Embed Size (px)

Citation preview

1

Yongqiang Cui, Shuai Zhai

Professor Marcel Blais

Math 574

12/1/16

Portfolio Optimization Project Report

Abstract

In this project, we close the portfolio established in the Portfolio Optimization Project. A

complete analysis of our portfolio including the construction, week-to-week performance,

week-to-week rebalancing process and overall performance will be given in this report. Ratio

analysis, Leverage analysis and basic risk measure are conducted by analyzing the portfolio

returns in time series. At the end of the project, a good-of-fit hypothesis test was performed to

determine the returns distribution’s consistence with our fitted distributions.

Introduction

The portfolio that we used to analyze is generated from Markowitz optimal portfolio from the

Portfolio Optimization Project. On 11/09/2016, The portfolio was constructed with calculated

weight of twenty stocks. The weight of different stocks was rebalanced each week until

12/06/2016, the date on which portfolio was closed. The total return of holding this portfolio

in this month is $22,923, with the initial capital of $500,000. Our portfolio value is increased

by 4.58% in the holding period. We choose S&P 500 as the market portfolio which grows

from 2,163.26 to 2,212.23 in the last month, with an increase of 2.25%. Thus, the overall

performance of our portfolio is good as it has a higher growth rate than our chosen market

portfolio.

Methodology

Our portfolio is formed based on the Modern portfolio theory, or mean-variance analysis,

introduced by Harry Markowitz in 1952. It is a mathematical framework for assembling a

portfolio of assets to maximize the expected return for a given level of risk, defined as

variance. (Markowitz, 1952)

Historical stock price of last one year was used to in our project to estimate the weights in

Markowitz optimal portfolio. We first use our data of stock price to calculate the optimal

portfolio with different expected return and variance, code listed in appendix (1). Then

combine the optimal portfolios to create an efficient frontier, code in appendix (2). Tangency

line with the intercept of risk-free rate of the efficient frontier, which is called the tangency

portfolio could be found using code appendix (3). After that, construct the Markowitz optimal

portfolio with the weights of tangency portfolio. In each of the following week, we will add

the stocks’ price of the new week into historical data and rebalance the weight of stocks in

the portfolio. The market value of stocks and the portfolio was recorded for analyzing

purpose.

