Embed Size (px)

Citation preview

The World Needs New Reserve Currency:from the perspective of global liquidity

Yao Yudong

People’s Bank of China

2015-06-25

Outline1 Global liquidity provision: History and Status quo

2 Global liquidity measurement

3 Dual pressure on global liquidity

4 Gold price in global liquidity shortage

5 How to solve global liquidity shortage

6 Plan to make RMB more freely usable

7 Shanghai Gold Exchange international board and RMB internationalization

The LBMA Bullion Market Forum 2015 25 June 2015

Opening Session - Dr. Yao Yudong 1

1 Global liquidity provision: History

• Bretton Woods system (1945-1971)

“Pegged rate" currency regime: other currencies pegged to USD with fixed relationship of USD to gold ($35 an ounce) Overemphasis on exchange rate stability, lack of rule on global liquidity

provision

Vulnerabilities: global liquidity provision may either be inadequate or excess 1950s: USD shortage and the Marshall Plan

1960s: excess supply of USD and Triffin Dilemma

First Amendment to Articles of Agreement, IMF (1969) Create SDR “to meet the long-term global need”

“The Council shall supervise … the continuing operation of the adjustment process and developments in global liquidity.”

Nixon shock and the end of Bretton Woods system.

1 Global liquidity provision: Status quo

• Main reserve currencies: USD, Euro, Sterling and Yen (SDR currencies)

• Problem remains:

Main reserve currency issuers may either fail to adequately meet the demand of a growing global economy for liquidity as they try to ease inflation pressures at home, or create excess liquidity in the global markets by overly stimulating domestic demand. Outbreak of Global financial crisis: USD shortage

2011-2013: excess supply of global liquidity and challenges for EMEs to maintain financial stability.

2015: QE exist and incoming rate hike for US, Expanded Asset Purchase Program for Euro Area and QQE for Japan.

The LBMA Bullion Market Forum 2015 25 June 2015

Opening Session - Dr. Yao Yudong 2

2 Global liquidity measurement

• Global liquidity indicators: Core global liquidity comes from main currency issuers. Both price indicators and quantity indicators should be

considered Quantity indicators became more important given zero lower

bound on nominal interest rate of main currency issuers

• We condiser:1. Global Base Money: base money of main currency issuers.2. Global M2: M2 of main currency issuers3. Money multiplier4. Global interest rate: Weighted sum of main currency

issuers’ policy interest rate (weighted by its SDR share)

2.1 Global M2

• Global M2 is expanding with a lower speed.

