Embed Size (px)

Citation preview

Escola de EngenhariaUniversidade do Minho Departamento de Sistemas de Informação »«MERCADOS E NEGÓCIOS: DINÂMICAS E ESTRATÉGIAS

»«wp 32 (2003)

1

WP 55 (2005) Working papers “Mercados e Negócios” TSI Outubro 2005

Precision industries: markets and trends

Eduardo J. C. Beira

Escola de EngenhariaUniversidade do Minho Departamento de Sistemas de Informação »«MERCADOS E NEGÓCIOS: DINÂMICAS E ESTRATÉGIAS

»«wp 55 (2005)

2

Precision industries: markets and trends

Eduardo J. C. Beira

ISTMA International Special Tooling and Machining Association (general manager) Universidade do Minho, Escola de Engenharia (Professor)

[email protected], www.istma.org; www.dsi.uminho.pt/~ebeira

Apresentado no 2005 Mori Seiki International Conference on Die and Mould Technology, Beijing, 17

Outubro de 2005

Escola de EngenhariaUniversidade do Minho Departamento de Sistemas de Informação »«MERCADOS E NEGÓCIOS: DINÂMICAS E ESTRATÉGIAS

»«wp 55 (2005)

3

First of all I would like to thank CDMIA for the kind invitation to address

this important conference. It is an honor to address the China die and mould

makers at this opportunity.

I apologize for not speaking Chinese. Anyway I hope that my English can be

easily understood.