2

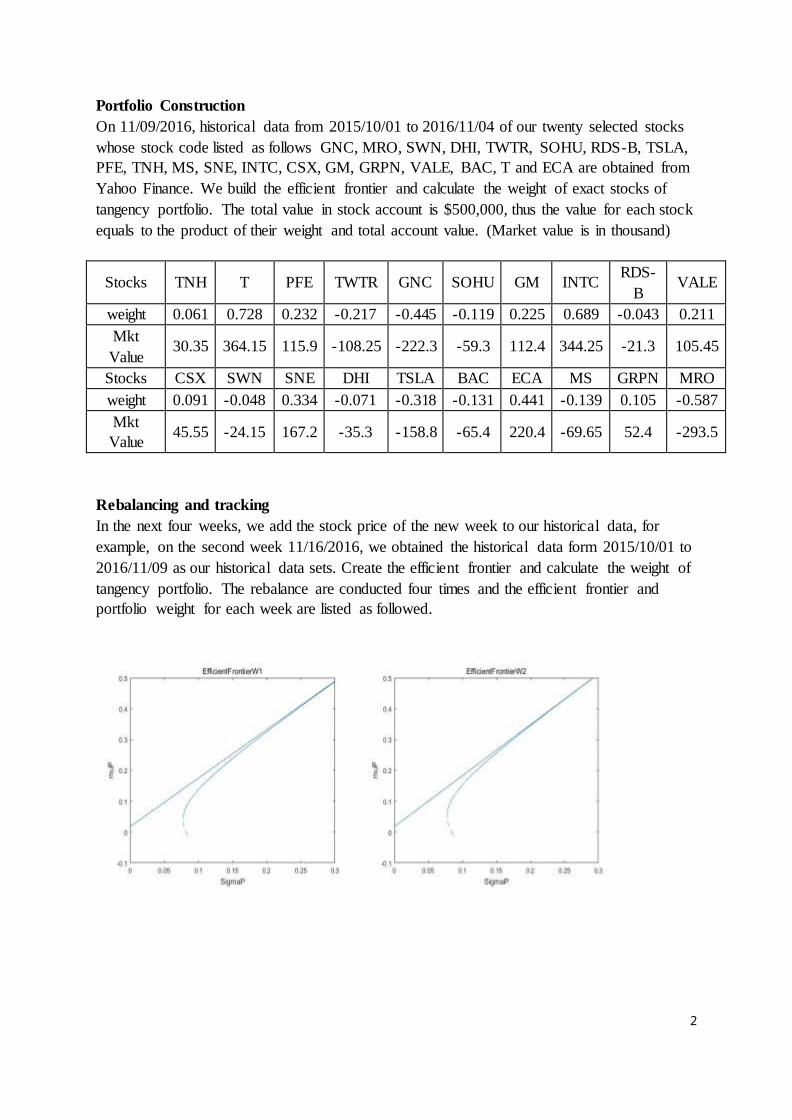

Portfolio Construction

On 11/09/2016, historical data from 2015/10/01 to 2016/11/04 of our twenty selected stocks

whose stock code listed as follows GNC, MRO, SWN, DHI, TWTR, SOHU, RDS-B, TSLA,

PFE, TNH, MS, SNE, INTC, CSX, GM, GRPN, VALE, BAC, T and ECA are obtained from

Yahoo Finance. We build the efficient frontier and calculate the weight of exact stocks of

tangency portfolio. The total value in stock account is $500,000, thus the value for each stock

equals to the product of their weight and total account value. (Market value is in thousand)

Stocks TNH T PFE TWTR GNC SOHU GM INTC RDS-

B VALE

weight 0.061 0.728 0.232 -0.217 -0.445 -0.119 0.225 0.689 -0.043 0.211

Mkt

Value 30.35 364.15 115.9 -108.25 -222.3 -59.3 112.4 344.25 -21.3 105.45

Stocks CSX SWN SNE DHI TSLA BAC ECA MS GRPN MRO

weight 0.091 -0.048 0.334 -0.071 -0.318 -0.131 0.441 -0.139 0.105 -0.587

Mkt

Value 45.55 -24.15 167.2 -35.3 -158.8 -65.4 220.4 -69.65 52.4 -293.5

Rebalancing and tracking

In the next four weeks, we add the stock price of the new week to our historical data, for

example, on the second week 11/16/2016, we obtained the historical data form 2015/10/01 to

2016/11/09 as our historical data sets. Create the efficient frontier and calculate the weight of

tangency portfolio. The rebalance are conducted four times and the efficient frontier and

portfolio weight for each week are listed as followed.

3

Date 11/9/2016 11/16/2016 11/23/2016 12/1/2016

Min up 0.0396 0.0511 0.051 0.0621

Min Variance 0.006 0.0061 0.0061 0.0061

From the comparison of efficient frontier, minimum variances are almost constant and its

corresponded portfolio returns increase in the last four weeks.

And the corresponding tangency portfolio weights are listed as followed:

2016/11/9 2016/11/16 2016/11/23 2016/11/30 Average

MRO -0.5870 -0.2965 -0.2843 -0.2231 -0.3477

GNC -0.4446 -0.3018 -0.2898 -0.2085 -0.3112

TWTR -0.2165 -0.1697 -0.1540 -0.1434 -0.1709

BAC -0.1308 0.2814 0.4481 0.5072 0.2765

SWN -0.0483 -0.1852 -0.1832 -0.1313 -0.1370

MS -0.1393 -0.0334 0.0847 -0.0648 -0.0382

SOHU -0.1186 -0.2562 -0.2887 -0.2137 -0.2193

DHI -0.0706 -0.4836 -0.3367 -0.2988 -0.2974

TSLA -0.3176 -0.3158 -0.3518 -0.2278 -0.3033

RDS B -0.0426 -0.1951 -0.2877 -0.2620 -0.1969

TNH 0.0607 0.1067 0.0758 0.0757 0.0797

CSX 0.0911 0.3590 0.2184 0.1932 0.2154

PFE 0.2318 0.2207 -0.0162 -0.0225 0.1035

GM 0.2248 0.4276 0.2434 0.2199 0.2789

SNE 0.3344 0.2072 0.1198 0.0357 0.1743

T 0.7283 0.8825 1.2254 1.1876 1.0060

INTC 0.6885 0.1652 0.1812 0.0938 0.2822

GRPN 0.1048 0.0602 0.0398 0.0330 0.0595

VALE 0.2109 0.1697 0.1457 0.1451 0.1679

ECA 0.4408 0.3570 0.4100 0.3045 0.3781

4

We attempted to keep the data period of exact one year by delating a week’s data at the

beginning and adding one week’s date at present. However, the results run by our Markowitz

Optimal Model do not make us satisfied. The weight of portfolio for a new week changes too

much too rebalance on Interactive Brokers. Thus, we choose to update new weeks’ stock

price and extend the period of our historical stock price. The returns covariance matrix does

not change a lot.

