Embed Size (px)

Citation preview

Wendy J. Dominguez, MBA

PORTFOLIO REVIEW4th Quarter 2015

Rick Rodgers, AIFA®

Prepared by: Josh Bond

THIS PAGE LEFT INTENTIONALLY BLANK

2INTEGRITY. BALANCE. OBJECTIVITY.

INNOVEST AT A GLANCE

—

———

——

——

———

—

——

—

—

——

—

—

—

—

—

—

—

—

—

—

—

—

—

—

—

————

*As of December 2015

Privileged and Confidential

3INTEGRITY. BALANCE. OBJECTIVITY.

Innovest’s History With Boulder Fire & Police

2001 ‐ 2003

2001: First quarterly performance report

2003: Replace the Putnam International Fund with the American Funds Europacific Growth Fund

2007: Replace the Calamos Growth Fund with Allianz CCM Mid Cap Growth & replace the Legg Mason Small Cap Value Fund with the ICM Small Cap Value

2007: Replace 50% of the allocation to the Europacific Growth Fund (REREX) and allocate it to the Dodge & Cox International Fund

2007: Conducted asset allocation study and updated asset allocation

2007: Coordinated the PIMCO share class change to reduce fees

2008: Conducted asset allocation study and updated asset allocation

2009: Add BlackRock High Yield Fund and Eaton Vance Floating Rate Fund

Provided quarterly performance reports and research reports each quarter and met with the Trustees

Updated and reviewed the Investment Policy Statement

Met with representatives from each investment strategy used in the plans

2003 ‐ 2006 2006 – 2009 2009 ‐ 2014

2004: Replace the One Group Mid Cap Growth Fund (OSGIX) with the Calamos Growth Fund

2005: Presented on Alternative Investment Vehicles,Asset Classes & Strategies

2005: Added the PIMCO Commodity Real Return Strategy Fund

2005: Conducted asset allocation study and updated asset allocation

2006: Conducted asset allocation study and updated asset allocation

2010: Replace Managers Cadence MC Inst. (MCMYX) with Munder Mid Cap Growth

2011: Coordinated the Eaton Vance share class change to reduce fees

Provided quarterly performance reports and research reports each quarter and met with the Administrative Committee

2013: Performed RFI for Administration and Record Keeping Services and Audit Services.

2014: Conducted asset allocation study and updated asset allocation

Conducted consultant fee review

Presented core fixed income search

4INTEGRITY. BALANCE. OBJECTIVITY.

Innovest’s History With Boulder Fire & Police

2015: Replaced PIMCO Total Return with Metropolitan West Total Return Bond Fund.

Replaced PIMCO Commodity Real Return with Credit Suisse Commodity Return.

Created an automated, online, and permanent Fiduciary File

2015

5INTEGRITY. BALANCE. OBJECTIVITY.

Performance Over Time

Risk and Return (Since Inception) Asset Allocation

Cumulative Performance over Time

Change in Account ValueLast

QuarterYear To

Date1

Year3

Years5

Years7

YearsSince

InceptionInception

DateBoulder F & P Total Fund 1.93 -3.25 -3.25 6.81 6.34 9.98 9.05 01/01/1985Boulder F & P Custom Benchmark 3.02 -1.26 -1.26 7.52 6.98 10.02 9.55Difference -1.09 -1.99 -1.99 -0.71 -0.64 -0.04 -0.50

Market ValueAs of

10/01/2015

Market ValueAs of

12/31/2015Change

$

Boulder F & P Total Fund 116,035,139 118,384,516 2,349,377

$0 $11,150,317 $22,300,634 $33,450,951 $44,601,268 $55,751,585

VT Retirement Income Advantage

JPMorgan High Yield Select

Met West Total Return

Crdt Suis Comm Rtn Strat

Vantage Trust Plus

Victory Munder Mid Cap Core Growth

ICM Small Company

Eaton Vance Floating Rate; I

Dodge & Cox Int'l

American Funds EuroPacific Gr

Boston Trust Fixed Income - Boulder F&P

Boston Trust Equity - Boulder F&P

$210,331

$2,116,118

$4,292,877

$4,846,113

$7,187,915

$7,224,152

$7,296,884

$7,380,536

$10,544,522

$10,735,829

$12,424,090

$44,125,148

8.5

9.0

9.5

10.0

10.5

11.0

11.5

Ret

urn

(%)

9.0 10.0 11.0 12.0 13.0 14.0 15.0 16.0 17.0Risk (Standard Deviation %)

S&P 500 Index

Boulder F & P Total Fund

Boulder F & P Total Fund Boulder F & P Custom Benchmark

-600 %

0%

600%

1,200%

1,800%

2,400%

3/85 9/86 3/88 9/89 3/91 9/92 3/94 9/95 3/97 9/98 3/00 9/01 3/03 9/04 3/06 9/07 3/09 9/10 3/12 9/13 12/15

Executive SummaryDecember 31, 2015

6INTEGRITY. BALANCE. OBJECTIVITY.

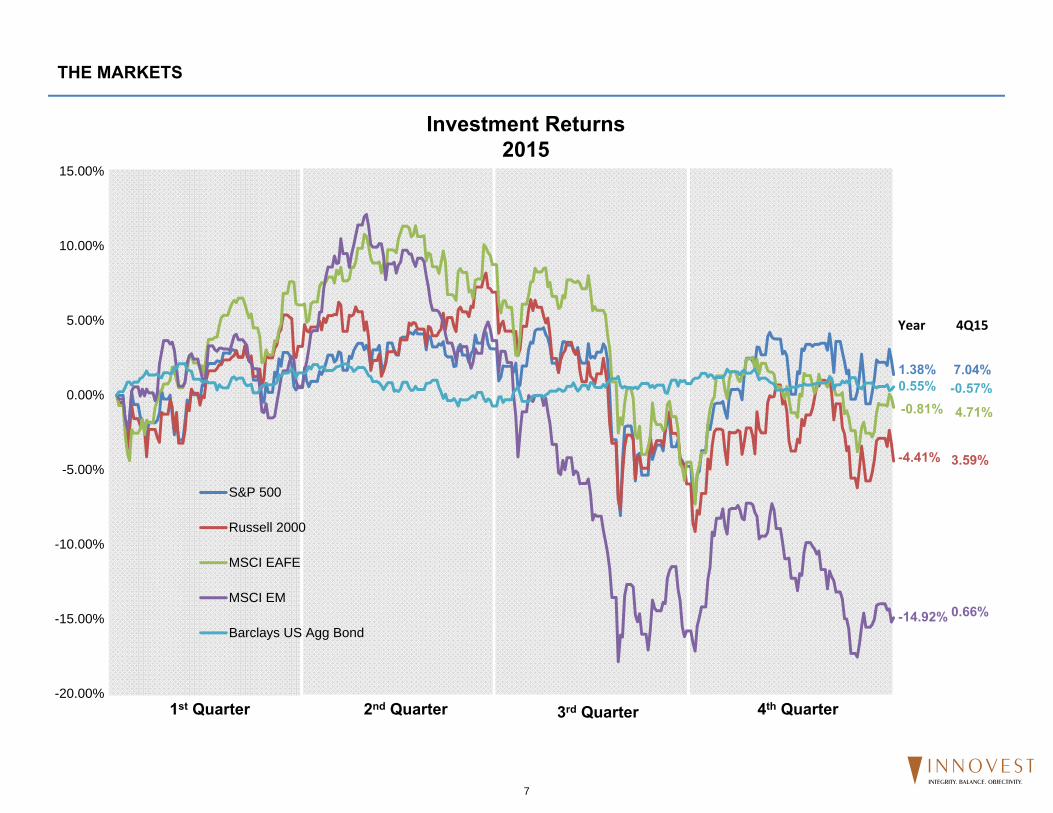

1.38%

-4.41%

-0.81%

-14.92%

0.55%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

S&P 500

Russell 2000

MSCI EAFE

MSCI EM

Barclays US Agg Bond

Year 4Q15

7.04%-0.57%

4.71%

3.59%

0.66%

THE MARKETS

Investment Returns2015

1st Quarter 2nd Quarter 3rd Quarter 4th Quarter

7INTEGRITY. BALANCE. OBJECTIVITY.

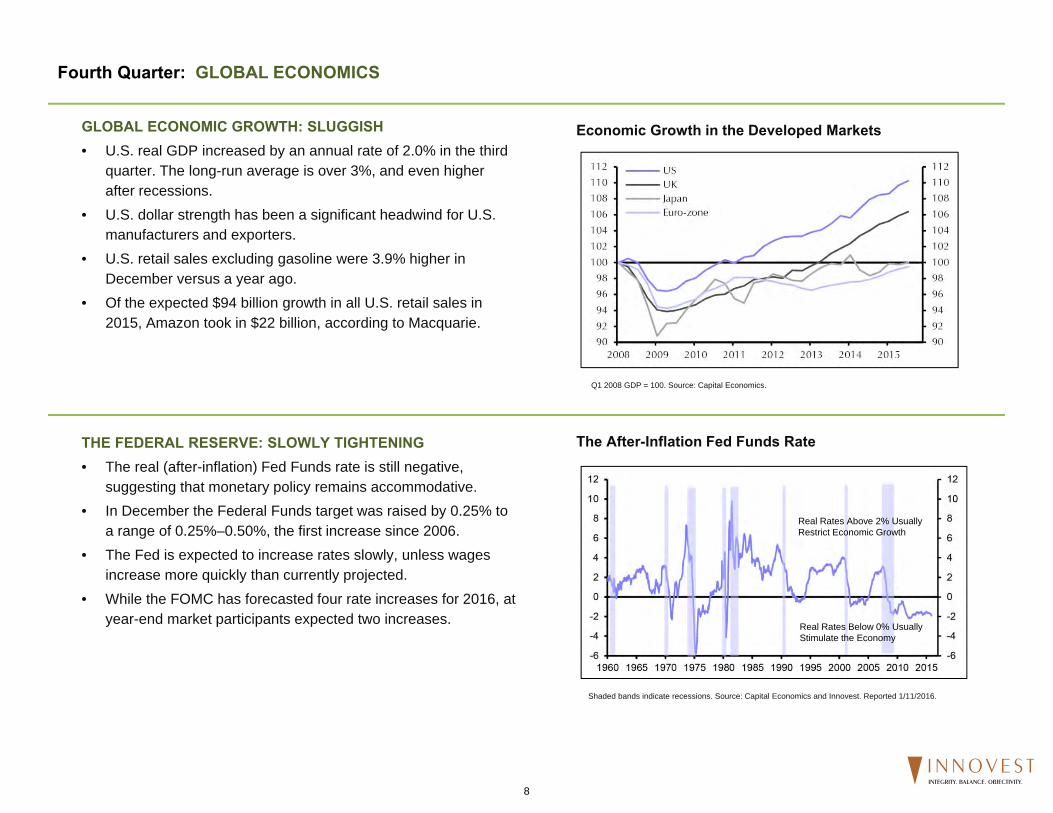

GLOBAL ECONOMIC GROWTH: SLUGGISH• U.S. real GDP increased by an annual rate of 2.0% in the third

quarter. The long-run average is over 3%, and even higher after recessions.

• U.S. dollar strength has been a significant headwind for U.S. manufacturers and exporters.

• U.S. retail sales excluding gasoline were 3.9% higher in December versus a year ago.

• Of the expected $94 billion growth in all U.S. retail sales in 2015, Amazon took in $22 billion, according to Macquarie.

THE FEDERAL RESERVE: SLOWLY TIGHTENING• The real (after-inflation) Fed Funds rate is still negative,

suggesting that monetary policy remains accommodative.• In December the Federal Funds target was raised by 0.25% to

a range of 0.25%–0.50%, the first increase since 2006.• The Fed is expected to increase rates slowly, unless wages

increase more quickly than currently projected. • While the FOMC has forecasted four rate increases for 2016, at

year-end market participants expected two increases.

Fourth Quarter: GLOBAL ECONOMICS

The After-Inflation Fed Funds Rate

Shaded bands indicate recessions. Source: Capital Economics and Innovest. Reported 1/11/2016.

Economic Growth in the Developed Markets

Q1 2008 GDP = 100. Source: Capital Economics.

Real Rates Below 0% Usually Stimulate the Economy

Real Rates Above 2% Usually Restrict Economic Growth

8INTEGRITY. BALANCE. OBJECTIVITY.

GLOBAL ECONOMICS, continued

CHINA: GROWING MORE SLOWLY• Chinese exports fell 1.8% in 2015, while imports declined

13.2%. The People’s Bank of China once again intervened to devalue the yuan to spur exports.

• Volatility in China’s currency and stock markets continued to impact investors’ sentiment throughout the world.

• Increasing labor costs have put downward pressure on Chinese corporate profits; however, higher wages boost consumption.

• China’s nominal level of GDP is now five times the size of what it was 10 years ago.

ENERGY: PRICES KEEP FALLING• Domestic oil production remained high, despite active drilling

rigs having declined by about 70% in the last 18 months.• West Texas Intermediate (WTI) started 2015 at $53 a barrel,

was near $60 at mid-year, and then collapsed to the mid-$30s at year-end.

• Global oil production is unlikely to decline soon, as OPEC has promised high production and Iran plans to pump aggressively.

• Lower gasoline prices in 2015 saved the average American driver about $540, as compared to 2014.

China’s Share of the Global Economy

Less Oil Drilling, Stubbornly High Production

Source: Capital Economics.

