Embed Size (px)

Citation preview

Portfolio Committee on Public Service and Administration and Performance Monitoring and evaluationReview of 2015/16 Annual performance plansPresenters: Carl Wessels – Senior Manager AGSA

Trudie Botha – Senior Manager AGSA

Reputation promise/mission

The Auditor-General of South Africa has a constitutional mandate and, as the Supreme Audit Institution (SAI) of South Africa, exists to strengthen ourcountry’s democracy by enabling oversight, accountability and governance in the public sector through auditing, thereby building public confidence.

2

Topics to discuss

3

Background

4

Audits performed by the AGSA

5

Clean administration – from annual audits

6

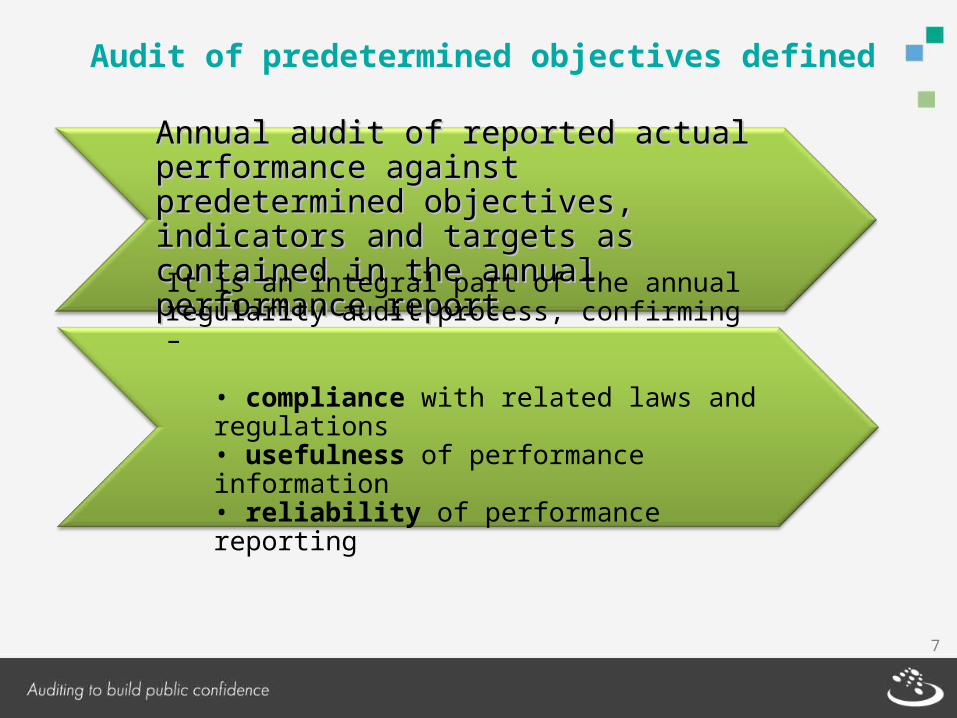

Annual audit of reported actual performance Annual audit of reported actual performance against predetermined objectives, indicators against predetermined objectives, indicators and targets as contained in the annual and targets as contained in the annual performance report performance report

It is an integral part of the annual regularity audit process, confirming –

• compliance with related laws and regulations• usefulness of performance information• reliability of performance reporting

Audit of predetermined objectives defined

7

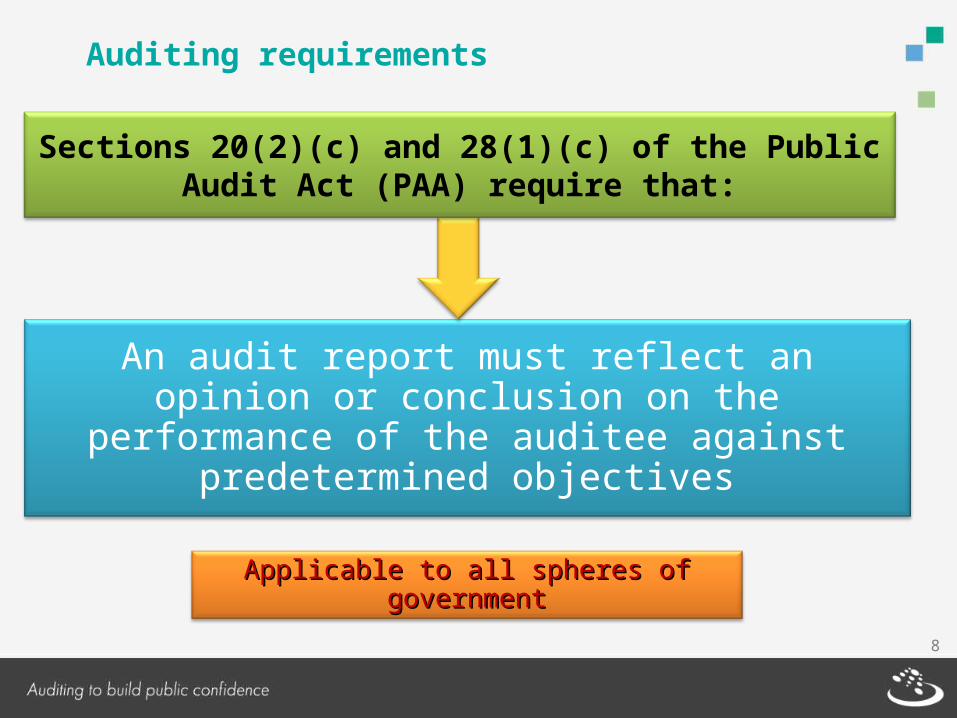

An audit report must reflect an opinion or conclusion on the performance of the auditee against predetermined

objectives

Sections 20(2)(c) and 28(1)(c) of the Public Audit Act (PAA) require that:

