Embed Size (px)

Citation preview

1

Pre-budget submission 2017

September 2016

Support healthy lifestyle choices to save lives and reduce health service pressures

2

Executive Summary

The Royal College of Physicians of Ireland calls for the following actions in

Budget 2017 to save lives and reduce the pressures on our health services.

Introduce a 20% tax on sugar sweetened drinks including juices and sports drinks with the

proceeds to be ring-fenced for actions to promote healthier living.

Fund research and evidence-based programmes and interventions for the prevention,

treatment and management of obesity and physical inactivity.

Adopt the Public Health (Alcohol) Bill to include setting Minimum Unit Pricing for alcohol

products.

Introduce a social responsibility levy on the alcohol industry.

Increase excise duties on alcohol products, in line with inflation

Increase excise duties on tobacco products.

Introduce an environmental levy on tobacco packs.

Remove VAT on nicotine replacement therapies.

Impose price cap regulation on tobacco industry profits.

Ensure adequate resourcing of the National Physical Activity Plan.

3

Fiscal actions to reduce alcohol consumption, consumption of sugar sweetened drinks, to reduce smoking

prevalence and to encourage physical activity are necessary as part of a suite of measures to reduce the

substantial healthcare and economic burden directly associated with these risk factors.

There is no single reason why people consume alcohol in a harmful way; no single cause of the obesity

epidemic. Likewise there is no single measure that will address these issues. Based on the evidence, there

are measures that will be effective, including fiscal measures, which should be introduced as part of a

multiplicity of measures to address the various risk factors and determinants of these health harms.

Chronic diseases, caused or worsened by unsafe use of alcohol, unhealthy diets, smoking and inactivity,

are major drivers of healthcare costs in Ireland. Ninety per cent of our total healthcare costs are spent on

the 30% of the population with chronic diseases.

Smoking related healthcare costs were estimated at €466 million in 2013.1

The estimated cost to the health system in 2012 of dealing with inpatients with either a wholly or

partially alcohol-attributable condition was €1.5 billion, which accounted for 11% of all public

healthcare expenditure that year.2

The estimated cost of overweight and obesity was €1.13 billion in 2009, of which direct

healthcare costs were almost €400m.3

The cost of physical inactivity is estimated to be approximately €1.5 billion annually. 4

4

About the Royal College of Physicians of Ireland

The Royal College of Physicians of Ireland (RCPI) has a longstanding record of leadership in the area of

public health policy. We have a number of policy groups comprised of members, fellows and trainees from

a range of medical specialities within RCPI, representatives from other medical and healthcare

professions, and relevant advocacy organisations.

Members of these groups work together to review the scale of the problem in Ireland, to examine the

evidence for effective interventions and to develop recommendations to prevent illness and to promote

wellbeing amongst the public. In recent years there has been a focus on alcohol, obesity and tobacco, and

recently policy groups have also been established on physical activity and ageing.

The Faculty of Public Health, which is part of RCPI, is also a strong advocate for public health policy, and

has been a driving force behind the establishment of many of the RCPI policy groups.

The economic cost of chronic disease

Chronic diseases are major drivers of healthcare costs as well as exacting a huge human toll. Ninety per

cent of our total healthcare costs are spent on the 30% of the population with chronic diseases.5 Many of

these diseases are caused or worsened by risk factors such as tobacco use, overweight and obesity, alcohol

consumption and physical inactivity. Prevalence of chronic conditions and accompanying lifestyle factors

are also strongly influenced by socio-economic status, level of education, employment and housing.

The healthcare and economic burden associated with some of these risk factors is alarming:

Smoking related healthcare costs were estimated at €466 million in 2013.1

The estimated cost to the health system in 2012 of dealing with inpatients with either a wholly or

partially alcohol-attributable condition was €1.5 billion, which accounted for 11.0% of all public

healthcare expenditure that year.2

The estimated cost of overweight and Obesity was €1.13 billion in 2009, of which direct

healthcare costs were almost €400m. 3

The cost of physical inactivity is estimated to be approximately €1.5 billion annually. 4

It will be impossible to sustain a healthcare system in the future unless disease prevention and self-

management is prioritised, resourced and rewarded.

Healthy Ireland has established a vision for keeping people well and has highlighted the need for cross-

sectoral actions to advance this vision. Sustained political support from all sectors, including the

Department of Finance, is necessary to make progress on reaching specific targets defined in the Healthy

Ireland framework. The World Health Organisation has also long recognised the potential of fiscal

measures to encourage health dietary behaviour. 6

5

Sugar sweetened drinks tax

The Royal College of Physicians of Ireland calls on the government to introduce a tax on sugar

sweetened drinks (SSDs), including juices and sports drinks, as committed to under the

programme for partnership government.

