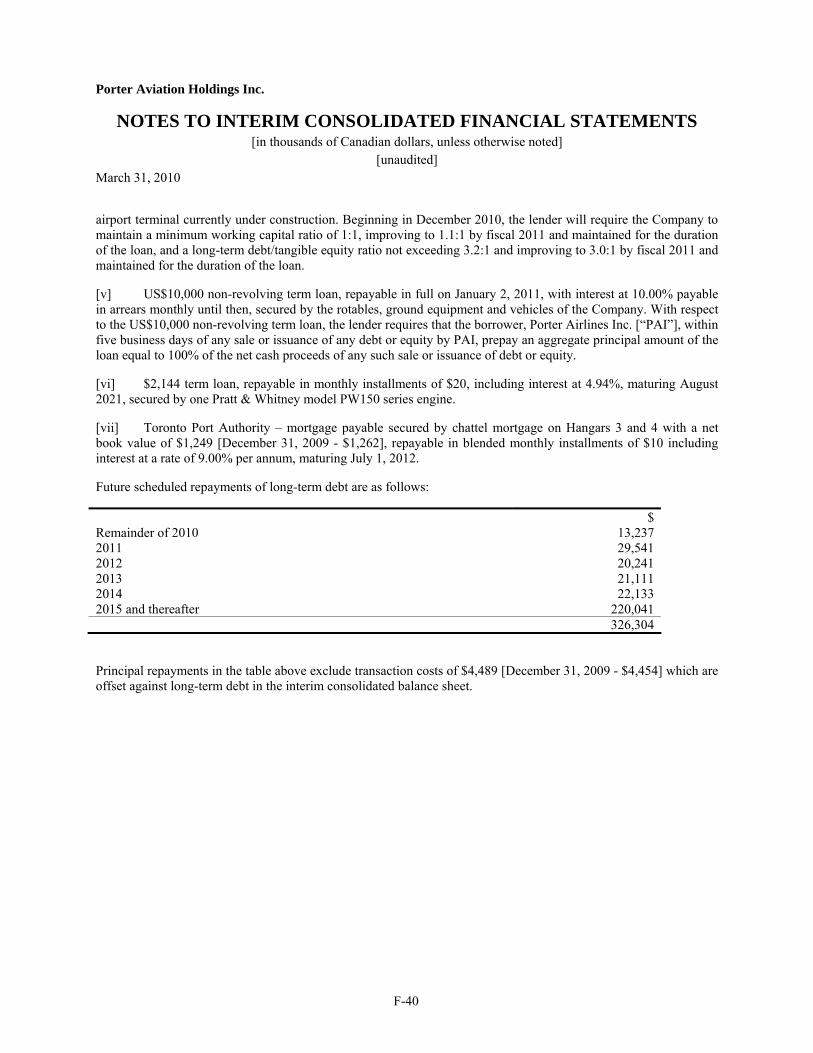

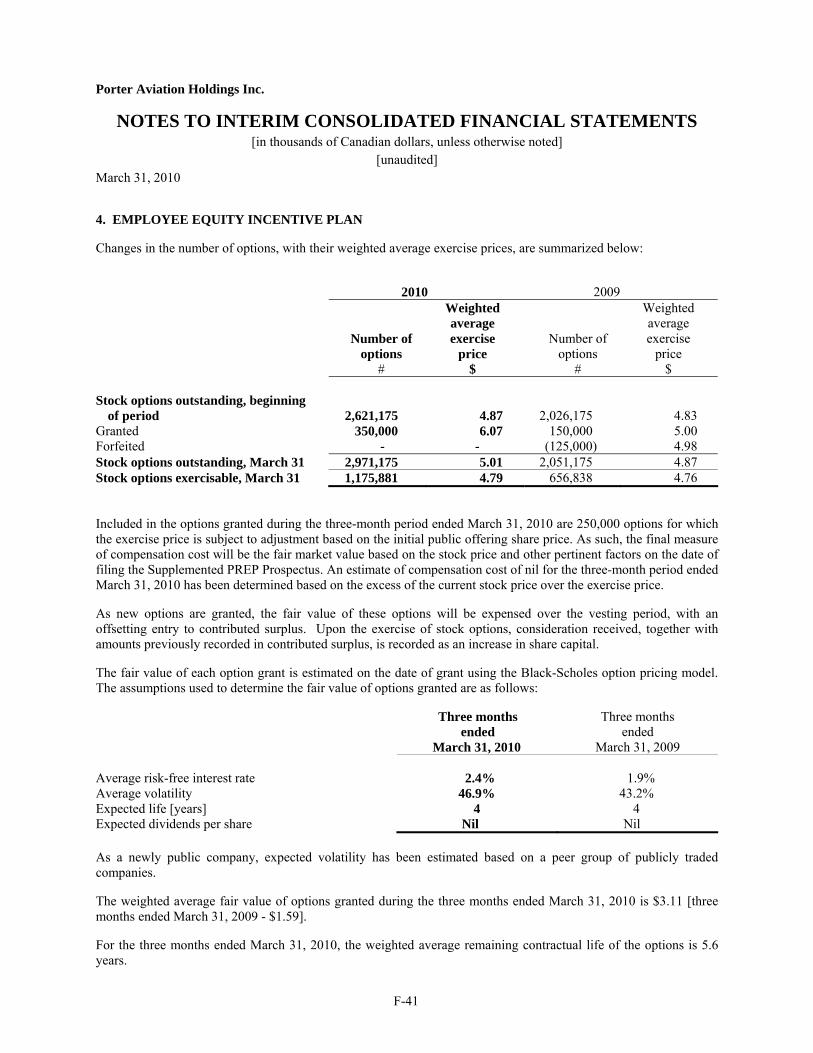

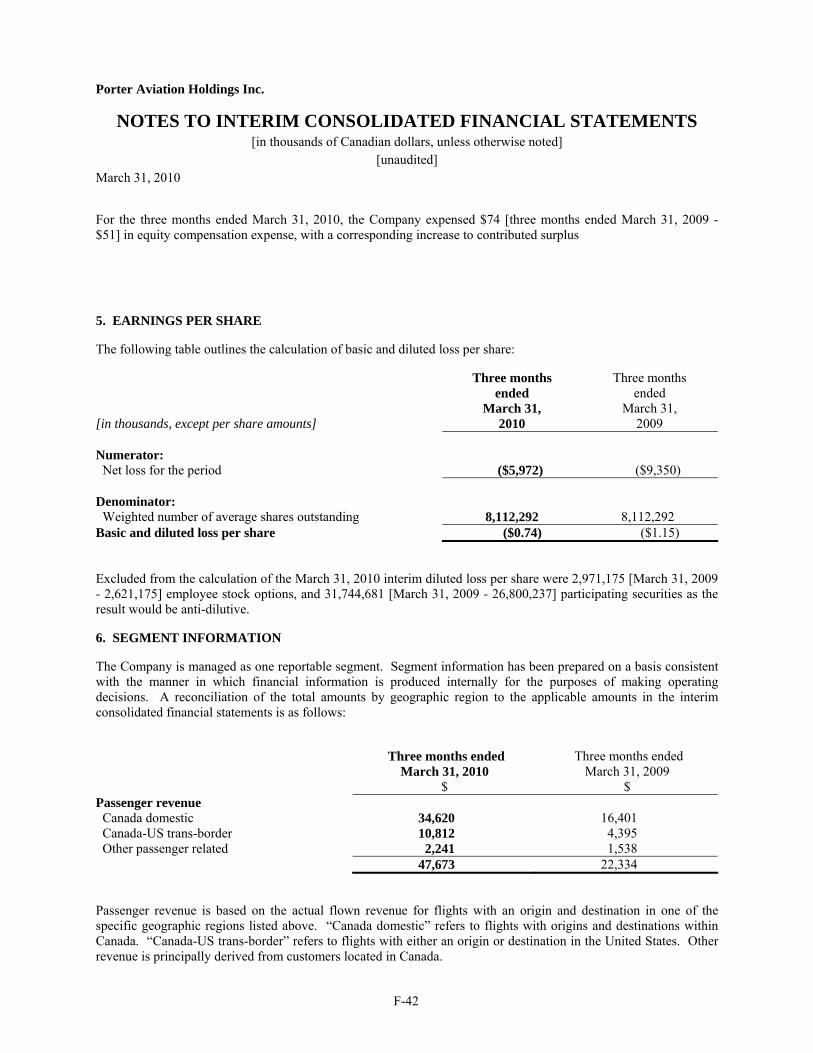

Embed Size (px)

Citation preview

No securities regulatory authority has expressed an opinion about these securities and it is an offence to claim otherwise. This prospectus constitutes a public offering of these securities only inthose jurisdictions where they may be lawfully offered for sale and therein only by persons permitted to sell such securities.This prospectus has been filed under procedures in each of the provinces and territories of Canada that permit certain information about these securities to be determined after the prospectushas become final and that permit the omission of that information from this prospectus. The procedures require the delivery to purchasers of a supplemented PREP prospectus containing theomitted information within a specified period of time after agreeing to purchase any of these securities. All of the information contained in the supplemented PREP prospectus that is notcontained in this base PREP prospectus will be incorporated by reference into this base PREP prospectus as of the date of the supplemented PREP prospectus.These securities have not been and will not be registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act”) or any state securities legislation and may not beoffered or sold in the United States except pursuant to an exemption from the registration requirements of the U.S. Securities Act and applicable state securities legislation. This prospectus does notconstitute an offer to sell or a solicitation of an offer to buy any of the securities offered hereby within the United States. See “Plan of Distribution”.

BASE PREP PROSPECTUSInitial Public Offering May 21, 2010

PORTER AVIATION HOLDINGS INC.$120,000,000

k Common Voting Shares andVariable Voting Shares

(depending on the residency of the purchaser)This prospectus qualifies the distribution (the “Offering”) of an aggregate of k common voting shares (the “Common Voting Shares”) and variable voting shares (the “Variable VotingShares” and, together with the Common Voting Shares, the “Offered Shares”) of Porter Aviation Holdings Inc. (“we”, “us”, the “Corporation” or “Porter”) at a price of $ k per Offered Share(the “Offering Price”). The Offered Shares are being offered by RBC Dominion Securities Inc., National Bank Financial Inc., BMO Nesbitt Burns Inc., CIBC World Markets Inc., TD SecuritiesInc., GMP Securities L.P., Credit Suisse Securities (Canada) Inc., Raymond James Ltd. and Versant Partners Inc. (collectively, the “Underwriters”). Purchasers of Offered Shares who areQualified Canadians (as defined herein) will receive Common Voting Shares and purchasers of Offered Shares who are not Qualified Canadians will receive Variable Voting Shares.

There is currently no market through which the Offered Shares may be sold and purchasers may not be able to resell the Offered Shares purchased under this prospectus. This mayaffect the pricing of the Offered Shares in the secondary market, the transparency and availability of trading prices, the liquidity of the Offered Shares, and the extent of issuerregulation. An investment in the Offered Shares is subject to a number of risks that should be considered by a prospective purchaser. Investors should carefully consider the risk factorsdescribed under “Risk Factors” before purchasing the Offered Shares. The Toronto Stock Exchange (“TSX”) has conditionally approved the listing of the Offered Shares to be issuedpursuant to the Offering and that may be sold pursuant to the exercise of the Over-Allotment Option (as defined below) under the symbol “ FLY ”, subject to the Corporation fulfilling allthe listing requirements of the TSX on or before August 9, 2010, including distribution of the Offered Shares to a minimum number of public holders.

Price: $ k per Offered Share

Price to the Public(1) Underwriters’ FeeNet Proceeds to

the Corporation(2)

Per Offered Share . . . . . . . . . . . . . . . . . . . . . . . . . . $ k $ k $ k

Total Offering(3) . . . . . . . . . . . . . . . . . . . . . . . . . . . $120,000,000 $ k $ k

(1) The Offering Price has been determined by negotiation between the Corporation and the Underwriters.(2) Before deducting the expenses of the Offering which are estimated to be approximately $ k , which expenses, together with the Underwriters’ fee , will be paid by the Corporation out of the proceeds of the Offering.(3) The Corporation has granted the Underwriters an over-allotment option (the “Over-Allotment Option”), exercisable, in whole or in part, at the sole discretion of the Underwriters, for a period of 30 days from the closing of

the Offering (the “Closing”), to purchase from the Corporation up to an additional k Offered Shares at the Offering Price solely to cover over-allotments, if any, and for market stabilization purposes. TheCorporation will pay the Underwriters’ fee in respect of Offered Shares sold under the Over-Allotment Option if the Over-Allotment Option is exercised. If the Over-Allotment Option is exercised in full, the total “Price tothe Public”, “Underwriters’ Fee” and “Net Proceeds to the Corporation” (before deducting expenses of the Offering) will be $138,000,000, $ k and $ k , respectively. This prospectus qualifies the distributionof the Over-Allotment Option and up to k Offered Shares to be sold by the Corporation upon exercise of the Over-Allotment Option. A purchaser who acquires Offered Shares forming part of the Underwriters’ over-allocation position acquires those shares under this prospectus, regardless of whether the position is ultimately filled through the exercise of the Over-Allotment Option or secondary market purchases. See “Plan ofDistribution”.

The following table sets out the number of Offered Shares that may be issued by the Corporation to the Underwriters pursuant to the Over-Allotment Option:

Maximum Number ofOffered Shares Available Exercise Period Exercise Price

Over-Allotment Option. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Option to acquire upto k Offered Shares

Up to 30 daysfollowing Closing

$ k per Offered Share

In connection with the Offering, the Underwriters may over-allot or effect transactions that stabilize or maintain the market price of the Offered Shares at levels other than those which otherwisemight prevail on the open market. See “Plan of Distribution”.

The Underwriters, as principals, conditionally offer the Offered Shares, subject to prior sale, if, as and when issued by the Corporation and accepted by the Underwriters in accordance with theconditions contained in the underwriting agreement referred to under “Plan of Distribution” and subject to the approval of certain legal matters on behalf of the Corporation by Ogilvy Renault LLPand on behalf of the Underwriters by Torys LLP.

RBC Dominion Securities Inc. and TD Securities Inc., Underwriters with respect to the Offering, are wholly-owned subsidiaries of Canadian chartered banks, both of which have madecredit facilities available to Porter. Consequently, Porter may be considered to be a connected issuer of such Underwriters under applicable Canadian securities legislation. See“Relationship Between the Corporation and Certain Underwriters”.In the opinion of Ogilvy Renault LLP, counsel to Porter, and Torys LLP, counsel to the Underwriters, on the basis of applicable legislation in effect on the date hereof, and subject to thequalifications and assumptions discussed under the heading “Eligibility for Investment”, the Common Voting Shares, on Closing, will be qualified investments under the Income Tax Act (Canada)and the regulations thereunder (the “Tax Act”) for trusts governed by registered retirement savings plans, registered retirement income funds, deferred profit sharing plans, registered disabilitysavings plans, registered education savings plans and tax-free savings accounts. See “Eligibility for Investment”.

Subscriptions will be received subject to rejection or allotment in whole or in part and the right is reserved to close the subscription books at any time without notice. It is expected that Closing willoccur on or about k , 2010, or such later date as the Corporation and the Underwriters may agree, but in any event not later than k , 2010. Certificates representing the Offered Sharessold in the Offering will be issued in registered form to CDS Clearing and Depository Services Inc. (“CDS”), or to its nominee, and deposited with CDS on the date of Closing. A purchaser ofOffered Shares will receive only a customer confirmation from the registered dealer from or through which the Offered Shares are purchased. See “Plan of Distribution”.

MYRTLE BEACH

BOSTON

HALIFAX

ST. JOHN’S

MONTRÉAL MONCTON

SUDBURY

THUNDER BAY

CHICAGO

QUÉBEC CITYMONT TREMBLANT

OTTAWA

TORONTO

NEW YORK

USA

CANADA

Seasonal routesItinéraires saisonniers

Announced routesItinéraires annoncés

Current routesItinéraires actuels

3

TABLE OF CONTENTS

Page Page

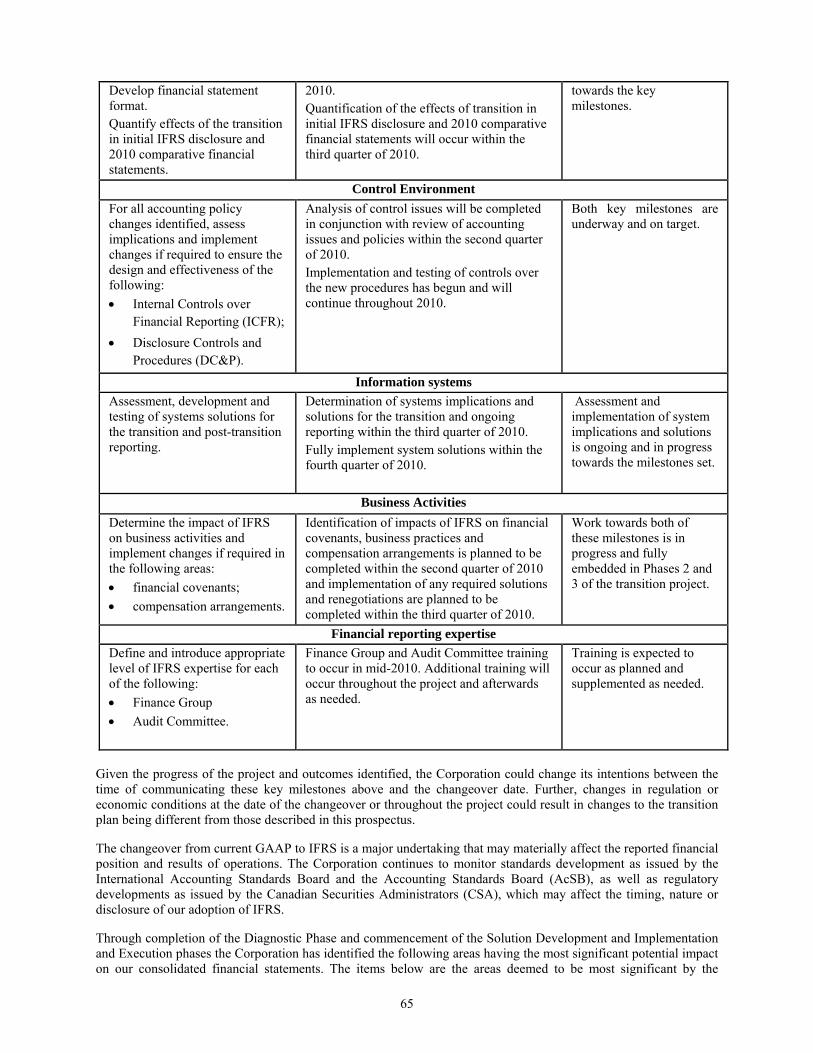

General Matters............................................................................... 4 GAAP and Non-GAAP Measures ................................................... 4 Forward-Looking Statements .......................................................... 4 Market Data and Industry Forecasts................................................ 5 Trademarks, Trade Names and Service Marks................................ 5 Prospectus Summary....................................................................... 6 Corporate Structure ....................................................................... 14