Applicable to all spheres of governmentApplicable to all spheres of government

Auditing requirements

8

Legislative requirements and framework for performance management and reporting

9

Public Finance Management Act , 1999 (Act No. 1 of 1999) (PFMA)Public Finance Management Act , 1999 (Act No. 1 of 1999) (PFMA)

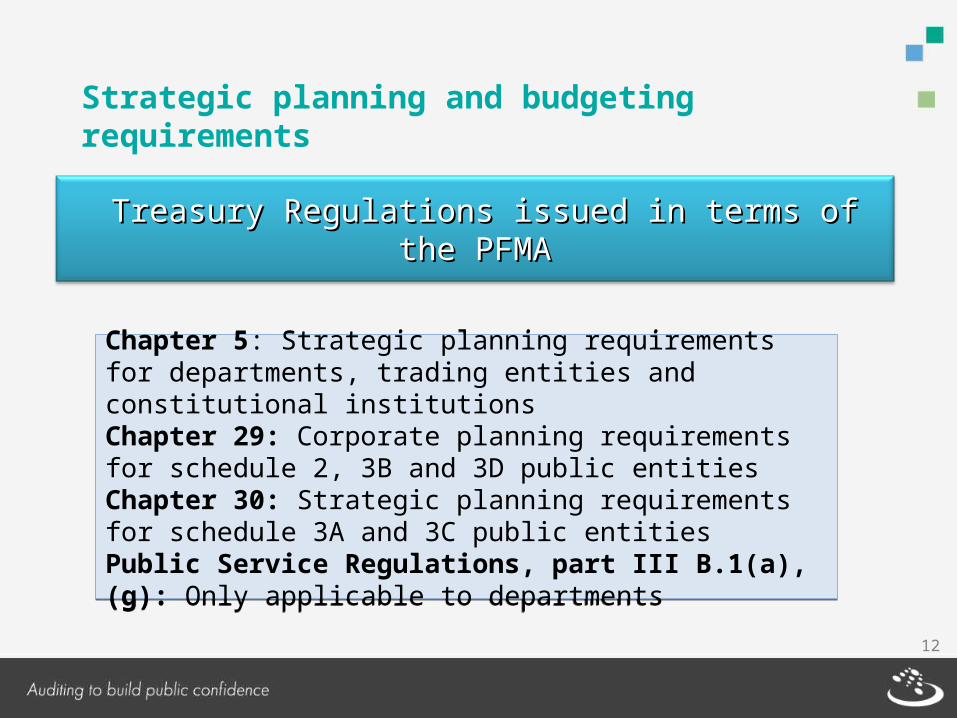

Treasury Regulations issued in terms of the PFMA, 2002Treasury Regulations issued in terms of the PFMA, 2002

National Treasury Framework for managing programme performance information (issued by the National Treasury in May 2007)

National Treasury Framework for managing programme performance information (issued by the National Treasury in May 2007)

This represents the performance management and reporting framework against which the performance information should be managed and reported.

The principles and requirements set out in the framework are used as a basis for the audit.

Guidelines, instruction notes issued by National TreasuryGuidelines, instruction notes issued by National Treasury

National Treasury Framework for strategic plans and annual performance plans(issued by the National Treasury in August 2010)

National Treasury Framework for strategic plans and annual performance plans(issued by the National Treasury in August 2010)

Legislative requirements and framework

10

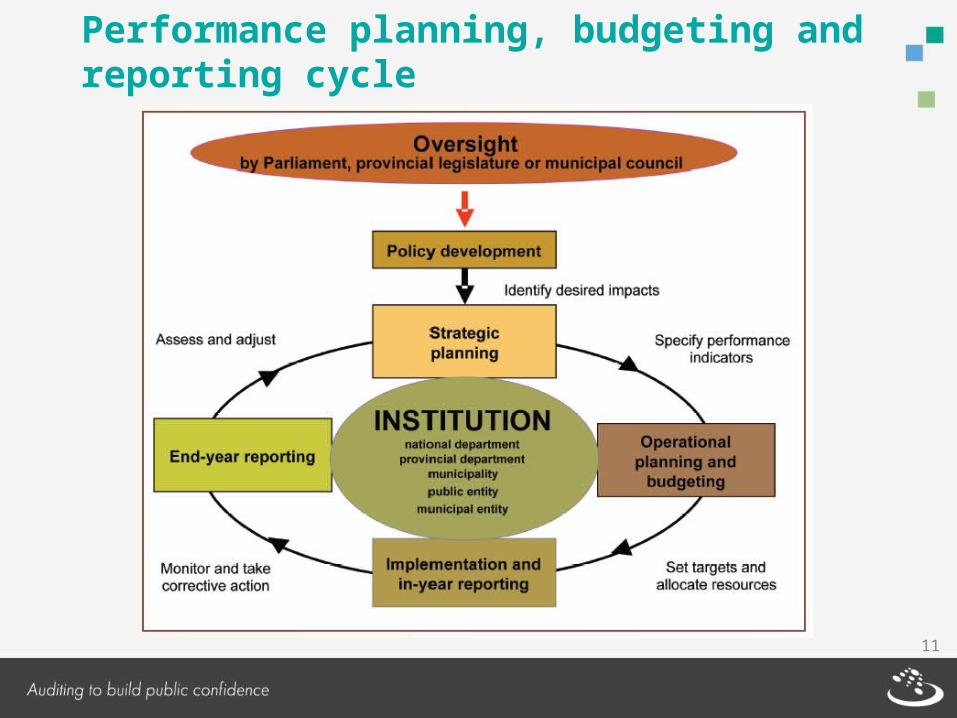

Performance planning, budgeting and reporting cycle

11

Chapter 5: Strategic planning requirements for departments, trading entities and constitutional institutionsChapter 29: Corporate planning requirements for schedule 2, 3B and 3D public entitiesChapter 30: Strategic planning requirements for schedule 3A and 3C public entitiesPublic Service Regulations, part III B.1(a), (g): Only applicable to departments

