Embed Size (px)

Citation preview

Preparing for the 2018 USProxy and Annual Reporting Season

Jennifer CarlsonPartner+1 650 331 [email protected]

Michael HermsenPartner+1 312 701 [email protected]

Kristen FordAssociate+1 713 238 [email protected]

Laura RichmanCounsel+1 312 701 [email protected] November 1, 2017

Presenters

2

Jennifer CarlsonPartner

Kristen FordAssociate

Michael HermsenPartner

Laura RichmanCounsel

Overview

• Pay ratio disclosure

• Say-on-pay and other compensation matters

• Proxy access and other shareholder proposals

• Institutional shareholder initiatives

• Trends in proxy disclosure• Trends in proxy disclosure

• Virtual meetings

• Director and officer questionnaires

• Annual report risk factors

• Exhibit hyperlinks and Form 10-K developments

• Certain financial reporting and audit committee matters

• Status of other Dodd-Frank compensation-related rulemaking

3

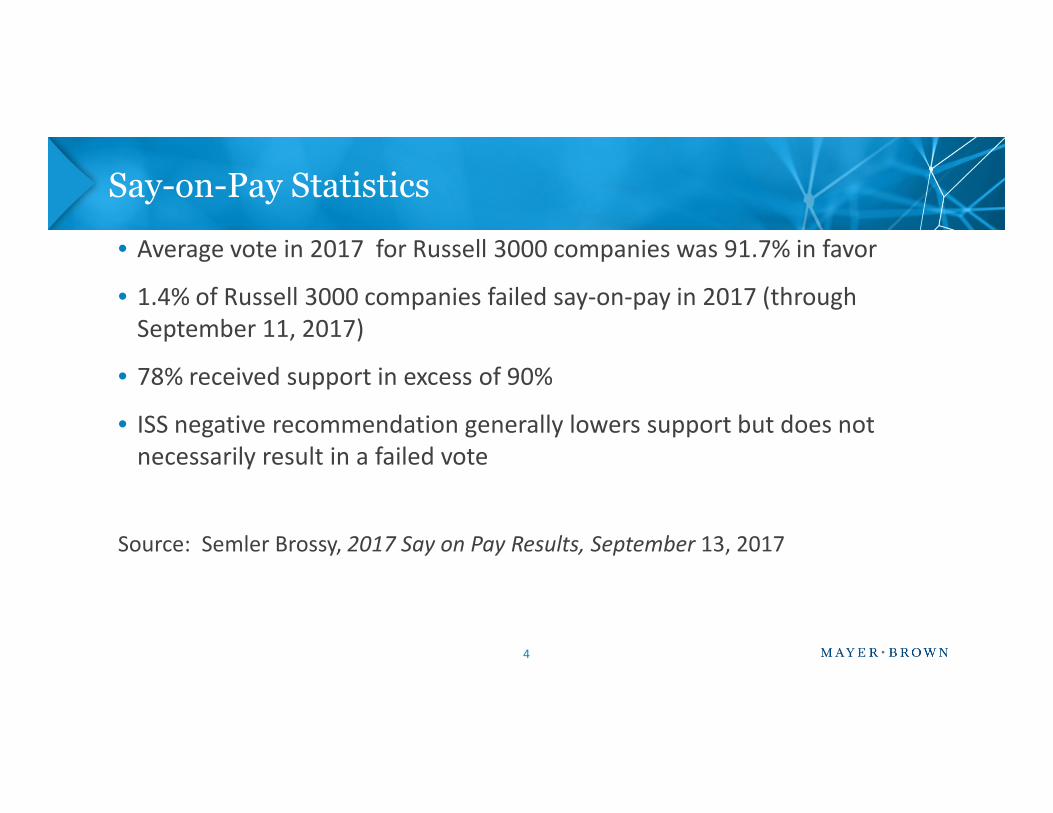

Say-on-Pay Statistics

• Average vote in 2017 for Russell 3000 companies was 91.7% in favor

• 1.4% of Russell 3000 companies failed say-on-pay in 2017 (throughSeptember 11, 2017)

• 78% received support in excess of 90%

• ISS negative recommendation generally lowers support but does notnecessarily result in a failed vote

Source: Semler Brossy, 2017 Say on Pay Results, September 13, 2017

4

Other Compensation-Related Proposals

• Say-When-on-Pay

– Vast majority supported annual voting

• Equity plan voting

– Only a small number of companies failed to win majority support– Only a small number of companies failed to win majority support

– But highest failure rate since mandatory say-on-pay

5

Say-on-Pay and Shareholder Engagement

• A year-round process

• Focused presentations

• Carefully consider who from the company participates

• Obtaining shareholder feedback

– CD&A disclosure of how prior year vote taken into account

– General governance considerations

– Identifying which aspects of the compensation program, if any, raise concern

– Previewing possible changes to the compensation program

6

Engaging with Proxy Advisory Firms

• Engaging with proxy advisory firms

– Regarding interpretations of positions

– Monitoring recommendations for accuracy

• Survey conducted by U.S. Chamber of Commerce’s Center for Capital Markets Competitivenessand Nasdaq found:and Nasdaq found:

– Many public companies find it difficult to have a substantive meeting with a proxy advisory firmregarding recommendations

• May be denied meeting

• May get a phone conversation only

• May only talk to junior analyst

• But some companies have productive meetings

– Outreach rarely leads to a new proxy advisory recommendation7

Disclosure and Presentation Highlights

• Use of proxy statement summaries to highlight say-on-pay

• Hyperlinked table of contents

• Use of graphics and color

• Emphasis on design• Emphasis on design

• Plain English

• Online version

• Filing PDF as well as EDGAR copy with SEC

8

Additional Proxy Statement Elements

• Table of contents and separate sections for CD&A

• Alphabetical index of frequently requested information

• Letter from Board and/or Lead Director

• Q&A with Chairman and/or Lead Director• Q&A with Chairman and/or Lead Director

• Value statement

• Goals description

• Governance graphics as well as compensation graphics

• Supplemental materials

9

Effective CD&A Disclosure for Say-on-Pay Votes

• Satisfying a disclosure obligation versus advocacy for advisory say-on-payvote

• Executive Summary

– Goals of program

– Recent changes

• Table of contents and distinct sections

• Clarifying link between pay and performance

• Use of graphics

10

Response to Prior Year Say-on-Pay Vote

• CD&A requirement

• Often part of a discussion of shareholder engagement

• Might describe changes to compensation program

• Might confirm that compensation committee believes the current

11

• Might confirm that compensation committee believes the currentcompensation program best meets the appropriate goals

Additional Soliciting Materials

• Additional soliciting materials often, but not always, used to respond tonegative proxy advisory recommendations

• Additional soliciting materials are used in other circumstances as well

• Additional soliciting materials must be filed with the SEC

12

• Types of additional soliciting materials include:

– Supplements to proxy statements

– Letters to shareholders

– Slides

– Scripts or talking points

Compensation Lawsuits

• First lawsuits alleged breaches of fiduciary duty following failed say-on-pay

• Second wave alleged insufficient compensation disclosures

– Sought to enjoin the shareholder vote unless the company provided additionalcompensation disclosures

• Lawsuits challenging specific compensation actions; for example, based on failure to comply• Lawsuits challenging specific compensation actions; for example, based on failure to complywith Section 162(m) of the Internal Revenue Code

• Lawsuits regarding outside director compensation

– Court treatment of director awards as self-dealing decisions

– Operative standard of review is entire fairness (rather than business judgment rule)

• Publicity surrounding pay-related lawsuits and settlements may have motivated morestrenuous responses to negative ISS recommendations