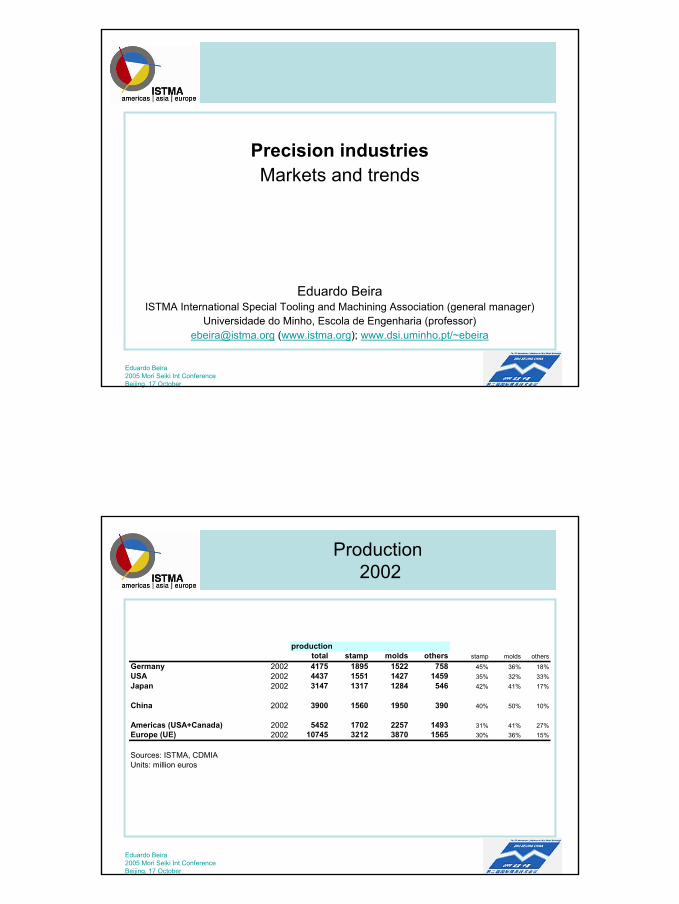

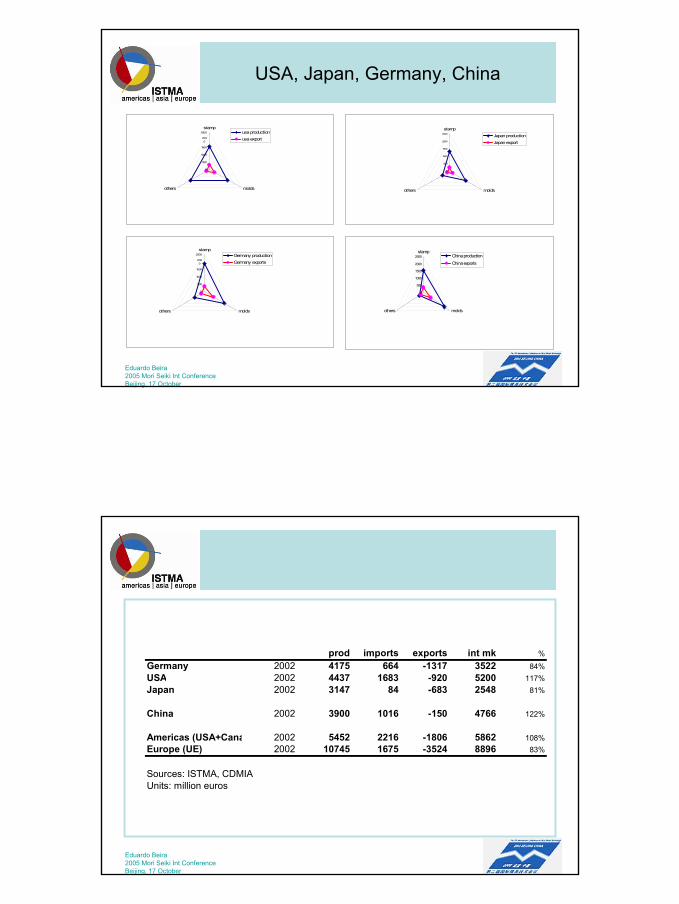

1. World precision industries are dominated by the die and mould making

sectors. This slide is based on ISTMA and CDMIA statistics for the most

important world producers (in million euros): Germany, USA, Japan, and now

China.

Production of other product behind dies and molds is specially important in

the USA (jigs and features, standard tooling components, ...).

The value of total production in China is now close to Germany and USA, and

higher than Japan.

China is now probably the most important mould making country in world

and one of the top die makers.

European Union, considered as a single entity, is the largest pool of

producers, both for die and for moulds.

2. This slide shows a radial representation (dies / mouds / others) of the

production and exports for the four countries previously considered.

Escola de EngenhariaUniversidade do Minho Departamento de Sistemas de Informação »«MERCADOS E NEGÓCIOS: DINÂMICAS E ESTRATÉGIAS

»«wp 55 (2005)

4

3. Considering the trade components (import and export) and the production of

all the components of the industry, it is possible to estimate the global internal

market of each country.

USA is the main importer, followed by China.

Germany and USA are the main exporters.

Although China may be now the largest world producer, the USA market is

still the largest consumer

European Union imports are similar to USA ones, but it is a stronger

exporter. The EU internal market is larger than both the USA or the China ones.

Note that China exports are less than 5% of its production, against 32% for

Germany and around 21 to 22% for USA and Japan.

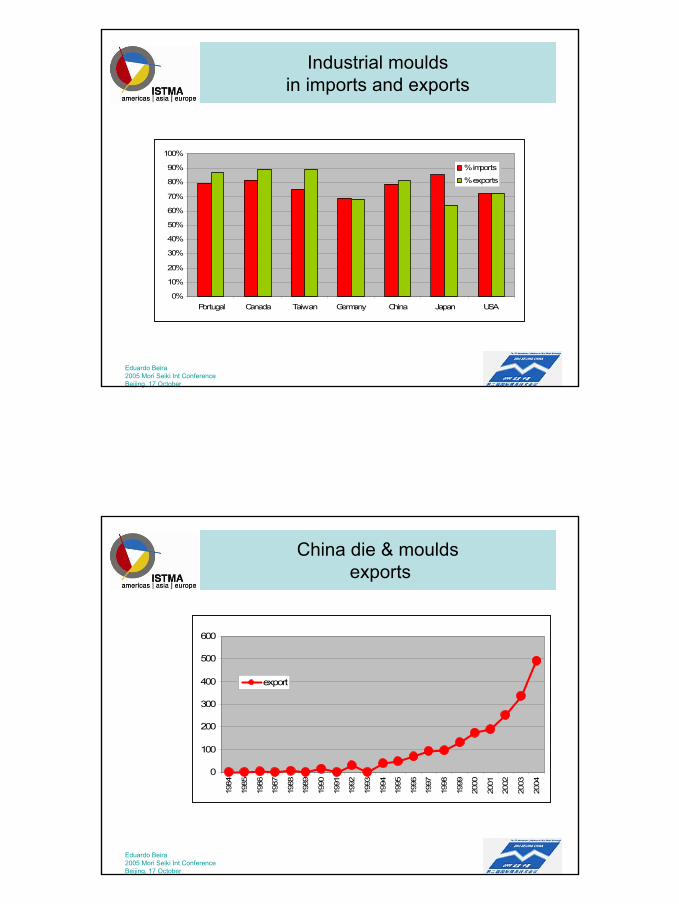

4. Industrial moulds (mainly for plastics) are the main components of the

international trade flows – usually around 70 to 90%.