Portfolio Performance

From the total value of Interactive Brokers Accounts which consists of $504,128 cash and

$499,823 Stock in the first week. The total account value ends up in $1,026,814, the invest

return of holding this portfolio for one month is $22,923. Our portfolio value is increased by

2.28% within the holding period. Compared to our chosen market portfolio S&P 500 which

grows from 2,163.26 to 2,212.23 in the last month, with an increase of 2.25%. The overall

performance of our portfolio is good as it has a higher rate of return.

Ratio Analysis:

We use the S&P 500 as benchmark and in our models, we use sample mean return estimate

p , use sample standard deviation of returns to estimate volatility and use the 10-year Treasury

Yield as our risk-free rate f :

5

Date Portfolio Return Market Return

Excess Return(up-

um)

Excess Return(up-

uf)

2016/12/6 0.001000514 0.003410879435 -0.002410365435 0.000921929058

2016/12/5 0.010795234 0.005821300668 0.004973933332 0.01071664906

2016/12/2 0.001143647 0.0003970644614 0.0007465825386 0.001065062058

2016/12/1 -0.038764015 -0.00351553795 -0.03524847705 -0.03884259994

2016/11/30 -0.005836422 -0.002653470376 -0.003182951624 -0.005915006942

2016/11/29 0.029008915 0.001335319659 0.02767359534 0.02893033006

2016/11/28 0.016074101 -0.005254478505 0.02132857951 0.01599551606

2016/11/25 0.021870169 0.003914329257 0.01795583974 0.02179158406

2016/11/23 -0.007135212 0.0008080111124 -0.007943223112 -0.007213796942

2016/11/22 0.02008148 0.002165427763 0.01791605224 0.02000289506

2016/11/21 0.007069175 0.007461386865 -0.0003922118647 0.006990590058

2016/11/18 0.007708739 -0.002386700318 0.01009543932 0.007630154058

2016/11/17 0.003950144 0.004676288736 -0.0007261447356 0.003871559058

2016/11/16 0.039926843 -0.001582285738 0.04150912874 0.03984825806

2016/11/15 -0.00288217 0.007480824323 -0.01036299432 -0.002960754942

2016/11/14 -0.030046657

-

0.0001155027836 -0.02993115422 -0.03012524194

2016/11/11 -0.035896756 -0.001397936775 -0.03449881923 -0.03597534094

2016/11/10 -0.011609604 0.001950759502 -0.0135603635 -0.01168818894

Mean 0.001469895833 0.001250871074 0.0002190247591 0.001391310891

Standard

Dev 0.02128609889 0.003713625597 0.020881997 0.02128609889

The plots of the portfolio returns are showed as followed:

Then we use the following measures to analyze our portfolio:

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

11/1

0/20

16

11/1

1/20

16

11/1

2/20

16

11/1

3/20

16

11/1

4/20

16

11/1

5/20

16

11/1

6/20

16

11/1

7/20

16

11/1

8/20

16

11/1

9/20

16

11/2

0/20

16

11/2

1/20

16

11/2

2/20

16

11/2

3/20

16

11/2

4/20

16

11/2

5/20

16

11/2

6/20

16

11/2

7/20

16

11/2

8/20

16

11/2

9/20

16

11/3

0/20

16

12

/1/2

01

6

12

/2/2

01

6

12

/3/2

01

6

12

/4/2

01

6

12

/5/2

01

6

12

/6/2

01

6

Daily Return

6

(1) Sharpe Ratio: p f

p

RS

(2) Treynor Ratio: p f

p

RT

,

2

PMp

M

(3) Information Ratio p f

Rp RM

RI

(4) Sortino Ratio:

Definition:The dispersion of X from a given value a is

2 2( ) ( )a x a f x dx

.

