Embed Size (px)

Citation preview

0

POSTAL AND TELECOMMUNICATIONS

REGULATORY AUTHORITY OF

ZIMBABWE

(POTRAZ)

ABRIDGED ANNUAL POSTAL AND

TELECOMMUNICATIONS SECTOR

PERFORMANCE REPORT

2017

Disclaimer:

This report has been prepared based on data provided by service providers. The information

provided in this quarterly report is subject to alteration in case of any revisions or updates

from the service providers. Although every effort has been made to ensure accuracy of the data

contained in this report, the Authority is not liable for the inaccuracy of any information.

1

TABLE OF CONTENTS 1. EXECUTIVE SUMMARY ................................................................................................... 4

2. SUBSCRIPTIONS ................................................................................................................. 7

2.1 MOBILE SUBSCRIPTIONS ........................................................................................... 7

2.2 FIXED TELEPHONY SUBSCRIPTIONS ...................................................................... 9

2.3 DATA & INTERNET SUBSCRIPTIONS .................................................................... 10

3. PENETRATION RATES .................................................................................................... 12

3.1 FIXED TELEDENSITY ................................................................................................ 12

3.2 MOBILE PENETRATION RATE................................................................................. 12

3.3 INTERNET PENETRATION RATE ............................................................................ 13

4. TRAFFIC AND USAGE PATTERNS ................................................................................ 14

4.1 VOICE TRAFFIC .......................................................................................................... 14

4.2 INTERNET & DATA TRAFFIC ................................................................................... 16

4.3 POSTAL & COURIER VOLUMES .............................................................................. 17

5. REVENUES & INVESTMENT .......................................................................................... 19

5.1 MOBILE......................................................................................................................... 19

5.3 IAP REVENUES & INVESTMENT ............................................................................. 20

6. MOBILE MONEY ........................................................................................................... 21

6.1 SUBSCRIPTIONS ......................................................................................................... 21

6.2 MOBILE MONEY AGENTS ........................................................................................ 22

6.3 VALUE OF TRANSACTIONS ..................................................................................... 23

7. TELECOMMUNICATIONS INFRASTRUCTURE .......................................................... 24

7.1 MOBILE BASE STATIONS ......................................................................................... 24

7.2 NATIONAL BACKBONE FIBRE LENGTH................................................................... 26

8. INTERNATIONAL INTERNET BANDWIDTH ............................................................... 27

9. EMPLOYMENT .................................................................................................................. 28

9.1 FIXED NETWORK .................................................................................................. 28

9.2 MOBILE NETWORK OPERATORS ........................................................................... 29

9.3 INTERNET ACCESS PROVIDERS ........................................................................ 29

9.4 POSTAL & COURIER ............................................................................................. 30

10. OUTLOOK ........................................................................................................................ 31

2

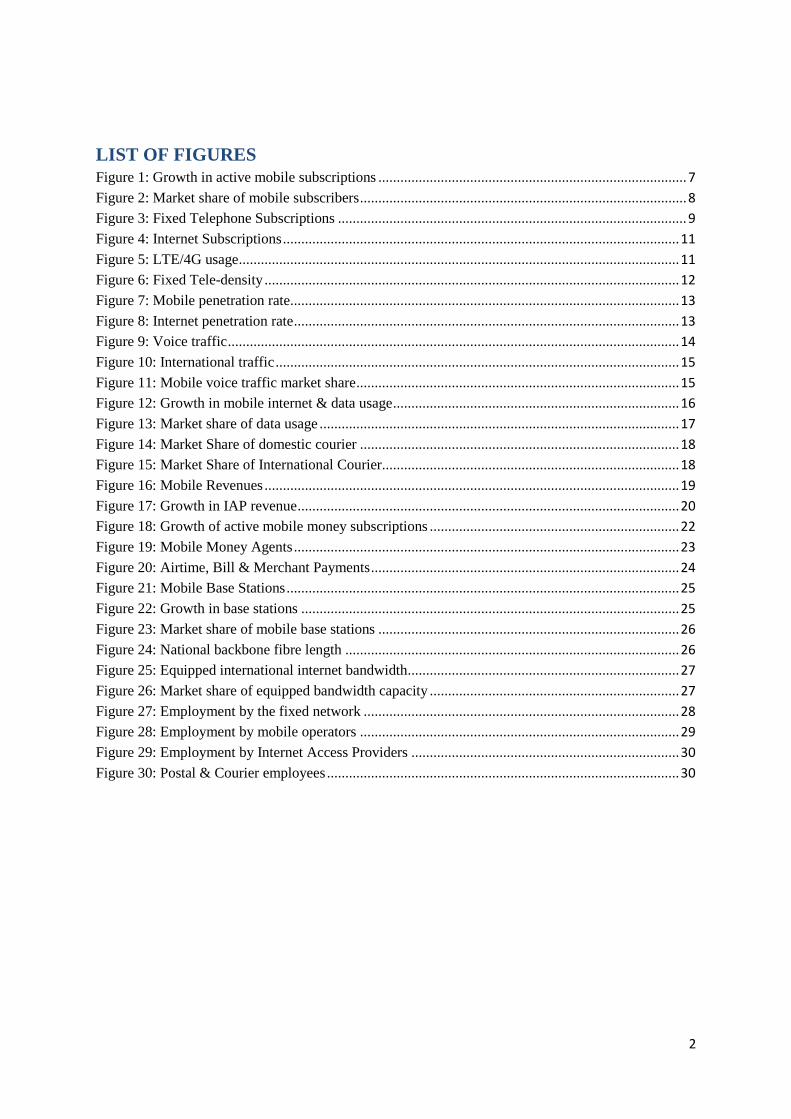

LIST OF FIGURES

Figure 1: Growth in active mobile subscriptions .................................................................................... 7

Figure 2: Market share of mobile subscribers ......................................................................................... 8

Figure 3: Fixed Telephone Subscriptions ............................................................................................... 9

Figure 4: Internet Subscriptions ............................................................................................................ 11

Figure 5: LTE/4G usage ........................................................................................................................ 11

Figure 6: Fixed Tele-density ................................................................................................................. 12

Figure 7: Mobile penetration rate.......................................................................................................... 13

Figure 8: Internet penetration rate ......................................................................................................... 13

Figure 9: Voice traffic ........................................................................................................................... 14

Figure 10: International traffic .............................................................................................................. 15

Figure 11: Mobile voice traffic market share ........................................................................................ 15

Figure 12: Growth in mobile internet & data usage .............................................................................. 16

Figure 13: Market share of data usage .................................................................................................. 17

Figure 14: Market Share of domestic courier ....................................................................................... 18

Figure 15: Market Share of International Courier................................................................................. 18

Figure 16: Mobile Revenues ................................................................................................................. 19

Figure 17: Growth in IAP revenue ........................................................................................................ 20

Figure 18: Growth of active mobile money subscriptions .................................................................... 22

Figure 19: Mobile Money Agents ......................................................................................................... 23

Figure 20: Airtime, Bill & Merchant Payments .................................................................................... 24

Figure 21: Mobile Base Stations ........................................................................................................... 25

Figure 22: Growth in base stations ....................................................................................................... 25

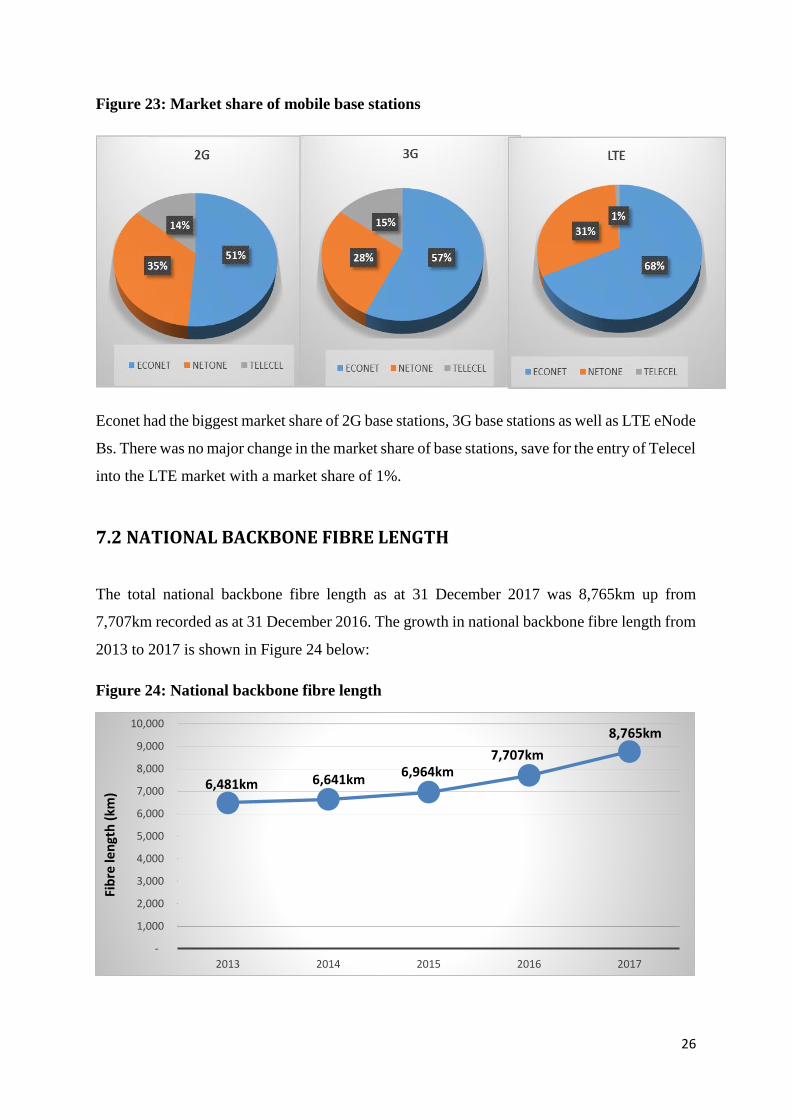

Figure 23: Market share of mobile base stations .................................................................................. 26

Figure 24: National backbone fibre length ........................................................................................... 26

Figure 25: Equipped international internet bandwidth .......................................................................... 27

Figure 26: Market share of equipped bandwidth capacity .................................................................... 27

Figure 27: Employment by the fixed network ...................................................................................... 28

Figure 28: Employment by mobile operators ....................................................................................... 29

Figure 29: Employment by Internet Access Providers ......................................................................... 30

Figure 30: Postal & Courier employees ................................................................................................ 30

3

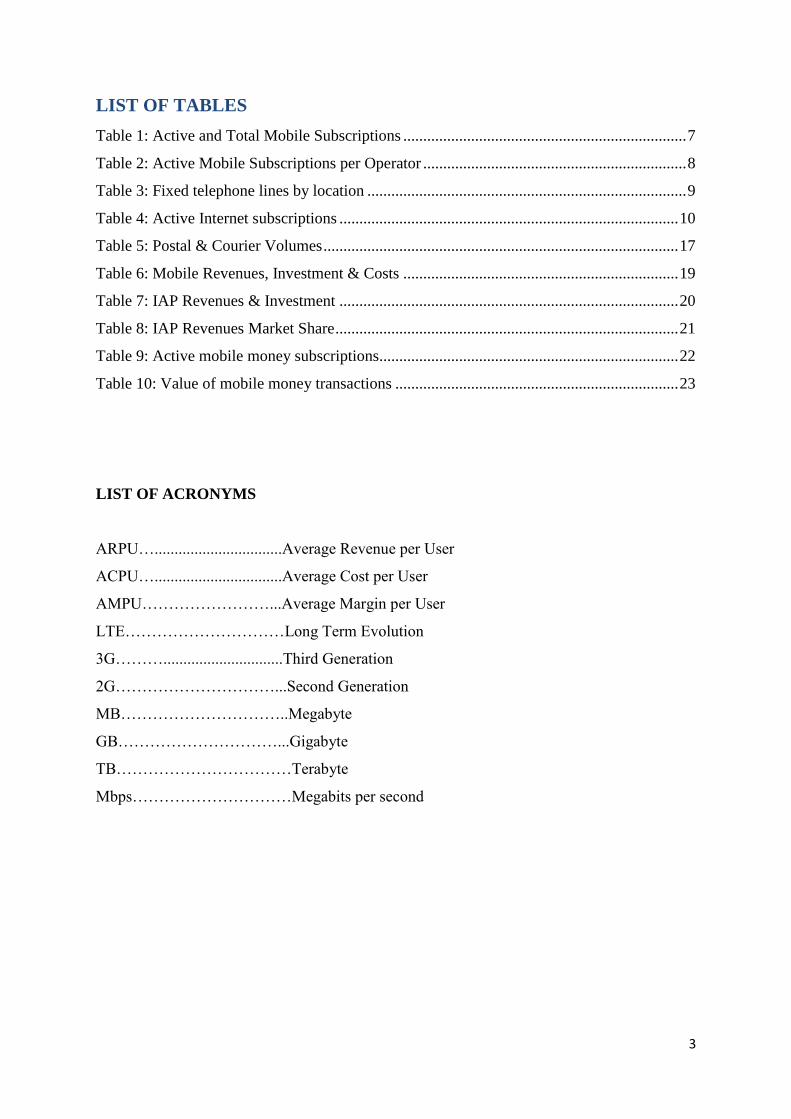

LIST OF TABLES

Table 1: Active and Total Mobile Subscriptions ....................................................................... 7

Table 2: Active Mobile Subscriptions per Operator .................................................................. 8

Table 3: Fixed telephone lines by location ................................................................................ 9

Table 4: Active Internet subscriptions ..................................................................................... 10

Table 5: Postal & Courier Volumes ......................................................................................... 17

Table 6: Mobile Revenues, Investment & Costs ..................................................................... 19

Table 7: IAP Revenues & Investment ..................................................................................... 20

Table 8: IAP Revenues Market Share ...................................................................................... 21

Table 9: Active mobile money subscriptions........................................................................... 22

Table 10: Value of mobile money transactions ....................................................................... 23

LIST OF ACRONYMS

ARPU…................................Average Revenue per User

ACPU…................................Average Cost per User

AMPU……………………...Average Margin per User

LTE…………………………Long Term Evolution

3G………..............................Third Generation

2G…………………………...Second Generation

MB…………………………..Megabyte

GB…………………………...Gigabyte

TB……………………………Terabyte

Mbps…………………………Megabits per second

4

1. EXECUTIVE SUMMARY

This report presents the performance of the various markets within the postal and

telecommunications sector during the period January to December 2017. The report covers

data on subscriptions, usage traffic, infrastructure deployment, revenues, investment and

employment in the postal and telecommunication sector. The data collected is also used by the

Authority to monitor and inform policy decisions aimed at facilitating orderly growth of these

sectors. The following trends characterised the postal and telecommunications sector in 2017:

Growth in mobile and internet subscriptions and a decline in fixed subscriptions

The total number of active fixed telephone lines declined by 13.6% to record 264,150 from

305,720 recorded in 2016. As a result, the fixed tele-density declined from 2.4% recorded in

2016 to reach 1.9% in 2017. Active mobile subscriptions increased by 9.4% to reach

14,092,104 in 2017 from 12,878,926 recorded in 2016; hence, the mobile penetration rate

increased by 7.9% reach 102.7% in 2017 from 94.8% recorded in 2016. The total number of

active internet subscriptions increased by 3.7% to reach 6,971,617 from 6,721,947

subscriptions recorded in 2016. As a result, the internet penetration rate increased by 0.8% to

reach 50.8% in 2017 from 50% recorded in 2016. Fibre internet registered the highest growth

in active subscriptions of 59.7% to reach 31,455 in 2017 from 19,698 recorded in 2016.

