Embed Size (px)

Citation preview

Domestic dominance

Regional leadership

Global ambitions

June 2017

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

2

Founded in 1964, Qatar Insurance Company (QIC) is the largest insurance powerhouse in the MENA region

QIC - KEY FACTS AND FIGURES – June 2017

3

Solid foundation

Strong financials

Five pillar strategy

Stable sources of income

Strong financial strength

High risk maturity

QIC steadily evolved from a domestic player to a regional leader on to global ambitions over 50 years

GWP: QAR 6.23 billion

Net profit: QAR 505 million

Direct insurance

Specialty insurance

Consistent underwriting performance over 50 years

Outstanding investment contribution

‘A’ (Excellent) AM Best financial strength rating

‘A’ / Stable outlook, Standard & Poor’s financial strength rating

Best in class Enterprise Risk Management practices

ROE: 12.3%

Market Capitalization: QAR 18.6 billion

Reinsurance Life and Medical Asset Management

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

52 YEARS OF OPERATIONAL EXCELLENCE

QIC established

Current Senior Management

appointed

KQIC (Kuwait) and OQIC (Oman) established

Qatar Re established

50th Anniversary and acquisition of

Antares

MENA: QIC No 1 of 116 companies Asia Pacific: QIC No 10 of 264 – excl. L&H World: QIC No 109 of 375 companies

En route to establishing a global footprint based on domestic dominance and regional leadership

4

1964 1968 1986 2002 2004 2006 2009 2011 2014

Q-Life & Medical established

Dubai branch established

Abu Dhabi branch established

QIC International established

QIC Europe Ltd established in

Malta

2015

Antares established Antares Asia in

Singapore

Qatar Re re-domiciled to Bermuda and

established branch in Dubai

Source: S&P CAPITAL IQ

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

SUSTAINED GROWTH FROM DIVERSIFIED SOURCES

17.1

18.4

18.1

14.7

12.3

8,541

14,545

15,139

20,449

18,691

Market Capitalization in QAR million

753

1,001

1,044

1,034

505

2016

2015

2014

2013

June 2016: Financial strength rating ‘A’ (strong), outlook stablewww.standardandpoors.com

Jan 2017: Financial strength rating of ‘A’ (excellent)www.ambest.com

Net profit (attributable to parent)

