Embed Size (px)

Citation preview

Powerloom Clusters of India

West specially the Britain and later US had enjoyed supremacy in world textile and

clothing trade for over two centuries but now the shift is taking place from the

West (US and EU countries) to the East particularly China, India and Pakistan. This

change has been necessitated in view of the implementation of free-trade policies

in the world under WTO from 1st January, 2005. In the last eight years since

2000, cotton consumption in US, EU and Japan has been decreasing fast while it

has been increasing very fast in China and South Asian countries like India, Pakistan

and Bangladesh.

Presently, China, India, Pakistan and Bangladesh share about 50 percent of US

imports of cloth and textiles. China has lion share of over 35 percent while India

and Pakistan share is small but better than other countries. India and Pakistan have

great potential as both produce large cotton crops and can exploit their resources

to increase their share in textile exports to US. In 2007, Pakistan was the second

largest exporter of clothing and textiles to US.

Small countries like Vietnam, Thailand and Sri Lanka are increasing their exports to

US. This is the trend of increase of total US imports from south Asian countries

which clearly shows shift of finished goods from the East to the West. Exports of

textile and clothing from China, India, Pakistan and other small Asian countries is

increasing substantially. Pakistan's exports of textile goods and cloth to EU was US

$3.965 billions in 2004-05, US $4.108 billions in 2005-06, US $4.443 billions in

2006-07. China's economy is second to US in the world and in next 20-25 years,

China may occupy top position surpassing US. The present economic and financial

conditions in US indicate that its economy may face bankruptcy if the situation

deteriorated further. Among EU countries, Germany, Italy and UK are economically

and financially stronger. In next quarter century, China would lead the world in

trade and finance with India, Pakistan and Bangladesh as its strong allies.

Different types and varieties of fabrics are used world wide in different

applications such as woven fabrics, knitted fabrics, non-woven fabrics and technical

textile products. Recent studies have highlighted that fabric weaving alone expends

around 28 million tones of fibre every year. It is predicted that global production

will grow by 25% between 2002 and 2012; to reach more than 35 million tones and

Asia is one of the key regions in future growth.

The top ten major importers of powerloom fabrics and made-ups of 100% cotton

are USA, UK, Germany, Italy, Bangladesh, France, Greece, UAE, Sri Lanka, and

Spain.

History of weaving looms can be traced back to 17th century. The first power loom

was invented by Edmund Cartwright in 1785.

The East India Company established its office in Calcutta in 1601 and started

trading in local as well as in exports specially to Great Britain. When the British

established their companies, India had developed its textiles sectors and was also

exporting cloth to China, Afthanistan, Central Asian states. Trade of cloth started

between Britain and India and it continued to grow till middle of 18th. Century,

when the Britain spinning and ginning machines were invented which boosted textile

industry. The British discouraged promotion of cloth in India and Indian raw cotton

was exported to UK for processing. Only in 1854, the first spinning mill of India was

established in Bombay by a Parsi entrepreneur and the first jute mill was

established in Calcutta by one English in 1885 and thereafter series of textile mills

were established in Bolmbay and in other parts of India.

Originally Power looms were with shuttle, and they were very slow. But as the

industrial demands for faster production accelerate, faster looms without shuttle

came in use in early part of 20th century. As developments and innovations take

place, various types of looms were developed for faster production. Today, Air-jet,

Water-jet, Rapier and other computer operated looms are used to maximize

production of special materials.

The decentralized powerloom sector is the lifeline of Indian Textile Industry. India

is having approximately 19.42 lakhs of powerlooms weaving almost 19,000 million

meters of fabric, and provides employment to more than 7 million workers over

430,000 units. Although the growth of power loom industry was slow initially; it has

started gearing up now. Number of shuttle less looms has augmented to almost

50,000 and from this about 35,000 looms are working in the decentralized sector.

The sector accounts for 63% of the total cloth production in the country.

The fibre and yarn-specific configuration of the textile industry includes almost all

types of textile fibres, natural fibres such as cotton, jute, silk and wool, synthetic,

man-made fibres such as polyester, viscose, nylon, acrylic and polypropylene.

Indian textiles, handlooms and handicrafts are exported to more than 100

countries, with the US being the largest buyer. Readymade garments (RMG) are the

largest export segment, accounting for almost 41 per cent of total textile exports.

RMG exports from India were worth US$ 9.06 billion in 2007-08. RMG exports

from India were worth US$ 8.18 billion during April-February 2008-09, as

compared to US$ 6.89 billion in the corresponding period of 2007-08

As per the latest figures available with the Ministry of Textiles, India exported

textiles worth US$ 17.62 billion during April-February 2008-09, a 7.08 per cent

increase over the corresponding period last year.

Most of the Power loom units are concentrated in semi urban, or rural area. Among

all, Maharashtra has highest number of powerlooms amounting to approximately 8

lakhs of powerloom, Tamilnadu is second with 5 lakh units, and Gujarat ranks third

with 4to4.5 lakh worth of power looms.

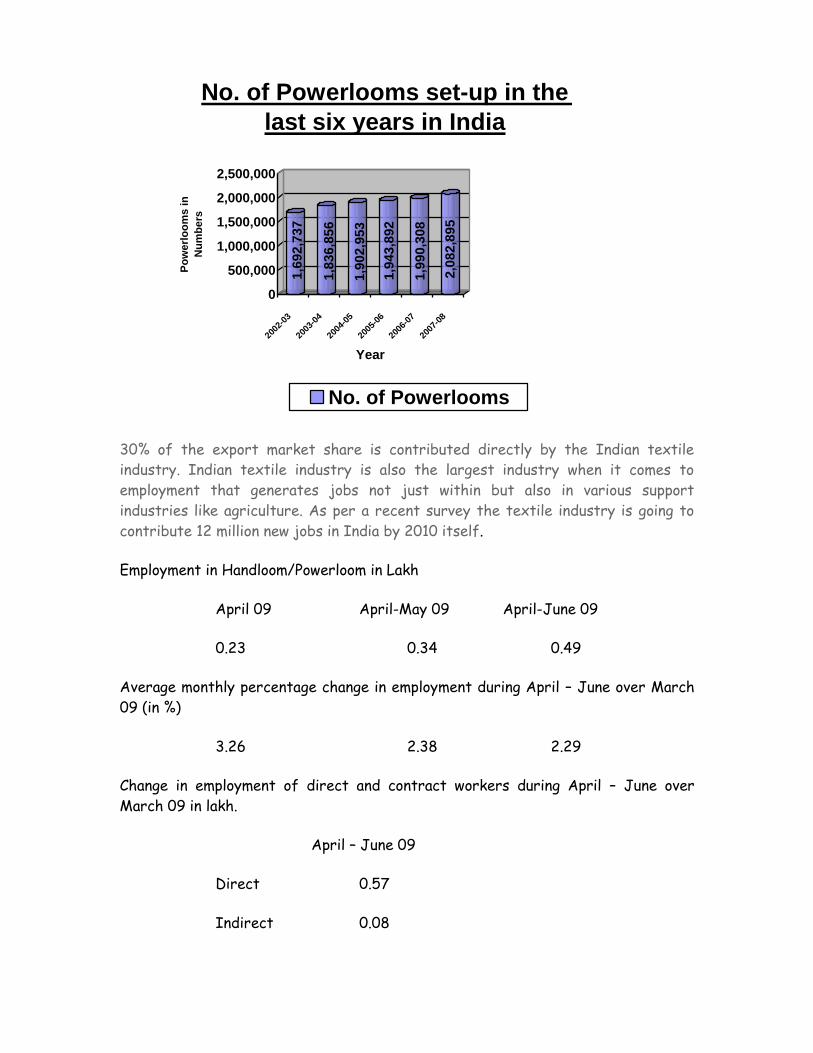

1,6

92,7

37

1,8

36,8

56

1,9

02,9

53

1,9

43,8

92

1,9

90,3

08

2,0

82,8

95

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000P

ow

erl

oo

ms i

n

Nu

mb

ers

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

Year

No. of Powerlooms set-up in the

last six years in India

No. of Powerlooms

30% of the export market share is contributed directly by the Indian textile

industry. Indian textile industry is also the largest industry when it comes to

employment that generates jobs not just within but also in various support

industries like agriculture. As per a recent survey the textile industry is going to

contribute 12 million new jobs in India by 2010 itself.

