Embed Size (px)

Citation preview

1

Preparing your Practice and Clients for the Super Changes

Mark Ellem - SuperConceptsSession 1

What you need to knowThis content of this presentation has been prepared to provide you with generalinformation only. It is not intended to take the place of professional advice and youshould not take action on specific issues in reliance on this information. In preparingthis information, we did not take into account the investment objectives, financialsituation or particular needs of any particular person. Before making an investmentdecision, you need to consider (with or without the assistance of an adviser) whetherthis information is appropriate to your needs, objectives and circumstances. You shouldobtain a copy of the relevant Product Disclosure Statement (PDS) before making adecision to invest in any financial product.

Any advice in this presentation is provided by SMSF Administration Solutions Pty Ltd,ACN 097 695 988, AFSL No. 291195 which is part of the AMP group of companies.

2

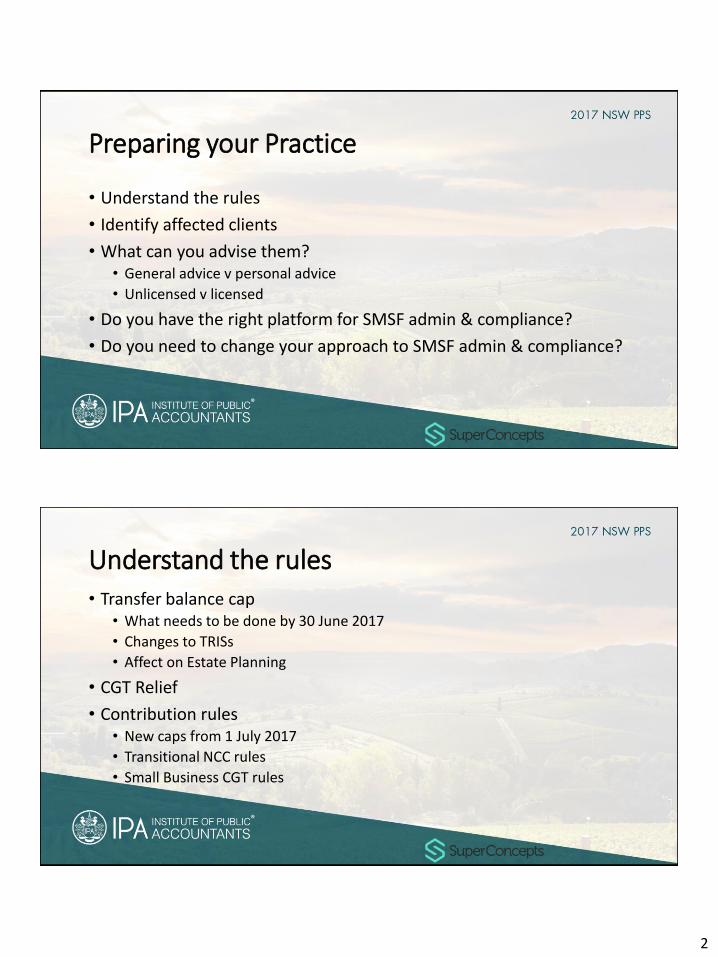

Preparing your Practice

• Understand the rules

• Identify affected clients

• What can you advise them?• General advice v personal advice

• Unlicensed v licensed

• Do you have the right platform for SMSF admin & compliance?

• Do you need to change your approach to SMSF admin & compliance?

