Embed Size (px)

Citation preview

Practice Note Apportioning the Price Paid for a Business Transferred as a Going Concern Index 1. Background 2. The Statutory Provisions 3. Legal Definitions of Goodwill 4. Trade Related Properties 5. Goodwill in Trade Related Properties 6. Valuing Goodwill and Other Intangible Assets 7. Valuing the Tangible Assets - Assumptions 8. Valuing the Tangible Assets – the Profits Approach 9. Valuing the Tangible Assets – the Investment Approach 10. RICS GN2 - Valuations of the ‘Operational Entity’ 11. Apportionment Approach – CGT and SDLT Cases 12. Residual Approach – Claims under Part 8, Corporation Tax Act 2009 13. Leasehold Interests 14. Examples Appendix 1 - Examples

1

1. Background

1.1 An apportionment of the price paid for a business as a going concern between the underlying assets may be required for tax purposes in a number of instances, for example:

a. For the purpose of calculating the capital gain arising on the disposal

of the separate assets in accordance with the Taxation of Chargeable Gains Act (TCGA) 1992.

b. On an acquisition for the purpose of calculating the Stamp Duty Land

Tax (SDLT) due on the interest in the land and buildings only.

c. On an acquisition for the purpose of calculating the allowances available under the Capital Allowances Act 2001, such as Machinery and Plant Allowances.

d. On acquisition of goodwill for the purpose of Part 8, Corporation Tax

Act 2009 (formerly Schedule 29 of the Finance Act 2002).

1.2 The price paid for a business sold as a going concern may include any or all of the following assets:

a. The land and buildings including landlord’s fixtures (‘the property’). b. The trade fixtures, fittings, furniture, furnishings and equipment (‘the

chattels’).

c. Any transferable licences.

d. Goodwill

e. Other separately identifiable intangible assets (e.g. registered trade marks).

The purchaser may also separately acquire consumables and stock but these are usually valued separately and will not normally be included in the sale price to be apportioned.

1.3 Some of the principles set out in this Practice Note are applicable to

apportionments for all types of businesses but the note deals mainly with the particular issues that have arisen where the property is a ‘trade related property’ valued using a profits approach, e.g. public houses, hotels, petrol filling stations, cinemas, restaurants, care homes etc (see paragraph 4 below). In these cases there can be particular difficulties in identifying the sum attributable to ‘goodwill’ and this is fundamental to the apportionment.

2. The Statutory Provisions

2.1 For the purposes of calculating a capital gain s.52 of the TCGA 1992 provides that any apportionment shall be on a ‘just and reasonable’ basis.

2

2.2 For the purposes of calculating any SDLT due paragraph 4, Schedule 4, FA 2003 similarly provides that any apportionment shall be on a ‘just and reasonable’ basis (subject to other provisions of the Capital Allowances Act).

2.3 For the purposes of calculating any Capital Allowances claimed s.562 CAA 2001 similarly provides that any apportionment should be on a just and reasonable basis unless other specific provisions disapply the application of s.562 in whole or in part.

2.4 For the purpose of calculating the cost of purchased goodwill Part 8 of the

Corporation Tax Act 2009 (CTA 2009) provides that ‘goodwill’ has the meaning it has for accounting purposes1. Accounting guidance (FRS210) provides that ‘purchased goodwill’ should be taken to be the "difference between the cost of an acquired entity and the aggregate of the fair values of that entity's identifiable assets and liabilities" (see paragraph 12 below).

2.5 Unlike the Capital Gains, SDLT and Capital Allowances provisions which

provide for an apportionment approach, the starting point for Part 8 of CTA 2009 is to consider whether the accounts are prepared in accordance with generally accepted accounting practice (GAAP)3. Where accounts are not GAAP compliant the “purchased goodwill” is to be calculated as if the company has prepared GAAP compliant accounts.

An apportionment adjustment under s.856(4) CTA 2009 can only be made in the circumstances where assets have been acquired together with other assets as part of one bargain and the values allocated to those particular assets have not already been allocated a value in accordance with GAAP i.e. fair value.

In practice, apportionment is only required in limited circumstances. For example if a company has not applied acquisition accounting, or not applied acquisition accounting correctly, and that failure is material (i.e. accounts are not GAAP compliant) the adjustment is to be made under section 717(1) CTA 2009. However, if that failure is not material (so the accounts remain GAAP compliant) then the adjustment will be made under section 856(4) CTA 2009.

2.6 The various statutory provisions do not define the method of arriving at a ‘just

and reasonable’ apportionment but any apportionment should generally seek to apportion the price paid between the underlying assets included in the sale on the basis of their relative values and the contribution they make to the price that is being apportioned.

3. Legal Definitions of Goodwill

3.1 Halsbury's Laws of England, 4th edition, Vol. 35 at page 1206 states that:

“The goodwill of a business is the whole advantage of the reputation and connection with customers together with the circumstances whether of habit or

1 Section 715(3) CTA 2009. 2 Financial Reporting Standard. 3 This note does not take account of the recently issued UK accounting standard, FRS 102, approved by the Financial Reporting Council in March 2013. This is only mandatory for accounting periods beginning on or after 1 January 2015, although it may be adopted early if desired. It is not expected there should be significant differences in practice to the principles applicable under existing UK GAAP.

3

otherwise, which tend to make that connection permanent4. It represents in connection with any business or business product the value of the attraction to the customers which the name and reputation possesses5.”

3.2 The definition contained in the Shorter Oxford Dictionary is:

“Goodwill is the privilege granted by the seller of a business to a purchaser of trading as his recognised successor; the possession of a ready-formed connection with customers considered as a separate element in the saleable value of a business.”

3.3 The leading legal authority on the meaning of goodwill is found in IRC v Muller

& Co Margarine Limited [1901] AC 217. In answer to the question "what is goodwill?" Lord Macnaghten said:

“It is a thing very easy to describe, very difficult to define. It is the benefit and advantage of the good name, reputation and connection of a business. It is the attractive force which brings in custom. It is the one thing which distinguishes an old-established business from a new business at its first stage.”

Lord Macnaghten went on to say that:

“Goodwill is composed of a variety of elements. It differs in its composition in different trades and in different businesses in the same trade. One element may preponderate here; and another there.”