Employment in Handloom/Powerloom in Lakh

April 09 April-May 09 April-June 09

0.23 0.34 0.49

Average monthly percentage change in employment during April – June over March

09 (in %)

3.26 2.38 2.29

Change in employment of direct and contract workers during April – June over

March 09 in lakh.

April – June 09

Direct 0.57

Indirect 0.08

Change in employment of exporting units over March 09 in lakh.

April 09 April – May 09 April – June 09

0.25 0.35 0.57

In handloom/powerloom sectors export units 0.57 lakh jobs have been added during

the period April – June over March 09.

(Source http://labourbureau.nic.in)

Table 1: Powerloom Clusters in India

S.No. State Name of the Cluster & Category

No. of units

Employment Person/family*

Turnover Cr./Annum

Exports Cr./Annum

Andhra

Pradesh Nagari, Horizontal 24000 500

Guntur

Warangal, Horizontal <1000 <1000 0-10

Sirsilla 20000 15000 * 50-60

Gujarat Kalol, Horizontal 100-500

1000-10000 0-10 M

Surat 1000-10000

>10000 100-1000 M

Gandhinagar

Chhatral

Haryana Bhiwani <100 1000-10000 100-1000 L

Panipat 5702 34892 405.7

Karnataka Belgaum 10-100 L

Bangalore, Horizontal 100-1000

Gadag Betgeri, Horizontal

100-500

<1000

Kerala Ernakulam M

Mallappuram, Horizontal

M

Palakkad M

Faizlure M

Madhya Pradesh

Burhanpur, Horizontal 9890

Jabalpur, Horizontal

Ujjain

Maharashtra Ichalkaranji, Horizontal

244

Malegaon, Horizontal 7500 100000 4900

Madhavnagar, Horizontal

Orissa Dhenkanal

Ganjam, Horizontal 1000-10000 0-10 M

Balasore, Horizontal 1000-10000 0-10 M

Punjab Amritsar , Horizontal 200 1500 400 50-60

Rajasthan Kishangarh, 400 5555

Horizontal

Beawar 60 950 24

Jaipur 25 300-400 50

Bhilwara, Horizontal 159 45-50

Tamil Nadu Surampatti, Erode 160 8000

Karur, Horizontal

Bhavani 160

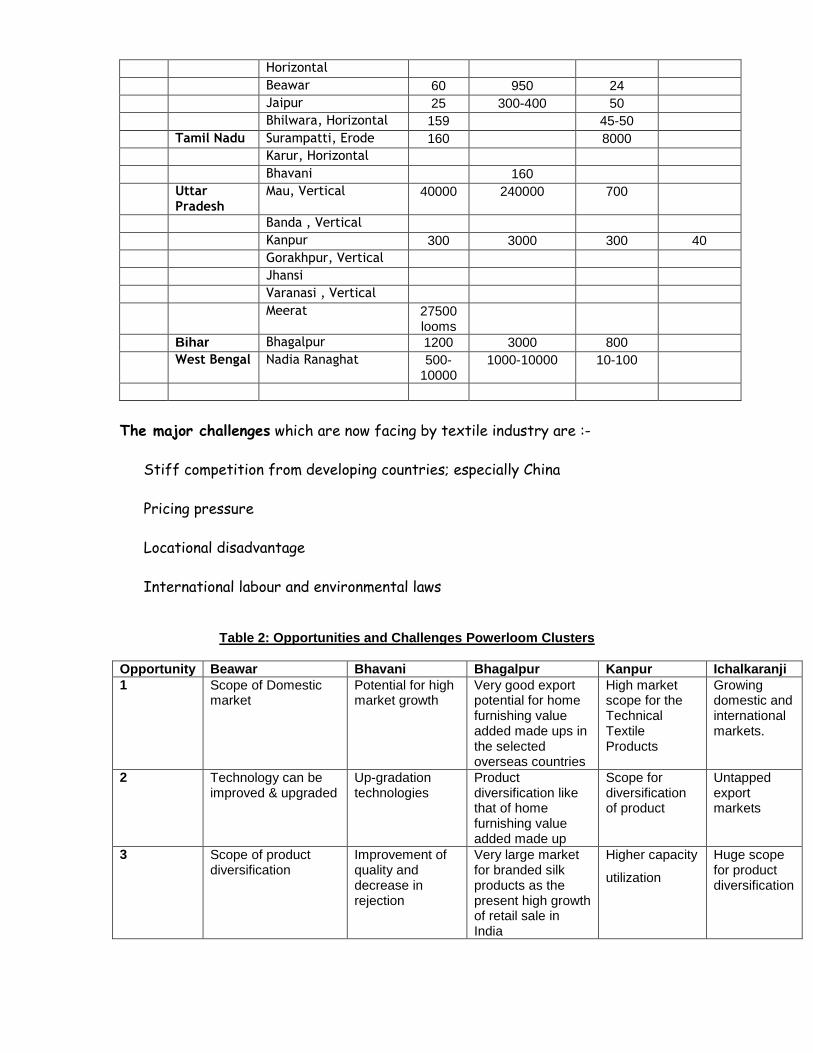

Uttar Pradesh

Mau, Vertical 40000 240000 700

Banda , Vertical

Kanpur 300 3000 300 40

Gorakhpur, Vertical

Jhansi

Varanasi , Vertical

Meerat 27500 looms

Bihar Bhagalpur 1200 3000 800

West Bengal Nadia Ranaghat 500-10000

1000-10000 10-100

The major challenges which are now facing by textile industry are :-

Stiff competition from developing countries; especially China

Pricing pressure

Locational disadvantage

International labour and environmental laws

Table 2: Opportunities and Challenges Powerloom Clusters

Opportunity Beawar Bhavani Bhagalpur Kanpur Ichalkaranji

1 Scope of Domestic market

Potential for high market growth

Very good export potential for home furnishing value added made ups in the selected overseas countries

High market scope for the Technical Textile Products

Growing domestic and international markets.

2 Technology can be improved & upgraded

Up-gradation technologies

Product diversification like that of home furnishing value added made up

Scope for diversification of product

Untapped export markets

3 Scope of product diversification

Improvement of quality and decrease in rejection

Very large market for branded silk products as the present high growth of retail sale in India

Higher capacity

utilization

Huge scope for product diversification

4 Scope of domestic market

Product and quality diversification

High labour cost in developed countries

Schemes / benefits of Government for Modernisation / Upgradation

Scope for sub-contract work from large units

5 Demand for export market

Technology can be improved or upgraded by implementing Govt schmes

To supply fabric to growing Readymade Garment Industry in Kanpur by diversification of products to Shirting / suiting

Network catering to bulk orders by distributing the work among the cluster's units

