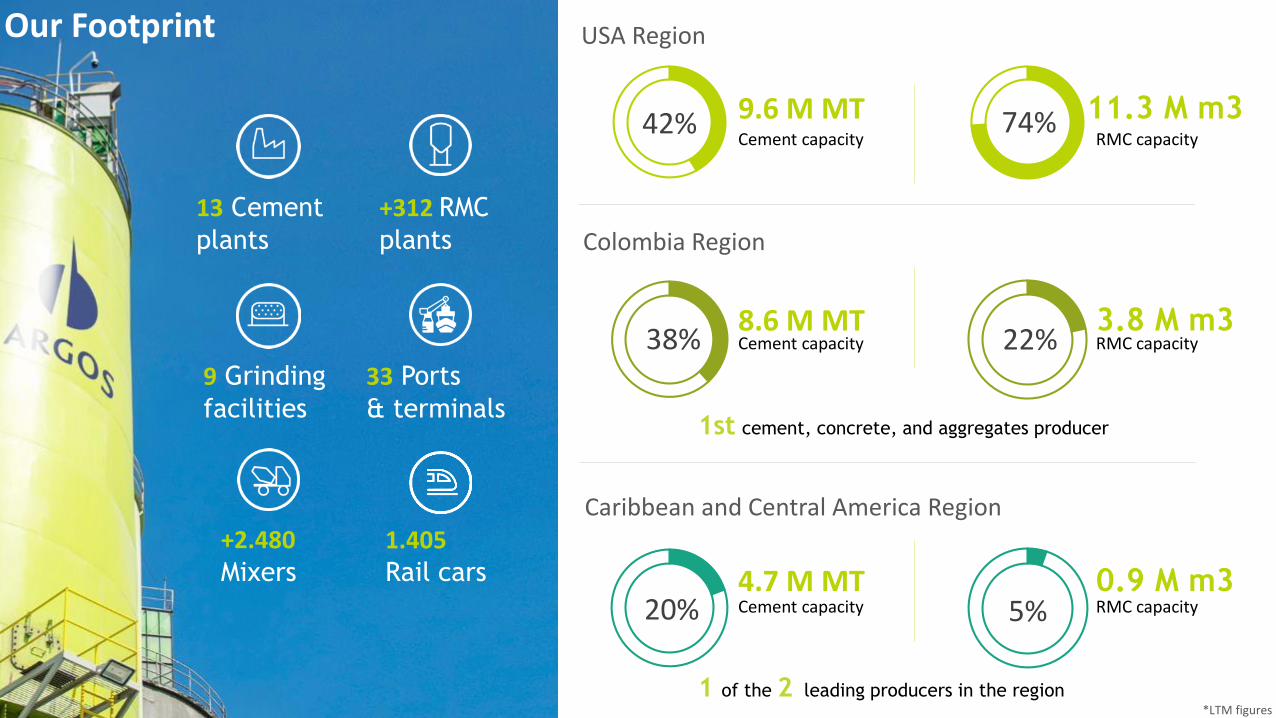

0.9 M m3RMC capacity5%

Caribbean and Central America Region

Colombia Region

USA Region

13 Cement

plants

+312 RMC

plants

9 Grinding

facilities

33 Ports

& terminals

+2.480 Mixers

1.405Rail cars

Our Footprint

Cement capacity

9.6 M MT 11.3 M m3RMC capacity

1st cement, concrete, and aggregates producer

8.6 M MTCement capacity

3.8 M m3RMC capacity

4.7 M MTCement capacity

1 of the 2 leading producers in the region*LTM figures

42%

38%

20%

6

Cement plants

RMC plants

Grinding facilities

Ports/Terminals

US Region: Recovery drives operational growth and EBITDA margin normalization

USD 78.3 MUSD 391 M4Q19 Revenues 4Q19 EBITDA*

20%4Q19 EBITDA margin*

Strategic location close to growing demand centers

Interconnected and privileged assets network:

Imports potential:

Leadership, with relevant market share

Focus on urban centers in RMC business

1.274 rail cars 36% cement sales to RMC operations

9 Ports 5.5 M Tons capacity

Value generation through innovation15 VASP** and/or LEED products

*EBITDA and EBITDA margin under IFRS 16

**Value Added Specialized Products

Construction drivers

Installed Capacity Cement

11.3 M M39.6M MTRMC

Infrastructure ResidentialCommercial

Positive macro fundamentals and reduction in interest rates maintains market stability