A volumetric tax is the preferred option and should be set at a rate to achieve a 20% price

increase.

The proceeds of this tax should be ring-fenced and used to promote healthier living and a healthier

future for all Irish children. i

We call on the Government to fund research and resource effective evidence-based programmes

and interventions for the prevention, treatment and management of obesity and physical

inactivity. This includes adequate resourcing of the National Obesity Strategy.

Ireland’s obesity levels have reached a crisis point. One in four Irish children are overweight or obese.

Two out of every three adults are overweight or obese.7 By 2025 it’s estimated that 37% of Irish women

and 38% of Irish men will be obese.8 Poorer socio-economic groups are among the most severely affected

by the obesity epidemic. For example it was reported in 2014 that the rate of overweight and obesity in

children was stabilising somewhat- but only in the more socially advantaged schools.9

The determinants of obesity are complex, and as such no one measure alone will reverse the trends. The

soon to be published National Obesity Strategy will describe a range of measures to reduce obesity levels.

We recommend that this strategy is adequately resourced and implemented in full.

The Royal College of Physicians of Ireland has consistently called for the introduction of a 20% tax on

sugar sweetened drinks as one component of a strategy of measures to reduce obesity. Such a tax has

strong support from the public 10 and from health campaigners nationally and internationally. There is

also widespread support from political parties, as evidenced by inclusion of this tax in the General

Election manifestos of the four major political parties and the commitment to the introduction of a 20%

tax on sugar sweetened beverages in the 2016 Programme for Partnership government. 11

Evidence supporting the introduction of a tax on sugar sweetened drinks includes:

There is ample evidence to show that that consumption of sugar sweetened drinks contributes to

obesity. 12 13 14 15 16 17 18 19

i Such as through a ‘Healthy Ireland’ fund as described by the Minister for Health Promotion in August 2016 or a

Children’s Health Fund, proposed by the Irish Heart Foundation.

6

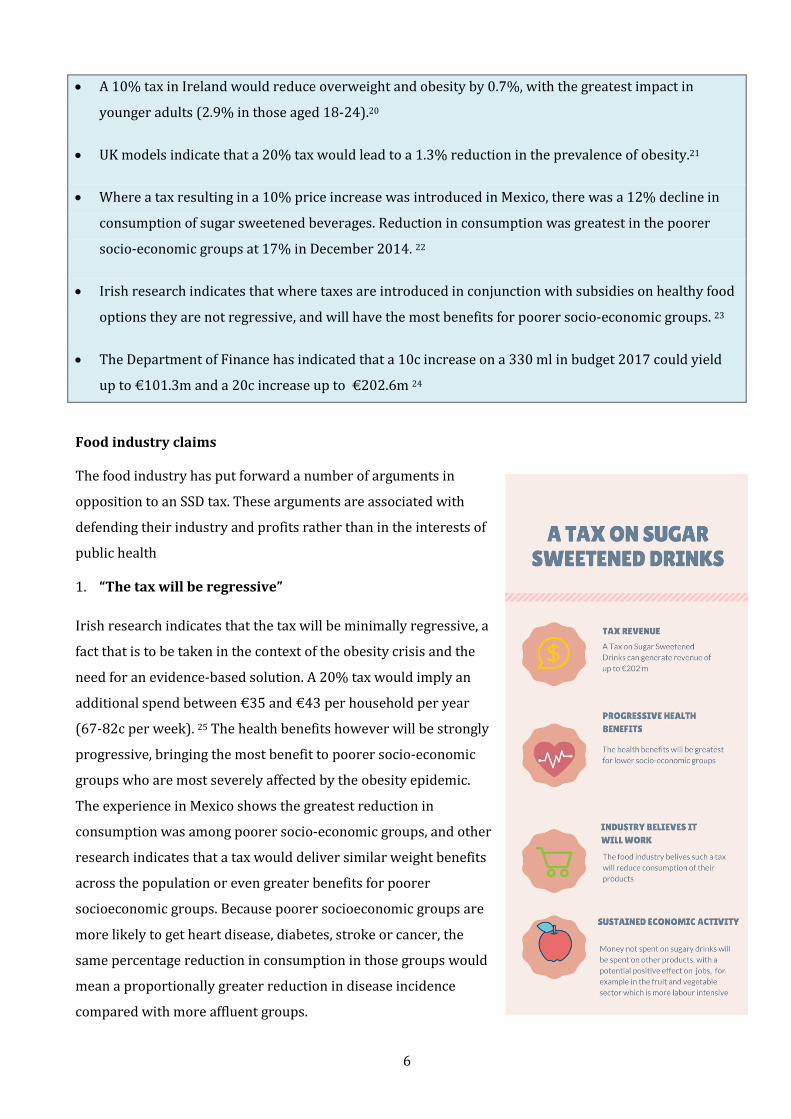

A 10% tax in Ireland would reduce overweight and obesity by 0.7%, with the greatest impact in