13

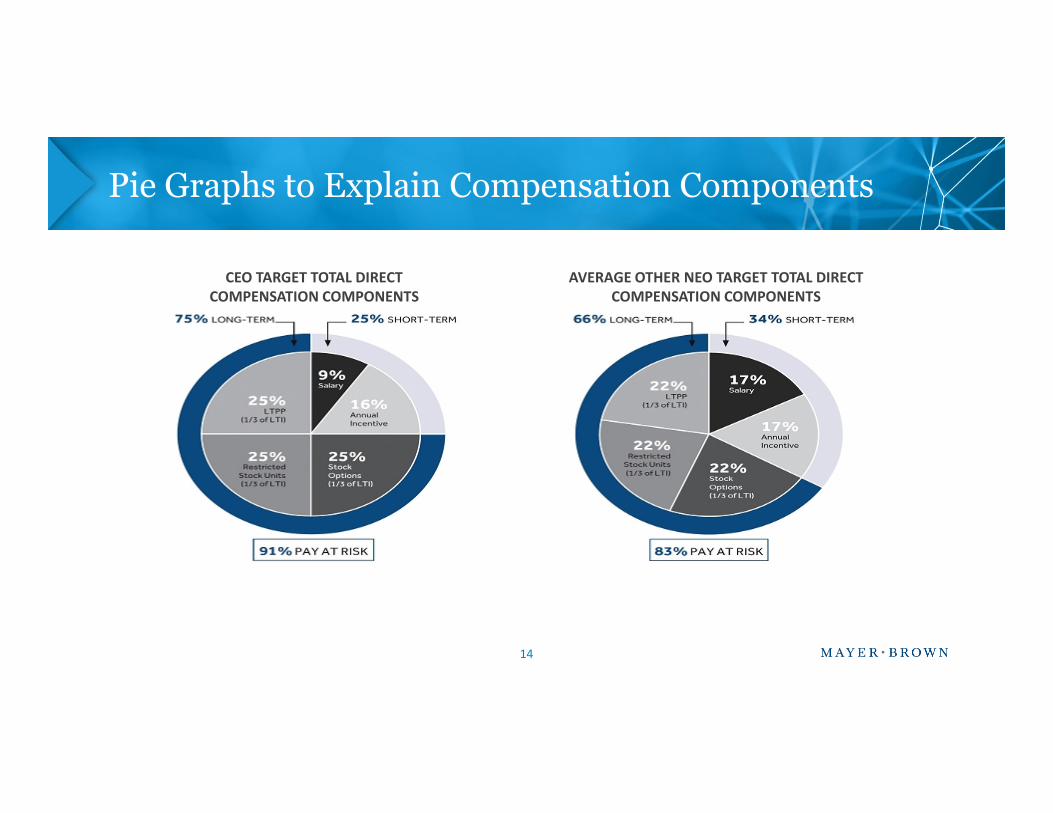

Pie Graphs to Explain Compensation Components

CEO TARGET TOTAL DIRECTCOMPENSATION COMPONENTS

AVERAGE OTHER NEO TARGET TOTAL DIRECTCOMPENSATION COMPONENTS

14

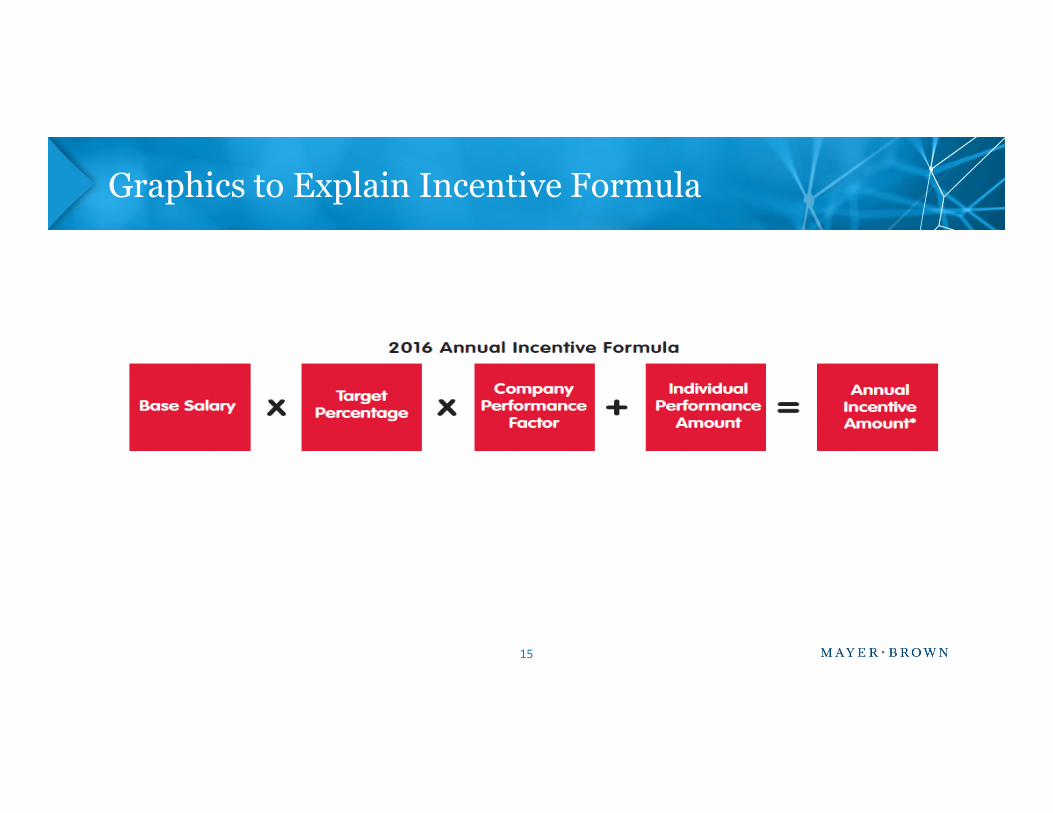

Graphics to Explain Incentive Formula

15

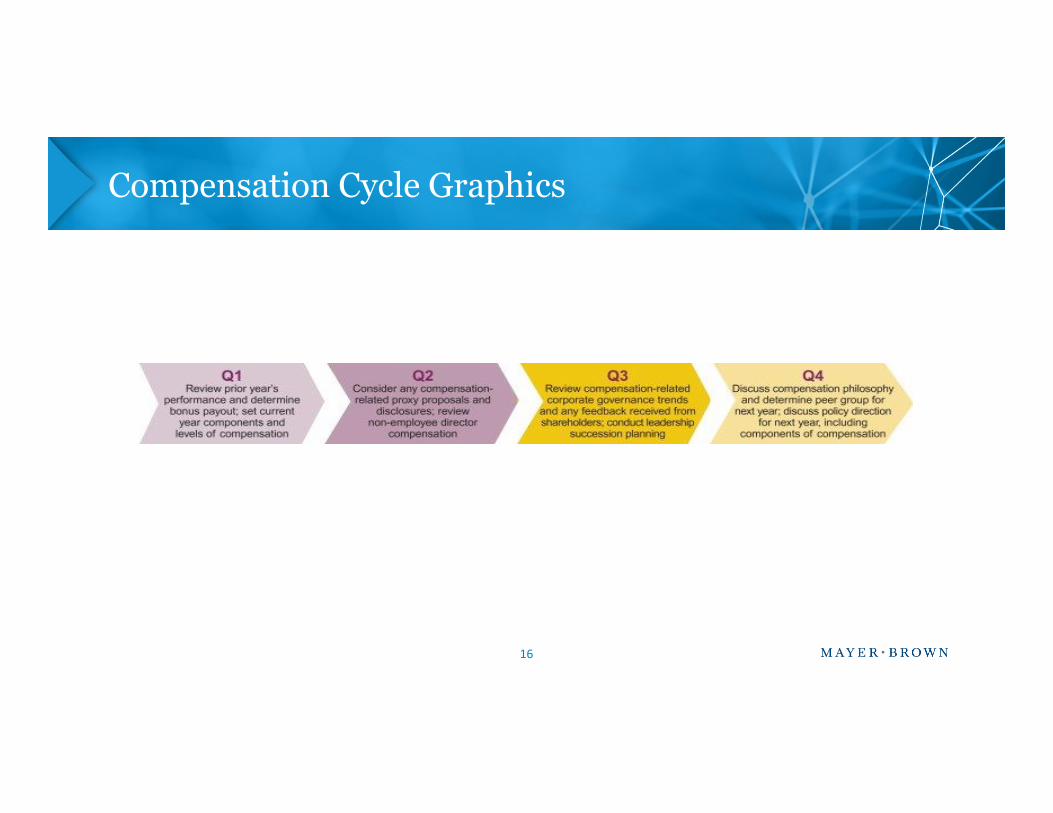

Compensation Cycle Graphics

16

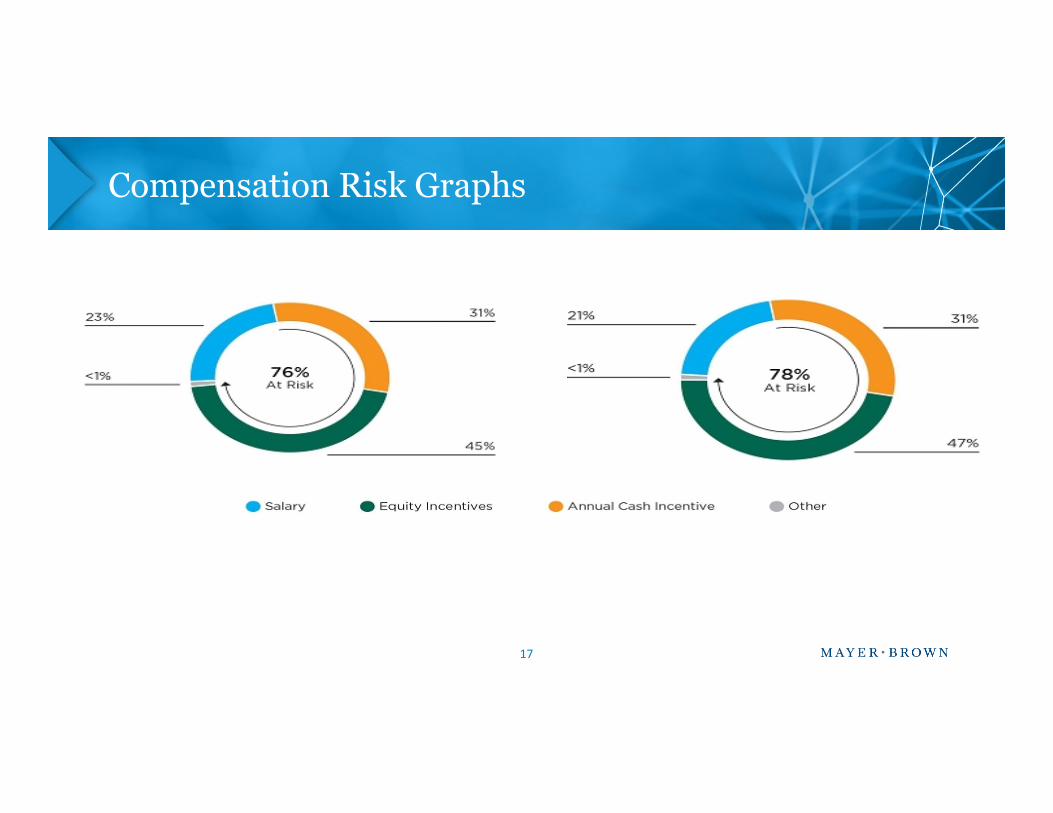

Compensation Risk Graphs

17

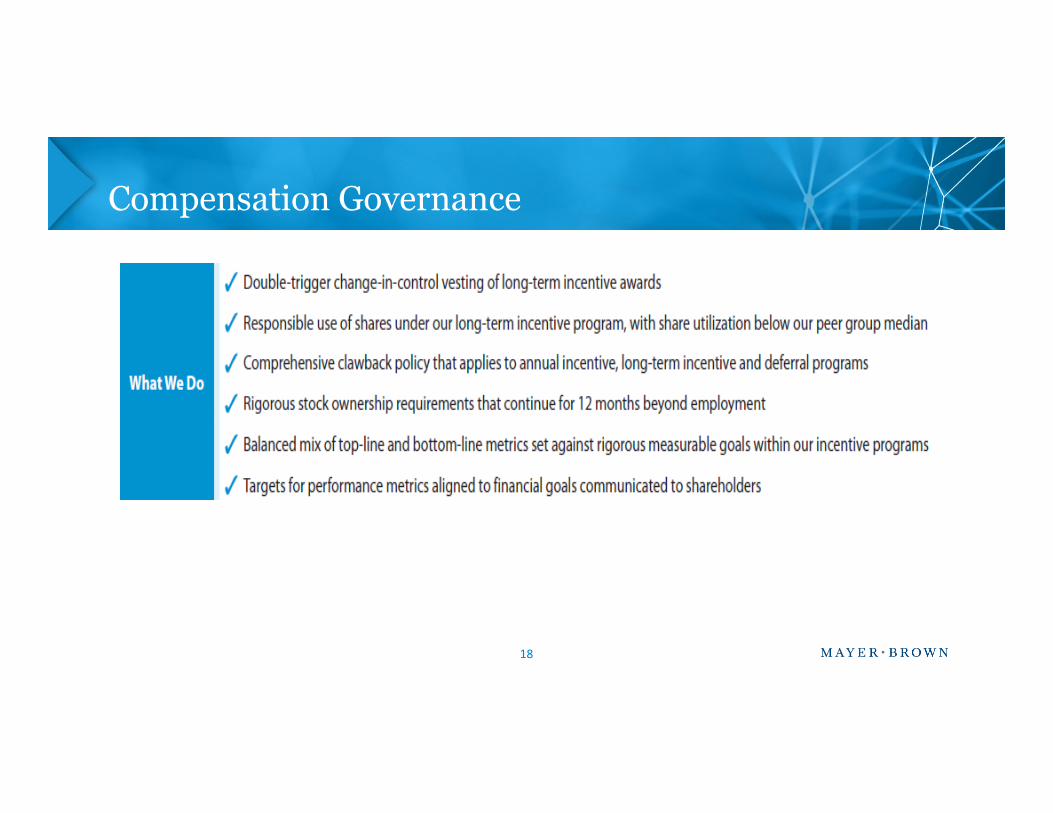

Compensation Governance

18

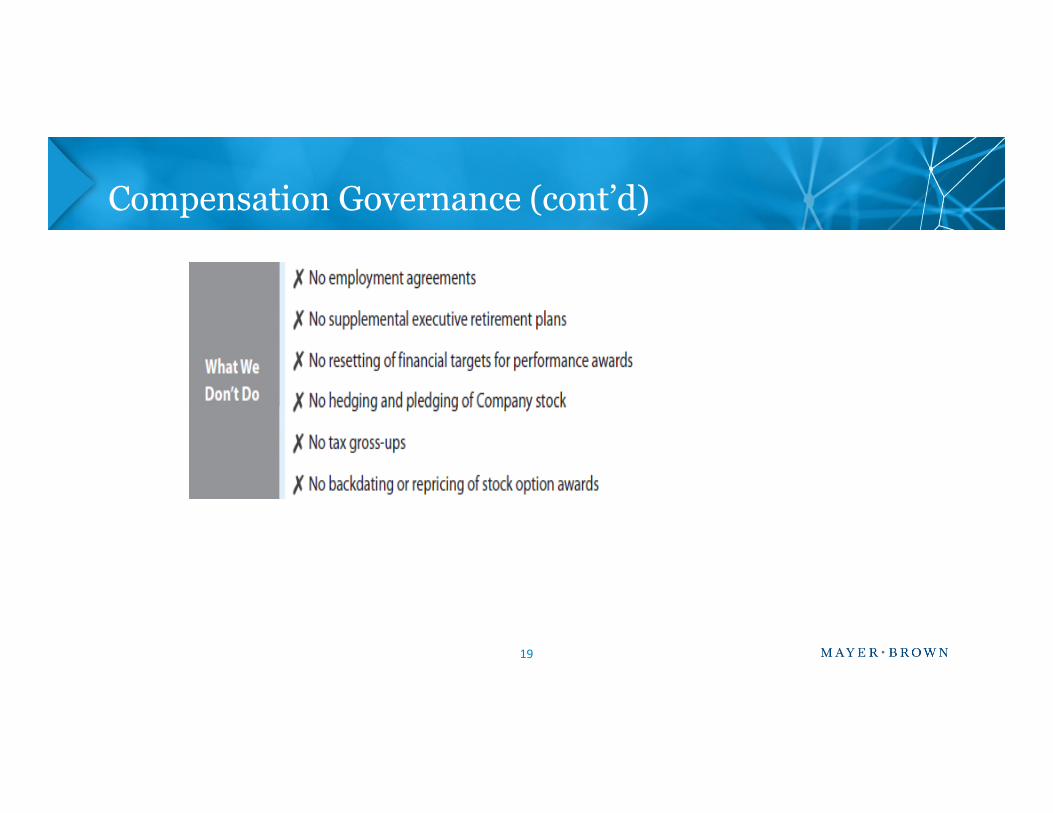

Compensation Governance (cont’d)

