Embed Size (px)

Citation preview

PrairieProvidentResourcesInc.

ConsolidatedFinancialStatements

AsatandfortheYearEndedDecember31,2020

Dated:March25,2021

INDEPENDENTAUDITOR’SREPORT

TotheShareholdersofPrairieProvidentResourcesInc.

Opinion

WehaveauditedtheconsolidatedfinancialstatementsofPrairieProvidentResourcesInc.anditssubsidiaries(the”Company”),which comprise the consolidated statements of financial position as at December 31, 2020 and 2019, and the consolidatedstatementsoflossandcomprehensiveloss,consolidatedstatementsofchangesinequity(deficit)andconsolidatedstatementsofcashflowsfortheyearsthenended,andnotestotheconsolidatedfinancialstatements,includingasummaryofsignificantaccountingpolicies.

In our opinion, the accompanying consolidated financial statements present fairly, in allmaterial respects, the consolidatedfinancial position of the Company as at December 31, 2020 and 2019, and its consolidated financial performance and itsconsolidatedcashflowsfortheyearsthenendedinaccordancewithInternationalFinancialReportingStandards(“IFRS”).

BasisforOpinion

Weconductedouraudit inaccordancewithCanadiangenerallyacceptedauditingstandards.OurresponsibilitiesunderthosestandardsarefurtherdescribedintheAuditor’sResponsibilitiesfortheAuditoftheConsolidatedFinancialStatementssectionofourreport.WeareindependentoftheCompanyinaccordancewiththeethicalrequirementsthatarerelevanttoourauditoftheconsolidatedfinancialstatementsinCanada,andwehavefulfilledourotherethicalresponsibilitiesinaccordancewiththeserequirements.Webelieve that the audit evidencewehaveobtained is sufficient and appropriate to provide a basis for ouropinion.

KeyAuditMatters

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of theconsolidated financial statements of the current period. This matter was addressed in the context of our audit of theconsolidatedfinancialstatementsasawhole,andinformingouropinionthereon,andwedonotprovideaseparateopiniononthismatter.Forthematterbelow,ourdescriptionofhowourauditaddressedthematterisprovidedinthatcontext.

We have fulfilled the responsibilities described in the Auditor’s responsibilities for the audit of the consolidated financialstatements section of our report, including in relation to this matter. Accordingly, our audit included the performance ofprocedures designed to respond to our assessment of the risks of material misstatement of the consolidated financialstatements.Theresultsofourauditprocedures,includingtheproceduresperformedtoaddressthematterbelow,providethebasisforourauditopinionontheaccompanyingconsolidatedfinancialstatements.

Keyauditmatter Howourauditaddressedthekeyauditmatter

Impairmentofpropertyandequipment.

AsatDecember31,2020,thecarryingamountofpropertyandequipmentwas$189.1million.FortheyearendedDecember31,2020,animpairmentlossof$78.3millionwasrecordedwithrespecttopropertyandequipment.TheCompany’sdisclosuresrelatedtopropertyandequipmentandrelatedimpairmentareincludedinNote2(d)UseofEstimatesandJudgments,Note3SignificantAccountingPoliciesandChangesinAccountingPoliciesandNote7PropertyandEquipment.Propertyandequipmentistestedforimpairmentonlywhencircumstancesindicatethatthecarryingamountofacashgeneratingunit(‘CGU’)mayexceeditsrecoverableamount.TherecoverableamountsofallCGUsweredeterminedatMarch31,2020usingthefairvaluelesscostofdisposalmethod.

AuditingtheCompany’sestimatedrecoverableamountsforallCGUswascomplexduetothesubjectivenatureoftheunderlyinginputsandassumptions.Theprimaryinputsnotedinthefairvaluelesscostofdisposalmodelwere

TotesttheCompany'sestimatedrecoverableamount,weperformedthefollowingprocedures,amongothers:

• EvaluatedtheCompany’sindependentreserveevaluator’scompetence,capabilityandobjectivityaswellasobtainedanunderstandingoftheworktheyperformed.Theappropriatenessoftheirworkasauditevidencewasevaluatedbyconsideringtherelevanceandreasonablenessofthemethodsandassumptionsutilized.

• Involvedourinternalvaluationspecialiststoassessthemethodologyapplied,andthevariousinputsutilizedindeterminingtheafter-taxdiscountratebyreferencingcurrentindustry,economic,andcomparablecompanyinformation,aswellascompanyandcash-flowspecificriskpremiums.

• Comparedforecastedbenchmarkcommoditypricingagainsthistoricalrealizedpricesandtootherthird-partypriceforecasts.

forecastedproduction,pricing,royalties,operatingcosts,futuredevelopmentcostsandanafter-taxdiscountrate.

• Assessed forecasted production, royalties, operatingcosts,andfuturedevelopmentcostsbycomparingthemtohistoricalresults.

• Evaluated the adequacy of the impairment notedisclosure included in Note 7 of the accompanyingconsolidated financial statements in relation to thismatter.

OtherInformation

Managementisresponsiblefortheotherinformation.TheotherinformationcomprisesManagement’sDiscussionandAnalysis.

Ouropinionontheconsolidatedfinancialstatementsdoesnotcovertheotherinformationandwedonotexpressanyformofassuranceconclusionthereon.

Inconnectionwithourauditoftheconsolidatedfinancialstatements,ourresponsibilityistoreadtheotherinformation,andindoingso,considerwhethertheother information ismaterially inconsistentwiththeconsolidatedfinancialstatementsorourknowledgeobtainedintheauditorotherwiseappearstobemateriallymisstated.

WeobtainedManagement’sDiscussionandAnalysispriortothedateofthisauditor’sreport. If,basedontheworkwehaveperformed,weconcludethatthereisamaterialmisstatementofthisotherinformation,wearerequiredtoreportthatfact.Wehavenothingtoreportinthisregard.

ResponsibilitiesofManagementandThoseChargedwithGovernancefortheConsolidatedFinancialStatements

Management is responsible for thepreparationand fairpresentationof the consolidated financial statements in accordancewith IFRS, and for such internal control asmanagement determines is necessary to enable the preparation of consolidatedfinancialstatementsthatarefreefrommaterialmisstatement,whetherduetofraudorerror.

Inpreparingtheconsolidatedfinancialstatements,managementisresponsibleforassessingtheCompany’sabilitytocontinueasagoingconcern,disclosing,asapplicable,mattersrelatedtogoingconcernandusingthegoingconcernbasisofaccountingunlessmanagementeitherintendstoliquidatetheCompanyortoceaseoperations,orhasnorealisticalternativebuttodoso.

ThosechargedwithgovernanceareresponsibleforoverseeingtheCompany’sfinancialreportingprocess.

Auditor’sResponsibilitiesfortheAuditoftheConsolidatedFinancialStatements

Ourobjectives are toobtain reasonable assurance aboutwhether the consolidated financial statements as awhole are freefrom material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion.Reasonableassuranceisahighlevelofassurance,butisnotaguaranteethatanauditconductedinaccordancewithCanadiangenerallyacceptedauditingstandardswillalwaysdetectamaterialmisstatementwhenitexists.Misstatementscanarisefromfraudorerrorandareconsideredmaterial if, individuallyorintheaggregate,theycouldreasonablybeexpectedtoinfluencetheeconomicdecisionsofuserstakenonthebasisoftheseconsolidatedfinancialstatements.

AspartofanauditinaccordancewithCanadiangenerallyacceptedauditingstandards,weexerciseprofessionaljudgmentandmaintainprofessionalskepticismthroughouttheaudit.Wealso:

• Identifyandassesstherisksofmaterialmisstatementoftheconsolidatedfinancialstatements,whetherduetofraudorerror,designandperformauditproceduresresponsivetothoserisks,andobtainauditevidencethatissufficientandappropriatetoprovideabasisforouropinion.Theriskofnotdetectingamaterialmisstatementresultingfromfraudishigher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions,misrepresentations,ortheoverrideofinternalcontrol.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that areappropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of theCompany’sinternalcontrol.

• Evaluatetheappropriatenessofaccountingpoliciesusedandthereasonablenessofaccountingestimatesandrelateddisclosuresmadebymanagement.

• Concludeon theappropriatenessofmanagement’suseof thegoing concernbasisof accountingand,basedon theauditevidenceobtained,whetheramaterialuncertaintyexistsrelatedtoeventsorconditionsthatmaycastsignificant

doubtontheCompany’sabilitytocontinueasagoingconcern.Ifweconcludethatamaterialuncertaintyexists,wearerequiredtodrawattentioninourauditor’sreporttotherelateddisclosuresintheconsolidatedfinancialstatementsor,ifsuchdisclosuresareinadequate,tomodifyouropinion.Ourconclusionsarebasedontheauditevidenceobtaineduptothedateofourauditor’sreport.However,futureeventsorconditionsmaycausetheCompanytoceasetocontinueasagoingconcern.

• Evaluate the overall presentation, structure and content of the consolidated financial statements, including thedisclosures,andwhethertheconsolidatedfinancialstatementsrepresenttheunderlyingtransactionsandeventsinamannerthatachievesfairpresentation.

Wecommunicatewiththosechargedwithgovernanceregarding,amongothermatters, theplannedscopeandtimingoftheauditandsignificantauditfindings,includinganysignificantdeficienciesininternalcontrolthatweidentifyduringouraudit.

Wealsoprovidethosechargedwithgovernancewithastatementthatwehavecompliedwithrelevantethical requirementsregardingindependence,andtocommunicatewiththemallrelationshipsandothermattersthatmayreasonablybethoughttobearonourindependence,andwhereapplicable,relatedsafeguards.

From the matters communicated with those charged with governance, we determine those matters that were of mostsignificanceintheauditoftheconsolidatedfinancialstatementsofthecurrentperiodandarethereforethekeyauditmatters.We describe thesematters in our auditor’s report unless law or regulation precludes public disclosure about thematter orwhen, inextremely rarecircumstances,wedetermine thatamatter shouldnotbecommunicated inour reportbecause theadverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of suchcommunication.

Theengagementpartnerontheauditresultinginthisindependentauditor’sreportisKimWiggins.