younger adults (2.9% in those aged 18-24).20

UK models indicate that a 20% tax would lead to a 1.3% reduction in the prevalence of obesity.21

Where a tax resulting in a 10% price increase was introduced in Mexico, there was a 12% decline in

consumption of sugar sweetened beverages. Reduction in consumption was greatest in the poorer

socio-economic groups at 17% in December 2014. 22

Irish research indicates that where taxes are introduced in conjunction with subsidies on healthy food

options they are not regressive, and will have the most benefits for poorer socio-economic groups. 23

The Department of Finance has indicated that a 10c increase on a 330 ml in budget 2017 could yield

up to €101.3m and a 20c increase up to €202.6m 24

Food industry claims

The food industry has put forward a number of arguments in

opposition to an SSD tax. These arguments are associated with

defending their industry and profits rather than in the interests of

public health

1. “The tax will be regressive”

Irish research indicates that the tax will be minimally regressive, a

fact that is to be taken in the context of the obesity crisis and the

need for an evidence-based solution. A 20% tax would imply an

additional spend between €35 and €43 per household per year

(67-82c per week). 25 The health benefits however will be strongly

progressive, bringing the most benefit to poorer socio-economic

groups who are most severely affected by the obesity epidemic.

The experience in Mexico shows the greatest reduction in

consumption was among poorer socio-economic groups, and other

research indicates that a tax would deliver similar weight benefits

across the population or even greater benefits for poorer

socioeconomic groups. Because poorer socioeconomic groups are

more likely to get heart disease, diabetes, stroke or cancer, the

same percentage reduction in consumption in those groups would

mean a proportionally greater reduction in disease incidence

compared with more affluent groups.

7

2. “The tax will make no difference to consumption.”

Evidence from countries where a tax has been introduced indicate that it works. In fact the food industry

has also stated that that it will lead to reduced sales in the sector which indicates that they believe a tax

will work.

3. “A tax on sugar sweetened drinks will not solve the obesity epidemic”

A multiplicity of measures is required to successfully address the various determinants of obesity. Some of

these include access and availability of affordable healthy food, safe exercise and leisure activity and

facilities, cultural and social norms, education and skills, genetic and biological factors as well as

individual lifestyle choices. A tax on sugar sweetened drinks is one of these measures, but it will be

successful as part as a comprehensive strategy which includes actions to address the multiple risk factors

of obesity.

4. “A tax will hit all consumers equally regardless of BMI or health status.”

Assessment of the impact of a tax on SSDs and pre-packaged sweetened products in Hungary found that in

the overweight or obese groups a greater proportion of people reduced their consumption of these

products when compared with those in the normal weight category. 26

5. “Jobs will be lost in the food and drinks sector.”

The industry seeks to raise concerns over job losses in the food and drinks sector as a result of the tax, but

this does not take into account that the money not spent on SSDs is likely to be spent on other goods so

that overall consumer spending remains constant. Research shows that an SSD tax combined with a

subsidy on fruit and vegetables may have a positive impact on jobs in that sector. 27

In summary, we believe that a tax on sugar sweetened drinks will be effective in reducing the obesity and

overweight epidemic crisis and we believe the industry objections are of either spurious or little

consequence in the face of the obesity epidemic.

8

Alcohol

The Royal College of Physicians of Ireland calls for adoption of the Public Health Alcohol

Bill introducing a Minimum Unit Price for Alcohol

We call for an increase in excise duties at least in line with inflation.

We call for introduction of a social responsibility levy on alcohol companies.

