Embed Size (px)

Citation preview

Transforming Newell Brands

May 2018

2

DisclaimerThis presentation and any of the information contained herein (this “Presentation”) is for general informational purposes only and is not complete. Under no circumstances is this Presentation intended to be, nor should it be construed as advice or a recommendation to enter into or conclude any transaction or buy or sell any security (whether on the terms shown herein or otherwise). This Presentation should not be construed as legal, tax, investment, financial or other advice. Additionally, this Presentation should not be construed as an offer to buy any investment in any fund or account managed by Starboard Value LP (“Starboard”). All investments involve risk, including the risk of total loss.

This Presentation is not an advertisement. The purpose of this Presentation is to communicate Starboard’s views regarding the companies discussed herein, including Newell Brands Inc. (“Newell,” “Newell Brands” or the “Company”). In making this Presentation available for distribution, Starboard is not acting as an investment adviser with respect to any recipient of this Presentation. Any mention within this Presentation of Starboard’s research process is incidental to the presentation of Starboard’s views regarding the companies described herein.

The views contained in this Presentation represent the opinions of Starboard as of the date hereof. Starboard reserves the right to change any of its opinions expressed herein at any time, but is under no obligation to update the data, information or opinions contained herein. The information contained in this Presentation may not contain all of the information required in order to evaluate the value of the companies discussed in this Presentation.

The views expressed in this Presentation are based on publicly available information, including information derived or obtained from filings made with the Securities and Exchange Commission and other regulatory authorities and from third parties. Starboard recognizes that there may be nonpublic or other information in the possession of the companies discussed herein that could lead these companies and others to disagree with Starboard’s conclusions. Starboard has not sought or obtained consent from any third party to use any statements or information indicated herein as having been obtained or derived from statements made or published by third parties. Any such statements or information should not be viewed as indicating the support of such third party for the views expressed herein. No agreement, arrangement, commitment or understanding exists or shall be deemed to exist between or among Starboard and any third party or parties by virtue of furnishing this Presentation.

None of Starboard, its affiliates, its or their representatives, agents or associated companies or any other person makes any express or implied representation or warranty as to the reliability, accuracy or completeness of the information contained in this Presentation, or in any other written or oral communication transmitted or made available to the recipient. Starboard, its affiliates and its and their representatives, agents and associated companies expressly disclaim any and all liability based, in whole or in part, on such information, errors therein or omissions therefrom.

The analyses provided herein may include certain forward-looking statements, estimates and projections prepared with respect to, among other things, the historical and anticipated operating performance of the companies discussed in this Presentation, access to capital markets, market conditions and the values of assets and liabilities, and the words “anticipate,” “believe,” “expect,” “potential,” “could,” “opportunity,” “estimate,” “plan,” and similar expressions are generally intended to identify such forward-looking statements. Such statements, estimates, and projections reflect Starboard’s various assumptions concerning anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies. Thus, actual results may vary materially from the estimates and projected results contained herein. No representations, express or implied, are made as to the accuracy or completeness of such statements, estimates or projections or with respect to any other materials herein and Starboard disclaims any liability with respect thereto. In addition, Starboard will not undertake and specifically disclaims any obligation to disclose the results of any revisions that may be made to any projected results or forward-looking statements in this Presentation to reflect events or circumstances after the date of such projected results or statements or to reflect the occurrence of anticipated or unanticipated events.

Clients and accounts managed by Starboard (the “Starboard Clients”) may beneficially own, and/or have an economic interest in, shares of certain of the companies discussed in this Presentation and as a result, Starboard and its clients have an economic interest in the forward-looking statements, estimates and projections discussed above and their impact on the companies discussed in this Presentation. The Starboard Clients are in the business of trading – buying and selling – securities, and may trade in the securities of the companies discussed in this Presentation. You should also assume that the Starboard Clients may from time to time sell all or a portion of their holdings of one or more of the companies in open market transactions or otherwise (including via short sales), buy additional shares (in open market or privately negotiated transactions or otherwise), or trade in options, puts, calls, swaps or other derivative instruments relating to some or all of such shares, regardless of the views expressed in this Presentation.

Starboard reserves the right to change its intentions with respect to its investments in the companies discussed in this Presentation and take any actions with respect to investments in such companies as it may deem appropriate, and disclaims any obligation to notify the market or any other party of any such changes or actions.

All registered or unregistered service marks, trademarks and trade names referred to in this Presentation are the property of their respective owners, and Starboard’s use herein does not imply an affiliation with, or endorsement by, the owners of these service marks, trademarks and trade names.

© Starboard Value LP 2018

All Rights Reserved

3

I. Executive Summary 4

II. Brief History of Newell Brands 14

III. Underperformance Creates Opportunity 20

A. Financial Performance 23

B. Issues Have Been Self-Inflicted 46

C. Culture 76

IV. The Opportunity to Improve Newell 83

A. SG&A Improvements 86

B. Procurement Improvements 115

C. Logistics Improvements 142

D. Working Capital Improvements 155

E. Empowering the Workforce to Improve Revenue Growth 163

V. Conclusion 170

TABLE OF CONTENTS

4

I. Executive Summary

5

We Are Excited About the Opportunity at Newell

We have been successful investing in companies with good core assets and helping these companies improve

culture, governance, and performance.

In the following pages, we detail our analysis of Newell Brands’ (“Newell” or the “Company”) business, its

operations, and the significant opportunity we see to create value at the Company.

It starts with people and culture.

– After our settlement with the Company last week, 75% of the Board will be reconstituted, bringing in new

people with fresh, objective, and experienced views on how best to create value at the Company.

– We believe this new Board will work to empower the people responsible for running Newell’s day-to-day

businesses while holding management accountable for reaching its revenue growth and profitability goals.

– We believe this new Board will be able to effectively oversee the Company’s potential divestitures by

comparing the after-tax value Newell can generate today vs. the risk-adjusted standalone operating potential

of the businesses.

With a renewed focus on operations and improving EBITDA, we believe Newell can increase annual profitability by

almost $1 billion, and in turn, substantially increase the stock price.

We are releasing this presentation so that management, the Board, and the shareholders can understand why

we believe there is such a great opportunity at Newell Brands

6

We have done extensive research on Newell Brands, including:

- Working with one of the leading operationally-focused consulting firms, and

- Conducting dozens of interviews with former employees, customers, and suppliers.

We believe there is substantial opportunity for improvement at Newell Brands.

We are sharing this research to provide management, employees, and the Board with

a directional roadmap for operational improvement.

In addition, we believe shareholders should understand the opportunity for

improvement at Newell.

We Are Excited About the Opportunity at Newell (cont’d)

7

We Believe that There Is a Significant Opportunity to

Create Value at Newell

We believe that a new, truly independent Board has a tremendous opportunity to oversee multiple

avenues to create significant shareholder value at Newell

A combination of operational improvements and asset sales could create significant value at Newell.

We believe there are several key tenets to create significant value at Newell:

1. Implement a comprehensive operational improvement plan, that includes:

A company-wide margin improvement plan that we believe will increase EBITDA by $585 to $966 million.

Substantial improvement in Working Capital of ~$800 million to ~$1.1 billion to generate excess cash.

2. Oversee the asset divestiture program.

We believe that a number of Newell’s assets could realize substantial after-tax multiples.

While we are in favor of asset sales, we believe that selling assets on their own is not a panacea for operational

issues and that those must simultaneously be addressed by the new Board.

3. Empower employees to make decisions by removing bureaucratic silos and granting them more P&L responsibility.

4. Enable a truly independent Board to oversee and hold management accountable for executing on its strategy.

1

2

3

4

Source: Company filings and Starboard estimates.

8

We Believe that Asset Sales Executed at the Right Multiples Can

Create Value, but the Process Has to Be Properly Executed…

A combination of asset sales and operational improvements can create significant value at Newell

We believe that Newell owns many valuable assets – and should evaluate strategic alternatives for them – but

the strategic review must be comprehensive and weigh ALL options to determine what is best for long-term

shareholder value creation.

Newell has fantastic brands and businesses. We believe that some of Newell’s assets have the potential to generate high

after-tax multiples and create shareholder value.

