Embed Size (px)

Citation preview

Preface

It is a report on the comprehensive study of “The Role of SME loan in small business

management”. The purpose of this endeavor is to acquire practical knowledge regarding

SMEs loan. The objective is to know how SMES play a vital role in the economic

development of our country. A group of students consisting five members from

university of Chittagong conducted the report. The group studies literature review for

secondary data collection and visits four companies named “Brac Bank Ltd, Datch

Bangla Bank Ltd, Eastern Bank Ltd and IDLC ltd. for primary data collection. Among

the four companies, the group finds responses from two companies. One company

suggested the group to collect data from their web sites. On the basis primary and

secondary data, the group prepares the report. The team gets inspiration from their class

teacher to make the paper. The report will be helpful to the persons e.g. students,

teachers, consultants, researchers, organizations, practitioners, etc.

Acknowledgement

Firstly we are grateful to the Almighty Allah for his mercy to completer the report. We

would like to thank our honorable teacher, Dr. A. F. M. Aowrangazab, professor,

Management Studies, University of Chittagong for his sincere assistance and suggestions

in preparing the project paper. Without his support, it was quite impossible to prepare the

project. We also would like to thank Mr. Md. Shahidul Islam, officer Dutch- Bangla

Bank Ltd. We remember him for that he has given valuable time despite his busy work.

We also get Assistance from the officers of Brac Bank ltd, Easter Bank Ltd. So thank to

them.

We also thank to our friends, classmates for their oral support.

TABLE OF CONTENTS

Page Title Page No

Executive Summary 2

Definition of SMEs 3

Present scenario of SMEs in Bangladesh 4

SME Foundation of Bangladesh 5

SMEs and Financial Institutions 9

Special initiatives of Government 13

Contributions of SMEs to national economy 15

Challenges or problems faced by SMEs 16

Prospects of SMEs in Bangladesh

Recommendations

Conclusion

References

Executive Summary

Small and Medium Enterprises (SMEs) have historically been one staples of the

enterprise landscape within economies globally. Especially growth with clear benefits for

poverty reduction puts a premium on integrating, productively and profitably, small and

medium enterprises in the very process of economic growth. The SMEs sub-sector plays

an increasingly dominant role in the technology assimilation and dissemination and in

economic development in Bangladesh as well. Small or Medium Entrepreneur like: an

entity, ideally not a public limited company with total assets at cost excluding land and

building from Tk. 50,000/- to Tk. 1.5 core. This paper attempts to clarify the nature of

SMEs in Bangladesh. The report also contains information on the current position,

problems of SMEs and role pf SMEs in Bangladesh. At the end some recommendations

are provided to remove the problems of SMEs.

Small and Medium Enterprises

According to Industrial policy 2006 SMEs is defined: (a) For manufacturing industries: (i) an enterprise would be treated as small if, in today’s market prices, the replacement cost of plant, machinery, structures, and other parts/components, fixtures, support utility, and associated technical services in between Tk. 50,000 to 1.5 core ( 0.05 million to Tk. 15 million) and workforce not more than 50 ; (ii) an enterprise would be treated as medium if, in today’s market prices, the replacement cost of plant, machinery, building, structures, and other parts/components, fixtures, support utility, and associated technical services in between Tk 1.5 core to Tk 20 core ( tk15 million to Tk. 200 million) and workforce not more than 150 ; From both definitions above, land and building is excluded. (b) For non-manufacturing (such as trading or other services): (i)An enterprise would be treated as small if the fixed capital in between Tk. 50,000 to Tk. 50, 00000(0.05 million to Tk. 5 million) and workforce not more than 25; (ii)An enterprise would be treated as medium if the fixed capital is in between Tk. 50,00000 to Tk. 10,00,00000(5 million to Tk. 100 million) and workforce not more than 50; From both definitions above, land and building is excluded.

Present Scenario of SME in Bangladesh

The present scenario of SMEs in Bangladesh is highlighted below:

Around 6 million SMEs are in operation.

Contribute around 50 percent of industrial outputs.

Employ about 31 million people.

Contribute around 25 percent of total GDP

About 60 to 65 percent SMEs located outside Dhaka and Chittagong metropolitan

city.

Most of the SMEs are labor intensive and low capital based.

Interest rate of SME loan is between 14 to 20 percent

The largest sector in terms of employment generation

Around 75 percent contribution to export earning

Prospects of SMEs in Bangladesh

Un-employment problem is a growing concern all over the world more particularly in

developing countries, and the panacea to the setback mostly lies in massive development

of labour incentive SME sector. SME in many cases can be set up at domestic and

household level contributing to cost cutting. Family members may also participate in the

process. Bangladesh is highly resourceful with so many seasonal fruits and also lots of

agricultural products. Pineapple and mango are best used to produce jam/jelly/juice etc

under SME. Tomato sauce and potato chips are popularly used all over the world. SME is

most suited for processing the items. If we can add more quality to the products and

ensure proper marketing, tremendous demand will be created in domestic and export

market. In RMG industries (knit) circular machines are used for knitting of the items. The

circular machines can also be set at household level to perform job works to feed RMG

industries for ultimate export of T/Polo Shirts etc. This is a subcontracting system where

RMG industries supply yarns to the entrepreneurs having circular machines. The system

has already been introduced in Dhaka and Narayangonj areas with growing demand.

Shoe making by small industries as job works of big shoe companies like BATA is a

glaring example of SME product. BATA supplies raw materials to lots of small factories

at household level in Dhaka city and gets the product (shoes) completed through

subcontract system. Lending in SME sector helps the banks to derive higher spread over

corporate one

Contribution of SMEs to national economy

In Bangladesh, SMEs play a significant role for the development of our economy. SMEs’ contributions are:

1. Creation of employment opportunities: 2. Up gradation of GDP growth rate: 3. Reduction of poverty: 4. Earning foreign currency: 5. Industrial raw-material supplier: 6. Earning govt. revenue: 7. Empowering women: 8. Optimum utilization of latent resources: 9. Development of standard of living: 10. Import substitution: 11. Ensure rural development: 12. Development of potential entrepreneurs

Statistical data about SMEs loan:

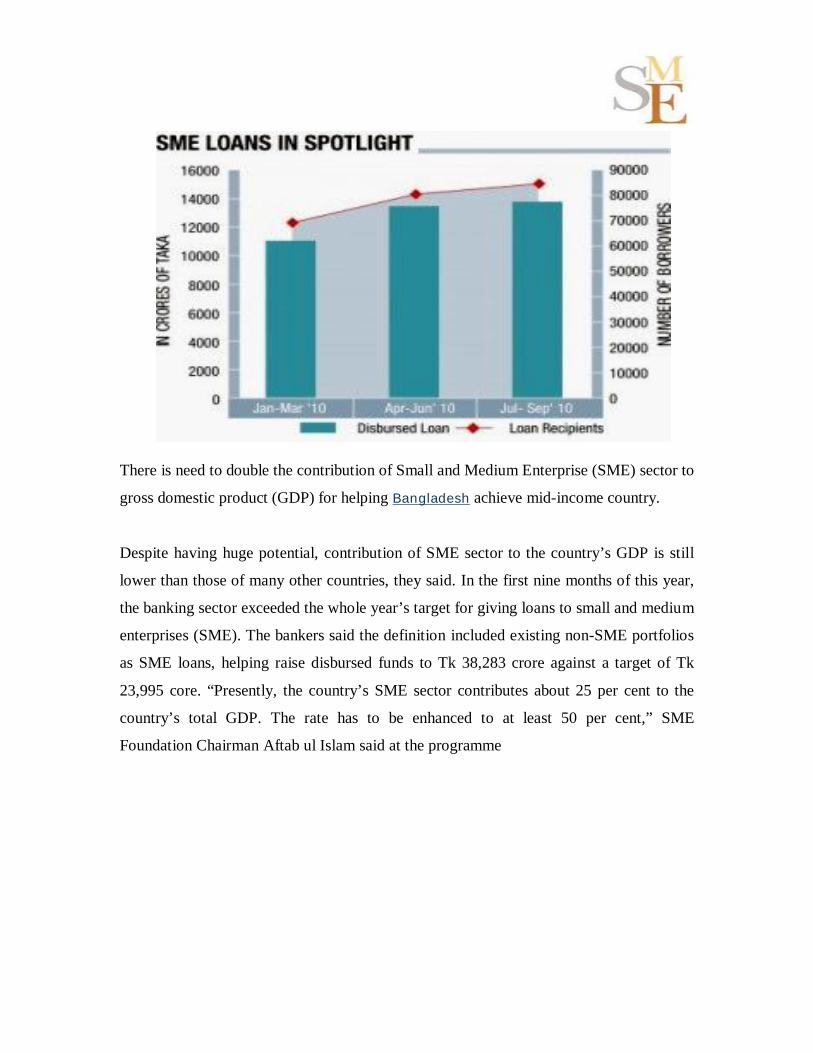

There is need to double the contribution of Small and Medium Enterprise (SME) sector to

gross domestic product (GDP) for helping Bangladesh achieve mid-income country.

Despite having huge potential, contribution of SME sector to the country’s GDP is still

lower than those of many other countries, they said. In the first nine months of this year,

the banking sector exceeded the whole year’s target for giving loans to small and medium

enterprises (SME). The bankers said the definition included existing non-SME portfolios

as SME loans, helping raise disbursed funds to Tk 38,283 crore against a target of Tk

23,995 core. “Presently, the country’s SME sector contributes about 25 per cent to the

country’s total GDP. The rate has to be enhanced to at least 50 per cent,” SME

Foundation Chairman Aftab ul Islam said at the programme

Special Initiatives of the Government

There is a government directive that 5% of a bank’s loan portfolio be set-aside for small

and cottage industry financing Govt. initiatives are:

a) BASIC Bank: (BASIC Bank was established in 1989 to finance small and cottage

industries. It is mentioned in its Memorandum of Articles that at least 50% of its loan-

able fund should be invested in Small Scale Industries (SSI). In 2003, the bank lent Taka

51.29 billion to SSI sector to a number of 418 projects. The Bangladesh Bank has been

providing refinance facility to this bank since 1999. A sum of Taka 250 million was

disbursed to BASIC in FY 2004 under this scheme.

(b) Palli Karma-Sahayak Foundation (PKSF): The Government established PKSF in May

1990 to work as an apex organization for the development of micro finance sector in

Bangladesh. PKSF is distributing micro-credit among the poor through 225 large and

small NGOs. Most of the beneficiaries are women. Government allocated Tk 217 million

in FY 2006-07 for this programme.

(c) Refinance Scheme for Small and Medium Enterprises: To help overcome the financial

Constraints of this sector and induce the banks and other financial institutions to provide

credit facilities to the SME sector, particularly the small entrepreneurs, Bangladesh Bank

introduced a refinance scheme with a special fund. The Government introduced a Tk. 100

million Refinancing Scheme through Bangladesh Bank. The World Bank and the Asian

Development Bank (ADB) will provide US$ 10 million and US$ 30 million respectively

to support this scheme. About 3000 SMEs have received credit under this scheme. For

the development of agro-product processing and software industries, the Government

allocated Tk 100 million to Equity Development Fund in the revised budget of FY 2005-

06. So far, 212 projects have been financed from this Fund.

(d) Credit Distribution Package: It has been announced by the SME Cell that 80% of total

resources available for SME would be allocated specially for small enterprises.

(e) Lead Bank: It has also been decided by the SME Cell that in the short run BASIC

Bank and BRAC Bank will be working together as lead banks and will be responsible for

distribution of the credit and venture capital fund. These two banks will closely work

with the previously mentioned Advisory Panel. Over the medium term, this responsibility

will devolve to the SME Foundation.

(f) SME Foundation: Asian Development Bank has expressed its interest to support the

Government to set up a Small and Medium Enterprises (SME) Foundation as part of its

country assistance strategy. Some other development partners will support the SME

foundation and it can be an apex body for these industries. The SME is one of the

Manilabased lender’s priority sectors and the bank would ready to channel more fund if

the disbursement and utilization of existing funds become faster. Over the medium term

and beyond (a time-frame of 18 or so months from now), the Government shall have to

form an SME Foundation as a pivotal platform for the delivery of all planning,

developmental, financing, awareness-raising, evaluation and advocacy services in the

name of all SME development as a crucially-important element of poverty alleviation.

SME Foundation of Bangladesh

The SME Foundation is an independent center of excellence created and generously

capitalized by the Government of Bangladesh.(SMEF) was formally inaugurated July 17,

2007, by Dr. A. B. Mirza Md. Azizul Islam, Hon’ble Advisor, ministries of Finance,

Commerce, Post & Telecommunications, and Government of the People’s Republic of

Bangladesh at a ceremony held at the Hotel Sonargaon, Dhaka. The mission is the

development Bangladesh’s small and medium enterprises (SMEs) in the present age of

globalization to generate employment and reduce poverty.

Objectives of Bangladesh SME Foundation

To promote, support, strengthen and encourage the growth and development of

SMEs in all productive sectors of the economy, including the service sector,

throughout the country.

To plan, program and finance interventions for delivery by private sector

organizations, including chambers, associations, trade bodies, research and

development institutions including universities, consultancy companies and

professionals to institute SME Awards.

To facilitate SME access to finance by creating and supporting appropriate

strategies and institutions.

To rationalize public sector approaches and support structures for SME

development through systematic capacity assessment and interventions for

organizational development and institutional capacity building.

To create a pro-growth and pro-poor business environment.

To create appropriate incentives, mechanisms and support structures to facilitate

the formation of new enterprises, ensuring enterprise competitiveness, and

promoting sustained growth of existing businesses.

To encourage improvement in SME business environment by gradually becoming

a one-stop facilitation window center for SMEs in getting licenses and approvals

from various agencies and department, and in accessing other required services.

To create a database and provide all needed information about SMEs.

To actively foster greater collaboration, in both design and commercialization,

between industry, civil-society and academia in the interest of harmonious

development of human resources, and delivery systems for SME development.

SME Loan Defined

SME loan is the financial support to small and medium sized enterprises and represents a

major function of the general business finance market. It is the major source of capital for

SMEs. In Bangladesh, Many commercial Banks and NGOs along with some Government

Banks are providing SME loan to the SMEs. Therefore, SME loan is the capital

disbursement to SMEs at a certain interest rate. Capital is supplied through the business

finance market in the form of bank loans and overdrafts; leasing and hire-purchase

arrangements.

Importance of SME loan in the economy of Bangladesh

Bangladesh is a developing country. About 90% of its businesses are small and medium.

So SMES are the main strength of its economy. To boost SMEs, The SME loan plays an

important role. Firstly, it assists to the growth of SMEs. Secondly, it inspires

businessmen to take risk of establishing businesses. The growth of SMEs again has

multiplier impacts on the socio-economic development of our country. For example, it

will increase per capita income and the result of it is high standard of living of the people.

In Addition, it will reduce unemployment problem from our country. Above all, SMEs

will eradicate poverty. On one hand, Due to capital shortage, Sustainable development of

SMEs has not been noticed in our country. On the other hand, the rate of interest of SME

loan is very high. Bangladesh Government are emphasizing on the empowerment of

women. Women involvement with business is one of them. In this case, capital shortage

is a main barrier for the educated women to come to set up businesses. So, the role of

SME loan is a beggar description.