In finance, we are concerned about downside dispersion from some value a i.e. X taking

values in ( , ]a define the semi variance of X about a is

2 2( ) ( )a x a f x dx

.

Given sample R1, R2, R3…Rn of returns with some distribution f(x), Define ,

,

i

i

i i

a R ay

R R a

,

then the downside sample semi variance is

2 2 2

1 1

1 1( ) [min(0, )]n n

a i i i iS y a R an n

So, we use

f

p f

S

to estimate the Sortiono Ratio

0

0p

r

r

.

Outcomes:

Sharp Ratio Treynor Ratio Information Ratio Sortino Ratio

0.06390022971 0.001292279398 0.008901856247 0.09195970697

The Sortino Ratio is a modification of the Sharpe Ratio but penalizes only those returns falling

below our expected return, while the Sharpe ratio penalizes both upside and downside volatility

equally. The difference between the Sharpe ratio and the Information Ratio is that the

Information Ratio aims to measure the risk-adjusted return in relation to a benchmark. A

variation of the Sharpe ratio is the Sortino ratio, which removes the effects of upward price

movements on standard deviation to measure only return against downward price volatility and

uses the semi variance in the denominator. The Treynor ratio uses systematic risk, or beta (β)

instead of standard deviation as the risk measure in the denominator.

7

Comparing through these ratios, it shows that all the ratios are all positive indicating that our

portfolio perform well. However, these values of ratios are not very high, Treynor Ratio and

Information Ratio are even around zero. We could conclude that although our portfolio could

make money, we still take additional risks.

(5) Maximum drawdown:

The maximum drawdown (MDD) up to time T is,

(0, ) (0, )( ) max[max ( ) ( )]

T tMDD T X t X

Peak value valley value Maximum drawdown Maximum drawdown/Peak Value

992236 925201 67035 6.76%

During this period, huge loss was suffered in our portfolio with a maximum drawdown of 6.76%

within four trading days.

(6) Portfolio alpha and beta

It is based on Jensen performance measure,

( )p p f p m f

Portfolio Beta 0.03333847659

Portfolio Alpha 0.0001460887197

With a positive Alpha 0.0001460887197, it means although our portfolio performs better than

the benchmark, its value is around 0 which means our portfolio’s performance is very close

to the market performance. And the Beta is 0.03, indicating that our portfolio return has

potential risk in some way.

(7) Comparison of our portfolio performance to industry benchmarks

As far as we are concerned, by comparing to the benchmarks, the overall performance of our

portfolio is very close to the benchmarks’. But we take additional risks comparing to the market.

850000900000950000

100000010500001100000

11/1

0/20

16

11/1

1/20

16

11/1

2/20

16

11/1

3/20

16

11/1

4/20

16

11/1

5/20

16

11/1

6/20

16

11/1

7/20

16

11/1

8/20

16

11/1

9/20

16

11/2

0/20

16

11/2

1/20

16

11/2

2/20

16

11/2

3/20

16

11/2

4/20

16

11/2

5/20

16

11/2

6/20

16

11/2

7/20

16

11/2

8/20

16

11/2

9/20

16

11/3

0/20

16

12/1

/201

6

12/2

/201

6

12/3

/201

6

12/4

/201

6

12/5

/201

6

12/6

/201

6

Market value

8

(8) While trading on Interactive Brokers, we are limited by the Margin calls. The portfolio

weight calculated by Markowitz Optimal Model sometimes cannot be exercised because you

need to short too much stocks. The margin calls will appear for some unreasonable weight of

portfolio. We adjust our portfolio by changing one or several stocks and calculate the weight

for new portfolio. Usually, we delate the stocks which requires to do more short position from

the Model. Repeat this process until we found an exercisable weight of tangency portfolio.