6 Scope of product diversification

Better power supply & facilities in Industrial Areas, Textile park

Abundant scope to supply to multinationals shops set up in India

7 Using better raw material, trained labour can produce better quality

8 Brand building of Bhagalpur silk value added product in the domestic as well international market

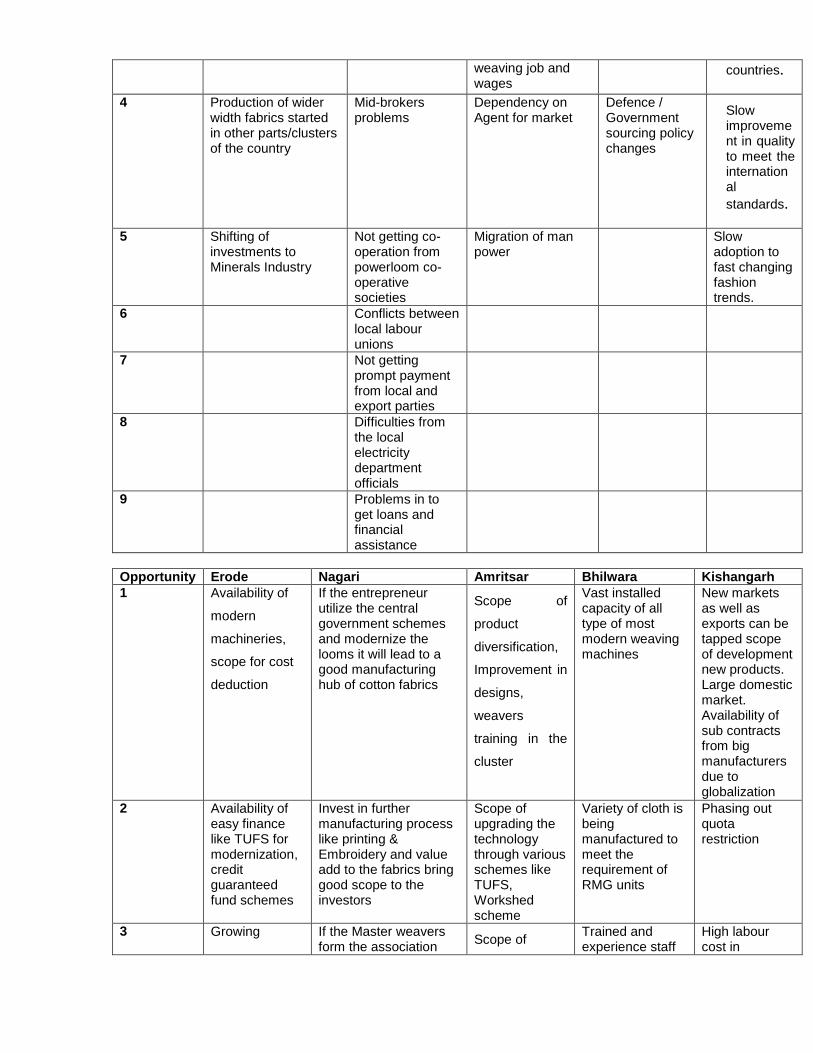

Challenges 1

Globalization Govt. policies methods and regulations

Threat from silk products from china and Mulberry silk products from Karnataka and other southern states

Change in

market trend

Entry of

multinational

in domestic

markets

2 Import of cheaper Chinese fabrics

Power supply problems

Absence of protection under WTO

Increase in cost

of production

Stiff competition from other countries like China, Indonesia, Thailand, Turkey, Bangladesh and Pakistan

3 Unhealthy price competition

Not getting proper price for good quality products

Weavers are day by day taking up other profession due to inadequate

Increasing market competition

Non-tariff barriers from developed

weaving job and wages

countries.

4 Production of wider width fabrics started in other parts/clusters of the country

Mid-brokers problems

Dependency on Agent for market

Defence / Government sourcing policy changes

Slow improvement in quality to meet the international

standards.

5 Shifting of investments to Minerals Industry

Not getting co-operation from powerloom co-operative societies

Migration of man power

Slow adoption to fast changing fashion trends.

6 Conflicts between local labour unions

7 Not getting prompt payment from local and export parties

8 Difficulties from the local electricity department officials

9 Problems in to get loans and financial assistance

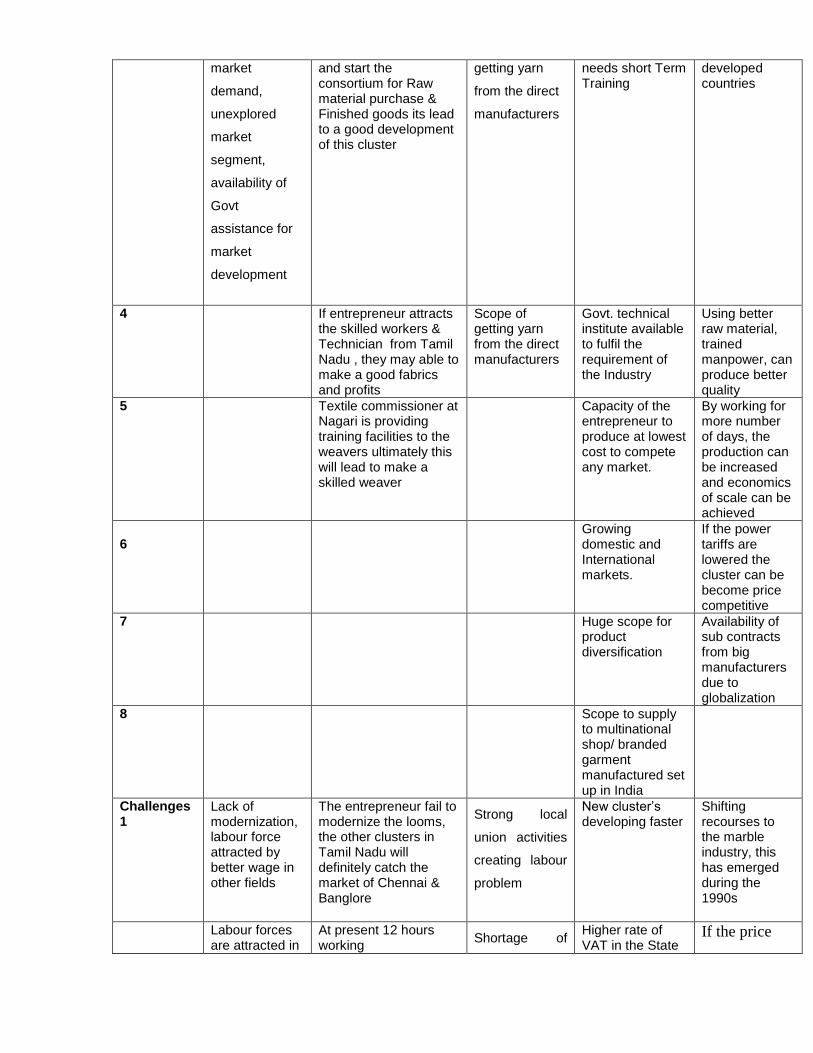

Opportunity Erode Nagari Amritsar Bhilwara Kishangarh

1 Availability of

modern

machineries,

scope for cost

deduction

If the entrepreneur utilize the central government schemes and modernize the looms it will lead to a good manufacturing hub of cotton fabrics

Scope of

product

diversification,

Improvement in

designs,

weavers

training in the

cluster

Vast installed capacity of all type of most modern weaving machines

New markets as well as exports can be tapped scope of development new products. Large domestic market. Availability of sub contracts from big manufacturers due to globalization

2 Availability of easy finance like TUFS for modernization, credit guaranteed fund schemes

Invest in further manufacturing process like printing & Embroidery and value add to the fabrics bring good scope to the investors

Scope of upgrading the technology through various schemes like TUFS, Workshed scheme

Variety of cloth is being manufactured to meet the requirement of RMG units

Phasing out quota restriction

3 Growing If the Master weavers form the association

Scope of Trained and experience staff

High labour cost in

market

demand,

unexplored

market

segment,

availability of

Govt

assistance for

market

development

and start the consortium for Raw material purchase & Finished goods its lead to a good development of this cluster

getting yarn

from the direct

manufacturers

needs short Term Training

developed countries

4 If entrepreneur attracts the skilled workers & Technician from Tamil Nadu , they may able to make a good fabrics and profits

Scope of getting yarn from the direct manufacturers

Govt. technical institute available to fulfil the requirement of the Industry

Using better raw material, trained manpower, can produce better quality

5 Textile commissioner at Nagari is providing training facilities to the weavers ultimately this will lead to make a skilled weaver

Capacity of the entrepreneur to produce at lowest cost to compete any market.

By working for more number of days, the production can be increased and economics of scale can be achieved

6

Growing domestic and International markets.

