Embed Size (px)

Citation preview

Poverty and Equity:Theory and Estimation

by

Jean-Yves Duclos

Departement d’economique and CREFA,Universite Laval, Canada

Preliminary version

This text is in large part an output of the MIMAP training programme financedby the International Development Research Center of the Government of Canada.The underlying research was also supported by grants from the Social Sciencesand Humanities Research Council of Canada and from the Fonds FCAR of theProvince of Quebec. I am grateful to Abdelkrim Araar and Nicolas Beaulieu fortheir excellent research assistance.

Corresponding address:Jean-Yves Duclos, Departement d’economique, Pavillon de Seve, Universite

Laval, Quebec, Canada, G1K 7P4; Tel.: (418) 656-7096; Fax: (418) 656-7798;Email: [email protected]

January 2002

Contents

I Introduction 5

1 Well-being and poverty 61.1 The welfarist approach. . . . . . . . . . . . . . . . . . . . . . . 61.2 Non-welfarist approaches. . . . . . . . . . . . . . . . . . . . . . 8

1.2.1 Basic needs and functionings. . . . . . . . . . . . . . . . 81.2.2 Capabilities. . . . . . . . . . . . . . . . . . . . . . . . . 10

1.3 A graphical illustration. . . . . . . . . . . . . . . . . . . . . . . 111.3.1 Exercises. . . . . . . . . . . . . . . . . . . . . . . . . . 14

1.4 Practical measurement difficulties. . . . . . . . . . . . . . . . . 14

2 Poverty measurement and public policy 162.1 Welfarist and non-welfarist policy implications. . . . . . . . . . 17

II Measuring poverty and equity 20

3 Notation 213.1 Continuous distributions. . . . . . . . . . . . . . . . . . . . . . 213.2 Discrete distributions. . . . . . . . . . . . . . . . . . . . . . . . 23

4 The measurement of inequality and social welfare 254.1 Lorenz curves. . . . . . . . . . . . . . . . . . . . . . . . . . . . 254.2 Gini indices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 274.3 Social welfare. . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

4.3.1 Atkinson indices. . . . . . . . . . . . . . . . . . . . . . 354.3.2 S-Gini indices . . . . . . . . . . . . . . . . . . . . . . . 36

4.4 Decomposable indices of inequality. . . . . . . . . . . . . . . . 374.5 Other popular indices of inequality. . . . . . . . . . . . . . . . . 39

5 Aggregating and comparing poverty 405.1 Cardinal versus ordinal comparisons. . . . . . . . . . . . . . . . 405.2 Aggregating poverty . . . . . . . . . . . . . . . . . . . . . . . . 41

5.2.1 The EDE approach. . . . . . . . . . . . . . . . . . . . . 415.2.2 The poverty gap approach. . . . . . . . . . . . . . . . . 42

5.3 Group-decomposable poverty indices. . . . . . . . . . . . . . . 46

1

5.4 Poverty and inequality. . . . . . . . . . . . . . . . . . . . . . . 475.5 Poverty curves. . . . . . . . . . . . . . . . . . . . . . . . . . . . 485.6 S-Gini poverty indices . . . . . . . . . . . . . . . . . . . . . . . 485.7 The normalization of poverty indices. . . . . . . . . . . . . . . . 495.8 Decomposing differences in poverty. . . . . . . . . . . . . . . . 50

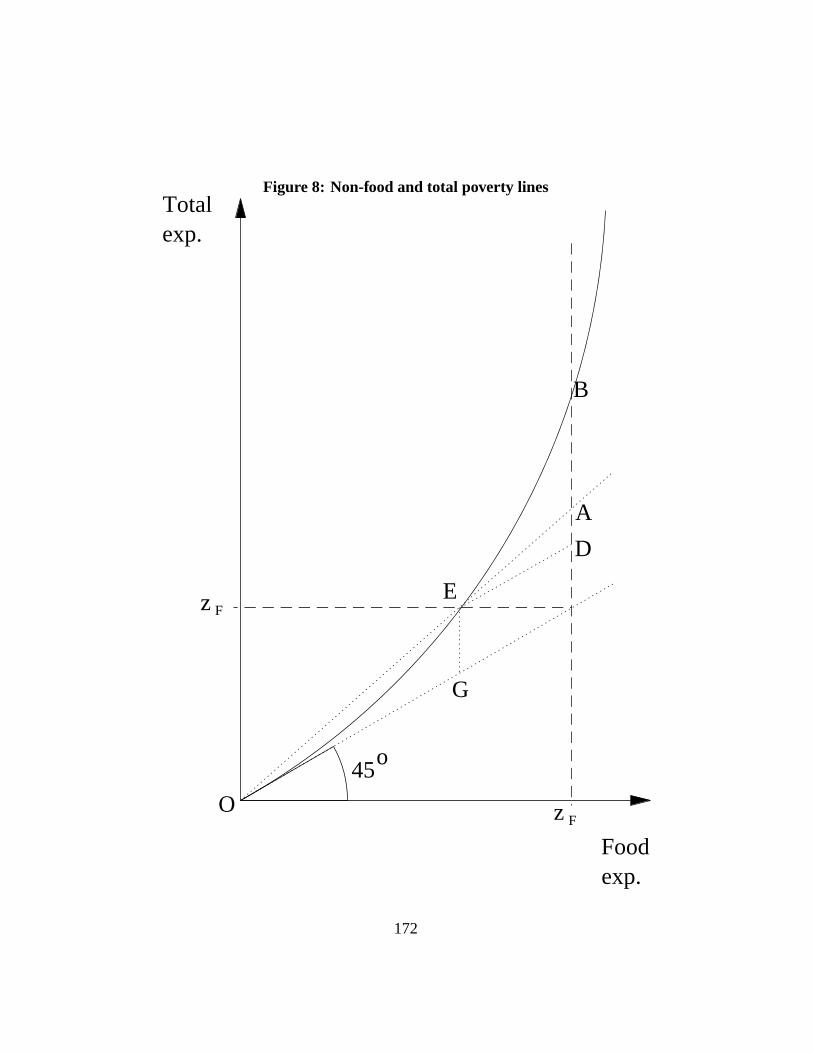

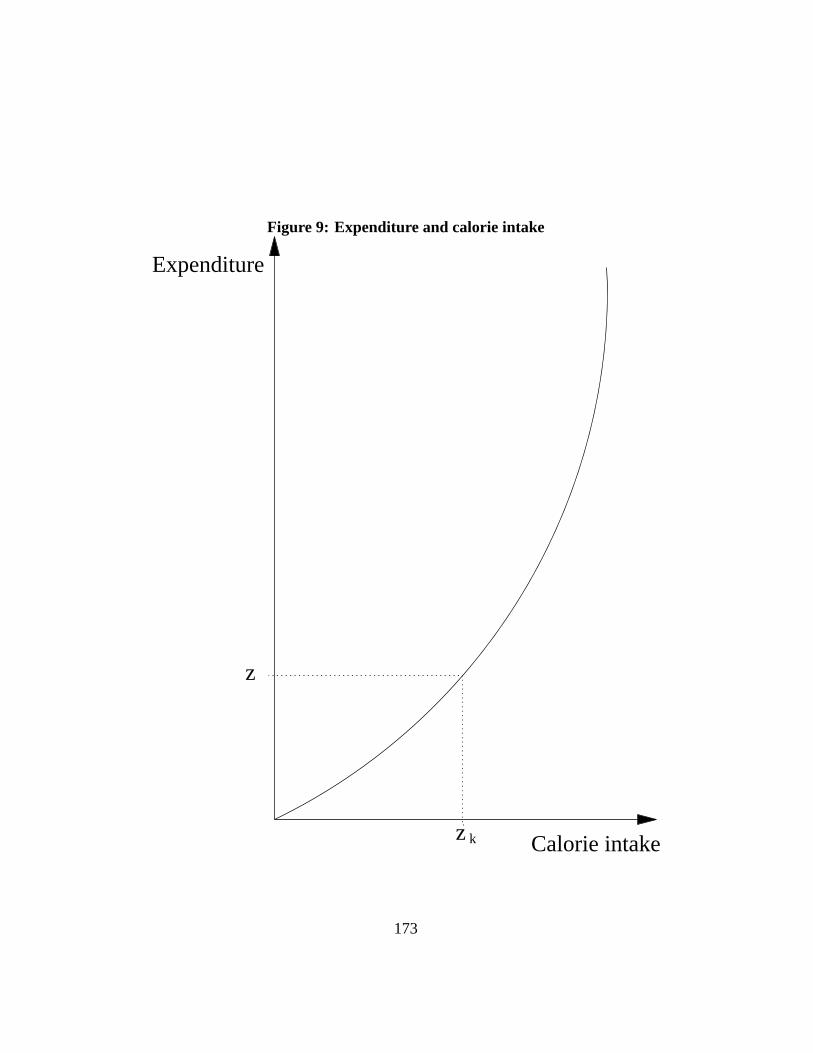

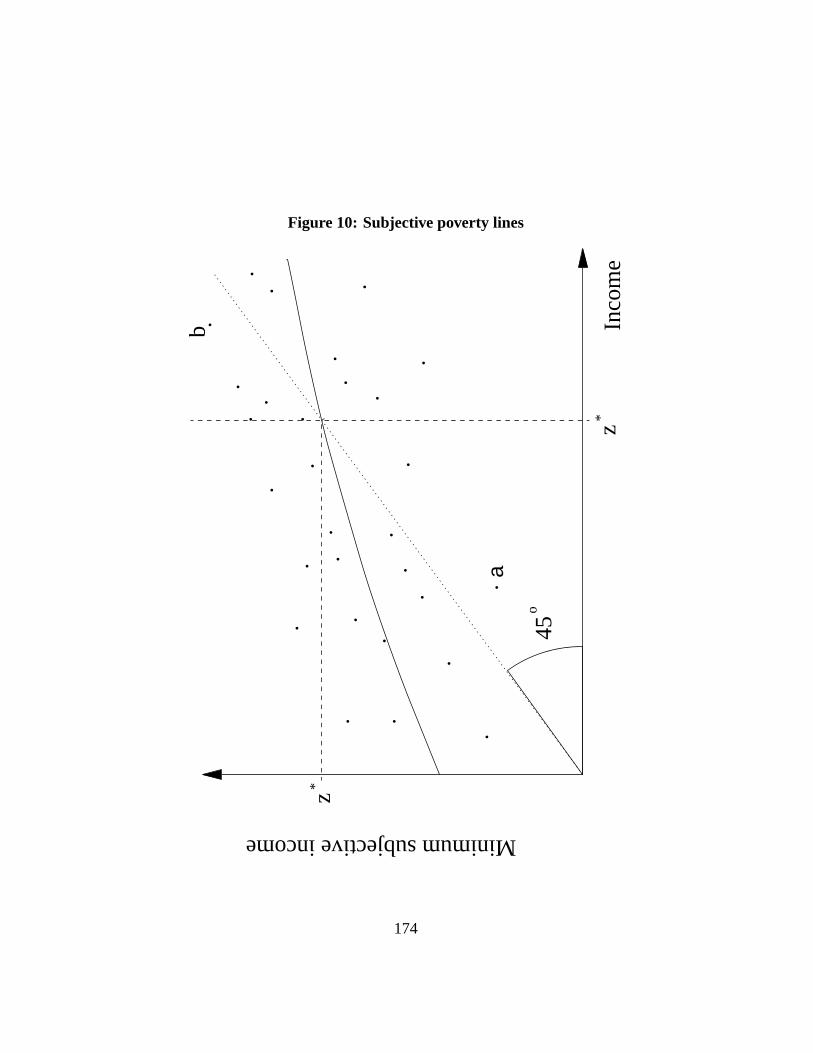

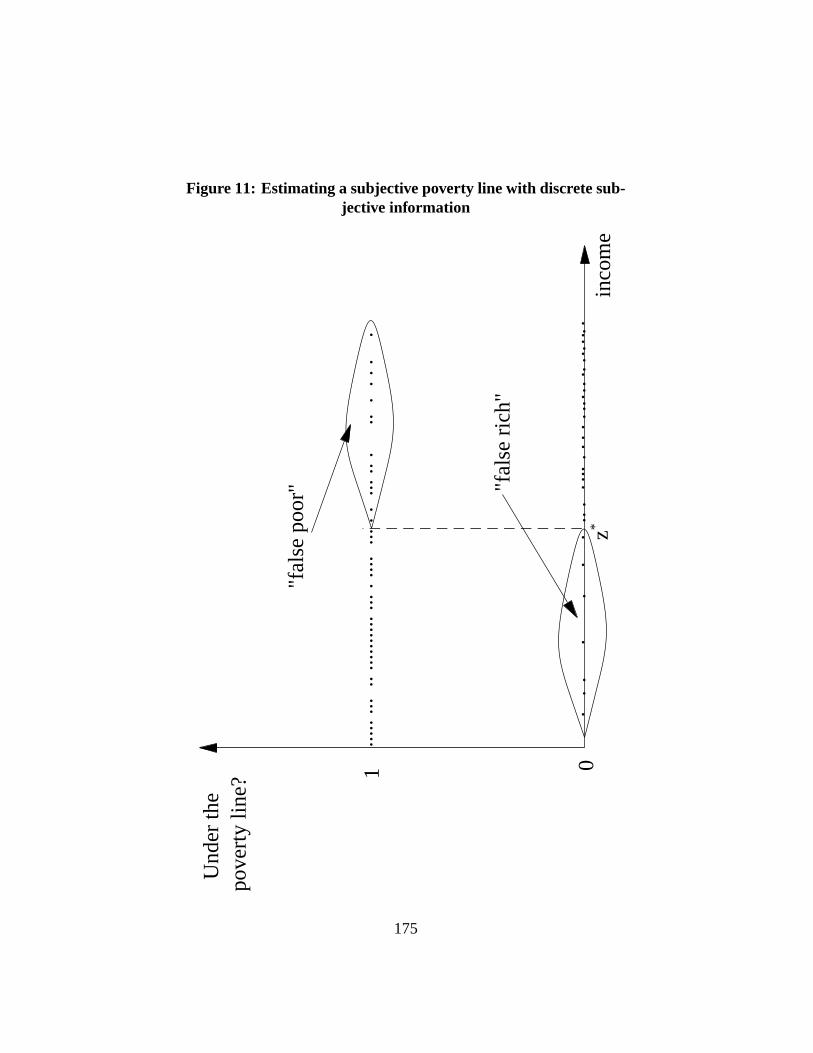

6 Estimating poverty lines 536.1 Absolute and relative poverty lines. . . . . . . . . . . . . . . . . 536.2 Social exclusion and relative deprivation. . . . . . . . . . . . . . 546.3 Estimating poverty lines. . . . . . . . . . . . . . . . . . . . . . 56

