Embed Size (px)

Citation preview

WINTER 2017/2018

U P D A T E

Practical Implications of Investment Theory

Many investment principlesused to develop invest-ment portfolios are derived

from one investment theory — the Capital Asset Pricing Model(CAPM). What exactly is this theory and how does it apply to yourinvestments?

The CAPM was developed over50 years ago by Harry Markowitz,who won a Nobel Prize for his work.His theory centers on the conceptthat adding an asset to a port-folio that is not highly correlatedwith other assets in the portfolio canreduce the variation risk. Hisapproach evaluated how a particularasset would impact a portfolio’s riskand return. Whether it makes senseto add that investment to a portfoliodepends as much on how the asset’sreturn will vary with returns of otherportfolio assets as on its own returnprospects.

This theory provides the under-lying rationale for asset allocation.The key is the returns of differentassets do not behave in the samemanner during different economictimes, so adding different assets canreduce the volatility in that portfolio.

While the return of a diversifiedportfolio may be lower than that of investing solely in the best-performing asset, it is typicallyviewed as an acceptable trade-off for reduced risk. Many people havealso realized it is difficult to identify

Continued on page 2

THE CHENEY – EPLEY – WOLBECK GROUP

THE CHENEY – EPLEY – WOLBECK GROUP AT MORGAN STANLEY

401 Main Street, Suite 1000, Peoria, IL 61602309-671-2800800-527-3579 • 309-671-3710 Faxwww.morganstanleyfa.com/cheneyepleywolbeckgroup

News and AnnouncementsWelcome to the Winter Edition of our client newsletter. On behalf of the Cheney-Epley-

Wolbeck group at Morgan Stanley, I’d like to wish you and your family a MerryChristmas and Happy New Year!

As you may know, both of my kids, Claire and John, attend Butler University in Indi-ana-polis. Claire is a senior. She will graduate in May with her degree in Marketing and aminor in Strategic Communications. She intends to begin her working career after gradua-tion in Indiana-polis. John is a freshman and football player at Butler. He tore his meniscuswith about three weeks remaining in the season and is scheduled for knee surgery in lateDecember. He is currently in the Business Exploratory Program.

Our team has been busy this fall/early winter working on IRA required minimum distri-butions and tax-loss harvesting (to minimize taxes). Hiral is settling into her new role as anAdvisor. Tessa is learning her new marketing role, while Shayne and Flo handle the daily oper-ational functions.

The stock market has had a great year! Many wonder when the next serious downturnwill occur. The answer is no one knows for sure. Normally, more serious downturns areassociated with recession or a policy mistake by the Fed (i.e. raising interest rates too high).One item we’ll be watching is the slope of the yield curve. If short-term rates move higherthan long-term rates (inverted yield curve), this would be worth noting. Stock market peakshave occurred on average 731 days later. The average gain during that time, however, is40.86%! (Source: Bloomberg, Oct. 31, 2017) As short-term rates move higher, we expectlong-term rates to rise as well (avoiding an inverted yield curve). Rising rates aren’t likelyto kill the recovery or bull market any time in the near future. The bull market and the U.S.economy have further to run.

As always, please call or e-mail if we can be of assistance. Regards,

Senior Vice President – Wealth ManagementFinancial AdvisorFinancial Planning Specialist CRC1964878

The views expressed herein are those of the author and do not necessarily reflect the views of Morgan Stanley Wealth Management or its affiliates. All opinions are subject to change without notice. Neither the information provided nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Past performance is no guarantee of future results.

U P D A T E

Practical Implicationscontinued from page 1

the best-performing asset in anygiven year, so a diversified portfolioprovides more consistent returns.

Some of the investment implica-tions drawn from this theory include:

4A properly diversified portfoliowill combine assets that do not

have highly correlated returns. Thus,when one asset is declining, otherassets may be increasing or notdecreasing as much.

4Rather than focusing on eachinvestment’s risk, investors

should consider their portfolio’soverall risk.

4 Including a small percentage ofa volatile investment may not

increase a portfolio’s overall risk,provided that investment’s returns donot vary closely with other assets’returns in the portfolio.

4When small portions of stocksare added to an all-bond port-

folio, risk initially decreases eventhough stocks are more volatile thanbonds.

4 Investors should consider howvarying percentages of differ-

ent asset classes will affect their portfolio’s risk and return.Managing Your Portfolio

Consider this investment processto incorporate this theory:

4Determine your risk/returnpreferences. You should

assess the potential downside as wellas upside for various investments toget a feel for how much risk you cantolerate.

4Decide on an asset allocationmix. Your asset allocation

strategy represents your personaldecisions about how much of yourportfolio should be allocated to various investment categories. After

considering your risk tolerance, timehorizon for investing, and returnneeds, you can form a target assetallocation mix. Within broad invest-ment categories, make allocationdecisions for each category.