in QAR million

Return on Equityin %

Earnings per sharein QAR

5

3.12

4.15

4.84

4.48

1.89

QIC

DirectInsurance

Antares

Specialty Insurance

Qatar Life & Medical

Life & Medical

Qatar Re

Reinsurance

QIC Asset Management

Asset Management

QIC Real Estate

Real Estate

QIC Group: Well diversified multi-pillar business set-up

2017 H1

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

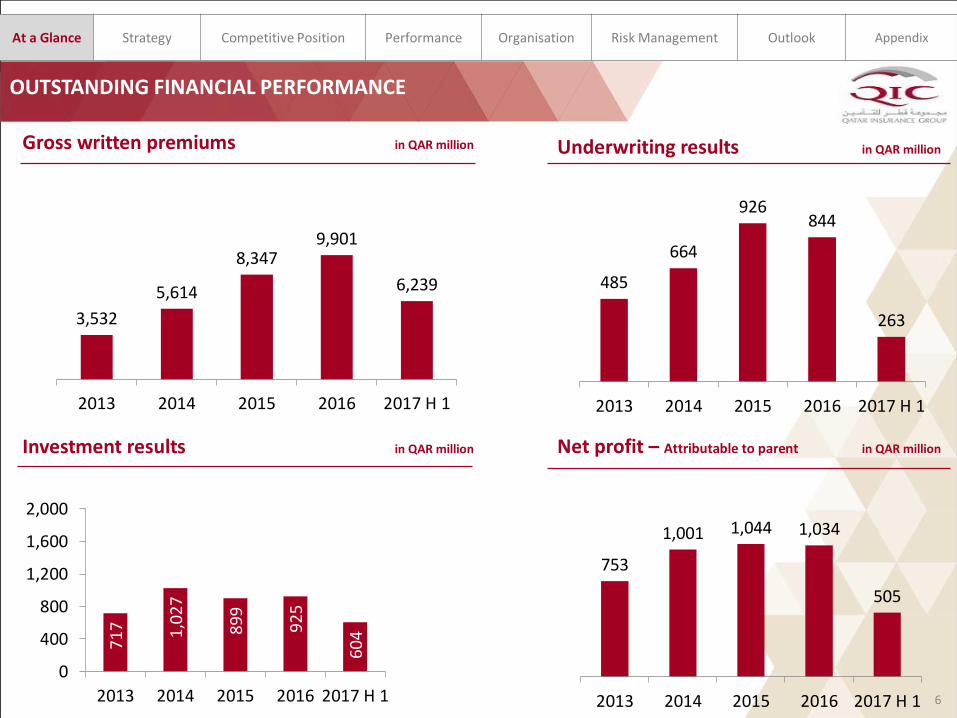

OUTSTANDING FINANCIAL PERFORMANCE7

17 1,02

7

89

9

92

5

60

4

0

400

800

1,200

1,600

2,000

2013 2014 2015 2016 2017 H 1

3,532

5,614

8,3479,901

6,239

2013 2014 2015 2016 2017 H 1

485

664

926844

263

2013 2014 2015 2016 2017 H 1

Investment results in QAR million

753

1,001 1,044 1,034

505

2013 2014 2015 2016 2017 H 1

Net profit – Attributable to parent in QAR million

Gross written premiums in QAR million Underwriting results in QAR million

6

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

Strategy

7

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

Bermuda London Zurich Malta Singapore

• Qatar Re US & NatCat

• Qatar Re HQ

• QIC Europe Ltd • Qatar Re Asia Branch

• Antares Asia

Doha Dubai

• QIC direct insurance operations (UAE)

• Qatar Re DIFC Branch

• QIC Group’s HQ and domestic operations

• QIC Capital

• Oman Qatar Insurance Company

8

Kuwait

• Kuwait Qatar Insurance Company

• QIC direct insurance operations (UAE)

EXPANDING GLOBALLY AND CONSOLIDATING REGIONAL LEADERSHIP

• Qatar Re Continental Europe and global operations

• Antares Group Holdings

• Antares Lloyds 1274 Syndicate

• Qatar Re Rep. Office

MuscatAbu Dhabi

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

QIC Domestic Reinsurance Specialty Life & Medical Asset Management

• Personal lines

o Motor

o Home

o Travel

o PAB

• Commercial lines

o Energy

o Marine & Aviation

o Medical

o Motor

o Property & Commercial

• Agriculture

• Credit & Surety

• Energy

• Engineering

• Facultative

• Marine & Aviation

• Motor

• Property

• Structured Finance

• Aviation

• Financial Institutions

• Marine

• Political and Financial Risk

• Professional indemnity

• Property Excess of Loss

• Terrorism

• Group Life

• Credit Life

• Mortgage Life

• Group Medical

• Proprietary asset management

• Third party asset management

• Collateralized reinsurance (CATCO)

BERMUDA

ZURICH

DOHA

SINGAPORE

LONDON

EXPERIENCED FOR THE FUTURE QATAR RE WORLDWIDE

LATEST NEWS PRODUCTS & SERVICES QATAR RE HUBS

QATAR RE

ANNOUNCES NEW

MANAGEMENT TEAM

Doha, Qatar – 13 May 2013

Lorem ipsum dolor sit amet consectetur

adipiscing elit videst empera de quae

aceribus volestibus adigendelita.

READ MORE READ MORE READ MORE

Qatar Re supports its clients with lead

quotations based on proprietary pricing

capabilities and superior underwriting skills.

Legals ©2014, Qatar Re. LLC

HOME QATAR RE HUBS

Doha

London

Zurich

ABOUT US

Introduction

Management

Corporate Strategy

Capitalization & Ratings

Risk Management

Regulatory Notice

The QIC Group

Careers

NEWS & MEDIAPRODUCTS

Agriculture

Credit & Survey

Energy

Engineering

Marine & Aviation

Motor XL

Property

CONTACT US

SEARCH JOINLOG IN

HOME ABOUT US PRODUCTS QATAR RE HUBS NEWS & MEDIA CONTACT US

“WE ARE COM M I TTED TO BUI LDI NG THE FI RST GLOBAL REI NSURANCE FRANCHI SE, BASED ON

EM ERGI NG M ARKET CAPITAL”

GUNTHER SAACKE

Chief Executive Of cer

BROAD SPECTRUM OF CAPABILITIES

9

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

Competitive Position

10

DOMINANT POSITION IN THE MENA REGION

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

Regional comparison (FY 2016) in QAR million

QIC consistently outperforms major regional insurance and reinsurance groups due to its focus on

Technical excellence in underwriting and asset management

Diversified growth across business segments and geographies11

28

,71

5

13,0

79

6,56

5

7,19

0

6,4

30

6,94

5

4,88

6

3,36

0

4,4

58

9,9

01

7,8

18

2,5

58

3,52

3

2,3

54

7,70

5

2,77

2

771 3,

100

1,03

4

777

300

80 203

612

156

-197

48

-5,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

QIC Tawuniya Orient Oman Ins. Co ADNIC Bupa Arabia Gulf Ins. Co Salama Med Gulf

Total Assets Gross premium Net profit attributable to parent

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

SIGNIFICANT POTENTIAL FOR GLOBAL AND REGIONAL GROWTH

QIC Domestic and regional o Dominant market share in Qatar and ahead

of its peers in MENAo Significant growth potential in rapidly

growing MENA insurance markets

QIC domestic/regional GWP

USD 804 million

MENA Life & Non-Life

USD 50 billion

Qatar Re o Ranked 35th amongst top 50 global reinsurers o Aspires to become a Top 10 reinsurer by 2025o Continues to expand geographically and by line

of business

USD 1.24 billion USD 6 billion

Qatar Re GWP GWP Top 10 reinsurer

Antareso Established as independent Managing

Agent at Lloyd’s, the world’s global insurance and reinsurance market of choice

o Ranks no. 32 within Lloyd’s by GWPo Synergies with QIC have potential to enhance growth