3.4 In the decision of the Special Commissioners in Balloon Promotions Ltd v

Wilson, SpC 524 [2006] STC (SCD) 167, goodwill for CG purposes was construed in accordance with legal rather than accountancy principles.

3.5 Traditionally goodwill has been subdivided into different types such as

‘inherent goodwill’, ‘adherent goodwill’ and ‘free goodwill’. These subdivisions are no longer considered helpful as they tend to cause confusion. ‘Inherent’ and ‘adherent’ goodwill are not really goodwill at all as they form part of the value of the property asset and are properly reflected within such.

4. Trade Related Properties

4.1 ‘Trade related property’ (TRP) is defined in the Royal Institution of Chartered Surveyors (RICS) Guidance Note 2 (GN2) as “any type of real property designed for a specific type of business where the property value reflects the trading potential for that business”6. Examples include hotels, public houses, restaurants, nightclubs, casinos, cinemas, theatres, care homes and petrol filling stations.

4.2 The essential characteristic of this type of property is that it has been

designed or adapted for a specific use where the property value is usually

4 See Trego v Hunt [1896] AC 7 at 16, 17, 23, 27, HL and H P Bulmer Ltd and Showerings Ltd v J Bollinger SA [1977] 2 CMLR 625, CA. 5 R J Reuter Co Ltd v Ferd Mulhens [1954] Ch 50 at 89, [1953] 2 All ER 1160 at 1179, CA per Evershed MR. 6 © Royal Institution of Chartered Surveyors (RICS)

4

intrinsically linked to the returns an owner or occupier can generate from such use.

4.3 TRPs are often individual and exhibit unique features in terms of their location,

character, size, consents and levels of adaptation or construction specific to their particular use. It is these features that lead to the need for specific valuation treatment within the valuation profession, often utilising a profits based methodology to determine market value. (This involves estimating the ‘trading potential’ of the property.)

4.4 ‘Trading potential’ is defined in the RICS GN2 as “the future profit, in the

context of a valuation of the property, that a reasonably efficient operator would expect to be able to realise from occupation of the property. This could be above or below the recent trading history of the property. It reflects a range of factors such as the location, design and character, level of adaptation and trading history of the property within the market conditions prevailing that are inherent to the property asset”7.

4.5 ‘Reasonably efficient operator’ (REO) is defined as “a concept where the

valuer assumes that the market participants are competent operators, acting in an efficient manner, of a business conducted on the premises. It involves estimating the trading potential rather than adopting the actual level of trade under the existing ownership, and it excludes personal goodwill”8. Assessing the trading potential of the property will therefore entail a review of the existing operator’s trading accounts and comparing the actual trading performance with that of similar trade related property types and styles of operation. The trading performance expected by a reasonably efficient operator may be the same as, greater than or less than the actual trading performance.

5. Goodwill in Trade Related Properties

5.1 It has in the past been argued that because the business in TRPs is usually largely or wholly incapable of being sold separately from the property there is little or no goodwill (see the Lands Tribunal decision in Coles Executors v IRC (1973) concerning the valuation of a public house for Estate Duty). On the sale of a business operated from such properties, unless there were other separately identifiable intangible assets included in the sale, the whole of the purchase price would normally be apportioned to the property and chattels, it being argued that there was no goodwill.

5.2 The above view was often put forward by purchasers seeking to claim Capital

Allowances on fixtures which formed part of the property. However, since the introduction of SDLT and the provisions now contained in Part 8 CTA 2009, HMRC has seen increasingly large sums apportioned to goodwill (away from the underlying property) in order to maximise the claim under Part 8 CTA 2009 and minimise the amount of SDLT payable.

5.3 HMRC accept that if a business is sold as a going concern the sale may

include some element of goodwill. The question to be answered is not whether

7 © Royal Institution of Chartered Surveyors (RICS) 8 © Royal Institution of Chartered Surveyors (RICS)

5

goodwill exists, but what is the value of that goodwill? That question has to be decided on the facts of each individual case and will vary depending on the type of property and use. In some cases the value of the goodwill may be nominal but in some it may be substantial.

6. Valuing Goodwill

6.1 There is a broad measure of agreement across the valuation, accountancy and legal professions that the value of goodwill is represented by the difference between the value of a business as a going concern and the value of the separately identifiable assets included in the sale. HMRC consider that the value of any goodwill in trade related properties should be arrived at by deducting the value of the separately identifiable assets included in the sale from the value of the business as a going concern.

6.2 The value of a business as a going concern will usually be represented by the

actual sale price achieved in the open market. However, if it is necessary to value a business as a going concern, because the sale price was not at arm’s length, then this is the responsibility of HMRC (SAV).

6.3 The value of the tangible assets is the responsibility of the VOA. If it is

necessary to value any other intangible assets (e.g. registered trademarks) included in the sale then this is the responsibility of HMRC Shares and Assets Valuation.

6.4 When the deductive method of arriving at the value of goodwill is adopted

difficulties may arise over the appropriate assumptions to be adopted when arriving at a valuation of the other business assets. This is addressed in the paragraphs below.

7. Valuing the Tangible Assets - Assumptions

7.1 Difficulties relating to the assumptions to be adopted when valuing the tangible assets often arise in cases involving TRPs. Some of the reasons for this are:

a. The established approach to valuation of this type of property typically

relies on ‘the profits method’ (see paragraph 8 below). In applying this valuation method there can sometimes be confusion in distinguishing the income and trading potential that runs with the operational property from any additional income arising from the actual operator’s business.

b. The value of such properties is often significantly reduced if the

property ceases to be occupied for any length of time because customers go elsewhere and the purchaser has to rebuild the level of trade. The enhanced value that arises as a result of the property having been occupied by the vendor and any predecessors for the particular use (ie. the property’s trading history) is part of what was previously described as ‘adherent’ goodwill but is properly part of the property value and is reflected in the property’s ‘trading potential’,

6

c. The property value is often significantly reduced if the property is stripped of chattels because the purchaser has to re-fit the premises before being ready to trade.

d. It can sometimes be difficult to obtain new licences where these have

been lost.

