Embed Size (px)

Citation preview

Potential Impacts of anAdvanced Energy Portfolio

Standard in Pennsylvania

Potential Impacts of anAdvanced Energy Portfolio

Standard in Pennsylvania

Ryan Pletka, P.E.

Black & Veatch

April 12, 2004

Supported by:Heinz Endowments

Community Foundation for the Alleghenies

2 0 0 5 E I A M i d t e r m E n e r g y O u t l o o k a n d M o d e l l i n g C o n f e r e n c e2 0 0 5 E I A M i d t e r m E n e r g y O u t l o o k a n d M o d e l l i n g C o n f e r e n c e

- 2

Study ObjectiveStudy Objective

1. Identify most cost effective mix of resources built in response to AEPS

2. Identify economic benefits or costs

Assess the Potential Economic Impacts of a 20 Percent Advanced

Energy Portfolio Standard (AEPS) in Pennsylvania

- 3

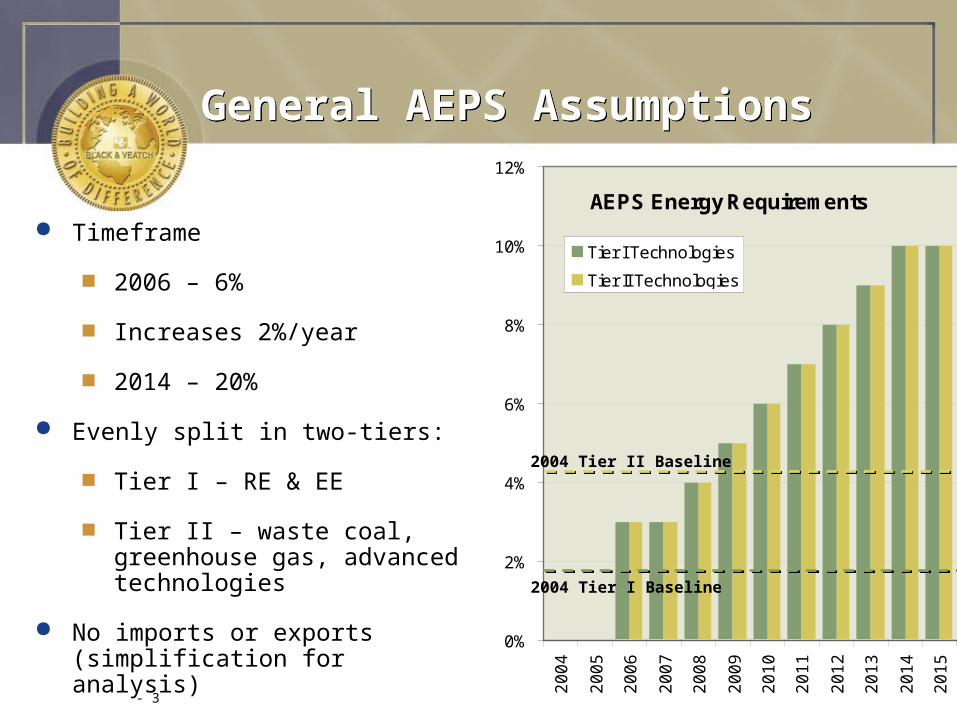

General AEPS AssumptionsGeneral AEPS Assumptions

Timeframe

2006 – 6%

Increases 2%/year

2014 – 20%

Evenly split in two-tiers:

Tier I – RE & EE

Tier II – waste coal, greenhouse gas, advanced technologies

No imports or exports (simplification for analysis)

Production Tax Credit through 2009

AEPS Energy Requirements

0%

2%

4%

6%

8%

10%

12%

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

Tier I Technologies

Tier II Technologies

2004 Tier I Baseline

2004 Tier II Baseline

- 4

AEPS Resource Assessment MethodologyAEPS Resource Assessment Methodology

Screen Technologies

Characterize Resources

Estimate Cost to Generate and Transmit Electricity

Apply Avoided Cost of Power Model

Develop Supply Curves

Develop Least-Cost Portfolio of Projects

- 5

AEPS Eligible ResourcesAEPS Eligible Resources

Tier I

Wind

Low-impact hydro

Biogas and coal mine methane

Biomass

Solar photovoltaics

“Energy conservation” – demand side, ie, consumers

“Energy efficiency” – supply side, ie, power plants

Solar thermal

Ocean and lake energy

Solid waste (non combustion)