-2

0

2

4

6

8

10

12

14

0

5000

10000

15000

20000

25000

20

04

-04

20

04

-08

20

04

-12

20

05

-04

20

05

-08

20

05

-12

20

06

-04

20

06

-08

20

06

-12

20

07

-04

20

07

-08

20

07

-12

20

08

-04

20

08

-08

20

08

-12

20

09

-04

20

09

-08

20

09

-12

20

10

-04

20

10

-08

20

10

-12

20

11

-04

20

11

-08

20

11

-12

20

12

-04

20

12

-08

20

12

-12

20

13

-04

20

13

-08

20

13

-12

20

14

-04

20

14

-08

20

14

-12

global M2 yoy growth rate(right axis)Billion SDR %

The LBMA Bullion Market Forum 2015 25 June 2015

Opening Session - Dr. Yao Yudong 3

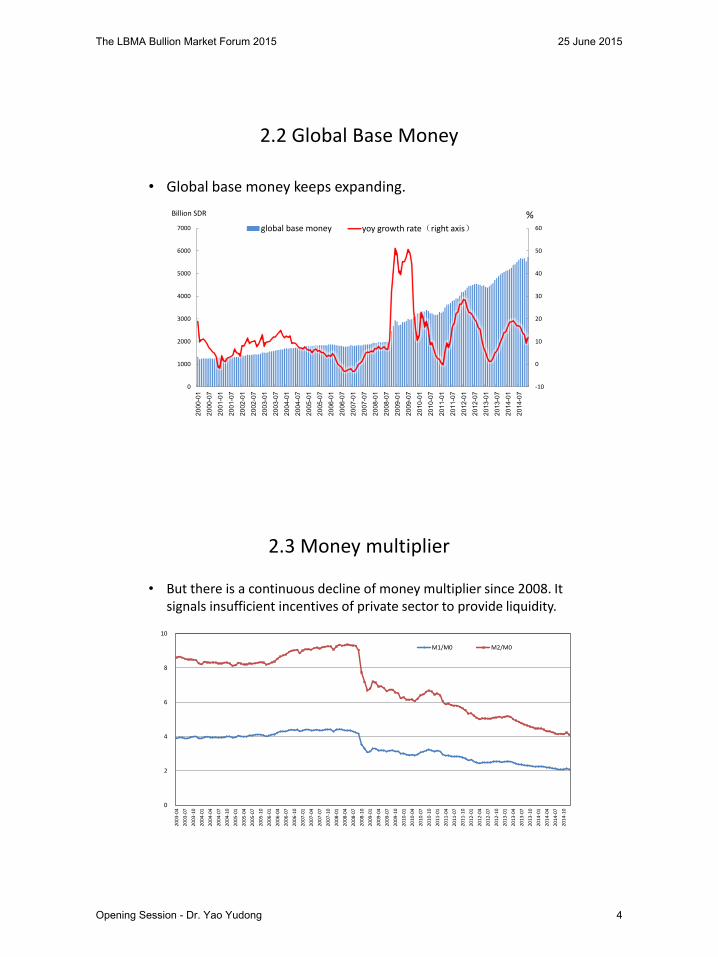

2.2 Global Base Money

• Global base money keeps expanding.

-10

0

10

20

30

40

50

60

0

1000

2000

3000

4000

5000

6000

7000

20

00-0

1

20

00-0

7

20

01-0

1

20

01-0

7

20

02-0

1

20

02-0

7

20

03-0

1

20

03-0

7

20

04-0

1

20

04-0

7

20

05-0

1

20

05-0

7

20

06-0

1

20

06-0

7

20

07-0

1

20

07-0

7

20

08-0

1

20

08-0

7

20

09-0

1

20

09-0

7

20

10-0

1

20

10-0

7

20

11-0

1

20

11-0

7

20

12-0

1

20

12-0

7

20

13-0

1

20

13-0

7

20

14-0

1

20

14-0

7

global base money yoy growth rate(right axis)

Billion SDR %

2.3 Money multiplier

• But there is a continuous decline of money multiplier since 2008. It signals insufficient incentives of private sector to provide liquidity.

0

2

4

6

8

10

20

03-0

4

20

03-0

7

20

03-1

0

20

04-0

1

20

04-0

4

20

04-0

7

20

04-1

0

20

05-0

1

20

05-0

4

20

05-0

7

20

05-1

0

20

06-0

1

20

06-0

4

20

06-0

7

20

06-1

0

20

07-0

1

20

07-0

4

20

07-0

7

20

07-1

0

20

08-0

1

20

08-0

4

20

08-0

7

20

08-1

0

20

09-0

1

20

09-0

4

20

09-0

7

20

09-1

0

20

10-0

1

20

10-0

4

20

10-0

7

20

10-1

0

20

11-0

1

20

11-0

4

20

11-0

7

20

11-1

0

20

12-0

1

20

12-0

4

20

12-0

7

20

12-1

0

20

13-0

1

20

13-0

4

20

13-0

7

20

13-1

0

20

14-0

1

20

14-0

4

20

14-0

7

20

14-1

0

M1/M0 M2/M0

The LBMA Bullion Market Forum 2015 25 June 2015

Opening Session - Dr. Yao Yudong 4

2.3 Why private sector has less incentive for providing liquidity?

• Global economic growth remains moderate Slow economic recovery and deleverage pressure.

