Embed Size (px)

Citation preview

Practical Aspects of Practical Aspects of Scrutiny AssessmentScrutiny Assessment

Presentation by:Presentation by:

CA RASESH SHAHCA RASESH SHAH

CA Rasesh Shah 2

IntroductionIntroduction

In the last two decades most of the In the last two decades most of the taxpayers of India had a wonderful time taxpayers of India had a wonderful time with the Income-tax Department.with the Income-tax Department.

This was because of the scheme of This was because of the scheme of department to cover most of the assessment department to cover most of the assessment under summary.under summary.

In recent times, the procedure for selection In recent times, the procedure for selection of the scrutiny cases underwent sea change.of the scrutiny cases underwent sea change.

As a result, many cases are picked up under As a result, many cases are picked up under scrutiny as per norms laid down by CBDT.scrutiny as per norms laid down by CBDT.

CA Rasesh Shah 3

Purpose of ScrutinyPurpose of Scrutiny

The purpose of the scrutiny assessment is to The purpose of the scrutiny assessment is to verify correctness of the income declared by verify correctness of the income declared by the assessee.the assessee.

Assessing officer may make the addition in Assessing officer may make the addition in respect of actual income understated by respect of actual income understated by assessee by suppressing receipt and/or assessee by suppressing receipt and/or inflating expenses. The assessing officer can inflating expenses. The assessing officer can also make addition under deeming provisions also make addition under deeming provisions of the Act like Sec. 68, 69, 69A, 69B, 69C of the Act like Sec. 68, 69, 69A, 69B, 69C even though there is no evidence of earning even though there is no evidence of earning of actual income by assessee.of actual income by assessee.

CA Rasesh Shah 4

Section 143(1)Section 143(1)

• Intimation u/s 143(1) shall be issued Intimation u/s 143(1) shall be issued only if:-only if:-

(i) (i) any tax or interest is due any tax or interest is due on the basis of return filed by on the basis of return filed by assessee orassessee or

(ii) (ii) any refund is due on the any refund is due on the basis of such return.basis of such return.

• Thus, prima facie adjustments are Thus, prima facie adjustments are now not permissible.now not permissible.

• Acknowledgement of return will be Acknowledgement of return will be treated as deemed intimation.treated as deemed intimation.

CA Rasesh Shah 5

Amendment of IntimationAmendment of Intimation

• Amendment of intimation / deemed Amendment of intimation / deemed intimation can be made u/s 154 of the Act.intimation can be made u/s 154 of the Act.

• Opportunity has to be given to assessee, if Opportunity has to be given to assessee, if amendment has the effect of reducing the amendment has the effect of reducing the refund or increasing the liability of refund or increasing the liability of assessee.assessee.

CA Rasesh Shah 6

Procedure of AssessmentProcedure of Assessment The notice u/s. 143(2) should be The notice u/s. 143(2) should be SERVEDSERVED on on

assessee within 12 months from the end of the assessee within 12 months from the end of the month in which return of income has been filed. month in which return of income has been filed.

The assessee is duty bound to comply with all The assessee is duty bound to comply with all the notices issued in the course of assessment the notices issued in the course of assessment proceeding.proceeding.

Assessee should reply all the queries raised Assessee should reply all the queries raised either by way of letter or order sheet entries.either by way of letter or order sheet entries.

If the assessee or his AR can not remain If the assessee or his AR can not remain present, adjournment application should be present, adjournment application should be filed before date of hearing. filed before date of hearing.