7.2 The valuation of the tangible assets must reflect the facts at the valuation date and not, for example, treat the property as stripped of chattels and empty of occupiers when it was not. There should be no assumption of an empty and bare property unless that is representative of the facts. If, contrary to the evident facts, it were to be assumed for the purposes of valuation that the property has lost any licences, been stripped of chattels and left vacant for a period of time then the value will be significantly reduced and the value of goodwill in the final apportionment, arrived at by deduction, would be unreasonably inflated. An assumption of vacant possession does not imply that the property is empty, but that physical and legal possession will pass on completion. Any parts of the property occupied by third parties is a matter of fact for consideration within the valuation. For example, in relation to care homes the presence of residents occupying under short terms licences at the valuation date will be a consequence of the property’s established use and a fact to be reflected in the property valuation. The valuer, or a purchaser, would nevertheless still have to make a judgement as to how many residents may choose to remain on a change of ownership. This may affect the timing and level of anticipated income to be reflected in the valuation.

7.3 When arriving at the value of goodwill using the approach outlined in paragraph 6 above, if all the tangible assets are included in the sale, it will usually be appropriate to value all the tangible assets together for sale as an ‘operational entity’ so that a purchaser can, if they wish, trade from the day of purchase . It is critical that this possibility is reflected to ensure a fair apportionment of the sale price (and any premium arising from a sale of combined assets) between the tangible and intangible elements so as to avoid any over or understatement.

7.4 The valuation of the property should have regard to any established use or

trading history up to the valuation date as this may influence both the timing and level of future income a purchaser would expect. A property that has been operational up to the date of valuation is likely to have a higher value than one that has been empty for six months because the purchaser will anticipate greater certainty and immediacy of a trading income stream due to continued customer patronage. Established use provides the likelihood of sustaining a level of use and income generation for the REO and reduces the risk of delay - a running start rather than a cold start.

7.5 Where the business is sold as a going concern, the benefit of contracts

entered into by the vendor with customers, staff and suppliers will normally pass to the purchaser and be reflected in the price paid for the business. However, these contracts do not form part of the tangible assets so, if they add any value, the added value should not be reflected in the valuation of the tangible assets. For example, in relation to a care home, prior to the sale the residents would have contracts with the owner to reside at the property and those contracts cannot be assumed to pass to a purchaser of the property.

7

However, many of the existing residents may wish to continue to reside in the property following any change of ownership and those residents would be free to enter into new contracts with the purchaser. Equally the purchaser of the property may be prepared to pay an additional sum to the vendor (over and above the property value) to acquire these contracts if it is perceived they provide greater certainty and immediacy of full trading incomes (that is goodwill or business value).

7.6 When arriving at the value of goodwill using the approach outlined in

paragraph 6 above it is considered appropriate to assume that the benefit of any contracts with customers, staff and suppliers would either have to be acquired separately from the vendor or the purchaser would have to make their own arrangements. It would be open to a purchaser to make their own arrangements with any existing customers, staff and suppliers who would be likely to be happy entering into new contracts following a change of ownership. For example, in relation to a public house, the existing operator may be achieving a higher than expected profit margin because of a favourable supply contract with a brewery. It cannot be assumed that the contract with the brewery would pass to a purchaser of the property but the purchaser may be able to enter into a similar contract with the existing supplier or another brewery in which event this will be reflected within the market bid for the property interest. This will be a matter of judgement on the facts and the market prevailing.

7.7 Applying the assumptions in paragraph 7.4 will have different effects depending on the facts in each particular case. For example:

a. A small public house to be run by the purchaser with help from part-

time bar staff. The purchaser has acquired the business as a going concern but there are no contracts with customers and the purchaser wishes to enter their own contracts with suppliers and employ their own staff. In such a case there may be no identifiable difference between the price paid for the business as a going concern and the price that a purchaser would pay to acquire all the tangible assets. In such a case the value of the goodwill may be nominal.

b. A specialist care home that is fully occupied by residents and is to be

run by the purchaser with the help of full-time qualified staff. There may be a difference between the price paid for such a business as a going concern and the price a purchaser would pay to acquire all the tangible assets, depending on the degree of difficulty the purchaser might anticipate in securing full occupancy and staffing (see paragraph 8.3 below). In such a case the value of the goodwill may be more substantial.

7.8 When purchasing such a business as a going concern the purchaser will often

have obtained a valuation of the tangible assets as an ‘operational entity’ in accordance with the RICS GN2 (see paragraph 10 below). In addition, an alternative valuation of the property based on special assumptions (e.g. vacant following a failure of the business, no accounts providing evidence of trade, stripped of chattels and licences lost) may also be obtained for bank lending purposes. For the purposes of calculating the value of goodwill it would not be appropriate to deduct a valuation based on such special assumptions that do not reflect the actual circumstances prevailing at the valuation date. It is important to recognise that the valuation of the property as

8

an ‘operational entity’ is a value of the property with chattels and readily available licences and is not a valuation of the actual business as a going concern (see paragraph 10 below). Whilst GN2 states that it does not apply to apportionments for tax purposes, HMRC/VOA consider that for the purpose of arriving at the value of goodwill (see paragraph 11.2, Step 2, below), it should normally be acceptable to deduct a GN2 valuation of the ‘operational entity’ as reflecting the established valuation approach to properties of this nature. RICS UKGN 3 provides guidance on valuations and apportionments for tax purposes and HMRC/VOA consider that, if all the tangible assets are prudently lotted together as an operational entity, a valuation in accordance with UKGN 3 would not give a lower figure.

8. Valuing the Tangible Assets – the Profits Approach

8.1 When valuing the tangible assets of an operational TRP, the aim should normally be to arrive at a capital value that fairly represents the price that an owner-occupier purchaser would be prepared to pay to acquire all the tangible assets together, having regard to the circumstances existing at the valuation date. Having decided on the appropriate assumptions (see paragraphs 7.3 - 7.6 above) it is then necessary to consider the most appropriate method of valuation. The appropriate method of valuation is a matter for the valuer having regard to the facts, but most TRPs are valued using the profits method of valuation. This valuation method requires consideration of both the level and timing of estimated trading income and is described in detail in the RICS GN2 but essentially it involves the following:

The valuer makes an assessment of the fair maintainable turnover

(FMT) that could be generated by a reasonably efficient operator (REO) of the ‘operational entity’ that is fully equipped and ready to trade.