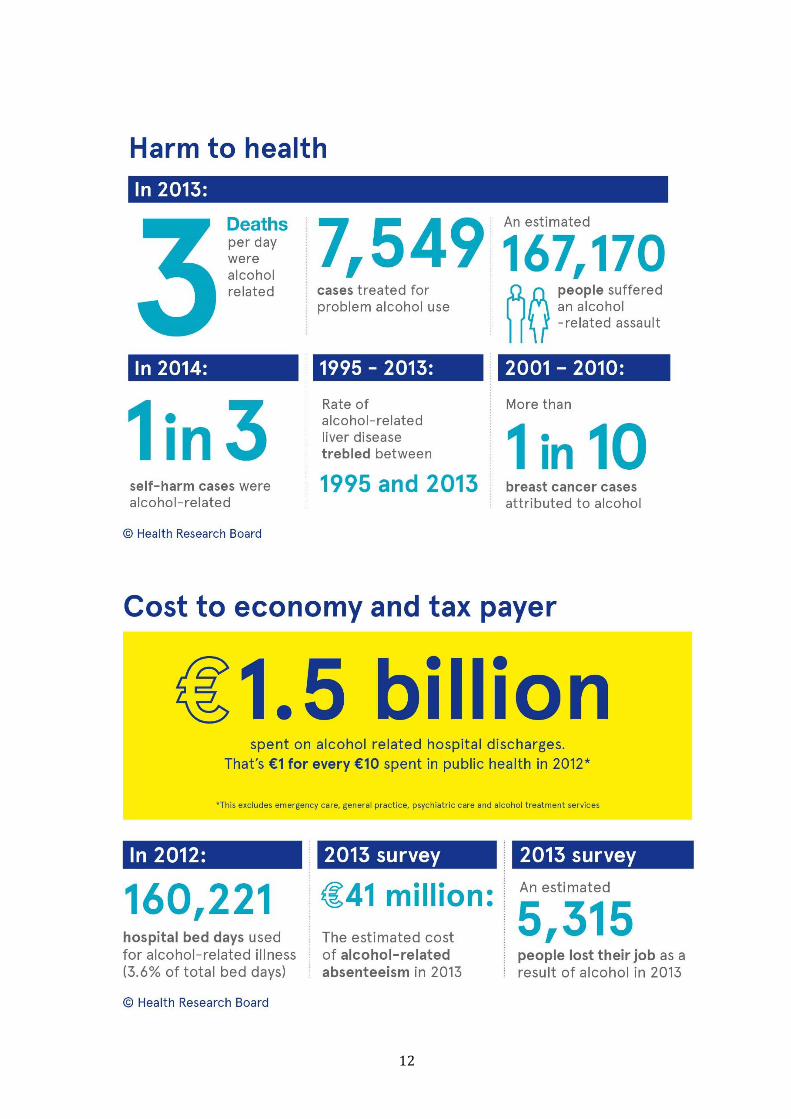

Every day 3 people die from alcohol. That's more than 1000 deaths per year. That equates to 6 or 7 large

aircraft crashing with no survivors, and is more than 7 times the number who die on Irish roads. This

crisis is worsening and the way we drink in Ireland is causing harm to every family and community and is

also putting enormous pressure on the health services. It contributes to high numbers of daily admissions

to accident and emergency departments as well as to the burden of disease and injuries in patients

admitted to hospitals all over Ireland.

Irish people continue to drink excessive amounts of alcohol often in a harmful pattern. Among the health

harms associated with this are increased rates of liver disease and cancer. Alcohol is associated with 900

new cancer cases in Ireland every year and 500 cancer deaths. At least half of all alcohol-related cancers

could be avoided by alcohol consumption within recommended limits.

If current consumption patterns continue, it is estimated that there will be a total of 230,000 people who

are alcohol dependent by 2021. 5

The Public Health Alcohol Bill was published in 2015 and contains a range of evidence-based measures

that target the pricing, availability and marketing of alcohol products – factors that are known to have the

greatest impact on harmful drinking. Adoption of this Bill will reduce alcohol consumption, will save lives

and reduce the unsustainable burden of alcohol on the health service.

Minimum Unit Pricing (MUP) is a targeted measure which will restrict the sale of the strongest and

cheapest alcohol in the off-trade and will reduce the cost to the state of alcohol-related harm. The

estimated effects of MUP have been modelled in the Irish context and suggest that MUP would reduce

consumption, alcohol related deaths, hospitalisations, crimes and workplace absences.

The same modelling also suggests that MUP would be far more effective than a ban on below cost selling.

We favour MUP over a ban on below cost selling as it targets the sale of the cheapest alcohol products,

which are the favoured drinks of the young drinker and the problem, dependent or addicted drinker.

Excise duties are used to deter consumption of alcohol products, and it has been shown that the effects of

price and tax changes on alcohol consumption are large in comparison with other prevention policies and

programmes. 28 Alcohol consumption is affected by the level of disposable income and if taxation is to be

effective then increases in tax need to keep pace with inflation.

