Embed Size (px)

Citation preview

Lehman Brothers 6th Annual Worldwide Wireless and Wireline ConferenceNYC, June 3, 2005

Christoph CaselitzPresident Siemens Communications Mobile Networks

Positioning to Win

Safe Harbor Statement

This presentation contains forward-looking statements and information – that is, statements related to future, not past, events. These statements may be identified either orally or in writing by words as “expects,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “estimates,” “will” or words of similar meaning. Such statements are based on our current expectations and certain assumptions, and are, therefore, subject to certain risks and uncertainties. A variety of factors, many of which are beyond Siemens' control, affect its operations, performance, business strategy and results and could cause the actual results, performance or achievements of Siemens worldwide to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements. For us, particular uncertainties arise, among others, from changes in general economic and business conditions, changes in currency exchange rates and interest rates, introduction of competing products or technologies by other companies, lack of acceptance of new products or services by customers targeted by Siemens worldwide, changes in business strategy and various other factors. More detailed information about certain of these factors is contained in Siemens' filings with the SEC, which are available on the Siemens website, www.siemens.com and on the SEC's website, www.sec.gov. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in the relevant forward-looking statement as anticipated, believed, estimated, expected, intended, planned or projected. Siemens does not intend or assume any obligation to update or revise these forward-looking statements in light of developments which differ from those anticipated.