Growth in data and internet usage and continued decline of voice traffic

Total voice traffic including fixed voice declined by 5.7% to record 4,400,994,563 minutes

from 4,666,909,037 minutes recorded in 2016. This is the fourth consecutive year in which a

decline in voice traffic has been recorded; however, the rate of decline has reduced from 20%

recorded in 2016. This can largely be attributed to the significant increase in mobile voice

traffic of 14% registered in the fourth quarter of 2017. The increase of mobile voice traffic can

be attributed to the euphoria of the festive season and the excitement for the new political

dispensation.

On the other hand, mobile internet and data usage increased by 89.8% to record 15.4 billion

Megabytes from 8.1 billion Megabytes of data consumed in 2016. Used incoming international

5

bandwidth capacity also increased by 46.4% to record 47,779Mbps from 32,645Mbps recorded

in 2016.

Continued decline of postal and courier volumes

Total postal and courier volumes declined by 7.1% to record 8,098,751 in 2017 from 8,721,550

recorded in 2016. International outgoing postal and courier recorded the biggest decline in

volumes by 9.5% to record 323,773 items from 357,655 recorded in 2016. Domestic postal

volumes also declined by 8.5% to record 5.8 million postal items from 6.3 million recorded in

2016. The decline in postal and courier volumes over the years is attributable to e-substitution,

which is the substitution of traditional paper communication for electronic methods such as

emails and WhatsApp, Twitter and Viber among others.

Growth in sector revenue

The year 2017 marked an upturn in sector revenues from the depressed growth experienced

since 2014. Total telecommunications revenue increased by 11.2% to record $1,109,899,246

from $998,094,747 recorded in 2016. Mobile revenues increased by 17.6% to record

$849,880,488 from $722,934,718 recorded in 2016. Revenues by IAPs registered the biggest

growth rate of 17.8% to record $186,843,531 from $158,565,855 recorded in 2016. The growth

in telecommunications revenue is attributed to the upsurge in the consumption of data and

internet in the country.

Market structures remain relatively unchanged

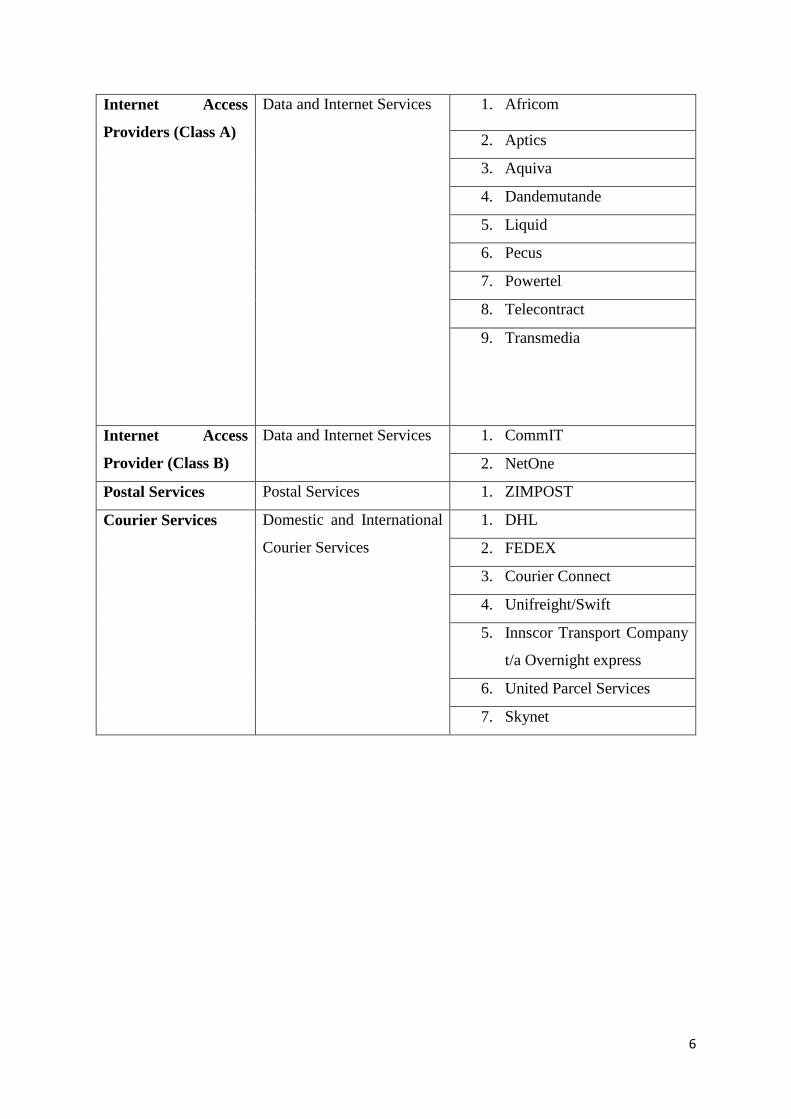

Market structures remained relatively unchanged across postal and telecommunications

markets in 2017. The list of the licensed operators in the various markets as at December 2017

is provided in the following table:

Market Service Description Licensed Operators

Fixed Telephone

Service

Fixed Voice and Fixed

Internet Services

1. TelOne

Mobile Cellular

Services

Mobile Voice and Internet

Services

1. Econet

2. NetOne

3. Telecel

6

Internet Access

Providers (Class A)

Data and Internet Services 1. Africom

2. Aptics

3. Aquiva

4. Dandemutande

5. Liquid

6. Pecus

7. Powertel

8. Telecontract

9. Transmedia

Internet Access

Provider (Class B)

Data and Internet Services 1. CommIT

2. NetOne

Postal Services Postal Services 1. ZIMPOST

Courier Services Domestic and International

Courier Services

1. DHL

2. FEDEX

3. Courier Connect

4. Unifreight/Swift

5. Innscor Transport Company

t/a Overnight express

6. United Parcel Services

7. Skynet

7

2. SUBSCRIPTIONS

2.1 MOBILE SUBSCRIPTIONS

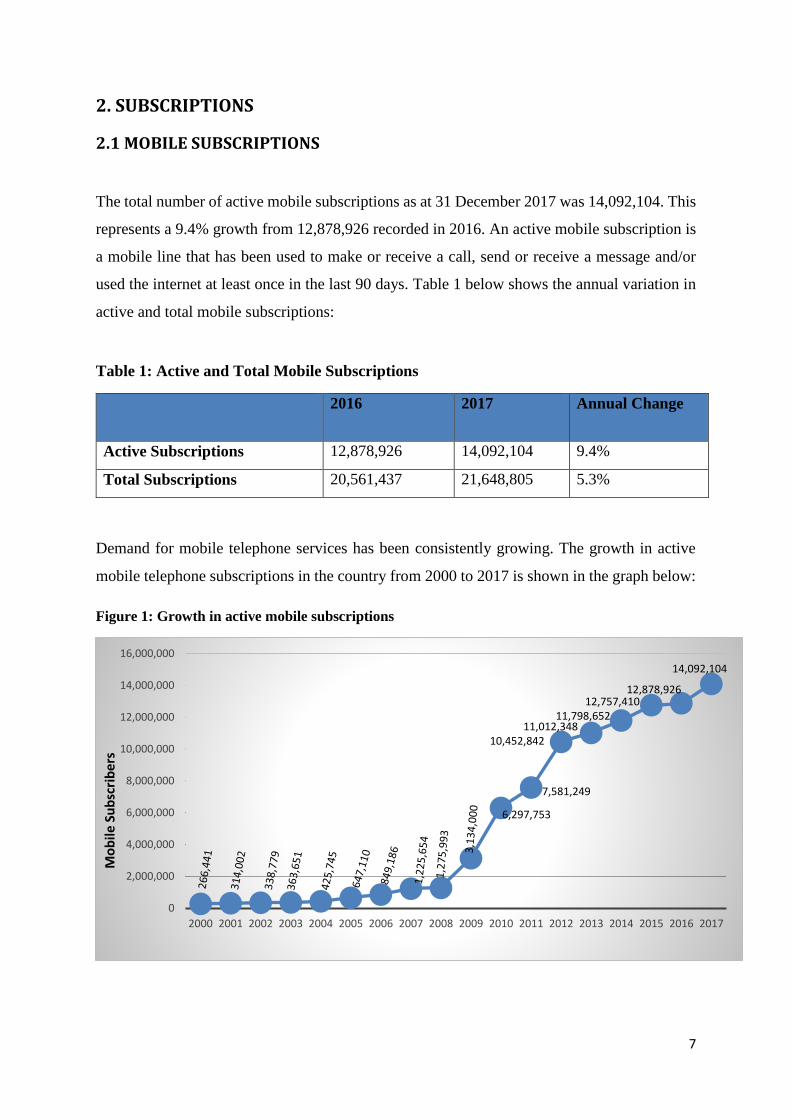

The total number of active mobile subscriptions as at 31 December 2017 was 14,092,104. This

represents a 9.4% growth from 12,878,926 recorded in 2016. An active mobile subscription is

a mobile line that has been used to make or receive a call, send or receive a message and/or

used the internet at least once in the last 90 days. Table 1 below shows the annual variation in

active and total mobile subscriptions:

Table 1: Active and Total Mobile Subscriptions

2016 2017 Annual Change

Active Subscriptions 12,878,926 14,092,104 9.4%

Total Subscriptions 20,561,437 21,648,805 5.3%

Demand for mobile telephone services has been consistently growing. The growth in active

mobile telephone subscriptions in the country from 2000 to 2017 is shown in the graph below:

Figure 1: Growth in active mobile subscriptions

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

6,297,753

7,581,249

10,452,84211,012,348

11,798,65212,757,410

Mo

bile

Su

bsc

rib

ers

14,092,104

12,878,926

8

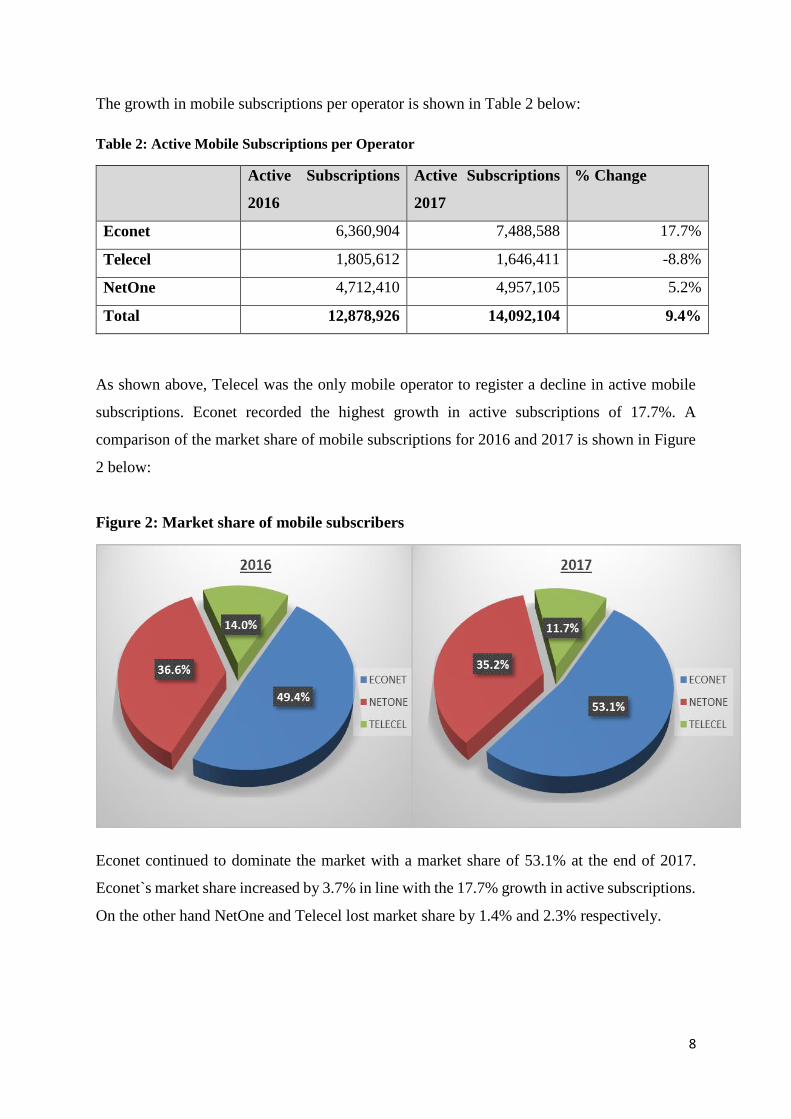

The growth in mobile subscriptions per operator is shown in Table 2 below:

Table 2: Active Mobile Subscriptions per Operator

Active Subscriptions

2016

Active Subscriptions

2017

% Change

Econet 6,360,904 7,488,588 17.7%

Telecel 1,805,612 1,646,411 -8.8%

NetOne 4,712,410 4,957,105 5.2%

Total 12,878,926 14,092,104 9.4%

As shown above, Telecel was the only mobile operator to register a decline in active mobile

subscriptions. Econet recorded the highest growth in active subscriptions of 17.7%. A

comparison of the market share of mobile subscriptions for 2016 and 2017 is shown in Figure

2 below:

Figure 2: Market share of mobile subscribers

Econet continued to dominate the market with a market share of 53.1% at the end of 2017.