CA Rasesh Shah 7

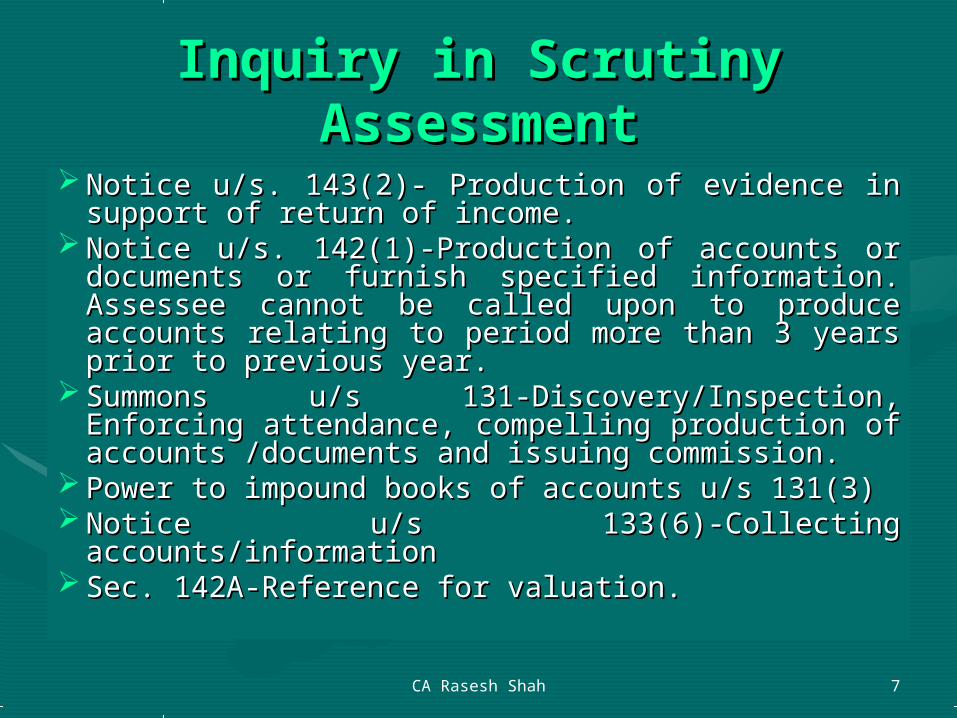

Inquiry in Scrutiny Inquiry in Scrutiny AssessmentAssessment

Notice u/s. 143(2)- Production of evidence in Notice u/s. 143(2)- Production of evidence in support of return of income.support of return of income.

Notice u/s. 142(1)-Production of accounts or Notice u/s. 142(1)-Production of accounts or documents or furnish specified information. documents or furnish specified information. Assessee cannot be called upon to produce Assessee cannot be called upon to produce accounts relating to period more than 3 years accounts relating to period more than 3 years prior to previous year.prior to previous year.

Summons u/s 131-Discovery/Inspection, Summons u/s 131-Discovery/Inspection, Enforcing attendance, compelling production of Enforcing attendance, compelling production of accounts /documents and issuing commission.accounts /documents and issuing commission.

Power to impound books of accounts u/s 131(3)Power to impound books of accounts u/s 131(3) Notice u/s 133(6)-Collecting Notice u/s 133(6)-Collecting

accounts/informationaccounts/information Sec. 142A-Reference for valuation. Sec. 142A-Reference for valuation.

CA Rasesh Shah 8

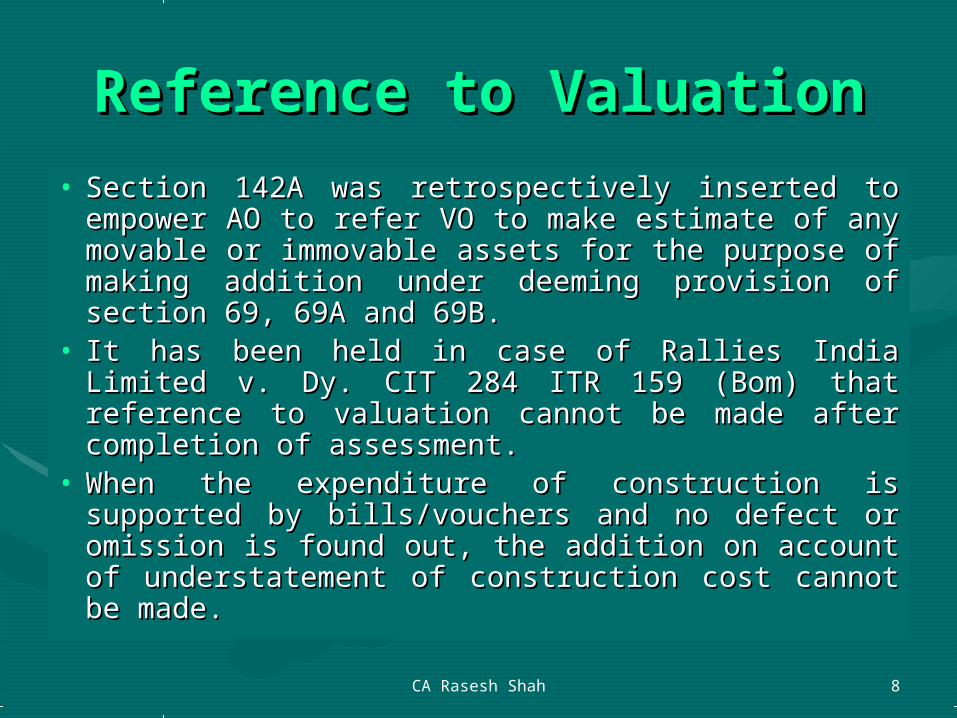

Reference to ValuationReference to Valuation• Section 142A was retrospectively inserted to Section 142A was retrospectively inserted to

empower AO to refer VO to make estimate of any empower AO to refer VO to make estimate of any movable or immovable assets for the purpose of movable or immovable assets for the purpose of making addition under deeming provision of making addition under deeming provision of section 69, 69A and 69B. section 69, 69A and 69B.

• It has been held in case of Rallies India Limited v. It has been held in case of Rallies India Limited v. Dy. CIT 284 ITR 159 (Bom) that reference to Dy. CIT 284 ITR 159 (Bom) that reference to valuation cannot be made after completion of valuation cannot be made after completion of assessment.assessment.

• When the expenditure of construction is supported When the expenditure of construction is supported by bills/vouchers and no defect or omission is found by bills/vouchers and no defect or omission is found out, the addition on account of understatement of out, the addition on account of understatement of construction cost cannot be made. construction cost cannot be made.

CA Rasesh Shah 9

Special Audit – Sec. Special Audit – Sec. 142(2A)142(2A)

• A.O may with the previous approval of Chief A.O may with the previous approval of Chief Commissioner or Commissioner, direct the assessee to Commissioner or Commissioner, direct the assessee to get the accounts audited by accountant.get the accounts audited by accountant.