Plans at state level materializing

Evident infrastructure needs

Positive momentum in the segment with more relative importance for Argos

COLOMBIA Region: National coverage offers a strong competitive advantage to capture infrastructure and housing growth

COP 157.2 BnCOP 604.1 Bn 26.0%

4Q19 Revenues 4Q19 EBITDA* 4Q19 EBITDA margin

Cement plants

RMC plants

Ports/Terminals

7 Cement plants

1 Port

48 RMC plants

8.7M MT 3.8M M3

Installed Capacity

Cement RMC

Multi-plant player, present across the country with the best logistic interconnection

+9,000 clients in retail segment

Presence in 801 municipalities (71% of the total territory)

15% of the country’s load is mobilized by Argos

+5,700 hardware stores trust us

Differentiated value proposition for the industrial and retail segment

Efficiency and competitiveness

Reduction of more USD 12/MT in 2017 through BEST

30% of revenues generated by innovative products in 2018

*Operating EBITDA y EBITDA margin under IFRS 16

Infrastructure drives construction for Argos strongest segment

Government strategies seek to boost the social housing and reduce inventory levels in regular housing segment

Leaders with more than 80 years of history and broad presence

Reduced imports and macro stability support price recovery

8

Tailor made business model

Positive moment of the market in Dominican Republic: Puerto Rico Reconstruction Plan underway:

7% of GDP growth in 2018

Growth economic activity year to day

5.9% Feb-19 USD 20 BnFunds approved in 1Q19 for reconstruction.

Reconstruction needs estimated at USD 139 Bn

Trading and vertical integration through the Caribbean Sea

47% market share in clinker and cement trading

Transport synergies through an interconnected network of ports, terminals and grinding facilities

11 puertos y terminales

Logistic flexibility

Supply to the Region from plant in Cartagena

Region with the highest ROCE (double digit)

Sources: Banco Central de la República Dominicana, US Department of Housing and Urban Development

*EBITDA y EBITDA margin under IFRS 16

4.7M MTCement RMC

0.9M M3

Installed Capacity

Caribbean and Central America Region: Presence in diversified markets offers flexibility

USD 28.5 MUSD 118 M 24.2%

4Q19 Revenues 4Q19 EBITDA* 4Q19 EBITDA margin

Cement plants

RMC plants

Grinding facilities

Ports/Terminals

Value generation through efficiency:

BEST Program

10

BESTBuilding efficiency and

sustainability for tomorrow Operational

transformation

Alternative

fuels

Reduction of

non core assetsAdministrative

synergies

Clinker to

cement ratio

Leaner and faster Improve ROCE Cost champions Sustainability leadersCustomer centered

11

What have we done?

What are we doing?:

+USD 530M

▪ Working capital optimization

▪ Capex optimization

▪ Additional divestments of non-core assets

▪ Growth through allies (Eg. Agregados Argos)

▪ Increase the operating free cash flow

▪ Fire power to grow

▪ ROCE improvement

▪ Focus on core assets

Goals:

divestments

BEST: Optimization of our assets base as a growth lever

Reduce leverage: 3.2x Net debt / EBITDA + dividends by end of 2020

12

Logistics

BEST: Next steps

Cement: Improvement of

capacity utilization

RMC Network &

Fleet optimization

Supply chain &

logistics

Drivers shortage

Building Efficiency and Sustainability

for Tomorrow

BEST USA 2.0

Energetics

Segmented value proposition

for market differentiation

14

Differentiated value propositionValue added for our customers

Experience and track record

+80 years of experience

Technical Know-how

Participation on emblematic projects in the Americas

Tailor-made service

Tailor-made products and processes

Innovative products

Microcement, advanced concrete, among others

Confidence and backup

Technical experts in high complexity projects

Customer centric

Constant focus on our customers needs

Knowledge transference

Constant training to our customers and suppliers

Accessibility

Presence in +15 countries, 14 states in the USA and

+800 municipalities in Colombia

QualityHigh quality product portfolio

Reputation

DJSI and Merco Colombia supports our trajectory, responsibility and commitment

Industrial Segment Retail Segment

Customer ally Recognized brand Privileged and interconnected network of assets+ +

v

...contributing to the productivity of our customers projects

Argos, at the forefront of the industry´s digital revolution.

