Embed Size (px)

Citation preview

SCM Risk Management Services (RMS) is committed to keeping a pulse on Canadian reconstruction costs through ongoing research and analysis of completed inspections and evaluations. Through Precise Pulse, RMS is pleased to share this information with our underwriting partners as part of our commitment to continually monitor costs, analyze total loss reconstruction costs, and update rmsPrecise™ to reflect these associated trends.

PRECISION AND STABILITY

Diverse Pressures in 2016RMS’ ongoing research and studies into reconstruction costs show that there are a number of diverse pressures in 2016 on expected costs to rebuild. We are assessing these pressures to determine the degree and stability of impacts on replacement costs both in the short and long term. The following trends are of particular interest:

• Prior to the Fort McMurray catastrophe, national reconstruction cost studies were already showing a national trend of increasing costs at the beginning of 2016, compared to the previous year (+3-5%). Generally, increases in the quality of material and design of housing stock across the country have fueled this pattern, along with continued healthy trends in housing starts and renovation investment. Of particular note are the significant increases in replacement costs for roofing components, which can be seen across the country (see adjacent section for further detail).

• While our replacement costs continued to closely match total loss costs early in 2016 (within 5%), the impacts of total losses from the Fort McMurray fire will have a significant impact on these comparisons as the year progresses. Through our rmsQuantify™ division, we are directly involved in assessing hundreds of post-loss costs at Fort McMurray. Insight from rmsQuantify™ and ClaimsPro provides a unique opportunity for RMS to accurately validate reconstruction costs as well as isolate the impact of inflated cost expected during the time of a catastrophe. As final assessments are still underway, this work will continue throughout 2016.

• Variance of inspected reconstruction cost estimates from insured Coverage A amount continues to emulate historical patterns of underinsurance, with more than 30% of inspected locations being underinsured by over 25%.

SOARING ROOFS - WE’VE GOT YOU COVEREDToday the roof is not just a cover over our heads, but is an important part of the aesthetic value and curb appeal of the home. Homeowners are spending more money than ever on roof covering and design. When it comes to replacing them after a loss, so is the insurance industry. Here is what we are finding through inspections and replacement cost studies:

• On average, replacement costs for roofing components have gone up over 7% from 2015 to 2016

• The biggest increase occurred in the Western Provinces with an average increase of 9%. This corresponds with a higher frequency of expensive roofing materials (cedar, metal, impact resistant shingles, and green roofing) seen during inspections in Western Canada.

Life expectancy of roofs vary due to location, climate, and installation practice, so frequent inspection is critical to prevent leaks and a resulting claim. Roofing is important from a costing component and an underwriting component as many water losses are related to roof conditions.

PRECISE PULSE Volume 1 - Issue 2

PRECISE PULSE 2

scm-rms.ca

TERRITORY TRENDS

Strong investment in construction in BC and Ontario continues to result in increased labour demand and costs in key urban areas. This investment is offset by some provinces with slowing new housing trends, but the overall increase at a national level is maintaining pressure on labour and material costs across the country.

Alberta has the largest drop in housing starts of all provinces due to the downturn in the oil industry, however this impact on construction costs is expected to be buoyed due to Fort McMurray re-construction.

Consistent with the housing start trends, data from our reconstruction cost studies across Canada show corresponding increases in construction costs for Ontario (5.6%) and BC (4.7%).

FEATURE ADJUSTMENTS

Through ongoing analysis of features identified during the inspection process, RMS has noted an increasing pattern of investment in outdoor living that is also impacting replacement cost valuations. Decks and porches are no longer just a place to hang out in the summer and watch the world go by, but in some houses, these are places to live and barbecue year round. According to the North American Deck and Railing association it’s estimated that 2.5 million new or replacement decks were built last year.

The following are some considerations related to roof costs and insurable losses:

• Neighbourhoods built in the boom years of the late 70’s and mid 80’s will be reaching the end of the average life cycle for their second roof, meaning inspection is key to loss mitigation

• Expensive design/materials, multiple elevations, and more skylights will continue to drive up costs

• Growing new housing starts will also add pressure to supply and demand for labour and materials

• Small catastrophic losses this year from ice, wind and hail in Ontario, Quebec, New Brunswick and Alberta will put added pressure on roofing materials and labour

• With the number of catastrophic losses affecting roofs this year, insurers should watch for “storm chaser roofers” who may repair damage at a lower quality. Industry roofing analysts indicate that a roof put on by a storm chaser may only last five to seven years.