Calgary,Alberta March25,2021

CONSOLIDATEDSTATEMENTSOFFINANCIALPOSITIONAsat($000s) Note

December31,2020

December31,2019

ASSETS

Cash 4,544 2,873

Restrictedcash 9 4,332 4,917

Accountsreceivable 21 7,875 8,667

Inventory 604 958

Prepaidexpensesandotherassets 2,654 3,282

Derivativeinstruments–current 21 798 11

Totalcurrentassets 20,807 20,708

Explorationandevaluation 6 5,785 10,183

Propertyandequipment 7 189,142 293,549

Right-of-useassets 8 3,948 6,119

Derivativeinstruments 21 — 332

Otherassets 634 634

Totalassets 220,316 331,525

LIABILITIES

Accountspayableandaccruedliabilities 14,683 18,479

Leaseliabilities–currentportion 11 2,548 2,520

Derivativeinstruments–current 21 — 4,325

Currentportionofdecommissioningliability 12 3,500 4,000

Warrantliability 10 686 84

Totalcurrentliabilities 21,417 29,408

Long-termdebt 9 103,071 113,595

Leaseliabilities–non-currentportion 11 2,606 5,121

Decommissioningliabilities 12 162,726 163,805

Otherliabilities 7,406 6,018

Totalliabilities 297,226 317,947

Commitmentsandcontingencies 23

SHAREHOLDERS’EQUITY

Sharecapital 13 136,534 135,958

Warrants 13 — 1,103

Contributedsurplus 3,662 2,919

Accumulateddeficit (217,645) (126,872)

Accumulatedothercomprehensiveincome(“AOCI”) 539 470

Totalequity (76,910) 13,578

Totalliabilitiesandshareholders’equity 220,316 331,525

Seeaccompanyingnotestotheconsolidatedfinancialstatements.

ApprovedbytheBoardofDirectors,

(signed)(signed)PatrickMcDonaldAjaySabherwalChairoftheBoardofDirectorsandDirectorChairoftheAuditCommitteeandDirector

5|Page

PrairieProvidentResourcesInc.

CONSOLIDATEDSTATEMENTSOFLOSSANDCOMPREHENSIVELOSSFortheyearsended

($000s) Note December31,2020 December31,2019

REVENUE

Oilandnaturalgasrevenue 17 51,720 97,891

Royalties (5,027) (10,086)

Oilandnaturalgasrevenue,netofroyalties 46,693 87,805

Unrealizedgain(loss)onderivativeinstruments 21 4,780 (10,618)

Realizedgain(loss)onderivativeinstruments 21 15,241 (2,169)

66,714 75,018

Otherincome 327 —

EXPENSES

Operating 18 37,271 46,626

Generalandadministrative 19 5,742 8,277

Depletionanddepreciation 7 27,887 39,826

Explorationandevaluation 6 4,183 996

Depreciationonright-of-useassets 8 2,170 2,743

Gainonpropertydispositions 5 (375) (263)

Loss(gain)onwarrantliability 10 260 (726)

Gainonmodificationoffinancialliabilities 9 (15,874) —

Impairmentloss(recovery) 6,7 78,459 (436)

Gainonforeignexchange (1,425) (3,826)

Changeinotherliabilities 1,361 (3,283)

Financecosts 20 17,995 17,588

Transaction,restructuringandothercosts 238 888

Totalexpenses–net 157,892 108,410

Netlossbeforetaxes (90,851) (33,392)

Currenttax(recovery)expense (78) 19

Deferredtaxrecovery — (332)

Nettaxrecovery 15 (78) (313)

Netloss (90,773) (33,079)

Othercomprehensiveincome(loss)

Itemsthatmaybereclassifiedtonetloss:

Foreigncurrencytranslationadjustment 160 —

Itemsthatwillnotbereclassifiedtonetloss:

Actuarial(loss)gainonemployeepost-retirementbenefitplan (91) 2

Totalothercomprehensiveincome(loss) 69 2

Comprehensiveloss (90,704) (33,077)

Netlosspershare

Basic&Diluted 13 (0.53) (0.19)

Seeaccompanyingnotestotheconsolidatedfinancialstatements.

6|Page

PrairieProvidentResourcesInc.

CONSOLIDATEDSTATEMENTSOFCHANGESINEQUITY(DEFICIT)

($000s) Note

ShareCapitalAmount Warrants

ContributedSurplus

AccumulatedDeficit AOCI

TotalEquity

BalanceatDecember31,2019 135,958 1,103 2,919 (126,872) 470 13,578

Shareissuancecosts 13 4 — — — — 4

Share-basedcompensation 14 — — 240 — — 240

Settlementofrestrictedshareunits(“RSU”),netofwithholdingtax 13 572 — (600) — — (28)

Actuariallossonpost-retirementbenefitplan — — — — (91) (91)

Warrantexpiries 13 — (1,103) 1,103 — — —

Exchangedifferencesontranslationofforeignoperations — — — — 160 160

Netloss — — — (90,773) — (90,773)

BalanceatDecember31,2020 136,534 — 3,662 (217,645) — 539 (76,910)

($000s) Note

ShareCapitalAmount Warrants

ContributedSurplus

AccumulatedDeficit AOCI

TotalEquity

BalanceatDecember31,2018 136,145 1,440 1,859 (92,861) 468 47,051

ImpactontransitiontoIFRS16 — — — (853) — (853)

BalanceatJanuary1,2019 136,145 1,440 1,859 (93,714) 468 46,198

Shareissuancecosts (57) — — — — (57)

Normalcourseissuerbid(“NCIB”) (509) — 377 — (132)

Share-basedcompensation — — 825 — — 825

Settlementofrestrictedshareunits(“RSU”)andperformanceshareunits("PSU"),netofwithholdingtax 405 — (479) — — (74)PurchaseofcommonsharesforRSUsettlement (26) — — — — (26)Actuarialgainonpost-retirmentbenefitplan — — — — 2 2

Warrantexpiries — (337) 337 — — —

IFRS16impact — — — (79) — (79)

Netloss — — — (33,079) — (33,079)

BalanceatDecember31,2019 135,958 1,103 2,919 (126,872) 470 13,578

Seeaccompanyingnotestotheconsolidatedfinancialstatements.

7|Page

PrairieProvidentResourcesInc.

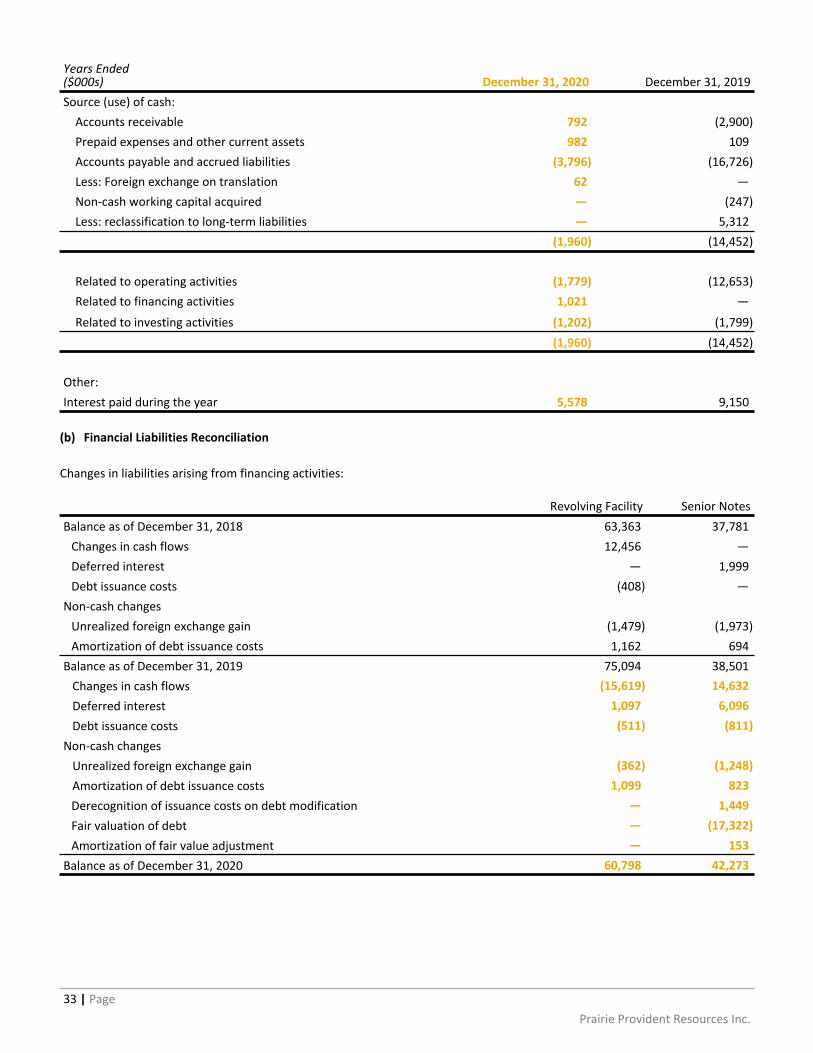

CONSOLIDATEDSTATEMENTSOFCASHFLOWSFortheyearsended($000s) Note December31,2020 December31,2019OPERATINGACTIVITIESNetloss (90,773) (33,079)Adjustmentsfornon-cashitems:Impairmentloss(recovery) 6,7 78,459 (436)Gainonmodificationoffinancialliabilities-net 9 (15,874) —Unrealized(gain)lossonderivativeinstruments 21 (4,780) 10,618Depletionanddepreciation 7 27,887 39,826Depreciationonright-of-useasset 8 2,170 2,743Explorationandevaluationexpense 6 4,183 996Accretionandnon-cashfinancecosts 20 5,520 6,244Unrealizedforeignexchangegain (1,512) (3,624)Changeinotherliabilities (480) (3,283)Gainonsaleofproperties 5 (375) (263)Loss(gain)onwarrantliability 10 260 (726)Deferredtaxrecovery 15 — (332)Share-basedcompensation 14 225 679

Settlementsofdecommissioningliabilities 12 (1,869) (3,801)DeferredinterestonSeniorNotes&RevolvingFacility 9,20 7,193 1,999Other,net 1,727 (528)Changeinnon-cashworkingcapital 16 (1,779) (12,653)Netcashfromoperatingactivities 10,182 4,380FINANCINGACTIVITIESDebtissuancecosts (980) (408)Shareissuancecosts 4 (57)PurchaseofcommonshareunderNCIB — (133)PurchaseofcommonshareforRSUsettlement — (26)Withholdingtaxesonsettlementofshare-basedcompensations 13 (28) (60)Repaymentofprincipalrelatedtoleaseobligations 11 (3,144) (3,803)ChangeinSeniorNoteborrowings 14,632 —ChangeinRevolvingFacilityborrowings 9 (15,619) 12,456Changeinnon-cashworkingcapital 16 1,021 —

Netcashfromfinancingactivities (4,114) 7,969INVESTINGACTIVITIESExplorationandevaluationexpenditures 6 (271) (2,678)Propertyandequipmentexpenditures 7 (3,758) (9,317)Proceedsfromdispositions(netofacquisitions) 249 285Changeinnon-cashworkingcapital 16 (1,202) (1,799)

Netcashusedininvestingactivities (4,982) (13,509)Changeincashandrestrictedcash 1,086 (1,160)Cashandrestrictedcashbeginningofperiod 7,790 8,950Cashandrestrictedcashendofperiod 8,876 7,790

Seeaccompanyingnotestoconsolidatedfinancialstatements.

8|Page

PrairieProvidentResourcesInc.

