Embed Size (px)

Citation preview

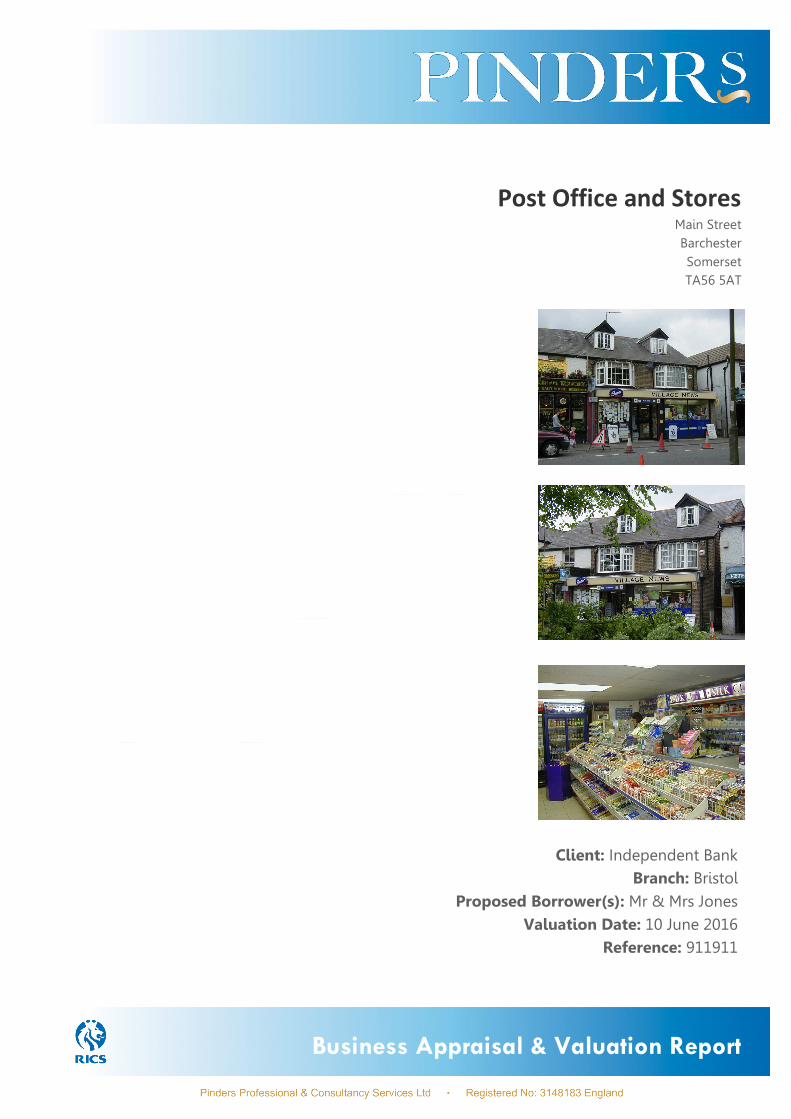

Post Office and Stores Main Street

Barchester

Somerset

TA56 5AT

Client: Independent Bank

Branch: Bristol

Proposed Borrower(s): Mr & Mrs Jones

Valuation Date: 10 June 2016

Reference: 911911

Business Appraisal & Valuation Report

911911 Page 2 of 34

Purpose and Limitations of Report

This report is provided to assist the instructing Client in consideration of the subject business/property in relation to the purpose stated opposite. Pinders accepts liability only to the Client and no other party, however involved. The report comprises a Business Appraisal & Valuation and expressly does not, in any way, constitute a building (structural) survey or a due diligence assessment. It remains the responsibility of the Client and, where appropriate, the borrower(s), to confirm the accuracy and validity of the information provided. Pinders accepts no liability to the Client, or any other party, should information relied upon in arriving at our opinions of value prove to be misrepresented, either fraudulently or otherwise. Whilst reference may be made within the report to aspects of tenure, title, planning and other statutory obligations, all such aspects should be verified by solicitors acting on behalf of the Client and/or the proposed borrower(s). The report is not intended as a substitute for the searches which would be expected in relation to any property/business acquisition or investment. We can confirm that neither the valuer nor Pinders has any known conflict of interest in accepting your instructions, nor any previous knowledge of the business or the potential borrower other than as specifically stated within the report. Unless specified elsewhere, this report has been prepared in accordance with our Conditions of Engagement and in accordance with The Royal Institution of Chartered Surveyors (RICS) Valuation - Professional Standards, for the sole purpose of assisting the Client and Proposed Borrower indicated above, in consideration of the subject business. The Explanatory Notes appended to this report also refer. Whilst the valuations contained within this report are expressed in a way which is suitable for lending purposes, any party, other than the Client shown above, wishing to rely upon the contents of the report for such purposes, will need to instruct Pinders to prepare and provide a further report, which addresses the party’s specific requirements. We can confirm that Pinders has in place appropriate Professional Indemnity Insurance in respect of this valuation. A copy certificate to this effect can be provided to the Client upon request.

911911 Page 3 of 34

Terms of Reference

Client: Independent Bank, Bristol

Proposed Borrower(s): Mr & Mrs Jones

Purpose of Report: An independent valuation in connection with the client's proposed purchase

Business Owner(s): Mr Evans

Person(s) Interviewed: Mr Evans

Previous Visits: None

Inspection Date: 1 June 2016

Valuation Date: 10 June 2016

Undertaken by: Stuart Planner MRICS (0088636)

Registered Valuer

Approved for Issue by: Wendy Webber MRICS (1129236)

Director

We appreciate that there may be many parties involved in consideration of this proposal and this report (inclusive of photographs, maps and site plans) will be provided by electronic mail in pdf file format (requires Acrobat Reader software) to facilitate easy transfer of information. However, we recommend that our lending clients rely only upon an authenticated hard copy of the report, which has the Pinders’ security seal attached below.

If you wish to discuss any aspect of this report, please contact our Operations team at:-

Pinder House

Central Milton Keynes MK9 1DS

Telephone: 01908 350500

Email: [email protected]

911911 Page 4 of 34

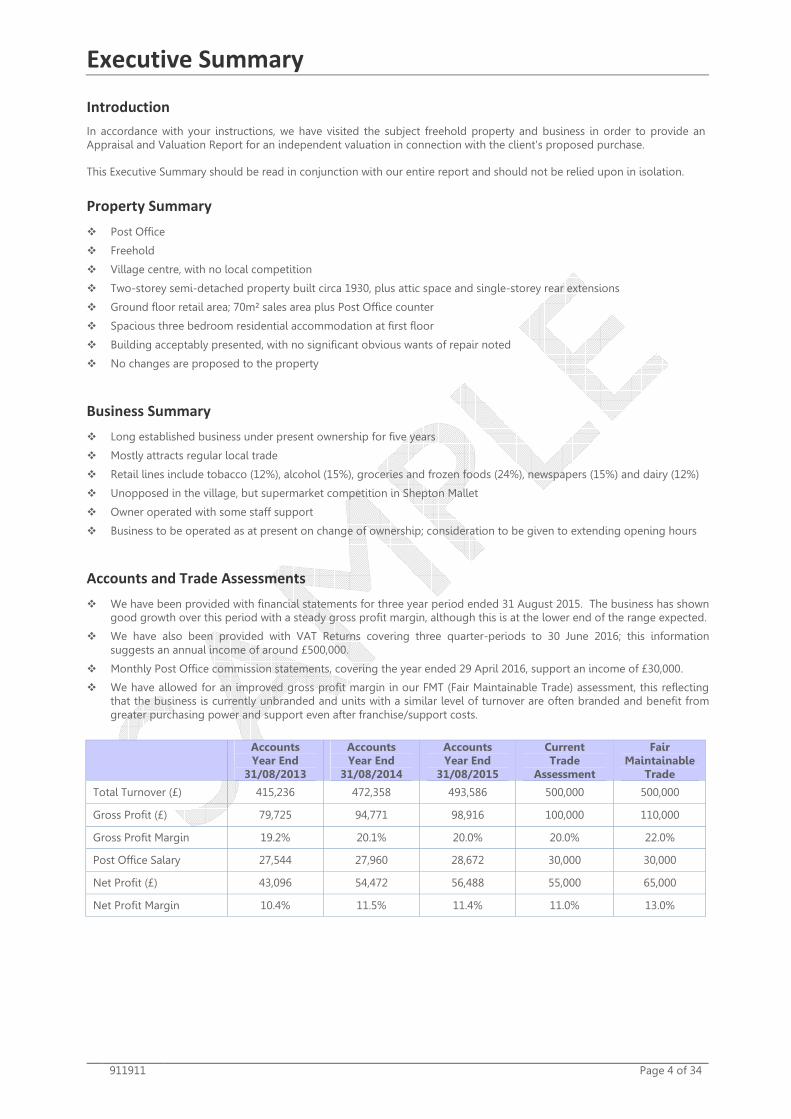

Executive Summary

Introduction

In accordance with your instructions, we have visited the subject freehold property and business in order to provide an Appraisal and Valuation Report for an independent valuation in connection with the client's proposed purchase. This Executive Summary should be read in conjunction with our entire report and should not be relied upon in isolation.

Property Summary

� Post Office

� Freehold

� Village centre, with no local competition

� Two-storey semi-detached property built circa 1930, plus attic space and single-storey rear extensions

� Ground floor retail area; 70m² sales area plus Post Office counter

� Spacious three bedroom residential accommodation at first floor

� Building acceptably presented, with no significant obvious wants of repair noted

� No changes are proposed to the property

Business Summary

� Long established business under present ownership for five years

� Mostly attracts regular local trade

� Retail lines include tobacco (12%), alcohol (15%), groceries and frozen foods (24%), newspapers (15%) and dairy (12%)

� Unopposed in the village, but supermarket competition in Shepton Mallet

� Owner operated with some staff support

� Business to be operated as at present on change of ownership; consideration to be given to extending opening hours

Accounts and Trade Assessments

� We have been provided with financial statements for three year period ended 31 August 2015. The business has shown good growth over this period with a steady gross profit margin, although this is at the lower end of the range expected.

� We have also been provided with VAT Returns covering three quarter-periods to 30 June 2016; this information suggests an annual income of around £500,000.

� Monthly Post Office commission statements, covering the year ended 29 April 2016, support an income of £30,000.

� We have allowed for an improved gross profit margin in our FMT (Fair Maintainable Trade) assessment, this reflecting that the business is currently unbranded and units with a similar level of turnover are often branded and benefit from greater purchasing power and support even after franchise/support costs.