Reported 1/4/2016. For commodities, average of consumption of steel, copper, aluminum, zinc, tin, lead, nickel, oil, gas, coal, nuclear, cement, pork and rice. Sources: EIU, BP, World Steel Association, OECD, USGS and J.P. Morgan.

9INTEGRITY. BALANCE. OBJECTIVITY.

STOCKS• In the six previous times that the Fed began to raise short-

term rates, subsequent one-year equity returns varied significantly.

• Developed international equity markets have tended to fare relatively well after the Fed’s previous initial rate hikes.

• The rising U.S. dollar in 2015 dragged down developed markets’ equity returns by 6.6%, and emerging markets equity returns by 9.3%.

• In the third quarter of 2015, S&P 500 earnings fell by 14.1% overall, but rose 3.5% excluding the energy sector.

BONDS• Bonds have provided mixed results subsequent to the six

previous times that the Fed began to raise short-term rates.• The year-end 2.59% yield on the Barclays Aggregate Index

provides little cushion if rates rise across the yield curve.• Taxable bonds in 2015 were challenged by the Fed liftoff,

falling energy prices, and a stronger dollar.• Energy issues pulled down returns on economically sensitive

high yield bonds and floating rate corporate loans.

Fourth Quarter: ASSET CLASS FUNDAMENTALS

Data are from the six rising Fed Funds rate cycles from 1983 to 2005. *The one-year municipal bond returns are based on the four most recent rising-rate periods; the one-year high-yield bond returns are based on the five most recent rising-rate periods; and the one-year floating rate corporate bond returns are based on the three most recent rising-rate periods. Past performance is no indication of future performance. Sources: Morningstar and Innovest.

Data are from the six rising Fed Funds rate cycles from 1983 to 2005. *The one-year emerging markets equity returns are based on the two most recent rising-rate periods. Past performance is no indication of future performance. Sources: Morningstar and Innovest.

Bonds: Average One-Year Returns After Initial Fed Rate Hikes

Stocks: Average One-Year Returns After Initial Fed Rate Hikes

5.4% 2.7%

20.8%22.2%

‐20.0%

‐10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

Large Cap U.S.Stocks

Small Cap U.S.Stocks

InternationalDevelopedStocks

EmergingMarkets Stocks*

3.0% 2.7% 3.5%

6.1%

‐4.0%‐2.0%

0.0%2.0%4.0%6.0%

8.0%10.0%12.0%

Core Fixed Income Municipal FixedIncome*

High Yield FixedIncome*

Floating RateCorporate Loans*

10INTEGRITY. BALANCE. OBJECTIVITY.

ASSET CLASS FUNDAMENTALS, continued

COMMODITIES• Most commodity prices finished 2015 near their 10-year

lows.• The prices of energy and industrial metals tumbled amid

concerns that China would not be able to absorb high and rising supply.

• China accounts for more than 30% of global consumption of many metals, cotton, rice, and soybean oil.

• McDonald’s reintroduced “The McRib” for a limited time, following a decline in pork prices.

MIDSTREAM ENERGY MLPs• According to Advisory Research, MLPs are currently priced

at a significant discount to their fair valuation.• Factors in the pullback in MLP prices included tax-loss

selling, oil and natural gas price weakness, concerns about MLPs’ growth prospects, and their access to capital markets.

• In the third quarter, 82 midstream companies announced third-quarter distributions that were, on average, 2.0% higher than the second quarter of 2015.

• At year-end, midstream MLPs yielded an average of 8.5%.

Commodity Prices: Near 10-Year Lows

A Z-score is a statistical measurement of a score’s relationship to the mean in a group of scores. Z-scores are calculated using daily prices over the past 10 years. Data are as of 12/31/15. Sources: FactSet and J.P. Morgan Asset Management.

Universe: all energy MLPs, excluding variable pay MLPs. Valuation inputs include yield, EV/Ebitda multiples, and the yield spread to the U.S. Corporate BB bond as of 12/31/2015. Sources: FactSet and Advisory Research.

MLPs: Significantly Undervalued

11INTEGRITY. BALANCE. OBJECTIVITY.

US Market Indices Performance US Market Sector Performance

Source: Investment Metrics, LLC

Source: Investment Metrics, LLCSource: Investment Metrics, LLC

S&P 500 Index Russell 2000 Index MSCI EAFE Index MSCI Emerging Markets Index

Barclays Capital Aggregate BC Municipal Bond Barclays U.S. Corp: High Yield S&P/LSTA Leveraged Loan Index

Alerian MLP Infrastructure DJ-UBS Commodity Index HFRI FoF Composite Index

0.0

15.0

-15.0

-30.0

-45.0

Re

turn

(%)

1

Quarter

1

Year

0.6

-0.4

-10.5

-24.7

-1.6

-31.7

-2.1-0.7

-2.1-4.5

1.53.3

-0.6

0.50.7

-14.6

4.7

-0.4

3.6

-4.4

7.0

1.4

S&P 500 S&P 500 Growth S&P 500 Value

Russell Midcap Index Russell Midcap Growth Index Russell Midcap Value Index

Russell 2000 Index Russell 2000 Growth Index Russell 2000 Value Index

0.0

6.0

12.0

-6.0

-12.0

Re

turn

(%)

1

Quarter

1

Year

2.9

-7.5

4.3

-1.4

3.6

-4.4

3.1

-4.8

4.1

-0.2

3.6

-2.4

6.1

-3.1

7.9

5.5

7.0

1.4

S&P 500 Consumer Discretionary S&P 500 Consumer Staples S&P 500 Energy

S&P 500 Financials S&P 500 Health Care S&P 500 Industrials

S&P 500 Information Technology S&P 500 Materials S&P 500 Telecom Services

S&P 500 Utilities

0.0

15.0

30.0

-15.0

-30.0

Re

turn

(%)

1

Quarter

1

Year

1.1

-4.8

7.63.4

9.7

-8.4

9.25.9

8.0

-2.5

9.26.96.0

-1.5

0.2

-21.1

7.6 6.65.8

10.1

Quarterly Market Summary December 31, 2015

Copyright © 2015 Investment Metrics, LLC. All rights reserved.

12INTEGRITY. BALANCE. OBJECTIVITY.

Intl Equity Region Performance Alternative Asset Class Performance

Fixed Income Market Sector Performance

Source: Investment Metrics, LLC

Source: Investment Metrics, LLCSource: Investment Metrics, LLC

Barclays U.S. Aggregate Barclays U.S. Treasury Barclays U.S. Credit Index Barclays U.S. Corp: High Yield

S&P/LSTA Leveraged Loan Barclays Global Aggregate JPM EMBI Global (USD)

0.0

3.0

-3.0

-6.0

Re

turn

(%)

1

Quarter

1

Year

1.51.2

-0.9

-3.2

-2.1

-0.7

-2.1

-4.5

-0.5-0.8-0.9

0.8

-0.6

0.5

HFRI Fund of Funds Composite Index S&P Developed Property

Bloomberg Commodity Index Total Return Alerian MLP Index

0.0

15.0

-15.0

-30.0

-45.0

Re

turn

(%)

1

Quarter

1

Year

-2.8

-32.6

-10.5

-24.7

4.70.90.6

-0.4

MSCI Japan MSCI Pacific ex Japan MSCI United Kingdom

MSCI Europe ex U.K. MSCI Emerging Markets

0.0

10.0

20.0

-10.0

-20.0

-30.0

Re

turn

(%)

1

Quarter

1

Year

0.7

-14.6

3.3

0.10.7

-7.5

8.3

-8.4

9.4 9.9

Quarterly Market Summary December 31, 2015

Copyright © 2015 Investment Metrics, LLC. All rights reserved.

13INTEGRITY. BALANCE. OBJECTIVITY.

Alternative Asset Class Returns December 31, 2015

Source: Christenson Investment Parnters Source: Christenson Investment Parnters

Source: Christenson Investment Parnters Source: Standard & Poors

‐31.1

‐24.8‐22.0

‐8.7

‐15.5

‐9.2‐5.8 ‐5.5

‐9.5 ‐9.0‐3.9

10.6

‐13.7

2.9

‐10.5

‐5.2 ‐5.0

1.54.5

18.4

‐40.0

‐30.0

‐20.0

‐10.0

0.0

10.0

20.0

30.0

Heatin

g Oil

Crud

e Oil

Natural Gas

Gasoline

Nickel

Copp

er

Zinc

Alum

inum Corn

Whe

at

Soybeans

Soybean Oil

Hogs

Cattle

Bloo

mbe

rg Com

m Inde

x

Silver

Gold

Coffe

e

Cotton

Sugar

Commodity Sector Returns

‐22.7

‐10.5‐8.2 ‐7.7

‐5.1‐3.5

11.2

‐25.0

‐20.0

‐15.0

‐10.0

‐5.0

0.0

5.0

10.0

15.0

Energy BloombergComm Index

IndustrialMetals

Grains PreciousMetals

Livestock Softs

Commodity Broad Sector Returns

‐4.3‐2.3 ‐1.8 ‐1.1 ‐0.6

0.0 0.0 0.5 0.6 0.7 1.6

‐10.0

‐5.0

0.0

5.0

10.0

15.0

20.0

Dedicated Short B

ias

Even

t Driv

en

Distressed

Managed

Futures

Convertib

le Arbitrage

Fixed Income Arbitrage

Equity M

arket N

eutral

Multi‐Strategy

Globa

l Macro

HFRI FoF

Com

posite

Long/Sho

rt Equ

ity

Hedge Fund Strategy Returns

‐6.1 ‐6.0‐4.7

‐1.8

2.34.4

5.57.0

9.5 9.8

‐8.0‐6.0‐4.0‐2.00.02.04.06.08.0

10.012.0

Emerging

Markets

Canada

United Kingdo

m

Europe

Singap

ore

Japa

n

S&P De

velope

d RE

IT

U.S.

Hon

g Ko

ng

Australia

Global REIT Country and Regional Returns

14INTEGRITY. BALANCE. OBJECTIVITY.

ASSET CLASS FUNDAMENTALS, continued

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

HighREITs 35.97 %

Commodities16.23 %

Fixed Income5.24 %

Int'l Stocks31.78 %

REITs 28.60 %

REITs 9.24 %

REITs 17.59 %

Smal l Cap Stocks38.82 %

REITs 31.78 %

REITs 4.23 %

REITs 7.31%

REITs 26.28%

High

Int'l Stocks26.34 %

Int'l Stocks11.17 %

Hedge Funds‐21.37 %

REITs 28.60 %

Smal l Cap Stocks26.85 %

Fixed Income7.84 %

Int'l Stocks17.32 %

Large Cap Stocks32.38 %

Large Cap Stocks13.69 %

Large Cap Stocks1.38 %

Large Cap Stocks7.31%

Smal l Cap Stocks19.70%

Smal l Cap Stocks18.37 %

Hedge Funds10.25 %

Divers i fed Portfol io‐24.23%

Smal l Cap Stocks27.17 %

Commodi es16.83 %

Large Cap Stocks2.11 %

Smal l Cap Stocks16.35 %

Int'l Stocks22.78%

Fixed Income5.97 %

Fixed Income0.55 %

Smal l Cap Stocks6.80%

Int'l Stocks18.41%

Large Cap Stocks15.79 %

Fixed Income6.97 %

Smal l Cap Stocks‐33.79 %

Large Cap Stocks26.46 %

Large Cap Stocks15.06 %

Divers i fied Portfol io‐0.50%

Large Cap Stocks16.00 %

Divers i fied Portfol io14.79%

Divers i fied Portfol io5.47%

Hedge Funds‐0.36%

Divers i fied Portfol io4.86%

Commodities18.09%

Divers i fied Portfol io13.25 %

Divers i fied Portfol io6.64 %

Commodities‐35.65 %

Divers i fied Portfol io19.48%

Divers i fied Portfol io12.25%

Smal l Cap Stocks‐4.18 %

Divers i fied Portfol io10.27%

Hedge Funds8.81 %

Smal l Cap Stocks4.89 %

Int'l Stocks‐0.81%

Fixed Income4.52%

Large Cap Stocks15.00%

Hedge Funds10.39 %

Large Cap Stocks5.49 %

Large Cap Stocks‐37.00 %

Commodi es18.91 %

Int'l Stocks7.75 %

Hedge Funds‐5.72 %

Hedge Funds5.28 %

REITs 1.86 %

Hedge Funds3.19%

Divers i fied Portfol io‐1.15%

Int'l Stocks3.03%

Divers i fied Portfol io9.59%

Fixed Income4.34 %

Smal l Cap Stocks‐1.57 %

REITs ‐39.20 %

Hedge Funds11.47 %

Fixed Income6.54 %

Int'l Stocks‐12.14 %

Fixed Income4.21 %

Fixed Income‐2.02 %

Int'l Stocks‐4.90%

Smal l Cap Stocks‐4.41%

Hedge Funds 2.26%

Hedge Funds5.45%

LowCommodi es

2.07 %REITs

‐17.55 %Int'l Stocks‐43.38 %

Fixed Income5.93 %

Hedge Funds5.70 %

Commodities‐13.32 %

Commodities‐1.06 %

Commodi es‐9.53 %

Commodi es‐17.01 %

Commodi es‐24.66%

Commodities ‐6.43%

Fixed Income3.21%

Low

Divers i fied Portfol io: 25% Large Cap Stocks , 10% Smal l Cap Stocks , 12% International Stocks , 25% Fixed Income, 3% REITs , 20% Hedge Funds , and 5% Commodities .