From this an assessment is made of the fair maintainable operating

profit (FMOP) reflecting the costs to be expected by a REO.

The market value of the property as an operational entity is then assessed by capitalising the FMOP at an appropriate rate of return reflecting the risks and rewards of the property and its trading potential.

8.2 A valuation of the tangible assets using the profits method has the following

advantages: a. it is widely used in the market to arrive at both going concern values

and valuations of the tangible assets as an operational entity under the RICS GN2.

b. it represents the value to an owner-occupier purchaser. c. the purchase price paid for the going concern and any GN2 valuation

of the tangible assets as an operational entity can be analysed to provide evidence of the FMT/FMOP and a multiplier for the actual subject property at the valuation date.

9

d. it produces a value for all the tangible assets to be valued together as a single operational entity.

8.3 When assessing the FMT/FM OP it must be remembered that in cases where

the existing contracts with customers, staff and suppliers are of some additional value it is necessary to have regard to this in the valuation. A valuer looking to determine the value of the operational property alone may have to make difficult judgements on whether staff and customers would choose to stay with the property or would realistically take their custom elsewhere if the property were to change hands. Whether this affects the value of the property or not will depend on the facts of the case and the market conditions prevailing at the valuation date. In cases where it is considered that there may be some delay before the REO could achieve the expected FMT/FMOP, this may either be reflected in the rate of return at which the FMT/FMOP is capitalised or a more specific discount may be made to reflect the reduced FMT/FMOP during the period whilst the trade is built up to the expected level.

9. Valuing the Tangible Assets – the Investment Method

9.1 A valuation based on the investment method (capitalising an estimated rental value) may be useful in some cases but as a primary method of valuation in apportionment cases the difficulties and flaws of this method are as follows: a. arriving at the capital value involves making difficult judgements not

only about the FMT/FMOP but also the percentage of profits to adopt as the rental value and the appropriate investment yield, both of which can only be derived from comparison with lettings and sales of other properties at different dates, which significantly increase the scope for disputes over the analysis and comparability of the evidence.

b. the available comparable rental evidence will relate to new lettings of

properties that have either not previously been let, have been vacant or have had rent reviews/renewals that disregard the occupation of the property by the tenant and predecessors in title in accordance with s.34 Landlord and Tenant Act 1954.

c. the approach requires the valuer to assume a hypothetical lease is in

place which introduces the possibility of a range of hypothetical assumptions as to the nature of the lease and associated terms, each of which could result in a different valuation conclusion.

d. the comparable rental evidence will relate to lettings where the tenant

has had to provide the chattels and the return on this capital and risk is reflected in the rents paid.

e. the valuation using this approach represents the value of the property

to an investor not an owner-occupier: the RICS GN2, paragraph 8.3, notes that the capitalisation rate adopted for investment valuations differs from that for vacant possession values.

f. the valuation produces a valuation of the property only to which it

is then necessary to add a valuation of the chattels. It will not include the premium value to an occupier of acquiring the tangible assets together as a package with the enhanced trading potential due to the

10

established trading history and the ability to continue trading from day one. Isolating the bare property asset may unfairly apportion any premium or share of marriage value away and overstate the intangible elements.

9.2 However, in cases where there are particular difficulties in arriving at a valuation using the profits method the investment method may provide a guide as to the minimum value of the property to an incoming purchaser.

Example

A simple example of the problems with the rental approach may be illustrated by considering a small public house like the one described in paragraph 7.7(a) above: Say the property was trading at no more than FMT/FMOP level, it had been sold as a going concern for £1m and an analysis of this sale price was say FMOP £125k pa x 8YP (Years Purchase). For illustration purposes, the rental value on a new letting without chattels may be say £62,500 and an investment yield may be say 8%. This would give a capital value of £781,250 leaving a balance of £218,750. If the in situ value of the chattels was say £50,000 this would leave a sum of £168,750 being attributed to the goodwill when in reality most valuers would agree that the purchaser had acquired nothing of any value beyond the value of the tangible assets. The excess is artificially created because the valuation of the property reflects its notional investment value whereas, just as with some other classes of property, the owner-occupier market is influenced by different factors and the price an owner-occupier may pay is not always the same as an investor.

10. RICS Red Book GN2 - Valuations of the ‘Operational Entity’

10.1 As indicated above, when purchasing a business operated from a TRP as a going concern the purchaser will often have obtained a valuation of the tangible assets as an ‘operational entity’ in accordance with the RICS Red Book GN2 - Valuation of Individual Trade Related Properties. The new GN2 (issued in May 2011) has helpfully clarified some of the areas of uncertainty that existed in the old GN1 that it replaced.

10.2 The guidance makes it clear that a valuation in accordance with GN2 should

relate only to the valuation of an individual property valued on the basis of trading potential. The valuation is of the property as a 'place to do business', not a valuation of the actual business itself. Valuations of businesses are covered in separate guidance. GN2 makes it clear that the trading potential of the property should be properly reflected within the property value and that the current operator’s goodwill (personal goodwill) is not to be reflected.

10.3 GN2 also makes it clear that the ‘operational entity’ “usually includes:

the legal interest in the land and buildings; the trade inventory, usually comprising all trade fixtures, fittings,

furnishings and equipment; and

11

the market’s perception of the trading potential, together with an assumed ability to obtain/renew existing licences, consents, certificates and permits.”9

10.4 Whilst GN2 states that it does not apply to apportionments for tax purposes,

HMRC/VOA consider that for the purpose of arriving at the value of goodwill (see paragraph 11.2, Step 2, below), it should normally be acceptable to deduct a GN2 valuation of the ‘operational entity’ as reflecting the established valuation approach to properties of this nature.

10.5 GN2 provides guidance on the valuation of individual TRPs. When

establishing the value of a portfolio of properties (whether they be TRPs or not), it is important to consider whether the sum of individual values would be enhanced by a portfolio premium (see RICS GN3).

.

11. Apportionment Approach – CGT and SDLT cases

11.1 In CGT and SDLT cases the apportionment of the sale price paid for a business as a going concern should be approached by first identifying the value of any goodwill (and other separately identifiable intangibles assets) along the lines described in paragraphs 6 – 10 above. After deducting this from the total sale price, the in-situ value of the chattels may then be deducted to leave the value of the property.