Understand the rules• Transfer balance cap

• What needs to be done by 30 June 2017

• Changes to TRISs

• Affect on Estate Planning

• CGT Relief

• Contribution rules• New caps from 1 July 2017

• Transitional NCC rules

• Small Business CGT rules

3

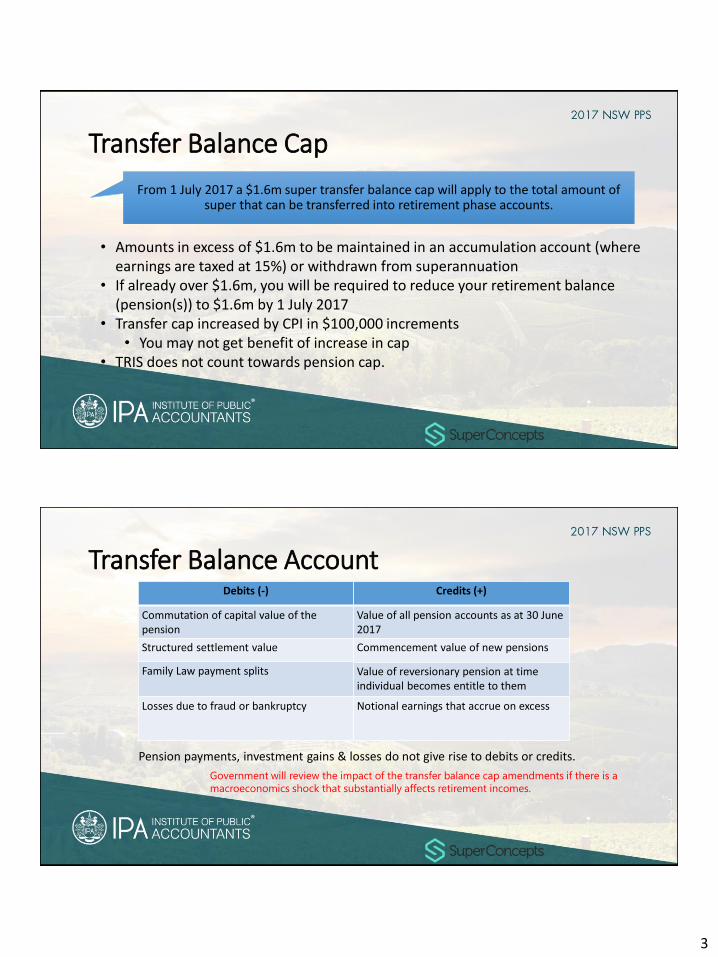

Transfer Balance Cap

From 1 July 2017 a $1.6m super transfer balance cap will apply to the total amount of super that can be transferred into retirement phase accounts.

• Amounts in excess of $1.6m to be maintained in an accumulation account (where earnings are taxed at 15%) or withdrawn from superannuation

• If already over $1.6m, you will be required to reduce your retirement balance (pension(s)) to $1.6m by 1 July 2017

• Transfer cap increased by CPI in $100,000 increments• You may not get benefit of increase in cap

• TRIS does not count towards pension cap.

Transfer Balance Account

Pension payments, investment gains & losses do not give rise to debits or credits.

Credits (+)

Value of all pension accounts as at 30 June 2017

Commencement value of new pensions

Value of reversionary pension at time individual becomes entitle to them

Notional earnings that accrue on excess

Debits (-)

Commutation of capital value of the pension

Structured settlement value

Family Law payment splits

Losses due to fraud or bankruptcy

Government will review the impact of the transfer balance cap amendments if there is a

macroeconomics shock that substantially affects retirement incomes.