Econet`s market share increased by 3.7% in line with the 17.7% growth in active subscriptions.

On the other hand NetOne and Telecel lost market share by 1.4% and 2.3% respectively.

9

2.2 FIXED TELEPHONY SUBSCRIPTIONS

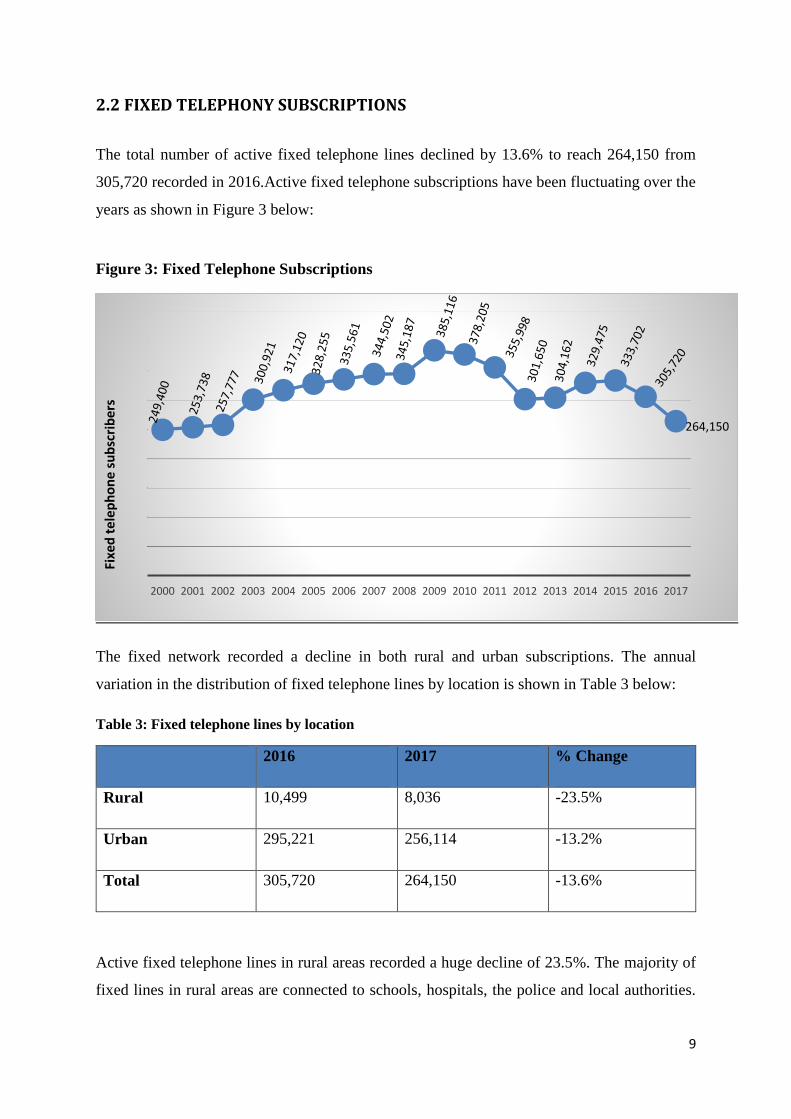

The total number of active fixed telephone lines declined by 13.6% to reach 264,150 from

305,720 recorded in 2016.Active fixed telephone subscriptions have been fluctuating over the

years as shown in Figure 3 below:

Figure 3: Fixed Telephone Subscriptions

The fixed network recorded a decline in both rural and urban subscriptions. The annual

variation in the distribution of fixed telephone lines by location is shown in Table 3 below:

Table 3: Fixed telephone lines by location

2016 2017 % Change

Rural 10,499 8,036 -23.5%

Urban 295,221 256,114 -13.2%

Total 305,720 264,150 -13.6%

Active fixed telephone lines in rural areas recorded a huge decline of 23.5%. The majority of

fixed lines in rural areas are connected to schools, hospitals, the police and local authorities.

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Fixe

d t

ele

ph

on

e s

ub

scri

ber

s

264,150

10

The decline could be attributed to the increasing number of institutions adopting mobile

numbers and VoIP numbers.

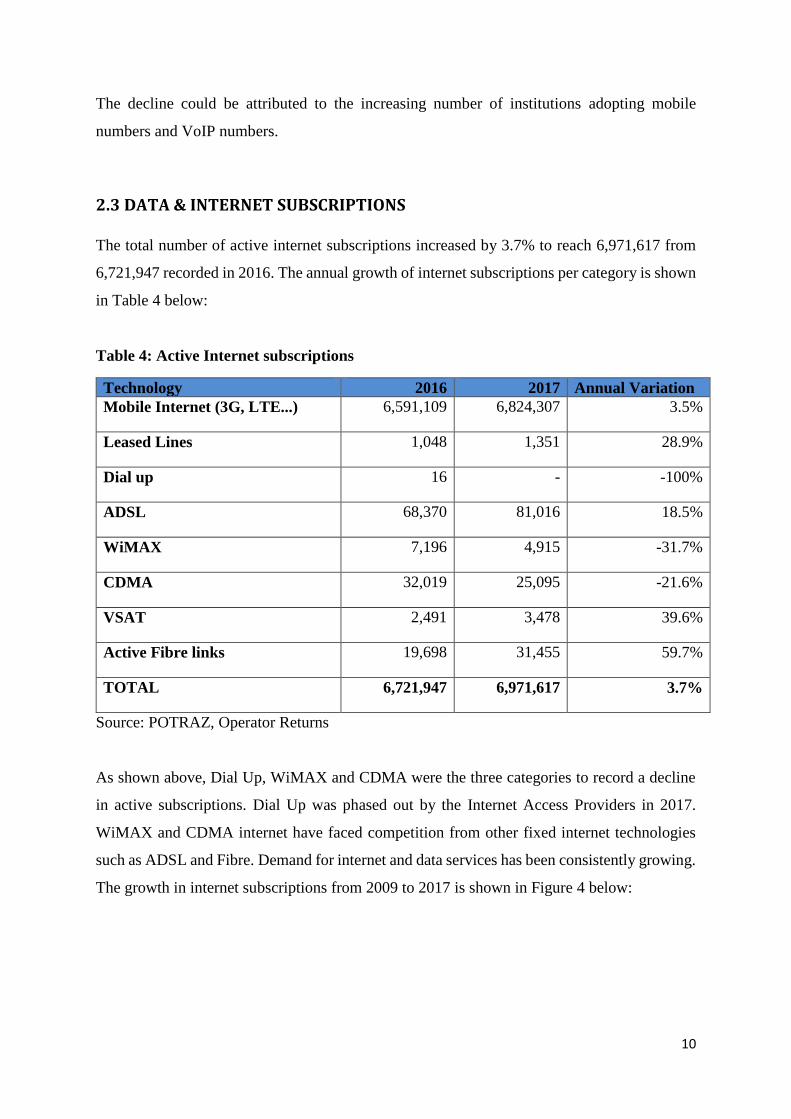

2.3 DATA & INTERNET SUBSCRIPTIONS

The total number of active internet subscriptions increased by 3.7% to reach 6,971,617 from

6,721,947 recorded in 2016. The annual growth of internet subscriptions per category is shown

in Table 4 below:

Table 4: Active Internet subscriptions

Technology 2016 2017 Annual Variation

Mobile Internet (3G, LTE...) 6,591,109 6,824,307 3.5%

Leased Lines 1,048 1,351 28.9%

Dial up 16 - -100%

ADSL 68,370 81,016 18.5%

WiMAX 7,196 4,915 -31.7%

CDMA 32,019 25,095 -21.6%

VSAT 2,491 3,478 39.6%

Active Fibre links 19,698 31,455 59.7%

TOTAL 6,721,947 6,971,617 3.7%

Source: POTRAZ, Operator Returns

As shown above, Dial Up, WiMAX and CDMA were the three categories to record a decline

in active subscriptions. Dial Up was phased out by the Internet Access Providers in 2017.

WiMAX and CDMA internet have faced competition from other fixed internet technologies

such as ADSL and Fibre. Demand for internet and data services has been consistently growing.

The growth in internet subscriptions from 2009 to 2017 is shown in Figure 4 below:

11

Figure 4: Internet Subscriptions

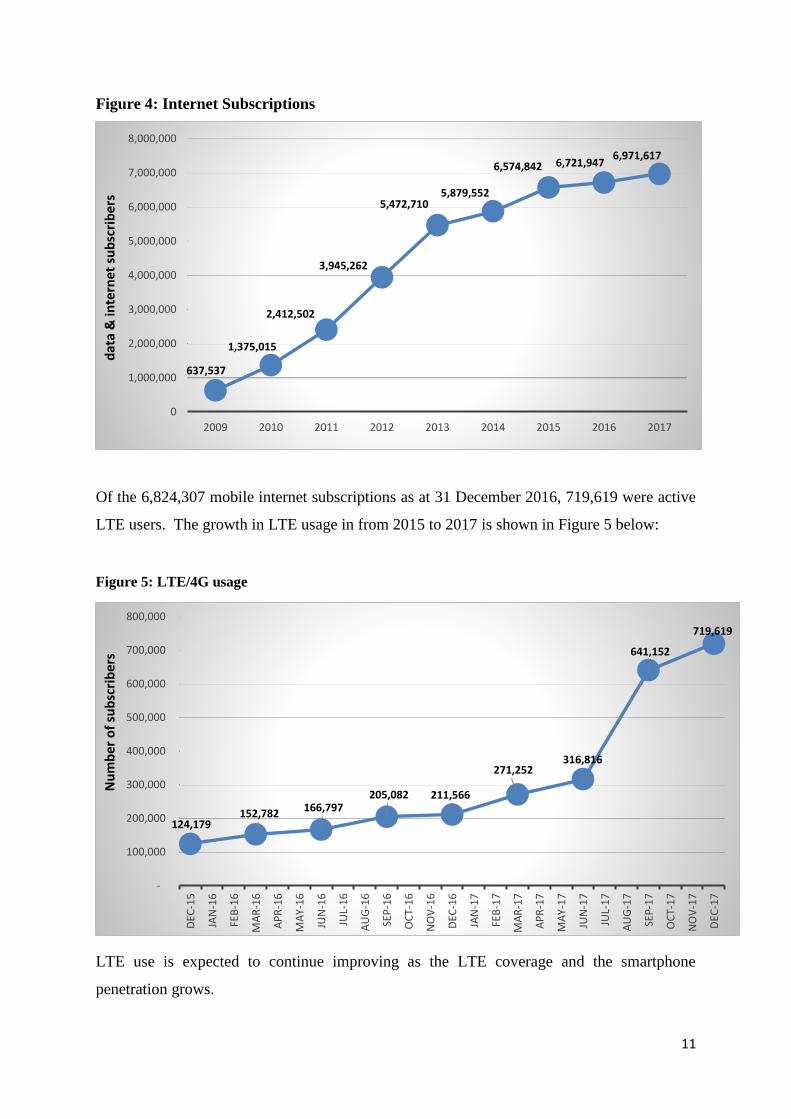

Of the 6,824,307 mobile internet subscriptions as at 31 December 2016, 719,619 were active

LTE users. The growth in LTE usage in from 2015 to 2017 is shown in Figure 5 below:

Figure 5: LTE/4G usage

LTE use is expected to continue improving as the LTE coverage and the smartphone

penetration grows.

637,537

1,375,015

2,412,502

3,945,262

5,472,7105,879,552

6,574,842 6,721,9476,971,617

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

2009 2010 2011 2012 2013 2014 2015 2016 2017

dat

a &

inte

rnet

su

bsc

rib

ers

124,179 152,782 166,797

205,082 211,566

271,252 316,816

641,152

719,619

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

DEC

-15

JAN

-16

FEB

-16

MA

R-1

6

AP

R-1

6

MA

Y-1

6

JUN

-16

JUL-

16

AU

G-1

6

SEP

-16

OC

T-1

6

NO

V-1

6

DEC

-16

JAN

-17

FEB

-17

MA

R-1

7

AP

R-1

7

MA

Y-1

7

JUN

-17

JUL-

17

AU

G-1

7

SEP

-17

OC

T-1

7

NO

V-1

7

DEC

-17

Nu

mb

ero

f su

bsc

rib

ers

12

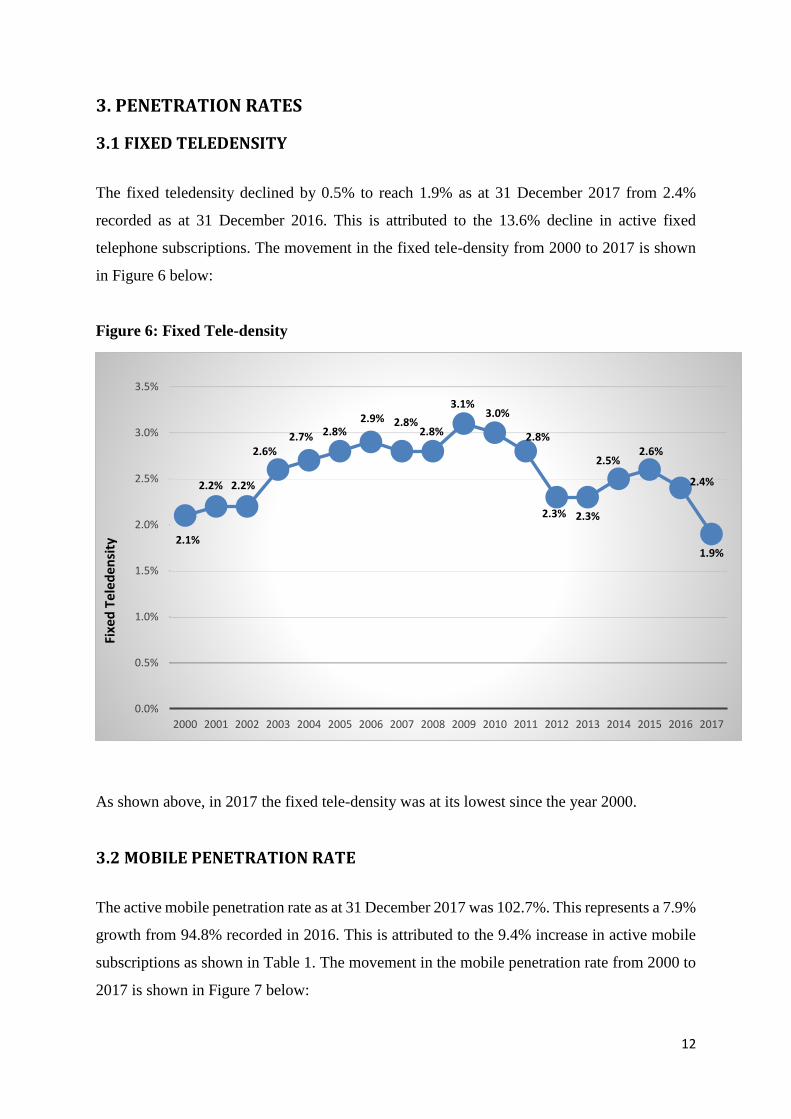

3. PENETRATION RATES

3.1 FIXED TELEDENSITY

The fixed teledensity declined by 0.5% to reach 1.9% as at 31 December 2017 from 2.4%

recorded as at 31 December 2016. This is attributed to the 13.6% decline in active fixed

telephone subscriptions. The movement in the fixed tele-density from 2000 to 2017 is shown

in Figure 6 below:

Figure 6: Fixed Tele-density

As shown above, in 2017 the fixed tele-density was at its lowest since the year 2000.