19

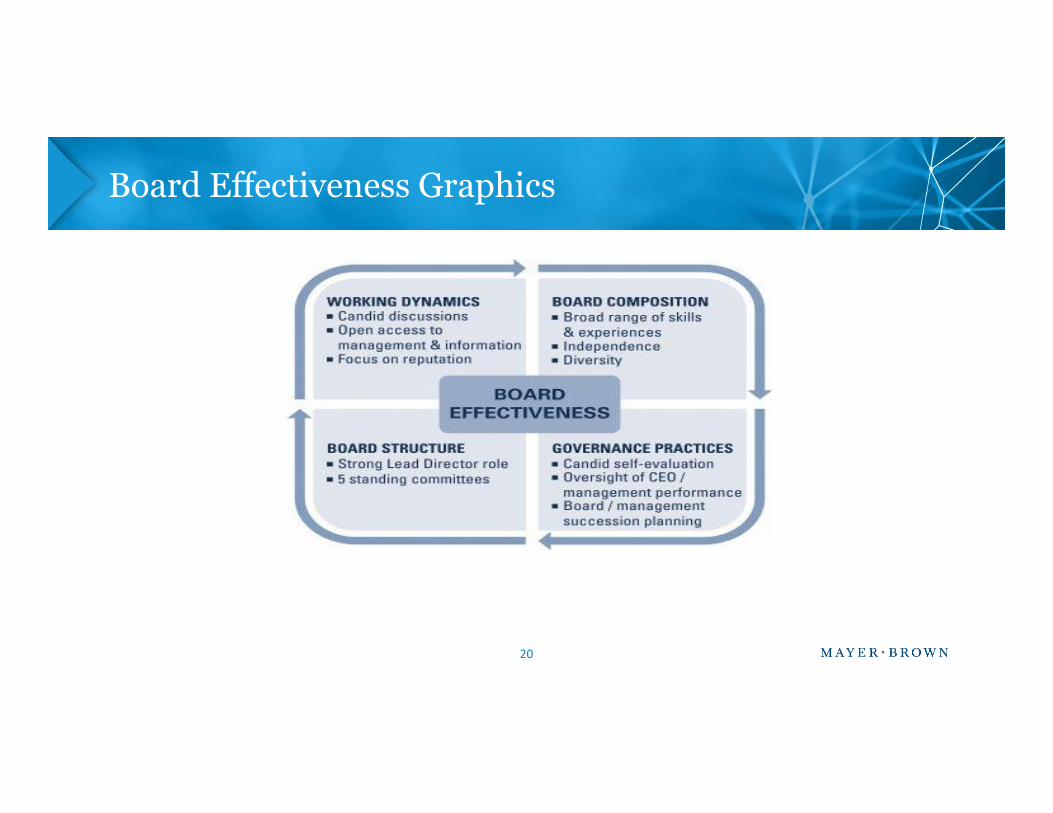

Board Effectiveness Graphics

20

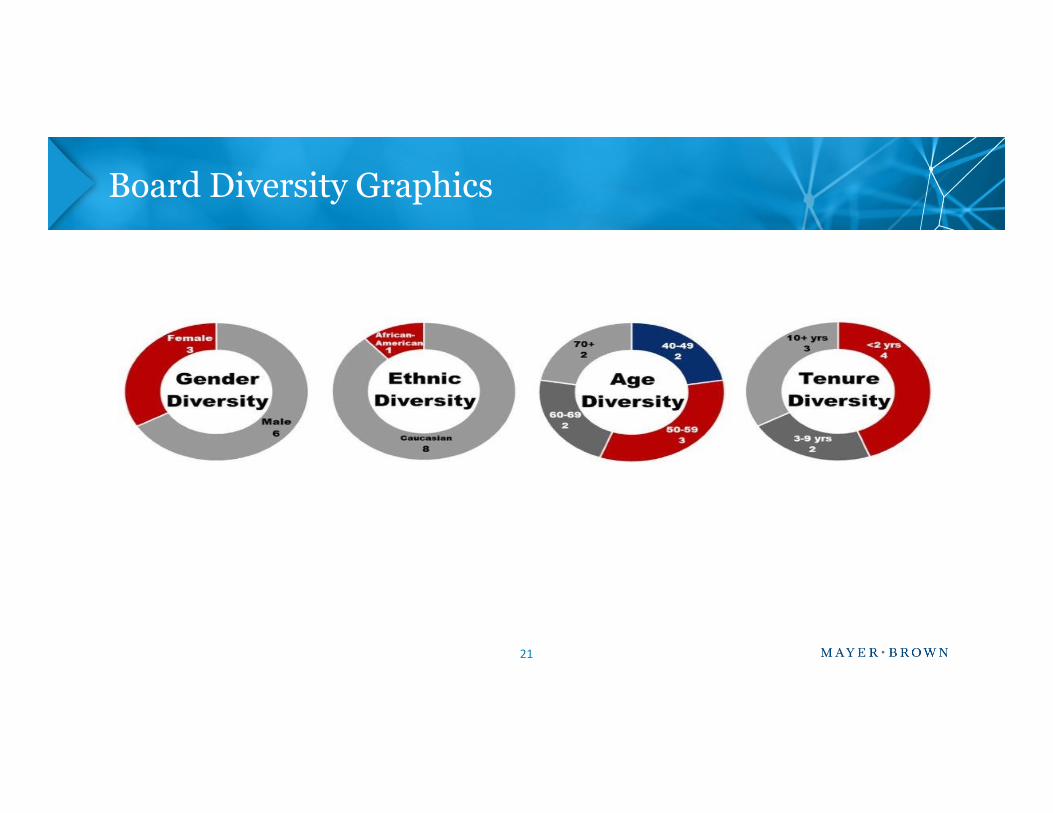

Board Diversity Graphics

21

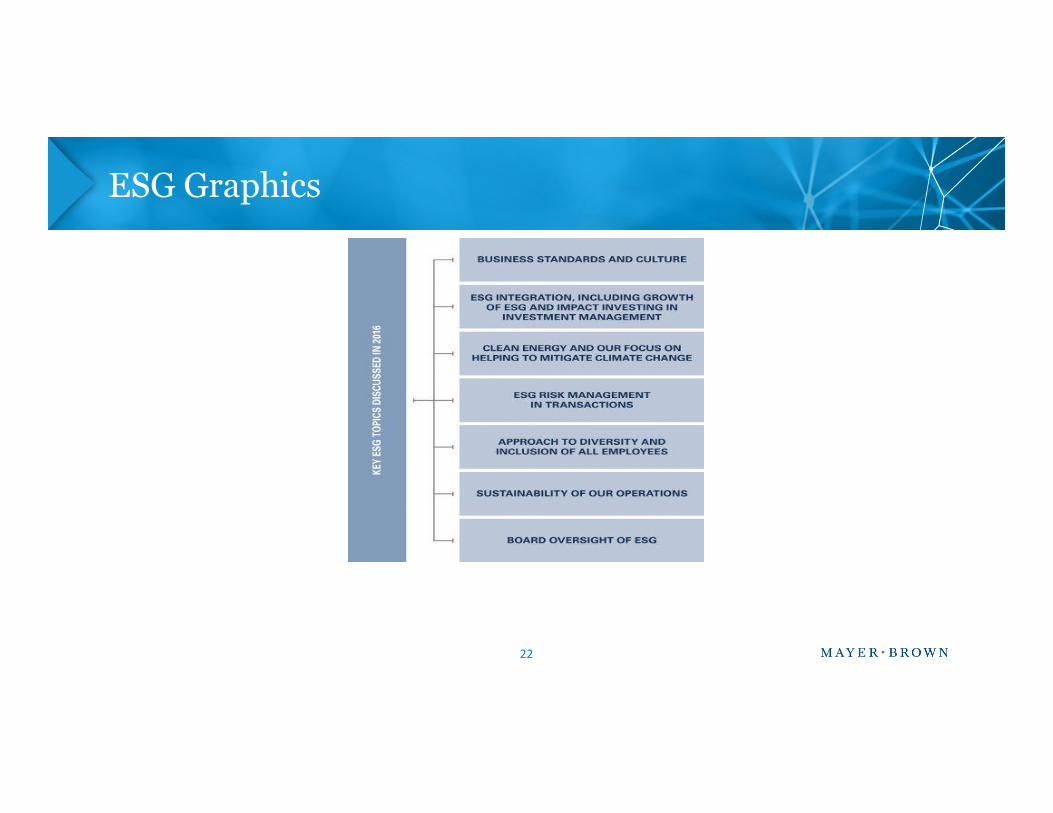

ESG Graphics

22

Investor Stewardship

• State Street Global Advisors has identified board diversity, and in particulargender diversity, as a key issue for its 2017 proxy voting

– Voted against the re-election of directors having the responsibility to nominatenew board members at 400 companies with all-male board that failed to makesignificant effort to address gender diversity on their boards

• BlackRock Investment Stewardship Engagement Priorities for 2017-2018identifies board gender balance, climate risk and human capitalmanagement as focus of engagement

• Vanguard open letter articulated focus on climate risk and gender diversity

23

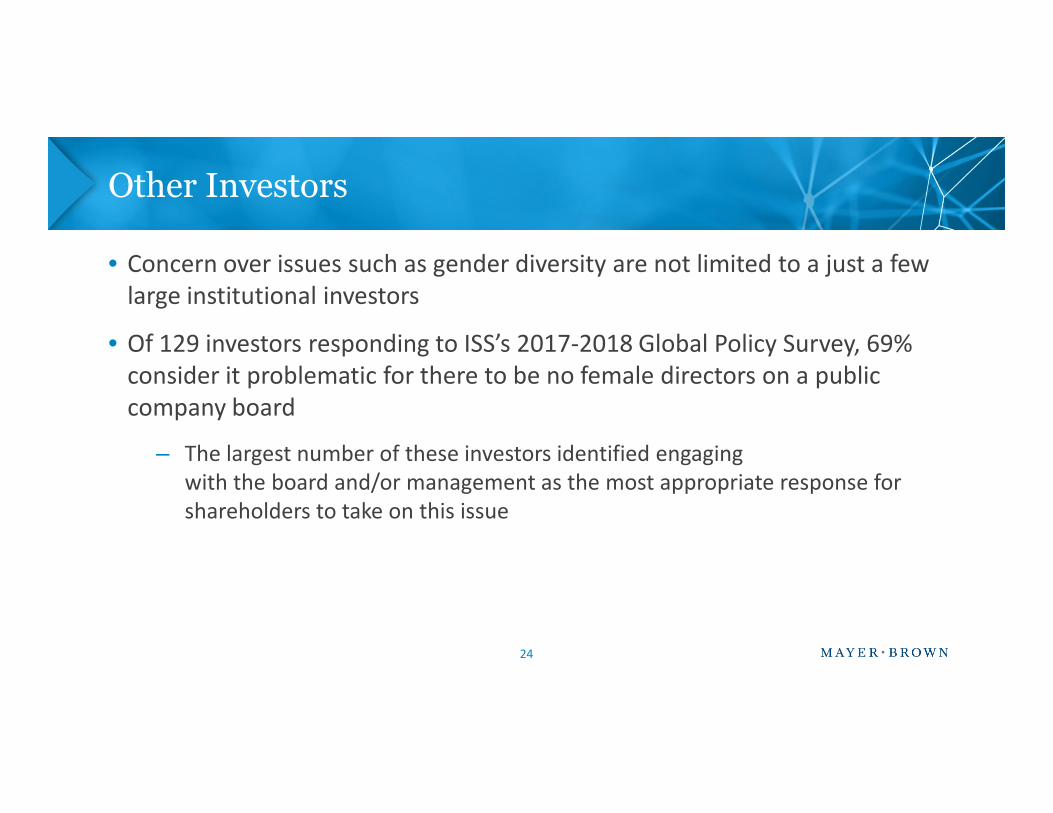

Other Investors

• Concern over issues such as gender diversity are not limited to a just a fewlarge institutional investors

• Of 129 investors responding to ISS’s 2017-2018 Global Policy Survey, 69%consider it problematic for there to be no female directors on a publiccompany boardcompany board

– The largest number of these investors identified engagingwith the board and/or management as the most appropriate response forshareholders to take on this issue