Accounts

Year End 31/08/2013

Accounts Year End

31/08/2014

Accounts Year End

31/08/2015

Current Trade

Assessment

Fair Maintainable

Trade

Total Turnover (£) 415,236 472,358 493,586 500,000 500,000

Gross Profit (£) 79,725 94,771 98,916 100,000 110,000

Gross Profit Margin 19.2% 20.1% 20.0% 20.0% 22.0%

Post Office Salary 27,544 27,960 28,672 30,000 30,000

Net Profit (£) 43,096 54,472 56,488 55,000 65,000

Net Profit Margin 10.4% 11.5% 11.4% 11.0% 13.0%

911911 Page 5 of 34

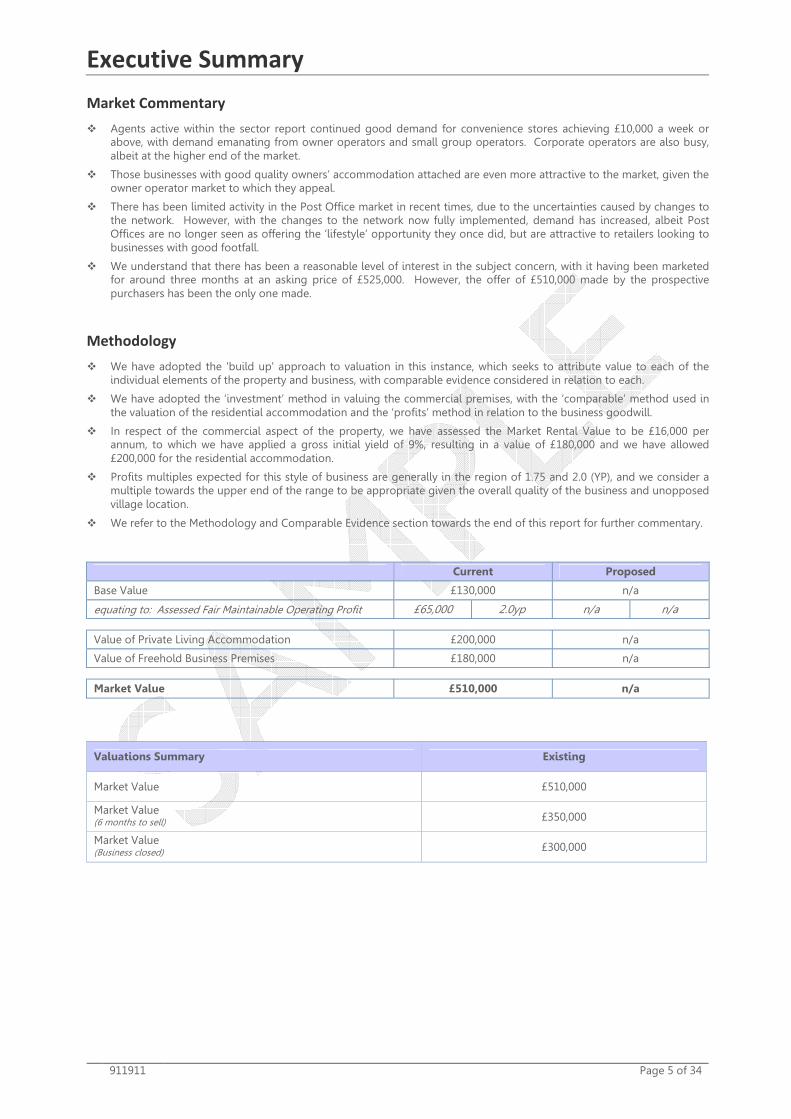

Executive Summary

Market Commentary

� Agents active within the sector report continued good demand for convenience stores achieving £10,000 a week or above, with demand emanating from owner operators and small group operators. Corporate operators are also busy, albeit at the higher end of the market.

� Those businesses with good quality owners’ accommodation attached are even more attractive to the market, given the owner operator market to which they appeal.

� There has been limited activity in the Post Office market in recent times, due to the uncertainties caused by changes to the network. However, with the changes to the network now fully implemented, demand has increased, albeit Post Offices are no longer seen as offering the ‘lifestyle’ opportunity they once did, but are attractive to retailers looking to businesses with good footfall.

� We understand that there has been a reasonable level of interest in the subject concern, with it having been marketed for around three months at an asking price of £525,000. However, the offer of £510,000 made by the prospective purchasers has been the only one made.

Methodology

� We have adopted the 'build up' approach to valuation in this instance, which seeks to attribute value to each of the individual elements of the property and business, with comparable evidence considered in relation to each.

� We have adopted the ‘investment’ method in valuing the commercial premises, with the ‘comparable’ method used in the valuation of the residential accommodation and the ‘profits’ method in relation to the business goodwill.

� In respect of the commercial aspect of the property, we have assessed the Market Rental Value to be £16,000 per annum, to which we have applied a gross initial yield of 9%, resulting in a value of £180,000 and we have allowed £200,000 for the residential accommodation.

� Profits multiples expected for this style of business are generally in the region of 1.75 and 2.0 (YP), and we consider a multiple towards the upper end of the range to be appropriate given the overall quality of the business and unopposed village location.

� We refer to the Methodology and Comparable Evidence section towards the end of this report for further commentary.

Current Proposed

Base Value £130,000 n/a

equating to: Assessed Fair Maintainable Operating Profit £65,000 2.0yp n/a n/a

Value of Private Living Accommodation £200,000 n/a

Value of Freehold Business Premises £180,000 n/a

Market Value £510,000 n/a

Valuations Summary Existing

Market Value £510,000

Market Value (6 months to sell)

£350,000

Market Value (Business closed)

£300,000

911911 Page 6 of 34

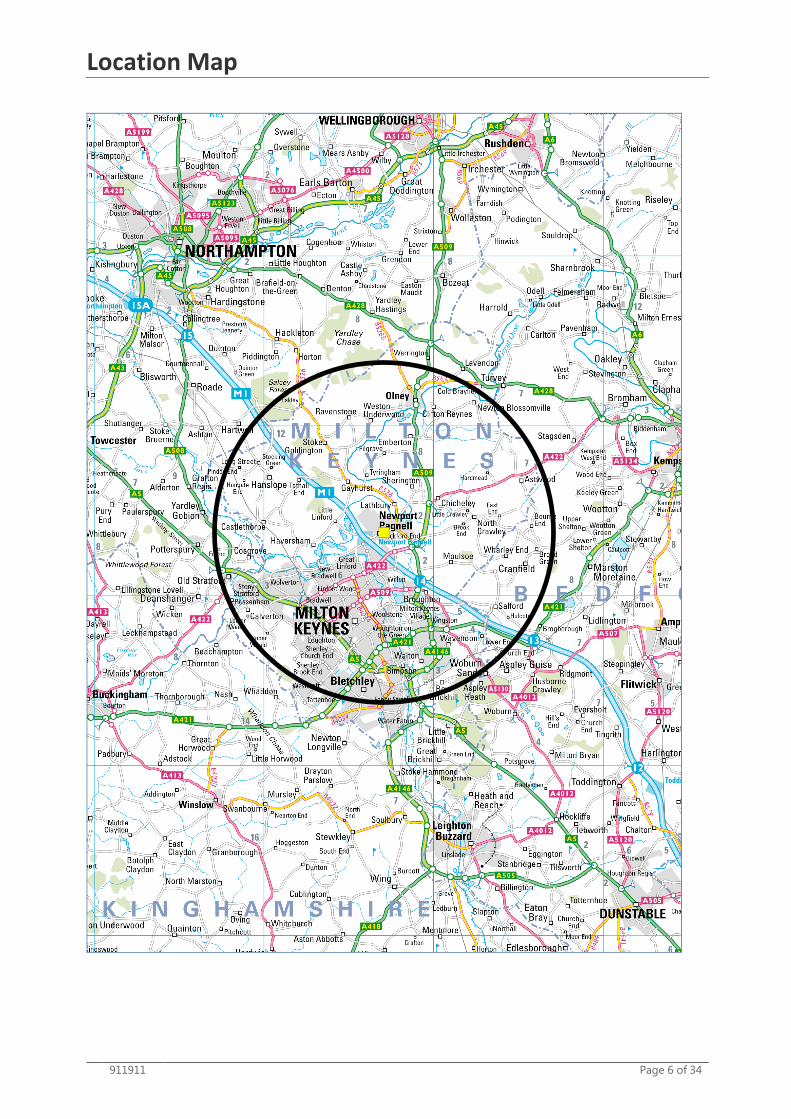

Location Map

911911 Page 7 of 34

Local Environment

Location

Barchester is a village situated three miles south-east of Shepton Mallet and five miles north-east of Castle Cary, in the Mendip district of Somerset. Shepton Mallet is the nearest reasonable sized town in the vicinity, with a population of approximately 8,000, and lies on the A37, which connects through to Bristol in the north, the nearest major city. The M5 is approximately 20 miles to the west, and the A303 London to Devon trunk road is accessed about 18 miles to the south. Shepton Mallet is an important retail centre for this part of Somerset, with many independent retailers located around the Market Place and High Street. The Townsend Retail Park on the edge of the town contains many multiples, including Tesco, Boots and Laura Ashley. The town also benefits from its proximity to the Bath and West Showground, which hosts major events and exhibitions throughout the year. Barchester is a small but prosperous village accessed via unclassified roads leading off the A37. It provides a wide range of housing, mostly owner occupied, and there has been a modest amount of new development. The subject concern is the only retail shop in the village, but there is a hairdressing salon, a food led pub, village hall, and a country house hotel. There is a limited bus service into Shepton Mallet. The subject property is located in the centre of the village facing a small green, with the hairdressers next door and is flanked on the other side by residential properties. Parking is freely available outside the shop and throughout the village

Environmental Matters

From our limited inspection of the property, we detected no evidence to suggest the existence of any current or past contamination. Information in the public domain suggests that this neighbourhood is in a radon affected area, as defined by the Health Protection Agency. Radon is a naturally occurring gas, which, in some areas, can be in higher concentrations and affect people’s health. In this regard, we refer to the Health Protection Agency on the www.hpa.org.uk website for further details. From our informal enquiries, there is no indication that the property or its immediate locality:

� is on or near landfills; � is located within a mining area; � is located within a tin mining area; � is in an area that has been identified as having a risk of subsidence or landslip; � is located within an area that is at risk of flooding; � is subject to water or land pollution; � has been used for the manufacture, storage or sale of hazardous/toxic materials such as chemicals, petroleum

products, pesticides, fertilisers, acids, asbestos, explosives, paint or radioactive materials; � is the site of below-ground storage tanks; � is close to incinerators or chimneys giving off heavy emissions.

Subject to the limitations of our inspection we have detected no evidence to suggest that deleterious or hazardous materials or techniques have been used in the construction or subsequent modification of the building.

We refer you to the paragraph headed ‘Environmental Matters’ within the appended Explanatory Notes.