3.2 MOBILE PENETRATION RATE

The active mobile penetration rate as at 31 December 2017 was 102.7%. This represents a 7.9%

growth from 94.8% recorded in 2016. This is attributed to the 9.4% increase in active mobile

subscriptions as shown in Table 1. The movement in the mobile penetration rate from 2000 to

2017 is shown in Figure 7 below:

2.1%

2.2% 2.2%

2.6%2.7% 2.8%

2.9% 2.8%2.8%

3.1%3.0%

2.8%

2.3% 2.3%

2.5%2.6%

2.4%

1.9%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Fixe

d T

ele

de

nsi

ty

13

Figure 7: Mobile penetration rate

As shown above, the active mobile penetration rate has been consistently increasing in line

with the growth in active mobile subscriptions.

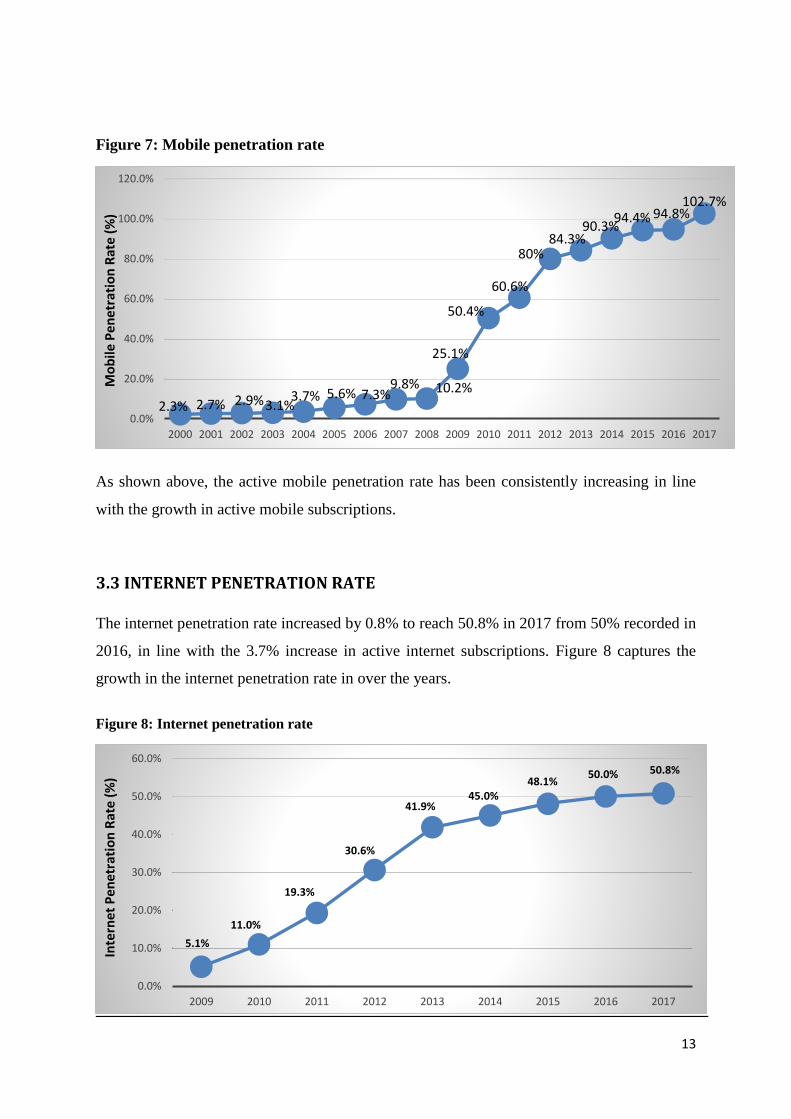

3.3 INTERNET PENETRATION RATE

The internet penetration rate increased by 0.8% to reach 50.8% in 2017 from 50% recorded in

2016, in line with the 3.7% increase in active internet subscriptions. Figure 8 captures the

growth in the internet penetration rate in over the years.

Figure 8: Internet penetration rate

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

94.4%90.3%

84.3%80%

60.6%

50.4%

25.1%

10.2%

2.3% 2.7% 2.9%3.1%3.7% 5.6% 7.3%

9.8%Mo

bile

Pe

net

rati

on

Rat

e (

%) 94.8%

102.7%

5.1%

11.0%

19.3%

30.6%

41.9%45.0%

48.1%50.0% 50.8%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

2009 2010 2011 2012 2013 2014 2015 2016 2017

Inte

rnet

Pe

net

rati

on

Rat

e (

%)

14

As shown in Figure 8 above, the internet penetration rate has been consistently increasing in

line with the growing number of active internet and data subscriptions. Demand for internet

and data services in the country is expected to continue growing as the internet coverage,

variety of services and the availability and accessibility of devices improves.

4. TRAFFIC AND USAGE PATTERNS

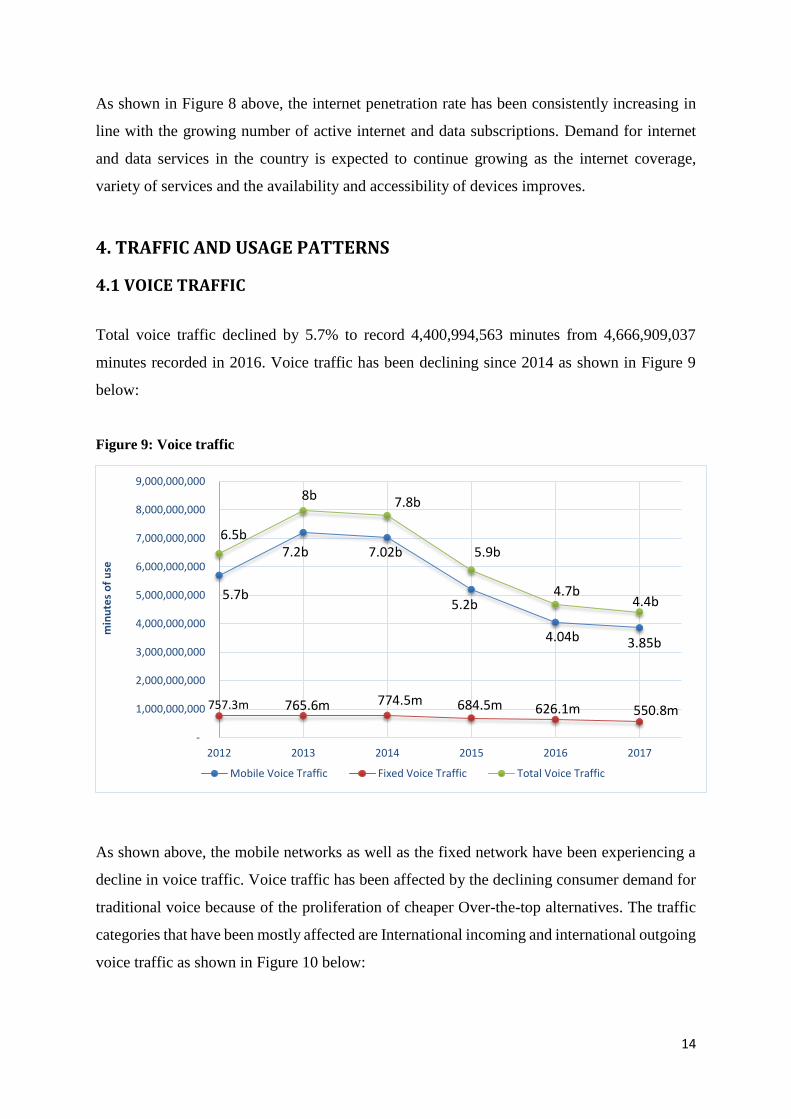

4.1 VOICE TRAFFIC

Total voice traffic declined by 5.7% to record 4,400,994,563 minutes from 4,666,909,037

minutes recorded in 2016. Voice traffic has been declining since 2014 as shown in Figure 9

below:

Figure 9: Voice traffic

As shown above, the mobile networks as well as the fixed network have been experiencing a

decline in voice traffic. Voice traffic has been affected by the declining consumer demand for

traditional voice because of the proliferation of cheaper Over-the-top alternatives. The traffic

categories that have been mostly affected are International incoming and international outgoing

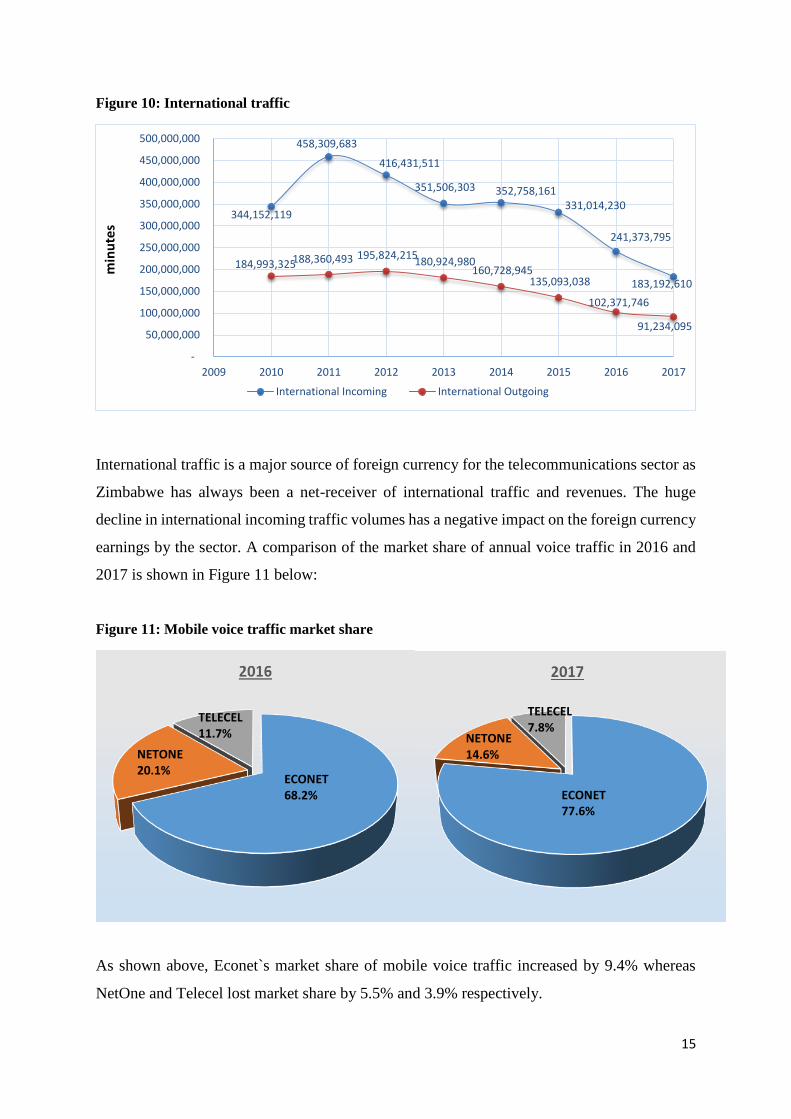

voice traffic as shown in Figure 10 below:

-

1,000,000,000

2,000,000,000

3,000,000,000

4,000,000,000

5,000,000,000

6,000,000,000

7,000,000,000

8,000,000,000

9,000,000,000

2012 2013 2014 2015 2016 2017

min

ute

s o

f u

se

Mobile Voice Traffic Fixed Voice Traffic Total Voice Traffic

4.4b 4.7b

5.9b

7.8b 8b

6.5b

5.7b

7.2b 7.02b

5.2b

4.04b 3.85b

757.3m

765.6m 774.5m 684.5m 626.1m 550.8m

15

Figure 10: International traffic

International traffic is a major source of foreign currency for the telecommunications sector as

Zimbabwe has always been a net-receiver of international traffic and revenues. The huge

decline in international incoming traffic volumes has a negative impact on the foreign currency

earnings by the sector. A comparison of the market share of annual voice traffic in 2016 and

2017 is shown in Figure 11 below:

Figure 11: Mobile voice traffic market share

As shown above, Econet`s market share of mobile voice traffic increased by 9.4% whereas

NetOne and Telecel lost market share by 5.5% and 3.9% respectively.