4

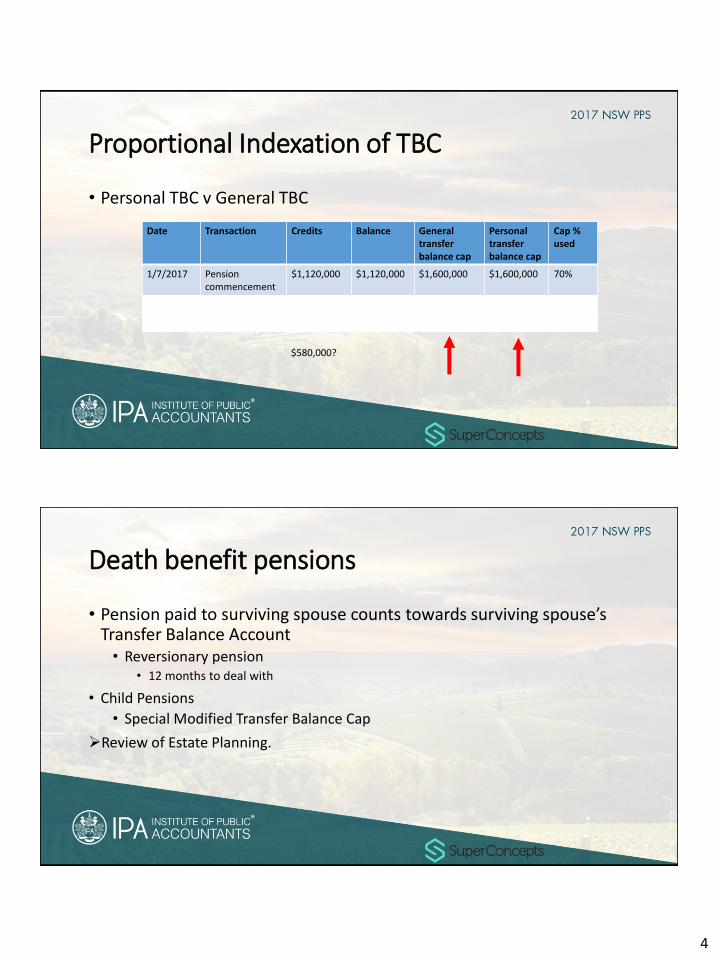

Proportional Indexation of TBC

• Personal TBC v General TBC

Date Transaction Credits Balance General transfer balance cap

Personal transfer balance cap

Cap % used

1/7/2017 Pension commencement

$1,120,000 $1,120,000 $1,600,000 $1,600,000 70%

31/7/2023 Pension commencement

$510,000 $1,630,000 $1,700,000 $1,630,000 100%

$580,000?

Death benefit pensions

• Pension paid to surviving spouse counts towards surviving spouse’s Transfer Balance Account• Reversionary pension

• 12 months to deal with

• Child Pensions

• Special Modified Transfer Balance Cap

Review of Estate Planning.

5

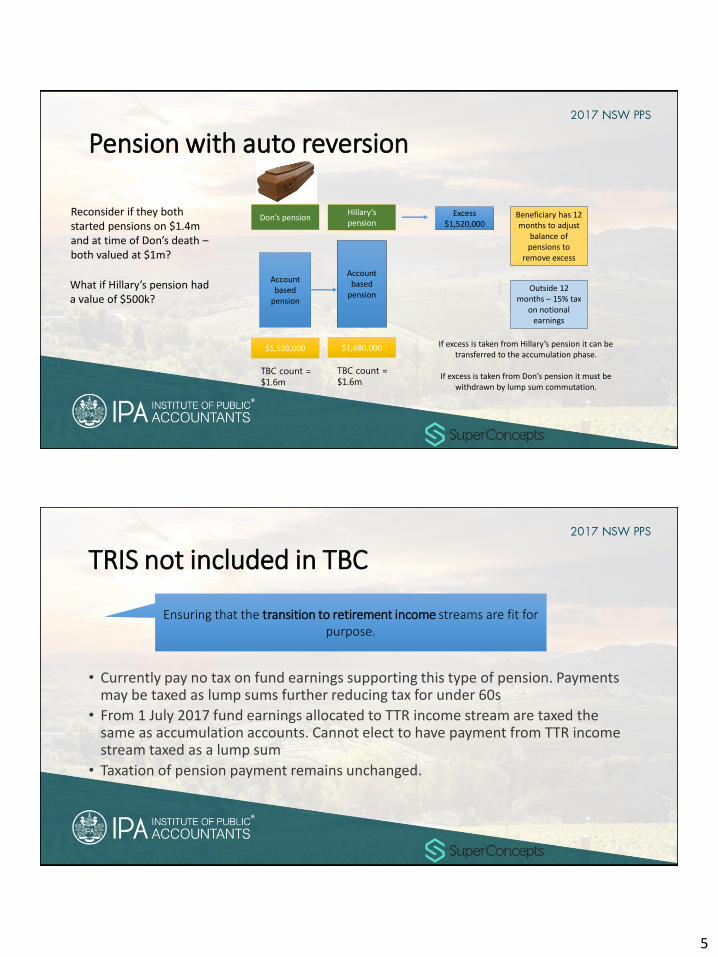

Pension with auto reversion

Account based

pension

Account based

pension

$1,520,000 $1,680,000

Beneficiary has 12 months to adjust

balance of pensions to

remove excess

Outside 12 months – 15% tax

on notional earnings

Excess $1,520,000

If excess is taken from Hillary’s pension it can be transferred to the accumulation phase.

If excess is taken from Don’s pension it must be withdrawn by lump sum commutation.

Don’s pensionHillary’s pension

TBC count =

$1.6m

TBC count =

$1.6m

Reconsider if they both started pensions on $1.4m and at time of Don’s death –both valued at $1m?

What if Hillary’s pension had a value of $500k?

TRIS not included in TBC

• Currently pay no tax on fund earnings supporting this type of pension. Payments may be taxed as lump sums further reducing tax for under 60s

• From 1 July 2017 fund earnings allocated to TTR income stream are taxed the same as accumulation accounts. Cannot elect to have payment from TTR income stream taxed as a lump sum

• Taxation of pension payment remains unchanged.

Ensuring that the transition to retirement income streams are fit for purpose.