911911 Page 8 of 34

Site Plan

911911 Page 9 of 34

Site & Aspects of Title

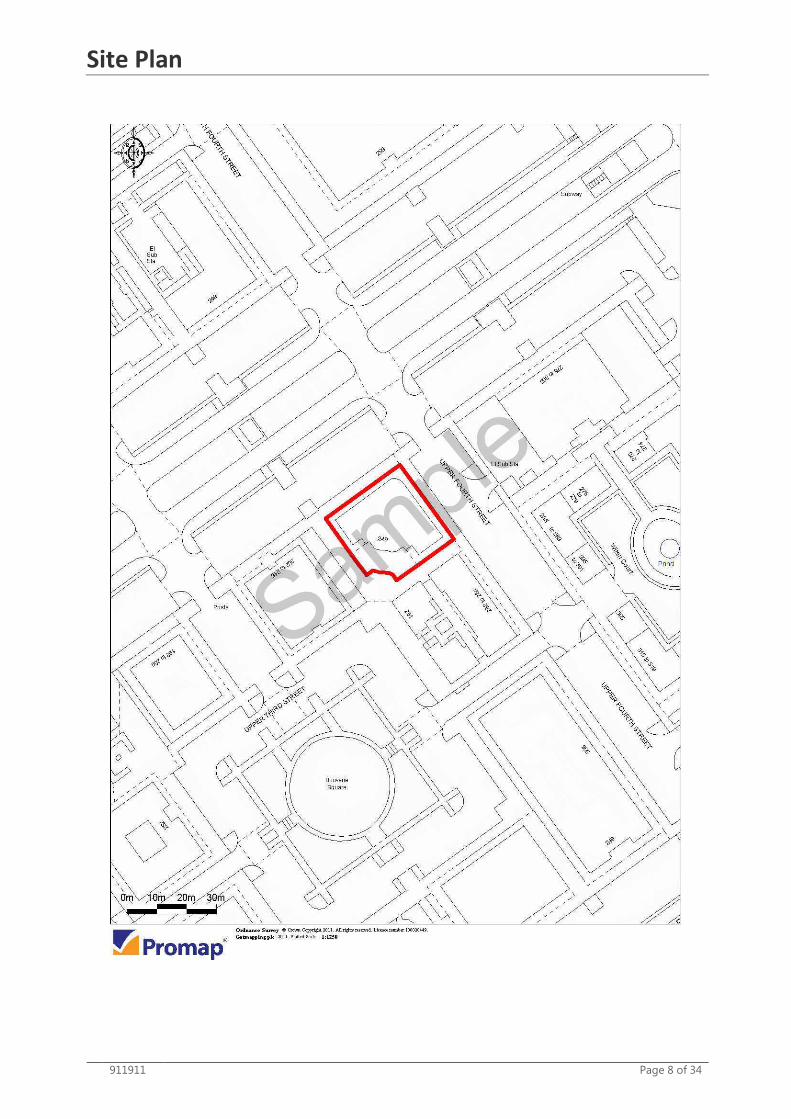

Site Plan

The plan shown opposite is taken from the most current Ordnance Survey digital mapping data and shows the subject property within its local environs. We advise that the area outlined in red corresponds with the property inspected. However, we recommend solicitors verify the boundaries.

It should be noted that this plan and the markings thereon indicate the approximate extent of the site inspected and no guarantee can be given as to whether this corresponds to that over which title is held. It remains the responsibility of the Client to investigate and confirm the legal boundaries and title applying to the property.

Restrictive Covenants, Rights of Way and Easements

Based on our investigations, we are aware of the following:

Rights of Way Restrictive Covenant Easements

� � �

We were advised by Mr Evans that there are no easements or restrictive covenants affecting the property. However, we were notified that the owners of Primrose Cottage have both vehicular and pedestrian right of way over part of the drive. We recommend that solicitors confirm these details in due course.

Tenure and Title

We are advised that the property is freehold and our valuations have been prepared accordingly.

Our valuations assume that any prospective purchaser would be granted full possession of the property, free of any restrictions on title and that all fixtures, fittings and items of equipment remaining would be provided on a fully unencumbered basis. Unless stated, we have not been provided with a report on title, but we would be pleased to co-operate with solicitors acting for the Client in respect of such a report should this be required.

911911 Page 10 of 34

External Property

911911 Page 11 of 34

External Property

Site Description/Potential

Based on the plan contained herein, the site has an area of 460m². It is rectangular, with the building situated to the front. There is a path on the left hand side leading to a rear service area, and also providing access to the residential accommodation, which is accessed via a metal staircase leading to a terrace at first floor level. There is an external storage shed and a small private garden to the rear of the site. We do not consider that there is any significant scope to extend the building further.

Buildings Description

The subject property comprises a two-storey semi-detached building, built circa 1930, with attic space in addition and single-storey rear extensions. The trading areas occupy the ground floor, with a window display and recessed shop entrance. There are bay windows on the first floor front elevation and dormer windows at second floor level. The following table summarises the apparent construction of the major building elements.

Element Description

Flat Roofs Section at the rear, clad with mineralised felt

Pitched Roofs Slate covering

Rainwater Goods Black sectional plastic

Walls Brick elevations, with some rendered sections

Window Frames Replacement double glazed PVC-U units

Services

We are advised that the property is connected to the following:

Mains Water Electricity Mains Drainage Mains Gas Central Heating

� � � � Oil

The property has a burglar alarm and CCTV system installed.

Systems and Equipment

Whilst it is beyond the scope of our instructions to undertake tests of services, equipment, fixtures and fittings, we assume that all such items are operating safely and efficiently and are appropriate for the purposes to which they are put.

911911 Page 12 of 34

External Property

911911 Page 13 of 34

External Property

Condition

It should be noted that we have not undertaken any form of survey, structural or otherwise and the following comments are based on our brief inspection of the property. Our valuations have been prepared on the assumption that there are no inherent structural defects associated with the property or any wants of repair which would attract a significant cost. Generally, the building is acceptably presented, with no significant obvious wants of repair noted. There are some minor wants of repair however, such as weathered paintwork, which we anticipate could be met within a rolling maintenance programme. As a general comment, flat roof coverings have a more limited lifespan and will require ongoing maintenance, prior to renewal. We are advised by Mr Evans that a survey of the property for asbestos was carried out by South West Environmental Services on 5 September 2011. We have had sight of this survey report, which indicated that no asbestos material was identified. Our valuations have been prepared on the assumption that there are no asbestos related issues which would attract a significant cost. An Energy Performance Certificate (EPC) was issued for the property on 10 March 2016, which rated the property as D.

Asbestos

All owners/occupiers of non-domestic properties and communal areas of domestic properties are required, under the Control of Asbestos Regulations (2012), to provide a record of an inspection to verify whether any form of asbestos is present. If asbestos is detected, then an appropriate management plan must be implemented. We have not inspected for asbestos and, unless otherwise stated, our valuations exclude any costs relating to this management plan.

Energy Performance Certificate and Display Energy Certificates

All non-domestic properties over 50m² in size require an EPC when constructed, sold or let. There are certain exemptions, for example, if the building is to be demolished. The certificate includes an energy efficiency rating between A (most efficient) and G. It is valid for a period of 10 years assuming there are no changes to the building or its' use.

From 9 January 2013, a DEC is required to be prominently displayed in all buildings that are occupied in whole or part by a public authority or by institutions frequently visited, providing a public service to a large number of persons, and that have a useable space of 500 m² or more. They are valid for a period of one year. The accompanying advisory report is valid for a period of seven years, or 10 years if the building is less than 1,000 m² in size, assuming no changes to the property or use. If available, for example the building has been constructed, sold or let, the EPC for these buildings also needs to be prominently displayed, although there is currently no requirement to commission an EPC specifically for this purpose. From April 2018, it will become unlawful to let properties with the two lowest ratings of F and G.

Please contact us for further information about arranging an asbestos survey or EPC

Reinstatement Assessment

It should be appreciated that an assessment of the likely costs of fully reinstating a property is a complex and detailed exercise usually undertaken by a building or quantity surveyor. The following estimate is provided purely for guidance purposes to assist the named client in their consideration of the stated business proposal. It should not be relied upon by either the named client, or any other party, as a basis for assessing levels of insurance cover and Pinders accept no liability in this regard. Whilst the estimate provided allows for the approximate costs of demolition, debris removal and professional fees, and assumes the use of modern materials, construction techniques and compliance with all current building regulations, it makes no allowance for any alterations to the layout or configuration of the property which may be required for the ongoing operation of the business. On these specific assumptions, we suggest that the reinstatement figure for the existing structure (exclusive of VAT) should not be less than £365,000.

911911 Page 14 of 34

Internal Property

911911 Page 15 of 34

Internal Description

Public Areas

Area Size m² (Approx) Description

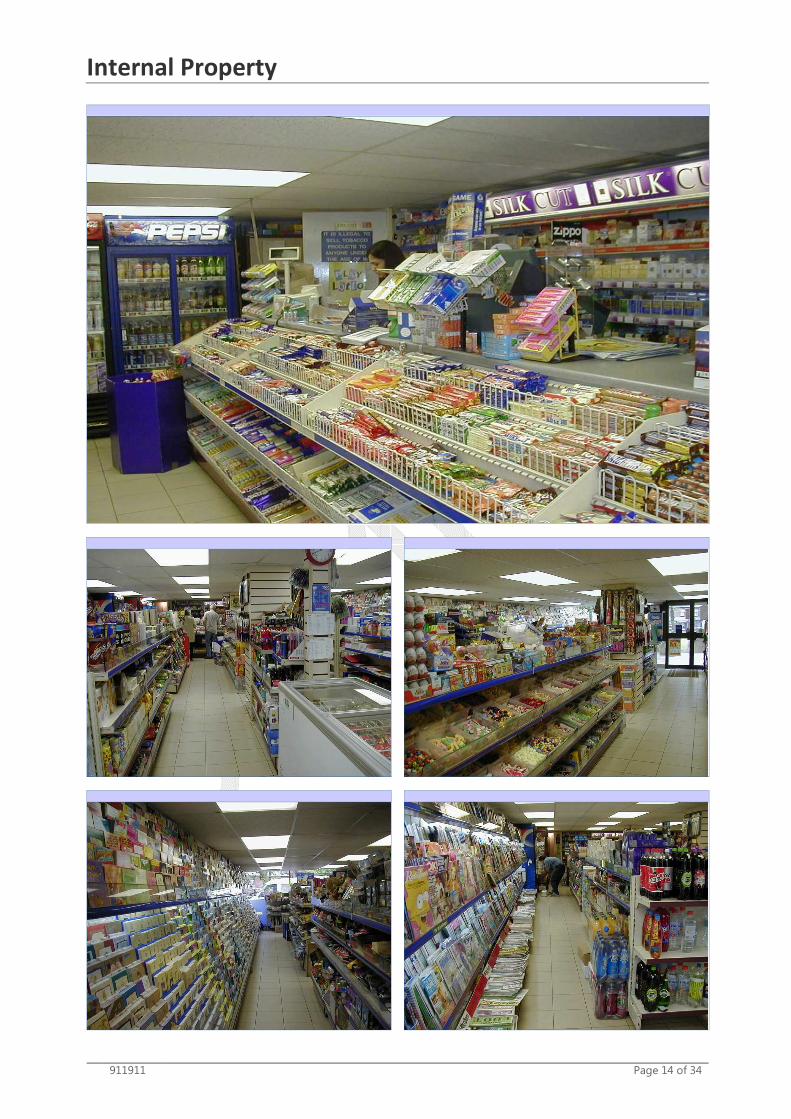

Retail Area 70.0 Fitted with a range of adjustable metal wall shelving, racking and other displays, together with a central gondola. Equipped with an open refrigerated cabinet for the display of beers, wines and minerals, a 'Bake & Bite' heated plate glass display cabinet, a hot drinks dispenser, an open refrigerated display cabinet for sandwiches, other savoury and dairy products, a double refrigerated display cabinet for soft drinks, a Lottery stand, double deep freeze display cabinet for frozen goods and an ice cream conserver. The counter has two service positions, EPOS till, lotto terminal, and cigarette gantry.

Post Office 13.0 Double counter behind security screen situated to the rear of the shop.

Service Areas

Area Size m² (Approx) Description

Office 8.1 Fitted with desk and shelving

Staff WC - Compact room with WC, sink and space for coats/bags.

Store 20.2 At rear of the building. Stock has to be delivered through the shop.

Measurement of Accommodation

We endeavour to measure the accommodation at the time of our inspection but, where this is not possible, we will either rely upon measurements taken from plans provided, schedules of measurements or other information advised to us by the owner of the business.

Residential Accommodation

The private living accommodation is located at first floor with there being internal access from the rear of the shop and separate external access. It is very well presented with carpets and laminate flooring, papered and painted walls and a range of domestic lighting. The kitchen and bathroom have been refitted in recent years. The residential accommodation comprises:

� Three Bedrooms – two double bedrooms and a third smaller room � Lounge � Dining Room � Kitchen – fitted kitchen with integral cooker and fridge freezer � Bathroom – domestic bathroom including bath with shower over, sink and WC, with additional separate WC

As indicated in the table below, the private accommodation measures approximately 100m², which is larger than most accommodation offered with a retail unit.