NOTESTOTHECONSOLIDATEDFINANCIALSTATEMENTS

FortheyearsendedDecember31,2020and2019

1. REPORTINGENTITY

PrairieProvidentResourcesInc.(“PPR”orthe“Company”)wasincorporatedunderthelawsoftheprovinceofAlbertaonJuly29,2016.Itsprincipalofficeislocatedat640–5thAvenueS.W.,Calgary,Alberta.TheCompany’scommonsharesarelistedontheTorontoStockExchangeunderthesymbol“PPR”.

PPR is an independent oil and natural gas exploration, development and production company. PPR’s reserves, producingproperties and exploration prospects are located primarily in the province of Alberta. The Company conducts certain of itsoperatingactivitiesjointlywithothersthroughunincorporatedjointarrangementsandtheseconsolidatedfinancialstatementsreflectonlytheCompany’sshareofassets,liabilities,revenuesandexpensesunderthesearrangements.TheCompanyconductsallofitsprincipalbusinessinonereportablesegment.

2. BASISOFPRESENTATION

(a) StatementofCompliance

These annual financial statements have been prepared in accordance with IFRS as issued by the International AccountingStandards Board (“IASB”). The Company’s significant accounting policies under IFRS are presented in Note 3. The annualfinancialstatementswereapprovedandauthorizedforissuebytheBoardofDirectorsofPPRonMarch25,2021(the“FinancialStatements”).

Certaincomparativefigureshavebeenreclassifiedtoconfirmwiththepresentationadoptedinthecurrentperiod.

(b) Basisofmeasurement

TheFinancialStatementshavebeenpreparedonthehistoricalcostbasisexceptforthosepresentedatfairvalueasdetailedintheaccountingpoliciesdisclosedinNote3-SignificantAccountingPoliciesandChangesinAccountingPolicies.

(c) FunctionalandPresentationCurrency

The Financial Statements are presented in Canadian dollars (CAN), which is also the Company’s functional currency. AllreferencestoUS$orUSDaretoUnitedStatesdollars.

(d) UseofEstimatesandJudgments

The preparation of financial statements in conformity with IFRS requires management tomake judgements, estimates andassumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, revenues andexpenses.Actualresultsmaydifferfromtheseestimates.

Estimatesandunderlyingassumptionsarereviewedonanongoingbasis.Revisionstoaccountingestimatesarerecognized intheperiodinwhichtheestimatesarerevisedandinanyfutureperiodsaffected.

On January 30, 2020, theWorld HealthOrganization declared the Coronavirus disease (COVID-19) outbreak a Public HealthEmergencyofInternationalConcernand,onMarch10,2020,declaredittobeapandemic.ActionstakenaroundtheworldtohelpmitigatethespreadofCOVID-19includerestrictionsontravel,quarantinesincertainareas,andforcedclosuresforcertaintypesofpublicplacesandbusinesses.Thesemeasureshavecaused,andwillcontinuetocausesignificantdisruptiontobusinessoperationsandasignificantincreaseineconomicuncertainty,withreduceddemandforcommoditiesleadingtovolatilepricesandcurrencyexchangerates,andadeclineinlong-terminterestrates.TheCompany'soperationsareparticularlysensitivetoareductioninthedemandfor,andpricesof,crudeoil,naturalgasandnaturalgasliquids.InadditiontotheimpactoncommoditypricesCOVID-19hascreatedmanyuncertaintiesinthecrudeoilandnaturalgasindustrywithrespecttoincreasedcounterpartycreditriskandvaluationoflong-livedpetroleumandnaturalgasassets.

The COVID-19 pandemic is an evolving situation that will continue to have widespread implications for our businessenvironment, operations and financial condition. Management cannot reasonably estimate the length or severity of thispandemic,ortheextenttowhichthedisruptionmaymateriallyimpactourfinancialresultsinfutureperiods.

9|Page

PrairieProvidentResourcesInc.

InformationaboutsignificantareasofestimationuncertaintyandcriticaljudgementsinapplyingaccountingpoliciesthathavethemostsignificanteffectontheamountsrecognizedintheFinancialStatementsareasfollows:

• PPR’soilandgasassetsaregroupedintocashgeneratingunits(“CGUs”).ACGUisthelowestlevelofintegratedassetsthatgenerate identifiablecash inflows thatare largely independentof thecash inflowsofotherassetsorgroupsofassets. The allocation of assets into CGUs requires significant judgement and interpretations with respect to theintegrationbetweenassets, geological formation,geographicalproximity, theexistenceof commonsalespointsandsharedinfrastructuresandthewayinwhichmanagementmonitorsitsoperations.TherecoverabilityofPPR’soilandgasassetsisassessedattheCGUlevel,andtherefore,thedeterminationofacostscouldhaveasignificantimpactonimpairmentlossesorimpairmentreversals;

• Reserves engineering is an inherently complex and subjective process of estimating underground accumulations ofpetroleum and natural gas. The process relies on interpretations of available geological, geophysical, engineering,economicandproductiondata.Theaccuracyofareservesestimateisafunctionofthequalityandquantityofavailabledata, the interpretation of that data, the accuracy of various economic assumptions and the judgement of thosepreparing theestimate.Because theseestimatesdependonmanyassumptions, all ofwhichmaydiffer fromactualresults, reservesestimates andestimatesof futurenet revenuemaybedifferent from the sales volumesultimatelyrecovered and net revenues actually realized. Changes inmarket conditions, regulatorymatters and the results ofsubsequent drilling, testing and production may require revisions to the original estimates. Estimates of reservesimpact: (i) theassessmentofwhetherornotanewwellhas foundeconomically recoverable reserves; (ii)depletionrates; (iii) the determination of net recoverable amount of oil and gas properties for impairment assessment andmeasurement, (iv) purchase price allocation for business combinations, and (v) the determination of reserve liveswhich affect the timing of decommissioning activities, all of which could have a material impact on earnings andfinancialpositions;

• Recoverableamountscalculatedforimpairmenttestingarebasedonestimatesoffuturecommodityprices,expectedvolumes,quantityofreservesanddiscountratesaswellasfuturedevelopmentcosts,royalties,andoperatingcosts.Thesecalculationsrequiretheuseofestimatesandassumptions,whichbytheirnature,aresubjecttomeasurementuncertainty. In addition, judgement is exercised by management as to whether there have been indicators ofimpairment or of impairment reversal. Indicators of impairment or impairment reversal may include, but are notlimited to a change in: market value of assets, asset performance, estimate of future prices, royalties and costs,estimatedquantityofreservesandappropriatediscountrates;

• Amountsrecordedfordecommissioningliabilitiesandtherelatedaccretionexpenserequiretheuseofestimateswithrespecttotheamountandtimingofdecommissioningexpenditures,inflationratesanddiscountrates.Actualcostsandcash outflows can differ from estimates because of changes in law and regulations, public expectations, marketconditions, discovery and analysis of site conditions and changes in technology. Decommissioning liabilities arerecognizedintheperiodwhenitbecomesprobablethattherewillbeafuturecashoutflow;

• Compensationcostsrecordedpursuanttoshare-basedcompensationplansaresubjecttotheestimatedfairvaluesoftheawardsonthegrantdateandtheestimatednumberofunitsthatwillultimatelyvest.TheCompanyusestheBlack-Scholesoptionvaluationmodel toestimate the fairvalueofoptions,which requires theCompany todetermine themost appropriate inputs including the expected life of the options, volatility, forfeiture rates and future dividends,whichbynaturearesubjecttomeasurementuncertainty;

• Derivativeriskmanagementcontractsarevaluedusingvaluationtechniqueswithmarketobservableinputs.Themostfrequently appliedvaluation techniques includeBlack-Scholesoptionvaluationmodel and forwardpricingand swapmodels. Themodels incorporate various inputs including the credit quality of counterparties, foreignexchange spotandforwardrates,volatilitiesofcommoditypricesandforwardratecurvesoftheunderlyingcommodity.Changesinanyoftheseassumptionswouldimpactfairvalueoftheriskmanagementcontractsandasaresult,futurenetincomeandothercomprehensiveincome;

• Taxinterpretations,regulationsandlegislationinthevariousjurisdictionsinwhichtheCompanyoperatesaresubjecttochange.TheCompany isalso subject to incometaxauditsand reassessmentswhichmaychange itsprovision forincome taxes. Therefore, the determination of income taxes is by nature complex, and requires making certainestimatesandassumptions.PPRrecognizesnetdeferredtaxbenefitrelatedtodeferredtaxassetstotheextentthatitis probable that the deductible temporary differences will reverse in the foreseeable future. Assessing therecoverability of deferred tax assets requires the Company tomake significant estimates related to expectations offuturetaxableincome.Estimatesoffuturetaxableincomearebasedonforecastcashflowsfromoperationsandthe

10|Page

PrairieProvidentResourcesInc.

application of existing tax laws in each jurisdiction. To the extent that future cash flows and taxable income differsignificantlyfromestimates,theabilityoftheCompanytorealizethenetdeferredtaxassetsrecordedatthereportingdatecouldbeimpacted;

• The determination of fair value requires judgement and is based on market information, where available andappropriate.Fairvalueisbestevidencedbyanindependentquotedmarketpriceforthesameassetor liability inanactivemarket.However,quotedmarketpricesandactivemarketsdonotalwaysexist.Inthoseinstances,fairvaluationtechniquesareused.TheCompanyappliesjudgementindeterminingthemostappropriateinputsandtheweightingascribedtoeachsuchinputaswellasitsselectionofvaluationmethodologies.Thecalculationoffairvalueisbasedonmarketconditionsasateachreportingdate,andmaynotbereflectiveofultimaterealizablevalue;

• Contingencies will only be resolved when one or more future events occur or fail to occur. The assessment ofcontingenciesinherentlyinvolvestheexerciseofsignificantjudgmentandestimatesoftheoutcomeoffutureevents;and

• Amounts recorded for capitalized general and administrative cost that is related to directly attributed supportingfunctions and activity to post-license exploration and evaluation assets and to development and producing CGUpropertiesrequirestheuseofestimatesandjudgmentsandisbyitsnaturesubjecttomeasurementuncertainty;

• Management applies judgment in reviewing each of its contractual arrangements to determine whether thearrangement contains a lease within the scope of IFRS 16. Leases that are recognized are subject to furthermanagement judgment and estimation in various areas specific to the arrangement. The Company determines thelease termas thenon-cancellable termof the lease, togetherwithanyperiods coveredbyanoption toextend thelease if it is reasonably certain to be exercised, or any periods covered by an option to terminate the lease, if it isreasonablycertainnottobeexercised.TheCompanyappliesjudgmentinevaluatingwhetheritisreasonablycertaintoexercisetheoptiontorenewbyconsideringallrelevantfactorsthatcreateaneconomicincentiveforittoexercisetherenewal. After the commencement date, the Company reassesses the lease term if there is a significant event orchange incircumstances that iswithin itscontrolandaffects itsability toexercise (ornot toexercise) theoption torenew(e.g.,achangeinbusinessstrategy).Wheretherateimplicitinaleaseisnotreadilydeterminable,thediscountrateofleaseobligationsareestimatedusingadiscountratesimilartoPPR'scompany-specificincrementalborrowingrate.ThisraterepresentstheratethatPPRwouldincurtoobtainthefundsnecessarytopurchaseanassetofasimilarvalue,withsimilarpaymenttermsandsecurityinasimilareconomicenvironment;and

• Managementappliesjudgementinreviewingmodificationsoffinancialliabilitiestodetermineifthemodificationsareconsidered substantial under the requirementsof IFRS9, including the considerationofqualitative andquantitativefactors.Theclassificationofamodificationasnon-substantialorsubstantialimpactstheaccountingtreatmentforthefinancialliabilityastotheimplementationofmodificationaccountingorextinguishmentaccountingandassuch,mayhavematerialimplicationsonthefinancialstatements.