24

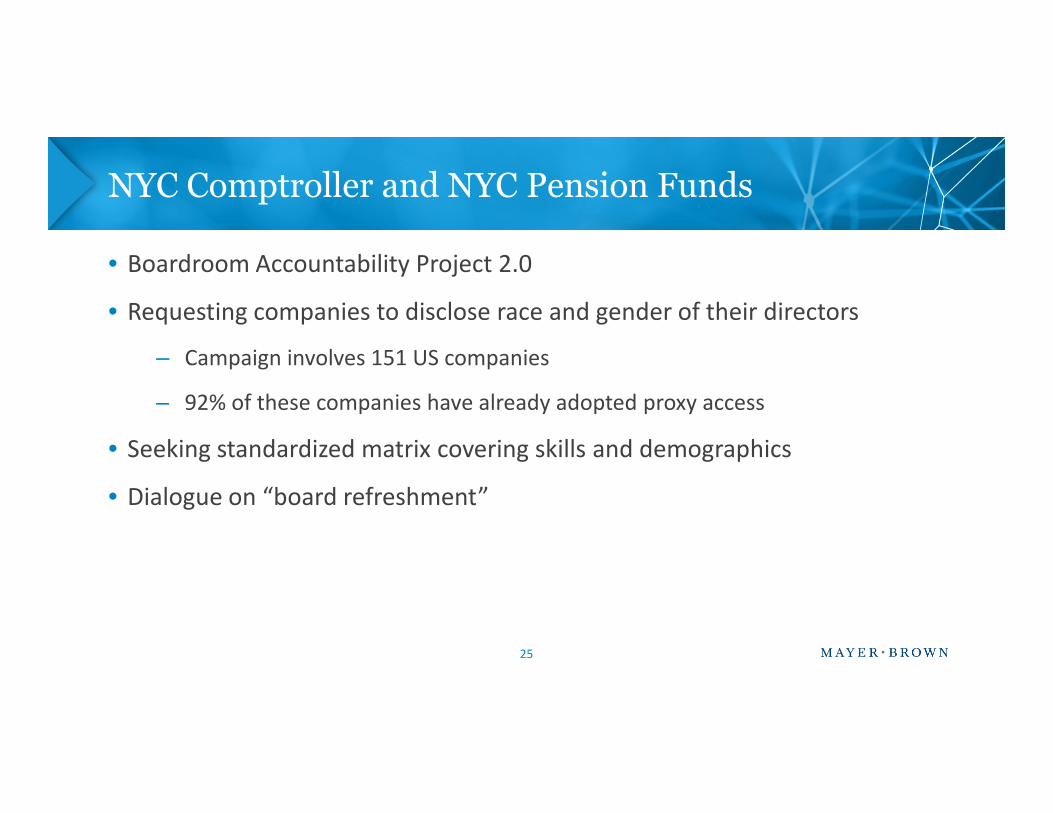

NYC Comptroller and NYC Pension Funds

• Boardroom Accountability Project 2.0

• Requesting companies to disclose race and gender of their directors

– Campaign involves 151 US companies

– 92% of these companies have already adopted proxy access– 92% of these companies have already adopted proxy access

• Seeking standardized matrix covering skills and demographics

• Dialogue on “board refreshment”

25

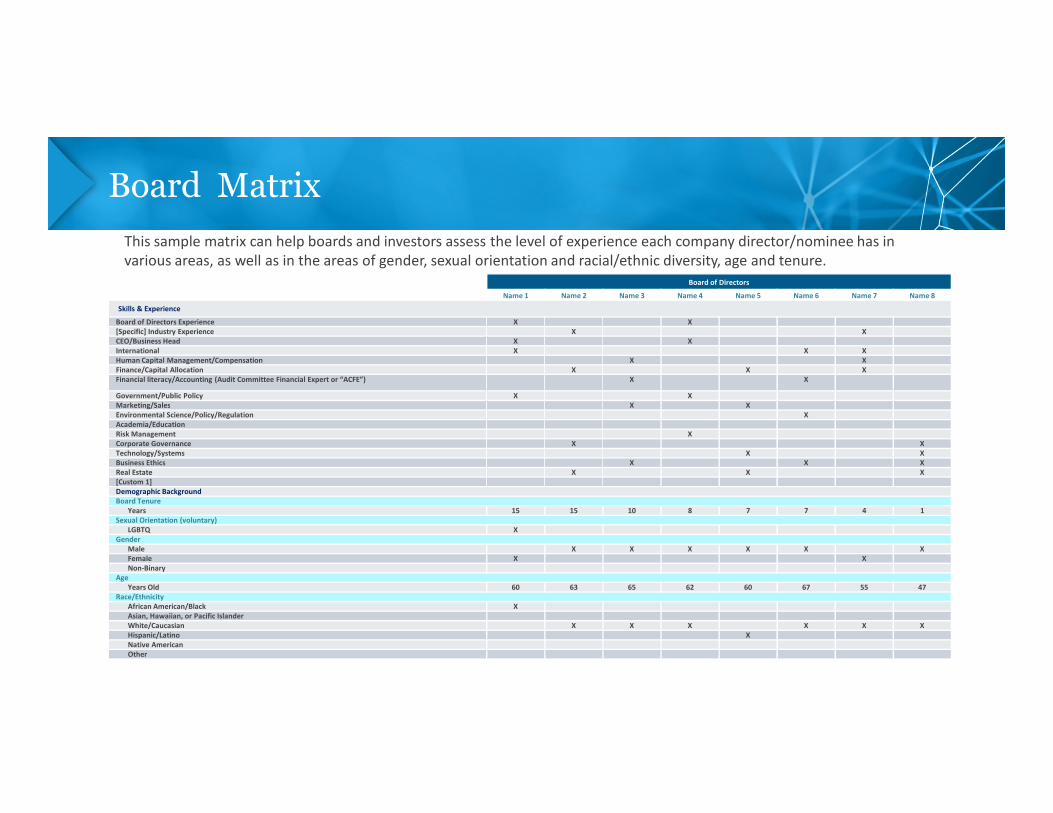

Board Matrix

This sample matrix can help boards and investors assess the level of experience each company director/nominee has invarious areas, as well as in the areas of gender, sexual orientation and racial/ethnic diversity, age and tenure.

Board of Directors

Name 1 Name 2 Name 3 Name 4 Name 5 Name 6 Name 7 Name 8

Skills & Experience

Board of Directors Experience X X[Specific] Industry Experience X XCEO/Business Head X XInternational X X XHuman Capital Management/Compensation X XFinance/Capital Allocation X X XFinancial literacy/Accounting (Audit Committee Financial Expert or “ACFE”) X X

Government/Public Policy X XMarketing/Sales X X

725531117 26

Marketing/Sales X XEnvironmental Science/Policy/Regulation XAcademia/EducationRisk Management XCorporate Governance X XTechnology/Systems X XBusiness Ethics X X XReal Estate X X X[Custom 1]Demographic BackgroundBoard Tenure

Years 15 15 10 8 7 7 4 1Sexual Orientation (voluntary)

LGBTQ XGender

Male X X X X X XFemale X XNon-Binary

AgeYears Old 60 63 65 62 60 67 55 47

Race/EthnicityAfrican American/Black XAsian, Hawaiian, or Pacific IslanderWhite/Caucasian X X X X X XHispanic/Latino XNative AmericanOther