9

A social responsibility levy on the alcohol industry was recommended by the steering group on a

National Substance Misuse Strategy in their 2012 report. 29 It was proposed that such a levy would

contribute to the cost of social marketing and awareness campaigns and would help fund sporting and

other events that provide alternatives to a drinking culture for young people. If MUP is introduced, a

social responsibility levy would also the State to capture some of the profit that may otherwise accrue to

industry.

Alcohol Action Ireland has estimated that a levy of just one cent per Irish standard drink (10 grammes of

alcohol) could generate over €30 million annually. 30 A levy would help to bridge any potential gap in

funding if the proposed ban on alcohol sponsorship in sport is introduced.

Key figures on alcohol-related harms

In 2014, Irish people drank on

average 11 litres per capita of pure

alcohol 2

4 in 10 people binge drink and

more than 1 in 5 binge drink at

least once a week.31

Every day in Ireland 3 people die as

a direct result of alcohol use. That

means more than 1000 deaths per

year. 2

The rate of alcoholic liver disease

trebled between 1995 and 2013. 2

In 2013, each day, 439 beds were occupied by people with a wholly alcohol-related condition.

Since 1995, the proportion of bed days occupied for alcohol related conditions has more than

doubled. 2

Alcohol was a factor in 38% of road traffic accidents between 2008 and 2012. 32

HRB 2014

10

Alcohol Price

In Finland alcohol tax cuts in 2004 were associated with a 17% increase in the number of sudden

deaths involving alcohol. 33

Alcohol has become much more affordable in Ireland in recent years. At current prices a woman

can reach her low risk weekly drinking limit for €6.30, while a man can reach his low risk limit for

less than €10. 34

Despite increases in excise duty in budgets 2013 and 2014, excise duty as a percentage of the price

of alcohol in the on-trade has decreased since 2003. 24

A 2016 determined that small increases in the price of alcohol, above inflation would substantially

reduce violence-related Emergency Department attendance in England and Wales.35

Another recent study that compared different alcohol taxation and price policies found that

Alcohol-content- based taxation and Minimum Unit Pricing target harmful drinking and would

lead to reductions in health inequalities across income groups. 36

A separate study examining taxation and minimum unit prices and their potential regressive

effects found regressive effects to be limited and found that MUP was more effective at reducing

consumption, especially for consumers in the lowest income group. 37

In Canada, a 10% increase in the MUP in Saskatchewan was associated with an 8.4% reduction in

consumption and after introduction of MUP in British Columbia, there was a reduction of 32% in

the number of alcohol related deaths within the first year. 38 39

The effect of an MUP ranging from 40c to 120c in Ireland has been modelled 40 and it estimated

that a €1 MUP would result in:

o Alcohol attributable deaths would reduce by 197 per year after 20 years.

o 5,878 fewer hospital admissions per year.

o Healthcare savings of €7.4m in year 1 and €254.7m over 20 years

o A fall in crime of 1,493 fewer offences per year and a reduction in costs of crime of €7m in

year 1 and €102.7m over 20 years.

o A total societal value for harm reductions for health, crime and workplace absence of

€1.7bn over 20 years.

A ban on below cost selling (implemented as a ban on selling alcohol for below the cost of duty

plus VAT) has also been modelled and is estimated to have a negligible impact on alcohol

consumption or related harms.40

11

Alcohol industry claims

There are a number of common claims made by the alcohol industry to argue against action on alcohol

pricing which are not made in the interest of public health

1. “Higher taxes will hurt the economy and result in reduced employment”

Past experience shows the industry passes on more than 100% of excise duty increases to drinkers. Excise

duty increases in budget 2013 saw the price of a pint of stout increase by 18c, double the increase in

excise duty that year.24 In this way the industry compensates for lost revenue and maintains its profits.

The alcohol industry chooses to ignore the fact that money not spent on alcohol is likely to be spent on

other goods and services, supporting jobs in other sectors. In addition, excise duties raise revenue for the

exchequer to spend on services or investment in the economy to create new jobs. An increase in excise of

10c on Beer, spirits and cider in Budget 2017 would raise over €100m. Conversely, a reduction in excise

on a bottle of wine of 50c would result in a €33m loss to the exchequer.24

Decreases in alcohol consumption resulting from increased excise duties will save the Government money

in healthcare costs, crime, lost productivity and other alcohol-related costs.

2. “Reducing excise duties will offer a better deal to the consumer”

As mentioned above, there is less than 100% pass through of excise duty changes in Ireland to the

consumer. 41 This means that in the case of a reduction in excise duties, industry usually benefits to a

greater degree than the consumer, while the state and its citizens pick up the bill for the alcohol harm.