However, the process should follow certain parameters:

– The analysis and process should be robust, comprehensive, and focused on exploring strategic alternatives for

ALL of Newell’s assets;

– Newell should look to sell brands and businesses only if they can receive a high after-tax multiple such that the

sale is value accretive;

– All asset sale offer prices should be compared to the risk-adjusted operating plan for each asset and need to

account for potential side effects to other businesses (e.g., raw materials purchasing power, volume discounts,

customer pricing strategies, etc.).

1

2

3

9

…But Asset Sales Are Not a Panacea for Operational

ImprovementWhile asset sales can unlock value, we believe that the focus needs to be on operational improvement, which is

essential to driving long-term value creation at Newell.

Based on our operational improvement plan, 2019 EBITDA would increase to ~$3.1 billion (with Working Capital

ultimately decreasing by ~$800 million to ~$1.1 billion), resulting in a significantly higher value for Newell.

– Our plan is based on improvements that should be well within the control of management and the Board, and, we

believe, that there is an opportunity to immediately begin implementing the plan.

– Management targeted $1 billion in synergies after the acquisition of Jarden which never came to fruition. We believe

many of these opportunities are still available and have been incorporated into our plan.

– Given the resulting significant improvement in free cash flow, asset divestitures are not required to substantially

lower the Company’s current leverage profile.

However, we do believe that some of Newell’s assets have the potential to generate high multiples.

– Given that Newell now intends to explore asset sales for approximately half of the Company, we believe the most

prudent course of action is to evaluate a comprehensive set of strategic alternatives for ALL of the businesses.

– At the very least, we believe that Newell’s industrial and commercial product assets, including Waddington, Process

Solutions, Rubbermaid Commercial Products, and Mapa, are candidates for divestitures given the potential for

strategic acquirers to pay accretive after-tax multiples.

– In addition, we believe that the Company’s portfolio of smaller consumer businesses and brands should be fully

examined to determine which assets are non-core and could potentially generate attractive after-tax sale multiples.

We believe that the Company needs to focus on operational improvements to ensure that the strategic

alternatives process maximizes the value of its assets

Source: Company filings and Starboard estimates.

10

$546

$776

$169

$61

$0

$200

$400

$600

$800

SG&A Procurement Logistics Total

EBITDA Impact

Midpoint of Potential EBITDA Improvement

from Enhanced Operational Execution

We believe that there is a substantial cost improvement and Working Capital opportunity at Newell

Source: Starboard’s proprietary report by a leading consulting firm.

We Have Identified Specific Opportunities to Increase

Annual EBITDA by $585 – $966 Million

Working Capital Opportunity

($ in millions)

We believe there is also the

potential to improve

Working Capital by $800

million to $1.1 billion,

which would significantly

increase cash available for

capital deployment

We have retained one of the leading operationally-

focused consulting firms to assist us with this analysis

11

We Have Identified Specific Opportunities to Increase

Annual EBITDA by $585 – $966 Million (cont’d)

– Selling, General & Administrative expenses are bloated, causing inefficiencies.

– Transformation and integration spend appears excessive and is not fully accounted for in the adjusted numbers.

– Layers of redundant executives and vice presidents add complexity.

– Newell is inefficient in business support categories, such as HR and Finance & Accounting.

– The Company appears to have a large Information Technology & support staff for a company of its size.

– Newell’s lax Travel & Entertainment expense policies have resulted in unnecessary costs.

Selling, General &

Administrative

Working Capital

Logistics

Procurement

– Newell’s Working Capital usage is currently much higher than comparable company benchmarks.

– Days Sales Outstanding and Days Inventory Outstanding are significantly higher than industry averages.

– Inventory levels are materially higher than peers.

– The Company has failed to meaningfully improve its cash conversion cycle over time.

– The Company has failed to integrate legacy Newell Rubbermaid and Jarden warehousing networks.

– Multiple Transportation Management Systems (TMSs) present organizational challenges and increase costs.

– Newell concentrated its product discharge to Southern California, giving the appearance of consolidation, but

costs may have actually increased on the back-end because a mile transported on land is much more expensive.

– Lack of collaboration with major retailers has led to unnecessary steps in the distribution process.

– The Company lacks a well structured low-cost-country (LCC) sourcing strategy and make-vs-buy strategy.

– Products in several segments are “over-spec’d” or “over-engineered” versus the competition.

– A decentralized sourcing strategy for materials hinders the Company’s ability to leverage best-in-class processes.

We believe there are a number of opportunities that can substantially improve operating performance.

Source: Starboard’s proprietary report by a leading consulting firm.

12

Fwd

Comparable Companies EV/EBITDA

Church & Dwight Co., Inc. 13.8x

The Clorox Company 12.4x

Colgate-Palmolive Company 14.0x

Fortune Brands Home & Security, Inc. 10.3x

Henkel AG & Co. KGaA 11.5x

Prestige Brands Holdings, Inc. 10.4x

The Procter & Gamble Company 11.8x

Reckitt Benckiser Group plc 14.1x

Spectrum Brands Holdings, Inc. 13.7x

Stanley Black & Decker, Inc. 11.4x

Tupperware Brands Corporation 6.3x

Unilever PLC 13.1x

Mean 11.9x

Median 12.1x

High 14.1x

Low 6.3x

Low Mid High

Net Sales 14,655$ 14,655$ 14,655$

Adj. EBITDA 2,557$ 2,557$ 2,557$

Margin (%) 17.4% 17.4% 17.4%

(-) Transformation Office Expenditure (247) (247)$ (247)$

Pro Forma Adj. EBITDA 2,310$ 2,310$ 2,310$

Cost Opportunities:

(+) Selling, General & Administrative 399$ 546$ 693$

(+) Procurement 137$ 169$ 200$

(+) Logistics 49$ 61$ 73$

Total Cost Opportunity 585$ 776$ 966$

Adjusted EBITDA 2,895$ 3,086$ 3,276$

Margin 19.8% 21.1% 22.4%

EBITDA Multiple 10.0x 10.5x 11.0x

Enterprise Value 28,953$ 32,402$ 36,041$

(-) Net Debt (10,103) (10,103) (10,103)

(+) Working Capital Opportunities 800$ 950$ 1,100$

Equity Value 19,650$ 23,249$ 27,038$

Newell Brands Value per Share 40.50$ 47.92$ 55.73$

Upon executing our operational turnaround plan, we believe we can create Newell at approximately 6.7x – 7.6x

pro forma EV / EBITDA, compared with an average multiple since the Jarden acquisition of ~11.4x. By

executing this plan, we believe there is significant upside.

We Believe An Operational Turnaround Could Create

Significant Shareholder Value

We believe Newell Brands represents an extremely compelling investment opportunity

Source: Bloomberg, CapitalIQ, Company filings, and Starboard estimates.

(1) Consensus FY 2019E Revenue and FY 2019E EBITDA (excluding estimates which account for divestiture plan).

(2) Includes Starboard estimate for Transformation Office expense of $247 million.

Value Creation Opportunity

($ in millions, except per share data)

Identifiable

EBITDA

improvement

opportunities

explained in

detail in

Section IV

Peer Multiples

We believe we are being

conservative in our

EBITDA multiple

estimate, which we place

at a discount to peers

(1)

(1)

(2)

13

We Believe That Newell Is Undervalued with Substantial

Opportunities to Create Value

We believe Newell could be worth $47.92 per share, or 81% upside from where it currently trades

Source: CapitalIQ, Bloomberg, Company filings, and Starboard estimates.

Note: Stock price as of April 20, 2018.

Value Creation Opportunity

$26.44

$47.92

$16.78

$2.74

$1.96

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

$55

Current

Stock Price

EBITDA Improvement

(10.5x Multiple)

Current EBITDA

(10.5x Multiple)

Working Capital

Improvements

Pro Forma

Stock Price

Pro forma for an operational turnaround, which we believe is well within control of management and the

Board, we believe that Newell is extremely undervalued.

14

II. Brief History of Newell Brands

15

The merger of Newell Rubbermaid and Jarden combined portfolios of extremely well-recognized

brands, which should have generated strong growth and value for shareholders

Source: Company filings.

Note: Acquisition price includes debt assumed and net of cash acquired.

A Transformational Acquisition Created One of the Most

Prominent Consumer Products CompaniesIn April 2016, Newell Rubbermaid acquired Jarden for $18 billion in cash and stock, creating one of the most

powerful forces in the consumer products space.

16

The Combined Business Generated ~$16 Billion in

Revenue…This was a transformational transaction, as Newell more than doubled its revenue, tripled its employee base,

and significantly increased its financial leverage.