4 Select individual invest-ments. Investigate a wide

range of options, but make sure youunderstand the basics of each, exam-ining their risk types as well as theirhistorical rates of return.

4Rebalance periodically. Overtime, your asset allocation will

stray from your desired allocationdue to varying rates of return on yourinvestments. Determine how muchvariation you are willing to tolerate.If portions of your portfolio havestrayed more than that, you shouldtake steps to get your allocation inline.

Please call if you’d like to dis-cuss your investment portfolio inmore detail. 444

FR2017-0619-0011

How to Make Saving Part of Your Budget

I f you want to make headwaywith your savings, you need todo a number on your budget.

Many financial experts agree thatyou should focus on the 50/20/30rule of budgeting.

The basics of this budget rule isyou divide your take-home pay intothree categories:

4Necessities — 50% of yourbudget should go toward the

things that you need to live day-to-day, such as housing, food, utilities,transportation, etc.

4 Savings — 20% of yourbudget should go toward con-

tributions to your 401(k) plan orIRA, cash savings, and also to paydown debt. While something like acar payment is part of your necessi-ties budget, extra payments toreduce your debt faster should comeout of this portion of your budget.

4Lifestyle — 30% of yourbudget should go to things

you like to do, such as dining out,going to the movies, hobbies, aswell as short-term savings forthings like vacations.

A 20% savings rate will helpensure that you will have a comfort-able retirement. However, this is notan easy thing for most Americans

to do, especially when you con-sider the personal savings rate was only 5.5% in January 2017(Source: Tradingeconomics.com,January 2017).

The major issue is many can’tdistinguish between necessities andlifestyle choices. For example, a caris a necessity for most people, butthe type of car you purchase is oftena lifestyle choice. This is also truefor the type of housing we chooseand the clothes we wear.

As with most things, it allcomes down to priorities. You needto look at where you are spendingyour money to make consciousdecisions about what is a necessityversus a lifestyle choice.

The main point here is that formany, choices are made withoutthinking of the impact they mayhave on long-term savings. Pleasecall if you’d like to discuss thistopic in more detail. 444

U P D A T E

Ways to Save for Retirement

We all know we’re sup-posed to save for retire-ment. But that’s often

easier said than done. There are manyreasons for Americans’ pitiful sav-ings rates, including stagnant wages and an increasing cost of living. But our own behavior plays arole as well. So, how can you savemore at a time when every dollarseems to buy a little less? Considerthese suggestions:

Get a budget and reducespending: If you’re looking to savemore, the first place to look is yourcurrent budget. Cutting spendingwhere possible will free up moremoney to set aside for the future.While some of your expenses arefixed — most of us need to spendmoney on housing, food, and trans-portation — others are flexible.Spending a little less on dining out,canceling subscription services, orchoosing a cheaper cell phone plancould free up $50 or $100 in yourmonthly budget to dedicate to retire-ment. That may not sound like a lot,but it’s a good place to start.

Get your match: If you’re luckyenough to work for a company thatoffers a 401(k) plan and matchesemployee contributions, make sureyou take advantage of it. Not con-tributing enough to get your match is

essentially turning down free money. Max out your 401(k) plans: In

2017, most people can contribute upto $18,000 a year to their 401(k)plan. Not everyone can afford to saveup to the max; but whatever yourincome, you should contribute asmuch to tax-advantaged retirementaccounts as you’re able.

Contribute to an IRA: If youcan’t contribute to a retirement planat work or you want to save evenmore for retirement, consider settingup an IRA. Assuming you meet cer-tain requirements, you can save up to$5,500 a year in these accounts.

Contribute to a health savingsaccount (HSA): For people who arereally intent on maximizing theirretirement savings, consider HSAs.HSAs are primarily intended as away for people who have high-deductible health plans to save formedical expenses. But any moneyyou don’t use for healthcare costsnow can be used to pay for healthcarein retirement.

Make catch-up contributions:Once you reach age 50, you’re eligi-ble to make catch-up contributions to401(k) plans and IRAs. You can con-tribute an additional $6,000 a year toyour 401(k) plan and an extra $1,000a year to your IRA. If you consistent-

ly make those contributions over thenext 15 years (assuming you retire at65), you’ll have an additional$105,000 for retirement — and that’swithout taking into account anygrowth in your investments.

Save in taxable accounts: Mostpeople focus on saving for retirementin various tax-advantaged accountslike a 401(k) plan. But if you can’tsave for retirement that way or wantto save even more, consider saving inmore traditional ways. You can investin a well-diversified investmentaccount, CDs, bonds, or other sav-ings vehicles. One advantage of put-ting some money in nonretirementaccounts is you won’t have to worryabout things like mandatory with-drawals when you reach age 70½.