Dies and tools do not travel as well as moulds.

The importance of moulds in the exports is smaller in the countries with

strong automotive industry (Germany, USA, Japan), where stamping dies have

an important share.

5. China exports (die and moulds) has been rising for twenty years, specially

during the last years.

Escola de EngenhariaUniversidade do Minho Departamento de Sistemas de Informação »«MERCADOS E NEGÓCIOS: DINÂMICAS E ESTRATÉGIAS

»«wp 55 (2005)

5

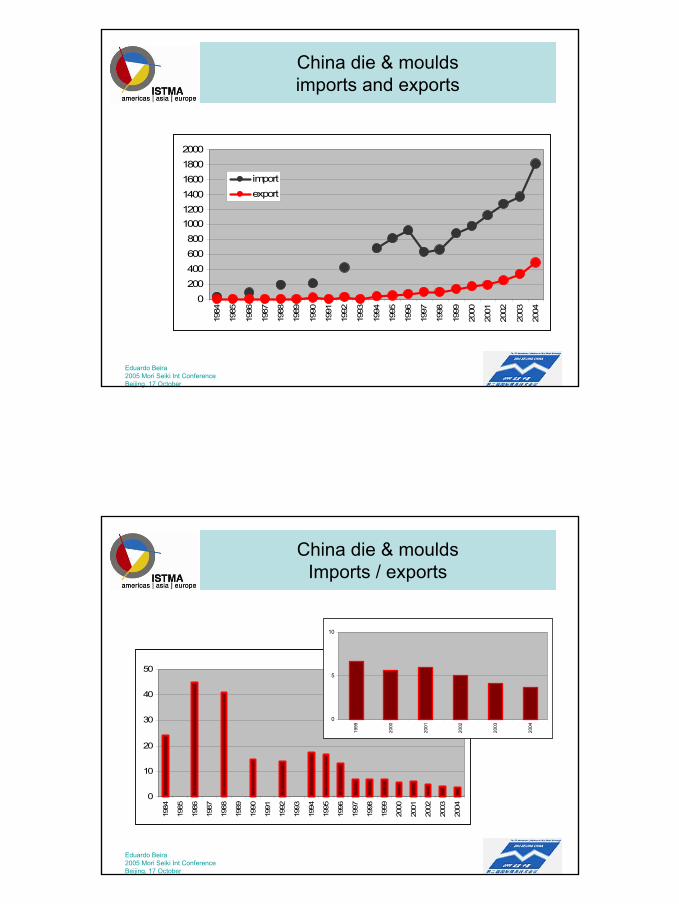

6. But imports of tools and dies for China have also increased.

7. The ratio imports / exports have decreased from around 20 to 4 during last 15

years.

During the last few years the ratio continues to decrease, although slowly.