The combined company formed one of the largest global providers of consumer and commercial products

Source: Company filings.

(1) Revenue based on each management team’s FY2016 projections on a stand-alone basis from the merger proxy (excluding the results of Venezuelan operations).

$5.9 Billion $10.1 Billion $16.1 Billion

2016 Net Sales(1)

Jarden

Newell

Rubbermaid

($ in billions)

17

…And ~$2.7 Billion in EBITDA with Significant Synergy

Opportunities

By acquiring Jarden, Newell more than doubled its EBITDA

$1.1 Billion $1.6 Billion $2.7 Billion

2016 Adjusted EBITDA(1)

Jarden

Newell

Rubbermaid

Following the Jarden acquisition, management promised $500 million in synergies (later increasing that target

to $1 billion in synergies) and EBITDA margins over 20% with greater than $3 billion in EBITDA.

($ in billions)

Source: Company filings.

(1) Adjusted EBITDA based on each management team’s FY2016 projections on a stand-alone basis from the merger proxy (excluding the results of Venezuelan operations).

18

(35%)

+4%

+29%

64

% U

nd

erperfo

rma

nce

Share Price Performance(1)

+7%

+24%

(2)

(3)

Since the Deal Closed, Newell Has Significantly

Underperformed…A series of operational missteps has caused Newell’s stock to underperform the S&P 500 by 64% since the

Jarden acquisition.

Newell has massively underperformed its sector and the overall market

Source: CapitalIQ.

(1) Total returns include dividends from April 18, 2016 (first day of trading as a combined company following Jarden acquisition) to February 8, 2018 (closing price before Newell confirmed receipt of Starboard’s director nominations).

(2) NWL’s 2017 Proxy Peer Group includes: MMM, AVY, TSE:6448, CLX, CL, DHR, TSX:DII.B, ECL, OM:ELUX B, EMR, EL, ITW, KMB, MAS, MAT, TSE:6503, SHW, ENXTPA:BB, SWK, VFC, and WHR.

(3) Includes CHD, CL, CLX, FBHS, XTRA:HEN3, PBH, PG, LSE:RB., SWK, SPB, TUP, and LSE:ULVR.

19

…But Continues to Own Fantastic Brands

Newell owns more than 50 leading brands that operate in large, growing, and unconsolidated global categories.

Newell’s diverse product portfolio contains many well-recognized and market-leading brands

Source: Company filings.

Note: Excludes Newell Brands “Other” segment.

FY2017 Net Sales $5.6B

Core Growth Rate 0.1%

Adj. Operating Margin 12.4%

Key Brands:

LIVE

FY2017 Net Sales $2.8B

Core Growth Rate 1.8%

Adj. Operating Margin 21.9%

Key Brands:

LEARN

FY2017 Net Sales $2.8B

Core Growth Rate 1.1%

Adj. Operating Margin 16.7%

Key Brands:

WORK

FY2017 Net Sales $2.6B

Core Growth Rate 1.4%

Adj. Operating Margin 12.0%

Key Brands:

PLAY

20

III. Underperformance Creates Opportunity

21

Newell’s Share Price Has Dramatically Underperformed Both

the Market and Its Peers…

Source: CapitalIQ.

(1) Total returns for all periods include dividends. Performance is measured as of February 8, 2018 (last closing price before Newell confirmed receipt of Starboard’s director nominations).

(2) NWL’s 2017 Proxy Peer Group includes: MMM, AVY, TSE:6448, CLX, CL, DHR, TSX:DII.B, ECL, OM:ELUX B, EMR, EL, ITW, KMB, MAS, MAT, TSE:6503, SHW, ENXTPA:BB, SWK, VFC, and WHR.

(3) Includes CHD, CL, CLX, FBHS, XTRA:HEN3, PBH, PG, LSE:RB., SWK, SPB, TUP, and LSE:ULVR.

(4) Newell Rubbermaid’s acquisition of Jarden Corporation closed on April 15, 2016.

One-Year Stock Price Chart

Newell’s stock price has materially underperformed the broader equity markets, its Proxy Peer Group and its

closest direct competitors over the last 1-, 3-, and 5-year periods.

Stock Price Chart since April 15, 2016(4)

Five-Year Stock Price Chart

Summary ReturnsTotal Shareholder Return

(1)

1 Year 3 Year 5 Year

Acquisition of

Jarden Corp.

S&P 500 Index 14.7% 33.7% 88.7% 28.7%

DJ U.S. Consumer Goods Index 4.1% 14.4% 48.8% 6.6%

2017 Proxy Peer Group (2)

15.0% 33.3% 100.8% 24.1%

Closest Direct Peers(3)

(1.9%) 20.6% 67.0% 3.8%

Newell Brands Inc. (38.3%) (22.3%) 27.7% (35.0%)

Underperformance vs. S&P 500 (53.0%) (56.0%) (61.1%) (63.7%)

Over/(Underperformance) vs. Consumer Goods Index (42.4%) (36.7%) (21.1%) (41.6%)

Over/(Underperformance) vs. 2017 Proxy Peer Group (53.3%) (55.7%) (73.1%) (59.1%)

Over/(Underperformance) vs. Closest Direct Peers (36.4%) (42.9%) (39.4%) (38.8%)

22

Newell Has Also Underperformed on a Number of

Important Metrics

Current quantitative and qualitative metrics show substantial room for improvement

Source: CapitalIQ, Bloomberg, Company filings, and Glassdoor.

(1) Includes CHD, CL, CLX, FBHS, XTRA:HEN3, PBH, PG, LSE:RB., SWK, SPB, TUP, and LSE:ULVR.

While many of these metrics are disappointing, they also point to substantial opportunity.

COGS (% of Revenue)

Revenue per Employee Board TurnoverOrganic Revenue Growth

EBITDA Margin Employee Morale

($ in million)

5 board

members

resigned in the

span of two

months

Newell ranks

dead last among

its peers in

several Glassdoor

categories

(1)

(1)

Significant

deceleration in

organic

revenue growth

over the past 8

quarters

23

III. Underperformance Creates Opportunity

A. Financial Performance

24

We believe that significant opportunity exists to dramatically improve Newell’s financial performance,

closing the gap versus peers on both margins and valuation

Financial Performance Has Been Suboptimal,

Substantial Opportunity Exists for ImprovementNewell has struggled to improve its margins and execute on its financial targets following the Jarden

acquisition. In addition, its poor communication and inability to achieve expectations has frustrated investors.

Newell’s margins are among the worst in its peer group and well below the peer average.

EBITDA margins are significantly below management’s targets and best-in-class peers, despite supposed synergy

realization from the Jarden transaction.

Compared to peers, Newell trades at some of the lowest multiples on several valuation metrics (e.g., EV/EBITDA,

P/E), reflecting investors’ lack of confidence.

Newell management was very optimistic about the combination with Jarden, but execution and communication since the

acquisition has been poor.

Management believed that the strategic rationale was compelling and that the combination created substantial scale

in key geographies, customers, and channels.

Newell’s management expected to achieve significant synergies from the Jarden acquisition, stating that they had

“clear line of sight to $500 million”, and even doubled the synergy target to $1 billion.

Newell management has been unable to achieve its guidance targets, which has severely frustrated investors.

Following the Jarden synergy capture, Newell management expected the Company to generate >$3 billion of

EBITDA with >20% EBITDA margins. However, EBITDA has declined since the Jarden acquisition.

Revenue growth has been consistently decelerating for the past 8 quarters and Newell lowered its financial

guidance several times throughout 2017.

Source: Company filings.

25

Newell’s Margins Are Substantially Below Peers

33.0%

28.8% 28.4%

25.9%

23.6%

21.4% 21.1% 20.9% 20.6% 20.0% 19.8%

16.9% 16.7% 16.6%

PBH LSE

RB

CL PG CHD CLX SPB LSE

ULVR

XTRA

HEN3

NWL

Mgmt Target

TUP NWL SWK FBHS

Source: CapitalIQ, Bloomberg, Company filings, and Starboard estimates.

Newell’s EBITDA margins are significantly below management’s targets and best-in-class peers, despite its

product portfolio consisting of valuable brands in large, growing, and unconsolidated global categories.

Newell’s peer group consists of a diverse set of companies operating in the Consumer Durables, Consumer Discretionary,

and Household Products industries.

Newell’s low EBITDA margins reflect a bloated cost structure and poor operating performance.