Antares GWP GWP Lloyd’s

USD 453 million USD 40 billion

QIC Group o Aspires to become a Top 50 international composite

insurance groupo Well diversified by geography, lines of business and

sectorso Ranked 109 worldwide by market cap

QIC Group GWP Global Non-Life GWP

USD 2.72 billion USD 1.4 trillion12

BERMUDA

ZURICH

DOHA

SINGAPORE

LONDON

EXPERIENCED FOR THE FUTURE QATAR RE WORLDWIDE

LATEST NEWS PRODUCTS & SERVICES QATAR RE HUBS

QATAR RE

ANNOUNCES NEW

MANAGEMENT TEAM

Doha, Qatar – 13 May 2013

Lorem ipsum dolor sit amet consectetur

adipiscing elit videst empera de quae

aceribus volestibus adigendelita.

READ MORE READ MORE READ MORE

Qatar Re supports its clients with lead

quotations based on proprietary pricing

capabilities and superior underwriting skills.

Legals ©2014, Qatar Re. LLC

HOME QATAR RE HUBS

Doha

London

Zurich

ABOUT US

Introduction

Management

Corporate Strategy

Capitalization & Ratings

Risk Management

Regulatory Notice

The QIC Group

Careers

NEWS & MEDIAPRODUCTS

Agriculture

Credit & Survey

Energy

Engineering

Marine & Aviation

Motor XL

Property

CONTACT US

SEARCH JOINLOG IN

HOME ABOUT US PRODUCTS QATAR RE HUBS NEWS & MEDIA CONTACT US

“WE ARE COM M I TTED TO BUI LDI NG THE FI RST GLOBAL REI NSURANCE FRANCHI SE, BASED ON

EM ERGI NG M ARKET CAPI TAL”

GUNTHER SAACKE

Chief Executive Of cer

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

Performance

13

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

STRONG TRACK RECORD OF TOP AND BOTTOM-LINE GROWTH..

254442

755

1,966

1,471

2012 2013 2014 2015 2016

Key Highlights (QAR million) 2013 2014 2015 2016 2017 H 1

Gross premium 3,532 5,614 8,347 9,901 6,239

Underwriting results 485 664 926 844 263

Net profit (attributable to parent) 753 1,001 1,044 1,034 505

Investment and other income 717 1,027 899 925 604

Earnings per share (restated) 3.12 4.15 4.84 4.48 1.89

Cash dividend per share 2.5 2.5 2.5 1.5 ---

Bonus share 25% 15% 10% 15% ---

Share price at 31 December 66.5 90.6 82 85 67

Operating Free Cash Flow growth in QAR million Total Assets in QAR million

CAGR 55%

11,633 16,332

23,673 28,715

32,629

2013 2014 2015 2016 2017 H1

CAGR 37%

14

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

…AND SHAREHOLDER VALUE CREATION

Dividends in QAR Return on Equity %

Market Value in QAR million

15

QIC shares outperformed QE Index and QE Insurance index

2.50 2.50 2.50 2.501.50

2.00 2.501.50 1.00

1.50

2012 2013 2014 2015 2016

Pay-out ratio

70%66% 85% 64% 62%

Dividend per share Bonus per share

8,541

14,545 15,139

20,449 18,691

5,187 5,705 5,8128,236 8,161

2013 2014 2015 2016 2017 H 1

Market Cap Book Value

17.5 17.1 18.4 18.114.7

12.4

2012 2013 2014 2015 2016 2017 H 1

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

CONSISTENT UNDERWRITING PERFORMANCE

CAGR 25%CAGR 40%

Combined ratio

Gross Premiums In QAR million Net Underwriting Results In QAR million

65%

65%

67%

69%

72%

11%

17%

17%

21%

22%

18%

16%

11%

8%

8%

2013 93%

2014 98%

2015 95%

2016 98%

2017 H 1 102%

Loss ratio Acquisition costExpense Ratio

93%

98%95%

98%

102%

2013 2014 2015 2016 2017 H1

Combined ratio16

2,5593,532

5,614

8,3479,901

2012 2013 2014 2015 2016

343484

664

926 844

2012 2013 2014 2015 2016

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

WELL DIVERSIFIED PORTFOLIO ENHANCES CAPITAL EFFICIENCY

Gross premiums, split by region 2017 H1 Gross premiums, split by line of business 2017 H1