• Opportunity must be provided to assessee before Opportunity must be provided to assessee before directing him to get the accounts audited.directing him to get the accounts audited.

• Max. time limit for special audit – 180 days.Max. time limit for special audit – 180 days.• Expenses pertaining to special audit shall be paid by Expenses pertaining to special audit shall be paid by

Central Government where directions are issued on or Central Government where directions are issued on or after 01/06/2007.after 01/06/2007.

• A.O cannot direct the special auditor to prepare books A.O cannot direct the special auditor to prepare books of accounts. Ref: Bajrang Textiles V. CIT - 3 SOT 115 of accounts. Ref: Bajrang Textiles V. CIT - 3 SOT 115 (Jodh.)(Jodh.)

• Special audit report is not binding on assessing officer.Special audit report is not binding on assessing officer.

CA Rasesh Shah 10

Best Judgment Asst. – Sect. Best Judgment Asst. – Sect. 144144

• Best judgment assessment can be made Best judgment assessment can be made in following cases, if:-in following cases, if:-(i) No return of income is filed, or(i) No return of income is filed, or(ii) Assessee fails to comply with all the (ii) Assessee fails to comply with all the terms terms

of notice issued u/s 142(1) or of notice issued u/s 142(1) or 142(2A) or 142(2A) or

section 143(2)section 143(2)• A.O should give opportunity before A.O should give opportunity before

passing order u/s 144.passing order u/s 144.• Opportunity not necessary where notice Opportunity not necessary where notice

u/s 142(1) is issued.u/s 142(1) is issued.

CA Rasesh Shah 11

Issue of directions - Sec. Issue of directions - Sec. 144A144A

• JCIT is empowered to issue directions to JCIT is empowered to issue directions to A.O to complete the assessment. A.O to complete the assessment. Directions can be issued, either on his – Directions can be issued, either on his –

(i) own motion or(i) own motion or (ii) on a reference being made by A.O or(ii) on a reference being made by A.O or (iii) on application of assessee.(iii) on application of assessee.

• Directions which are prejudicial to Directions which are prejudicial to assessee shall not be issued without assessee shall not be issued without giving opportunity of hearing to assessee.giving opportunity of hearing to assessee.

CA Rasesh Shah 12

Reassessment–Sec. 147Reassessment–Sec. 147

• Notice u/s 148 cannot be issued after expiry of Notice u/s 148 cannot be issued after expiry of 4 years from the end of relevant A.Y, if:-4 years from the end of relevant A.Y, if:-

(i) Assessment is completed u/s 143(3)/147 &(i) Assessment is completed u/s 143(3)/147 &

(ii) Income chargeable to tax has escaped (ii) Income chargeable to tax has escaped

assessment not on account of failure on part assessment not on account of failure on part of of

assessee to disclose fully & truly all material assessee to disclose fully & truly all material

facts.facts.• Notice cannot be issued on the basis of mere Notice cannot be issued on the basis of mere

change of opinion.change of opinion.

CA Rasesh Shah 13

Notice u/s 143(2) r.w.s. 147Notice u/s 143(2) r.w.s. 147

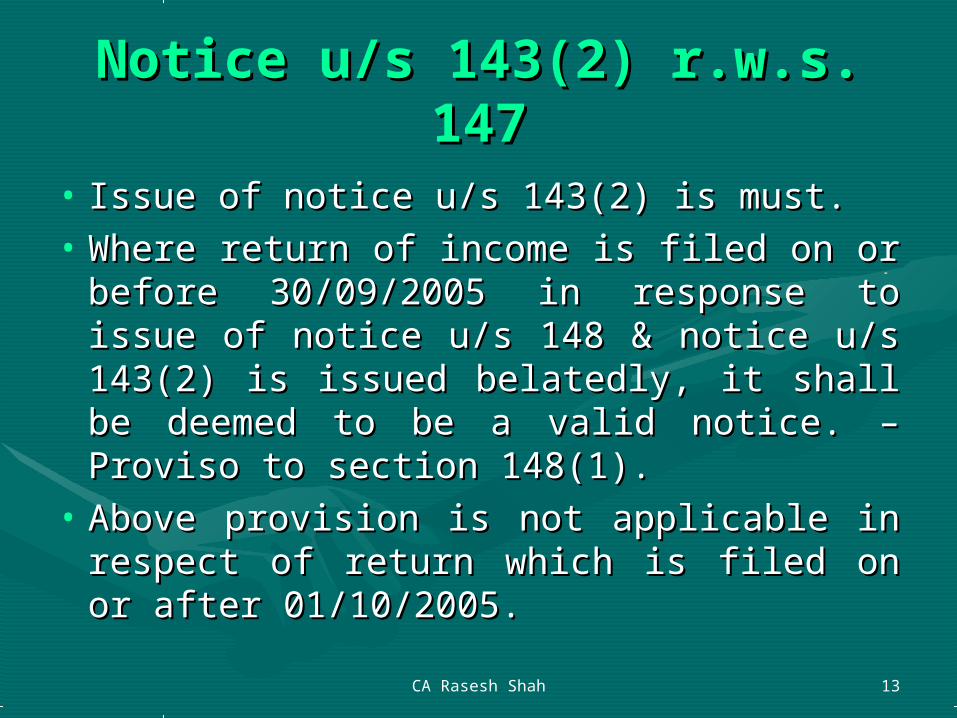

• Issue of notice u/s 143(2) is must.Issue of notice u/s 143(2) is must.• Where return of income is filed on or Where return of income is filed on or

