Embed Size (px)

Citation preview

Port Terminal Operations Tomorrow Port investment and operations in the era of mega carriers and contested markets EATON SMART HONG KONG HOTEL 19 October 2012

Dr Jonathan Beard, Eric Jin Xiaobin, Jolke Helbing, Jamie Simpson

Productivity – squeezing the most from what

you have − Port reform − What to measure − Impact of market forces

Meeting carrier requirements − Infrastructure & service requirements − Transhipment markets

Financing expansion: adapting to uncertainty & risk − Focus on efficiency and competition − New sources of finance − Securing the hinterland

Context

icfi.com | ghkint.com icfi.com | ghkint.com

Port Performance

Global performance metric:

India – Nhava Sheva BOT Productivity 3x versus the state run alternatives Greater reliability & service levels

South China Private sector negotiated concessions with international terminal

operators (ITOs) Stimulate competition by multiple operators Most productive terminals in the world

1960s 2000s Productivity (‘000 mt/m of quay/yr) ~1,000 20,000+ % of ocean going ship time in port 60% 25%

Improvements across a range of markets

icfi.com | ghkint.com icfi.com | ghkint.com

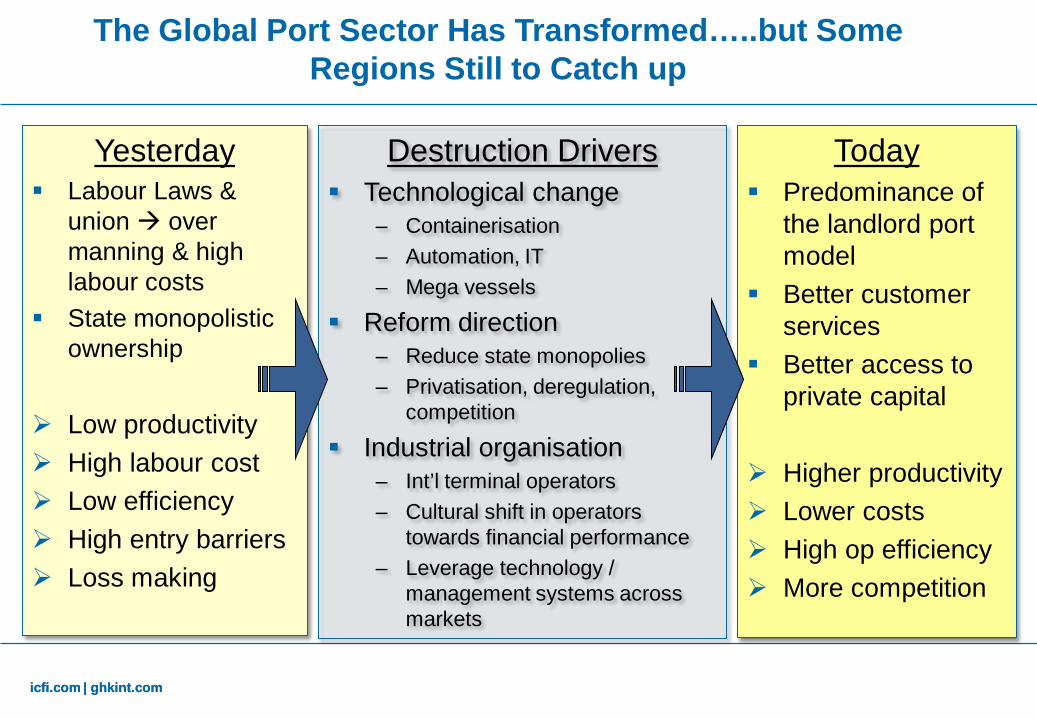

Today Predominance of

the landlord port model

Better customer services

Better access to private capital

Higher productivity Lower costs High op efficiency More competition

Yesterday Labour Laws &

union over manning & high labour costs

State monopolistic ownership

Low productivity High labour cost Low efficiency High entry barriers Loss making