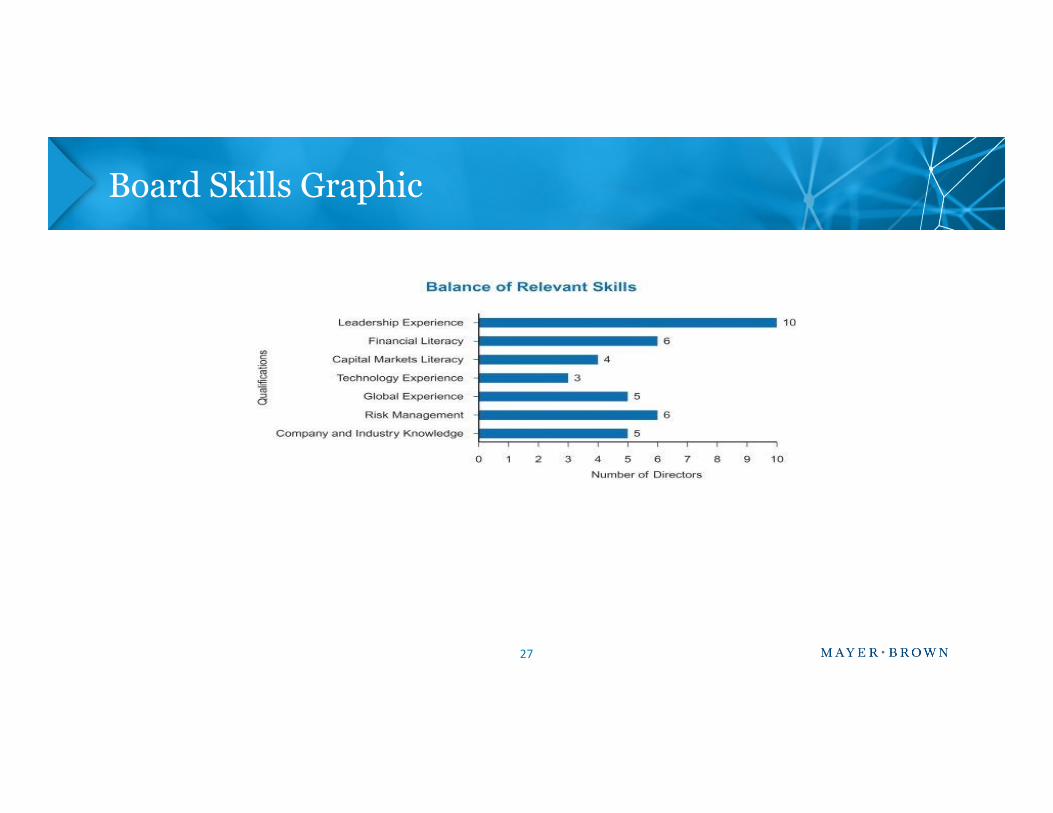

Board Skills Graphic

27

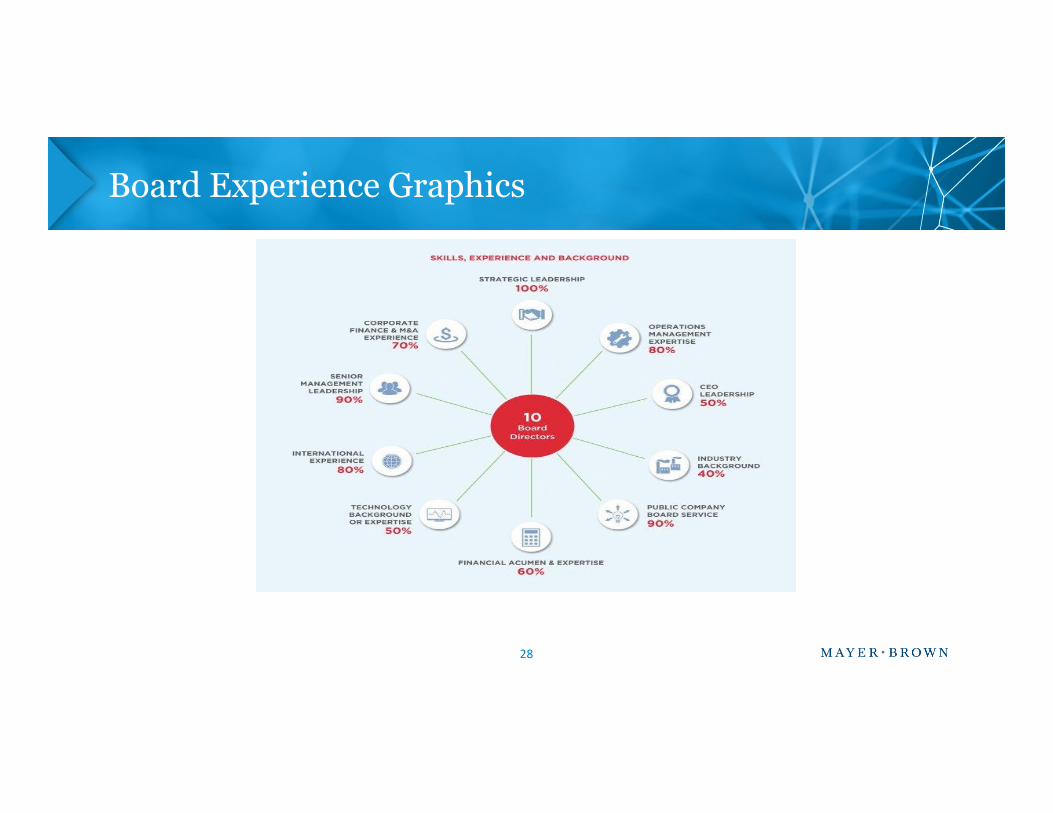

Board Experience Graphics

28

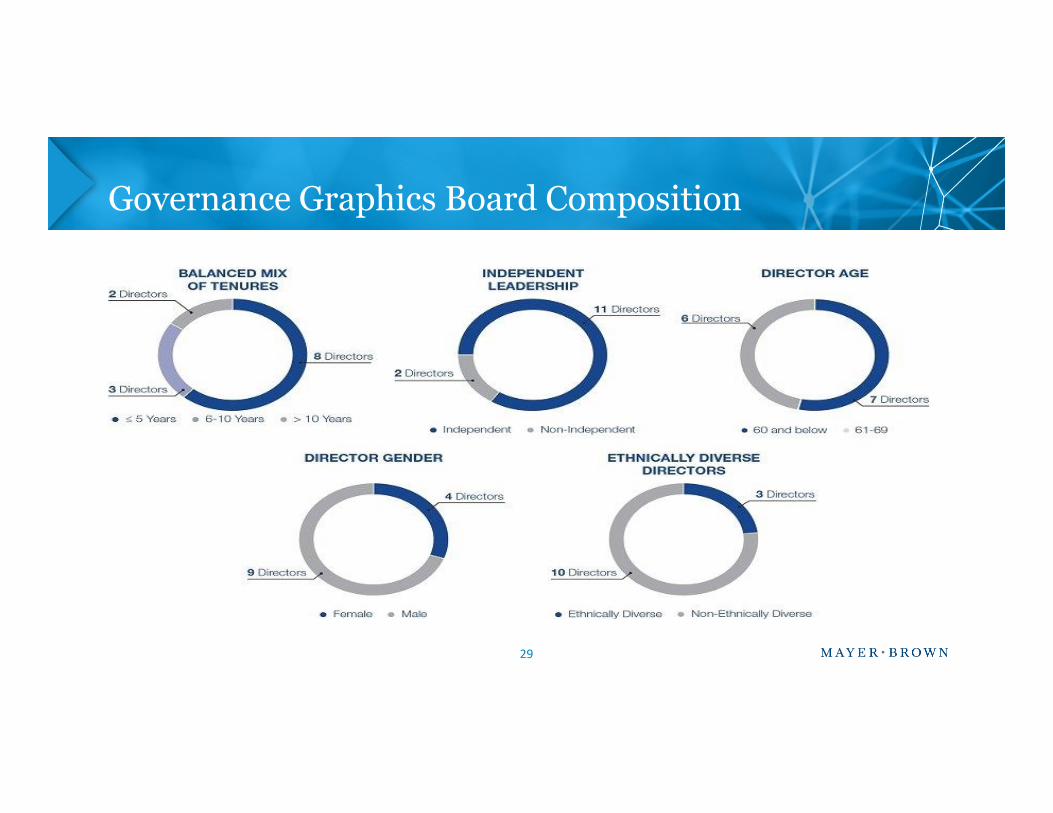

Governance Graphics Board Composition

29

Proxy Access and Shareholder Proposals

• Proxy access

• “Fix it” proposals

• Environmental & social proposals• Environmental & social proposals

• Trends for 2018 season

But first, the shareholder proposal process under Rule 14a-8…

30

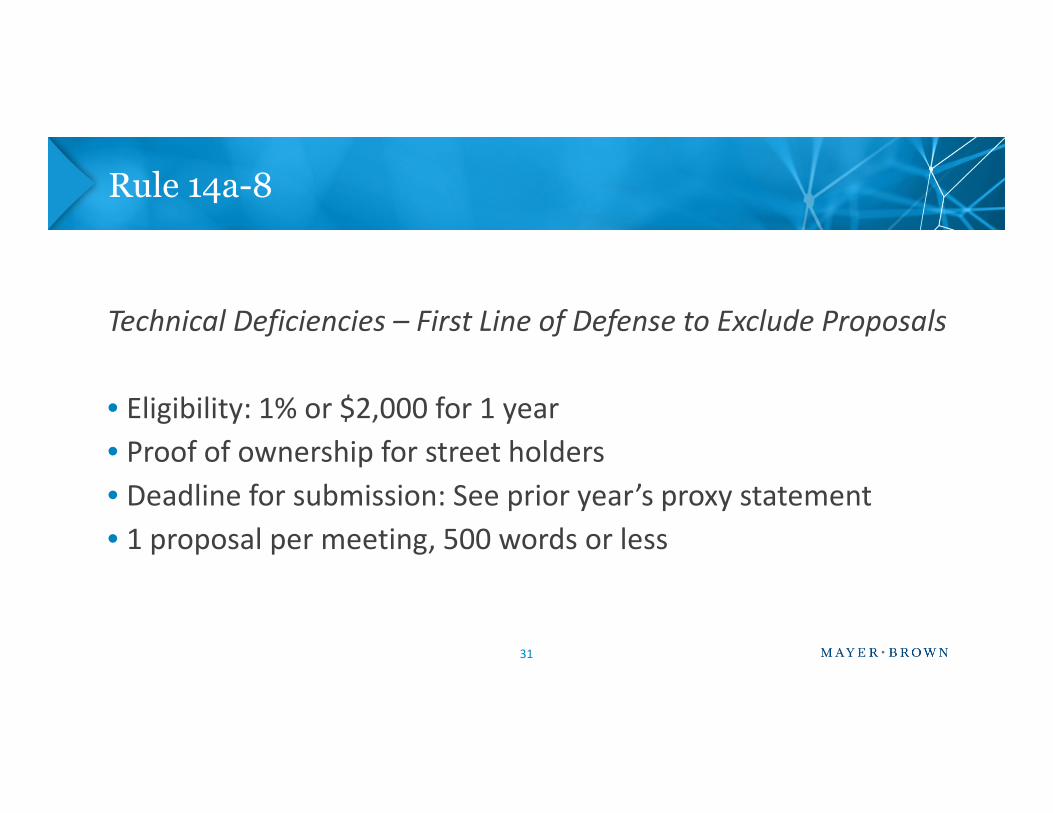

Rule 14a-8

Technical Deficiencies – First Line of Defense to Exclude Proposals

• Eligibility: 1% or $2,000 for 1 year• Eligibility: 1% or $2,000 for 1 year

• Proof of ownership for street holders

• Deadline for submission: See prior year’s proxy statement

• 1 proposal per meeting, 500 words or less

31

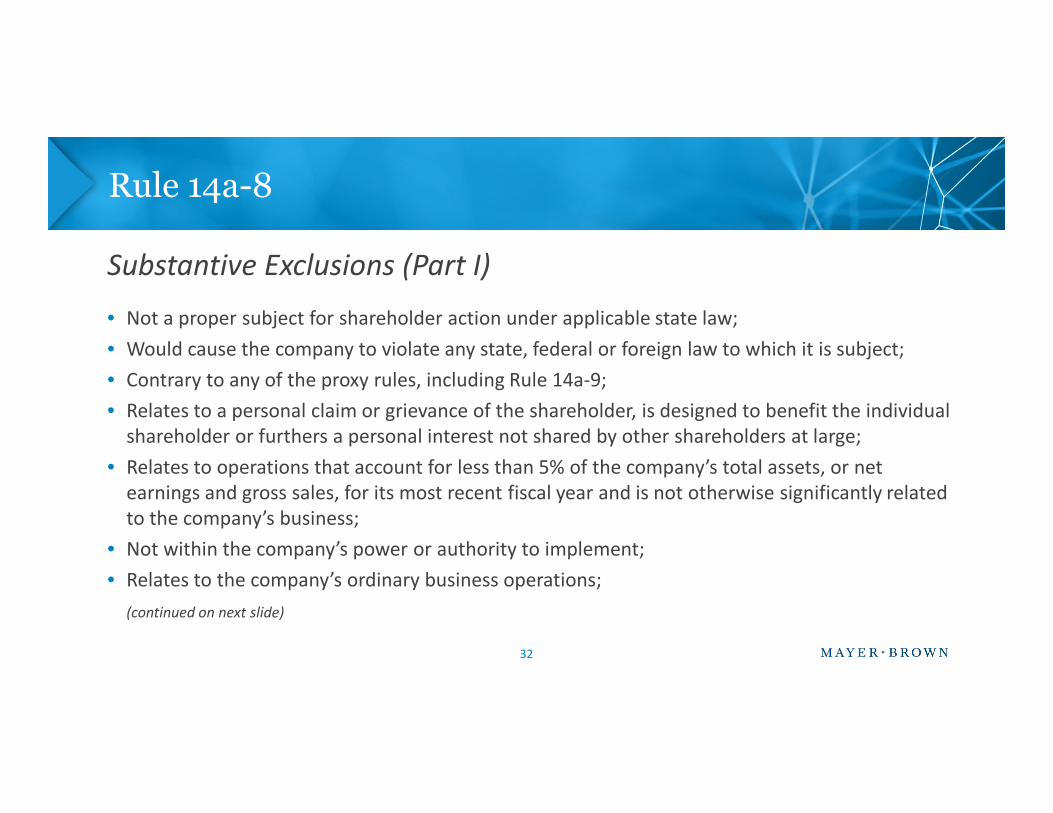

Rule 14a-8

Substantive Exclusions (Part I)

• Not a proper subject for shareholder action under applicable state law;

• Would cause the company to violate any state, federal or foreign law to which it is subject;

• Contrary to any of the proxy rules, including Rule 14a-9;

• Relates to a personal claim or grievance of the shareholder, is designed to benefit the individual• Relates to a personal claim or grievance of the shareholder, is designed to benefit the individualshareholder or furthers a personal interest not shared by other shareholders at large;

• Relates to operations that account for less than 5% of the company’s total assets, or netearnings and gross sales, for its most recent fiscal year and is not otherwise significantly relatedto the company’s business;

• Not within the company’s power or authority to implement;

• Relates to the company’s ordinary business operations;

(continued on next slide)

32

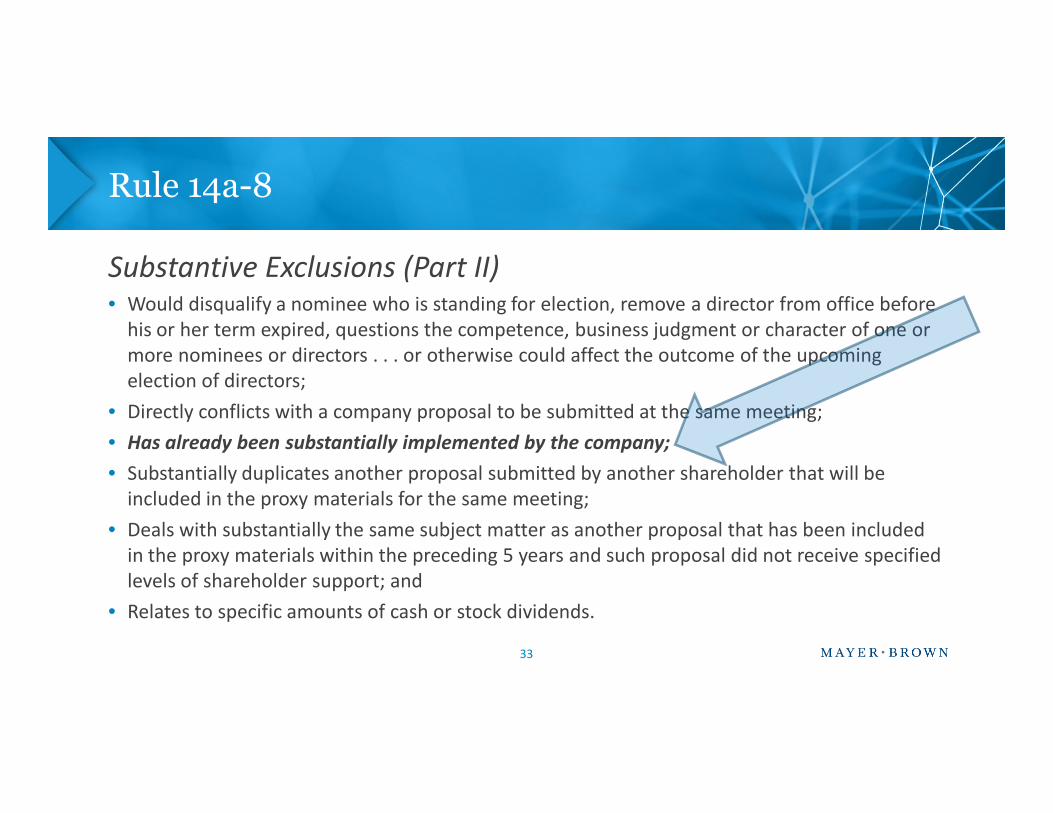

Rule 14a-8

Substantive Exclusions (Part II)• Would disqualify a nominee who is standing for election, remove a director from office before

his or her term expired, questions the competence, business judgment or character of one ormore nominees or directors . . . or otherwise could affect the outcome of the upcomingelection of directors;

• Directly conflicts with a company proposal to be submitted at the same meeting;

33

• Directly conflicts with a company proposal to be submitted at the same meeting;

• Has already been substantially implemented by the company;

• Substantially duplicates another proposal submitted by another shareholder that will beincluded in the proxy materials for the same meeting;

• Deals with substantially the same subject matter as another proposal that has been includedin the proxy materials within the preceding 5 years and such proposal did not receive specifiedlevels of shareholder support; and

• Relates to specific amounts of cash or stock dividends.