3. SIGNIFICANTACCOUNTINGPOLICIESANDCHANGESINACCOUNTINGPOLICIES

(a) BasisofConsolidation

At December 31, 2020, the Financial Statements included the accounts of PPR and its wholly owned subsidiaries, includingPrairie Provident Resources Canada Ltd. (“PPR Canada”), Lone Pine Resources, Lone Pine Resources (Holdings) Inc., ArsenalEnergyUSAInc.,andArsenalEnergyHoldingsLtd.SubsidiariesareconsolidatedfromthedatetheCompanyobtainscontrolandcontinues to be consolidated until the date such control ceases. Control is achievedwhen PPR is exposed, or has rights, tovariablereturnsfromits involvementwiththeinvesteeandhastheabilitytoaffectthosereturnsthroughitspowerovertheinvestee. The financial statements of the subsidiaries are prepared for the same reporting period as the Company, usingconsistent accounting policies. All inter-entity transactions have been eliminated upon consolidation between PPR and itssubsidiariesintheseconsolidatedfinancialstatements.PPR'soperationsareviewedasasingleoperatingsegmentbythechiefoperatingdecisionmakeroftheCompanyforthepurposeofresourceallocationandassessingperformance.

(b) JointArrangements

PPR conducts someof its oil and gas activities through joint operations. Joint operation is a typeof joint arrangement overwhich two or more parties have joint control and rights to the assets and obligations for the liabilities, relating to thearrangement.Jointcontrol isthecontractuallyagreedsharingofcontrolofanarrangement,whichexistsonlywhendecisionsabouttherelevantactivities(beingthosethatsignificantlyaffectthereturnsofthearrangement)requireunanimousconsentof

11|Page

PrairieProvidentResourcesInc.

thepartiessharingcontrol.PPRdoesnothaveanyjointarrangementsthatarematerialtotheCompany,orthatarestructuredusingseparatevehicles. In relationto its interests in jointoperations,PPRrecognizes in theFinancialStatements its shareofassets,liabilities,revenuesandexpensesofthearrangements.

(c) BusinessCombinations

Businesscombinationsareaccountedforusingtheacquisitionmethodofaccounting.Thefairvalueoftheassetsacquired,theliabilitiesassumedandtheconsiderationtransferredismeasuredattheacquisitiondate.Transactioncostsrelatedtobusinesscombinationsareexpensedwhenincurred.

Ifthefairvalueoftheconsiderationexceedsthenetidentifiableassetsacquired,itisrecordedasgoodwill.Iftheconsiderationis less than the fair value of the net identifiable assets acquired, the difference is recognized as a gain in the consolidatedstatementoflossandcomprehensiveloss.

(d) Revenue

Revenuefromthesaleofcrudeoil,naturalgasandnaturalgasliquidsismeasuredpertheconsiderationspecifiedincontractswithcustomers. Revenueisrecognizedwhenthecustomerobtainscontrolofthegoods.TheCompanysatisfiesperformanceobligations and the customer obtains control upon the delivery of crude oil, natural gas and natural gas liquids, which isgenerallyatapointintime.Whilethetransactionpriceisvariableunderthetermsofthecontract,atthetimeofdelivery,thereisonlyaminimalriskofachangeinthetransactionpricetobeallocatedtothevolumesold.Accordingly,atthepointofsalethere is not a significant risk of revenue reversal relative to the cumulative revenue recognized, and there is no need toconstrain any variable consideration. The amount of revenue recognized is based on the agreed upon transaction price,wherebyanyvariabilityinrevenueisrelatedspecificallytotheCompany’seffortstodeliverproduction.Therefore,theresultingrevenueisallocatedtotheproductiondeliveredintheperiodduringwhichthevariabilityoccurs.

TheCompanydoesnothavecontractswithcustomerswheretheperiodbetweenthetransferofthepromisedgoodsorservicestothecustomerandpaymentbythecustomerexceedsoneyear.Asaconsequence,theCompanydoesnotadjustanyofthetransactionpricesforthetimevalueofmoney.

(e) ExplorationandEvaluationAssetsandPropertyandEquipment

(i) RecognitionandMeasurement

ExplorationandEvaluation(“E&E”)Assets

Pre-licensecostsarerecognizedintheconsolidatedstatementsoflossandcomprehensivelossasincurred.

E&E costs, including the costs of acquiring licenses, obtaining geological and geophysical data, drilling andcompletingE&Ewells, andbuildingassociated facilities are initially capitalizedasE&Eassets according to thenature of the expenditure. E&E assets may include estimated decommissioning costs associated with E&Edecommissioning obligations. The costs are accumulated by well, field or exploration area pendingdeterminationoftechnicalfeasibilityandcommercialviability.E&Eassetsarenotamortized.

The technical feasibility and commercial viability of extracting a hydrocarbon resource are considered to bedeterminable when proved and/or probable reserves are determined to exist. A review of each explorationlicenseorfieldiscarriedout,atleastannually,toascertainwhetherprovedand/orprobablereserveshavebeendiscovered.Upondeterminationofprovedand/orprobablereserves,E&Eassetsattributabletothosereservesare tested for impairment and if estimated recoverable amounts exceed carrying values the E&E assets, aretransferred to petroleum and natural gas properties, within property and equipment assets. The cost ofundeveloped land that expires and E&E expenditures determined to be unsuccessful are derecognized byrecordingexplorationandevaluationexpense.

ProductionandDevelopment(“P&D”)Assets

P&Dassetsgenerallyrepresentcostsincurredinacquiringanddevelopingprovedand/orprobablereserves,andbringing inor enhancingproduction from such reserves.Development costs include the initial purchasepriceand directly attributable costs relating to land and mineral leases, geological and seismic studies, propertyacquisitions, development drilling, construction of gathering systems and infrastructure facilities,decommissioning costs, transfers fromE&Eassets, and forqualifyingassets,borrowing costs. These costsare

12|Page

PrairieProvidentResourcesInc.

accumulatedonafieldoranareabasis(majorcomponents).Thecostsoftheday-to-dayservicingofpropertyandequipmentarerecognizedinoperatingexpensesasincurred.

The production and development items of property and equipment, which includes oil and natural gasdevelopment, properties and production assets, are measured at cost less accumulated depletion anddepreciation and accumulated impairment losses, net of impairment reversals. Development assets includecertainstockequipmentthatisexpectedtobeusedinthenormalcourseofP&Dfielddevelopment.

Gains and losses on disposal of an item of property and equipment, including petroleum and natural gasproperties,aredeterminedbycomparingthenetproceedsfromdisposalwiththecarryingamountofpropertyandequipmentandare recognizedonanetbasison theconsolidatedstatementsof lossandcomprehensiveloss.

(ii) DepletionandDepreciation

ThenetcarryingvalueofP&Dassetsisdepletedusingtheunit-of-productionmethodbyreferencetotheratioofproduction in the year to the related proved plus probable reserves, taking into account estimated futuredevelopment costs necessary to convert those reserves into production. Future development costs areestimatedtakingintoaccountthelevelofdevelopmentrequiredtoproducethereserves.Theseestimatesarepreparedbyindependentreserveengineersatleastannually.

Proved plus probable reserves are estimated annually by independent and qualified reserve evaluators andrepresenttheestimatedquantitiesofpetroleumandnaturalgaswhichgeological,geophysicalandengineeringdatademonstratewithaspecifieddegreeofcertaintytoberecoverableinfutureyearsfromknownreservoirsandwhichareconsideredcommerciallyproducible.

Reservesaretheremainingquantitiesof,petroleumandnaturalgasfromknownaccumulationsestimatedtoberecoverable from a given date forward. The estimates of reserves are determined from drilling, geological,geophysical and engineering data based on established technology and specified economic conditions. Fordepletionpurposes,relativevolumesofpetroleumandnaturalgasproductionandreservesareconvertedattheenergyequivalentconversionrateofsixthousandcubicfeetofnaturalgastoonebarrelofcrudeoil.

Forotherassets,depreciationisrecognizedinprofitorlossonastraight-lineordeclining-balancebasisovertheestimated useful life of each part of an item of property and equipment. Leasehold improvements aredepreciatedover thetermof the lease.Leasedassetsaredepreciatedover theshorterof the leasetermandtheirusefullivesunlessitisreasonablycertainthattheCompanywillobtainownershipbytheendoftheleaseterm.

Computerequipment isdepreciatedusing thedeclining-balancebasis at a rateof30percentper year.Officefurnitureisdepreciatedonastraightlinebasisoverfiveyears.

Depreciationmethods,usefullivesandresidualvaluesarereviewedateachreportingdate.

(iii) Impairment

E&EAssets

E&E assets are assessed for impairment if: (i) sufficient data exists to determine technical feasibility andcommercialviability;and(ii)atsuchtimethatfactsandcircumstancesindicatethatthecarryingamountexceedsthe recoverable amount. If the recoverable amount does not exceed the carrying amount, an impairmentadjustmentisrecognizedinnetlossandcomprehensiveloss.

Forthepurposesofimpairmenttesting,E&EassetsareallocatedtoCGUsbasedongeographicalproximity.E&Eassets that are not related to established CGUs with reserves, such as undeveloped land holdings, seismic,equipment,andexplorationdrillinginQuebec,theNorthwestTerritoriesandotherexploratoryproperties,aresubject to impairment testing basedon the nature and estimated recoverable amount of the respective costcomponents.

13|Page

PrairieProvidentResourcesInc.

P&DAssets

PPR assesses, at each reporting date, whether there is an indication that an asset may be impaired. If anyindicationexists,theCompanyestimatestheasset’srecoverableamount.Anasset’srecoverableamountisthehigher of an asset’s fair value less cost of disposal (“FVLCD”) and its value-in-use (“VIU”). The recoverableamount isdeterminedforan individualasset,unlesstheassetdoesnotgeneratecash inflowsthatare largelyindependentofthosefromotherassetsorgroupsofassets.Insuchcase,animpairmenttestisperformedattheCGUlevel.ACGUisagroupofassetsthatPPRaggregatesbasedontheirabilitytogeneratelargelyindependentcashflows.AsatDecember31,2020,theCompanyhasfiveprincipaloperatingCGUs–Evi,Michichi(previouslyknownasWheatland),Princess,ProvostandOther.