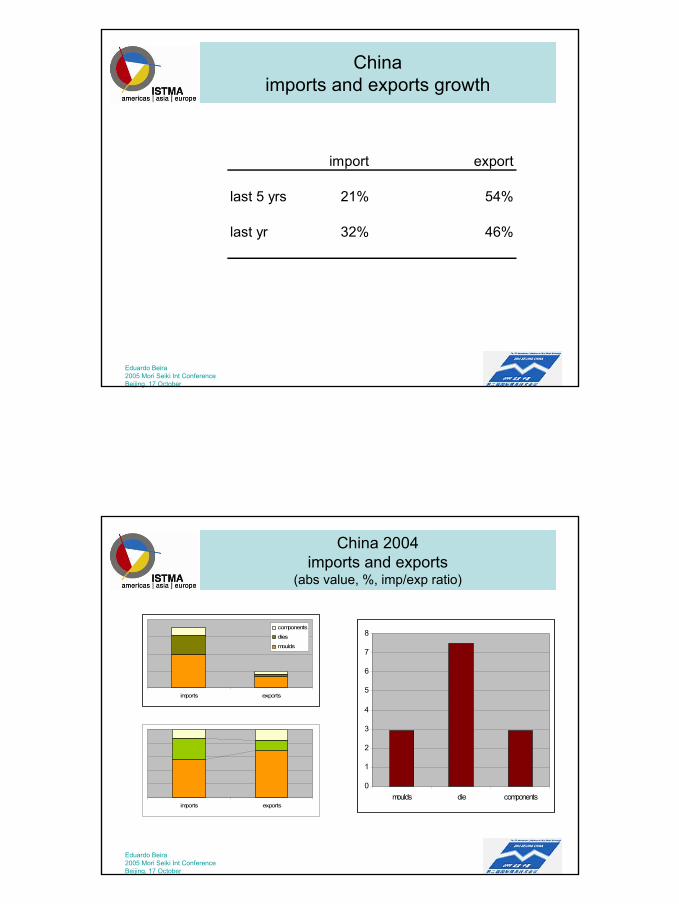

8. The data shows a strong growth of the activity of tool, die and mould making

in China.

During last 5 years, the growth of imports have been around 21% per year,

but the growth of exports have been higher, around 50% per year.

Growth during last year has been 32% for imports and 46% for exports.

9. The structure of China imports and exports is different (data from CDMIA

2004).

The ratio imports / exports has been close to 3 for moulds and components for

moulds, but higher (around 7 to 8) for dies.

Escola de EngenhariaUniversidade do Minho Departamento de Sistemas de Informação »«MERCADOS E NEGÓCIOS: DINÂMICAS E ESTRATÉGIAS

»«wp 55 (2005)

6

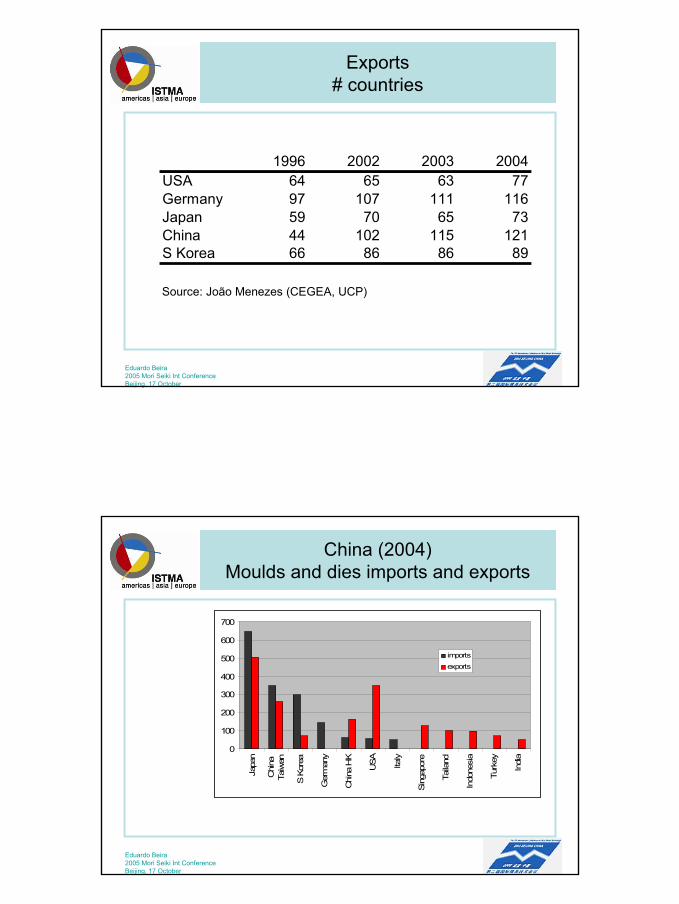

10. The number of destinations of the China export activity have increased with

time. A study has recently compared the number of export destinations for the

several players.

In 2004 exports from China to 121 countries were recorded in the

international trade databases. This is three times more destinations that in 1996

(five years before).

The destinations of Japan, USA and Korea exports are few.

11. CDMIA data shows different profiles for the countries of origin of imports and

the countries of destination for exports.