3. “High excise duties hurt tourism”

This is not borne out by past experience. In 2013 and 2014, excise duties on alcohol were increased. At the

same time, 2013 and 2014 saw successive increases in overseas tourist visits to Ireland with a growth of

6% in 2013 and a further 6% in 2014. This included growth in the numbers visiting from Britain (4%in

2013 and 4.7% in 2014). 42 43

What will be achieved by increases in excise duties and introduction of MUP is a reduction in deaths from

alcohol-related conditions, less hospitals beds occupied on a daily basis because of alcohol and a reduction

in the cost of alcohol harm to the state.

The alcohol industry continues to increase profits year on year.44 45 46 The sector remains highly profitable

and any argument from the drinks industry that portrays it as an industry struggling in the face of high

excise duties is simply not based on fact.

12

13

Tobacco

The Royal College of Physicians of Ireland recommends a minimum of a 50 cents increase on a

packet of 20 cigarettes and a proportionate increase on related products on an annual basis.

We recommend a reduction of the price differential between roll your own products (RYO) and

cigarettes is also a priority.

We recommend introduction of an environmental levy on tobacco packs.

We recommend removal/reduction of VAT on nicotine replacement patches.

We recommend iintroduction of price cap regulation or a levy on tobacco industry profits.

Smoking continues to be a major health hazard in Ireland. Tobacco Free Ireland 2013 set a target of

reducing the smoking prevalence rate to less than 5% by the year 2025. Figures published in 2016

showing the substantial economic impact of smoking illustrate more than ever the need to achieve this

reduction. 1 Excise duty is a key tool to achieve further reductions in smoking prevalence. A reduction of

the price differential between roll your own products (RYO) and cigarettes is also necessary.

In previous pre-budget submissions RCPI has recommended increases in excise duty, an environmental

levy on tobacco packs, removal of VAT on Nicotine Replacement Patches, and price cap regulation on

tobacco industry products. We call again for the introduction of these measures in budget 2017.

Environmental levy on tobacco packs

Tobacco waste is our biggest urban waste issue according to the Department of the Environment. The cost

of smoking related littering is estimated at €69 million.1 Thus the introduction of a levy on tobacco packs

will help to balance this economic cost.

Removal of Vat on Nicotine patches

Ireland’s VAT rate of 23% on nicotine patches is too high, and it should be reduced or removed as an

initiative to encourage smokers to quit smoking. The current VAT level on nicotine patches in the UK are

5% and the Minister for Finance should still consider lowering VAT on nicotine patches to the lowest

possible level.

Price Cap regulation

Price cap regulation or a levy on the tobacco industry profits has been proposed by the Irish Heart

Foundation and the Irish Cancer Society, and was included in the Department of Health’s Tobacco Free

Ireland Action plan.47 48 49 This regulation would set a maximum price that tobacco companies can charge

for their product. The price would be based on an assessment of the genuine costs each firm faces in its

operations, and an assumption about the efficiency savings it would be expected to make. This would

ensure that the tobacco industry’s excess profits are transferred to government revenues that can be used

14

to fund smoking cessation services. The Government can ensure that the tobacco industry properly

contributes to the costs it imposes on the State and on its citizens.

The economic cost of smoking in Ireland in 2013.1

5950 deaths attributed to smoking and exposure to second hand smoke.

200,000 hospital episodes

Total Health Service cost of €460m

Cost of lost productivity over €1bn

Cost of smoking related littering €69m

15

Physical Activity

The Royal College of Physicians of Ireland calls on the Government to fully support and resource

the National Physical Activity Plan.

In Ireland, physical inactivity is responsible for 8.8% of the disease burden from coronary heart disease;

10.9% of type 2 diabetes; 15.2% of breast cancers and 15.7% of colon cancers. 50 In the case of all of these

major diseases, Irish statistics are worse than both European and global averages.

Regular physical activity has appropriately been described a ‘wonder drug’ and offers health

improvements far greater than for many drugs. Despite this, neither the adult nor child population in

Ireland are active enough. Two thirds of adults to not meet national physical activity guidelines; 1 in 10

adults are sedentary. 4

The National Physical Activity Plan was published in 2016 and should be supported, resourced and fully

implemented.

16

References

1 ICF International (2016) An assessment of the economic cost of smoking in Ireland.

2 Mongan, D and Long J (2016) HRB Overview Series. Alcohol in Ireland: consumption, harm, cost and

policy response. Dublin Health Research Board

3 Safefood (2012). The cost of overweight and obesity on the island of Ireland. Safefood; 2012.

4 Department of Health and Department of Transport, Tourism and Sport (2016) Get Ireland Active-

National Physical Activity Plan for Ireland.