Periodic Table of Returns 2006 ‐ 2015

Avg Annual Returns '06‐'15

Avg Annual Risk

'06‐'15

Indices : Large Cap Stocks (S&P 500), Smal l Cap Stock (Russel l 2000), Int'l Stocks (MSCI EAFE), Fixed Income (Barclays Aggregate), REITs (DJ‐Wilshire REIT), Hedge Funds (HFRI Fund of Funds Compos ite), and Commodities (Bloomberg Commodity).

15INTEGRITY. BALANCE. OBJECTIVITY.

Client Type: Money Purchase Pension PlanTime Horizon: Greater than Five YearsExpected Return: 3.75% to 4.75% over CPIRisk Tolerances: Expected downside of -17.8% to -20.8% per year based on a statistical confidence level of 95% (1)

Asset Allocation Performance Benchmarks

Strategic Asset Investment Primary Peer GroupLower Limit Allocation Upper Limit Category Manager Index Universe

Domestic Equity Domestic Equity Large Cap Equity* 32.00% 35.00% 38.00% Large Cap Boston Tr Eqty S&P 500 Core Equity

Mid Cap Growth 3.50% 6.50% 9.50% Mid Cap Growth Victory Munder MC Core Gr Russell Mid Cap Index Mid Cap Growth Small Cap Value 3.50% 6.50% 9.50% Small Cap Value ICM Sm Cap Value Russell 2000 Index Small Cap Value

International Equity 16.00% 19.00% 22.00% International Equity Europacific R-4 MSCI EAFE International GrowthDodge & Cox Intl MSCI EAFE International Value

Domestic Fixed Income* 12.00% 15.00% 18.00% Domestic Fixed Income Boston Tr Fixed Inc BC Aggregate Core Bond1.00% 4.00% 7.00% MetWest Total Return BC Aggregate Core Bond

High Yield 0.00% 2.00% 5.00% High Yield JP Morgan HY BC:HY Credit High Yield

Floating Rate Corporate Loans 4.00% 7.00% 10.00% Floating Rate Corporate Loans Eaton Vance Floating CSFB Leveraged Loan Loan Participation

Commodities 2.00% 5.00% 8.00% Commodities Credit Suisse Commodity Bloomberg Commodity N/A100.00%

Total Portfolio Strategic Benchmark: 50.00% 70% S&P 500/30% BC Aggregate6.50% Russell Mid Cap Index 6.50% Russell 2000 Index

19.00% MSCI EAFE4.00% BC Aggregate2.00% BC:HY Credit 7.00% CSFB Leveraged Loan5.00% Bloomberg Commodity

100.00%

Total Portfolio Secondary Benchmark: CPI + 4.75%

*Balanced allocation to Boston Trust is 50% of the portfolio which is split 70% to large cap equity and 30% to domestic fixed income

INVESTMENT POLICY SUMMARY

Client Variables

(1) There is a 5% probability that the 1 year modeled loss of -17.8% to -20.8% will be exceeded. Risk tolerances are based on 2015 capital markets assumptions. NOTE: The 1 year modeled loss will vary from year to year depending on future capital market assumptions.

16INTEGRITY. BALANCE. OBJECTIVITY.

Boulder Fire & PoliceAverage plan assets $118,384,516Estimated Investment, Recordkeeping and Administrative Costs 0.57%Estimated Total Plan Expenses 0.67%

Weighted average (bps)

Employer Paid Employee Paid TotalAsset based fee retained by funds 48 -$ 572,146$ 572,146$ Revenue sharing paid to plan provider 14 -$ 168,970$ 168,970$ Per participant fee 0 -$ -$ -$ Administration/Recordkeeping fee 0 -$ -$ -$ Custodial/Trust fees 0 -$ -$ -$ Direct participant paid fees

Loan origination 0 -$ -$ -$ Loan maintenance 0 -$ -$ -$ QDRO 0 -$ -$ -$ Miscellaneous 0 -$ -$ -$

Rebate to plan -6 -$ (68,344)$ (68,344)$

Total Investment, Recordkeeping and Administrative Costs 57 -$ 672,773$ 672,773$

Third party plan paid feesInvestment Consultant 6 37,135$ 37,135$ 74,269$

Operating BudgetAudit 1 9,000$ -$ 9,000$ Trustee Education 1 10,500$ -$ 10,500$ Insurance 1 9,000$ -$ 9,000$ Miscellaneous Expenses 0 1,500$ -$ 1,500$ Legal 2 20,000$ -$ 20,000$

Total Plan Expenses 67 87,135$ 709,908$ 797,042$

Total Plan Expenses in Basis Points 7 60 67

Fee review reflects an estimate for the following time period ending: 12/31/2015

Benchmarking: The plan's estimated investment, recordkeeping and administrative costs of 0.57% as shown above, compare favorably to 401(k) Source data, a universe of 49 similarly sized 401(k) plans with an average investment, recordkeeping and administrative cost of 1.12%

Dollars ($)

Total Plan Expenses

Annual Fee Review

17INTEGRITY. BALANCE. OBJECTIVITY.

September 30, 2015

Allocation Differences

0.0% 4.0% 8.0%-4.0 %-8.0 %

Commodities

Floating Rate Corporate Loans

High Yield

Fixed Income

International Equity

Small Cap Equity

Mid Cap Equity

Large Cap Equity

-0.4 %

0.3%

0.0%

-3.1 %

-1.4 %

-0.2 %

-0.3 %

5.0%

December 31, 2015

Allocation Differences

0.0% 4.0% 8.0% 12.0%-4.0 %-8.0 %

Commodities

Floating Rate Corporate Loans

High Yield

Fixed Income

International Equity

Small Cap Equity

Mid Cap Equity

Large Cap Equity

-0.6 %

-0.4 %

-0.1 %

-3.9 %

0.2%

0.1%

0.0%

4.8%

September 30, 2015Market Value

($)Allocation

(%)Target

(%)Large Cap Equity 43,249,709 40.02 35.00Mid Cap Equity 6,718,803 6.22 6.50Small Cap Equity 6,785,733 6.28 6.50International Equity 19,020,970 17.60 19.00Fixed Income 17,148,253 15.87 19.00High Yield 2,190,391 2.03 2.00Floating Rate Corporate Loans 7,935,477 7.34 7.00Commodities 5,009,026 4.64 5.00Total Fund 108,058,361 100.00 100.00

December 31, 2015Market Value

($)Allocation

(%)Target

(%)Large Cap Equity 44,125,148 39.76 35.00Mid Cap Equity 7,224,152 6.51 6.50Small Cap Equity 7,296,884 6.57 6.50International Equity 21,280,351 19.17 19.00Fixed Income 16,716,967 15.06 19.00High Yield 2,116,118 1.91 2.00Floating Rate Corporate Loans 7,380,536 6.65 7.00Commodities 4,846,113 4.37 5.00Total Fund 110,986,269 100.00 100.00

Asset Allocation vs. Target Allocation

18INTEGRITY. BALANCE. OBJECTIVITY.

AllocationMarketValue

($)%

Performance(%)

LastQuarter

YearTo Date

1Year

3Years

5Years

10Years

SinceInnovestInception

SinceInception

InceptionDate

Large Cap EquityBoston Trust Equity - Boulder F&P 44,125,148 37.27 5.11 -0.95 -0.95 13.44 10.68 7.56 6.65 10.37 07/01/1990S&P 500 Index 7.04 1.38 1.38 15.13 12.57 7.31 5.00 9.35IM U.S. Large Cap Equity (MF) Median 6.29 0.00 0.00 13.84 11.14 6.49 4.51 8.98

Mid Cap EquityVictory Munder Mid Cap Core Growth 7,224,152 6.10 1.43 -4.36 -4.36 12.11 10.15 7.53 8.15 12.57 01/01/2010Russell Midcap Growth Index 4.12 -0.20 -0.20 14.88 11.54 8.16 5.85 13.89IM U.S. Mid Cap Growth Equity (MF) Median 2.87 -0.49 -0.49 13.14 9.78 7.35 5.44 12.24

Small Cap EquityICM Small Company 7,296,884 6.16 3.44 -3.20 -3.20 10.68 8.57 7.13 9.34 6.18 01/01/2008Russell 2000 Value Index 2.88 -7.47 -7.47 9.06 7.67 5.57 8.17 5.58IM U.S. Small Cap Value Equity (MF) Median 2.52 -7.07 -7.07 9.05 7.81 5.51 8.91 5.51

International EquityDodge & Cox Int'l 10,544,522 8.91 0.83 -11.35 -11.35 3.87 2.65 3.83 N/A 0.23 01/01/2008MSCI EAFE Value Index (Net) 2.68 -5.68 -5.68 3.14 2.55 1.96 3.64 -1.60IM International Large Cap Value Equity (MF) Median 2.61 -2.64 -2.64 2.97 2.07 2.48 2.82 -1.95

American Funds EuroPacific Gr 10,735,829 9.07 2.87 -0.82 -0.82 5.08 3.62 4.58 N/A 6.62 04/01/2004MSCI EAFE Growth Index (Net) 6.67 4.09 4.09 6.83 4.60 4.03 3.32 5.51IM International Large Cap Growth Equity (MF) Median 4.40 -0.57 -0.57 4.15 3.31 4.21 4.27 6.24

Fixed IncomeBoston Trust Fixed Income - Boulder F&P 12,424,090 10.49 -0.54 1.68 1.68 1.05 2.97 4.36 5.08 5.96 07/01/1990Barclays Aggregate Index -0.57 0.55 0.55 1.44 3.25 4.52 4.97 6.27IM U.S. Broad Market Core Fixed Income (MF) Median -0.64 0.01 0.01 1.10 3.14 4.26 4.69 6.17

Met West Total Return 4,292,877 3.63 -0.40 0.29 0.29 2.22 4.69 6.38 6.31 0.29 01/01/2015Barclays Aggregate Index -0.57 0.55 0.55 1.44 3.25 4.52 4.97 0.55IM U.S. Broad Market Core Fixed Income (MF) Median -0.64 0.01 0.01 1.10 3.14 4.26 4.69 0.01

High YieldJPMorgan High Yield Select 2,116,118 1.79 -2.03 -4.54 -4.54 1.58 4.31 6.50 7.18 5.97 01/01/2010Barclays US Corp: High Yield -2.07 -4.47 -4.47 1.69 5.04 6.96 7.59 6.65IM U.S. High Yield Bonds (MF) Median -1.80 -3.96 -3.96 1.36 4.19 5.62 6.38 5.78

Floating Rate Corporate LoansEaton Vance Floating Rate; I 7,380,536 6.23 -2.26 -1.63 -1.63 1.24 2.85 3.42 N/A 8.08 04/01/2009Credit Suisse Leveraged Loan Index -1.97 -0.39 -0.39 2.58 3.75 4.08 4.44 8.98Loan Participation Mutual Funds Median -2.19 -1.53 -1.53 0.99 2.57 2.99 3.48 7.20

Table of ReturnsDecember 31, 2015

Returns prior to 7/1990 provided by PMC

19INTEGRITY. BALANCE. OBJECTIVITY.

Table of ReturnsDecember 31, 2015

AllocationMarketValue

($)%

Performance(%)

LastQuarter

YearTo Date

1Year

3Years

5Years

10Years

SinceInnovestInception

SinceInception

InceptionDate

CommoditiesCrdt Suis Comm Rtn Strat 4,846,113 4.09 -10.34 -24.96 -24.96 -17.49 -13.52 -6.46 N/A -24.96 01/01/2015Bloomberg Commodity Index Total Return -10.52 -24.66 -24.66 -17.29 -13.47 -6.43 -1.03 -24.66IM Commodities General (MF) Median -9.97 -24.78 -24.78 -17.69 -12.99 -6.46 N/A -24.78

Balanced AccountBoston Trust Balanced - Boulder F&P 56,549,237 47.77 3.74 -0.59 -0.59 10.76 9.12 7.18 6.72 9.92 07/01/199070% S&P/30% BC Aggr 4.77 1.34 1.34 10.99 9.87 6.73 5.27 8.67IM U.S. Balanced (SA+CF) Median 3.13 -1.18 -1.18 8.03 7.95 6.29 6.11 8.76

VT Retirement Income Advantage 210,331 0.18 2.85 -1.10 -1.10 5.88 5.44 N/A N/A 4.56 04/01/2013VT Retirement Income Advantage Custom Index 3.50 0.88 0.88 7.57 6.96 N/A N/A 6.21IM U.S. Balanced (SA+CF) Median 3.13 -1.18 -1.18 8.03 7.95 6.29 6.11 6.06

Stable ValueVantage Trust Plus (gross) 7,187,915 6.07 0.57 2.34 2.34 2.44 2.77 3.72 4.16 3.48 07/01/2007Vantage Trust Plus (net) 0.43 1.77 1.77 1.87 2.20 3.18 N/A 2.93Ryan 3 Yr GIC Master Index 0.31 1.16 1.16 1.09 1.43 2.82 3.45 2.61IM U.S. GIC/Stable Value (SA+CF) Median 0.46 1.81 1.81 1.68 2.15 3.07 3.96 2.81

Total FundBoulder Fire and Police 118,384,516 100.00 1.93 -3.25 -3.25 6.81 6.34 5.99 6.21 9.05 01/01/1985Boulder Fire & Police Custom Benchmark 3.02 -1.26 -1.26 7.52 6.98 5.58 5.39 9.55CPI +4.75% 0.56 5.51 5.51 5.79 6.36 6.69 6.92 7.52

Returns prior to 7/1990 provided by PMC

20INTEGRITY. BALANCE. OBJECTIVITY.