before 30/09/2005 in response to issue of before 30/09/2005 in response to issue of notice u/s 148 & notice u/s 143(2) is notice u/s 148 & notice u/s 143(2) is issued belatedly, it shall be deemed to be issued belatedly, it shall be deemed to be a valid notice. – Proviso to section a valid notice. – Proviso to section 148(1).148(1).

• Above provision is not applicable in Above provision is not applicable in respect of return which is filed on or respect of return which is filed on or after 01/10/2005.after 01/10/2005.

CA Rasesh Shah 14

Reasons u/s 148(2)Reasons u/s 148(2)

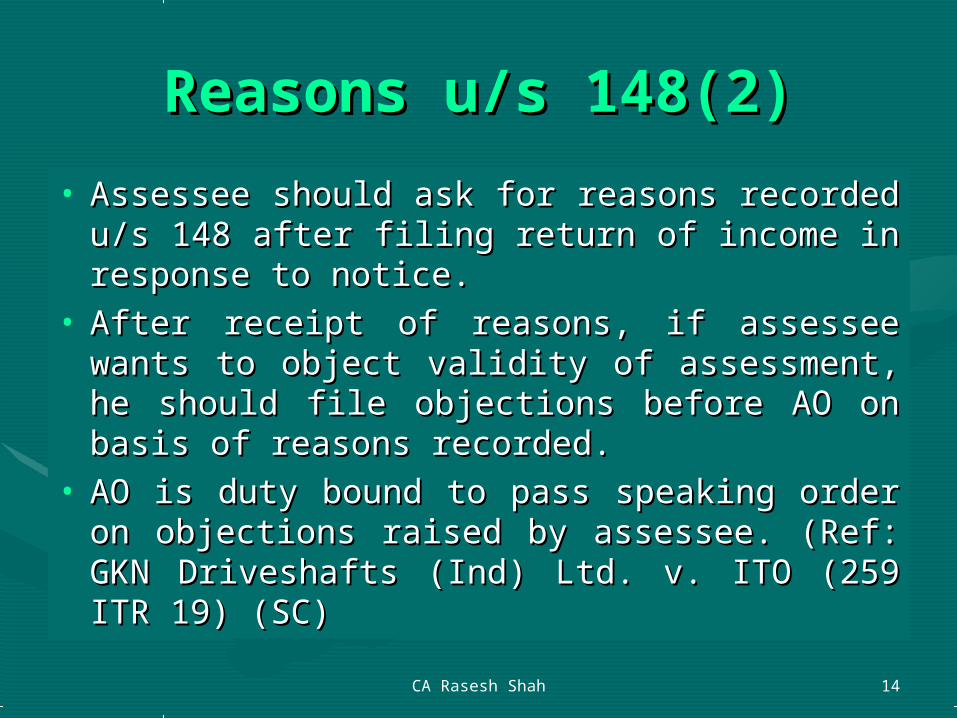

• Assessee should ask for reasons recorded u/s Assessee should ask for reasons recorded u/s 148 after filing return of income in response 148 after filing return of income in response to notice.to notice.

• After receipt of reasons, if assessee wants to After receipt of reasons, if assessee wants to object validity of assessment, he should file object validity of assessment, he should file objections before AO on basis of reasons objections before AO on basis of reasons recorded. recorded.

• AO is duty bound to pass speaking order on AO is duty bound to pass speaking order on objections raised by assessee. (Ref: GKN objections raised by assessee. (Ref: GKN Driveshafts (Ind) Ltd. v. ITO (259 ITR 19) Driveshafts (Ind) Ltd. v. ITO (259 ITR 19) (SC)(SC)

CA Rasesh Shah 15

Scope of ReassessmentScope of Reassessment

• No general information can be gathered No general information can be gathered by AO during reassessment. Only specific by AO during reassessment. Only specific inquiry can be made qua items of inquiry can be made qua items of reassessment and roving inquiry is not reassessment and roving inquiry is not permitted. So assessing officer cannot permitted. So assessing officer cannot make additions in respect of items not make additions in respect of items not covered by reasons recorded u/s 148. covered by reasons recorded u/s 148. (Vipan Khanna v. CIT (255 ITR 220) (Vipan Khanna v. CIT (255 ITR 220) (P&H)(P&H)

CA Rasesh Shah 16

Sanctity of InquirySanctity of Inquiry

The Supreme Court in the case of The Supreme Court in the case of Dhirajlal Girdherilal v. CIT (26 ITR 736), Dhirajlal Girdherilal v. CIT (26 ITR 736), Dhkershwari Cotton Mills Ltd. V. CIT (26 Dhkershwari Cotton Mills Ltd. V. CIT (26 ITR 755), Omar Salay Mohammed v. CIT ITR 755), Omar Salay Mohammed v. CIT (37 ITR 151), Lalchand Bhagatlal Ambica (37 ITR 151), Lalchand Bhagatlal Ambica Ram v. CIT (37 ITR 288) and CIT v. Ram v. CIT (37 ITR 288) and CIT v. Daulatram Rawatmal v. CIT (26 ITR 736) Daulatram Rawatmal v. CIT (26 ITR 736) held that the assessment is liable to be held that the assessment is liable to be cancelled if it is based on conjectures, cancelled if it is based on conjectures, surmises and presumptions and not on surmises and presumptions and not on hard rock of facts and relevant materialhard rock of facts and relevant material..