Leverage Analysis

Date Total Debt

Leverage

Ratio

2016/12/6 2336947.85 2.33694785

2016/12/5 2314261.48 2.31426148

2016/12/2 2287899.17 2.28789917

2016/12/1 2303301.716 2.303301716

2016/11/30 2696540.848 2.696540848

2016/11/29 2654664.216 2.654664216

2016/11/28 2673747.689 2.673747689

2016/11/25 2703091.755 2.703091755

2016/11/23 2691175.457 2.691175457

2016/11/22 2826370.712 2.826370712

2016/11/21 2795538.602 2.795538602

2016/11/18 2748163.639 2.748163639

2016/11/17 2747769.797 2.747769797

2016/11/16 2732490.91 2.73249091

2016/11/15 2574427.828 2.574427828

2016/11/14 2538839.014 2.538839014

2016/11/11 2534622.348 2.534622348

2016/11/10 2531621.124 2.531621124

2016/11/9 2516046.038 2.516046038

The leverage ratio of our portfolio stays around 2.5, which is the highest level that avoid the

margin calls. A higher leverage ratio will cause margin calls and we need to adjust the portfolio

0

1

2

3

11/9/20…

11/11/2…

11/13/2…

11/15/2…

11/17/2…

11/19/2…

11/21/2…

11/23/2…

11/25/2…

11/27/2…

11/29/2…

12/1/20…

12/3/20…

12/5/20…

Leve

rage

Rat

io

Date

Leverage Ratio vs. Date

Leverage Ratio

9

composition by changing several stocks.

Capstone Part

Basic risk Measure

In this part, we use volatility of returns, Value-at-risk (VaR) and Conditional value-at- risk

(CVaR) as the weekly risk measures of our portfolio. For VaR and CVaR, we use the parametric

method to estimate them with both a normal and a student-t returns distribution and three

different confidence level (1%, 5%, 10%).

Method introduction:

Gaussian VaR and CVaR

Let 2-x /21

2e

(x)= denote the PDF of the standard normal distribution, and let (x)

denote the corresponding CDF with ' . The Gaussian quantile function ( )Q is the

function satisfying the condition

( ( ))Q

for all : 0 1 .

In the case of a Gaussian distribution with mean and variance 2 , the quantile function

of that distribution is then ( )Q and the corresponding “Value at Risk”, or VaR, is just

the negative of the quantile, which is

( ) ( )VaR Q

The CVaR is a related entity, giving the average in a tail bounded by the corresponding VaR

level. In general, for a density function ( )f x linked to a random variable X, we would need to

know

( )1[ | ( )] ( )

Q

E X X Q xf x dx

In the case, because ' x , so that for a standard normal distribution

1[ | ( )] ( ( ))E X X Q Q

and applying a scaling and translation to get the general case gives us, for the loss

( ) ( ( ))CVaR Q

In the case of a Gaussian system, there is no substantive diff erence between the VaR and CVaR

10

measures: both take the form

( ) ( )Risk

where ( ) ( )Q in the case of VaR and 1

( ) ( ( ))Qu

in the case of CVaR.

Student’s T VaR and CVaR

The pdf of the Student’s T distribution is

2 ( 1)/2

1 [( 1) / 2] 1( , )

[ / 2] (1 / ) v

vh t v

v t vv

It is like the pdf function in Gaussian case. Define the quantile function ( , )TQ n for a standard

univariate T distribution (n is the degree of freedom). If we wish to parametrize the problem

again by mean and standard deviation, the VaR will be given by

2( ) ( , )T

nVaR Q n

n

The relevant function for this case is not the (negative of the) standard T quantile but the

negative of the scaled unit variance T quantile

2( ) ( , ) ( , )T

nQ n Q n

n

:

The VaR measure of risk is now in standard form ( ) .

For the CVaR, we need to find the integral of ( , )nh n and we can find the function

1

/2 2 2 21

( )( )2( , )

2 ( )2

v vv v t

k t vv

Then the CVaR with mean and variance 2 is now

2 1( ) ( , )T

nCVaR k Q n

n

( ),

and now the 2 1

( ) ( , )T

nk Q n

n

( ),

By calculation by MATLAB, we get the four weeks’ VaR and CVaR. (William, 2011)

11

Volatility analysis:

We compare the volatility of our portfolio returns with the market volatility, which in our case

is the volatility of the S&P500 index.

Week1 Week2 Week3 Week4

Portfolio Return Volatility 2.99% 0.97% 2.75% 0.56%

Market Volatility 0.37% 0.37% 0.38% 0.27%

By comparing across weeks, the Week4 has the smallest volatility (0.56%), and the Week2 also

has a smaller volatility (0. 97%).The volatilities of week1 and week3 are near 3%. As the result,

the Week2 and Week4 shows the lower risk of all four weeks. So, our portfolio has a relevantly

high volatility to the market performance. And comparing to the market performance, our

portfolio has a relevantly high volatility to the market volatility. Our portfolio shows higher

risk than it should have. (Wagner, 2007)

VaR analysis:

We sort the four weeks VaR data and plot them.