11.2 In practice, to arrive at the sum attributable to the property, the approach outlined in paragraph 11.1 above will involve the following steps:

Step 1 - Estimate the market value of all the tangible assets together as an operational entity having regard to the guidance above. (See paragraph 11.3 below.)

Step 2 - Identify the sum attributable to goodwill and any other

intangible assets included in the sale by deducting the value of the property, licences and chattels (Step 1 value) from the sale price (or market value) of the business as a going concern. (See paragraph 11.4 below.)

Step 3 - Identify the sum attributable to the chattels by

estimating their ‘in-situ’ value (i.e. the value to an incoming purchaser. (See paragraph 11.5 below).

Step 4 - Identify the sum attributable to the property by

deducting the value of the chattels (Step 3 value) from the Step 1 value. (See paragraph 11.6 below).

Step 5 - Stand back and consider whether the answer produced

is reasonable in the particular circumstances of the case. (See paragraph 11.7 below).

11.3 Step 1

9 © Royal Institution of Chartered Surveyors (RICS)

12

The market value of the tangible assets should be assessed as at the date of disposal/sale on the basis defined in UKGN3 (Valuations for CGT, IHT and SDLT) reflecting the assumptions in paragraphs 7.2 and 7.4 above. HMRC/VOA consider that, for the purpose of arriving at the value of goodwill, it should normally be acceptable to deduct a GN2 valuation of the ‘operational entity’.

In particular the valuation should reflect the following:

a. the market's perception of the trading potential of the property

excluding the actual operator’s goodwill (and any ‘super profits’ beyond the expected FMT).

b. the benefit of any transferable licences, consents and certificates. (If

any of the licences etc have been lost or are in jeopardy at the valuation date that fact should be reflected in the valuation)10.

c. all the facts pertaining at the valuation date such as the availability of

possession, the fact that the property is fully equipped and ready to trade, the fact that the property was in use up to point of transfer etc.

d. the assumption that any accounts available to the purchaser are

available at the valuation date to inform judgments as to reasonable future trading potential.

e. that the purchaser may either bring in their own staff or seek to re- employ some of the existing staff.

f. that the purchaser will take into account the likelihood of any future bookings sticking with the property if they choose to run the business in the same manner as the vendor.

g. that the purchaser will take into account the likelihood of any existing care home residents opting to stay with the property if they choose to run the business in the same manner as the vendor.

11.4 Step 2

The sum attributable to goodwill and any other intangible assets included in the sale should be arrived at by deducting the value of the tangible assets (from Step 1 above) from the sale price (or market value) of the business.

11.5 Step 3

The sum attributable to any chattels included in the sale should be arrived at

by estimating the value of the chattels to an incoming purchaser. The value of the chattels to an incoming purchaser will normally be based on their depreciated replacement cost but in some cases they may be of no value, for example, if the purchaser intends to refit the premises.

10 Some licences may be a separate asset for CGT purposes

13

11.6 Step 4

The sum attributable to the property should be arrived at by deducting the value of the chattels (the Step 3 value) from the value of the tangible assets (the Step 1 value).

11.7 Step 5

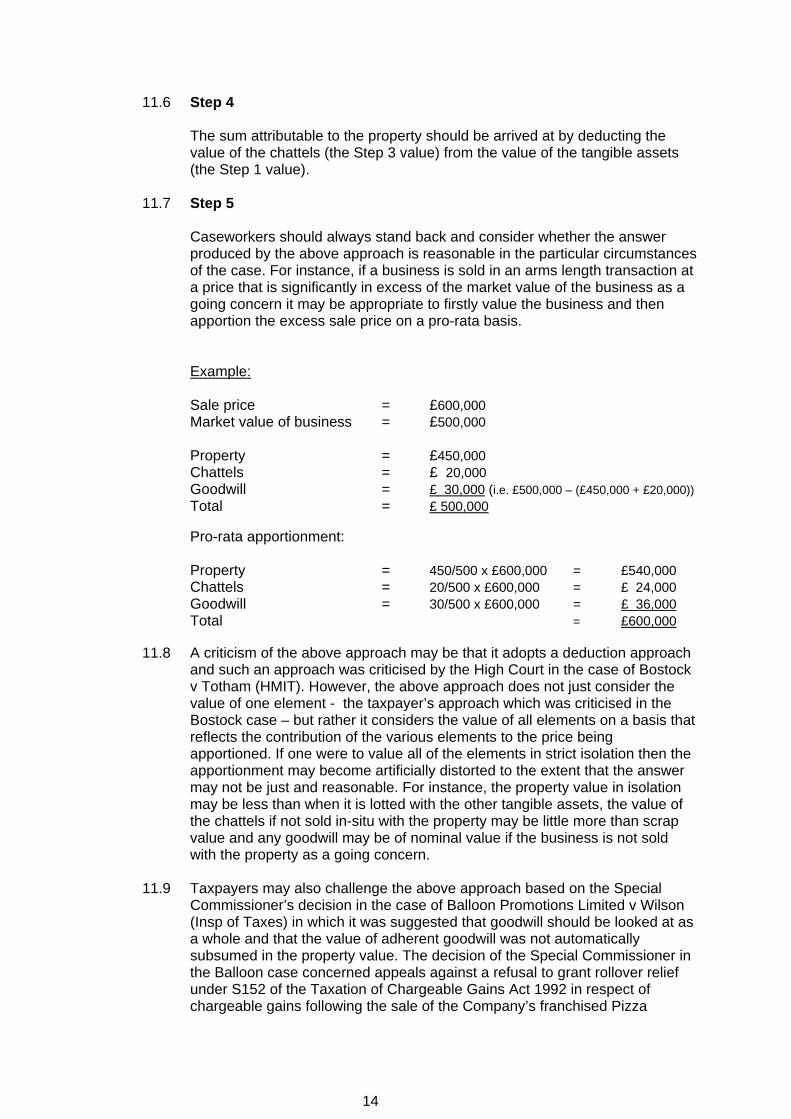

Caseworkers should always stand back and consider whether the answer produced by the above approach is reasonable in the particular circumstances of the case. For instance, if a business is sold in an arms length transaction at a price that is significantly in excess of the market value of the business as a going concern it may be appropriate to firstly value the business and then apportion the excess sale price on a pro-rata basis.

