Embed Size (px)

DESCRIPTION

SEC preliminary prospectus Century

Citation preview

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 1/648

The Prospectus is being displayed in the website to make the Prospectus accessible

to more investors. The Philippine Stock Exchange, Inc. (“PSE”) assumes no

responsibility for the correctness of any statements made or opinions or reportsexpressed in the Prospectus. Furthermore, the PSE makes no representation as to

the completeness of the Prospectus and disclaims any liability whatsoever for any

loss arising from or in reliance in whole or in part on the contents of the Prospectus.

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 2/648

SUBJECT TO COMPLETION

PRELIMINARY PROSPECTUS DATED APRIL 04, 2014

STRICTLY CONFIDENTIAL

Century Pacific Food, Inc.(Incorporated in the Republic of the Philippines)

Primary Offer of 229,654,404 Common Shares

Offer Price of up to ₱14.50 per Offer Share

to be listed and traded on the Main Board of The Philippine Stock Exchange, Inc.

Join t I ssue Managers, Joint L ead Underwr iters and Joint Bookrunners

BDO Capital & Investment

CorporationBPI Capital Corporation First Metro Investment

Corporation

Fi nancial Adviser

Evercore Asia Limited

The date of this Prospectus is []

T h e i n

f o r m a t i o n i n t h i s P r e l i m i n a r y P r o s p e c t u s i s s u b j e c t t o c o m p l e t i o n a n d a m e n d m e n t i n t h e f i n a l p r o s p e c t u s . N o o f f e r o r i n v i t a t i o n s h a l

l b e m a d e o r

r e c e i v e d , a n d n o a g r e e m e n t s h a l l b e m a d e

, o n t h e b a s i s o f t h i s d o c u m e n t , t o p

u r c h a s e o r s u b s c r i b e f o r a n y O f f e r

S h a r e s .

THE PHILIPPINES SECURITIES AND EXCHANGE COMMISSION HAS

NOT APPROVED THESE SECURITIES OR DETERMINED IF THIS

PROSPECTUS IS ACCURATE OR COMPLETE. ANY

REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 3/648

Century Pacific Food, Inc.

7th Floor, Centerpoint Building

Julia Vargas corner Garnet Street

Ortigas Center

1605 Pasig City, Metro ManilaPhilippines

Telephone Number: + (632) 633 85 55

Corporate Website: www.centurypacific.com.ph

This Prospectus relates to the offer and sale of 229,654,404 new common shares by way of

primary offer (the ―Offer‖), with a par value of ₱1.00 per share (the ―Offer Shares‖), of

Century Pacif ic Food, Inc., a corporation organized under Philippine law (the ―Company‖,

―CNPF‖, or the ―Issuer‖) to be listed and traded in the Main Board of The Philippine Stock

Exchange, Inc. (the ―PSE‖). The trading symbol of the Company shall be ―CNPF‖. See ― Plan

of Distribution‖.

The Offer Shares shall be offered at a price of up to ₱14.50 per Offer Share (the ―OfferPrice‖). The determination of the Offer Price is further discussed on page 64 of this

Prospectus and was determined through a book-building process, as well as discussions

between the Company and BDO Capital & Investment Corporation (―BDO Capital‖), BPI

Capital Corporation (―BPI Capital‖), and First Metro Investment Corporation (―First Metro‖),

collectively, the ―Joint Issue Managers, Joint Lead Underwriters, and Joint Bookrunners‖ or

simply, the ―Joint Lead Underwriters‖. A total of 2,229,654,404 Common Shares will be

outstanding after the Offer. The Offer Shares will comprise up to 10.30% of the outstanding

Common Shares after the Offer.

Pursuant to its amended articles of incorporation, the Company has an authorized amount of

capital stock of ₱6,000,000,000.00 divided into 6,000,000,000 Common Shares with a par

value of ₱1.00 per share, of which 2,000,000,000 Common Shares are outstanding as of the

date of this Prospectus. The Offer Shares shall be Common Shares of the Company.

The Company will be listed on the Main Board of the PSE. As a newly incorporated

company, CNPF will be relying on the track record of its wholly owned subsidiaries, General

Tuna Corp. (―GTC‖) and Snow Mountain Dairy Corp. (―SMDC‖). In this respect, both GTC

and SMDC, satisfy the requirements of the PSE Revised Listing Rules i.e., that such

subsidiary (i) must have a cumulative consolidated earnings before interest, taxes,

depreciation, and amortization (―EBITDA‖), excluding non-recurring items, of at least ₱50

million for three full fiscal years immediately preceding the application for listing, (ii) a

minimum EBITDA of ₱10 million for each of the three fiscal years , and (iii) must further be

engaged in materially the same businesses and must have a proven track record ofmanagement throughout the last three years prior to the filing of the application. With

SMDC‘s EBITDA of approximately ₱26 million, ₱39 million and ₱67 million for 2011, 2012

and 2013, respectively and GTC‘s EBITDA of approximately ₱196 million, ₱244 million and

₱286 million for 2011, 2012 and 2013, respectively, CNPF‘s subsidiaries are in full

compliance with the financial requirements. Moreover, GTC and SMDC have both been in

existence and operating since 1997 and 2001, respectively and have had a proven track record

of management since then. The PSE Revised Listing Rules prohibit CNPF from divesting its

shareholdings in GTC and SMDC for a period of three years from the date the Offer Shares

are listed on the PSE; provided that the prohibition shall not apply if the divestment is

approved by a majority of CNPF‘s shareholders.

The total proceeds to be raised by the Company from the sale of the Offer Shares will be up to

approximately ₱3,330.0 million. The estimated net proceeds to be raised by the Company

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 4/648

from the sale of the Offer Shares (after deducting estimated fees and expenses payable by the

Company of approximately ₱278.5 million) will be approximately ₱3,051.5 million. The

Company intends to use the proceeds it receives from the Offer for payment of financial

obligations, capital expenditures to increase production capacity and cost efficiency, working

capital and/or potential acquisitions. For a more detailed discussion on the proceeds from the

Offer and the Company‘s proposed use of proceeds, please see ―Use of Proceeds‖ beginningon page 55 of this Prospectus.

The Joint Lead Underwriters (as defined below) will receive a transaction fee from the

Company equivalent to 1.5% of the gross proceeds from the sale of the Offer Shares. These

are inclusive of the amounts to be paid to other participating underwriters and selling agents

and exclusive of the amounts to be paid to the PSE Trading Participants, where applicable.

For a more detailed discussion on the fees to be received by the Joint Lead Underwriters,

please see ― Plan of Distribution‖ beginning on page 59 of this Prospectus.

Each holder of Common Shares will be entitled to such dividends as may be declared by the

Company‘s Board of Directors (the ―Board‖ or ―Board of Directors‖), provided that any share

dividends declaration requires the approval of shareholders holding at least two-thirds of itstotal ―outstanding capital stock.‖ The Corporation Code of the Philippines, Batas Pambansa

Blg. 68 (the ―Philippine Corporation Code‖), has defined ―outstanding capital stock‖ as the

total shares of stock (―Shares‖) issued to subscribers or stockholders, whether paid in full or

not, except for treasury shares. Dividends may be declared only from the Company‘s

unrestricted retained earnings. The Company has approved a dividend policy of maintaining

an annual cash and/or share dividend pay-out of up to 30% of its net income from the

preceding year, subject to the requirements of applicable laws and regulations, the terms and

conditions of its outstanding bonds and loan facilities, and the absence of circumstances that

may restrict the payment of such dividends, such as where the Company undertakes major

projects and developments. The Company‘s Board may, at any time, modify the Company‘s

dividend policy depending upon the Company‘s capital expenditure plans and/or any terms offinancing facilities entered into to fund its current and future operations and projects. The

Company can give no assurance that it will pay any dividends in the future. See ― Dividends

and Dividend Policy‖.

45,930,800 Offer Shares (or 20% of the Offer Shares) are being offered to all of the trading

participants of the PSE (the ―PSE Trading Participants‖) and 22,965,400 Offer Shares (or

10% of the Offer Shares) are being offered to local small investors (the ―Local Small

Investors‖ or ―LSIs‖) in the Philippines. The remaining 160,758,204 Offer Shares (or 70% of

the Offer Shares) are being offered by the Joint Lead Underwriters to the Qualified

Institutional Buyers (the ―QIBs‖) and to the general public. Prior to the closing of the Offer,

any Offer Shares not taken up by the PSE Trading Participants and Local Small Investors

shall be distributed by the Joint Lead Underwriters to their clients or to the general public.The Joint Lead Underwriters firmly underwrite any shares left unsubscribed after the Offer.

For a more detailed discussion of the underwriting commitment of the Joint Lead

Underwriters, see ― Plan of Distribution‖ on page 59 of this Prospectus.

All of the Common Shares to be sold pursuant to the Offer have identical rights and

privileges. The Common Shares may be owned by any person or entity regardless of

citizenship or nationality, subject to the nationality limits under Philippine law. The

Philippine Constitution and related statutes set forth restrictions on foreign ownership for

companies engaged in certain activities. The Company currently does not own any land in the

Philippines but if the Company acquires land in the future, its foreign shareholdings may not

exceed 40% of its issued and outstanding voting capital shares. See ― Philippine Foreign Exchange and Foreign Ownership Controls‖.

