Embed Size (px)

DESCRIPTION

financial markets (fund raising)

Citation preview

NEW ISSUE MANAGEMENT

INITIAL PUBLIC OFFER (IPO)

INTRODUCTIONInitial Public Offering refers to the selling of shares

by a private company to the public for the first time. Initial Public Offering is a source of funds raised from the primary market. All subsequent public offerings are known as Follow-on Public Offerings or Secondary Market Offerings.

An IPO is an abbreviation for Initial Public Offer. When a company goes public for the first time or issues a fresh stock of shares, it offers it to the public directly. This happens in the primary market. The primary market is where a company makes its first contact with the public at large.

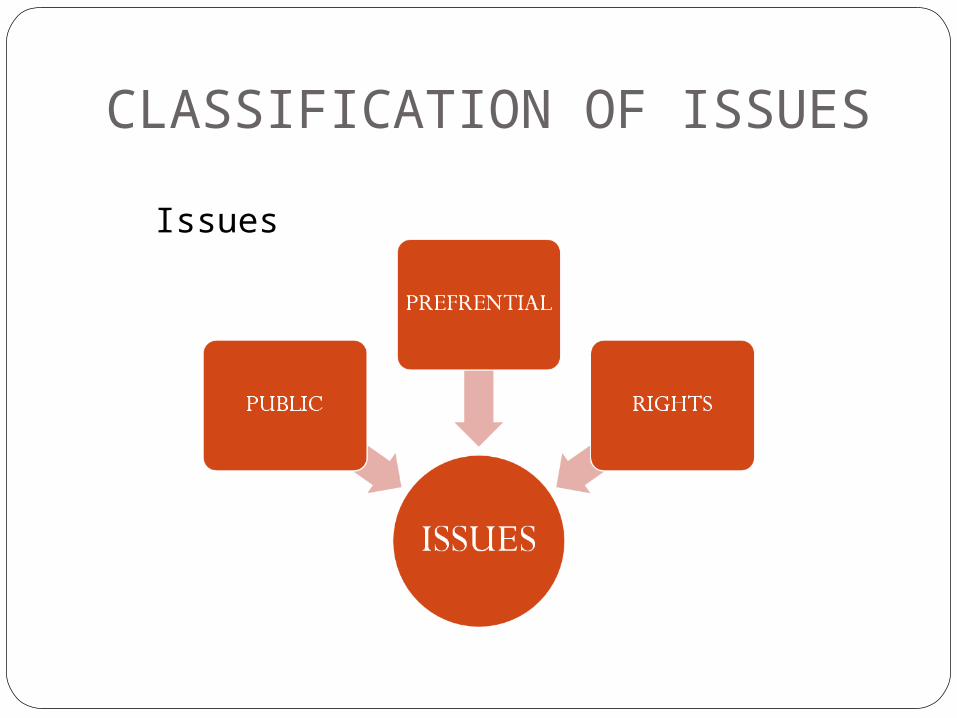

CLASSIFICATION OF ISSUES Issues

UNDER PUBLIC ISSUE

PRIMARY ISSUE MARKET OR NEW ISSUE MARKETPRIMARY MARKETS- Include all types of

securities being sold for the first time.Becomes part of the Secondary market

after offered in Primary market.

Primary Market Offer consist of-1.FPO’s,new offerings of listed companies that have sold securities to the public before, and2.IPO’s,where an unlisted company is selling

securities to the public for the first time.

PLACEMENT OF THE ISSUEINITIAL ISSUES ARE FLOATED-1.Through prospectus.2.Bought out deals/Offer for sale.3.Private placement.4.Rights issue.5.Book building.

OFFER THROUGH PROSPECTUS Invites offers for subscription or purchase of any

shares or debentures from the public. The salient features of the prospectus are-1.General information about the company.2.Capital structure of the company.3.Terms of the present issue.4.Particluars of the issue-issue opening, closing and

earliest closing date of the issue.5.Company management and project.6.Detalis of the outstanding litigations.7.Management perception of risk factors.8.Justification of the issue premium.9.Financial information-cost of project, project

earnings.

OFFER FOR SALEPromoter places his shares with an

investment banker (bought out dealer or sponsor) who offer it to the public at a later date

Hold on period is 70 days to more than a year.

Bought out dealer decides the price after analyzing the viability, gestation period, promoter’s background andfuture projections.

Bought out dealer sheds the shares at a premium to the public.