• Financial regulation Liquidity Coverage Ratio introduced by Basel III. Volcker Rule discourages market making.

• Shortage of safe asset Central banks of main reserve currency issuers

occupied a large amount of safe asset through QE, reduced the access of private sector to qualified collaterals .

2.4 Global Policy Rate

• Since 2008, global policy rate has been kept very low. US Base Money expansion is the largest contributing factor

-10.00

0.00

10.00

20.00

30.00

40.00

50.00

60.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

20

00

/02

20

00

/08

20

01

/02

20

01

/08

20

02

/02

20

02

/08

20

03

/02

20

03

/08

20

04

/02

20

04

/08

20

05

/02

20

05

/08

20

06

/02

20

06

/08

20

07

/02

20

07

/08

20

08

/02

20

08

/08

20

09

/02

20

09

/08

20

10

/02

20

10

/08

20

11

/02

20

11

/08

20

12

/02

20

12

/08

20

13

/02

20

13

/08

20

14

/02

20

14

/08

global policy rate global base money growth(right axis)

% %

The LBMA Bullion Market Forum 2015 25 June 2015

Opening Session - Dr. Yao Yudong 5

3 Dual pressure on global liquidity

Global Base Money Growth

McCallum rule

Global Base Money Growth

Actual growthGlobal Real GDP Growth Global Inflation

2008 10.7 41.3 3.0 4.6

2009 15.7 9.9 0.0 3.3

2010 13.5 2.1 5.3 4.4

2011 19.0 23.5 4.1 4.8

2012 11.2 6.9 3.3 4.0

2013 11.5 13.3 3.2 3.5

2014 14.2 11.2 3.3 3.9

2015 13.7 19 3.8 3.8

2016 13.7 19 4.0 3.6

2017 13.8 5 4.0 3.6

2018 13.8 5 4.0 3.5

2019 13.8 5 4.0 3.5

Resources:Wind & WEO,data from 2015 to 2019 are estimated。

Pressure I : conflict of economic interests between short-term domestic and long-term international objectives for reserve currency issuers.

Global Base Money Growth by McCallum Rule

Pressure II: US policy rate hikes

• Fed policy normalization will tighten USD liquidity.

Given policy rate on zero lower bound, the initial raise has significant tightening effect, even with a small step.

• Policy rate hikes and exchange rate appreciation will encourage hoarding USD, making liquidity shortage intensified.

• Accounting for almost 50% of global M2, USD shortage will put substantial pressure on global liquidity.