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 5/648

Before making an investment decision, investors should carefully consider the risks

associated with an investment in the Common Shares. These risks include:

1. Risks relating to the Company’s business

CNPF‘s financial performance may be materially and adversely affected byfluctuations in prices or disruption in the supply of key raw materials;

CNPF‘s sales growth depends on successful introduction of new products and new product extensions, which is subject to consumer preference and other market factorsat the time of introduction;

Actual or alleged contamination or deterioration of, or safety concerns about, CNPF‘sfood products or similar products produced by third parties could give rise to productliability claims and harm CNPF‘s reputation;

Competition in CNPF‘s businesses may adversely affect its financial condition andresults of operations;

CNPF relies on the strength of its brands;

Consolidation of distribution channels in the Philippines may adversely affect

CNPF‘s financial condition and results of operations; CNPF relies on key suppliers for certain raw materials and the failure by such

suppliers to adhere to and perform contractual obligations may adversely affectCNPF‘s business and results of operations;

CNPF has a limited history as a separate entity;

CNPF generally does not have long-term contracts with its customers, and it issubject to uncertainties and variability in demand and product mix;

CNPF is exposed to the credit risks of its customers, and delays or defaults in payment by its customers could have a material adverse effect on CNPF‘s financialcondition, results of operations and liquidity;

Any infringement or failure to protect CNPF‘s trademarks and proprietary rights

could materially and adversely affects its business; CNPF‘s strategy of growth, including acquisitions, entering new product categories

and international expansion, may not always be successful or may entail significantcosts, which could adversely affect its business, financial condition and results ofoperations;

CNPF may be subject to labor unrest, slowdowns and increased wage costs;

CNPF is effectively controlled by the Po family and their interests may differ fromthe interests of other shareholders;

CNPF‘s international operations may present operating, financial and legalchallenges, particularly in countries where CNPF has little or no experience;

CNPF‘s existing insurance policies and self -insurance measures may not be sufficientto cover the full extent of any losses;

CNPF‘s businesses and operations are substantially dependent upon key executives;and

Problems may develop among partners of joint ventures operated by CNPF, whichmay result in disruptions to these businesses.

2. Risks relating to the Philippines

The substantial majority of CNPF‘s income is derived from sales in the Philippinesand, therefore, a slowdown in economic growth in the Philippines could materiallyadversely affect CNPF‘s financial condition and results of operation;

A decline in the value of the Peso against the U.S. dollar and other currencies would

increase many of CNPF‘s costs; and

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 6/648

Any political instability or acts of terrorism in the Philippines may adversely affectCNPF.

3. Risks relating to the Offer and the Offer Shares

The Offer Shares may not be suitable investments for all investors; There can be no guarantee that the Offer Shares will be listed on the PSE;

There has been no prior market for the Common Shares, so there may be no liquidityin the market for the Offer Shares and the price of the Offer Shares may fall;

The market price of the Common Shares may be volatile, which could cause the valueof investors‘ investments in the Company to decline;

Future sales of Common Shares in the public market could adversely affect the prevailing market price of the Common Shares and Shareholders may experiencedilution in their holdings;

Investors may incur immediate and substantial dilution as a result of purchasing OfferShares; and

The Company may be unable to pay dividends on the Common Shares.

4. Risks relating to certain statistical information in this Prospectus

The Prospectus contains forward-looking statements that are, by their nature, subjectto significant risks and uncertainties.

The pro forma financial information included herein may not be indicative of actualresults;

Certain information contained herein is derived from unofficial publications; and

The section of this Prospectus entitled ― Industry‖ was not independently verified bythe Company or the Joint Lead Underwriters, and the sources therein may not becompletely independent or independent at all.

Please refer to the section entitled ― Risk Factors‖ beginning on page 35 of this Prospectus,

which, while not intended to be an exhaustive enumeration of all risks, must be considered in

connection with a purchase of the Offer Shares.

The information contained in this Prospectus relating to the Company and its operations has

been supplied by the Company, unless otherwise stated herein. To the best of its knowledge

and belief, the Company, which has taken reasonable care to ensure that such is the case,

confirms that the information contained in this Prospectus relating to it and its operations is

correct, and that there is no material misstatement or omission of fact which would make any

statement in this Prospectus misleading in any material respect and that the Company hereby

accepts full and sole responsibility for the accuracy of the information contained in this

Prospectus with respect to the same.

An application for listing of the Common Shares was approved on March 26, 2014 by the

board of directors of the PSE, subject to the fulfillment of certain listing conditions. The PSE

assumes no responsibility for the correctness of any statements made or opinions expressed in

this Prospectus. The PSE makes no representation as to its completeness and expressly

disclaims any liability whatsoever for any loss arising from reliance on the entire or any part

of this Prospectus. Such approval for listing is permissive only and does not constitute a

recommendation or endorsement of the Common Shares by the PSE or the Securities and

Exchange Commission of the Philippines (the ―SEC‖).

Prior to the Offer, there has been no public market for the Common Shares. Accordingly,there has been no market price for the Common Shares derived from day-to-day trading.

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 7/648

An application has been made to the SEC to register the Offer Shares under the provisions of

the Securities Regulation Code of the Philippines (Republic Act (―R.A.‖) No. 8799) (the

―SRC‖).

A REGISTRATION STATEMENT RELATING TO THE OFFER SHARES HAS

BEEN FILED WITH THE SEC BUT HAS NOT YET BEEN DECLAREDEFFECTIVE. NO OFFER TO BUY THE OFFER SHARES CAN BE ACCEPTED

AND NO PART OF THE PURCHASE PRICE CAN BE ACCEPTED OR RECEIVED

UNTIL THE REGISTRATION STATEMENT HAS BECOME EFFECTIVE, AND

ANY SUCH OFFER MAY BE WITHDRAWN OR REVOKED, WITHOUT

OBLIGATION OR COMMITMENT OF ANY KIND, AT ANY TIME PRIOR TO

NOTICE OF ITS ACCEPTANCE GIVEN AFTER THE EFFECTIVE DATE. AN

INDICATION OF INTEREST IN RESPONSE HERETO INVOLVES NO

OBLIGATION OR COMMITMENT OF ANY KIND. THIS PROSPECTUS SHALL

NOT CONSTITUTE AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER

TO BUY ANY OFFER SHARES.

The Offer Shares are offered subject to receipt and acceptance of any order by the Companyand subject to its right to reject any order in whole or in part. It is expected that the Offer

Shares will be delivered in book-entry form against payment to the Philippine Depository and

Trust Corporation (the ―PDTC‖) on or about [], 2014.

By:

Christopher T. Po President and Chief Executive Officer

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 8/648

No representation or warranty, express or implied, is made by the Company or the Joint LeadUnderwriters, regarding the legality of an investment in the Offer Shares under any legal,investment or similar laws or regulations. No representation or warranty, express or implied,is made by the Joint Lead Underwriters as to the accuracy or completeness of the informationherein and nothing contained in this Prospectus is, or shall be relied upon as, a promise orrepresentation by the Joint Lead Underwriters. The contents of this Prospectus are notinvestment, legal or tax advice. Prospective investors should consult their own counsel,accountant and other advisors as to legal, tax, business, financial and related aspects of a

purchase of the Offer Shares. In making any investment decision regarding the Offer Shares, prospective investors must rely on their own examination of the Company and the terms ofthe Offer, including the merits and risks involved. Any reproduction or distribution of thisProspectus, in whole or in part, and any disclosure of its contents or use of any informationherein for any purpose other than considering an investment in the Offer Shares is prohibited.

No person has been authorized to give any information or to make any representations other

than those contained in this Prospectus and, if given or made, such information or

representations must not be relied upon as having been authorized by the Company or the

Joint Lead Underwriters. This Prospectus does not constitute an offer to sell or the solicitationof an offer to purchase any securities other than the Offer Shares or an offer to sell or the

solicitation of an offer to purchase such securities by any person in any circumstances in

which such offer or solicitation is unlawful. Neither the delivery of this Prospectus nor any

sale of the Offer Shares offered hereby shall, under any circumstances, create any implication

that there has been no change in the affairs of the Company since the date hereof or that the

information contained herein is correct as of any time subsequent to the date hereof.

Certain statistical information and forecasts in this Prospectus relating to the Philippines and

other data used in this Prospectus were obtained or derived from internal surveys, industry

forecasts, market research, governmental data, publicly available information and/or industry

publications. Industry publications generally state that the information they contain has been

obtained from sources believed to be reliable. However, there is no assurance that suchinformation is accurate or complete. Similarly, internal surveys, industry forecasts, market

research, governmental data, publicly available information and/or industry publications have

not been independently verified by the Company or the Joint Lead Underwriters and may not

be accurate, complete, up-to-date, balanced or consistent with other information compiled

within or outside the Philippines.

The Company reserves the right to withdraw the offer and sale of Offer Shares at any time,

and Joint Lead Underwriters reserve the right to reject any commitment to subscribe for the

Offer Shares in whole or in part and to allot to any prospective purchaser less than the full

amount of the Offer Shares sought by such purchaser. If the Offer is withdrawn or

discontinued, the Company shall subsequently notify the SEC and the PSE. The Joint LeadUnderwriters and certain related entities may acquire for their own account a portion of the

Offer Shares.