CA Rasesh Shah 17

Sanctity of InquirySanctity of Inquiry

In In C. Vasantlal & Co. v. CIT (45 ITR 206) (SCC. Vasantlal & Co. v. CIT (45 ITR 206) (SC), ), the Supreme Court held that it was open to an the Supreme Court held that it was open to an income-tax officer to collect materials to income-tax officer to collect materials to facilitate assessment even by private enquiry. facilitate assessment even by private enquiry. But if he desires to use materials so collected, But if he desires to use materials so collected, the assessee must be informed of the materials the assessee must be informed of the materials (Dhakeshwari Cotton Mills Ltd. v. CIT (26 ITR (Dhakeshwari Cotton Mills Ltd. v. CIT (26 ITR 775)(SC). 775)(SC). The The Supreme Court in case of Supreme Court in case of Kishinchand Chellaram v. CIT(125 ITR 713)Kishinchand Chellaram v. CIT(125 ITR 713) held held that materials collected cannot be kept that materials collected cannot be kept back from assessee by revenue authoritiesback from assessee by revenue authorities

CA Rasesh Shah 18

Sanctity of InquirySanctity of Inquiry

• The details of comparable case should be The details of comparable case should be given by assessing officer and if it is not given by assessing officer and if it is not given, assessee should ask for the same. given, assessee should ask for the same.

• Assessee should demand cross examination Assessee should demand cross examination of witnesses who furnished adverse of witnesses who furnished adverse information /statement to assessing officer.information /statement to assessing officer.

• If cross examination is not demanded, the If cross examination is not demanded, the assessee cannot plead at later stage that as assessee cannot plead at later stage that as cross examination is not allowed, the cross examination is not allowed, the addition is wrong. addition is wrong.

CA Rasesh Shah 19

Penalties under Penalties under assessmentassessment

In case of the addition, assessing officer may In case of the addition, assessing officer may initiate penalty proceeding u/s. 271(1)(c) for initiate penalty proceeding u/s. 271(1)(c) for concealment of income.concealment of income.

If the notices are not complied, assessing If the notices are not complied, assessing officer may initiate penalty proceedings u/s. officer may initiate penalty proceedings u/s. 271(1)(b). 271(1)(b).

Where there is failure to state truth, refusal Where there is failure to state truth, refusal to sign any statement and non-compliance of to sign any statement and non-compliance of the summons u/s 131, the assessing officer the summons u/s 131, the assessing officer may initiate penalty proceeding u/s 272(A)(1). may initiate penalty proceeding u/s 272(A)(1).

CA Rasesh Shah 20

Fall In Gross ProfitFall In Gross Profit

• Assessee should explain fall in gross profit Assessee should explain fall in gross profit by showing that margin of profit was low by showing that margin of profit was low during relevant year compared to past during relevant year compared to past years.years.

• In absence of omission or defects in books In absence of omission or defects in books of accounts and records, addition cannot of accounts and records, addition cannot be made. Case laws:be made. Case laws:CIT v. Vikarm Plastic (239 ITR 161) (Guj)CIT v. Vikarm Plastic (239 ITR 161) (Guj)CIT v. Dr. Rajnikant Dave (281 ITR 6) (Del) CIT v. Dr. Rajnikant Dave (281 ITR 6) (Del)

CA Rasesh Shah 21

Estimate of ProductionEstimate of Production

• A.O cannot reject book results merely on A.O cannot reject book results merely on the basis of disparity in consumption of the basis of disparity in consumption of electricity vis a vis production without any electricity vis a vis production without any supporting evidence.supporting evidence.

Case Law:Case Law:

St. Teresa’s Oil Mills v. State of Kerala St. Teresa’s Oil Mills v. State of Kerala (76 ITR 365) (Ker) (76 ITR 365) (Ker)

CA Rasesh Shah 22

New LoansNew Loans• Assessee should prove identity, capacity of lenders Assessee should prove identity, capacity of lenders

as well as genuineness of transaction.as well as genuineness of transaction.• Where lender is assessed to tax, assessee can avoid Where lender is assessed to tax, assessee can avoid

addition by filing confirmation with particulars of addition by filing confirmation with particulars of PAN.PAN.