SME and financial institutions

BRAC Bank started its journey in 2001 and in just 8 years proved to be country's fastest

growing bank. Today, the bank has 74 Branches, 60 SME Service Centers, 3 SME/Krishi

Branches, more than 212 ATMs and 424 SME Unit offices across the country. It has

disbursed over BDT 10,000 cores of SME loan and has over 500,000 individual

customers who access online banking facilities.

BRAC SME Products

Brac Bank has various SME schemes which are descried below:

Apurbo:

Apurbo is a combination of term loan and overdraft facility for the entrepreneurs

involved in trading, manufacturing, service, agriculture, non-farm activities, agro-based

industries etc. This product is available for the country wide entrepreneurs throughout

around 137 Branches and 424 SME Unit Offices across the country.

Eligibility

Having business for last 3 years & owner of registered land/property

Anonno rin: is a commercial term loan for small scaled business.

Eligibility

Having business for last 2 years & legal trade license

Any legal Business, Sole proprietorship, partnership, private limited company

Diggoon rin: a loan on deposit for small & medium size business. Eligibility

Having business for last 2 years & legal trade license

Any legal Business, Sole proprietorship, partnership, private limited company

Prothoma Rin: is a term loan for small scaled business operated by women entrepreneur. Eligibility

Having business for last 2 years & legal trade license

Any legal Business, Sole proprietorship, partnership, private limited company

Aroggo rin: is a term loan for small & medium size private Health Services Provider. Eligibility

Having medical business for last 2 years & legal trade license

Any legal Business, Sole proprietorship, partnership, private limited company

Durjoy rin: is a banking facility (combination of term loan and overdraft without any tangible security for working capital purpose and/or fixed asset purchase) targeted to SME customers. Eligibility

Having business for last 2 years & legal trade license

Any legal Business, Sole proprietorship, partnership, private limited company

Trade Plus rin:

is a composite facility for small & medium sized import-oriented businesses to meet their trade finance requirements. Eligibility

Having import-export experience for last 2 years

Any legal Business, Sole proprietorship, partnership, private limited company

Proshar rin: is a term loan for small & medium size manufacturing business. Eligibility

Having business for last 2 years & legal trade license

Any legal Business, Sole proprietorship, partnership, private limited company

two personal guarantors & post dated cheques

Business Equity Loan: is a term loan for commercial purpose. Eligibility

Having business in Dhaka or Chittagong metropolitan areas Having business for last 2 years & legal trade license

Bizness loan: is a term loan facility for all types of business who have healthy bank transactions Eligibility

Having business for last 2 years & legal trade license

two personal guarantors & post dated cheques

Supplier & Distributor Loan: is a loan for various suppliers & distributors to expand their businesses. Eligibility

Hypothecation on present & future assets, two personal guarantors & post dated cheques

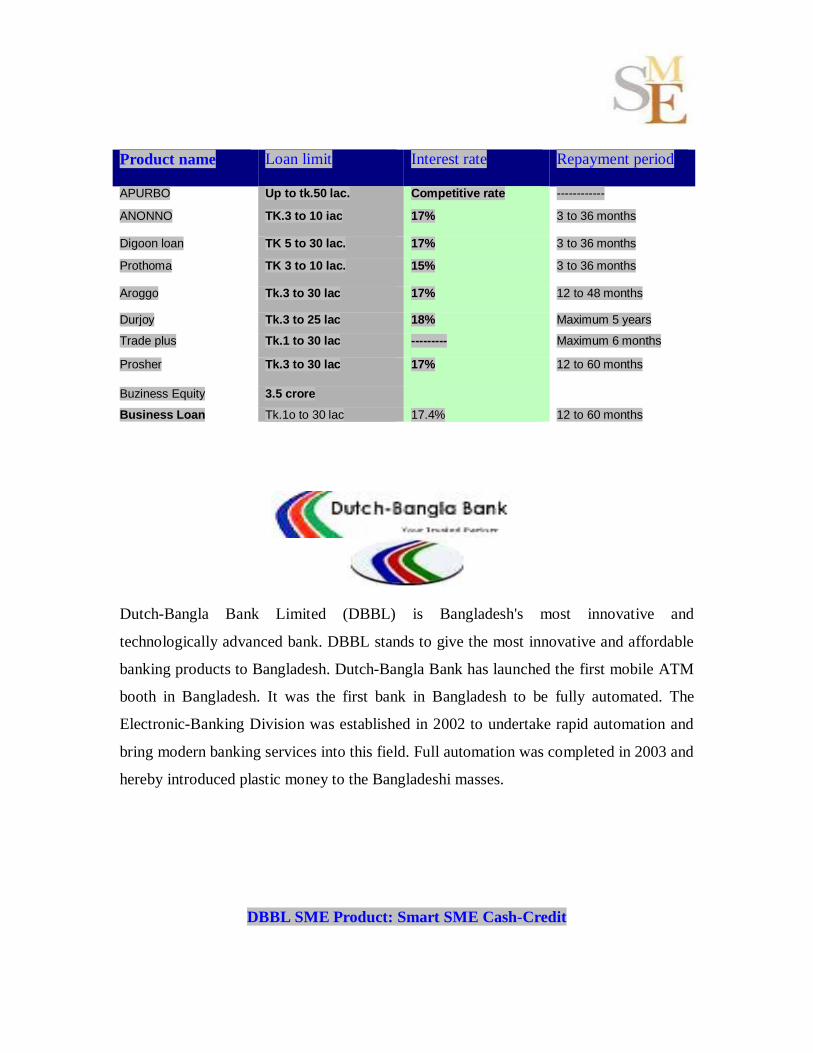

\ Table-1: Brac Bank SME Products

Product name Loan limit Interest rate Repayment period

APURBO Up to tk.50 lac. Competitive rate ------------

ANONNO TK.3 to 10 iac

17% 3 to 36 months

Digoon loan TK 5 to 30 lac. 17% 3 to 36 months

Prothoma TK 3 to 10 lac. 15% 3 to 36 months

Aroggo Tk.3 to 30 lac 17% 12 to 48 months

Durjoy Tk.3 to 25 lac 18% Maximum 5 years

Trade plus Tk.1 to 30 lac --------- Maximum 6 months

Prosher Tk.3 to 30 lac 17% 12 to 60 months

Buziness Equity 3.5 crore

Business Loan Tk.1o to 30 lac 17.4% 12 to 60 months

Dutch-Bangla Bank Limited (DBBL) is Bangladesh's most innovative and

technologically advanced bank. DBBL stands to give the most innovative and affordable

banking products to Bangladesh. Dutch-Bangla Bank has launched the first mobile ATM

booth in Bangladesh. It was the first bank in Bangladesh to be fully automated. The

Electronic-Banking Division was established in 2002 to undertake rapid automation and

bring modern banking services into this field. Full automation was completed in 2003 and

hereby introduced plastic money to the Bangladeshi masses.