2018E EBITDA Margins

Peer Average: 23.1%

Newell’s EBITDA margins are among the worst in its peer group and substantially below the peer average

26

21.9x 21.3x 20.2x

19.3x 19.0x 17.2x 17.1x 17.1x 17.0x

15.8x

10.5x 9.9x 9.0x

SPB CL CHD LSE

ULVR

CLX PG LSE

RB

SWK XTRA

HEN3

FBHS PBH NWL TUP

And the Company Now Trades at a Significant Discount to

Peers

14.1x 14.0x 13.8x 13.7x 13.1x

12.4x 11.8x 11.5x 11.4x

10.4x 10.3x 9.4x

6.3x

LSE

RB

CL CHD SPB LSE

ULVR

CLX PG XTRA

HEN3

SWK PBH FBHS NWL TUP

Poor operating performance and missed expectations have led to Newell trading at a substantial discount to peers on several key valuation metrics.

Enterprise Value / CY2018E EBITDA

Price / CY2018E EPS

Peer Average: 17.1x

Peer Average: 11.9x

Source: CapitalIQ and Bloomberg.

Note: Market data as of April 20, 2018.

Newell is deeply undervalued relative to peer valuations

27

87.5% 86.3% 85.2% 85.1%83.5% 82.7% 82.5% 80.3% 79.5% 78.0%

74.6% 72.9%69.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

NWL FBHS SWK SPB TUP XTRA

HEN3

LSE

UVLR

CLX CHD PG CL LSE

RB

PBH

Newell Brands Maintains the Highest Expense Ratio Even

After “Synergies” from the Jarden Acquisition

Cost Profile (% of Revenue)

Compared to peers, Newell’s total expense ratio is the highest, indicating a substantial opportunity to reduce

costs.

An opportunity exists to significantly reduce costs and improve margins at Newell

$14.7B $5.3B $12.7B $5.0B $2.3B €20.0B €53.7B $6.0B $3.8B $65.7B $15.5B £11.5B $1.0B

2017

Revenue:

Source: CapitalIQ, Bloomberg, and Company filings.

Note: Based on LTM cost of goods sold and total operating expenses.

(1) Includes Starboard estimate for Transformation Office expense of $247 million.

(1)

28

Newell CEO Michael Polk was extremely bullish on the acquisition of Jarden

“The combination creates substantial scale in key

geographies, customers and channels, enabling us to leverage

an advantaged set of brand development and commercial

capabilities to accelerate the deployment and impact of our

portfolio in international markets, in key customers and in fast-

growing channels like e-commerce.”

- CEO Michael Polk,

Jarden Corp. and Newell Rubbermaid Merger Call (December 2015)

Newell was Optimistic About the Operational Prospects of

the Jarden Acquisition The Newell and Jarden combination was intended to establish a best-in-class brand portfolio with unmatched

growth potential and the opportunity to realize sizeable revenue and cost synergies.

“The strategic rationale for combining the two companies is clear and compelling. Both Newell Rubbermaid and Jarden

have strong portfolios of leading brands that are number one or number two in their categories. The combined brand portfolio

is quite concentrated, with the top 30 brands delivering about 80% of the revenue, which will enable us to focus investment

quite easily.”- CEO Michael Polk, Jarden Corp. and Newell Rubbermaid Merger Call (December 2015)

Source: Company filings.

Merger Presentation - “A Winning Combination” (December 14, 2015)

29

Newell Expected to Achieve Significant Synergies from the

Jarden Acquisition…

Newell promised significant synergy realization from the Jarden acquisition

Newell predicted substantial upside from the anticipated cost synergies.

Shareholders put their faith in Michael Polk and the management team, realizing there was tremendous strategic

value between the two assets and various ways to win, including:

– Revenue synergies with the complementary business models;

– Substantial cost synergies in purchasing, manufacturing and corporate expenses;

– Greater leverage with retailers and suppliers, with opportunities for supply chain optimization; and

– A lower tax rate on Jarden businesses, among many others.

Many sell-side analysts believed that the synergy estimate, representing less than 4% of the combined cost structure,

was conservative, and there was the potential for much more.

“We have a clear line of sight to $500 million in anticipated cost synergies…And we wouldn’t have taken [on the merger

with Jarden had we] not seen tremendous upside beyond what we’re committing to today.”

- CEO Michael Polk, Jarden Corp. and Newell Rubbermaid Merger Call (December 2015)

1

2

3

4

Source: Company filings.

30

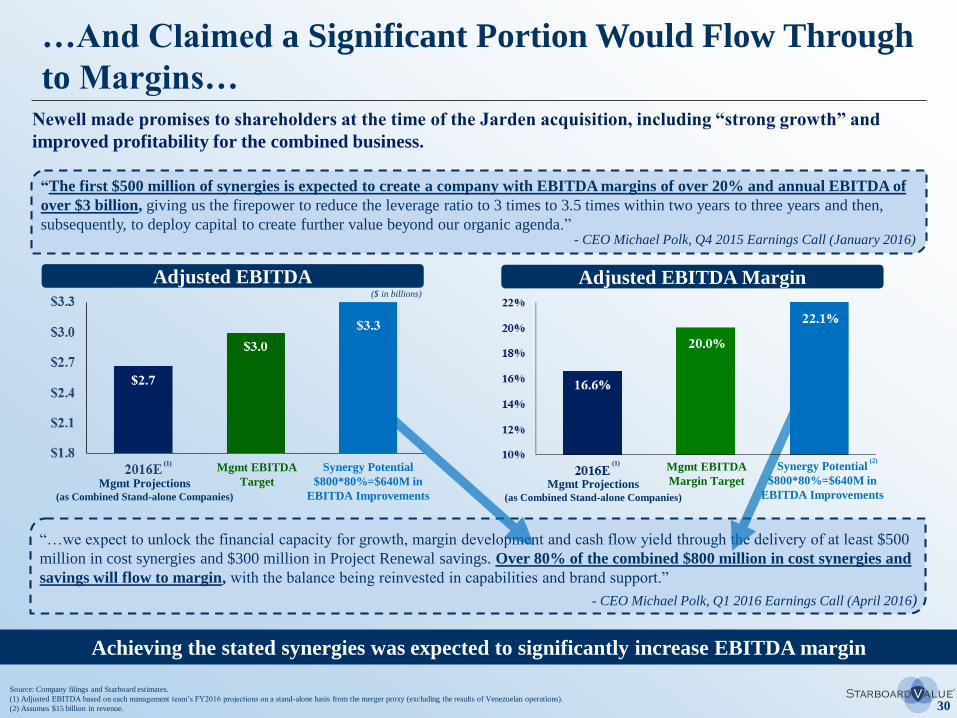

…And Claimed a Significant Portion Would Flow Through

to Margins…

Achieving the stated synergies was expected to significantly increase EBITDA margin

Newell made promises to shareholders at the time of the Jarden acquisition, including “strong growth” and

improved profitability for the combined business.

“The first $500 million of synergies is expected to create a company with EBITDA margins of over 20% and annual EBITDA of

over $3 billion, giving us the firepower to reduce the leverage ratio to 3 times to 3.5 times within two years to three years and then,

subsequently, to deploy capital to create further value beyond our organic agenda.”- CEO Michael Polk, Q4 2015 Earnings Call (January 2016)

“…we expect to unlock the financial capacity for growth, margin development and cash flow yield through the delivery of at least $500

million in cost synergies and $300 million in Project Renewal savings. Over 80% of the combined $800 million in cost synergies and

savings will flow to margin, with the balance being reinvested in capabilities and brand support.”

- CEO Michael Polk, Q1 2016 Earnings Call (April 2016)

Adjusted EBITDA($ in billions)

Mgmt Projections(as Combined Stand-alone Companies)

Mgmt EBITDA

Target

Mgmt EBITDA

Margin Target

Source: Company filings and Starboard estimates.

(1) Adjusted EBITDA based on each management team’s FY2016 projections on a stand-alone basis from the merger proxy (excluding the results of Venezuelan operations).

(2) Assumes $15 billion in revenue.