Each offeree of the Offer Shares, by accepting delivery of this Prospectus, agrees to the

foregoing.

Forward-Looking Statements

This Prospectus contains forward-looking statements that are, by their nature, subject to

significant risks and uncertainties. These forward-looking statements include, without

limitation, statements relating to:

known and unknown risks;

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 9/648

uncertainties and other factors that may cause the Company‘s actual results,

performance or achievements to be materially different from expected future results;

and

performance or achievements expressed or implied by forward-looking statements.

Such forward-looking statements are based on numerous assumptions regarding the

Company‘s present and future business strategies and the environment in which the Company

will operate in the future. Important factors that could cause some or all of the assumptions

not to occur or cause actual results, performance or achievements to differ materially from

those in the forward-looking statements include, among other things:

the Company‘s ability to successfully implement its current and future strategies;

the Company‘s ability to anticipate and respond to local and regional trends,

including demand for canned and processed fish, meat and dairy products or other

future products the Company may offer;

the Company‘s ability to successfully manage its future business, financial condition,

results of operations and cash flow;

the Company‘s ability to secure additional financing and manage its capital structure

and dividend policy;

the condition of, and changes in, the relationship of the Company with the Philippine

Food and Drug Administration (―Philippine FDA‖), the Philippine Bureau of Internal

Revenue (―BIR‖) or other Philippine regulatory authorities or licensors;

general political, social and economic conditions in the Philippines;

regional geopolitical dynamics involving the Philippines and/or its neighbors;

the condition of and changes in the Philippine, Asian or global economies;

changes in interest rates, inflation rates and the value of the Peso against the U.S.

dollar and other currencies;

changes to the laws, regulations and policies applicable to or affecting the Company;

competition in the Philippine food processing and food distribution industries;

legal or regulatory proceedings in which the Company is or may become involved;

and

uncontrollable events, such as war, civil unrest or acts of international or domestic

terrorism, the outbreak of contagious diseases, accidents and natural disasters.

Additional factors that could cause the Company‘s actual results, performance or

achievements to differ materially from forward-looking statements include, but are not

limited to, those disclosed under ― Risk Factors‖ and elsewhere in this Prospectus. These

forward-looking statements speak only as of the date of this Prospectus. The Company and

Joint Lead Underwriters expressly disclaim any obligation or undertaking to release, publicly

or otherwise, any updates or revisions to any forward-looking statement contained herein to

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 10/648

reflect any change in the Company‘s expectations with regard thereto or any change in events,

conditions, assumptions or circumstances on which any statement is based.

This Prospectus includes statements regarding the Company‘s expectations and projections

for future operating performance and business prospects. The words ―believe,‖ ―plan,‖

―expect,‖ ―anticipate,‖ ―estimate,‖ ―project,‖ ―intend,‖ ―seek,‖ ―target,‖ ―aim,‖ ―may,‖ ―will,‖―would,‖ ―could,‖ and similar words identify forward-looking statements. In addition, all

statements other than statements of historical facts included in this Prospectus are forward-

looking statements. Statements in this Prospectus as to the opinions, beliefs and intentions of

the Company accurately reflect in all material respects the opinions, beliefs and intentions of

its management as to such matters as of the date of this Prospectus, although the Company

gives no assurance that such opinions or beliefs will prove to be correct or that such intentions

will not change. This Prospectus discloses, under the section ― Risk Factors‖ and elsewhere,

important factors that could cause actual results to differ materially from the Company‘s

expectations. All subsequent written and oral forward-looking statements attributable to the

Company or persons acting on behalf of the Company are expressly qualified in their entirety

by the above cautionary statements.

The Joint Lead Underwriters have exercised due diligence in ascertaining that all material

representations contained in this Prospectus, including its amendments and supplements, are

true and correct and that no material information was omitted, which was necessary in order

to make the statements contained in said documents not misleading.

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 11/648

TABLE OF CONTENTS

Page

GLOSSARY OF TERMS........................................................................................................3

SUMMARY ............................................................................................................................7

SUMMARY OF THE OFFER .............................................................................................. 21

SUMMARY PRO FORMA CONSOLIDATED FINANCIAL INFORMATION................. 28

SUMMARY COMBINED FINANCIAL INFORMATION.................................................. 31

SUMMARY PARENT FINANCIAL INFORMATION OF CNPF ...................................... 35

SUMMARY CONSOLIDATED FINANCIAL INFORMATION OF CNPF ....................... 38

RISK FACTORS ................................................................................................................... 41

USE OF PROCEEDS ............................................................................................................ 55

PLAN OF DISTRIBUTION .................................................................................................. 59

DIVIDENDS AND DIVIDEND POLICY ............................................................................ 63

DETERMINATION OF THE OFFER PRICE ...................................................................... 64

DILUTION ............................................................................................................................ 66