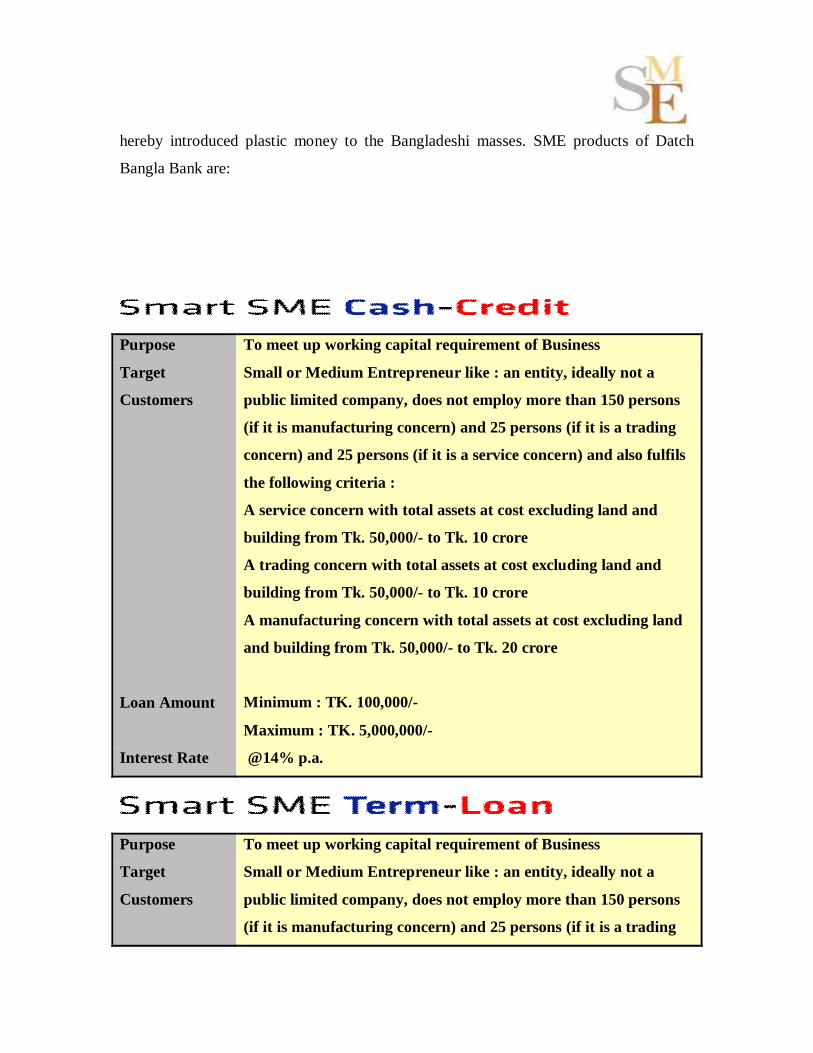

DBBL SME Product: Smart SME Cash-Credit

DBBL SME Product: Smart SME Term Loan

Purpose To meet up working capital requirement of Business

Loan Amount Minimum : TK. 100,000/-

Maximum : TK. 5,000,000/-

Interest Rate @14% p.a

Purpose To meet up working capital requirement of Business

Target

Customers

Small or Medium Entrepreneur like : an entity, ideally not a

public limited company, does not employ more than 150 persons

(if it is manufacturing concern) and 25 persons (if it is a trading

concern) and 25 persons (if it is a service concern) and also fulfils

the following criteria :

A service concern with total assets at cost excluding land and

building from Tk. 50,000/- to Tk. 10 crore

A trading concern with total assets at cost excluding land and

building from Tk. 50,000/- to Tk. 10 crore

A manufacturing concern with total assets at cost excluding land

and building from Tk. 50,000/- to Tk. 20 crore

Loan Amount Minimum : TK. 100,000/-

Maximum : TK. 5,000,000/-

Interest Rate @14% p.a.

DBBL SME Product: Small Shop Financing Scheme

Purpose The purpose of the loan may be Seasonal Financing of inventory

or Trade Receivable or both to the business entity

Nature of

Business

Wholesalers, Manufacturers / Assemblers and Retailers of

machinery, accessories, agriculture items, etc

Loan Amount Maximum TK. 500,000/-

Interest Rate @ 17% p.a. with quarterly rests

Primary

security

Secured by marketable stocks

DBBL SME Product:DBBL Smart Women Entrepreneur

Purpose To meet capital requirement owned by Women Entrepreneur

Loan Amount Minimum : TK. 100,000/-

Maximum : TK. 5,000,000/-

Interest Rate @13% p.a

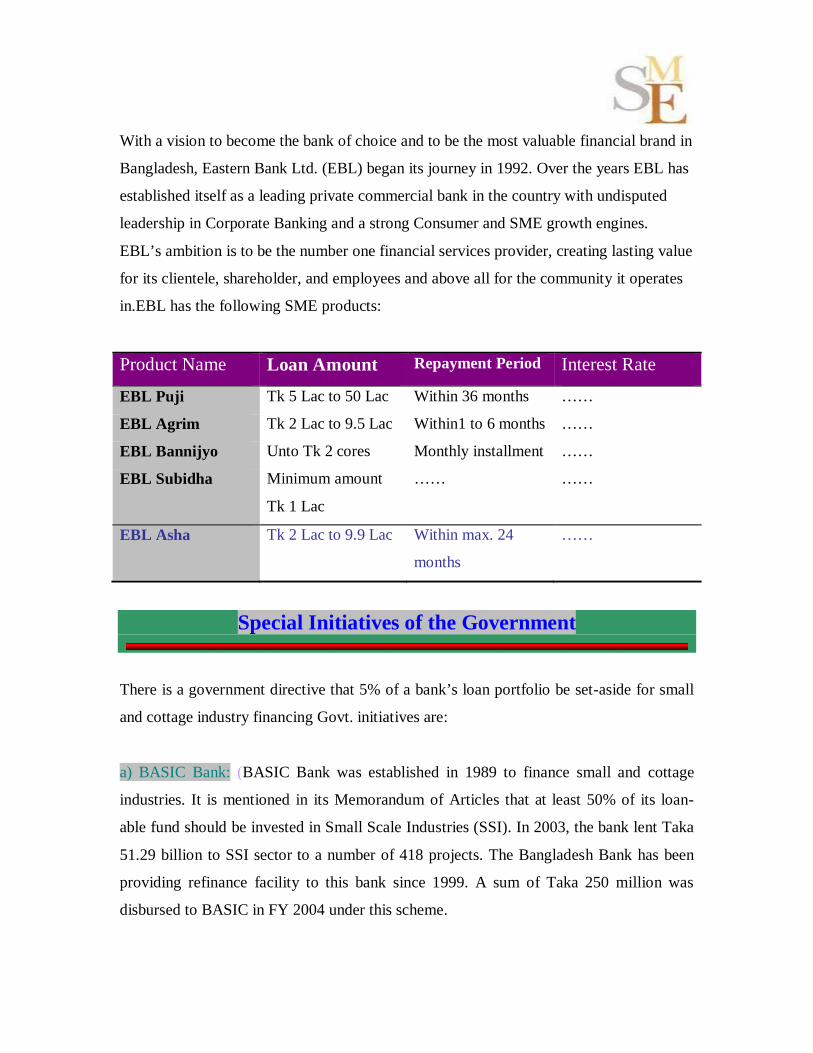

Eastern Bank Ltd

With a vision to become the bank of choice and to be the most valuable financial brand in

Bangladesh, Eastern Bank Ltd. (EBL) began its journey in 1992. Over the years EBL has

established itself as a leading private commercial bank in the country with undisputed

leadership in Corporate Banking and a strong Consumer and SME growth engines.

EBL’s ambition is to be the number one financial services provider, creating lasting value

for its clientele, shareholder, and employees and above all for the community it operates

in.