The degree of freedom of T distribution is 3 according to the MATLAB function mle ().

VaR(Gaussian) VaR(T)

Confidence level 1% 5% 10% Confidence level 1% 5% 10%

Week1 0.0777 0.0573 0.0464 Week1 0.086 0.0547 0.0422

Week2 0.0165 0.0098 0.0063 Week2 0.0192 0.009 0.0049

Week3 0.0595 0.0408 0.0308 Week3 0.0672 0.0385 0.054

Week4 0.0087 0.0049 0.0029 Week4 0.0104 0.0033 9.85E-04

2.99%

0.97%

2.75%

0.56%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

Week1 Week2 Week3 Week4

Volalitility

12

To explain the VaR clearly, we choose the VaR(Gaussian) with the confidence level 5% of the

Week1 as an example, 0.0573 means that there is a 0.05 probability that the portfolio return

will fall by more than 0.0573 this week. It can also be said that with 95% confidence that the

worst daily loss will not exceed 0.0573. So for the same confidence leve, the high VaR means

the higher potential risk that the porfolio has.

By comparing the tables and plots, with the same confidence and distribution, the VaR of

Week2 and Week4 is always very small. With the 5% and 10% confidence level of T

distributuion, we find that the returns of Week2 and Week4 still show lower risks.

CVaR analysis:

The CVaR is the second name of Expected Shortfall (ES). For example, with 5% level, the

"expected shortfall at 5% level" is the expected return on the portfolio in the worst 5% of cases.

So, with the same confidence level, the higher the CVaR, the lower the risk of the portfolio has.

For the tendency of the CVaR is same for the different confidence level. We choose the case

with 5% confidence level to analyze. (Carlo & Dirk, 2002).

5% confidence level CVaR(Gaussian) CVaR(T)

Week1 -0.98 -1.02

Week2 -0.33 -0.55

Week3 -0.91 -0.94

Week4 -0.19 -0.37

0.0777

0.0165

0.0595

0.0087

0.0573

0.0098

0.0408

0.0049

0.0464

0.0063

0.0308

0.0029

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

Week1 Week2 Week3 Week4

VaR(Gaussian)

1% 5% 10%

0.086

0.0192

0.0672

0.0104

0.0547

0.009

0.0385

0.0033

0.0422

0.0049

0.054

9.85E-04

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

Week1 Week2 Week3 Week4

VaR(T)

1% 5% 10%

13

`

By comparing the table and plots with two distributions, the Week2 and Week4 suffer from the

lower expected loss. Meanwhile, the Week1 and Week3 have higher risks.

Goodness-of fit Hypothesis

Form a time series of daily returns from our factor modeling project. Here we choose the

French and Fama model include F1 (Short-Term Reversal Factor). Time series of daily

returns and the bate values of this model are both obtained from factor modeling project.

French&F1 beta0 Mkt-RF SMB HML ST_Rev E(R)

VALE 0.000314 0.014083 -0.004220 0.009180 0.018838 -0.002803

ECA 0.001019 0.012178 0.013284 0.026709 0.018977 -0.003691

GRPN 0.000135 0.008741 0.007860 -0.003348 0.007406 -0.004060

MRO 0.000738 0.014722 0.008103 0.021085 0.012380 -0.003185

SWN 0.000840 0.009314 0.010014 0.020318 0.021306 -0.005241

BAC 0.000176 0.013188 0.001662 0.007796 -0.002979 0.000468

TWTR 0.000152 0.008076 0.011793 -0.005722 0.007450 -0.002960

TSLA -0.000204 0.010725 -0.002283 -0.008123 0.002006 0.001080

MS 0.000205 0.015092 0.003453 0.007975 -0.003709 -0.000358

CSX 0.000105 0.011817 0.000131 0.003794 0.001772 -0.001069

DHI 0.000070 0.012115 0.004077 0.000071 -0.000445 0.000955

TNH 0.000180 0.004035 0.001439 0.004614 0.005232 -0.001230

-1.20

-1.00

-0.80

-0.60

-0.40

-0.20

0.00

Week1 Week2 Week3 Week4

CVaR

CVaR(Gaussian) CVaR(T)