344,152,119

458,309,683

416,431,511

351,506,303 352,758,161 331,014,230

241,373,795

183,192,610

184,993,325 188,360,493 195,824,215 180,924,980

160,728,945 135,093,038

102,371,746

91,234,095

-

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

350,000,000

400,000,000

450,000,000

500,000,000

2009 2010 2011 2012 2013 2014 2015 2016 2017

International Incoming International Outgoing

min

ute

s

ECONET 68.2%

NETONE 20.1%

TELECEL 11.7%

ECONET 77.6%

NETONE 14.6%

TELECEL 7.8%

16

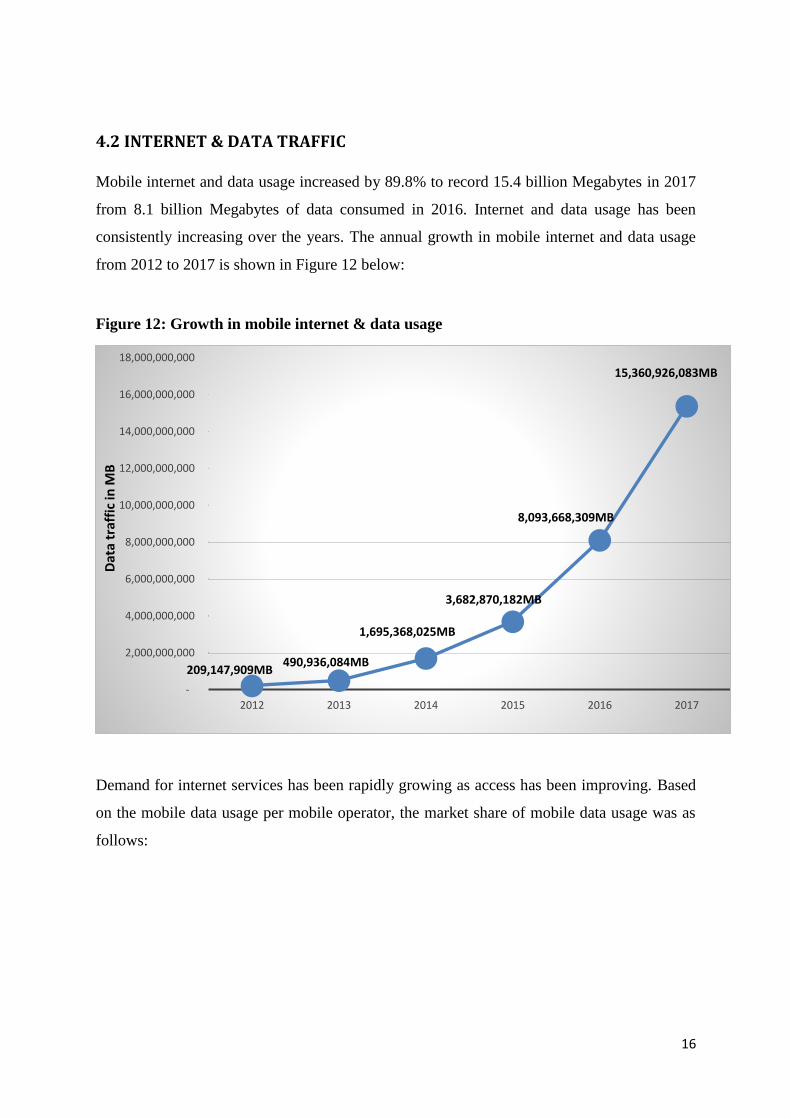

4.2 INTERNET & DATA TRAFFIC

Mobile internet and data usage increased by 89.8% to record 15.4 billion Megabytes in 2017

from 8.1 billion Megabytes of data consumed in 2016. Internet and data usage has been

consistently increasing over the years. The annual growth in mobile internet and data usage

from 2012 to 2017 is shown in Figure 12 below:

Figure 12: Growth in mobile internet & data usage

Demand for internet services has been rapidly growing as access has been improving. Based

on the mobile data usage per mobile operator, the market share of mobile data usage was as

follows:

-

2,000,000,000

4,000,000,000

6,000,000,000

8,000,000,000

10,000,000,000

12,000,000,000

14,000,000,000

16,000,000,000

18,000,000,000

2012 2013 2014 2015 2016 2017

Dat

atr

affi

c in

MB

1,695,368,025MB

490,936,084MB

3,682,870,182MB

8,093,668,309MB

209,147,909MB

15,360,926,083MB

17

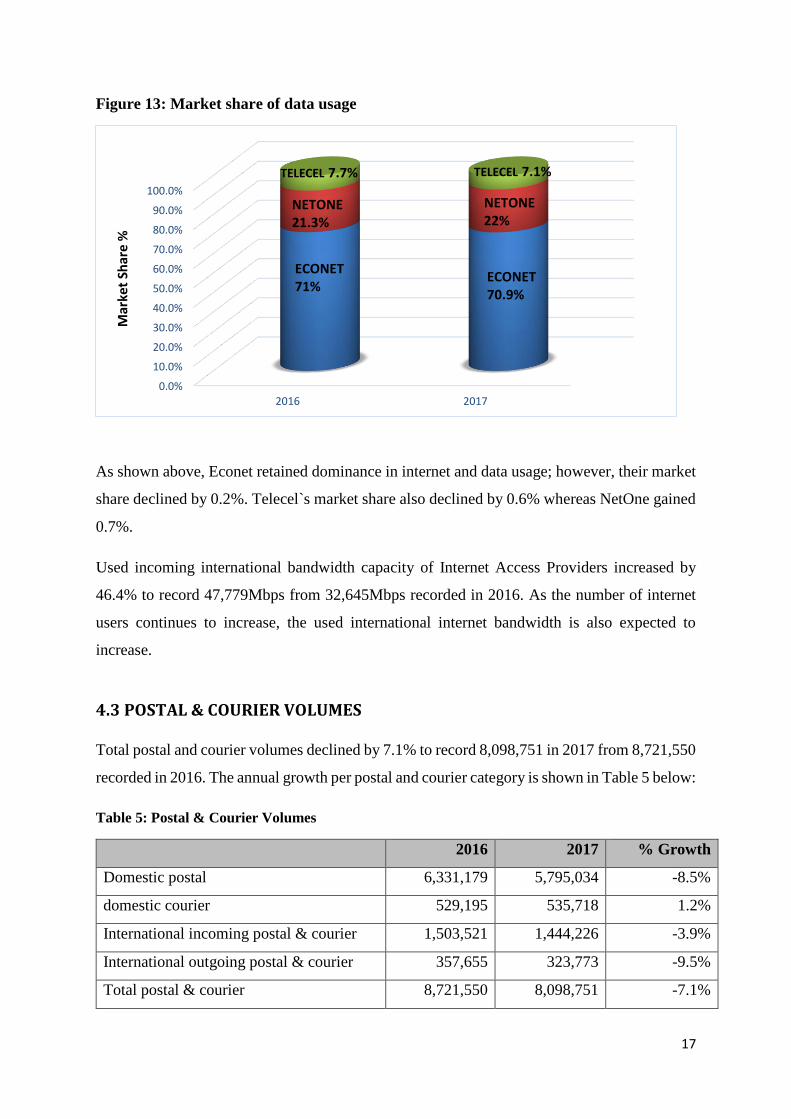

Figure 13: Market share of data usage

As shown above, Econet retained dominance in internet and data usage; however, their market

share declined by 0.2%. Telecel`s market share also declined by 0.6% whereas NetOne gained

0.7%.

Used incoming international bandwidth capacity of Internet Access Providers increased by

46.4% to record 47,779Mbps from 32,645Mbps recorded in 2016. As the number of internet

users continues to increase, the used international internet bandwidth is also expected to

increase.

4.3 POSTAL & COURIER VOLUMES

Total postal and courier volumes declined by 7.1% to record 8,098,751 in 2017 from 8,721,550

recorded in 2016. The annual growth per postal and courier category is shown in Table 5 below:

Table 5: Postal & Courier Volumes

2016 2017 % Growth

Domestic postal 6,331,179 5,795,034 -8.5%

domestic courier 529,195 535,718 1.2%

International incoming postal & courier 1,503,521 1,444,226 -3.9%

International outgoing postal & courier 357,655 323,773 -9.5%

Total postal & courier 8,721,550 8,098,751 -7.1%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

2016 2017

ECONET71%

NETONE 21.3%

TELECEL 7.7%

ECONET70.9%

NETONE22%

TELECEL 7.1%

Mar

ket

Shar

e %

18

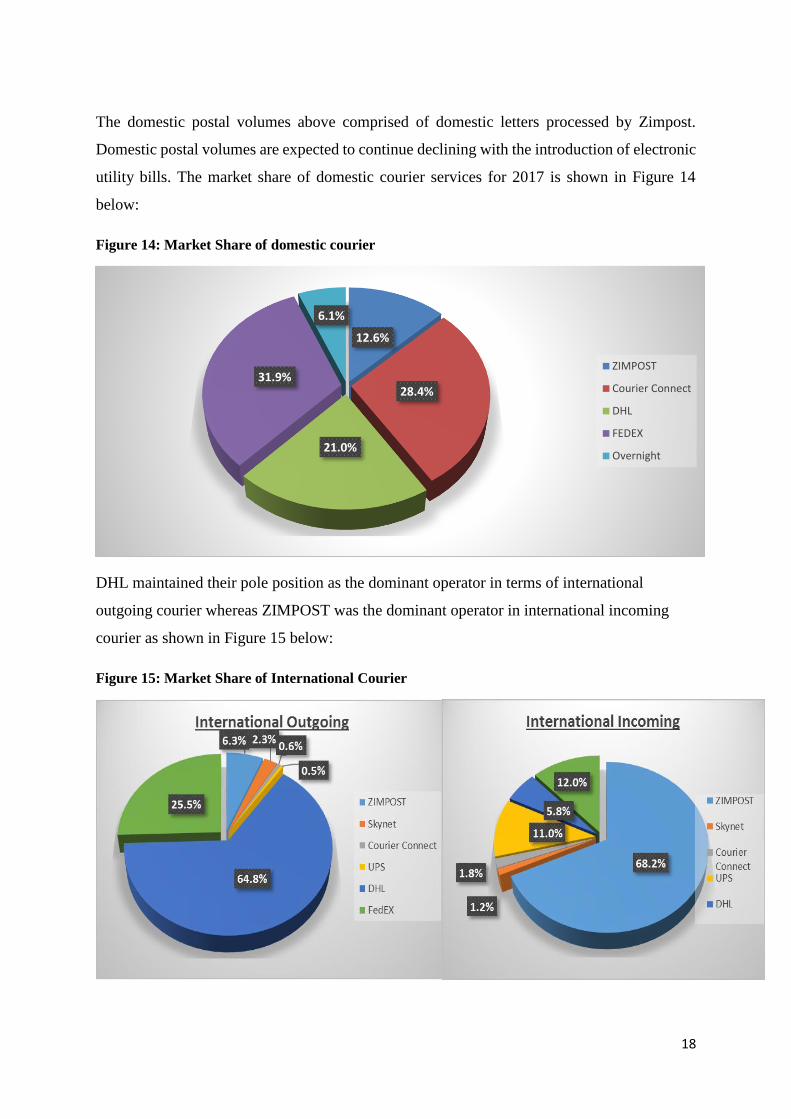

The domestic postal volumes above comprised of domestic letters processed by Zimpost.

Domestic postal volumes are expected to continue declining with the introduction of electronic

utility bills. The market share of domestic courier services for 2017 is shown in Figure 14

below:

Figure 14: Market Share of domestic courier

DHL maintained their pole position as the dominant operator in terms of international

outgoing courier whereas ZIMPOST was the dominant operator in international incoming

courier as shown in Figure 15 below:

Figure 15: Market Share of International Courier

12.6%

28.4%

21.0%

31.9%

6.1%

ZIMPOST

Courier Connect

DHL

FEDEX

Overnight

19

ZIMPOST`s dominance in international incoming courier is attributable to the fact that they

are cheapest channel for receiving courier items in Zimbabwe, especially when purchasing

goods on e-commerce sites such as Aliexpress.

5. REVENUES & INVESTMENT

5.1 MOBILE

Mobile revenue, costs and investment information is shown in Table 6 below:

Table 6: Mobile Revenues, Investment & Costs

2016 2017 % Growth

Revenues $722,934,718 $849,880,489 17.6%

Operating costs $503,441,339 $527,345,083 4.7%

Investment $187,677,658 $100,853,947 -46.3%

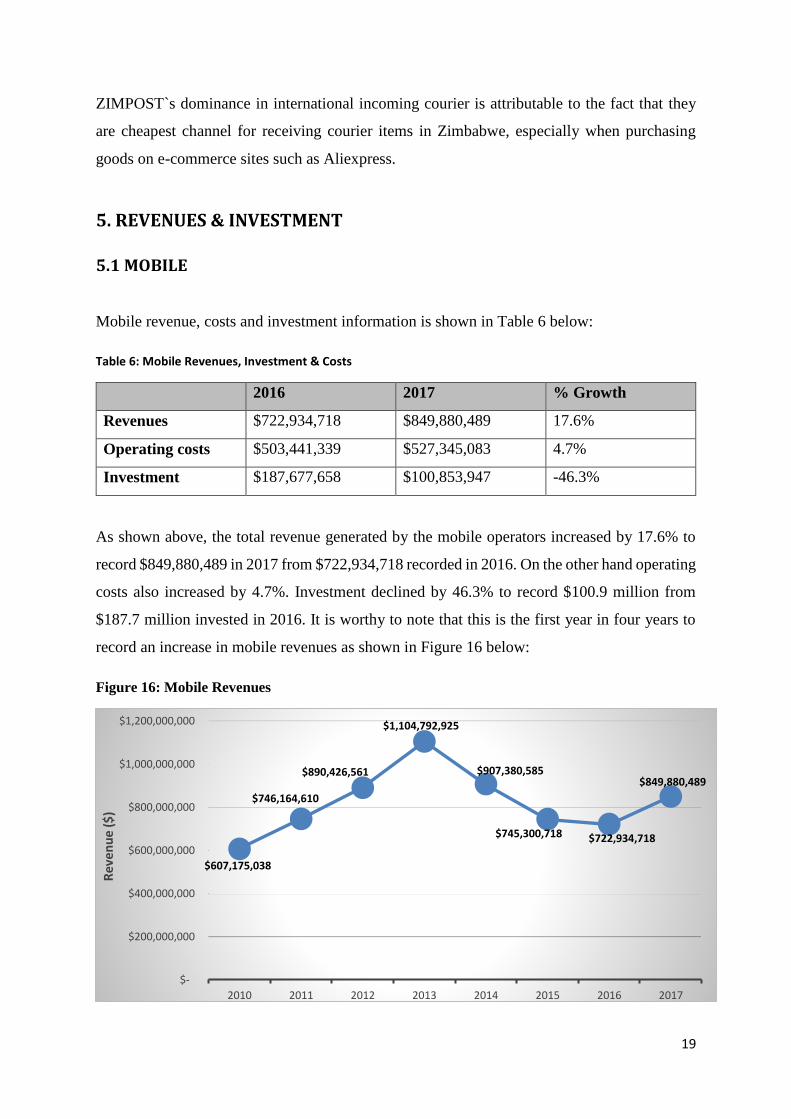

As shown above, the total revenue generated by the mobile operators increased by 17.6% to

record $849,880,489 in 2017 from $722,934,718 recorded in 2016. On the other hand operating

costs also increased by 4.7%. Investment declined by 46.3% to record $100.9 million from

$187.7 million invested in 2016. It is worthy to note that this is the first year in four years to

record an increase in mobile revenues as shown in Figure 16 below:

Figure 16: Mobile Revenues

$607,175,038

$746,164,610

$890,426,561

$1,104,792,925

$907,380,585

$745,300,718 $722,934,718

$849,880,489

$-

$200,000,000

$400,000,000

$600,000,000

$800,000,000

$1,000,000,000

$1,200,000,000

2010 2011 2012 2013 2014 2015 2016 2017

Rev

enu

e ($

)

20

The growth in mobile revenues is attributable to the growth in mobile internet and data usage

as well as mobile money.