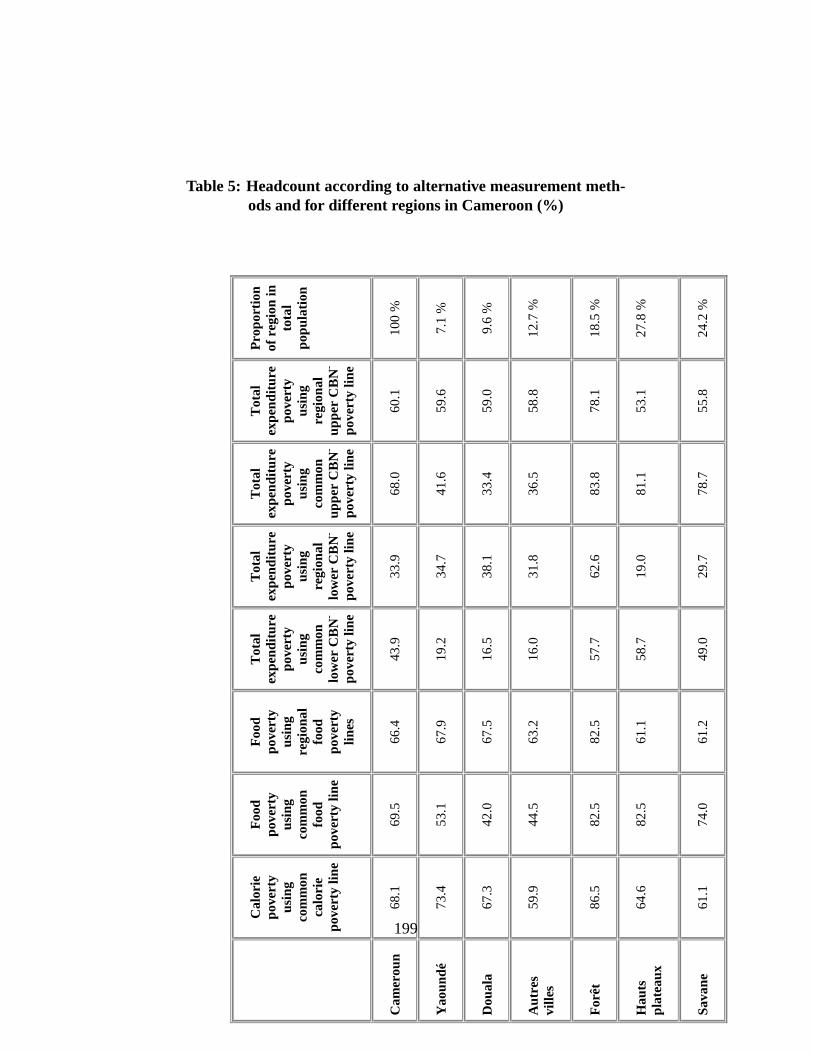

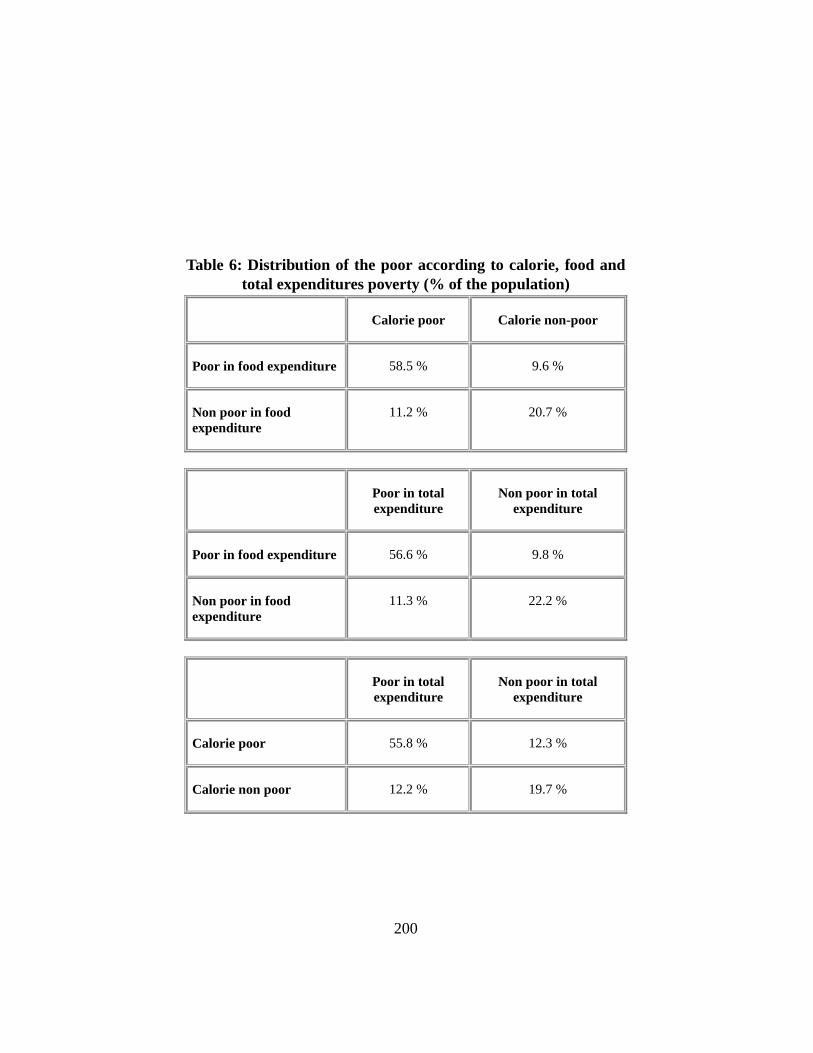

6.3.1 Cost of basic needs. . . . . . . . . . . . . . . . . . . . . 566.3.2 Cost of food needs. . . . . . . . . . . . . . . . . . . . . 566.3.3 Non-food poverty lines. . . . . . . . . . . . . . . . . . . 596.3.4 Food energy intake. . . . . . . . . . . . . . . . . . . . . 616.3.5 Illustration for Cameroon. . . . . . . . . . . . . . . . . . 636.3.6 Relative and subjective poverty lines. . . . . . . . . . . . 64

7 The measurement of progressivity, equity and redistribution 687.1 Taxes and concentration curves. . . . . . . . . . . . . . . . . . . 687.2 Indices of concentration. . . . . . . . . . . . . . . . . . . . . . . 707.3 Progressivity comparisons. . . . . . . . . . . . . . . . . . . . . 72

7.3.1 Deterministic tax and benefit systems. . . . . . . . . . . 727.3.2 General tax and benefit systems. . . . . . . . . . . . . . 73

7.4 Reranking and horizontal inequity. . . . . . . . . . . . . . . . . 757.5 Redistribution. . . . . . . . . . . . . . . . . . . . . . . . . . . . 797.6 Indices of progressivity and redistribution. . . . . . . . . . . . . 80

8 Issues in the empirical measurement of well-being and poverty 828.1 Survey issues. . . . . . . . . . . . . . . . . . . . . . . . . . . . 828.2 Income versus consumption. . . . . . . . . . . . . . . . . . . . 848.3 Price variability . . . . . . . . . . . . . . . . . . . . . . . . . . . 858.4 Household heterogeneity. . . . . . . . . . . . . . . . . . . . . . 89

8.4.1 Equivalence scales. . . . . . . . . . . . . . . . . . . . . 898.4.2 Household decision-making and within-household inequal-

ity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

III Ethical robustness of poverty and equity comparisons 95

2

9 Poverty dominance 969.1 Primal approach. . . . . . . . . . . . . . . . . . . . . . . . . . . 1009.2 Dual approach. . . . . . . . . . . . . . . . . . . . . . . . . . . . 1049.3 Assessing the limits to dominance. . . . . . . . . . . . . . . . . 105

10 Inequality dominance 10710.1 Primal approach. . . . . . . . . . . . . . . . . . . . . . . . . . . 10810.2 Dual approach. . . . . . . . . . . . . . . . . . . . . . . . . . . . 10910.3 Inequality and progressivity. . . . . . . . . . . . . . . . . . . . . 109

11 Welfare dominance 11111.1 Primal approach. . . . . . . . . . . . . . . . . . . . . . . . . . . 11211.2 Dual approach. . . . . . . . . . . . . . . . . . . . . . . . . . . . 113

IV Poverty and equity: policy design and assessment 115

12 Poverty alleviation: policy and growth 11612.1 Measuring the benefits of public spending. . . . . . . . . . . . . 11612.2 Checking the distributive effect of public expenditures. . . . . . 11612.3 The impact of targeting and public expenditure reforms on poverty117

12.3.1 Group-targeting a constant amount. . . . . . . . . . . . . 11912.3.2 Inequality-neutral targeting. . . . . . . . . . . . . . . . . 12012.3.3 Price changes. . . . . . . . . . . . . . . . . . . . . . . . 12112.3.4 Tax/subsidy policy reform. . . . . . . . . . . . . . . . . 12412.3.5 Income-component and sectoral growth. . . . . . . . . . 126

12.4 Overall growth elasticity of poverty. . . . . . . . . . . . . . . . 12612.5 The Gini elasticity of poverty. . . . . . . . . . . . . . . . . . . . 128

13 The impact of policy and growth on inequality 12913.1 Growth, tax and transfer policy, and price shocks. . . . . . . . . 12913.2 Tax and subsidy reform. . . . . . . . . . . . . . . . . . . . . . . 131

V Estimation and inference for distributive analysis 133

14 Non parametric estimation for distributive analysis 13414.1 Density estimation. . . . . . . . . . . . . . . . . . . . . . . . . 134

14.1.1 Univariate density estimation. . . . . . . . . . . . . . . . 134

3

14.1.2 Statistical properties of kernel density estimation. . . . . 13614.1.3 Choosing a window width. . . . . . . . . . . . . . . . . 13714.1.4 Multivariate density estimation. . . . . . . . . . . . . . . 13914.1.5 Simulating from a nonparametric density estimate. . . . 139

14.2 Non-parametric regression. . . . . . . . . . . . . . . . . . . . . 141

15 Symbols 144

16 References 151

17 Graphs and tables 164

4

Part I

Introduction

5

1 Well-being and poverty

The assessment of well-being for poverty analysis is traditionally characterizedaccording to two main approaches, which, following Ravallion (1994), we willterm the welfarist and the non-welfarist approaches. The first approach tends toconcentrate in practice mainly on comparisons of ”economic well-being”, whichwe will also call ”standard of living” or ”income” (for short). As we will see, thisapproach has strong links with traditional economic theory, and it is also widelyused by economists in the operations and research work of organizations such asthe World Bank, the International Monetary Fund, and Ministries of Finance andPlanning of both developed and developing countries. The second approach hashistorically been advocated mainly by social scientists other than economists andpartly in reaction to the first approach. This second approach has neverthelessalso been recently and increasingly advocated by economists and non-economistsalike as a sound multidimensional complement to the classical standard of livingapproach.

1.1 The welfarist approach

The welfarist approach is strongly anchored in classical micro-economics, where,in the language of economists, ”welfare” or ”utility” are generally key in account-ing for the behavior and the well-being of individuals. Classical micro-economicsusually postulates that individuals are rational and that they can be presumed tobe the best judges of the sort of life and activities which maximize their utilityand happiness. Given their initial endowments (including time, land and phys-ical and human capital), individuals make production and consumption choicesusing their set of preferences over bundles of consumption and production activ-ities, and taking into account the available production technology and the con-sumer and producer prices that prevail in the economy. Under these assumptionsand constraints, a process of individual and rational free choice will maximizethe individuals’ utility; under additional assumptions (including that markets arecompetitive, that agents have perfect information, and that there are no externali-ties – assumptions that are thus very restrictive), a society of individuals all actingindependently under this freedom of choice process will also lead to an outcomeknown as Pareto-efficient, in that no one’s utility could be further improved bygovernment intervention without decreasing someone else’s utility.

Underlying the welfarist approach to poverty, there is a premise that goodnote should be taken of the information revealed by individual behavior when

6

it comes to assessing poverty. This says, more particularly, that the assessmentof someone’s well-being should be consistent with the ordering of preferencesrevealed by that person’s free choices. For instance, a person could be observedto be poor by the total consumption or income standard of a poverty analyst. Thatsame person could nevertheless be able (i.e., have the working capacity) to be non-poor. This could be revealed by the observation of a deliberate and free choiceon the part of the individual to work and consume little, when the capability towork and consume more nevertheless exists. By choosing to spend little (possiblyfor the benefit of greater leisure), the person reveals that he is happier than if heworked and spent more. Although he could be considered poor by the standard ofa (non-welfarist) poverty analyst, a welfarist judgement should conclude that thisperson is not poor. As we will discuss later, this can have important implicationsfor the design and the assessment of public policy.

A pure welfarist approach faces important practical problems. To be opera-tional, pure welfarism requires the observation of sufficiently informative revealedpreferences. This is rarely the case, however. For instance, for someone to bedeclared poor or not poor, it is not enough to know that person’s current charac-teristics and living standard status, but it must also be inferred from that person’sactions whether he judges his utility status to be above a certain utility povertylevel. Another – more fundamental – problem with the pure welfarist approach isthe need to assess levels of utility or ”psychic happiness”. How are we to measurethe actual pleasure derived from experiencing economic well-being? Moreover, itis highly problematic to attempt to compare that level of utility across individuals– it is well known that such a procedure poses serious ethical problems. Prefer-ences are heterogeneous, personal characteristics, needs and enjoyment abilitiesare diverse, households differ in size and composition, and prices vary across timeand space. Besides, it is not clear that we should accept as ethically significantthe actual level of utility felt by individuals. Why should a difficult-to-satisfy richperson be judged less happy than an easily-contented poor person? That is, whyshould a ”grumbling rich” be judged ”poorer” than a ”contented peasant” (see Sen(1983), p.160)?

Hence, welfarist comparisons of poverty almost invariably use imperfect butobservable proxies for utilities, such as income or consumption. These money-metric indicators are often adjusted for differences in needs, prices, and householdsizes and compositions, but they clearly do remain far-from-perfect indicators ofutility and well-being. Indeed, economic theory tells us little about how to useconsumption or income to make consistent interpersonal comparisons of well-being. Besides, the consumption and income proxies are rarely able to take full

7

account of the role for well-being of public goods and non-market commodities,such as safety, liberty, peace, health. In principle, such commodities can be val-ued using reference or ”shadow” prices. In practice, this is very difficult to doaccurately and consistently.

1.2 Non-welfarist approaches

1.2.1 Basic needs and functionings

There are two major non-welfarist approaches, the basic-needs approach and thecapability approach. The first approach focuses on the need to attain some basicmultidimensional outcomes that can be observed and monitored relatively easily.These outcomes are usually (explicitly or implicitly) linked with the concept offunctionings, a concept developed in Amartya Sen’s influential work:

Living may be seen as consisting of a set of interrelated ’function-ings’, consisting of beings and doings. A person’s achievement inthis respect can be seen as the vector of his or her functionings. Therelevant functionings can vary from such elementary things as beingadequately nourished, being in good health, avoiding escapable mor-bidity and premature mortality,etc., to more complex achievementssuch as being happy, having self-respect, taking part in the life of thecommunity, and so on (Sen (1997), p.39).

In this view, functionings can be understood to beconstitutiveelements of well-being. The functioning approach would generally not attempt to compress theseelements into a single dimension such as utility or happiness. Utility or hap-piness is viewed as a single and reductive aggregate of functionings, which aremultidimensional in nature. The functioning approach focuses instead on multi-ple specific and separate outcomes, such as the enjoyment of a particular type ofcommodity consumption, being healthy, literate, well-clothed, well-housed, notin shape,etc..

The functioning approach is closely linked with the well-known basic needsapproach, and the two are often difficult to distinguish in their practical applica-tion. Functionings, however, are not synonymous with basic needs. Basic needscan be understood as the physical inputs that are usually required for individualsto achieve some functionings. Hence, basic needs are usually defined in terms ofmeans rather than outcomes, for instance, as living in the proximity of providersof health care services (but not necessarily being in good health), as the number

8

of years of achieved schooling (not necessarily as being literate), as living in ademocracy (but not necessarily as participating in the life of the community), andso on. In other words,

Basic needs may be interpreted in terms of minimum specified quan-tities of such things as food, shelter, water and sanitation that are nec-essary to prevent ill health, undernourishment and the like (Streetenet al. (1981)).

Unlike functionings, which can be commonly defined for all individuals, thespecification of basic needs depends on the characteristics of individuals and ofthe societies in which they live. For instance, the basic commodities required forsomeone to be in good health and not to be undernourished will depend on the cli-mate and on the physiological characteristics of individuals. Similarly, the clothesnecessary for one not to feel ashamed will depend on the norms of the society inwhich he lives, and the means necessary to travel, on whether he is handicappedor not. Hence, although the fulfillment of basic needs is an important elementin assessing whether someone has achieved some functionings, this assessmentmust also use information on one’s characteristics and socio-economic environ-ment. Human diversity is such that equality in the space of basic needs generallytranslates into inequality in the space in functionings.