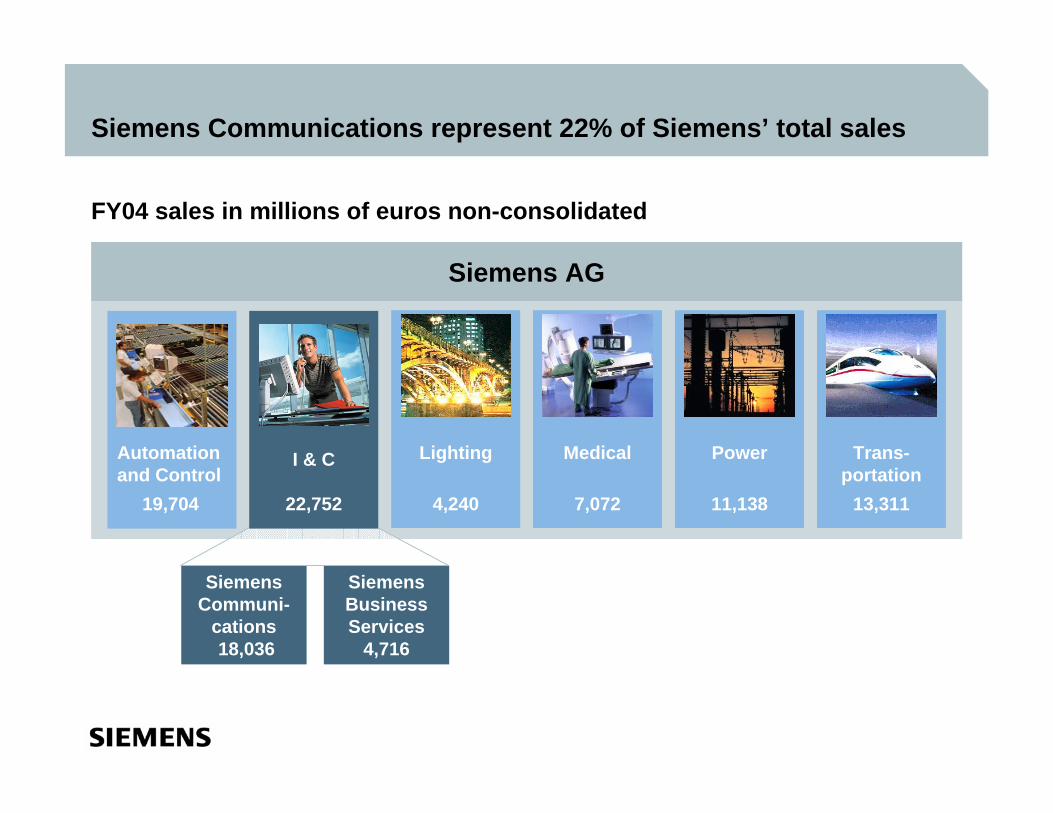

Siemens AG

Trans-portation

13,311

Power

11,138

Medical

7,072

Lighting

4,240

Automation and Control

19,704

FY04 sales in millions of euros non-consolidated

Siemens Communications represent 22% of Siemens’ total sales

Siemens Communi-

cations18,036

Siemens Business Services

4,716

I & C

22,752

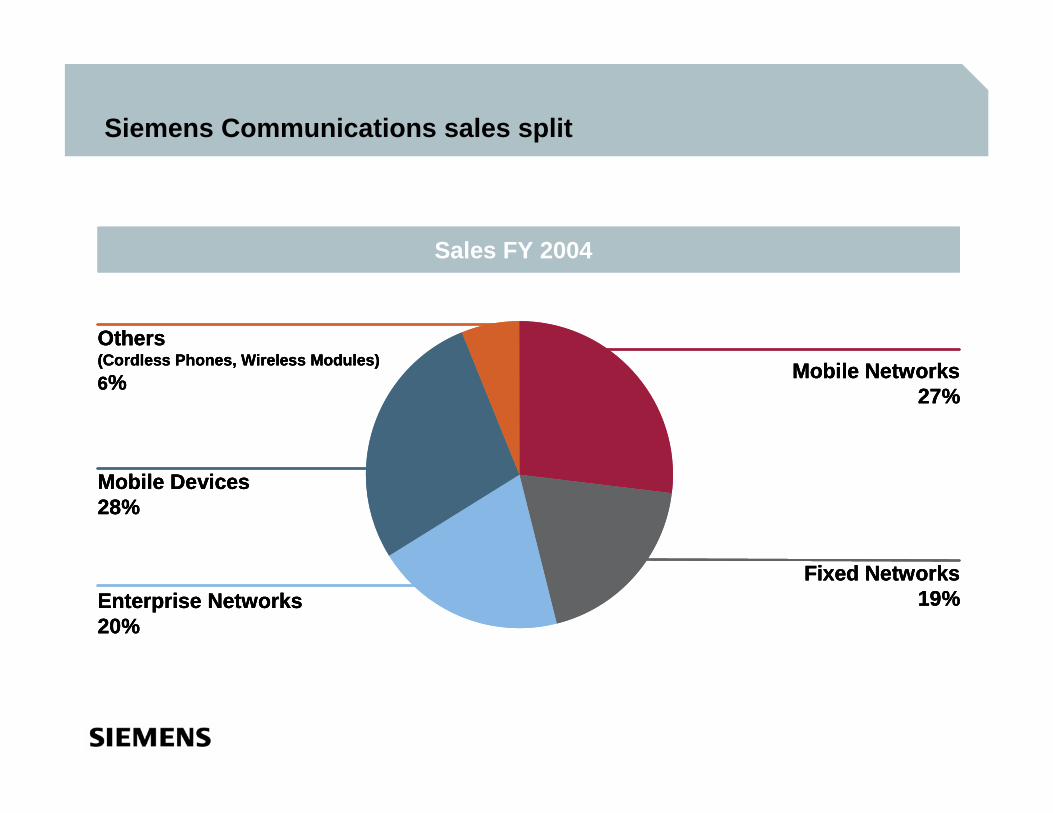

Siemens Communications sales split

Sales FY 2004

Others(Cordless Phones, Wireless Modules)6%

Mobile Devices28%

Fixed Networks19%

Mobile Networks 27%

Enterprise Networks 20%

Sales FY 2004

Others(Cordless Phones, Wireless Modules)6%

Mobile Devices28%

Fixed Networks19%

Mobile Networks 27%

Enterprise Networks 20%

Sales FY 2004

Others(Cordless Phones, Wireless Modules)6%

Mobile Devices28%

Fixed Networks19%

Mobile Networks 27%

Enterprise Networks 20%

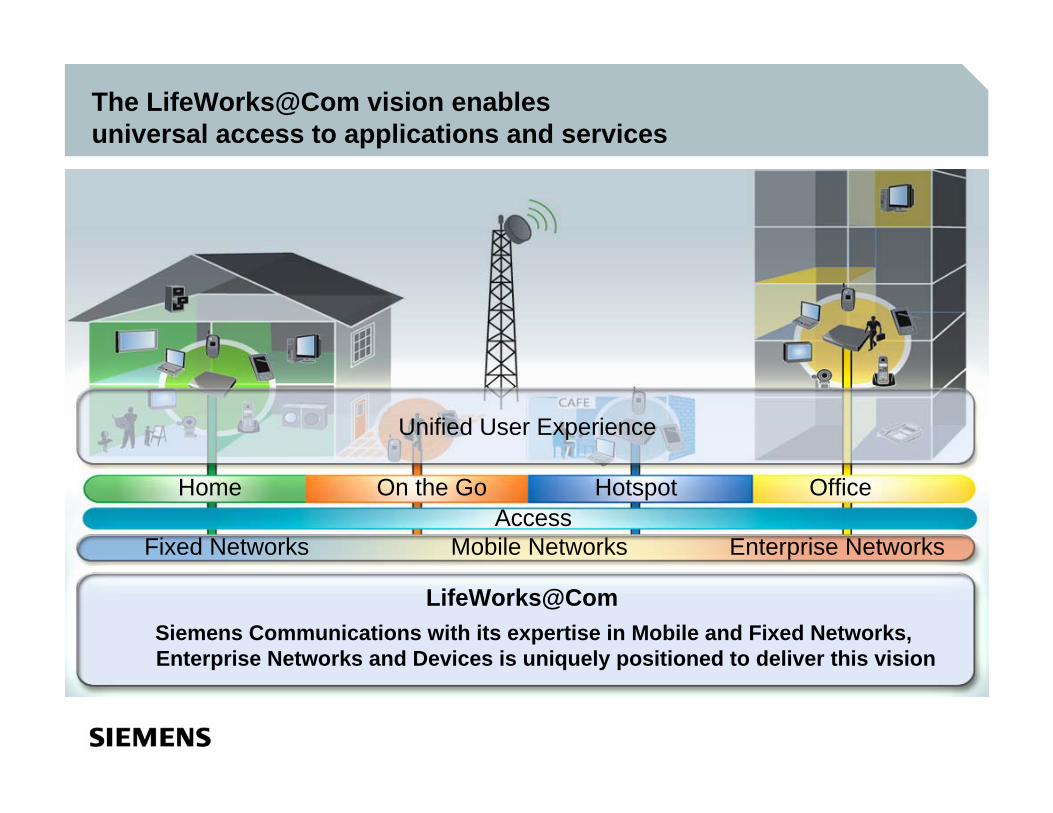

The LifeWorks@Com vision enables universal access to applications and services

Siemens Communications with its expertise in Mobile and Fixed Networks, Enterprise Networks and Devices is uniquely positioned to deliver this vision