5 HSE (2016) Planning for Health: Trends and Priorities to Inform Health Service Planning.

6 World Health Organisation (2004). Global Strategy on diet, physical activity and health. WHO,

Geneva.

7 RCPI Policy Group on Obesity (2013). The Race We Don’t want to win. Royal College of Physicians of

Ireland, Dublin.

8 NCD Risk Factor Collaboration. Country Profile: Ireland. www.ncdrisc.org/country-profile.html

9 Heinen M et al (2014) The Childhood Obesity Surveillance Initiative (COSI) in the Republic of Ireland:

Findings from 2008, 2010 and 2012. Health Service Executive, Dublin.

10 Ipsos MRBI nationwide poll of 1,008 adults for the Irish Heart Foundation, May 2014. See

http://www.irishheart.ie/iopen24/irish‐public‐supports‐sugary‐drink‐obesity‐rate‐n‐467.html

11 Government of Ireland (2016) Programme for Partnership Government.

http://www.merrionstreet.ie/merrionstreet/en/imagelibrary/programme_for_partnership_government.

12 Te Morenga L.A., Mallard S., and Mann J. (2013) Dietary sugars and body weight: systematic review

and meta-analyses of randomised controlled trials and cohort studies. BMJ 15;346:e7492.

13 InterAct consortium (2013). Consumption of sweet beverages and type 2 diabetes incidence in

European adults: results from EPIC-InterAct. Diabetologia 56 (7), 1520–1530.

14 De Boer M.D., Scharf R.J., and Demmer R.T. (2013) Sugar-Sweetened Beverages and Weight Gain in

2- to 5- Year-Old Children. Pediatrics 133 (3), 413 - 420.

15 Malik V.S., Pan A., Willett W.C., and Hu F.B. (2013) Sugar-sweetened beverages and weight gain in

children and adults: a systematic review and meta-analysis. American Journal of Clinical nutrition

2013 98 (4), 1084 – 1102.

16 Qi, Q et al. (2012). Sugar-Sweetened Beverages and Genetic Risk of Obesity. N. Engl. J. Med. 367,

1387–1396. doi:10.1056/NEJMoa1203039.

17 Woodward-Lopez G. (2011) To what extent have sweetened beverages contributed to the obesity

epidemic? Public Health Nutrition 14 (3), 499-509

17

18 Imamura F. et al. Consumption of sugar sweetened beverages, artificially sweetened beverages, and

fruit juice and incidence of type 2 diabetes: systematic review, meta-analysis, and estimation of

population attributable fraction. BMJ 2015;351:h3576

19 Committee on Nutrition and the Council on Sports Medicine and Fitness (2011) Sports drinks and

energy drinks for children and adolescents: are they appropriate? Pediatrics 127 (6), 1182–9.

20 Briggs AD, Mytton OT, Madden D, O Shea D, Rayner M, Scarborough P. The potential impact on obesity

of a 10% tax on sugar-sweetened beverages in Ireland, an effect assessment modelling study. BMC Public

Health. 2013 Sep 17;13(1):860.

21 Briggs ADM, Mytton OT, Kehlbacher A, Tiffin R, Rayner M, Scarborough P. Overall and income specific

e-ect on prevalence of overweight and obesity of 20% sugar sweetened drink tax in UK: econometric and

comparative risk assessment modelling study. BMJ. 2013;347:f6189.

22 Colchero M Arantxa, Popkin Barry M, Rivera Juan A, Ng Shu Wen. Beverage purchases from stores in

Mexico under the excise tax on sugar sweetened beverages: observational study BMJ 2016; 352 :h6704

23 Madden D. The Poverty Effects of a “Fat-Tax” In Ireland. Health Econ. 2013 Oct 17.

24 Department of Finance Tax Strategy Group (2016). General Excise Paper- Tobacco products Tax,

Alcohol Products Tax and Tax on Sugar-Sweetened Drinks.

http://www.finance.gov.ie/sites/default/files/160720%20TSG%201602%20General%20Excises%20TS

G%202016.pdf

25 Collins, M. Presentation at Irish Heart Foundation Seminar ‘20% Tax on Sugar Sweetened Drinks’.

Monday 23rd June 2014. The Gibson Hotel. Dublin 1

26 Martos, E, (2015). The Hungarian policies to reduce population sugar intake. Presentation, European

Public Health Conference 14-17 October 2015

https://eupha.org/repository/sections/fn/Eva_Martos_Sugar_in_Hungary_Milan_2015.pdf

27 Madden, D (2013) Presentation ‘Food, Fat and Fiscal Measures’.

Irish Heart Foundation Seminar, 20th March 2013. Presentation available at:

http://www.irishheart.ie/media/pub/foot_fat_and_fiscal_measures__some_observations__david_madden.