Fuel cells fueled by Tier I resources

Tier II Resources

Waste Coal

New facilities

Air pollution controls at existing facilities

Integrated gasification combined cycle

Fuel cells fueled by non-Tier I resources

Greenhouse gas (GHG) reductions

- 6

Wind AssessmentWind Assessment

Pennsylvania wind resources relatively modest

GIS analysis based on latest NREL data

Capital Cost:

Base: $1,175-$1,275/kW

Transmission: +$20-$110/kW

“Expensive” resources: +$500/kW (50% of total)

Included 300 MW, class 5, offshore wind farm in Lake Erie

- 7

Biomass Cofiring AssessmentBiomass Cofiring Assessment

Pennsylvania has good biomass resources and lots of coal plants

Focused on cofiring at 38 existing coal units

Capital cost: $100-$700/kW

Biomass resources

Only sustainable and clean resources identified

Assessment based on ORNL database

Biomass collected from 75 mile radius around plants

- 8

Energy Conservation / Efficiency AssessmentEnergy Conservation / Efficiency Assessment

Good opportunity for energy conservation/efficiency in PA

Analysis Based on B&V, ACEEE assessments

Residential measures

Commercial & Industrial measures

Over 16,000 GWh of potential identified over 20 years

About 10% of PA consumption

Wide range of costs and payback potential

Consumers won’t necessarily implement measures even if economical

- 9

Waste Coal Combustion Waste Coal Combustion

Excellent waste coal resource in Pennsylvania

To be eligible for AEPS, waste coal projects must be low emissions

Analysis Based on PA DEP waste coal assessments

3 Planned New Site Developments

15 Environmental control upgrades at existing plants

Environmental control upgrade projects also receive substantial revenue from emissions credit markets

- 10

Properly Characterizing Resource CostProperly Characterizing Resource Cost

One of the largest modeling differences between renewables and fossil fuels is that costs vary tremendously based on renewable resource quality

There are a limited number of very good renewable / advanced project sites

Costs rise as “low-hanging” projects are developed

Supply curves capture these effects

- 11

- 15

- 10

- 5

0

5

10

15

20

1 161 321 481 641 801 962

Generation, GWhLeve

lized C

ost

Pre

miu

m,

$/M

Wh

Ad

Biogas Supply Curve 2006Premium over Avoided CostsBiogas Supply Curve 2006Premium over Avoided Costs

~60 MW~70 MW~30 MW

- 12

2010 Supply Curve

- 60

- 40

- 20

0

20

40

60

80

100

120

23 3,476 6,929 10,382 13,835 17,288 20,741

Generation, GWh

Leveli

zed C

ost,

$/M

Wh

Additional Renewable Generation Required: 3154 GWh

Aggregate Tier I Supply Curve 2010Aggregate Tier I Supply Curve 2010

Wind

Biomass Cofiring

Biogas

Solar

Hydro

Fuel Cells - Tier I

Energy Efficiency

Energy Conservation

Wind

Biomass Cofiring

Biogas

Solar

Hydro

Fuel Cells - Tier I

Energy Efficiency

Energy Conservation

Tier I

2010 requirement

Biomass Cofiring and Energy Efficiency / Conservation add Significant Flexibility

Pre

miu

m

- 13

Aggregate Tier II Supply Curve 2010Aggregate Tier II Supply Curve 2010

2010 Supply Curve

0

20

40

60

80

100

120

16 2,354 4,693 7,032 9,371 11,710 14,049Generation, GWh

Leveli

zed C

ost,

$/M

Wh

Additional Renewable Generation Required: 2955 GWh

Waste Coal New

Waste Coal Environmental Compliance

Integrated Gasification Combined Cycle

Fuel Cells - Tier II

GHG Offsets

Waste Coal New

Waste Coal Environmental Compliance

Integrated Gasification Combined Cycle

Fuel Cells - Tier II

GHG Offsets

Tier II

2010 requirement

Pre

miu

m

- 14

Tier I Cost Premium Supply CurvesTier I Cost Premium Supply Curves

(60.00)