14

T 0.000012 0.007878 -0.001435 0.002348 -0.001589 0.000227

INTC -0.000029 0.009575 -0.002245 0.000318 0.000403 0.000390

GM 0.000012 0.010057 -0.002267 0.001510 0.001890 -0.000126

GNC 0.000317 0.010536 0.015396 0.001217 0.001803 -0.001497

PFE -0.000110 0.008961 -0.000972 -0.004850 0.001589 -0.000093

SNE -0.000046 0.011447 -0.002676 -0.001292 0.003126 -0.000470

RDS-B 0.000327 0.009771 0.001995 0.010535 0.005610 -0.001448

SOHU 0.000160 0.006784 0.003418 -0.000794 0.012175 0.000764

Fit our returns distribution to both normal and a t density distribution. For normal distribution,

we calculate the mean, standard deviation and the z value to create the plot. For Student T

distribution, degree of freedom is required to be considered. We calculated it using MATLAB

function mle () which turns out to be 8.3174.

0123456789

-2.8

2828

0613

-2.6

239

-2.4

195

-2.2

152

-2.0

108

-1.8

064

-1.6

020

-1.3

977

-1.1

933

-0.9

889

-0.7

846

-0.5

802

-0.3

758

-0.1

714

0.03

29

0.2

373

0.4

417

0.6

460

0.85

04

1.05

48

1.2

592

1.4

635

1.6

679

1.87

23

2.07

66

2.2

810

2.4

854

2.6

898

2.89

41

3.09

85

3.30

29

PDF&Histogram of Normal Dist

0123456789

-2.8

2828

0613

-2.6

239

-2.4

195

-2.2

152

-2.0

108

-1.8

064

-1.6

020

-1.3

977

-1.1

933

-0.9

889

-0.7

846

-0.5

802

-0.3

758

-0.1

714

0.03

29

0.23

73

0.44

17

0.64

60

0.85

04

1.05

48

1.25

92

1.46

35

1.66

79

1.87

23

2.07

66

2.28

10

2.48

54

2.68

98

2.89

41

3.09

85

3.30

29

CDF&Histogram of Student's T Dist

15

Then use the time series of daily returns to perform a goodness- of-fit hypothesis test. Assign

data to 60 intervals in a histogram and acquire the frequency for each interval. Then denote Pi

as the probability of normal distribution with Cumulative Distribution Function F, calculate Pi

for each interval i using formula. (Jensen, 1968)

1

t

( ) ( ) ( )i i i

i hIn erval

P f y dy F y F y

iN Pg =theoretical frequency.

Chi-square test statistic:

22

1

( )n i i

ii

u N P

N P

g

g

Use the same formula to calculate the 2 value for Student-t distribution

0

2

4

6

8

10

12

14

-0.0

270

-0.0

243

-0.0

216

-0.0

189

-0.0

162

-0.0

135

-0.0

108

-0.0

081

-0.0

054

-0.0

027

0.00

00

0.00

27

0.00

54

0.00

82

0.01

09

0.01

36

0.01

63

0.01

90

0.02

17

0.02

44

0.02

71

Histogram of Original Data

Frequency

0

0.2

0.4

0.6

0.8

1

1.2

-0.03 -0.02 -0.01 0 0.01 0.02 0.03 0.04

CDF

Normal Student-T

16

Then we can calculate p-value,

H0: Distribution fit our data

H1: Distribution not fit our data

Normal student-t

2 0.05879 0.4016

p-value 0.971033 0.9999

Both P-value is quite high which means we can reject H0 at very high confidence level. Very

strong evidence against H0 that these two distributions fit our data. Both distributions are not

good to estimate our model.

Conclusion

More attention should be paid during stock selection. In this project, lots of effort was put on

adjusting our stock composition to avoid margin calls. On the other hand, Markowitz Optimal

Model has a good performance and it will be a good choice to construct a portfolio next time.

If we are to re-do this project in the spring semester, we will follow most of the approach in

this project since it brings a good rate of return. While choosing stocks, some with unusua l

behavior in price should not be considered because they will increase the difficulty of

constructing portfolio. Meanwhile, we could use the methods we have learned and constructed

models to evaluate the risk of our portfolios. Because from the risk management part of our

portfolio, we could find that although we can get positive returns, there is still potential risks

affecting our portfolio performance. The risk management is also a significant issue while we

want to pursue the higher return.