Regulated Mortgages

From 31 October 2004, mortgage applications relating to commercial property, where more than 40% of the property is used for residential purposes, are to be treated as Regulated Mortgage Contracts by the Financial Services Authority.

� Approximate total of site plus any upper floors of building 450m² 100%

� Approximate area currently used for residential purposes 100m² 22%

� Approximate area currently used for commercial and service areas* 350m² 78%

* The approximate area currently used for commercial purposes has been arrived at on a residual basis and relates to the GEA of the site and buildings

As the figures in the above table are derived from a combination of external mapping data and (possibly restricted) measurements taken on site, they should only be viewed as an approximate guide.

911911 Page 16 of 34

Internal Description

Access

Level access to premises Level access to public areas Disabled WC

� � �

There is level access into the shop, with there being a wide entrance door and level access to the retail area and serving counters. There are some changes in level to the staff/store areas.

The Equality Act 2010

The Equality Act came into force on 1 October 2010. The Act consolidates and brings together previous equality laws including the law on disability discrimination. Operators are under a duty to make reasonable adjustments to the provision of their services to accommodate people with disabilities. The duty is anticipatory - so adjustments must be made before a claim for disability discrimination is brought. What will constitute a reasonable adjustment very much depends on the size and nature of the service.

Decoration and Furnishing

The shop has an open plan layout, with modern display shelving and several fridge and freezer units some with glazed doors. We have been told that around £20,000 has been spent on improving the retail area in the last five years.

911911 Page 17 of 34

Statutory Authorities

For the purpose of this report and our valuations, we have assumed that there are no matters outstanding or that would be of concern to any of the Statutory Authorities, or any matters that would have a detrimental impact on Market Value.

Planning and Highways

From our online investigations and as advised by Mr Evans, we understand the following:

Listed Building Conservation Area Tree Preservation Orders Section 106 Agreements Adopted highway

� � � � �

We have accessed the online planning database of the Local Authority, which revealed the following planning history in relation to the subject property:

Reference Date Decision Proposal

04/00907 20/05/2008 Approved Single storey extension

The layout of the property at the time of our visit broadly accords with the plans available online associated with this application. Our valuations are prepared on the specific assumption that planning permission exists for the property's existing use.

Rates, Water and Environmental Charges

The rateable value of the subject property is £4,600. Within our calculations we have made an allowance of £750 for rates, water rates and environmental charges, reflecting that the subject concern benefits from 100% rural rates relief. The residential accommodation falls within Council Tax band C, this having a charge of £1,123 for the 2016/17 period.

Fire Authority

The fire authority no longer routinely inspects premises, and it is the responsibility of the occupier to undertake an appropriate Fire Risk Assessment. We are advised that a Fire Risk Assessment has been prepared and is regularly reviewed, with fire fighting equipment and sensors etc being regularly tested and serviced.

Regulatory Reform (Fire Safety) Order 2005

We have not undertaken any form of Fire Risk Assessment for the premises, nor can we confirm the adequacy, or otherwise of any Risk Assessments seen. We recommend that business proprietors fully acquaint themselves with the requirements of the Regulatory Reform (Fire Safety) Order 2005, which cover statutory fire prevention in almost every commercial property.

Environmental Health Authority

Mr Evans confirmed that the subject concern is registered under the provisions of the Food Safety Act 1990 and it is assumed that the business meets fully with the requirements of this legislation. The business received a rating of 5 out of 5 ‘very good’ on the 24 February 2016, under the Food Hygiene Rating System.

Food Safety Act 1990

We recommend that business proprietors fully acquaint themselves with the terms and conditions of the Food Safety Act 1990 and its various subordinate regulations. These include the introduction of a scheme for compulsory registration of all food premises under The Food Premises (Registration) Regulations 1991, the latter relating to England, Scotland and Wales, and applying to most types of businesses, with few exemptions.

Licensing

The Premises Licence Ref No: 012345 issued by Somerset County Council permits the sale of alcohol Monday to Saturday 6am to 10pm and Sunday 7am to 10pm. The Registered Owner and Designated Premises Supervisor are both shown as Mr Evans.

The Licensing Act 2003

The Licensing Act 2003 provides that premises where a licensable activity takes place require a Premises Licence. For the purpose of this report and our valuations, we have assumed that the business will have the necessary licences in place to continue to trade as existing and/or proposed.

911911 Page 18 of 34

Local Sector Profile

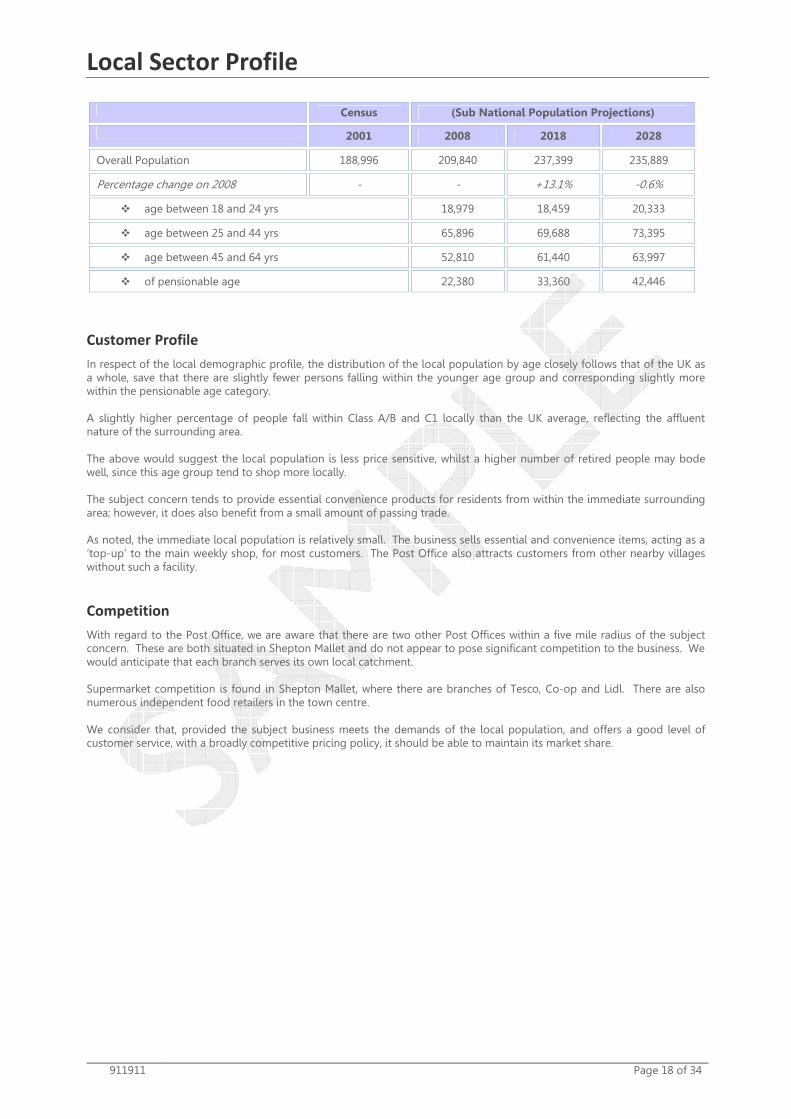

Census (Sub National Population Projections)

2001 2008 2018 2028

Overall Population 188,996 209,840 237,399 235,889

Percentage change on 2008 - - +13.1% -0.6%

� age between 18 and 24 yrs 18,979 18,459 20,333

� age between 25 and 44 yrs 65,896 69,688 73,395

� age between 45 and 64 yrs 52,810 61,440 63,997

� of pensionable age 22,380 33,360 42,446

Customer Profile

In respect of the local demographic profile, the distribution of the local population by age closely follows that of the UK as a whole, save that there are slightly fewer persons falling within the younger age group and corresponding slightly more within the pensionable age category. A slightly higher percentage of people fall within Class A/B and C1 locally than the UK average, reflecting the affluent nature of the surrounding area. The above would suggest the local population is less price sensitive, whilst a higher number of retired people may bode well, since this age group tend to shop more locally. The subject concern tends to provide essential convenience products for residents from within the immediate surrounding area; however, it does also benefit from a small amount of passing trade. As noted, the immediate local population is relatively small. The business sells essential and convenience items, acting as a ‘top-up’ to the main weekly shop, for most customers. The Post Office also attracts customers from other nearby villages without such a facility.

Competition

With regard to the Post Office, we are aware that there are two other Post Offices within a five mile radius of the subject concern. These are both situated in Shepton Mallet and do not appear to pose significant competition to the business. We would anticipate that each branch serves its own local catchment. Supermarket competition is found in Shepton Mallet, where there are branches of Tesco, Co-op and Lidl. There are also numerous independent food retailers in the town centre. We consider that, provided the subject business meets the demands of the local population, and offers a good level of customer service, with a broadly competitive pricing policy, it should be able to maintain its market share.

911911 Page 19 of 34

The Business

Business History

This is a long established business, which has been under the present ownership for just over five years. Mr and Mrs Evans are now planning to retire. The business has been refurbished and upgraded over the years, with an extension added by the previous owners in 2008, and the premises subject to a complete refit in 2012. The freehold property and business was placed on the market with a national agent three months ago at £525,000. There have been four viewings, and an offer of £510,000, made by the proposed purchasers, has provisionally been accepted.

Historic Accounts

We have been provided with financial statements prepared by Stanley & Co, Accountants of Bridgwater for the three year period ended 31 August 2015. We understand that the figures relate solely to the subject business. The figures show turnover increasing by 13.7% between 2013 and 2014, and by 4.5% between 2014 and 2015. The largest increase was as a result of the shop refit which was completed in 2012. The gross profit margin has been consistent over the three years and whilst this is in line with our expectations, it is towards the lower end of the range we would expect for an unopposed store in a less price sensitive area. The Post Office salary has increased year on year, which we understand is the result of the closure of at least one sub-Post Office in a nearby village. The net profit margin has shown a modest improvement and is also within expectations, albeit again towards the lower end of the range expected, especially considering the inclusion of the Post Office salary. The main expenses are in line with our expectations for a convenience store of this size. Staff costs have been between 9% and 9.5% of turnover over the period and repairs/maintenance costs have averaged £3,000 over the last two years.