Whether unidimensional or multidimensional in nature, most applications ofboth the welfarist and the non-welfarist approaches to poverty measurement dorecognize the role of needs and of socio-economic environments in achievingwell-being. Streetenet al. (1981) and others have nevertheless argued that thebasic needs approach is less abstract than the welfarist approach in recognizingthat role. As mentioned above, assessing the fulfillment of basic needs it can alsobe seen as a useful practical and operational step towards appraising the achieve-ment of the more abstract ”functionings”.

Clearly, however, there are important degrees in the multidimensional achieve-ments of basic needs and functionings. For instance, what does it mean preciselyto be ”adequately nourished”? Which degree of nutrition adequacy is relevant forpoverty assessment? Should the means needed for the adequate nutrition function-ing only allow for the simplest possible diet and for highest nutritional efficiency?These problems also crop up in the estimation of poverty lines in the welfaristapproach. A multidimensional approach extends them to several dimensions. Inaddition, how ought we to understand such functionings as the functioning ofself-respect? The appropriate width and depth of the concept of basic needs and

9

functionings is admittedly ambiguous, as there are degrees of functionings whichmake life enjoyable in addition to being purely sustainable or satisfactory. Finally,could some of the dimensions be substitutes in the attainment of a given degreeof well-being? That is, could it be that one could do with lower needs and func-tionings in some dimensions if he has high achievements in the other dimensions?Such possibilities of substitutability are generally ignored (and are indeed hard toidentify precisely) in the multidimensional non-welfarist approaches.

1.2.2 Capabilities

A second alternative to the welfarist approach is called the capability approach,also pioneered and advocated in the last two decades by the work of Sen. Thecapability approach is defined by thecapacityto achieve functionings, as definedabove. In Sen’s words (1997),

the capability to function represents the various combinations of func-tionings (beings and doings) that the person can achieve. Capabilityis, thus, a set of vectors of functionings, reflecting the person’s free-dom to lead one type of life or another. (p.40)

What matters for the capability approach is the ability of an individual to functionwell in society; it isnot the functionings actually attained by the person. Havingthe capability to achieve ”basic” functionings is the source of freedom to livewell, and is thereby sufficient in the capability approach for one not to be poor ordeprived.

The capability approach thus distances itself from achievements of specificoutcomes or functionings. In this, it imparts considerable value to freedom ofchoice: a person will not be judged poor even if he chooses not to achieve somefunctionings, so long as he would be able to attain them if he so chose. Thisdistinction between outcomes and the capability to achieve the outcomes also rec-ognizes the importance of preference diversity and individuality in determiningfunctioning choices. It is, for instance, not everyone’s wish to be well-clothed orto participate in society, even if the capability is present.

An interesting example of the distinction between fulfilment of basic needs,functioning achievement and capability is given by Townsend’s (1979, Table 6.3)deprivation index. The deprivation index is built from answers to questions suchas whether someone ”has not had an afternoon or evening out for entertainment inthe last two weeks”, or ”has not had a cooked breakfast most days of the week”. It

10

may be, however, that one chooses deliberately not to go out for entertainment (heprefers to watch television), or that he chooses not to have a cooked breakfast (be-cause he does not have time to prepare it), although he does have the capacity to doboth. That person therefore achieves the functioning of being entertained withoutmeeting the basic need of going out once a fortnight, and does have the capacityto achieve the functioning of having a good breakfast, although he chooses not to.

The difference between the capability and the functioning or basic needs ap-proach is in fact somewhat analogous to the difference between the use of incomeand consumption as indicators of living standards. Income shows the capability toconsume, and ”consumption functioning” can be understood as the outcome of theexercise of that capability. There is consumption only if a person chooses to enacthis capacity to consume out a given income. In the basic needs and functioningapproach, deprivation comes from a lack of direct consumption or functioning ex-perience; in the capability approach, poverty arises from the lack of incomes andcapabilities, which are imperfectly related to the actual functionings achieved.

Although the capability set is multidimensional, it thus exhibits a parallel withthe unidimensional income indicator, whose size determines the size of the ”bud-get set”:

Just as the so-called ’budget set’ in the commodity space representsa person’s freedom to buy commodity bundles, the ’capability set’ inthe functioning space reflects the person’s freedom to choose frompossible livings (Sen (1997, p. 40)).

This illustrates further the fundamental distinction between the space of achieve-ments, the extents of freedoms and capabilities, and the resources required togenerate these freedoms and to attain these achievements.

1.3 A graphical illustration

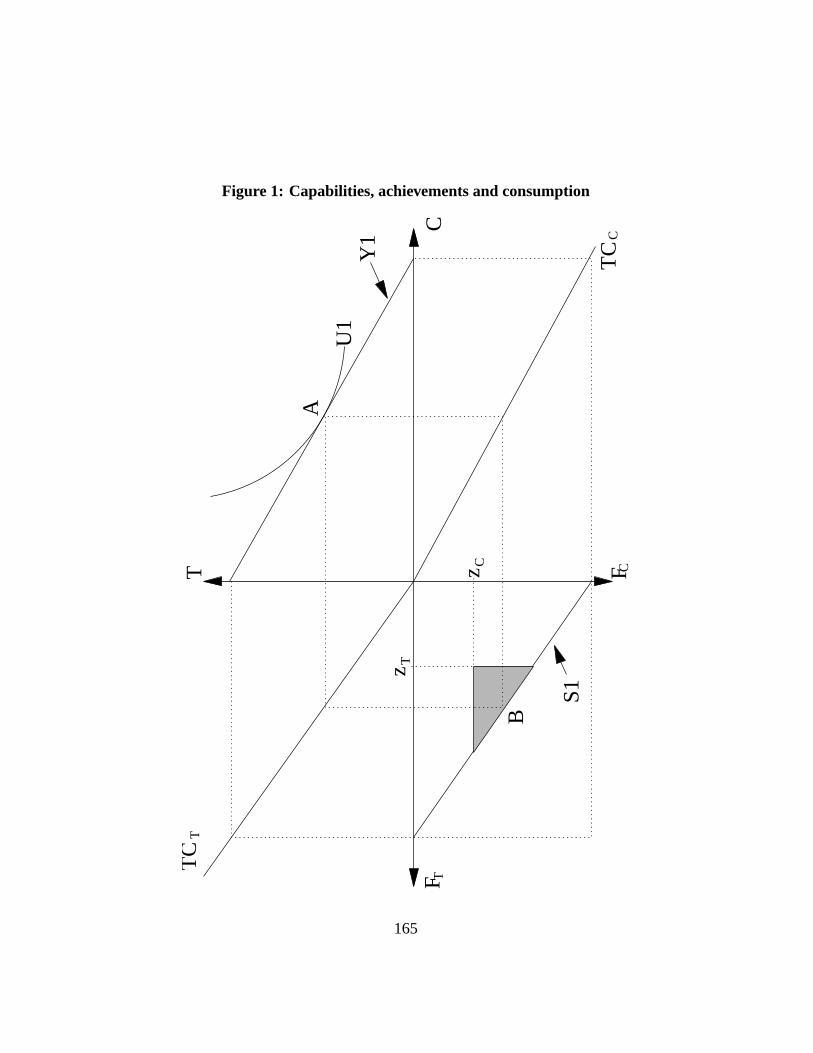

To illustrate the links between the main approaches to assessing poverty, considerFigure1. Figure1 shows in four quadrants the links between income, consump-tion of two commodities – transportation and clothing goods – and the function-ings associated to each of these two goods. The northeast quadrant shows a typicaltwo-good budget set for the two goodsT andC, namely, for transportation andclothing respectively, and with a budget constraintY 1. The curveU1 shows theutility indifference curve along which the consumer chooses his preferred com-modity bundle, which is here located at pointA.

11

The southeastern and the northwestern quadrants then transform the consump-tion of goodsT and C into associated functioningsFT and FC . This is donethrough the Functioning Transformation CurvesTCT andTCC , for transforma-tion of consumption ofT andC into transportation and clothing functionings.The curvesTCT andTCC appear in the northwest and the southeast quadrantsrespectively. These curves thus bring us from the northeastern space of com-modities,C, T, into the southwestern space of functionings,FC , FT. Usingthese transformation functions, we can draw a budget constraintS1 in the spaceof functionings from the traditional commodity budget constraint,Y 1. Since theconsumer chooses pointA in the space of commodities, he enjoysB’s combi-nation of functionings. But all of the functionings within the constraintS1 canalso be attained by the consumer. The triangular area between the origin and theline S1 thus represents the individual’s capability set. It is the set of functioningswhich he is able to attain.

Now assume that functioning thresholds ofzC andzT must be exceeded (ormust be potentially exceeded) for one not to be considered poor by the non-welfarist approaches. Given the transformation functionsTCT andTCF , a budgetconstraintY 1 makes the individualcapableof not being poor in the functioningspace. But this does not guarantee that the individual will choose a combinationof functionings that will exceedzC andzT : this will also depend on the individ-ual’s preferences. At pointA, the functionings achieved are above the minimumfunctioning threshold fixed in each dimension. Other points within the capabilityset would also surpass the functioning thresholds: these points are shown in theshaded triangle to the northeast of pointB. Since part of the capability set allowsthe individual to be non-poor in the space of functionings, the capability approachwould also declare the individual not to be poor.

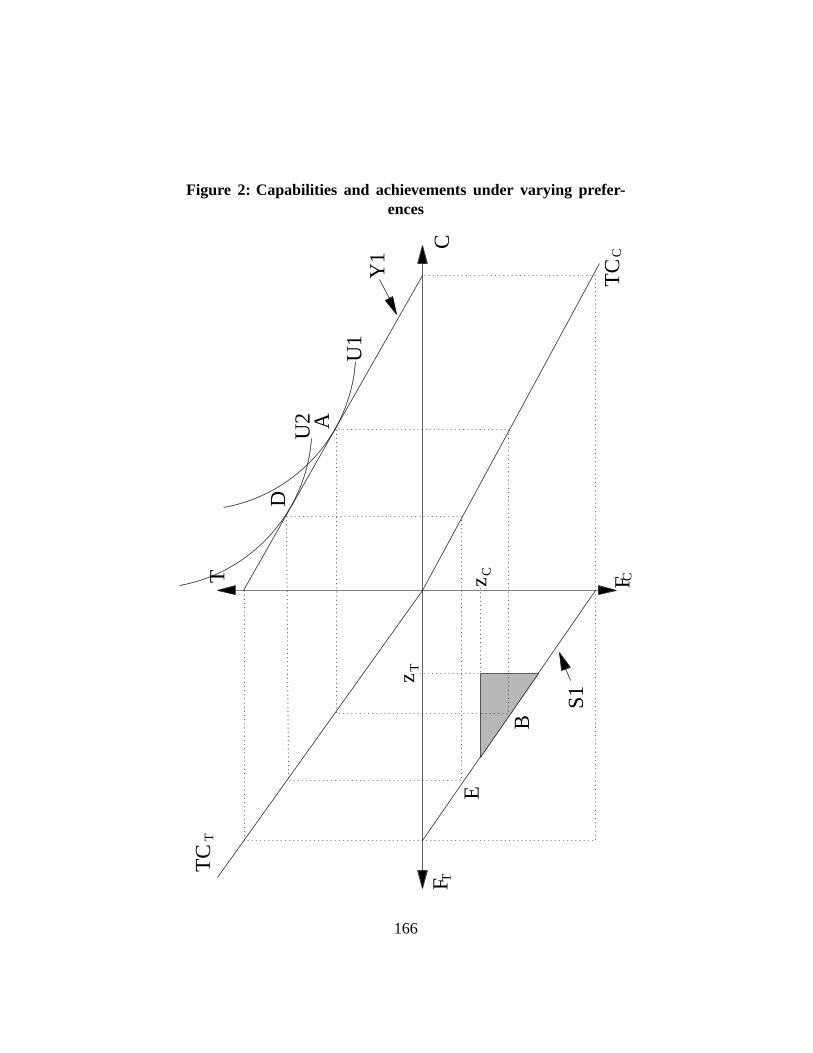

So would conclude, too, the functioning approach since the individualchoosesfunctionings abovezC andzT . Such a concordance does not always have to pre-vail, however. Consider Figure2. The commodity budget set and the Function-ing Transformation Curves have not changed, so that the capability set has notchanged either. But there has a been a shift of preferences fromU1 to U2, so thatthe individual now prefers pointD to pointA, and also prefers to consume lessclothing than before. This makes his preferences for functionings to be locatedat pointE, thus failing to exceed the minimum clothing functioningzC required.Hence, the person would be considered non poor by the capability approach, butpoor by the functioning approach. Whether an individual with preferencesU2 isreally poorer than one with preferencesU1 is debatable, of course, since the twohave exactly the same ”opportunity sets”, that is, have access to exactly the same

12

commodity and capability sets.An important message of the capability approach is that two persons with the

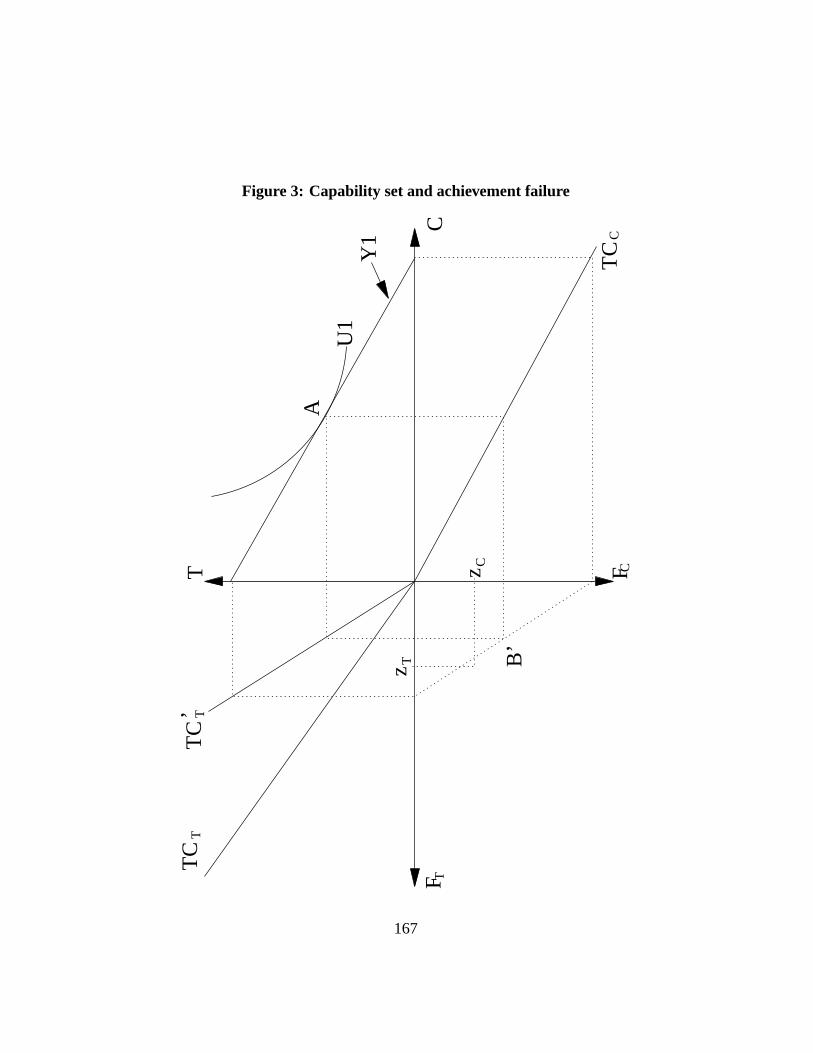

same commodity budget set can face different capability sets. This is illustratedin Figure3, where the Functioning Transformation Curve for transportation hasshifted fromTCT to TC ′

T . This may due to the presence of a handicap, whichmakes it more costly in transportation expenses to generate a given level of trans-portation functioning (disabled persons would need to expend more to go fromone place to another). This shift of theTCT curve moves the capability constraintto S1′ and thus contracts the capability set. With the handicap, there is no pointwithin the new capability set that would surpass both functioning thresholdszC

andzT . Hence, the person is deemed poor by the capability approach and (nec-essarily so) by the functioning approach. Whether the welfarist approach wouldalso declare the person to be poor would depend on whether it takes into accountthe differences in needs implied by the difference between theTCT and theTC ′

T

curves.For the welfarist approach to be reasonably consistent with the functioning

and capability approaches, it is thus essential to consider the role of transforma-tion functions such as theTC curves. If this is done, we may (in our simpleillustration at least) assess a person’s poverty status either in the commodity orin the functioning space. In other words, we may determine whether someone iscapability-poor either from observing his consumption of different goods, of fromobserving his attained functionings.