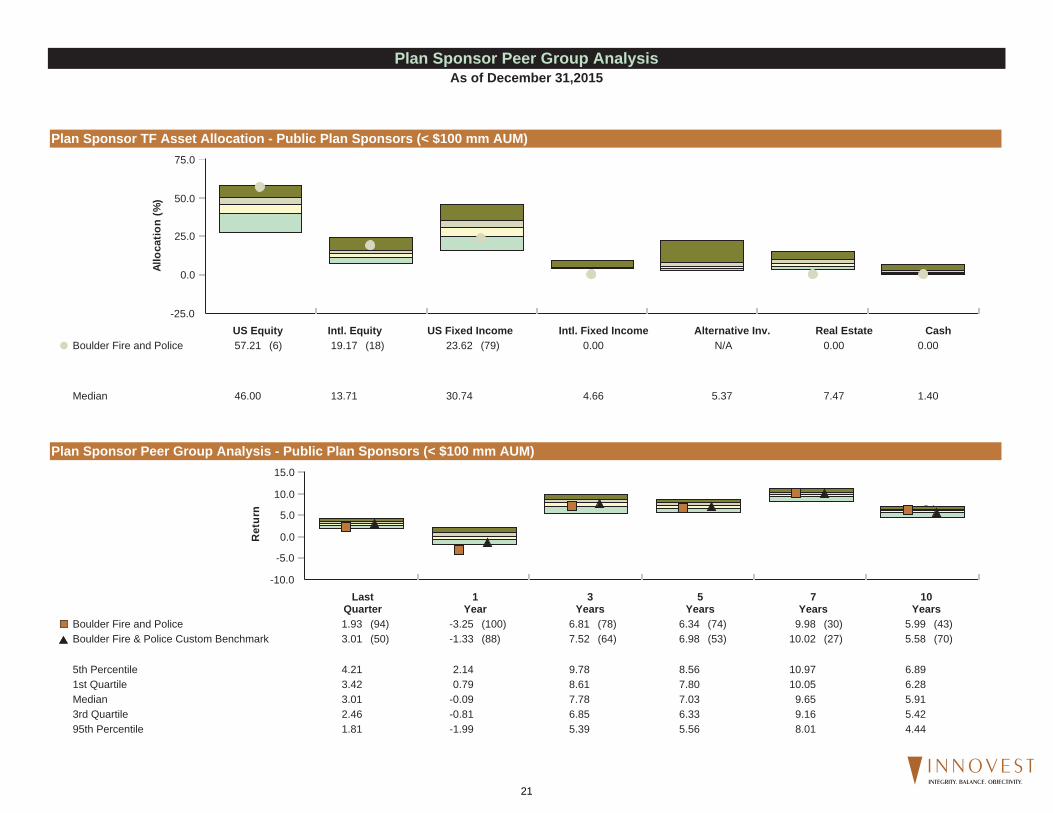

Plan Sponsor TF Asset Allocation - Public Plan Sponsors (< $100 mm AUM)

Plan Sponsor Peer Group Analysis - Public Plan Sponsors (< $100 mm AUM)

-25.0

0.0

25.0

50.0

75.0Al

loca

tion

(%)

US Equity Intl. Equity US Fixed Income Intl. Fixed Income Alternative Inv. Real Estate CashBoulder Fire and Police 57.21 (6) 19.17 (18) 23.62 (79) 0.00 N/A 0.00 0.00

5th Percentile 57.94 24.10 46.21 8.93 22.26 14.70 6.591st Quartile 50.66 15.81 35.83 4.94 7.85 10.08 2.57

Median 46.00 13.71 30.74 4.66 5.37 7.47 1.403rd Quartile 40.15 11.20 24.60 4.29 3.97 5.07 0.6995th Percentile 27.29 7.57 15.63 3.83 2.71 3.26 0.05

-10.0

-5.0

0.0

5.0

10.0

15.0

Ret

urn

1.82.5

-2.0-0.8

5.46.9

5.66.38.09.2

4.45.4

LastQuarter

1Year

3Years

5Years

7Years

10Years

Boulder Fire and Police 1.93 (94) -3.25 (100) 6.81 (78) 6.34 (74) 9.98 (30) 5.99 (43)

Boulder Fire & Police Custom Benchmark 3.01 (50) -1.33 (88) 7.52 (64) 6.98 (53) 10.02 (27) 5.58 (70)

5th Percentile 4.21 2.14 9.78 8.56 10.97 6.891st Quartile 3.42 0.79 8.61 7.80 10.05 6.28Median 3.01 -0.09 7.78 7.03 9.65 5.913rd Quartile 2.46 -0.81 6.85 6.33 9.16 5.4295th Percentile 1.81 -1.99 5.39 5.56 8.01 4.44

Plan Sponsor Peer Group AnalysisAs of December 31,2015

21INTEGRITY. BALANCE. OBJECTIVITY.

Plan Sponsor TF Asset Allocation - Public Plan Sponors ($100mm - $1 Bln AUM)

Plan Sponsor Peer Group Analysis - All Public Plans ($100mm - $500mm AUM)

-25.0

0.0

25.0

50.0

75.0Al

loca

tion

(%)

US Equity Intl. Equity US Fixed Income Intl. Fixed Income Alternative Inv. Real Estate CashBoulder Fire and Police 57.21 (4) 19.17 (43) 23.62 (49) 0.00 N/A 0.00 0.00

5th Percentile 54.24 29.52 39.55 15.68 29.24 14.32 5.811st Quartile 46.85 22.41 31.43 6.20 17.23 11.23 1.85

Median 38.06 17.97 23.24 5.27 11.93 8.72 0.993rd Quartile 30.55 13.92 17.17 4.41 4.12 5.52 0.5495th Percentile 21.73 8.01 11.44 1.93 1.47 2.53 0.02

-10.0

-4.0

2.0

8.0

14.0

20.0

Ret

urn

1.42.6

-2.4-1.0

3.46.3

4.46.4 7.9

9.5

4.25.6

LastQuarter

1Year

3Years

5Years

7Years

10Years

Boulder Fire and Police 1.93 (89) -3.25 (100) 6.81 (72) 6.34 (76) 9.98 (60) 5.99 (45)

Boulder Fire & Police Custom Benchmark 3.01 (45) -1.33 (77) 7.52 (61) 6.98 (71) 10.02 (60) 5.58 (79)

5th Percentile 4.00 2.54 10.20 9.21 11.83 7.031st Quartile 3.46 0.99 8.87 8.15 10.92 6.25Median 2.96 0.07 8.10 7.32 10.20 5.873rd Quartile 2.58 -0.96 6.31 6.38 9.50 5.6395th Percentile 1.39 -2.39 3.42 4.37 7.88 4.21

Plan Sponsor Peer Group AnalysisAs of December 31,2015

22INTEGRITY. BALANCE. OBJECTIVITY.

Cumulative Performance Over Time

Risk and Return

Boulder Fire and Police Boulder Fire & Police Custom Benchmark CPI + 4.75%

-500 %

0%

500%

1,000%

1,500%

2,000%

2,500%

3/85 9/86 3/88 9/89 3/91 9/92 3/94 9/95 3/97 9/98 3/00 9/01 3/03 9/04 3/06 9/07 3/09 9/10 3/12 9/13 12/15

8

9

10

11

12

Ret

urn

(%)

8 9 10 11 12 13 14 15 16 17 18 19Risk (Standard Deviation %)

Boulder Fire and Police

S&P 500 Index

Total Portfolio Performance AnalysisAs of December 31,2015

23INTEGRITY. BALANCE. OBJECTIVITY.

THIS PAGE LEFT INTENTIONALLY BLANK

24INTEGRITY. BALANCE. OBJECTIVITY.

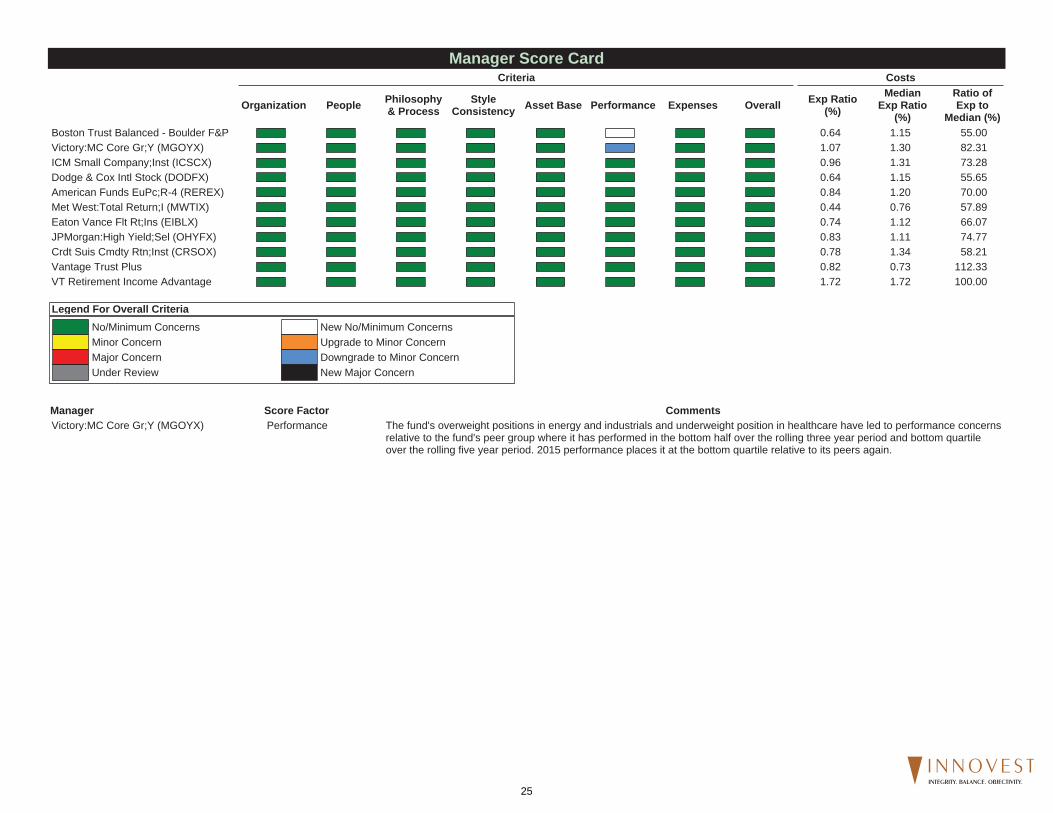

Criteria

Organization People Philosophy& Process

StyleConsistency Asset Base Performance Expenses Overall

Costs

Exp Ratio(%)

MedianExp Ratio

(%)

Ratio ofExp to

Median (%)Boston Trust Balanced - Boulder F&P 0.64 1.15 55.00Victory:MC Core Gr;Y (MGOYX) 1.07 1.30 82.31ICM Small Company;Inst (ICSCX) 0.96 1.31 73.28Dodge & Cox Intl Stock (DODFX) 0.64 1.15 55.65American Funds EuPc;R-4 (REREX) 0.84 1.20 70.00Met West:Total Return;I (MWTIX) 0.44 0.76 57.89Eaton Vance Flt Rt;Ins (EIBLX) 0.74 1.12 66.07JPMorgan:High Yield;Sel (OHYFX) 0.83 1.11 74.77Crdt Suis Cmdty Rtn;Inst (CRSOX) 0.78 1.34 58.21Vantage Trust Plus 0.82 0.73 112.33VT Retirement Income Advantage 1.72 1.72 100.00

Legend For Overall CriteriaNo/Minimum ConcernsMinor ConcernMajor ConcernUnder Review

New No/Minimum ConcernsUpgrade to Minor ConcernDowngrade to Minor ConcernNew Major Concern

Manager Score Factor CommentsVictory:MC Core Gr;Y (MGOYX) Performance The fund's overweight positions in energy and industrials and underweight position in healthcare have led to performance concerns

relative to the fund's peer group where it has performed in the bottom half over the rolling three year period and bottom quartileover the rolling five year period. 2015 performance places it at the bottom quartile relative to its peers again.

Manager Score Card

25INTEGRITY. BALANCE. OBJECTIVITY.

THIS PAGE LEFT INTENTIONALLY BLANK

26INTEGRITY. BALANCE. OBJECTIVITY.

STRATEGY INFORMATION

ROLLING 3 YEAR RETURN AND PERCENTILE RANKINGS

PEER GROUP ANALYSIS - IM U.S. Balanced (SA+CF)

CALENDAR YEAR RETURNS AND PERCENTILE RANKINGS

RISK VS. RETURN (5 YEARS*)

*If less than 5 years, data is since account inception.

Firm and Management:Domenic Colasacco is a portfoliomanager and president of the Adviser.Mr. Colasacco is also the president ofBoston Trust & InvestmentManagement Company and has servedas its Chief Investment Officer since1980. Mr. Colasacco managesportfolios for individual and institutionalclients and also manages the BostonTrust Equity Fund. Mr. Colasacco is aholder of the Chartered FinancialAnalyst (CFA) designation and amember of the Boston SecurityAnalysts Society.