6

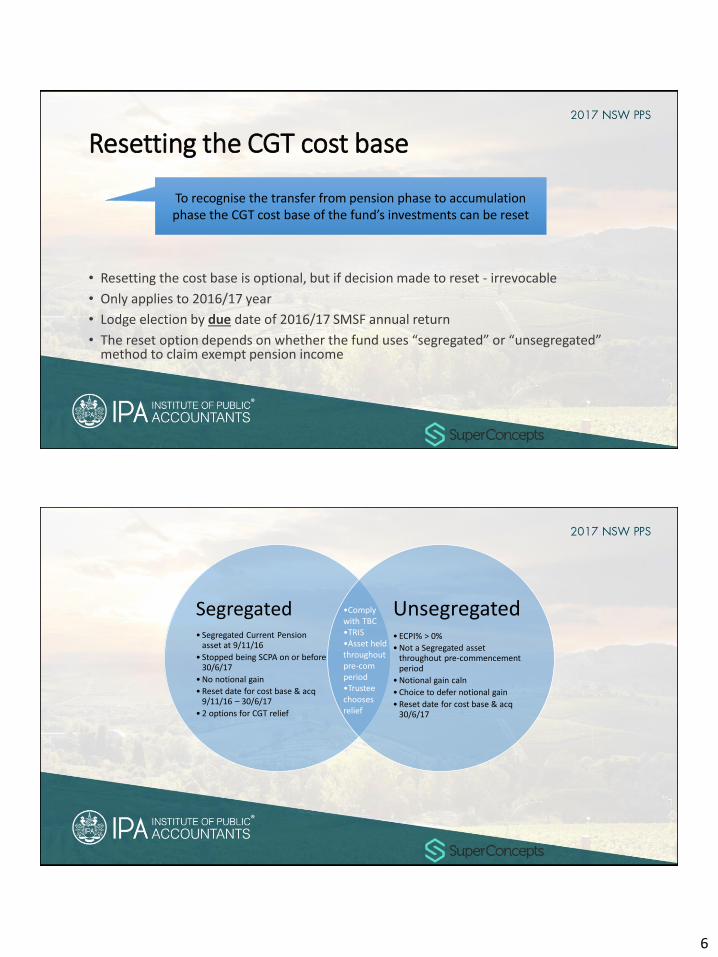

Resetting the CGT cost base

• Resetting the cost base is optional, but if decision made to reset - irrevocable

• Only applies to 2016/17 year

• Lodge election by due date of 2016/17 SMSF annual return

• The reset option depends on whether the fund uses “segregated” or “unsegregated” method to claim exempt pension income

To recognise the transfer from pension phase to accumulation phase the CGT cost base of the fund’s investments can be reset

Segregated• Segregated Current Pension

asset at 9/11/16

• Stopped being SCPA on or before 30/6/17

• No notional gain

• Reset date for cost base & acq 9/11/16 – 30/6/17

• 2 options for CGT relief

Unsegregated• ECPI% > 0%

• Not a Segregated asset throughout pre-commencement period

• Notional gain caln

• Choice to defer notional gain

• Reset date for cost base & acq 30/6/17

•Comply with TBC•TRIS•Asset held throughout pre-com period•Trustee chooses relief