The LBMA Bullion Market Forum 2015 25 June 2015

Opening Session - Dr. Yao Yudong 6

3.2 Global liquidity shortage has severe consequences

• Exchange rate fluctuation

• Capital outflows from EMEs to US

• Global deflation

• Slower economic growth

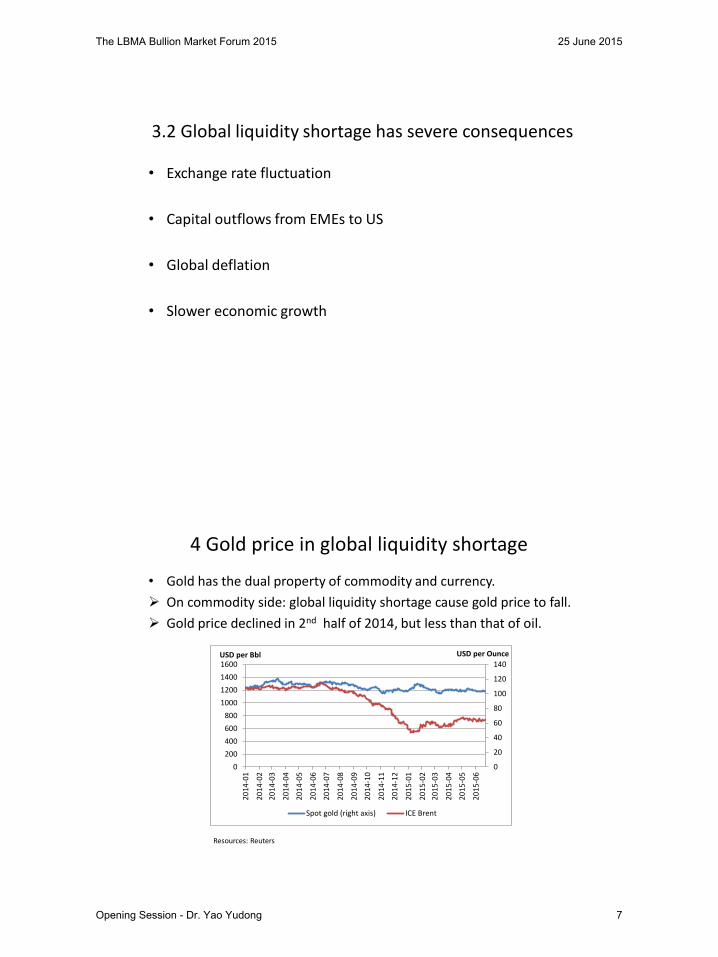

4 Gold price in global liquidity shortage

• Gold has the dual property of commodity and currency.

On commodity side: global liquidity shortage cause gold price to fall.

Gold price declined in 2nd half of 2014, but less than that of oil.