Name, Address and Incorporation............................................ 14 Intercorporate Relationships .................................................... 14

Business of the Corporation .......................................................... 15 Industry Overview.................................................................... 15 Passenger Traffic Through Toronto ......................................... 18 Company Overview ................................................................. 19 Key Measures of Operating and Financial Performance .......... 21 Business Strategy ..................................................................... 25 Growth Strategy ....................................................................... 28 Current and Planned Aircraft Fleet........................................... 32 BBTCA .................................................................................... 32 Fare Offering............................................................................ 35 Operations................................................................................ 35 Sales and Distribution .............................................................. 36 Marketing and Communications .............................................. 37 Trademarks .............................................................................. 37 Employee and Labour Relations .............................................. 37 Safety Management System..................................................... 37 Corporate Social Responsibility ............................................... 38

Regulatory Environment ............................................................... 38 Domestic .................................................................................. 38

Use of Proceeds............................................................................. 40 Selected Consolidated Financial and Operational Information ................................................................................... 40 Management Discussion and Analysis .......................................... 42

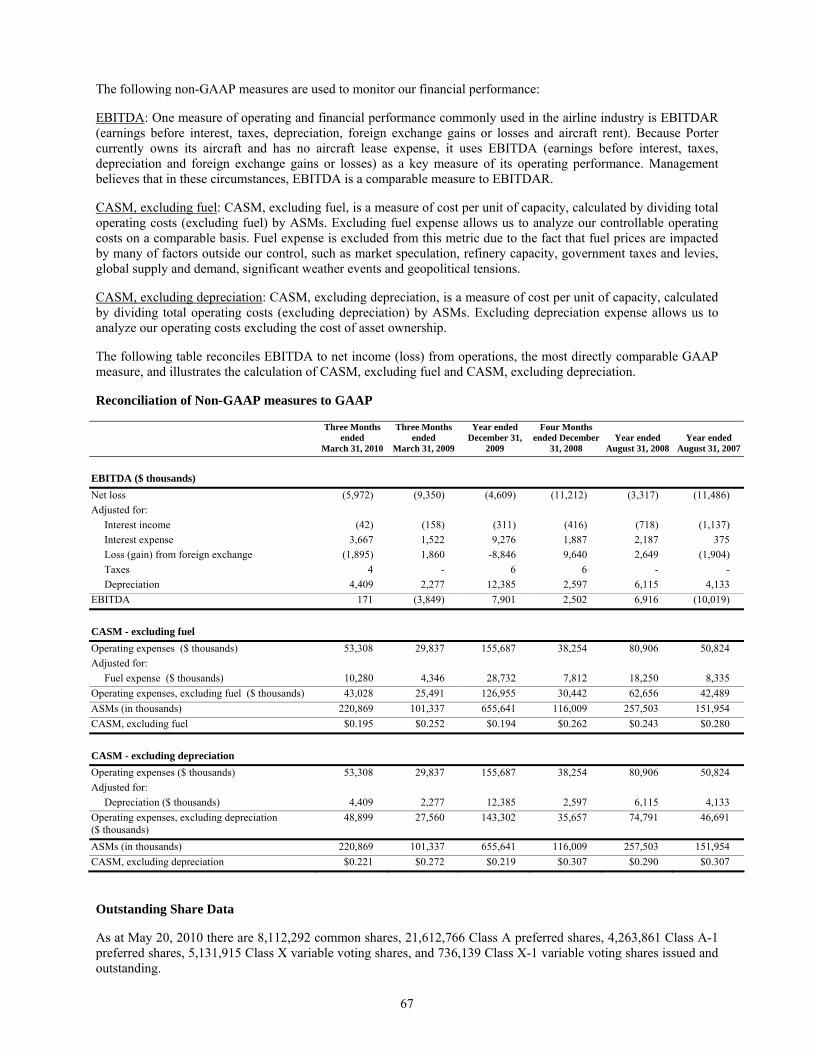

Basis of Presentation ................................................................ 42 Overview.................................................................................. 42 Results of Operations ............................................................... 44 Liquidity and Capital Resources .............................................. 54 Contractual Obligations and Off-Balance Sheet Arrangements........................................................................... 56 Debt Financing......................................................................... 57 Related Party Transactions....................................................... 60 Financial Instruments and Risk Management........................... 60 Critical Accounting Estimates.................................................. 62 Changes in Accounting Policies............................................... 63 Future Changes in Accounting Policies.................................... 63 Conversion to International Financial Reporting Standards ..... 64 Non-GAAP Financial Measures............................................... 66 Reconciliation of Non-GAAP measures to GAAP................... 67 Outstanding Share Data............................................................ 67

Dividend Policy ............................................................................ 68 Pre-Closing Reorganization .......................................................... 68 Description of Securities ............................................................... 68

Common Voting Shares ........................................................... 69 Variable Voting Shares ............................................................ 70 Preferred Shares ....................................................................... 71

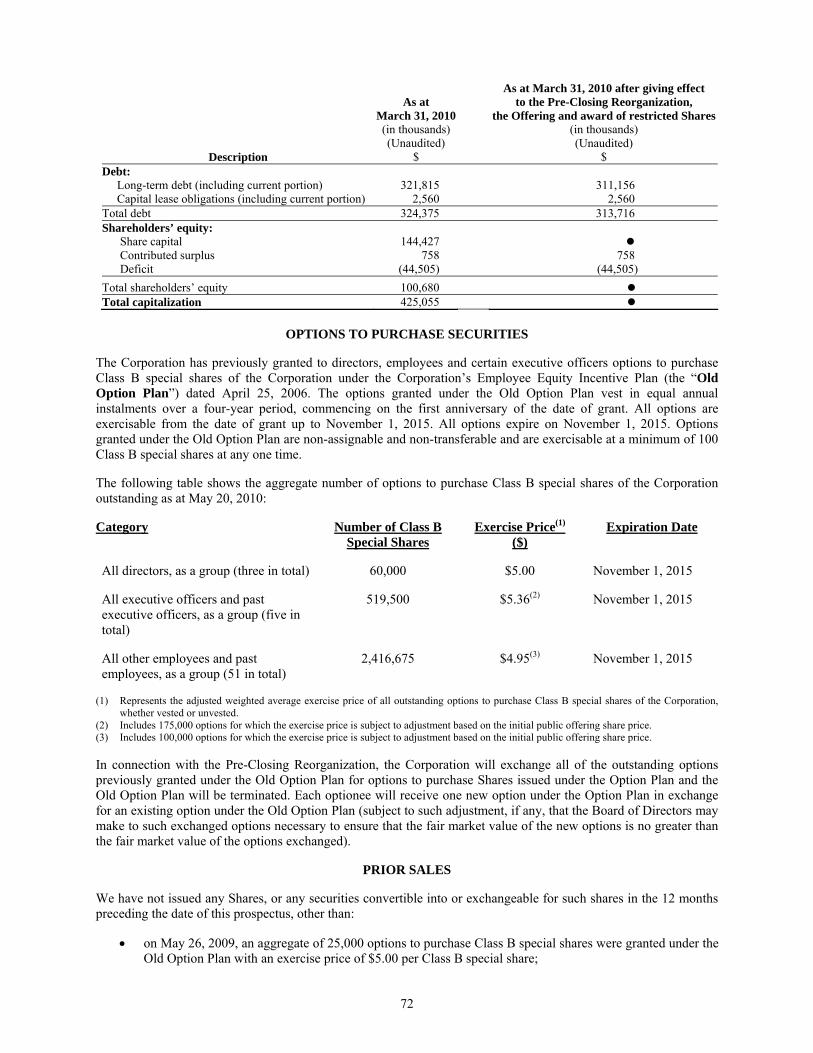

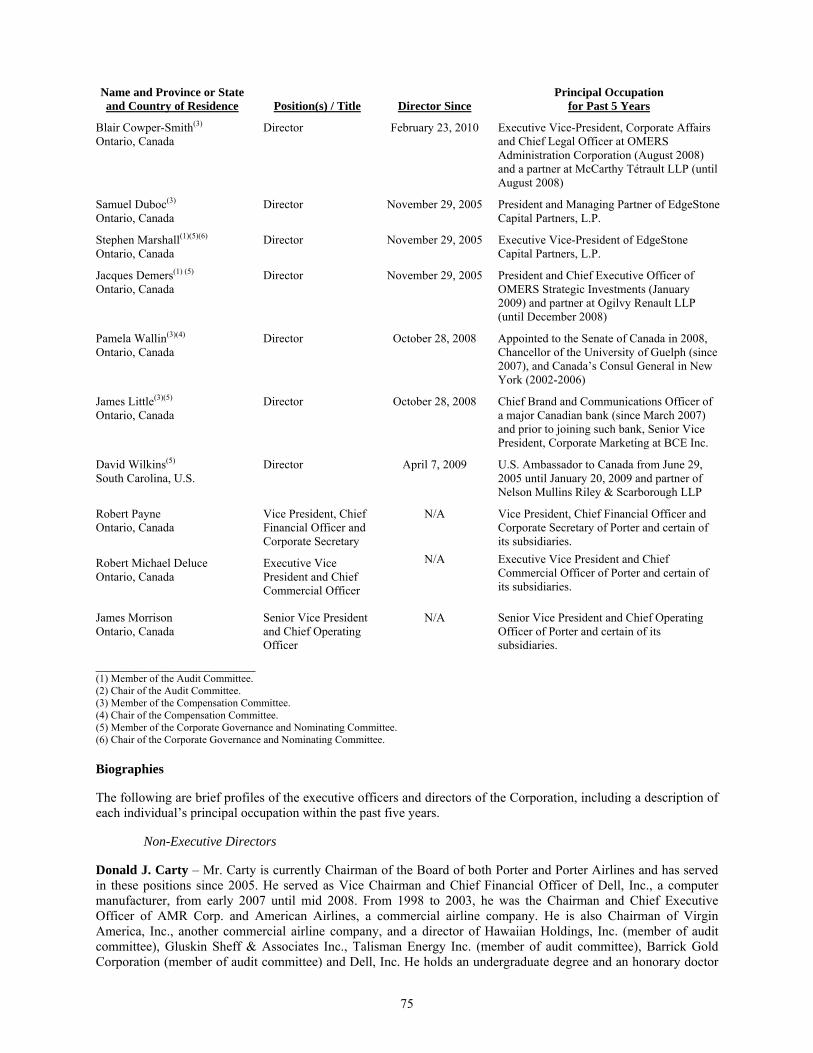

Consolidated Capitalization .......................................................... 71 Options to Purchase Securities ...................................................... 72 Prior Sales ..................................................................................... 72 Trading Price and Volume ............................................................ 73 Principal Shareholders .................................................................. 73 Registration Rights Agreement ..................................................... 74 Directors and Executive Officers .................................................. 74

Directors and Executive Officers ............................................. 74 Biographies .............................................................................. 75 Cease Trade Orders or Bankruptcies........................................ 77 Penalties or Sanctions .............................................................. 78 Conflicts of Interest.................................................................. 78 Indemnification and Insurance................................................. 78

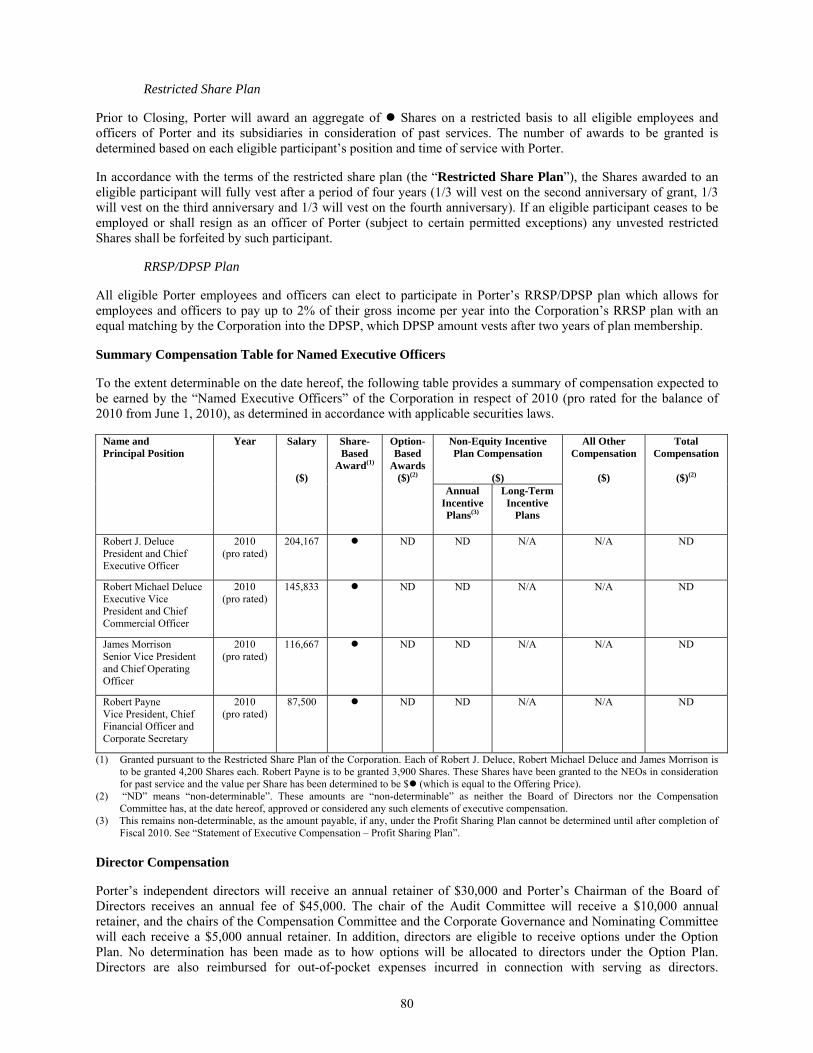

Statement of Executive Compensation.......................................... 78 Compensation Policy and Objectives....................................... 78 Elements of Compensation ...................................................... 78 Summary Compensation Table for Named Executive Officers .................................................................................... 80 Director Compensation ............................................................ 80

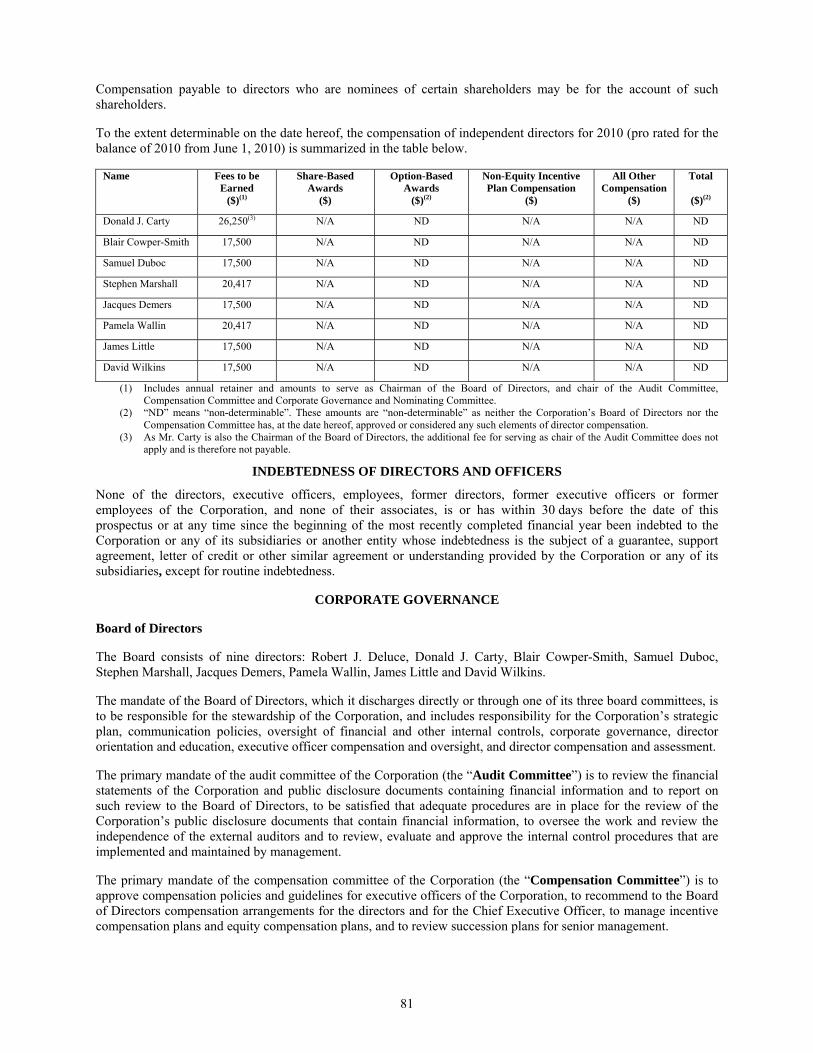

Indebtedness of Directors and Officers ......................................... 81 Corporate Governance .................................................................. 81

Board of Directors.................................................................... 81 Ethical Business Conduct......................................................... 82 Nomination and Assessment of Directors ................................ 83 Compensation Committee........................................................ 83 Audit Committee...................................................................... 83

Plan of Distribution....................................................................... 84 Over-Allotment Option ............................................................ 85 Price Stabilization, Short Positions and Passive Market Making..................................................................................... 85 Pricing of the Offering ............................................................. 86 Lock-Up................................................................................... 86 Fees and Expenses ................................................................... 86 Book Entry System .................................................................. 87

Qualified Canadian Declaration .................................................... 87 Relationship Between the Corporation and Certain Underwriters ................................................................................. 87 Risk Factors .................................................................................. 87

Risks Relating to Porter ........................................................... 88 Risks Relating to the Industry .................................................. 93 Risks Relating to the Offering.................................................. 96

Material Contracts......................................................................... 97 Certain Canadian Federal Income Tax Considerations ................. 98

Residents of Canada................................................................. 98 Non-Resident Holders.............................................................. 99

Eligibility for Investment ............................................................ 100 Interest of Management and Others in Material Transactions................................................................................ 100 Experts ........................................................................................ 100 Legal Proceedings and Regulatory Actions ................................ 101 Auditors, Transfer Agent and Registrar ...................................... 102 Purchasers’ Statutory Rights of Withdrawal and Rescission....... 102 Glossary of Terms....................................................................... 103 Index To Financial Statements.....................................................F-1 Auditors’ Consent ......................................................................F-51 Appendix “A” – Board Mandate................................................. A-1 Appendix “B” – Audit Committee Mandate ............................... B-1 Certificate of the Corporation ..................................................... C-1 Certificate of the Underwriters.................................................... C-2

4

GENERAL MATTERS

Unless otherwise noted or the context otherwise indicates, “Porter”, the “Corporation”, “we”, “us” and “our” refers to Porter Aviation Holdings Inc. together, if the context requires, with one or more of its subsidiaries. Unless otherwise indicated, the disclosure contained in this prospectus (i) assumes that the Over-Allotment Option has not been exercised, (ii) gives effect to the transactions referred to under the heading “Pre-Closing Reorganization”, (iii) includes Shares awarded on a restricted basis pursuant to the Corporation’s Restricted Share Plan, and (iv) excludes Shares reserved for issuance under the Corporation’s Option Plan.