911911 Page 20 of 34

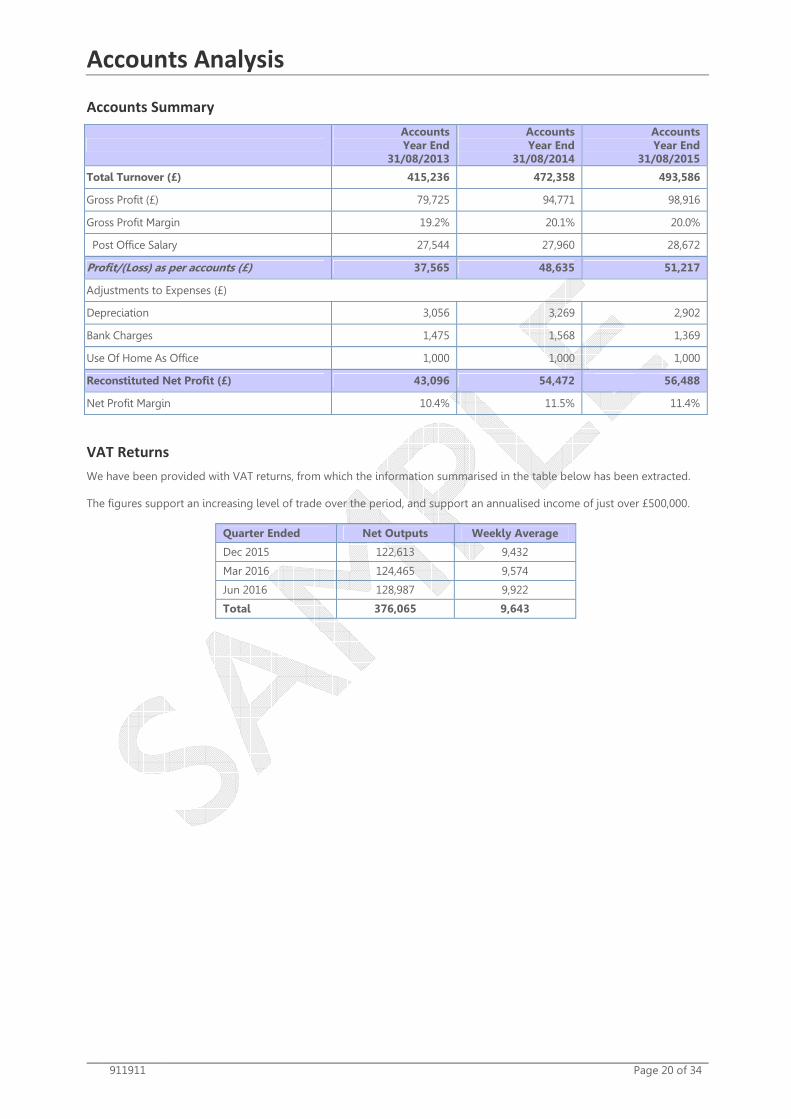

Accounts Analysis

Accounts Summary

Accounts Year End

31/08/2013

Accounts Year End

31/08/2014

Accounts Year End

31/08/2015

Total Turnover (£) 415,236 472,358 493,586

Gross Profit (£) 79,725 94,771 98,916

Gross Profit Margin 19.2% 20.1% 20.0%

Post Office Salary 27,544 27,960 28,672

Profit/(Loss) as per accounts (£) 37,565 48,635 51,217

Adjustments to Expenses (£)

Depreciation 3,056 3,269 2,902

Bank Charges 1,475 1,568 1,369

Use Of Home As Office 1,000 1,000 1,000

Reconstituted Net Profit (£) 43,096 54,472 56,488

Net Profit Margin 10.4% 11.5% 11.4%

VAT Returns

We have been provided with VAT returns, from which the information summarised in the table below has been extracted. The figures support an increasing level of trade over the period, and support an annualised income of just over £500,000.

Quarter Ended Net Outputs Weekly Average

Dec 2015 122,613 9,432

Mar 2016 124,465 9,574

Jun 2016 128,987 9,922

Total 376,065 9,643

911911 Page 21 of 34

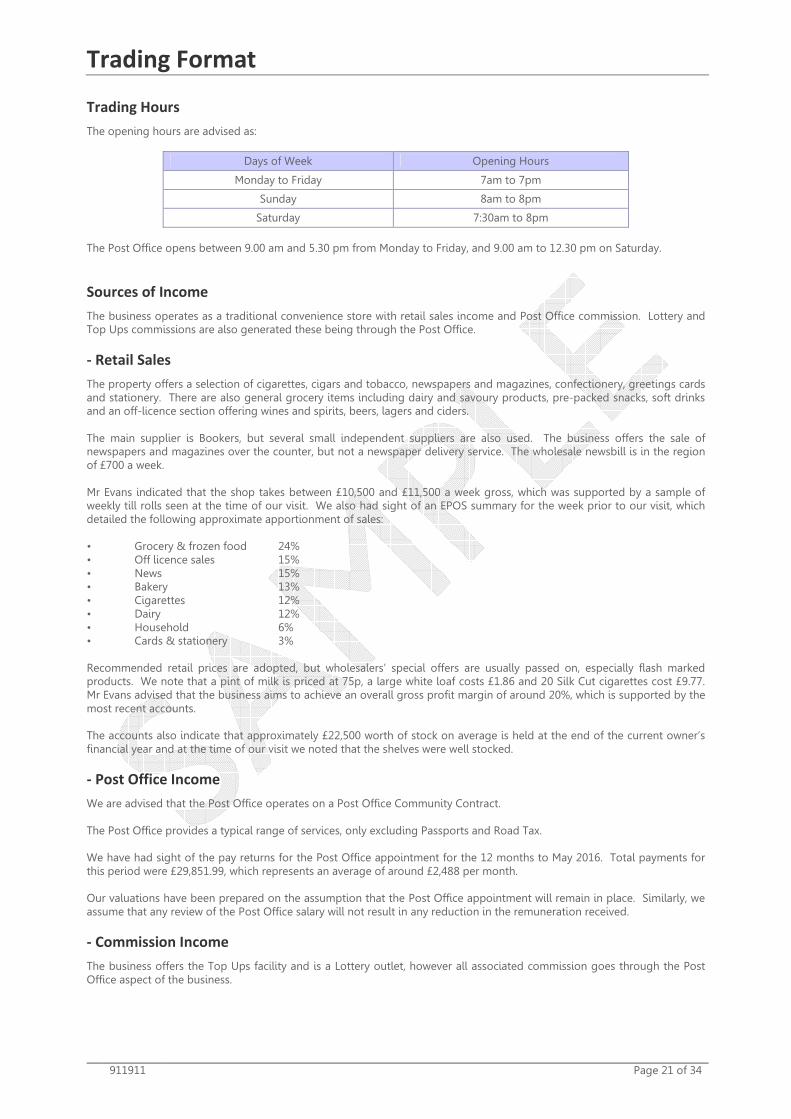

Trading Format

Trading Hours

The opening hours are advised as:

Days of Week Opening Hours

Monday to Friday 7am to 7pm

Sunday 8am to 8pm

Saturday 7:30am to 8pm

The Post Office opens between 9.00 am and 5.30 pm from Monday to Friday, and 9.00 am to 12.30 pm on Saturday.

Sources of Income

The business operates as a traditional convenience store with retail sales income and Post Office commission. Lottery and Top Ups commissions are also generated these being through the Post Office.

- Retail Sales

The property offers a selection of cigarettes, cigars and tobacco, newspapers and magazines, confectionery, greetings cards and stationery. There are also general grocery items including dairy and savoury products, pre-packed snacks, soft drinks and an off-licence section offering wines and spirits, beers, lagers and ciders. The main supplier is Bookers, but several small independent suppliers are also used. The business offers the sale of newspapers and magazines over the counter, but not a newspaper delivery service. The wholesale newsbill is in the region of £700 a week. Mr Evans indicated that the shop takes between £10,500 and £11,500 a week gross, which was supported by a sample of weekly till rolls seen at the time of our visit. We also had sight of an EPOS summary for the week prior to our visit, which detailed the following approximate apportionment of sales: • Grocery & frozen food 24% • Off licence sales 15% • News 15% • Bakery 13% • Cigarettes 12% • Dairy 12% • Household 6% • Cards & stationery 3% Recommended retail prices are adopted, but wholesalers’ special offers are usually passed on, especially flash marked products. We note that a pint of milk is priced at 75p, a large white loaf costs £1.86 and 20 Silk Cut cigarettes cost £9.77. Mr Evans advised that the business aims to achieve an overall gross profit margin of around 20%, which is supported by the most recent accounts. The accounts also indicate that approximately £22,500 worth of stock on average is held at the end of the current owner’s financial year and at the time of our visit we noted that the shelves were well stocked.

- Post Office Income

We are advised that the Post Office operates on a Post Office Community Contract. The Post Office provides a typical range of services, only excluding Passports and Road Tax. We have had sight of the pay returns for the Post Office appointment for the 12 months to May 2016. Total payments for this period were £29,851.99, which represents an average of around £2,488 per month. Our valuations have been prepared on the assumption that the Post Office appointment will remain in place. Similarly, we assume that any review of the Post Office salary will not result in any reduction in the remuneration received.

- Commission Income

The business offers the Top Ups facility and is a Lottery outlet, however all associated commission goes through the Post Office aspect of the business.

911911 Page 22 of 34

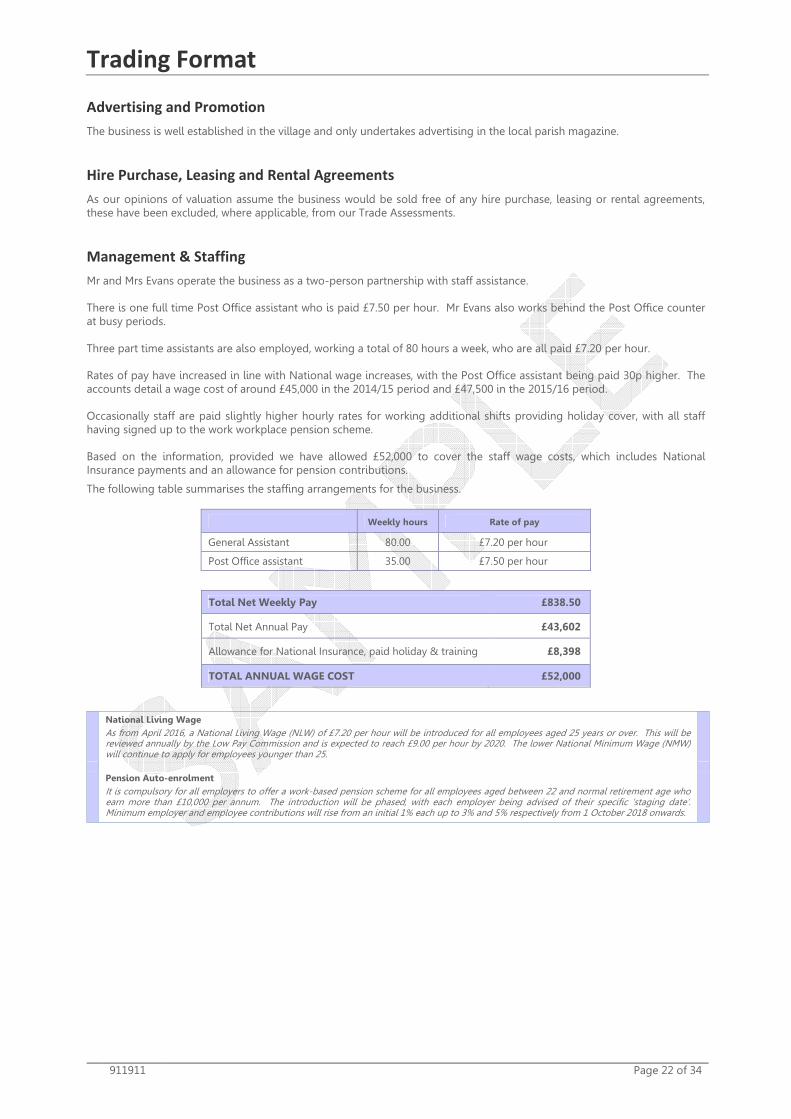

Trading Format

Advertising and Promotion

The business is well established in the village and only undertakes advertising in the local parish magazine.

Hire Purchase, Leasing and Rental Agreements

As our opinions of valuation assume the business would be sold free of any hire purchase, leasing or rental agreements, these have been excluded, where applicable, from our Trade Assessments.