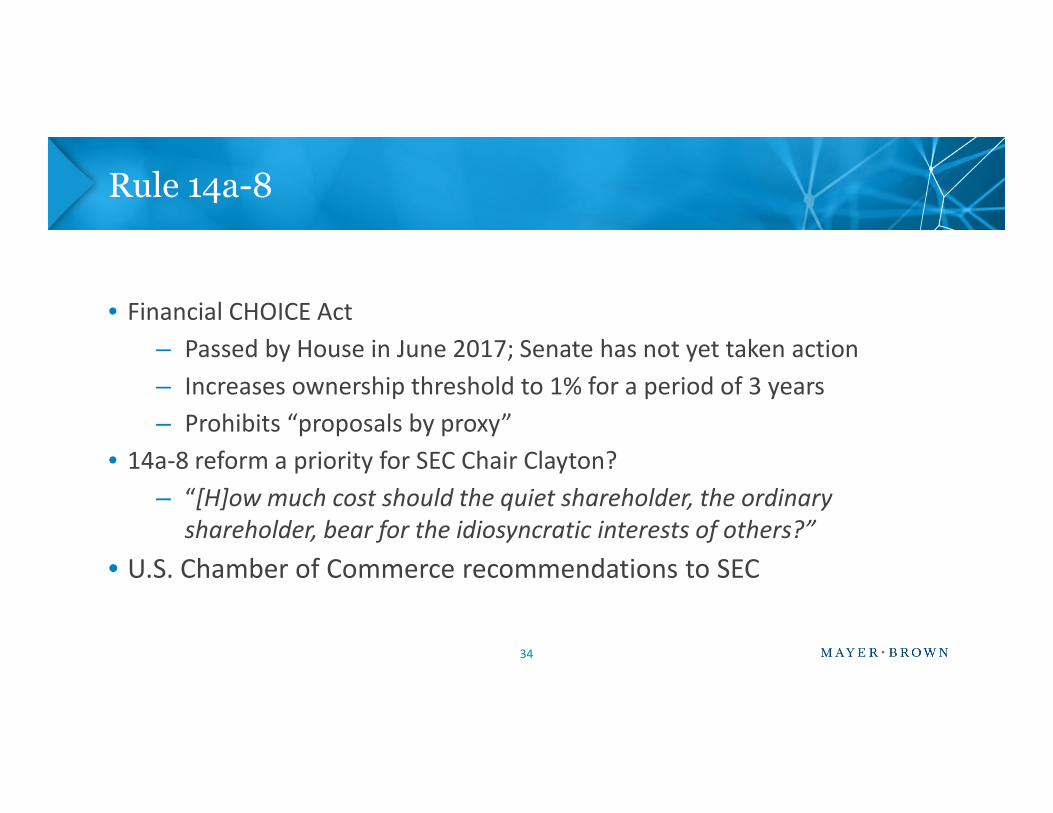

Rule 14a-8

• Financial CHOICE Act

– Passed by House in June 2017; Senate has not yet taken action

– Increases ownership threshold to 1% for a period of 3 years

– Prohibits “proposals by proxy”

• 14a-8 reform a priority for SEC Chair Clayton?

– “[H]ow much cost should the quiet shareholder, the ordinaryshareholder, bear for the idiosyncratic interests of others?”

• U.S. Chamber of Commerce recommendations to SEC

34

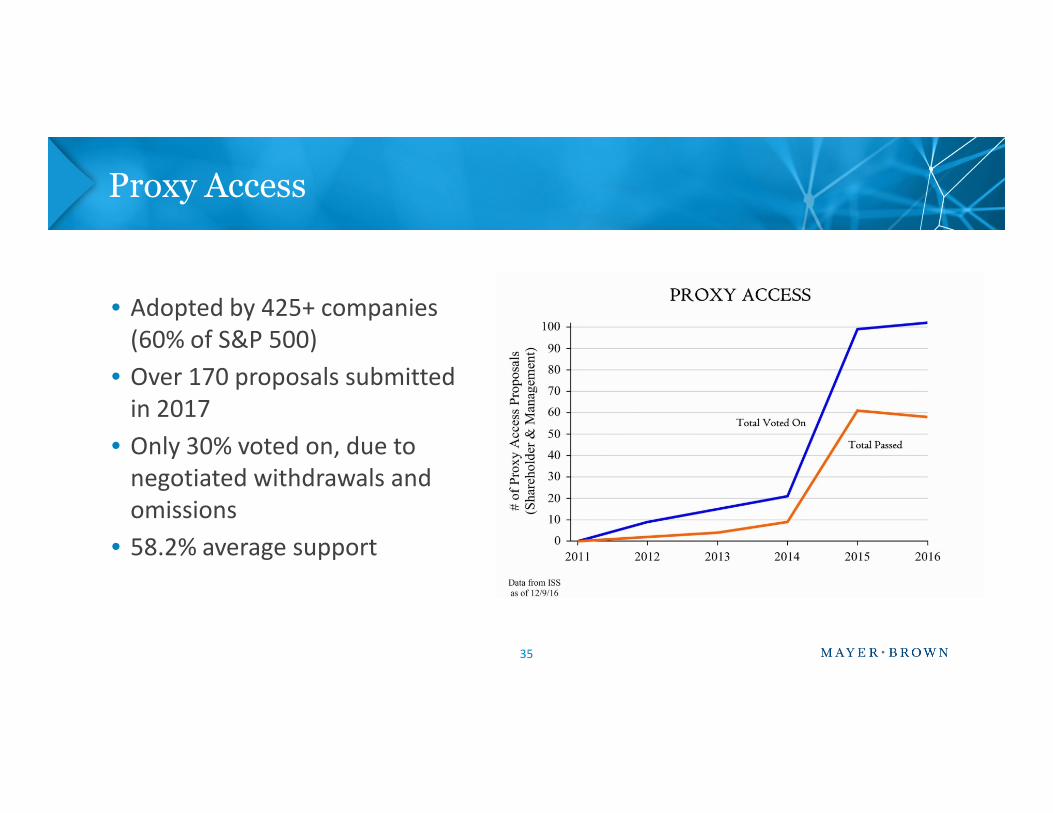

Proxy Access

• Adopted by 425+ companies(60% of S&P 500)

• Over 170 proposals submittedin 2017in 2017

• Only 30% voted on, due tonegotiated withdrawals andomissions

• 58.2% average support

35

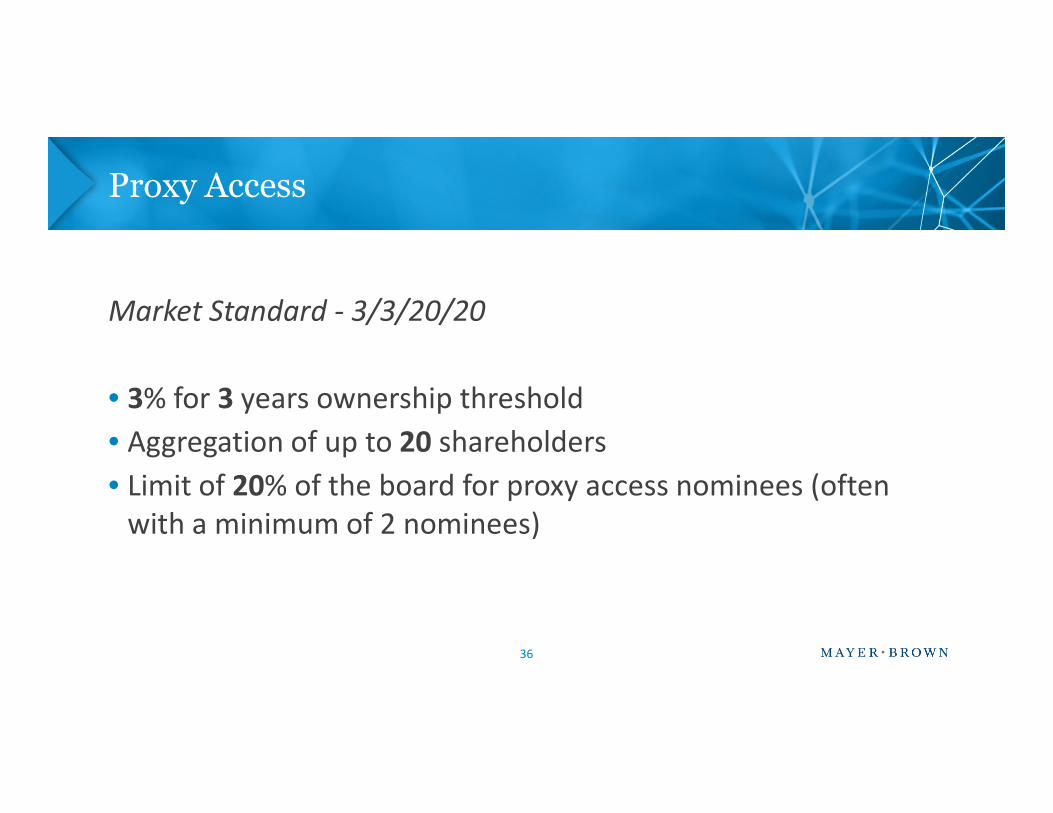

Proxy Access

Market Standard - 3/3/20/20

• 3% for 3 years ownership threshold• 3% for 3 years ownership threshold

• Aggregation of up to 20 shareholders

• Limit of 20% of the board for proxy access nominees (oftenwith a minimum of 2 nominees)

36

Proxy Access

“Fix-It” Proposals

• “Single issue” versus “enhancement package”

• Recent examples:

– Oshkosh (November 2016) – Permitted exclusion for– Oshkosh (November 2016) – Permitted exclusion forpartial adoption of enhancement package in linewith market standard

– H&R Block (July 2017) – Denied exclusion ofproposal to eliminate aggregation cap

• Frequency: Moderate to High

• Support: Low

37

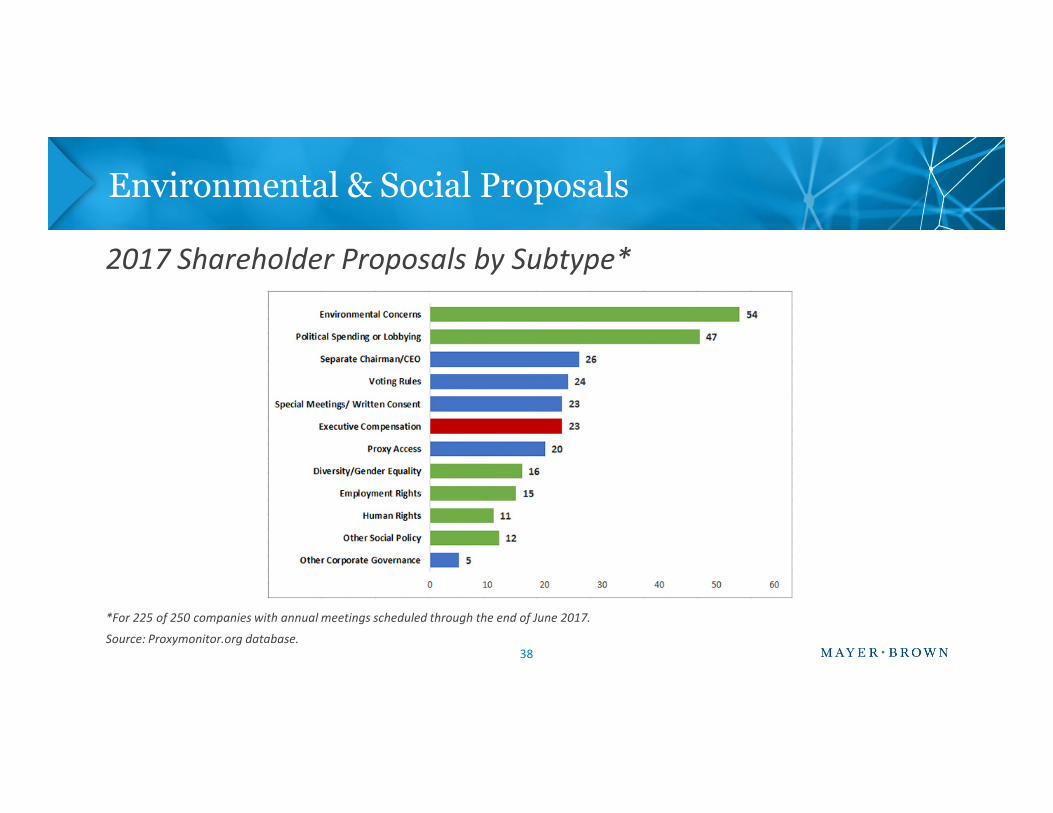

Environmental & Social Proposals

2017 Shareholder Proposals by Subtype*

*For 225 of 250 companies with annual meetings scheduled through the end of June 2017.