28 RCPI Pre-budget Submission 2014. Royal College of Physicians, Dublin

29 DoH (2012) Steering Group Report on a National Substance Misuse Strategy. Department

of Health and Children, Dublin.

30 http://alcoholireland.ie/download/publications/Pre%20Budget%20Submission%20Summary.pdf

31 Healthy Ireland Survey 2015. Summary of Findings.

32 Fatal Collisions 2008-2012 Alcohol as a Factor. Road Safety Authority.

33 Koski A, Sire´n R, Vuori E, et al. Alcohol tax cuts and increase in alcohol-positive sudden

deaths: a time-series intervention analysis. Addiction 2007;102:362–8

18

34 http://alcoholireland.ie/facts/price-and-availability/#

35 Page N, Sivarajasingam V, Matthews K, Heravi S, Morgan P, Shepherd J.Preventing violence-related

injuries in England and Wales: a panel studyexamining the impact of on-trade and off-trade alcohol prices.

Inj Prev. 2016 Jul11. pii: injuryprev-2015-041884.

36 Meier PS, Holmes J, Angus C, Ally AK, Meng Y, Brennan A. Estimated Effects of Different Alcohol Taxation

and Price Policies on Health Inequalities: AMathematical Modelling Study. PLoS Med. 2016 Feb 23;13(2)

37 Vandenberg B, Sharma A. Are Alcohol Taxation and Pricing Policies Regressive? Product-Level Effects of

a Specific Tax and a Minimum Unit Price for Alcohol. Alcohol Alcohol. 2016 Jul;51(4):493-502.

38 Zhao et al (2013) The relationship between changes to minimum alcohol prices, outlet

densities and alcohol attributable deaths in British Columbia in 2002-2009. Addiction, 108:

doi: 10.1111/add.12139

39 Zhao et al (2012) The raising of minimum alcohol prices in Saskatchewan, Canada:

impacts on consumption and implications for public health. Stockwell. American Journal of

Public Health: 2012, 102(12), p. e103–e110.

40 Angus, Colin and Meng, Yang and Ally, Abdallah and Holmes, John and Brennan, Alan . (2014) Model-

based appraisal of minimum unit pricing for alcohol in the Republic of Ireland. ScHARR, University of

Sheffield.

41 Rabinovich, L et al (2012). Further study on the affordability of alcoholic beverages in the EU: A focus on

excise duty pass-through, on- and off-trade sales, price promotions and statutory regulations. Santa

Monica, CA: RAND Corporation, 2012. http://www.rand.org/pubs/technical_reports/TR1203.html.

42

http://www.failteireland.ie/FailteIreland/media/WebsiteStructure/Documents/3_Research_Insights/3_

General_SurveysReports/Tourism-facts-2014.pdf

43

http://www.failteireland.ie/FailteIreland/media/WebsiteStructure/Documents/3_Research_Insights/3_

General_SurveysReports/Tourism-facts-2013.pdf?ext=.pdf

44 http://www.irishtimes.com/business/agribusiness-and-food/diageo-reports-stronger-first-half-profit-

as-it-gains-in-europe-1.2513690

45 http://www.ibec.ie/IBEC/Press/PressPublicationsdoclib3.nsf/vPages/Newsroom~irish-brewers-

association-release-irish-beer-2015'-report-23-08-2016?OpenDocument?OpenDocument#.V8AdNvkrKUk

46 http://www.reuters.com/article/heineken-nl-results-idUSL8N12S17Z20151028

47 Irish Heart Foundation and Irish Cancer Society (2013) Pre-Budget Submission 2014.

48 Pre-Budget Submission (2016)- Tobacco Profits Levy &Tobacco Taxation. Irish Cancer Society and the

Irish Heart Foundation

49

https://www.hse.ie/eng/about/Who/TobaccoControl/framework/Tobacco_free_Ireland_Action_plan.pdf

19

50 Lee, I.-M., Shiroma, E. J., Lobelo, F., Puska, P., Blair, S. N., & Katzmarzyk, P. T. (2012). Impact of Physical

Inactivity on the World’s Major Non-Communicable Diseases. Lancet, 380(9838), 219–229.