• Case Laws:Case Laws:Addl. CIT Vs. Hanuman Agrawal (151 ITR 150) (Pat)Addl. CIT Vs. Hanuman Agrawal (151 ITR 150) (Pat)CIT Vs. Orissa Corporation (P) Ltd. (159 ITR 78) CIT Vs. Orissa Corporation (P) Ltd. (159 ITR 78) (SC)(SC)CIT Vs. Gopal & Co. (204 ITR 285) (Gau.)CIT Vs. Gopal & Co. (204 ITR 285) (Gau.)Jalan Timbers Vs. CIT (223 ITR 11) (Gau.)Jalan Timbers Vs. CIT (223 ITR 11) (Gau.)CIT Vs. Rohini Builders (256 ITR 360) (Guj.)CIT Vs. Rohini Builders (256 ITR 360) (Guj.)

CA Rasesh Shah 23

New Share CapitalNew Share Capital

• In case of new share capital, assessee is In case of new share capital, assessee is required to prove only identity of shareholders. required to prove only identity of shareholders. Case Laws:Case Laws:

CIT Vs. Steller InvCIT Vs. Steller Inv. Ltd. Ltd (192 ITR 287) (Del) (192 ITR 287) (Del)

CIT Vs. Kwick Travels (199 ITR 85) (St.) (Del) CIT Vs. Kwick Travels (199 ITR 85) (St.) (Del)

CIT Vs. Sophia FinCIT Vs. Sophia Fin.. Ltd. (205 ITR 98) (Del) (FB) Ltd. (205 ITR 98) (Del) (FB)

CIT Vs. Steller InvCIT Vs. Steller Inv.. Ltd. (251 ITR 263) (SC) Ltd. (251 ITR 263) (SC)

CA Rasesh Shah 24

Receipts by way of GiftReceipts by way of Gift

• In case of gift, the heavy burden is cast on In case of gift, the heavy burden is cast on assessee to prove the genuineness of assessee to prove the genuineness of gifts. The burden to produce donor is on gifts. The burden to produce donor is on assessee. assessee.

• If donor is assessed to tax and confirmed If donor is assessed to tax and confirmed donation of money to assessee by donation of money to assessee by personally appearing before AO, the personally appearing before AO, the addition can be avoided. addition can be avoided. Case Law:-Case Law:-

• Murlidhar Lahorimal Vs. CMurlidhar Lahorimal Vs. CIT(280 ITR IT(280 ITR 512) (Guj)512) (Guj)

CA Rasesh Shah 25

Source of SourceSource of Source• Assessee is not required to prove source of the Assessee is not required to prove source of the

source of credit. source of credit.

Case Laws:Case Laws:Hastimal V. CIT (49 ITR 273)(Mad.)Hastimal V. CIT (49 ITR 273)(Mad.)Tolaram Daga V. CITTolaram Daga V. CIT (59 ITR 632)(Assam)(59 ITR 632)(Assam)Nemichand Kothari v. CIT (264 ITR 254) (Gau)Nemichand Kothari v. CIT (264 ITR 254) (Gau)Murlidhar Lahorimal Vs. CMurlidhar Lahorimal Vs. CIT(280 ITR 512) (Guj)IT(280 ITR 512) (Guj)

CA Rasesh Shah 26

Remission/Cessation of Remission/Cessation of LiabilityLiability

• Section 41(1) cannot be applied for current Section 41(1) cannot be applied for current year when liability was incurred. year when liability was incurred.

• There must be some benefit in the form of There must be some benefit in the form of remission or cessation.remission or cessation.

• The burden is on revenue that assessee The burden is on revenue that assessee claimed deduction in past years.(Ref: CIT v. claimed deduction in past years.(Ref: CIT v. Pranlal Doshi-201 ITR 756).Pranlal Doshi-201 ITR 756).

• In CIT v. Sugauli Sugar Works P.LtdIn CIT v. Sugauli Sugar Works P.Ltd ( (236 ITR 236 ITR 518 (SC)518 (SC) and Ambica Mills Ltd v. CIT(54 ITR and Ambica Mills Ltd v. CIT(54 ITR 167) (Guj), it was held that167) (Guj), it was held that the fact that the the fact that the period of limitation prescribed by the period of limitation prescribed by the Limitation Act had expired, does not mean that Limitation Act had expired, does not mean that the debt was extinguished merely because the debt was extinguished merely because remedy by way of suit was barred. remedy by way of suit was barred.

CA Rasesh Shah 27

Payments to AssociatesPayments to Associates

• In In CIT v. Voltamp Transformers P. Ltd. v. CIT v. Voltamp Transformers P. Ltd. v. CIT (129 ITR 105CIT (129 ITR 105) (Guj) (Guj)), it was, it was held held that that payments payments are not to be judged from the are not to be judged from the viewpoint of a revenue officer but from the viewpoint of a revenue officer but from the viewpoint of a businessman. viewpoint of a businessman.

• In CBDT’sIn CBDT’s circular circular dated dated 6/7/68, it has 6/7/68, it has been observed that “The income-tax officer been observed that “The income-tax officer is expected to exercise his judgement in a is expected to exercise his judgement in a reasonable and fair mannerreasonable and fair manner and provision and provision is is not be applied in a manner which will not be applied in a manner which will cause hardship in bona fide cases.” cause hardship in bona fide cases.”