EBL SME Product: EBL PUJI

Features

Any business purpose loan from Tk. 500,000 to Tk. 5,000,000

To be repaid within maximum 36 months (Next loan is repayable within 60

months)

Collateral security required along with charge on business assets

Loan repayable in equal monthly installment

Any sole proprietorship, partnership, or private limited companies having

minimum 3 years of successful business operation

Monthly cash flow to support the proposed loan installment

EBL SME Product: EBL Agrim

Features

Any legal business purpose, loan facility minimum BDT 200,000 – maximum BDT

950,000 No collateral security required

Loan tenure 1 month to 6 months

Single shot payment at maturity but interest will be realized on monthly basis

Partial payment and early payment allowed- no additional fee required

Eligibility

Business cash flow to support the proposed loan in one shot

Necessary documents of business required

Bank account in the name of the enterprise or entrepreneurs

Personal guarantee required

EBL SME Product:EBL Bannijyo

Features

Credit facility up to BDT 20,000,000 to any legitimate import business

Nil margin LC facility

No requirement of land/building mortgage

Post import facility up to 6 months

30%-40% of total limit in the form of FD as collateral required

Over Draft facility to support day to day general expenses

Eligibility Any legitimate business with three years of operation and at least one year

experience in import business

Necessary import related documents

Business cash flow to support repayment

EBL SME Product: EBL Subidha

Features Minimum account opening amount BDT 100,000

Minimum deposit requirement for interest earning BDT 100,000

Daily interest bearing and half-yearly interest paying account

Free Monthly Statement for the Current Account and Free Half-yearly Statement

for the Shubidha Account

No Ledger Fee if the Shubidha Account average balance is BDT 100,000 or more;

incase of amount less than that a semi-annual ledger fee of BDT 300 will be

applicable

24-hour money withdrawal facility at any VISA ATM

No Intercity Transaction Fee Up to BDT 10,00,000

Any EBL Branch Banking Facility

Internet Banking facility

Evening banking facility at selected EBL branches - you can deposit and

withdraw money from 6 p.m. to 8 p.m. at these branches

Eligibility

Any legitimate business entity - sole proprietorship, partnership or private limited

company, with valid trade license and other documents as per Bangladesh Bank

requirements, can open EBL Shubidha.

EBL SME Product: EBL Asha

Features Any business purpose loan from Tk. 200,000 to Tk. 990,000

To be repaid within maximum 24 months (Next loan is repayable within 60

months)

No requirements for collateral security

Loan repayable in equal monthly installment

Eligibility

Any sole proprietorship, or private limited companies having minimum 1.5 years

of successful business operation

Monthly cash flow to support the proposed loan installment

2 personal guarantee

EBL SME Product: EBL Uddog

Features Any legal business purpose, loan minimum BDT 6,00,000 – maximum BDT

50,00,000

Without land/building mortgage

To be repaid within maximum 60 months.

Loan repayable in monthly installments

50% of the loan amount in the form of fixed deposit is needed.

Eligibility Any successful enterprise minimum one and a half years in same or relevant

business can apply for loan.

Business income to support the proposed loan installment

Necessary documents of business are required

Bank account in the name of enterprise or the entrepreneurs.

EBL SME Product: EBL Mukti

Features Credit facility up to BDT 300,000 (three lac) in any legitimate business

No requirement of land/building mortgage

Yearly interest rate is 10%, which is the lowest in the country

Repayable in 18 months

Facility is only for Women Entrepreneurs

Eligibility Any legitimate business with at least two years of operation Business Cash Flow to support repayment

Table-2: Eastern Bank SME Products

Product Name Loan Amount Repayment Period Interest Rate

EBL Puji Tk 5 Lac to 50 Lac Within 36 months ……

EBL Agrim Tk 2 Lac to 9.5 Lac Within1 to 6 months ……

EBL Bannijyo Unto Tk 2 cores Monthly installment ……

EBL Subidha Minimum amount

Tk 1 Lac

…… ……

EBL Asha

Tk 2 Lac to 9.9 Lac Within max. 24

months

……

Problems in Providing SME Loan

a) Delay in repayment of loan: Executives of various banks opined that many

borrowers show their inability to repay the loan amount in time. They also told that borrowers have lack of commitment in the repayment of loan.

b) Trustworthiness of loan borrowers: Since the borrowers cannot show

sufficient security or personal guarantor in getting loan, so the bank can not enable to provide loan in spite of their willingness.

c) Lack of Entrepreneurial Knowledge: It is the precondition of banks that

every borrower must have business knowledge to get loan .But most of the borrowers don’t know how to operate businesses properly. Therefore banks become unable to sanction loan.

d) Inability to submit complete business plan: Borrowers require submitting

business plan in getting SME loan. But most of the time, they cannot submit business plan or if they submit, most of the cases it is incomplete.

e) . Improper preparation of financial statement: Financial statements contain

ins and outs of business that show the business performance for a certain period of time. Executives informed that borrowers cannot prepare these statements properly.

f) Lack of available fund: Many executives of banks argue that banks cannot

supply much SME loans in spite of huge demand due to capital shortage. So some banks cannot keep pace with the other banks in the race of heavy competition.

g) Lack of govt. support: Although many supports from govt. are available but that are not sufficient .In this case Govt. can sanction more fund to various commercial banks, so that they can provide required loan amount to their borrowers.

h) .Unavailability of collateral free bank loan: Maximum SME initiatives

come from single brain without any institutional orientation. They do not afford providing a collateral or guarantor to produce before bank to get a small loan. Due to such problems banks are not interested to give loan to borrowers.

i) High Bank interest rate: As banks have to incur huge cost in terms of

employees compensations, administrative costs etc., the rate of interest of SME loan is high .So borrowers cannot afford of this high interest rate which eventually hampers in SME loan disbursement

j)

Recommendations

1) Proper education and knowledge: Various commercial banks which are

providing SME loan can also give some consultancy support to the loan borrowers in

preparing their financial statements and continuation of their business successfully.

2) Guidance to prepare business plan: Many loan borrower usually prepare their

business plan appropriately duo to lack of proper knowledge in this case banks can guide

them in preparing the business plan.

3) Reduction of interest rate: Bank should reduce interest rate of SME loan to

encourage entrepreneurs to help set up new business and expand existing enterprises.

4) Increasing amount of SME Loan: Banks should allocate more SME fund to

assist entrepreneurs getting required loan to run their businesses and play significant role

to reduce unemployment and poverty.

5) Increase Govt. support: As we mentioned earlier that SME is an important sector

in the development of economy. So govt. can take initiatives to train new entrepreneurs.

Besides, Govt. can sanction available fund to commercial banks to distribute SME loan.

Finally it can give some tax exemption on SME loan interest to motivate bankers to raise

their loan facility.

Conclusion

SMEs, therefore, play an important role in the economic development of developing

countries like Bangladesh. But the SMEs in of our country Faces many problem.

Although Many Private Banks, NGOs and Public Banks are working to the development

of SMEs, Lack of coordination among these organizations are highly noticed. That is

why; Sustainable development of SME sectors has not been achieved. Some managers of

different banking institutions have mentioned a set of problems related to the

advancement of SMEs in Bangladesh. Considering the problems, we suggest some

recommendations in this report that can be followed by Govt. and Non-Government

organizations to the up gradation of these boosting sectors.

References:

SME FAIR-2011 at Engineering Institute Bangladesh Bureau of Statistics Economic Survey-2003 Bangladesh Bank at New market Company visits to Commercial Banks www.smef.org.bd http://www.moind.gov.bd http://www.financialinfobd.com http://www.bracbank.com/

www.dutchbanglabank.com https://www.easternbank.com http://en.wikipedia.org/wiki/Small_and_medium_enterprises

SME and financial institutions

BRAC Bank started its journey in 2001 and in just 8 years proved to be country's fastest

growing bank. Today, the bank has 74 Branches, 60 SME Service Centers, 3 SME/Krishi

Branches, more than 212 ATMs and 424 SME Unit offices across the country. It has

disbursed over BDT 10,000 cores of SME loan and has over 500,000 individual

customers who access online banking facilities. Brac Bank ltd. has the following SME

products:

Apurbo Rin: is a loan facility for Small & Medium Entrepreneurs. Apurbo is a

combination of term loan and overdraft facility for the entrepreneurs involved in trading,

manufacturing, service, agriculture, non-farm activities, agro-based industries etc.

Anonno rin: is a term loan for small scaled business. Diggoon rin: a loan on deposit for small & medium size business. Prothoma Rin: is a term loan for small scaled business operated by women entrepreneur. Aroggo rin: is a term loan for small & medium size private Health Services Provider. Durjoy rin: is a banking facility (combination of term loan and overdraft without any tangible security for working capital purpose and/or fixed asset purchase) targeted to SME customers. Trade Plus rin:is a composite facility for small & medium sized import-oriented businesses to meet their trade finance requirements.