LifeWorks@Com

AccessFixed Networks Mobile Networks Enterprise Networks

Unified User Experience

Home On the Go Hotspot Office

0

175

350

525

700

Latin America Mideast & Africa Asia Pacific

Total mobile subscriber baseGSM subscriber base

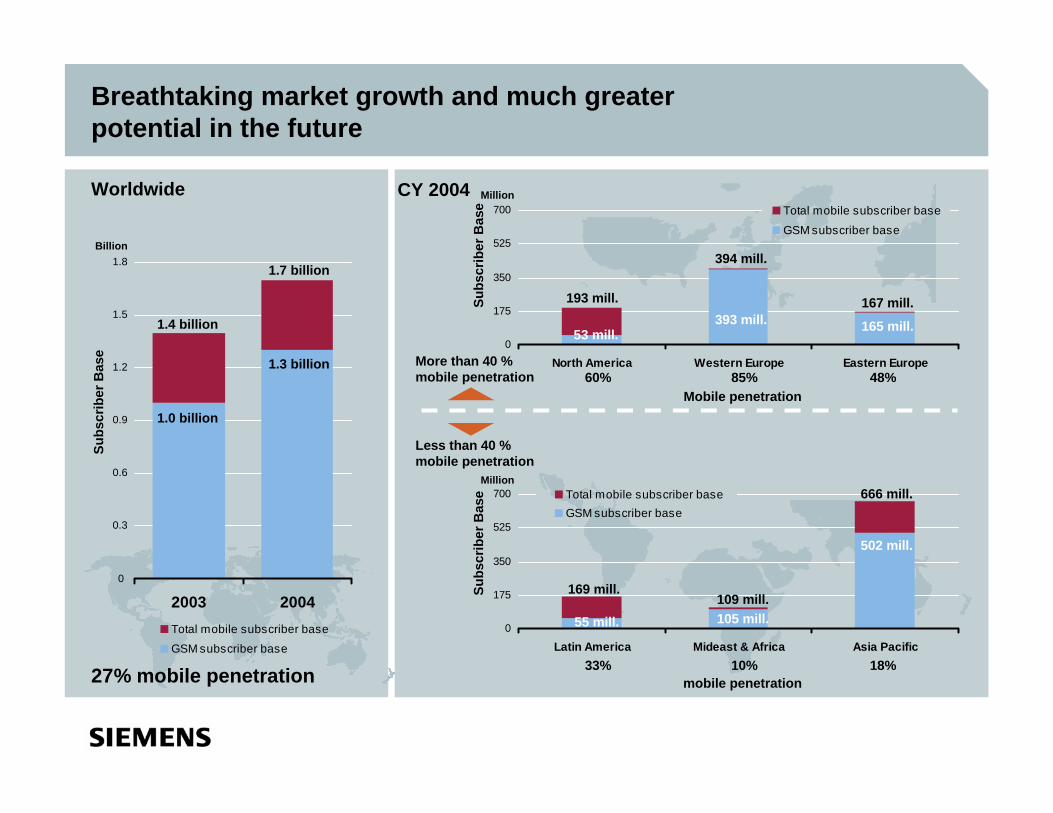

Breathtaking market growth and much greater potential in the future

Worldwide

More than 40 % mobile penetration

Less than 40 % mobile penetration

0,0

0,3

0,6

0,9

1,2

1,5

1,8

2003 2004Total mobile subscriber baseGSM subscriber base

1.0 billion

1.4 billion

Billion

1.3 billion

1.7 billion

27% mobile penetration

0

175

350

525

700

North America Western Europe Eastern Europe

Total mobile subscriber base

GSM subscriber base

48%85%60%

Subs

crib

er B

ase

Subs

crib

er B

ase

193 mill.

53 mill.

394 mill.

393 mill.167 mill.

165 mill.

Subs

crib

er B

ase

169 mill.

55 mill.109 mill.105 mill.

666 mill.

502 mill.