If the power tariffs are lowered the cluster can be become price competitive

7 Huge scope for product diversification

Availability of sub contracts from big manufacturers due to globalization

8 Scope to supply to multinational shop/ branded garment manufactured set up in India

Challenges 1

Lack of modernization, labour force attracted by better wage in other fields

The entrepreneur fail to modernize the looms, the other clusters in Tamil Nadu will definitely catch the market of Chennai & Banglore

Strong local

union activities

creating labour

problem

New cluster’s developing faster

Shifting recourses to the marble industry, this has emerged during the 1990s

Labour forces are attracted in

At present 12 hours working

Shortage of Higher rate of VAT in the State

If the price

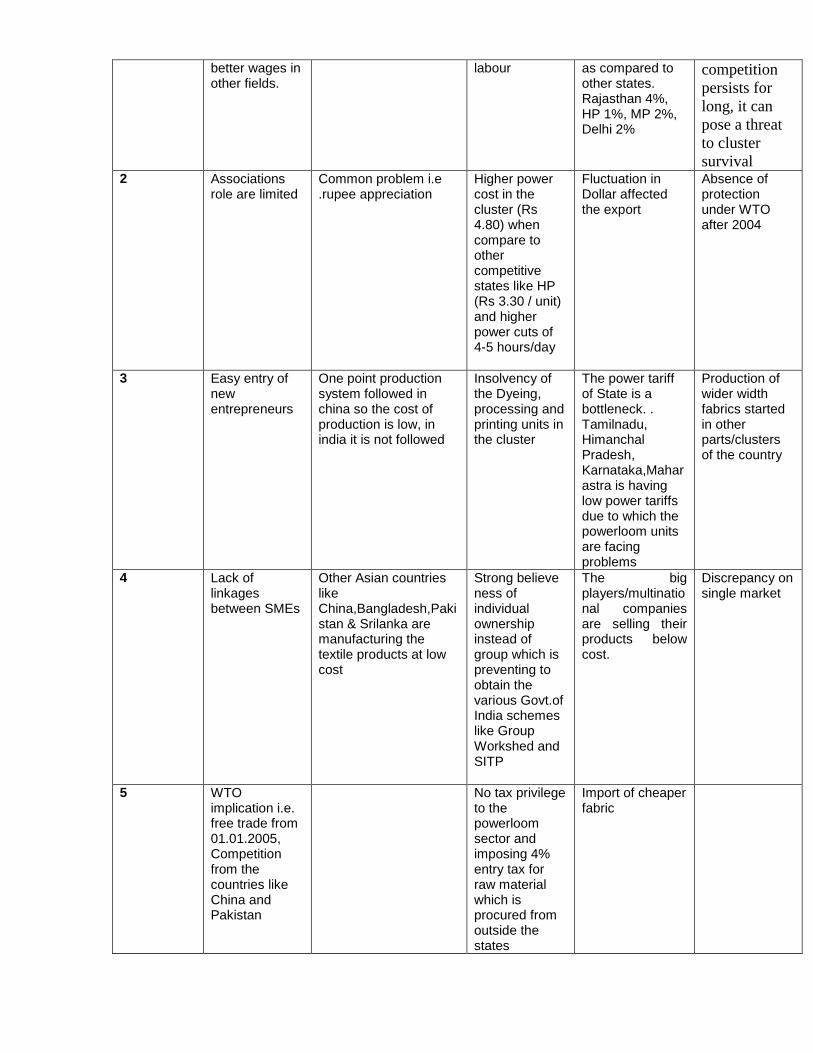

better wages in other fields.

labour

as compared to other states. Rajasthan 4%, HP 1%, MP 2%, Delhi 2%

competition

persists for

long, it can

pose a threat

to cluster

survival 2 Associations

role are limited Common problem i.e .rupee appreciation

Higher power cost in the cluster (Rs 4.80) when compare to other competitive states like HP (Rs 3.30 / unit) and higher power cuts of 4-5 hours/day

Fluctuation in Dollar affected the export

Absence of protection under WTO after 2004

3 Easy entry of new entrepreneurs

One point production system followed in china so the cost of production is low, in india it is not followed

Insolvency of the Dyeing, processing and printing units in the cluster

The power tariff of State is a bottleneck. . Tamilnadu, Himanchal Pradesh, Karnataka,Maharastra is having low power tariffs due to which the powerloom units are facing problems

Production of wider width fabrics started in other parts/clusters of the country

4 Lack of linkages between SMEs

Other Asian countries like China,Bangladesh,Pakistan & Srilanka are manufacturing the textile products at low cost

Strong believe ness of individual ownership instead of group which is preventing to obtain the various Govt.of India schemes like Group Workshed and SITP

The big players/multinational companies are selling their products below cost.

Discrepancy on single market

5 WTO implication i.e. free trade from 01.01.2005, Competition from the countries like China and Pakistan

No tax privilege to the powerloom sector and imposing 4% entry tax for raw material which is procured from outside the states

Import of cheaper fabric

6 Shift towards buyers market from seller market

Seasonal fluctuations (-1’ at winter & 48’ at summer)

7 Competition with the other clusters like ludhiana, panipat and bhilwara

8 Lower technology up-gradation due to lower subsidy sealing limit (8 lakhs) of 2nd hand imported looms under the 20% MMS of Govt. of India which is normally preferred by the entrepreneurs for jacquard designs

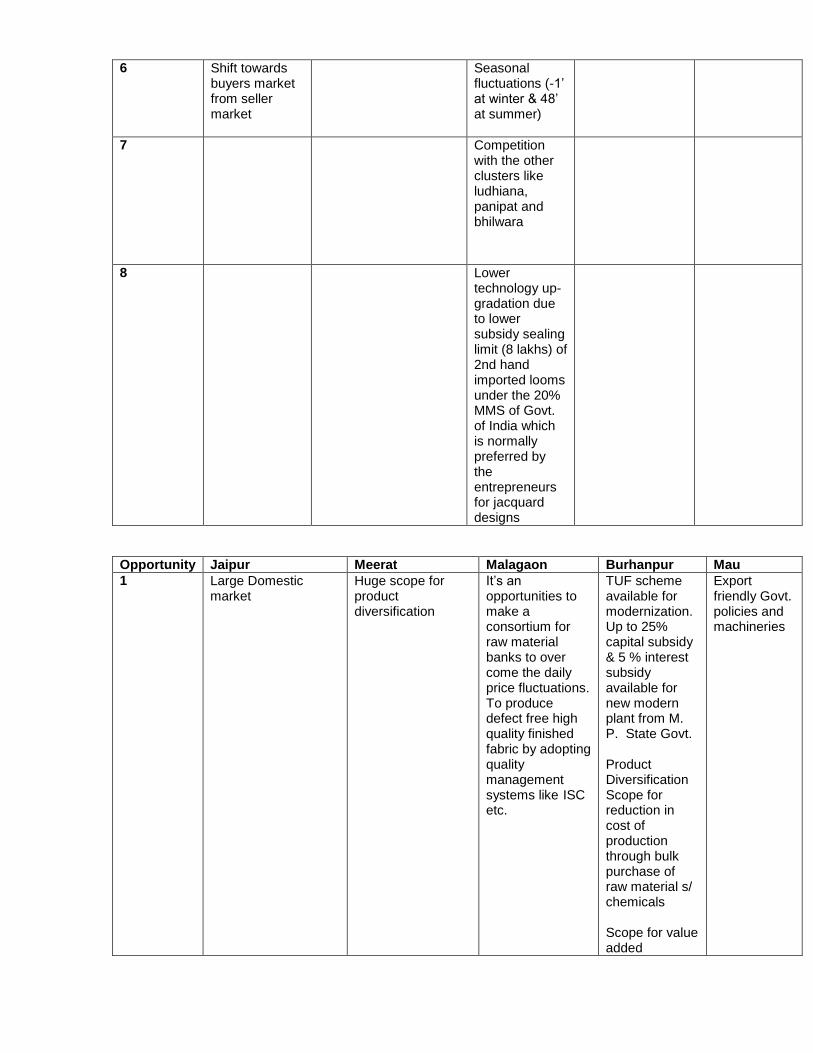

Opportunity Jaipur Meerat Malagaon Burhanpur Mau

1 Large Domestic market

Huge scope for product diversification

It’s an opportunities to make a consortium for raw material banks to over come the daily price fluctuations. To produce defect free high quality finished fabric by adopting quality management systems like ISC etc.