Management & Staffing

Mr and Mrs Evans operate the business as a two-person partnership with staff assistance. There is one full time Post Office assistant who is paid £7.50 per hour. Mr Evans also works behind the Post Office counter at busy periods. Three part time assistants are also employed, working a total of 80 hours a week, who are all paid £7.20 per hour. Rates of pay have increased in line with National wage increases, with the Post Office assistant being paid 30p higher. The accounts detail a wage cost of around £45,000 in the 2014/15 period and £47,500 in the 2015/16 period. Occasionally staff are paid slightly higher hourly rates for working additional shifts providing holiday cover, with all staff having signed up to the work workplace pension scheme. Based on the information, provided we have allowed £52,000 to cover the staff wage costs, which includes National Insurance payments and an allowance for pension contributions. The following table summarises the staffing arrangements for the business.

Weekly hours Rate of pay

General Assistant 80.00 £7.20 per hour

Post Office assistant 35.00 £7.50 per hour

Total Net Weekly Pay £838.50

Total Net Annual Pay £43,602

Allowance for National Insurance, paid holiday & training £8,398

TOTAL ANNUAL WAGE COST £52,000

National Living Wage

As from April 2016, a National Living Wage (NLW) of £7.20 per hour will be introduced for all employees aged 25 years or over. This will be reviewed annually by the Low Pay Commission and is expected to reach £9.00 per hour by 2020. The lower National Minimum Wage (NMW) will continue to apply for employees younger than 25.

Pension Auto-enrolment

It is compulsory for all employers to offer a work-based pension scheme for all employees aged between 22 and normal retirement age who earn more than £10,000 per annum. The introduction will be phased, with each employer being advised of their specific ‘staging date’. Minimum employer and employee contributions will rise from an initial 1% each up to 3% and 5% respectively from 1 October 2018 onwards.

911911 Page 23 of 34

Current and Fair Maintainable Trade

Basis for Current Trade Assessment

We have prepared our Current Trade Assessment on the basis of the accounts provided for the three year period ended August 2015, together with VAT Returns to June 2016 and other trading details provided as noted, which support an income in the region of £500,000. We have also allowed for additional income in relation to the Post Office salary, which includes Top Ups and Lottery commission. The accounting information shows that the gross profit margin has been consistent over the last two years at around 20%, and we have adopted this figure within our assessment of current trade. Business costs have been assessed having regard to the accounting information provided, with adjustments to allow for inflation given their dated nature. Wage costs have however been assessed having regard to the advised staffing arrangements and as previously detailed. Should additional trading information become available, which supports a different level of turnover and profitability to that outlined herein, then we reserve the right to amend our assessment of trade and opinions of value accordingly.

Basis for Fair Maintainable Trade Assessment

The recommended method of valuation of trading businesses is the profits method of valuation, with an appropriate yield/multiplier applied to the assessed Fair Maintainable Operating Profit (FMOP). The FMOP is the level of profit which can reasonably be expected to be sustained by the business when operated by a normally efficient operator. It should exclude any influence on trade, positive or negative, which may result from an exceptional operator. We have shown our opinion of Fair Maintainable Trade (FMT) in the table opposite. For the sake of transparency, we have shown a comparison with the levels of income and expenditure which we have assessed as currently being demonstrated by the business. We have commented below on the reasons for any differences between these two trade assessments. Whilst there may be scope for further development of the business we have reflected a continuation of the current level of trade in our FMT assessment. The gross profit margin is however at the lower end of the range expected and we have allowed for an improved margin of around 22%, particularly as we are aware that many units of this size now trade under a brand such as Spar and Londis, and benefit from group purchasing discounts. Business costs are broadly as we would expect however we have made some adjustments as noted. Businesses of this style are generally operated by a two-person partnership with staff support, as at present, and we have not therefore made adjustments to the wage costs.

911911 Page 24 of 34

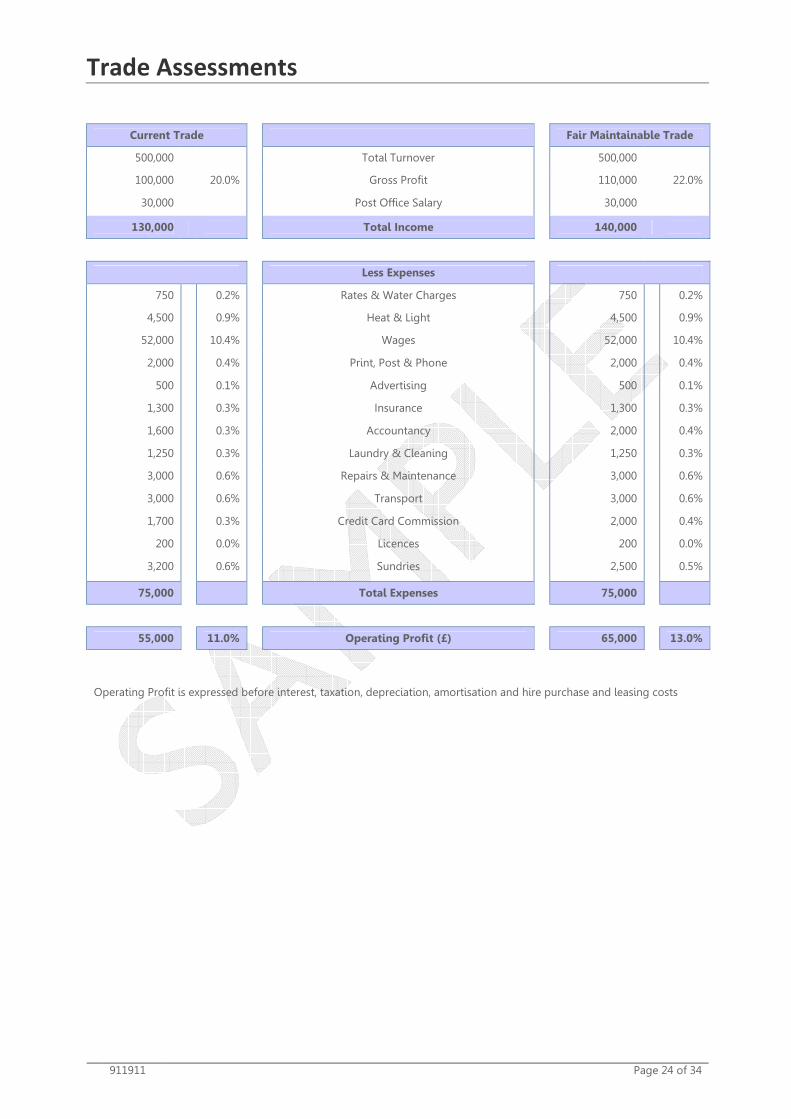

Trade Assessments

Current Trade Fair Maintainable Trade

500,000 Total Turnover 500,000

100,000 20.0% Gross Profit 110,000 22.0%

30,000 Post Office Salary 30,000

130,000 Total Income 140,000

Less Expenses

750 0.2% Rates & Water Charges 750 0.2%

4,500 0.9% Heat & Light 4,500 0.9%

52,000 10.4% Wages 52,000 10.4%

2,000 0.4% Print, Post & Phone 2,000 0.4%

500 0.1% Advertising 500 0.1%

1,300 0.3% Insurance 1,300 0.3%

1,600 0.3% Accountancy 2,000 0.4%

1,250 0.3% Laundry & Cleaning 1,250 0.3%

3,000 0.6% Repairs & Maintenance 3,000 0.6%

3,000 0.6% Transport 3,000 0.6%

1,700 0.3% Credit Card Commission 2,000 0.4%

200 0.0% Licences 200 0.0%

3,200 0.6% Sundries 2,500 0.5%

75,000 Total Expenses 75,000

55,000 11.0% Operating Profit (£) 65,000 13.0%

Operating Profit is expressed before interest, taxation, depreciation, amortisation and hire purchase and leasing costs

911911 Page 25 of 34

Future Proposals

We understand that Mr and Mrs Jones have previous retail experience and initially they are not proposing any significant changes to the business, aiming to settle in the business and ensure that the good level of customer service is maintained. In the medium term they are proposing to operate the business under the Spar banner and are considering extending the opening hours to 10pm on weekdays and potentially also on Saturday. In addition a family member who lives locally may also work within the business. Extended opening hours will accordingly have an impact on wage costs, which will vary depending on the level of owner input and reliance on employed staff and the opening hours. Given that the proposals are at an early stage and are not due to be implemented in the next year or so, we do not consider it appropriate to provide a trade Projection at this stage.

911911 Page 26 of 34

Methodology and Comparable Evidence

In assessing the value of the subject concern, we have adopted the 'build up' approach to valuation. This entails assessing the freehold value of both the residential and commercial elements of the property, and then adding the value of the business goodwill. In arriving at our opinion of value of the commercial premises, we have had regard to the ‘investment’ method of valuation, which involves assessing the Market Rental Value of the property, which is capitalised by an appropriate yield. We have had regard to the ‘comparable’ method in respect of the residential accommodation and the ‘profits’ method in respect of the business goodwill.

Rental and Yield Comparables

In respect of relevant comparable evidence for the above, we are aware of the following:

Location Date Rent £ per m²

Church Street, Cheddar May-2016 £25,000 £170

Swan Lane, Wells Jul-2016 £18,000 £145

Malden Road, Wells Aug-2015 £20,000 £155

We consider that the Cheddar property is the most relevant comparable, being a well presented Spar store, albeit in a slightly better trading position, hence the higher rental rate achieved. The units in Wells were both in tertiary trading positions, one being a hairdresser, the other an independent NCT concern. Having regard to the location, quality of the unit and standard of fit out we consider a rental of around £160 per m² on an overall basis to be reasonable, which based on our assessment of the Net Internal Area, supports a Market Rental Value of £16,000 per annum. The following freehold retail investments have been sold at auction:

Location Date Rent Sale Price Yield

Devon Road, Glastonbury May-2015 £26,300 £375,000 7.0%

Broad Street, Wells Jul-2016 £20,000 £275,000 7.3%

Fir Tree Road, Bridgwater Jul-2016 £9,000 £100,000 9.0%

The Glastonbury and Wells units were let to WH Smith and William Hill respectively, the strength of the covenants being reflected in the yield. The Bridgwater unit was let to a private individual, the yield representing a higher risk. We have not been able to obtain any more local investment sales evidence relating to retail units in rural locations, largely because, like the subject property, these are often owner occupied. Having regard to the above, we have reflected the higher risk of the subject location and that the property is most likely to appeal to the owner operator market in adopting a yield of 9%; this results in a freehold value for the commercial premises of £180,000.

Business/Goodwill Comparables

We are aware of the following deals,

Location Date Sale Price Description Goodwill YP

Bridgwater Jul-2015 £355,000 PO salary £25,000; shop sales £350,000 1.75

Nr Honiton, Devon May-2016 £395,000 PO salary £18,000; shop sales £395,000 1.85

Nr Bridport, Dorset Aug-2015 £450,000 PO salary £33,000; shop sales £425,000 2.0

The above units include owners’ accommodation of between two and four bedrooms, with the multiples noted relating to the goodwill aspects of the sales and are based on a two–person owner operated scenario The Bridport comparable is the most direct comparable for the subject business, being in a village location. The above comparables support a range of multiples of between 1.75 and 2.0 (YP), and we consider a multiple towards the upper end of the range to be reasonable given the overall quality of the business and unopposed village location.