Investment Strategy:The strategy strives to provide long-term growth of capital through adiversified portfolio of stocks, bondsand money market investments. Theallocation among these assets isactively managed based both on theirrelative values and the changingeconomic outlook. By forecastingfinancial market returns across a widerange of possible economic scenarios,they vary the allocation in a mannerthat is designed to provide protectionagainst falling markets in unfavorableeconomic environments, while alsoproviding opportunity to participate inrising markets. The strategy providesbroad diversification across stockmarket sectors; individual equityselections focus on companies withsuperior financial track records.

-20.0

-12.0

-4.0

4.0

12.0

20.0

Ret

urn

LastQuarter

YearTo Date

1Year

3Years

5Years

7Years

10Years

Boston Tr Bal - Boulder F&P 3.74 (29) -0.59 (44) -0.59 (44) 10.76 (15) 9.12 (18) 10.99 (40) 7.18 (26)

70% S&P/30% BC Aggr 4.77 (13) 1.34 (18) 1.34 (18) 10.99 (13) 9.87 (7) 11.75 (21) 6.73 (35)

Median 3.13 -1.18 -1.18 8.03 7.95 10.32 6.29

-8.0

-4.0

0.0

4.0

8.0

12.0

16.0

Ret

urn

(%)

0.0 4.0 8.0 12.0 16.0Risk (Standard Deviation %)

Return StandardDeviation

Boston Tr Bal - Boulder F&P 9.12 8.79

70% S&P/30% BC Aggr 9.87 8.41

Median 7.95 9.03

2014 2013 2012 2011 2010 2009 2008Boston Tr Bal - Boulder F&P 11.13 (12) 23.02 (24) 10.04 (72) 3.45 (24) 14.13 (27) 17.53 (77) -20.93 (38)IM U.S. Balanced (SA+CF) Median 7.08 18.94 11.13 1.51 12.41 20.67 -22.51

70% S&P/30% BC Aggr 11.39 (10) 21.12 (30) 12.49 (35) 4.08 (21) 12.92 (40) 20.44 (52) -26.03 (75)IM U.S. Balanced (SA+CF) Median 7.08 18.94 11.13 1.51 12.41 20.67 -22.51

3Years

EndingDec-2015

3Years

EndingDec-2014

3Years

EndingDec-2013

3Years

EndingDec-2012

3Years

EndingDec-2011

3Years

EndingDec-2010

3Years

EndingDec-2009

Boston Tr Bal - Boulder F&P 10.76 (15) 14.58 (25) 11.88 (19) 9.12 (22) 11.54 (47) 1.98 (39) 1.13 (28)IM U.S. Balanced (SA+CF) Median 8.03 12.98 10.63 8.51 11.39 1.44 0.11

70% S&P/30% BC Aggr 10.99 (13) 14.92 (23) 12.35 (14) 9.75 (13) 12.28 (39) 0.20 (69) -1.87 (81)IM U.S. Balanced (SA+CF) Median 8.03 12.98 10.63 8.51 11.39 1.44 0.11

Boston Tr Bal - Boulder F&P 12/31/15

27INTEGRITY. BALANCE. OBJECTIVITY.

STRATEGY INFORMATION

ROLLING 3 YEAR RETURN AND PERCENTILE RANKINGS

PEER GROUP ANALYSIS - IM U.S. Large Cap Core Equity (SA+CF)

CALENDAR YEAR RETURNS AND PERCENTILE RANKINGS

RISK VS. RETURN (5 YEARS*)

*If less than 5 years, data is since account inception.

Firm and Management:Domenic Colasacco is a portfoliomanager and president of the Adviser.Mr. Colasacco is also the president ofBoston Trust & InvestmentManagement Company and has servedas its Chief Investment Officer since1980. Mr. Colasacco managesportfolios for individual and institutionalclients and also manages the BostonTrust Equity Fund. Mr. Colasacco is aholder of the Chartered FinancialAnalyst (CFA) designation and amember of the Boston SecurityAnalysts Society.

Investment Strategy:The portfolio consists of stocks from allmarket capitalizations; small, mediumand large. The portfolio is constructedwith a bottom up approach to securityselection, however, macro themes areconsidered in deciding which sectorslook most attractive. Each potentialholding is put through a number ofscreens which consider earningsgrowth and relative valuation.

-12.0

-4.0

4.0

12.0

20.0

28.0

Ret

urn

LastQuarter

YearTo Date

1Year

3Years

5Years

7Years

10Years

Boston TrEq - Boulder F&P 5.11 (73) -0.95 (76) -0.95 (76) 13.44 (78) 10.68 (81) 13.40 (83) 7.56 (59)

S&P 500 Index 7.04 (25) 1.38 (51) 1.38 (51) 15.13 (53) 12.57 (53) 14.81 (57) 7.31 (70)

Median 5.94 1.39 1.39 15.26 12.63 14.94 7.75

3.0

6.0

9.0

12.0

15.0

18.0

Ret

urn

(%)

0.0 5.0 10.0 15.0 20.0Risk (Standard Deviation %)

Return StandardDeviation

Boston TrEq - Boulder F&P 10.68 11.98

S&P 500 Index 12.57 12.46

Median 12.63 13.04

2014 2013 2012 2011 2010 2009 2008Boston TrEq - Boulder F&P 13.00 (57) 30.44 (78) 12.03 (85) 1.56 (56) 16.91 (24) 24.19 (65) -30.73 (17)IM U.S. Large Cap Core Equity (SA+CF) Median 13.41 33.21 15.66 1.98 14.80 26.53 -35.97

S&P 500 Index 13.69 (45) 32.39 (60) 16.00 (46) 2.11 (50) 15.06 (44) 26.46 (51) -37.00 (62)IM U.S. Large Cap Core Equity (SA+CF) Median 13.41 33.21 15.66 1.98 14.80 26.53 -35.97

3Years

EndingDec-2015

3Years

EndingDec-2014

3Years

EndingDec-2013

3Years

EndingDec-2012

3Years

EndingDec-2011

3Years

EndingDec-2010

3Years

EndingDec-2009

Boston TrEq - Boulder F&P 13.44 (78) 18.20 (80) 14.06 (82) 9.97 (65) 13.82 (56) 0.19 (18) -1.29 (17)IM U.S. Large Cap Core Equity (SA+CF) Median 15.26 20.69 16.37 10.67 14.08 -1.83 -4.31

S&P 500 Index 15.13 (53) 20.41 (57) 16.18 (56) 10.87 (48) 14.11 (49) -2.85 (69) -5.63 (74)IM U.S. Large Cap Core Equity (SA+CF) Median 15.26 20.69 16.37 10.67 14.08 -1.83 -4.31

Boston TrEq - Boulder F&P 12/31/15

28INTEGRITY. BALANCE. OBJECTIVITY.

TOP TEN HOLDINGS PORTFOLIO CHARACTERISTICS

DISTRIBUTION OF MARKET CAP SECTOR DISTRIBUTION

PortfolioWeight

(%)

BenchmarkWeight

(%)

ActiveWeight

(%)

QuarterlyReturn

(%)Microsoft Corp 3.01 2.48 0.53 26.20Apple Inc 2.95 3.28 -0.33 -4.16Nike Inc 2.76 0.47 2.29 1.90Johnson & Johnson 2.48 1.59 0.89 10.843M Co 2.32 0.52 1.80 6.95Express Scripts Holding Co 2.21 0.33 1.88 7.97Exxon Mobil Corp 2.10 1.81 0.29 5.78Alphabet Inc 2.10 1.26 0.84 24.73Comcast Corp 2.08 0.77 1.31 -0.38Accenture PLC 2.06 0.36 1.70 7.49

% of Portfolio 24.07 12.87

Portfolio BenchmarkWtd. Avg. Mkt. Cap ($) 121,396,213,136 137,341,633,345Median Mkt. Cap ($) 59,113,285,160 17,668,607,200Price/Earnings ratio 19.71 19.30Price/Book ratio 3.22 3.105 Yr. EPS Growth Rate (%) 7.89 7.89Current Yield (%) 1.97 2.17Beta (5 Years, Monthly) 0.95 1.00Number of Stocks 69 504

Boston Trust Equity - Composite S&P 500 Index

0.0

15.0

30.0

45.0

60.0

>100 Bil 75 Bil - 100 Bil 25 Bil - 75 Bil 15 Bil - 25 Bil 2 Bil - 15 Bil 0 - 2 Bil

44.4

7.2

27.8

9.8 10.8

0.0

32.6

8.8

31.1

11.2

16.3

0.0

Boston Trust Equity - Composite

S&P 500 Index

0.0 5.0 10.0 15.0 20.0 25.0

Utilities

Telecommunication Services

Materials

Information Technology

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

2.0

0.0

3.4

19.5

12.3

17.1

16.9

5.3

11.6

12.1

3.0

2.4

2.8

20.7

10.0

15.2

16.5

6.5

10.1

12.9

Boston Trust Equity - Composite 12/31/15

29INTEGRITY. BALANCE. OBJECTIVITY.

PERFORMANCE - 1 Quarter TOTAL ATTRIBUTION - 1 Quarter

ACTIVE RETURN - 1 Quarter

Boston Trust Equity - Composite

S&P 500 Index

0.0 5.0 10.0 15.0 20.0-5.0-10.0

Utilities

Telecommunication Services

Materials

Information Technology

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

-4.1

7.1

11.6

7.8

2.8

9.4

5.6

5.6

4.5

-1.2

1.1

7.6

9.9

9.0

8.1

9.2

6.0

0.2

7.6

5.8

0.0 0.4 0.8-0.4-0.8-1.2-1.6

Utilities

Telecommunication Services

Materials

Information Technology

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

-0.1

0.0

0.0

-0.2

-0.7

0.0

0.0

0.4

-0.4

-1.0

Buy-and-Hold Portfolio 5.01Portfolio Trading 0.37Actual Return 5.39Benchmark Return 7.04Actual Active Return -1.66

Stock Selection -1.77Sector Selection 0.14Interaction -0.36Total Selection -1.99

Portfolio Trading 0.37Benchmark Trading 0.04Active Trading Impact 0.33

Buy & Hold Active Return -1.66

Boston Trust Equity - Composite 12/31/15

30INTEGRITY. BALANCE. OBJECTIVITY.

PERFORMANCE - 3 Years TOTAL ATTRIBUTION - 3 Years

ACTIVE RETURN - 3 Years

Boston Trust Equity - Composite

S&P 500 Index

0.0 8.0 16.0 24.0 32.0-8.0-16.0

Utilities

Telecommunication Services

Materials

Information Technology

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

2.7

7.1

18.2

15.1

7.5

18.0

15.0

-1.1

9.8

19.8

11.5

5.7

7.3

17.9

14.7

23.5

15.5

-3.1

16.0

20.0

0.0 0.4 0.8 1.2-0.4-0.8-1.2-1.6

Utilities

Telecommunication Services

Materials

Information Technology

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

0.1

0.2

0.5

-0.6

-1.1

-0.6

-0.1

0.2

-0.8

0.0

Buy-and-Hold Portfolio 12.95Portfolio Trading 0.42Actual Return 13.37Benchmark Return 15.13Actual Active Return -1.76

Stock Selection -2.09Sector Selection 0.23Interaction -0.31Total Selection -2.16

Portfolio Trading 0.42Benchmark Trading 0.01Active Trading Impact 0.41

Buy & Hold Active Return -1.76

Boston Trust Equity - Composite 12/31/15

31INTEGRITY. BALANCE. OBJECTIVITY.

STRATEGY INFORMATION

ROLLING 3 YEAR RETURN AND PERCENTILE RANKINGS

PEER GROUP ANALYSIS - IM U.S. Fixed Income (SA+CF)

CALENDAR YEAR RETURNS AND PERCENTILE RANKINGS

RISK VS. RETURN (5 YEARS*)

*If less than 5 years, data is since account inception.

Firm and Management:Domenic Colasacco is a portfoliomanager and president of the Adviser.Mr. Colasacco is also the president ofBoston Trust & InvestmentManagement Company and has servedas its Chief Investment Officer since1980. Mr. Colasacco managesportfolios for individual and institutionalclients and also manages the BostonTrust Equity Fund. Mr. Colasacco is aholder of the Chartered FinancialAnalyst (CFA) designation and amember of the Boston SecurityAnalysts Society.

Investment Strategy:Boston Trust's approach to fixedincome investing combines top downeconomic scenario forecasts withbottom up fundamental research. Usingmacroeconomic-based quantitativetools, the investment team forecastsinterest rate changes for a range ofpossible economic outcomes. Theseforecasts contribute to portfoliostrategies with respect to interest ratesand the yield curve. In selectingindividual securities, Boston Trustapplies long-held standards for superiorfinancial quality, appropriate risk, anddiversification.

