Embed Size (px)

Citation preview

POSITIVE ACCOUNTING THEORY (PAT)

ASNUR FATEM ALI

1. Bonus plan hypothesis2. Debt covenant hypothesis3. Political cost hypothesis

INTRODUCTION

◦1) Positive Accounting Theory (PAT) concerned with predicting such actions as the choices of accounting policies by firms & how firms will respond to proposed new accounting standard.

◦2) PAT uses theory to predict the choices that management will make regarding their choice of accounting policies.

◦3) This theory is introduced as a way to merge efficient securities markets with economic consequences.

◦4) PAT takes the view that firms will conduct themselves in the way that maximizes their own best interests.

◦5) Managers do not always do what is best for shareholders, but what will be the most beneficial to their organization.

◦6) The choices that an organization makes are dependant on what industry they are in, and the factors within that industry.7) PAT emphasizes that an organization’s choice of accounting policies is motivated by keeping contract costs down.

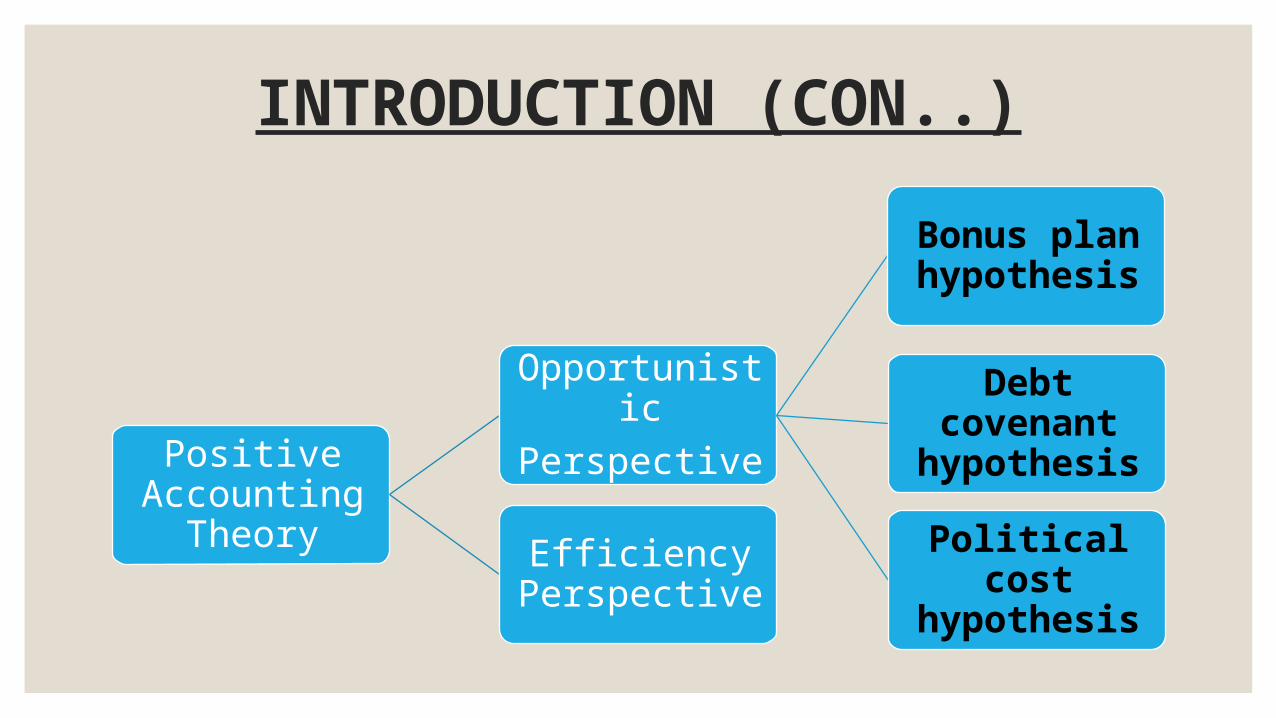

INTRODUCTION (CON..)

