Embed Size (px)

Citation preview

Innovation in Retail PaymentsActivities of the CPSS Working Group on InnovationDirk Schrade

The views and opinions expressed in this presentation are those of the speaker and do not necessarily reflect the position of the CPSS or Deutsche Bundesbank.

CPSS – World Bank Retail Forum

First impression: Retail payments – a classical business

2

Dirk SchradeSource: EHI 2011

Cash59%

Debit card32%

Credit card5%

Others4%

POS-Payments in Germany 2009

1950

Ancient chariot

600 B. C.

TV

Videorecorder

Compact disc

Internet

DVD

MP3-Player

Year

1928

1976

1981

1989

1996

1996

1990

27-28 February 2012, Miami

CPSS – World Bank Retail Forum

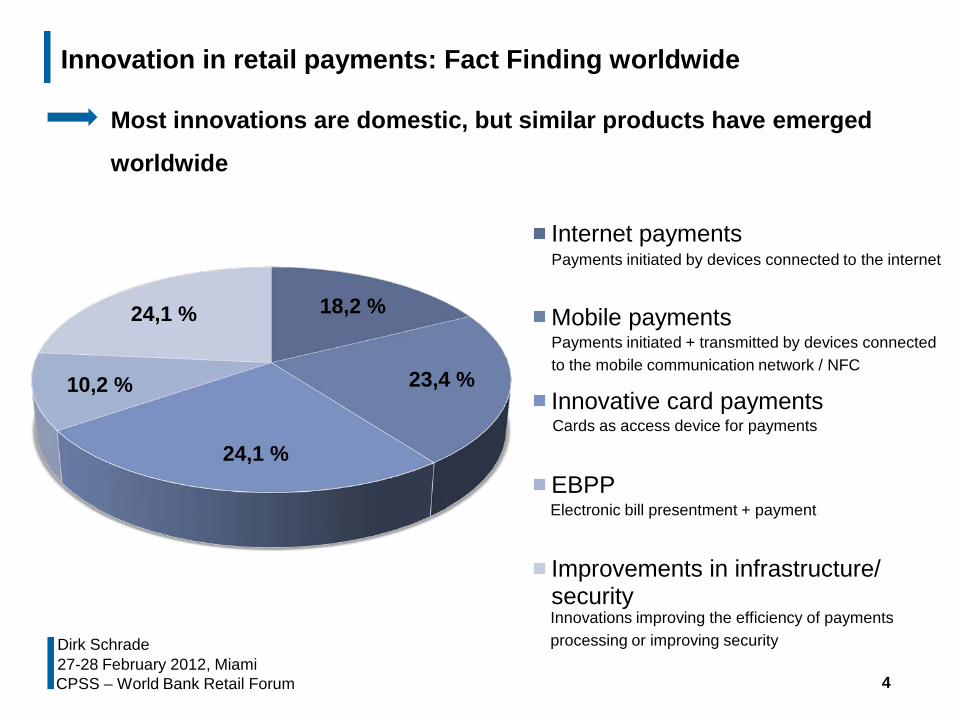

Innovation in retail payments: Fact Finding worldwide

Market is dynamic, but few innovation have significant market impact so far

3

Dirk Schrade27-28 February 2012, Miami

Fact finding exercise

− Focus: top innovations in the respective markets, irrespective of whether being innovative in all markets

− Time horizon: last decade

− CPSS member countries + selected other countries

− Including also some international products

Participation of 30 central banks

Altogether: 122 innovations reported

CPSS – World Bank Retail Forum

Most innovations are domestic, but similar products have emerged

worldwide

4

Dirk Schrade27-28 February 2012, Miami

18,2 %

23,4 %

24,1 %

10,2 %

24,1 %

Internet payments

Mobile payments

Innovative card payments

EBPP

Improvements in infrastructure/ security

Payments initiated by devices connected to the internet

Cards as access device for payments

Payments initiated + transmitted by devices connected to the mobile communication network / NFC