SELECTED PRO FORMA CONSOLIDATED FINANCIAL INFORMATION ................. 68

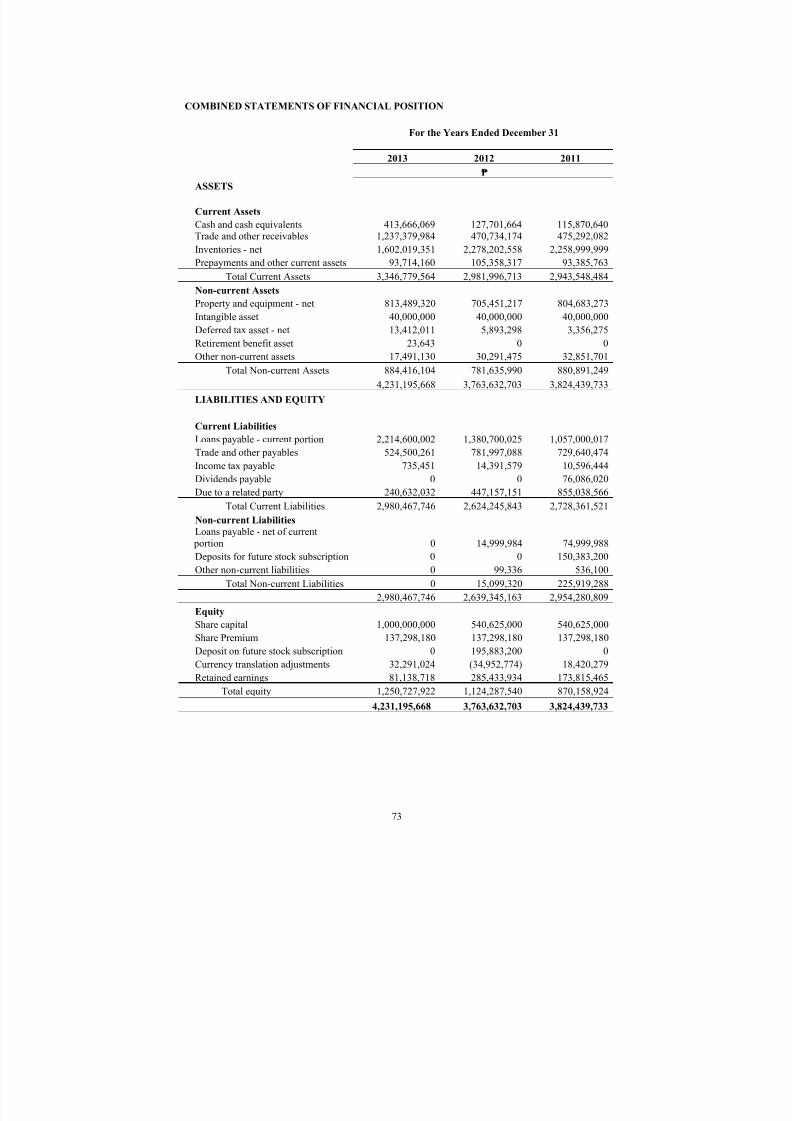

SELECTED COMBINED FINANCIAL INFORMATION .................................................. 72

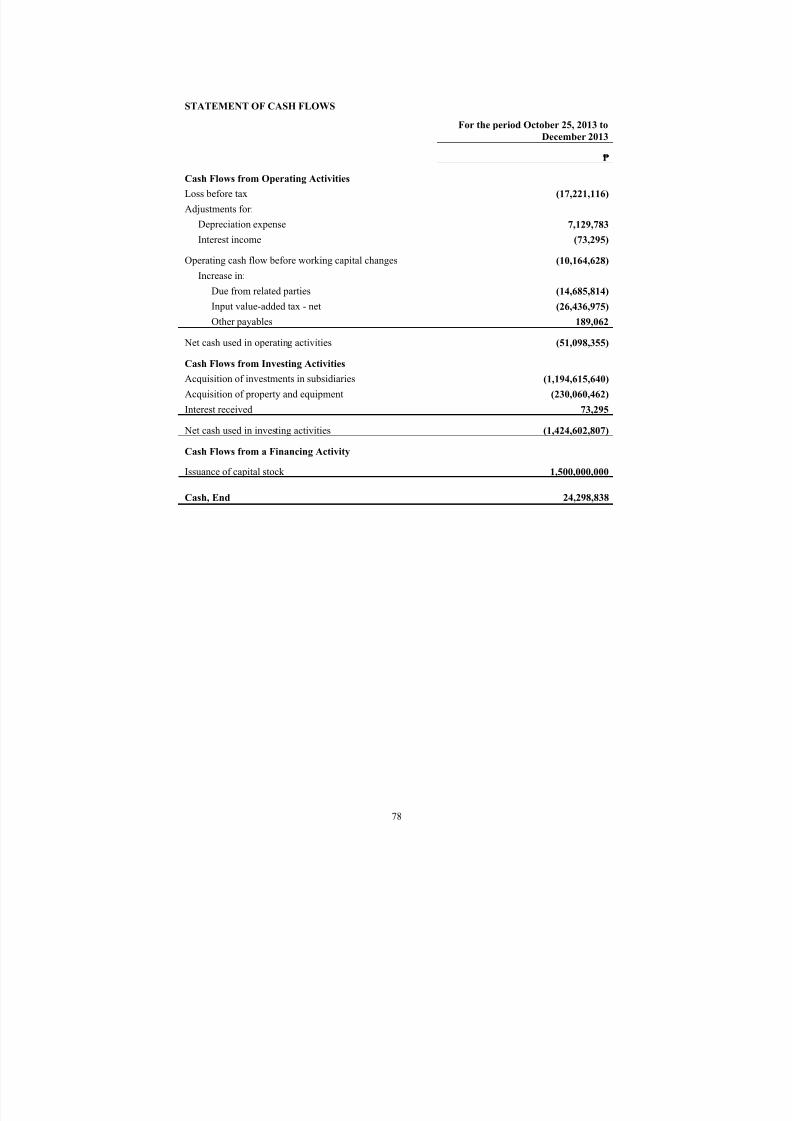

SELECTED PARENT FINANCIAL INFORMATION OF CNPF ....................................... 76

SELECTED CONSOLIDATED FINANCIAL INFORMATION OF CNPF ........................ 79

MANAGEMENT‘S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS OF THE PRO FORMA CONSOLIDATEDFINANCIAL INFORMATION OF CNPF ....................................................................... 82

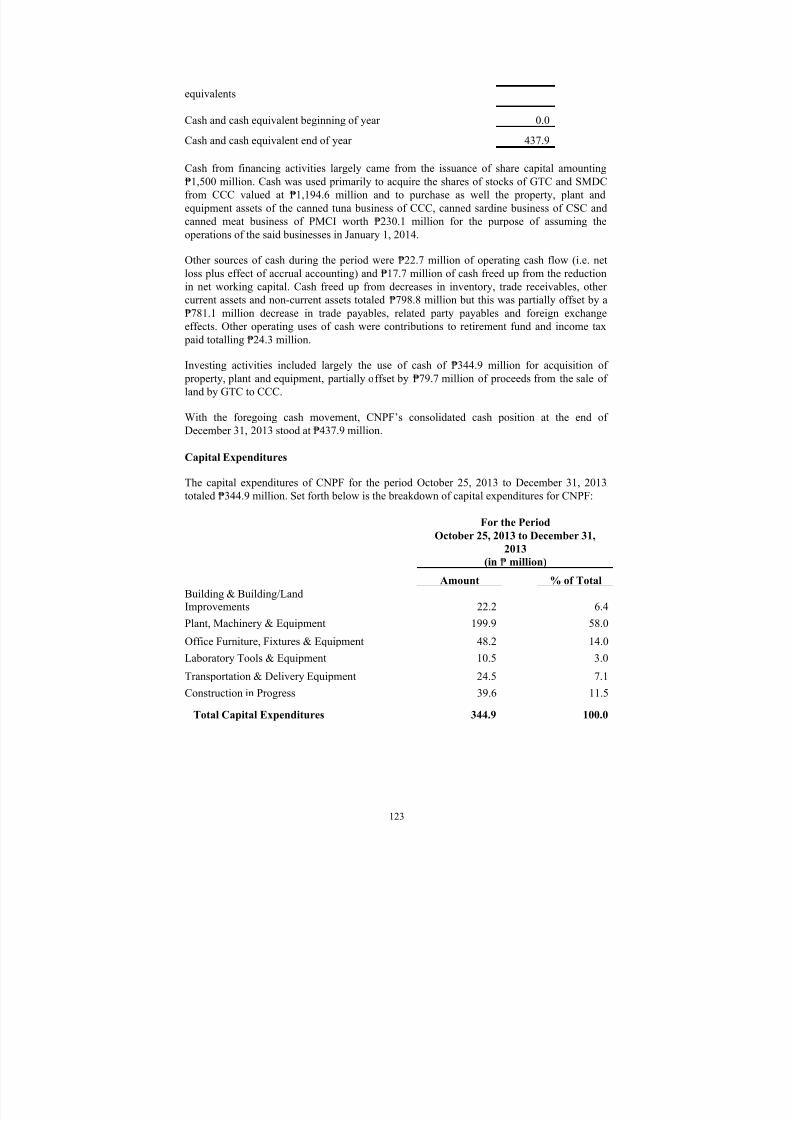

MANAGEMENT‘S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS OF THE COMBINED FINANCIALINFORMATION FOR GTC AND SMDC ....................................................................... 98

MANAGEMENT‘S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION

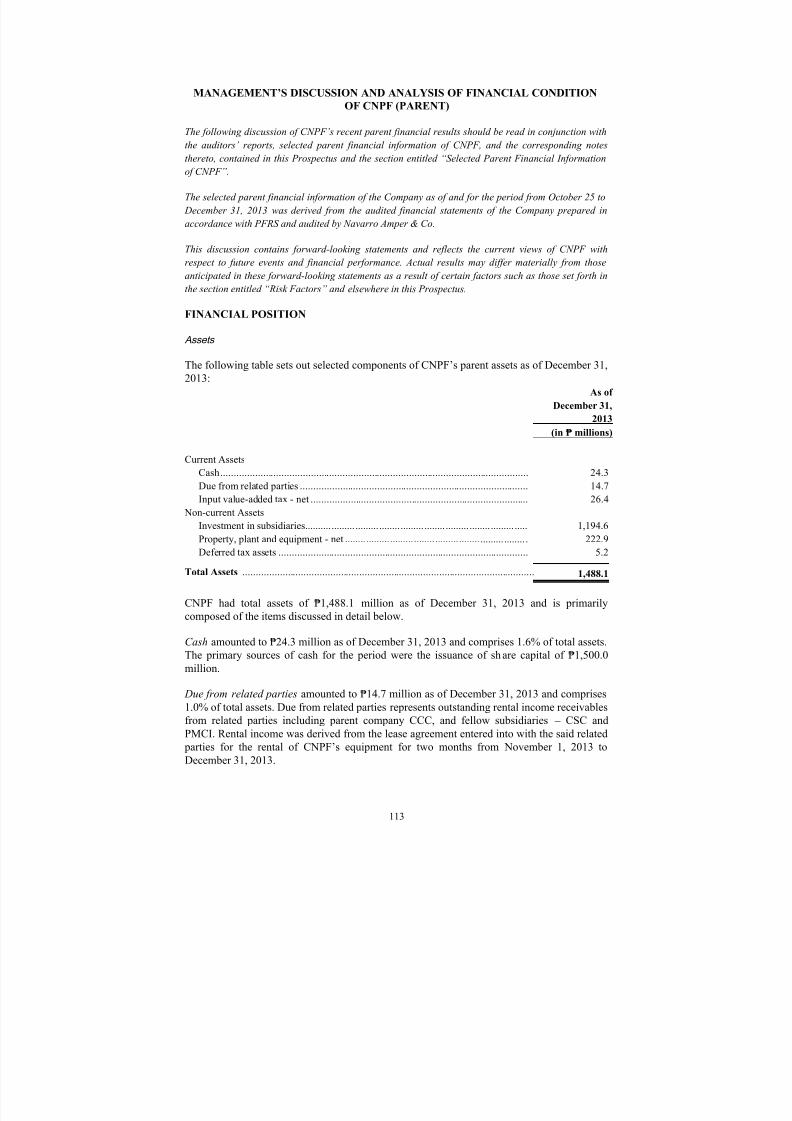

OF CNPF (PARENT)..................................................................................................... 113

MANAGEMENT‘S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS OF THE CONSOLIDATED FINANCIAL

INFORMATION OF CNPF ........................................................................................... 116

BUSINESS .......................................................................................................................... 127

INDUSTRY......................................................................................................................... 158

REGULATORY .................................................................................................................. 174

BOARD OF DIRECTORS AND SENIOR MANAGEMENT ............................................ 183

PRINCIPAL SHAREHOLDERS ........................................................................................ 192

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 12/648

MATERIAL CONTRACTS ................................................................................................ 195

RELATED PARTY TRANSACTIONS .............................................................................. 196

DESCRIPTION OF THE SHARES .................................................................................... 198

THE PHILIPPINE STOCK MARKET ............................................................................... 206

PHILIPPINE TAXATION .................................................................................................. 212

PHILIPPINE FOREIGN EXCHANGE AND FOREIGN OWNERSHIP CONTROLS ...... 218

LEGAL MATTERS ............................................................................................................ 220

INDEPENDENT AUDITORS ............................................................................................ 221

INDEX TO FINANCIAL STATEMENTS ......................................................................... F-1

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 13/648

GLOSSARY OF TERMS

In this Prospectus, unless the context otherwise requires, the following terms shall have themeanings set forth below.