Positive Accounting

Theory

OpportunisticPerspective

Bonus plan hypothesis

Debt covenant

hypothesis

Political cost

hypothesis

Efficiency Perspective

BONUS PLAN HYPOTHESIS

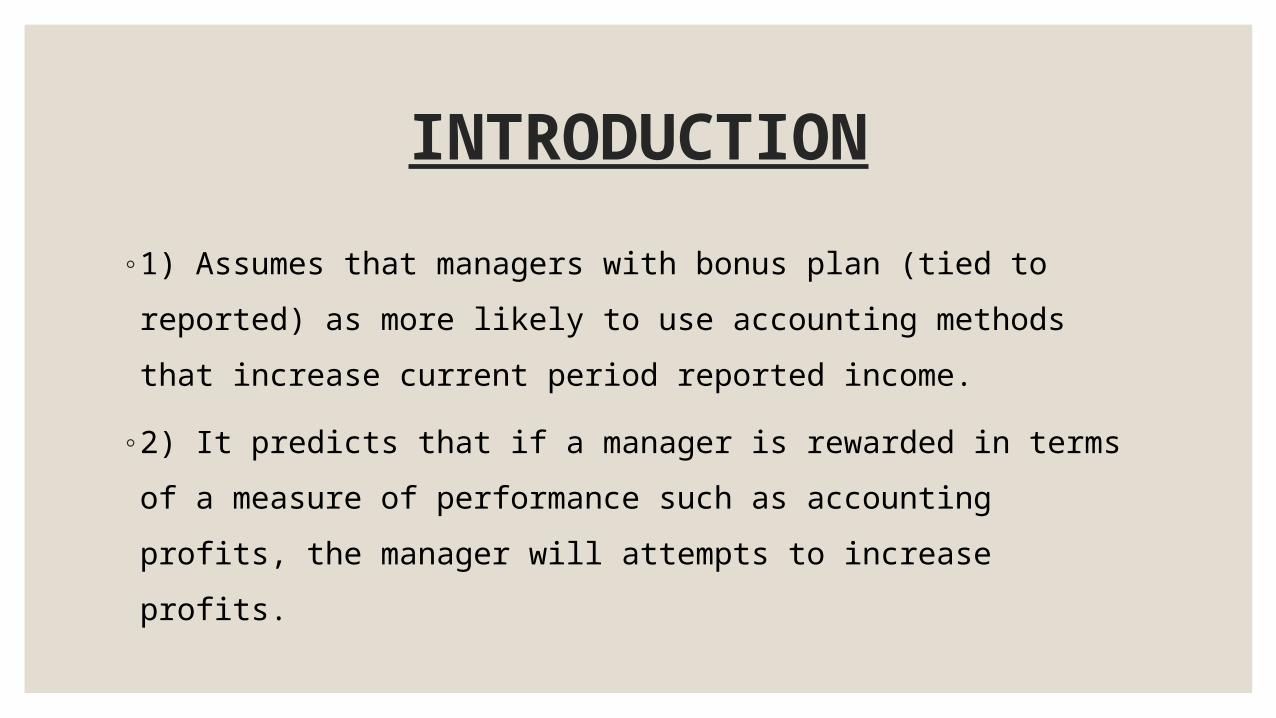

INTRODUCTION

◦1) Assumes that managers with bonus plan (tied to reported)

as more likely to use accounting methods that increase current

period reported income.

◦2) It predicts that if a manager is rewarded in terms of a

measure of performance such as accounting profits, the

manager will attempts to increase profits.

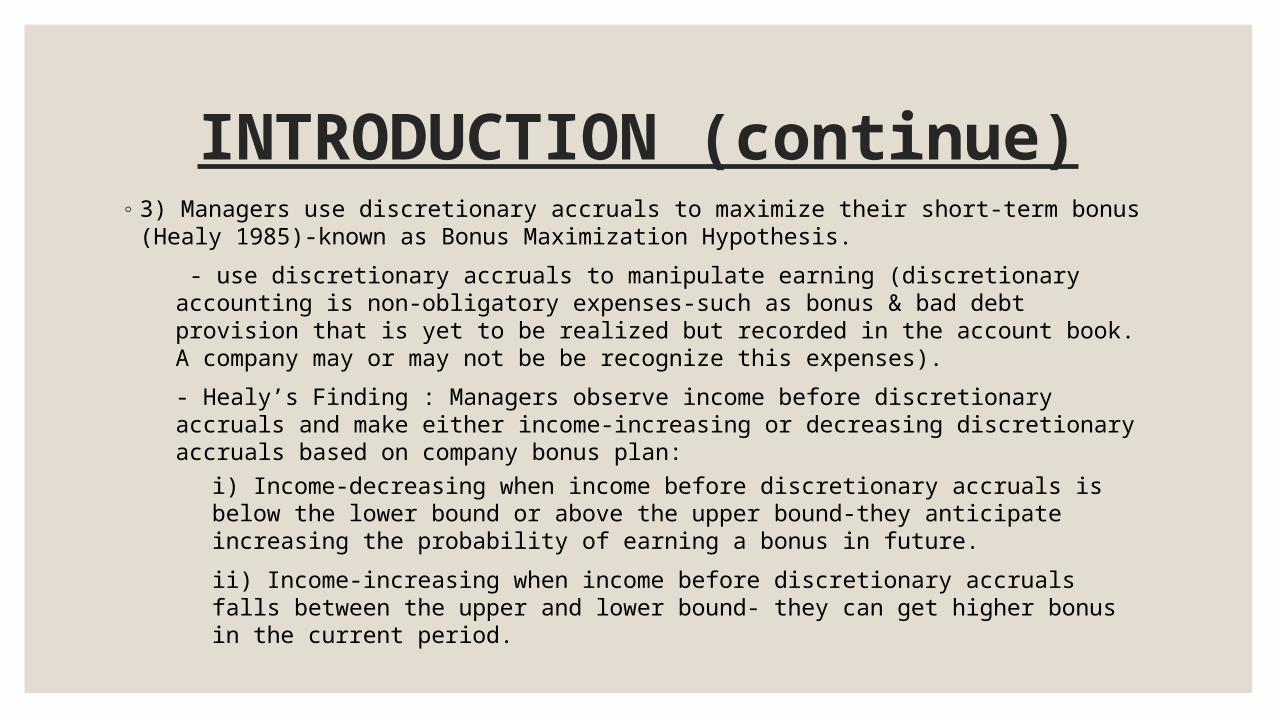

INTRODUCTION (continue)◦ 3) Managers use discretionary accruals to maximize their short-term bonus (Healy