7

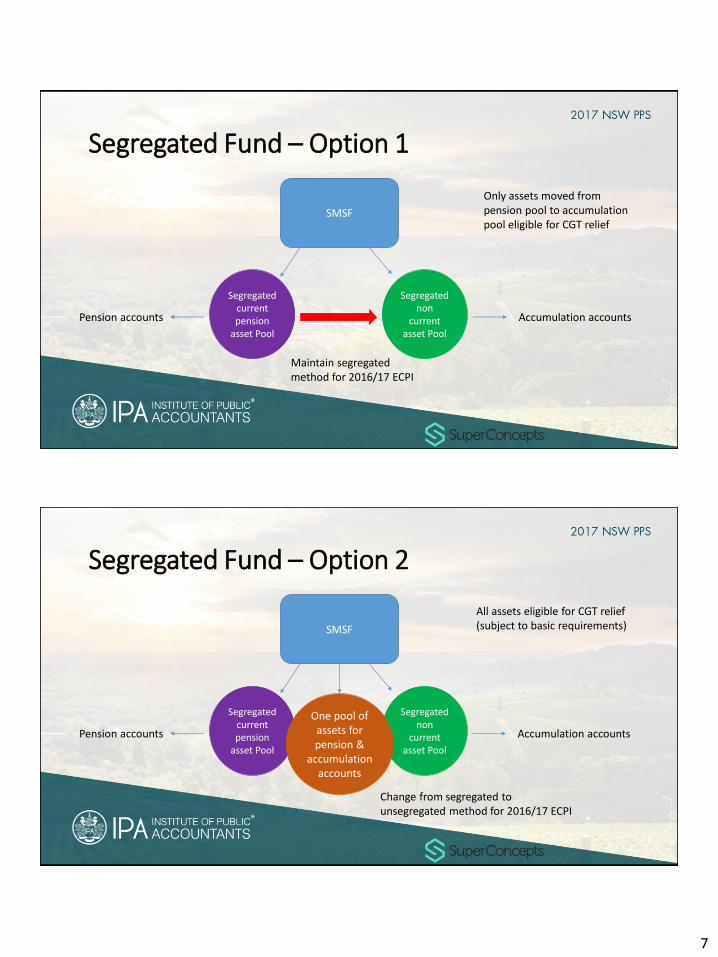

Segregated Fund – Option 1

SMSF

Segregated current pension

asset Pool

Segregated non

current asset Pool

Only assets moved from pension pool to accumulation pool eligible for CGT relief

Maintain segregated method for 2016/17 ECPI

Pension accounts Accumulation accounts

Segregated Fund – Option 2

SMSF

Segregated current pension

asset Pool

Segregated non

current asset Pool

All assets eligible for CGT relief (subject to basic requirements)

Change from segregated to unsegregated method for 2016/17 ECPI

Pension accounts Accumulation accounts

One pool of assets for pension &

accumulation accounts

8

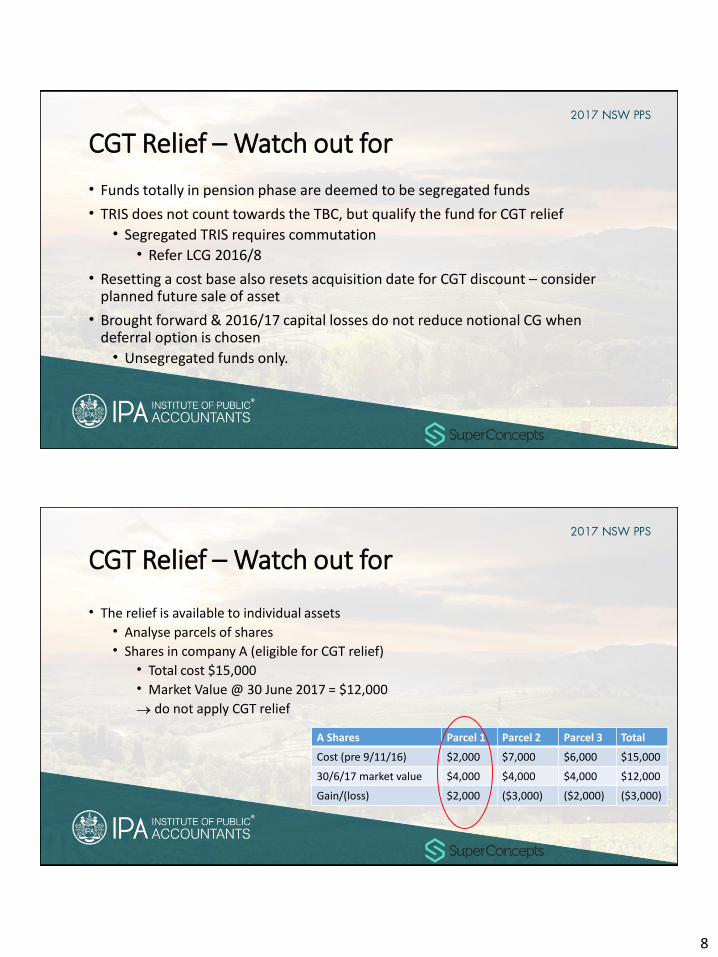

CGT Relief – Watch out for

• Funds totally in pension phase are deemed to be segregated funds

• TRIS does not count towards the TBC, but qualify the fund for CGT relief• Segregated TRIS requires commutation

• Refer LCG 2016/8

• Resetting a cost base also resets acquisition date for CGT discount – consider planned future sale of asset

• Brought forward & 2016/17 capital losses do not reduce notional CG when deferral option is chosen

• Unsegregated funds only.