▪ Self service from beginning to end

▪ Make online orders

▪ Track the delivery of orders

▪ Generate quality reports

▪ Visualize historical transactions

▪ Make online payments

Successful track-record deploying a

disciplined growth strategy

17

+USD 4.3Bn invested in the last 10 years

13%CAGR revenues

2012-2018

9%CAGR EBITDA

2012-2018

EBITDA* (COP billion)Revenue (COP billion)

USD M 482385 447 524 484 553 547

+ +

Organic growth

▪ 2005: Merge of 8 cement companies in

Colombia

▪ 2012: Non-cement assets spin-off

▪ 2016: BEST as a program to maximize

competitivity

Disciplined growth strategy Boosting the EBITDA growth and value generation

Puerto Rico USD 8 M

West Virginia USD 660 MPuerto Rico terminal USD 18 MFrench Guiana USD 69 MVulcan FL USD 720 MLafarge Honduras USD 305 MLafarge USA USD 760 MHolcim Caribbean USD 157 MRMCC USA USD 243 MCemento Andino USD 192 MSSC USA USD 245 M

Acquisitions

Cartagena USD 560M

Rioclaro USD 93M

Energy plants in Colombia USD 68M

Panama grinding facility expansion USD 65M

Harleyville VCM USD 58M

Cartagena´s distribution center USD 35M

White cement conversion USD 23M

Oil-well cement development USD 1M

Note: COLGAAP figures 2010-2013, IFRS figures 2014-2019

USD M 2,437 2,656 2,833 2,881 2,790 2,892 2,848

* Operating EBITDA without adoption of IFRS 16: excluding, among others, non-recurring income related to the sale of self-generators in Colombia (COP 27 BN 4Q19) and land valuation in Colombia (COP 25 BN 4Q19)

(organic and inorganic)

Focus and reorganization

4.3804.968

5.817

7.9128.597 8.586 8.418

9.375

2012 2013 2014 2015 2016 2017 2018 2019

2,856

791

978 968

1.519

1.672

1.481 1.486 1.536

18,1%19,7%

16,6%19,2% 19,4%

17,2% 17,7% 16,4%

2012 2013 2014 2015 2016 2017 2018 2019

468

2.218 2.503

2.108 2.348

-

1.000

2.000

3.000

4.000

5.000

6.000

2018 2019

3Q 4Q

425 388

413 421

-

100

200

300

400

500

600

700

800

900

2018 2019

3Q 4Q

Track record of successfully implementing a disciplined growth strategy

WV, USA – Heidelberg (2016)

USD 660M

Cement Plant 2.2 M MT

Terminals 8 Florida, USA – Vulcan Cement Investment (2014)

USD 720M

Cement Plant 1.6 M MT

Ports

Grinding facilities 1.9 M MT

RMX 3.3 M m3

Blocks 109 M units / year

2

French Guiana – Lafarge (2014)

€50M

Grinding Facility 0.2 M MT

(100% ownership)

Port concession

€231 M

Cement Plant

Grinding facility

1.0 M MT

0.3 M m3

(53% ownership)

Puerto Rico

2015: USD18.3M

Port

(60% ownership)

2017: USD 8M(60% ownership)

Cement Plant

0.6 M MT

USA – Lafarge (2011)

USD 760M

Honduras – Lafarge (2013)

Colombia

USA

Caribbean and Central America

Ports & terminals

Grinding facilities 1

RMX 79 plants

6

Cement Plant 2

Healthy financial position and

flexibility to pursue growth

20

Match between currencies and EBITDA generation and competitive cost of debt

Extended debt’s average life for enhanced flexibility

Expedite access to the Colombian capital markets

▪ Recognized as a recurrent issuer

Local and international banks

Stock portfolio provides additional flexibility

▪ Two types of shares (CEMARGOS and PFCEMARGOS)

Debt Structure per currency (December 2019)

Access to diverse sources of financial flexibility

▪ Grupo Sura: 6% (Common share)

Flexible debt structure and access to funding sources to finance growth

Cost of debt:

▪ 7.6% COP

▪ 4.1% USD

310 300 211420

121303

159312 388

184 126

401

165

999983

0

0

0

19

2620

00

0

0

200

400

600

800

1.000

1.200

1.400

2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2038 2042

Bonds Banks

21

Delivering on our plan to reduce leverage

▪ Non Core assets divestment plan

▪ Capex Optimization

▪ Working capital improvement

▪ EBITDA growth

3.2x Net debt / EBITDA

www.argos.co/ir

[email protected] recognition, given by the Colombian Stock

Exchange, does not certify the quality of the registered

stock, nor does it guarantee the solvency of the issuer.