1985)-known as Bonus Maximization Hypothesis.

- use discretionary accruals to manipulate earning (discretionary accounting is non-obligatory expenses-such as bonus & bad debt provision that is yet to be realized but recorded in the account book. A company may or may not be be recognize this expenses).

- Healy’s Finding : Managers observe income before discretionary accruals and make either income-increasing or decreasing discretionary accruals based on company bonus plan:

i) Income-decreasing when income before discretionary accruals is below the lower bound or above the upper bound-they anticipate increasing the probability of earning a bonus in future.

ii) Income-increasing when income before discretionary accruals falls between the upper and lower bound- they can get higher bonus in the current period.

EXECUTIVE COMPENSATION, INVESTMENT OPPORTUNITIES, AND EARNINGS

MANAGEMENT:HIGH-TECH FIRMS VERSUSLOW-TECH FIRMS

Author : 1) Sun S.Kwon (School of Administrative Studies ,Atkinson College, York

University)

2) Qin Jennifer Yin(Department of Accounting, College of Business, University

of Texas at San Antonio)

Published in : Journal of Accounting, Auditing and Finance, 21(2), 2006, pp. 119- 148.

EXECUTIVE COMPENSATION, INVESTMENT OPPORTUNITIES, AND EARNINGS MANAGEMENT: HIGH-TECH FIRMS VERSUS LOW-TECH FIRMS

INTRODUCTION

1) Questions exist on whether high-tech firms and low-tech firms use performance measures,

including stock and accounting performance, in the same way when determining

compensation contracts.

2) Prior research indicates that the market valuation for high-tech stocks differs from that for

traditional stocks.

3) Hand (2000) asserts that the conventional assumption that accounting information maps into

the equity market value in a linear and stationary manner is not relevant to technology-

intensive firms.

4) Although the relevance of performance measures for valuing a firm may differ for executive

contracting purposes, the link between executive pay and reported earnings is sensitive to

the underlying value in earnings (Bushman et al. [2000]).

EXECUTIVE COMPENSATION, INVESTMENT OPPORTUNITIES, AND EARNINGS MANAGEMENT: HIGH-TECH FIRMS VERSUS LOW-TECH FIRMS

INTRODUCTION (Con..)

5) The nature of the high-tech business may provide one possible reason for these differences.

High-tech firms must invest more in such intangible assets as R&D, human resources, customer

acquisition, brand development, and other information technology in comparison to low-tech

firms.

6) To survive in the fast-changing, fiercely competitive high-tech market, these firms also incur

greater and more frequent unusual or nonrecurring expenses, including :

7) inventory write-downs, restructuring/ reorganization expenses, and write- downs or write-offs

of receivables and intangibles that potentially lower their earnings reports.

8) Further, investment projects typically are more difficult to observe and monitor than assets-

in-place (Smith & Watts [1992]; Krishnan & Kumar [2001]), and

9) This increases the information asymmetry between the principal (shareholders) and the agent

(managers) in high-tech firms, creating a need to monitor managers’ performance through

compensation contracts (Jensen & Meckling [1976]; Fama & Jensen [1983]).