18%10%33%

Mobile penetration

CY 2004

mobile penetration

Million

1.8

1.5

1.2

0.9

0.6

0.3

0

Million

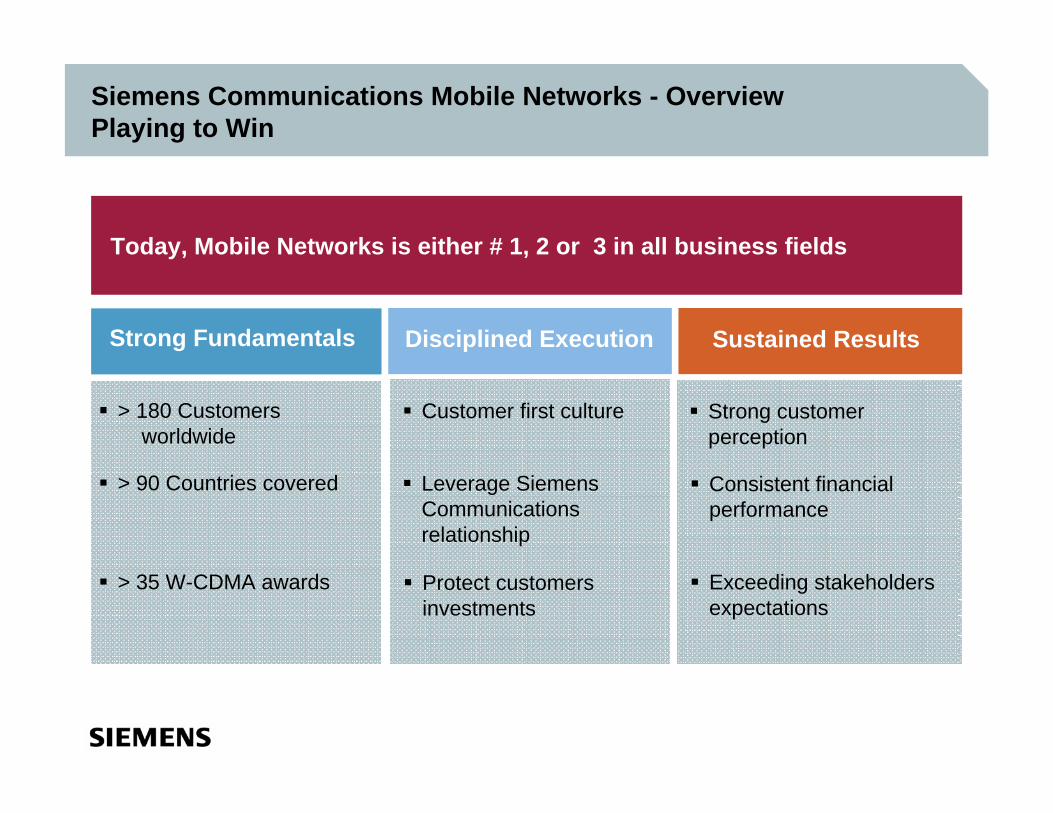

Siemens Communications Mobile Networks - OverviewPlaying to Win

Today, Mobile Networks is either # 1, 2 or 3 in all business fields

Strong Fundamentals Disciplined Execution Sustained Results

> 180 Customersworldwide

Customer first culture Strong customer perception

> 90 Countries covered

> 35 W-CDMA awards

Leverage Siemens Communications relationship

Protect customers investments

Consistent financial performance

Exceeding stakeholders expectations

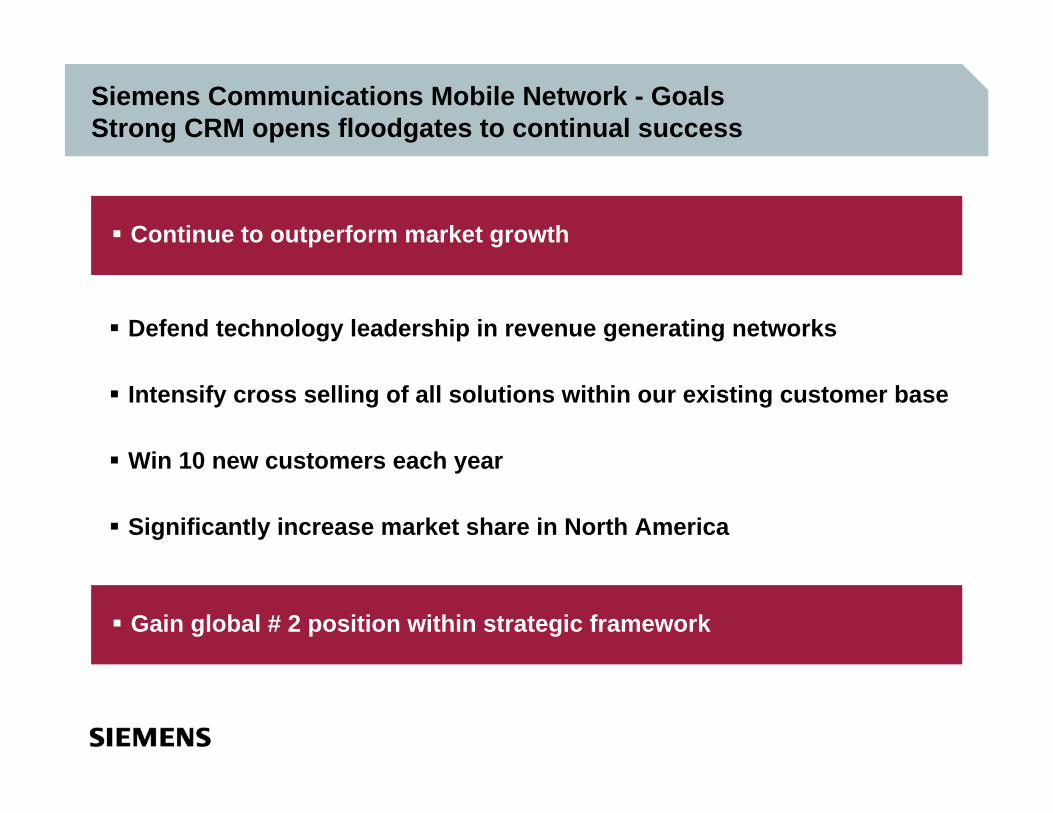

Siemens Communications Mobile Network - GoalsStrong CRM opens floodgates to continual success