Example: Sale price = £600,000 Market value of business = £500,000

Property = £450,000 Chattels = £ 20,000 Goodwill = £ 30,000 (i.e. £500,000 – (£450,000 + £20,000))

Total = £ 500,000 Pro-rata apportionment: Property = 450/500 x £600,000 = £540,000 Chattels = 20/500 x £600,000 = £ 24,000 Goodwill = 30/500 x £600,000 = £ 36,000

Total = £600,000

11.8 A criticism of the above approach may be that it adopts a deduction approach and such an approach was criticised by the High Court in the case of Bostock v Totham (HMIT). However, the above approach does not just consider the value of one element - the taxpayer’s approach which was criticised in the Bostock case – but rather it considers the value of all elements on a basis that reflects the contribution of the various elements to the price being apportioned. If one were to value all of the elements in strict isolation then the apportionment may become artificially distorted to the extent that the answer may not be just and reasonable. For instance, the property value in isolation may be less than when it is lotted with the other tangible assets, the value of the chattels if not sold in-situ with the property may be little more than scrap value and any goodwill may be of nominal value if the business is not sold with the property as a going concern.

11.9 Taxpayers may also challenge the above approach based on the Special

Commissioner’s decision in the case of Balloon Promotions Limited v Wilson (Insp of Taxes) in which it was suggested that goodwill should be looked at as a whole and that the value of adherent goodwill was not automatically subsumed in the property value. The decision of the Special Commissioner in the Balloon case concerned appeals against a refusal to grant rollover relief under S152 of the Taxation of Chargeable Gains Act 1992 in respect of chargeable gains following the sale of the Company’s franchised Pizza

14

Express restaurants to the franchisor. Whilst the decision includes discussion of existing legal authorities dealing with goodwill the conclusions reflect the particular circumstances of the case. It is worth noting that in this case the values of the property interests submitted by the taxpayers were not challenged and there was no evidence to demonstrate whether or not those values included adherent goodwill. As previously mentioned, the subdivisions of goodwill that were previously used are no longer considered helpful as they tend to cause confusion. The view now is that what used to be referred to as ‘inherent’ and ‘adherent’ goodwill are, in reality, attributes which add value to the property in which a business is carried on and that they do not represent goodwill at all.

12. Residual Approach – Part 8 CTA 2009 cases

12.1 As noted above (paragraph 2.4), for the purpose of calculating the cost of purchased goodwill Part 8 CTA 2009 provides that ‘goodwill’ has the meaning it has for accounting purposes. UK GAAP (FRS10 Goodwill and intangible assets) provides that ‘purchased goodwill’ should be taken to be the "difference between the cost of an acquired entity and the aggregate of the fair values of that entity's identifiable assets and liabilities. Positive goodwill arises when the acquisition cost of the entity exceeds the aggregate fair values of the identifiable assets and liabilities. Negative goodwill arises when the aggregate fair values of the identifiable assets and liabilities of the entity exceed the acquisition cost". Thus, purchased goodwill recognised for accounting purposes is a ‘residual’11. For the avoidance of doubt, purchased goodwill only arises for accounting purposes where there has been a business acquisition (combination).

12.2 UK GAAP (FRS 7 Fair values in acquisition accounting) requires fair values to be used in measuring the identifiable assets and liabilities of an acquired business at the date of acquisition and that the identifiable net assets which should be recognised (as forming part of the business combination) to be measured at fair values that reflect conditions at the date of acquisition. FRS 7, para. 9 requires that the fair value of a tangible fixed asset should be based on: a. market value, if assets similar in type and condition are bought and

sold on an open market [as here]; or b. depreciated replacement cost [generally not applicable here].

12.3 In determining what is meant by ‘market value’ within FRS 7, FRS 15

(Tangible fixed assets) is instructive, paragraphs 53 and 56 in particular (notwithstanding they are in the section of the standard dealing with revalued properties). FRS 15 is authoritative literature which explains what is meant by ‘market value’ in the context of valuing property. Paragraph 85 also provides support that for TRPs trading potential is reflected within the value of, and is inseparable from, the property.

11 IFRS 3, (Appendix A) defines goodwill as; “[a]n asset representing the future economic benefits arising from other assets acquired in a business combination that are not individually identified and separately recognised”.

15

FRS 15, para. 53 (inter alia) states:

“The following valuation bases should be used for revalued properties that are not impaired: (a) non-specialised properties should be valued on the basis of existing use value (EUV) …”.

FRS 15, para. 56 states:

“Certain types of non-specialised properties are bought and sold, and therefore valued, as businesses. The EUV of a property valued as an operational entity is determined by having regard to trading potential, but excludes personal goodwill that has been created in the business by the present owner or management and is not expected to remain with the business in the event of the property being sold”.

FRS 15, para. 85 states:

"It would not be appropriate, however, to treat the trading potential associated with a property that is valued as an operational entity, such as a public house or hotel, as a separate component where the value and life of any such trading potential is inherently inseparable from that of the property".

Therefore, for non-specialised properties (which include TRPs), HMRC considers the use of an EUV basis of valuation is required by UK GAAP in the context of the fair value exercise in a business acquisition. Furthermore, there is support for using EUV to determine the fair value of non-specialised properties in PwC’s Manual of accounting (UK GAAP). This, inter alia, states that “in acquisition accounting, properties that would normally be valued under the alternative accounting rules [i.e. within the revaluation option within FRS 1512] on an existing use value basis in the acquired company’s financial statements (that is those occupied for the purpose of the business) would also usually be valued on this basis in the fair value exercise”13. Although PwC add that “there may be some confusion as to what market value means… The most commonly used bases are market value and existing use value”14, they go on to comment that “existing use value is the basis normally used for valuing properties that are occupied in the company's business …”15.

12.4 For companies preparing accounts under IFRS16, the relevant accounting standards are IFRS 3 (Business Combinations), IFRS 13 (Fair Value Measurement) and IAS 16 (Property, Plant and Equipment). In general, though in particular circumstances there may be exceptions (e.g. market value and fair value may not be the same), it is not considered likely in relation to TRPs there will be substantial differences between accounts drawn up under

12 HMRC comment within parentheses. 13 2012 edition, see paragraph 25.267. 14 2012 edition, see paragraph 25.262. 15 2012 edition, see paragraph 25.265. 16 International Financial Reporting Standards.