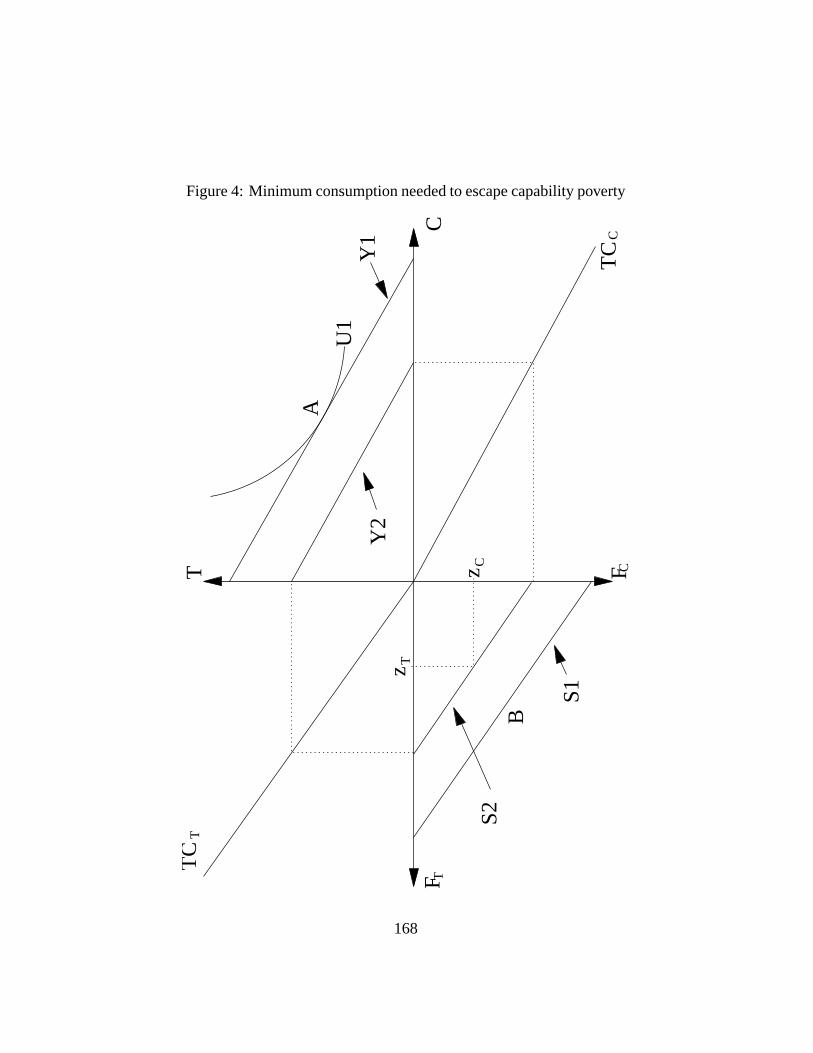

To see this, consider Figure4. Figure4 is the same as Figure1 except for theaddition of the commodity budget constraintY 2 which shows the minimum con-sumption level needed for one not to be poor according to the capability approach.According to the capability approach, the capability set must contain at least onecombination of functionings abovezC andzT , and this condition is just met by thecapability constraintS2 that is associated with the commodity budgetY 2. Hence,to know whether someone is poor according to the capability approach, we maysimply check whether his commodity budget constraint lies belowY 2.

Even if the actual commodity budget constraint lies aboveY 2, the individualmay well choose a point outside the non-poor functioning set, as we discussedabove in the context of Figure2. Clearly then, the minimum total consumptionneeded for one to be non poor according to the functioning or basic needs ap-proach generally exceeds the minimum total consumption needed for one to benon poor according to the capability approach. More problematically, this mini-mum total consumption depends in principle on the preferences of the individuals.On Figure2, for instance, we saw that the individual with preferenceU2 was con-

13

sidered poor by the functioning approach, although another individual with thesame budget and capability sets was considered non-poor by the same approach.

1.3.1 Exercises

1. Show on a figure such as Figure1 the impact of an increase in the price ofthe transportation commodity on the commodity and capability constraints.

2. On a figure such as Figure4, show the minimal commodity budget set thatensures that the person

(a) is just able to attain one of the two minimum levels of functioningszC

or zT ;

(b) chooses a combination of functionings such that one of them exceedsthe corresponding minimum level of functioningszC or zT ;

(c) is just able to attain both minimum levels of functioningszC andzT ;

(d) chooses a combination of functionings such that both exceed the cor-responding minimum level of functioningszC andzT .

(e) How do these four minimal commodity constraints compare to eachother?

1.4 Practical measurement difficulties

How are we to measure capabilities? Unless a person chooses to enact them in theform of functioning achievements, capabilities are not easily inferred. Achieve-ment of all basic functionings implies non-deprivation in the space of all capa-bilities; but a failure to achieve all basic functionings does not imply capabilitydeprivation. This makes the monitoring of functioning and basic needs an imper-fect tool for the assessment of capability deprivation. Besides, and as for basicneeds, there are clearly degrees of capabilities, some basic and some wider.

Non-welfarist (capability and basic needs) approaches to poverty measure-ment also suffer from some comparability problems. This is because they typi-cally generate multidimensional qualitative poverty criteria: their fulfilment typ-ically takes a simple dichotomic yes/no form. It is unlikely that true well-beingis such a dichotomic and discontinuous function of achievement and capabilities.Indeed, for most of the functionings assessed empirically, there are degrees ofachievement, such as for being healthy, literate, living without shame,etc... It

14

is important to take into account the varying degrees of poverty in assessing andcomparing the intensity of poverty. Besides, how should we assess adequately thedegree of poverty of someone who has the capability to achieve two functioningsout of three, but not the third? Is that person necessarily ”better off” than some-one who can achieve only one, or even none of them? Are all capabilities of equalimportance when we assess well-being?

The multidimensionality of the non-welfarist criteria also translates into greaterimplementation difficulties than for the usual proxy indicators of the welfarist ap-proach. In the welfarist approach, the size of the multidimensional budget is or-dinarily summarized by income or total consumption, which can be thought ofas a unidimensional indicator of freedom. A similar transformation into a uni-dimensional indicator is more difficult with the capability and basic needs ap-proaches. One possibility solution is to use ”efficiency-income units reflectingcommand over capabilities rather than command over goods and services” (Sen(1984, p.343), as we illustrated above when discussing Figure4. This, however,is practically difficult to do, since command over many capabilities is hard totranslate in terms of a single indicator, and since the ”budget units” are hardlycomparable across functionings such as well-nourishment, literacy, feeling self-respect, and taking part in the life of the community. On Figure4, anyone withan income belowY 2 would be judged capability-poor. But by how much doespoverty vary among these capability-poor? A natural measure would be a func-tion of the budget constraint. It is more difficult to make such measurements andcomparisons in the capability set.

Furthermore, although there are many different combinations of consump-tion and functionings that are compatible with a unidimensional money-metricpoverty threshold, the welfarist approach will generally not impose multidimen-sional thresholds. For instance, the welfarist approach will usually not require forone not to be poor that both food and non-food expenditures be larger than theirrespective food and non-food poverty lines. As indicated above, this simplifiesthe identification of the poor and the analysis of poverty.

15

2 Poverty measurement and public policy

The measurement of well-being and poverty plays a central role in the discussionof public policy and safety nets in particular. It is used, among other things, toidentify the poor and the non-poor, to design optimal poverty relief schemes, toestimate the errors of exclusion and inclusion in the set of the poor (also known asType I and Type II errors), and to assess the equity of poverty alleviation policy.How many of the poor, for instance, are excluded from safety net programmes? Isit the poorest of the poor who benefit most from public policy? Would a differentsort of poverty alleviation policy reduce deprivation further?

An important example of the central role of poverty measurement in the set-ting of public policy is the optimal selection of safety net targeting indicators. Thetheory of optimal targeting suggests that it will commonly be best to target indi-viduals on the basis of indicators that are as easily observable and as exogenousas possible, while being as correlated as possible with the true poverty status ofthe individuals. Indicators that are not readily observable by programme admin-istrators are of little practical value. Indicators that can be changed effortlesslyby individuals will be distorted by the presence of the programme, and will losetheir poverty-informative value. Whether available indicators are sufficiently cor-related with the deprivation of individuals in a population is given by a povertyprofile. The value of this profile will naturally be highly dependent on the partic-ular assumptions and the approach used to measure well-being and poverty.

Estimation of the errors of inclusion and exclusion of the poor is also a prod-uct of poverty profiling and measurement. These errors are central in the trade-offinvolved in choosing a wide coverage of the population – at relatively low ad-ministrative and efficiency costs – and a narrower coverage – with more generousforms of support for the fewer beneficiaries. However, as Van de Walle (1998)puts it, a narrower coverage of the population, with presumably smaller errors ofinclusion of the non-poor, does not inevitably lead to a more equitable treatmentof the poor:

Concentrating solely on errors of leakage to the non-poor can lead topolicies which have weak coverage of the poor (Van de Walle (1998,p.366)).

The terms of this trade-off are again given by a poverty assessment exercise.Another lesson of optimal redistribution theory is that it is ordinarily better to

transfer resources from groups with a high level of average well-being to those

16

with a lower one. What matters even more, however, is the distribution of well-being within each of the groups. For instance, equalising mean well-being acrossgroups does not usually eliminate poverty since there generally exist within-groupinequalities. Even within the richer group, for instance, there normally will befound some deprived individuals, whom a rich-to-poor cross-group redistributiveprocess would clearly not take out of poverty. The within- and between-groupdistribution of well-being that is required for devising an optimal redistributivescheme can be again revealed by a comprehensive poverty profile.

2.1 Welfarist and non-welfarist policy implications

The distinction between the welfarist and non-welfarist approaches to povertymeasurement often matters (implicitly or explicitly) for the assessment and thedesign of public policy. As described above, a welfarist approach holds that in-dividuals are the best judges of their own well-being. It would thus in principleavoid making appraisals of well-being that conflict with the poor’s views of theirown situation. A typical example of a welfarist public policy would be the provi-sion of adequate income-generating opportunities, leaving individuals decide andreveal whether these opportunities are utility maximising, keeping in mind theother non-income-generating opportunities that are open to them.

A non-welfarist policy analyst would argue, however, that raising income op-portunities is not necessarily the best policy option. This is partly because indi-viduals are not necessarily best left with their own resolutions, at least in an in-tertemporal setting, for their educational and environmental choices for instance.In other words, the poor’s short-run preoccupations may harm their long-termself-interest. For example, individuals may choose not to attend skill-enhancingprogrammes because they appear overly time costly in the short-run, and becausethey are not sufficiently convinced or aware of their long-term benefits.

Hence, if left to themselves, the poor will not necessarily spend their incomeincrease on functionings that basic-needs analysts would normally consider a pri-ority, such as good nutrition and health. Thus, fulfilling ”basic needs” cannotbe satisfied only by the generation of private income, but may require significantamounts of targeted and in-kind public expenditures on areas such as education,public health and the environment. This would be so even if the poor did notpresently believe that these areas were deserving of public expenditures. Further-more, social cohesion concerns are arguably not well addressed by the maximiza-tion of private utility, and raising income opportunities will not fundamentallysolve problems caused by adverse intra-household distributions of well-being, for

17

instance.An objection to the basic needs approach is that it is clearly paternalistic since

it supposes that it is in the absolute interests of all to meet a set of often arbi-trarily specified needs. Indeed, as emphasised above, non-welfarist approachesin general may use criteria for identifying and helping the poor that may con-flict with the poor’s views and utility maximizing options. For poverty alleviationpurposes, this could go as far as enforced enrolment in community developmentprogrammes. This would not only conflict with the preferences of the poor, butwould also clearly undermine their freedom to choose. Freedom to choose may,however, be one of the basic capabilities which contribute fundamentally to well-being.

A further example of the possible tension between welfarist and non-welfaristapproaches to public policy comes from optimal taxation theory, which is linkedto optimal poverty alleviation theory. In the tradition of classical microeconomics,which values leisure in the production and labour market decisions of individu-als, pure welfarists would incorporate the utility of leisure in the overall utilityfunction of workers, poor and non-poor alike. In its support to the poor, the gov-ernment would then take care of minimizing the distortion of their labor/leisurechoices so as not to create overly high ”deadweight losses”. Classical optimal tax-ation theory then shows that giving a positive weight to such things as labor/leisuredistortions suggests a generally lower benefit reduction rates on the income of thepoor than otherwise. Taking into account such abstract things is less typical ofthe basic needs and functioning approaches. Such approaches would, therefore,usually be less reluctant to target programme benefits more sharply on the poor,and exact steeper benefit reduction rates as income or well-being increases.

Relative to the pure welfarist approach, non-welfarist approaches are also typ-ically less reluctant to impose utility-decreasing (or ”workfare”) costs as side ef-fects of participation in poverty alleviation schemes. These side effects are in factoften observed in practice. For instance, it is well-known that income supportprogrammes frequently impose participation costs on benefit claimants. Theseare typically non-monetary costs. Such costs can be both physical and psycholog-ical: providing manual labor, spending energy, spending time away from home,sacrificing leisure and home production, finding information about application andeligibility conditions, corresponding and dealing with the benefit agency, queuing,keeping appointments, complying with application conditions, revealing personalinformation, feeling ”stigma” or a sense of guilt,etc...

Although non-monetary, these costs have a clear impact on participants’ netutility from participating in the programmes. When they are negatively correlated

18

with unobserved (or difficult to observe) entitlement indicators, they can provideself-selection mechanisms that enhance the efficiency of poverty alleviation pro-grammes, for welfarists and non-welfarists alike. One unfortunate effect of thesecosts is, however, that many truly-entitled and truly deserving individuals mayshy away from the programmes because of the costs they impose. Although pro-gramme participation could raise their income and consumption above a money-metric poverty line, some individuals will prefer not to participate, revealing thatthey find apparent poverty utility dominant over programme participation. Wel-farists would in principle take these costs into account when assessing the meritsof the programmes. Non-welfarists would typically not do so, and would thereforejudge the programmes more favorably.

The width of the definition of functionings is clearly also important for theassessment and the design of public policy. For instance, public spending oneducation is often promoted on the basis of its impact on productivity and growth.But education can also be seen as a means to attain the functioning of literacy andparticipation in the community. This provides an additional strong support forpublic expenditures on education. Analogous arguments also apply, for instance,to public expenditures on health, transportation, and the environment.