17

Superior geographical and product diversification translates into high capital efficiency

QIC is the only MENA composite insurer with a sizeable international footprint: Qatar Re, Antares and QIC Europe account for 71% of QIC’s total GWP in 2017 H1

Motor business generates 37% of the total GWP

European and Asian business poised for particularly strong growth (based on newly established QIC Europe and Singapore offices of Qatar Re and Antares)

Domestic16%

Regional13%

International71%

Motor 37%

Health & Life14%

Property23%

Energy 5%

Agriculture2%

Marine & Aviation10%

Credit & Surety2%

Liability 5%

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

STRONG TECHNICAL PERFORMANCE IN A HIGHLY COMPETITIVE ENVIRONMENT

Marine and Aviation 2015 2016

Gross premium 943 1,171

Underwriting Results 140 118

Loss ratio 62% 65%

Operating profit 14.9% 10.1%

Property & Casualty 2015 2016

Gross premium 6,489 7,471

Underwriting Results 694 624

Loss ratio 65% 66%

Operating profit 10.7% 8.4%

Life & Medical 2015 2016

Gross premium 915 1,259

Underwriting Results 82 94

Loss ratio 79% 86%

Operating profit 9% 7%

24%

15% (10%)

(16%)

38%15%

in QAR million

in QAR million

in QAR million

18

Gross premium

2015 2016

Underwriting Results

2015 2016

Gross premium

2015 2016

Underwriting Results

2015 2016

Gross premium

2015 2016

Underwriting Results

2015 2016

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

STRONG INVESTMENT YIELD DESPITE LOW INTEREST RATE ENVIRONMENT

Investment portfolio composition 2017 H 1

Investment versus underwriting incomeInvested Assets versus investment income

19

8,28

3

9,56

7

11,4

24 15,4

11

17,4

66

717

1,02

7

899

925

604

-2,500

1,500

5,500

9,500

13,500

17,500

2013 2014 2015 2016 2017 HI

Invested Assets Investment income

in QAR million

40% 39% 46% 48%30%

60% 61% 54% 52%70%

2013 2014 2015 2016 2017 H 1

Underwriting income Investment income

Bonds 45%

Cash 39%

Equity 5%

Private Equity & Funds 8%

Real Estate 3%

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

FOCUS ON SECTOR BALANCE AND SECURITY OF INVESTMENTS

20

Equity: Industry exposure Equity: Currency exposure

Fixed income: Rating Fixed income: Mix by sectorFixed income: Geographic mix

51%

11%

11%

10%

5%

4%4% 3% 1% Financial

Utilities

Basic Materials

Industrial

Consumer, Cyclical

Energy

Communications

Consumer, Non-cyclical

Diversified

71%

24%

3% 2%

A- & Above BBB- to BBB+Not Rated Below BBB-

29%

27%18%

12%

10%

3% 1%

ME-ex Qatar Qatar

Europe North America

Asia Australia

Africa LATAM

54%

23%

9%

5%

4% 3% 2%

Financial GovernmentOthers UtilitiesCommunications Basic MaterialsEnergy Consumer Non-Cyclical

89%

4%

4%2% 1%

QAR

SAR

OMR

KWD

AED

USD

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

HEALTHY INCOME EMANATING FROM QIC ASSET MANAGEMENT

104.8 110.4123.1

51.3

4.7

2013 2014 2015 2016 2017 H 1

Advisory fee income in QAR million

1,19

0

1,67

8

1,80

9

1,75

4

859

717 1,

027

89

9

92

5

60

4

59.2% 61.2%

49.0%

52.0%

70%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

0

600

1,200

1,800

2,400

2013 2014 2015 2016 2017 H1

Total income Investment income

Contribution of investment income in % and QAR million

21

QIC Asset Management consistently contributes about 70% to the Group’s total income

Third party asset management has become a growing and sizable source of income

Efficient treasury function managing the liquidity and balance sheet assets and liabilities

Function provides efficient asset and risk diversification to the Group’s balance sheet

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

EXCELLENT FINANCIAL STRENGTH RATIOS

% 2013 2014 2015 2016

Invested assets to total assets 71% 59% 62% 67%

Invested assets to net technical reserves 339% 188% 119% 139%

Cash and bank deposits to net technical reserves 137% 52% 37% 63%

2013 2014 2015 2016

Eligible Capital 5,688 6,071 7,217 8,066

Solvency Ratio 133% 121% 115% 134%

Solvency: Increased capital utilization, ratio remains strong

Assets

22

133%

121%

115%

134%

2013 2014 2015 2016

Solvency Ratio

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

STRONG FINANCIAL STRENGTH

2015 2016 2017 H 1

Share capital 1,846.21 2,411.39 2773.09

Legal reserve and Share Premium 1,514.14 3145.62 3250.47

General reserve 287.00 287.00 287.00

Catastrophe special reserve 277.34 329.53 381.23

Fair value reserve 139.20 110.87 (109.65)

Retained earnings 1,748.39 1,951.70 1579.60

Equity attributable to parent 5,812.28 8,236.11 8161.74

Non-controlling interest 181.79 232.11 243.14

Total equity 5,994.07 8,468.22 8404.88

Financial strength rating for QIC

QIC Group equity in QAR million

Rating: ‘A’ / StableOutlook: Stable

o “We view QIC as an increasingly diversified insurance group with relatively mature operations in the still-growing Gulf Cooperation Council region, and with rapidly expanding reinsurance operations in Europe.”