CA Rasesh Shah 28

Claim of ExpenditureClaim of Expenditure

• In In CIT v. Dhanrajgiri Raja Narasingiriji CIT v. Dhanrajgiri Raja Narasingiriji (91 ITR 544)(91 ITR 544),, it was held by Supreme it was held by Supreme Court that ‘It is not open to the Court that ‘It is not open to the department to prescribe what expenditure department to prescribe what expenditure an assessee should incur and in what an assessee should incur and in what circumstances he should incur that circumstances he should incur that expenditure. Every businessman knows expenditure. Every businessman knows his interest best.’his interest best.’

CA Rasesh Shah 29

Investment in stockInvestment in stock

• In the case of difference between stock as In the case of difference between stock as reported to revenue and bank, no addition reported to revenue and bank, no addition can be made if there is difference in value can be made if there is difference in value and not quantity. (Ashokkumar v. ITO) and not quantity. (Ashokkumar v. ITO) (201 CTR 178) (J & K).(201 CTR 178) (J & K).

• In case of difference in stock in quantities, In case of difference in stock in quantities, the addition can be avoided on basis of the addition can be avoided on basis of following case laws.following case laws.CIT v. General Metal Works (172 ITR 173) (All)CIT v. General Metal Works (172 ITR 173) (All)CIT v Sind. Rice & Gen. Mills(281 ITR 428) (PH)CIT v Sind. Rice & Gen. Mills(281 ITR 428) (PH)CIT v. Padmavati Cotton (236 ITR 340) (Mad) CIT v. Padmavati Cotton (236 ITR 340) (Mad)

CA Rasesh Shah 30

Business Income v. Business Income v. Capital GainCapital Gain

Various Parameters:Various Parameters:

• The intention at the time of purchase The intention at the time of purchase • The length of period of holdingThe length of period of holding• The frequency of transactionsThe frequency of transactions• Owned fund v. Borrowed fundOwned fund v. Borrowed fund• Time devotedTime devoted• The infrastructure and set up employedThe infrastructure and set up employed• The volume of transactionThe volume of transaction• Alternative occupationAlternative occupation• The ratio of purchase and sales/holdingThe ratio of purchase and sales/holding• Circumstances responsible for saleCircumstances responsible for sale• Post utilisation of proceedsPost utilisation of proceeds• Treatment in books of accountTreatment in books of account• MOA/AOAMOA/AOA• No. of scripts No. of scripts

CA Rasesh Shah 31

Circulars and Case LawsCirculars and Case Laws

• Instruction No. 1827 dated 31/8/89Instruction No. 1827 dated 31/8/89• Draft Circular dated 16/5/2007Draft Circular dated 16/5/2007• Cir. No. 4/2007 dated 16/6/2007Cir. No. 4/2007 dated 16/6/2007• Deepaben A. Shah 99 ITD 218 (Ahd)Deepaben A. Shah 99 ITD 218 (Ahd)• Fidelity Northstar Star 288 ITR 641 (AAR)Fidelity Northstar Star 288 ITR 641 (AAR)• Revashankar Kothari 283 ITR 338 (Guj)Revashankar Kothari 283 ITR 338 (Guj)• Smt. Neerja Birla v. Asst CIT 66 ITD 148 Smt. Neerja Birla v. Asst CIT 66 ITD 148

(Mum)(Mum)• Janak S. Rangwalla v. Asst CIT (11 SOT 627) Janak S. Rangwalla v. Asst CIT (11 SOT 627) • General Ele.Pension Trust (280 ITR 425) (AAR)General Ele.Pension Trust (280 ITR 425) (AAR)• Ramanarain Sons Ltd v. CIT(41 ITR 534) (SC)Ramanarain Sons Ltd v. CIT(41 ITR 534) (SC)

CA Rasesh Shah 32

Bogus/Non-genuine Bogus/Non-genuine PurchasesPurchases

• Assessee should place evidence in form of Assessee should place evidence in form of bills, challan, entry in stock register, payment bills, challan, entry in stock register, payment by crossed cheques etc. by crossed cheques etc.

• Case Laws:Case Laws:Dy. CIT v Adinath IndDy. CIT v Adinath Ind--252 ITR 476 (GUJ)252 ITR 476 (GUJ)ITO v SunsteelITO v Sunsteel--92 TTJ 1126 (AHD)92 TTJ 1126 (AHD)SSriri Rama Multi Rama Multitec tec v ACITv ACIT--92 TTJ 568 (AHD)92 TTJ 568 (AHD)CIT V S. M. Omer– 201 ITR 608 (CAL)CIT V S. M. Omer– 201 ITR 608 (CAL)CIT V. M.K. Brothers-163 ITR 249(GUJ)CIT V. M.K. Brothers-163 ITR 249(GUJ)Balaji TexBalaji Tex.. Ind Ind..P.LP.L.. V ITO–49 ITD 177(BOM) V ITO–49 ITD 177(BOM)J. R. SolJ. R. Sol.. Ind Ind.. P.L V ACIT–68 ITD 165 (CHD.) P.L V ACIT–68 ITD 165 (CHD.)Milkfood Ltd. V. DCIT – 65 TTJ 848 (DEL)Milkfood Ltd. V. DCIT – 65 TTJ 848 (DEL)