Chapter 5: Strategic planning requirements for departments, trading entities and constitutional institutionsChapter 29: Corporate planning requirements for schedule 2, 3B and 3D public entitiesChapter 30: Strategic planning requirements for schedule 3A and 3C public entitiesPublic Service Regulations, part III B.1(a), (g): Only applicable to departments

Treasury Regulations issued in terms of the PFMATreasury Regulations issued in terms of the PFMA

Strategic planning and budgeting requirements

12

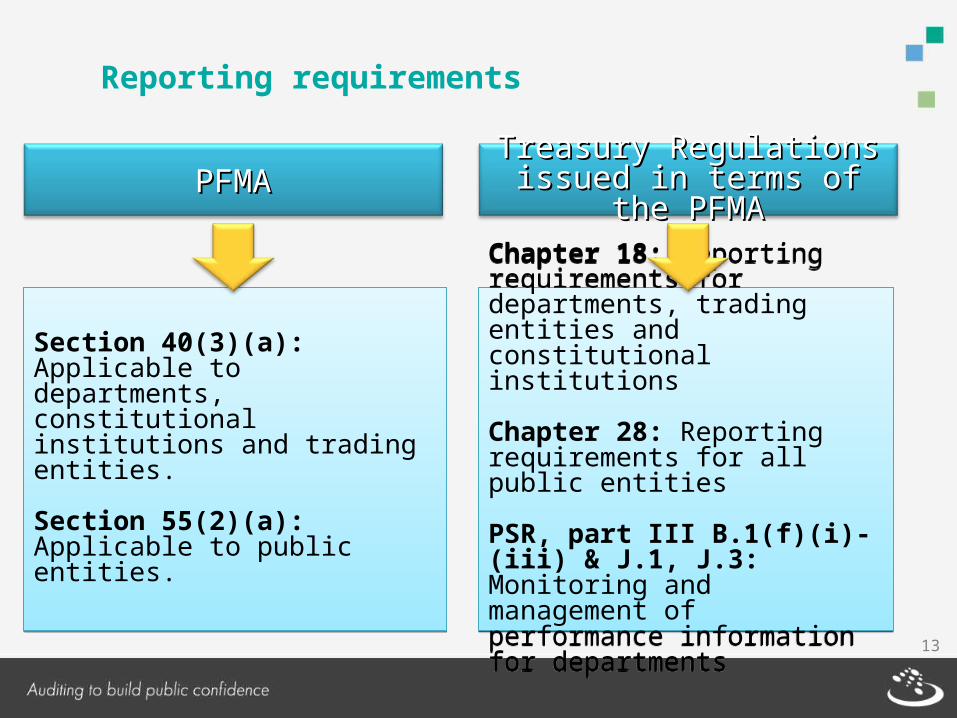

Section 40(3)(a): Applicable to departments, constitutional institutions and trading entities.

Section 55(2)(a): Applicable to public entities.

Section 40(3)(a): Applicable to departments, constitutional institutions and trading entities.

Section 55(2)(a): Applicable to public entities.

PFMAPFMA

Chapter 18: Reporting requirements for departments, trading entities and constitutional institutions

Chapter 28: Reporting requirements for all public entities

PSR, part III B.1(f)(i)-(iii) & J.1, J.3: Monitoring and management of performance information for departments

Chapter 18: Reporting requirements for departments, trading entities and constitutional institutions

Chapter 28: Reporting requirements for all public entities

PSR, part III B.1(f)(i)-(iii) & J.1, J.3: Monitoring and management of performance information for departments

TreasuryTreasury RegulationsRegulations issued in issued in terms of the PFMAterms of the PFMA

Reporting requirements

13

Annual performance report submission

All departments, constitutional institutions, trading entities and public entities must submit the annual performance report for audit purposes with the annual financial statements (by 31 May) to enable the auditors to perform the necessary final audit procedures.