Rating: ‘A’/ (Excellent)Outlook: Stable

o “The ratings for Qatar Insurance Company S.A.Q. (QIC) reflect its very strong risk-adjusted capitalisation, robust underwriting performance and global business diversification.”

23

Organisation

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

24

STRONG GEOGRAPHIC AND SECTOR DIVERSIFICATION

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

25

BERMUDA

ZURICH

DOHA

SINGAPORE

LONDON

EXPERIENCED FOR THE FUTURE QATAR RE WORLDWIDE

LATEST NEWS PRODUCTS & SERVICES QATAR RE HUBS

QATAR RE

ANNOUNCES NEW

MANAGEMENT TEAM

Doha, Qatar – 13 May 2013

Lorem ipsum dolor sit amet consectetur

adipiscing elit videst empera de quae

aceribus volestibus adigendelita.

READ MORE READ MORE READ MORE

Qatar Re supports its clients with lead

quotations based on proprietary pricing

capabilities and superior underwriting skills.

Legals ©2014, Qatar Re. LLC

HOME QATAR RE HUBS

Doha

London

Zurich

ABOUT US

Introduction

Management

Corporate Strategy

Capitalization & Ratings

Risk Management

Regulatory Notice

The QIC Group

Careers

NEWS & MEDIAPRODUCTS

Agriculture

Credit & Survey

Energy

Engineering

Marine & Aviation

Motor XL

Property

CONTACT US

SEARCH JOINLOG IN

HOME ABOUT US PRODUCTS QATAR RE HUBS NEWS & MEDIA CONTACT US

“WE ARE COM M I TTED TO BUI LDI NG THE FI RST GLOBAL REI NSURANCE FRANCHI SE, BASED ON

EM ERGI NG M ARKET CAPITAL”

GUNTHER SAACKE

Chief Executive Of cer

Group level

Operations

Direct Insurance:

• Personal Lines• Commercial Lines

Qatar

GCC

Europe

Reinsurance:

• Property & Casualty

• Facultative Lines

Global

Specialty Re/insurance:

• Commercial Lines

Global

Life and Medical:

• Medical Lines

• Life Lines

Qatar

GCC

Asset management:

• Proprietary and TP asset management

Global

Sector

Geography

Risk Management

26

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

STRICT ADHERANCE TO CLEARLY DEFINED ERM PROCEDURES

27

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

1. Establishing Goals: Risk Appetite & Tolerance statement, Strategy & Business Plan for the year

2. Identifying Risks: Risk Registers

3. Analyzing Risks: Risk Score

4. Prioritizing Risks: Risk Prioritization Matrix

5. Risk Mitigation: Control Analysis 6.

Co

mm

un

ica

tin

g an

d C

on

sult

ing

Gro

up

Ris

k St

eeri

ng

Co

mm

itte

es,

En

tity

Bo

ard

, En

tity

R

isk

Co

mm

itte

e,

Au

dit

Ris

k C

om

mit

tee

7. M

on

ito

rin

g an

d R

evie

win

gO

ngo

ing

Pro

cess

o ERM is broken down into Risk Management, Capital Management and Exposure monitoring

o Governance structure follows the three lines of defence model with dedicated Risk Committees in each entity of the company

o Each entity committee reports into the group’s risk steering committee, which reports to the Group’s Board and Audit committee

o Risks are monitored and maintained according to risk categories such as insurance, market, credit, operational and group

o Each risk is assessed for impact and probability along with the controls in place to mitigate

o Risk are reviewed quarterly

o QIC has in place a full-blown stress and scenario testing framework

o QIC conducts analysis into emerging risks

o Risk appetite and tolerance set at the group and entity level with the position against these metrics monitored on an on-going basis

Risk Management at QIC Enterprise risk management cycle

Outlook

28

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

ASPIRING TO BECOME A GLOBAL TOP 50 COMPOSITE INSURER

29

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

Well-diversified business mix Balanced geographical mix Distinct sources of income