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

Ret

urn

LastQuarter

YearTo Date

1Year

3Years

5Years

7Years

10Years

Boston Tr FI - Boulder F&P -0.54 (61) 1.68 (14) 1.68 (14) 1.05 (82) 2.97 (72) 3.75 (76) 4.36 (68)

Barclays Agg -0.57 (63) 0.55 (55) 0.55 (55) 1.44 (66) 3.25 (66) 4.09 (72) 4.52 (64)

Median -0.43 0.69 0.69 1.77 3.86 5.29 4.88

-3.0

0.0

3.0

6.0

9.0

Ret

urn

(%)

-4.0 0.0 4.0 8.0 12.0 16.0Risk (Standard Deviation %)

Return StandardDeviation

Boston Tr FI - Boulder F&P 2.97 2.58

Barclays Agg 3.25 2.79

Median 3.86 2.80

2014 2013 2012 2011 2010 2009 2008Boston Tr FI - Boulder F&P 3.71 (58) -2.15 (84) 4.08 (75) 7.76 (33) 6.55 (65) 4.93 (83) 5.33 (23)IM U.S. Fixed Income (SA+CF) Median 4.42 -0.25 6.83 6.41 7.59 10.53 1.31

Barclays Agg 5.97 (36) -2.02 (81) 4.21 (74) 7.84 (32) 6.54 (65) 5.93 (78) 5.24 (24)IM U.S. Fixed Income (SA+CF) Median 4.42 -0.25 6.83 6.41 7.59 10.53 1.31

3Years

EndingDec-2015

3Years

EndingDec-2014

3Years

EndingDec-2013

3Years

EndingDec-2012

3Years

EndingDec-2011

3Years

EndingDec-2010

3Years

EndingDec-2009

Boston Tr FI - Boulder F&P 1.05 (82) 1.84 (83) 3.15 (74) 6.12 (67) 6.41 (73) 5.60 (64) 6.22 (42)IM U.S. Fixed Income (SA+CF) Median 1.77 3.88 4.30 7.19 8.76 6.33 5.84

Barclays Agg 1.44 (66) 2.66 (70) 3.26 (72) 6.19 (66) 6.77 (69) 5.90 (59) 6.04 (46)IM U.S. Fixed Income (SA+CF) Median 1.77 3.88 4.30 7.19 8.76 6.33 5.84

Boston Tr FI - Boulder F&P 12/31/15

32INTEGRITY. BALANCE. OBJECTIVITY.

TOP TEN HOLDINGS

PORTFOLIO CHARACTERISTICS vs. Barclays Aggregate Index

CREDIT QUALITY DISTRIBUTION vs. Barclays Aggregate Index

SECTOR DISTRIBUTION vs. Barclays Aggregate Index

MATURITY DISTRIBUTION vs. Barclays Aggregate Index

Portfolio BenchmarkEffective Duration 5.40 5.68Avg. Maturity 6.55 7.94Avg. Quality AA Aa2Yield To Maturity (%) 2.18 2.51Holdings Count 25 9,720

Boston Trust Fixed Income - Boulder F&P Barclays Aggregate Index

0.0

15.0

30.0

45.0

60.0

75.0

US Tr e

asurie

s

A gencie

sM BS

A BS

CM BSC re

di t

Other

0.0 0.0 0.0 0.0 0.0 0.0 0.0

7.4

57.2

3.10.0 0.0

28.2

4.1

Boston Trust Fixed Income - Boulder F&PCompany %

FED HOME LN 2.875% 6/14/24 2.27FED HOME LN MTG 2.375% 1/13/22 2.26FED NAT MTG ASSN 2.625% 9/6/24 1.80TREASURY INFL IDX .625% 01/15/ 1.43FED FARM CR BKS 3.500% 12/20/2 0.95FED HOME LOAN BANK 2.250% 3/11 0.90FHLB 2.750% 12/13/24 0.89PRINCETON UNIVERSITY 4.950% 03 0.79HUBBELL INC 5.950% 6 0.77FED NATL MTG ASSN 1.875% 02/19 0.72

Boston Trust Fixed Income - Boulder F&P Barclays Aggregate Index

0.0

20.0

40.0

60.0

80.0

100.0

A AA AA AB BB BB NR

72.4

3.7

10.713.2

0.0 0.0

68.6

0.0

24.0

4.20.0

3.2

Boston Trust Fixed Income - Boulder F&P Barclays Aggregate Index

0.0

20.0

40.0

60.0

80.0

100.0

0 to

3 Y ea

rs

3 to

5 Y ea

rs

6 to

10 Y ea

rs

11 to

20 Y ea

rs

20+ Y ea

rs

22.226.6

36.7

3.3

11.215.5 16.5

64.9

0.13.0

Boston Trust Fixed Income - Boulder F&P 12/31/15

33INTEGRITY. BALANCE. OBJECTIVITY.

FUND INFORMATION

ROLLING 3 YEAR RETURN AND PERCENTILE RANKINGS

PEER GROUP ANALYSIS - IM U.S. Mid Cap Growth Equity (MF)

CALENDAR YEAR RETURNS AND PERCENTILE RANKINGS

RISK VS. RETURN (5 YEARS*)

*If less than 5 years, data is since inception of fund share class.

Firm and Management:Tony Dong has been the lead managerhere since February 2001. He's workedat Munder since 1988 and managedlarge-cap, growth-at-a-reasonable pricestrategies before taking over this fund.He's backed here by four comanagers:Andy Mui, Brian Matuszak, GeorgeSanders, and Geoffrey Wilson.

Investment Strategy:The Munder team seek companies thattrade cheaply relative to their growthprospects, using a broad range ofvaluation measures. They keep theFund's sector weightings within 3percentage points of those of the fund'sbenchmark, the S&P Midcap 400 Index.They'll typically hold 70-100 stocks andcap position sizes at 3%. And they'rerelatively patient investors; portfolioturnover has averaged around 50%.

Innovest's Assessment:Munder’s low beta bias is likely tooutperform during market drawdownsand when quality growth companies arein favor. Underperformance is expectedwhen low quality, high beta companiesoutpace high quality securities andduring speculative growth rallies.

-20.0

-12.0

-4.0

4.0

12.0

20.0

28.0

Ret

urn

LastQuarter

YearTo Date

1Year

3Years

5Years

7Years

10Years

Victory Munder MC Core Gr 1.43 (83) -4.36 (80) -4.36 (80) 12.11 (63) 10.15 (45) 15.26 (56) 7.53 (44)

Russell Midcap Growth Index 4.12 (33) -0.20 (49) -0.20 (49) 14.88 (25) 11.54 (21) 18.04 (9) 8.16 (29)

Median 2.87 -0.49 -0.49 13.14 9.78 15.40 7.35

-5.0

0.0

5.0

10.0

15.0

Ret

urn

(%)

9.0 12.0 15.0 18.0 21.0Risk (Standard Deviation %)

Return StandardDeviation

Victory Munder MC Core Gr 10.15 13.49

Russell Midcap Growth Index 11.54 13.61

Median 9.78 14.11

2014 2013 2012 2011 2010 2009 2008Victory Munder MC Core Gr 10.17 (23) 33.71 (64) 16.01 (28) -0.77 (23) 25.48 (49) 32.80 (70) -43.45 (41)Russell Midcap Growth Index 11.90 (13) 35.74 (48) 15.81 (30) -1.65 (28) 26.38 (44) 46.29 (24) -44.32 (46)IM U.S. Mid Cap Growth Equity (MF) Median 7.40 35.50 14.18 -4.65 25.34 40.04 -45.01

3Years

EndingDec-2015

3Years

EndingDec-2014

3Years

EndingDec-2013

3Years

EndingDec-2012

3Years

EndingDec-2011

3Years

EndingDec-2010

3Years

EndingDec-2009

Victory Munder MC Core Gr 12.11 (63) 19.56 (36) 15.46 (23) 13.04 (18) 18.25 (56) -1.96 (61) -3.15 (53)Russell Midcap Growth Index 14.88 (25) 20.71 (19) 15.63 (22) 12.91 (20) 22.06 (16) 0.97 (37) -3.18 (53)IM U.S. Mid Cap Growth Equity (MF) Median 13.14 18.37 13.90 11.11 18.72 -0.79 -2.99

Victory Munder MC Core Gr 12/31/15

34INTEGRITY. BALANCE. OBJECTIVITY.

TOP 10 HOLDINGS

STYLE MAP (07/01/98 - 12/31/15)

SECTOR ALLOCATIONASSET ALLOCATION

PORTFOLIO CHARACTERISTICS

UP/DOWN CAPTURE (01/01/11 - 12/31/15)

L Brands Inc ORD 1.99 %SBA Communications Corp ORD 1.94 %Biomarin Pharmaceutical Inc ORD 1.88 %Cognizant Technology Solutions Corp ORD 1.88 %Avago Technologies Ltd ORD 1.84 %Advance Auto Parts Inc ORD 1.74 %Affiliated Managers Group Inc ORD 1.73 %Radian Group Inc ORD 1.71 %Lincoln National Corp ORD 1.71 %Macerich Co 1.70 %

Total Securities 85Avg. Market Cap $12,538 MillionP/E 27.80P/B 4.73Div. Yield 1.78%Annual EPS 20.235Yr EPS 21.553Yr EPS Growth 21.69

3 Years 5 Yearsvs. Russell Midcap Growth IndexBeta 0.96 0.97

Victory Munder MC Core Gr Russell Midcap Growth Index

0.0 5.0 10.0 15.0 20.0 25.0 30.0

UtilitiesTelecommunication Services

MaterialsInformation Technology

IndustrialsHealth Care

FinancialsEnergy

Consumer StaplesConsumer Discretionary

Other

0.0% 25.0% 50.0% 75.0% 100.0% 125.0%

Other

Fixed Income

Convertibles

Cash

Equities

0.0%

0.0%

0.0%

0.2%

99.8%

Style History Dec-2015

Average Style Exposure

Cap

italiz

atio

n

Manager Style

Large Cap Growth

Small Cap GrowthSmall Cap Value

Large Cap Value

Victory Munder MC Core Gr

50.0

75.0

100.0

125.0

150.0U

p C

aptu

re

50.0 70.0 90.0 110.0 130.0 150.0Down Capture

Victory Munder MC Core Gr 12/31/15

35INTEGRITY. BALANCE. OBJECTIVITY.

FUND INFORMATION

ROLLING 3 YEAR RETURN AND PERCENTILE RANKINGS

PEER GROUP ANALYSIS - IM U.S. Small Cap Value Equity (MF)

CALENDAR YEAR RETURNS AND PERCENTILE RANKINGS

RISK VS. RETURN (5 YEARS*)

*If less than 5 years, data is since inception of fund share class.

Firm and Management:ICM's Small Cap Value effort began in1989, and today Bill Heaphy, ChiefInvestment Officer, and Sim Wootenserve as co-portfolio managers of theICM Small Company Portfolio. Bothhave research responsibilities and Billserves as Director of Research for thesmall cap team. Gary Merwitz, RobJacapraro, Josh Overholt and MattFleming are analysts on the small capteam.

Investment Strategy:Management starts with a universe ofstocks with market caps of around $1billion and narrows the list throughscreens and company analysis. Theteam favors well-managed companieswith good growth prospects that aretrading at attractive valuations. It tendsto sell when valuations get too high orwhen the company doesn't meetexpectations.

Innovest's Assessment:The strategy should outperform in downand stable markets and when lessercapitalized companies are leading. Thefund should underperform during bullmarkets when companies with little orno earnings are in vogue due to itssensitivity to high valuations; althoughthis may be subdued due to its higherweighting of lesser capitalizedcompanies. The fund should alsounderperform when financials andutilities lead due to management'sperpetual aversion to the sectors.

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

Ret

urn

LastQuarter

YearTo Date

1Year

3Years

5Years

7Years

10Years

ICM Small Company 3.44 (35) -3.20 (14) -3.20 (14) 10.68 (25) 8.57 (29) 13.92 (36) 7.13 (15)

Russell 2000 Value Index 2.88 (44) -7.47 (56) -7.47 (56) 9.06 (50) 7.67 (52) 11.72 (79) 5.57 (50)

Median 2.52 -7.07 -7.07 9.05 7.81 13.27 5.51

-2.5

0.0

2.5

5.0

7.5

10.0

12.5

Ret

urn

(%)

0.0 6.0 12.0 18.0 24.0Risk (Standard Deviation %)

Return StandardDeviation

ICM Small Company 8.57 15.88

Russell 2000 Value Index 7.67 15.20

Median 7.81 15.27

2014 2013 2012 2011 2010 2009 2008ICM Small Company 2.87 (55) 36.16 (40) 16.93 (41) -4.85 (59) 22.73 (79) 34.46 (30) -35.11 (65)Russell 2000 Value Index 4.22 (34) 34.52 (56) 18.05 (33) -5.50 (64) 24.50 (60) 20.58 (80) -28.92 (25)IM U.S. Small Cap Value Equity (MF) Median 3.30 35.08 16.25 -3.78 24.99 28.27 -32.16

3Years

EndingDec-2015

3Years

EndingDec-2014

3Years

EndingDec-2013

3Years

EndingDec-2012

3Years

EndingDec-2011

3Years

EndingDec-2010

3Years

EndingDec-2009

ICM Small Company 10.68 (25) 17.88 (52) 14.85 (48) 10.94 (62) 16.23 (48) 2.31 (64) -3.39 (21)Russell 2000 Value Index 9.06 (50) 18.29 (43) 14.49 (55) 11.57 (49) 12.36 (95) 2.19 (65) -8.22 (55)IM U.S. Small Cap Value Equity (MF) Median 9.05 17.94 14.78 11.50 16.20 3.19 -7.52

ICM Small Company 12/31/15

36INTEGRITY. BALANCE. OBJECTIVITY.