5.3 IAP REVENUES & INVESTMENT

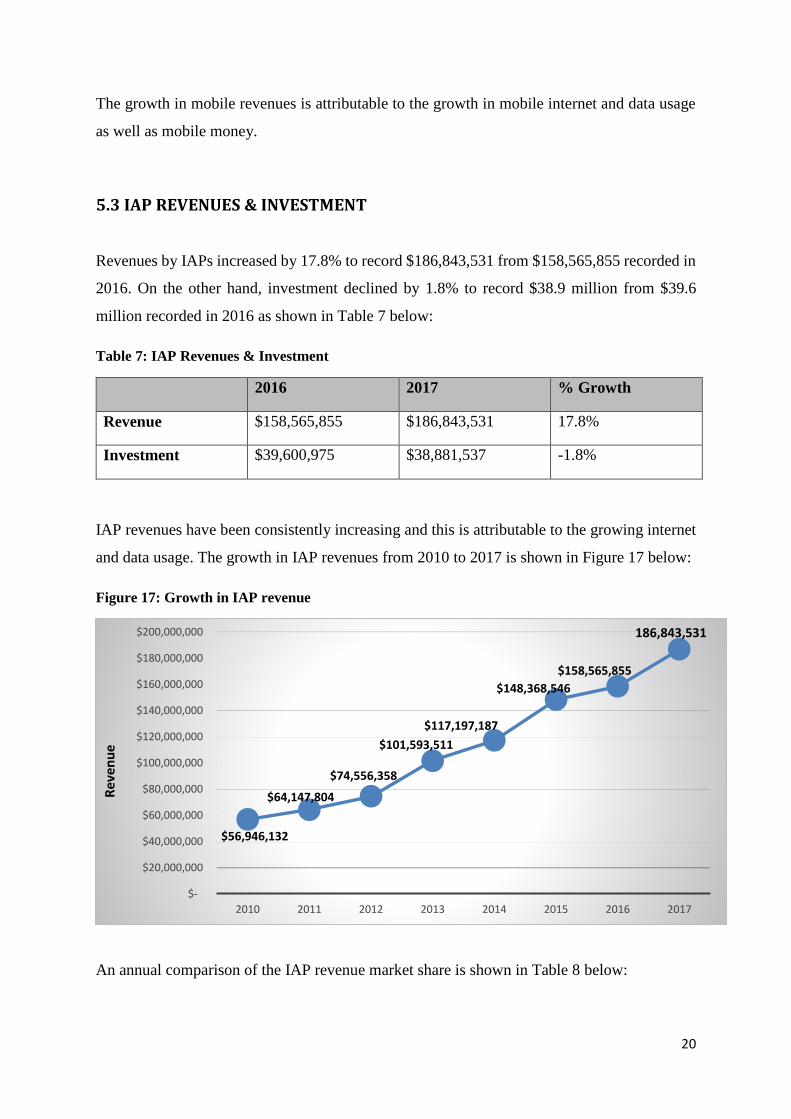

Revenues by IAPs increased by 17.8% to record $186,843,531 from $158,565,855 recorded in

2016. On the other hand, investment declined by 1.8% to record $38.9 million from $39.6

million recorded in 2016 as shown in Table 7 below:

Table 7: IAP Revenues & Investment

2016 2017 % Growth

Revenue $158,565,855 $186,843,531 17.8%

Investment $39,600,975 $38,881,537 -1.8%

IAP revenues have been consistently increasing and this is attributable to the growing internet

and data usage. The growth in IAP revenues from 2010 to 2017 is shown in Figure 17 below:

Figure 17: Growth in IAP revenue

An annual comparison of the IAP revenue market share is shown in Table 8 below:

$-

$20,000,000

$40,000,000

$60,000,000

$80,000,000

$100,000,000

$120,000,000

$140,000,000

$160,000,000

$180,000,000

$200,000,000

2010 2011 2012 2013 2014 2015 2016 2017

Re

ven

ue

$56,946,132

$64,147,804

$74,556,358

$101,593,511

$117,197,187

$148,368,546

$158,565,855

186,843,531

21

Table 8: IAP Revenues Market Share

Market Share of

IAP Revenues 2016

Market Share of

IAP Revenues 2017

% Change

Liquid 50.3% 52.6% 2.3%

TelOne 22.9% 23.0% 0.1%

Powertel 16.8% 13.9% -2.9%

Dandemutande 5.2% 6.1% 0.9%

Africom 3.1% 3.0% -0.1%

Telecontract 1.5% 1.3% -0.2%

Aquiva 0.2% 0.2% 0.0%

Aptics* 0.0% 0.0% 0.0%

Total 100% 100% 0.0%

Powertel, Africom and Telecontract lost market share in line with the decline in their annual

revenues.

6. MOBILE MONEY

6.1 SUBSCRIPTIONS

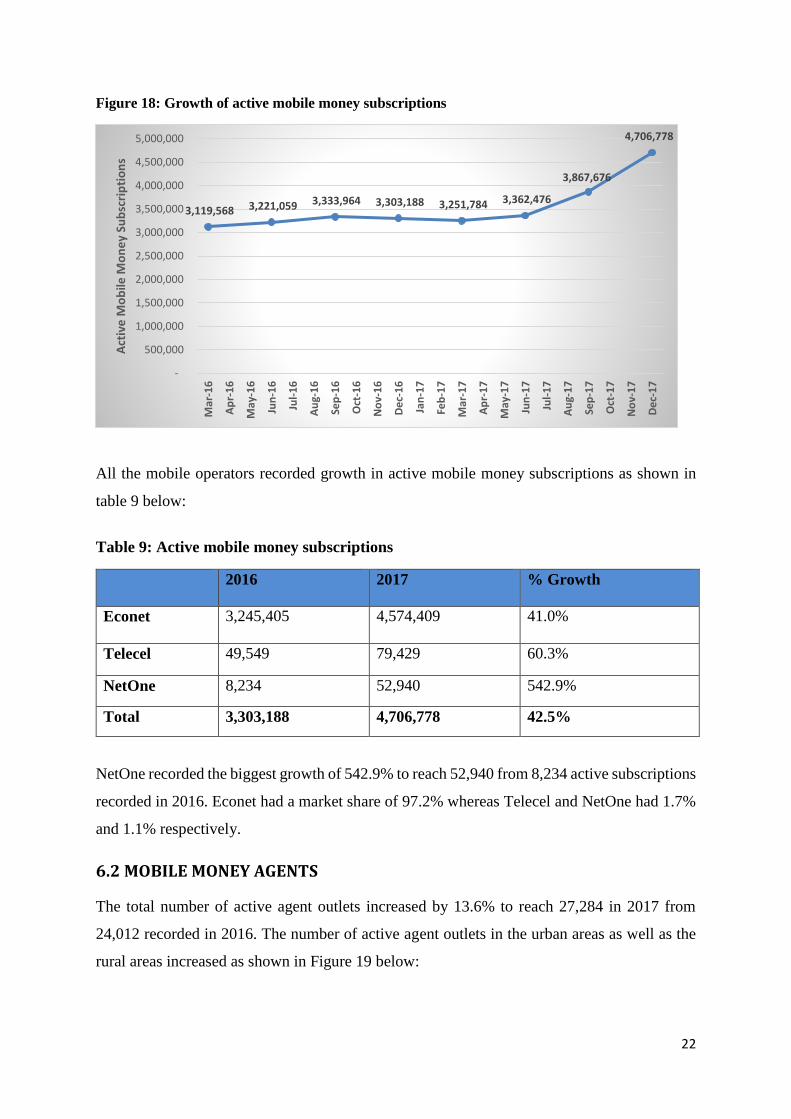

The total number of active mobile money subscriptions increased by 42.5% to reach 4,706,778

in 2017 from 3,303,188 recorded in 2016. Big leaps in active mobile money subscriptions

were experienced in 2017. Mobile money provided an effective alternative to cash for making

payments in the midst of the liquidity crisis. The growth in mobile money subscriptions is

shown in Figure 18 below:

22

Figure 18: Growth of active mobile money subscriptions

All the mobile operators recorded growth in active mobile money subscriptions as shown in

table 9 below:

Table 9: Active mobile money subscriptions

2016 2017 % Growth

Econet 3,245,405 4,574,409

41.0%

Telecel 49,549 79,429 60.3%

NetOne 8,234 52,940 542.9%

Total 3,303,188 4,706,778 42.5%

NetOne recorded the biggest growth of 542.9% to reach 52,940 from 8,234 active subscriptions

recorded in 2016. Econet had a market share of 97.2% whereas Telecel and NetOne had 1.7%

and 1.1% respectively.

6.2 MOBILE MONEY AGENTS

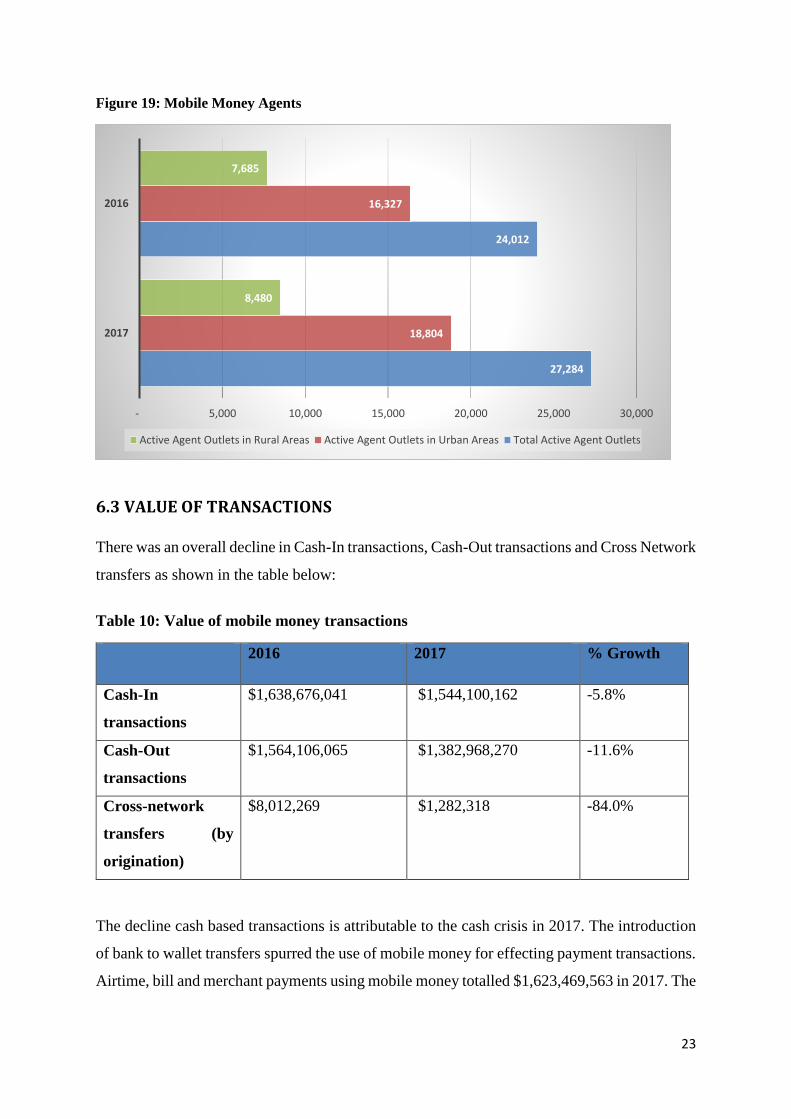

The total number of active agent outlets increased by 13.6% to reach 27,284 in 2017 from

24,012 recorded in 2016. The number of active agent outlets in the urban areas as well as the

rural areas increased as shown in Figure 19 below:

3,119,568 3,221,059 3,333,964 3,303,188 3,251,784 3,362,476

3,867,676

4,706,778

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

De

c-1

6

Jan

-17

Feb

-17

Mar

-17

Ap

r-1

7

May

-17

Jun

-17

Jul-

17

Au

g-1

7

Sep

-17

Oct

-17

No

v-1

7

De

c-1

7

Act

ive

Mo

bile

Mo

ne

y Su

bsc

rip

tio

ns

23

Figure 19: Mobile Money Agents

6.3 VALUE OF TRANSACTIONS

There was an overall decline in Cash-In transactions, Cash-Out transactions and Cross Network

transfers as shown in the table below:

Table 10: Value of mobile money transactions

2016 2017 % Growth

Cash-In

transactions

$1,638,676,041 $1,544,100,162 -5.8%

Cash-Out

transactions

$1,564,106,065 $1,382,968,270 -11.6%

Cross-network

transfers (by

origination)

$8,012,269 $1,282,318 -84.0%

The decline cash based transactions is attributable to the cash crisis in 2017. The introduction

of bank to wallet transfers spurred the use of mobile money for effecting payment transactions.