WherethecarryingamountofanassetorCGUexceedsitsrecoverableamount,theassetisconsideredimpairedandiswrittendowntoitsrecoverableamount.TodetermineVIU,theCompanyestimatesthepresentvalueofthe futurenetcash flowsexpectedtoderive fromthecontinueduseof theassetorCGU.Discountrates thatreflectthemarketassessmentsofthetimevalueofmoneyandtherisksspecifictotheassetorCGUareused.IndeterminingFVLCD,discountedcashflowsandrecentmarkettransactionsaretaken intoaccount, ifavailable.These calculationsare corroboratedbyvaluationmultiplesorotheravailable fair value indicators. Forassetsexcluding goodwill, an assessment ismade at each reporting date as towhether there is any indication thatpreviously recognized impairment lossesmayno longerexistormayhavedecreased. If such indicationexists,thepreviouslyrecognizedimpairmentlossisreversed.Thereversalislimitedsuchthatthecarryingamountoftheassetdoesnotexceeditsrecoverableamount,nordoesitexceedthecarryingamountthatwouldhavebeendetermined,netofdepreciation,hadnoimpairmentlossbeenrecognizedfortheassetinpriorperiods.

(f) FinancialInstruments

(i) RecognitionandMeasurement

PPRrecognizesfinancialassetsandfinancial liabilities, includingderivatives,ontheconsolidatedstatementsoffinancial position when the Company becomes a party to the contract. The Company initially measures allfinancial instruments at fair value. Subsequent measurement of the financial instrument is based on itsclassification.Financialassetsandfinancialliabilitiesareclassifiedintothefollowingcategories:amortizedcost,fairvaluethroughothercomprehensiveincome(“FVOCI”)andfairvaluethroughprofitandloss(“FVPL”).

Financial assets and financial liabilities classifiedas FVPLaremeasuredat fair valuewith subsequent changesrecognizedthroughnetincome(loss).Financialassetsandliabilitiesclassifiedasamortizedcostaremeasuredatamortizedcostusing theeffective interestmethodofamortization.Under theeffective interest ratemethod,anytransactionfees,costs,discountsandpremiumsdirectlyrelatedtothefinancialinstrumentsarerecognizedincomprehensivelossovertheexpectedlifeoftheinstrument.FinancialassetsclassifiedasFVOCIaremeasuredatfairvalueswithchangesinthosefairvaluesrecognizedinothercomprehensiveloss.

(ii) LiabilitiesandEquity

Financial instruments are classified as a liability or equity based on the substance of the contractualarrangement.An instrument isclassifiedasa liability if it isacontractualobligationtodelivercashoranotherfinancialasset,ortoexchangefinancialassetsorfinancialliabilitiesonpotentiallyunfavorableterms.Acontractisalsoclassifiedasaliabilityifitisanon-derivativeandcouldobligatetheCompanytodeliveravariablenumberofitsownsharesoritisaderivativeotherthanonethatcanbesettledbythedeliveryofafixedamountofcashor another financial asset for a fixed number of the Company’s own equity instruments. An instrument isclassifiedasequityifitevidencesaresidualinterestintheCompany’sassetsafterdeductingallliabilities.

(iii) DerivativeFinancialInstruments

Derivative financial instruments areusedby theCompany tomanage its exposure tomarket risks relating tocommodityprices.TheCompany’spolicyisnottousederivativefinancialinstrumentsforspeculativepurposes.Theestimateof fairvalueofallderivative instruments isbasedonquotedmarketprices,or in theirabsence,thirdpartymarketindicationsandforecastsandincludesanestimateofthecreditqualityofcounterpartiestothederivativeinstruments.Theestimatedfairvalueoffinancialassetsandliabilitiesissubjecttomeasurementuncertainty.

14|Page

PrairieProvidentResourcesInc.

TheCompanyhasnotdesignateditsfinancialderivativecontractsaseffectiveaccountinghedges,andthereforehasnotappliedhedgeaccounting,eventhoughtheCompanyconsidersallcommoditycontractstobeeconomichedges. As a result, all financial derivative contracts are measured at fair value, with any gains and lossesrecordedintheconsolidatedstatementofloss.

(iv) DerecognitionofFinancialInstruments

Afinancialliabilityisderecognizedwhentheobligationundertheliabilityisdischarged,cancelledorexpires.Thedifferencebetween thecarryingvalueof the liabilityand theultimateconsiderationpaid is recognized in theconsolidatedstatementoflossandcomprehensiveloss.Ifequityinstrumentsareissuedtoextinguishafinancialliability,theequityinstrumentsaretreatedasconsiderationpaidandmeasuredattheirfairvalueatthedateofextinguishment.Whenanexistingfinancialliabilityisreplacedbyanotherfromthesamelenderonsubstantiallydifferentterms,orthetermsofanexistingliabilityaresubstantiallymodified,suchanexchangeormodificationistreatedasthederecognitionoftheoriginalliabilityandtherecognitionofanewliability.Thedifferenceintherespectivecarryingamountsisrecognizedinthestatementofprofitorlossandothercomprehensiveincome.

(v) Impairment

TheCompanyrecognizesallowancesforlossesonitsfinancialassetsmeasuredatamortizedcostsbasedonthelifetimeexpectedcreditlossesanticipatedtooccurfromallexpecteddefaultsoverthelifeoffinancialasset.Tocalculate the expected credit loss, PPR applies the simplified approach applying a provision matrix wherebyfinancial assets are grouped into categories based on counterparty characteristics and aging categories. TheCompany considers past experience and forward-looking information if such information is reasonable andsupportable,availablewithoutunduecostsandeffort,andcanhaveasignificantimpactonthelossestimate.

Lossallowancesforfinancialassetsmeasuredatamortizedcostaredeductedfromthegrosscarryingamountoftheassetsand impairment lossesare recognized inprofitand loss.OncetheCompanyhaspursuedcollectionactivitiesand ithasbeendetermined that the incrementalcostofpursuingcollectionoutweighs thebenefits,PPR derecognizes the gross carrying amount of the financial asset and the associated allowance from theconsolidatedstatementoffinancialposition.

(vi) Offsetting

Financialassetsandliabilitiesareoffsetandthenetamountreportedinthestatementoffinancialpositionwhenthereisalegallyenforceablerighttooffsettherecognizedamountsandthereisanintentiontosettleonanetbasisorrealizetheassetandsettletheliabilitysimultaneously.

(g) FairValueMeasurement

PPRmeasuresderivativesatfairvalueateachbalancesheetdateand,forthepurposesofimpairmenttesting,usesFVLCDtodetermine the recoverableamountof someof itsnon-financial assets.Also, fair valuesof financial instrumentsmeasuredatamortized cost aredisclosed inNote21. Fair value is theprice thatwouldbe received to sell an assetor paid to transfer aliabilityinanorderlytransactionbetweenmarketparticipantsatthemeasurementdate.ThefairvaluemeasurementisbasedonthepresumptionthatthetransactiontoselltheassetortransfertheliabilitytakesplaceeitherinthefollowingmarketsthatareaccessiblebytheCompany:

• theprincipalmarketfortheassetorliability,or

• intheabsenceofaprincipalmarket,themostadvantageousmarketfortheassetorliability.

Thefairvalueofanassetoraliabilityismeasuredusingtheassumptionsthatmarketparticipantswouldusewhenpricingtheasset or liability, assuming thatmarket participants act in their economic best interest. A fair valuemeasurement of a non-financialassettakesintoaccountamarketparticipant'sabilitytogenerateeconomicbenefitsbyusingtheassetinitshighestand best use or by selling it to anothermarket participant that would use the asset in its highest and best use. PPR usesvaluationtechniquesthatareappropriateinthecircumstancesandforwhichsufficientdataareavailabletomeasurefairvalue,maximizingtheuseofrelevantobservable inputsandminimizingtheuseofunobservable inputs. AllassetsandliabilitiesforwhichfairvalueismeasuredordisclosedintheFinancialStatementsarecategorizedwithinthefairvaluehierarchy;describedasfollows,basedonthelowest-levelinputthatissignificanttothefairvaluemeasurementasawhole:

• Level1—Quoted(unadjusted)marketpricesinactivemarketsforidenticalassetsorliabilities;

15|Page

PrairieProvidentResourcesInc.

• Level 2—Valuation techniques forwhich the lowest-level input that is significant to the fair valuemeasurement isdirectlyorindirectlyobservable;and

• Level 3—Valuation techniques forwhich the lowest-level input that is significant to the fair valuemeasurement isunobservable.

Forassetsandliabilitiesthatarerecognizedinthefinancialstatementsonarecurringbasis,PPRdetermineswhethertransfershaveoccurredbetweenlevelsinthehierarchybyreassessingcategorization(basedonthelowest-levelinputthatissignificanttothefairvaluemeasurementasawhole)attheendofeachreportingperiod.

(h) Provisions

(i) ProvisionsandContingencies

ProvisionsarerecognizedwhentheCompanyhasapresentobligation(legalorconstructive)asaresultofapastevent, it isprobable thatanoutflowof resourcesembodyingeconomicbenefitswillbe required tosettle theobligationandareliableestimatecanbemadeof theamountof theobligation.WheretheCompanyexpectssomeorallof aprovision tobe reimbursed, forexample,underan insurancecontract, the reimbursement isrecognizedasaseparateassetbutonlywhenthereimbursement isvirtuallycertain.Theexpensesrelatingtoprovisionsaregenerallypresentedintheconsolidatedstatementsoflossnetofanyreimbursementexceptfordecommissioningliabilities.Iftheeffectofthetimevalueofmoneyismaterial,provisionsarediscountedusingacurrent discount rate that reflects,where appropriate, the risks specific to the liability.Where discounting isused,theincreaseintheprovisionduetothepassageoftimeisrecognizedasafinancecost.

Acontingencyisdisclosedwheretheexistenceofanobligationwillonlybeconfirmedbyfutureevents,orwheretheamountofapresentobligationcannotbemeasuredreliablyorwilllikelynotresultinaneconomicoutflow.Contingentassetsareonlydisclosedwhentheinflowofeconomicbenefitsisprobable.

(ii) DecommissioningLiabilities

PPRrecognizesdecommissioning liabilitiesrelatedto itsobligationstodismantle,retireandreclaimitsoilandgasproperties.Decommissioningobligationsaremeasuredatthepresentvalueofmanagement’sbestestimateof expenditures required to settle thepresentobligationat thebalance sheetdate. Thepresent valueof theestimatedobligationisrecordedasaliabilitywithacorrespondingincreaseinthecarryingamountoftherelatedasset.Theobligationissubsequentlyadjustedattheendperiodtoreflectthepassageoftimeandchangesintheestimatedfuturecashflowsunderlyingtheobligation.Theincreaseintheprovisionduetothepassageoftimeisrecognizedasaccretioncostswhereasincreasesordecreasesduetochangesintheestimatedfuturecashflowsorchangesinthediscountratearecapitalized.Actualcostsincurreduponsettlementortowardsthesettlementof the decommissioning obligations are charged against the provision to the extent the provision wasestablished.