TOP 10 HOLDINGS

STYLE MAP (05/01/89 - 12/31/15)

SECTOR ALLOCATIONASSET ALLOCATION

PORTFOLIO CHARACTERISTICS

UP/DOWN CAPTURE (01/01/11 - 12/31/15)

Dreyfus Treasury Prime Cash Management;Inst 2.60 %Ameris Bancorp ORD 1.59 %Kite Realty Group Trust 1.45 %Hanmi Financial Corp ORD 1.43 %Belden Inc ORD 1.42 %Integrated Device Technology Inc ORD 1.34 %NorthWestern Corp ORD 1.28 %South State Corp ORD 1.25 %Idacorp Inc ORD 1.25 %Ascena Retail Group Inc ORD 1.25 %

Total Securities 120Avg. Market Cap $1,496 MillionP/E 27.14P/B 1.87Div. Yield 2.33%Annual EPS 15.035Yr EPS 11.173Yr EPS Growth 6.48

3 Years 5 Yearsvs. Russell 2000 Value IndexBeta 1.01 1.03

ICM Small Company Russell 2000 Value Index

0.0 10.0 20.0 30.0 40.0 50.0 60.0

UtilitiesTelecommunication Services

MaterialsInformation Technology

IndustrialsHealth Care

FinancialsEnergy

Consumer StaplesConsumer Discretionary

Other

0.0% 25.0% 50.0% 75.0% 100.0% 125.0%

Other

Fixed Income

Convertibles

Cash

Equities

0.0%

0.0%

0.0%

2.6%

97.4%

Style History Dec-2015

Average Style Exposure

Cap

italiz

atio

n

Manager Style

Large Cap Growth

Small Cap GrowthSmall Cap Value

Large Cap Value

ICM Small Company

50.0

75.0

100.0

125.0

150.0U

p C

aptu

re

50.0 70.0 90.0 110.0 130.0 150.0Down Capture

ICM Small Company 12/31/15

37INTEGRITY. BALANCE. OBJECTIVITY.

FUND INFORMATION

ROLLING 3 YEAR RETURN AND PERCENTILE RANKINGS

PEER GROUP ANALYSIS - IM International Large Cap Value Equity (MF)

CALENDAR YEAR RETURNS AND PERCENTILE RANKINGS

RISK VS. RETURN (5 YEARS*)

*If less than 5 years, data is since inception of fund share class.

Firm and ManagementThe International Stock Fund ismanaged by the InternationalInvestment Policy Committee. The ninemembers of this committee have anaverage tenure at Dodge & Cox of 24years. In addition, all the firm's analystsare involved in security selection due totheir global coverage responsibilities.

Investment StrategyThe Fund invests primarily in adiversified portfolio of equity securitiesissued by non-U.S. companies from atleast three different countries, includingemerging markets. The Fund focuseson countries whose economic andpolitical systems appear more stableand are believed to provide someprotection to foreign shareholders. TheFund invests primarily in medium-to-large well established companiesbased on standards of the applicablemarket. In selecting investments, theFund invests primarily in companiesthat, in Dodge & Cox’s opinion, appearto be temporarily undervalued by thestock market but have a favorableoutlook for long-term growth.

Innovest's AssessmentWe believe this collaborative researchapproach will continue generatingshareholder value over full marketcycles; however, performance maysuffer during periods driven by moremacroeconomic events or a disregardfor company specific fundamentals.The strategy’s notable allocation todeveloping countries also suggests thatrelative performance may be partiallydictated by the market’s preference foremerging market securities.

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

Ret

urn

LastQuarter

YearTo Date

1Year

3Years

5Years

7Years

10Years

Dodge & Cox Intl 0.83 (99) -11.35 (100) -11.35 (100) 3.87 (32) 2.65 (34) 9.69 (3) 3.83 (17)

MSCI EAFE Value Idx 2.68 (46) -5.68 (92) -5.68 (92) 3.14 (44) 2.55 (39) 6.67 (25) 1.96 (64)

Median 2.61 -2.64 -2.64 2.97 2.07 6.22 2.48

-1.5

0.0

1.5

3.0

4.5

Ret

urn

(%)

12.0 14.0 16.0 18.0Risk (Standard Deviation %)

Return StandardDeviation

Dodge & Cox Intl 2.65 15.93

MSCI EAFE Value Idx 2.55 15.68

Median 2.07 14.97

2014 2013 2012 2011 2010 2009 2008Dodge & Cox Intl 0.08 (1) 26.31 (1) 21.03 (5) -15.97 (80) 13.69 (7) 47.46 (7) -46.69 (63)MSCI EAFE Value Idx -5.39 (25) 22.95 (9) 17.69 (44) -12.17 (34) 3.25 (77) 34.23 (25) -44.09 (48)IM International Large Cap Value Equity (MF) Median -8.37 21.25 17.18 -13.48 5.39 27.94 -44.32

3Years

EndingDec-2015

3Years

EndingDec-2014

3Years

EndingDec-2013

3Years

EndingDec-2012

3Years

EndingDec-2011

3Years

EndingDec-2010

3Years

EndingDec-2009

Dodge & Cox Intl 3.87 (32) 15.23 (1) 8.71 (12) 4.96 (5) 12.10 (9) -3.67 (7) -4.24 (10)MSCI EAFE Value Idx 3.14 (44) 11.04 (1) 8.32 (18) 2.19 (55) 6.77 (25) -8.15 (33) -7.35 (42)IM International Large Cap Value Equity (MF) Median 2.97 9.35 7.14 2.49 6.07 -9.13 -7.40

Dodge & Cox Intl 12/31/15

38INTEGRITY. BALANCE. OBJECTIVITY.

TOP 10 HOLDINGSPORTFOLIO CHARACTERISTICS

STYLE MAP (06/01/01 - 12/31/15)

SECTOR ALLOCATION

ASSET ALLOCATION

REGION ALLOCATION

TOP 5 COUNTRIES

UP/DOWN CAPTURE (01/01/11 - 12/31/15)

Sanofi SA ORD 4.03 %Naspers Ltd ORD 3.90 %Schlumberger NV ORD 3.24 %Roche Holding AG Par 3.20 %Barclays PLC ORD 2.79 %HP Inc ORD 2.49 %Samsung Electronics Co Ltd ORD 2.48 %Credit Suisse Group AG ORD 2.32 %Novartis AG DR 2.31 %Standard Chartered PLC ORD 2.07 %

Total Securities 90Avg. Market Cap $64,313 MillionP/E 23.06P/B 2.85Div. Yield 3.04%

0.0% 50.0% 100.0% 150.0%

Fixed Income

Convertibles

Other

Cash

Equities

0.0%

0.0%

0.2%

0.7%

99.1%

Switzerland 14.26 %United Kingdom 13.34 %Japan 12.80 %France 9.30 %Germany 6.27 %

3 Years 5 Yearsvs. MSCI EAFE Value IdxBeta 0.95 0.97

Dodge & Cox Intl MSCI EAFE Value Idx

0.0 8.0 16.0 24.0 32.0 40.0 48.0

UtilitiesTelecommunication Services

MaterialsInformation Technology

IndustrialsHealth Care

FinancialsEnergy

Consumer StaplesConsumer Discretionary

Dodge & Cox Intl MSCI EAFE Value Idx

0.0 8.0 16.0 24.0 32.0 40.0 48.0 56.0

OtherFrontier Markets

Middle EastUnited Kingdom

Europe ex UKJapan

Pacific ex JapanEM Mid East+Africa

North AmericaEM Latin America

EM EuropeEM Asia

Style History Dec-2015

Average Style Exposure

Cap

italiz

atio

n

Manager Style

MSCI EAFE Growth Index

MSCI Emerging Markets IndexMSCI EAFE Small Cap

MSCI EAFE Value Index

Dodge & Cox Intl

50.0

75.0

100.0

125.0

150.0

Up

Cap

ture

50.0 70.0 90.0 110.0 130.0 150.0Down Capture

Dodge & Cox Intl 12/31/15

39INTEGRITY. BALANCE. OBJECTIVITY.

FUND INFORMATION

ROLLING 3 YEAR RETURN AND PERCENTILE RANKINGS

PEER GROUP ANALYSIS - IM International Large Cap Growth Equity (MF)

CALENDAR YEAR RETURNS AND PERCENTILE RANKINGS

RISK VS. RETURN (5 YEARS*)

*If less than 5 years, data is since inception of fund share class.

Firm and Management:Like all American Funds, this fundboasts many experienced managers,most of whom have been with thecompany for more than a decade. Thismultimanager system eases personneltransitions, like the June 2014departure of long-time manager RobertLovelace, who moved to an affiliate.Each of the fund's nine managers runsa portion of the fund's assetsindependently. In addition, a portion ofthe portfolio (less than 25% of assets)is run by the firm's analyst staff.

Investment Strategy:This fund's managers are focused onlong term capital growth. They primarilyinvest in common stocks of Europeanand Pacific Basin issuers that haveprospects of above average capitalappreciation. The managers may usecash to moderate volatility, typicallyholding 5-10% of fund assets in cash.The Fund usually has a stake inemerging-markets companies and willsometimes hold preferred stock andconvertibles debt.

Innovest's Assessment:The fund’s propensity to focus intenselyon bottom-up, fundamental factors canlead to periods of underperformancewhen the market is less concernedabout company fundamentals and moredriven by thematic and macroeconomicfactors. Additionally, the fund is likely tolag when highly cyclical stocks andgenerally lower quality companiessignificantly outperform the overallmarket. Finally, the fund’s immenseasset base is likely to present somechallenges in the fund’s ability to buildmeaningful positions in smallercompanies and opportunistically tradein less liquid markets.

-12.0

-8.0

-4.0

0.0

4.0

8.0

12.0

16.0

Ret

urn

LastQuarter

YearTo Date

1Year

3Years

5Years

7Years

10Years

American Funds EuPc 2.87 (78) -0.82 (59) -0.82 (59) 5.08 (22) 3.63 (41) 8.92 (36) 4.60 (36)

MSCI EAFE Growth Index (Net) 6.67 (4) 4.09 (8) 4.09 (8) 6.83 (4) 4.60 (18) 8.92 (37) 4.03 (58)

Median 4.40 -0.57 -0.57 4.15 3.31 8.58 4.21

-1.5

0.0

1.5

3.0

4.5

6.0

7.5

Ret

urn

(%)

10.0 12.0 14.0 16.0 18.0Risk (Standard Deviation %)

Return StandardDeviation

American Funds EuPc 3.63 13.70

MSCI EAFE Growth Index (Net) 4.60 14.40

Median 3.31 14.48

2014 2013 2012 2011 2010 2009 2008American Funds EuPc -2.64 (28) 20.15 (33) 19.21 (44) -13.58 (48) 9.40 (64) 39.10 (19) -40.53 (16)MSCI EAFE Growth Index (Net) -4.43 (43) 22.55 (13) 16.86 (70) -12.11 (31) 12.25 (37) 29.36 (71) -42.70 (45)IM International Large Cap Growth Equity (MF) Median -4.98 18.39 18.85 -13.61 11.10 33.27 -43.61

3Years

EndingDec-2015

3Years

EndingDec-2014

3Years

EndingDec-2013

3Years

EndingDec-2012

3Years

EndingDec-2011

3Years

EndingDec-2010

3Years

EndingDec-2009

American Funds EuPc 5.08 (22) 11.72 (20) 7.37 (45) 4.07 (58) 9.56 (41) -3.27 (12) -0.53 (5)MSCI EAFE Growth Index (Net) 6.83 (4) 11.03 (37) 7.97 (33) 4.85 (34) 8.47 (69) -5.94 (48) -4.78 (52)IM International Large Cap Growth Equity (MF) Median 4.15 10.65 7.32 4.32 9.31 -6.08 -4.75

American Funds EuPc 12/31/15

40INTEGRITY. BALANCE. OBJECTIVITY.

TOP 10 HOLDINGSPORTFOLIO CHARACTERISTICS

STYLE MAP (05/01/84 - 12/31/15)

SECTOR ALLOCATION

ASSET ALLOCATION

REGION ALLOCATION

TOP 5 COUNTRIES

UP/DOWN CAPTURE (01/01/11 - 12/31/15)

Novo Nordisk A/S ORD 4.65 %Novartis AG ORD 2.46 %Barclays PLC ORD 2.29 %SoftBank Group Corp ORD 2.10 %Associated British Foods PLC ORD 1.80 %Prudential PLC ORD 1.78 %Bayer AG ORD 1.71 %HDFC Bank Ltd ORD 1.69 %Nintendo Co Ltd ORD 1.69 %Baidu Inc DR 1.40 %

Total Securities 466Avg. Market Cap $54,014 MillionP/E 24.23P/B 4.67Div. Yield 2.15%

0.0% 50.0% 100.0% 150.0%

Convertibles

Other

Cash

Fixed Income

Equities

0.0%

0.2%

0.4%

11.1%

88.3%

Japan 13.67 %United Kingdom 12.80 %United States 9.73 %France 7.45 %India 7.04 %

3 Years 5 Yearsvs. MSCI EAFE Growth Index (Net)Beta 0.87 0.93

American Funds EuPc MSCI EAFE Growth Index (Net)

0.0 4.0 8.0 12.0 16.0 20.0 24.0

UtilitiesTelecommunication Services

MaterialsInformation Technology

IndustrialsHealth Care

FinancialsEnergy

Consumer StaplesConsumer Discretionary

Other

American Funds EuPc MSCI EAFE Growth Index (Net)

0.0 10.0 20.0 30.0 40.0 50.0 60.0 70.0

OtherFrontier Markets

Middle EastUnited Kingdom

Europe ex UKJapan

Pacific ex JapanEM Mid East+Africa

North AmericaEM Latin America

EM EuropeEM Asia

Style History Dec-2015

Average Style Exposure

Cap

italiz

atio

n

Manager Style

MSCI EAFE Growth Index

MSCI Emerging Markets IndexMSCI EAFE Small Cap

MSCI EAFE Value Index

American Funds EuPc

50.0

75.0

100.0

125.0

150.0

Up

Cap

ture

50.0 70.0 90.0 110.0 130.0 150.0Down Capture

American Funds EuPc 12/31/15

41INTEGRITY. BALANCE. OBJECTIVITY.