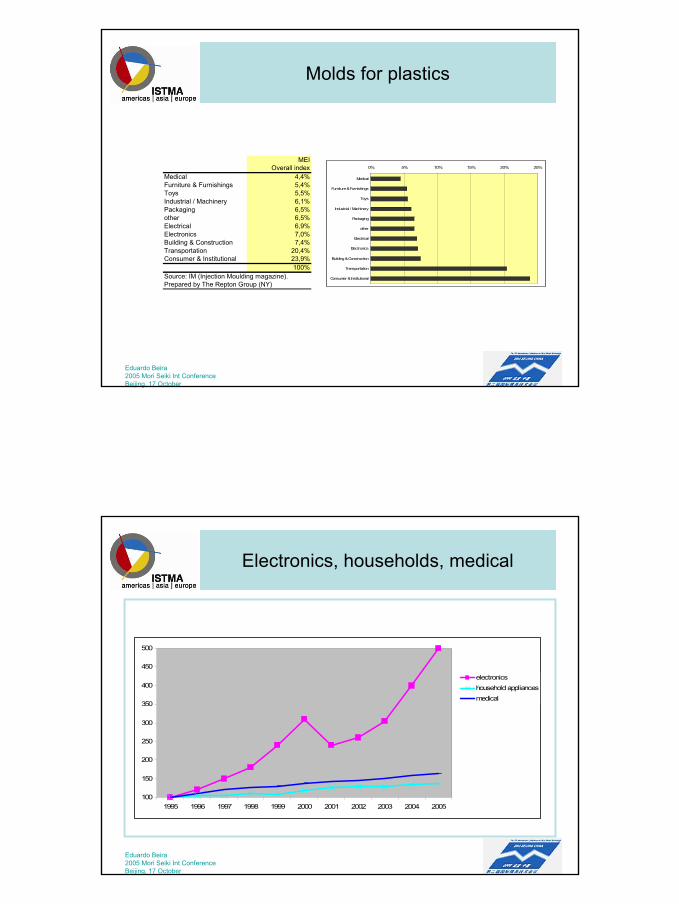

12. Industrial moulds for plastics are the principal component of international

trade.

This slide shows the importance of different economic sectors for the plastics

moulding activity (based on the USA market).

Consumer products (home appliances and other homewares included) and

transportation are the main customers, driving close to half of the moulding

activity.

Electronics represents around 7%, as well has packaging.

Medical product represent 4 to 5%.

Toys and furniture components represent 5 to 6% each.

To forecast the short term trends for moulds we need to consider the

customer sectors for plastic parts.

Escola de EngenhariaUniversidade do Minho Departamento de Sistemas de Informação »«MERCADOS E NEGÓCIOS: DINÂMICAS E ESTRATÉGIAS

»«wp 55 (2005)

7

13. A recent study by NTMA, the ISTMA national association in the USA,

forecasted the several sectors for 2005 (in the USA market).

The general expectation is positive for the second half of 2005.

Growth continues very strong for electronics products.

Trends continue positive for medical parts and household appliances,

although with a lower rate.