19

Part II

Measuring poverty and equity

20

3 Notation

In what follows in this book, we will denote living standards by the variabley. The indices we will use will sometimes require these living standards to bestrictly positive, and, for expositional simplicity, we will assume that this is al-ways the case. Strictly positive values ofy are required, for instance, for theWatts poverty index and for many of the decomposable inequality indices. It isof course reasonable to expect indicators of living standards such as monthly oryearly consumption to be strictly positive. This assumption is less natural for otherindicators, such as income, for which capital losses or retrospective tax paymentscan generate negative values.

Let p = F (y) be the proportion of individuals in the population who enjoya level of income that is less than or equal toy. F (y) is called the cumulativedistribution function (cdf) of the distribution of income; it is non-decreasing iny,and varies between 0 and 1, withF (0) = 0 andF (∞) = 1. For expositionalsimplicity, we may assume thatF (y) is continuously differentiable and strictlyincreasing iny (a reasonable assumption for large-population distributions of in-come). The density function, which is the first-order derivative of thecdf, is de-noted asf(y) = F ′(y) and is strictly positive sinceF (y) is assumed to be strictlyincreasing iny.

3.1 Continuous distributions

A useful tool throughout the analysis will be the concept of “quantiles”. Quantileswill help simplify greatly the exposition and the computation of several distribu-tive measures. They will also sometimes serve as direct tools to analyze and com-pare distributions of living standards (to check first-order dominance in the dualapproach for instance). The quantileQ(p) is defined asF (Q(p)) = p, or using theinverse distribution function, asQ(p) = F−1(p). Q(p) is thus the living standardlevel below which we find a proportionp of the population. Alternatively, it is theliving standard of that individual whose rank – or percentile – in the distributionis p. A proportionp of the population is poorer than he is; a proportion1 − p isricher than him.

This is illustrated in Figure14. The horizontal axis shows percentilesp of thepopulation. The quantilesQ(p) that correspond to differentp values are shownon the vertical axis. The larger the rankp, the higher the corresponding livingstandardQ(p). Alternatively, living standardsy appear on the vertical axis ofFigure14, and the proportion of individuals whose income is below or equal to

21

thosey are shown on the horizontal axis. At the maximum income level,ymax,that proportionF (ymax) equals 1. The median is given byQ(0.5), which is theliving standard which splits the distribution exactly in two halves.

We will define most of the distributive measures (indices and curves) in termsof integrals over a range of percentiles. This is a familiar procedure in the contextof continuous distributions. We will see below why this is also generally validin the context of discrete distributions, even though the use of summation signsis more familiar in that context. Using integrals will make the definitions andthe exposition simpler, and will help focus on what matters more, namely, theinterpretation and the use of the various indices and curves that we will consider.

The most common summary index of a distribution is its mean. Using integralsand quantiles, it is defined as:

µ =∫ 1

0Q(p)dp. (1)

µ is therefore simply the area underneath the quantile curve. This corresponds tothe grey area shown on Figure14. Since the horizontal axis varies uniformly from0 to 1,µ is also the average height of the quantile curveQ(p), and this is givenby µ on the vertical axis. As for most distributions of income, the one shownon Figure14 is skewed to the left, which gives rise to a meanµ that exceeds themedianQ(p). Said differently, the proportion of individuals underneath the mean,F (µ), exceeds one half.

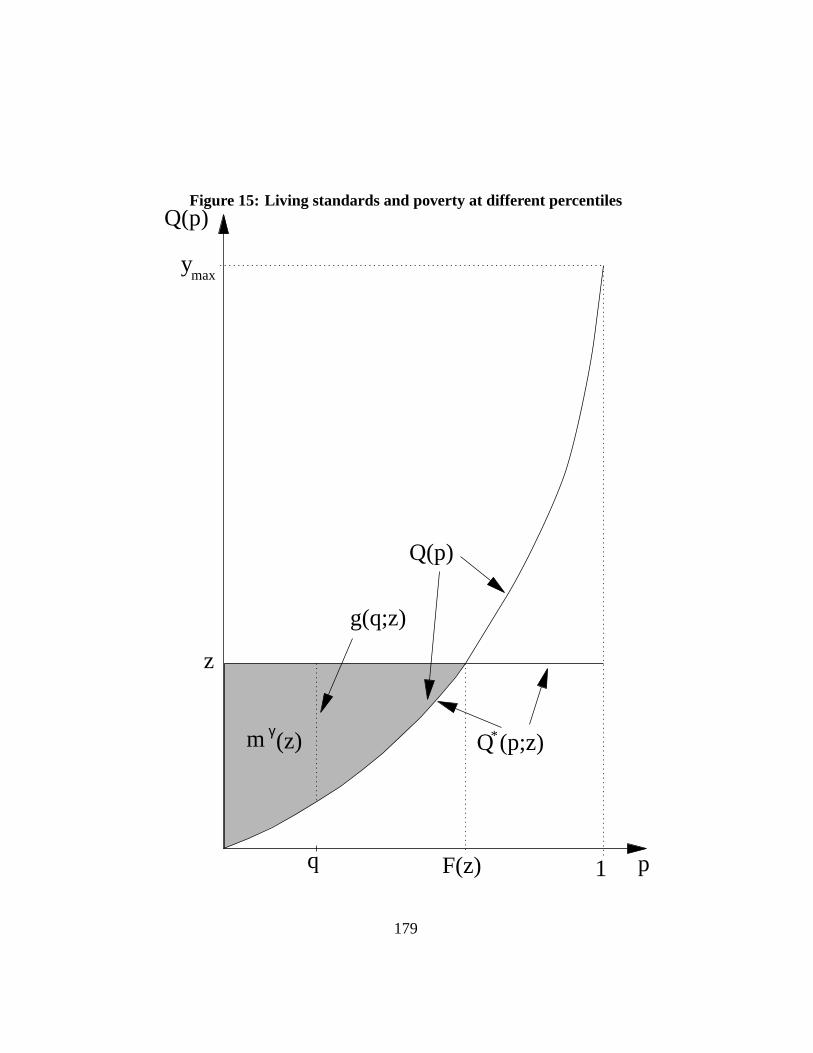

For poverty comparisons, we will also need the concept of quantiles censoredat a poverty linez. These are denoted byQ∗(p; z) and defined as:

Q∗(p; z) = min(Q(p), z). (2)

Censored quantiles are therefore just the incomesQ(p) for those in poverty(below z) andz for those whose income exceeds the poverty line. This is illus-trated on Figure15, which is similar to Figure14. QuantilesQ(p) and censoredquantilesQ∗(p; z) are identical up top = F (z), or up toQ(p) = z. After thispoint, censored quantiles equalz and diverge from incomeQ(p).

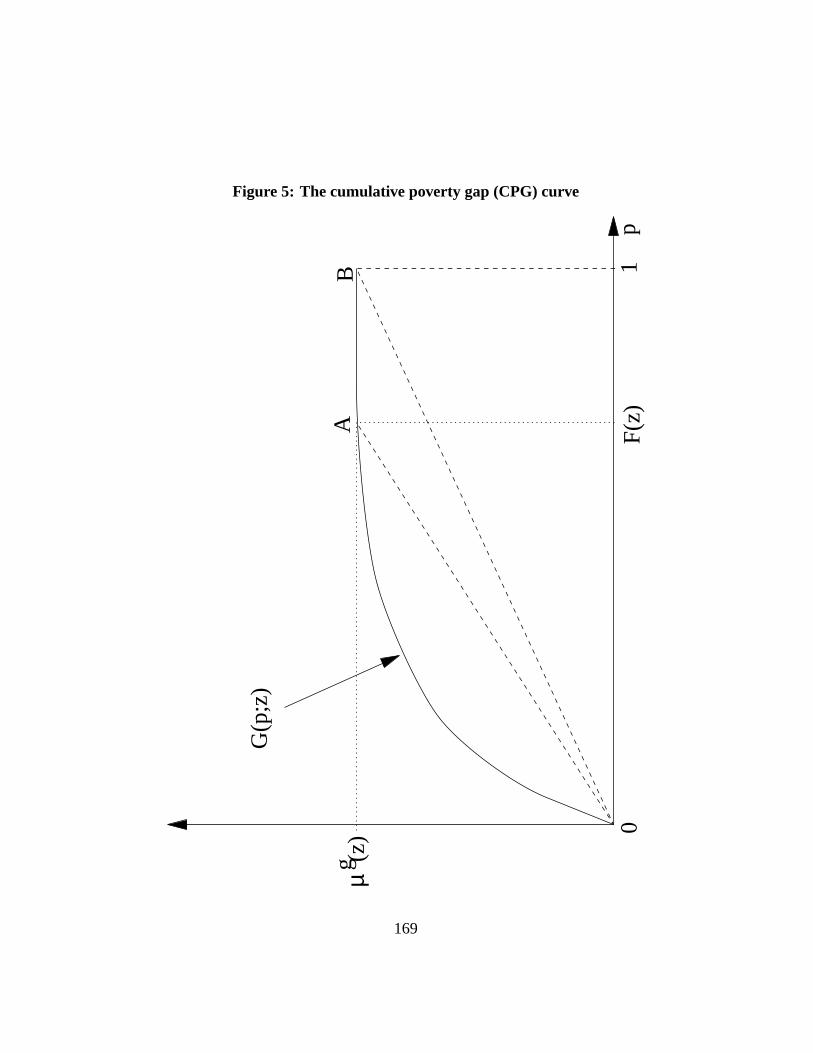

Censoring income atz helps focus attention on poverty, since the precisevalue of those living standards that exceedz is irrelevant for poverty analysisand poverty comparisons (at least so long as we considerabsolutepoverty; moreon this later). The mean of the censored quantiles is denoted asµ∗(z):

22

µ∗(z) =∫ 1

0Q∗(p; z)dp. (3)

This is again the area underneath the curve of censored incomesQ∗(p; z). Thepoverty gap at percentilep, g(p; z), is the difference between the poverty line andthe censored quantile atp, or equivalently the shortfall (when applicable) of livingstandardQ(p) from the poverty line:

g(p; z) = z −Q∗(p; z) = max(z −Q(p), 0). (4)

When income atp exceeds the poverty line, the poverty gap equals zero. A short-fall g(q; z) at rankq is shown on Figure15 by the distance betweenz andQ(q).The larger one’s rankp in the distribution – the higher up in the distribution ofincome – the lower the poverty gapg(p; z). The proportion of individuals with apositive poverty gap is given byF (z) (see the Figure). The average poverty gapthen equalsµg(z):

µg(z) =∫ 1

0g(p; z)dp. (5)

µg(z) is the size of the area in grey shown in Figure15.

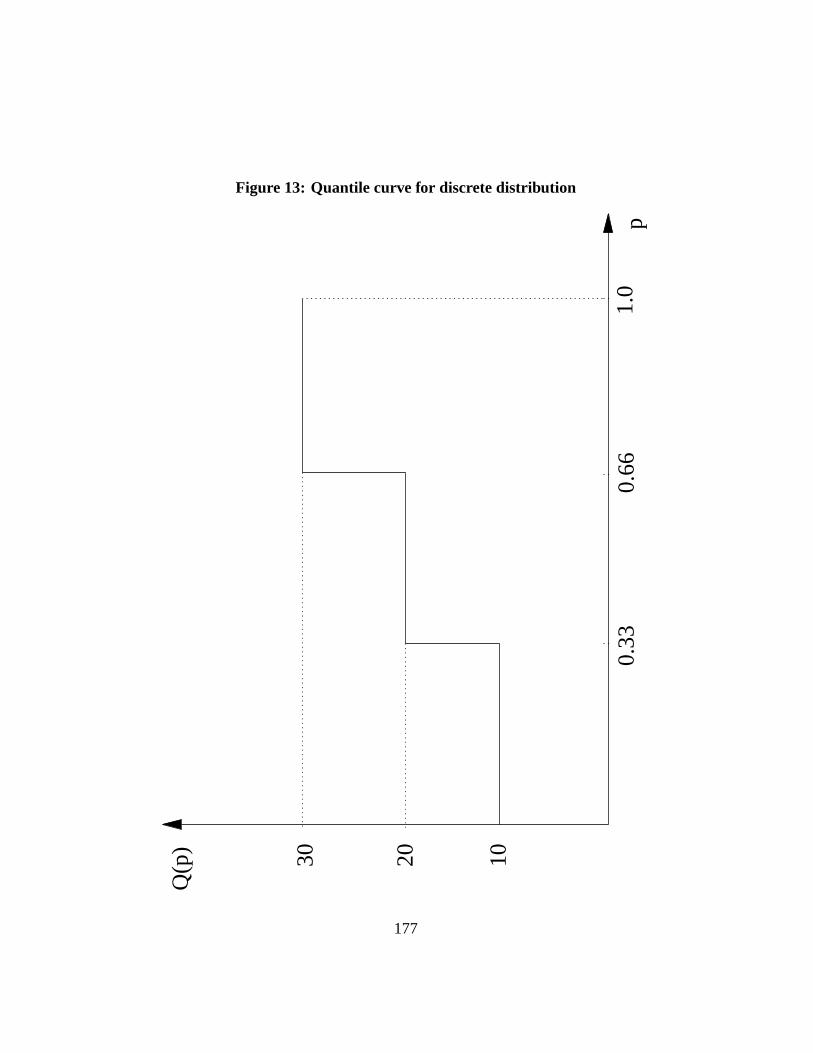

3.2 Discrete distributions

To see how to rewrite the above definitions using summation signs and discretedistributions, we need a little more notation. Say that we are interested in adistribution of n living standards. We first order then observations ofyi inincreasing values ofy, such thaty1 ≤ y2 ≤ y3 ≤ ... ≤ yn−1 ≤ yn. Wethen definen discrete quantiles of living standards asQ(pi) = yi, for pi =1/n, 2/n, 3/n, ..., (n− 1)/n, 1.

This is illustrated in Table?? wheren = 3 and where the incomes in increas-ing values are 10, 20 and 30. Figure13 graphs those quantiles as a function ofp.

The formulae for discrete distributions are then computed in practice by re-placing the integral sign in the continuous case by a summation sign, by summingacross all observed sample quantiles, and by dividing the sum by the number ofobservationsn. Thus, the meanµ of a discrete distribution can be expressed as:

23

µ =1

n

n∑

i=1

Q(pi). (6)

As indicated by equation (1), the mean of the discrete distribution of Table??,which is 20, is simply the integral of the quantile curve shown on Figure13. Inother words, it is the sum of the area of the three boxes each of length 1/3 that canbe found underneath the filled curve.

Discrete distributions are in fact what is always observed in samples and inreal-life populations of households or individuals, however large those samplesor populations may be. For clarity, we will mention from time to time how in-dices and curves can be estimated using the more familiar summation signs. Formore information, you can also consultDAD’s User Guidewhere the estimationformulae shown use summation signs and thus apply to discrete distributions.

24

4 The measurement of inequality and social welfare

4.1 Lorenz curves

The Lorenz curve has been for the several decades the most popular graphi-cal tool for visualizing and comparing the inequality in income. As we will see,it provides complete information on the whole distribution of income as a pro-portion of the mean. It therefore gives a more comprehensive description of therelative standards of living than any one of the traditional summary statistics ofdispersion can give, and it is also a better starting point when looking at the in-equality of income than the computation of the many inequality indices that havebeen proposed. As we will see, its popularity also comes from its use as a deviceto order distributions in terms of inequality, in such a way as to check whether theordering is necessarily the same for (and is therefore robust over) all inequalityindices within a large class of inequality indices. The Lorenz curve is defined asfollows:

L(p) =1

µ

∫ p

0Q(q)dq. (7)

The numerator shows the absolute contribution toper capita income of thebottomp proportion (the100p% poorest) of the population.µ is average income.L(p) thus indicates the cumulative percentage of total income held by a cumu-lative proportionp of the population, when individuals are ordered in increasingvalues of their income. For instance, ifL(0.5) = 0.3, then we know that the 50%poorest individuals hold 30% of the total income in the population.