(i) Share-BasedCompensation

PPRhasnotofferedanyawardsthatareclassifiedascash-settledawards. Forequitysettledshare-basedawardsgrantedtoofficers,directorsandemployees,thegrantdatefairvalueofsuchawardsisrecognizedascompensationcostswithinoperatingand general and administrative expenses,with a corresponding increase in contributed surplus over the vesting period. TheCompany also capitalizes a portion of the share-based compensation that is directly attributable to capital projects, with acorrespondingdecreasetocompensationexpense.

Thefairvalueofoption-basedawardsismeasuredusingBlack-Scholesoptionvaluationmodel.Non-optionbasedawardsarevaluedbasedonthefairvalueofPPR'sunderlyingsharesatgrantdate.Aforfeiturerateisestimatedonthegrantdateandisadjustedtoreflecttheactualnumberofawardsthatvest.Upontheexerciseoftheshare-basedawards,anyconsiderationpaidtogetherwiththeamountpreviouslyrecognizedincontributedsurplusisrecordedasanincreaseinsharecapital.Intheeventthat vestedawardsexpire,previously recognized compensationexpenseassociatedwith suchawards isnot reversed. In theevent that awards are forfeited, previously recognized compensation expense associatedwith the unvested portion of suchawardsisreversed.

(j) Post-RetirementObligation

TheCompanysponsorsanunfundedpost-retirementbenefitsplantocertainretirees,whichisclosedtonewentrants.Expenseforthepost-retirementbenefitsplanincludestheinterestcostonpost-retirementbenefitsobligations.

16|Page

PrairieProvidentResourcesInc.

Theliabilityofthepost-retirementbenefitsplanisactuariallydeterminedusingtheprojectedunitcreditactuarialcostmethodproratedon service and reflects theCompany’sbest estimateof futurehealth care costs and retiree longevity. Theaccruedbenefit obligation is discounted using the market interest rate on high-quality corporate debt instruments as at themeasurementdate.TheCompanyaccountsforitspost-retirementbenefitsplanbyrecognizingtheunderfundedstatusoftheplanasaliabilityinitsconsolidatedstatementsoffinancialposition.InterestcostsontheunfundedobligationarerecordedinFinanceCosts.Anyactuarialgainsorlossesarerecognizedintheyearinwhichthechangesoccurthroughothercomprehensiveincome.

(k) Flow-throughShares

Pursuant to the termsof the flow-through share agreements, the resourceexpendituredeductions for income taxpurposesrelatedtoexploratoryanddevelopmentactivitiesfundedbyflow-throughsharesarerenouncedtoinvestorsinaccordancewithtaxlegislation.Sharecapitalisstatedatthemarketvalueofshareswithouttheflow-throughfeatureatthetimeofissue,withaliability recognizedrepresentingthedifferencebetweencashreceivedandmarketvalue.Thepremiumpaid for flow-throughshares inexcessof thatmarket valueof the shares isdrawndownanddeferred tax is recognizedat the time thequalifyingexplorationanddevelopmentexpendituresarerenouncedandincurred.

(l) IncomeTax

Incometaxexpensecomprisescurrentanddeferredtax.Incometaxexpenseisrecognizedinprofitorlossexcepttotheextentthatitrelatestoitemsrecognizeddirectlyinequity,inwhichcaseitisrecognizedinequity.

Currenttaxistheexpectedtaxpayableonthetaxableincomefortheyear,usingtaxratesenactedorsubstantivelyenactedatthereportingdate,andanyadjustmenttotaxpayableinrespectofpreviousyears.

Deferred tax is recognized on the temporary differences between the carrying amounts of assets and liabilities for financialreportingpurposes and the amountsused for taxationpurposes.Deferred tax is not recognizedon the initial recognitionofassetsorliabilitiesinatransactionthatisnotabusinesscombination.

Deferred tax ismeasuredat the tax rates thatareexpected tobeapplied to temporarydifferenceswhentheyare reversed,basedonthelawsthathavebeenenactedorsubstantivelyenactedbythereportingdate.Deferredtaxassetsandliabilitiesareoffset ifthere isa legallyenforceablerighttodoso,andtheyrelateto incometaxes leviedbythesametaxauthorityonthesametaxableentity,orondifferenttaxableentities,buttheyintendtosettlecurrenttaxliabilitiesandassetsonanetbasisortheirtaxassetsandliabilitieswillberealizedsimultaneously.

Adeferredtaxassetisrecognizedtotheextentthatitisprobablethatfuturetaxableprofitswillbeavailableagainstwhichthetemporarydifferencecanbeutilized.Deferredtaxassetsarereviewedateachreportingdateandarereducedtotheextentthatitisnolongerprobablethattherelatedtaxbenefitwillberealized.

(m) Inventory

Inventoriesarestatedatthelowerofcostandnetrealizablevalue.Thecostofmaterialsisthepurchasecost,determinedonfirst-in, first-outbasis.Thenetrealizablevalue isbasedontheestimatedsellingprice intheordinarycourseofbusiness, lessestimatedcostsnecessarytosell.

(n) ForeignCurrency

TransactionsinforeigncurrenciesaretranslatedtoCanadiandollarsatexchangeratesineffecttothedatesofthetransactions.MonetaryassetsandliabilitiesdenominatedinforeigncurrenciesaretranslatedtoCanadiandollarsattheperiodendexchangerate. Non-monetary assets and liabilities denominated in foreign currencies that are measured at historical cost are notsubsequentlyre-translated.Foreigncurrencydifferencesarisingontranslationarerecognizedintheconsolidatedstatementofloss.

(o) GovernmentGrants

Governmentgrantsare recognizedwhen there is reasonableassurance thatPPRwill complywith theconditionsattached tothemandthegrantswillbereceived.Ifagrantisreceivedbeforeit iscertainwhethercompliancewithallconditionswillbeachieved,thegrantisrecognizedasadeferredliabilityuntilsuchconditionsaremet.Whentheconditionsofagrantrelatetoincomeorexpense,itisrecognizedintheconsolidatedstatementofloss.Whenconditionsofagrantrelatetoanunderlyingasset,itisrecognizedasareductiontothecarryingamountoftherelatedasset.

17|Page

PrairieProvidentResourcesInc.

(p) Leases

WhenPPRispartytoa leasearrangementasthe lessee, itrecognizesaright-of-useasset("ROUasset")andacorrespondingleaseobligationontheconsolidatedstatementsoffinancialpositiononthedatethataleasedassetbecomesavailableforuse.

ROU assets are measured at cost, less any accumulated depreciation and impairment losses, and adjusted for anyremeasurementofleaseliabilities.ThecostofROUassetsincludestheamountofleaseliabilitiesrecognized,initialdirectcostsincurred,andleasepaymentsmadeatorbeforethecommencementdatelessanyleaseincentivesreceived.TheROUassetisdepreciatedover the leasetermonastraight-linebasisover theshorterof itsestimateduseful lifeandthe leaseterm.ROUassetsaresubjecttoimpairment.

Lease liabilities include the net present value of fixed payments (including in-substance fixed payments), less any leaseincentives receivable,variable leasepayments thatarebasedonan indexora rate,amountsexpected tobepayableby thelesseeunderresidualvalueguarantees,theexercisepriceofapurchaseoptionifthelesseeisreasonablycertaintoexercisethatoption,andpaymentsofpenaltiesforterminatingthelease,iftheleasetermreflectsthelesseeexercisingthatoption.Theselease payments are discounted using the Company’s incremental borrowing ratewhere the rate implicit in the lease is notreadilydeterminable.TheCompanyusesasinglediscountrateforaportfolioofleaseswithreasonablysimilarcharacteristics.Thevariable leasepaymentsthatdonotdependonan indexoraratearerecognizedasexpense intheperiodonwhichtheeventorconditionthattriggersthepaymentoccurs.Afterthecommencementdate,theamountofleaseliabilitiesisincreasedtoreflecttheaccretionofinterestandreducedfortheleasepaymentsmade.Inaddition,thecarryingamountofleaseliabilitiesis remeasured if there is amodification, a change in the lease term,a change in the in-substance fixed leasepaymentsorachangeintheassessmenttopurchasetheunderlyingasset.

Leasepaymentsonshort-termleasesor leaseson low-valueassetsareexpensed intheconsolidatedstatementsof lossonastraight-linebasisovertheleaseterm.

4. ADOPTIONOFNEWACCOUNTINGSTANDARDSANDNEWACCOUNTINGPRONOUNCEMENTS

NewAccountingPronouncements

IBORReformanditsEffectsonFinancialReporting-Phase2

InAugust2020, the IASB issued InterestRateBenchmarkReform -Phase2whichamended requirements in IFRS9FinancialInstruments,IAS39FinancialInstruments:RecognitionandMeasurement,IFRS7FinancialInstruments:Disclosures,andIFRS16Leases,relatingtochangesinthebasisfordeterminingcontractualcashflowsoffinancialassets,financialliabilities,andleaseliabilities. This will be effective January 1, 2021. The Company is currently evaluating the impact of the standard on itsconsolidatedfinancialstatements.

5. ASSETACQUISITIONSANDDISPOSITIONS

During2020,PPRdisposedofcertainnon-corepropertiesandundevelopedlandforthetotalproceedsof$0.2million(2019—$0.3million).Theassociatedpropertyandequipment,explorationandevaluationassetanddecommissioning liabilitieswerederecognized,resultinginanetgainof$0.4million(2019—$0.3million)ondisposition.

18|Page

PrairieProvidentResourcesInc.

6. EXPLORATIONANDEVALUATIONASSETS

($000s) December31,2020 December31,2019

CostBalance–beginningofyear 66,799 65,642

Additions 271 2,678

Acquisitions — (59)

Transferstooilandgaspropertyandequipment — (1,122)

Adjustmentsduetochangeinestimatesindecommissioningliabilities(Note12) (343) 656

Explorationandevaluationexpense (4,183) (996)

CostBalance–endofyear 62,544 66,799

Provisionforimpairment–beginningofyear (56,616) (55,960)

Impairmentloss (143) (656)

Provisionforimpairment–endofyear (56,759) (56,616)

Netbookvalue–beginningofyear 10,183 9,682

Netbookvalue–endofyear 5,785 10,183

Explorationandevaluation(“E&E”)assetsconsistoftheCompany’sundevelopedlandandexplorationandpilotprojectswhicharependingthedeterminationofprovenorprobablereserves.