Electronic bill presentment + payment

Innovations improving the efficiency of payments processing or improving security

Innovation in retail payments: Fact Finding worldwide

CPSS – World Bank Retail Forum

Fact Finding worldwide – Trends

Acceleration of payment processing gained importance

5

Dirk Schrade27-28 February 2012, Miami

Faster interbankprocessing

Faster initiationof payments

CPSS – World Bank Retail Forum

Fact Finding worldwide – Trends

Financial inclusion as driving force for innovation

6

Dirk Schrade27-28 February 2012, Miami

Special bank accounts with limited payments-related services or prepaid

accounts with non-banks:

→ addressing the issue of the relatively high cost of a standard bank account

Business correspondents/agents:

→ Providing alternatives to the traditional branch, ATM and POS terminal at retailers

New means for transaction initiation + authentication:

→ Mobile phones + networks as devices for accessing payment services

CPSS – World Bank Retail Forum

Fact Finding worldwide – Trends

Role of non-banks is significantly increasing

7

Dirk Schrade27-28 February 2012, Miami

Non-banks competing in areas that are not yet dominated by banks

Possible trigger: use of innovative technoglogy

Focus: internet and mobile payments

High relevance of cooperation between banks + non-banks

in mobile payments and EBPP

No relevance of non-banks only cooperation

CPSS – World Bank Retail Forum 8

Dirk Schrade27-28 February 2012, Miami

Innovation

Userhabits

Cooperation

Security

Standardisation

Drivers and barriers – overview

Regulation

Price +price structure

Technicaldevelopments

CPSS – World Bank Retail Forum

Drivers and barriers

9

Dirk Schrade27-28 February 2012, Miami

Userhabits

Fulfilment of the criteria by payment instruments from the users’ point of view

Source: Deutsche Bundesbank 2009

CPSS – World Bank Retail Forum

Drivers and barriers

Regulatory regime for the provision of payment services

Improving competition by opening up the payments market

for non-banks:→ Lowering of the entry barriers to the payments market in many countries

Improving competition by intervening in the pricing policy:→ A more transparent pricing in order not to distort the user choice

Facilitating the use of innovative payment services:→ Removing legal obstacles eg for EBPP

→ Relaxing requirements in order to promote financial inclusion

10

Dirk Schrade27-28 February 2012, Miami

Regulation

CPSS – World Bank Retail Forum

Drivers and barriers

11

Dirk Schrade27-28 February 2012, Miami

Cooperation

The complexity of the M-payments chain The role of a Trusted Service Manager

CPSS – World Bank Retail Forum

Drivers and barriers

12

Dirk Schrade27-28 February 2012, Miami

Facilitates the achievement of a necessary critical mass

Enables competition + creates stable ground for new players to come into

the market

Additional revenue gained by standardisation enables the dedication of more

resources for the development of new products

Also possible drawbacks with regard to innovation, e. g. by diminishing the

incentive to innovate or by restricting competition

May raise competition issues if certain parties are excluded from the

standard-setting processing or do not have access to the results

Standardisation

CPSS – World Bank Retail Forum

Drivers and barriers

13

Dirk Schrade27-28 February 2012, Miami

Card payments:− Card-not-present transactions: stronger authentication procedures

− Contactless card payments: limits on the amounts + certification procedures

Internet payments:− Authentication of the payer‘s identity

− Protection of the online banking environment

Mobile payments: applications must be adequately insulated + certified

Improvements in infrastructure:− Communication over open networks: adequate encryption methods + authentication

− Faster processing: strong authentication for primary bank account

Security

CPSS – World Bank Retail Forum

Future developments

14

Dirk Schrade27-28 February 2012, Miami

Strong potential user demand

Targeting cash (low value)

Penetration of NFC-enabled HW

E-commerce as main driver

Growing c. b. activity

Traditional instruments:

no optimal choice

Potential user demand

High penetration at global level

Combination with e-money

[mobile money]