All references to “$” or “dollars” in this prospectus are to Canadian dollars, unless indicated otherwise. Certain totals, subtotals and percentages throughout this prospectus may not reconcile due to rounding.

Words importing the singular number include the plural, and vice versa, and words importing any gender include all genders.

Certain capitalized terms and phrases used in this prospectus are defined in the “Glossary of Terms” beginning on page 103.

GAAP AND NON-GAAP MEASURES

Unless otherwise indicated and as hereinafter provided, all financial statement data in this prospectus has been prepared using Canadian generally accepted accounting principles (“GAAP”). Porter’s consolidated financial statements included in this prospectus have been prepared in accordance with GAAP. This prospectus makes reference to certain non-GAAP measures. These non-GAAP measures are not recognized measures under GAAP, do not have a standardized meaning prescribed by GAAP and are therefore unlikely to be comparable to similar measures presented by other companies. Rather, these measures are provided as additional information to complement those GAAP measures by providing a further understanding of the Corporation’s results of operations from management’s perspective. Accordingly, they should not be considered in isolation nor as a substitute for analysis of our financial information reported under GAAP. See “Selected Consolidated Financial and Operational Information” and “Management Discussion and Analysis – Non-GAAP Financial Measures” for the definition of the non-GAAP measures used and presented in this prospectus and a reconciliation of these non-GAAP measures to the most directly comparable GAAP measures.

FORWARD-LOOKING STATEMENTS

This prospectus contains “forward-looking statements” within the meaning of Canadian legislation, concerning the business, operations and financial performance and condition of Porter. Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or state that certain actions, events or results “may”, “could”, “would”, “might”, “will” or “will be taken”, “occur” or “be achieved”. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made, and they are subject to known and unknown risks, uncertainties, assumptions and other factors that may cause the actual results, level of activity, performance or achievements of Porter to be materially different from those expressed or implied by such forward-looking statements, including but not limited to assumptions discussed in “Business of the Corporation – Key Measures of Operating and Financial Performance” and the following factors described in greater detail in “Risk Factors”: our dependence on Billy Bishop Toronto City Airport, a failure to achieve our growth strategy, price and availability of jet fuel, our ability to obtain financing for additional aircraft, dependence on relations with third parties, dependence on our ability to hire and retain qualified personnel, litigation risks, foreign currency and interest rate fluctuations, our use of a single type of aircraft, limited fleet size, maintenance costs increase as our fleet ages, dependence on technology, significant changes in corporate culture or customer experience, unionization or increased labour costs, limitations due to restrictive covenants, lack of operational history, ability to obtain additional capital, economic conditions, terrorist attacks and security measures, a localized epidemic or global pandemic, major safety incidents, environmental requirements, insurable and uninsurable risks, seasonal nature of the business, competition, government intervention, regulations, rulings and decisions, airport user fees and air navigation fees, external factors such as weather conditions or special events, Shares have no prior public market and the share price may decline after the Offering, volatile market price for Offered Shares, we have no plans to pay dividends, future sale of Shares, influence by existing shareholders, future sales of Shares by our existing shareholders, and discretion in use of proceeds.

5

These factors and assumptions are not intended to represent a complete list of the factors and assumptions that could affect us; however, these factors and assumptions should be considered carefully. Although management of Porter has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. Porter does not undertake to update any forward-looking statements that are contained herein, except in accordance with applicable securities laws.

MARKET DATA AND INDUSTRY FORECASTS

Market data and certain industry forecasts used throughout this prospectus were obtained from internal surveys, market research, publicly available information and independent industry publications. Industry publications generally state that the information contained therein has been obtained from sources believed to be reliable, but the accuracy and the completeness of such information is not guaranteed and neither Porter nor the Underwriters make any representation as to the accuracy of such information. Similarly, internal surveys, industry forecasts, market research and publicly available information while believed to be reliable, have not been independently verified from third party sources and neither Porter nor the Underwriters make any representation as to the accuracy of such information.

TRADEMARKS, TRADE NAMES AND SERVICE MARKS

This prospectus includes trademarks, such as Porter® and VIPorter®, which are protected under applicable intellectual property laws and are the property of Porter. Solely for convenience, our trademarks and trade names referred to in this prospectus may appear without the ® symbol, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks and trade names. Any other trademarks used in this prospectus are the property of their respective owners.

6

PROSPECTUS SUMMARY

The following is a summary of the principal features of the Offering and should be read together with the more detailed information and financial data and statements (including “Risk Factors”) contained elsewhere in this prospectus. Please refer to the “Glossary of Terms” beginning on page 103 of this prospectus for a list of defined terms and phrases used herein.

Company Overview

Porter is a holding company that operates its business through a number of wholly-owned subsidiaries. Porter’s core airline business is operated through Porter Airlines. Porter is Canada’s third largest scheduled airline with an expanding flight network that includes a number of short-haul routes throughout Eastern and Central Canada and the U.S. Porter is focused on quality-conscious passengers who travel during the week primarily for business and on the weekend for leisure.

Porter launched its airline on October 23, 2006 with a fleet of two aircraft offering round-trip flights between Toronto and Ottawa. As of April 30, 2010, Porter operates a fleet of 20 aircraft with service to 12 North American destinations: Ottawa, Montreal, Halifax, Thunder Bay, St. John’s, Quebec City, Sudbury and Mont Tremblant in Canada and New York, Chicago, Boston and Myrtle Beach in the U.S.

Business Strengths

Innovative Growth Company in the Airline Business

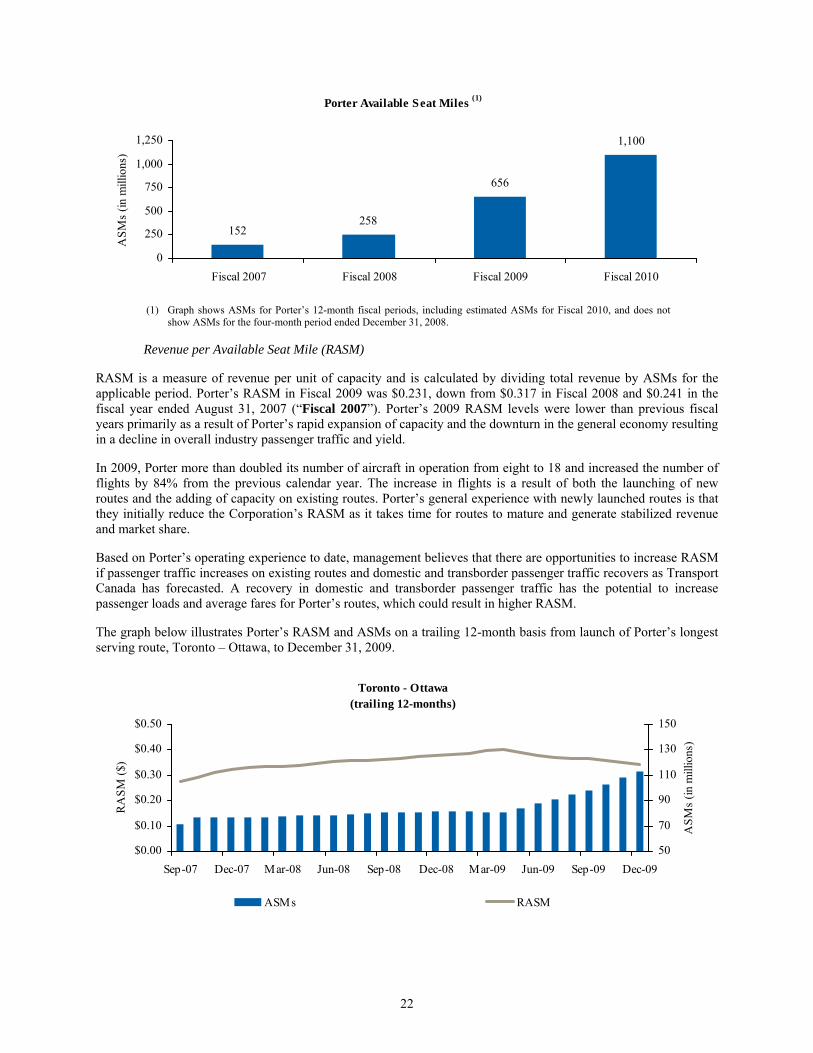

Since its inception, Porter has experienced significant growth. Porter combines a low cost operating structure with a focus on higher yield passengers who value premium service. As a result, Porter has achieved an industry leading breakeven load factor (an airline’s load factor multiplied by total operating expenses divided by total revenue) relative to North American publicly traded airlines. The number of passengers Porter has flown per year has grown significantly from approximately 300,000 in calendar 2007 (first full year of operations) to over 900,000 in calendar 2009 (this number consists of approximately 800,000 passengers flying through BBTCA and the balance flying through Porter’s point-to-point airports). Porter’s capacity, measured in Available Seat Miles (or ASMs), has also grown significantly from approximately 152 million in Fiscal 2007 to an estimated level of 1.1 billion ASMs (based on the current schedule of flights and expected completion rate1 for Fiscal 2010). Porter has also been successful in gaining significant market share on competitive routes such as Toronto – Ottawa and Toronto – Montreal.

Porter’s growth strategy includes expanding its existing network by increasing passenger load factors on existing flights, increasing the number of round trips on existing or announced routes and expanding its short-haul network to include new destinations and additional point-to-point markets in Eastern Canada and the U.S. Additional opportunities for growth include potential code-sharing arrangements with other airlines and access to potential new markets through U.S. customs preclearance, if approved, at Porter’s primary hub airport, BBTCA.

Premium Service Offering

Porter’s premium service offering targets quality-conscious business and leisure travelers. Porter applies a straightforward structure of three classes of fares with differing levels of flexibility. All of Porter’s passengers are offered the same standard of premium in-flight service, including complimentary food and beverage service, complimentary passenger lounge access at BBTCA and Ottawa International Airport and a simplified loyalty program to reward frequent travelers with free airline travel.

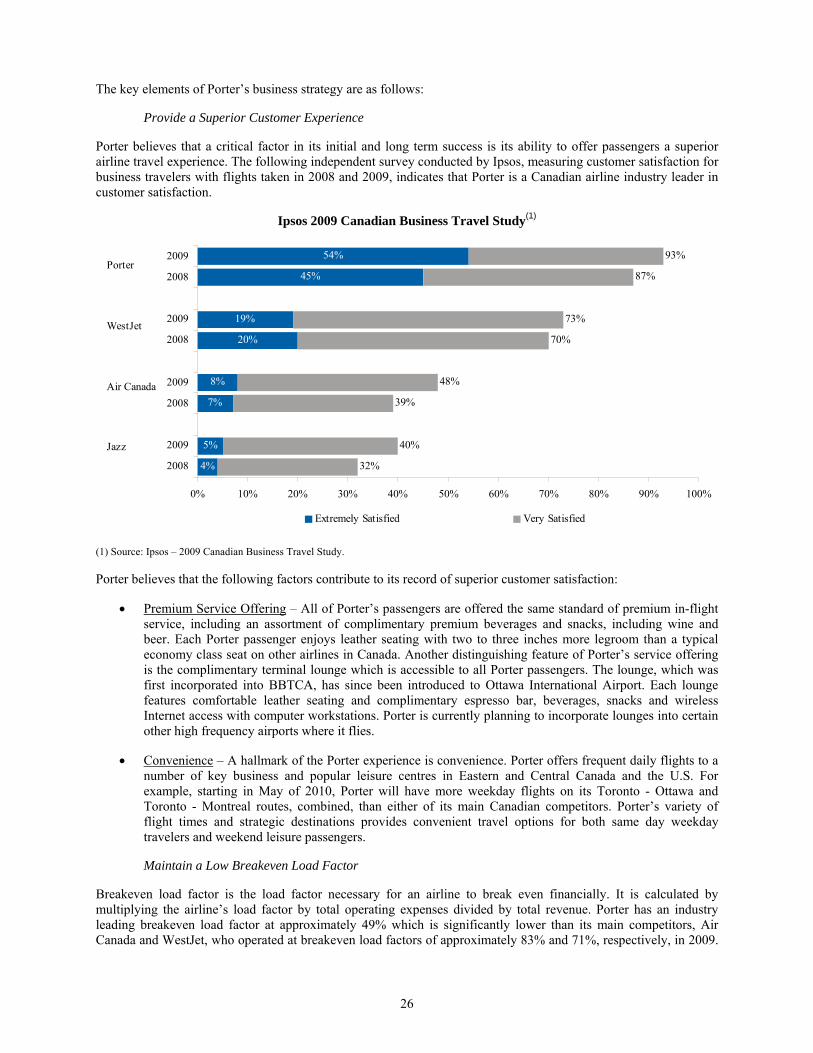

Porter has achieved industry leading customer satisfaction among business travelers, as independently measured by Ipsos, demonstrating Porter’s superior customer service performance.

Integrated, Scalable, Low Cost Platform

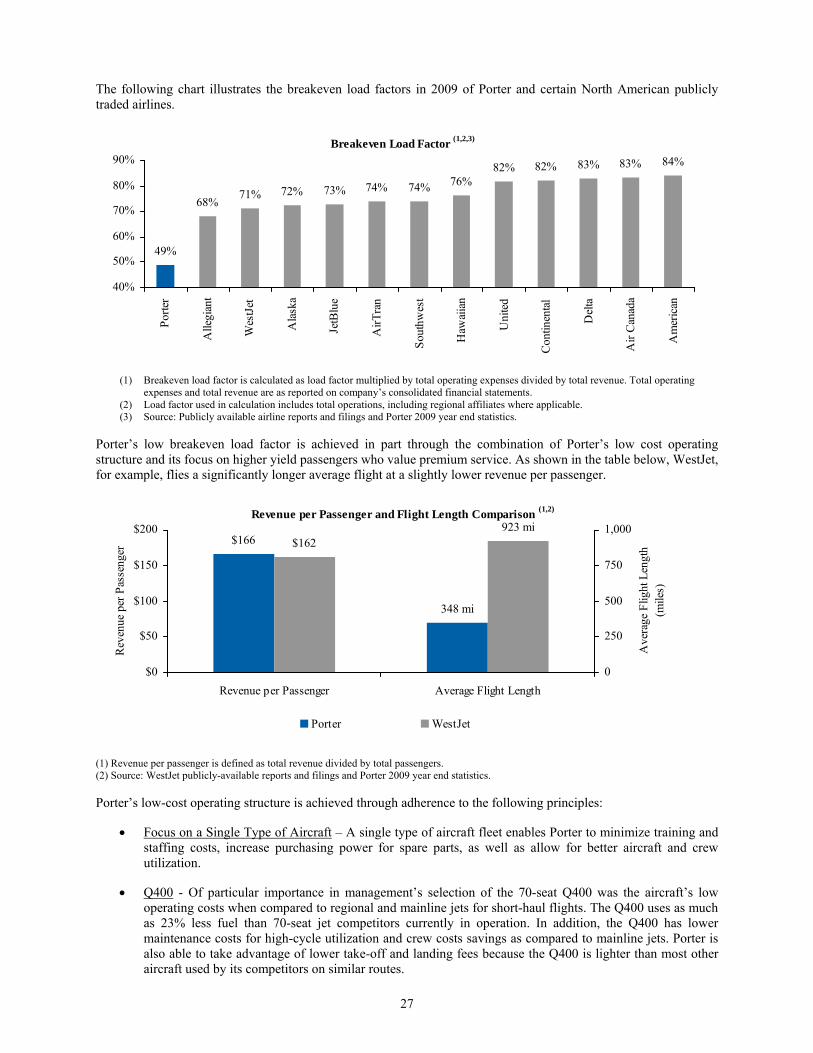

Porter achieves industry leading breakeven load factors (approximately 49% in 2009), significantly below its Canadian competitors WestJet and Air Canada (approximately 71% and 83% in 2009, respectively), and below the successful U.S. carriers Southwest Airlines Co. and JetBlue Airways Corporation (approximately 74% and 73% in 2009, respectively). Porter utilizes a single class of aircraft, the Q400, which helps to control the overall cost of fleet operations and maintenance. As at December 31, 2009, Porter had a non-unionized workforce made up of 847 full-time equivalent employees (“FTE”), with an FTE-to-aircraft ratio of approximately 47 versus WestJet with a ratio 1 Completion rate refers to the number of completed scheduled flights, excluding flights cancelled due to adverse weather conditions, maintenance or other unforeseen factors.