Mgmt Projections(as Combined Stand-alone Companies)

(1) (1)Synergy Potential

$800*80%=$640M in

EBITDA Improvements

Adjusted EBITDA Margin

Synergy Potential

$800*80%=$640M in

EBITDA Improvements

(2)

31

…Then Even Doubled the Synergy Target

Less than one year after closing the Jarden acquisition, Newell management doubled its synergy target

“We've been conservative in our

assumptions, but we'll pursue every

opportunity we uncover. We have no

revenue synergies, no working capital

benefits, and no tax synergies in our deal

economics and have a very clear line of

sight to at a minimum $500 million of

cost synergies.”

- CEO Michael Polk, Q4 2015 Earnings Call

January 2016

“But we believe we can now deliver $1 billion of synergies, on top of that $300 million in project renewal savings. That gets us to $1.3 billion in cumulative savings over the timeframe from 2016 through 2021. And so, that's going to be an important part of the algorithm. It drives margin development.”

- CEO Michael Polk, 2017 CAGNY Investor Conference

February 2017

Following the announcement of

the merger with Jarden,

management provided a synergy

target of $500 million, claiming

the target was conservative…

…leading them to double the

synergy target to $1 billion just

one year later

Source: Company filings.

32

Sell-side Analysts Were Also Excited by the Combination

Wall Street echoed Newell management’s bullishness towards the Jarden acquisition

Source: Wall Street equity research.

Research analysts also saw strategic value in the acquisition, highlighting the combination’s potential and their

excitement within their research reports.

“We Are Positive on JAH Deal”

“JAH Acquisition Adds Significant Scale

and Cost Synergies”

“…JAH and NWL have complementary

portfolios, unmasking significant revenue growth

opportunities in cross-selling, geographic expansion

and retail relationships.”

- Gabelli, February 2016

“The Perfect Recipe”

“The deal makes a lot of sense from a

financial perspective, particularly once

synergies kick in.”

“We see tremendous merit in the potential merger

and note the following:

(1) Business models are complementary; not competitive; we see

minimal anti-trust risk; there is limited direct product or

category overlap;

(2) Both companies are specialists in durable goods businesses,

with margin rich consumables (non-staples) businesses;

(3) Mix based product margins are quite different, with NWL

exceeding JAH by nearly 700bps; we expect merger synergies

to be concentrated in COGS at the onset, based on baseline

savings in procurement, sourcing, logistics, warehousing, and

distribution;

(4) The combined entity would have near $16 billion in revenue in

2016; $10 billion domestic and $6 billion in international

markets;

(5) Combined EBITDA (pre-synergy) nears $2.5 billion; $500M in

identified synergies appears conservative in our view;

(6) Both companies have 10%+ exposure to mass retail but we note

that NWL is more exposed to big box specialty including home

improvement, office, and baby while JAH has exposure to club,

sporting goods, and department stores.”

- Piper Jaffray, December 2015

- Raymond James, December 2015

- Gabelli, February 2016

- Piper Jaffray, December 2015

- JP Morgan, December 2015

33

What Exactly Comprised the Synergy Opportunity?

Newell believed that the combination with Jarden would generate significant scale benefits

Source: Company filings.

The Company promised to deliver $500 million (and later $1 billion) in cost synergies from the Jarden

acquisition.

Excerpts from Newell’s Presentation upon Deal Announcement

The Jarden acquisition made Newell one of the largest consumer products companies in the world.

This combination was expected to generate meaningful economies of scale in purchasing, SG&A leverage,

distribution, and transportation, among other expense categories.

Newell stated that the Jarden acquisition created ~2x – 4x the scale at major retailers.

34

Management identified several areas of opportunity to achieve the $500 million of cost savings.

Newell’s management team outlined numerous initiatives to achieve the $500 million synergy target

Source: Company filings.

What Exactly Comprised the Synergy Opportunity? (cont’d)

- Deutsche Bank Global Consumer Conference (June 2016)

35

Newell management expected to deliver the $500 million of synergies earlier than its previous forecast

Management also articulated a specific timeline to achieve the stated synergies.

Source: Company filings.

What Exactly Comprised the Synergy Opportunity? (cont’d)

- Barclays Consumer Staples Conference (September 2016)

36

The Company has reported almost $600 million in synergies and savings over the past two years.

However, EBITDA has actually declined during that timeframe

Yet, EBITDA Has Declined Since the Acquisition…

Adjusted EBITDA Comparison

($ in billions)

Jarden

Newell

Rubbermaid

$2.6$2.4

Newell has reported significant synergies and savings since the combination with Jarden. Yet, EBITDA has

actually declined two years post the acquisition.

Source: Company filings and Starboard estimates.

(1) Adjusted EBITDA based on each management team’s FY2016 projections on a stand-alone basis from the merger proxy (excluding the results of Venezuelan operations); adjusts for Tools segment sale.

(2) Adjusts for Tools segment sale and includes Starboard estimate for Transformation Office expense of $247 million.

(1) (2)

Transformation Office

Expenditure

37

…And Estimates are Heading in the Wrong Direction

Following Newell’s recent financial results and 2018 outlook, we estimate that management’s implied

EBITDA guidance for 2018 has fallen 18% below its original EBITDA target

Management Commentary on Jarden Acquisition

“The first $500 million of synergies is expected

to create a company with EBITDA margins of

over 20% and annual EBITDA of over $3

billion…”

Goal #1:

Source: Company filings, CapitalIQ, and Bloomberg.

(1) Wall Street consensus FY2018 EBITDA estimate.

- CEO Michael Polk, Q4 2015 Earnings Call

($ in billions)

Adj. EBITDA & EBITDA Margin Since Merger

20%

17.7%

16.6%

16.9%

(Q4 2015)

(1)

18% below

original

targets

Despite the promise to shareholders of over $3 billion in EBITDA, the Company has thus far failed in reaching

its goal.

“But we believe we can now deliver $1 billion

of synergies, on top of that $300 million in

project renewal savings.”

- CEO Michael Polk, 2017 CAGNY Investor Conference

38

The Company Also Failed to Hit Revenue Growth Targets

Source: Company filings, CapitalIQ, and Bloomberg.

(1) Wall Street consensus estimate of FY2018 “core growth” rate.

Management Commentary on Jarden Acquisition Actual Results – Core Growth Pre & Post-Merger

“Our ambition is to bring together and leverage

the best talent and capabilities from both

companies to drive strong growth…”

Goal #2:

- CEO Michael Polk, Q4 2015 Earnings Call (January 2016)

Revenue growth has massively decelerated and may turn negative in 2018

Despite the promise to shareholders of “strong growth,” core revenue growth has continued to meaningfully

decelerate.

NWL acquisition of JAH

closed on 4/15/2016

(1)

“The key tenet that underpins the strategy is

that this company is going to be growth-led…”

- CEO Michael Polk, Barclays Conference (September 2016)

39

Less than seven months after management doubled its synergy target, analysts were becoming more skeptical.

As a Result, Sell-side Analysts Started Becoming Skeptical

of the Company’s Targets and Guidance

Analysts expressed a lack of confidence in Newell’s execution and strategic vision

Analyst Commentary

Source: Wall Street equity research.

“We had expected Newell’s first $500M of cost synergies,

including ~$300M (or ~$0.50 in EPS) in FY18 to drop to the

bottom line, consistent with Newell’s initial guidance. This

had been a key driver of our positive thesis on Newell

Brands…However, the company’s “soft-guide” for ~$3.30 in

FY18 EPS, based on inferred low double-digit % growth off

of the lowered FY17 base, suggests materially higher

reinvestment levels than we (and Newell) had previously

expected.”- Jefferies, September 2017

“Headwinds Exist…but Bigger Issue Is Loss of

Confidence in Management and the Story — We think

the reason the stock has round-tripped to roughly where

it was when the JAH acquisition was first announced in

December 2015 is a lack of investor confidence that the

integration of these businesses is progressing to plan, and

doubt that the strategic vision of NWL’s CEO will

play out as he hopes.”

- Citi, September 2017

“Following the additional commentary today,

including on slower category growth and risk of

additional investment spending, we are less confident in

the bottom-line delivery at NWL.”

- Oppenheimer, September 2017

“While partially owing to cash restructuring/synergy-

related costs to unlock material savings, Newell’s

heretofore lack of progress in this area…and the

market’s concern regarding the company’s ability to

ultimately deliver on its long-term operating cash

flow targets should continue to weigh on the stock’s

multiple, in our view.”