AsatDecember31,2020,theCompanyrecognizedanimpairmentlossof$0.5millionagainstundevelopedlandleasesinthePrincess area thatwere due to expire in the first quarter of 2021. The FVLCDwas determined to be zero, using amarketapproachbasedontheestimatedsellingpriceoflandintherelatedareawithsimilartermstoexpiry.Keyassumptionsincludedestimated selling prices of assets with similar geographic location, remaining term and related risk profile. The fair valuemeasurementwasnon-recurringandwasclassifiedaslevel3inthefairvaluehierarchy(seeNote3(g)forinformationonthefairvaluehierarchy).Theimpairmentlosswaspartiallyoffsetby$0.3millionofimpairmentrecoveryforchangesinestimatesofdecommissioningliabilitiesrelatedtoE&Epropertieswithzerocarryingvalue.

During2019,PPRrecognized$0.7millionofnon-cashE&Eimpairmentrelatedtochangesinestimatesusedindecommissioningliabilities.

FortheyearendedDecember31,2020,PPRrecognized$4.2million(2019-$1.0million)ofE&Eexpenserelatedtoexpiredandsurrenderedleasesinvariousareas.

DuringtheyearendedDecember31,2020,PPRdidnotcapitalizeanydirectlyattributablegeneralandadministrativeexpensesorshare-basedcompensationtoE&Eassets(December31,2019-nil).

19|Page

PrairieProvidentResourcesInc.

7. PROPERTYANDEQUIPMENT

($000s)

Productionand

DevelopmentOffice

Equipment

YearEndedDecember31,

2020

Cost:

Balance–beginningofyear 675,931 4,654 680,585

Additions 3,863 7 3,870

Disposition,netofacquisitions(Note5) (320) (11) (331)

Adjustmentsduetochangeinestimatesindecommissioningliabilities(Note12)

(1,785) — (1,785)

Balance–endofyear 677,689 4,650 682,339

Accumulatedimpairment,depletionanddepreciation:

Balance–beginningofyear (383,210) (3,826) (387,036)

Depletionanddepreciation (27,578) (267) (27,845)

Impairmentloss (78,316) — (78,316)

Balance–endofyear (489,104) (4,093) (493,197)

Netbookvalue–beginningofyear 292,721 828 293,549

Netbookvalue–endofyear 188,585 557 189,142

($000s)

Productionand

DevelopmentOffice

Equipment

YearEndedDecember31,

2019

Cost:

Balance–beginningofyear 645,891 4,618 650,509

Additions 9,654 36 9,690

Disposals (7) — (7)

Adjustmentsduetochangeinestimatesindecommissioningliabilities

19,271 — 19,271

Transfersfromexplorationandevaluationassets 1,122 — 1,122

Balance–endofyear 675,931 4,654 680,585

Accumulatedimpairment,depletionanddepreciation:

Balance–beginningofyear (344,830) (3,518) (348,348)

Depletionanddepreciation (39,472) (308) (39,780)

Impairmentrecovery 1,092 — 1,092

Balance–endofyear (383,210) (3,826) (387,036)

Netbookvalue–beginningofyear 301,061 1,100 302,161

Netbookvalue–endofyear 292,721 828 293,549

As at December 31, 2020, an estimated $222.4 million in future development costs associated with proved plus probableundevelopedreserveswereincludedinthecalculationofdepletion(December31,2019-$304.0million).

(a) CapitalizationofGeneralandAdministrativeandShare-BasedCompensationExpenses

20|Page

PrairieProvidentResourcesInc.

DuringtheyearendedDecember31,2020,$0.2million(2019–$1.6million)ofdirectlyattributablegeneralandadministrativeexpenses,includingnominalamount(2019–$0.1million)ofshare-basedcompensationexpenses,werecapitalizedtopropertyandequipment.

(b)Impairment

At December 31, 2020, the Company assessed its production and development assets for indicators of impairment orimpairmentreversalandnonewerenoted.InadditiontotheimpairmentlossrecognizedasatMarch31,2020(seediscussionbelow),duringtheyearendedDecember31,2020,PPRrecognizedanon-cashP&D impairment lossof$1.7million (2019—$1.1million)relatedtochangesindecommissioningliabilitiesofcertainpropertiesthathadzerocarryingvalue.

AtMarch 31, 2020, the decreases in crude oil and natural gas benchmark prices as compared to December 31, 2019wereconsideredindicatorsofimpairmentforthepropertyandequipment.Asaresult,theCompanycompletedimpairmenttestsonallofitscashgeneratingunits("CGU's")anddeterminedthatthecarryingamountsofcertaintheCGUsexceededtheirfairvalueless costs of disposal ("FVLCD"). The FVLCD values used to determine the recoverable amounts of the Company’s CGUs areclassified as Level 3 in the fair value hierarchy (see Note 3(g) for information on the fair value hierarchy) as certain keyassumptionsarenotbasedonobservablemarketdatabutrathertheCompany'sbestestimate.TheFVLCDwasestimatedusinganafter-taxdiscountrateof12.5%.

AsaresultoftheimpairmenttestatMarch31,2020,PPRrecognizedatotalof$76.6million(2019-$nil)non-cashimpairmentloss.UnderIFRS,impairmentlossesrelatedtoPP&EmaybereversedinfutureperiodsiftherecoverablevalueoftheimpairedCGUincreases.AtMarch31,2020,aonepercentchangeinthediscountratewouldhaveresultedina$3.3millionchangeinthe impairmentexpenseanda fivepercentchange in the forecastedcash flowswould resulted ina$2.8million impairmentexpense.

ImpairmentlossbyCGUwasasfollows:

Yearsended($000s) December31,2020 December31,2019

EVICGU 51,719 —

PrincessCGU 5,790 —

ProvostCGU 12,982 —

OtherCGU 6,096 —

Totalimpairmentloss 76,587 —

The following tableoutlinesbenchmarkpricesandassumptions,basedon the forecastprovidedbyour independent reserveevaluatorSprouleAssociatesLimited,usedincompletingtheimpairmenttestsasatMarch31,2020.

WTI($US/bbl)

EdmontonLight

($CAD/bbl)

AECO($CAD/MMBtu)

Exchangerate

($USequals,$1CAD) Inflationrate

2020 25.00 24.29 1.43 0.70 —%

2021 37.00 43.15 2.05 0.73 1%

2022 48.00 58.67 2.33 0.75 2%

2023 48.96 59.84 2.41 0.75 2%

2024 49.94 61.04 2.48 0.75 2%

2025 50.94 62.26 2.56 0.75 2%

Thereafter(inflationpercentage) 2% 2% 3% 0.75 2%

During the year ended December 31, 2019, the decreases in crude oil and natural gas benchmark prices as compared toDecember31,2018wereconsideredpotentialindicatorsofimpairment.Asaresult,theCompanycompletedimpairmenttestsonallofitsCGUsinaccordancewithIAS36anddeterminedthatthecarryingamountsoftheCGUsdidnotexceedtheirFVLCD.

21|Page

PrairieProvidentResourcesInc.

8. RIGHT-OF-USEASSETS

($000s) OfficeLeases FacilityLease OtherLeases Total

Cost:

Balance–January1,2019 3,056 6,687 313 10,056

Additionsandadjustments (1,115) — — (1,115)

Disposition/Derecognition (79) — — (79)

Balance–December31,2019 1,862 6,687 313 8,862

Additionsandadjustments — — 20 20

Disposition/derecognition — — (21) (21)

Balance–December31,2020 1,862 6,687 312 8,861

Accumulateddepreciation:

Balance–January1,2019 — — — —

Depreciation (990) (1,605) (148) (2,743)

Balance–December31,2019 (990) (1,605) (148) (2,743)

Depreciation (459) (1,605) (106) (2,170)

Balance–December31,2020 (1,449) (3,210) (254) (4,913)

Netbookvalue–December31,2019 872 5,082 165 6,119

Netbookvalue–December31,2020 413 3,477 58 3,948

22|Page

PrairieProvidentResourcesInc.

9. LONG-TERMDEBT

($000s) December31,2020 December31,2019

RevolvingFacility

USDAdvances(US$16.0million(December31,2019-US$27.6million))1 20,371 35,847

CADAdvances(US$30.0million(December31,2019-US$30.0million))2 40,530 40,530

CADDeferredInterest(US$0.5million(December31,2019-US$nil))1 590 —

Totalprincipal-RevolvingFacility 61,491 76,377

SeniorNotesIssuedOctober31,2017

Principal(US$16.0million)1 20,371 20,780

Deferredinterest(US$4.4million(December31,2019-US$1.8million))1 5,611 2,363

TotalPrincipalandDeferredInterest-October31,2017SeniorNotes 25,982 23,143

SeniorNotesIssuedNovember21,2018

Principal(US$12.5million)1 15,915 16,235

Deferredinterest(US$2.6million(December31,2019-US$0.7million))1 3,338 922

TotalPrincipalandDeferredInterest-November21,2018SeniorNotes 19,253 17,157

SeniorNotesIssuedDecember21,2020

Principal(US$11.4million(December31,2019-US$nil))1 14,500 —

Deferredinterest(US$0.04million(December31,2019-US$nil))1 48 —

TotalPrincipalandDeferredInterest-December21,2020SeniorNotes 14,548 —

TotalPrincipalandDeferredInterest-SeniorNotes 59,783 40,300

Unamortizeddeferredfinancingfees (691) (2,154)

UnamortizedvalueallocatedtoWarrantLiability (343) (928)

Unamortizedvalueallocatedtofairvalueadjustment (17,169) —

Long-termdebt 103,071 113,595

1Converted using themonth end exchange rate of $1.00USD to$1.27CAD as atDecember 31, 2020 and $1.00USD to $1.30CAD as atDecember31,2019.2Convertedusingtheexchangerateatthetimeofborrowingof$1.00USDto$1.35CAD.

(a) RevolvingFacility

On December 21, 2020, PPR renewed and amended its senior secured revolving note facility (“Revolving Facility”) with aborrowingbaseofUS$57.7million (December31,2020—US$60.0million)andextendedthematuritydateof theRevolvingFacility from April 30, 2021 to December 31, 2022. The borrowing base is subject to a reduction to US$53.8 million onDecember 31, 2021 and to semi-annual redeterminations thereafter, without limiting the lenders' right to require aredeterminationatanytime.Thenextborrowingbasere-determinationdatewillbearoundApril2022basedonyear-end2021reserveevaluations.

BorrowingsundertheRevolvingFacilityarerepayableattheCompany’selectionatparplusaccruedinterestandanyapplicablebreakage costs. Repayments generally will not affect the aggregate commitment or borrowing base under the RevolvingFacility, except in certain extraordinary circumstances where a repayment will reduce the borrowing base. The RevolvingFacilityisdenominatedinUSD,butaccommodatesCADadvancesuptothelesserofCAN$54millionorUS$30million.AllnoteswereissuedatparbyPPRCanadaandareguaranteedbyPrairieProvidentResourcesInc.andcertainofitsothersubsidiariesand securedbyaUS$200milliondebenture.AsatDecember31,2020, theCompanyhadUS$11.2million (CAN$14.3millionequivalent)borrowingcapacityundertheRevolvingFacility.