Proshar rin: is a term loan for small & medium size manufacturing business. Business Equity Loan: is a term loan for commercial purpose Bizness loan: is a term loan facility for all types of business who have healthy bank transactions Supplier & Distributor Loan: is a loan for various suppliers & distributors to expand their businesses Product name Loan limit Interest rate Repayment period

APURBO Up to tk.50 lac. Competitive rate ------------

ANONNO TK.3 to 10 iac

17% 3 to 36 months

Digoon loan TK 5 to 30 lac. 17% 3 to 36 months

Prothoma TK 3 to 10 lac. 15% 3 to 36 months

Aroggo Tk.3 to 30 lac 17% 12 to 48 months

Durjoy Tk.3 to 25 lac 18% Maximum 5 years

Trade plus Tk.1 to 30 lac --------- Maximum 6 months

Prosher Tk.3 to 30 lac 17% 12 to 60 months

Buziness Equity 3.5 crore

Business Loan Tk.1o to 30 lac 17.4% 12 to 60 months Table-1: Brac Bank SME Products

Dutch-Bangla Bank Limited (DBBL) is Bangladesh's most innovative and

technologically advanced bank. DBBL stands to give the most innovative and affordable

banking products to Bangladesh. Dutch-Bangla Bank has launched the first mobile ATM

booth in Bangladesh. It was the first bank in Bangladesh to be fully automated. The

Electronic-Banking Division was established in 2002 to undertake rapid automation and

bring modern banking services into this field. Full automation was completed in 2003 and

hereby introduced plastic money to the Bangladeshi masses. SME products of Datch

Bangla Bank are:

Purpose To meet up working capital requirement of Business

Target

Customers

Small or Medium Entrepreneur like : an entity, ideally not a

public limited company, does not employ more than 150 persons

(if it is manufacturing concern) and 25 persons (if it is a trading

concern) and 25 persons (if it is a service concern) and also fulfils

the following criteria :

A service concern with total assets at cost excluding land and

building from Tk. 50,000/- to Tk. 10 crore

A trading concern with total assets at cost excluding land and

building from Tk. 50,000/- to Tk. 10 crore

A manufacturing concern with total assets at cost excluding land

and building from Tk. 50,000/- to Tk. 20 crore

Loan Amount Minimum : TK. 100,000/-

Maximum : TK. 5,000,000/-

Interest Rate @14% p.a.

Purpose To meet up working capital requirement of Business

Target

Customers

Small or Medium Entrepreneur like : an entity, ideally not a

public limited company, does not employ more than 150 persons

(if it is manufacturing concern) and 25 persons (if it is a trading

concern) and 25 persons (if it is a service concern) and also fulfils

the following criteria :

A service concern with total assets at cost excluding land and

building from Tk. 50,000/- to Tk. 10 crore

A trading concern with total assets at cost excluding land and

building from Tk. 50,000/- to Tk. 10 crore

A manufacturing concern with total assets at cost excluding land

and building from Tk. 50,000/- to Tk. 20 crore

Loan Amount Minimum : TK. 100,000/-

Maximum : TK. 5,000,000/-

Interest Rate ( @14% p.a

Purpose The purpose of the loan may be Seasonal Financing of inventory

or Trade Receivable or both to the business entity

Nature of

Business

Wholesalers, Manufacturers / Assemblers and Retailers of

machinery, accessories, agriculture items, etc

Loan Amount Maximum TK. 500,000/-

Interest Rate @ 17% p.a. with quarterly rests

Primary

security

Secured by marketable stocks

Eastern Bank Ltd

With a vision to become the bank of choice and to be the most valuable financial brand in

Bangladesh, Eastern Bank Ltd. (EBL) began its journey in 1992. Over the years EBL has

established itself as a leading private commercial bank in the country with undisputed

leadership in Corporate Banking and a strong Consumer and SME growth engines.

EBL’s ambition is to be the number one financial services provider, creating lasting value

for its clientele, shareholder, and employees and above all for the community it operates

in.EBL has the following SME products:

Product Name Loan Amount Repayment Period Interest Rate

EBL Puji Tk 5 Lac to 50 Lac Within 36 months ……

EBL Agrim Tk 2 Lac to 9.5 Lac Within1 to 6 months ……

EBL Bannijyo Unto Tk 2 cores Monthly installment ……

EBL Subidha Minimum amount

Tk 1 Lac

…… ……

EBL Asha

Tk 2 Lac to 9.9 Lac Within max. 24

months

……

Special Initiatives of the Government

There is a government directive that 5% of a bank’s loan portfolio be set-aside for small

and cottage industry financing Govt. initiatives are:

a) BASIC Bank: (BASIC Bank was established in 1989 to finance small and cottage

industries. It is mentioned in its Memorandum of Articles that at least 50% of its loan-

able fund should be invested in Small Scale Industries (SSI). In 2003, the bank lent Taka

51.29 billion to SSI sector to a number of 418 projects. The Bangladesh Bank has been

providing refinance facility to this bank since 1999. A sum of Taka 250 million was

disbursed to BASIC in FY 2004 under this scheme.

(b) Palli Karma-Sahayak Foundation (PKSF): The Government established PKSF in May

1990 to work as an apex organization for the development of micro finance sector in

Bangladesh. PKSF is distributing micro-credit among the poor through 225 large and

small NGOs. Most of the beneficiaries are women. Government allocated Tk 217 million

in FY 2006-07 for this programme.

(c) Refinance Scheme for Small and Medium Enterprises: To help overcome the financial

Constraints of this sector and induce the banks and other financial institutions to provide

credit facilities to the SME sector, particularly the small entrepreneurs, Bangladesh Bank

introduced a refinance scheme with a special fund. The Government introduced a Tk. 100

million Refinancing Scheme through Bangladesh Bank. The World Bank and the Asian

Development Bank (ADB) will provide US$ 10 million and US$ 30 million respectively

to support this scheme. About 3000 SMEs have received credit under this scheme. For

the development of agro-product processing and software industries, the Government

allocated Tk 100 million to Equity Development Fund in the revised budget of FY 2005-

06. So far, 212 projects have been financed from this Fund.

(d) Credit Distribution Package: It has been announced by the SME Cell that 80% of total

resources available for SME would be allocated specially for small enterprises.

(e) Lead Bank: It has also been decided by the SME Cell that in the short run BASIC

Bank and BRAC Bank will be working together as lead banks and will be responsible for

distribution of the credit and venture capital fund. These two banks will closely work

with the previously mentioned Advisory Panel. Over the medium term, this responsibility

will devolve to the SME Foundation.

(f) SME Foundation: Asian Development Bank has expressed its interest to support the

Government to set up a Small and Medium Enterprises (SME) Foundation as part of its

country assistance strategy. Some other development partners will support the SME

foundation and it can be an apex body for these industries. The SME is one of the

Manilabased lender’s priority sectors and the bank would ready to channel more fund if

the disbursement and utilization of existing funds become faster. Over the medium term

and beyond (a time-frame of 18 or so months from now), the Government shall have to

form an SME Foundation as a pivotal platform for the delivery of all planning,

developmental, financing, awareness-raising, evaluation and advocacy services in the

name of all SME development as a crucially-important element of poverty alleviation.

Contribution of SMEs to national economy

In Bangladesh, SMEs play a significant role for the development of our economy. SMEs’ contributions are:

13. Creation of employment opportunities: 14. Up gradation of GDP growth rate: 15. Reduction of poverty: 16. Earning foreign currency: 17. Industrial raw-material supplier: 18. Earning govt. revenue: 19. Empowering women: 20. Optimum utilization of latent resources: 21. Development of standard of living: 22. Import substitution: 23. Ensure rural development: 24. Development of potential entrepreneurs Statistical data about SMEs loan:

There is need to double the contribution of Small and Medium Enterprise (SME) sector to

gross domestic product (GDP) for helping Bangladesh achieve mid-income country.