7

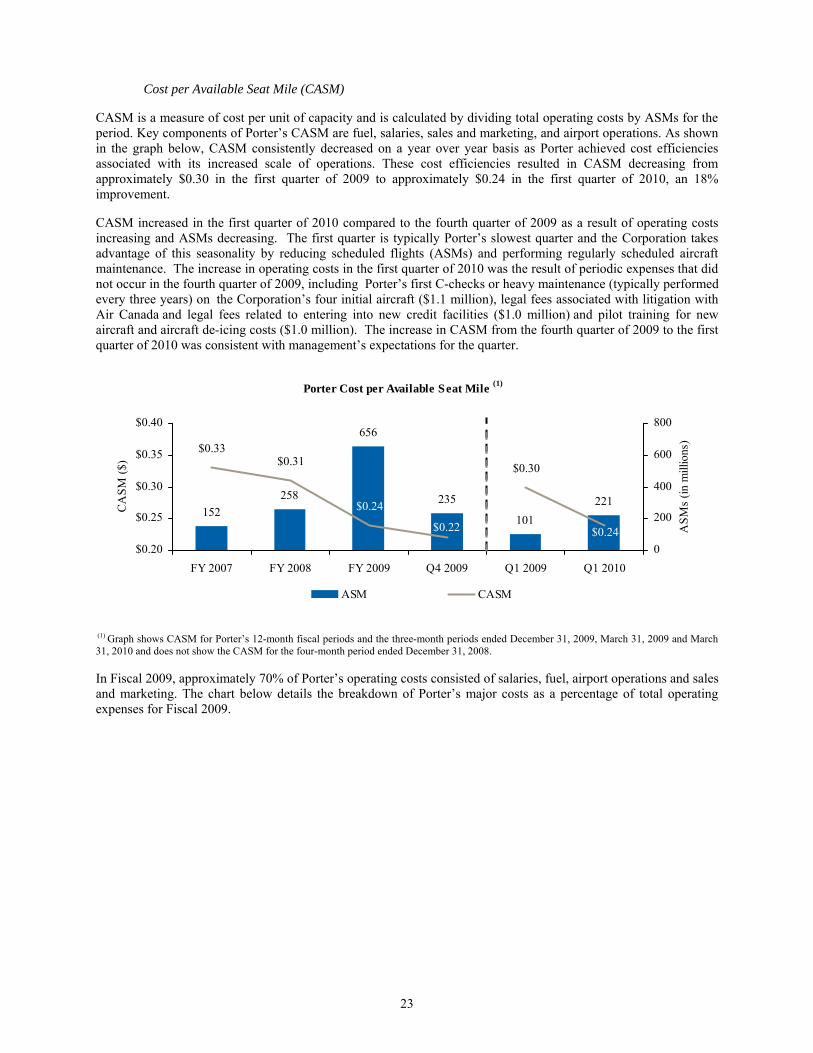

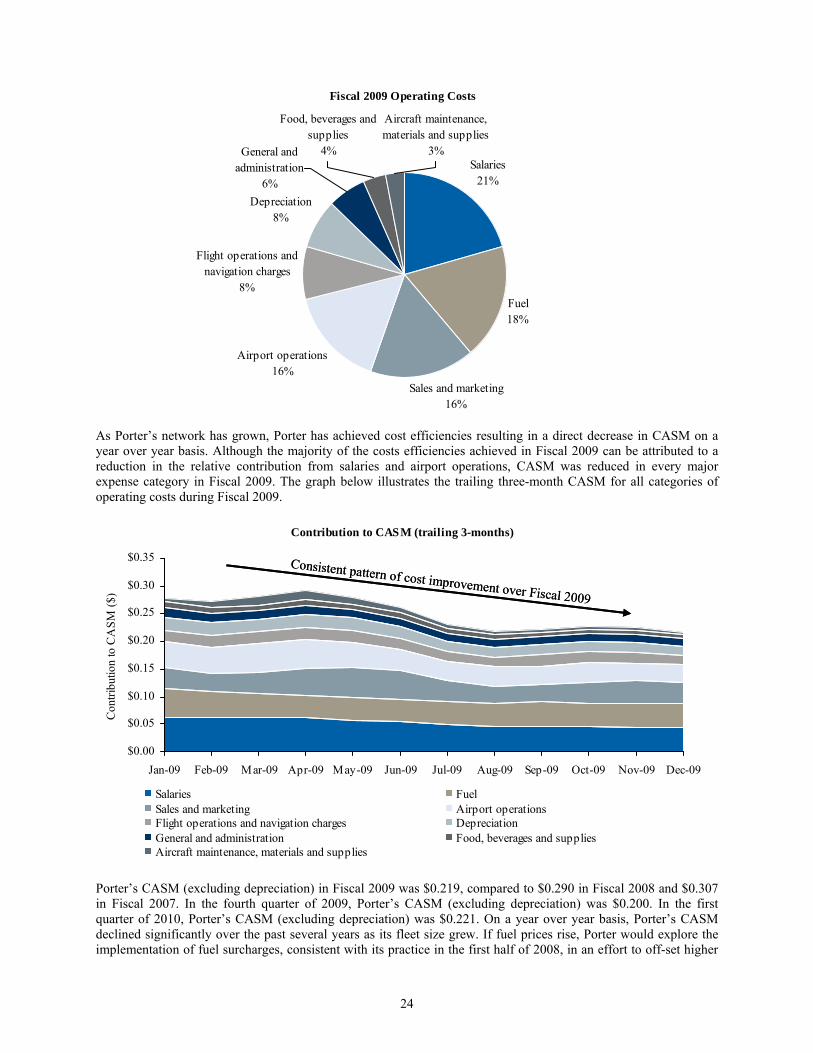

of approximately 73, resulting in lower labour costs relative to certain of its competitors. Porter reduced its Cost per Available Seat Mile (or CASM) by approximately 35% from $0.334 in Fiscal 2007 to $0.217 in the fourth quarter of 2009.

Porter has constructed and operates the new terminal at BBTCA, the first phase of which (comprising approximately 75% of the total development) opened in March 2010. The terminal has been built to accommodate Porter’s long-term growth plans and is part of a vertically integrated infrastructure that, in addition to the terminal, includes operation of four hangers, a corporate flight centre, office space, ramp handling and fuel facilities. The new approximately 150,000 square foot terminal has been designed to accommodate more than two million passengers annually. The remainder of the facility is scheduled to be completed by the end of 2010.

Modern Fleet

Porter operates a fleet of 20 Q400 turboprop aircraft. Over the next 12 months, management expects to acquire up to seven additional aircraft. Any additional acquisitions by Porter will be dependent on a number of factors including Porter’s financial condition, aircraft pricing and availability of financing. All of Porter’s aircraft were new when initially purchased and the average age of Porter’s fleet is less than two years. The Q400 represents state-of–the-art aviation technology and is optimized for short-haul operations. The Q400 is estimated to use as much as 23% less fuel than comparable jet aircraft currently in operation and features a revolutionary noise and vibration suppression system.

Strategic Base of Operations – Downtown Toronto at BBTCA

Porter has a long-term lease, together with operating rights, at BBTCA until 2033. Porter’s primary hub in Toronto is strategically located to serve some of the busiest routes in Canada. Porter’s new approximately $49 million terminal facility at BBTCA provides travelers with reduced travel time, convenience and an enhanced overall customer experience. BBTCA is located approximately three kilometres from the Toronto downtown core and Canada’s primary financial district, compared to Pearson Airport which is approximately 28 kilometres away. With quick check-in and security clearance and a short taxi to the runway, passengers traveling with Porter in or out of downtown Toronto may save up to two hours on a round trip when compared to flying out of Pearson Airport.

Proven Management Team

Porter is led by Robert J. Deluce, an experienced and respected Canadian airline owner and operator who has served in senior management roles in a number of Canadian airlines, including White River Air Services Limited, norOntair, Austin Airways Limited, Air Creebec, Air Ontario Inc., Air Manitoba and Canada 3000 Airlines Limited (which he exited six years prior to it ceasing operations in 2001). Mr. Deluce’s highly experienced team includes James Morrison (Senior Vice President and Chief Operating Officer), Robert Michael Deluce (Executive Vice President and Chief Commercial Officer) and Robert Payne (Chief Financial Officer). The Board of Directors of Porter brings together significant airline, public company and corporate governance experience. The Chairman of the Board, Donald J. Carty, is the Chairman of Virgin America, Inc., the former Chairman and CEO of American Airlines and the former President and CEO of CP Air (a predecessor to Canadian Airlines). Primary investors include REGCO Capital Corp. (an entity controlled by Robert J. Deluce), OSI Transportation Corporation (an indirect wholly-owned subsidiary of OMERS Administration Corporation), EdgeStone and GEAM International Private Equity Fund, L.P.

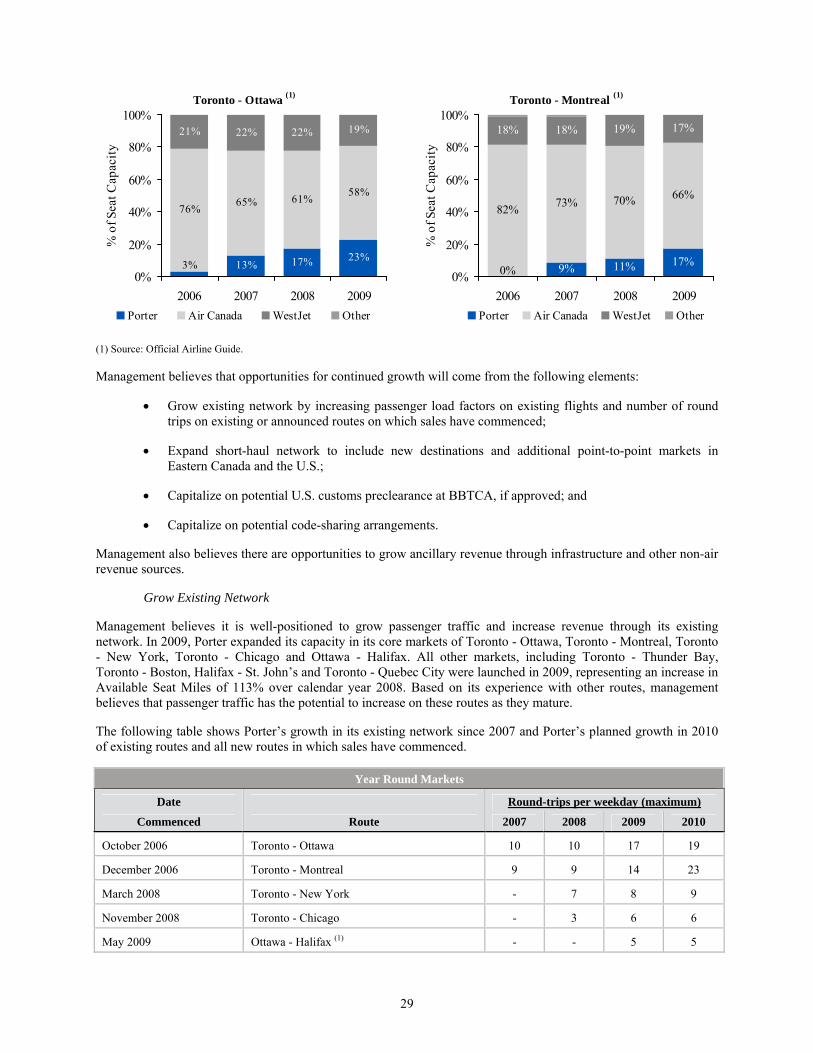

Growth Strategy

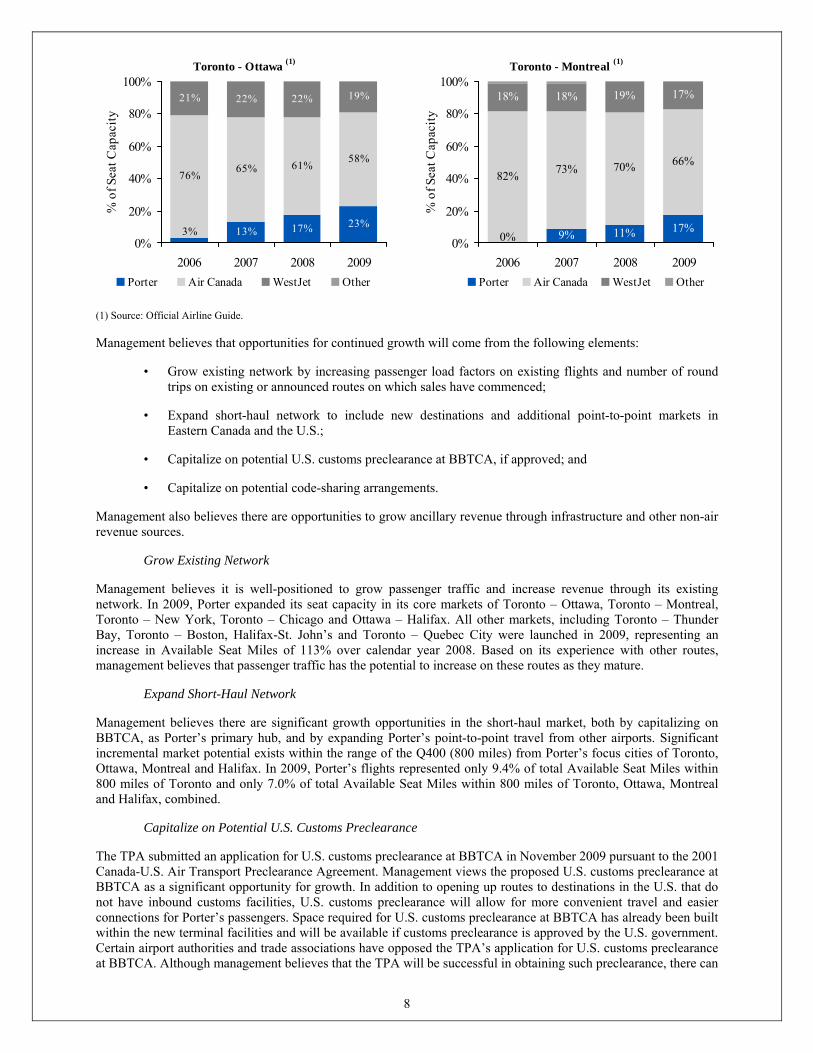

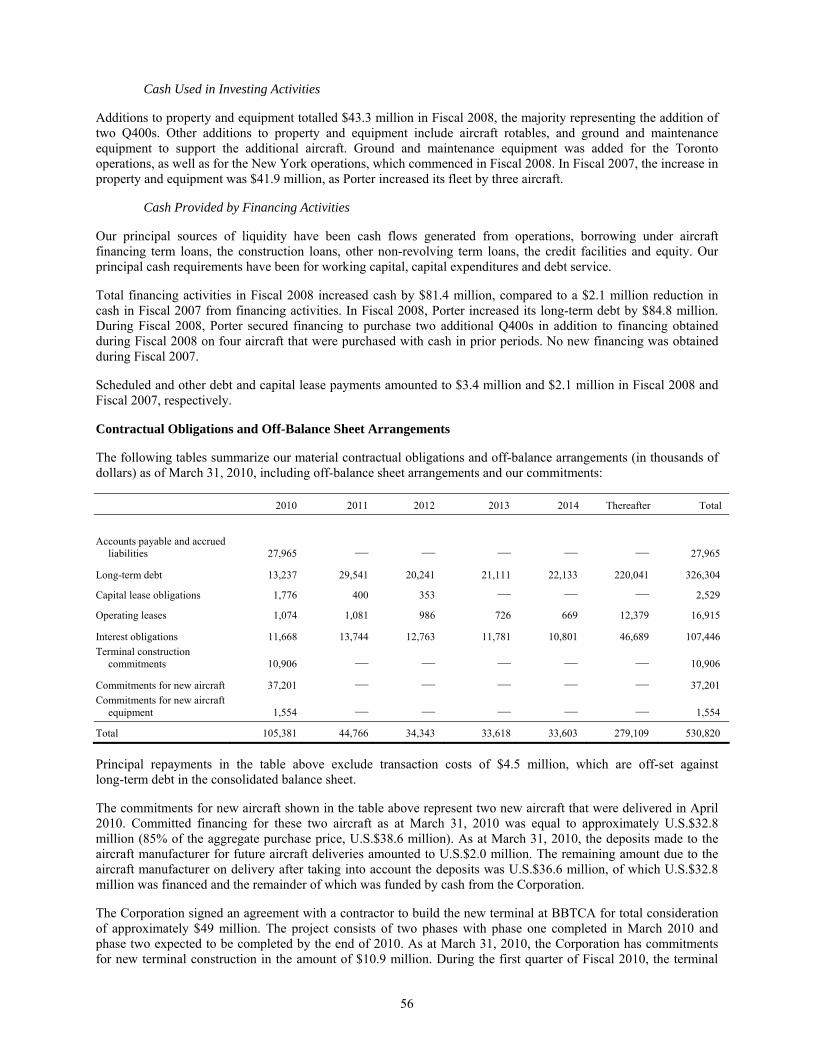

Since its inception in 2006, Porter has been successful in gaining significant market share, especially in its longest serving routes, Toronto – Ottawa and Toronto – Montreal, which are also two of the busiest domestic routes in Canada. As illustrated in the chart below, Porter’s capacity share (by number of seats) grew to 23% on the Toronto – Ottawa route and 17% on the Toronto – Montreal route, respectively, by 2009.

8

Toronto - Ottawa (1)

13% 17% 23%

76% 65% 61% 58%

21% 22% 22% 19%

3%0%

20%

40%

60%

80%

100%

2006 2007 2008 2009

% o

f Sea

t Cap

acity

Porter Air Canada WestJet Other

Toronto - Montreal (1)

9% 11% 17%

82% 73% 70% 66%

18% 18% 19% 17%

0%0%

20%

40%

60%

80%

100%

2006 2007 2008 2009

% o

f Sea

t Cap

acity

Porter Air Canada WestJet Other

(1) Source: Official Airline Guide.

Management believes that opportunities for continued growth will come from the following elements:

• Grow existing network by increasing passenger load factors on existing flights and number of round trips on existing or announced routes on which sales have commenced;

• Expand short-haul network to include new destinations and additional point-to-point markets in Eastern Canada and the U.S.;

• Capitalize on potential U.S. customs preclearance at BBTCA, if approved; and

• Capitalize on potential code-sharing arrangements.

Management also believes there are opportunities to grow ancillary revenue through infrastructure and other non-air revenue sources.

Grow Existing Network

Management believes it is well-positioned to grow passenger traffic and increase revenue through its existing network. In 2009, Porter expanded its seat capacity in its core markets of Toronto – Ottawa, Toronto – Montreal, Toronto – New York, Toronto – Chicago and Ottawa – Halifax. All other markets, including Toronto – Thunder Bay, Toronto – Boston, Halifax-St. John’s and Toronto – Quebec City were launched in 2009, representing an increase in Available Seat Miles of 113% over calendar year 2008. Based on its experience with other routes, management believes that passenger traffic has the potential to increase on these routes as they mature.