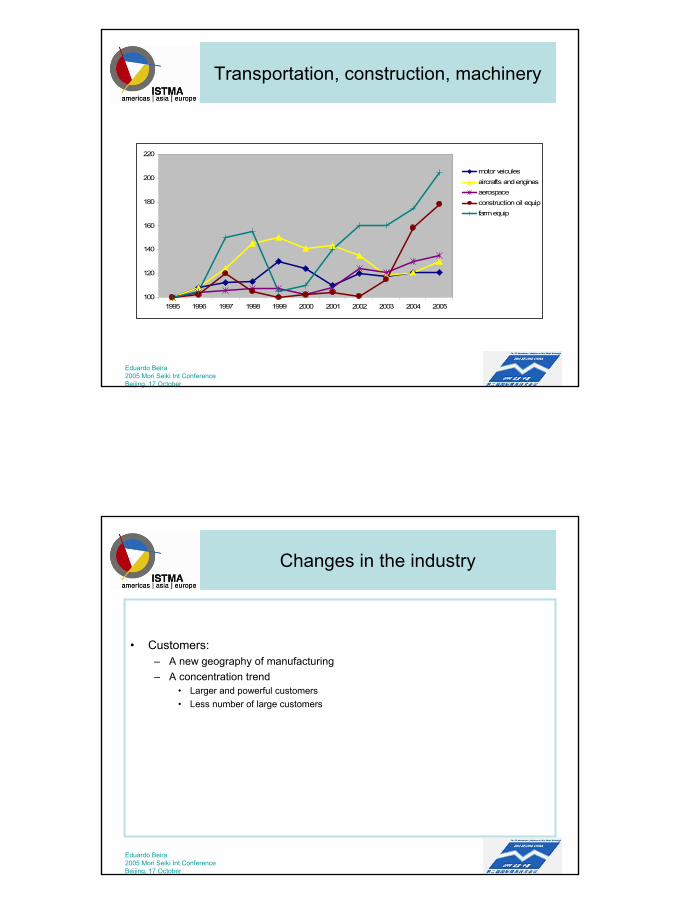

14. The prospects are good for some markets related with equipments and

machinery (farm equipments, equipments for construction and oil industries,

aerospace), although close to flat for motor vehicles and parts, and not very

strong for aircrafts.

These news about the automotive industries are not the heaven for mould

makers, due to the importance of the sector for some of the most important

players.

15. This is an global industry experimenting important changes.

First all its customers are changing.

There is a new geography of the customer manufacturing activities, with a

change eastwards of the centre of gravity of moulding of parts and assembling.

Escola de EngenhariaUniversidade do Minho Departamento de Sistemas de Informação »«MERCADOS E NEGÓCIOS: DINÂMICAS E ESTRATÉGIAS

»«wp 55 (2005)

8

The customers are also merging and concentrating activities. This means

larger and more powerful customers and also few customers. The competitive

landscape is changing.

16. But the suppliers (die and mould makers) are also changing – specially the

mould makers.

There are new competitors and new regional dynamics (China included).

Customers are demanding a larger spectrum of integrated services for more

complex products.

More complex relationships with the clients need to be managed and the

global scale.

All these demands new skills, specially for marketing and commercial

activities. This is true both for the incumbents (that need a new positioning) and

for newcomers (that need to find some autonomy for the sales channel).

17. Of course technologies are changing, with new materials, fast techniques and

nano scales.

But the more important changes will be in the services components of the

business.

Managing the customer relationships will become a critical issue – specially

how to deal with the large and powerful OEMs and first tiers, and how to find

specialized markets for specialization.

But demands for pre and after sales service will continue to increase,

demanding more sophisticated skills inn the international market.

Escola de EngenhariaUniversidade do Minho Departamento de Sistemas de Informação »«MERCADOS E NEGÓCIOS: DINÂMICAS E ESTRATÉGIAS

»«wp 55 (2005)

9

And financial services will be an issue for the future. The “business model”

for the mould exploitation is mature for innovative financial practices, that will

demand large financial resources. The future is not only a question of

manufacturing cost, but overall use of the mould along its life cycle.

18. Mould makers all over the world face a “brave new world” of competitive

markets.

More complex products in old or new materials will demand more dies and

moulds.

Precision industries will have an increasingly important future.

We estimate that until the end of this decade, 2/3 of the moulds for OEMs

and first tiers multinational will be made in East Asia and other low cost

countries.

European and USA mould makers will compete for the remaining 1/3 of high

precision and high complexity moulds on a basis of concurrent engineering,

certified quality, integrated and innovative services and also advanced

technologies.

19. The case of the motor or automotive industry is specially important due to

their importance as clients for plastic parts.

The motor industry faces a fragmentation of model varieties, shorter life

cycles for the car models, smaller and “on demand” production runs, and needs

flexible and modular designs for manufacturing. The Economist recently printed

that this is an industry reinventing itself.

Escola de EngenhariaUniversidade do Minho Departamento de Sistemas de Informação »«MERCADOS E NEGÓCIOS: DINÂMICAS E ESTRATÉGIAS

»«wp 55 (2005)

10

The relationship between the industry and its suppliers has become difficult.

The hard procurement model may be on the limits. May be the more cooperative

and soft and long term approach from some OEMS (Chrysler and Honda, for

instance) will change the hard approach from GM or Ford.

Trust relationships between networks of suppliers in different countries and

the manufacturers will be need.

20. Please allow me some final words about ISTMA, the International Special

Tooling and Machining Association.