16

UK GAAP and IFRS (unless, in IFRS, market or other factors suggest that a different use by market participants would maximise the value of the asset).

12.5 ‘Negative goodwill’ (i.e. a gain resulting from a bargain purchase) can arise,

under both UK GAAP and IFRS. Within UK GAAP, negative goodwill is carried on the balance sheet and recognised in the profit and loss account in the periods in which non-monetary assets are recovered (by depreciation or disposal) or in which the benefits are expected to be realised. Within IFRS, however, the gain resulting from a bargain purchase is recognised in profit or loss on the acquisition date.

12.6 In HMRC’s view, for TRPs, the EUV of the tangible assets required for the

purpose of calculating the cost of purchased goodwill under Part 8 CTA 2009 will normally be represented by the market value of the assets as an operational entity, in accordance with the guidance contained in the RICS GN2.

13. Leasehold Interests

13.1 In some cases it will be necessary to apportion the price paid for a leasehold interest but the same principles apply. The valuations and apportionment should be approached using the same assumptions and approach described above.

13.2 It should be borne in mind that for TRPs it is not uncommon for leasehold

interests to be sold for substantial premiums even when the rent has recently been reviewed. The premium in such cases may be attributable to any or all of the following:

a. The reviewed rent may not reflect the full rental value because it may

disregard the enhanced trading potential attributable to the occupation of the property by the tenant and predecessors (in accordance with s.34 LTA 1954).

b. The reviewed rent may not reflect the value of improvements carried

out by the tenant or predecessors when fitting out the property (in some cases the rent may only represent a shell rent).

c. The value of the chattels and fittings belonging to the tenant. d. The premium value to an occupier of offering the tangible assets

together as a package with the enhanced trading potential due to the established trading history and the ability to continue trading from day one.

e. There may be some element of goodwill, particularly if the business is

trading at above FMT level and contracts of some value are included in the sale.

f. There may be other separately identifiable intangible assets included

in the sale (eg. registered trade marks).

17

g. Market perception and prevailing conditions whereby it is expected there will be some ‘key money’ or premium to acquire the interest in order to move in to this market sector or specific trading location.

13.3 The value of any goodwill and other intangible assets included in the sale

should be determined by adopting the same valuation assumptions and approach outlined in paragraphs 7 and 8 above.

14. Examples

14.1 Examples illustrating the application of the approaches outlined in paragraphs 11 and 12 above are set out in Appendix 1.

18

APPENDIX 1

Examples All the figures used in the examples below are for illustrative purposes only. Example 1 The Facts A owns and runs a public house. The business has been struggling for some years because the owner is nearing retirement and has lost interest in the business. The level of trade has fallen over the last 2 years and profit margins are low because wage costs are higher than would be expected due to overstaffing. The Figures The salient figures are as follows:-

FMT – the actual trade based on an average of the last two years accounts is only £445k pa but the estimated FMT (assuming a reasonably efficient operator17) is £500k pa.

FMOP – the actual operating profit is only £70k pa but the estimated FMOP18, reflecting lower wage costs, is £125k pa.

The business has been sold as a going concern for £875k. This price reflects the potential to increase the trade up to the FMOP level but also the possible delay before this level of trade could be achieved.

The chattels are included in the accounts at a net book value of £25k but their market value to an incoming purchaser would be £35k.

The market value of the property as an operational entity is £875k. This is based on a FMOP of £125k pa x 7 Years Purchase (YP).

The market value of the property based on ‘special assumptions’ is £450k (this assumes that the property has been empty and closed for 6 months, no trading accounts are available, the chattels have all been removed, the licences have been lost and a sale is required within 180 days).

The purchaser claims that the sum that should be attributed to goodwill is the purchase price less the separate values of the property (assuming it to be empty etc) and the chattels, ie. £875k – (£450k + £25k) = £400k.

Apportionment for SDLT Purposes

17 ‘Reasonably efficient operator’ is defined as “a concept where the valuer assumes that the market participants are competent (but not exceptional) operators, acting in an efficient manner, of a business conducted on the premises. It involves estimating the trading potential rather than adopting the actual level of trade under the existing ownership”. (© Royal Institution of Chartered Surveyors). 18 ‘Fair Maintainable Operating Profit (FMOP)’ is defined as “the level of profit, stated prior to depreciation and finance costs relating to the asset itself (and rent if leasehold), that the reasonably efficient operator (REO) would expect to derive from the fair maintainable turnover (FMT) based on an assessment of the market’s perception of the potential earnings of the property. It should reflect all costs and outgoings of the REO, as well as an appropriate annual allowance for periodic expenditure, such as decoration, refurbishment and renewal of the trade inventory” (© Royal Institution of Chartered Surveyors).

19

The HMRC/VOA approach to the apportionment required for SDLT purposes would be as follows:

The value of the goodwill, reflecting its value when sold with the property, is the sale price paid for the business as a going concern less the value of all the tangible assets as an operational entity. In this case that would be £875k - £875k = nil. However, as the business has been sold as a going concern something needs to be apportioned to goodwill so a nominal sum of £1 is adopted, leaving a net sale price of £874,999.

The sum attributed to the property is in this case the net sale price (£874,999) less the value of the chattels, reflecting their value when sold with the property (£35k), which is £839,999.

Calculation of Goodwill Figure for Relief Under Part 8 CTA 2009 The HMRC/VOA approach to the calculation of the sum paid for goodwill for the purposes of relief under Part 8 CTA 2009 would be as follows:

Price paid for the going concern less the value of the tangible assets as an operational entity, ie. £875k - £875k = nil.

Example 2 The Facts B owns and runs a public house. The business has been exceptionally well run for a number of years. The level of trade and profits are much higher than would be expected for a similar pub in this location. The Figures The salient figures are as follows:-

FMT – the actual trade based on an average of the last two years accounts is £600k pa but the estimated FMT (assuming a reasonably efficient operator) is only £500k pa.

FMOP – the actual operating profit is £180k pa but the estimated FMOP, reflecting typical profit margins, is only £125k pa.

The business has been sold as a going concern for £1.1m. This price reflects the purchaser’s belief that they can continue to operate the business in the same manner as the vendor and sustain at least a proportion of the exceptional actual level of profits.