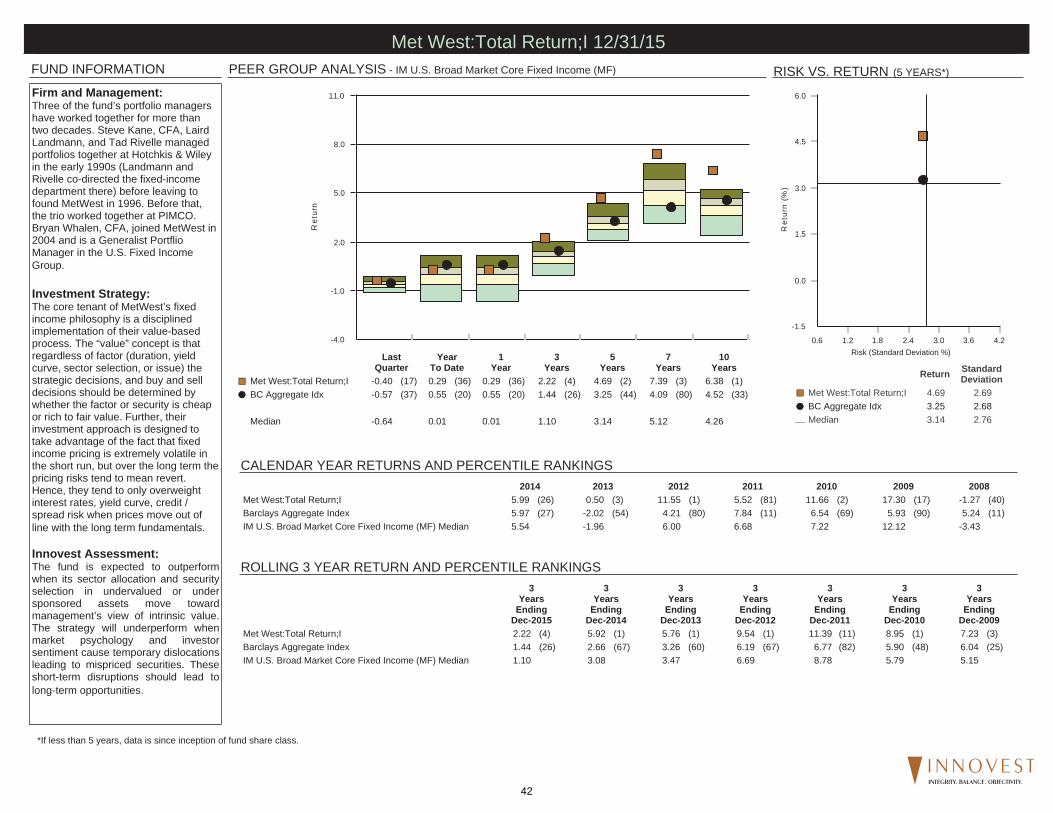

FUND INFORMATION

ROLLING 3 YEAR RETURN AND PERCENTILE RANKINGS

PEER GROUP ANALYSIS - IM U.S. Broad Market Core Fixed Income (MF)

CALENDAR YEAR RETURNS AND PERCENTILE RANKINGS

RISK VS. RETURN (5 YEARS*)

*If less than 5 years, data is since inception of fund share class.

Firm and Management:Three of the fund’s portfolio managershave worked together for more thantwo decades. Steve Kane, CFA, LairdLandmann, and Tad Rivelle managedportfolios together at Hotchkis & Wileyin the early 1990s (Landmann andRivelle co-directed the fixed-incomedepartment there) before leaving tofound MetWest in 1996. Before that,the trio worked together at PIMCO.Bryan Whalen, CFA, joined MetWest in2004 and is a Generalist PortflioManager in the U.S. Fixed IncomeGroup.

Investment Strategy:The core tenant of MetWest’s fixedincome philosophy is a disciplinedimplementation of their value-basedprocess. The “value” concept is thatregardless of factor (duration, yieldcurve, sector selection, or issue) thestrategic decisions, and buy and selldecisions should be determined bywhether the factor or security is cheapor rich to fair value. Further, theirinvestment approach is designed totake advantage of the fact that fixedincome pricing is extremely volatile inthe short run, but over the long term thepricing risks tend to mean revert.Hence, they tend to only overweightinterest rates, yield curve, credit /spread risk when prices move out ofline with the long term fundamentals.

Innovest Assessment:The fund is expected to outperformwhen its sector allocation and securityselection in undervalued or undersponsored assets move towardmanagement’s view of intrinsic value.The strategy will underperform whenmarket psychology and investorsentiment cause temporary dislocationsleading to mispriced securities. Theseshort-term disruptions should lead tolong-term opportunities.

-4.0

-1.0

2.0

5.0

8.0

11.0

Ret

urn

LastQuarter

YearTo Date

1Year

3Years

5Years

7Years

10Years

Met West:Total Return;I -0.40 (17) 0.29 (36) 0.29 (36) 2.22 (4) 4.69 (2) 7.39 (3) 6.38 (1)

BC Aggregate Idx -0.57 (37) 0.55 (20) 0.55 (20) 1.44 (26) 3.25 (44) 4.09 (80) 4.52 (33)

Median -0.64 0.01 0.01 1.10 3.14 5.12 4.26

-1.5

0.0

1.5

3.0

4.5

6.0

Ret

urn

(%)

0.6 1.2 1.8 2.4 3.0 3.6 4.2Risk (Standard Deviation %)

Return StandardDeviation

Met West:Total Return;I 4.69 2.69

BC Aggregate Idx 3.25 2.68

Median 3.14 2.76

2014 2013 2012 2011 2010 2009 2008Met West:Total Return;I 5.99 (26) 0.50 (3) 11.55 (1) 5.52 (81) 11.66 (2) 17.30 (17) -1.27 (40)Barclays Aggregate Index 5.97 (27) -2.02 (54) 4.21 (80) 7.84 (11) 6.54 (69) 5.93 (90) 5.24 (11)IM U.S. Broad Market Core Fixed Income (MF) Median 5.54 -1.96 6.00 6.68 7.22 12.12 -3.43

3Years

EndingDec-2015

3Years

EndingDec-2014

3Years

EndingDec-2013

3Years

EndingDec-2012

3Years

EndingDec-2011

3Years

EndingDec-2010

3Years

EndingDec-2009

Met West:Total Return;I 2.22 (4) 5.92 (1) 5.76 (1) 9.54 (1) 11.39 (11) 8.95 (1) 7.23 (3)Barclays Aggregate Index 1.44 (26) 2.66 (67) 3.26 (60) 6.19 (67) 6.77 (82) 5.90 (48) 6.04 (25)IM U.S. Broad Market Core Fixed Income (MF) Median 1.10 3.08 3.47 6.69 8.78 5.79 5.15

Met West:Total Return;I 12/31/15

42INTEGRITY. BALANCE. OBJECTIVITY.

TOP SECTOR ALLOCATIONSPORTFOLIO CHARACTERISTICS

STYLE MAP (04/01/00 - 12/31/15)

QUALITY ALLOCATION

ASSET ALLOCATION

MATURITY DISTRIBUTION

UP/DOWN CAPTURE (01/01/11 - 12/31/15)

GNMA and Other Mtg Backed 40.81 %Government Agency Securities 28.76 %Corporate Notes/Bonds 19.08 %Asset Backed Securities 8.21 %

Avg. Coupon 2.49 %Nominal Maturity 7.84 YearsEffective Maturity N/ADuration 4.81 YearsSEC 30 Day Yield 3.85Avg. Credit Quality AA

0.0% 50.0% 100.0% 150.0%

Convertibles

Equities

Other

Cash

Fixed Income

0.0%

0.0%

0.9%

2.2%

96.9%

0.0% 20.0% 40.0% 60.0% 80.0% 100.0%

Not RatedD Rated

Equities/OtherBB AND B Rated

CCC, CC AND C rated

AA RatedBBB Rated

A RatedGovernment/AAA

0.2%

0.2%

0.9%

2.5%

3.4%

3.9%

8.8%

10.6%

69.6%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0%

>30Yrs

Other

<1Yr

10-20Yrs

20-30Yrs

3-5Yrs

1-3Yrs

5-10Yrs

0.0%

0.9%

6.9%

7.9%

9.3%

16.1%

19.4%

39.5%

Style History Dec-2015

Average Style Exposure

Cap

italiz

atio

n

Manager Style

Barclays Capital Long Term Govt Bond

Barclays Capital Long U.S. CreditBarclays Capital U.S. Credit 1-5 Year Index

Barclays Capital 1-5 Yr Gov

Met West:Total Return;I

50.0

75.0

100.0

125.0

150.0U

p C

aptu

re

50.0 70.0 90.0 110.0 130.0 150.0Down Capture

Met West:Total Return;I 12/31/15

43INTEGRITY. BALANCE. OBJECTIVITY.

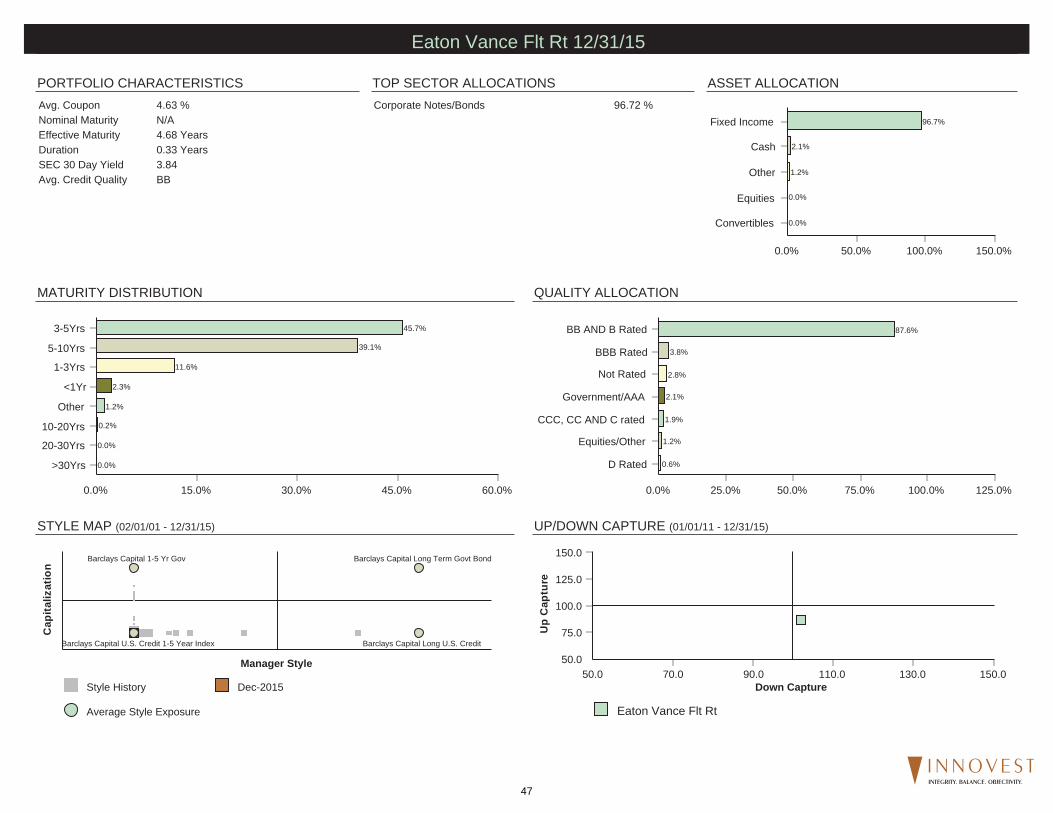

FUND INFORMATION

ROLLING 3 YEAR RETURN AND PERCENTILE RANKINGS

PEER GROUP ANALYSIS - IM U.S. High Yield Bonds (MF)

CALENDAR YEAR RETURNS AND PERCENTILE RANKINGS

RISK VS. RETURN (5 YEARS*)

*If less than 5 years, data is since inception of fund share class.

Firm and Management:William J. Morgan joined J.P. Morgan in2005. He is the high yield team leaderand the portfolio manager for allaccounts in the high yield, aggressiveincome high yield, and insurance asset"BB' default rating styles. He is amember of the High Yield ManagementReview Committee and is alsoresponsible for managing the HighYield Team's credit analysts. Prior tojoining the firm, he held the same roleat Banc One High Yield Partners, LLCand Pacholder Associates, Inc.

Investment Style:The team utilizes a flexible approachthat seeks to generate excess return byutilizing the full range of opportunitiespresented by the high yield market,from investment grade credits trading athigh yield spreads to distressed anddefaulted securities and post-reorganization debt securities.

Innovest's Assessment:The JPMorgan High Yield Fund hashistorically had an overweight allocationto BB and B-rated credits; therefore it islikely to underperform in markets wherelower-rated high yield credits (CCC andlower) perform well. The strategy islikely to outperform when higher qualityhigh yield credits are in favor or wheninvestors generally favor less riskyassets. Additionally, the strategy shouldperform well in market environmentswhere bottom-up fundamental creditresearch is rewarded.

-16.0

-10.0

-4.0

2.0

8.0

14.0

20.0

Ret

urn

LastQuarter

YearTo Date

1Year

3Years

5Years