Source: Proxymonitor.org database.38

Environmental & Social Proposals

Climate Change Proposals

• Three “2°C proposals” receivedmajority support in 2017

Sponsored by New York State

39

• Sponsored by New York StateCommon Retirement Fund andCalifornia Public EmployeesRetirement System

• Frequency: High

• Support: High

Environmental & Social Proposals

Board & Workplace Diversity Proposals

• Most board diversity proposals withdrawnfollowing agreement to address throughrecruitment

40

recruitment

• 2 proposals received majority support

• Frequency: Moderate

• Support: Moderate

Environmental & Social Proposals

Gender Pay Gap Proposals

• Half of these proposals withdrawn following agreement to comply

• Likely to be refiled in 2018

41

• Frequency: Low to Moderate

• Support: Low

Other Proposals

• Political spending and lobbying

– Frequency: High

– Support: Low to Moderate

• Independent chairman

• Holy Land principles

– Frequency: Moderate

– Support: Low

• Human rights committee

42

• Independent chairman

– Frequency: Moderate

– Support: Low

• Traditional governance reform

– Frequency: Low

– Support: Low

• Human rights committee

– Frequency: Low

– Support: Low

• Sustainability report

– Frequency: Low

– Support: Moderate

What to Expect in 2018?

• Potential reform to shareholder approval process to limitinvestor participation

• Surge of “fix-it” proposals, particularly to lift aggregation caps

43

Surge of “fix-it” proposals, particularly to lift aggregation caps

• Increase in frequency and support for climate changeproposals

• Continued discussion on gender diversity and equalityproposals

• Steady stream of political spending and lobbying proposals

Pay Ratio Disclosure Rule

• Section 953(b) of the Dodd-Frank Act

• Proposed in 2013; adopted on August 5, 2015

• Disclosure generally required for the first fiscal year commencing on orafter January 1, 2017

– Required in proxy statements for the 2018 annual meeting

– Include in any filing that requires executive compensation disclosure

• Exempt companies: emerging growth companies, smaller reportingcompanies, foreign private issuers, MJDS filers, registered investmentcompanies

44

Pay Ratio Disclosure Rule: Overview

• Pay Ratio Disclosure, new Item 402(u) of Regulation S-K:

– Median annual total compensation of all company employees (except CEO);

– Annual total compensation of CEO;

– The ratio of these two amounts (either numerically in relation to 1, as in 50-to-1, or narratively as a multiple of the other, as in 50 times; andto-1, or narratively as a multiple of the other, as in 50 times; and

– Brief non-technical overview of the methodology used to identify the medianemployee and his or her compensation

45

Pay Ratio Disclosure Rule: Employees Covered

• “Employee” is an individual employed by the company or anyof its consolidated subsidiaries:

– U.S. employees

– Non-U.S. employees with two exemptions

– Full-time, part-time, seasonal or temporary employees

– NOT independent contractors or “leased” workers, unless the companydetermines their compensation

• Median employee can be determined on any day within thelast three months of the fiscal year

46

Pay Ratio Disclosure Rule:Non-U.S. Employee Data Privacy Exemption

• May exclude employees in jurisdictions with data privacy laws that makethe company unable to comply with the rule without violating those laws

• The company must exercise reasonable efforts to comply with thedisclosure requirements including, at a minimum:

– Seeking or using an exemption, and obtaining a legal opinion if no exemption– Seeking or using an exemption, and obtaining a legal opinion if no exemptiongranted (include as an exhibit)

• If the company uses an exemption:

– It must: list excluded jurisdictions and the approximate number of employeesexcluded, identify the specific data privacy law, exclude all non-U.S.employees in the jurisdiction, explain how complying with the rule violatessuch law and disclose the company’s efforts to seek or use an exemption

47

Pay Ratio Disclosure Rule:Non-U.S. Employee de minimis Exemption

• If a company’s non-U.S. employees equal 5% or less of the company’s totalemployees, the company may exclude all non-U.S. employees

or• If a company’s non-U.S. employees exceed 5% of the company’s total employees,

the company may exclude up to 5% of its total employees who are non-U.S.employeesemployees

• A company using the de minimis exemption must disclose:

– The jurisdiction(s) involved, approximate number of employees excluded in eachjurisdiction, total number of U.S. and non-U.S. employees irrespective of the exemption(data privacy or de minimis), and total number of U.S. and non-U.S. employees used forthe de minimis calculation

• Employees excluded pursuant to the data privacy exemption count toward the 5%de minimis exemption 48

Pay Ratio Disclosure Rule: The Median Employee

• Identify the “median employee” using a method based on the company’sown facts and circumstances

– Based on any consistently used compensation measure

– A company may identify the median employee based on total compensation of the fullemployee population or may use a statistical sample or another reasonable methodemployee population or may use a statistical sample or another reasonable method

• Disclose the date used to identify the median employee

• Identify once every three years, unless a change in employee population orcompensation arrangements would result in a significant change to the payratio disclosure

49

Pay Ratio Disclosure Rule: The Median Employee(cont’d)

• After identification, median employee total compensation isgenerally calculated following the summary compensationtable requirements

• Reasonable estimates• Reasonable estimates

• Certain adjustments allowed

– Annualize compensation for all permanent employees

– Cost-of-living adjustment

• Present median employee’s total compensation and pay ratiowithout the adjustments for context

50

Pay Ratio Disclosure Rule: Transition Rules

• Exempt company (e.g., EGCs, SRCs, etc.)

– First fiscal year in which it exits exempt status

• IPO company

– Not required in an IPO prospectus or certain Form 10 registration statements– Not required in an IPO prospectus or certain Form 10 registration statements

• Business combinations/acquisitions

– Acquired employees may be omitted from the identification of the medianemployee for the fiscal year in which the transaction became effective

– Company must disclose the approximate number of employees omitted

51

SEC Guidance

• SEC Release 34-10415 (September of 2017)

– Use of reasonable estimates, assumptions and methodologies and statisticalsampling

– Use of internal records

– Independent contractors

• Division of Corporation Finance Guidance Guidance (September of 2017)

– 4 examples of sampling and other reasonable methodologies

– 3 hypothetical examples

52

SEC Guidance (cont’d)

• CDIs (October of 2016 and September of 2017)

– Inability to use hourly rates as a CACM

– Time period issues involved in identifying the median employee

– Furloughed employees– Furloughed employees

– Any measure that reasonably reflects annual comp may be a CACM

– May refer to the ratio as a reasonable estimate

53

Pay Ratio Disclosure Rule: Practical Considerations

• Liability: Pay ratio disclosures will be considered “filed,” not “furnished,”and therefore will be subject to certifications by the CEO and CFO and topotential securities law liabilities

• 2018 compliance date is coming up quickly

• Impact on Employee Morale

• Where to include the disclosure in the proxy statement

• Whether to disclose more that just the required information

• Recognition of pay equality as a political issue

• Local laws tied to SEC pay ratio disclosure

54

Clawback Proposal

• Section 954 of the Dodd-Frank Act

• SEC proposed rules on July 1, 2015

• Comment period ended on September 14, 2015

• The proposal directs the stock exchanges to establish listing standards that• The proposal directs the stock exchanges to establish listing standards thatprohibit the listing of any security of a company that does not adopt andimplement a written policy requiring the recovery of certain incentive-based executive compensation

• Private ordering resulting from concerns of proxy advisory firms

55

Pay-for-Performance Proposal

• Section 953(a) of the Dodd-Frank Act

• SEC proposed rules on April 29, 2015

• Comment period ended on July 6, 2015

• The proposed rule would require companies to include a new• The proposed rule would require companies to include a newtable in their proxy statements showing the relationshipbetween compensation actually paid and performance, withperformance measured both by company TSR and peer groupTSR

56

Hedging Policy Disclosure Proposal

• Section 955 of the Dodd-Frank Act

• SEC proposed rules on February 9, 2015

• Comment period ended on April 20, 2015

• The proposed rule would require companies to disclose whether theypermit employees and directors to hedge the company’s securitiesThe proposed rule would require companies to disclose whether theypermit employees and directors to hedge the company’s securities

• Many companies already discuss hedging policies in their CD&A – either toaddress concerns of proxy advisory firms or in response to Item 402(b) ofRegulation S-K, which requires disclosure of material informationnecessary to understand compensation policies and includes hedgingpolicies as an example of information that should be provided, if material

57

Other Disclosure Issues – New Audit Report Standard

• PCAOB AS 3101, The Auditor’s Report on an Audit of Financial StatementsWhen the Auditor Expresses an Unqualified Opinion

• Content & formatting changes effective December 15, 2017

– Auditor tenure

– Auditor independence

– Addressees (shareholders and board)

– Changes to standardized language

– Changes to standardized form

58

Other Disclosure Issues – New Audit Report Standard

• Critical Audit Matters (“CAMs”) – any matter arising from the audit that wascommunicated or required to be communicated to the AC and that:

1) relates to accounts or disclosures that are material to the financials; and

2) involved especially challenging, subjective or complex auditor judgment

• Risks of material misstatement, including significant risks• Risks of material misstatement, including significant risks

• Significant judgment or estimation by management

• Nature and timing of significant unusual transactions and related effort and judgment

• Auditor subjectivity in applying audit procedures

• Nature and extent of effort required, including specialized skills/knowledge

• Nature of audit evidence obtained

• Effective annual periods ending on/after 6/30/2019 for LAFs and 12/15/2020 for other filers

59

Other Disclosure Issues – Audit Committee Reporting

• Possible Revisions to Audit Committee Disclosures (2015 SEC concept release):

– Oversight of auditors

– Process for appointing/retaining auditors

– Consideration of audit firm and engagement team qualifications– Consideration of audit firm and engagement team qualifications

• PCAOB standards and investor pressure

• Voluntary disclosures:

– Auditor qualifications considered by audit committee

– Choice of auditor “in best interests of the company”

– Explanations for increases in auditor fees60

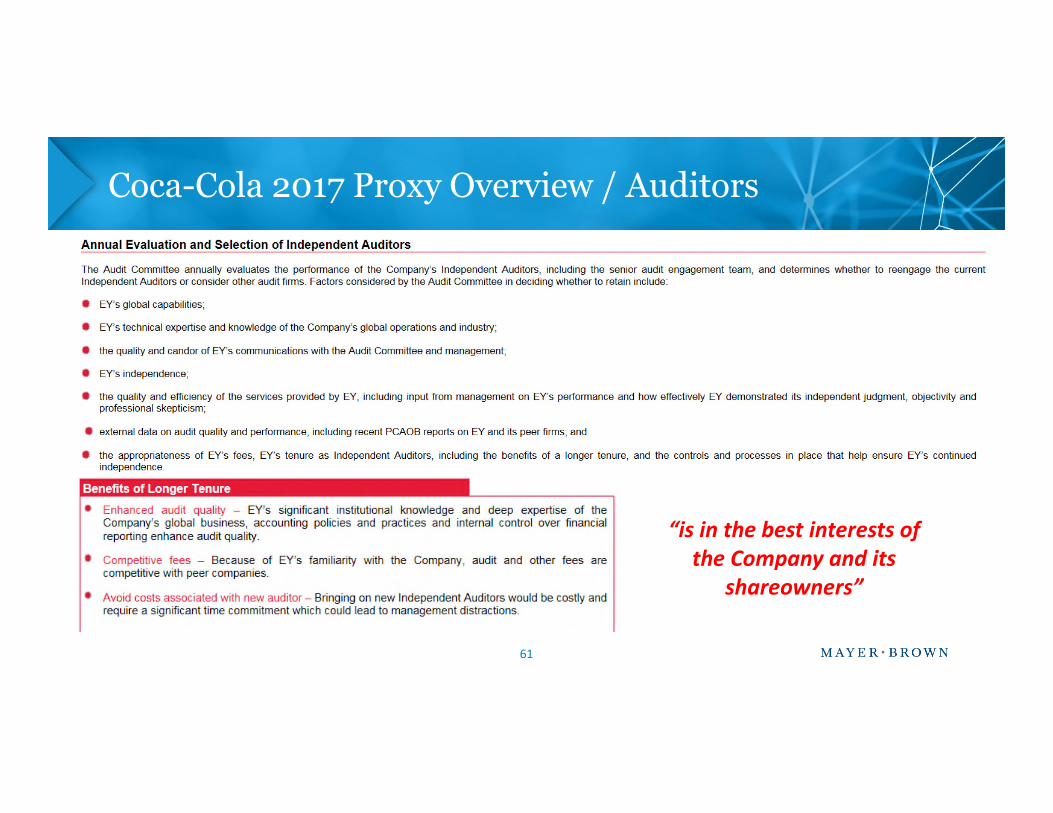

Coca-Cola 2017 Proxy Overview / Auditors

61

“is in the best interests ofthe Company and its

shareowners”