14

Key performance accountability documents

• Consistent structures to facilitate understanding and accountability

• Enable linkage between plans and actual performance

15

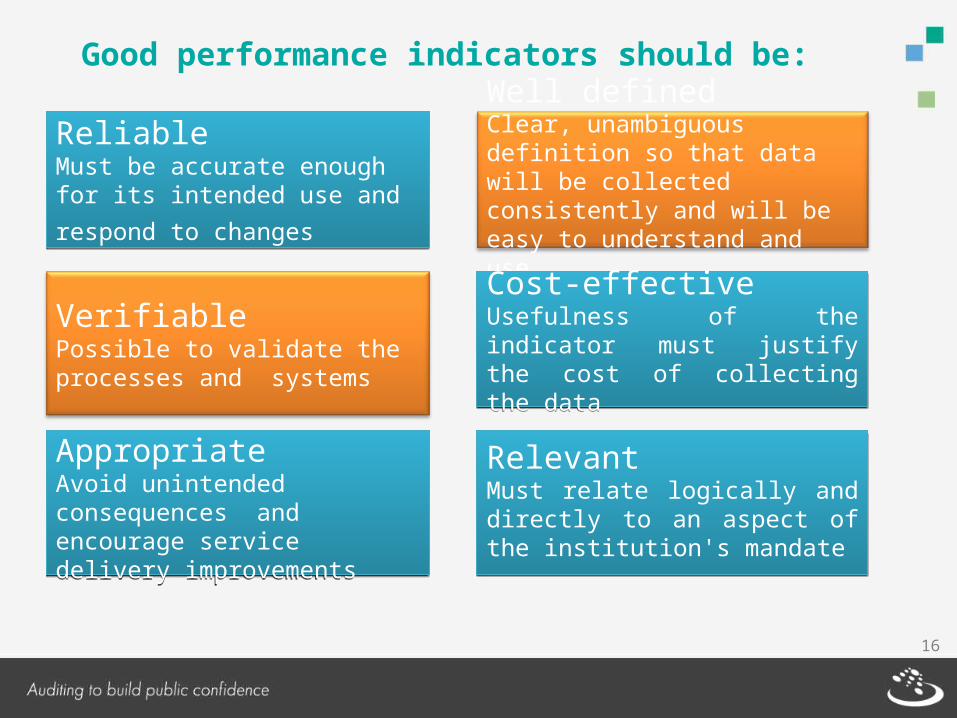

AppropriateAvoid unintended consequences and encourage service delivery improvements

AppropriateAvoid unintended consequences and encourage service delivery improvements

ReliableMust be accurate enough for its intended use and respond to

changes

ReliableMust be accurate enough for its intended use and respond to

changes

RelevantMust relate logically and directly to an aspect of the institution's mandate

RelevantMust relate logically and directly to an aspect of the institution's mandate

Well definedClear, unambiguous definition so that data will be collected consistently and will be easy to understand and use

VerifiablePossible to validate the processes and systems

Cost-effectiveUsefulness of the indicator must justify the cost of collecting the data

Cost-effectiveUsefulness of the indicator must justify the cost of collecting the data

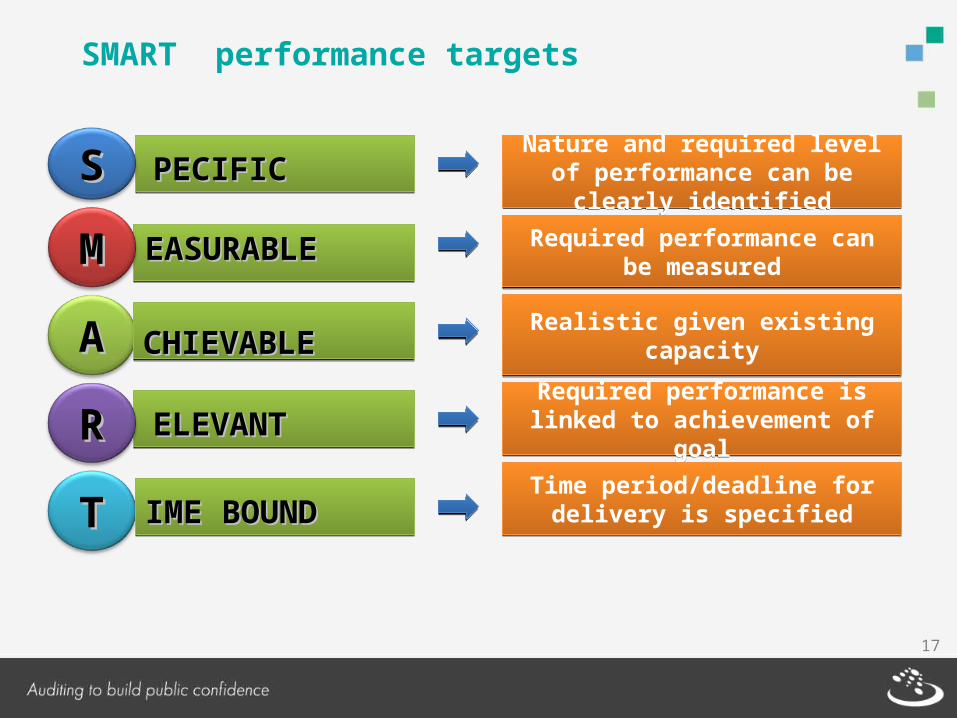

Good performance indicators should be:

16

SMART performance targets

SS

MM

AA

RR

TT

Nature and required level of performance can be clearly identified

Nature and required level of performance can be clearly identified

Required performance can be measured

Required performance can be measured

Realistic given existing capacityRealistic given existing capacity

Required performance is linked to achievement of goal

Required performance is linked to achievement of goal

Time period/deadline for delivery is specified

Time period/deadline for delivery is specified

PECIFICPECIFIC

EASURABLEEASURABLE

ELEVANTELEVANT

CHIEVABLECHIEVABLE

IME BOUNDIME BOUND

17

Audit process

18

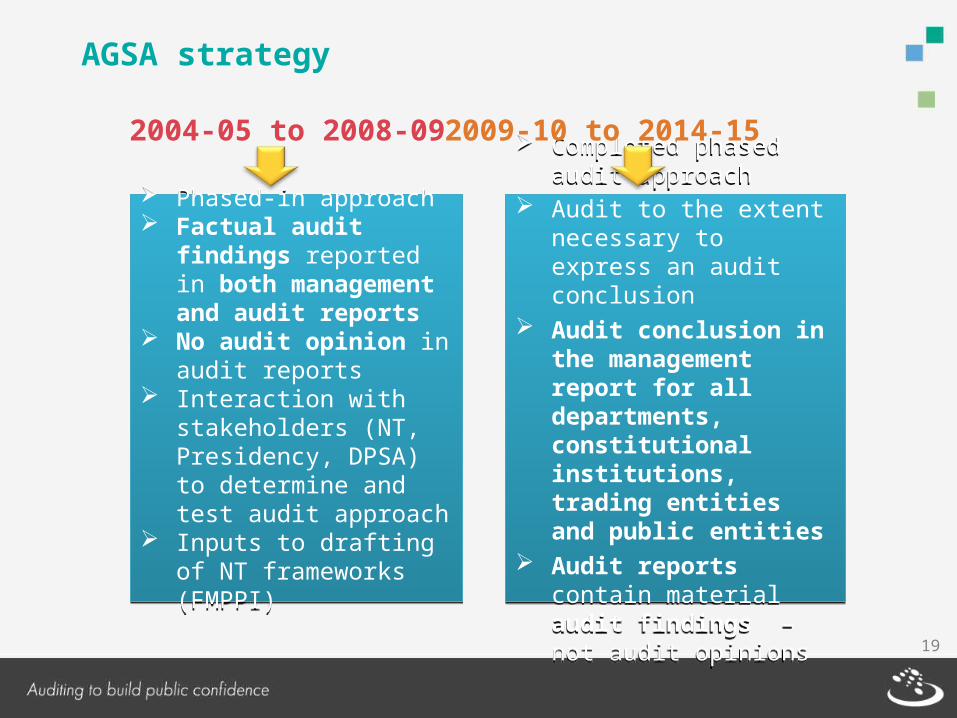

Completed phased audit approach

Audit to the extent necessary to express an audit conclusion

Audit conclusion in the management report for all departments, constitutional institutions, trading entities and public entities

Audit reports contain material audit findings – not audit opinions

Completed phased audit approach

Audit to the extent necessary to express an audit conclusion

Audit conclusion in the management report for all departments, constitutional institutions, trading entities and public entities

Audit reports contain material audit findings – not audit opinions

Phased-in approach Factual audit findings

reported in both management and audit reports

No audit opinion in audit reports

Interaction with stakeholders (NT, Presidency, DPSA) to determine and test audit approach

Inputs to drafting of NT frameworks (FMPPI)

Phased-in approach Factual audit findings

reported in both management and audit reports

No audit opinion in audit reports

Interaction with stakeholders (NT, Presidency, DPSA) to determine and test audit approach

Inputs to drafting of NT frameworks (FMPPI)

2004-05 to 2008-09 2009-10 to 2014-15

AGSA strategy

19

Validity

Accuracy

Completeness

Applicable to performance management and reporting

PresentationMeasurabilityRelevanceConsistency

Compliance with regulatory Compliance with regulatory requirementsrequirements

UsefulnessUsefulness

ReliabilityReliability

Audit criteria

20

Understand and test the design and implementation of the performance management systems, processes and

relevant controls 11

Test the measurability, relevance, presentation and consistency of planned and reported performance information22

Conclude on the reliability of the reported performance for selected programmes or objectives55

Test the reported performance information against relevant source documentation to verify the validity,

accuracy and completeness of reported performance information44

Audit approach

21

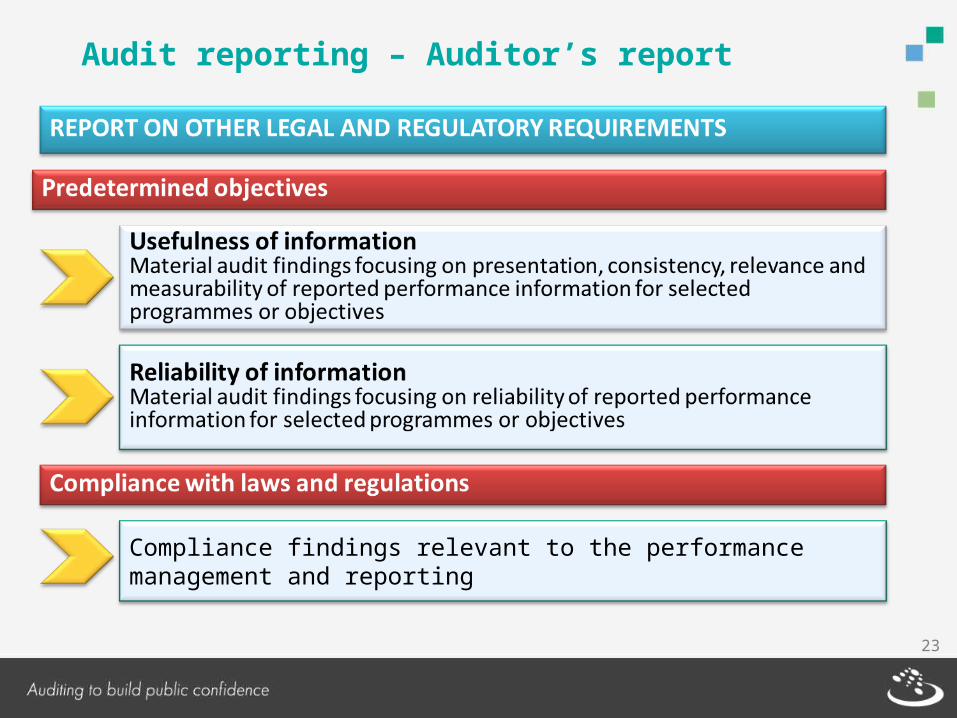

USEFULNESS of reported performance for selected programmes or objectives

RELIABILITY of the reported performance for selected programmes or objectives

Audit reporting – Management report

22

Compliance findings relevant to the performance management and reporting

Audit reporting – Auditor’s report

23

Roles and responsibilities

24

Roles and responsibilities:

Ministers/MECs

Accounting officer or head of an

institution (assisted by chief information

officer)Line managers Other officials

To ensure that institutions under their control set up appropriate performance information systems

Accountable for establishing and maintaining the systems to manage performance information

Accountable for establishing and maintaining the performance information processes and systems within their areas of responsibility

Responsible for capturing, collating and checking performance data relating to their activities

25

Understanding and monitoring of the accounting officer’s mandate are key to improving internal control environment

Role of accounting officer

Robust financial and performance management

systems

Effective, efficient and transparent systems for

•financial and risk management

•internal controls (under control of audit committee)

•procurement and evaluation

• Effective, efficient, economical and transparent use of resources

• Prevention of unauthorised, irregular and fruitless and wasteful expenditure and, if discovered, reporting to treasury

• Efficient and economic management of available working capital

Oversight and accountability

• Manage and safeguard assets and liabilities

• Take appropriate disciplinary steps against any official contravening the PFMA

Commitment and ethical behaviour

Chapter 5 of the Public Finance Management Act, 1999

The role of the accounting officer is critical to ensure:

timely, credible information + accountability + transparency + service delivery

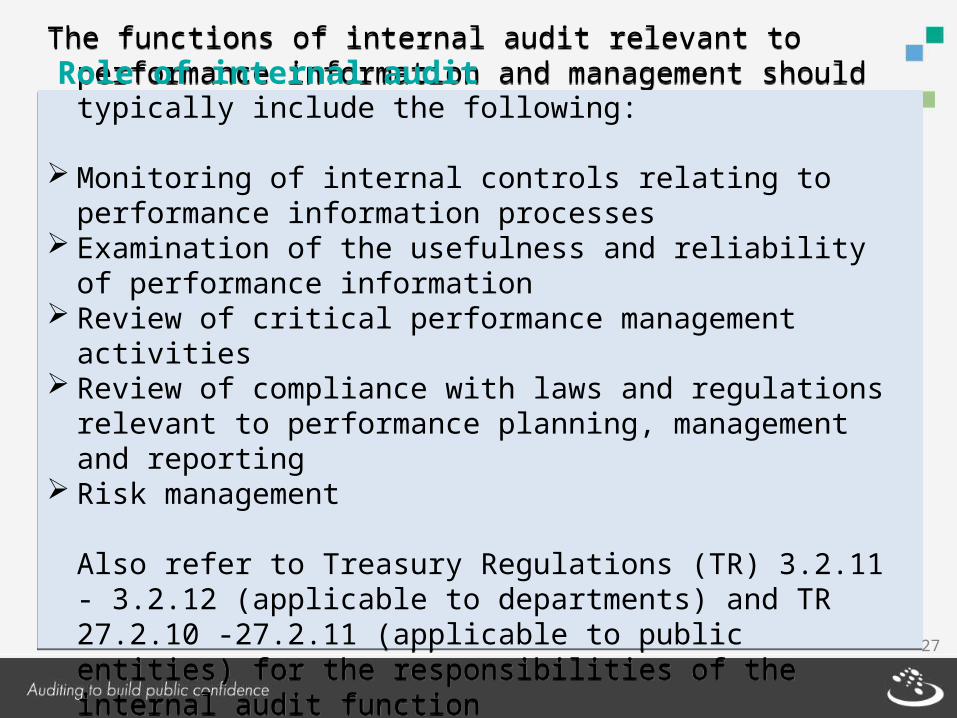

The functions of internal audit relevant to performance information and management should typically include the following:

Monitoring of internal controls relating to performance information processes

Examination of the usefulness and reliability of performance information

Review of critical performance management activities Review of compliance with laws and regulations relevant to

performance planning, management and reporting Risk management

Also refer to Treasury Regulations (TR) 3.2.11 - 3.2.12 (applicable to departments) and TR 27.2.10 -27.2.11 (applicable to public entities) for the responsibilities of the internal audit function

The functions of internal audit relevant to performance information and management should typically include the following:

Monitoring of internal controls relating to performance information processes

Examination of the usefulness and reliability of performance information

Review of critical performance management activities Review of compliance with laws and regulations relevant to

performance planning, management and reporting Risk management

Also refer to Treasury Regulations (TR) 3.2.11 - 3.2.12 (applicable to departments) and TR 27.2.10 -27.2.11 (applicable to public entities) for the responsibilities of the internal audit function