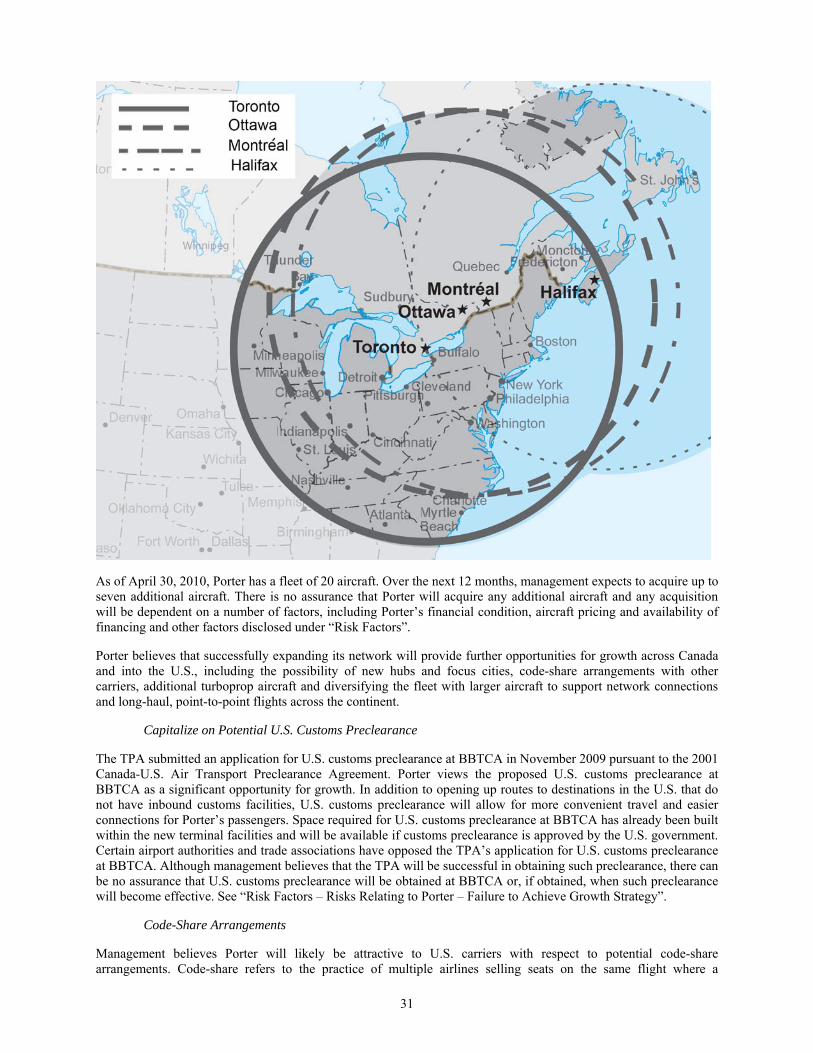

Expand Short-Haul Network

Management believes there are significant growth opportunities in the short-haul market, both by capitalizing on BBTCA, as Porter’s primary hub, and by expanding Porter’s point-to-point travel from other airports. Significant incremental market potential exists within the range of the Q400 (800 miles) from Porter’s focus cities of Toronto, Ottawa, Montreal and Halifax. In 2009, Porter’s flights represented only 9.4% of total Available Seat Miles within 800 miles of Toronto and only 7.0% of total Available Seat Miles within 800 miles of Toronto, Ottawa, Montreal and Halifax, combined.

Capitalize on Potential U.S. Customs Preclearance

The TPA submitted an application for U.S. customs preclearance at BBTCA in November 2009 pursuant to the 2001 Canada-U.S. Air Transport Preclearance Agreement. Management views the proposed U.S. customs preclearance at BBTCA as a significant opportunity for growth. In addition to opening up routes to destinations in the U.S. that do not have inbound customs facilities, U.S. customs preclearance will allow for more convenient travel and easier connections for Porter’s passengers. Space required for U.S. customs preclearance at BBTCA has already been built within the new terminal facilities and will be available if customs preclearance is approved by the U.S. government. Certain airport authorities and trade associations have opposed the TPA’s application for U.S. customs preclearance at BBTCA. Although management believes that the TPA will be successful in obtaining such preclearance, there can

9

be no assurance that U.S. customs preclearance will be obtained at BBTCA or, if obtained, when such preclearance will become effective.

Code-Share Arrangements

Management believes Porter will likely be attractive to U.S. carriers with respect to potential code-share arrangements. Code-share refers to the practice of multiple airlines selling seats on the same flight where a passenger may purchase a seat on one airline although the flight is operated by a cooperating airline under a different flight number or code. Porter, with its existing and new suppliers, is currently examining the computer system upgrades, operational procedures and back-office processes necessary to enable Porter to have the technical capability to enter into code-share arrangements by 2011.

Grow Ancillary Revenue

As is customary at many airports, all new commercial operators will be required to enter into a commercial operating agreement with the TPA before they commence operations out of BBTCA. Presently, Porter is the only commercial airline operating from BBTCA. Any additional commercial operators at BBTCA would lease terminal space and gates from Porter’s wholly-owned subsidiary, CCTC. As a substantial portion of the costs to build the new terminal at BBTCA have been incurred, Porter will not need to incur significant incremental costs prior to leasing terminal space. Management expects Porter to earn revenue from selling advertising space at the new terminal and expects that Porter may also earn rental income from concessions, retail shopping and other services provided in the terminal. Other potential revenue sources for Porter at BBTCA include leasing hangar and administrative space and selling fuel to other air carriers.

While Porter’s approach to travel partnerships has been predominantly informal during its start-up phase, management believes that Porter’s growing brand recognition and service offering may provide Porter with an opportunity to enter into retail and entertainment partnerships to package its flights with non-air travel products or services including hotels, rental cars and insurance. Porter is currently examining the upgrade of its technology with existing and new suppliers to enable it to capitalize on this opportunity by 2011.

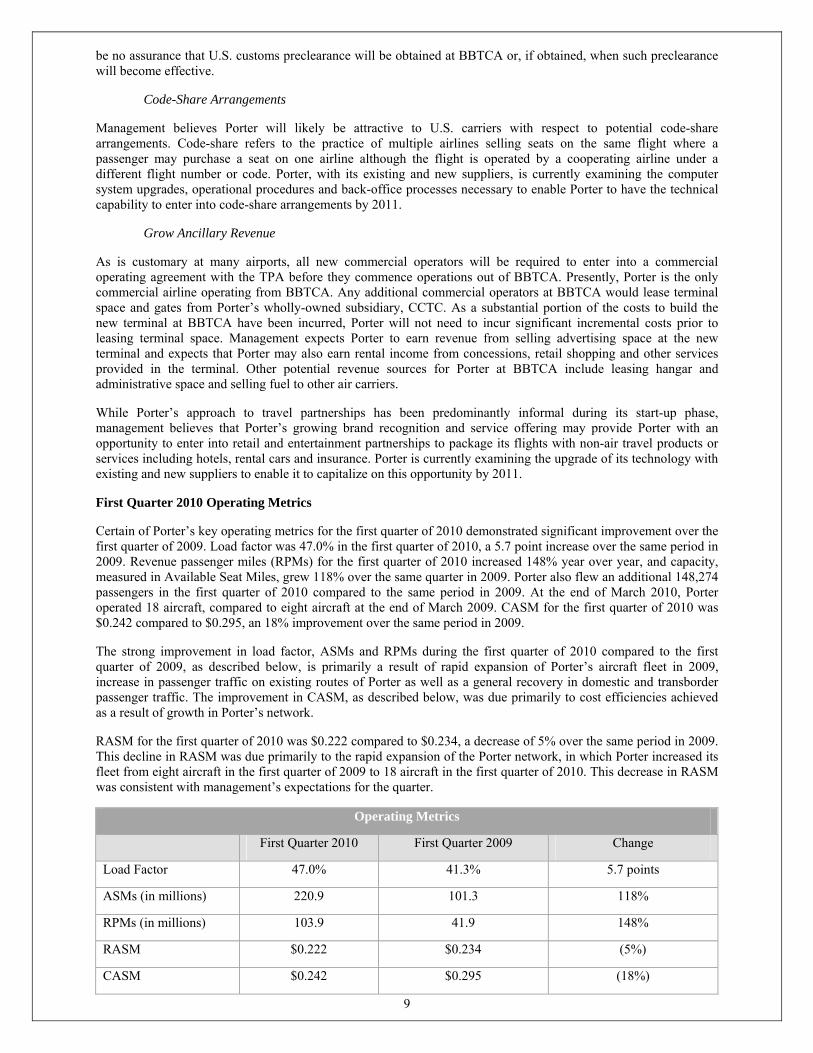

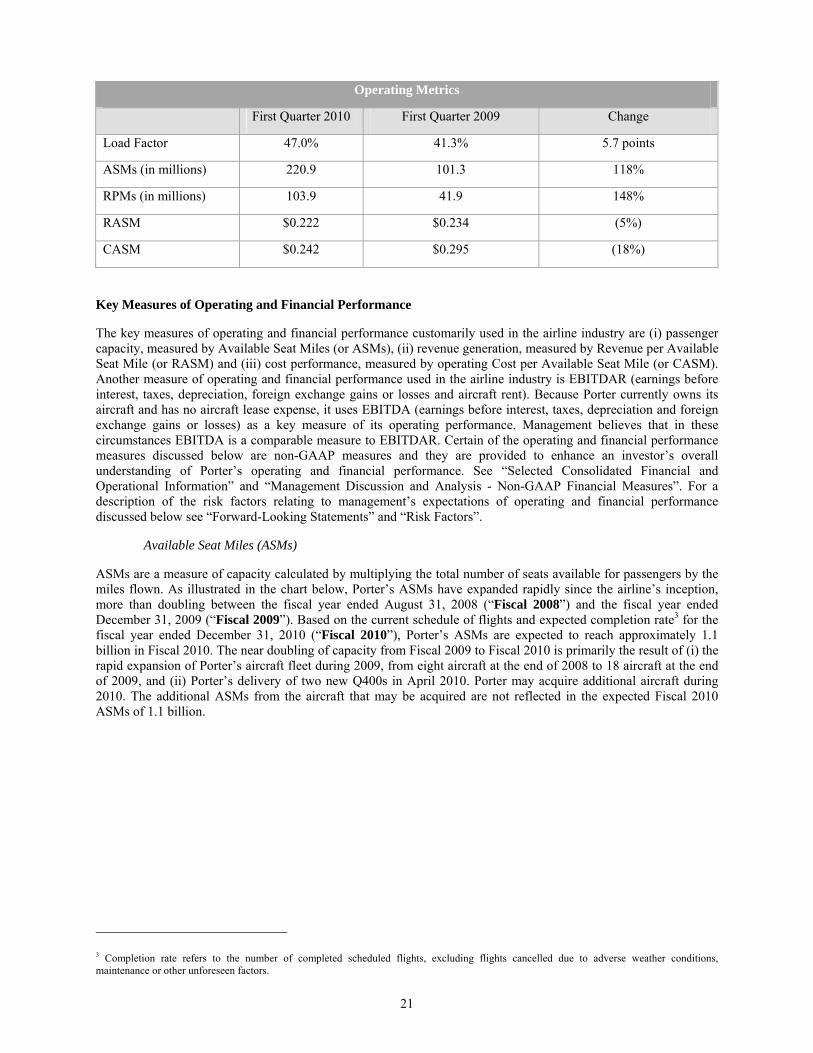

First Quarter 2010 Operating Metrics

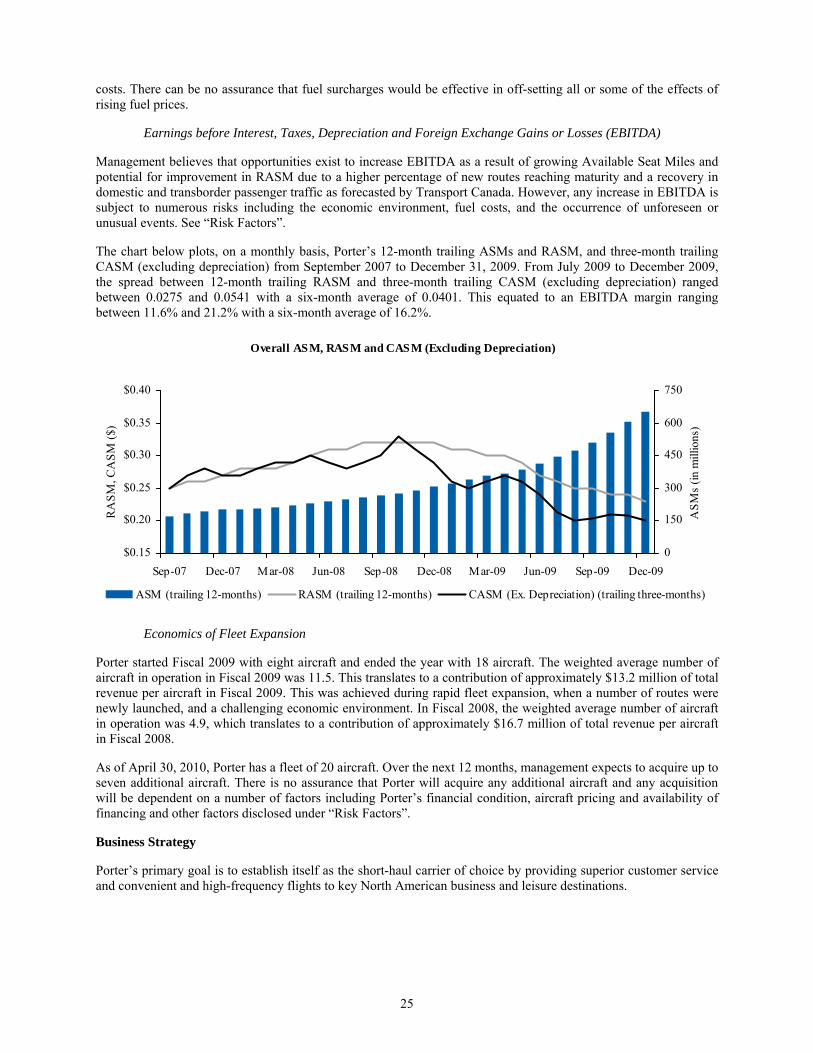

Certain of Porter’s key operating metrics for the first quarter of 2010 demonstrated significant improvement over the first quarter of 2009. Load factor was 47.0% in the first quarter of 2010, a 5.7 point increase over the same period in 2009. Revenue passenger miles (RPMs) for the first quarter of 2010 increased 148% year over year, and capacity, measured in Available Seat Miles, grew 118% over the same quarter in 2009. Porter also flew an additional 148,274 passengers in the first quarter of 2010 compared to the same period in 2009. At the end of March 2010, Porter operated 18 aircraft, compared to eight aircraft at the end of March 2009. CASM for the first quarter of 2010 was $0.242 compared to $0.295, an 18% improvement over the same period in 2009.

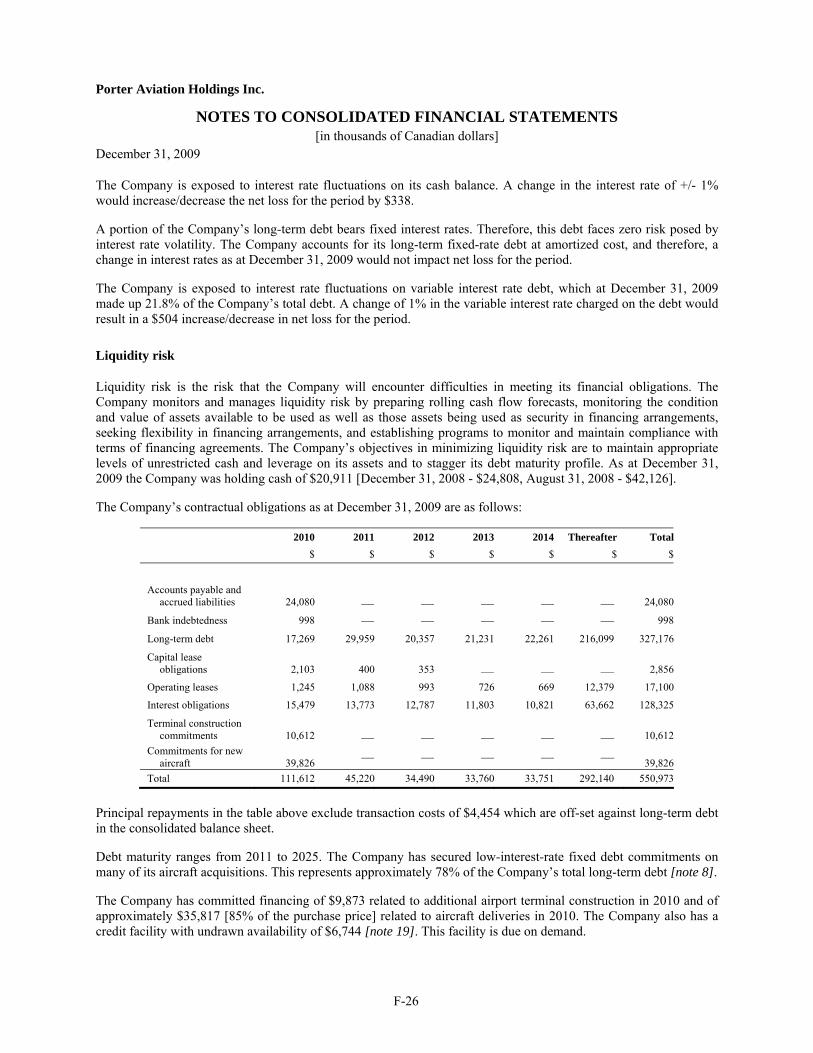

The strong improvement in load factor, ASMs and RPMs during the first quarter of 2010 compared to the first quarter of 2009, as described below, is primarily a result of rapid expansion of Porter’s aircraft fleet in 2009, increase in passenger traffic on existing routes of Porter as well as a general recovery in domestic and transborder passenger traffic. The improvement in CASM, as described below, was due primarily to cost efficiencies achieved as a result of growth in Porter’s network.

RASM for the first quarter of 2010 was $0.222 compared to $0.234, a decrease of 5% over the same period in 2009. This decline in RASM was due primarily to the rapid expansion of the Porter network, in which Porter increased its fleet from eight aircraft in the first quarter of 2009 to 18 aircraft in the first quarter of 2010. This decrease in RASM was consistent with management’s expectations for the quarter.