A discrete formulation of the Lorenz curve is easily provided. Recall thatdiscrete incomeyi are ordered such thaty1 ≤ y2 ≤ ... ≤ yn, with percentilespi = i/n, for i = 1, ..., n. Fori = 1, ...n, the discrete Lorenz curve is then definedas:

L(pi = i/n) =1

nµ

i∑

j=1

Q (pj) . (8)

If needed, other values ofL(p) in (8) can be obtained by interpolation.The Lorenz curve has several interesting properties. It ranges from 0 atp =

0 to 1 atp = 1, since a proportionp = 1 of the population must also hold a

25

proportionL(p = 1) = 1 of the aggregate income. It is increasing asp increases,since more and more incomes are then added up. This is also seen by the fact thatthe derivative ofL(p) equalsQ(p)/µ,

dL(p)

dp=

Q(p)

µ. (9)

This is positive if income are stricly positive, as we have assumed. Hence byobserving the slope of the Lorenz curve at a particular value ofp, we also knowthep-quantile relative to the mean, or in other words, the standard of living of anindividual at rankp as a proportion of the overall mean standard of living. Theslope ofL(p) thus portrays the whole distribution of mean-normalised income.The Lorenz curve is also convex inp, since asp increases, the new incomes thatare being added up are greater than those that have already been counted. Math-ematically, a curve is convex when its second derivative is positive, and the morepositive that second derivative, the more convex is the curve. We can show thatthe second-order derivative of the Lorenz curve equals:

d2L(p)

dp2=

1

f(Q(p))(10)

which is positive. The larger the densityf(Q(p)) of income at a quantileQ(p),the more convex the Lorenx curve atL(p).

Some measures of central tendency can also be identified by a look at theLorenz curve. In particular, the median (as a proportion of the mean) is givenby Q(0.5)/µ, and thus by the slope of the Lorenz curve atp = 0.5. Since manydistributions of incomes are skewed to the right, the mean exceeds the medianand Q(p = 0.5)/µ will typically be less than one. The mean living standardin the population is found at the percentile at which the slope ofL(p) equals 1,that is, whereQ(p) = µ. Again, this percentile will often be larger than 0.5,namely, where the median living standard is located. The percentile of the mode(or modes) is whereL(p) is least convex, since by equation (10) this is where thedensityF (Q(p)) is highest.

If all had the same income, the Lorenz curve would equalp: population sharesand shares of total income would be identical. An important graphical element ofa Lorenz curve is thus its distance,p − L(p), from the line of perfect equality inincome.

Simple summary measures of inequality can already be obtained from thegraph of the Lorenz curve. The share in total income of the bottomp propor-tion of the population is given byL(p); the greater that share, the more equal is

26

the distribution of income. Analogously, the share in total income of the richestpproportion of the population is given by1−L(p); the greater that share, the moreunequal is the distribution of income. These two simple indices of inequality areoften used in the literature. An interesting but less well-known index of inequalityis given by the minimum (hypothetical) proportion of total income that the gov-ernment would need to reallocate across the population to achieve perfect equalityin income; this proportion is given by the maximum value ofp − L(p), which isattained where the slope ofL(p) is 1 (i.e., atL(p = F (µ))). It is therefore equalto F (µ) − LF (F (µ)) and is also called the Schutz coefficient. We will revert tothat coefficient later when we discuss relative poverty.

Mean-preserving equalising transfers of income are often call Pigou-Daltontransfers; in money-metric terms, they involve a marginal transfer of $1, say, froma richer to a poorer person, and they keep the mean of income constant. Allindices of inequality which do not increase (and sometimes fall) following anysuch equalising transfers are said to obey the Pigou-Dalton principle of transfers.These equalising transfers also have the consequence of moving the Lorenz curveunambiguously closer to the line of equality. Let the Lorenz curveLB(p) of adistributionB be everywhere above the Lorenz curveLA(p). We can thus thinkof B as having been obtained fromA through a series of equalising transfers,applied to the distributionA. Hence, inequality indices which obey the principleof transfers will unambiguously indicate more inequality inA than inB. We willcome back to this important link in the Section10on making robust comparisonsof inequality.

4.2 Gini indices

Compared to perfect equality, inequality thus removes a proportionp − L(p) oftotal income from the bottom100 · p% of the population. If we aggregate that“deficit” p − L(p) between population shares,p, and shares in income,L(p),across all values ofp between 0 and 1, we get half the well-known Gini index:

Gini index of inequality2

=∫ 1

0(p− L(p)) dp. (11)

The Gini index thus assumes that all “share deficits” acrossp are equally impor-tant. It thus computes the average distance between cumulated population sharesand cumulated shares in income. One can, however, also think of other weights toaggreate the distancep − L(p). The class oflinear inequality measures is given

27

by the use of rank- or percentile-dependent weights, sayκ(p), applied to that dis-tance. A popular one-parameter functional specification for such weights is givenby

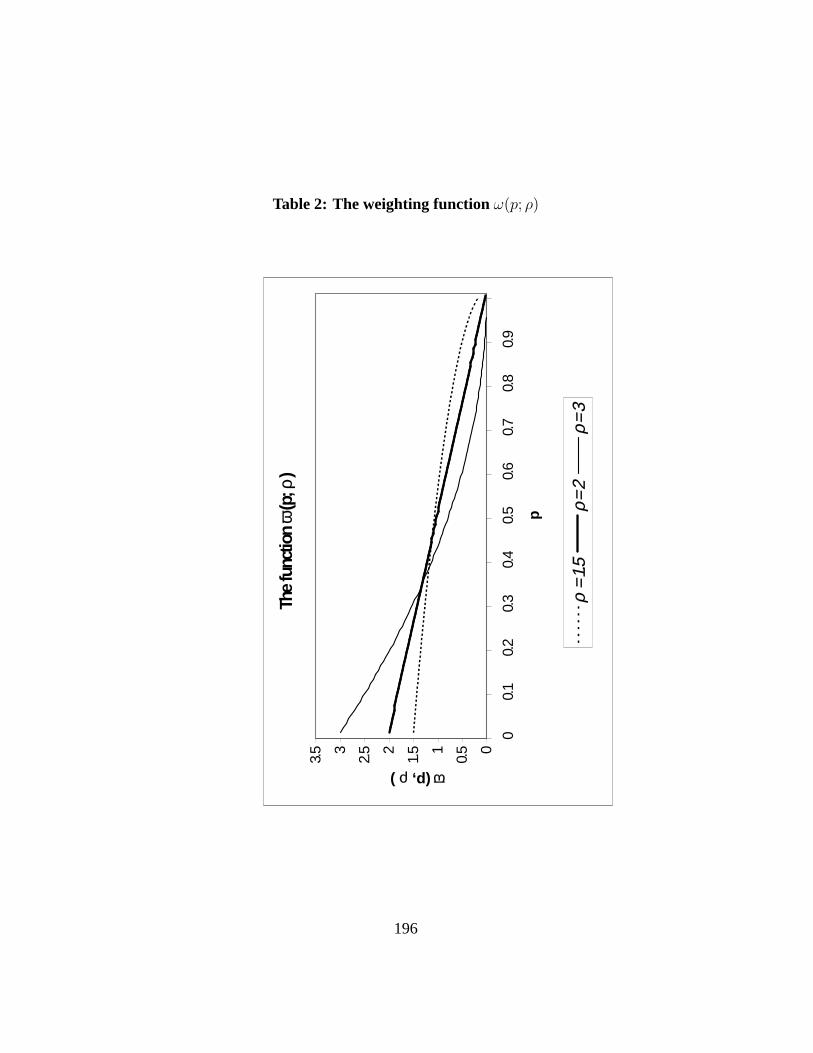

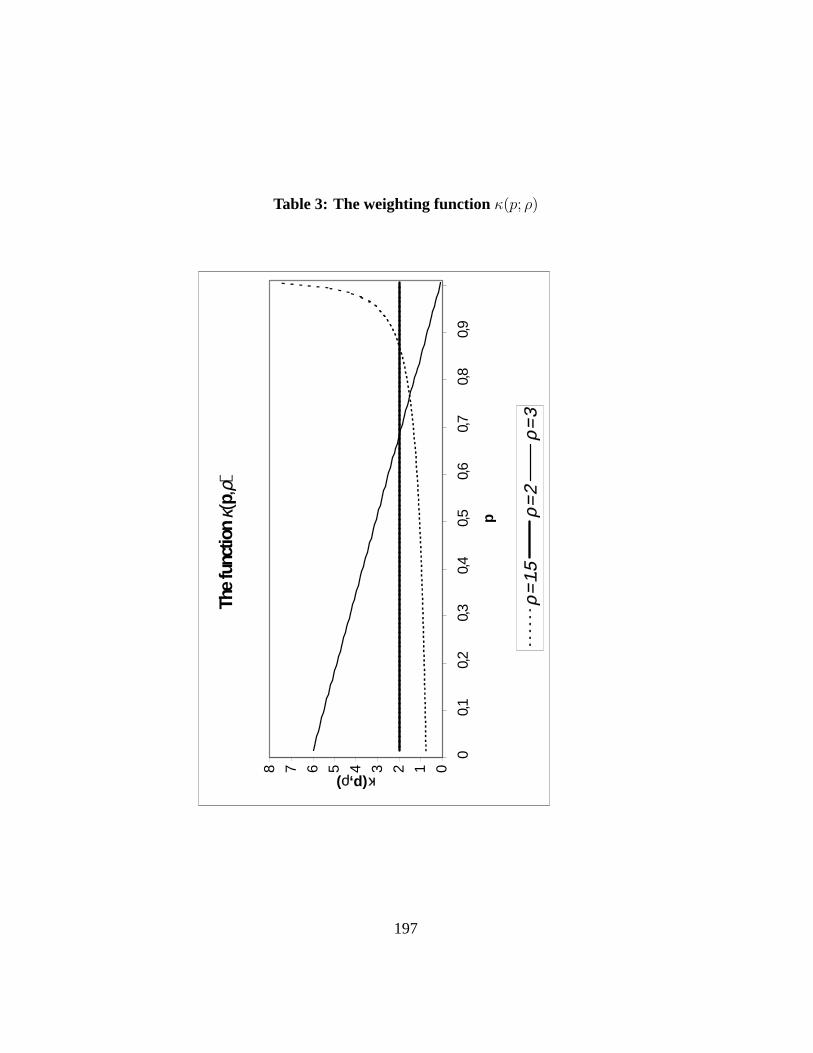

κ(p; ρ) = ρ(ρ− 1)(1− p)(ρ−2) (12)

which depends on the value of a single “ethical” parameterρ which must begreater than 1 for the weightsκ(p; ρ) to be positive everywhere. The shape ofκ(p; ρ) is shown on Figure3 for three different values ofρ. The larger the valueof ρ, the larger the value ofκ(p; ρ) for smallp.

Using (12) gives what is called the class of S-Gini (or “Single-Parameter”Gini) inequality indices:

I(ρ) =∫ 1

0(p− L(p))κ(p; ρ)dp. (13)

Note that whenρ = 2, we have thatI(2) is the standard Gini index. This isbecauseκ(p; ρ = 2) ≡ 2, which then gives equal weight to all distancesp−L(p).When1 < ρ < 2, relatively more weight is given to the distances occurring atlarger values ofp, as shown by Figure3. Conversely, whenρ > 2, relatively moreweight is given to the distances occurring at lower values ofp. Changingρ thuschanges the “ethical” concern which we feel for the “shares deficits” at variouscumulative proportions of the population.

Let ω(p; ρ) be defined as follows:

ω(p; ρ) =∫ 1

pk(q, ρ)dq = ρ(1− p)ρ−1. (14)

Note thatω(p; ρ) > 0 and that∂ω(p; ρ)/∂p < 0 whenρ > 1. The shape ofω(p; ρ)is shown on Figure2 for ρ equal to 1.5, 2 and 3. Since

∫ 10 ω(p; ρ)dp = 1 for any

value ofρ, the area under each of the three curves on Figure2 equals 1 too.The functionsκ(p; ρ) andω(p; ρ) can be given an interpretation in terms of

densities of the poor, densities which will be useful to interpret some of the rela-tionships to be described below. Assume thatr individuals are randomly selectedfrom the population. The probability that the income ofall of theser individualswill exceedQ(p) is given by[1− F (Q(p))]r, and thus the probability of finding aliving standard belowQ(p) in such samples is1− [1− F (Q(p))]r = 1− [1− p]r.The density of the lowest rank of income in a sample ofr randomly selected in-come is the derivative of that probability with respect top, which is

r (1− p)r−1 . (15)

28

This helps us interpret the weightsκ(p; ρ) and ω(p; ρ). By equation (12),κ(p; ρ) is ρ times the density of the lowest living standard in a sample ofρ − 1randomly selected individuals; analogously, by equation (14), ω(p; ρ) is the den-sity of the lowest living standard in a sample ofρ randomly selected individuals.

Using (14) and by integration by parts of equation (13), we can then show that:

I(ρ) =1

µ

∫ 1

0(µ−Q(p))ω(p; ρ)dp. (16)

This says that the deviation of income from the mean is weighted by weightswhich fall with the ranks of individuals in the population. Since, in equation (16),I(ρ) is a (piece-wise) linear function of the incomeQ(p), it is a member of theclass of linear inequality measures, a feature which will prove useful in measuringprogressivity and vertical equity later.

We might be interested in determining the impact of some inequality-changingprocess on the inequality indices of type (16). One such process that can be han-dled nicely spreads income away from the mean by a proportional factorλ, andthus corresponds to some form of bi-polarization of incomes away from the mean(loosely speaking). This is equivalent to a process that adds(λ− 1) (Q(p) − µ)to Q(p), since

µ− (Q(p) + (λ− 1) (Q(p)− µ)) = λ (µ−Q(p)) . (17)

As can be checked from equation (16), this changesI(ρ) proportionally byλ,which also says that the elasticity ofI(ρ) with respect toλ, whenλ equals 1initially, is equal to 1 whatever the value of the parameterρ.

This bi-polarization away from the mean is also equivalent to a process thatincreases the distancep − L(p) by a factorλ. That this gives the same changein I(ρ) can be checked from equation (13). This bi-polarization process thusincreases the ”deficit”p − L(p) between population sharesp and income sharesL(p) by a constant factorλ across population shares or ranks. We will see laterhow this distance-increasing process leads to a nice illustration of the possibleimpact of changes in inequality on poverty.

As shown on Figure2, the larger the value ofρ, the greater the weight givento the deviation of low incomes from the mean. Whenρ becomes very large, theindex I(ρ) equals the proportional deviation from the mean of the lowest livingstandard. Whenρ = 1, the same weightω(p; ρ = 1) ≡ 1 is given to all devi-ations from the mean, which then makes the inequality indexI(ρ = 1) always

29

equal to 0, regardless of the distribution of income under consideration. Hence,ρ is a parameter of inequality aversion that determines our ethical concern for thedeviation of quantiles from the mean at various ranks in the population. In thissense, it is analogous to the parameterε of relative inequality aversion which wewill discuss below in the context of the Atkinson indices. For the standard Giniindex of inequality, we have thatρ = 2 and thus thatω(p; ρ = 2) = 2 · (1 − p);hence in assessing the standard Gini, the weight on the deviation of one’s livingstandard from the mean decreases linearly with one’s rank in the distribution ofincome. In a discrete formulation, the weightsω(p; ρ) take the form of:

ω(pi; ρ) =(n− i + 1)ρ − (n− i)ρ

nρ. (18)

The S-Gini indices of inequality have nice properties. First, they are graphi-cally easily interpreted as a weighted area underneath the Lorenz curve. Second,they range between 0 (when all incomes are equal to the mean or when the ethicalparameterρ is set to 1) and 1 (when incomes are concentrated in the hands of onlyone individual, or whenρ is large and the lowest living standard is close to 0).Since the Lorenz curve moves towardsp when a Pigou-Dalton equalising trans-fer is exerted, the value of the S-Gini indices also decreases with such transfers.Finally, the S-Gini indices can be shown to be equal to the following covarianceformula:

I(ρ) =−cov

(Q(p), ρ (1− p)(ρ−1)

)

µ(19)

which makes their computation simple using common spreadsheet or statisticalsoftwares. The traditional Gini is then simply:

I(ρ = 2) =2 cov(Q(p), p)

µ(20)

which is just a proportion of the covariance between incomes and their ranks.A further useful interpretive property of the standard Gini index is that it equals

half the mean-normalised average distance between all incomes:

I(ρ = 2) =

∫ 10

∫ 10 |Q(p)−Q(q)|dpdq

2 µ. (21)

30

Thus, if we find that the Gini index of a distribution of income equals 0.4, then weknow that the average distance between the incomes of that distribution is of theorder of 80% of the mean.