Continue to outperform market growth

Defend technology leadership in revenue generating networks

Intensify cross selling of all solutions within our existing customer base

Win 10 new customers each year

Significantly increase market share in North America

Gain global # 2 position within strategic framework

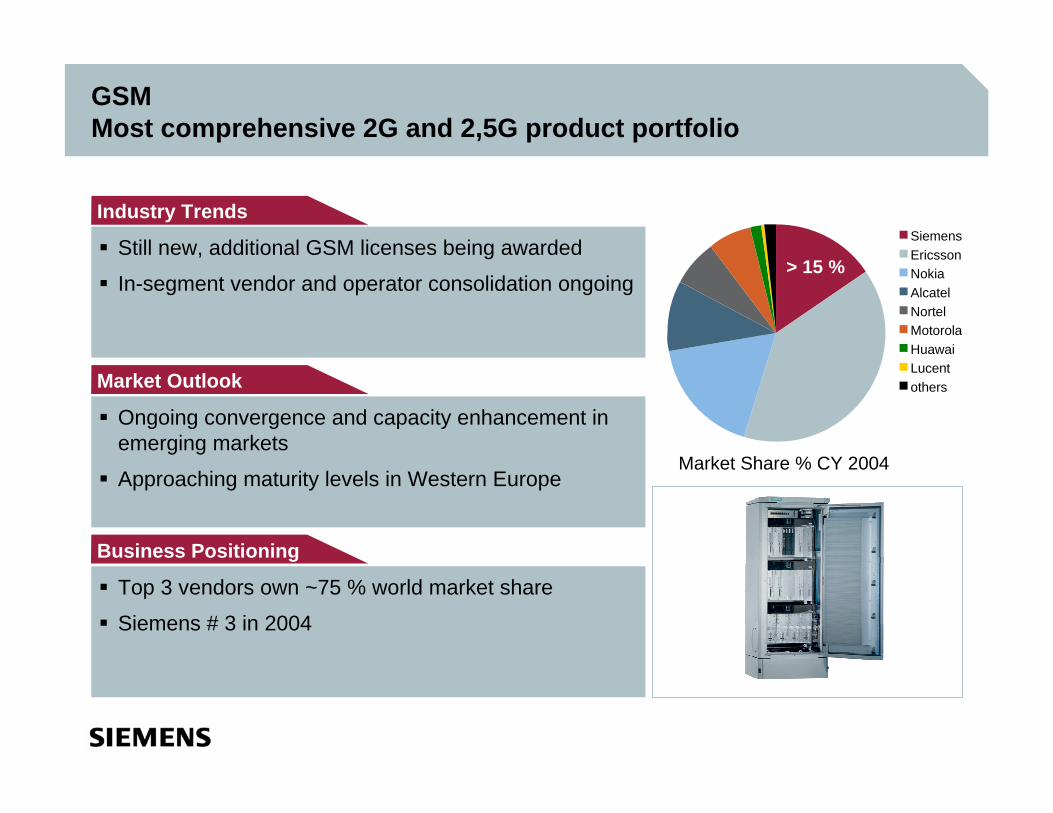

GSMMost comprehensive 2G and 2,5G product portfolio

Market Share % CY 2004

Still new, additional GSM licenses being awarded

In-segment vendor and operator consolidation ongoing

Industry Trends

Ongoing convergence and capacity enhancement in emerging markets

Approaching maturity levels in Western Europe

Market Outlook

Top 3 vendors own ~75 % world market share

Siemens # 3 in 2004

Business Positioning

> 15 %

SiemensEricssonNokiaAlcatelNortelMotorolaHuawaiLucentothers

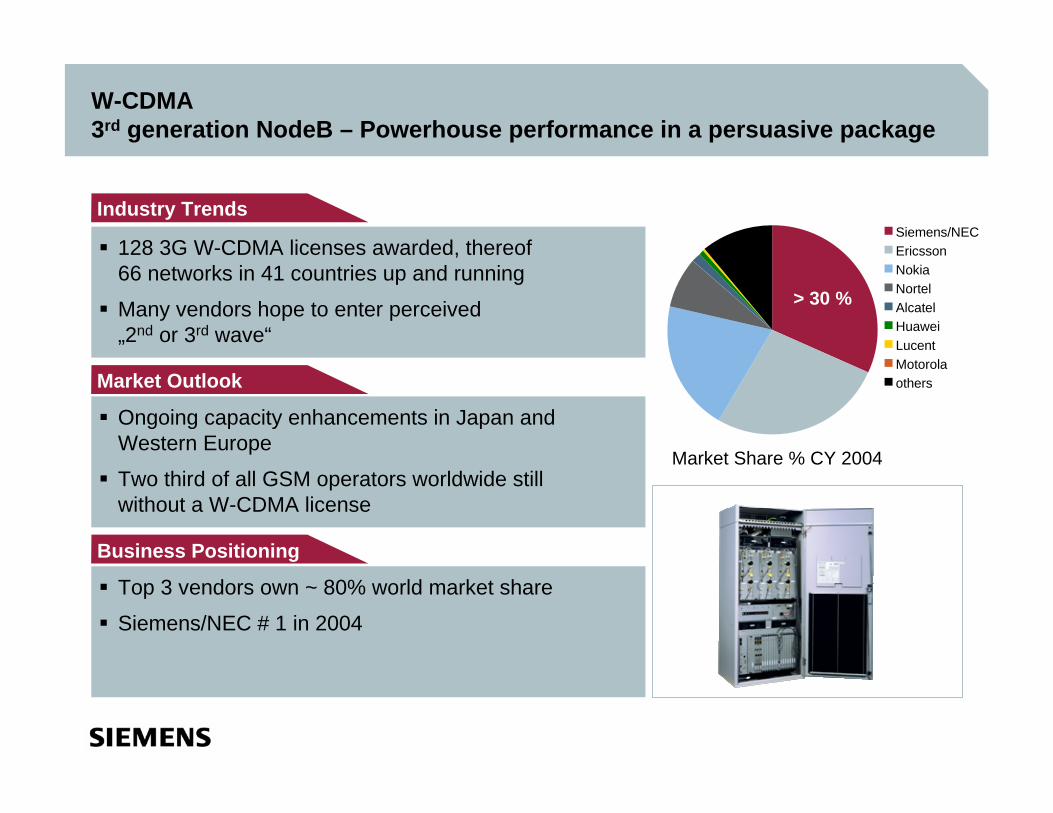

W-CDMA3rd generation NodeB – Powerhouse performance in a persuasive package

128 3G W-CDMA licenses awarded, thereof 66 networks in 41 countries up and running

Many vendors hope to enter perceived „2nd or 3rd wave“

Ongoing capacity enhancements in Japan and Western Europe

Two third of all GSM operators worldwide still without a W-CDMA license

Top 3 vendors own ~ 80% world market share

Siemens/NEC # 1 in 2004

Industry Trends

Market Outlook

Business Positioning

Market Share % CY 2004

> 30 %

Siemens/NECEricssonNokiaNortelAlcatelHuaweiLucentMotorolaothers

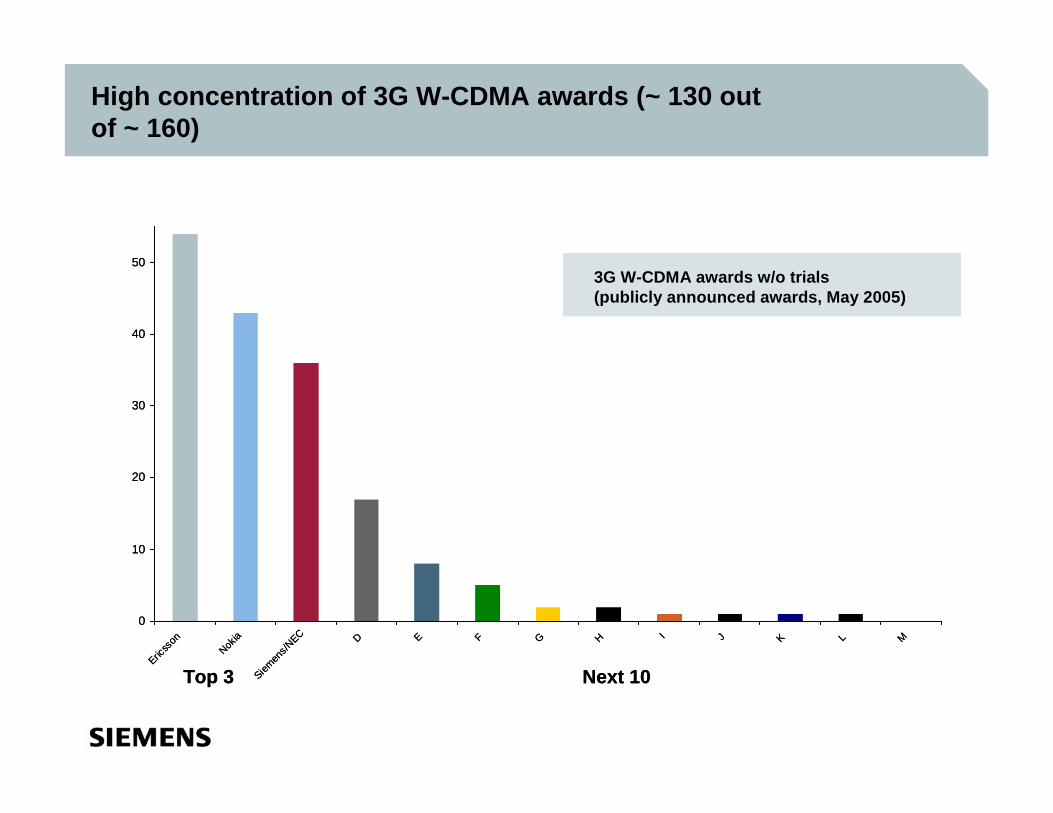

High concentration of 3G W-CDMA awards (~ 130 out of ~ 160)

0

10

20

30

40

50

Ericss

on

Nokia

Siemen

s/NEC D E F G H I J K L M

Top 3 Next 10

3G W-CDMA awards w/o trials(publicly announced awards, May 2005)

0

10

20

30

40

50

Ericss

on

Nokia

Siemen

s/NEC D E F G H I J K L M

Top 3 Next 10

3G W-CDMA awards w/o trials(publicly announced awards, May 2005)3G W-CDMA awards w/o trials(publicly announced awards, May 2005)