Take enough risk: Saving asmuch as possible is key to having ahealthy retirement portfolio. Butsquirreling away dollars alone isn’tenough. To really make the most ofyour money, you need to invest it.That means investing more in stockswhen you’re younger and graduallydialing down risk as you get closer toretirement. Being smart about risk isessential to meeting your retirementsavings goals.

Don’t take early withdrawals:When times get tough, people oftenturn to the money they’ve set asidefor retirement to close the gap. But ifit’s at all possible, avoid touchingthat cash. Not only would you fallbehind on your savings — creating agap that is nearly impossible to makeup — you would also get hit withpenalties. Unless you need thatmoney for a true emergency, like theprospect of losing your home or amajor health crisis, leave it alone.You’ll be glad you did so when thetime comes to stop working. 444

FR2017-0619-0011

U P D A T E

Pay Yourself First

The advice sounds simple enough — to force your-self to save regularly, treat those savings as a billto yourself and pay that bill first every month.

But when you’re faced with a stack of bills, you’re likely

to skip paying yourself. If you’re looking for ways tostart paying yourself first, consider the following:

4Reduce spending, diverting those reductions tosavings. One way to accomplish this is to cut back

on your spending, perhaps reducing your expendituresfor dining out, traveling, clothing, or entertainment. Butfor many people, this feels too much like sacrifice, mak-ing it difficult to stick with this strategy. Another alter-native is to find ways to spend less for the same items.

4 Save all unexpected income. Immediately saveany money from tax refunds, bonuses, cash gifts,

and inheritances. Before you get used to any salaryincreases, put that raise into savings.

4Make saving automatic. Resolve to immediatelyset up an investment account that automatically

deducts money from your bank account every month.Another good alternative is to sign up for your compa-ny’s 401(k) plan. (Keep in mind that any automaticinvesting plan, such as dollar cost averaging, does notassure a profit or protect against loss in declining markets. Because such a strategy involves periodicinvestment, consider your financial ability and willing-ness to continue purchases through periods of low pricelevels.) 444

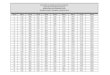

MarketDataMONTH END % CHANGE

STOCKS: NOV 17 OCT 17 SEP 17 YTD 12-MON.Dow Jones Ind. 24272.35 23377.24 22405.09 22.8% 26.9%S&P 500 2647.58 2575.26 2519.36 18.3 20.4Nasdaq Comp. 6873.97 6727.67 6495.96 27.7 29.1Wilshire 5000 27433.82 26687.97 26148.54 17.9 20.0PRECIOUS METALS:Gold 1280.20 1270.15 1283.10 10.4 8.7Silver 16.34 16.68 16.77 1.8 -1.0INTEREST RATES: NOV 17 OCT 17 SEP 17 DEC 16 NOV 16Prime rate 4.25 4.25 4.25 3.75 3.50Money market rate 0.33 0.32 0.27 0.29 0.293-month T-bill rate 1.29 1.02 1.05 0.56 0.4920-year T-bond rate 2.62 2.61 2.57 2.86 2.66Dow Jones Corp. 3.11 3.08 2.97 3.17 3.16Bond Buyer Muni 3.96 4.03 4.04 4.26 4.28Sources: Barron’s, Wall Street Journal. An investor may not invest directly in an index.

FR2017-0619-0011

The Cheney – Epley – Wolbeck Group at Morgan Stanley

Florence A. JackSenior Client Service Associate309.671.2860Hiral HudsonFinancial Advisor Associate309.671.2866Tessa BonelloClient Service Associate309.671.2869

Douglas S. CheneySenior Vice President – Wealth ManagementFinancial Advisor • 309.671.2879Daren F. EpleySenior Vice President – Wealth ManagementFinancial AdvisorFinancial Planning Specialist • 309.671.4660Patrick J. Wolbeck, CFP®

Vice President – Wealth ManagementFinancial AdvisorFinancial Planning Specialist • 309.671.2878

This newsletter was produced by Integrated Concepts Group, Inc. on behalf of Morgan Stanley Financial Advisors Douglas S. Cheney, Daren F. Epley, and Patrick J. Wolbeck. The opinionsexpressed in this newsletter are solely those of the author and do not necessarily reflect those of Morgan Stanley. Morgan Stanley can offer no assurance as to its accuracy or completenessand the giving of the same is not deemed an offer or solicitation on Morgan Stanley’s part with respect to the sale or purchase of any securities or commodities.Tax laws are complex and subject to change. This information is based on current federal tax laws in effect at the time this was written. Morgan Stanley Smith Barney LLC (“Morgan Stanley”), its affiliates, and Morgan Stanley Financial Advisors do not provide tax or legal advice. Individuals should consult their personal tax advisor for matters involving taxation and taxplanning and their attorney for matters involving personal trusts, estate planning, and other legal matters.Investments and services offered by Morgan Stanley Smith Barney LLC, Member SIPC. 2017-PS-50

NOT FDIC INSURED • NOT A BANK DEPOSIT • MAY LOSE VALUE