Operating Metrics

First Quarter 2010 First Quarter 2009 Change

Load Factor 47.0% 41.3% 5.7 points

ASMs (in millions) 220.9 101.3 118%

RPMs (in millions) 103.9 41.9 148%

RASM $0.222 $0.234 (5%)

CASM $0.242 $0.295 (18%)

10

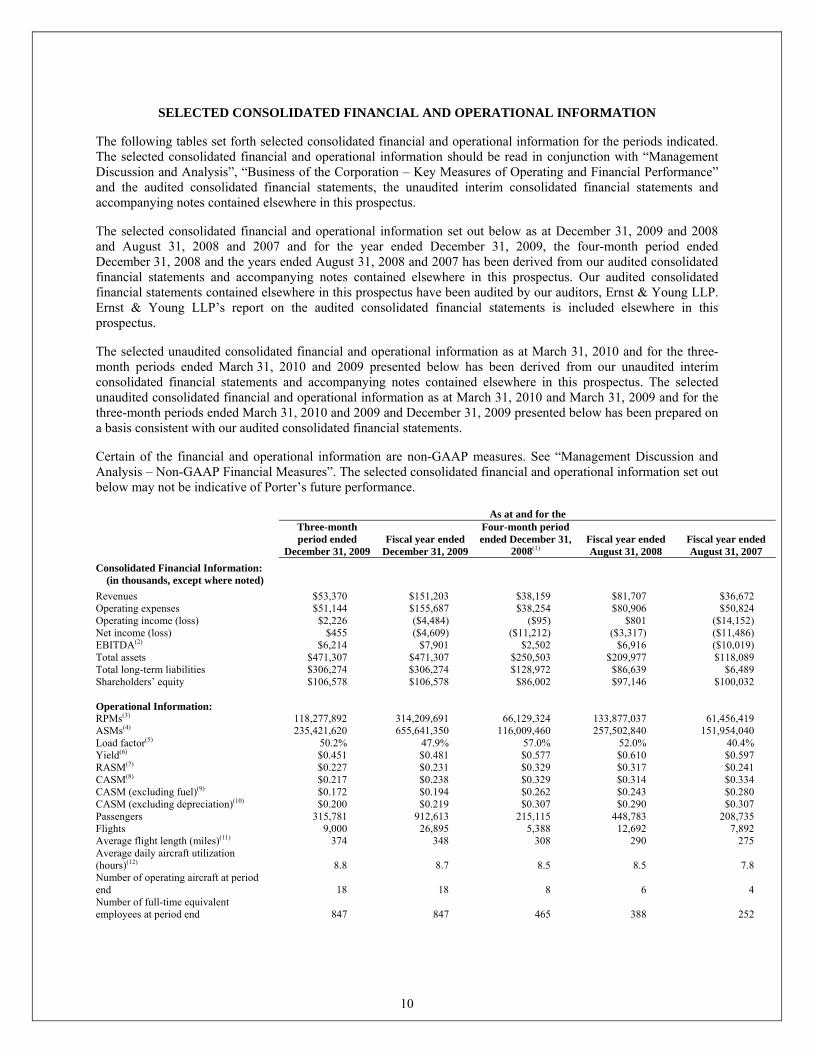

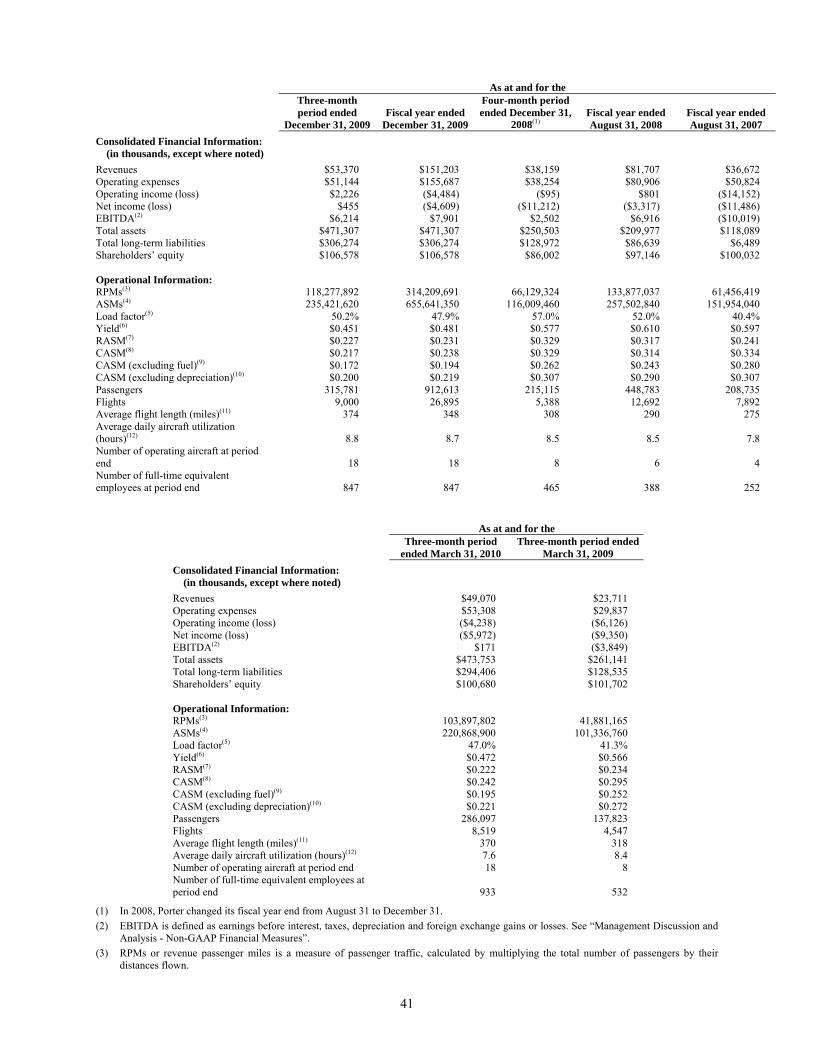

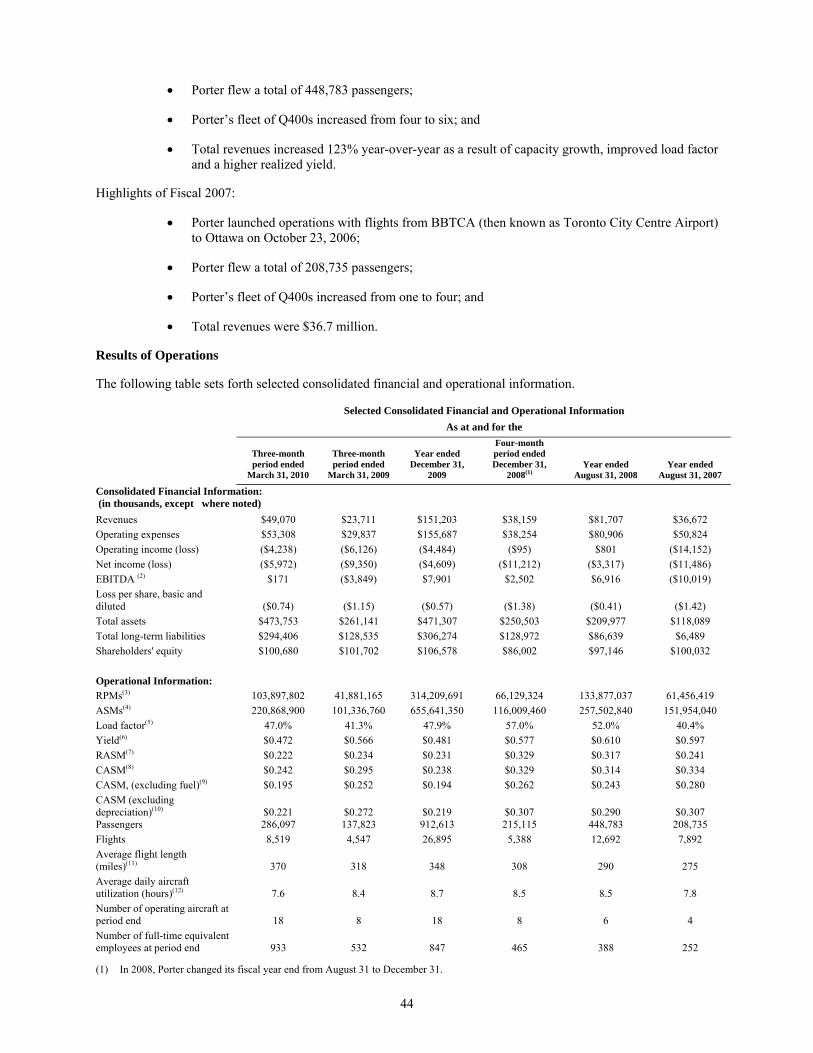

SELECTED CONSOLIDATED FINANCIAL AND OPERATIONAL INFORMATION

The following tables set forth selected consolidated financial and operational information for the periods indicated. The selected consolidated financial and operational information should be read in conjunction with “Management Discussion and Analysis”, “Business of the Corporation – Key Measures of Operating and Financial Performance” and the audited consolidated financial statements, the unaudited interim consolidated financial statements and accompanying notes contained elsewhere in this prospectus.

The selected consolidated financial and operational information set out below as at December 31, 2009 and 2008 and August 31, 2008 and 2007 and for the year ended December 31, 2009, the four-month period ended December 31, 2008 and the years ended August 31, 2008 and 2007 has been derived from our audited consolidated financial statements and accompanying notes contained elsewhere in this prospectus. Our audited consolidated financial statements contained elsewhere in this prospectus have been audited by our auditors, Ernst & Young LLP. Ernst & Young LLP’s report on the audited consolidated financial statements is included elsewhere in this prospectus.

The selected unaudited consolidated financial and operational information as at March 31, 2010 and for the three-month periods ended March 31, 2010 and 2009 presented below has been derived from our unaudited interim consolidated financial statements and accompanying notes contained elsewhere in this prospectus. The selected unaudited consolidated financial and operational information as at March 31, 2010 and March 31, 2009 and for the three-month periods ended March 31, 2010 and 2009 and December 31, 2009 presented below has been prepared on a basis consistent with our audited consolidated financial statements.

Certain of the financial and operational information are non-GAAP measures. See “Management Discussion and Analysis – Non-GAAP Financial Measures”. The selected consolidated financial and operational information set out below may not be indicative of Porter’s future performance.

As at and for the

Three-month period ended

December 31, 2009Fiscal year ended

December 31, 2009

Four-month period ended December 31,

2008(1) Fiscal year ended August 31, 2008

Fiscal year ended August 31, 2007

Consolidated Financial Information: (in thousands, except where noted)

Revenues $53,370 $151,203 $38,159 $81,707 $36,672 Operating expenses $51,144 $155,687 $38,254 $80,906 $50,824 Operating income (loss) $2,226 ($4,484) ($95) $801 ($14,152) Net income (loss) $455 ($4,609) ($11,212) ($3,317) ($11,486) EBITDA(2) $6,214 $7,901 $2,502 $6,916 ($10,019) Total assets $471,307 $471,307 $250,503 $209,977 $118,089 Total long-term liabilities $306,274 $306,274 $128,972 $86,639 $6,489 Shareholders’ equity $106,578 $106,578 $86,002 $97,146 $100,032 Operational Information: RPMs(3) 118,277,892 314,209,691 66,129,324 133,877,037 61,456,419 ASMs(4) 235,421,620 655,641,350 116,009,460 257,502,840 151,954,040 Load factor(5) 50.2% 47.9% 57.0% 52.0% 40.4% Yield(6) $0.451 $0.481 $0.577 $0.610 $0.597 RASM(7) $0.227 $0.231 $0.329 $0.317 $0.241 CASM(8) $0.217 $0.238 $0.329 $0.314 $0.334 CASM (excluding fuel)(9) $0.172 $0.194 $0.262 $0.243 $0.280 CASM (excluding depreciation)(10) $0.200 $0.219 $0.307 $0.290 $0.307 Passengers 315,781 912,613 215,115 448,783 208,735 Flights 9,000 26,895 5,388 12,692 7,892 Average flight length (miles)(11) 374 348 308 290 275 Average daily aircraft utilization (hours)(12) 8.8 8.7 8.5 8.5 7.8 Number of operating aircraft at period end 18 18 8 6 4 Number of full-time equivalent employees at period end 847 847 465 388 252

11

As at and for the

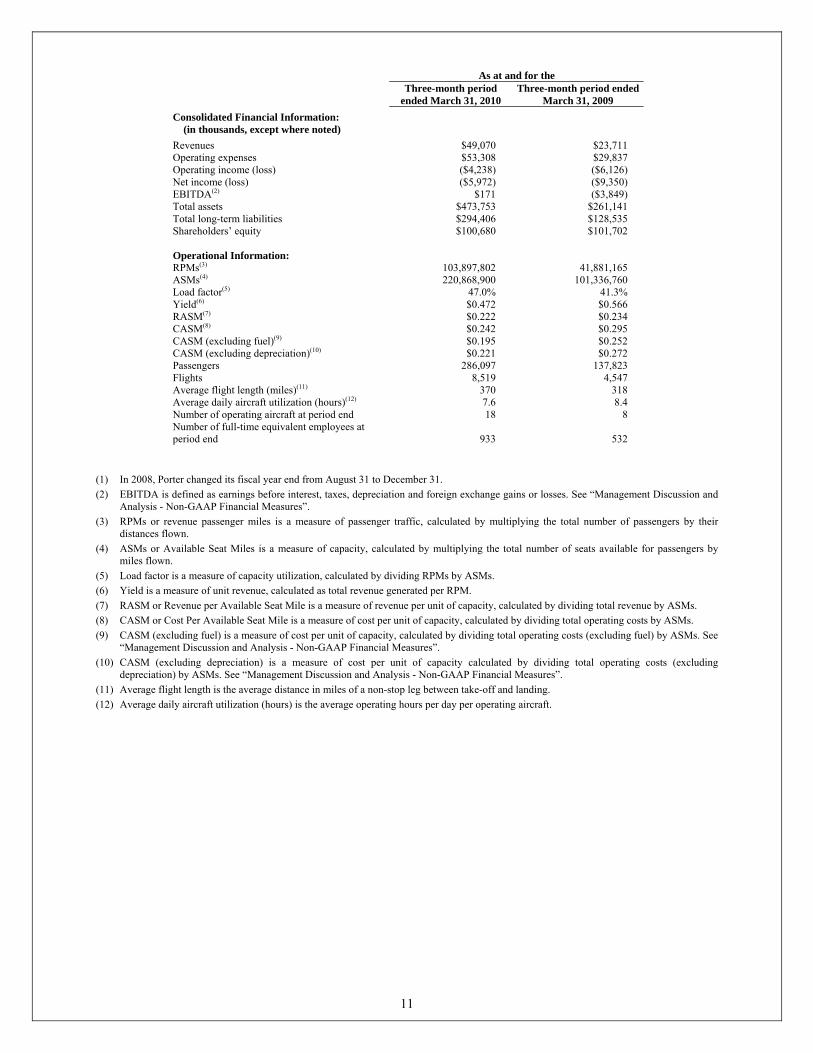

Three-month period

ended March 31, 2010 Three-month period ended

March 31, 2009 Consolidated Financial Information: (in thousands, except where noted)

Revenues $49,070 $23,711 Operating expenses $53,308 $29,837 Operating income (loss) ($4,238) ($6,126) Net income (loss) ($5,972) ($9,350) EBITDA(2) $171 ($3,849) Total assets $473,753 $261,141 Total long-term liabilities $294,406 $128,535 Shareholders’ equity $100,680 $101,702 Operational Information: RPMs(3) 103,897,802 41,881,165 ASMs(4) 220,868,900 101,336,760 Load factor(5) 47.0% 41.3% Yield(6) $0.472 $0.566 RASM(7) $0.222 $0.234 CASM(8) $0.242 $0.295 CASM (excluding fuel)(9) $0.195 $0.252 CASM (excluding depreciation)(10) $0.221 $0.272 Passengers 286,097 137,823 Flights 8,519 4,547 Average flight length (miles)(11) 370 318 Average daily aircraft utilization (hours)(12) 7.6 8.4 Number of operating aircraft at period end 18 8 Number of full-time equivalent employees at period end 933 532

(1) In 2008, Porter changed its fiscal year end from August 31 to December 31. (2) EBITDA is defined as earnings before interest, taxes, depreciation and foreign exchange gains or losses. See “Management Discussion and

Analysis - Non-GAAP Financial Measures”. (3) RPMs or revenue passenger miles is a measure of passenger traffic, calculated by multiplying the total number of passengers by their

distances flown. (4) ASMs or Available Seat Miles is a measure of capacity, calculated by multiplying the total number of seats available for passengers by

miles flown. (5) Load factor is a measure of capacity utilization, calculated by dividing RPMs by ASMs. (6) Yield is a measure of unit revenue, calculated as total revenue generated per RPM. (7) RASM or Revenue per Available Seat Mile is a measure of revenue per unit of capacity, calculated by dividing total revenue by ASMs. (8) CASM or Cost Per Available Seat Mile is a measure of cost per unit of capacity, calculated by dividing total operating costs by ASMs. (9) CASM (excluding fuel) is a measure of cost per unit of capacity, calculated by dividing total operating costs (excluding fuel) by ASMs. See

“Management Discussion and Analysis - Non-GAAP Financial Measures”. (10) CASM (excluding depreciation) is a measure of cost per unit of capacity calculated by dividing total operating costs (excluding

depreciation) by ASMs. See “Management Discussion and Analysis - Non-GAAP Financial Measures”. (11) Average flight length is the average distance in miles of a non-stop leg between take-off and landing. (12) Average daily aircraft utilization (hours) is the average operating hours per day per operating aircraft.

12

THE OFFERING

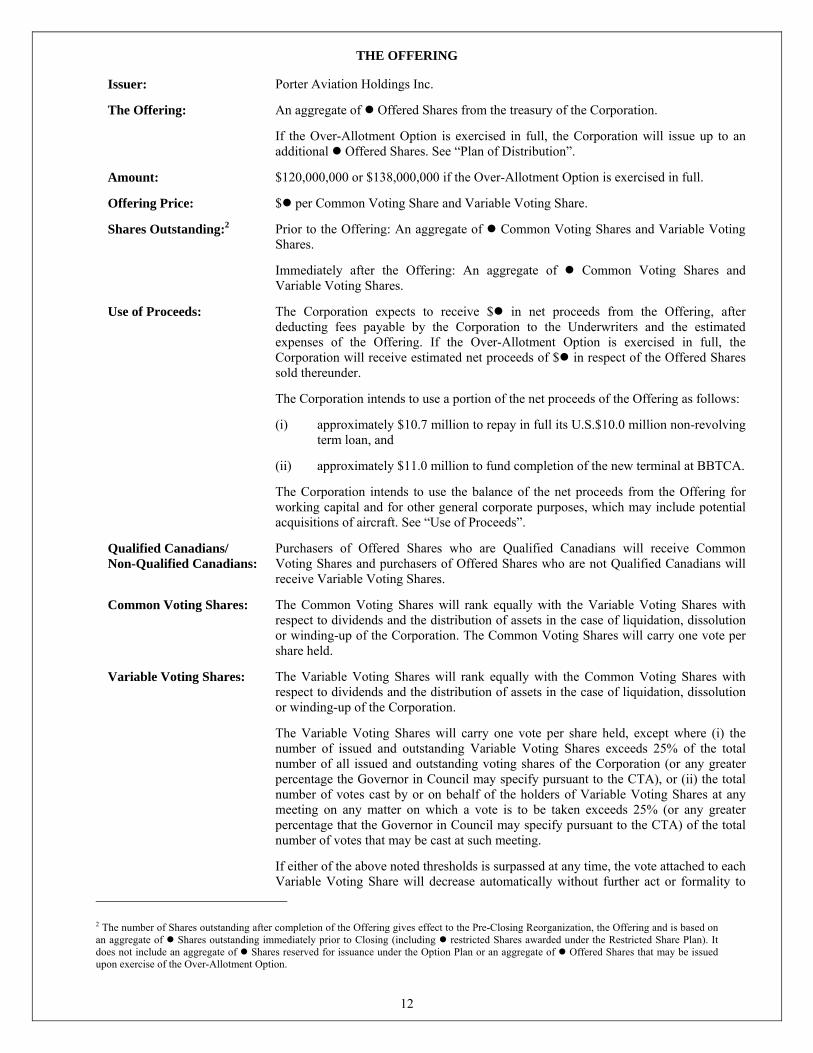

Issuer: Porter Aviation Holdings Inc.