23|Page

PrairieProvidentResourcesInc.

Thedeterminationoftheborrowingbaseismadebythelenders,intheirsolediscretion,takingintoconsiderationtheestimatedvalue of PPR’s oil and natural gas properties in accordancewith the lenders’ customary practices for oil and gas loans. If aborrowingbasedeficiencyexistsbecauseofare-determination,thelenderisrequiredtonotifytheCompanyofsuchshortfall.TheCompanymayrepaytheshortfallamountbyeithermakingoneinstallmentwithin90daysorsixequalconsecutivemonthlyinstallmentsbeginningwithin30daysaftertheCompany'sreceiptoftheborrowingbasedeficiencynotice.

AmountsborrowedundertheRevolvingFacilitycanbedrawnintheformofUSDorCADprimeadvancesbearinginterestbasedon reference bankUSD and CADprime lending rates announced from time to time, or LIBOR advances (in the case ofUSDamounts)orCDORadvances(inthecaseofCADamounts)bearinginterestbasedonLIBORandCDORratesineffectfromtimetotime,plusanapplicablemargin.ApplicableMarginsperannumforCDOR,CADprime,LIBORandUSDprimeadvancesare650basispointsandstandbyfeesonanyundrawnborrowingcapacityare87.5basispointsperannum.

AsatDecember31,2020,PPRhadoutstandinglettersofcreditof$4.2million(December31,2019–$4.9million).ThelettersofcreditareissuedbyafinancialinstitutionatwhichPPRhaspostedcashdepositscollateral.Therelateddepositsareclassifiedasrestrictedcashonthestatementoffinancialpositionandthebalanceisinvestedinshort-termmarketdepositswithmaturitydatesofoneyearorlesswhenpurchased.

AsatDecember31,2020,$0.7millionofdeferredcostsrelatedtotheRevolvingFacilitywasnettedagainst itscarryingvalue(December31,2019–$1.3million).

(b) SubordinatedSeniorNotes

OnDecember21,2020,PPRamendeditsagreementsforseniornotesoriginallyissuedonOctober31,2017andNovember21,2018withtotalprincipaloutstandingofUS$28.5million(the"SeniorNotesdue2023").Undertheamendments,thematuritydate was extended fromOctober 21, 2021 to June 30, 2023. The annual interest rate on the Senior Notes due 2023wasreducedfrom15%perannumtoniluntilJune30,2021,andwillthereafterriseto4%attheearlierof15monthsafterclosing(March2022)andthelastdayofthefiscalquarterforwhichtheCompany'strailing12-monthseniorleverageratiois2.5orless,andto8%attheearlierof20monthsafterclosing(August2022)andthelastdayofthefiscalquarterforwhichtheCompany'strailing12-monthseniorleverageratiois2.0orless.

Additionally, on December 21, 2020 PPR purchased additional US$11.4 million senior notes ("Senior Notes due 2026",collectively with the Senior Notes due 2023, "Senior Notes") (CAN$14.5 million using the December 31, 2020 month-endexchangerateof$1.00USDto$1.27CAD)bearinginterestat12%perannum.NetproceedsfromtheissuanceofSeniorNotesdue2026wereappliedagainstborrowingsundertheRevolvingFacilityuponissuance.

InterestonSeniorNotesispayablequarterly.TheSeniorNoteagreementsprovidethat,untilcertaincriteriaaremet,includingcompliancewithoriginalfinancialcovenantratiosontheRevolvingFacilityasatOctober31,2017(whenthefacilitywasfirstimplemented), the absence of any borrowing base deficiency, and a projected ability to meet any scheduled paymentobligationsunder theRevolvingFacility for thenext12-monthperiod,PPRmayelect todeferall interestsdueon theSeniorNotes.ThetermsoftheRevolvingFacilityrequirethattheCompanymakethiselectionandnotpaycashinterestontheSeniorNotesuntilthesecriteriaaresatisfied.PPRwillthereafterbepermittedtoelecttodeferupto4.00%perannumofinterestontheSeniorNotes.

Inconjunctionwith the issuancesof theSeniorNotesdue2026, theCompany issueda totalof34,292,360warrantswithanexercisepriceof$0.0192pershareforaneight-yeartermexpiringonDecember21,2028(seeNote10).

InaccordancewithIFRS9,PPRaccountedforthechangestotermsoftheSeniorNotesdue2023asanextinguishmentandassuch,thepreviouslyrecordedliabilitieswerederecognizedandnewliabilitiesfortheSeniorNoteswererecordedattheirfairvalueasatDecember21,2020.Inaddition,theSeniorNotesdue2026wereinitiallyrecognizedatfairvaluewhichwaslowerthanthefacevalueofthenotes.Thefairvaluewascalculatedusingthepresentvalueofexpectedfuturecashflows,discountedat17.5%.Thefairvaluemeasurementwasnon-recurringandwasclassifiedaslevel3inthefairvaluehierarchy(seeNote3(g)forinformationonthefairvaluehierarchy).Collectively,themodificationofSeniorNotesdue2023andtheinitialrecognitionofSeniorNotesdue2026resultedintherecognitionofagainof$15.9millioninthefourthquarterof2020.Thegainisnetof$1.4millionoffinancingcosts.Aone-percentagepointincreaseinthediscountratewouldresultinaincreaseof$1.4milliontothegainonthemodificationoffinancialliabilities.

24|Page

PrairieProvidentResourcesInc.

AsatDecember31,2020,$nildeferredcostsrelatedtoPPR’sSeniorNoteswasnettedagainstitscarryingvalue(December31,2019–$0.9million).

(c) Covenants

The note purchase agreement for the Revolving Facility, the Senior Note agreement and related parent and subsidiaryguaranteescontainvariouscovenantsonthepartoftheCompanyanditssubsidiariesincludingcovenantsthatplacelimitationsoncertain typesofactivities, including restrictionsor requirementswith respect toadditionaldebt, liens,asset sales, capitalexpenditures, hedging activities, investments, dividends andmergers andacquisitions. In addition, capital expenditures andacquisitionsaregenerallylimitedtoconsistencywiththeCompany'sannualdevelopmentplan,ascreatedandupdatedbytheCompanyfromtimetotimeandapprovedbythelenders.

The note purchase agreement for the Revolving Facility and the subordinated Senior Note purchase agreement include thesamefinancialcovenants,with15%lessrestrictivethresholdsundertheSeniorNoteagreements.FinancialcovenantsarenotapplicableforthequarterendedDecember31,2020.FuturethresholdsforfinancialcovenantsundertheRevolvingFacilityforthequartersendedfromMarch31,2021toSeptember30,2022varybyquarterandareasfollows:

a. seniorleverage,pursuanttowhichtheratioofsenioradjustedindebtedness1toEBITDAX2forthefourquartersmostrecentlyendedcannotexceedbetween3.61to1.00and6.36to1.00;

b. assetcoverage,pursuanttowhichtheratioofadjustednetpresentvalueofestimatedfuturenetrevenuefromprovedreserves(discountedat10%perannum)toadjustedindebtedness3asofthedateofanyreservesreportcannotbelessthanfrom0.34to1.00to0.47to1.00;and

c. current ratio, pursuant to which the ratio of consolidated current assets, plus any undrawn capacity under theRevolvingFacility,toconsolidatedcurrentliabilitiesattheendofanyfiscalquartercannotbelessthanfrom0.9to1.0to 1.0 to 1.0. Under the agreements, current assets exclude derivative assetswhile current liabilities excludes thecurrent portion of long-term debt, lease liabilities, decommissioning obligations, derivative liabilities and non-cashliabilities.

1Underthedebtagreements,senioradjustedindebtednessisdefinedasAdjustedIndebtedness(asdefinedbelow)lesssubordinatedborrowings.2Under thedebt agreements, EBITDAX is definedasnet earnings (loss) before financing charges, foreignexchangegain (loss), E&Eexpense, income taxes,

depreciation, depletion, amortization, other non-cash items of expense and non-recurring items, adjusted formajor acquisitions andmaterial dispositionsassumingthatsuchtransactionshadoccurredonthefirstdayoftheapplicablecalculationperiod(“pro-formaadjustments”).3Underthedebtagreements,AdjustedIndebtednessisdefinedasborrowingslessoutstandinglettersofcreditforwhichPPRhasissuedcashcollateral.

TheCompanywasincompliancewithallapplicablecovenantsasatDecember31,2020.

25|Page

PrairieProvidentResourcesInc.

10. WARRANTLIABILITY

WarrantExpiringOctober31,2022

WarrantExpiringOctober31,2023

WarrantExpiringDecember21,2028

NumberofWarrants Amount

NumberofWarrants Amount

NumberofWarrants Amount

PPRWarrantLiability,December31,2019 2,318 24 6,000 60 — —

Cancelled (2,318) — (6,000) — — — —

Issued — — — — 34,292 342

Fairvalueadjustment — (24) — (60) — 344

PPRWarrantLiability,December31,2020 — — — — 34,292 686

Inconjunctionwith themodificationofSeniorNotesdue2023andthe issuanceofSeniorNotesdue2026 (seeNote9),PPRissuedatotalof34,292,360warrantswithanexercisepriceof$0.0192pershareforaneight-yeartermexpiringonDecember21,2028.WarrantsissuedconcurrentwiththeissuanceofSeniorNotesonOctober31,2017andNovember21,2018totaling2,318,000,withanexercisepriceof$0.549and6,000,000,withanexercisepriceof$0.282,respectively,werecancelledinfull.

Thewarrants issuedwereclassifiedas financial liabilitiesdue toacashlessexerciseprovisionandaremeasuredat fairvalueuponissuanceandateachsubsequentreportingperiod,withthechangesinfairvaluerecordedintheconsolidatedstatementoflossandcomprehensiveloss.ThefairvalueofthesewarrantsisdeterminedusingtheBlack-Scholesoptionvaluationmodel.Thesewarrantsareexercisableanytimeandthusthevalueofthesewarrantsispresentedascurrentliabilityintheconsolidatedstatementoffinancialposition.ThevalueofthewarrantliabilityasatDecember31,2020was$0.7million(December31,2019-$0.1million).Fortheyearof2020,PPRrecordedalossinfairvalueof$0.3million(2019—$0.7milliongain)againstwarrantliabilities.

ThefairvalueofthewarrantsasatDecember31,2020of$0.02perwarrantwasestimatedusingthefollowingassumptions:

December31,2020

WarrantsExpiringDecember21,

2028

Riskfreeinterestrate 0.46%

Expectedlifeofoptions(years) 7.92

Expectedvolatility 151%

Stockprice $0.02

Dividendspershare —

11. LEASELIABILITIES

($000s) December31,2020 December31,2019

Openingbalance 7,641 11,531

Additionsandadjustments 27 (1,115)

Financeexpense 658 1,028

Leasepayments (3,172) (3,803)

Endingbalance 5,154 7,641

Less:currentportion 2,548 2,520