TUF scheme available for modernization. Up to 25% capital subsidy & 5 % interest subsidy available for new modern plant from M. P. State Govt. Product Diversification Scope for reduction in cost of production through bulk purchase of raw material s/ chemicals Scope for value added

Export friendly Govt. policies and machineries

production

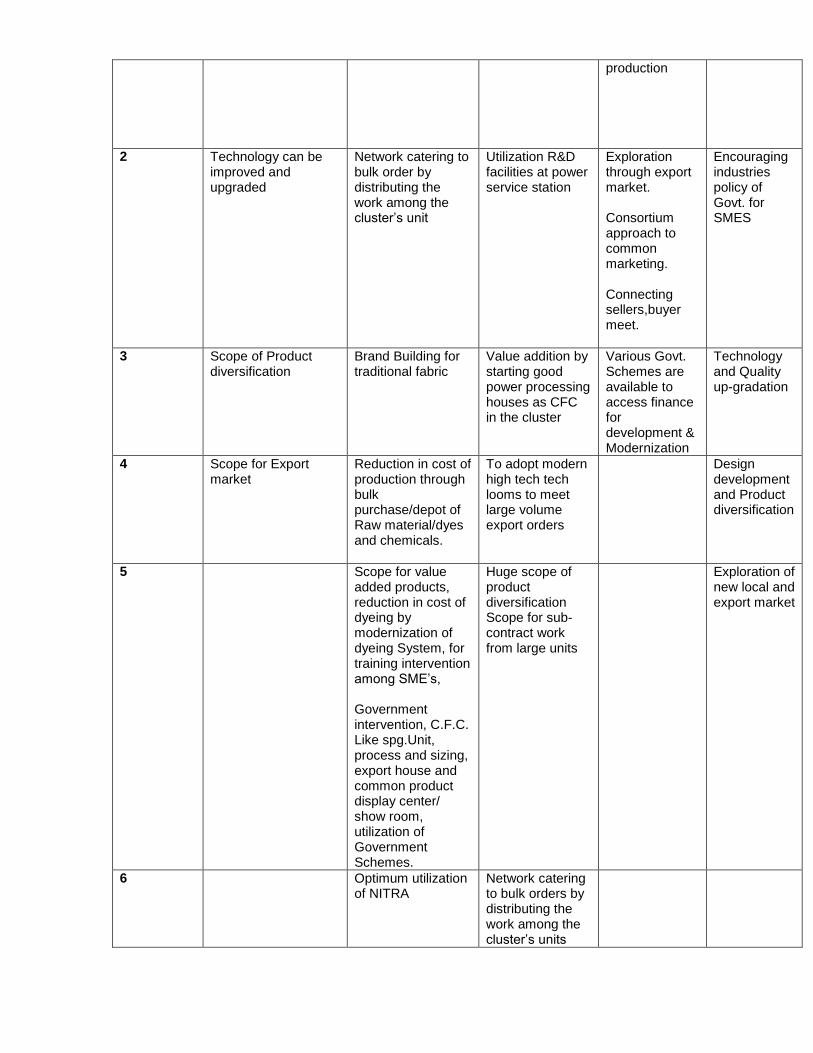

2 Technology can be improved and upgraded

Network catering to bulk order by distributing the work among the cluster’s unit

Utilization R&D facilities at power service station

Exploration through export market. Consortium approach to common marketing. Connecting sellers,buyer meet.

Encouraging industries policy of Govt. for SMES

3 Scope of Product diversification

Brand Building for traditional fabric

Value addition by starting good power processing houses as CFC in the cluster

Various Govt. Schemes are available to access finance for development & Modernization

Technology and Quality up-gradation

4 Scope for Export market

Reduction in cost of production through bulk purchase/depot of Raw material/dyes and chemicals.

To adopt modern high tech tech looms to meet large volume export orders

Design development and Product diversification

5 Scope for value added products, reduction in cost of dyeing by modernization of dyeing System, for training intervention among SME’s, Government intervention, C.F.C. Like spg.Unit, process and sizing, export house and common product display center/ show room, utilization of Government Schemes.

Huge scope of product diversification Scope for sub-contract work from large units

Exploration of new local and export market

6 Optimum utilization of NITRA

Network catering to bulk orders by distributing the work among the cluster’s units

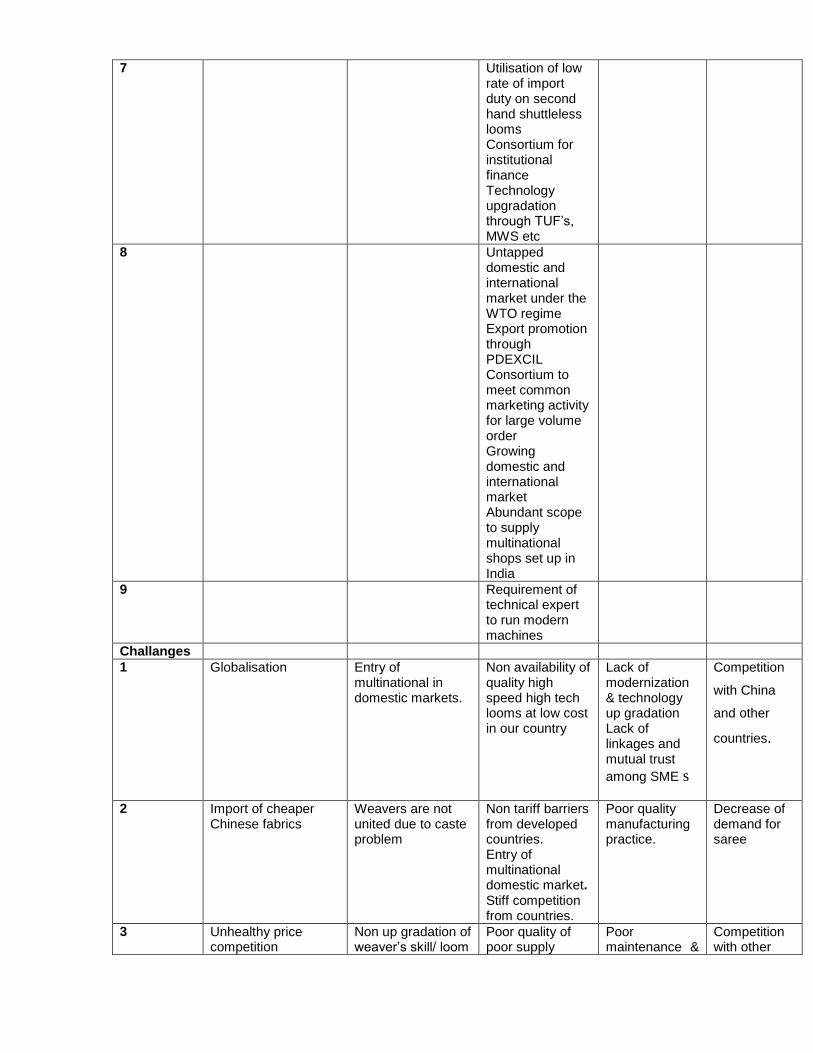

7 Utilisation of low rate of import duty on second hand shuttleless looms Consortium for institutional finance Technology upgradation through TUF’s, MWS etc

8 Untapped domestic and international market under the WTO regime Export promotion through PDEXCIL Consortium to meet common marketing activity for large volume order Growing domestic and international market Abundant scope to supply multinational shops set up in India

9 Requirement of technical expert to run modern machines

Challanges

1 Globalisation

Entry of multinational in domestic markets.

Non availability of quality high speed high tech looms at low cost in our country

Lack of modernization & technology up gradation Lack of linkages and mutual trust

among SME s

Competition

with China

and other

countries.

2 Import of cheaper Chinese fabrics

Weavers are not united due to caste problem

Non tariff barriers from developed countries. Entry of multinational domestic market. Stiff competition from countries.

Poor quality manufacturing practice.