CIT V. KCIT V. Kashiramashiram T Textile Millsextile Mills P. Ltd. - 284 ITR 61 P. Ltd. - 284 ITR 61 (GUJ)(GUJ)

CA Rasesh Shah 33

Assessment after Assessment after revisionrevision

• It has been held that the issue which is It has been held that the issue which is not touched upon on revision cannot be not touched upon on revision cannot be basis for making addition in assessment basis for making addition in assessment taken in pursuance of order u/s 263-Ref: taken in pursuance of order u/s 263-Ref: CIT v. D. N. Doshani & Co. (280 ITR 275) CIT v. D. N. Doshani & Co. (280 ITR 275) (Guj)(Guj)

CA Rasesh Shah 34

Inclusion of taxes/duties-Sec-Inclusion of taxes/duties-Sec-145A145A

• Our Institute suggested exclusive method but Our Institute suggested exclusive method but section 145A talks about inclusive method. section 145A talks about inclusive method. Both methods are revenue neutral. Both methods are revenue neutral.

• So auditor gives reconciliation in the tax audit So auditor gives reconciliation in the tax audit report & demonstrates that even when report & demonstrates that even when adjustments are made as per provisions of adjustments are made as per provisions of section 145A, there is no impact on the figure section 145A, there is no impact on the figure of net profit / loss.of net profit / loss.

• However, AO makes adjustment only to the However, AO makes adjustment only to the figure of closing stock so as to make addition.figure of closing stock so as to make addition.Case Laws:Case Laws:CIT v. Indo Nippon Chemicals Ltd (261 ITR 275) (SC)CIT v. Indo Nippon Chemicals Ltd (261 ITR 275) (SC)Dy. CIT v. Gandhar Oil Ltd. (104 TTJ 630) (Mum)Dy. CIT v. Gandhar Oil Ltd. (104 TTJ 630) (Mum)

CA Rasesh Shah 35

Whether stock can be valued at Market Whether stock can be valued at Market Price?Price?

• The stock cannot be valued at market price, if it is The stock cannot be valued at market price, if it is higher than cost price. higher than cost price. Case Law:Case Law:Sanjeev Woolen Mills v. CIT (279 ITR 434) (SC)Sanjeev Woolen Mills v. CIT (279 ITR 434) (SC)

• If the value of closing stock is disturbed in any year, If the value of closing stock is disturbed in any year, the corresponding adjustment in value of opening the corresponding adjustment in value of opening stock of next year should be given. stock of next year should be given. Case Law:Case Law:CIT v. Chandrika Towers (275 ITR 173) (MP)CIT v. Chandrika Towers (275 ITR 173) (MP)

CA Rasesh Shah 36

Addition on basis of Addition on basis of Stamp DutyStamp Duty

• Addition cannot be made on basis of Addition cannot be made on basis of increased stamp duty payable by assessee increased stamp duty payable by assessee on higher valuation made by revenue on higher valuation made by revenue authorities. authorities. Case Laws:Case Laws:

Dinesh Mittal v. ITO (193 ITR 770) (All)Dinesh Mittal v. ITO (193 ITR 770) (All) CGT v. R. Damodaran (247 ITR 698) (Mad)CGT v. R. Damodaran (247 ITR 698) (Mad)

CA Rasesh Shah 37

Destruction of books of Destruction of books of accountsaccounts

• I.T authorities can accept the audit I.T authorities can accept the audit report where books of accounts are report where books of accounts are destroyed & they can also draw destroyed & they can also draw inference from the same regarding inference from the same regarding supporting materials for deductions supporting materials for deductions claimed.claimed.

Case LawCase Law:- :-

CIT. V. Jay Engg. Works Ltd. – 113 ITR CIT. V. Jay Engg. Works Ltd. – 113 ITR 389(Del)389(Del)

CA Rasesh Shah 38

Protective AssessmentProtective Assessment

• Protective assessment has been Protective assessment has been recognised by judicial decisions although recognised by judicial decisions although there is no specific provision in the Act.there is no specific provision in the Act.

• If substantive assessment is not made, If substantive assessment is not made, protective assessment becomes protective assessment becomes substantive assessment. substantive assessment.

• There cannot be recovery in case of There cannot be recovery in case of protective assessment. protective assessment.

• Although protective assessment is Although protective assessment is permissible, protective penalty order is permissible, protective penalty order is not permissible. not permissible.

CA Rasesh Shah 39

New Claim During New Claim During AssessmentAssessment

• It has been held by Supreme Court in It has been held by Supreme Court in Goetze (India) Ltd. Vs. CGoetze (India) Ltd. Vs. CIT (284 ITR 323) IT (284 ITR 323) that new claim for deduction cannot be that new claim for deduction cannot be entertained by entertained by assessing authorityassessing authority other other than by way of filing revised return of than by way of filing revised return of income. income.

• However, the above decision does not However, the above decision does not impinge on the power of ITAT to admit impinge on the power of ITAT to admit new claim.new claim.

CA Rasesh Shah 40

The presentation can be The presentation can be downloaded from downloaded from

Knowledge Area of Knowledge Area of www.raseshca.comwww.raseshca.com

ThanksThanks