EXECUTIVE COMPENSATION, INVESTMENT OPPORTUNITIES, AND EARNINGS MANAGEMENT: HIGH-TECH FIRMS VERSUS LOW-TECH FIRMS

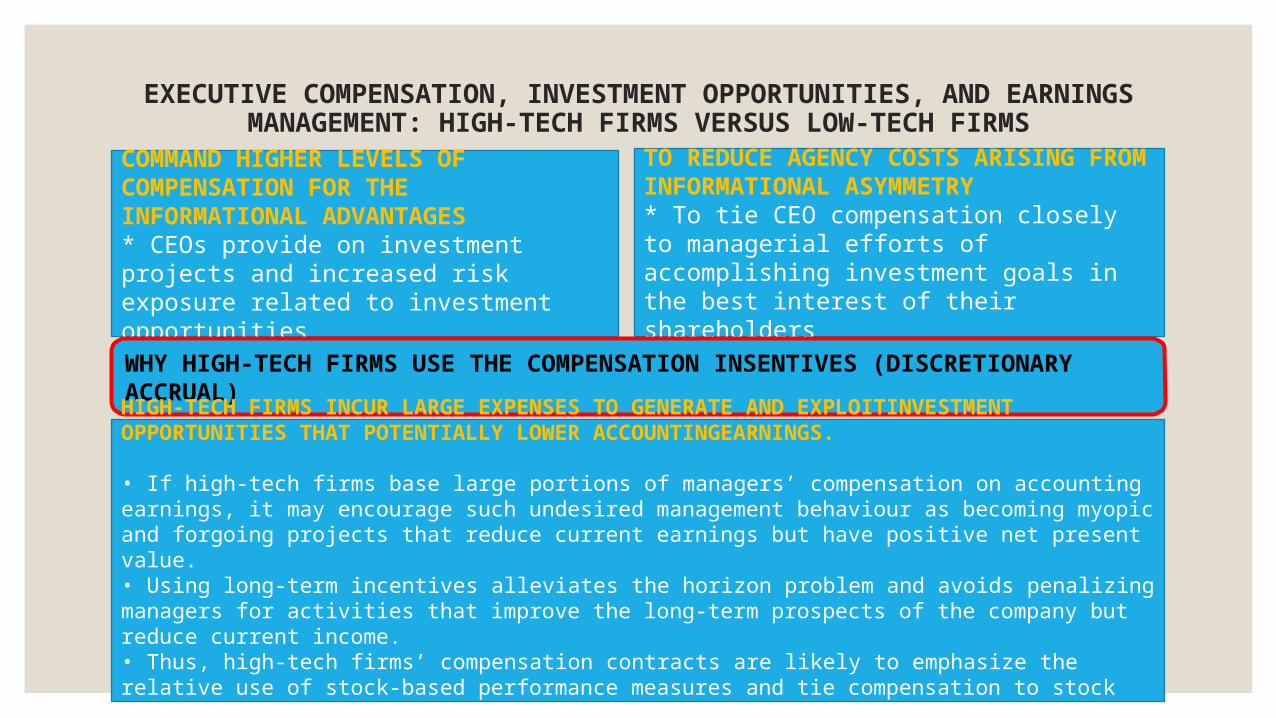

COMMAND HIGHER LEVELS OF COMPENSATION FOR THE INFORMATIONAL ADVANTAGES* CEOs provide on investment projects and increased risk exposure related to investment opportunities

TO REDUCE AGENCY COSTS ARISING FROM INFORMATIONAL ASYMMETRY* To tie CEO compensation closely to managerial efforts of accomplishing investment goals in the best interest of their shareholders

WHY HIGH-TECH FIRMS USE THE COMPENSATION INSENTIVES (DISCRETIONARY ACCRUAL)

HIGH-TECH FIRMS INCUR LARGE EXPENSES TO GENERATE AND EXPLOITINVESTMENT OPPORTUNITIES THAT POTENTIALLY LOWER ACCOUNTINGEARNINGS.

• If high-tech firms base large portions of managers’ compensation on accounting earnings, it may encourage such undesired management behaviour as becoming myopic and forgoing projects that reduce current earnings but have positive net present value.• Using long-term incentives alleviates the horizon problem and avoids penalizing managers for activities that improve the long-term prospects of the company but reduce current income.• Thus, high-tech firms’ compensation contracts are likely to emphasize the relative use of stock-based performance measures and tie compensation to stock returns.