Decrease of demand for saree

3 Unhealthy price competition

Non up gradation of weaver’s skill/ loom

Poor quality of poor supply

Poor maintenance &

Competition with other

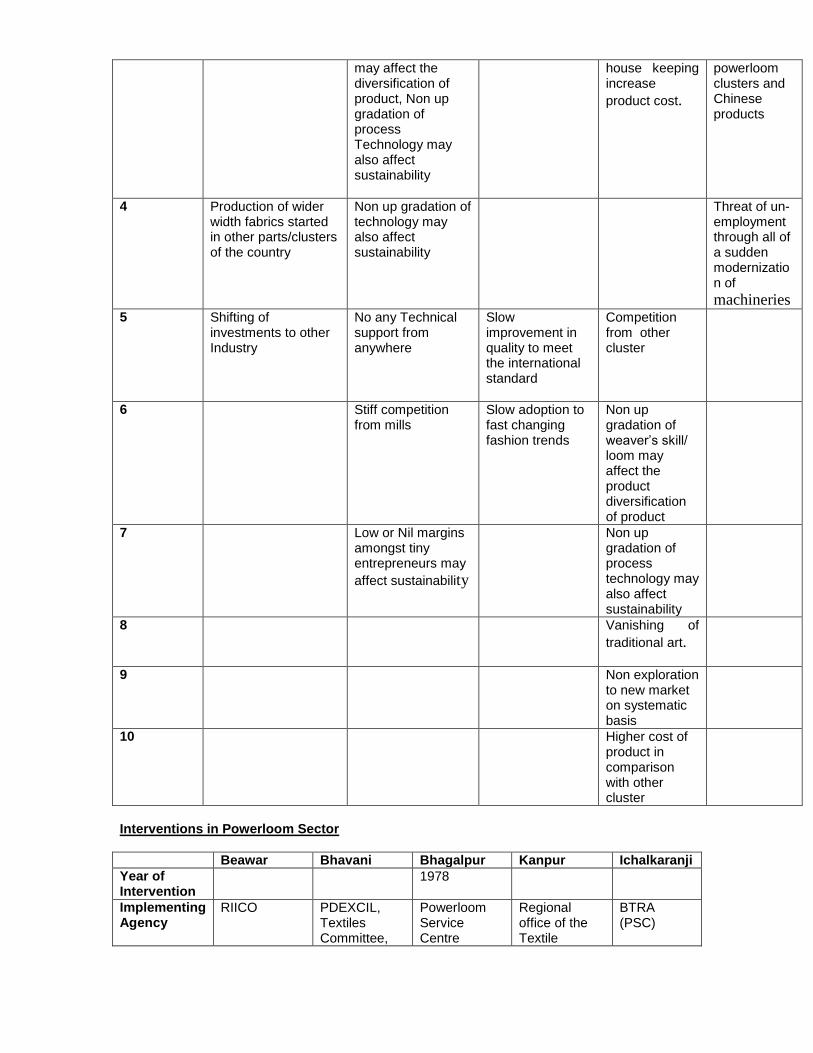

may affect the diversification of product, Non up gradation of process Technology may also affect sustainability

house keeping increase

product cost.

powerloom clusters and Chinese products

4 Production of wider width fabrics started in other parts/clusters of the country

Non up gradation of technology may also affect sustainability

Threat of un-employment through all of a sudden modernization of machineries

5 Shifting of investments to other Industry

No any Technical support from anywhere

Slow improvement in quality to meet the international standard

Competition from other cluster

6 Stiff competition from mills

Slow adoption to fast changing fashion trends

Non up gradation of weaver’s skill/ loom may affect the product diversification of product

7 Low or Nil margins amongst tiny entrepreneurs may

affect sustainability

Non up gradation of process technology may also affect sustainability

8 Vanishing of

traditional art.

9 Non exploration to new market on systematic basis

10 Higher cost of product in comparison with other cluster

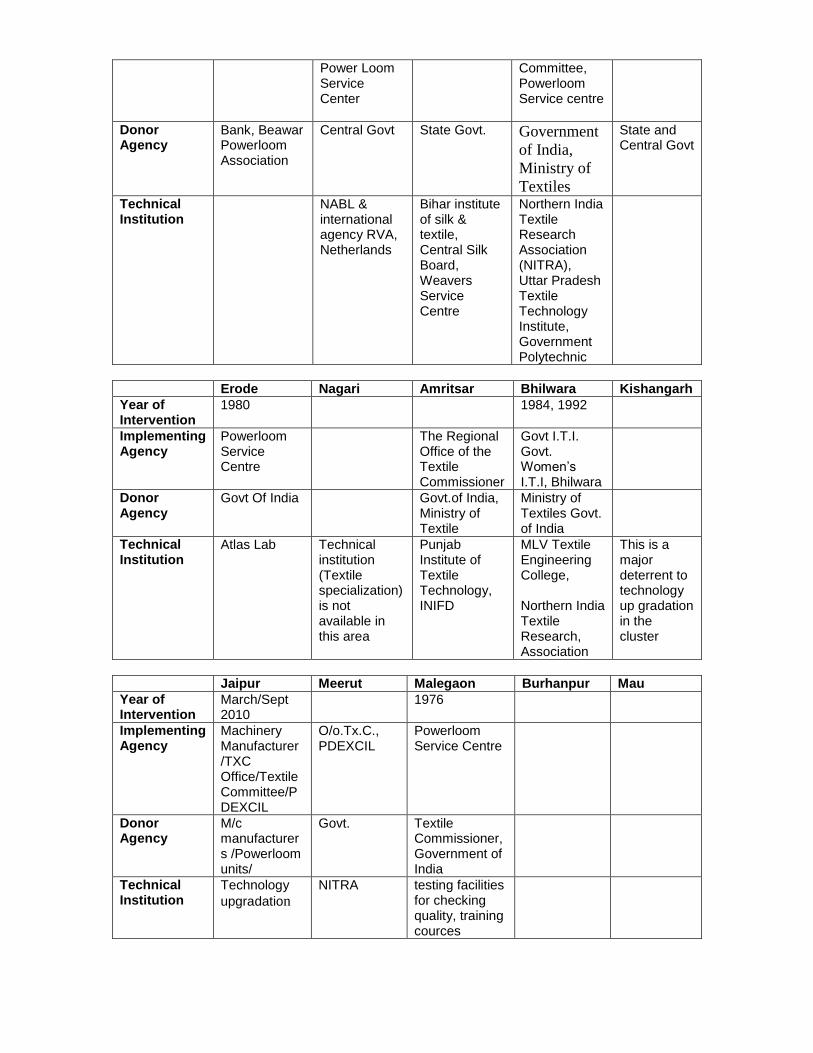

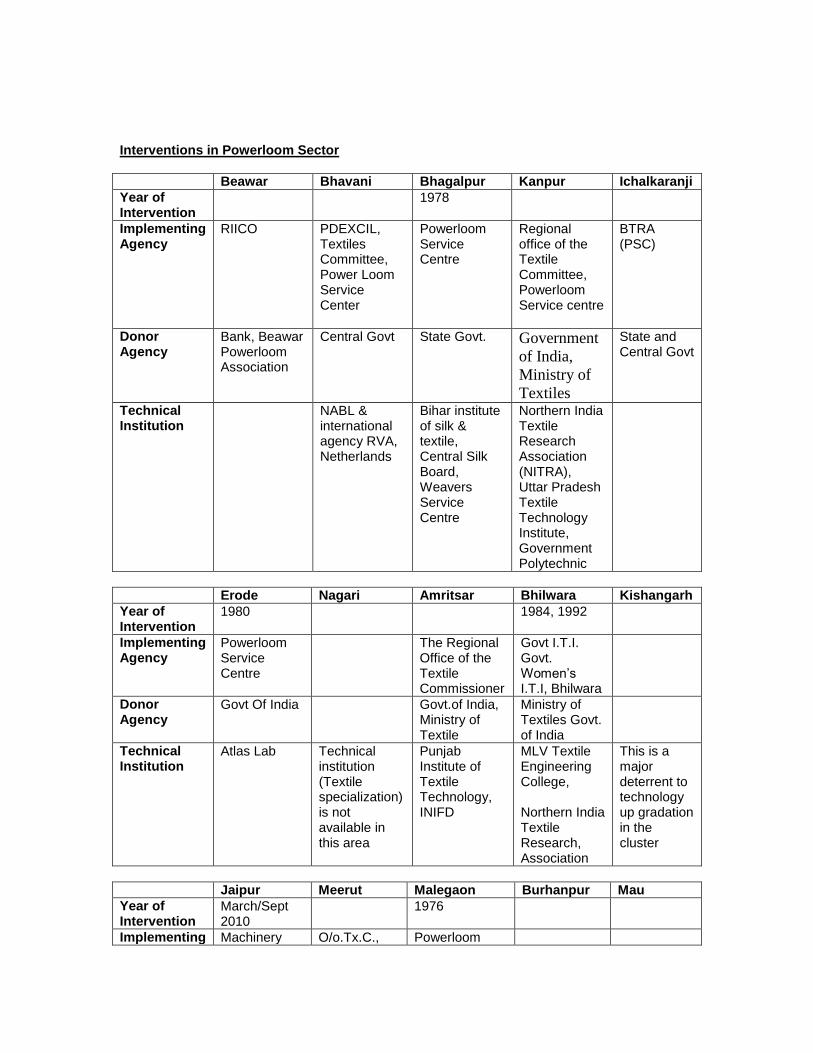

Interventions in Powerloom Sector

Beawar Bhavani Bhagalpur Kanpur Ichalkaranji

Year of Intervention

1978

Implementing Agency

RIICO PDEXCIL, Textiles Committee,

Powerloom Service Centre

Regional office of the Textile

BTRA (PSC)