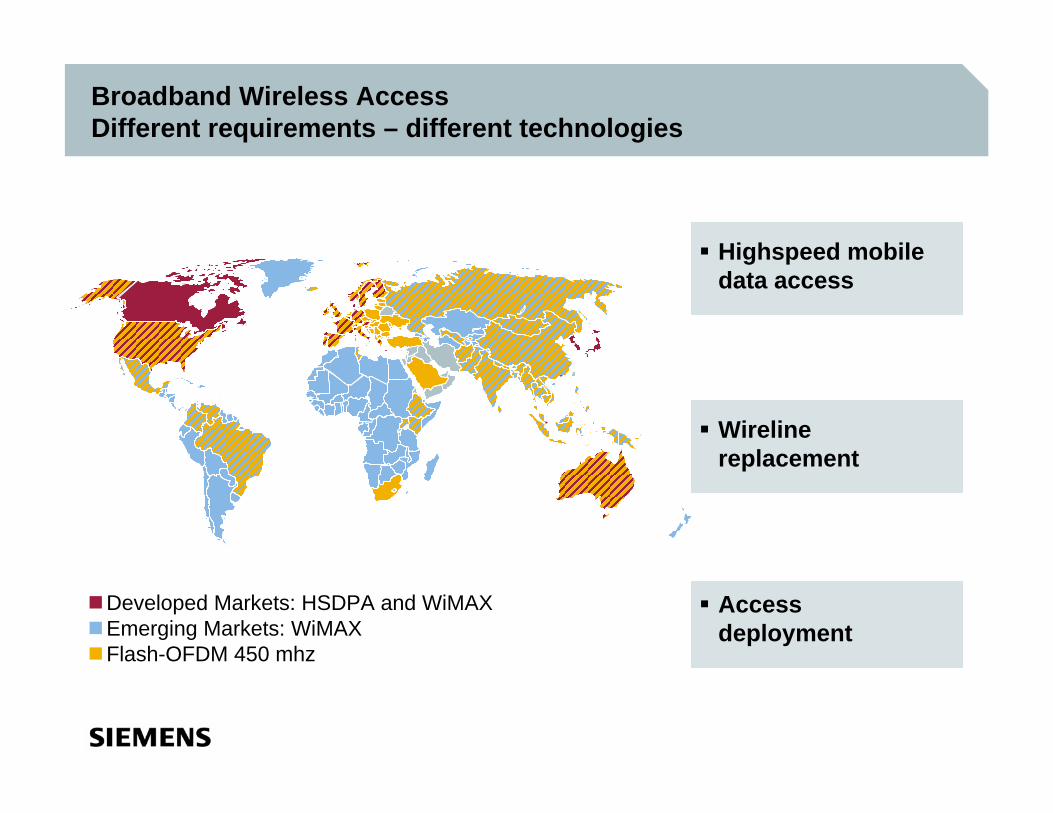

Broadband Wireless AccessDifferent requirements – different technologies

Developed Markets: HSDPA and WiMAXEmerging Markets: WiMAXFlash-OFDM 450 mhz

Highspeed mobile data access

Wireline replacement

Access deployment

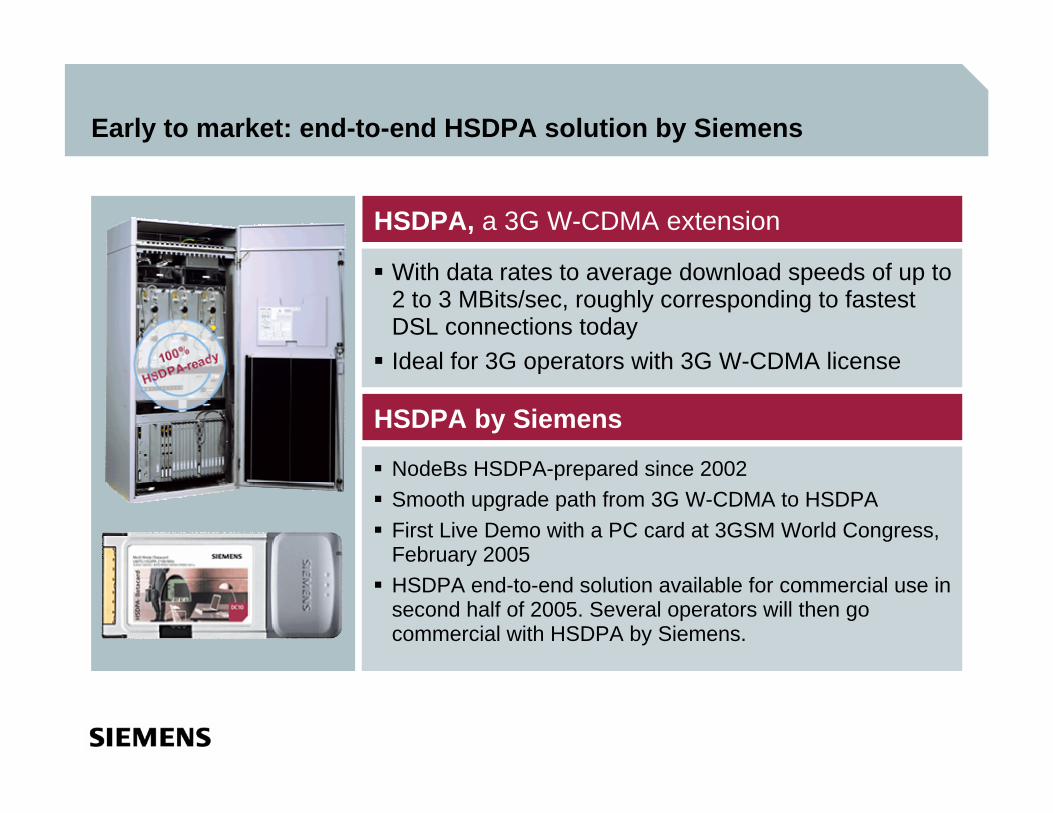

Early to market: end-to-end HSDPA solution by Siemens

With data rates to average download speeds of up to 2 to 3 MBits/sec, roughly corresponding to fastest DSL connections todayIdeal for 3G operators with 3G W-CDMA license

NodeBs HSDPA-prepared since 2002Smooth upgrade path from 3G W-CDMA to HSDPA First Live Demo with a PC card at 3GSM World Congress, February 2005HSDPA end-to-end solution available for commercial use in second half of 2005. Several operators will then go commercial with HSDPA by Siemens.