EXECUTIVE COMPENSATION, INVESTMENT OPPORTUNITIES, AND EARNINGS MANAGEMENT: HIGH-TECH FIRMS VERSUS LOW-TECH

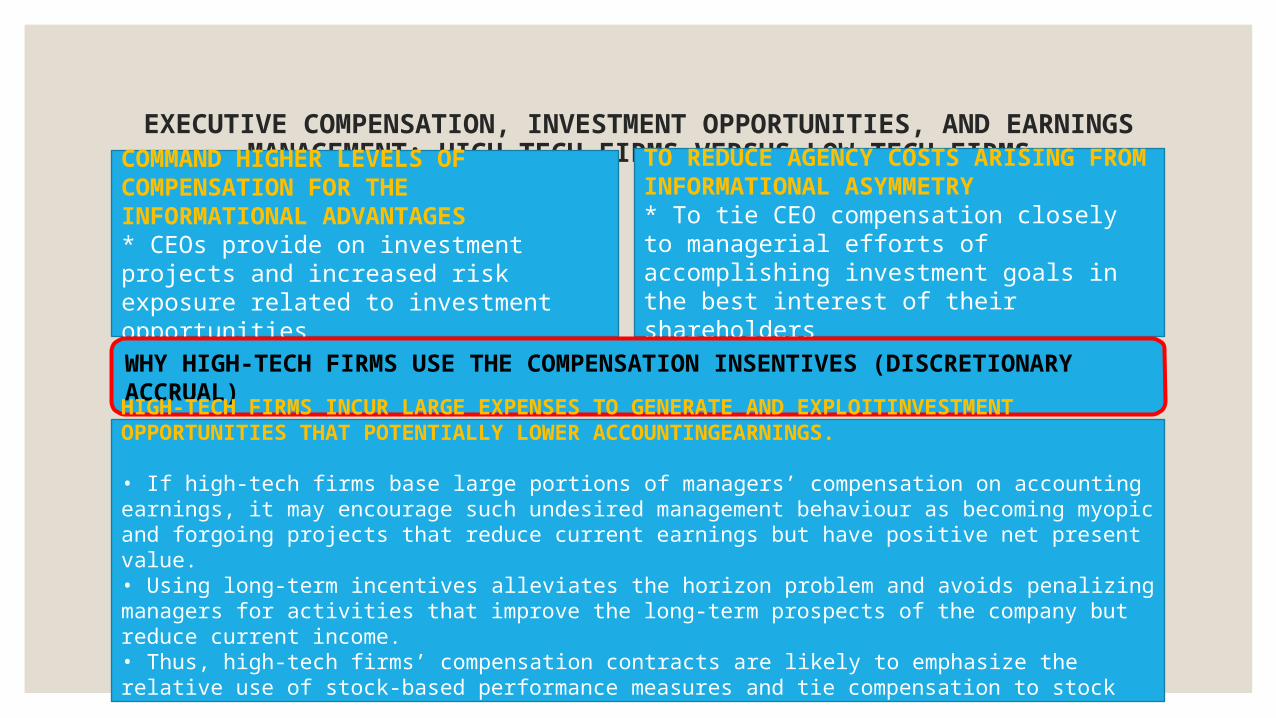

FIRMSCOMMAND HIGHER LEVELS OF COMPENSATION FOR THE INFORMATIONAL ADVANTAGES* CEOs provide on investment projects and increased risk exposure related to investment opportunities

TO REDUCE AGENCY COSTS ARISING FROM INFORMATIONAL ASYMMETRY* To tie CEO compensation closely to managerial efforts of accomplishing investment goals in the best interest of their shareholders

WHY HIGH-TECH FIRMS USE THE COMPENSATION INSENTIVES (DISCRETIONARY ACCRUAL)

HIGH-TECH FIRMS INCUR LARGE EXPENSES TO GENERATE AND EXPLOITINVESTMENT OPPORTUNITIES THAT POTENTIALLY LOWER ACCOUNTINGEARNINGS.

• If high-tech firms base large portions of managers’ compensation on accounting earnings, it may encourage such undesired management behaviour as becoming myopic and forgoing projects that reduce current earnings but have positive net present value.• Using long-term incentives alleviates the horizon problem and avoids penalizing managers for activities that improve the long-term prospects of the company but reduce current income.• Thus, high-tech firms’ compensation contracts are likely to emphasize the relative use of stock-based performance measures and tie compensation to stock returns.

EXECUTIVE COMPENSATION, INVESTMENT OPPORTUNITIES, AND EARNINGS MANAGEMENT: HIGH-TECH FIRMS VERSUS LOW-TECH FIRMS

◦RESEARCH OBJECTIVE

◦1) Examine the systematic differences between high-tech &

low-tech firms in compensation policies.

◦2) Examine the sensitivity of compensation to market &

accounting performance.

◦3) Examine earning management in the presence of

investment opportunities.

EXECUTIVE COMPENSATION, INVESTMENT OPPORTUNITIES, AND EARNINGS MANAGEMENT: HIGH-TECH FIRMS VERSUS LOW-TECH FIRMS

◦ HYPHOTHESIS

1) High-tech firms pay higher levels of executive compensation than low-tech firms

2) High-tech firms payless in cash salaries and bonuses but offer more stock options than

low-tech firms

3) The Association between changes in compensation and changes in stock performance is

higher, and the association between changes compensation and changes in accounting

performance is lower, for high-tech firms than for low-tech firms.

4) The Association between compensation discretionary accruals is higher in high-tech

firms than in low-tech firms, especially when earning before discretionary accruals are

lower than analysts’ earnings forecast

EXECUTIVE COMPENSATION, INVESTMENT OPPORTUNITIES, AND EARNINGS MANAGEMENT: HIGH-TECH FIRMS VERSUS LOW-TECH FIRMS

◦ SENSITIVITY TEST (CONFOUNDING FACTORS)

• SIZE EFFECT

Compensation relates to firm size :

- large firm typically have more complex structures and require a greater level of managerial effort than small

firms

- Even Though firm size does not differ significantly between high-tech and low-tech firms it may have

affected previous regression results because firm size was not explicitly controlled for in the regression

• REGULATION EFFECT

executive compensation varies inversely with levels of regulation because regulations restrict the chief

executive officer’s investment discretion and reduce the marginal product of the decision

• DEBT EFFECT

Debt to-asset ratios differ significantly between high-tech and low-tech firms, so it is particularly important to

control for the effect of debt.

EXECUTIVE COMPENSATION, INVESTMENT OPPORTUNITIES, AND EARNINGS MANAGEMENT: HIGH-TECH FIRMS VERSUS LOW-TECH FIRMS

◦ CONCLUSION

1) high-tech firms generally pay a higher level of total compensation than low-tech firms.