Power Loom Service Center

Committee, Powerloom Service centre

Donor Agency

Bank, Beawar Powerloom Association

Central Govt State Govt.

Government

of India,

Ministry of

Textiles

State and Central Govt

Technical Institution

NABL & international agency RVA, Netherlands

Bihar institute of silk & textile, Central Silk Board, Weavers Service Centre

Northern India Textile Research Association (NITRA), Uttar Pradesh Textile Technology Institute, Government Polytechnic

Erode Nagari Amritsar Bhilwara Kishangarh

Year of Intervention

1980 1984, 1992

Implementing Agency

Powerloom Service Centre

The Regional Office of the Textile Commissioner

Govt I.T.I. Govt. Women’s I.T.I, Bhilwara

Donor Agency

Govt Of India Govt.of India, Ministry of Textile

Ministry of Textiles Govt. of India

Technical Institution

Atlas Lab Technical institution (Textile specialization) is not available in this area

Punjab Institute of Textile Technology, INIFD

MLV Textile Engineering College, Northern India Textile Research, Association

This is a major deterrent to technology up gradation in the cluster

Jaipur Meerut Malegaon Burhanpur Mau

Year of Intervention

March/Sept 2010

1976

Implementing Agency

Machinery Manufacturer /TXC Office/Textile Committee/PDEXCIL

O/o.Tx.C., PDEXCIL

Powerloom Service Centre

Donor Agency

M/c manufacturers /Powerloom units/

Govt. Textile Commissioner, Government of India

Technical Institution

Technology

upgradation

NITRA testing facilities for checking quality, training cources

The Powerloom Development & Export Promotion Council (PDEXClL) set up by the

Ministry of Textiles in 1995 has been making constant endeavors to develop the

powerloom industry and to promote exports of powerloom textiles. The Council has

been organizing Buyer - Seller meets for the domestic as well as export markets in

addition to participation in national and international fairs to promote the exports

of powerloom textiles. The Council has been facilitating modernization and quality

improvement in the industry through seminars & workshops. The PDEXCIL has also

been actively working as interface between the Govt. and the industry on various

policy related matters.

Technical Institution

Power Loom Development Export Promotion Council (PDEXCIL),

Powerloom Service Centre,

District Industries Centre,

Deputy Development Officer (Textile) Office,

Textile Technology Institute,

Government Polytechnic,

Directorate of Handlooms & Textiles office,

Small Industries Corporation,

Industrial Consultants

Northern India Textile Research Association (NITRA)

Textile Committee

The Office Of The Textile Commissioner

Indian National Institution Of Fashion Designing (INIFD)

Textile Engineering College

Govt I.T.I.

Govt. Women’s I.T.I.

Institute of silk & textile,

Financial Institution

Corporation, Bank

State bank of India

Visya Bank

Indian Bank

Mercantile Bank

State Co-operative bank

Industrial Investment Corporation Ltd UCO Bank Syndicate Bank

Bank of India

Bank of Baroda

Central Bank

Maharashtra Bank

Janta Co-operative

Dena Bank

Urban Co-operative

Union Bank

Sangli Bank

United Western Bank

Sanmati Co-operative Bank

Canara bank

Handloom Export Promotion Council (HEPC)

National Small Industries Corporation

Small Industries Development Bank Of India

Industrial Development Bank Of India

State Bank of Bikaner and Jaipur,

Oriental Bank of Commerce

Canara Bank

Allahabad Bank

Bank of Maharashtra

Union Bank

UTI Bank

Dena Bank

Association

District Power loom Association, Laghu Udyog Sangh Beawar,

RIICO Rajasthan Industrial Infrastructure Corporation Organization

Powerloom Weavers Association

Shawl club (India)

Textile Manufacturing Association (TMA

District Small Industries Association

Synthetic Weaving Mills Association

Chamber of Commerce and Industries

Sulzer weaving Mills Association

Textile processing association

Regional Office of the Textile Commissioner

Association of Powerloom Modernisation

Powerloom Action Committee

Yarn Merchants Association

Cloth merchant Association

Ready Made Garment Association

Industrial Co-operative Association Ltd

Computer Added Textile Design Center,

District Handloom & Handicraft Office

Power loom Development & Export Promotion Council

Power loom Weavers Co-op Federation.

The Textile and Apparel supply chain

Interventions in Powerloom Sector

Beawar Bhavani Bhagalpur Kanpur Ichalkaranji

Year of Intervention

1978

Implementing Agency

RIICO PDEXCIL, Textiles Committee, Power Loom Service Center

Powerloom Service Centre

Regional office of the Textile Committee, Powerloom Service centre

BTRA (PSC)

Donor Agency

Bank, Beawar Powerloom Association

Central Govt State Govt.

Government

of India,

Ministry of

Textiles

State and Central Govt

Technical Institution

NABL & international agency RVA, Netherlands

Bihar institute of silk & textile, Central Silk Board, Weavers Service Centre

Northern India Textile Research Association (NITRA), Uttar Pradesh Textile Technology Institute, Government Polytechnic

Erode Nagari Amritsar Bhilwara Kishangarh

Year of Intervention

1980 1984, 1992

Implementing Agency

Powerloom Service Centre

The Regional Office of the Textile Commissioner

Govt I.T.I. Govt. Women’s I.T.I, Bhilwara

Donor Agency

Govt Of India Govt.of India, Ministry of Textile

Ministry of Textiles Govt. of India

Technical Institution

Atlas Lab Technical institution (Textile specialization) is not available in this area