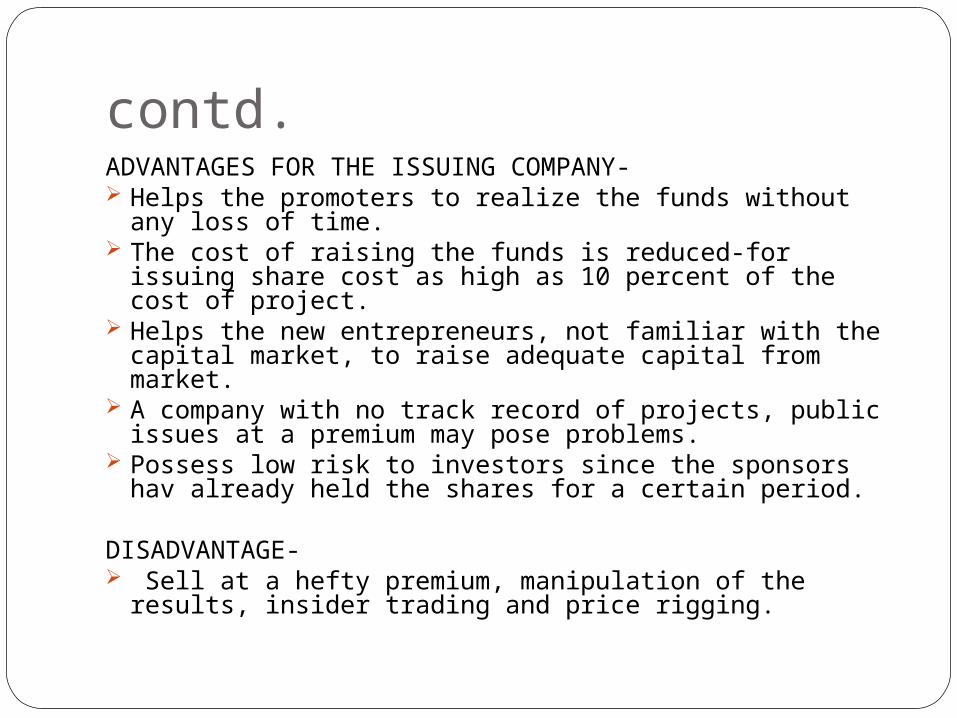

contd.ADVANTAGES FOR THE ISSUING COMPANY- Helps the promoters to realize the funds without any

loss of time. The cost of raising the funds is reduced-for issuing

share cost as high as 10 percent of the cost of project. Helps the new entrepreneurs, not familiar with the

capital market, to raise adequate capital from market. A company with no track record of projects, public

issues at a premium may pose problems. Possess low risk to investors since the sponsors hav

already held the shares for a certain period.

DISADVANTAGE- Sell at a hefty premium, manipulation of the results,

insider trading and price rigging.

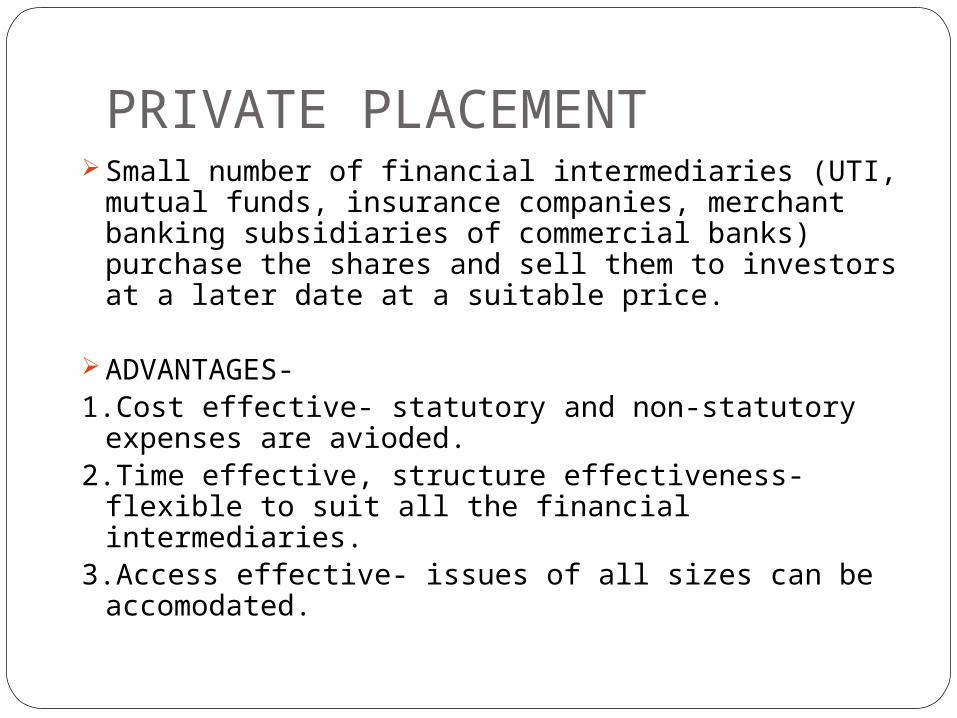

PRIVATE PLACEMENT Small number of financial intermediaries (UTI,

mutual funds, insurance companies, merchant banking subsidiaries of commercial banks) purchase the shares and sell them to investors at a later date at a suitable price.