- Jefferies, September 2017

40

Consensus Estimates Reflected this Skepticism

FY2017 Consensus Adjusted EBITDA Estimates

FY2017 EBITDA was 19% below initial estimates following the closing of the Jarden transaction

“The first $500 million of synergies is expected to create a company with EBITDA margins of over 20% and annual

EBITDA of over $3 billion, giving us the firepower to reduce the leverage ratio to 3 times to 3.5 times within two years to

three years and then, subsequently, to deploy capital to create further value beyond our organic agenda.”

- CEO Michael Polk, Q4 2015 Earnings Call (January 2016)

Management Long-Term EBITDA Target

Actual 2017

Adj. EBITDA

Source: Bloomberg and CapitalIQ.

Note: Estimates not normalized for acquisitions and divestitures.

41

Newell has repeatedly missed consensus expectations on numerous financial metrics over the past several quarters, frustrating shareholders, and failing to gain momentum despite its iconic portfolio of brands.

Source: Bloomberg and Company filings.

(1) Based on FY2017 EPS consensus estimate prior to Newell issuing its FY2017 guidance.

(2) Consensus estimates prior to announcement of preliminary results on January 25, 2018.(3) Stock price reaction on January 25, 2018 (day Newell announced preliminary 2017 results).

Newell Has Consistently Overpromised and Under-delivered…

Earnings Surprise History – Last 3 Quarters

Q2 2017

Earnings

Q3 2017

Earnings

Revised

Guidance

Q4 2017

Earnings(2)

(3)

Newell’s ability to achieve consensus expectations deteriorated significantly throughout 2017

42

(35%)

+4%

+29%

64

% U

nd

erperfo

rma

nce

+7%

+24%

A series of operational missteps has caused Newell’s stock price to underperform the S&P 500 by 64% in less

than 2 years.

…And Shareholders Have Suffered…

Newell has massively underperformed its sector and the overall market

Share Price Performance(1)

(2)

(3)

Source: CapitalIQ.

(1) Total returns include dividends from April 18, 2016 (first day of trading as a combined company following Jarden acquisition) to February 8, 2018 (closing price before Newell confirmed receipt of Starboard’s director nominations).

(2) NWL’s 2017 Proxy Peer Group includes: MMM, AVY, TSE:6448, CLX, CL, DHR, TSX:DII.B, ECL, OM:ELUX B, EMR, EL, ITW, KMB, MAS, MAT, TSE:6503, SHW, ENXTPA:BB, SWK, VFC, and WHR.

(3) Includes CHD, CL, CLX, FBHS, XTRA:HEN3, PBH, PG, LSE:RB., SWK, SPB, TUP, and LSE:ULVR.

43

Since the acquisition of Jarden, approximately $10 billion in shareholder value has been destroyed.

Value at Time of Acquisition:

Value Today:$10 billion in shareholder value has

been destroyed in less than 2 years

Source: Company filings and CapitalIQ (adjusted for dividends).

Note: As of February 8, 2018 (closing price before Newell confirmed receipt of Starboard’s director nominations).

The operational issues at Newell have resulted in a significant destruction of shareholder value

…As Significant Shareholder Value Has Been Destroyed

44

The Communication to Shareholders Has Been Confusing

While management has tried to put a positive spin on the operating performance issues, shareholders

remain extremely concerned

Only exacerbating the poor execution and share price performance, management commentary regarding

Newell’s performance has been confusing for shareholders, leaving more questions than answers.

Quote Author

Source: Company filings.

“So we’re right where we thought we would be,

although our business performance hasn’t been

up to our expectations.”

CEO Michael Polk

(CAGNY Conference – February 2018)

“And we delivered $358 million of synergies and

savings in 2017. Some of that did not flow through

the margin…for a variety of reasons, but quite clear

that that money is in the bank…”

CEO Michael Polk

(CAGNY Conference – February 2018)

“So on balance, I think we’ve had a phenomenal

year. Despite the fact that we're struggling on the

top line and the flow through to earnings

associated with revenue…”

CEO Michael Polk

(Town Hall Presentation– February 2018)

45

In contrast to management’s remarks, adjusted operating margins declined 138bps in FY2017 vs. FY2016

While management continually boasted about its success in achieving synergy targets, the Company’s

operating margins showed a completely different story.

“…the work we’re doing on cost synergies and Project Renewal savings is

having a meaningful positive impact on margins.”

Q1’17 Adj. Operating Margin

“We delivered over $80 million of savings and synergies in the second

quarter, which contributed to strong normalized operating margin growth…”

Q2’17 Adj. Operating Margin

“We have delivered the cost synergies and Renewal savings we

committed to deliver…”

Q3’17 Adj. Operating Margin

“When coupled with procurement benefits, this results in over $350

million [in FY2017] in savings and synergies that flowed to the P&L.”

Q4’17 Adj. Operating Margin

Source: Company filings.

In Our View, Newell Management Needs to Communicate

a Better Plan to Turn the Business Around and Execute

46

III. Underperformance Creates Opportunity

B. Issues Have Been Self-Inflicted

47

We believe that issues specific to Newell are responsible for the Company’s underperformance, and there is a

significant opportunity for improvement

While Newell Has Blamed Poor Performance on the Macro Environment,

We Believe it Is Self-Inflicted and Can Be Improved

Newell management has frequently blamed poor performance on the macro environment, yet peers have fared

far better.

While the retail macro environment has been stressed, Newell’s peers have performed far better.

Newell’s peers have shown consistent organic revenue growth and gross margin expansion.

As a result, Newell’s share price has significantly underperformed its peers over the past year.

We believe that Newell’s issues resulted from poor execution versus industry headwinds.

Many of Newell’s issues are self-inflicted due to communication problems within the Company.

Limited communication between corporate functions (e.g., e-commerce, R&D, brand marketing, etc.) and the

divisions / brands leads to inefficiencies and higher costs.

In the following pages, we discuss several examples of poor communication resulting in strained customer

relationships and negative financial consequences.

We believe that there are numerous opportunities to fix the internal communication issues.

By returning more responsibility and accountability to the divisions / brands, Newell can streamline

communication, accelerate time to market, and improve customer relationships.

Source: Company filings.

48

The Company has been vehement that its operational issues are macro related

Newell claims poor results and guidance reductions are due to the weak retail environment.

Q2 2017 Earnings Call

(August 4, 2017)

“That said, like most others in our industry, we continue to face pressure from retailer inventory

reductions and retailer consolidation in the U.S.” – CEO Michael Polk

Barclays Conference

(September 7, 2017)

“We're making good progress despite a tougher landscape than we originally envisioned. The

landscape issue is really retail environment related and also market growth related. We are existing

now in sluggish markets, a little bit worse than where we were when this whole process started and

where we envisioned the deal…” – CEO Michael Polk

Q3 2017 Earnings Call

(November 2, 2017)

“We had a top customer bankruptcy, forcing a future re-plan on one of our best performing businesses.

We had unrelenting retailer inventory destocking, creating a headwind for revenue as our retail

partners adjust to slowing market growth and changes in shopping patterns. You name it, we experienced

it this quarter.”– CEO Michael Polk

Q4 2017 Earnings Call

(February 16, 2018)

“What's changed is the retail environment, and what's unique about our portfolio and that does not

change with the change in portfolio footprint is the exposure to the stressed segment of the U.S. retail

landscape. And that will continue to be bit of an overhang on the business with probably episodic events

like the ones we're dealing with right now.”– CEO Michael Polk

CAGNY Conference

(February 22, 2018)

“The external environment is tougher than what we anticipated when we did the deal and even at the

beginning of this year, and it's not that the markets are really having troubles or consumer purchasing

behaviors have slowed down in any way. In fact, it's the opposite, the consumer markets are quite robust.

But the retail landscape given our category footprint and our exposure to a group of stressed retailers

is more troubling than what we anticipated.”– CEO Michael Polk

Note: Emphasis added to quotations.

While Newell Has Blamed Poor Performance on the Macro Environment,

We Believe it Is Self-Inflicted and Can Be Improved (cont’d)

49

Facing the Same Retail Environment, Peers Have Fared

Much Better

Despite experiencing similar retail trends, Newell’s peers have outperformed

Stock price performance between Newell and the Company’s peers has differed significantly.

(45%)

(1%)

(5%)

(2%)

12%

8%

Source: CapitalIQ.

Note: Stock price return from May 9, 2017 (day of Newell Brands 2017 Annual Meeting) to February 8, 2018 (last closing price before Newell confirmed receipt of Starboard’s director nominations).