Punjab Institute of Textile Technology, INIFD

MLV Textile Engineering College, Northern India Textile Research, Association

This is a major deterrent to technology up gradation in the cluster

Jaipur Meerut Malegaon Burhanpur Mau

Year of Intervention

March/Sept 2010

1976

Implementing Machinery O/o.Tx.C., Powerloom

Agency Manufacturer /TXC Office/Textile Committee/PDEXCIL

PDEXCIL Service Centre

Donor Agency

M/c manufacturers /Powerloom units/

Govt. Textile Commissioner, Government of India

Technical Institution

Technology

upgradation

NITRA testing facilities for checking quality, training cources

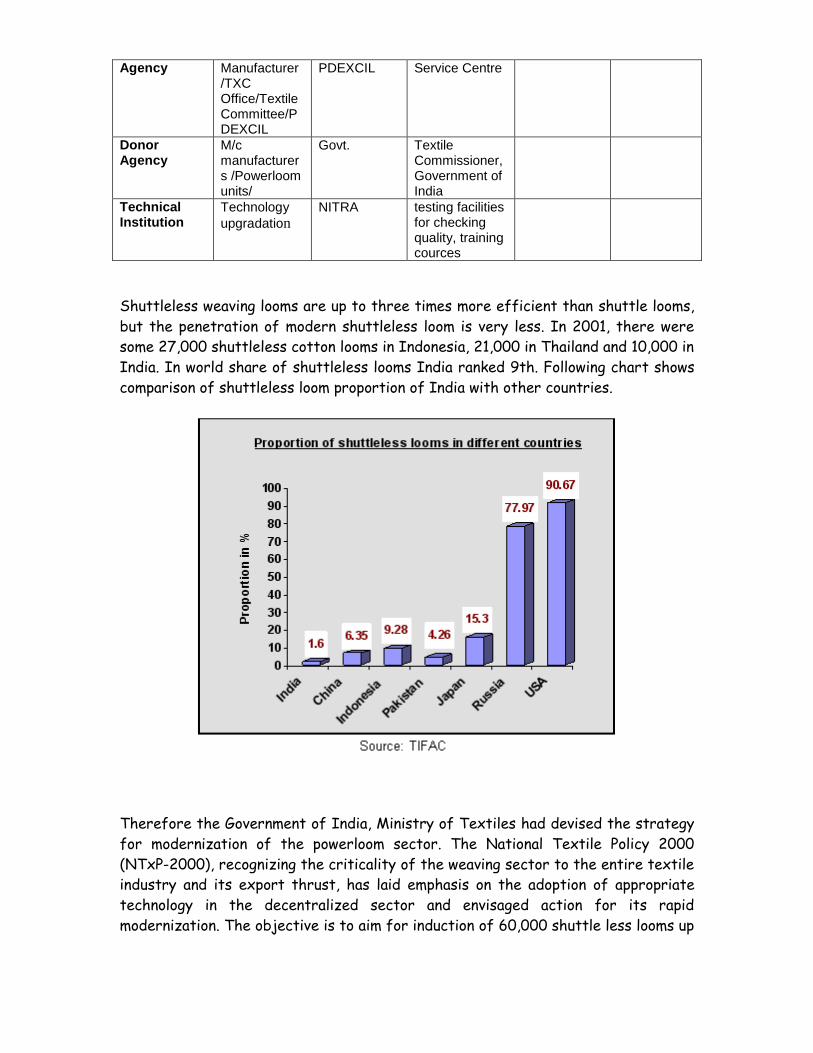

Shuttleless weaving looms are up to three times more efficient than shuttle looms,

but the penetration of modern shuttleless loom is very less. In 2001, there were

some 27,000 shuttleless cotton looms in Indonesia, 21,000 in Thailand and 10,000 in

India. In world share of shuttleless looms India ranked 9th. Following chart shows

comparison of shuttleless loom proportion of India with other countries.

Therefore the Government of India, Ministry of Textiles had devised the strategy

for modernization of the powerloom sector. The National Textile Policy 2000

(NTxP-2000), recognizing the criticality of the weaving sector to the entire textile

industry and its export thrust, has laid emphasis on the adoption of appropriate

technology in the decentralized sector and envisaged action for its rapid

modernization. The objective is to aim for induction of 60,000 shuttle less looms up

to the end of 2007 in the decentralized powerloom sector which will lead to a

quantum leap in technology upgradation.

The industry is very happy that the government has brought in many schemes to

modernise the textile industry like TUFS (Technology Upgradation Fund Scheme),

TCIDS (Textile Centre Infrastructure Development Scheme), CLCS (Credit Linked

Capital Subsidy), SITP (Scheme for Integrated Textile Park), Group Workshed

Scheme, NCUTE (Nodal Centre for Upgradation of Textile Education). These

schemes can be extended and awareness can be brought among the industry to

utilize the schemes.

The Union Budget 2001 gives a further impetus to this trend by allocating Rs.10

crores to set up "Integrated Apparel Parks" to enable the dereserved garment

units to modernise. Also, to set up 50,000 shuttleless looms and to convert 2.5 lakh

traditional looms to automatic ones, the provision under the technology upgradation

fund scheme (TUFS) is raised from Rs.50 crores to Rs.200 crores

To develop the power loom units within our catchment’s area so that it can continue

to dominate the domestic market & can develop strongly in exports by evaluating its

advantages & securing its shortcomings.

Critical Services Required for powerloom

Human Resource Development – Training

Regular training courses on pre-weaving and weaving technology, fabric design,

machine maintenance and other local needs to weavers and loom owners to

acquire, improve and update their skills in line with the latest and appropriate

technology in the sector.

Short duration courses for quality checkers and production supervisors on

different type of fabric defects, methods of mending such defects and

methods of prevention.

Assistance to trainees in their placement in the industry or for setting up of

their own units, and maintain contact with them.

Incentives from the State Governments and Facilitation or other suitable

accommodation for outstation trainees.

Quality Testing

Reliable textile testing services for checking quality parameters to power

loom and allied sectors through our testing laboratory (if available).

Guidance and Consultancy

Loom modernisation, design and product development, improvement in quality

and productivity, cost reduction through minimization of waste etc.

Repair and preventive maintenance of looms, accessories and preparatory

machinery.

On-site consultancy to on a felt-need basis, in respect of production and

process management.

Design Development, Exchange,Warehousing and Commercilisation

Contemporary and demand-oriented designs, via in-house skills with the help

of CAD/CAM system (if available).

A bank of designs and motifs, from internal and external sources and

through networking with National Design Centre (NDC).

Local design development by tapping local and innovative design skills.

Marketing Support

Local trade expositions, organized by the industry and trade association(s).

Participation of the local sector in export promotion programmes, in national &

international trade fairs, buyer-seller meets, trade delegations/sales-cum-study

teams, directly and through the Export Promotion Councils.

Promotion of the use of information technology and e-commerce as a marketing

tool.

Coordination and Facilitation

With all concerned institutions, including financial institutions, for a common

approach to the development of the sector.

For the transmission of the concerns and problems of the sector to the relevant

authorities.

For collectivisation of interests, through the formation of co-operatives, local

self-help action groups etc. to enhance access to credit, inputs and markets.

Implementation of Government Programmes/Schemes

Special development programmes in the decentralized powerloom sector, viz.

Programme for modernisation of weaving capacities by induction of 2.5 lakh semi

automatic/automatic looms in the decentralised sector, as Implementing

Agency. TUFS, through appropriate awareness campaigns and support services,

in respect of choice of technology, project formulation and compliance with

banking requirements and project implementation.

Welfare scheme for the powerloom weavers, viz., group insurance scheme,

workshed scheme etc.

Review Committee Meeting of Nitra PLSCS

Review Committee Meeting of PLSC Managers are being held at NITRA

under the Chairmanship of Director NITRA: Quarterly review committee

meeting of all PLS centres are being held at NITRA.

Due to the changes in the international scenario on the implementation of WTO

agreement on textile industry, our country is facing some implications. We need to

prepare our self to meet the challenges of global competition by increasing the

productivity & by improving quality of our products.

The powerloom sector occupies a pivotal position in the Indian textile industry.

Though current growth of this sector has been restricted by technological

obsolescence, fragmented structure, low productivity and low-end quality products,

in future Technology would play a lead role in this sector and will improve quality

and productivity levels. Innovations would also be happening in this sector, as many

developed countries would be innovating new generation machineries that are likely

to have low manual interface and power cost. Indian textile industry should also

turn into high technology mode to collect the benefits of scale operations and

quality.

To reap benefits of these developments Indian powerloom industry has to prepare

itself for drastic technological changes and will have to focus on area such as

Technology upgradation: modernization of Power loom Service Centres and testing

facilities; Clustering of facilities to achieve optimum levels of production; Welfare

schemes for ensuring a healthy and safe working environment for the workers in

future.

Sources :

DS – a. Bhagalpur, b. Beawar, c. Amritsar, d. Erode, e. Kishangarh, f. Mau, g. Nagari,

h. Bhavani, i. Bhilwara, j. Burhanpur, k. Jaipur, l. Ichalkaranji, n. Kanpur, n. Malegaon,

o. Meerat

Indian Textile Industries

Emerging SMEs of India Textile

Confederation of India Textile India http://www.citiindia.com

http://www.smallindustriesindia.com/clusteres/unido/methcludata.htm#basic

Office of Textile Commission

R&D Research

Unido

SIDO

MSME Foundation

Office of Powerloom Dev Council

Powerloom Produc Dev Sector

Clusterkraft

Thomex.com

AP Online

PDEXCIL

Sitra