2) high-tech firms use lower cash salaries and bonuses but larger amounts of stock options grants when rewarding CEOs

3) the association between compensation and stock returns is higher for high-tech firms, and find no difference in the association between compensation and accounting returns in both groups

4) the positive association between bonus and discretionary accruals is higher for high- tech firms than for low-tech firms, especially when earnings before discretionary accruals are lower than the mean earnings forecast.

5) The results are robust to various sensitivity analyses, including controlling for potentially confounding effects related to size, debt, and regulation; using alternative specifications of accounting and market performance measures; and a variety of procedures to attenuate the effects of extreme values.

6) The overall results indicate systematic differences between high-tech and low-tech firms in compensation policies, choices of performance indicators, and the treatment of earnings management. The interpretation is that differences in information environment between high-tech and low-tech firms lead to different structures for compensation contracts.

DEBT COVENANT HYPOTHESIS

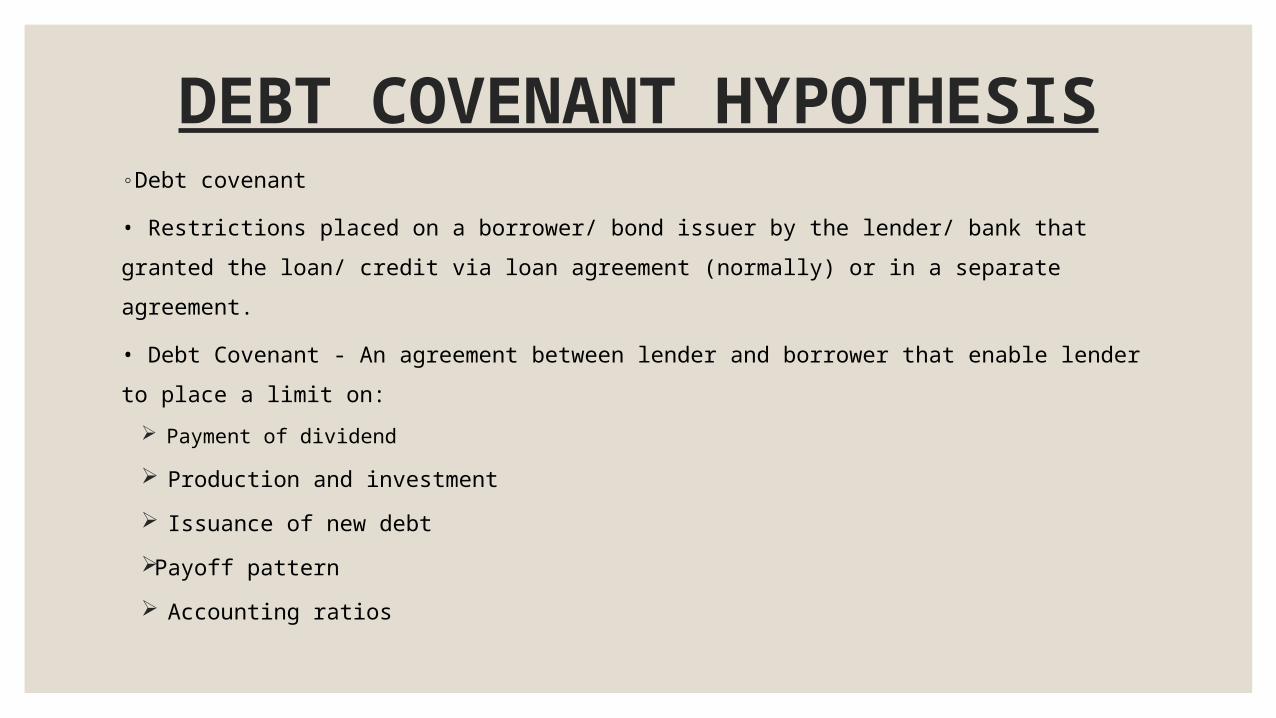

DEBT COVENANT HYPOTHESIS

◦Debt covenant

• Restrictions placed on a borrower/ bond issuer by the lender/ bank that granted

the loan/ credit via loan agreement (normally) or in a separate agreement.