CGT Relief – Watch out for

• The relief is available to individual assets• Analyse parcels of shares• Shares in company A (eligible for CGT relief)

• Total cost $15,000• Market Value @ 30 June 2017 = $12,000

do not apply CGT relief

A Shares Parcel 1 Parcel 2 Parcel 3 Total

Cost (pre 9/11/16) $2,000 $7,000 $6,000 $15,000

30/6/17 market value $4,000 $4,000 $4,000 $12,000

Gain/(loss) $2,000 ($3,000) ($2,000) ($3,000)

9

CGT Relief – Watch out for

• Level of ECPI% in future years (unsegregated funds)• 2016/17 ECPI% = 65%• 2019/20 ECPI% = 85%

• Part IVA application

• Segregated method to claim ECPI will be restricted from 2017/18 income year

• Lodge 2016/17 return by due date

• SMSF accounting and admin platform to record application of CGT relief & deferred notional capital gain

Contributions

• Maximise concessional caps in 2016/17• Drops to $25,000 2017/18 for all

• 2016/17 “reserved” contribution limited to $25,000

• Maximise non concessional caps in 2016/17• No $1.6m eligibility test

• Close out bring forward NCC by 30 June 2017 lower transitional NCC• Triggered 2015/16 $460,000

• Triggered 2016/17 $380,000

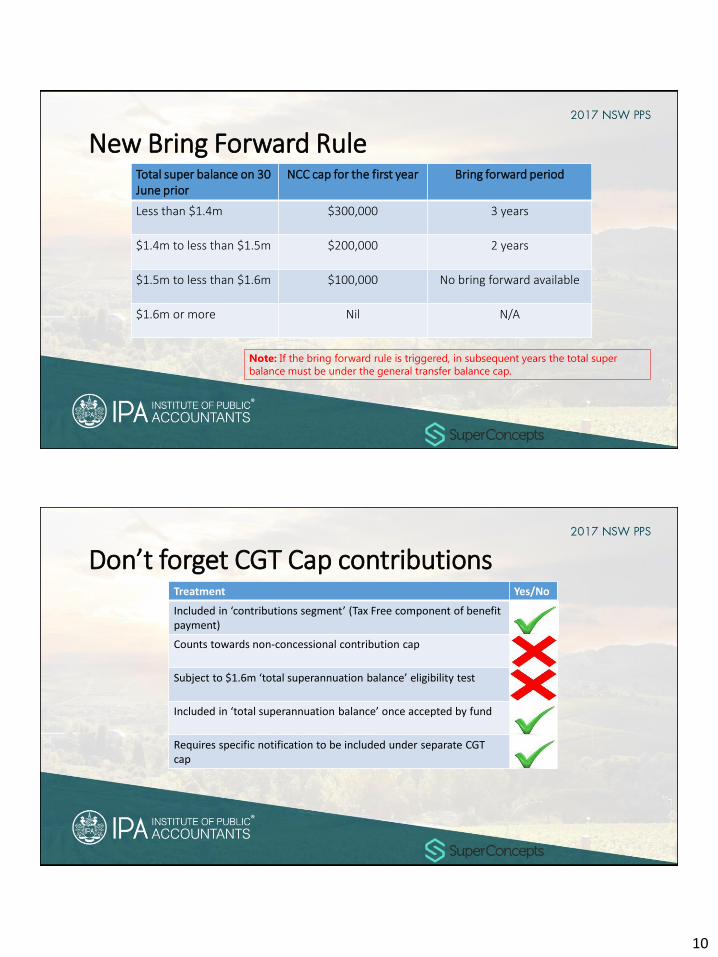

10

New Bring Forward RuleTotal super balance on 30 June prior

NCC cap for the first year Bring forward period

Less than $1.4m $300,000 3 years

$1.4m to less than $1.5m $200,000 2 years

$1.5m to less than $1.6m $100,000 No bring forward available

$1.6m or more Nil N/A

Note: If the bring forward rule is triggered, in subsequent years the total super

balance must be under the general transfer balance cap.

Don’t forget CGT Cap contributionsTreatment Yes/No

Included in ‘contributions segment’ (Tax Free component of benefit payment)