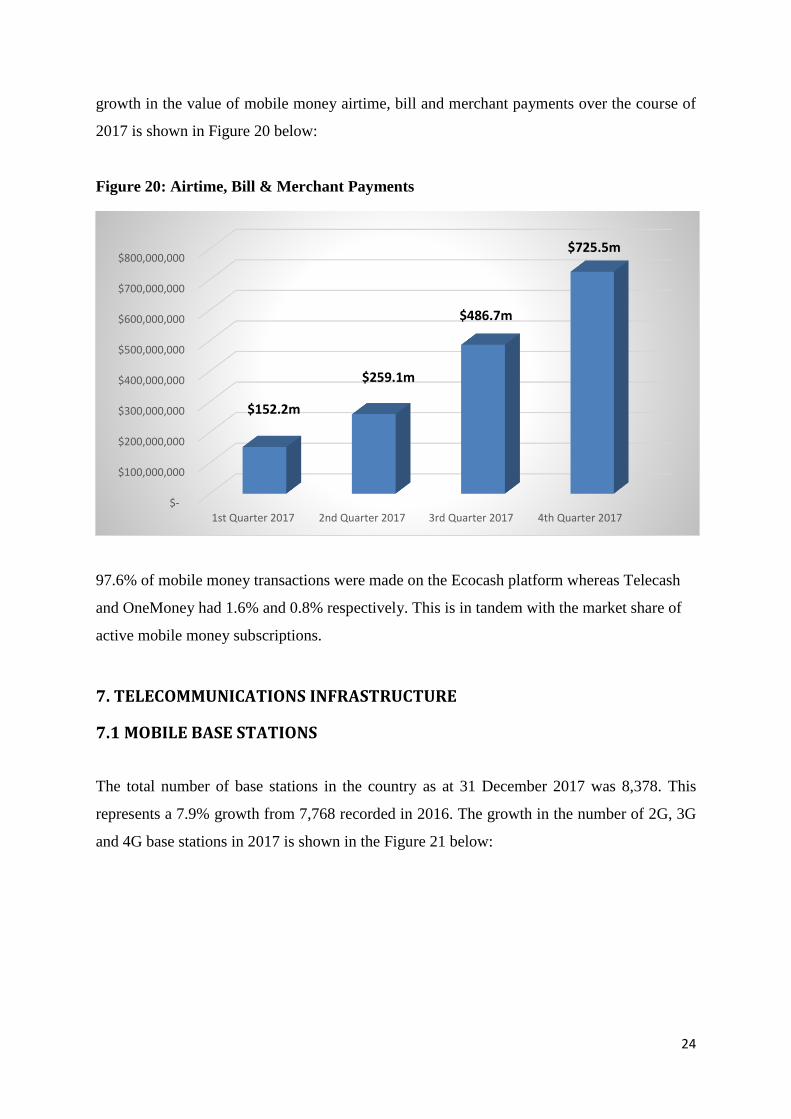

Airtime, bill and merchant payments using mobile money totalled $1,623,469,563 in 2017. The

27,284

24,012

18,804

16,327

8,480

7,685

- 5,000 10,000 15,000 20,000 25,000 30,000

2017

2016

Active Agent Outlets in Rural Areas Active Agent Outlets in Urban Areas Total Active Agent Outlets

24

growth in the value of mobile money airtime, bill and merchant payments over the course of

2017 is shown in Figure 20 below:

Figure 20: Airtime, Bill & Merchant Payments

97.6% of mobile money transactions were made on the Ecocash platform whereas Telecash

and OneMoney had 1.6% and 0.8% respectively. This is in tandem with the market share of

active mobile money subscriptions.

7. TELECOMMUNICATIONS INFRASTRUCTURE

7.1 MOBILE BASE STATIONS

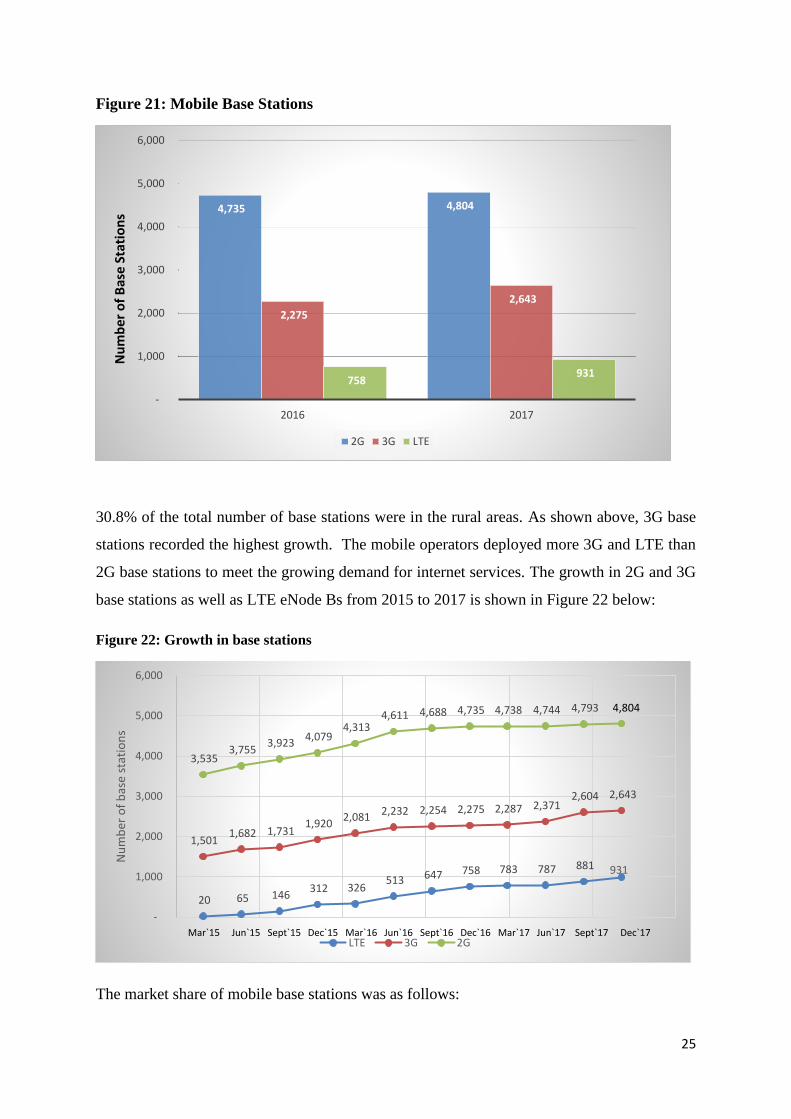

The total number of base stations in the country as at 31 December 2017 was 8,378. This

represents a 7.9% growth from 7,768 recorded in 2016. The growth in the number of 2G, 3G

and 4G base stations in 2017 is shown in the Figure 21 below:

$-

$100,000,000

$200,000,000

$300,000,000

$400,000,000

$500,000,000

$600,000,000

$700,000,000

$800,000,000

1st Quarter 2017 2nd Quarter 2017 3rd Quarter 2017 4th Quarter 2017

$152.2m

$259.1m

$486.7m

$725.5m

25

Figure 21: Mobile Base Stations

30.8% of the total number of base stations were in the rural areas. As shown above, 3G base

stations recorded the highest growth. The mobile operators deployed more 3G and LTE than

2G base stations to meet the growing demand for internet services. The growth in 2G and 3G

base stations as well as LTE eNode Bs from 2015 to 2017 is shown in Figure 22 below:

Figure 22: Growth in base stations

The market share of mobile base stations was as follows:

4,735 4,804

2,275

2,643

758 931

-

1,000

2,000

3,000

4,000

5,000

6,000

2016 2017

2G 3G LTE

Nu

mb

er o

f B

ase

Stat

ion

s

20 65 146 312 326

513 647 758 783 787 881

1,501 1,682 1,731

1,920 2,081

2,232 2,254 2,275 2,287 2,371 2,604 2,643

3,535 3,755

3,923 4,079

4,313 4,611 4,688 4,735 4,738 4,744 4,793

-

1,000

2,000

3,000

4,000

5,000

6,000

Nu

mb

er o

f b

ase

stat

ion

s

LTE 3G 2GMar`15 Jun`15 Sept`15 Dec`15 Mar`16 Jun`16 Sept`16 Dec`16 Mar`17 Jun`17 Sept`17 Dec`17

931

4,804

26

Figure 23: Market share of mobile base stations

Econet had the biggest market share of 2G base stations, 3G base stations as well as LTE eNode

Bs. There was no major change in the market share of base stations, save for the entry of Telecel

into the LTE market with a market share of 1%.

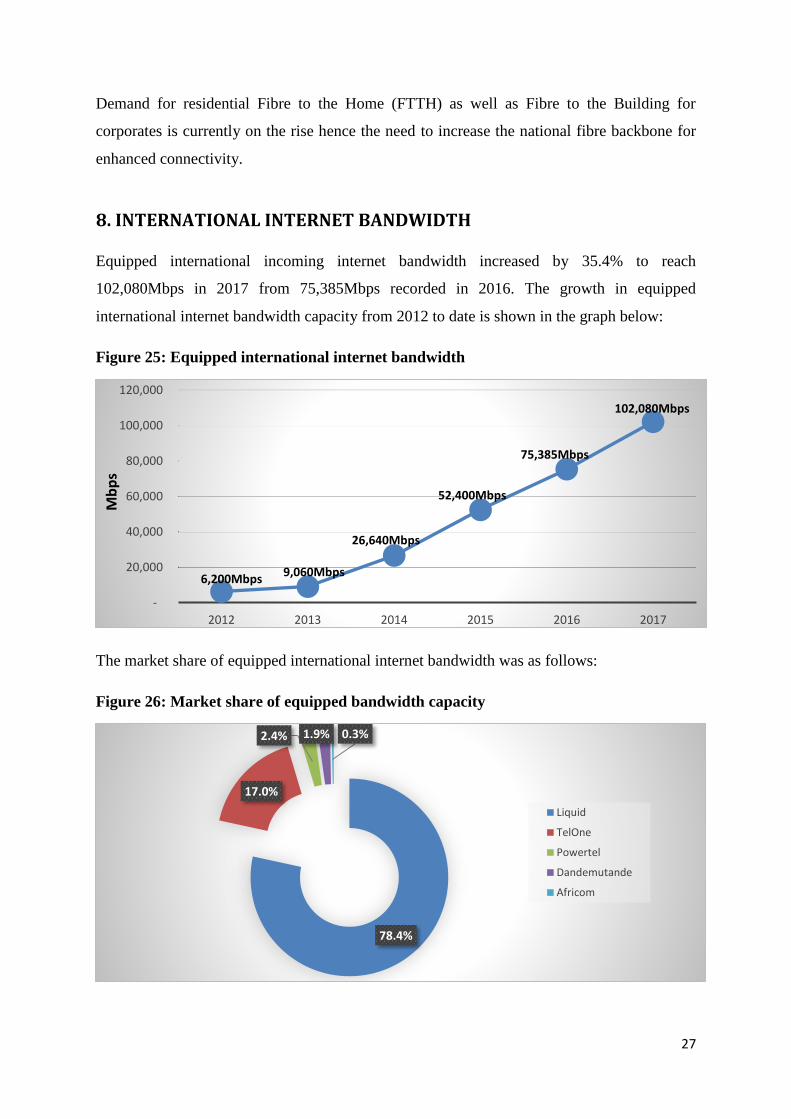

7.2 NATIONAL BACKBONE FIBRE LENGTH

The total national backbone fibre length as at 31 December 2017 was 8,765km up from

7,707km recorded as at 31 December 2016. The growth in national backbone fibre length from

2013 to 2017 is shown in Figure 24 below:

Figure 24: National backbone fibre length

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2013 2014 2015 2016 2017

Fib

re le

ngt

h (

km)

6,481km 6,641km6,964km

7,707km

8,765km

27

Demand for residential Fibre to the Home (FTTH) as well as Fibre to the Building for

corporates is currently on the rise hence the need to increase the national fibre backbone for

enhanced connectivity.

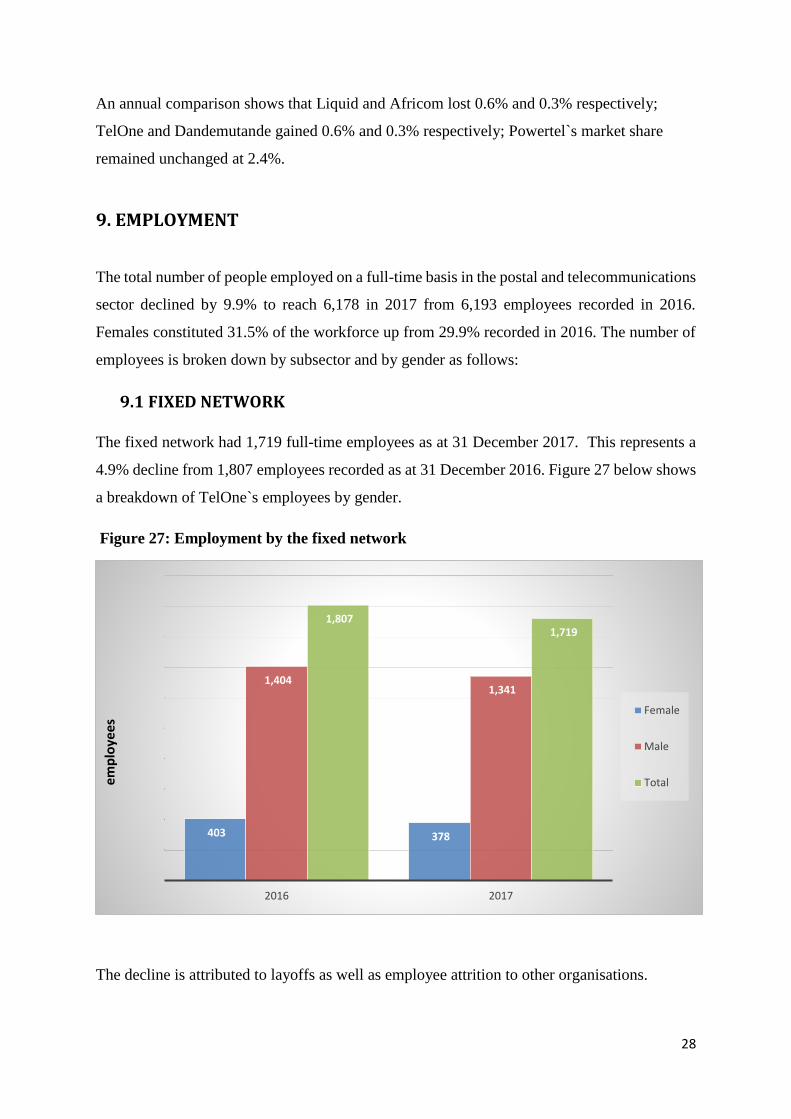

8. INTERNATIONAL INTERNET BANDWIDTH

Equipped international incoming internet bandwidth increased by 35.4% to reach

102,080Mbps in 2017 from 75,385Mbps recorded in 2016. The growth in equipped

international internet bandwidth capacity from 2012 to date is shown in the graph below:

Figure 25: Equipped international internet bandwidth

The market share of equipped international internet bandwidth was as follows:

Figure 26: Market share of equipped bandwidth capacity

-

20,000

40,000

60,000

80,000

100,000

120,000

2012 2013 2014 2015 2016 2017

6,200Mbps

Mb

ps

9,060Mbps

26,640Mbps

52,400Mbps

75,385Mbps

102,080Mbps

78.4%

17.0%

2.4% 1.9% 0.3%

Liquid

TelOne

Powertel

Dandemutande

Africom

28

An annual comparison shows that Liquid and Africom lost 0.6% and 0.3% respectively;

TelOne and Dandemutande gained 0.6% and 0.3% respectively; Powertel`s market share

remained unchanged at 2.4%.