A final interesting interpretation of the Gini index is in terms of average rel-ative deprivation, which has been linked in the sociological and psychologicalliterature to subjective well-being, social protest and political unrest. For this, itis usual to quote from the classic work of Runciman (1966), who defines relativedeprivation as follows:

The magnitude of a relative deprivation is the extent of the differencebetween the desired situation and that of the person desiring it (as hesees it). (p.10)

Sen (1973), Yitzhaki(1979) and Hey and Lambert(1980) follow Runciman’slead to propose for each individual an indicator of relative deprivation which mea-sures the distance between his income and the income of all those relative to whomhe feels deprived. Thus, let the relative deprivation of an individual with incomeQ(p), when comparing himself to another individual with incomeQ(q), be givenby:

δ(p, q) =

0, if Q(p) ≥ Q(q)Q(q)−Q(p), if Q(p) < Q(q)

. (22)

The expected relative deprivation of an individual at rankp is thenδ(p):

δ(p) =∫ 1

0δ(p, q)dq (23)

which, we can show, can be computed asδ(p) = µ(1− L(p))−Q(p)(1− p). Aswe did for the “shares deficits” above, we can aggregate the relative deprivationat every percentilep by applying the weightsκ(p; ρ). We can show that this givesthe S-Gini index of inequality:

I(ρ) =1

ρ µ

∫ 1

0δ(p)κ(p; ρ)dp. (24)

Hence, the S-Gini indices are also an indicator of the average relative deprivationfelt in a population. By equations (12), (15) and (24), they equal the expectedrelative deprivation of the poorest individual in a sample ofρ − 1 randomly se-lected individuals. The greater the value ofρ, the more important is the relativedeprivation of the poorer in computingI(ρ).

31

4.3 Social welfare

We now introduce the concept of a social welfare function. Unlike the conceptof relative inequality, which considers incomes relative to the mean, the conceptof social welfare will allow us to measure and compare theabsoluteincomesof populations. We will see, however, that under some popular conditions onthe shape of social welfare functions, the measurement of inequality and socialwelfare can be nicely linked and integrated, and that the tools used for the twoconcepts are then similar.

The social welfare functions we will consider will take the form of:

W =∫ 1

0U(Q(p))ω(p)dp (25)

where for expositional simplicity we will restrictω(p) to be of the special formω(p; ρ) defined by equation (14). U(Q(p)) is a “utility function” of incomeQ(p).Social welfare is then the expected utility of the poorest individual in a sample of(ρ− 1) individuals.

The first requirement that we wish to impose on the form ofW is that it behomothetic. Homotheticity ofW is analogous to the requirement on consumerutility functions that expenditure shares of the different consumption goods beconstant as income increases, or the requirement on production functions thatthe ratio of the marginal products of inputs stays constant when all inputs aredoubled. For social welfare measurement, homotheticity implies that the ratio ofthe marginal social utilities of any two individuals in a population stays the sameeven when all incomes are doubled or halved1. For (25) to be homothetic, weneedU(Q(p)) to take the popular form ofU(Q(p); ε), where

U(Q(p); ε) =

Q(p)1−ε

(1−ε), when ε 6= 1

ln Q(p), when ε = 1. (26)

Hence,W in equation (25) will depend on the parametersρ and onε, and we willdenote this asW (ρ, ε).

Homotheticity of a social welfare function has an important advantage: thesocial welfare function can then be used to measure relative inequality, the mostcommon concept of inequality in the literature on the distribution of income. Tosee how this can be done, defineξ(ρ, ε) as the equally distributed living standardthat is equivalent, in terms of social welfare, to the actual distribution of income

1The marginal social utility of a living standardQ(p) is given by∂W/∂Q(p) = W (1).

32

(we will refer toξ as the EDE living standard).ξ(ρ, ε) is then implicitly definedas:

∫ 1

0U (ξ(ρ, ε); ε) ω(p; ρ) dp =

∫ 1

0U(Q(p); ε) ω(p; ρ) dp. (27)

Since∫ 10 ω(p; ρ)dp = 1, ξ(ρ, ε) is such that:

U (ξ(ρ, ε); ε) =∫ 1

0U(Q(p); ε)ω(p; ρ)dp (28)

or, alternatively:

ξ(ρ, ε) = U−1ε

(∫ 1

0Uε(Q(p))ω(p; ρ)dp

)= U−1

ε (W (ρ, ε)) (29)

whereU−1ε (·) is the inverse utility function:

U−1ε (x) =

(1− ε)s

11−ε , when ε 6= 1,

exp (x) , when ε = 1,. (30)

The index of inequalityI corresponding to the social welfare functionW is thendefined as the distance between the EDE living standard and mean income, as aproportion of mean income:

I =µ− ξ

µ= 1− ξ

µ. (31)

When using the specific formsW (ρ, ε) andξ(ρ, ε), this givesI(ρ, ε).Clearly, then, the EDE living standard is a simple function of average living

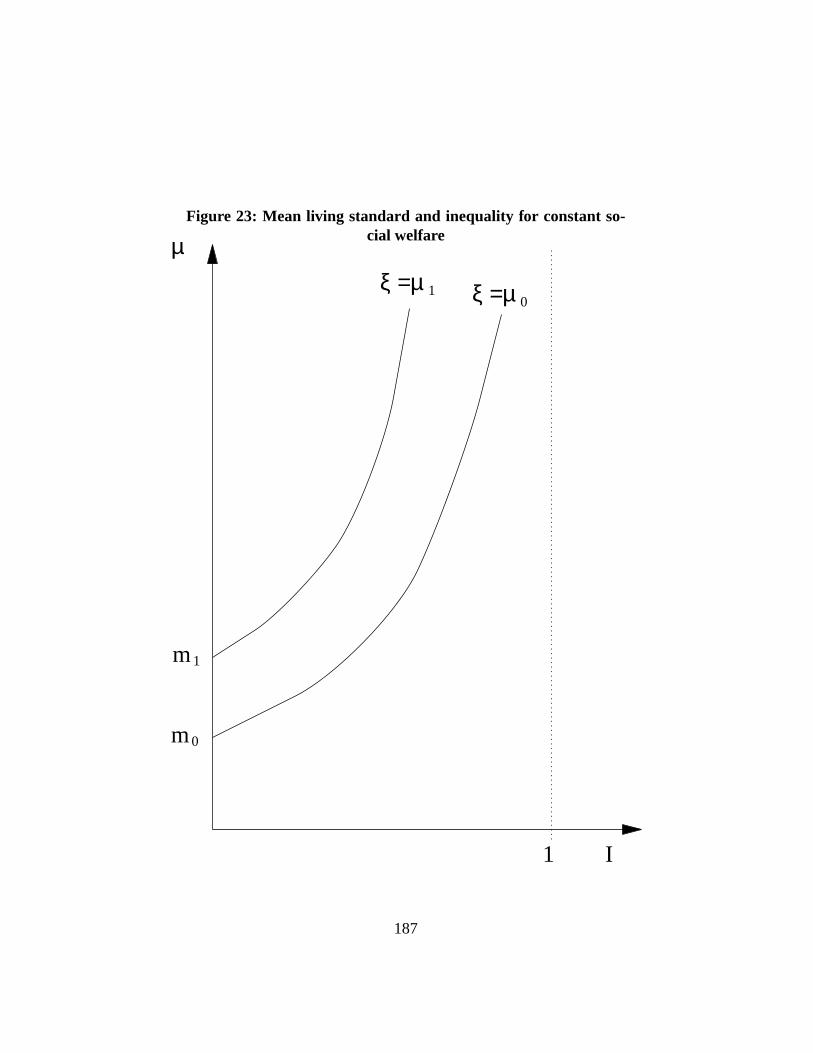

standard and inequality in its distribution, withξ = µ · (1 − I). Compare to theW , ξ also has the advantage of being money metric and thus of being easily un-derstood and compared to other economic indicators that can also be expressed inmoney-metric terms. To increase social welfare, we can either try to increaseµ,or increase equality of income1− I by decreasing inequalityI. Two distributionsof income can display the same social welfare even with different average incomeif these differences are offset by differences in inequality. This is shown in Figure23, starting initially with two different levels of mean incomeµ0 andµ1 and zeroinequality. We then have thatξ = µ0 andξ = µ1. To preserve the same level ofsocial welfare in the presence of inequality, mean income must be higher: this is

33

shown by the positive slope of the constantξ functions. Furthermore, as inequal-ity becomes large, further increases inI must be matched by higher and higherincreases in mean income for social welfare not to fall.

Defined as in (31), inequality has an interesting interpretation: it measures thedifference between the mean level of actual income and the (lower) level neededinstead to achieve the same level of social welfare when income is distributedequally across the population. This difference being expressed as a proportion ofmean income,I thus shows theper capitaproportion of income that is wastedin social terms because of its unequal distribution. Society as a whole would bejust as well-off with an equal distribution of a proportion of just1− I of the totalactual income.I can thus be interpreted as a money-metric indicator of the socialcost of inequality.

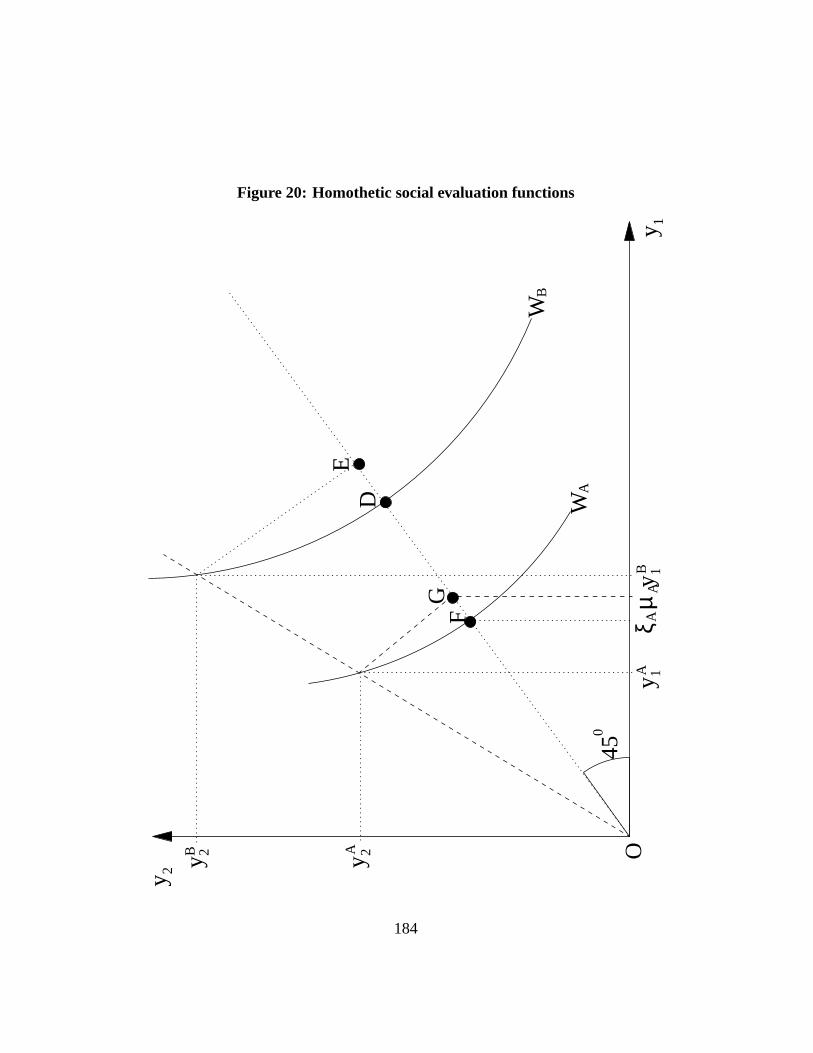

Let a distributionA of income just be a proportional re-scaling of a distributionB. In other words, for a constantλ > 0, we have thatQA(p) = λQB(p) for all p.If the social welfare function used for the computation ofI is homothetic, it mustbe thatIA = IB. This is illustrated in Figure20 for the case of two incomesyA

1

andyA2 for the case of an initial distributionA andyB

1 andyB2 for a ”scaled-up”

distributionB. Social welfare inA is given byWA. The social indifference curveWA shown in Figure20also depicts the many other combinations of incomes thatwould yield the same level of social welfare. One of these combinations, at pointF , corresponds to a situation of equality of income where both individuals enjoyξA. ξA is therefore the equally distributed living standard that is socially equivalentto the distribution(yA

1 , yA2 ).

The average living standard inA is given byµA, which is pointG in Figure20. Hence two distributions of income, one made of the vector(yA

1 , yA2 ) and the

other of the vector(ξA, ξA), generate the same level of social welfare, the firstwith an unequally distributed average living standardµA and the other with anequally distributed average living standardξA. Hence, the distance between pointF and pointG in Figure20 can be understood as the ”cost of inequality” in thedistributionA of income. Taking that distance as a proportion ofµA (see equation(31)) gives the index of inequality in the distributionA.

The fact thatyA1 = λyB

1 andyA2 = λyB

2 for the sameλ can be seen from thefact that the two vectors of income lie along the same ray from the origin. If thefunction W is homothetic, then inequality inA must be the same as inequalityin B. In other words, the distance between pointsD andE as a proportion ofthe distanceOE must be the same as the distance between pointsF andG as aproportion of the distanceOG.

34

4.3.1 Atkinson indices

Two special cases ofW (ρ, ε) are of particular interest in assessing social welfareand relative inequality. The first is when the rank of income is not important incomputing social welfare: this is obtained whenρ = 1, and it yields the well-known Atkinson additive social welfare function,W (ε):

W (ε) = W (ρ = 1, ε) =∫ 1

0U (Q(p); ε)) dp. (32)

The Atkinson social welfare function has often been interpreted as a utilitariansocial welfare function, whereU(Q(p); ε) is an individual utility function dis-playing decreasing marginal utilities of income, or whereU(Q(p); ε) correspondsto a concave social evaluation of a concave individual utility of income. It can beargued, however, that “it is fairly restrictive to think of social welfare as a sumof individual welfare components”, and that one might feel that “the social valueof the welfare of individuals should depend crucially on the levels of welfare (orincomes) of others” (Sen (1973, p.30 and 41). The unrestricted formW (ρ, ε) al-lows for such interdependence and is therefore more flexible than the Atkinsonadditive formulation. In the light of the above, we can also interpretW (ρ, ε) asthe expected utility of the poorest individual in a group ofρ randomly selectedindividuals. This interpretation of the social evaluation functionW (ρ, ε) confirmswhy it is not additive or separable in individual welfare: the social welfare weighton individual utility U(Q(p); ε) depends on the rankp of the individual in thewhole distribution of income.