BFAR Bureau of Fisheries and Aquatic Resources

BIR The Philippine Bureau of Internal Revenue

Board of Directors or Board The Board of Directors of the Company

BOC The Philippine Bureau of Customs

BSP Bangko Sentral ng Pilipinas, the central bank of thePhilippines

CCC Century Canning Corporation

Century Group Century Canning Corporation, together with its subsidiariesand affiliates

CIO Chief Information Officer of the Company

Common Shares Common shares of the Company with par value of ₱1.00 pershare

Company or CNPF Century Pacific Food, Inc., incorporated on October 25,2013 in the Philippines; references to the Company or CNPFinclude references to its subsidiaries, unless the context

otherwise provides

Corporation Code or

Philippine Corporation

Code

The Corporation Code of the Philippines, Batas PambansaBlg. 68

CSC Columbus Seafoods Corporation

DA Department of Agriculture

Director(s) the Director(s) of the Company

DTI Department of Trade and Industry

DOH Department of Health

EBIT Net operating income before interest and tax as calculated by the Company and as presented in this Prospectus

ECC Environmental Compliance Certificate

EIS Environmental Impact Statement

EMB Environmental Management Bureau

FARMC Fisheries and Aquatic Resources Management Councils

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 14/648

GDP Gross Domestic Product

GMP Good Manufacturing Practices

GNP Gross National Product

GTC General Tuna Corporation

HACCP Hazard Analysis Critical Control Point

Halal An Arabic term which means allowed, lawful, legal, or permissible under the Shariah (Islamic Law).

HDMF Home Development Mutual Fund

IEE Initial Environmental Examination

IFRS International Financial Reporting Standards

IPO Tax The tax on sale, barter, exchange or other dispositionthrough an IPO of shares of stock in closely heldcorporations as provided under Section 127 of the Tax Code

IRO Investor Relations Officer of the Company

ITH Income Tax Holiday

LGU Local Government Unit

Listing Date the date of listing and when trading of the Common Shares

commences on The Philippine Stock Exchange, Inc.

LSI Local Small Investors

Moody’s Moody‘s Investors Service

MPO Rule on Minimum Public Ownership

MT Metric Ton

Navarro Amper & Co. Member of Deloitte Touche Tohmatsu Limited

NHIP National Health Insurance Program

NMIS National Meat Inspection Service

Offer The offer and issuance of the Offer Shares

Offer Price Up to ₱14.50 per Offer Share

Offer Shares 229,654,404 new Common Shares

Offer Settlement Date On or about 06 May 2014

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 15/648

OFWs Overseas Filipino Workers

PCD Philippine Central Depository

PHP or P Philippine Peso

PDS Philippine Dealing System

PDTC The Philippine Depository & Trust Corporation

PFRS Philippine Financial Reporting Standards

PHIC Philippine Health Insurance Corporation

Philippine FDA Philippine Food and Drug Administration

Philippine Labor Code Presidential Decree No. 442, as amended.

PMCI The Pacific Meat Company, Inc.

PNP Philippine National Police

PSA Philippine Standards on Auditing

PSE The Philippine Stock Exchange, Inc.

PSE Trading Participants All trading participants of the PSE

QIB or Qualified

Institutional Buyer

Qualified buyers within the meaning of Section 10.1(l) of

the SRC

R.A. Republic Act

ROS Return on Sale

SCCP Securities Clearing Corporation of the Philippines

SEC Securities and Exchange Commission

SKU stock keeping unit; a store‘s or catalog‘s product and service

identification code, often portrayed as a machine-readable

bar code that helps the item to be tracked for inventory

SMDC Snow Mountain Dairy Corporation

SSOP Standard Sanitation Operating Procedure

sq. m. Square meter(s)

SRC Securities Regulation Code of the Philippines

Tax Code National Internal Revenue Code of 1997 of the Philippines

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 16/648

(Republic Act No. 9337) and its implementing rules, as

amended

US$ United States Dollar

US FDA United States Food and Drug Administration

VAT Value-added tax

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 17/648

SUMMARY

The following summary is qualified in its entirety by, and is subject to, the more detailed information

presented in this Prospectus, including the Company’s pro forma consolidated financial statements and

related notes included elsewhere in this Prospectus. Capitalized terms not defined in this summary are

defined in the ―Glossary of Terms,‖ ―Risk Factors,‖ ―Business‖ or elsewhere in this Prospectus.

Overview

CNPF traces its history from the Century Group, a leading branded food company primarily

engaged in the development, processing, marketing and distribution of processed fish and

meat, as well as processed dairy products in the Philippines.

In October 2013, the Century Group began to undertake a general corporate reorganization

transaction. Prior to the corporate restructuring, the company‘s businesses were operated by

different companies:

Seafood

Century Canning Corporation (―CCC‖) incorporated on December 12, 1978 handled the

Group‘s sales and distribution for canned and processed tuna, sardines and bangus. Products

are marketed under 555 for sardines, Century Tuna and 555 for tuna. Columbus Seafood

Corporation (―CSC‖), incorporated on December 20, 1994, operated the manufacturing plant

for the sardines. General Tuna Corporation (―GTC‖), incorporated on March 10, 1997,

operated the tuna processing both for local and export sales.

Meat

The Pacific Meat Company, Inc. (―PMCI‖), incorporated on June 28, 1994, manufacturedcanned and frozen processed meat under the brand names Argentina, Swift and 555.

Dairy

Snow Mountain Dairy Corporation (―SMDC‖), incorporated on February 14, 2001, handles

the dairy and sinigang mixes under the brands of Birch Tree, Angel , Home Pride and Kaffe de

Oro.

In order to streamline and rationalize the Group‘s operations, the business operations of CCC,

CSC and PMCI were folded into CNPF, the listing vehicle. The business operations of CCC

and CSC were folded into CNPF under the canned and processed fish segment. The canned

meat business operations of PMCI were folded into CNPF under the canned meat segment.

SMDC, handling the dairy and mixes segment, and GTC, handling the private label canned,

pouched and frozen tuna products for export, were retained as separate corporate entities as

wholly-owned subsidiaries of CNPF.As a result, the pro forma financial statements of CNPF

are a product of the combination of the businesses of CCC, PMCI, CSC, GTC and SMDC.

With this operating history spanning the last 35 years, CNPF has established a strong brand

and product portfolio through, and supported by, continuous product innovation and

acquisition of brands from third parties. Its brands are well-recognized in the Philippines and

include 555 for sardines, Century Tuna and 555 for tuna, Argentina and Swift for canned

meats and Angel and Birch Tree for canned and powdered milk. CNPF was the largest

producer of canned foods in the Philippines in terms of retail value according to Euromonitordata for February 2013. The quality of CNPF‘s products has been recognized by numerous

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 18/648

consumer and industry association awards. For example, Century Tuna received the Trusted

Brand Award from Reader‘s Digest in 2011, 2012 and 2013 and Argentina Corned Beef

received the same award in 2012 and 2013. As of December 31, 2013, CNPF offered 283

products which can be found in 3,772 modern retail outlets, approximately 225,168 directly

served general trade outlets and 330,749 indirectly served points of sale, totaling over559,689 points of sale throughout the Philippines.

CNPF operates five production facilities and distributes its products through 14 distribution

centers strategically located across the Philippines. CNPF distributes its products directly to

retailers, as well as through third-party distributors. As at December 31, 2013, CNPF

maintained 200 manufacturer direct-to-retail accounts reaching 3,772 retail outlets in the

Philippines. In addition, as at December 31, 2013, CNPF held distribution agreements with 39

distributors, reaching approximately 225,168 retail outlets ranging from supermarkets to sari-

sari stores. Furthermore, as of December 31, 2013, CNPF exports both private label and

branded products, which are distributed across North America, Europe, Asia, Australia, and

the Middle East.

For the year ended December 31, 2013, CNPF‘s net revenue was ₱19,023 million. CNPF‘s

net profit after tax for the same period was ₱743.9 million.

Business Segments

CNPF‘s business operations are divided into four main business segments: canned and

processed fish, canned meat, dairy and mixes and tuna export.

The canned and processed fish segment produces a variety of tuna, sardine and other fish and

seafood- based products. CNPF‘s key brands in the canned and processed fish segment include

Century Tuna, 555, Blue Bay and Fresca.

The canned meat segment produces corned beef, meatloaf and a variety of other meat-based

products. Key brands in this segment include Argentina, Wow and Swift .

The dairy and mixes segment primarily comprises canned milk, powdered milk and other

dairy products, as well as coffee mixes and sinigang mix. Key brands include Angel , Birch

Tree, Kaffe de Oro and Home Pride.

CNPF also produces private label canned, pouched and frozen tuna products for export to

major overseas markets including North America, Europe, Asia, Australia, and the Middle

East. In addition, CNPF‘s branded products are also exported to overseas mark ets and are

distributed across North America, Europe, Asia, Australia, and the Middle East.

