Embed Size (px)

Citation preview

TM

2017- 18

2 Pantomath Capital Advisors Pvt. Ltd.

TM

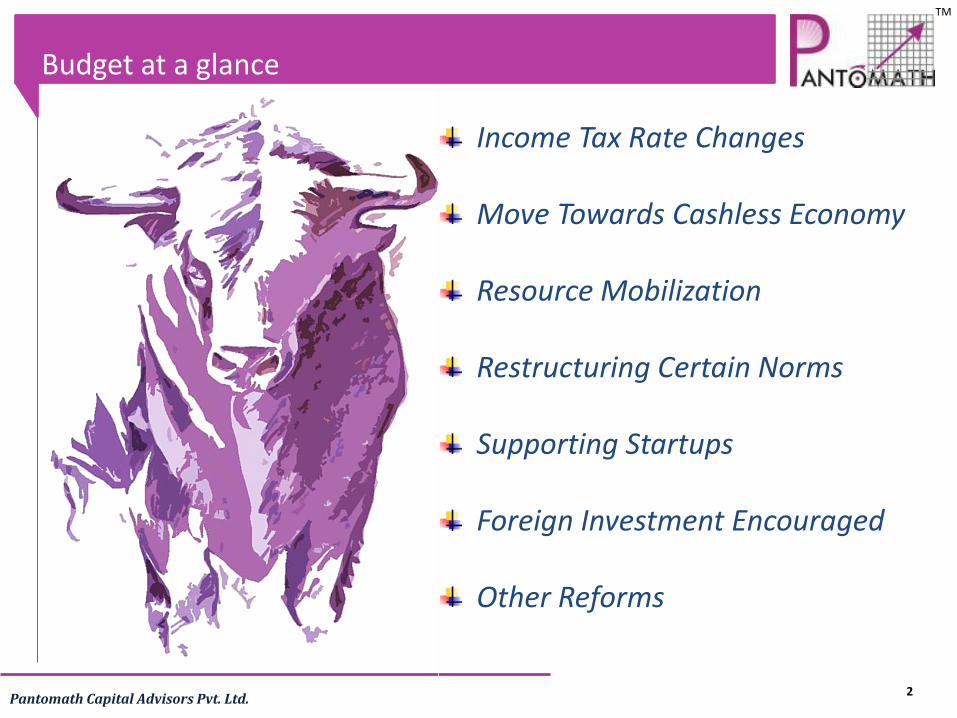

Budget at a glance

Income Tax Rate Changes

Move Towards Cashless Economy Resource Mobilization Restructuring Certain Norms

Supporting Startups

Foreign Investment Encouraged Other Reforms

3 Pantomath Capital Advisors Pvt. Ltd.

TM

Income Tax Rate Changes

• Reduced tax rate at 25 percent (existing 30 percent) for Corporates having Turnover / Gross Receipts upto INR 50 Cr. This rate reduction shall provide a tax breather to SMEs.

• Reduced tax rate at 5 percent (existing 10 percent) for individuals between slab of INR 2.5-5 lakhs.

• Presumptive tax rate u/s 44AD reduced to 6% from 8% earlier (for non cash transactions).

• Surcharge of 10% has been introduced for total income between Rs 50 lakhs to Rs 1 Cr for Individuals/HUF.

NCOME AX

4 Pantomath Capital Advisors Pvt. Ltd.

TM

Move Towards Cashless Economy

This move is towards a cashless economy to reduce generation and circulation of black money

in the country.

• Restricting cash transaction by introduction of new section 269ST, to provide that no person shall receive an amount of Rs 3 lakhs in cash : from a person in a day, in a single transaction; or for transactions relating to one event or on an occasion from a person.

• Restricting cash donations u/s 80G to Rs.2,000 /- (existing limit Rs.10,000/-).

• Disallowance of expenditure in cash in excess of Rs.10,000/- (existing limit Rs.20,000) u/s 40A(3). This limit shall also be applicable to cash payments for capital expenditure for the purpose of depreciation allowance or deduction under investment linked incentive deduction for which no limit existed currently.

• No deduction shall be allowed in respect of capital expenditure in excess of Rs 10,000/- u/s 35AD.

5 Pantomath Capital Advisors Pvt. Ltd.

TM

Resource Mobilization

• Exemption u/s 54EC shall include investment in Central Government notified bonds redeemable after 3 years (earlier only bonds od NHAI and RECL were eligible).

• Shifting of base year from 1981 to 2001 for capital gains computation.

• For classifying any immovable property as long term asset the period of holding is reduced to 24 months from earlier 36 months.

• Maximum amount of loss from house property that can be set off from other heads of income shall be restricted to Rs 2,00,000/- in a year. Rest shall be carry forward upto 8 years and sett off against house property income only in subsequent years.