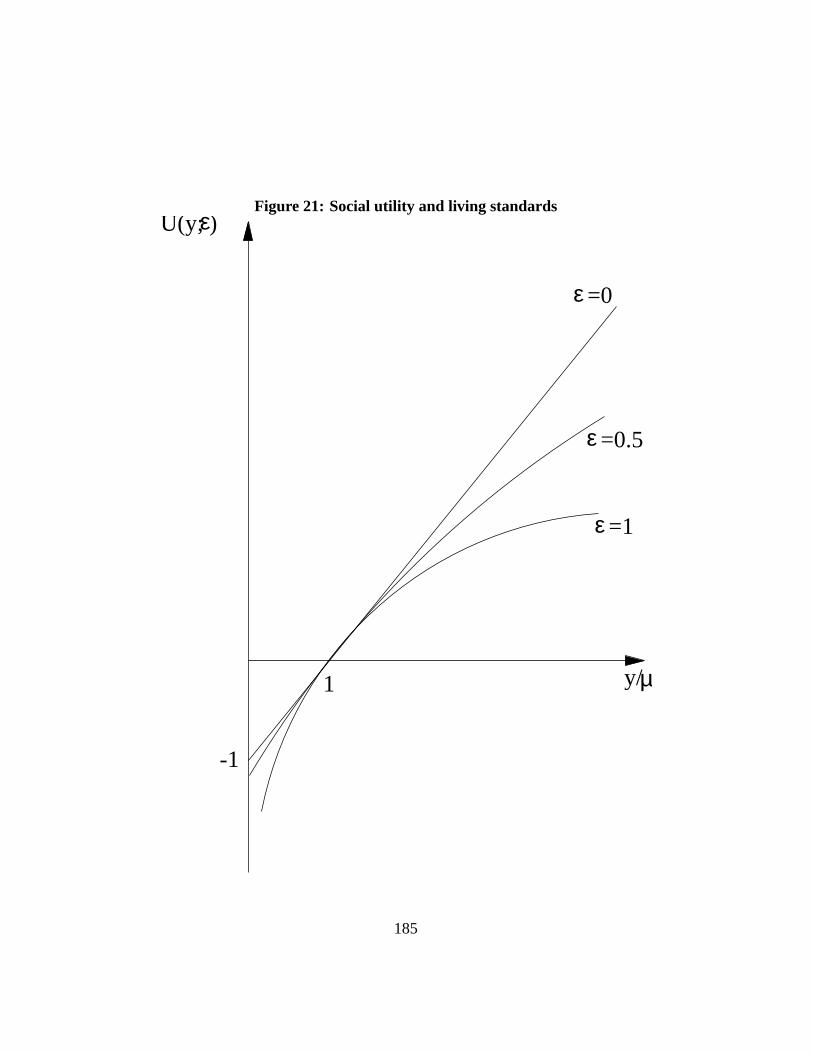

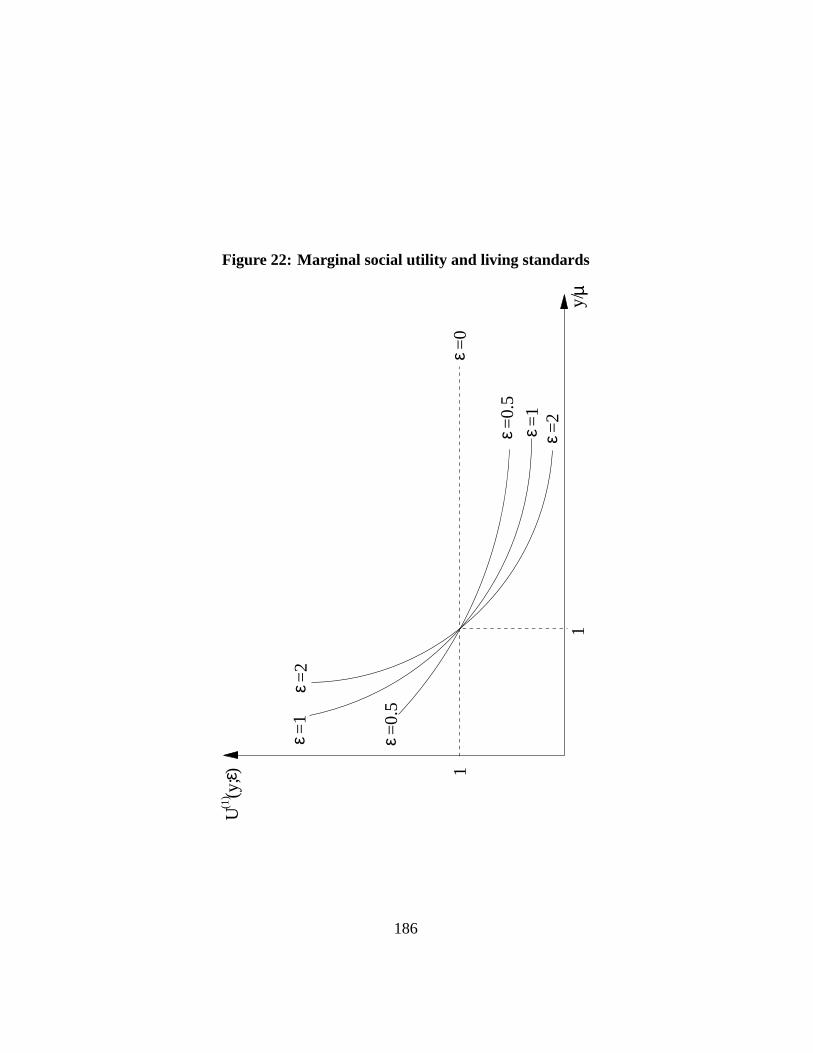

Figure21shows the shape of the utility functionsU (y; ε)) for different valuesof ε2. Incomes are shown on the horizontal axis as a proportion of their mean, andutility U (y; ε)) can be read on the vertical axis. A normalizationU (µ; ε)) = 1has been applied for graphical convenience. Although for all values ofε, theslope ofU (y; ε)) is positive, it is obviously not always the same across all valuesof y. This is made more explicit on Figure22 which shows the marginal socialutility of incomeU (1) (y; ε)) for different values ofε. Again, a normalization ofU (1) (µ; ε)) = 1 was made. Forε = 0, the marginal social utility is constant:increasing by a given amount a poor person’s living standard has the same socialwelfare impact as increasing by the same amount a richer person’s living standard.For ε > 0, however, increasing the poor’s income is socially more desirable than

2This is drawn from Cowell ???.

35

increasing the rich’s. The larger the value ofε, the faster the marginal social utilityfalls with y.

By (29) and (31), the Atkinson inequality index is then given by:

I(ε) = I(ρ = 1, ε) =

1−(∫ 1

0Q(p)(1−ε)dp

) 11−ε

µ, when ε 6= 1,

1−exp

(∫ 1

0ln(Q(p))dp

)

µ, when ε = 1.

(33)

The Atkinson indices are said to exhibit constant relative inequality aversion, sincethe elasticity ofU (1)(Q(p); ε) with respect toQ(p), is constant and equal toε:

Q(p) U (2)(Q(p); ε)

U (1)(Q(p); ε)= ε. (34)

Figure18 illustrates graphically the link between the Atkinson social evalua-tion functionsW (ε) and their associated inequality indices. For this, suppose apopulation of only two individuals, with incomesy1 andy2 as shown on the hori-zontal axis. Mean income is given byµ = (y1 + y2) /2 (the middle point betweeny1 and y2). The ”utility function” U(y; ε) has a positive but decreasing slope.W (ε) is then given by(U (y1) + U (y2)) /2, the middle point betweenU (y1) andU (y2).

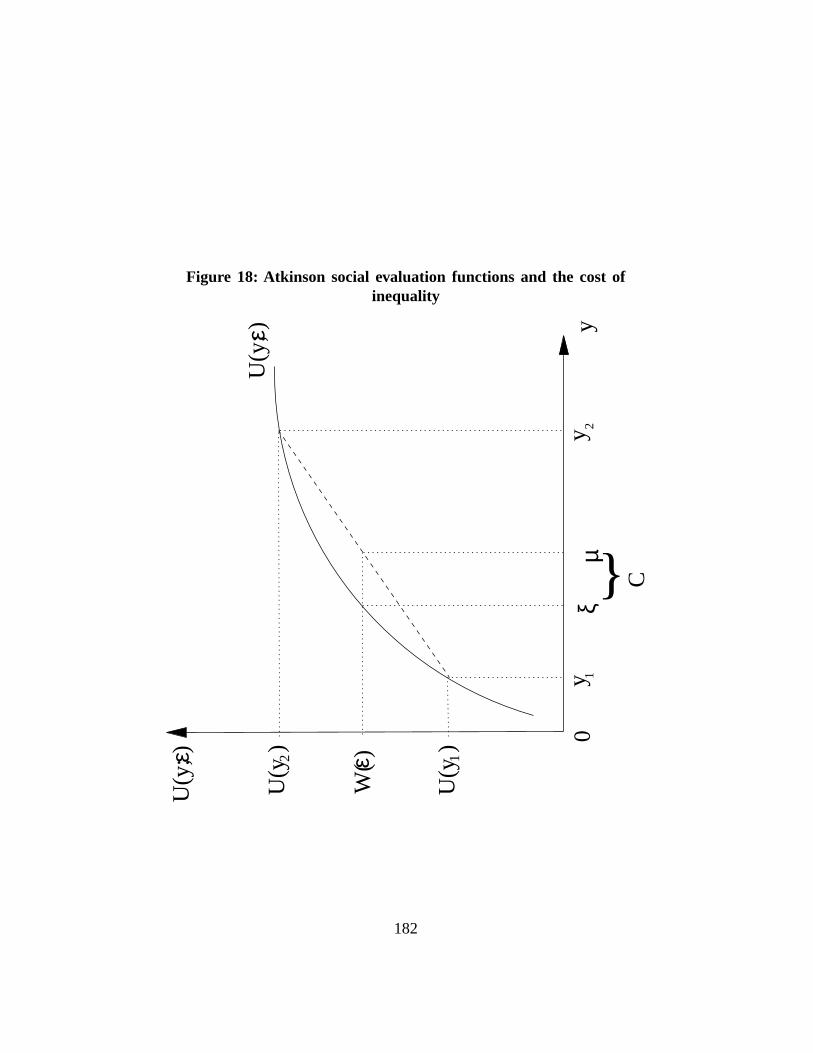

If equally distributed, an average mean living standard ofξ would be sufficientto generate that same level of social welfare, since on Figure18 we have thatW (ε) = U(ξ, ε). The cost of inequality is thus given by the distance betweenµandξ, shown asC on Figure18. Inequality is the ratioC/µ.

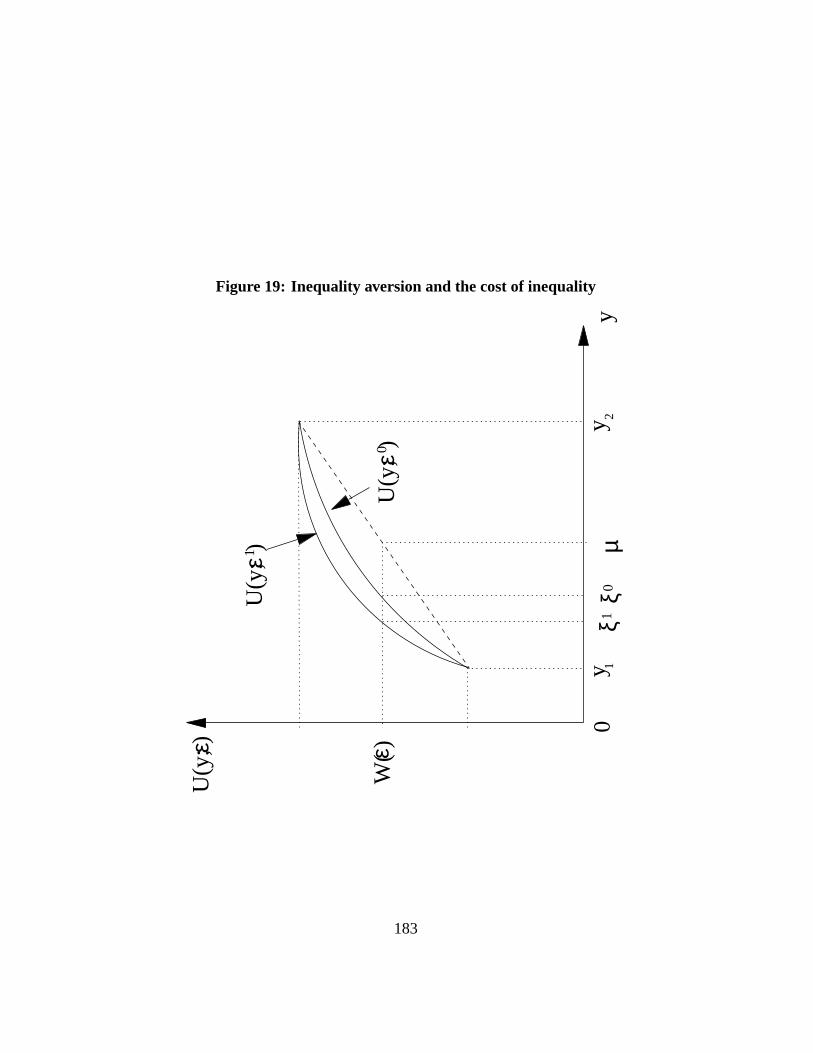

Graphically, the more ”concave” the functionU(y; ε), the greater the cost ofinequality and the greater the inequality indicesI(ε). This can be seen on Figure19where two functionsU(y; ε) have been drawn, with different relative inequalityaversion parametersε0 < ε1. This difference leads toξ0 > ξ1, and therefore toI(ε0) < I(ε1). A specification with greater inequality aversion leads to a greaterinequality index, and to the judgement that a greater proportion of average incomeis socially wasted because of the inequality in its distribution.

4.3.2 S-Gini indices

The second special case is obtained when the utility functionsU(Q(p); ε) are lin-ear in the levels of living standard, and thus whenε = 0. This yields the class of

36

S-Gini social welfare functions, on which the S-Gini inequality indices are based:

W (ρ) = W (ρ, ε = 0) =∫ 1

0Q(p)ω(p; ρ) dp. (35)

Social welfare is thus the expected living standard of the poorest individual in agroup ofρ randomly selected individuals. By (29), this is also the EDE livingstandard. Hence, the inequality indices are then given by:

I(ρ, ε = 0) = 1−∫ 10 Q(p)ω(p; ρ)dp

µ(36)

=

∫ 10 (µ−Q(p))ω(p; ρ)dp

µ(37)

which is seen by (16) to be the same as the S-Gini indicesI(ρ). Hence, socialwelfare and the EDE living standard equal theper capitaliving standard correctedby the extent of relative deprivation in those incomes:

W (ρ) = µ− 1

ρ

∫ 1

0δ(p)κ(p; ρ)dp. (38)

A useful curve for the analysis of the distribution of absolute incomes is theGeneralised Lorenz curve. It is defined asGL(p):

GL(p) = µ · L(p). (39)

The Generalised Lorenz curve has all of the attributes of the Lorenz curve, exceptfor the fact that it does not normalise income by the mean. By (13), (31) and(35), we note that the Generalised Lorenz curve has a nice graphical link with theS-Gini index of social welfare:

W (ρ) =∫ 1

0GL(p)κ(p; ρ)dp. (40)

4.4 Decomposable indices of inequality

A frequent goal is to explain the total amount of inequality in a distribution bythe extent of inequality found among socio-economic groups (“intra” or “within”group inequality) and across them (“inter” or “between” group inequality). A use-ful class of relative inequality indices that allow one to do this is called the class

37

of decomposable inequality indices. Although that class can be given a justifi-cation in terms of social welfare functions, this exercise is less transparent andintuitive than for the class of inequality indices considered above. For all practicalpurposes, we can express these decomposable inequality indices as Generalisedindices of entropy, defined asI(θ):

I(θ) =

1θ(θ−1)