Despite having huge potential, contribution of SME sector to the country’s GDP is still

lower than those of many other countries, they said. In the first nine months of this year,

the banking sector exceeded the whole year’s target for giving loans to small and medium

enterprises (SME). The bankers said the definition included existing non-SME portfolios

as SME loans, helping raise disbursed funds to Tk 38,283 crore against a target of Tk

23,995 core. “Presently, the country’s SME sector contributes about 25 per cent to the

country’s total GDP. The rate has to be enhanced to at least 50 per cent,” SME

Foundation Chairman Aftab ul Islam said at the programme

Challenges or problems faced by SME

01.Poor Infrastructure and utility supply: There is a tendency of urbanized

industrialization in Bangladesh. Everything is Dhaka based to create one more hours of

traffic jam and pollute the Boriganga once again. This is because infrastructure facility is

so measurable in any rural destination of Bangladesh. Utility mainly electricity and gas

supply is impossible to get connected in any rural even sub urban areas. Existing SMEs

are suffering badly due to load shedding of electricity. Production oriented SMEs are

incurring losses by paying idle workers wages during long load shedding period. In one

particular period of each year gas pressure remains so little that it makes no sense. So

poor infrastructure and disrupted utility supply is the major barrier for our SMEs.

02.Unavailability of collateral free bank loan Maximum SME initiatives come from

single brain without any institutional orientation. They do not afford providing a

collateral or guarantor to produce before bank to get a small loan. They are only dream

sellers sometime with excellent ideas. Financing those ideas to bring the dreams into

reality should be there. Government has to take some risk of distributing collateral free

bank loan to the SME entrepreneurs is essential here. I am fully confident that thousands

of SME defaulters can not be equal to a single bank defaulter in large industry of

Bangladesh.

03. Limited access to information People have ideas to produce useful items. But

information is not available on demand of these products. So they can not place the

product into a demand full market in right time. Then loss incurs and SMEs suffers badly.

In such case government has to take initiative so that SME information goes to general

peoples reach. Only one SMEWP is not sufficient to distribute SME information to the

whole nation. Because how many SME entrepreneurs know to browse internet is a big

question.

04. Traditional Technology SME owners generally use local technology to produce goods

but these are not productive enough to fulfill market demand, or not producing quality /

beautiful products to compete with the low cost Indian & Chinese products freely

available in our local market. As a result our SME entrepreneurs are losing their

livelihood due to poor technical know-how.

05. Low productivity of labor Bangladeshi SME sectors are employing about 82% of

workforce and producing around 50% of industrial output. This statistics proves that our

labors are low productive. It may be for their inefficiency, may be for poor technology or

what ever it is.

06. Lack of entrepreneurship development program In Bangladesh there is no agency

even not a single educational institution called Entrepreneurship Development Institute,

basically to create entrepreneurs there is no hard and fast faculty but for effective

entrepreneurship generation entrepreneurship education. But in Malaysia there is a

Ministry called ‘Ministry of Entrepreneur and Cooperative Development’. They have

different divisions and wings for operating training, motivation, innovative support for

entrepreneurship development.

07. Lack of sector specific skilled manpower There is not educational institute or

technical college in Bangladesh equip with modern technologies of our fast growing

industrial sector for training up people to employ in that sector. For example there is not

plastic and rubber faculty in Bangladesh though it's a growing sector with tremendous

export potentials. Scenario is same in other promising sectors as well.

08. Complicated bureaucratic procedures: To start a manufacturing plant we need a series

of license, registrations and clearances. For example to start an SME we need-

a. Trade license issued by the local government office (UP Chairman, City Corporation

office)

b. Trademark registration register by the Office of Patent, Design and

Trademark Register under the Ministry of Industry

c. TIN Number from NBR or Income tax Office under ministry of Finance,

d. VAT registration from the same authority,

e. Membership of any trade body (district chamber or sect oral association),

f. Import registration certificate from CCI & E under ministry of commerce

g. Export Registration Certificate from the previous office.

h. Environment Clearance from the ministry of environment

i. Fire clearance from the fire Bridget and many more.

Completing all these formality is not so easy and every desk needs bribe to be passing out

with your file. This time consuming and corruption promoting system should be making

easier. Any SME owners can start his / her business without any prior permission and

concern local agency will go to him collect government prescribed revenue and provide

his registration or clearance. Thus SME entrepreneurs can get relief from harassment and

real SME promotion will take place.

09. Lack of marketing knowledge: One of the major problems of our SMEs is not to

know the market. Where and when his / her product should be sold? They do not know

how to get export market access. Even how their products have to be promoted for

consumer's attraction with low cost promotion is not known to them.

Government can take the lead to promote our SME products in home and abroad. All our

missions abroad should have one SME product display and sales center for introducing

our SME products in abroad. All our international airports, tourist spots and five star

hotels should have one SME product display and sales center for the same. Marketing

training can be given to the small entrepreneurs to educate them in marketing

techniques.

10. High Bank interest rate: To make profit with 13% bank loan, employing people,

paying rents, and other utility charges SMEs have to do sales products with a 50% plus

rate of their manufacturing cost. But with 5 - 7% bank interest rate our competitors in

India or China will not take the market vacant for Bangladesh SMEs. To sustain in a

competitive global market we have no option but to produce quality goods in a cheap

rate. But by paying double digit interest it is not possible. As a result to remain us

competitive we have to reduce bank interest rate up to single digit. Especially for the

SMEs the interest rate should be -

- Investment amount of TK. 50 thousand - 5 lac should be completely collateral free

and the interest rate would be not more than 3 per cent.

- Investment amount of TK. 5.5 lac -50 lac with collateral or a guarantor's

recommendation with less than 5 per cent interest rate.

- Investment amount of Tk. 51 lac - 10 crore and above with all shorts of collaterals

with less than 7 per cent interest rate.

11. Lack of government support to search export market: Our poor SME owners are not

capable to search their products market in abroad.

Government has to take the lead here through SME Foundation to search new export

market and facilitating access to that markets. If primarily government plays the match

makers role then individual or collective platform will be raised to continue the effort to

export into those markets.

12. High competition due to liberalization: our SME products have to face extensive

competition due to the stronger flow of free market economy and globalization of trade in

our native market as well.

13. Lack of testing facility: Day by day private standards of the importing countries are

becoming toughest. To get access to any western market we must have to comply with

WTO SPS requirements and other international standards. In Bangladesh we are till not

having facility to test many sectoral products. So upgrading our testing laboratories

according to current need is important. BSTI should take lead to ensure all accreditations

and testing facilities to all promising export oriented sectors in this regard. Obviously

BSTI deserves strong financial support to execute this program. More standard service

providing firms should be there from private sectors as well to provide ISO, HAACP,

Credit rating and other international standard certification in Bangladesh so that our SME

products get international recognition from the standard view point.

15. Absence of skilled channel of distribution to ensure fare price of growers: If we look

into the cottage industry in rural Bangladesh we are producing many diversified products

in different sectors. But producers are not getting the deserving price for these due to lack

of market orientation. A strong market platform can help producers to deserve price and

inspire to produce more. Gramen Check took an initiative to marketing hand loom

products, Arong, Agura are marketing some fashion products but nation wide or export

oriented initiative is lagging behind. SME Foundation can enlarge there mandate to

establish such an SME Channel of Distribution for the shack of the SME sector.

16. Lack of veterinary / animal health care facility: SME is not limited with only

industrial products; it includes farming, hatching and growing as well. But veterinary

health care or plant healthcare facility is rarely available in Bangladesh. Government

should take active initiative to facilitate such services through livestock and poultry

wings of the government. Thus agro farming can be booted up at the same time country

nutrition problem can be solved.

17. Absence of SME support centers: Till now a few consulting firms are providing

consultation services but with high charges. We should have more SME support centers

to give advice to the potential entrepreneurs to prepare project proposal, formulating

marketing strategy, designing products, upgrading products quality for the SMEs.