HSDPA, a 3G W-CDMA extension

HSDPA by Siemens

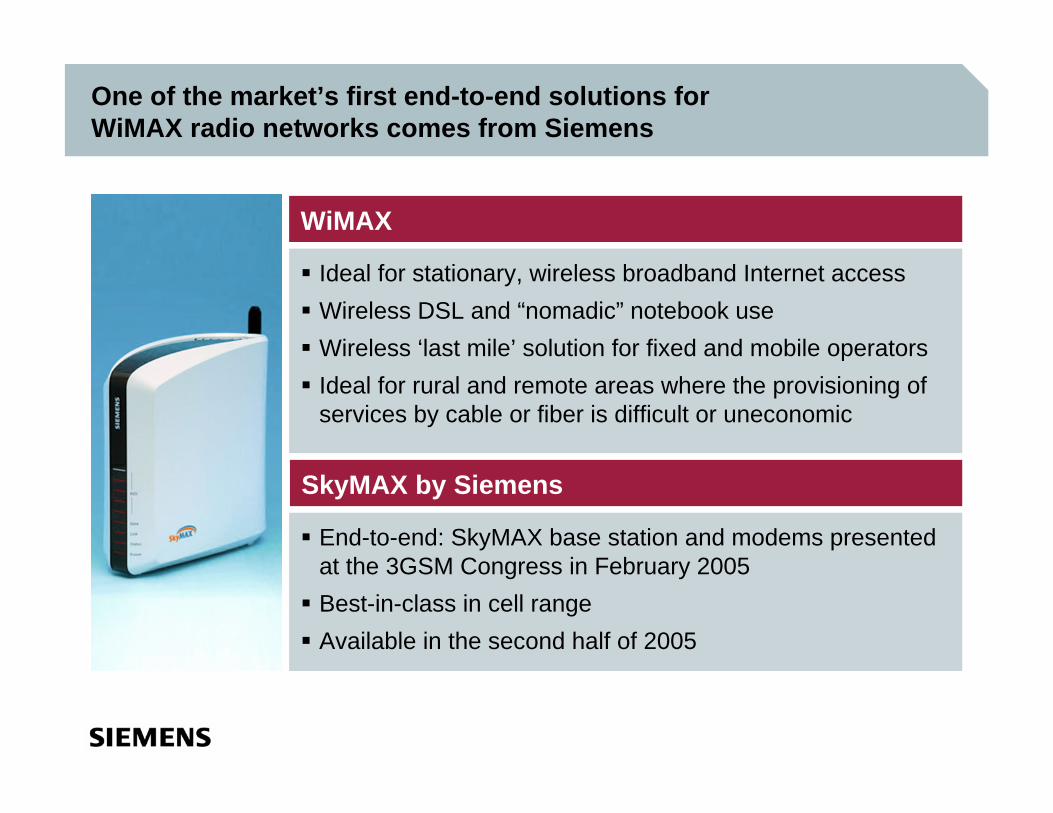

One of the market’s first end-to-end solutions for WiMAX radio networks comes from Siemens

Ideal for stationary, wireless broadband Internet accessWireless DSL and “nomadic” notebook useWireless ‘last mile’ solution for fixed and mobile operatorsIdeal for rural and remote areas where the provisioning of services by cable or fiber is difficult or uneconomic

End-to-end: SkyMAX base station and modems presented at the 3GSM Congress in February 2005Best-in-class in cell rangeAvailable in the second half of 2005

WiMAX

SkyMAX by Siemens

Only Siemens provides Flash-OFDM 450 MHz products

Network technology from Flarion

For operators with access to the 450MHz spectrum

Cost effective delivery of high speed data services over a wide coverage area

Flash-OFDM

Only Siemens provides Flash-OFDM 450 MHz products

Integration of Flash-OFDM technology into Siemens NodeBs and network management systems possible

End-to-end solution for Flash-OFDM 450 MHz will be available by the second quarter of 2005

Flash-OFDM by Siemens

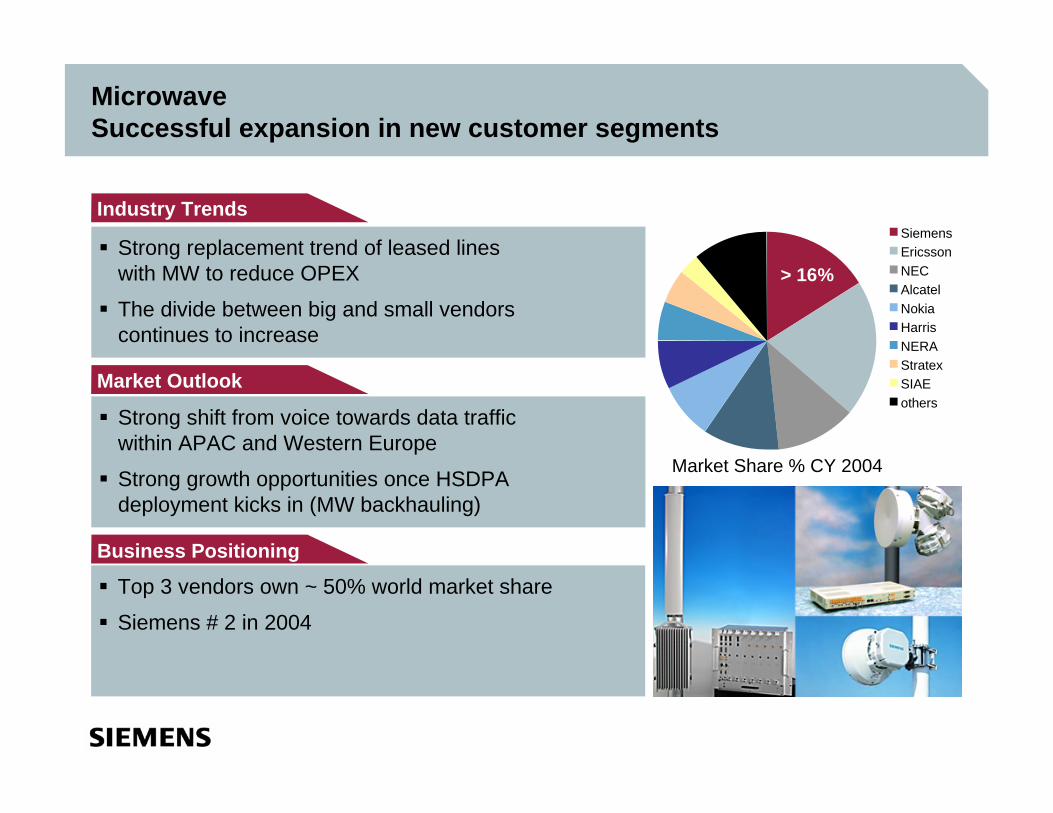

MicrowaveSuccessful expansion in new customer segments

Strong replacement trend of leased lines with MW to reduce OPEX

The divide between big and small vendors continues to increase

Strong shift from voice towards data traffic within APAC and Western Europe

Strong growth opportunities once HSDPA deployment kicks in (MW backhauling)