6 Pantomath Capital Advisors Pvt. Ltd.

TM

• Exemption of long term capital gains tax on income arising on transfer of equity share u/s 10(38) for shares acquired or on after 1st day of October, 2004 shall be available only if the acquisition is chargeable to STT.

• Shares allotted pursuant to preferential allotment etc shall not be exempt under LTCG tax. However, shares allotted under IPO, FPO and other specified corporate transactions shall continue to be covered under LTCG Tax.

• This move aims to curb misuse of capital market platform to book tax free gains through penny stocks.

• In case of transfer of unquoted equity shares, FMV to be considered for capital gains calculation in case where FMV is higher than the actual consideration.

• Conversion of preference shares into equity shares shall not be considered as transfer, hence not liable to tax. Earlier this exclusion was only available for conversion of Bonds and Debentures to equity shares.

Conversion of Equity Shares

Into Preference

Shares

No Tax Liability

Restructuring Certain Norms (1 of 2)

7 Pantomath Capital Advisors Pvt. Ltd.

TM

• Widening the scope of income from other sources by extending the taxability u/s 56(2)(vii) to all tax payers (earlier applicable to only individuals, HUF, firms & Cos).

• In case of real estate developers, no notional income shall be considered as income

from house property for property held as stock in trade upto 1 year from end of FY in which certificate of completion is obtained.

• In order to reduce compliance burden on tax payers, expenditure in respect of

which payment is made to persons referred u/s 40A(2)(b) are to be excluded from domestic transfer pricing provisions u/s 92BA.

• Expenditure to be disallowed if TDS is not deducted from any payment made to resident.

• R & D Cess Act 1986 shall be revoked w.e.f April 2017.

Restructuring Certain Norms (2 of 2)

8 Pantomath Capital Advisors Pvt. Ltd.

TM

Supporting Startups

• In order to promote start ups, carry forward and set off of loss u/s 79 shall now be allowed even if there is a change in the voting rights of the shareholders, provided all the shareholders company remain unchanged from the year in which losses were suffered and 7 years have not been elapsed.

• Deduction of profits for start ups u/s 80IAC shall

now be allowed for 3 out of 7 years.

• MAT credit shall now be allowed to be carried forward upto 15 years (currently allowed upto 10 years).

9 Pantomath Capital Advisors Pvt. Ltd.

TM

Foreign Investment Encouraged

• Income chargeable u/s 9 for deemed income arising from indirect transfers shall not be applicable to Foreign Institutional Investors (FII) and Foreign Portfolio Investors (FPI).

• Concessional withholding rate (TDS) of 5% u/s 194LC charged on interest earned by foreign entities in external commercial borrowings or in bonds and Government securities is extended to 2020. This benefit is also extended to Rupee Denominated Bonds (RDB).

• Capital gains on transfer of RDBs from non residents to non residents shall be exempt.

• Capital gains on transfer of shares of a private limited by a non resident shall be taxed at reduced rate of 10 percent.

• Abolishment of Foreign Investment and Promotion Board (FIPB).

10 Pantomath Capital Advisors Pvt. Ltd.

TM

Other Reforms

• Threshold limit of total sales, turnover or gross receipts increased to 2 Crores (earlier 1 Crore) for requirement audit u/s 44AB.

• Simplified one pager tax return to be filed for individuals with Income up to Rs 5 lakhs.

• Individuals and HUFs are not required to keep BOA if their turnover is upto Rs 25 lakhs or income is upto Rs 2.5 lakhs.

• Rationalisation of time frame for completion of assessment and reassessment.

• If delay in refund is attributable to deductor than interest on such delay refund shall not be payable to deductor.

• Fees for delay in furnishing of return u/s 234F shall be to Rs 5000 (upto 31st Dec of relevant AY ) and Rs 10000/- thereafter.

• In order to promote ease of doing business, Govt has decided to merger Authority of Advance Ruling (AAR) for income tax, central excise , customs duty and service tax.

Disclaimer All data and information is provided for informational purposes only and is not intended for any factual use. It should not be considered as binding / statutory provisions. Neither Pantomath Capital Advisors nor any of its group company, directors, or employs shall be liable for any of the data or content provided for any actions taken in reliance thereon.

Website: www.pantomathgroup.com

E-mail: [email protected]

Online Initiatives: www.smeipo.net | www.dobusinessinindia.in

Landline: (022) 6194 6700 / 2659 8691 Fax: (022) 2659 8690

Corporate Office : Mumbai 406-08, Keshava Premises Bandra Kurla Complex, Bandra (East) Mumbai - 400 051

Other Branch Offices at: Ahmedabad, Jaipur, Nagpur and Surat

Let’s Take It Forward….

Capital Advisors (P) Ltd

Progress with Values

Associate Offices at: Indore, Jamnagar, Jodhpur, Nashik, Pune

Market’s Development Carrier

Entrepreneurs’ Preferred Choice

Investors’ Delight