911911 Page 27 of 34

Methodology and Comparable Evidence

Residential Comparables

We have been unable to obtain any comparable evidence relating to the sale of two or three bedroom flats in the surrounding rural area. However, within the last six months we are aware of the sale of four semi-detached houses (two and three bedroom) in the village, with a price range of between £285,000 and £310,000, and a modern two bedroom flat in a nearby town sold for £250,000 in March. Having regard to the location in a high value area and that the accommodation is above, and forms part of, a commercial property, we consider a value of around £200,000 for the private living accommodation is reasonable. There is similarly a lack of evidence available in respect of rental values however we are aware that a two bedroom flat above a neighbouring shop has recently been let at £550 pcm, although this was said to be relatively compact. In addition, a two bedroom terrace property on Albert Street has recently been let at £650 pcm and a three bedroom town house on Victoria Road at £800 pcm. On the basis of the size of the subject accommodation, but also reflecting its location above commercial premises, we consider a rate of £700 pcm to be appropriate in this instance, which after allowing for management costs, landlord costs and a void period, would suggest an annual rent of £7,000.

Methodology

On the basis of the above, we consider that the ground floor retail premises have a rental value of £16,000 per annum, which we have capitalised at a gross initial yield in the order of 9%, resulting in a freehold value of £180,000. With regard to the goodwill value of the business, we have allowed for a profits multiplier of around 2.0 YP on a dedicated two person partnership basis, which based on our assessment of FMOP (including post office remuneration) of £65,000 results in a goodwill value of £130,000. In addition, we have included £200,000 for the residential element of the property.

Current Proposed

Base Value £130,000 n/a

equating to: Assessed Fair Maintainable Operating Profit £65,000 2.0yp n/a n/a

Value of Private Living Accommodation £200,000 n/a

Value of Freehold Business Premises £180,000 n/a

Market Value £510,000 n/a

911911 Page 28 of 34

Additional Commentary

Marketability

We consider that the most likely purchaser of a Post Office and shop of this nature would be owner operators, who would typically live in the residential accommodation and seek an owner occupancy lifestyle. We consider that there would be reasonable demand for the subject concern from this sector, if the business is correctly and competitively priced. We doubt that the business would be attractive to other sectors. We would comment that should the shop close then the commercial space could be readily absorbed into the residential accommodation. Whilst this would require investment at some cost the additional ground floor space would add value to the property. This would be subject to receipt of the necessary planning permission, which would not necessarily be easily secured, given the loss of the retail amenity to the village.

Loan Security

Clearly, the value of a trading business is subject to fluctuation over time, resulting from the trading performance of the business, changes in local market forces, legislation and national economic conditions. Whilst it is for the lender to assess the risk attached to such fluctuations over the period of any loan, and to determine an appropriate level of security, we are unaware of any foreseeable events or circumstances, other than those detailed within this report, which would suggest that the subject property is unsuitable security for loan purposes and we would expect this business to be able to maintain its value in relation to the general economic and market conditions. Additionally we would expect the property to have a useful economic life over a typical loan term for a business of this nature, which we note to be 25 years in this instance. This assumes that the necessary maintenance and upgrades are made to the property to ensure that it continues to meet legislative and market requirements. Whilst it is possible for sales to complete quickly, in the current market we would not consider it unusual for a marketing period of 7-9 months to be required. However, if the property were disposed of in the event of foreclosure, or if a restrictive time period were imposed then we would expect a reduction in realisable value. It is impossible to be definitive as to the extent of this as it would be dependent upon the particular circumstances, but the valuations subject to assumptions contained herein provide some illustration of this scenario.

911911 Page 29 of 34

Valuations

Opinions of Current Valuation reflect the asset as inspected and described within the body of our report, subject to any stated assumptions.

MARKET VALUE subject to:-

[i] the asset is a fully equipped and operational entity, valued with regard to trading potential;

[ii] accounts or records of trade would be available to a prospective purchaser;

[iii] no time restrictions have been placed on the marketing of the asset.

(a) The Market Value of the current asset subject to the assumptions above is .............................................................£510,000

(five hundred and ten thousand pounds)

MARKET VALUE subject to:-

[i] the asset is a fully equipped and operational entity, valued with regard to trading potential;

[ii] accounts or records of trade would be available to a prospective purchaser;

[iii] a sale of the asset has been required within a 6 month period.

(b) The Market Value of the current asset subject to the assumptions above is .............................................................£350,000

(three hundred and fifty thousand pounds)

MARKET VALUE subject to:-

[i] the asset is empty but is valued with regard to trading potential;

[ii] accounts or records of trade would not be available to a prospective purchaser;

[iii] no time restrictions have been placed on the marketing of the asset;

[iv] the inventory remains in situ;

[v] the licences have been lost or breached.

(c) The Market Value of the current asset subject to the assumptions above is .............................................................£300,000

(three hundred thousand pounds)

Sale Price

We are advised that a sale price of four hundred and ten thousand pounds £410,000 has provisionally been negotiated between the parties. We consider this to be acceptable based on the trading information provided and local market activity.

The term asset refers to the property and/or business inspected and as described within our report. Our valuations assume the asset would be transferred free of any liabilities or encumbrances other than as expressly stated.

In view of the unpredictability of the conveyancing process, valuations which are expressed subject to a specified time restriction are provided on the basis that a sale has been agreed within that timescale, subject to contract, rather than legally completed.

Where the term ‘Inventory’ is used, it is assumed to include all items of relocatable furniture and equipment (beds, chairs, tables, crockery, etc) but not permanently installed fixtures and fittings, sanitary ware, floor-coverings, etc. All opinions of valuation are exclusive of any belongings (chattels) owned personally by the operator.

911911 Page 30 of 34

Valuations

Basis of Valuation

The bases of value above are as defined by The Royal Institution of Chartered Surveyors (RICS) Valuation - Professional Standards, and are subject to the qualifications and limitations referred to within this report. Full definitions of the valuations are outlined below.

Market Value - The estimated amount for which an asset or liability should exchange on the valuation date between a willing buyer and a willing seller in an arm’s-length transaction after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion.

Market Rental Value - The estimated amount for which an interest in real property should be leased on the valuation date between a willing lessor and a willing lessee on appropriate lease terms in an arm’s-length transaction, after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion.

Market Value – Special Assumptions

Unless otherwise specified, this valuation assumes that the asset is to be offered for sale free of any perceived blight resulting from factors such as the threat of action by statutory authorities or the appointment of Receivers. It should be appreciated that the impact of the specified restricted sale period will be more significant during periods where transactions are prolonged due to uncertain market conditions.

Market Value – Business Closed

We have provided our opinion of the value of the asset should it cease to trade and be offered for sale as an empty unit. Unless otherwise specified, this valuation assumes that the vacant asset is to be offered for sale free of any perceived blight resulting from factors such as the threat of action by statutory authorities or the appointment of Receivers, but it should be appreciated that the value of empty asset may vary considerably depending on the circumstances of the business closure. It is also important to recognise that this valuation assumes continuation of the existing use and excludes the possibility of any change of use being permitted.

911911 Page 31 of 34

Appendix 1 - National Sector Profile

Post Office Ltd provides services to just under 20 million customers each week, including around half of all small businesses in the UK, through a network of 11,818 branches. 373 of these branches are Crown branches operated by Post Office Ltd directly, whilst all other branches are operated by independent businesses or multiple retailers, typically as part of retail premises. 2012 was a significant and eventful year for the post office network, and following reforms contained within the Postal Services Act 2011, Post Office Ltd, along with its network of post offices, became independent from the Royal Mail Group on 1 April 2012. Furthermore, 2012 saw the introduction of a £1.34 billion funding package, the largest investment and support programme in the history of the Post Office, dedicated to modernise and transform approximately half of the branch network and provide network subsidy, in a bid to offset rising costs and falling trade, helping to safeguard the network’s future. The Government has stated that, in return for the funding package, Post Office Ltd must maintain a network of at least 11,500 branches. Following an initial pilot scheme, the full UK wide roll-out of 4,000 ‘main’ and approximately 2,000 ‘local’ branches commenced in Summer 2012, and is set to conclude in 2015. Local branches offer a downgraded service within other commercial premises, such as convenience stores. The aim of the new format is to improve efficiencies, with the integrated approach meaning that Post Office services can be offered over extended hours to match those of the premises that they operate in. Customers however will not be able to apply for driving licences, send bulky mail overseas or pay car tax. For the retailer, it is seen as an opportunity to drive footfall, with a projected increase in shop sales of up to 25%. The Post Office expects 'Locals' to offer 87% of the transactions of a regular Post Office and 95% of the volume. Initial teething problems are said to have included concerns as to whether staff are adequately trained and whether customers have sufficient privacy. Postmasters have further expressed fears that longer opening hours will increase costs that may not be met by an increase in sales, and that the only retailers that could make Locals financially viable are the large multinationals, who could absorb losses or pass additional costs to the customer. Tesco took part in the Locals pilot last year, through their One Stop convenience chain, and may soon become a key player.

In November 2012 the Post Office won the new DVLA contract for car tax disc supply. This contract is for seven years and is

worth £450m, with an option to extend for a further three years. This will also allow the Post Office to run applications for

driving licences and changes to licence photocards and is a vital component for keeping the Post Office open. There are said to be seven in ten villages now without a shop, and many rural post offices are left with nowhere to operate as a 'Local'. But by remodelling small post offices into 'Locals', the Government hopes to ensure their long term viability; it remains to be seen whether this scheme will truly deliver the goods. Subpostmasters who convert to a main style branch will receive investment for their branch of up to £15,000, or up to £30,000 or up to £45,000, depending on the branch size. Subpostmasters who convert to a local style will receive investment of up to £10,000 for their branch. However, the new network structure means changes in the structure of subpostmaster remuneration, as this will be based solely on fully variable transaction fees rather than the current mix of fixed pay and transaction fees. The changes are designed to reduce the Post Office's £450m annual bill for sub-postmaster remuneration. Post Offices are often seen as lifestyle businesses and often attract first-time purchasers. In this respect, the quality of the living accommodation may be considered an important factor. However, prospective purchasers also perceive the Post Office salary as secure income and, traditionally, it has been the main trading consideration of proposed purchasers, and so it remains to be seen what impacts these changes to remuneration will have on the network in the future, and indeed, the desirability of the new business models to prospective purchasers. Furthermore, the level of retail sales will become an increasingly significant factor.

911911 Page 32 of 34

Explanatory Notes

(Effective from 19 May 2014)

This Appendix forms part of the Report, and it is assumed that the Client is fully conversant with its contents.

(a) Definitions

Unless the context otherwise requires, the following terms have the meanings ascribed (where appropriate, references in the singular will also apply in the plural):-

"Pinders" means Pinders Professional & Consultancy Services Limited whose registered office is at Pinder House, Central Milton

Keynes, MK9 1DS.

"the Client" means the person(s) or body from whom the instructions to prepare the Report have been received. Reference to the Client, who shall be identified on the front page of the Report, shall in all cases be interpreted to mean only this person(s) or body.

"Proposed Borrowers" means the individual(s) or company whose proposal is the subject of the Report. Any reference to Proposed Borrowers within these Explanatory Notes also applies to alternative forms such as "Proposed Purchasers", "Proposed Vendors", etc.

"the Property" means all those freehold/leasehold premises which have been inspected by Pinders and reported upon.

"the Business" means the business trade or profession carried on or to be carried on by the Proposed Borrower in respect of which Pinders has been requested to prepare the Report.

"the Report" means a Report on the Property and/or Business prepared by Pinders.