Positioning

Top 3 vendors own ~ 50% world market share

Siemens # 2 in 2004

Industry Trends

Market Outlook

Business Positioning

Market Share % CY 2004

> 16%

SiemensEricssonNECAlcatelNokiaHarrisNERAStratexSIAEothers

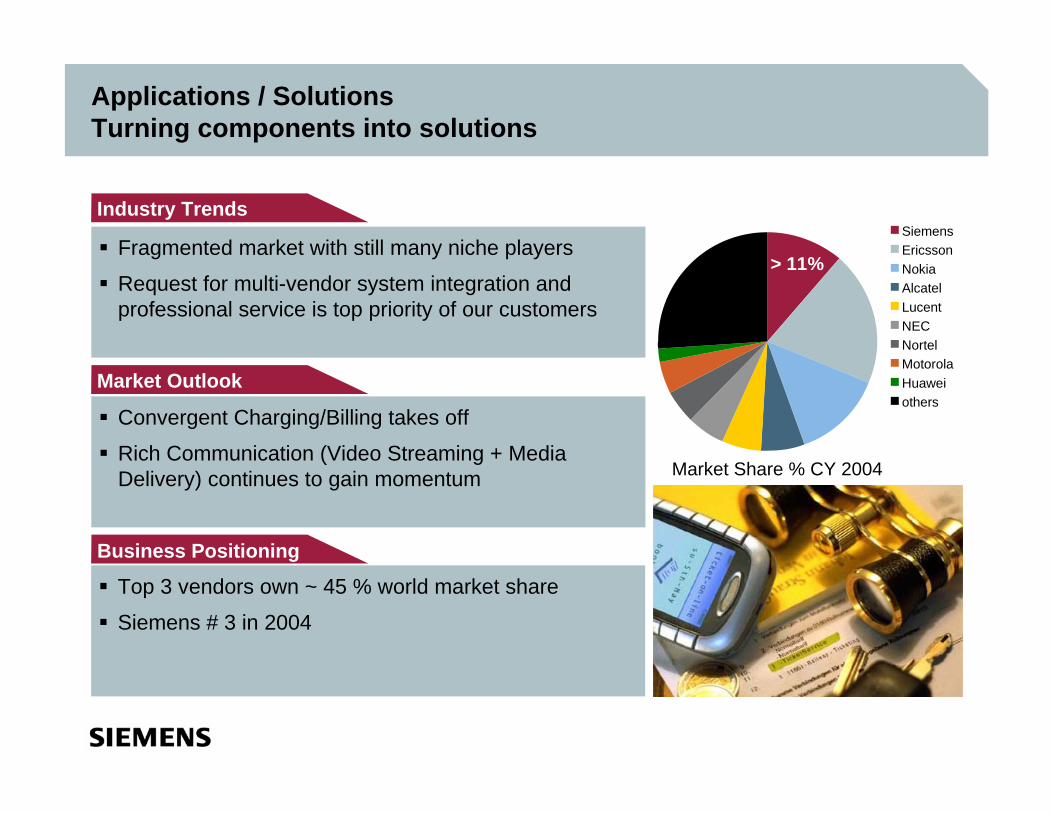

Applications / SolutionsTurning components into solutions

Fragmented market with still many niche players

Request for multi-vendor system integration and professional service is top priority of our customers

Convergent Charging/Billing takes off

Rich Communication (Video Streaming + Media Delivery) continues to gain momentum

Top 3 vendors own ~ 45 % world market share

Siemens # 3 in 2004

Industry Trends

Market Outlook

Business Positioning

Market Share % CY 2004

> 11%

SiemensEricssonNokiaAlcatelLucentNEC NortelMotorolaHuaweiothers

Summary

Continue to outperform market growth

Profitable Growth

Intensify cross selling of all solutions within our existing customer base

Defend technology leadership in revenue generating networks

Reconciliations and definitions

”Group profit from Operations” is reconciled to ”Income before income taxes” of Operations under ”Reconciliation to financial statements” on the table ”Segment information.” See ”Financial Reports/Fiscal 2005, Quarter 2 / Financial Statements” at our Investor Relations website under www.siemens.com

The allocated equity for SFS is determined and influenced by the respective credit ratings of the rating agencies and by the expected size and quality of its portfolio of leasing and factoring assets and equity investments and is determined annually. This allocation is designed to cover the risks of the underlying business and is in line with common credit risk management standards in banking. The actual risk profile of the SFS portfolio is monitored and controlled monthly and is evaluated against the allocated equity.

”ROE” (Return on equity) margin for SFS was calculated as SFS' income before income taxes divided by the allocated equity for SFS. Allocated equity for SFS as of September 30, 2004 was €1.015 billion. See also Siemens' Form 20-F at our Investor Relations website under www.siemens.com

Siemens ties a portion of its executive incentive compensation to achieving economic value added (EVA) targets. EVA measures the profitability of a business (using Group profit for the Operating Groups and income before income taxes for the Financing and Real estate businesses as a base) against the additional cost of capital used to run a business, (using Net capital employed for the Operating Groups and risk-adjusted equity for the Financing and Real estate businesses as a base). A positive EVA means that a business has earned more than its cost of capital, and is therefore defined as value-creating. A negative EVA means that a business is earning less than its cost of capital and is therefore defined as value-destroying. Other organizations that use EVA may define and calculate EVA differently.

A reconciliation of EVA may be found on our Investor Relations website under www.siemens.com

Siemens Investor Relations Team

Webpage: http://www.siemens.com Investor Relations

e-mail: [email protected]

Fax: +49-89-636-32830

Marcus Desimoni +49-89-636-32445

Dr. Constantin Birnstiel +49-89-636-36165

Irina Pchelova +49-89-636-33693

Christina Schmöe +49-89-636-32677

Susanne Wölfinger +49-89-636-30639