(1) NWL’s 2017 Proxy Peer Group includes: MMM, AVY, TSE:6448, CLX, CL, DHR, TSX:DII.B, ECL, OM:ELUX B, EMR, EL, ITW, KMB, MAS, MAT, TSE:6503, SHW, ENXTPA:BB, SWK, VFC, and WHR.

(1)

50

6%

5%

3%

3% 3% 3%

0%

(2%)

5%

4% 4%5%

7% 7%

8%

5%

4%

1%

2%

3%3%

5%5% 5%

2%

1%

0%

2%2%

8%

6%

2%

5%

5%

4% 4%

5%

-3%

-1%

1%

3%

5%

7%

9%

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17 Q2'17 Q3'17 Q4'17

NWL SWK CHD CL FBHS

While Newell’s Revenue Is Declining, Its Peers Are

Growing Consistently

Peers have been able to weather the “difficult environment” without reporting a quarter of negative

organic revenue growth. Unfortunately, Newell cannot say the same

Source: Company filings, peer filings, and Starboard estimates.

Organic Revenue Growth

While the macro environment may be more difficult, the Company’s peers are demonstrating substantially

better organic growth than Newell.

51

While Newell’s Gross Margins Are Deteriorating, Its Peers’

Are Continuing to Expand

While peers have been able to expand gross margins, Newell Brands’ contracted significantly in 2017

Source: Company filings and peer filings.

Change in Adjusted Gross Margin Year-over-Year

While the macro environment may be more difficult, Newell Brands’ peers are operating more effectively and

performing significantly better.

Q1’17 Q2’17 Q3’17 Q4’17 2017

(415bps) (24bps) (104bps) (412bps) (206bps)

163bps (15bps) 63bps (17bps)44bps

80bps 115bps 1bp (46bps)35bps

72bps 43bps (2bps) (36bps)19bps

103bps (80bps) (13bps) 52bps16bps

52

Many Specific Operational Missteps, Not the Macro

Environment, Have Led to this Underperformance

In the following pages, we detail clear examples of customer frustration, brand

destruction, and other actions that have contributed to the Company’s poor operational

execution.

Based on our research, we believe that the communication at Newell has resulted in a number of issues at the

Company and can be greatly improved.

The Company has drastically missed expectations, and has blamed the macro environment.

Our question: So why have competitors fared so much better than Newell in this environment?

We believe the culprit is not the macro environment.

We believe the Company’s issues are self-inflicted and there is substantial room for improvement.

These issues are fixable, and by implementing the appropriate changes, Newell can substantially

improve its margins

53

The Structure of the Organization Has Resulted in High

Costs, Massive Inefficiencies, and Declining Revenue

Source: Industry research and interviews.

While Newell continues to blame the macro environment, we believe that many of these issues are actually self-

inflicted.

We believe that Newell’s organization is inefficient, and its processes result in high costs, poor employee morale, and

frustrated customers.

Corporate appears to make decisions without fully informing the divisions / brands, which has resulted in

significant customer and brand issues, including gross margin erosion.

The R&D process lacks communication between corporate and the divisions / brands, which results in a low

number of new products reaching the market, high kill rates, duplicative functions, and far higher costs.

In many cases the division / brand leaders are so removed from new product design that the Company

could be working on new products for a year before the division / brand leader is involved. This results in

lengthy time to market and high product kill ratios.

The e-commerce group is too separated from the divisions and appears to determine online pricing without

communicating with the divisions, resulting in inconsistent pricing that, in some cases, violates the Company’s

own minimum pricing policy or results in different pricing to the same customers between online and brick-and-

mortar (i.e., Walmart vs Walmart.com).

These issues frustrate customers and lead to Newell giving large promotional concessions, which

drastically lowers margins.

Newell’s organizational structure appears to be a significant contributor to the issues facing the Company

54

Newell’s Siloed Organizational Structure Causes Massive

Communication Issues, Resulting in High Costs

CORPORATE

Division CEO / Head of Brand

CFO │ COO │ Supply Chain │ HR │

Regional Presidents

Reports to e-commerce head

Determines online pricing regardless of

whether retailer has brick-and-mortar

store

Division / Brand Level E-commerce

Research and

Development

Brand Marketing

Limited communication among the different functional groups not only results in duplicative costs, but also

frustrates customers and causes poor employee morale.

Reports to Richard Davies

New product design operated out of

Kalamazoo, MI

Works on new product development

Reports to Richard Davies

National marketing and website design

New product development and pricing

Prices online products

without the knowledge of

division / brand, sometimes

violating Company’s own

minimum pricing policy for

some retailers, and in other

cases, results in presenting

different prices to the same

retailer (i.e., Walmart vs

Walmart.com)

Operates Design center in a

silo away from Division;

months or years of research

with high kill rate because

Division leaders have little

to no input

Limited communication

with Division Trade

Marketing and Sales (who

have customer relationships)

which results in bringing

forward products that

retailers don’t want

Given revenue and

operating plan from

corporate with

limited control over

actual P&L levers

Source: Industry research and interviews.

Lack of communication

Field Sales

Trade Marketing

Engineering (Plant

and Supply Chain)

Can also reside in Corporate

depending on the division /

brand

If no Field Sales in Division,

would have to speak with

channel sales in corporate to

know product sales trends;

Very limited communication

with Brand Marketing

Very limited communication

with R&D, resulting in new

products having to be

redesigned along with

sourcing issues

Responsible for

ultimately selling the

product

Responsible for in-store

promotions and in-store

support

Responsible for

manufacturing

engineering products

55

When Corporate Fails to Communicate with the Brands: Textbook

Way to Harm a Brand – The Yankee Candle Story

Source: Jarden filings.

Yankee Candle is one of the most recognized brands in the candle industry with ~600 retail store locations.

Yankee Candle has been a prominent, high quality candle brand for

many years.

In an effort to expand its reach, Yankee Candle (before Newell

acquired Jarden), created a value-priced candle line called

“American Home by Yankee Candle” so major retailers could carry

product without diluting the flagship Yankee Candle brand.

From Jarden’s 2015 CAGNY presentation – focused

strategy on breaking into mass retailing without

harming flagship Yankee Candle brand

56

When Corporate Fails to Communicate with the Brands: Textbook

Way to Harm a Brand – The Yankee Candle Story (cont’d)

The first way to kill the value of a brand is to put it right next to the Walmart knockoff that is a quarter of the price

As a result of this action, Walmart a) cut the price of the product, and b) placed it right next to the lowest-

end candles on the market.

Why would you put a high quality

brand next to a cheap knockoff?

In 2017, in an effort to generate additional near-term sales, Newell did away with the American Home brand

and began rolling out its higher-end, flagship Yankee Candle brand into large retailers.

Yankee Candle

$19.87

Low Quality Candles

priced at ~$3 - $5

Now the high-end Yankee Candle brand is lost in a sea of low-end knockoff candles in Walmart. How does the

opinion of its core customer base stay the same when Yankee Candle is now next to the $4 candles at Walmart?

Source: Industry research and interviews.

57

In an Effort to Grow Sales, Newell Allowed Walmart to

Discount Yankee Candle by Almost $10 per Candle

Source: Industry research and interviews, www.yankeecandle.com, and www.walmart.com.

Why would Newell push the Yankee Candle brand into Walmart at a 30% discount to the price at its own stores?

Walmart - $19.87Yankee Candle Store - $27.99

Not considering the long-term effects of a decision like this can be dangerous

58

So What Do You Think Happened Next?

We believe that this had a negative impact on gross margins

Source: www.bedbathandbeyond.com, industry research and interviews.

Clearly, other large retailers would get upset if they realized Walmart was selling the same candle at a large

price discount. So, Bed Bath & Beyond demanded a lower wholesale price from Newell, so it could offer a

competitive retail price.

Bed Bath & Beyond today - $21.99

A more than 20% reduction at a major retailer

not only severely impacts profitability, but also

draws customers away from Company owned

stores to capitalize on better prices!

59

Newell’s actions resulted in a number of large retailers significantly reducing their prices of Yankee Candle

products. However, the same product is still sold in its own Yankee Candle stores for $27.99!

Many Major Retailers Ended Up Cutting Prices

This decision resulted in retail partners cutting their prices by 20% - 30%; clearly a bad outcome for the business

Source: www.yankeecandle.com, www.walmart.com, www.bedbathandbeyond.com, www.target.com, www.amazon.com, industry research and interviews.