(40.00)

(20.00)

-

20.00

40.00

60.00

80.00

100.00

120.00

0 5,000 10,000 15,000 20,000

Generation, GWh

Leveli

zed C

ost

Pre

miu

m,

$/M

Wh

Ad

Last Project Developed for 2006

2006

(60.00)

(40.00)

(20.00)

-

20.00

40.00

60.00

80.00

100.00

120.00

0 5,000 10,000 15,000 20,000

Generation, GWh

Leveli

zed C

ost

Pre

miu

m,

$/M

Wh

Ad

Last Project Developed for 2008

20082006

(60.00)

(40.00)

(20.00)

-

20.00

40.00

60.00

80.00

100.00

120.00

0 5,000 10,000 15,000 20,000

Generation, GWh

Leveli

zed C

ost

Pre

miu

m,

$/M

Wh

Ad

Last Project Developed for 2010

2010 20082006

(60.00)

(40.00)

(20.00)

-

20.00

40.00

60.00

80.00

100.00

120.00

0 5,000 10,000 15,000 20,000

Generation, GWh

Leveli

zed C

ost

Pre

miu

m,

$/M

Wh

Ad

Last Project Developed for 2012

2012 200820102006

(60.00)

(40.00)

(20.00)

-

20.00

40.00

60.00

80.00

100.00

120.00

0 5,000 10,000 15,000 20,000

Generation, GWh

Leveli

zed C

ost

Pre

miu

m,

$/M

Wh

Ad

Last Project Developed for 2014

2014

2008

2010

2012

2006

(60.00)

(40.00)

(20.00)

-

20.00

40.00

60.00

80.00

100.00

120.00

0 5,000 10,000 15,000 20,000

Generation, GWh

Leveli

zed C

ost

Pre

miu

m,

$/M

Wh

Ad

Last Project Developed in 2016

20122014

2016 2010 2008

2006

- 15

Tier II Cost Premium Supply CurvesTier II Cost Premium Supply Curves

(60.00)

(40.00)

(20.00)

-

20.00

40.00

60.00

80.00

100.00

120.00

0 5,000 10,000 15,000 20,000

Generation, GWh

Leveli

zed C

ost

Pre

miu

m,

$/M

Wh

Ad

Last Project Developed for 2008

2008

(60.00)

(40.00)

(20.00)

-

20.00

40.00

60.00

80.00

100.00

120.00

0 5,000 10,000 15,000 20,000

Generation, GWh

Leveli

zed C

ost

Pre

miu

m,

$/M

Wh

Ad

Last Project Developed for 2010

20102008

(60.00)

(40.00)

(20.00)

-

20.00

40.00

60.00

80.00

100.00

120.00

0 5,000 10,000 15,000 20,000

Generation, GWh

Leveli

zed C

ost

Pre

miu

m,

$/M

Wh

Ad

Last Project Developed for 2012

20122008 2010

(60.00)

(40.00)

(20.00)

-

20.00

40.00

60.00

80.00

100.00

120.00

0 5,000 10,000 15,000 20,000

Generation, GWh

Leveli

zed C

ost

Pre

miu

m,

$/M

Wh

Ad

Last Project Developed for 2014

20142008 2010 2012

(60.00)

(40.00)

(20.00)