Large customer base

Users highly technophile

Security issues

Traditional instruments

No global standards

Efficient alternatives:

cards / internet payments

Cooperation issues

No real currency

No clear business case

Traditional infrastructures

Internet payments

NFC

Mobile payments

Virtualcurrencies

Opportunitites…. …threats

CPSS – World Bank Retail Forum

Innovation in payments

Innovation will take time…

1527-28 February 2012, MiamiDirk Schrade

0

1

2

3

4

5

6

7

8

9

10

1990 1995 2000 2005

Rat

io o

f yea

r to

tal t

o 19

92 to

tal

Households Using a Debit Card

CPSS – World Bank Retail Forum 16

Dirk Schrade27-28 February 2012, Miami

Innovation in payments

Innovation is already pulling down walls…

Chip-basedcard payments / e-money

E-money providers offeringdifferent access channels /

access devices

CPSS – World Bank Retail Forum

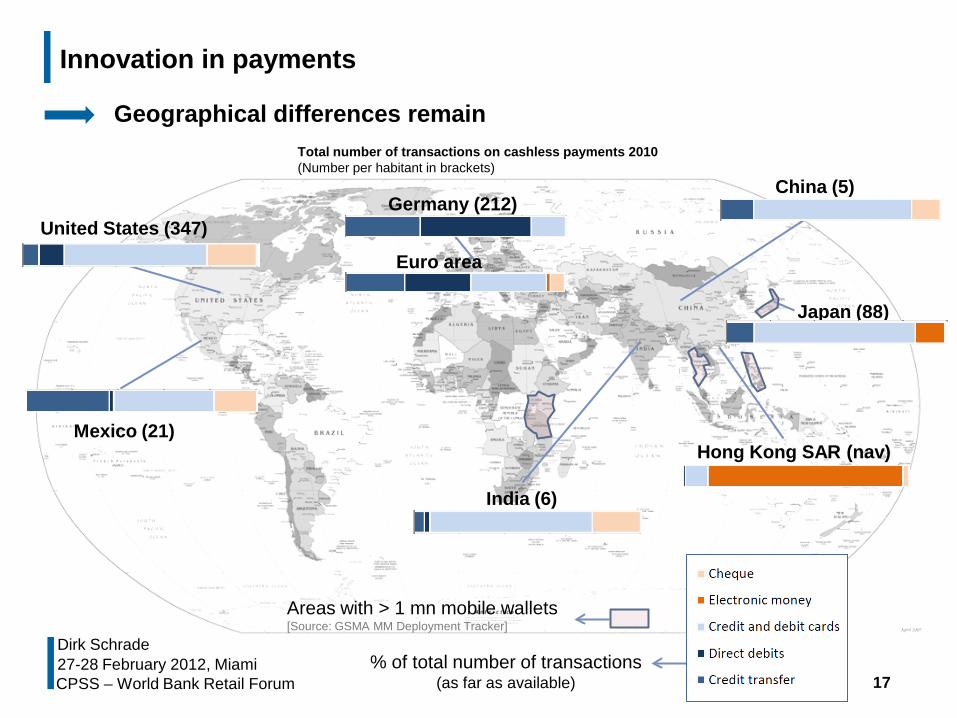

Geographical differences remain

17

Dirk Schrade27-28 February 2012, Miami

Innovation in payments

United States (347)

% of total number of transactions(as far as available)

Mexico (21)

Japan (88)

Total number of transactions on cashless payments 2010(Number per habitant in brackets)

India (6)

Hong Kong SAR (nav)

Germany (212)China (5)

Euro area

Areas with > 1 mn mobile wallets[Source: GSMA MM Deployment Tracker]

CPSS – World Bank Retail Forum 18

Dirk Schrade27-28 February 2012, Miami

Outlook: Retail payments – still a classical business?

„He who rejects change is the architect of decay“ (H. Wilson)