9. EMPLOYMENT

The total number of people employed on a full-time basis in the postal and telecommunications

sector declined by 9.9% to reach 6,178 in 2017 from 6,193 employees recorded in 2016.

Females constituted 31.5% of the workforce up from 29.9% recorded in 2016. The number of

employees is broken down by subsector and by gender as follows:

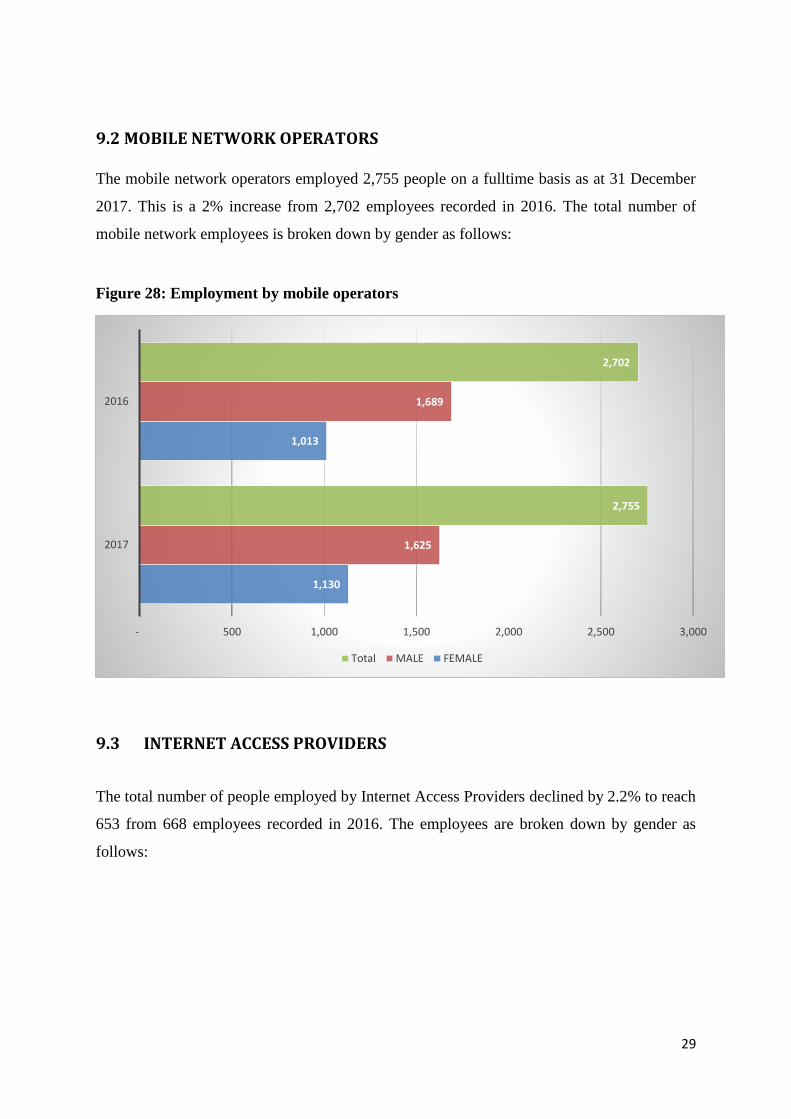

9.1 FIXED NETWORK

The fixed network had 1,719 full-time employees as at 31 December 2017. This represents a

4.9% decline from 1,807 employees recorded as at 31 December 2016. Figure 27 below shows

a breakdown of TelOne`s employees by gender.

Figure 27: Employment by the fixed network

The decline is attributed to layoffs as well as employee attrition to other organisations.

403 378

1,404 1,341

1,807 1,719

2016 2017

Female

Male

Totalemp

loye

es

29

9.2 MOBILE NETWORK OPERATORS

The mobile network operators employed 2,755 people on a fulltime basis as at 31 December

2017. This is a 2% increase from 2,702 employees recorded in 2016. The total number of

mobile network employees is broken down by gender as follows:

Figure 28: Employment by mobile operators

9.3 INTERNET ACCESS PROVIDERS

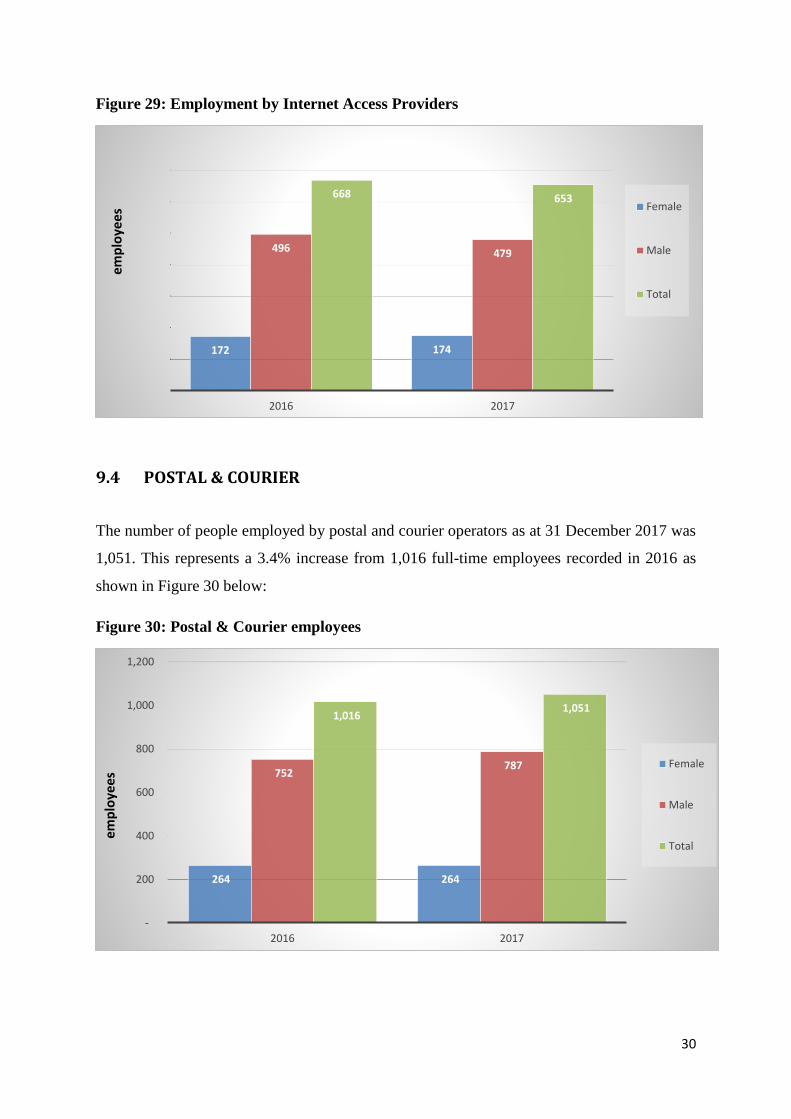

The total number of people employed by Internet Access Providers declined by 2.2% to reach

653 from 668 employees recorded in 2016. The employees are broken down by gender as

follows:

1,130

1,013

1,625

1,689

2,755

2,702

- 500 1,000 1,500 2,000 2,500 3,000

2017

2016

Total MALE FEMALE

30

Figure 29: Employment by Internet Access Providers

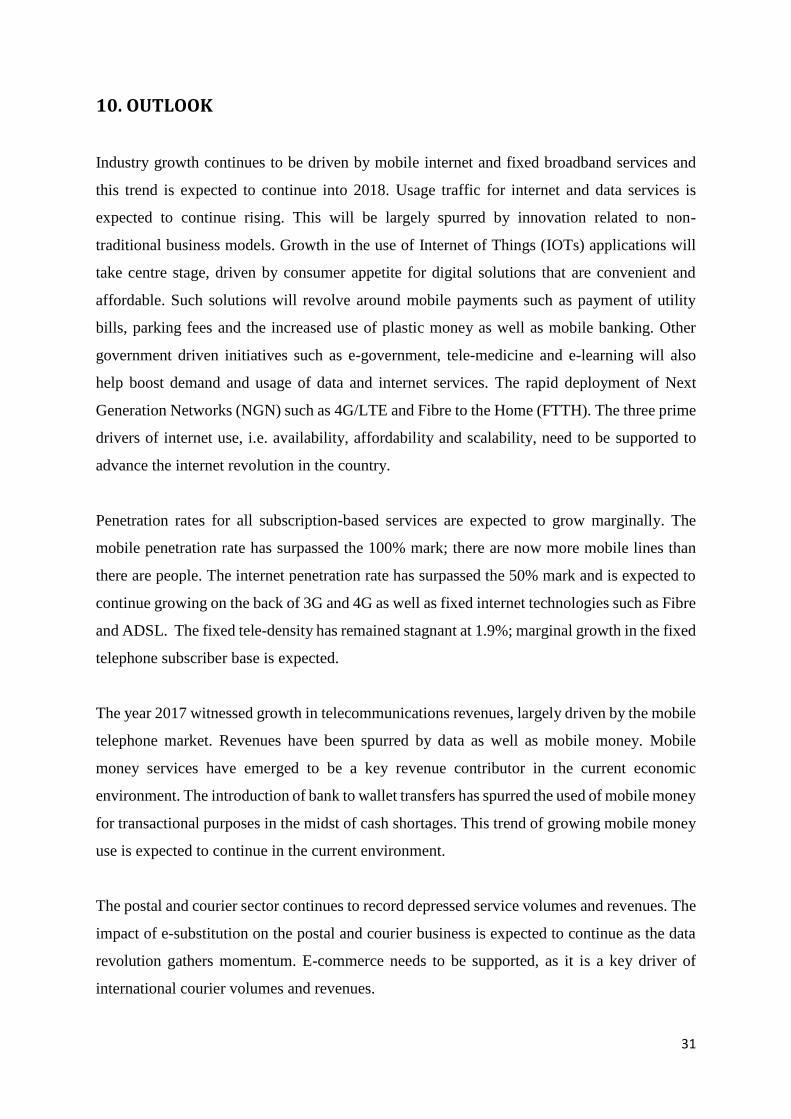

9.4 POSTAL & COURIER

The number of people employed by postal and courier operators as at 31 December 2017 was

1,051. This represents a 3.4% increase from 1,016 full-time employees recorded in 2016 as

shown in Figure 30 below:

Figure 30: Postal & Courier employees

172 174

496 479

668 653

2016 2017

Female

Male

Total

emp

loye

es

264 264

752 787

1,016 1,051

-

200

400

600

800

1,000

1,200

2016 2017

Female

Male

Total

emp

loye

es

31

10. OUTLOOK

Industry growth continues to be driven by mobile internet and fixed broadband services and

this trend is expected to continue into 2018. Usage traffic for internet and data services is

expected to continue rising. This will be largely spurred by innovation related to non-

traditional business models. Growth in the use of Internet of Things (IOTs) applications will

take centre stage, driven by consumer appetite for digital solutions that are convenient and

affordable. Such solutions will revolve around mobile payments such as payment of utility

bills, parking fees and the increased use of plastic money as well as mobile banking. Other

government driven initiatives such as e-government, tele-medicine and e-learning will also

help boost demand and usage of data and internet services. The rapid deployment of Next

Generation Networks (NGN) such as 4G/LTE and Fibre to the Home (FTTH). The three prime

drivers of internet use, i.e. availability, affordability and scalability, need to be supported to

advance the internet revolution in the country.

Penetration rates for all subscription-based services are expected to grow marginally. The

mobile penetration rate has surpassed the 100% mark; there are now more mobile lines than

there are people. The internet penetration rate has surpassed the 50% mark and is expected to

continue growing on the back of 3G and 4G as well as fixed internet technologies such as Fibre

and ADSL. The fixed tele-density has remained stagnant at 1.9%; marginal growth in the fixed

telephone subscriber base is expected.

The year 2017 witnessed growth in telecommunications revenues, largely driven by the mobile

telephone market. Revenues have been spurred by data as well as mobile money. Mobile

money services have emerged to be a key revenue contributor in the current economic

environment. The introduction of bank to wallet transfers has spurred the used of mobile money

for transactional purposes in the midst of cash shortages. This trend of growing mobile money

use is expected to continue in the current environment.

The postal and courier sector continues to record depressed service volumes and revenues. The

impact of e-substitution on the postal and courier business is expected to continue as the data

revolution gathers momentum. E-commerce needs to be supported, as it is a key driver of

international courier volumes and revenues.