Walmart - $19.87 Bed Bath & Beyond - $21.99

Amazon - $21.99

Target - $19.99

YankeeCandle.com - $27.99

60

Especially When Yankee Candle Has Close to 600 Stores

Selling at Full Price!

Why was this a good idea?

Source: www.yankeecandle.com, Mapline, industry research and interviews.

Newell is undercutting its own stores…and it operates a lot of stores.

Map of Yankee Candle Locations

61

The Appliance Business Opportunity

We believe that an issue like this is clearly self-inflicted, not macro related

Newell has pointed to “structural issues” and “destocking” to account for the struggling appliance business, but

we believe that the real issue was poor decision making.

We don’t believe this is a “destocking” or a “structural” issue. We believe the issue stems from the Company’s decision to fire

almost the entire sales force right before the selling season.

During the integration of legacy Newell and Jarden, the management team “integrated” sales offices in an attempt to shift

towards a more centralized strategy – resulting in the termination of more than 150 former Jarden sales executives.

However, two problems ensued in this relationship driven industry – (1) the recently terminated sales executives had the

relationships with the buyers, and (2) it was just prior to selling season!

“…Appliances in particular, that has some structural issues within its portfolio that need to be addressed through the work

we're doing on design, the work we're doing on innovation, the work we're doing in the brand arena.”

- CEO Michael Polk, 2018 CAGNY Investor Conference

NWL fires legacy

Jarden appliance

salesforce –

integrates

appliances with

legacy NWL

salespeople

Sell-in for

upcoming 3rd and

4th quarter

appliance season

Newell reverses

course and tries to

re-hire legacy

salesforce

NWL misses

appliance

expectations in key

sales season

Q1 2017 Q3 2017 Q4 2017Q2 2017

Source: Company filings, industry research and interviews.

62

The R&D Process Appears to Be a Key Reason for Inflated

Costs and Slowing Revenue Growth

Source: Industry research and interviews.

The process is led by corporate, not by the division / brands.

Corporate relies on test scores in determining new product design rather than conversations with retailers, pricing,

competition, or manufacturability.

Division leaders are not brought into the new product design process for sometimes up to a year after corporate

determines new concept, despite the fact that they are the ones who speak with the retailers and are responsible for

manufacturing.

This results in high kill rates when corporate finally realizes that competition exists, pricing is too high, or a product

cannot actually be manufactured.

In some cases, the Company seems to wait until the product is already manufactured to bring it in front of retailers

and then realizes that they don’t want it, thereby killing the product after multiple years of development.

The process is too lengthy and Newell misses opportunities to market.

Speed to market is one of the most important factors in new product success and revenue growth, yet Newell’s

complex structure, which cuts off division leaders, can lead to multiple years from concept to new product

production.

Newell appears to measure success based on quantity of concepts (approximately 1,300 last year alone!) rather than actual

new products to market or the revenue and return they generate.

The brand leaders live and breathe their brands and their respective categories. These are the people

that need to be empowered to drive innovation and revenue growth

1

2

3

63Source: Company filings, industry research and interviews.

In our research, we have focused extensively on Newell’s innovation and R&D process because we believe

there are massive inefficiencies.

Step 1: New Product Design (Led by Corporate R&D and Corporate Brand Marketing)

Over the next few pages, we detail what we believe to be the current R&D process at Newell. There are many issues with

the process that result in wasted time, higher than expected costs, frustrated retailers, and new product delays.

The corporate R&D design team in Kalamazoo, MI, along with corporate brand marketing, will generate new ideas for

products that theoretically solve a problem in the marketplace.

They are not experts in individual brands.

The division / brand leaders, who have the relationships with the retailers and are the experts in each brand, are generally

not involved and are unaware of what this corporate team is working on.

The design team, which operates in a silo in Kalamazoo, will draw up these new concepts.

Richard Davies, who operates out of the UK, oversees this process.

Rather than relying on the divisions / brands who are close to the retail customer and

know the competitive landscape, new product development is instead done in a

completely different location and generally without the knowledge of those who know

the business the best

The R&D Process Appears to Be a Key Reason for Inflated

Costs and Slowing Revenue Growth (cont’d)

64

Corporate makes decisions based on theoretical scores without the division / brand leaders having

input, whether the retailer wants the product, or whether it is even possible to manufacture

Step 2: Consumer Research

Once decided on a sketch and concept at

Kalamazoo, the idea will go through Newell’s

corporate consumer research team.

Again, the consumer research team is not brand

specific, so the division / brand still generally

has no idea about these new products.

The consumer research group will score each

product with a consumer panel, but they will

not typically discuss price, specification or any

details, just high level thoughts.

Corporate will then make its decisions based on

these theoretical index scores without the

proper input from division / brand leaders.

Steps 1 and 2 can take up to 6 months and

the divisions / brands are not involved.

Products moving forward are based on consumer index scores, but do

not properly take into account price, competition, retail customer

desires or even whether it is possible to manufacture the product!

They “trust the index number” and “don’t

take into account what matters like

competition, price, or even the retailer”

-Former Senior Executive

Source: Company filings, industry research and interviews.

The R&D Process Appears to Be a Key Reason for Inflated

Costs and Slowing Revenue Growth (cont’d)

65

A year into the process, the division / brand specific executives still have minimal involvement

Step 3: Decision to Move Forward with R&D

After the consumer research stage, the division / brand leader finally gets notified – but not in a meaningful way.

The division / brand leader is invited to listen to a call, which typically lasts 30-45 minutes, where up to 70 new

concepts will be discussed by corporate.

Richard Davies and Bill Burke (COO) listen to each idea from corporate in rapid-fire and make approvals.

Since they are not experts in each industry, they rely primarily on index scores.

Division / brand leaders do not have the right to eliminate an idea, even if it already exists or they know the

retailer would not want it.

New product concepts are then approved (assuming they have a high index score) to go back to corporate engineering.

At this point, which can easily be 6-12 months, there is generally still no real view on price, cost, and feasibility

(since division operations are not on the call), and they typically have not shared the products or ideas with the

retailer.

The “quality of thinking was quite low”

-Former Senior Executive

“There was no debate, not enough time”

-Former Senior Executive

When discussing the rapid fire process to make approvals, one former senior executive stated:

Source: Company filings, industry research and interviews.

The R&D Process Appears to Be a Key Reason for Inflated

Costs and Slowing Revenue Growth (cont’d)

66

Typically a year or more into the product development, there is still no answer on actual cost, limited

interaction with the divisions, limited/no conversations with the retailer, and corporate R&D

engineering is still trying to determine whether the product can actually be manufactured!

Step 4: Corporate R&D Engineering

Now the concept goes back to the R&D engineering team at corporate, led again by Richard Davies.

Once again, there is no knowledge or input from the division / brand leaders.

This group at corporate develops a theoretical cost and materials model, and tries to determine whether the product can

actually be manufactured.

Importantly, since the division supply chain and operations is typically not involved, actual pricing may differ

materially from theoretical pricing.

If R&D Engineering determines

the product cannot be

manufactured, the idea is killed

(yet a year may have been wasted)

Division / brand supply chain and

operations is not engaged, so

“theoretical” cost may differ

materially from actual cost

Sometimes the R&D team will

learn that someone else has

already patented the device and

cannot design around it, therefore

being forced to kill the idea

Source: Company filings, industry research and interviews.

The R&D Process Appears to Be a Key Reason for Inflated

Costs and Slowing Revenue Growth (cont’d)

67

Step 5: Decision to move forward with commercial engineering

Once again, the division / brand leader is invited to listen to a call between corporate R&D, Richard Davies, and Bill

Burke to determine whether to pursue commercial engineering.

Corporate R&D explains whether the product can be theoretically manufactured and provides theoretical cost estimates.

Importantly, the supply chain and operations within the division has typically still not adequately engaged on the

product to determine whether it is even possible to manufacture and the actual cost estimate of manufacturing.

Richard Davies and Bill Burke then vote on proceeding to commercial engineering and trade marketing.

The division / brand leader can provide thoughts and input, but still has no ability to kill the product.

The division / brand leader still has no ability to kill the product

We may now be well over a year into the process and the division / brand leader, division operations,

and division trade marketing have had little involvement, resulting in retailers most likely not having

been told about the product

Source: Company filings, industry research and interviews.