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 19/648

For the year ended December 31, 2013, the contribution of each business segment to CNPF‘s

total revenue, based on CNPF‘s pro forma consolidated financial information as of and for the

year ended December 31, 2013, is as follows:

Year ended December 31, 2013

(in ₱ millions)

Revenue

% of

Total

Net

Income

% of

Total

Canned and Processed Fish 7,014 36.9 137 18.4

Canned Meat 4,598 24.2 360 48.4

Dairy and Mixes 1,548 8.1 45 6.0

Tuna Export 5,863 30.8 210 28.2

Other Segment Income (―CNPF‖) (8) (1)

Total 19,023 100.0 744 100.0

The abovementioned revenue and net income were derived from the historical auditedseparate financial statements of the Company, GTC, SMDC, CCC, PMCI and CSC thenadjusted to give the pro forma effect of the consolidation of the businesses of the saidcompanies as shown in the table below:

Year ended

December 31,

2013 (in ₱

millions)

AcquisitionsTotal before

Pro Forma

Adjustments

Pro forma

Adjustments

Pro forma

ConsolidatedCNPF GTC SMDC CSC PMCI CCC

Net sales - 5,863 1,556 1,633 5,063 5,505 19,620 (597) 19,023

Cost of Sales - 5,623 1,222 1,420 3,932 4,071 16,269 (572) 15,697

Gross profit - 240 334 213 1,130 1,434 3,351 (25) 3,326

Other Income 13 127 0 35 24 859 1,058 (882) 176

Operating

profit 13 367 334 248 1,154 2,293 4,409 (907) 3,502

Operating

expenses 30 148 275 160 763 1,366 2,743 (328) 2,415

Finance cost - 49 2 3 25 52 131 (19) 112

OtherExpense - 3 - 7 4 - 14 - 14

Profit (loss)

before tax (17) 166 57 78 363 875 1,521 (561) 960

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 20/648

Income tax

expense (5) 28 15 25 105 48 217 (1) 216

Profit after

tax (12) 138 42 52 257 827 1,304 (560) 744

Pro forma adjustments were made to the December 31, 2013 historical consolidated financialinformation of the Company and its subsidiaries (GTC and SMDC), and the acquired

businesses (CSC, PMCI, CCC), which include the following:

Consolidation of the Company and its subsidiaries (GTC and SMDC) and elimination of

investment and equity amounting to ₱1.137 million.

Recognition of identified assets and liabilities of CCC, CSC and PMCI and the related

operations as well as the accumulated earnings as of December 31, 2013. The difference

between the balance of the assets acquired and liabilities assumed was recognized in

retained earnings.

Elimination of frozen processed meat business from PMCI.

Elimination of intercompany and inter-business transactions and account balances.

Elimination of cash dividends from GTC and SMDC amounting to ₱382 million and gain

from the sale of shares of stocks of GTC and SMDC between CCC and the Company

Recognition of rental expense in relation to the land and office spaces that were not sold

to the Company and elimination of depreciation related to aforementioned assets.

Re-computation of income tax to include the effects of the pro forma adjustments.

CCC and CSC (Canned and Processed Fish). Net sales from the canned and processed fish

business segment totaled ₱7,013.8 million, or 37% of total CNPF sales, for the year ended

December 31, 2013. Of these sales, canned tuna and milkfish contributed ₱5,380.8 million

while canned sardine accounted for ₱1,633.0 million. Gross profit for the segment totaled

₱1,659.2 million, or a gross profit rate of 24%. This gross profit consisted of ₱1,383.4 million

from canned tuna and milkfish and ₱275.8 million for canned sardine. Net income for the

segment totaled ₱136.5 million, or an equivalent segment return on sales of 2%. Of this

segment net income, ₱158.8 million was shared by canned tuna and milkfish while ₱161.4

million was from canned sardine.

GTC (Tuna Export). Net sales from the tuna export business segment totaled ₱5,862.7

million. This represented 31% of total CNPF sales and comprised sales of canned tuna,

pouched tuna and frozen loins to the private-label export market. Gross profit was ₱301.6

million, or a segment gross profit rate of 5%. Net income totaled ₱209.6 million for a segment

return on sales of 4%.

PMCI (Canned Meat). Net sales from the canned meat business were ₱4,598.6 million for the

year ended December 31, 2013, which represented 24% share of the total CNPF sales. Net

sales included sales to the modern trade accounts, general trade accounts, food service

accounts and export accounts for canned products including corned beef, meat loaves, ready-

to-eat viands. Gross profit for canned meat was ₱1,040 million, or a segment gross profit rate

of 31%. Net income for canned meat totaled ₱360.1 million, or a return on sales of 8%.

SMDC (Dairy and Mixes). Net sales from the dairy and mixes business was ₱1,548 million

for the year ended December 31, 2013, which represents 8% share of the total CPF sales. Net

sales includes sales of evaporated milk, condensed milk, creamers, full cream powdered milk,

flavour mixes and 3-in-1 coffee products. Gross profit for the segment amounted to ₱ 325.5

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 21/648

million for an equivalent gross profit rate of 21%. Net income totaled ₱45.5 million, or a 3%

return on sales ratio.

Competitive Strengths

The Company believes that the following are its key business strengths:

Established market leadership positions with iconic, well-recognized and trusted brands

The Company is the largest producer of canned foods in the Philippines in terms of retail

value according to Euromonitor data for February 2013. In addition, the Company‘s brands

have established market-leading positions within each of their respective segments. For

example, based on data from AC Nielsen, in 2012, the Company was the market leader in the

Philippines in domestic canned tuna, with a market share of 87% by sales. In addition, based

on AC Nielsen data as of August 2013, the Company was the market leader in corned beef

with a market share of 42.5% by sales and the market leader in meat loaf with a market share

of 25.6% by sales.

Several of the Company‘s brands have a long heritage and are well-recognized and trusted

brands in the Philippines. The Company believes that customers associate its brands with

health and quality. Such brands include Century Tuna which was launched in 1986, Argentina

Corned Beef which was launched in 1995 and Angel which was launched in 2002. TheCompany has also grown its brand portfolio through brand acquisitions, including the

acquisition of Blue Bay in 2001, Birch Tree in 2003, Kaffe de Oro and Home Pride in 2008

and Swift in 2012. As a result of the heritage and strength of the Company‘s brands as well as

their high standards of quality, the Company has won a number of industry, consumer and

marketing awards including the Agora Awards‘ Marketing Company of the Year Award for

Century Canning Corporation (2011) and the Trusted Brand Award by Reader‘s Digest for

Century Tuna (2011, 2012 and 2013) and Argentina Corned Beef (2012 and 2013).

The Company continues to enhance brand recognition among consumers by consistently

maintaining high product quality, as well as through active and targeted marketing and

promotional campaigns such as using well-recognized celebrities to endorse its products. The

Company believes that its well-recognized brands have allowed it to develop strong customer

loyalty resulting in repeat purchases that provide it with greater pricing power relative to its

competitors.

Furthermore, the Company believes that the established reputations and market-leading

positions of its brands provide a strong platform to maintain and grow its market shares

through new products, product line extensions and expansion of its distribution networks.

Multi-category, multi-brand product portfolio catering to different customer tastes and

price points

The Company has a diverse product portfolio with multiple product lines across fish, meatsand dairy. As of December 31, 2013, the Company had a portfolio comprising 128 SKUs for

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 22/648

tuna products, 101 SKUs for canned meat products, 25 SKUs for sardine products and 29

SKUs for dairy and mixes products. The Company produces numerous product variants to

cater to different customer tastes. For example, the Company produces chicken, pork and

tuna-based vienna sausages to capture the full range of consumer preferences for this product.

In addition, the Company packages its products in different sizes to target different customer price points. This diverse product portfolio allows it to capture a larger share of the

consumers' wallets and provides broader avenues for future growth, both within and across its

key product categories. In addition, this also reduces its dependence on any single product

category or brand, and makes the Company more resilient to changes in the competitive

landscape or price fluctuations in raw material that may impact one product category more

than another.

In addition, leveraging on the Company's strong reputation and recognition for product

quality, the Company has also developed a multi-brand strategy within each product segment

that allows it to broaden its reach to customers more easily than its competitors. Within each

of its product segments, the Company offers a wide portfolio of brands and products to meet a

diverse range of consumer tastes, preferences and price points allowing for a comprehensivecoverage of the Filipino consumer market. For example, in the canned tuna segment, the

Century Tuna brand targets the up-market canned tuna consumer whereas the 555 Tuna brand

is aimed at the budget or cost-conscious canned tuna consumer. This allows the Company to

broaden its customer base and capture the benefits from growth in disposable income from a

larger proportion of the population. In addition, this segmentation allows the Company to

target consumers in different regions with different demographics with the right brand, as

well as react quickly and opportunistically to changes in consumer preferences and to act

defensively against any action by competitors.

The Company‘s diverse product portfolio also provides marketing and product synergies

across segments. For example, product recipes and formulations achieved through internalresearch and development are shared across product segments. In addition, international best

practices implemented in the tuna export segment are shared across the Company‘s various

production lines, improving production processes and enhancing product quality.

Strong track record of product innovation and successful introduction of new products

Product innovation and development has been an important element in the Company‘s

business strategy and has been crucial to the Company‘s success. The Company has

demonstrated strong innovative capabilities as shown by its consistent track record of

launching new products to address changing consumer needs and preferences. For example,

the Company differentiates its products from plain canned tuna/meat by developing new

flavors and dishes that are designed and packaged as ready-to-eat meals. In particular, theCompany‘s ready-to-eat dishes use tuna as the main ingredient in traditionally beef, pork and

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 23/648

chicken- based dishes such as kaldereta, adobo and afritada to increase consumers‘ acceptance

of the product while providing consumers with a healthier alternative. In the dairy segment,

the Company has successfully introduced two-in-one products such as Angel Kremdensada (a

combination of all-purpose cream and condensed milk) and Angel KremQueso (a combination

of all-purpose cream and cheese) to provide convenient and cost-effective options forconsumers. In addition to innovative products, the Company has noticed a shift in preference

from canned products to flexible packaging or products sealed in pouches. In response, the

Company has started to produce pouched tuna products.