ISTMA is a federation of national associations of companies in the precision

industries, specially die and mould making. The China national association is

CDMIA (China Die & Mould Industry Association).

ISTMA is organized around three regional branches (Europe, Asia and

Americas).

CDMIA is affiliated with ISTMA through FADMA / ISTMA Asia.

21. ISTMA new website (www.istma.org) is an international platform for

knowledge and information sharing for the companies affiliated with the national

associations.

Companies can register to have access to the information exclusive for the

members of the affiliated associations, like the statistics reports, the business

conditions surveys, the reports from the regional and worldwide meetings and

internal documents.

Soon the international Terminology will be available as a web service.

Escola de EngenhariaUniversidade do Minho Departamento de Sistemas de Informação »«MERCADOS E NEGÓCIOS: DINÂMICAS E ESTRATÉGIAS

»«wp 55 (2005)

11

22. This slide shows some of the formats for presentation of the important

business conditions surveys. The survey runs every semester and allows the

companies to benchmark their business perceptions against other companies in

different countries and also the same country.

Europe and Americas regularly run the survey.

ISTMA Asia has not been regular. We hope this can be improved in the

future and we expect that China companies will contribute for the survey.

23. ISTMA provides an international and global network of companies and their

national associations. It offers an important platform for international

cooperation.

We are very happy and proud with the contribution of the Chinese companies

and CDMIA and we expect to improve the relationship in the future.

24. Thanks very much for your attention.

And my best wishes for CDMIA and the China die and mould making

companies.

1

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

Precision industriesMarkets and trends

Eduardo BeiraISTMA International Special Tooling and Machining Association (general manager)

Universidade do Minho, Escola de Engenharia (professor)[email protected] (www.istma.org); www.dsi.uminho.pt/~ebeira

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

Production2002

productiontotal stamp molds others stamp molds others

Germany 2002 4175 1895 1522 758 45% 36% 18%USA 2002 4437 1551 1427 1459 35% 32% 33%Japan 2002 3147 1317 1284 546 42% 41% 17%

China 2002 3900 1560 1950 390 40% 50% 10%

Americas (USA+Canada) 2002 5452 1702 2257 1493 31% 41% 27%Europe (UE) 2002 10745 3212 3870 1565 30% 36% 15%

Sources: ISTMA, CDMIAUnits: million euros

2

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

USA, Japan, Germany, China

0

500

1000

1500

2000

2500

stamp

moldsothers

usa productionusa export

0

500

1000

1500

2000

2500

stamp

moldsothers

Japan productionJapan export

0

500

1000

1500

2000

2500

stamp

moldsothers

Germany productionGermany exports

0

500

1000

1500

2000

2500stamp

moldsothers

China productionChina exports

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

prod imports exports int mk %Germany 2002 4175 664 -1317 3522 84%USA 2002 4437 1683 -920 5200 117%Japan 2002 3147 84 -683 2548 81%

China 2002 3900 1016 -150 4766 122%

Americas (USA+Cana 2002 5452 2216 -1806 5862 108%Europe (UE) 2002 10745 1675 -3524 8896 83%

Sources: ISTMA, CDMIAUnits: million euros

3

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

Industrial moulds in imports and exports

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Portugal Canada Taiwan Germany China Japan USA

% imports

% exports

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

China die & mouldsexports

0

100

200

300

400

500

600

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

export

4

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

China die & moulds imports and exports

0200400600800

100012001400160018002000

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

importexport

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

China die & mouldsImports / exports

0

10

20

30

40

50

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

0

5

10

1999

2000

2001

2002

2003

2004

5

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

Chinaimports and exports growth

import export

last 5 yrs 21% 54%

last yr 32% 46%

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

China 2004imports and exports

(abs value, %, imp/exp ratio)

imports exports

components

dies

moulds

0

1

2

3

4

5

6

7

8

moulds die componentsimports exports

6

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

Exports# countries

1996 2002 2003 2004USA 64 65 63 77Germany 97 107 111 116Japan 59 70 65 73China 44 102 115 121S Korea 66 86 86 89

Source: João Menezes (CEGEA, UCP)