Role of internal audit

27

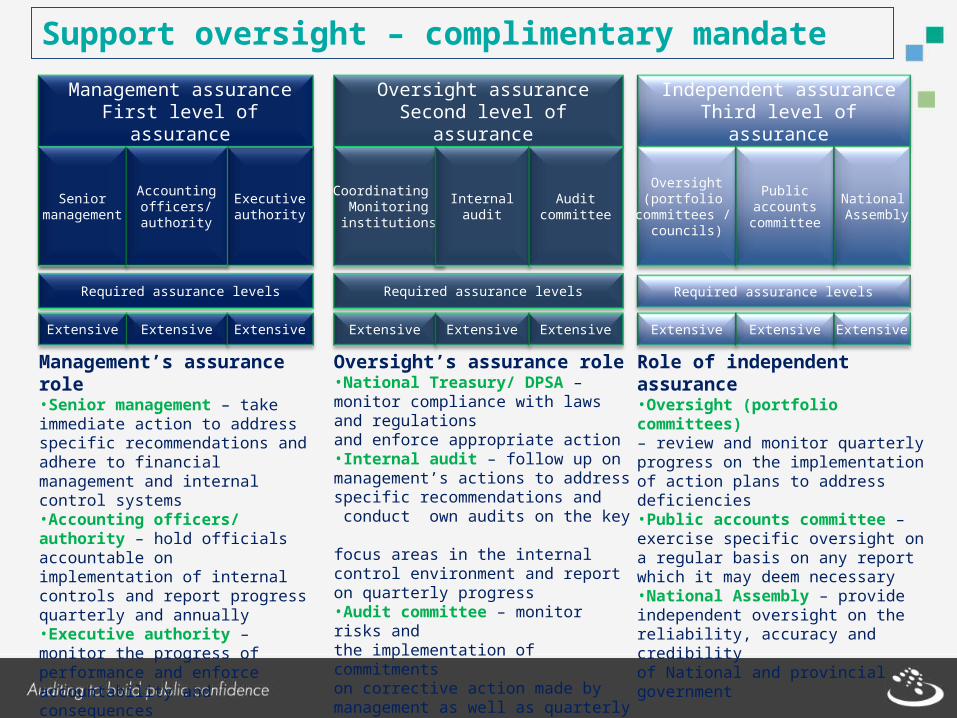

Seniormanagement

Accountingofficers/authority

Executiveauthority

Required assurance levels

Extensive Extensive Extensive

Management’s assurance role•Senior management – take immediate action to address specific recommendations and adhere to financial management and internal control systems•Accounting officers/ authority – hold officials accountable on implementation of internal controls and report progress quarterly and annually•Executive authority – monitor the progress of performance and enforce accountability and consequences

Management assuranceFirst level of assurance

Seniormanagement

Accountingofficers/authority

Support oversight – complimentary mandate

Oversight assuranceSecond level of assurance

Coordinating /Monitoringinstitutions

Internalaudit

Auditcommittee

Extensive Extensive Extensive

Required assurance levels

Oversight’s assurance role•National Treasury/ DPSA – monitor compliance with laws and regulations and enforce appropriate action•Internal audit – follow up on management’s actions to address specific recommendations and conduct own audits on the key focus areas in the internal control environment and report on quarterly progress•Audit committee – monitor risks andthe implementation of commitments on corrective action made by management as well as quarterly progress on the action plans

Independent assuranceThird level of assurance

Oversight(portfolio

committees / councils)

Publicaccounts

committee

National Assembly

Extensive Extensive Extensive

Required assurance levels

Role of independent assurance•Oversight (portfolio committees) – review and monitor quarterly progress on the implementation of action plans to address deficiencies •Public accounts committee – exercise specific oversight on a regular basis on any report which it may deem necessary•National Assembly – provide independent oversight on the reliability, accuracy and credibility of National and provincial government