"date of Inspection" the date on which Pinders’ representative carried out the inspection of the premises.

"date of Valuation" the date on which the opinion of value applies.

(b) Limitations of Report

Pinders has prepared this Report for use only by the Client to assist them in the consideration of the proposal stated and in respect of the subject business and/or premises, and for no other purpose whatever. It is confidential to the Client and other than for information purposes it is not for use by the Proposed Borrowers or any other party in any way.

Pinders accepts responsibility to the Client alone that the Report will be prepared with the skill, care and diligence to be expected of a competent business valuer and appraiser, but accepts no responsibility whatsoever to any person other than the Client. No person or body other than the Client may rely on the Report and neither the whole, nor any part of the Report, nor any reference thereto, is to be included in any published document, circular or statement, nor published in any way without the written approval of Pinders as to the form and context in which it may appear.

The Report may include an appraisal of a business concern together with comments as to its trading potential. In making such assessments Pinders accept no responsibility for loss of whatever nature which may result directly or indirectly from:

� the suppression, deception or falsification of material facts by the Vendor, Proprietor, and/or Proposed Borrowers;

� any mismanagement of the business;

� insufficient capitalisation, stock and staffing levels;

� changes in the financial and market situation compared to those prevailing at the date of the Report;

� material alterations to the nature, character, extent and pricing structure of the business;

� failure to maintain all proper and prudent insurance cover.

This Report is not intended to replace any of the investigations or enquiries normally undertaken in connection with the purchase or mortgage of a property/business and we do not accept responsibility for loss of whatever nature directly or indirectly arising out of failure to make such enquiries. Such enquiries include, but are not limited to, the taking of independent professional advice from solicitors and accountants, the entering into of a professionally drawn acquisition agreement with the appropriate warranties being taken from the Vendor or Proprietor, the taking up of all necessary trade and bank references, the inspection of the Vendor’s or Proprietor’s or Proposed Borrowers' accounts, examinations of all necessary consents, regulations, permissions, licences and bylaws.

Furthermore it is the Client’s responsibility to ensure that all trading information provided to Pinders is substantiated by audited/certified accounts and, where appropriate, an Accountant’s Certificate. Any discrepancy arising from such documentation should be reported to Pinders as soon as practicable in order that any necessary adjustments may be made to the Report. The Report may point to further enquiries being necessary and failure to make such enquires will be taken as evidence of non-reliance upon the Report and valuations therein.

It must be remembered that the Report does not contain a decision as to whether the stated proposal should proceed. It should also be noted that we do not supply "investment advice" either for the purposes of the Financial Services Act 1986 or at all. We do not offer advice as to whether shareholdings or debentures should be taken in the case of an incorporated business or equity acquired in the case of an unincorporated business or partnership. Should the Client and/or the Proposed Borrowers require such advice, they should seek assistance from their independent financial adviser.

Unless otherwise stated, the Report is not a Report of a survey, whether "Building Survey", "Structural Survey" or otherwise and no such building or structural survey has been carried out. In making the Report regard will be had to the apparent state of repair, construction and condition of the Property, taking into consideration major defects which are obvious in the course of a visual inspection of so much of the exterior and interior of the Property as is accessible at the time of inspection with safety, and without undue difficulty. The inspection will view those parts of the Property as can be seen whilst standing at ground level within the boundaries of the site and adjacent public/communal areas and whilst standing at the various floor levels, which Pinders considers reasonably necessary to provide the service, having regard to its purpose.

Pinders shall be under no duty to examine those parts of the Property which are covered, unexposed or inaccessible, or to raise boards, inspect woodwork, move anything, or use a moisture detecting meter. Neither shall Pinders have a duty to arrange for the testing of electrical, heating or other services which, unless indicated to the contrary, shall be assumed to be in a working and serviceable condition. If Pinders’ inspection suggests that there may be material hidden defects Pinders will so advise and may exceptionally defer submitting a final Report until the results of further investigations are available. It is assumed that those parts of any building erected on the Property which have not been inspected or made available for inspection would not reveal material defects of such a nature as to cause Pinders to alter the Report and Valuation.

911911 Page 33 of 34

In making the Report Pinders has made the following assumptions:

(i) We have not arranged for any investigation to be carried out to determine whether or not any deleterious or hazardous material has been used in the construction of this property, or has since been incorporated, and we are therefore unable to report that the property is free from risk in this respect. For the purpose of this Report we have assumed that such investigation would not disclose the presence of any such material to any significant extent.

(ii) Pinders cannot give any opinion whatsoever regarding the structural design of any construction upon the property nor as to the suitability of any foundations to such constructions.

(iii) That the plant, machinery, equipment, fixtures and fittings are in serviceable order, adequate for the effective trading of the business, and will remain so for the foreseeable future.

(c) Aspects of Title

In making the Report Pinders has made the following assumptions:

� That the Property is not subject to any unusual or especially onerous covenants, restrictions, encumbrances or outgoings which might affect Pinders’

valuation or which might prevent all or part of the Property from being properly used in connection with the Business.

� That the Title is as described to Pinders and as referred to in this Report and that there is good and marketable Title to the Estate or Interest which

Pinders has valued. Unless indicated to the contrary, title deeds and/or lease documents have not been inspected. Any interpretation of leases and

other legal documents and legal assumptions given in our capacity as Business Valuers and Appraisers must be verified by a suitably qualified lawyer

if it is to be relied upon.

� That the valuation of the Property/Business is unaffected by any matters which would be revealed by any searches and replies to such enquiries as are

raised or should properly be raised by the Client/Proposed Borrower and/or by Solicitors acting on his/their behalf or by any statutory notice,

restriction or liability; Pinders must be advised of any variations as to this assumption.

� That the Property and/or Business, its use or intended use, or its condition is not in any way unlawful or in breach of any provisions of the Town and

Country Planning Acts, Building Control, Licensing Acts, Registered Homes Act, Environmental Health Acts, or other statutory requirements, and that

the Property has direct access from a publicly maintained highway.

� Pinders’ understanding of the boundaries is noted, but Pinders has no knowledge (expressed or implied) of the responsibilities for fencing and legal

advice should be sought in this respect, if required. Pinders assumes that such boundaries show the true extent of the property and that there are no

potential or existing boundaries or other disputes or claims outstanding. Where indicated site areas are obtained from published plans or as advised

to Pinders. They are not derived from a physical site survey and are approximate unless otherwise indicated. Unless otherwise stated, any

measurements noted are carried out in accordance with the Code of Measuring Practice issued by the Royal Institution of Chartered Surveyors.

Pinders shall be under no obligation to verify any of these assumptions. It remains the responsibility of the Client to ensure that all appropriate enquiries and investigations are made and the report is not intended to replace any of those enquiries/investigations.

(d) Environmental Matters

Pinders has not carried out, nor has it commissioned, a site investigation, geographical or geophysical survey and therefore can give no opinion or assurance or guarantee that the ground has sufficient load bearing strength to support the existing constructions or any other construction that may be erected upon it in the future. Pinders cannot give any opinion or assurance or guarantee that there are no underground mineral or other workings beneath the site or in the vicinity nor that there is any fault or disability underground. It is not possible for Pinders, therefore, to certify that any land is capable of further development or redevelopment at a reasonable cost for the use for which there is permission.

Unless otherwise stated, we are not aware of the content of any environmental audit or any other environmental investigation or soil survey which may have been carried out on the property and which may draw any attention to contamination or the possibility of any subsequent contamination. In our undertaking we will assume that no contaminative or potentially contaminative uses have ever been carried out in the property. We have not carried out an investigation into past or present uses, either of the property or of any neighbouring land, to establish whether there is any potential for contamination to the subject property from these uses or sites, and have therefore assumed that none exist. Should it be established subsequently that any contamination exists at the property or on any neighbouring land, or that the premises have been or are being put to a contaminated use, this might reduce the values now reported.

(e) Generally

This Report has been prepared in good faith on the basis of enquiries made and information supplied to us. We reserve the right to claim qualified privilege in respect of any part of this Report should the contents be subsequently challenged by a party claiming to be aggrieved at anything stated herein. Sections 12 to 16 of the Supply of Goods and Services Act 1982 (or any statutory enactment thereof for the time being in force) are hereby excluded.

Valuations may be relied upon for the stated purpose as at the date specified. It is for the Client alone to make judgement as to their reliance upon the contents of the Report thereafter. In normal market conditions the value may not change materially in the short term (approximately 3-6 months). However, the property market is constantly changing and is susceptible to many external factors which can affect investor confidence and corresponding values.

Value added tax, taxation, grants and allowances are not included in capital and rental values as, unless otherwise specified in the report, these are always stated on a basis exclusive of any VAT liability even though VAT will in certain circumstances be payable. Unless otherwise specified no account is taken of any existing or potential liabilities arising for Capital Gains or other taxation or as a result of grants or capital allowances.

In the event of a dispute arising in connection with a valuation or the contents of the Report, unless expressly agreed otherwise in writing, Pinders Professional & Consultancy Services Limited and the Client will submit to the jurisdiction of the British Courts only. This will apply wherever the property or Client is located, or the advice provided.

Pinders are deemed to be "External Valuers" with no other current or presently foreseeable fee earning relationship concerning the subject property and/or business apart from the valuation fee. Pinders will disclose to the best of its knowledge previous inspections undertaken. Pinders is not however able to disclose any present or previous relationship with any of the interested parties, contrary to the requirements of the Valuation - Professional Standards of the Royal Institution of Chartered Surveyors.

None of our employees, partners or consultants individually has a contract with you or owes you a duty of care or personal responsibility. You agree that you will not bring any claim against any such individuals personally in connection with our services.

If you suffer loss as a result of our breach of contract or negligence, our liability shall be limited to a just and equitable proportion of your loss having regard to the extent of responsibility of any other party. Our liability shall not increase by reason of a shortfall in recovery from any other party, whether that shortfall arises from an agreement between you and them, your difficulty in enforcement, or any other cause.

911911 Page 34 of 34

Our contract with you for the provision of this valuation is subject to English/Scots Law (as appropriate to the location of the subject property). Any dispute in relation to this contract, or any aspect of the valuation, shall be subject to the exclusive jurisdiction of the Courts of England and Wales/Scotland, and shall be determined by the application of English/Scots Law regardless of who initiates proceedings in relation to the valuation. (f) Valuations

The valuations provided will be made on the assumptions stated within the Report and/or these Explanatory Notes in respect of the individual subject business/property, unless otherwise agreed, on whichever of the following or other bases as have been agreed between Pinders and the Client, such bases where applicable to be as defined or referred to in the Valuation - Professional Standards of the Royal Institution of Chartered Surveyors.

The valuations provided are for the value of the business/property as described. No account has been taken of any special tax or other inducement or liability which may arise as a result of any transaction in contemplation nor of normal costs involved in the execution of such a transaction. The full definitions of the valuations provided in the Report are set out below: If the Report contains other valuation bases, these are as specifically requested by the Client with our advice identified within the Report to be on a basis not recommended by the Royal Institution of Chartered Surveyors, and provided for guidance purposes only.

DEFINITIONS OF VALUATION

Market Value (MV) The estimated amount for which an asset or liability should exchange on the date of valuation between a willing buyer and a willing seller in an arm’s-length transaction after proper marketing wherein the parties had each acted knowledgeably, prudently and without compulsion.

Market Value

with special assumptions

Opinions of Market Valuation can be provided in accordance with special assumptions which are indicated by the client. These assumptions will be clearly stated within the body of the report.