A portfolio of powerful franchises

Continue to capitalize on transactional opportunities

Grow QIC Europe

Expand into Asia / Pacific on the back of Qatar and Antares

Further grow medical and life lines in the domestic and regional market

Further build 3rd party investment capabilities

Continue to generate investment income above index and peers

QIC Europe Ltd: Become a common platform for QIC’s entrée into the European insurance markets

Use synergies with Qatar Re in reinsurance and Antares in specialty insurance

Qatar Re: Leverage acknowledged market and product expertise to expand on a global scale, broaden product offering

Antares: Capitalize on Lloyd’s expansion and leverage synergies with Qatar Re

BERMUDA

ZURICH

DOHA

SINGAPORE

LONDON

EXPERIENCED FOR THE FUTURE QATAR RE WORLDWIDE

LATEST NEWS PRODUCTS & SERVICES QATAR RE HUBS

QATAR RE

ANNOUNCES NEW

MANAGEMENT TEAM

Doha, Qatar – 13 May 2013

Lorem ipsum dolor sit amet consectetur

adipiscing elit videst empera de quae

aceribus volestibus adigendelita.

READ MORE READ MORE READ MORE

Qatar Re supports its clients with lead

quotations based on proprietary pricing

capabilities and superior underwriting skills.

Legals ©2014, Qatar Re. LLC

HOME QATAR RE HUBS

Doha

London

Zurich

ABOUT US

Introduction

Management

Corporate Strategy

Capitalization & Ratings

Risk Management

Regulatory Notice

The QIC Group

Careers

NEWS & MEDIAPRODUCTS

Agriculture

Credit & Survey

Energy

Engineering

Marine & Aviation

Motor XL

Property

CONTACT US

SEARCH JOINLOG IN

HOME ABOUT US PRODUCTS QATAR RE HUBS NEWS & MEDIA CONTACT US

“WE ARE COM M I TTED TO BUI LDI NG THE FI RST GLOBAL REI NSURANCE FRANCHI SE, BASED ON

EM ERGING M ARKET CAPI TAL”

GUNTHER SAACKE

Chief Executive Of cer

Domestic17%

Regional13%

International70%

Third party Asset Management 3%

Investments49%

Re/ Insurance

48%Motor38%

Health & Life 13%

Property13%

Energy 5%

Agriculture2%

Marine & Aviation 12%

Credit & Surety 9%

Liability8%

30

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

PROFIT AND LOSS ACCOUNT, 2013 – 2017 H 1

31

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

Income Statement (QAR ‘000) 2013 2014 2015 2016Growth ( YOY)

CAGR 2017 H 1

Gross Written Premium 3,531,707 5,613,767 8,347,210 9,901,394 19% 40% 6,239,181

Net earned premium 1,974,085 3,678,344 5,787,173 8,359,887 44% 54% 4,081,465

Net claims incurred (1,280,266) (2,394,403) (3,862,113) (5,761,487) 49% 54% (2,925,698)

Net commission (211,301) (620,093) (999,317) (1,754,717) 76% 92% (892,952)

Net underwriting income 482,518 663,848 925,743 843,683 -9% 25% 262,815

Investment and Other Income 719,622 1,027,488 898,596 924,851 3% 14% 604,210

G&A Expenses (423,783) (665,926) (760,350) (716,956) -6% 27% (347,690)