PRECISE PULSE 3

scm-rms.ca

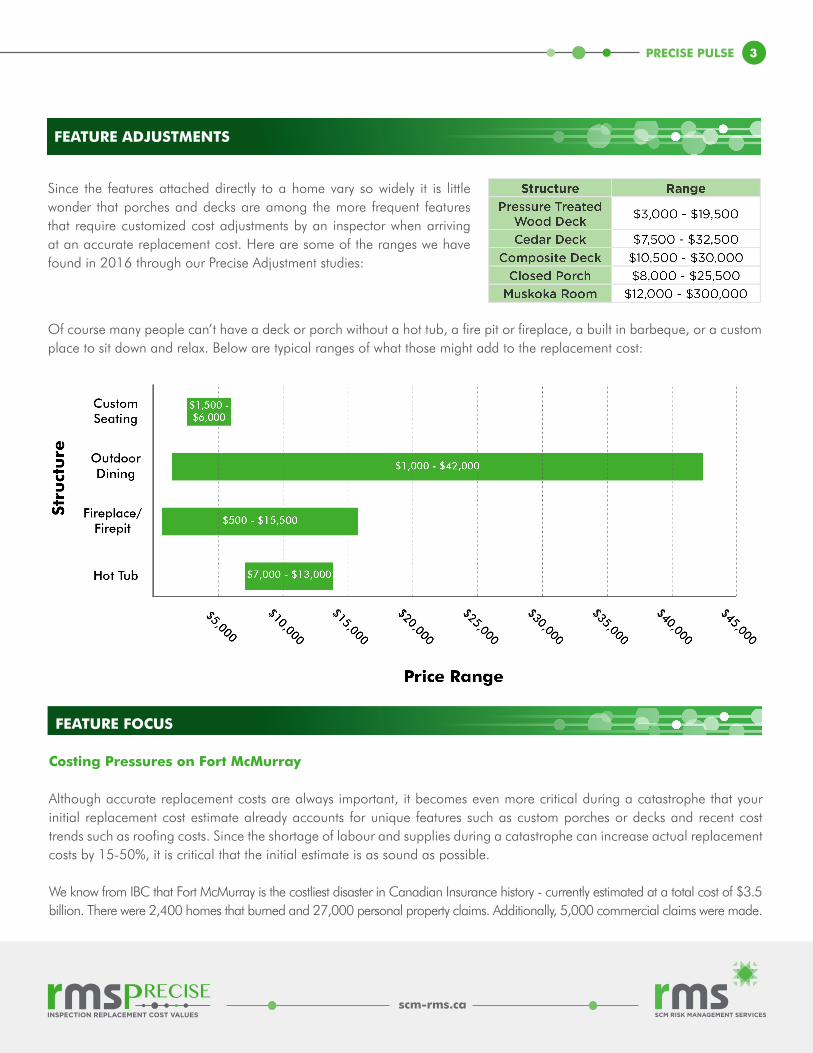

Since the features attached directly to a home vary so widely it is little wonder that porches and decks are among the more frequent features that require customized cost adjustments by an inspector when arriving at an accurate replacement cost. Here are some of the ranges we have found in 2016 through our Precise Adjustment studies:

FEATURE ADJUSTMENTS

Of course many people can’t have a deck or porch without a hot tub, a fire pit or fireplace, a built in barbeque, or a custom place to sit down and relax. Below are typical ranges of what those might add to the replacement cost:

FEATURE FOCUS

Costing Pressures on Fort McMurray

Although accurate replacement costs are always important, it becomes even more critical during a catastrophe that your initial replacement cost estimate already accounts for unique features such as custom porches or decks and recent cost trends such as roofing costs. Since the shortage of labour and supplies during a catastrophe can increase actual replacement costs by 15-50%, it is critical that the initial estimate is as sound as possible.

We know from IBC that Fort McMurray is the costliest disaster in Canadian Insurance history - currently estimated at a total cost of $3.5 billion. There were 2,400 homes that burned and 27,000 personal property claims. Additionally, 5,000 commercial claims were made.

PRECISE PULSE 4

scm-rms.ca

As the damage in Fort McMurray is

assessed, this information must be properly analyzed to paint a clear picture of

what’s to come.

From the inspection work that RMS has historically completed in the Fort McMurray area, we are aware that there are property characteristics that may not be accounted for in the initial Coverage A amounts where inspections were not completed.

For example, inspections completed between 2006 to 2016 in Fort McMurray show that homes have the following characteristics:

FEATURE FOCUS CON’T

• 55% are 16 years of age or less

• 72% have a garage attached to the home

• 55% have a porch attached to the home

• 80% have a deck attached to the home

• 76% have a basement for foundation

• Average square footage is 2334

In addition to features that are typically unaccounted for in non-inspected properties, staff from rmsQuantify™ encountered a number of sobering items while on-site at Fort McMurray that will directly impact replacement values. Due to the extreme heat and devastation, we have had to assess and account for unique costs such as foundation instability, debris removal issues, pollution and contamination. These examples could significantly increase the total loss cost. These are costs in addition to increased labour costs and decreased supply during a catastrophe that apply significant pressure on total replacement costs values.

Additionally, waiting for areas to be released so that homeowners can return and insurers can assess the extent of damage can cause an increase in total claim costs and impact policy limits. Contemplating the full scope of the property in question is equally important. Aside from building construction costs, the costs of trees, permanent detached structures such as decks and patios are often overlooked until a large scale catastrophic event occurs. These items can cost tens of thousands of dollars to replace and are often difficult to quantify after catastrophes like Fort McMurray.

“The devastation in Fort McMurray has no doubt had a significant impact on the lives of those residing, and working in the area,” begins Patrick Garuk, President of RMS. “The trickle down impacts of the building reconstruction costs will undoubtedly play a role in the longer term impacts on Canadian reconstruction costs. We consider ourselves fortunate to be in a position to bring this valuable information to our customers so that they, in turn, can better protect their customers. RMS is in a unique position to be able to analyze pre and post catastrophe inspection data, as well as the claims reconstruction data within our two divisions, and deliver these benefits to our customers, helping to make their service offering better.”