The chattels are included in the accounts at a net book value of £25k but their market value to an incoming purchaser would be £40k.

The market value of the property as an operational entity (excluding exceptional profits) is £950k. This is based on a FMOP of £125k pa x 7.6 Years Purchase (YP) based on evidence of other sales and reflecting a sustainable volume of trade for the property.

The market value of the property based on ‘special assumptions’ is £550k (this assumes that the property has been empty for 6 months, no trading accounts are available, the chattels have all been removed, the licences have been lost and a sale is required within 180 days).

20

The purchaser claims that the sum that should be attributed to goodwill is the purchase price less the separate values of the property (assuming it to be empty etc) and the chattels, ie. £1.1m – (£550k + £25k) = £525k.

Apportionment for SDLT Purposes The HMRC/VOA approach to the apportionment required for SDLT purposes would be as follows:

The value of the goodwill, reflecting its value when sold with the property, is the sale price paid for the business as a going concern less the value of all the tangible assets as an operational entity. In this case that would be £1.1m - £950k = £150k.

The sum attributed to the property is in this case the value of the tangible assets as an operational entity (£950k) less the value of the chattels, reflecting their value when sold with the property (£35k), which is £915k.

Calculation of Goodwill Figure for Relief Under Part 8 CTA 2009 The HMRC/VOA approach to the calculation of the sum paid for goodwill for the purposes of relief under Part 8 CTA 2009 would be as follows:

Price paid for the going concern less the value of the tangible assets as an operational entity, ie. £1.1m - £950k = £150k.

Example 3 The Facts A owns and runs a modern residential care home. The business has been run in a reasonably efficient but not exceptional manner for a number of years. The occupancy rate, fees and level of profits are what would be expected for a similar residential care home in this location. The Figures The salient figures are as follows:-

FMT – the actual trade based on an average of the last two years accounts is £935k pa and this accords with the valuers estimate of FMT (assuming a reasonably efficient operator)

FMOP – the actual operating profit is £330k pa and the estimated FMOP is also £330k pa.

The business has been sold as a going concern for £2.3m. This price reflects the purchaser’s belief that they can continue to operate the business in the same manner as the vendor and maintain the actual level of trade. This is based on the actual operating profit of £330k pa x 7 Years Purchase (YP).

The chattels are included in the accounts at a net book value of £75k and their market value to an incoming purchaser would be £75k.

The market value of the property as an operational entity is £2.2m. This is based on a FMOP of £330k pa x 6.7 Years Purchase (YP). The YP reflects the risk that on a change of ownership some residents and staff may choose to move elsewhere and there may therefore be some delay before the full FMOP is achieved.

21

The market value of the property based on ‘special assumptions’ is £1.4m (this assumes that the property has been closed for 3 months, no trading accounts are available, the chattels have all been removed, the licences have been lost and a sale is required within 180 days).

The purchaser claims that the sum that should be attributed to goodwill is the purchase price less the separate values of the property (assuming it to be empty etc) and the chattels, ie. £2.3m – (£1.4m + £75k) = £825k.

Apportionment for SDLT Purposes The HMRC/VOA approach to the apportionment required for SDLT purposes would be as follows:

The value of the goodwill, reflecting its value when sold with the property, is the sale price paid for the business as a going concern less the value of all the tangible assets as an operational entity. In this case that would be £2.3m - £2.2m = £100k.

The sum attributed to the property is in this case the value of the tangible assets as an operational entity (£2.2m) less the value of the chattels, reflecting their value when sold with the property (£75k), which is £2.125m.

Calculation of Goodwill Figure for Relief Under Part 8 CTA 2009 The HMRC/VOA approach to the calculation of the sum paid for goodwill for the purposes of relief under Part 8 CTA 2009 would be as follows:

Price paid for the going concern less the value of the tangible assets as an operational entity, ie. £2.3m - £2.2m = £100k.

Example 4 The Facts B owns and runs a modern residential care home. The business has been very well run for a number of years with the owner working all hours. Whilst the occupancy rates, fees and level of profits are all higher than would be expected for a similar residential care home in this location, wage costs are lower than considered appropriate. The Figures The salient figures are as follows:-

FMT – the actual trade based on an average of the last two years accounts is £950k pa but the estimated FMT is only £900k pa.

FMOP – the actual operating profit is £400k pa but the estimated FMOP is only £330k pa.

The business has been sold as a going concern for £2.525 m. This price reflects the purchaser’s belief that they can continue to operate the business in the same exceptional manner as the vendor and maintain the actual level of occupancy, fees and profits. This is based on the actual operating profit of £400k pa x 6.3 Years Purchase (YP).

The chattels are included in the accounts at a net book value of £50k and their market value to an incoming purchaser would be £50k.

22

23

The market value of the property as an operational entity is £2.3m. This is based on a FMOP of £330k pa x 6.95 Years Purchase (YP). The YP reflects the risk that on a change of ownership some residents and staff may choose to move elsewhere and there may therefore be some delay before the full FMOP is achieved.

The market value of the property based on ‘special assumptions’ is £1.575m (this assumes that the property has been closed for 3 months, no trading accounts are available, the chattels have all been removed, the licences have been lost and a sale is required within 180 days).

The purchaser claims that the sum that should be attributed to goodwill is the purchase price less the separate values of the property (assuming it to be empty etc) and the chattels, ie. £2.525m – (£1.575m + 50k) = £1m.

Apportionment for SDLT Purposes The HMRC/VOA approach to the apportionment required for SDLT purposes would be as follows:

The value of the goodwill, reflecting its value when sold with the property, is the sale price paid for the business as a going concern less the value of all the tangible assets as an operational entity. In this case that would be £2.525m - £2.3m = £225k.

The sum attributed to the property is in this case the value of the tangible assets as an operational entity (£2.3m) less the value of the chattels, reflecting their value when sold with the property (£50k), which is £2.25m.

Calculation of Goodwill Figure for Relief Under Part 8 CTA 2009 The HMRC/VOA approach to the calculation of the sum paid for goodwill for the purposes of relief under Part 8 CTA 2009 would be as follows:

Price paid for the going concern less the value of the tangible assets as an operational entity, ie. £2.525m - £2.3m = £225k.