• Debt Covenant - An agreement between lender and borrower that enable lender to

place a limit on:

Payment of dividend

Production and investment

Issuance of new debt

Payoff pattern

Accounting ratios

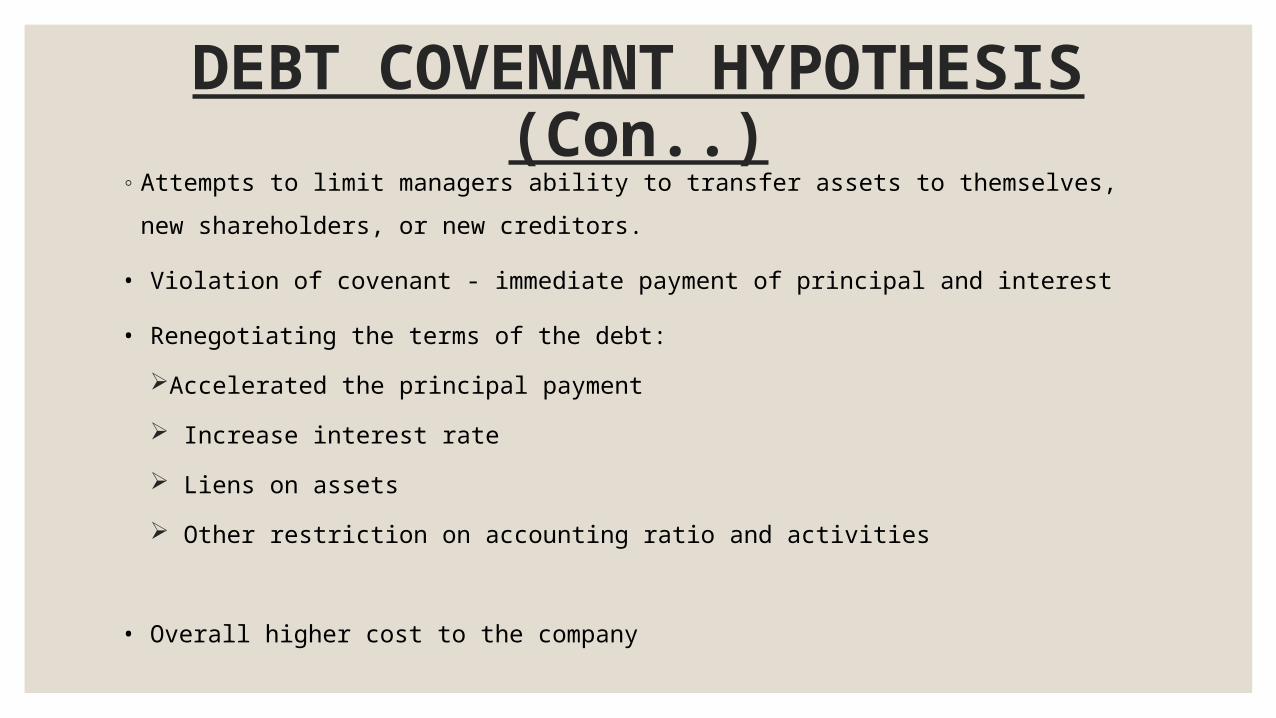

DEBT COVENANT HYPOTHESIS (Con..)

◦ Attempts to limit managers ability to transfer assets to themselves, new

shareholders, or new creditors.

• Violation of covenant - immediate payment of principal and interest

• Renegotiating the terms of the debt:

Accelerated the principal payment

Increase interest rate

Liens on assets

Other restriction on accounting ratio and activities

• Overall higher cost to the company

DEBT COVENANT HYPOTHESIS (Con..)