The Offering: An aggregate of Offered Shares from the treasury of the Corporation.

If the Over-Allotment Option is exercised in full, the Corporation will issue up to an additional Offered Shares. See “Plan of Distribution”.

Amount: $120,000,000 or $138,000,000 if the Over-Allotment Option is exercised in full.

Offering Price: $ per Common Voting Share and Variable Voting Share.

Shares Outstanding:2 Prior to the Offering: An aggregate of Common Voting Shares and Variable Voting Shares.

Immediately after the Offering: An aggregate of Common Voting Shares and Variable Voting Shares.

Use of Proceeds: The Corporation expects to receive $ in net proceeds from the Offering, after deducting fees payable by the Corporation to the Underwriters and the estimated expenses of the Offering. If the Over-Allotment Option is exercised in full, the Corporation will receive estimated net proceeds of $ in respect of the Offered Shares sold thereunder.

The Corporation intends to use a portion of the net proceeds of the Offering as follows:

(i) approximately $10.7 million to repay in full its U.S.$10.0 million non-revolving term loan, and

(ii) approximately $11.0 million to fund completion of the new terminal at BBTCA.

The Corporation intends to use the balance of the net proceeds from the Offering for working capital and for other general corporate purposes, which may include potential acquisitions of aircraft. See “Use of Proceeds”.

Qualified Canadians/ Non-Qualified Canadians:

Purchasers of Offered Shares who are Qualified Canadians will receive Common Voting Shares and purchasers of Offered Shares who are not Qualified Canadians will receive Variable Voting Shares.

Common Voting Shares: The Common Voting Shares will rank equally with the Variable Voting Shares with respect to dividends and the distribution of assets in the case of liquidation, dissolution or winding-up of the Corporation. The Common Voting Shares will carry one vote per share held.

Variable Voting Shares: The Variable Voting Shares will rank equally with the Common Voting Shares with respect to dividends and the distribution of assets in the case of liquidation, dissolution or winding-up of the Corporation.

The Variable Voting Shares will carry one vote per share held, except where (i) the number of issued and outstanding Variable Voting Shares exceeds 25% of the total number of all issued and outstanding voting shares of the Corporation (or any greater percentage the Governor in Council may specify pursuant to the CTA), or (ii) the total number of votes cast by or on behalf of the holders of Variable Voting Shares at any meeting on any matter on which a vote is to be taken exceeds 25% (or any greater percentage that the Governor in Council may specify pursuant to the CTA) of the total number of votes that may be cast at such meeting.

If either of the above noted thresholds is surpassed at any time, the vote attached to each Variable Voting Share will decrease automatically without further act or formality to

2 The number of Shares outstanding after completion of the Offering gives effect to the Pre-Closing Reorganization, the Offering and is based on an aggregate of Shares outstanding immediately prior to Closing (including restricted Shares awarded under the Restricted Share Plan). It does not include an aggregate of Shares reserved for issuance under the Option Plan or an aggregate of Offered Shares that may be issued upon exercise of the Over-Allotment Option.

13

equal the maximum permitted vote per Variable Voting Share such that (i) the Variable Voting Shares as a class shall not carry more than 25% (or any greater percentage that the Governor in Council may specify pursuant to the CTA) of the total voting rights attached to the aggregate number of the Corporation’s issued and outstanding voting shares; and (ii) the Variable Voting Shares as a class shall not, for a given shareholders’ meeting, carry more than 25% (or any greater percentage that the Governor in Council may specify pursuant to the CTA) of the total number of votes that may be cast at the meeting. See “Description of Securities”.

Conversion of Shares: Each issued and outstanding Variable Voting Share shall be automatically converted into one Common Voting Share if (i) such Variable Voting Share becomes beneficially owned and controlled, directly or indirectly, by a Qualified Canadian, or (ii) the provisions contained in the CTA relating to foreign ownership restrictions are repealed and not replaced with other similar provisions in applicable legislation. Each issued and outstanding Common Voting Share shall be automatically converted into one Variable Voting Share if such Common Voting Share becomes beneficially owned or controlled, directly or indirectly, by a holder who is not a Qualified Canadian. See “Description of Securities”.

Over-Allotment Option: The Corporation has granted the Underwriters an Over-Allotment Option to cover over-allotments, if any, and for market stabilization purposes. The Over-Allotment Option may be exercised by the Underwriters, in whole or in part, at their sole discretion, for a 30-day period following Closing and entitles the Underwriters to purchase up to an additional Offered Shares at the Offering Price. The Corporation will pay the Underwriters’ fee in respect of Offered Shares sold under the Over-Allotment Option if the Over-Allotment Option is exercised. If the Over-Allotment Option is exercised in full, the total price to the public will be $138,000,000, the Underwriters’ fee will be $ and the net proceeds to the Corporation will be $ . See “Plan of Distribution”.

Risk Factors: An investment in the Offered Shares is subject to a number of risks, including risks related to: our dependence on Billy Bishop Toronto City Airport, a failure to achieve our growth strategy, price and availability of jet fuel, our ability to obtain financing for additional aircraft, dependence on relations with third parties, dependence on our ability to hire and retain qualified personnel, litigation risks, foreign currency and interest rate fluctuations, our use of a single type of aircraft, limited fleet size, maintenance costs increase as our fleet ages, dependence on technology, significant changes in corporate culture or customer experience, unionization or increased labour costs, limitations due to restrictive covenants, lack of operational history, ability to obtain additional capital, economic conditions, terrorist attacks and security measures, a localized epidemic or global pandemic, major safety incidents, environmental requirements, insurable and uninsurable risks, seasonal nature of the business, competition, government intervention, regulations, rulings and decisions, airport user fees and air navigation fees, external factors such as weather conditions or special events, Shares have no prior public market and the share price may decline after the Offering, volatile market price for Offered Shares, we have no plans to pay dividends, future sale of Shares, influence by existing shareholders, future sales of shares by our existing shareholders, and discretion in use of proceeds.

Dividend Policy: The Corporation does not currently anticipate paying any dividends on its Offered Shares. The Corporation currently intends to use its earnings to finance the expansion of its business and to reduce indebtedness. See “Dividend Policy”.

Registration Rights Agreement:

On Closing, REGCO Capital Corp. (an entity controlled by Robert J. Deluce, President and Chief Executive Officer of Porter) OSI Transportation Corporation, GEAM International Private Equity Fund, L.P. and EdgeStone will enter into a registration rights agreement with Porter which will provide these holders with certain demand and “piggy-back” registration rights in accordance with and subject to the terms and restrictions set forth in such agreement. These holders of Shares will own % of the outstanding Shares immediately after giving effect to the Offering. See “Registration Rights Agreement”.

14

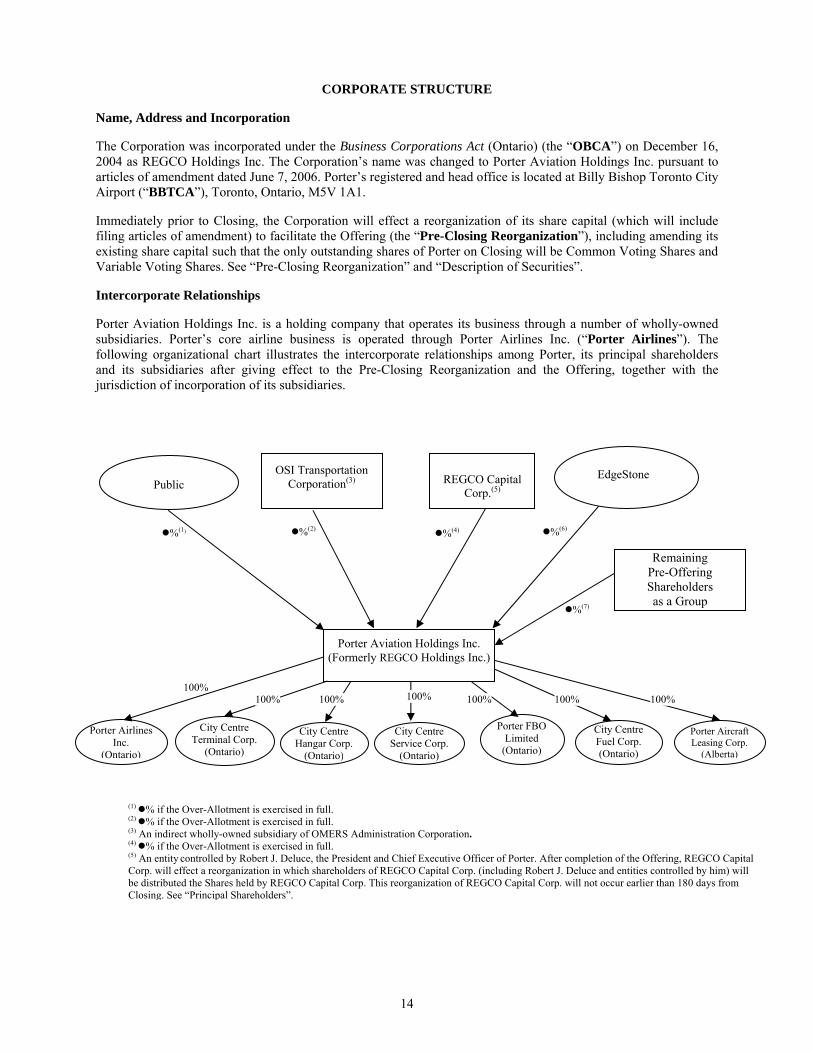

CORPORATE STRUCTURE

Name, Address and Incorporation

The Corporation was incorporated under the Business Corporations Act (Ontario) (the “OBCA”) on December 16, 2004 as REGCO Holdings Inc. The Corporation’s name was changed to Porter Aviation Holdings Inc. pursuant to articles of amendment dated June 7, 2006. Porter’s registered and head office is located at Billy Bishop Toronto City Airport (“BBTCA”), Toronto, Ontario, M5V 1A1.

Immediately prior to Closing, the Corporation will effect a reorganization of its share capital (which will include filing articles of amendment) to facilitate the Offering (the “Pre-Closing Reorganization”), including amending its existing share capital such that the only outstanding shares of Porter on Closing will be Common Voting Shares and Variable Voting Shares. See “Pre-Closing Reorganization” and “Description of Securities”.

Intercorporate Relationships

Porter Aviation Holdings Inc. is a holding company that operates its business through a number of wholly-owned subsidiaries. Porter’s core airline business is operated through Porter Airlines Inc. (“Porter Airlines”). The following organizational chart illustrates the intercorporate relationships among Porter, its principal shareholders and its subsidiaries after giving effect to the Pre-Closing Reorganization and the Offering, together with the jurisdiction of incorporation of its subsidiaries.

%(1)

Porter Aviation Holdings Inc. (Formerly REGCO Holdings Inc.)

%(2)

100%

Public EdgeStone

Porter Airlines Inc.

(Ontario)

Remaining Pre-Offering Shareholders as a Group

%(7)

%(6)

REGCO Capital Corp.(5)

%(4)

OSI Transportation Corporation(3)

City Centre Terminal Corp.

(Ontario)

City Centre Hangar Corp.

(Ontario)

Porter FBO Limited

(Ontario)

City Centre Fuel Corp. (Ontario)

Porter AircraftLeasing Corp.

(Alberta)

City Centre Service Corp.

(Ontario)

(1) % if the Over-Allotment is exercised in full. (2) % if the Over-Allotment is exercised in full. (3) An indirect wholly-owned subsidiary of OMERS Administration Corporation. (4) % if the Over-Allotment is exercised in full. (5) An entity controlled by Robert J. Deluce, the President and Chief Executive Officer of Porter. After completion of the Offering, REGCO Capital Corp. will effect a reorganization in which shareholders of REGCO Capital Corp. (including Robert J. Deluce and entities controlled by him) will be distributed the Shares held by REGCO Capital Corp. This reorganization of REGCO Capital Corp. will not occur earlier than 180 days from Closing. See “Principal Shareholders”.

100% 100% 100% 100% 100% 100%

15

BUSINESS OF THE CORPORATION

Industry Overview

General

The airline industry plays an important role in both the Canadian and global economy. The airline industry is particularly important in Canada given the country’s large territory and widely dispersed population. In 2008, Canadian airlines carried over 75 million business and leisure passengers, with over 86 million daily seat-miles across the country. Canadian carriers also play an important role in the transport of goods within the country and in the import/export market. In 2008, over $100 billion of goods were imported to and exported from Canada by air, representing 19% of imports and 26% of exports for the year. Based on Transport Canada data, the airline industry contributed over $16 billion of revenue to the Canadian economy in 2007 and employed over 86,000 people in 2008.

Historically, the North American airline industry has been dominated by large, well-established network carriers. Over the past three decades though, governments have gradually reduced economic regulation of commercial aviation, which has resulted in a more open and competitive environment for domestic and transborder airline services. This deregulation has transformed the airline industry, allowing new market entrants, including low-cost carriers, to emerge and compete successfully with full-service airlines.

Relying on a simplified operational model and product offering, many low-cost carriers in North America have been able to operate profitably with lower fares than full-service carriers. However, a number of low-cost Canadian carriers such as Jetsgo Corporation, Zoom Airlines Inc., Canada 3000 Inc., Roots Air and CanJet Airlines have been unable to effectively compete on a long-term basis due to a variety of factors including limited distribution strategies, inability to sustain pricing, economic downturns and poor execution of operating plans.

As a result of the competitive pressure from low-cost carriers and a succession of challenging factors faced by all industry participants, including the events of September 11, 2001, the SARS crisis, high fuel prices and a global economic recession, some full-service airlines have been forced to restructure their operations through both court-supervised and voluntary processes and implement substantial changes including labour concessions, the renegotiation of significant contracts and a focus on long-haul premium business routes. In addition, there has been an increased emphasis on producing ancillary revenue through the introduction of baggage fees, in-flight food and beverage charges and fuel surcharges.

Carriers must also address low levels of customer satisfaction. In recent years, airline passengers have become increasingly dissatisfied with airline travel. In particular, airport security has become progressively more time-consuming for travelers, especially in large, international airports that accommodate many different airlines. As a result, many passengers find that air travel can be a frustrating experience.

In response to reduced service levels and heightened passenger frustration with full-service carriers, the industry has seen many low-cost carriers moving towards a “hybrid” airline model - a strategy that blends low-cost carrier traits with some full-service carrier business practices to help grow their passenger base and expand market share. Some of the full-service carrier attributes being introduced by these hybrid low-cost carriers include use of global distribution system services, code-share arrangements, multiple fare options, advanced ticketing procedures, multiple aircraft types, multiple classes of service, and long-haul (including international) destinations.

Partially in response to this trend, a number of business models focusing on smaller, secondary city centre airports have emerged. Over the span of a few decades, secondary airports have gained passenger share in New York, Chicago, Houston, Dallas, Paris, London and other large urban centres. Some, like London City Airport, six miles from the downtown financial district, have emerged as convenient alternatives for passengers. Some of these secondary airports distinguish themselves from their larger international competitors by offering a faster and more efficient travel experience.

In an effort to manage operating costs, airlines have increasingly focused on the fuel efficiency of their aircraft and are continually looking at cost effective opportunities to refurbish their fleet with more economical aircraft. Manufacturers have responded to this demand by developing more fuel efficient aircraft such as the Bombardier Q400 turboprop aircraft (the “Q400”). Optimized for short-haul airline operations, the Q400 offers lower costs relative to similarly sized mainline jets through reduced fuel burns (attributed to the new Pratt & Whitney PW150A turboprop engine), lower maintenance costs for high-cycle utilization and crew cost savings.

16

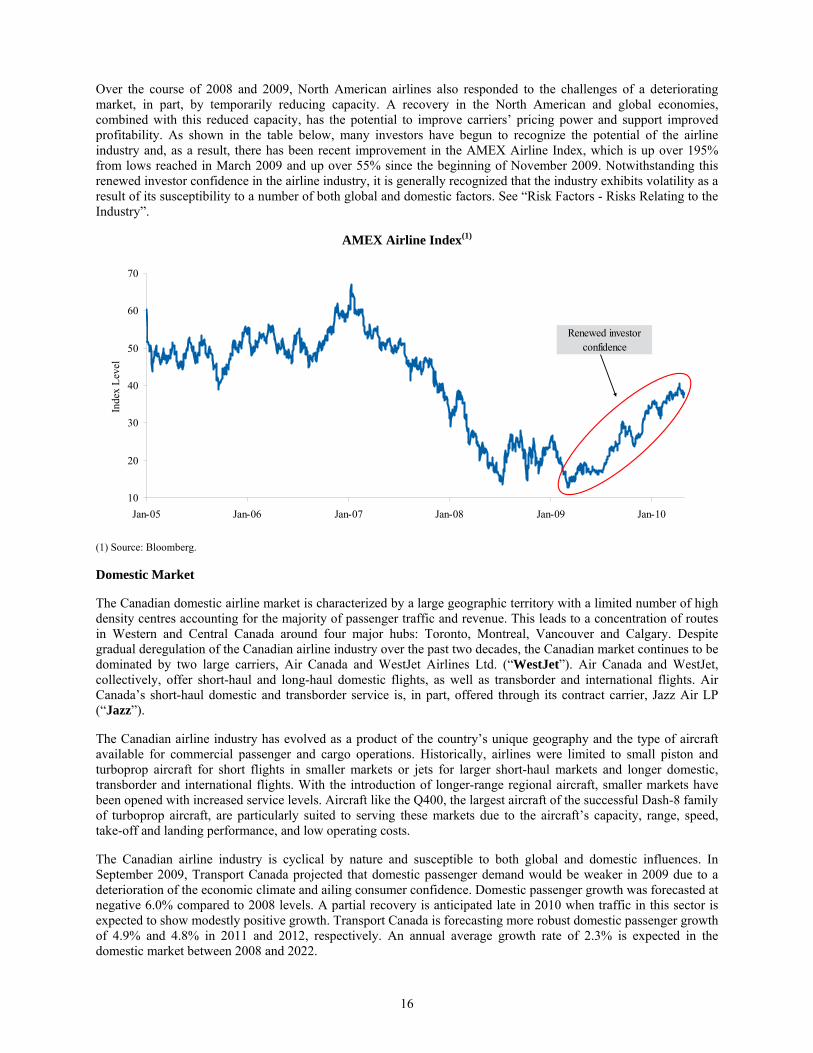

Over the course of 2008 and 2009, North American airlines also responded to the challenges of a deteriorating market, in part, by temporarily reducing capacity. A recovery in the North American and global economies, combined with this reduced capacity, has the potential to improve carriers’ pricing power and support improved profitability. As shown in the table below, many investors have begun to recognize the potential of the airline industry and, as a result, there has been recent improvement in the AMEX Airline Index, which is up over 195% from lows reached in March 2009 and up over 55% since the beginning of November 2009. Notwithstanding this renewed investor confidence in the airline industry, it is generally recognized that the industry exhibits volatility as a result of its susceptibility to a number of both global and domestic factors. See “Risk Factors - Risks Relating to the Industry”.