17

Appendix:

m-files

1.

(1).

function [ optimalWeights ] = optimalPortfolio( expReturns, CovMatrix, expPortfolioReturn)

mu = expReturns ;

Omega = CovMatrix;

N=length(mu);

muP=expPortfolioReturn;

One = ones(length(mu),1) ;

invOmega = inv(Omega) ;

A = One'*invOmega*mu ;

B = mu'*invOmega*mu ;

C = One'*invOmega*One ;

D = B*C - A^2 ;

h=invOmega*(C*mu/D-A*One/D);

g=invOmega*(B*One/D-A*mu/D);

optimalWeights =h*muP+g;

end

(2).

N=length(expPortfolioReturn);

for i=1:N

[ optimalWeights] = optimalPortfolio( expReturns, CovMatrix, expPortfolioReturn(i));

SigmaStar(i)=sqrt(optimalWeights'*CovMatrix*optimalWeights);

end

plot(SigmaStar,expPortfolioReturn)

title('efficientFrontier')

xlabel('SigmaP')

ylabel('muP')

(3). function [ TangencyWeights ] = TangencyPortfolio( expReturns, CovMatrix,muf)

mu = expReturns ;

Omega = CovMatrix;

N=length(mu);

One = ones(length(mu),1) ;

invOmega = inv(Omega) ;

A = One'*invOmega*mu ;

B = mu'*invOmega*mu ;

C = One'*invOmega*One ;

D = B*C - A^2 ;

h=invOmega*(C*mu/D-A*One/D);

g=invOmega*(B*One/D-A*mu/D);

18

w=invOmega*(mu-muf*One);

TangencyWeights=w/(One'*w);

end

2.

function [ Sharp,Treynor,Sortino,Alpha,Beta ] = Ratios( Rp, Rm,uf)

n=length(Rp);

uRp=mean(Rp);

StDRp=std(Rp);

uRm=mean(Rm);

StDRm=std(Rm);

ExcessRpm=Rp-Rm;

uExcessRpm=mean(ExcessRpm);

StDexcess=std(ExcessRpm);

Sharp=(uRp-uf)/StDRp;

A=cov(Rp,Rm);

B=A(1,2)/var(Rm);

for i=1:n

Rpf(i)=Rp(i)-uf;

end

meanRpf=mean(Rpf);

Treynor =meanRpf/B;

Information=ExcessRpm/StDexcess;

Beta=A(1,2)/var(ExcessRpm);

Alpha=uExcessRpm-uf+Beta*(uRm-uf);

for i=1:n

if (Rp(i)-uf)<0

negative(i)=Rp(i)-uf;

end

end

Downside=(sumsqr(negative)/n)^0.5;

Sortino=meanRpf/Downside;

end

2.

function [VaRnormal,CVaRnormal,VaRt,CVaRt,CVaRTt] = ValueAtRisk(returns,alpha,v)

n=length(returns);

m=mean(returns);

sigma=std(returns);

S=sqrt(sigma^2*n/(n-1));

x=norminv([alpha 1-alpha],0,1);

19

t=tinv(alpha,v);

C=x(1);

VaRnormal=-m-sigma*C;

CVaRnormal=-m+sigma*C/alpha;

VaRt=-m-sigma*sqrt((v-2)/v)*t;

CVaRTt=(-((v^(-1/2)*(v+t^2)))/(alpha*beta(v/2,1/2)*(n-1)))*((1+t^2/n)^(-(v+1/2)));

end

Reference

1. Markowitz, H. (1952). Portfolio Selection. The Journal of Finance, 7(1), 77.

doi :10.2307/2975974

2. Wagner, H. (2007). Volatility's Impact On Market Returns. Retrieved December 12, 2016,

from http://www.investopedia.com/articles/financial-theory/08/volatility.asp

3. Carlo Acerbi; Dirk Tasche (2002). "Expected Shortfall: a natural coherent alternative to

Value at Risk" (pdf). Economic Notes. 31: 379–388. doi:10.1111/1468-0300.00091

4. William T. S. (2011). Risk, VaR, CVaR and their associated Portfolio Optimizations when

Asset Returns have a Multivariate Student T Distribution;

5. Jensen, M.C. (1968), “The Performance of Mutual Funds in the Period 1945-1964,”

Journal of Finance 23, 1968, pp. 389-416.