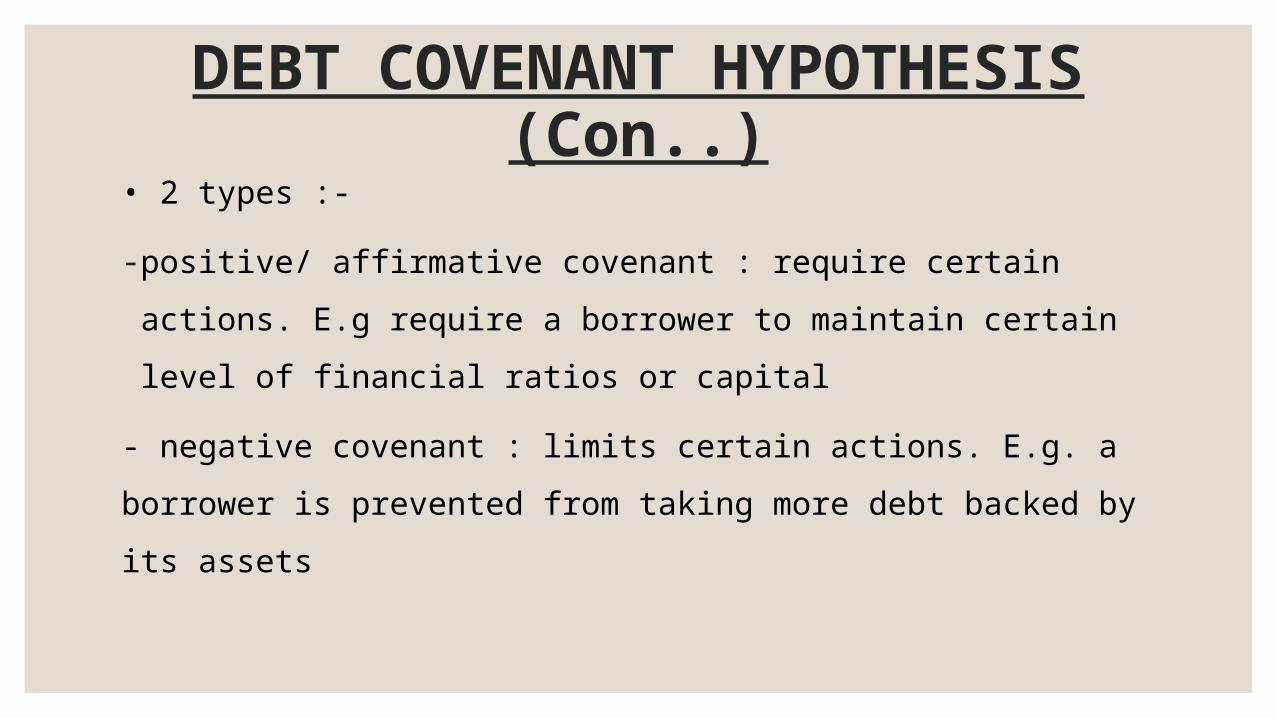

• 2 types :-

- positive/ affirmative covenant : require certain actions. E.g

require a borrower to maintain certain level of financial ratios

or capital

- negative covenant : limits certain actions. E.g. a borrower is

prevented from taking more debt backed by its assets

DEBT COVENANTS AND ACCOUNTING CONSERVATISM BY VALERY V. NIKOLAEV

Author : Valeri V.Nikolaev (The University of Chicago Booth

School of Business)

Published in : Journal of Accounting Research Vol. 48 No. 1

March 2010

Purpose of study - test whether firm that rely on covenants

in their public debt contracts recognize economic losses in

earnings in a more timely fashion.

ROLE OF DEBT COVENANT• Debt covenant limit a manager’s ability to opportunistically

expropriate wealth from bondholder when a firm approach economic

distress.

• But this only become binding if the accounting system recognize the

deterioration of company’s financial position.

• Timely loss recognition is expected to improve the efficiency

more likely to binding in distress

Thus, limit opportunistic action by manager.

ROLE OF TIMELY LOSS RECOGNITION AND THE USE OF COVENANTS

Timely loss recognition enhance efficiency of debt contracting

in:

By facilitate early transfer of decision right to bondholders

Facilitate the signalling role of covenants.

HYPOTHESES

Timely recognition of economic losses increase with the use of

debt covenants in public debt contract

Companies that rely on debt covenants more extensively

exhibit a greater increase in timely recognition of economic

losses following debt issue.

FINDING

Public debt contract employ more covenants exhibit timelier

recognition of economic losses

Exhibit higher level of timely loss recognition both before and

after the issue

Extensively experience an increase in timely loss recognition

after the issue. Thus, use of covenants in public debt contracts

is associated with increased demand for timely loss

recognition.

POLITICAL COST HYPOTHESIS

POLITICAL COST

◦The term political costs is used to refer to the costs that

particular groups external to the firm might be able to impose

on the firm, such as the costs associated with increased taxes,

increased wage claims or product boycott.

◦Government, trade unions, environmental lobby groups or

particular consumer groups affect organizations.

POLITICAL COST (conts)

◦The demands placed on firms by particular interest groups

might be affected by the accounting results of the firm.

◦For example, if a firm were to record high profits, this might be

used as an excuse for the trade unions to take action to

increase their members’ share of profits in the form of higher

wages.

POLITICAL COST (conts)◦High profits might also be used by particular groups that lobby for increased taxes or decreased subsidies on grounds of the firm’s ability to pay.

◦For example, Watts and Zimmerman (1986) examined the highly publicized claims about US oil companies made by consumers, unions and government within the USA in late 1970s.

◦These claims were that oil companies were making excessive reported profits and were in effect exploiting the nation.

◦It is considered that such claims could have led to the imposition of additional taxes in the form of ‘excess profits’ taxes.

POLITICAL COST (conts)◦Governments seeking re-election could be motivated to take action against unpopular firms if it was felt that they would secure a net increase in electoral support.

◦This obviously assumes that the actions of most politicians are motivated by a desire to be re-elected – perhaps not an unrealistic assumption and certainly consistent with the PAT contention that actions of all individuals can best be explained by the assumption of self interest.

◦It is argued within PAT that accounting numbers can be used as a means of providing ‘excuses’ for effecting wealth transfers in the political process.

POLITICAL COST (conts)

◦High profits might also be used by consumer groups to justify

assuming a position that prices are too high.

◦Media reports of high corporate profitability trigger political

costs of a firm.

POLITICAL COST (conts)◦In a sense, the reported accounting profits of particular organizations are used as an excuse to push for higher wages, which could be costly for these organizations.

◦However, if reported profits were not so high, perhaps this would reduce the likelihood of demands for increased wages.

◦Therefore, if managers consider that there might be claims for increased wages in particular years, those managers might elect to adopt income-decreasing accounting methods.

◦For example, they might depreciate assets over fewer years, thereby increasing depreciation expenses and consequently reducing profits.

THANK YOU