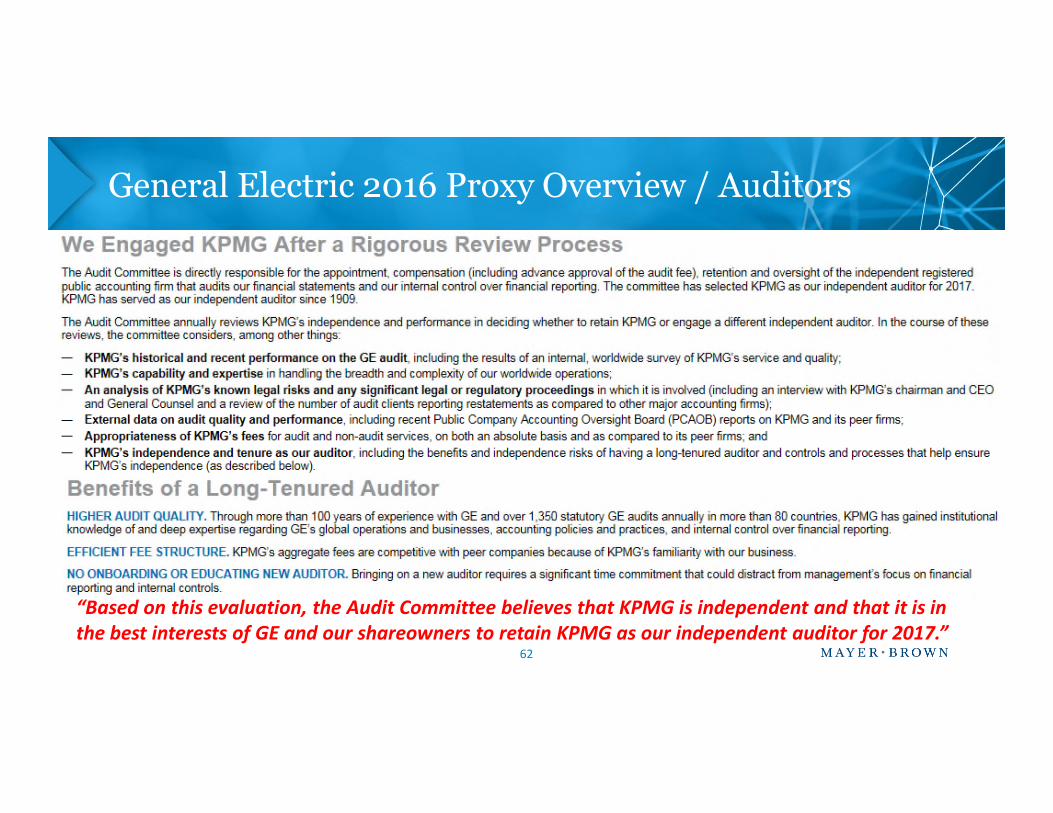

General Electric 2016 Proxy Overview / Auditors

62

“Based on this evaluation, the Audit Committee believes that KPMG is independent and that it is inthe best interests of GE and our shareowners to retain KPMG as our independent auditor for 2017.”

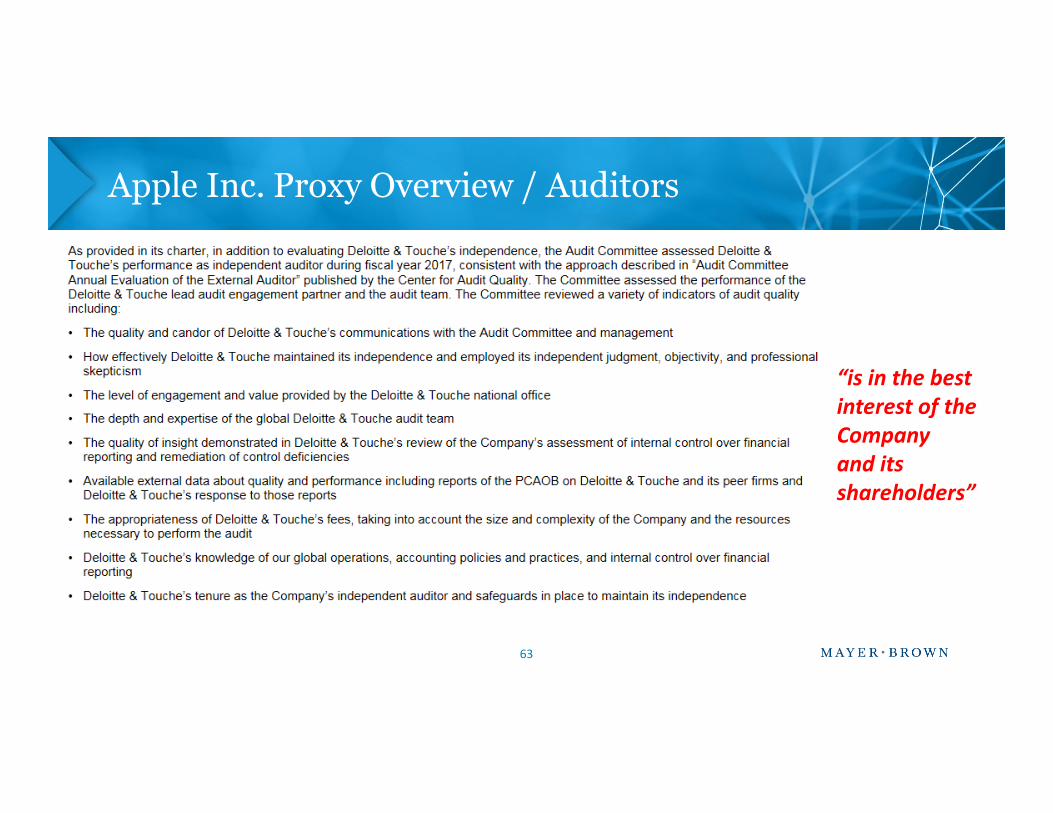

Apple Inc. Proxy Overview / Auditors

“is in the bestinterest of the

63

interest of theCompanyand itsshareholders”

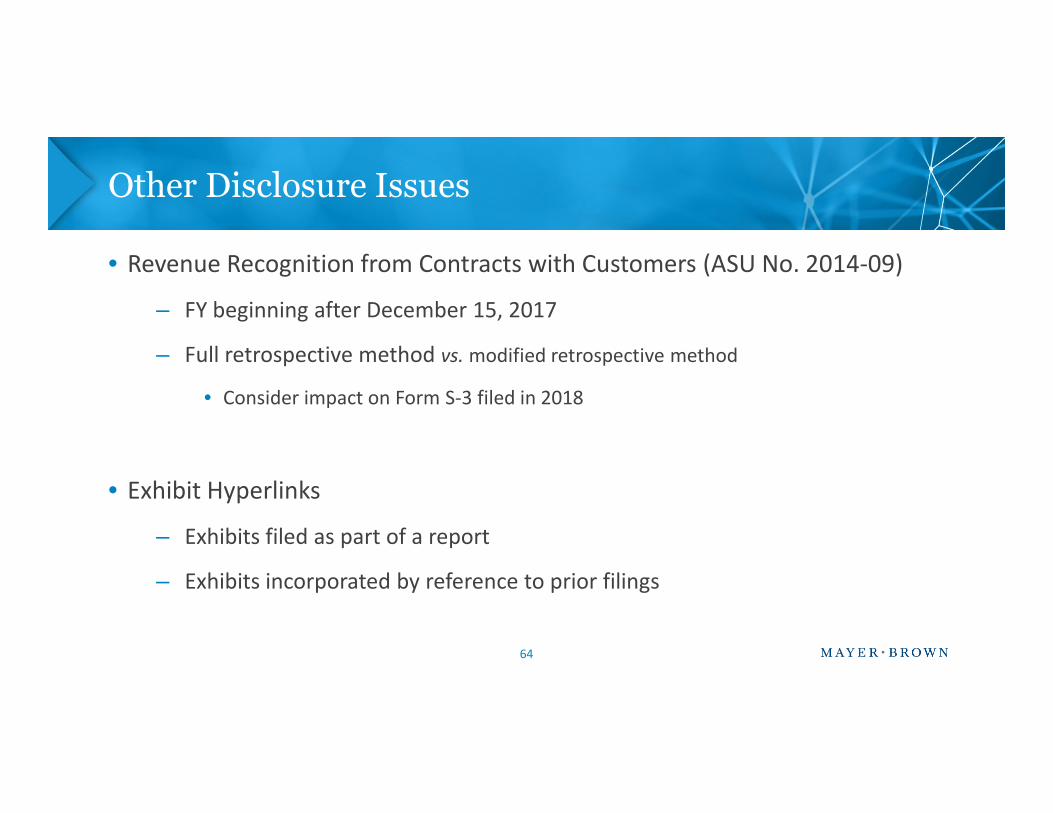

Other Disclosure Issues

• Revenue Recognition from Contracts with Customers (ASU No. 2014-09)

– FY beginning after December 15, 2017

– Full retrospective method vs. modified retrospective method

• Consider impact on Form S-3 filed in 2018• Consider impact on Form S-3 filed in 2018

• Exhibit Hyperlinks

– Exhibits filed as part of a report

– Exhibits incorporated by reference to prior filings

64

Other Disclosure Issues – Non-GAAP

• Regulation G and Item 10(e) of Regulation S-K

• Use in proxy statements

– Target levels for incentive compensation

– All other non-GAAP disclosures subject to Reg G and 10(e)– All other non-GAAP disclosures subject to Reg G and 10(e)

• Cross-references to reconciliation

– Pay-related disclosures: may use a prominent cross-reference to proxystatement annex

– Measures included in 10-K: may use a prominent cross-reference to specific10-K pages

65

Other Disclosure Issues – Risk Factor Updates

• Review existing risk factors

• Consider new/expanded risk factors

– Cybersecurity/Privacy

– Political changes– Political changes

– Brexit

– Climate Change/Sustainability

– Shareholder activism

– Others based on specific industry/location/challenges

66

Other Disclosure Issues – Form 10-K

• Optional Item 16 of Form 10-K

– Summary of information in Form 10-K

– Brief, presented fairly and accurately

– Include hyperlink/cross-reference for each item summarized– Include hyperlink/cross-reference for each item summarized

– Only reference information included in 10-K when filed

– Need not update for Part III information that is in a later-filed proxy orinformation statement

• 10-K cover page – emerging growth company additions

67

Other Annual Meeting Matters – Virtual Meetings

• Increasing numbers of virtual-only meetings

– 200 through Q3 2017

– 155 in 2016; 26 in 2012

• Criticism includes shareholder proposals and policies by investors to voteagainst directors

• Hybrid physical/virtual vs. virtual-only

68

Other Annual Meeting Matters

• Planning and preparation

• D&O questionnaires

• Logistics• Logistics

• Security

• Admissions

69

Reminders

• A recording and link to the materials from this program will be distributed by email to you inthe next day or two.

• For those applying for CLE credit, please note that certificates of attendance will be distributedwithin 30 days of the program date.

70

QUESTIONS?

Mayer Brown is a global legal services provider comprising legal practices that are separate entities (the "Mayer Brown Practices"). The Mayer Brown Practices are: Mayer Brown LLP and Mayer Brown Europe-Brussels LLP, both limited liability partnerships established in Illinois USA;Mayer Brown International LLP, a limited liability partnership incorporated in England and Wales (authorized and regulated by the Solicitors Regulation Authority and registered in England and Wales number OC 303359); Mayer Brown, a SELAS established in France; Mayer BrownJSM, a Hong Kong partnership and its associated legal practices in Asia; and Tauil & Chequer Advogados, a Brazilian law partnership with which Mayer Brown is associated. Mayer Brown Consulting (Singapore) Pte. Ltd and its subsidiary, which are affiliated with Mayer Brown, providecustoms and trade advisory and consultancy services, not legal services. "Mayer Brown" and the Mayer Brown logo are the trademarks of the Mayer Brown Practices in their respective jurisdictions.

![Preliminary Proxy Statement [X ]Definitive Proxy Statement ... · table of contents united states securities and exchange commission washington, dc 20549 schedule 14a information](https://img.pdfslide.us/doc/110x75/5f9fee269adfd874b52be58e/preliminary-proxy-statement-x-definitive-proxy-statement-table-of-contents.jpg)