0

20

40

60

80

100

120

140

0

200

400

600

800

1000

1200

1400

1600

20

14

-01

20

14

-02

20

14

-03

20

14

-04

20

14

-05

20

14

-06

20

14

-07

20

14

-08

20

14

-09

20

14

-10

20

14

-11

20

14

-12

20

15

-01

20

15

-02

20

15

-03

20

15

-04

20

15

-05

20

15

-06

USD per OunceUSD per Bbl

Spot gold (right axis) ICE Brent

Resources: Reuters

The LBMA Bullion Market Forum 2015 25 June 2015

Opening Session - Dr. Yao Yudong 7

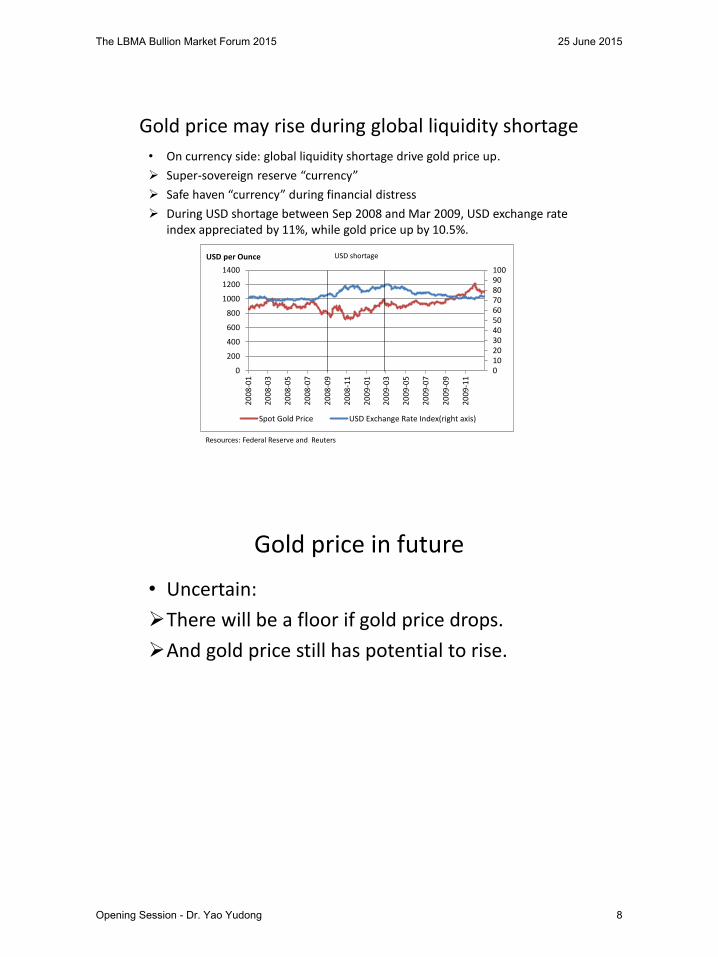

Gold price may rise during global liquidity shortage

• On currency side: global liquidity shortage drive gold price up.

Super-sovereign reserve “currency”

Safe haven “currency” during financial distress

During USD shortage between Sep 2008 and Mar 2009, USD exchange rate index appreciated by 11%, while gold price up by 10.5%.

0102030405060708090100

0

200

400

600

800

1000

1200

1400

20

08

-01

20

08

-03

20

08

-05

20

08

-07

20

08

-09

20

08

-11

20

09

-01

20

09

-03

20

09

-05

20

09

-07

20

09

-09

20

09

-11

USD per Ounce

Spot Gold Price USD Exchange Rate Index(right axis)

USD shortage

Resources: Federal Reserve and Reuters

Gold price in future

• Uncertain:

There will be a floor if gold price drops.

And gold price still has potential to rise.

The LBMA Bullion Market Forum 2015 25 June 2015

Opening Session - Dr. Yao Yudong 8

5 How to solve global liquidity shortage

• World needs new reserve currency as well as gold. Gold is not able to solve the problem alone, given its limited volume.

• Reserve currency diversification

• RMB has the potential to complement global liquidity. RMB ranks 5th in international payment and 7th in international reserve.

Increasing bilateral currency swap agreements signal rising demand of RMB liquidity.

Cross-border RMB policy framework has been established.

• RMB included in the SDR will increase SDR’s representativeness, and promote reform of the international monetary system.

• No matter whether RMB could be included in the SDR basket, the world will need RMB to play an increasingly important role given global liquidity shortage.