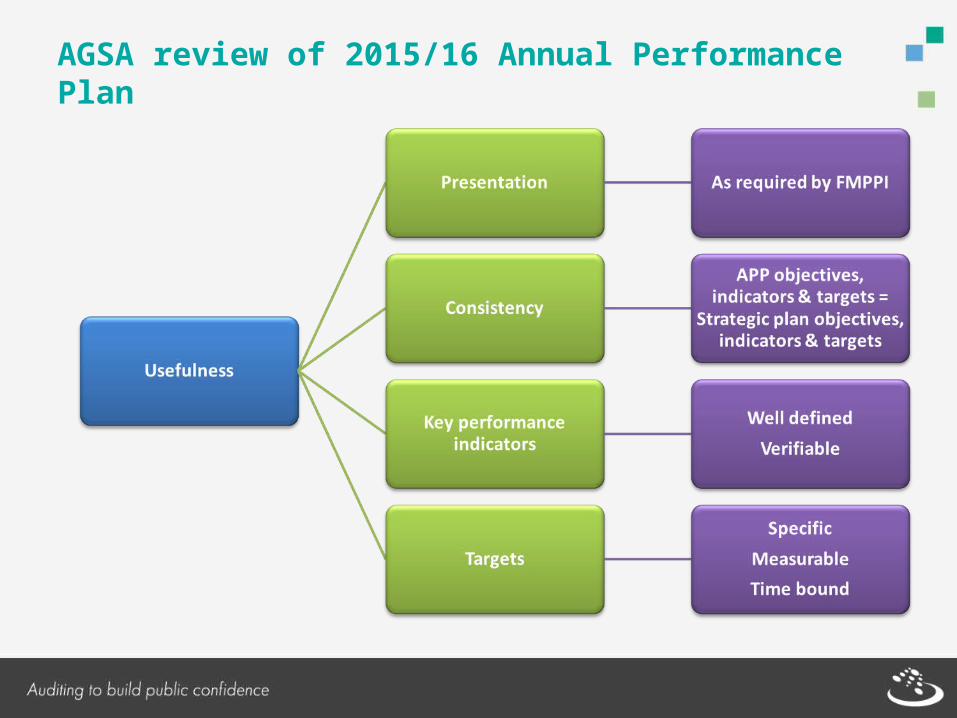

Interim review of 2015/16 Annual Performance Plans

29

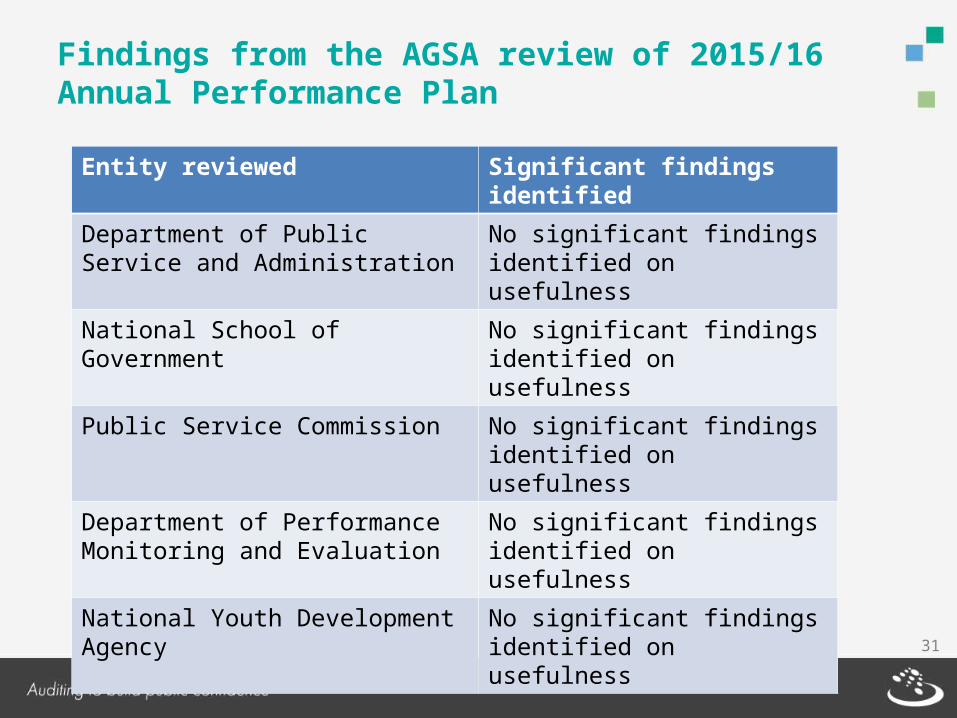

AGSA review of 2015/16 Annual Performance Plan

31

Entity reviewed Significant findings identified

Department of Public Service and Administration

No significant findings identified on usefulness

National School of Government No significant findings identified on usefulness

Public Service Commission No significant findings identified on usefulness

Department of Performance Monitoring and Evaluation

No significant findings identified on usefulness

National Youth Development Agency No significant findings identified on usefulness

Findings from the AGSA review of 2015/16 Annual Performance Plan

32

Oversight responsibility of Portfolio Committee

32

33

End-year reporting

Strategic Planning

Implementation and in-year reporting

Operational planning and

budgeting

Policy development

INSTITUTIONNational department

Provincial departmentMunicipalityPublic entity

Municipal entity

OVERSIGHT:Parliament, provincial legislature or municipal council

Oversight model

Accountability

34

Role of Portfolio Committees (Rule 201)

Oversight component - Portfolio committee mandate

Considerations for Portfolio Committees when dealing with performance monitoring

Portfolio Committee

should track any changes to the

APP

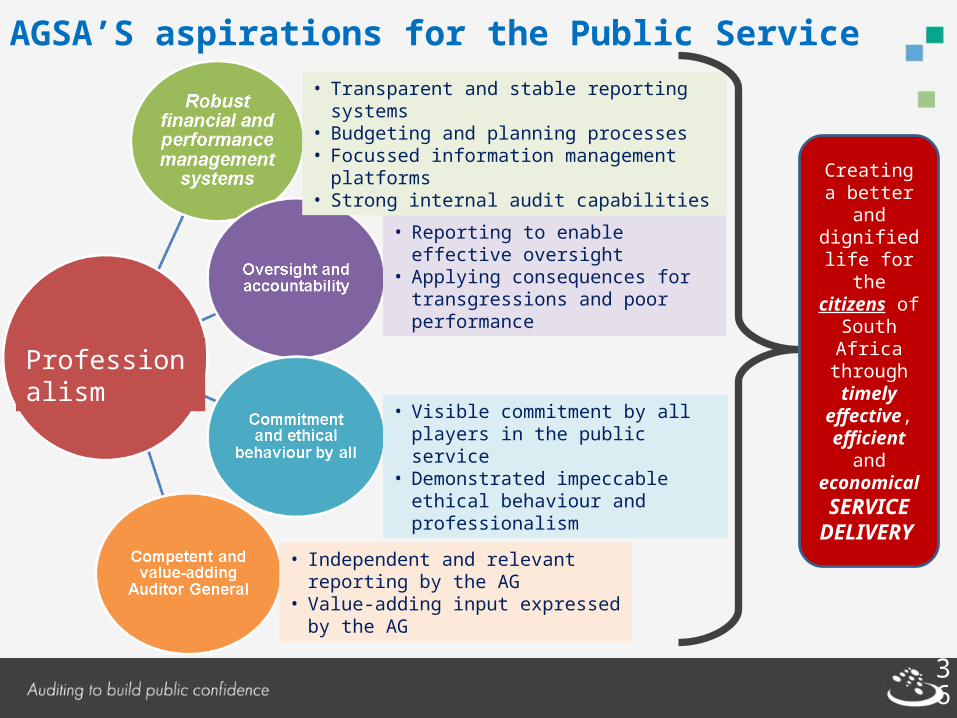

• Transparent and stable reporting systems• Budgeting and planning processes• Focussed information management platforms• Strong internal audit capabilities

• Reporting to enable effective oversight

• Applying consequences for transgressions and poor performance

• Visible commitment by all players in the public service

• Demonstrated impeccable ethical behaviour and professionalism

• Independent and relevant reporting by the AG

• Value-adding input expressed by the AG

Professionalism

Creating a better and

dignified life for the

citizens of South Africa

through timely

effective, efficient

and economical SERVICE DELIVER

Y

AGSA’S aspirations for the Public Service

36

Questions

37