Counts towards non-concessional contribution cap

Subject to $1.6m ‘total superannuation balance’ eligibility test

Included in ‘total superannuation balance’ once accepted by fund

Requires specific notification to be included under separate CGT cap

11

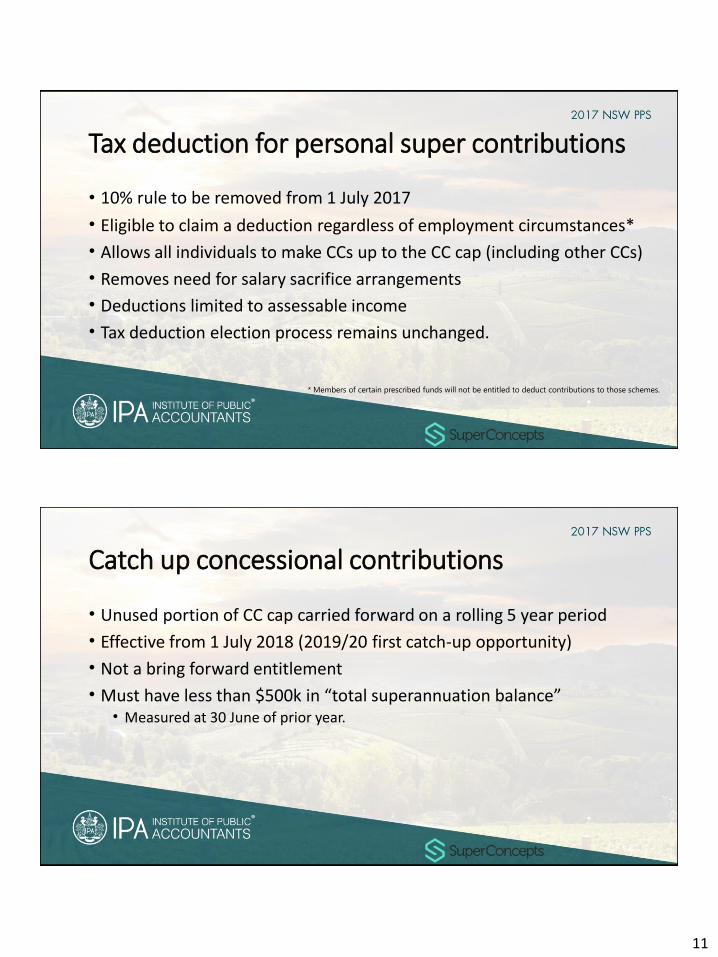

Tax deduction for personal super contributions

• 10% rule to be removed from 1 July 2017

• Eligible to claim a deduction regardless of employment circumstances*

• Allows all individuals to make CCs up to the CC cap (including other CCs)

• Removes need for salary sacrifice arrangements

• Deductions limited to assessable income

• Tax deduction election process remains unchanged.

* Members of certain prescribed funds will not be entitled to deduct contributions to those schemes.

Catch up concessional contributions

• Unused portion of CC cap carried forward on a rolling 5 year period

• Effective from 1 July 2018 (2019/20 first catch-up opportunity)

• Not a bring forward entitlement

• Must have less than $500k in “total superannuation balance”• Measured at 30 June of prior year.

12

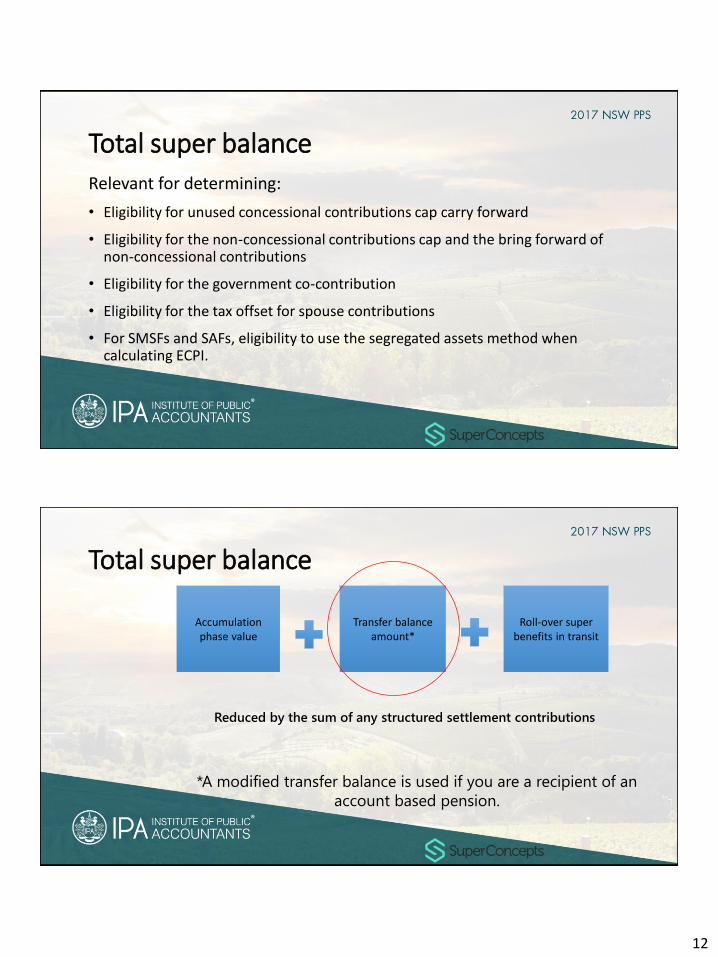

Total super balance

Relevant for determining:

• Eligibility for unused concessional contributions cap carry forward

• Eligibility for the non-concessional contributions cap and the bring forward of non-concessional contributions

• Eligibility for the government co-contribution

• Eligibility for the tax offset for spouse contributions

• For SMSFs and SAFs, eligibility to use the segregated assets method when calculating ECPI.

Total super balance

Accumulation phase value

Transfer balance amount*

Roll-over super benefits in transit

*A modified transfer balance is used if you are a recipient of an

account based pension.

Reduced by the sum of any structured settlement contributions

13

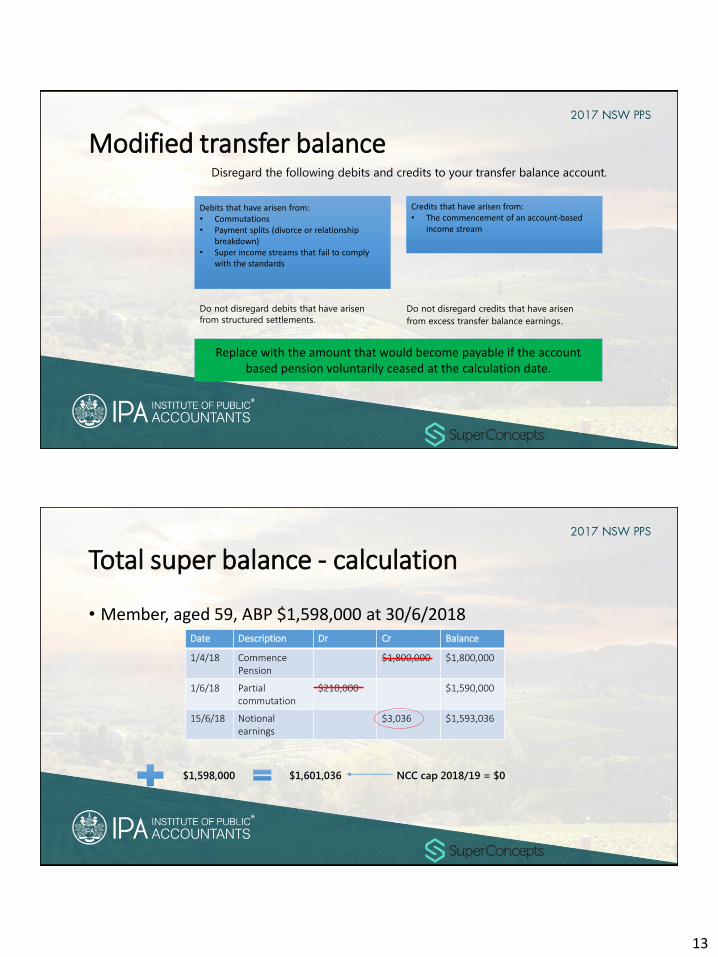

Modified transfer balanceDisregard the following debits and credits to your transfer balance account.

Credits that have arisen from:• The commencement of an account-based

income stream

Debits that have arisen from:• Commutations• Payment splits (divorce or relationship

breakdown)• Super income streams that fail to comply

with the standards

Do not disregard credits that have arisen

from excess transfer balance earnings.

Replace with the amount that would become payable if the account based pension voluntarily ceased at the calculation date.

Do not disregard debits that have arisen

from structured settlements.

Total super balance - calculation

• Member, aged 59, ABP $1,598,000 at 30/6/2018Date Description Dr Cr Balance

1/4/18 Commence Pension

$1,800,000 $1,800,000

1/6/18 Partial commutation

$210,000 $1,590,000

15/6/18 Notional earnings

$3,036 $1,593,036

$1,598,000 $1,601,036 NCC cap 2018/19 = $0

14

Other changes

• Reduction of Div 293 threshold

• Abolition of anti-detriment payment

• Increase threshold for $540 tax offset for spouse contribution

• Partial commutation of pension will not count towards min pension

• Amendment to SG maximum base

• Requirement for actuarial certificate for unsegregated fund????

• Special rules for defined benefit capped pensions and child pensions