Furthermore, the Company has a strong ability to bring its products to the market using

innovative marketing strategies. The Company‘s marketing campaigns are jointly developed

between its highly experienced in-house marketing team and independent creative agencies.

The Company employs the use of celebrity endorsements in its marketing strategies to link

each product to the intended branding message. Over the years the Company has launched

numerous successful marketing campaigns, including a focused marketing campaign for

Argentina Corned Beef , which became the leading brand in its segment. The Company viewsits ability to market its products as a critical success factor and invests heavily in advertising

and endorsements. The Company‘s ability to develop new products and successfully bring

them to the market allows the Company to further segment each product category and tailor it

to consumers‘ tastes and preferences, preventing product commoditization.

Extensive market penetration through multi-channel distribution network

The Company operates and manages one of the most extensive distribution networks across

the Philippines, with its products available in every major city, creating a significant

competitive advantage.

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 24/648

The Company has developed strong relationships directly with retailers, including modern

and general trade stores, as well as through third-party distributors. Approximately 58% of the

Company‘s distribution is through modern trade and approximately 42% is through general

trade. As of December 31, 2013, the Company‘s modern trade coverage holds 200 direct

accounts and 3,772 outlets, comprising national retail chains with outlets across the

Philippines, such as Robinsons Supermarkets, SM Supermarkets, Metro department stores,

Puregold and 7-Eleven, as well as regional retailers. The Company‘s general trade coverage

has grown significantly from approximately 70,000 outlets in 2010 to approximately 225,168

outlets including sari-sari stores, wet markets, wholesalers and regional supermarkets in

2013. The Company operates 14 distribution centers, allowing the Company to respond

quickly to changes in customer demand.

In addition, the Company employs its own sales and distribution force consisting of

approximately 159 personnel, including sales administration and support functions. The

Company believes that employing a majority of its sales force in-house has resulted in a

relatively higher level of motivation and incentivization among its employees that hascontributed to the strong growth in the sales of the Company‘s products. This arrangement

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 25/648

also enables the Company to work closely with its customers and develop strong relationships

with them. The Company continually seeks ways to expand the reach of its distribution

network, especially in the Mindanao and Visayas regions. The Company believes that its

multi-channel distribution network and its strong relationships with customers has allowed it

to maximize customer reach and has been one of the key factors to its success in building anddeveloping its market-leading positions.

CNPF‘s extensive distribution network is supported by its strategically located production

facilities. The Company‘s tuna processing facility, with an installed capacity of 360 MT per

day as of December 31, 2013, is located in General Santos, Mindanao, which is the heart of

the Philippine tuna industry as it is geographically adjacent to two large tuna fishing grounds,

the Western Pacific Ocean and the waters between Southern Philippines and Indonesia. In

addition, one of the Company‘s sardine processing facilities, with an installed capacity of 200

MT per day as of December 31, 2013, is located in Zamboanga, which is the center of the

Philippine sardine industry. The proximity to the source of supply ensures the availability of

fresh fish, a critical element in maintaining a high quality product and lowering the

Company‘s logistics costs. The Company‘s meat processing plant and milk and mixes plant,located in Laguna and Taguig, respectively, are also strategically located close to major

markets, which reduces the cost of transporting products to customers. The Company‘s meat

processing plant has an installed capacity of 194 MT per day as of December 31, 2013 while

the Company‘s milk and mixes plant has an installed capacity of 11,000 cases per day as of

December 31, 2013.

Highly scalable export business that supplies processed tuna to leading international

companies and distributes branded products to high growth markets

The Company‘s export business, comprising private label processed tuna as well as branded

products, is complementary to its domestic business as it helps increase scale and reduce

costs, increasing the Company‘s competitiveness. An additional benefit of the scalability of

the export business is that it allows the export business to focus on quality and achieve higher

margins.

The Company has developed a reputation in the international food manufacturing community

as a reliable and trusted partner. It has supplied some of the largest food manufacturers

globally, including Chicken of the Sea, Bumblebee Foods LLC, Subway, Princes, Rio Mare,

Hagoromo, Hoko and California Garden. The Company is constantly looking to enter into

additional agreements with potential partners. The Company believes that supplying leading

global food manufacturers in some of the most stringently regulated markets in the world

represents an endorsement of the quality of the Company‘s products.

The Company currently supplies to brands and retailers in five continents and covers major

markets including North America, Europe, Asia and Australia, and the Middle East, broken

down as follows:

2013 2012 2011

% of total exports

North America 7% 12% 38%

Europe 44% 16% 16%

Asia and Australia 49% 67% 40%

Middle East 0% 5% 6%

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 26/648

The Company was the leading Philippine exporter of canned tuna and frozen tuna loin

products for the year ended December 31, 2013, with a market share of 34% according to data

from the Philippine Bureau of Customs (the ―BOC‖).

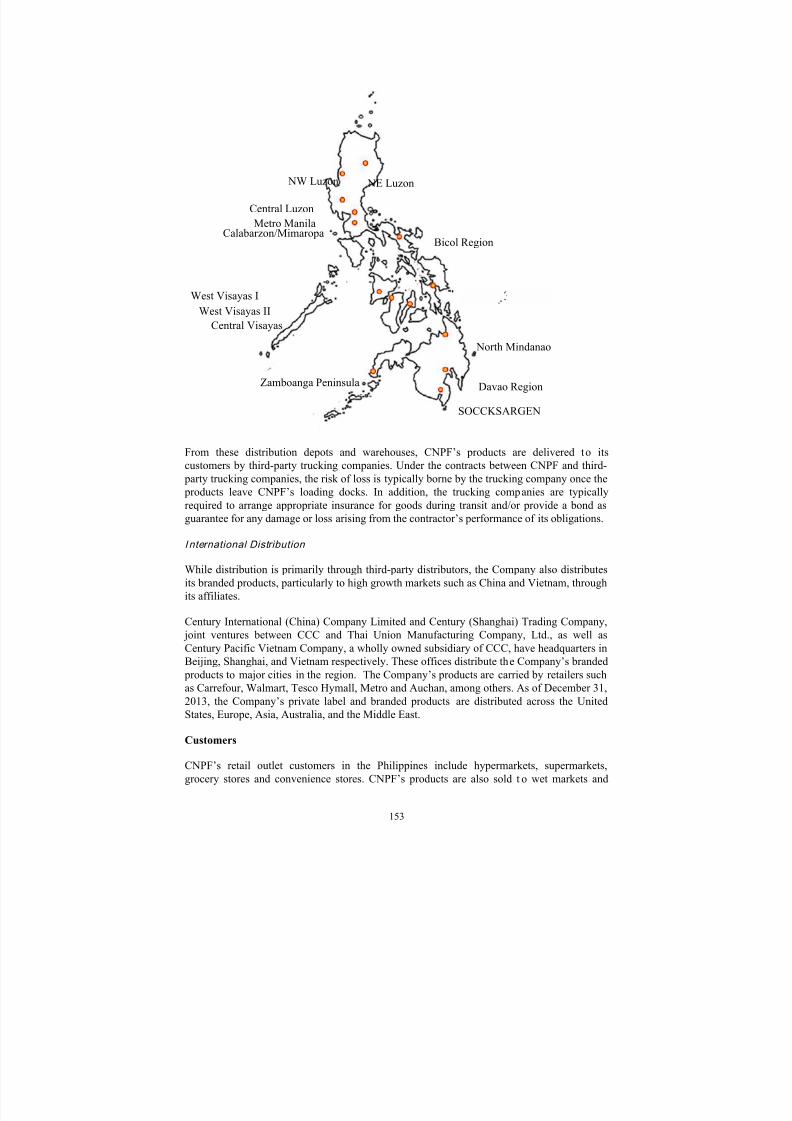

The Company also distributes its branded products internationally, particularly to China and

Vietnam, through its affiliates. Century International (China) Company Limited and Century

Shanghai Trading Company, joint ventures between CCC and Thai Union Manufacturing

Company, Ltd., as well as Century Pacific Vietnam Company, a wholly owned subsidiary of

CCC, have headquarters in Beijing, Shanghai, and Vietnam, respectively. These offices

distribute the Company‘s branded products to major cities in the region. The Company‘s

products are carried by retailers such as Carrefour, Walmart, Tesco Hymall, Metro and

Auchan, among others. As of December 31, 2013, the Company‘s private label and branded

products are distributed across North America, Europe, Asia, Australia, and the Middle East.