6 Plan to make RMB more freely usable

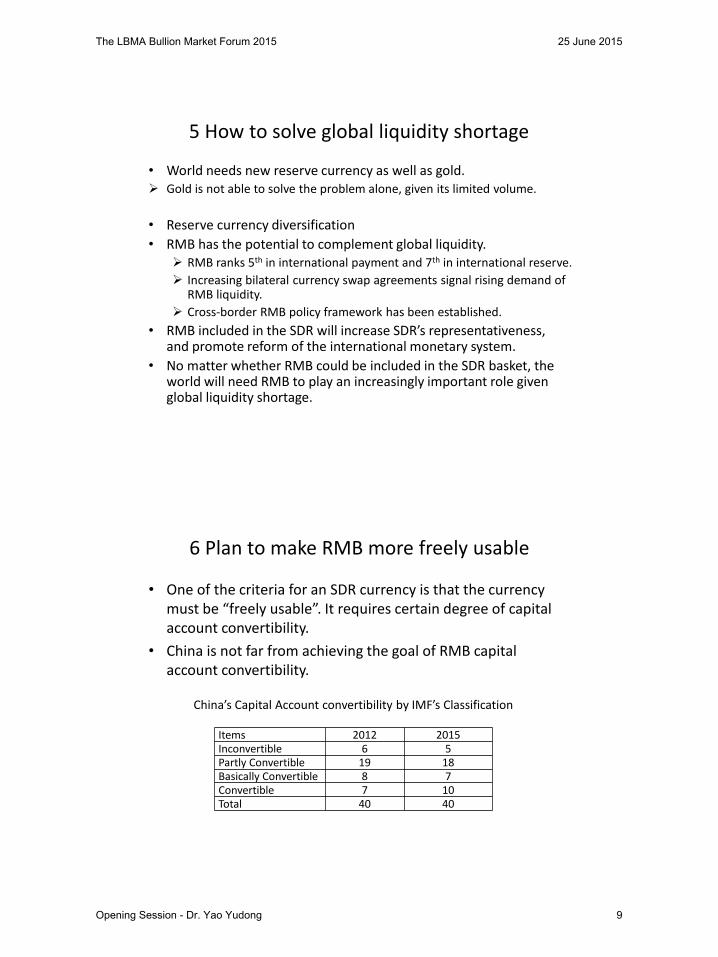

• One of the criteria for an SDR currency is that the currency must be “freely usable”. It requires certain degree of capital account convertibility.

• China is not far from achieving the goal of RMB capital account convertibility.

Items 2012 2015 Inconvertible 6 5 Partly Convertible 19 18 Basically Convertible 8 7 Convertible 7 10 Total 40 40

China’s Capital Account convertibility by IMF’s Classification

The LBMA Bullion Market Forum 2015 25 June 2015

Opening Session - Dr. Yao Yudong 9

Next step

• Personal investment channel: Qualified Domestic Individual Investors(QDII2).

• Capital market: Shenzhen-Hong Kong Stock Connect program, nonresidents will be allowed to issue financial products on the domestic markets with the exception of derivatives, and improved access to the Chinese capital markets by overseas institutional investors.

• Foreign Exchange Regulations: requirements for ex ante approvals in most cases will be removed, and an effective system for ex post monitoring and macroprudential management will be built.

• International use of the RMB: remove unnecessary policy barriers and provide the necessary infrastructure.

• Risk prevention.

Managed convertibility of Capital Account

• After achieving RMB capital account convertibility, China will continue to manage capital account transactions, but in a largely transformed manner, including using macroprudential measures.

• China will retain capital account management in the following four cases:

Money laundering, financing of terrorism, and transactions that overly exploit tax havens.

Macroprudential management of external debt.

Short-term speculative capital flows.

Balance of payments statistics and monitoring

The LBMA Bullion Market Forum 2015 25 June 2015

Opening Session - Dr. Yao Yudong 10

7 Shanghai Gold Exchange (SGE) international board and RMB internationalization

7.1 Gold market is vital to RMB internationalization

• Key function of an international currency: invoicing Presently, most global commodities (petroleum, natural gas, etc.) are

denominated in USD

• RMB has the potential to become an invoicing currency for gold China has been the world’s largest gold producer for 8 consecutive

years

China has one of the fastest growing gold consumption in the world

Shanghai Gold Exchange is the largest exchange-based trading venue for physical gold globally

7.2 SGE international board drives RMB internationalization

1. Promoting the free exchange of RMB in connection with gold investment

Provides a new investment channel for gold for offshore RMB

Facilitates the cross-border use of RMB and the two-way opening up of China’s financial market

2. Enhancing RMB’s role in resource allocation International board gold is quoted and traded in RMB and is attracting

international investors to China’s gold market

China is exerting an ever greater influence on int’l gold market system, helping the formation of a global, RMB-denominated gold price benchmark, as well as raising gold market’s ability to discover and track gold prices in RMB

Increasing number of market participants are investing in gold with RMB or exchanging gold for RMB.

The LBMA Bullion Market Forum 2015 25 June 2015

Opening Session - Dr. Yao Yudong 11

7.2 SGE international board drives RMB internationalization

3. Improving the balance sheet and reducing the portfolio risk of gold holders

Gold price has distinct price movement characteristics and relatively weak correlation with prices of other financial assets. Incorporating gold into a basket of other assets will help mitigate a portfolio’s systemic risk

Including gold assets in a basket of other RMB-denominated assets will help improve the balance sheet and reduce credit risk, therefore encouraging foreign investment using RMB

Thank you!

The LBMA Bullion Market Forum 2015 25 June 2015

Opening Session - Dr. Yao Yudong 12