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

China (2004)Moulds and dies imports and exports

0

100

200

300

400

500

600

700

Japa

n

Chi

naTa

iwan

S K

orea

Ger

man

y

Chi

na H

K

USA

Italy

Sing

apor

e

Taila

nd

Indo

nesi

a

Turk

ey

Indi

a

importsexports

7

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

Molds for plastics

MEIOverall index

Medical 4,4%Furniture & Furnishings 5,4%Toys 5,5%Industrial / Machinery 6,1%Packaging 6,5%other 6,5%Electrical 6,9%Electronics 7,0%Building & Construction 7,4%Transportation 20,4%Consumer & Institutional 23,9%

100%Source: IM (Injection Moulding magazine). Prepared by The Repton Group (NY)

0% 5% 10% 15% 20% 25%

Medical

Furniture & Furnishings

Toys

Industrial / Machinery

Packaging

other

Electrical

Electronics

Building & Construction

Transportation

Consumer & Institutional

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

Electronics, households, medical

100

150

200

250

300

350

400

450

500

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

electronicshousehold appliancesmedical

8

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

Transportation, construction, machinery

100

120

140

160

180

200

220

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

motor veiculesaircrafts and enginesaerospaceconstruction oil equipfarm equip

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

Changes in the industry

• Customers:– A new geography of manufacturing– A concentration trend

• Larger and powerful customers• Less number of large customers

9

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

Changes in the industry (II)

• Die and mould makers:– New competitors– New regional dynamics– New “broadband” of the offer for the supply chain– New integrated skills

• Additional 1% to 2% of sales profitability can be achieved through better reutilization of knowledge along the supply chain (McKinsey)

• Mold making and moulding integrated service– More complex partnerships and global competition – More complex products – New marketing and commercial skills

• For incumbents• For newcomers

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

Changes in the industry (III)

• Technologies are changing– Fast prototyping– Hybrid moulds– Multimaterial and assembling moulding– Nano scales– New materials

• But the more important changes for the present and next years will be in the service components of the business

– Customer relations management• Partnerships with OEMs and first tiers• Finding innovative niches of specialized product companies

– Pre and post sales service– Commercial skills in the international market– Financial

10

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

Next years

• Mouldmakers face a “brave new world”– Highly competitive at the regional / global levels– Demanding new skills

• OEMs and first tiers (multinationals) demand for moulds

– around 2/3 of their mould will be made in East Asia and other low cost countries (new competitors).

– European and USA mould makers will compete for the remaining 1/3 of high precision and high complexity moulds on a basis of concurrent engineering, certified quality, integrated and innovative services and also advanced technologies.

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

Motor industry

• Fragmentation of model variety• shorter life cycles• smaller production runs • higher demand for flexible and modular design and manufacturing

• “An industry reinventing itself”– The Economist, 2004

• Will the agressive client / supplier procurement model prevail?– GM / Ford vs Chrysler / Honda

• Will a more cooperative and concurrent approach emerge?– Trust will be critical.

11

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

ISTMARegional branches

Asia (FADMA) AustraliaChinaChina TaiwanIndiaJapanKoreaMalasyaPhilippinesSingaporeTaiwan

Europa EstoniaCzech RepublicFinlandFranceGermanyHungaryItalyPortugalSloveniaSpainSwedenSwitzerland Americas USA

CanadaArgentina

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

www.istma.organ international platform of knowledge and information

12

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

ISTMA

• International Terminology

• Annual Statistics reports

• Business conditions surveys

• Regional and world meetings

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

36,4%

22,7%

31,8%

-4,5%-18,2%

-9,1%

-13,6%

-100,0%

-50,0%

0,0%

50,0%

100,0%quotes

shipments

backlog

prof itsemployment

investment

prices

Business conditions surveys

22% 22%23%

8%

13%14%

15%

29%28%

32%

24%

28%

33%30%

0%

10%

20%

30%

40%

1 2 1 2 1 2 1 2

2002 2003 2004 2005

portugal m

europe m

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 2 1 2 1 2 1

2002 2002 2003 2003 2004 2004 2005

excellent

very good

good

fair

poor

54,5%

63,6%

31,8%

63,6%

54,5%

72,7%

59,1%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

quotes

shipments

backlog

profits

employment

investment

prices

13

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

ISTMA

• An international and global network of companies and national associations• A platform for cooperation

Eduardo Beira2005 Mori Seiki Int ConferenceBeijing, 17 October

• Thank you!• And the best wishes for China die and mould makers