Net profit 778,357 1,025,410 1,063,989 1,051,578 -1% 14% 504,904

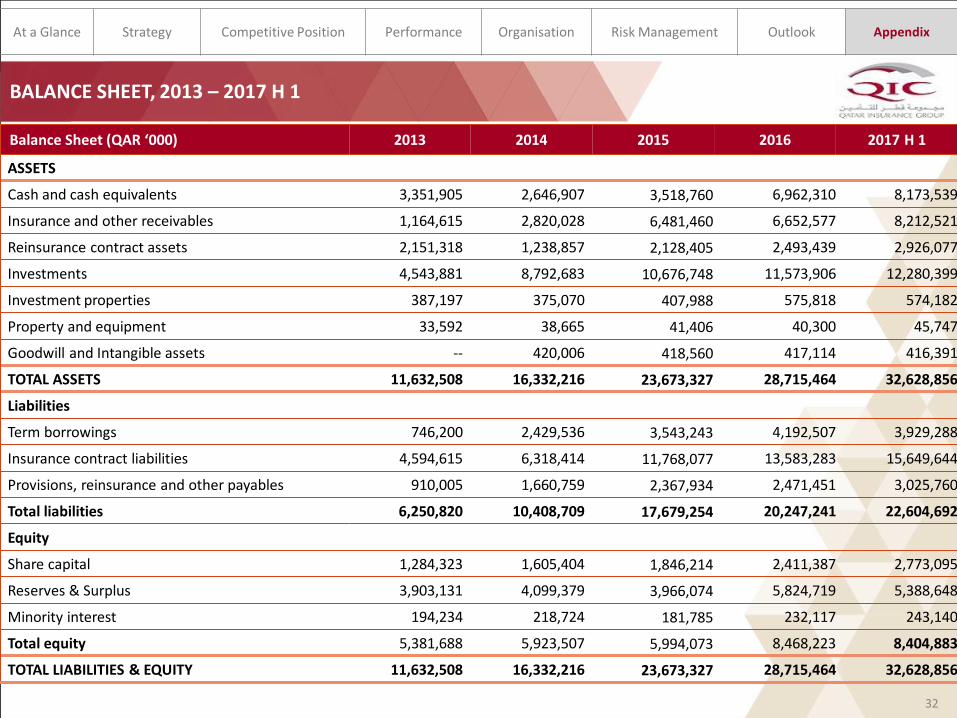

BALANCE SHEET, 2013 – 2017 H 1

32

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

Balance Sheet (QAR ‘000) 2013 2014 2015 2016 2017 H 1

ASSETS

Cash and cash equivalents 3,351,905 2,646,907 3,518,760 6,962,310 8,173,539

Insurance and other receivables 1,164,615 2,820,028 6,481,460 6,652,577 8,212,521

Reinsurance contract assets 2,151,318 1,238,857 2,128,405 2,493,439 2,926,077

Investments 4,543,881 8,792,683 10,676,748 11,573,906 12,280,399

Investment properties 387,197 375,070 407,988 575,818 574,182

Property and equipment 33,592 38,665 41,406 40,300 45,747

Goodwill and Intangible assets -- 420,006 418,560 417,114 416,391

TOTAL ASSETS 11,632,508 16,332,216 23,673,327 28,715,464 32,628,856

Liabilities

Term borrowings 746,200 2,429,536 3,543,243 4,192,507 3,929,288

Insurance contract liabilities 4,594,615 6,318,414 11,768,077 13,583,283 15,649,644

Provisions, reinsurance and other payables 910,005 1,660,759 2,367,934 2,471,451 3,025,760

Total liabilities 6,250,820 10,408,709 17,679,254 20,247,241 22,604,692

Equity

Share capital 1,284,323 1,605,404 1,846,214 2,411,387 2,773,095

Reserves & Surplus 3,903,131 4,099,379 3,966,074 5,824,719 5,388,648

Minority interest 194,234 218,724 181,785 232,117 243,140

Total equity 5,381,688 5,923,507 5,994,073 8,468,223 8,404,883

TOTAL LIABILITIES & EQUITY 11,632,508 16,332,216 23,673,327 28,715,464 32,628,856

QATAR: A THRIVING ECONOMY

33

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

125.

1

16

9.8

190.

3

201.

9

210.

1

174.

6

19.6%

13.4%

4.9%4.6% 4.0%

4.7%

2.00%

6.00%

10.00%

14.00%

18.00%

22.00%

0

50

100

150

200

250

2010 2011 2012 2013 2014 2015**

GDP Growth rate

GDP and real GDP growth in USD billion*

*Source: IMF 2015, ** Projections

Budget surplus 9.1% per annum over the past 5 years

Highest credit rating in the GCC S&P: AA; Fitch: AA;Moody’s: Aa2

Strong population growth Tripled since 2003, 2.6 million in 20162.8

million by 2020

World‘s highest GDP per capita USD 145,000 in 2014

Hydrocarbon vs. Non-hydrocarbon sectors in GDP*

Hydrocarbon reserves ≈ USD 25 trillion

World largest exporter of LNG 77 million tonnesper annum

Investments into infrastructure ≈ USD 150 billionby 2020

National Rail Project ≈ USD 40 billion

*Source: QNB Qatar Economic Insight, 2015

Strong fundamentals Diversifying the economy

125 170 190 202 210

53% 58% 57% 54% 51%

47% 42% 43% 46% 49%

2010 2011 2012 2013 2014

34

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

QATAR’S GROWING INSURANCE SECTOR

878

1,197

1,516

1,9942,200

2010 2011 2012 2013 2014

Total premiums in USD million*

*Source: Swiss Re SIGMA

Insurance Penetration 2015

Source: Swiss Re, Central Bank of Bahrain, EIU Country Data via BVDep

Insurance regulation

BahrainChina

Germany

India

Japan

KuwaitOman Qatar

KSAUAE

UK

USA

0%

2%

4%

6%

8%

10%

12%

1,000 10,000 100,000Pre

miu

ms

as %

of

GD

P

GDP per Capita (Log scale) in USD

Qatar Central Bank (QCB) is the single financial regulator for financial institutions in Qatar

QCB has responsibility for the design and implementation of policies relating to the regulation, control and supervision of financial services and financial markets in Qatar

QCB pursues a consistent risk-based micro-prudential framework in line with global regulatory standards

QIC International and QLM are regulated by the Qatar Financial Centre Regulatory Authority, which is in charge of the insurance sector regulation, reporting to the QCB