ADVANTAGES-1.Cost effective- statutory and non-statutory

expenses are avioded.2.Time effective, structure effectiveness- flexible

to suit all the financial intermediaries.3.Access effective- issues of all sizes can be

accomodated.

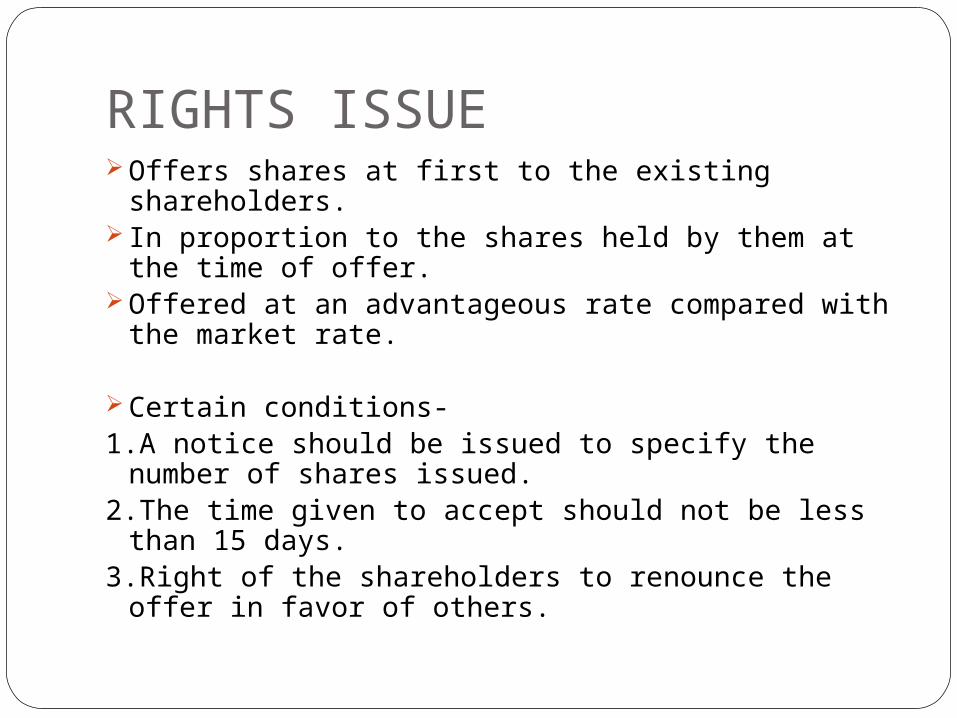

RIGHTS ISSUE Offers shares at first to the existing shareholders. In proportion to the shares held by them at the

time of offer. Offered at an advantageous rate compared with

the market rate.

Certain conditions-1.A notice should be issued to specify the number

of shares issued.2.The time given to accept should not be less than

15 days.3.Right of the shareholders to renounce the offer in

favor of others.

BOOK BUILDINGProcess of price discovery- Not a fixed price for its shares. Indicates a price band that mentions the lowest

(referred to as floor) and the highest (cap) prices. The spread between the floor and the cap of the

price band shall not be more than 20%. The cap should not be more than 120% of the floor price.

Price is finalized by the book runner and the issuer company.

• Malegam committee- introduction of book building process OCT 1995.

• Originally, companies issuing more than Rs.100 cr. Allowed; Later SEBI allowed for issue of any size.

contd. NIRMA offering a maximum of 100 lakh equity shares

through this process, 1st company to adopt the mechanism.

An example of pricing securities- GOOGLE’s IPO offer- Google’s IPO offer on the Dutch auction basis,

similar o the book building process. Target range between U.S.$105 and U.S.$ 135 per

share. Market response to offer not too good, final issue

price U.S.$ 85. Enabled Google to find price that market was willing

to pay for its issue.

RED HERRING PROSPECTUSProspectus without details of either price or number

of shares being offered or the amount of issue.

A preliminary registration statement that must be filed with the SEBI describing a new issue of stock(IOP) and the prospectus of the issuing company.

It is known as a RED HERRING because it contains a passage in red that states the company is not attempting to sell their shares before the registration is approved by SEBI.