-

20.00

40.00

60.00

80.00

100.00

120.00

0 5,000 10,000 15,000 20,000

Generation, GWh

Leveli

zed C

ost

Pre

miu

m,

$/M

Wh

Ad

No Projects Developed in 2016

20122014

2016

20102008

- 16

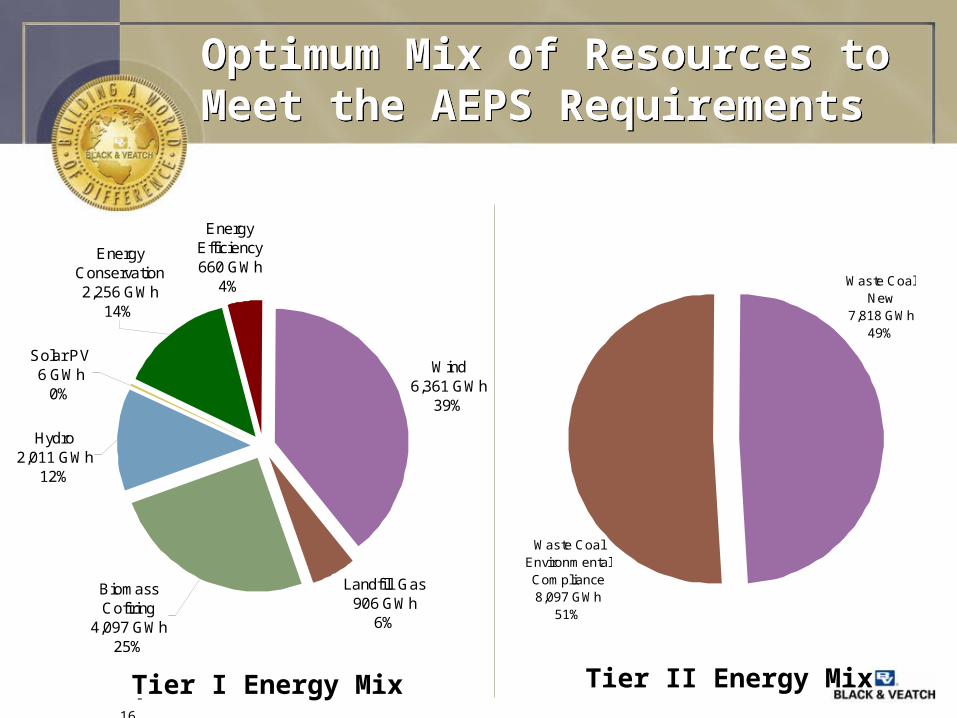

Optimum Mix of Resources to Meet the AEPS RequirementsOptimum Mix of Resources to Meet the AEPS Requirements