AMEX Airline Index(1)

10

20

30

40

50

60

70

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10

Inde

x Le

vel .

Renewed investor confidence

(1) Source: Bloomberg.

Domestic Market

The Canadian domestic airline market is characterized by a large geographic territory with a limited number of high density centres accounting for the majority of passenger traffic and revenue. This leads to a concentration of routes in Western and Central Canada around four major hubs: Toronto, Montreal, Vancouver and Calgary. Despite gradual deregulation of the Canadian airline industry over the past two decades, the Canadian market continues to be dominated by two large carriers, Air Canada and WestJet Airlines Ltd. (“WestJet”). Air Canada and WestJet, collectively, offer short-haul and long-haul domestic flights, as well as transborder and international flights. Air Canada’s short-haul domestic and transborder service is, in part, offered through its contract carrier, Jazz Air LP (“Jazz”).

The Canadian airline industry has evolved as a product of the country’s unique geography and the type of aircraft available for commercial passenger and cargo operations. Historically, airlines were limited to small piston and turboprop aircraft for short flights in smaller markets or jets for larger short-haul markets and longer domestic, transborder and international flights. With the introduction of longer-range regional aircraft, smaller markets have been opened with increased service levels. Aircraft like the Q400, the largest aircraft of the successful Dash-8 family of turboprop aircraft, are particularly suited to serving these markets due to the aircraft’s capacity, range, speed, take-off and landing performance, and low operating costs.

The Canadian airline industry is cyclical by nature and susceptible to both global and domestic influences. In September 2009, Transport Canada projected that domestic passenger demand would be weaker in 2009 due to a deterioration of the economic climate and ailing consumer confidence. Domestic passenger growth was forecasted at negative 6.0% compared to 2008 levels. A partial recovery is anticipated late in 2010 when traffic in this sector is expected to show modestly positive growth. Transport Canada is forecasting more robust domestic passenger growth of 4.9% and 4.8% in 2011 and 2012, respectively. An annual average growth rate of 2.3% is expected in the domestic market between 2008 and 2022.

17

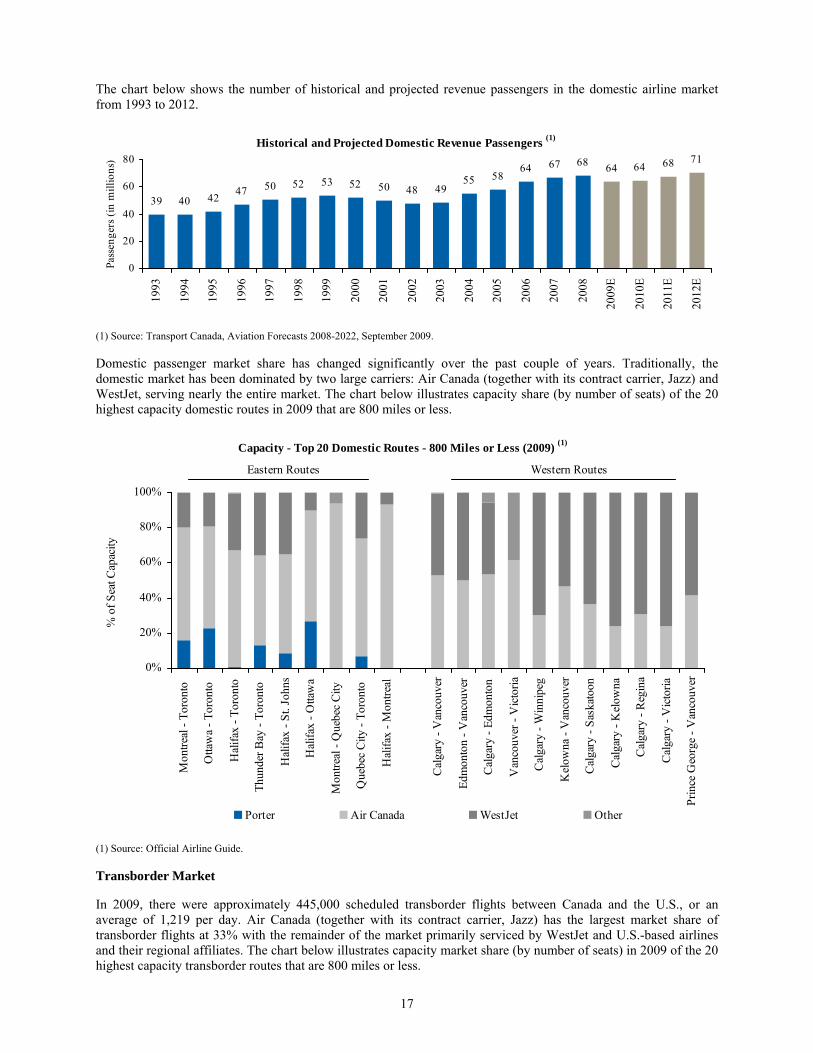

The chart below shows the number of historical and projected revenue passengers in the domestic airline market from 1993 to 2012.

Historical and Projected Domestic Revenue Passengers (1)

39 40 42 47 50 52 53 52 50 48 4955 58

64 67 68 64 64 68 71

0

20

40

60

8019

93

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

E

2010

E

2011

E

2012

E

Pass

enge

rs (i

n m

illio

ns)

(1) Source: Transport Canada, Aviation Forecasts 2008-2022, September 2009.

Domestic passenger market share has changed significantly over the past couple of years. Traditionally, the domestic market has been dominated by two large carriers: Air Canada (together with its contract carrier, Jazz) and WestJet, serving nearly the entire market. The chart below illustrates capacity share (by number of seats) of the 20 highest capacity domestic routes in 2009 that are 800 miles or less.

Capacity - Top 20 Domestic Routes - 800 Miles or Less (2009) (1)

0%

20%

40%

60%

80%

100%

Mon

treal

- To

ront

o

Otta

wa

- Tor

onto

Hal

ifax

- Tor

onto

Thun

der B

ay -

Toro

nto

Hal

ifax

- St.

John

s

Hal

ifax

- Otta

wa

Mon

treal

- Q

uebe

c C

ity

Que

bec

City

- To

ront

o

Hal

ifax

- Mon

treal

Cal

gary

- V

anco

uver

Edm

onto

n - V

anco

uver

Cal

gary

- Ed

mon

ton

Van

couv

er -

Vic

toria

Cal

gary

- W

inni

peg

Kel

owna

- V

anco

uver

Cal

gary

- Sa

skat

oon

Cal

gary

- K

elow

na

Cal

gary

- R

egin

a

Cal

gary

- V

icto

ria

Prin

ce G

eorg

e - V

anco

uver

% o

f Sea

t Cap

acity

Porter Air Canada WestJet Other

Eastern Routes Western Routes

(1) Source: Official Airline Guide.

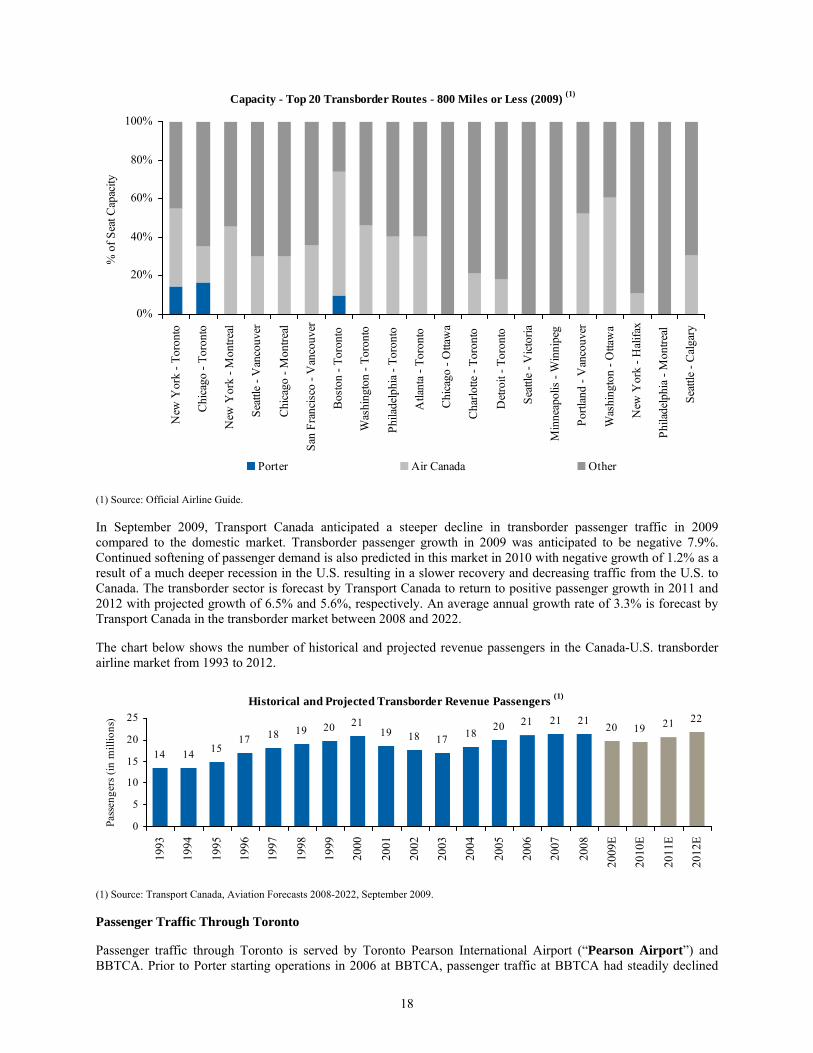

Transborder Market

In 2009, there were approximately 445,000 scheduled transborder flights between Canada and the U.S., or an average of 1,219 per day. Air Canada (together with its contract carrier, Jazz) has the largest market share of transborder flights at 33% with the remainder of the market primarily serviced by WestJet and U.S.-based airlines and their regional affiliates. The chart below illustrates capacity market share (by number of seats) in 2009 of the 20 highest capacity transborder routes that are 800 miles or less.

18

Capacity - Top 20 Transborder Routes - 800 Miles or Less (2009) (1)

0%

20%

40%

60%

80%

100%

New

Yor

k - T

oron

to

Chi

cago

- To

ront

o

New

Yor

k - M

ontre

al

Seat

tle -

Van

couv

er

Chi

cago

- M

ontre

al

San

Fran

cisc

o - V

anco

uver

Bos

ton

- Tor

onto

Was

hing

ton

- Tor

onto

Phila

delp

hia

- Tor

onto

Atla

nta

- Tor

onto

Chi

cago

- O

ttaw

a

Cha

rlotte

- To

ront

o

Det

roit

- Tor

onto

Seat

tle -

Vic

toria

Min

neap

olis

- W

inni

peg

Portl

and

- Van

couv

er

Was

hing

ton

- Otta

wa

New

Yor

k - H

alifa

x

Phila

delp

hia

- Mon

treal

Seat

tle -

Cal

gary

% o

f Sea

t Cap

acity

Porter Air Canada Other

(1) Source: Official Airline Guide.

In September 2009, Transport Canada anticipated a steeper decline in transborder passenger traffic in 2009 compared to the domestic market. Transborder passenger growth in 2009 was anticipated to be negative 7.9%. Continued softening of passenger demand is also predicted in this market in 2010 with negative growth of 1.2% as a result of a much deeper recession in the U.S. resulting in a slower recovery and decreasing traffic from the U.S. to Canada. The transborder sector is forecast by Transport Canada to return to positive passenger growth in 2011 and 2012 with projected growth of 6.5% and 5.6%, respectively. An average annual growth rate of 3.3% is forecast by Transport Canada in the transborder market between 2008 and 2022.

The chart below shows the number of historical and projected revenue passengers in the Canada-U.S. transborder airline market from 1993 to 2012.

Historical and Projected Transborder Revenue Passengers (1)

14 14 1517 18 19 20 21

19 18 17 18 20 21 21 21 20 19 21 22

0

5

10

15

20

25

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

E

2010

E

2011

E

2012

E

Pass

enge

rs (i

n m

illio

ns)

(1) Source: Transport Canada, Aviation Forecasts 2008-2022, September 2009.

Passenger Traffic Through Toronto

Passenger traffic through Toronto is served by Toronto Pearson International Airport (“Pearson Airport”) and BBTCA. Prior to Porter starting operations in 2006 at BBTCA, passenger traffic at BBTCA had steadily declined

19

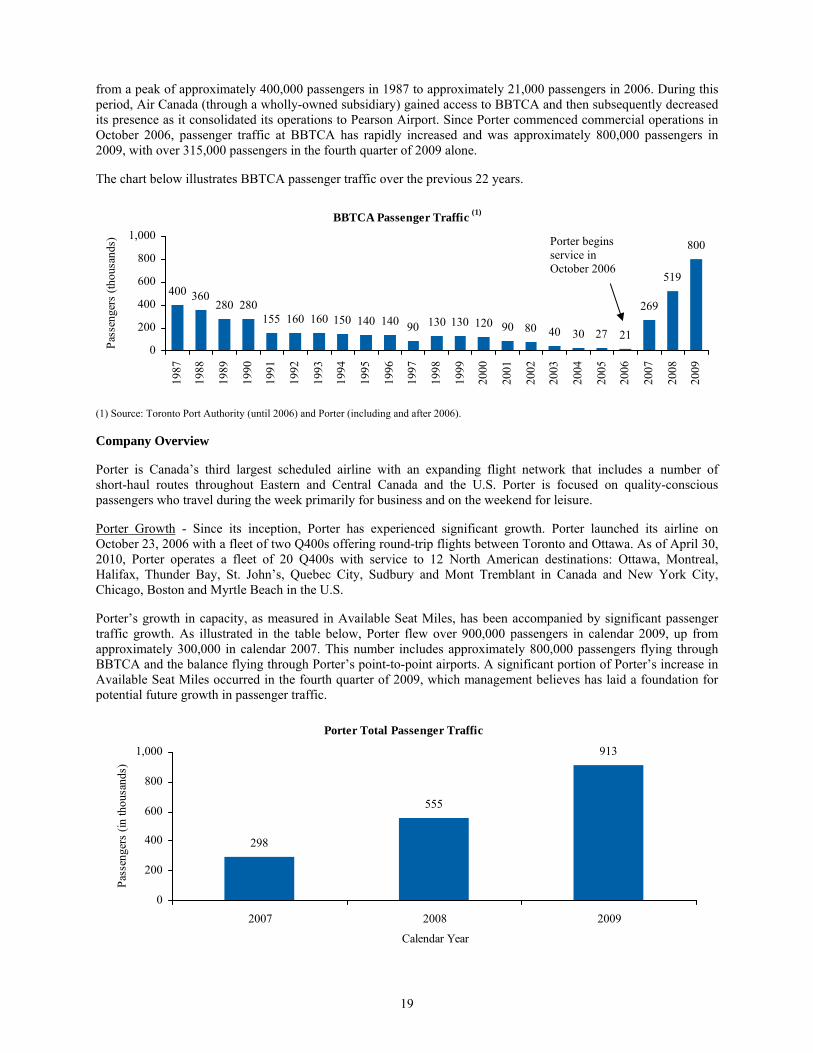

from a peak of approximately 400,000 passengers in 1987 to approximately 21,000 passengers in 2006. During this period, Air Canada (through a wholly-owned subsidiary) gained access to BBTCA and then subsequently decreased its presence as it consolidated its operations to Pearson Airport. Since Porter commenced commercial operations in October 2006, passenger traffic at BBTCA has rapidly increased and was approximately 800,000 passengers in 2009, with over 315,000 passengers in the fourth quarter of 2009 alone.

The chart below illustrates BBTCA passenger traffic over the previous 22 years.

BBTCA Passenger Traffic (1)

400 360280 280

155 160 160 150 140 140 90 130 130 120 90 80 40 30 27 21

269

519

800

0

200

400

600

800

1,000

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Pass

enge

rs (t

hous

ands

)

(1) Source: Toronto Port Authority (until 2006) and Porter (including and after 2006).

Company Overview

Porter is Canada’s third largest scheduled airline with an expanding flight network that includes a number of short-haul routes throughout Eastern and Central Canada and the U.S. Porter is focused on quality-conscious passengers who travel during the week primarily for business and on the weekend for leisure.

Porter Growth - Since its inception, Porter has experienced significant growth. Porter launched its airline on October 23, 2006 with a fleet of two Q400s offering round-trip flights between Toronto and Ottawa. As of April 30, 2010, Porter operates a fleet of 20 Q400s with service to 12 North American destinations: Ottawa, Montreal, Halifax, Thunder Bay, St. John’s, Quebec City, Sudbury and Mont Tremblant in Canada and New York City, Chicago, Boston and Myrtle Beach in the U.S.

Porter’s growth in capacity, as measured in Available Seat Miles, has been accompanied by significant passenger traffic growth. As illustrated in the table below, Porter flew over 900,000 passengers in calendar 2009, up from approximately 300,000 in calendar 2007. This number includes approximately 800,000 passengers flying through BBTCA and the balance flying through Porter’s point-to-point airports. A significant portion of Porter’s increase in Available Seat Miles occurred in the fourth quarter of 2009, which management believes has laid a foundation for potential future growth in passenger traffic.

Porter Total Passenger Traffic

298

555

913

0

200

400

600

800

1,000

2007 2008 2009

Calendar Year

Pass

enge

rs (i

n th

ousa

nds)

Porter begins service in October 2006

20

BBTCA - Porter’s hub airport, BBTCA, is located approximately three kilometres from Toronto’s downtown core and Canada’s primary financial district. Porter’s wholly-owned subsidiary, City Centre Terminal Corp. (“CCTC”), has exclusive rights to develop and operate terminal space at BBTCA. In February 2010, CCTC completed the first phase of construction, comprising approximately 75% of the total $49 million new terminal. The terminal, which measures approximately 150,000 square feet, is designed to accommodate more than two million passengers annually. The remainder of the new facility is scheduled to be completed by the end of 2010. The new terminal will feature both domestic and transborder lounges, as well as check-in and baggage claim areas. Space has been allocated for future concession opportunities, including duty-free shopping, car rental, ATM and food, beverage and convenience outlets.