18. Absence of an individual SME Policy: There is an SME policy strategy 2005. But

many of its articles become obsolete today. So drafting and implementing an individual

SME policy based on current need is very much essential today. It should be conform to

our import policy and export policy for greater benefit out of it.

Prospects of SMEs in Bangladesh

Un-employment problem is a growing concern all over the world more particularly in

developing countries, and the panacea to the setback mostly lies in massive development

of labour incentive SME sector. SME in many cases can be set up at domestic and

household level contributing to cost cutting. Family members may also participate in the

process. Bangladesh is highly resourceful with so many seasonal fruits and also lots of

agricultural products. Pineapple and mango are best used to produce jam/jelly/juice etc

under SME. Tomato sauce and potato chips are popularly used all over the world. SME is

most suited for processing the items. If we can add more quality to the products and

ensure proper marketing, tremendous demand will be created in domestic and export

market. In RMG industries (knit) circular machines are used for knitting of the items. The

circular machines can also be set at household level to perform job works to feed RMG

industries for ultimate export of T/Polo Shirts etc. This is a subcontracting system where

RMG industries supply yarns to the entrepreneurs having circular machines. The system

has already been introduced in Dhaka and Narayangonj areas with growing demand.

Shoe making by small industries as job works of big shoe companies like BATA is a

glaring example of SME product. BATA supplies raw materials to lots of small factories

at household level in Dhaka city and gets the product (shoes) completed through

subcontract system. Lending in SME sector helps the banks to derive higher spread over

corporate one

Recommendations

(1) Uniform Definition of SMEs: There should be a consensus on developing a uniform

definition of each category of SMEs with generic classification around the country. It

should be given standard industrial code (SIC). Without uniform definition, formulation

policy and its implementation are not possible.

(2) Seed Money, Leasing, Venture Capital and Investment Funding: There is a need for

improving different aspects of financial services of SMEs, such as seed money, leasing,

venture capital and investment funding. There is a lack of long-term loans; interest rates

are high, Guarantee/Security issues, exchange risks etc. All these limit the development

of SMEs. Finance, both short and long term, should be provided at market cost of capital.

Fund should be made available through encouragement for setting up ‘Venture Capital’

organization in Bangladesh. The concept of venture capital (VC) has successfully

operating in the USA, EU countries, and Canada.

(3) Establishment of Small Business Investment and Lending Corporation (SBILC): We

should start with ‘something effective’ for industrial development in general and the

SMEs sector in particular. Such a step, for example, could be the establishment of a

separate Corporate body. That means a separate financing institution could be developed,

with joint ownership of the public and private sector. To make the proposed initiative

effective in achieving its goals, government may set up a Small Business Investment and

Lending Corporation (SBILC). The SBILC can be formed under Small Business

(4) Internal methods of financing SMEs: Small business owners should not rely solely on

financial institutions and government agencies for capital. Instead, the business itself has

the capacity to generate capital. This type of financing, called bootstrap financing, is

available to virtually every small business and encompasses factoring, leasing rather than

purchasing equipment, using credit cards, and managing the business frugally.

Another source of financing could be raising fund from share market by flotation of IPO

by SME under ‘Group IPO Scheme (GIPS)’. In the case of GIPS, a group of SME would

utilize their assets for issuance of public shares to be managed by an independent agency.

(5) Seeking International Financing: Various international donor agency/bank extends

financing to SMEs through National Development Financing Institutions (NDFIs). It is

found that they are not explored properly. The procedure of those donor agencies/banks

for loan facilities to SMEs through NDFIs may be reviewed and term and conditions may

be examined in order to make international financing more accessible to SMEs in the

country.

(6) The Role of Donors, particularly IDB: Donors, particularly IDB, may come forward

to assist the financial institutions in alleviating the constraints faced by SMEs, primarily

the access to credit and capacity building. Funding support in the form of grant may be

sought from IDB for Technical Assistance and Consulting Services for products and skill

development for the SMEs. In this area, BSCIC may also be involved for providing

promotional and technical support services to the SMEs with funding support of IDB.

(7) Assistance for SMEs from Board of Investments and Export Development Centres:

Public sector agencies like Board of Investments and Export Development Centres can

also provide useful information to SMEs. They can provide necessary information about

trade fairs in member countries as well as training in organization of exhibitions. They

can identify foreign buyers and assist local SMEs in establishing contacts with them.

Information on changing demand conditions in various international markets can be pro

vided and advisory services on exploring trade opportunities can be provided to

prospective exporters.

(9) BSCIC to be reorganized: Most entrepreneurs and businessmen express their

dissatisfaction about BSCIC. BSCIC fails to provide needed services to the small

industries due to manifold reasons; primarily due to its unorganized management. BSCIC

has to be reorganized so that enacted policy for SMEs can be implemented to help grow

small industries in the country in a better manner. Alternatively, a separate organization

such as Small and Medium Enterprise Development Authority (SMEDA) may be

established to act as a one-stop consultancy Agency to: (a) act as a body for facilitating

policy making for SMEs, (b) provide and facilitate support services for SMEs, (c) act as a

resource base for the SMEs, and (d) represent SMEs on domestic and international

forums. The authority may be state supported, private or jointly supported organization.

(10)Developing Institutional Network through Public-Private Partnership: The design of

most government agencies appears to be overly bureaucratic and unsuitable for

effectively supporting SMEs in Bangladesh. As such, re-organization of the design of

these agencies has for long been overdue. Public-private sector partnership, by

redesigning the existing public agencies, could be developed, developing appropriate

institutional network. The objective behind this would be to utilize the strengths of public

and private agencies, while neutralizing the limitations, if any, inherent in their existing

organizational design.

(11) Establishment of R&D Institute for Enterprise and Entrepreneurship Development,

Training and Research Institute: In a country like Bangladesh, where entrepreneurial

initiative is rare and shy, a separate institute for enterprise and entrepreneurship

development, training and research should be developed. To make it a ‘centre of

excellence’ in SMEs development, it should be designed, involving educational

institutions, business associations, relevant government bodies, private research agencies,

and individual consultants having experience in SMEs development.

(12) Implementation and Monitoring of Policy Measures for SMEs: Only policy

prescription is not the end, if it is not implemented through different measures timely and

properly.

Conclusion

SMEs, therefore, play an important role in the economic development of developing

countries like Bangladesh. But the SMEs in of our country Faces many problem.

Although Many Private Banks, NGOs and Public Banks are working to the development

of SMEs, Lack of coordination among these organizations are highly noticed. That is

why; Sustainable development of SME sectors has not been achieved. Some managers of

different banking institutions have mentioned a set of problems related to the

advancement of SMEs in Bangladesh. Considering the problems, we suggest some

recommendations in this report that can be followed by Govt. and Non-Government

organizations to the up gradation of these boosting sectors.

References: SME FAIR-2011 at Engineering Institute Bangladesh Bureau of Statistics Economic Survey-2003 Bangladesh Bank at New market Company visits to Commercial Banks www.smef.org.bd http://www.moind.gov.bd http://www.financialinfobd.com http://www.bracbank.com/ www.dutchbanglabank.com https://www.easternbank.com http://en.wikipedia.org/wiki/Small_and_medium_enterprises

![… · ltd/ Islami Bank Bangladesh I-tci/Jamuna Bank Lid/ Trust Bank Ltd/AB Bank Ltd/ Dhaka Bank Ltd/ Pubali Bank Ltd/Basic Bank I-Ic]/South East, Bank Ltd/ Dutch Bangla Bank Ltd](https://img.pdfslide.us/doc/110x75/5eaae1285617c3695347ef52/-ltd-islami-bank-bangladesh-i-tcijamuna-bank-lid-trust-bank-ltdab-bank-ltd.jpg)