PRICING OF ISSUE Prior to 1992, governed by Controller of Capital Issues

Act 1947, fixation of a fair price on the basis of the net asset calue per share.

Era of free pricing in 1992, SEBI does not play any role in price fixation.

Issuer in consultation with merchant banker shall decide the price.

FIXED PRICE- company and LM fix a price. PRICE DISCOVERY THROUGH BOOK BUILDING-

company and LM stipulate a floor price or a price band and leave it to market forces to determine the final price.

AT PREMIUM- companies are permitted to price their issues at a premium.

AT PAR VALUE- in certain cases companies are not permitted to fix their issue prices at premium.

INTERMEDIARIES TO THE ISSUE INTERMEDIARIES TO THE ISSUE ARE-1.Merchant bankers to the issue or Book running

lead managers (BRLM).2.Registrars to the issue.3.Bankers to the issue.4.Auditors of the company.5.Underwriters to the issue.6.Solicitors7.Advertising agencies.8.Financial institutions.9.Government / statutory agencies

LEAD MANAGER Appointed by company to manage public issue

programmes. BRLM-A merchant banker possessing valid SEBI

registration. Main duties-1.Drafting of prospectus.2.Preparing the budget of expenses related to the issue.3.Suggesting the appropriate timings of the public issue.4.Assisting in marketing the public issues successfully.5.Advising the company in the appointment of registrars

to the issue, underwriters, brokers, bankers to the issue, advertising agents.

6.Detecting the various agencies involved in public issue.

contd.The merchant banking division of the

financial institutions, subsidiaries of commercial banks, foreign banks, private sector banks and private agencies are available to act as lead managers.

Some of them are SBI capital markets ltd. Bank of Baroda, Canara bank, DSP financial consultant ltd. ICICI securities and Finance company ltd. Etc.

ROLE OF LEAD MANAGER IN PRE AND POST ISSUE.

PRE ISSUE1.Due diligence

2.Design of offer

doc.prospectus,mem,

3.Ensure the formalities with SE,ROC & SEBI.4.Appointment

with intermediaries.

5.Marketing strategy.

POST ISSUE1.Mgt of escrow act.2.Co-ordinate non-

institutional allocation.

3.Intimation of allocation.

4.Dispatch of refunds to bidders.

5.Follow up steps-Finalization of trading,

dealing of instruments, dispatch

of certificates & demat of deliver of

shares.6.Look at the functioning of

agencies.

REGISTRAR. Finalizes the list of eligible allotees after

deleting the invalid applications. Corporate action for crediting of shares to

demat accounts of the applicants. Dispatch of refund orders to those applicable. Receive the share application from various

collection centres Recommend the basis of allotment in

consultation with the regional stock exchange for approval.

Arrange for the dispatching of the share certificates.

BANKERS TO THE ISSUE.Ensure that the funds are collected and

transferred to the Escrow accounts.Estimates of collection and advising the

issuer about the closure of the issue.

UNDERWRITERS Underwriting means they will subscribe to the

balance shares if all the shares offered at the IPO are not picked up.

Could be a banker, broker, merchant banker or financial institution.

Insurance against the possibility of inadequate subscription.

Done for a commission The aspects considered before appointing are-1.Experience in the primary market.2.Past underwriting performance and default.3.Outstanding underwriting commitment.4.The network of investor clientele of the underwriter.5.His overall reputation.

KEY TERMSGREEN SHOE OPTION- An option of allocating shares in excess of the

shares included in the public issue. Post-listing price stabilizing mechanism for a

period not exceeding 30 days through a Stabilizing Agent.

Issue would be over allotted to the extent of a maximum of 15% of the issue size.

Provides an investor more probability of getting shares.

Post-listing price may show relatively more stability as compared to market.

QUALIFIED INSTITUTIONAL BUYERS (QIB’s)- Institutional buyers who are perceived to possess

expertise and the financial muscle to evaluate and invest in the capital markets.

What to look for before investing in an IPO

1. Valuation: First thing to look at is how aggressively the IPO is Priced. The more aggressively it is priced the lesser the chances of price appreciation.

2. Promoter’s Goodwill: the Promoter’s Goodwill is an important parameter in analyzing an IPO as a goodwill creates trust in taking decision for applying for an IPO.

3. Broker’s Report: Brokers can provide an investor with all the info he needs on the co. so an investor must take advice from his stock broker before applying for an IPO.

4. Ratings: SEBI has now made it mandatory for every co. to get its IPO rated through any approved rating agencies like CRISIL, ICRA etc. but remember that it does not provide guarantee of success.