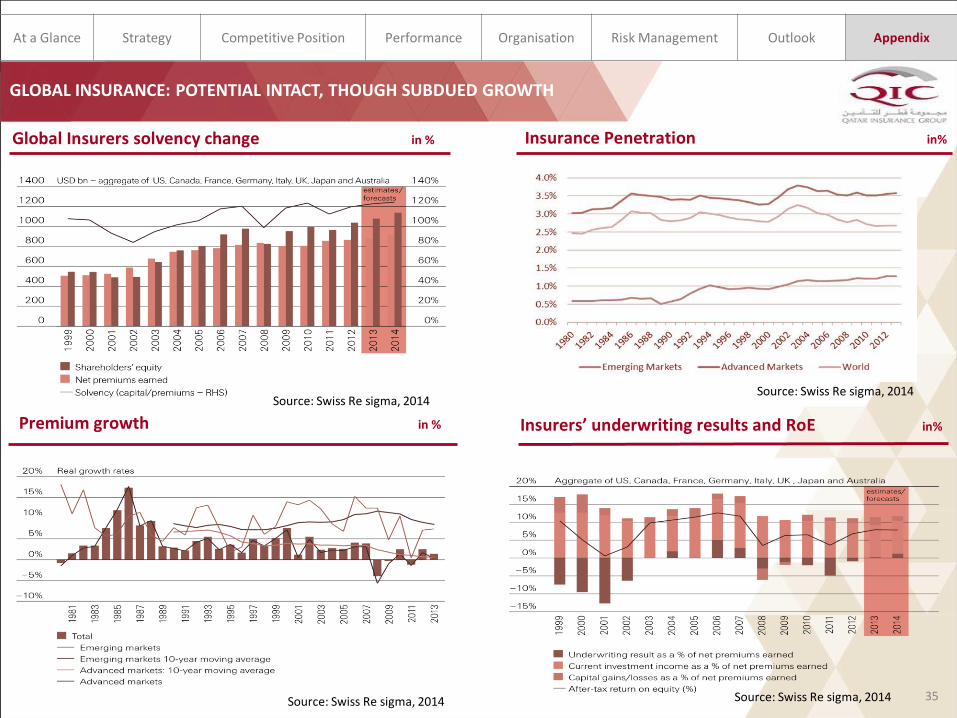

GLOBAL INSURANCE: POTENTIAL INTACT, THOUGH SUBDUED GROWTH

35

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

Global Insurers solvency change in % Insurance Penetration in%

Source: Swiss Re sigma, 2014 Source: Swiss Re sigma, 2014

Source: Swiss Re sigma, 2014 Source: Swiss Re sigma, 2014

Premium growth in % Insurers’ underwriting results and RoE in%

QIC MANAGEMENT TEAM

36

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

Khalifa A. Al SubaeyGroup President & CEO

Ali Saleh Al FadalaSr. Deputy Group President

& CEO

Sunil TalwarGroup CEO - InternationalAhmed El Tabbakh

SVP Group Finance and Advisor to the Group President & CEO

Salem Al-MannaiDeputy Group President & CEO-Mena Region

P.E. Alexander Advisor to the Group President & CEO

Varghese David Group Chief Financial Officer

Stephen RedmondManaging Director-Antares

Sandeep Nanda Group Chief Investment Officer

Gunther SaackeCEO - Qatar Re

Navin KumarCEO-OQIC

Andy RossCEO-QEL

Mark GrahamGroup Chief Risk Officer

Ilango T.COO-UAE Operations

Hassan H. Al JaidahCEO-KQIC

QIC BOARD OF DIRECTORS AND MAJOR SHAREHOLDERS

37

At a Glance Strategy Competitive Position Performance Organisation Risk Management Outlook Appendix

QIC shareholders in %

o Government of 13.92%Qatar

o Qatari Royal 13.71%Family and Associates

o Foreign 9.53%Institutional Investors

o Free Float Remainder

Sheikh Khalid bin Mohammed bin Ali Al-ThaniChairman & Managing Director

Abdullah bin Khalifa Al-AttiyaDeputy Chairman

Khalifa A. Al SubaeyGroup President & CEO

Hussain Ibrahim Al-FardanBoard Member

Jassim Mohammed Al-JaidahBoard Member

Sheikh Hamad bin Faisal bin Thani Al ThaniBoard Member

Sheikh Jassim bin Hamad bin Jassim bin Jabor Al ThaniBoard Member

Sheikh Faisal bin Thani bin Faisal Al-ThaniBoard Member

Sheikh Saoud bin Khalid bin Hamad Al ThaniBoard Member

Khalaf Ahmed Al-MannalBoard Member

The shareholders in its AGM held on 19th Feb 2017 appointed 2 additional directors :1. Sheikh Abdulrahman bin Saud bin Fahad Al Thani2. Ali Youssef Hussein Ali Kamal

THANK YOU

38