CNPF has earned a number of international accreditations for food safety and quality. CNPF

has been accredited by the US FDA, the Canadian Food Inspection Agency, the British Retail

Consortium, the European Union, the Orthodox Union and the Islamic Dawah Council. Inaddition, all of CNPF‘s processing facilities apply the Hazard Analysis and Critical Control

Points (the ―HACCP‖) plan, a management system which addresses food safety through the

analysis and control of biological, chemical and physical hazards from raw material

production, procurement and handling to manufacturing, distribution and consumption of the

finished product

Experienced and dedicated management team

The Company is led by an experienced and dedicated management team with a proven track

record of success. Members of the senior management team have an average of over 25 years

of industry experience, including experience working in large, multinational corporations in

the food industry. The management team is well accustomed to the Philippine operating

environment and has effectively managed the Company both in times of strong economic

growth as well as through periods of economic downturn and political instability. The

strength and depth of the experience of the Company‘s management team have been

demonstrated by their successful implementation of a range of efficiency programs and

product innovations, which has resulted in continued profitability and market leadership for

the Company over the years. In addition, management team has a proven track record of

turning previously under-promoted and neglected brands, such as Birch Tree and Blue Bay,

into successful brands by applying the Company‘s strategies, such as proper branding and

extensive national distribution coverage.

The Company believes that members of its management team are highly regarded in theindustry, and they hold a variety of leadership positions in food industry organizations, such

as the Sardine Association of the Philippines, the Philippine Association of Meat Processors

Inc., the Tuna Canners‘ Association of the Philippines. The management team‘s industry

leadership positions also create a valuable local business network for the Company.

Strategies

The Company seeks to strengthen its leading market position in the Philippines and expand its

business operations by implementing the following business strategies:

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 27/648

Actively develop and manage product and brand portfolios to target different price

points and respond to emerging market trends

The Company has a history of driving growth through new and innovative products,

capitalizing on emerging market trends and introducing extensions of successful product

lines. The Company will continue growing its existing product categories and deliver

innovative products under trusted brands and the Company is committed to developing and

expanding its product categories to meet evolving consumer tastes and preferences. In

addition, the Company will continue to market different brands to target different consumer

price points. For example, the Company believes that there are growth opportunities in the

canned meat market and plans to target the premium segment through the development of the

Swift brand.

The Company also intends to continuously review its product offerings to rationalize

unprofitable products from its portfolio. To enhance the stability of its revenue stream and

profit margins, the Company plans to increase the percentage of sales of products that have

performed well and which the Company believes will continue to do so. For example, asPhilippine consumers have become more health conscious, the Company‘s marketing strategy

has evolved to highlight the health benefits of Century Tuna and to present the Company‘s

ready-to-eat tuna viands as healthier alternatives to traditional beef, pork and chicken-based

dishes. The Company has also noticed a shift in consumer preference from canned products to

products in sealed pouches or flexible packaging. The Company has pre-empted this shift in

preference and has developed the capability to produce pouched products. The Company

intends to increase its product offerings in pouched or flexible packaging, which the

Company believes will develop new product segments and further penetrate the ready-to-eat

meal segment.

In addition, the Company is ranked second in the Philippine condensed/evaporated milk

market and third in the Philippine all-purpose cream segment, according to AC Nielsen. The

Company sees a strong growth opportunity for the dairy market and has developed various

initiatives to grow its dairy business. For example, the Company has responded to changing

consumer preferences and plans to develop ready-to-drink products. The Company also plans

to continue aggressively promoting the Angel and Birch Tree brands through marketing

campaigns within the next two years. In particular, the Company plans to grow the Angel

brand through improved formulations, smaller packaging sizes for more budget-conscious

consumers and achieving a market leading position in the two-in-one product platform for

canned milk and cream. For the Birch Tree brand, the Company intends to expand into adult

and children‘s milk segments through powdered milk, flavored milk drinks and other product

formats.

Expand distribution network to capitalize on growing retail segments and target

customers in high growth segments

The Company plans to capitalize on rapidly growing retail segments such as 24-hour

convenience trade and modern trade channels, and to expand its distribution network,

targeting to reach 250,000 directly served points of sale in 2014. In particular, the Company

plans to expand its distribution network in the Philippines by increasing the number of retail

outlets that its regional sales force services directly. At the same time, the Company is

working with its distributors to increase its penetration of general trade outlets, particularly in

more remote areas such as Mindanao and the Visayas. In addition, there are regions in the

Philippines such as Central Visayas where the Company is not the market leader due the

incumbency of regional market leaders. However, the Company believes that with sustained

presence through a well-developed distribution network in those regions, the Company will

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 28/648

be able to gain market share in those areas. The Company believes that the Philippine market

is still underserved in certain product categories and there are growth opportunities to

improve its distribution network. The Company plans to penetrate these underserved areas by

reaching out to a greater number of smaller informal retailers such as sari-sari stores and wet

markets.

Another area the Company has identified as a growth avenue is the food service segment.

While sales to food service customers, such as, but not limited to, Jollibee, KFC, Starbucks

and 7-Eleven, contributed less than 3% of the Company‘s total revenue for the year ended

December 31, 2013, the Company believes there are significant opportunities to work closely

with customers and expand existing relationships, as well as establish relationships with a

wider range of customers in this segment. The Company understands the needs of its food

service customers and proactively suggests new products or recipes suited for such

customers‘ business. As its food service customers continue to expand their business, the

Company intends to further collaborate with such customers and increase its sales in this

segment.

Enter into new product categories

In addition to growing and developing its existing product and brand portfolio, the Company

plans to enter into new product categories. The Company believes its competitive strengths

and deep understanding of the Philippine market provide significant advantages when

entering into new product categories. In 2014, the Company plans to start marketing and

distributing beverage products, such as coconut water, by leveraging on the Company‘s

extensive distribution network and experienced sales and marketing personnel. The

Company‘s marketing strategy will highlight the health benef its of these beverage products in

line with the Company‘s health and wellness theme and will enable the Company to penetrate

new product categories.

The Company also entered into a distribution agreement with Kapal Api of Indonesia in

November 16, 2012 to distribute Kapal Api‘s coffee products in the Philippines. Kapal Api is

an Indonesian company engaged in, among others, the operation of a coffee plantation, the

production of non-dairy creamer, the production of espresso machines, and the distribution of

coffee and coffee products.

Optimize export business to further penetrate the private label export market and

increase presence of branded products in overseas markets

As the current leading tuna exporter in the Philippines, the Company is well positioned to

increase its market share in the export business. The Company intends to increase the numberof partners for its private label export business in order to gain greater scale and better

capitalize on economies of scale. The Company believes this should further improve profit

margins of its export business.

The Company currently distributes its branded products across North America, Europe, Asia,

Australia, and the Middle East. The Company has noticed increasing brand awareness among

Filipino communities around the world and similar demands from Latino communities. While

overseas Filipino communities were the initial target customer base for its branded exports,

the Company has seen growing demand for its products in mainstream markets as the

Company continues to build the presence of its branded products in overseas markets. The

Company intends to capitalize on this trend and has started to sell its branded products to

Walmart, Albertsons and Kroger in the US, as well as negotiate with other retailers to have its

products sold in Asian food sections of their stores. The Company plans to enter into

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 29/648

distribution agreements with several other large retailers in North America likely within the

next 12 months.

Opportunistic acquisition and development of strong regional brands

The Company has a proven track record of turning previously under-promoted and neglected

brands into market leading brands by applying its strategies, such as proper marketing and

extensive national distribution coverage. For example, Birch Tree was a strong brand in the

Philippines in the 1970s but lost significant market share as it did not receive marketing

support for many years prior to the Company‘s acquisition of the brand in 2003. After

acquiring the brand, the Company initially relied on its distribution network to increase the

penetration of Birch Tree products in modern and general trade outlets. The Company then

supported the brand through a strategic marketing campaign. Through the Company‘s efforts,

the Birch Tree brand was able to grow to 22.0% market share in the full cream milk powder

segment as of July 2011, according to AC Nielsen. The Company will continue to seize

acquisition opportunities and acquire brands opportunistically to penetrate new market

segments. Examples include the Century Group‘s recent acquisition of Swift from RFMCorporation in 2012, which allowed the Century Group to compete in the premium canned

meats segment, and the Century Group‘s acquisition of the Home Pride and Kaffe De Oro

brands in 2008.

Cost improvements through backward integration, streamlined logistics and cost-

engineering

The Company is focused on increasing the efficiency of its existing operations and

implementing targeted cost-saving initiatives in its businesses. In particular, the Company

intends to implement cost improvements through backward integration. The Company

sources the majority of its requirements from third-party suppliers. However, the Company

will be building a second tin can manufacturing facility which, upon completion by the end of

2014, is expected to produce approximately 25% to 30% of the Company‘s tin can

requirements. By producing a significant portion of its tin can requirements internally, the

Company will be able to improve its profit margins by sourcing the tin cans at cost and

reducing logistics costs associated with purchasing from third-party suppliers.

In addition, the Company‘s research and development team is an integral part of the

continued effort to identify cost improvements while maintaining high product quality

standards. For example, the Company‘s research and development team has been able to

increase the use of alternative raw materials, such as soy-based proteins, to lower production

costs for certain products. The Company estimates that research and development costs

accounts for less than 1% of its revenues.

The Company continues to periodically review and streamline its inter-island logisticsnetwork in order to improve operational and cost efficiencies. For example, the Company

7/21/2019 PreliminaryProspectus - Century

http://slidepdf.com/reader/full/preliminaryprospectus-century 30/648

plans to curtail the operations of or consolidate under-utilized depots and warehouses thereby

reducing costs while maintaining appropriate service coverage. The Company is also able to

leverage on its economies of scale to further rationalize its production and distribution costs.