Wind 6,361 GWh

39%

Energy Efficiency660 GWh

4%

Hydro2,011 GWh

12%

Solar PV6 GWh

0%

Biomass Cofiring

4,097 GWh25%

Landfill Gas906 GWh

6%

Energy Conservation2,256 GWh

14%

Tier I Energy Mix

Waste Coal New

7,818 GWh49%

Waste Coal Environmental Compliance8,097 GWh

51%

Tier II Energy Mix

- 17

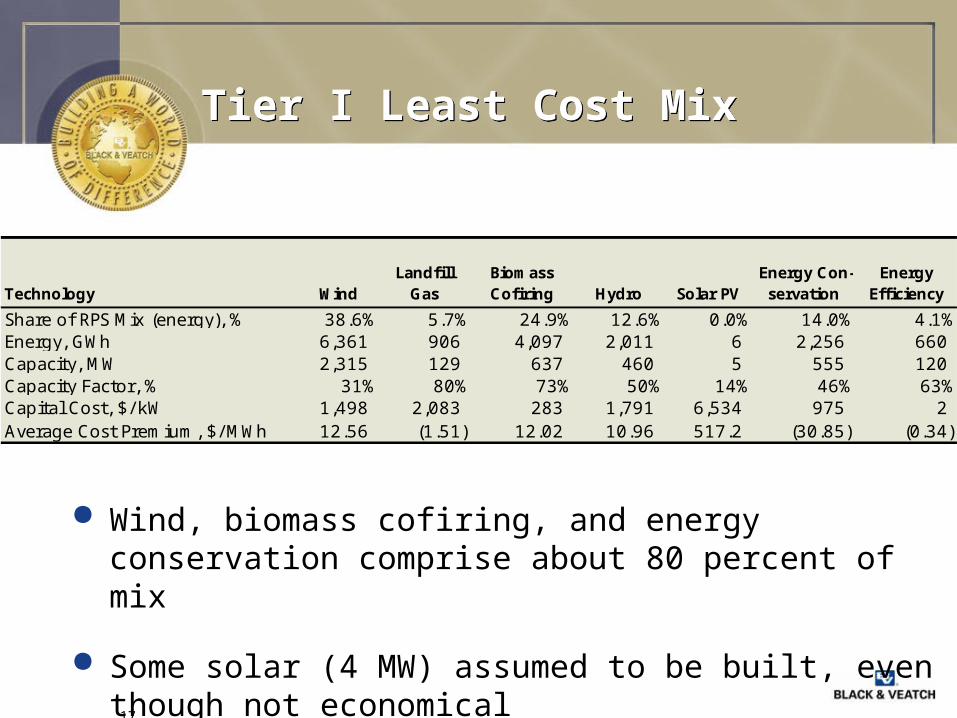

Tier I Least Cost Mix Tier I Least Cost Mix

Wind, biomass cofiring, and energy conservation comprise about 80 percent of mix

Some solar (4 MW) assumed to be built, even though not economical

Technology Wind Landfill

GasBiomass Cofiring Hydro Solar PV

Energy Con-servation

Energy Efficiency

Share of RPS Mix (energy), % 38.6% 5.7% 24.9% 12.6% 0.0% 14.0% 4.1%Energy, GWh 6,361 906 4,097 2,011 6 2,256 660 Capacity, MW 2,315 129 637 460 5 555 120 Capacity Factor, % 31% 80% 73% 50% 14% 46% 63%Capital Cost, $/ kW 1,498 2,083 283 1,791 6,534 975 2 Average Cost Premium, $/ MWh 12.56 (1.51) 12.02 10.96 517.2 (30.85) (0.34)

- 18

Economic Impacts AssessmentEconomic Impacts Assessment

Compared building a 20% AEPS portfolio to building the “Business As Usual” (BAU) portfolio

Cost of electricity

Economic impacts (Jobs, Output, Earnings)

Fossil fuel prices

BAU Portfolio: 50% coal, 40% combined cycle, 10% simple cycle

Portfolios equated on an equivalent energy production basis

RPS portfolio: 6,470 MW

BAU portfolio: 2,460 MW

Environmental externalities purposely not assessed

- 19

Cumulative Economic ImpactsCumulative Economic Impacts

Cost of Electricity

Employment Impact (job-years)

Earnings Impact Output Impact

AEPS Portfolio $ 3.9 Billion 165,689 $ 6.6 Billion $ 18.9 Billion

BAU Portfolio $ 6.6 Billion 94,753 $ 4.1 Billion $ 11.9 BillionDifference - $ 2.7 Billion 70,937 $ 2.5 Billion $ 6.9 Billion

Economic Benefits of the AEPS Portfolio compared to Business as Usual

Cost of electricity: reduced by $2.7 billion (cumulative present value), about 1% when spread over all consumption

Employment: Creates over 70,000 additional job-years over 20 years (average of new 3,500 jobs)

State output: Creates about $7 billion in increased state output

Personal Income: Creates about $2.5 billion in additional earnings

- 20

Pennsylvania Employment Impacts, “Job-years” per MWPennsylvania Employment Impacts, “Job-years” per MW

-

5

10

15

20

25

30

35

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Construction

Operation

Constr

ucti

on

-

5

10

15

20

25

30

35

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Construction

Operation

Const

ruct

ion O

pera

tion

RPS portfolio: 6,470 MW

BAU portfolio: 2,460 MW

Impacts proportional to the percent of project expenditures made in PA

in various industries

- 21

AEPS Enacted into Law in Late 2004AEPS Enacted into Law in Late 2004

Our model does not match what was finally signed into law

Solar PV Standard - 0.5% of electricity demand in 15 years (~680 MW)

Implementation Challenges

Ensuring new projects are deployed to meet the requirements of Tier I

Geographic Scope

Definition of Low-Impact Hydro

Long-Term Contracts

Encouraging demand-side management

Tier II over-subscription

Developing rules

- 22

Conclusions and AcknowledgementsConclusions and Acknowledgements

Acknowledgements

Community Foundation for the Alleghenies – Mike Kane

Heinz Endowments

PA DEP

REPP

Industry Contact

Ryan Pletka

Black & Veatch

913-458-8222