Destruction Drivers Technological change

– Containerisation – Automation, IT – Mega vessels

Reform direction – Reduce state monopolies – Privatisation, deregulation,

competition

Industrial organisation – Int’l terminal operators – Cultural shift in operators

towards financial performance – Leverage technology /

management systems across markets

The Global Port Sector Has Transformed…..but Some Regions Still to Catch up

icfi.com | ghkint.com

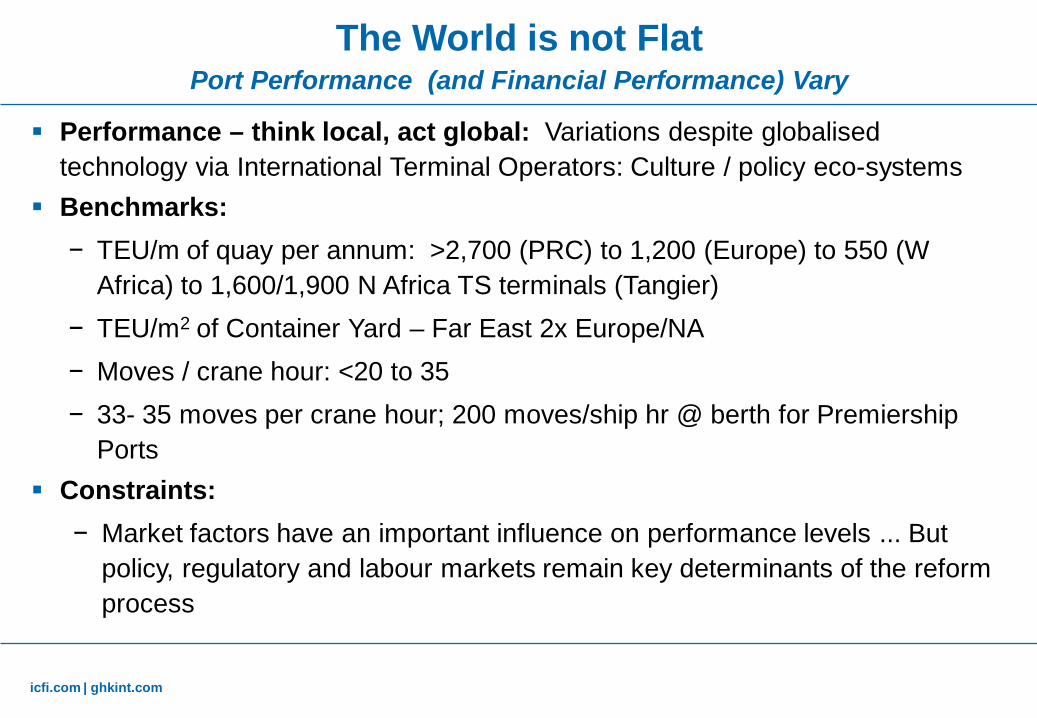

The World is not Flat Port Performance (and Financial Performance) Vary

Performance – think local, act global: Variations despite globalised technology via International Terminal Operators: Culture / policy eco-systems

Benchmarks: − TEU/m of quay per annum: >2,700 (PRC) to 1,200 (Europe) to 550 (W

Africa) to 1,600/1,900 N Africa TS terminals (Tangier) − TEU/m2 of Container Yard – Far East 2x Europe/NA − Moves / crane hour: <20 to 35 − 33- 35 moves per crane hour; 200 moves/ship hr @ berth for Premiership

Ports Constraints:

− Market factors have an important influence on performance levels ... But policy, regulatory and labour markets remain key determinants of the reform process

icfi.com | ghkint.com icfi.com | ghkint.com

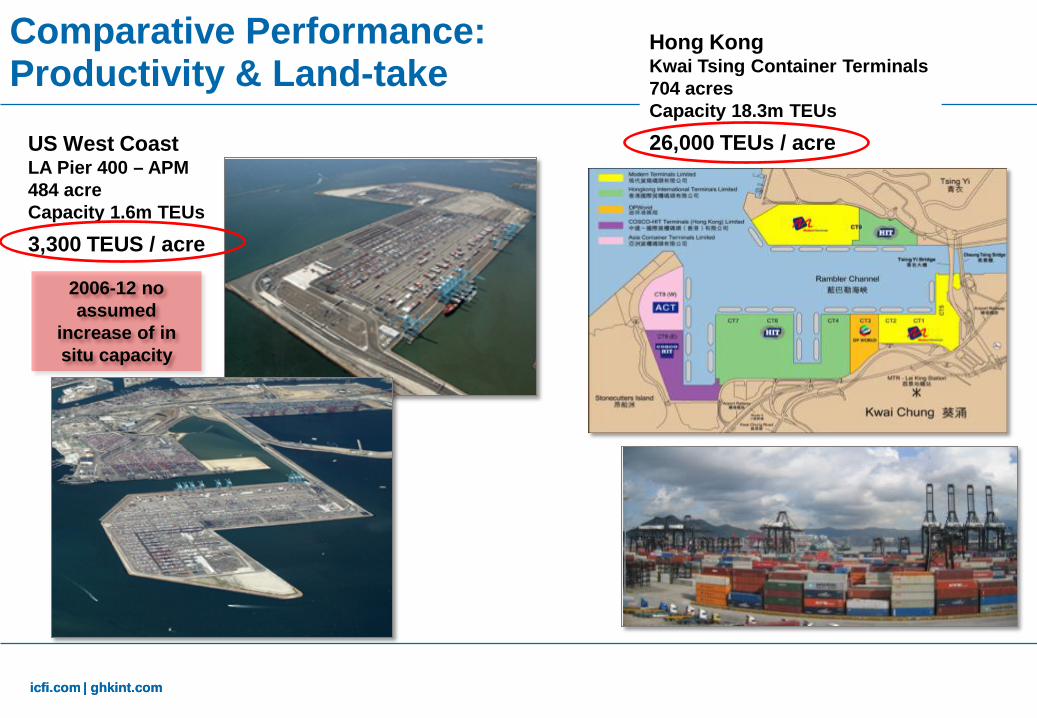

Hong Kong Kwai Tsing Container Terminals 704 acres Capacity 18.3m TEUs

26,000 TEUs / acre

US West Coast LA Pier 400 – APM 484 acre Capacity 1.6m TEUs

3,300 TEUS / acre

Comparative Performance: Productivity & Land-take

2006-12 no assumed

increase of in situ capacity

icfi.com | ghkint.com icfi.com | ghkint.com

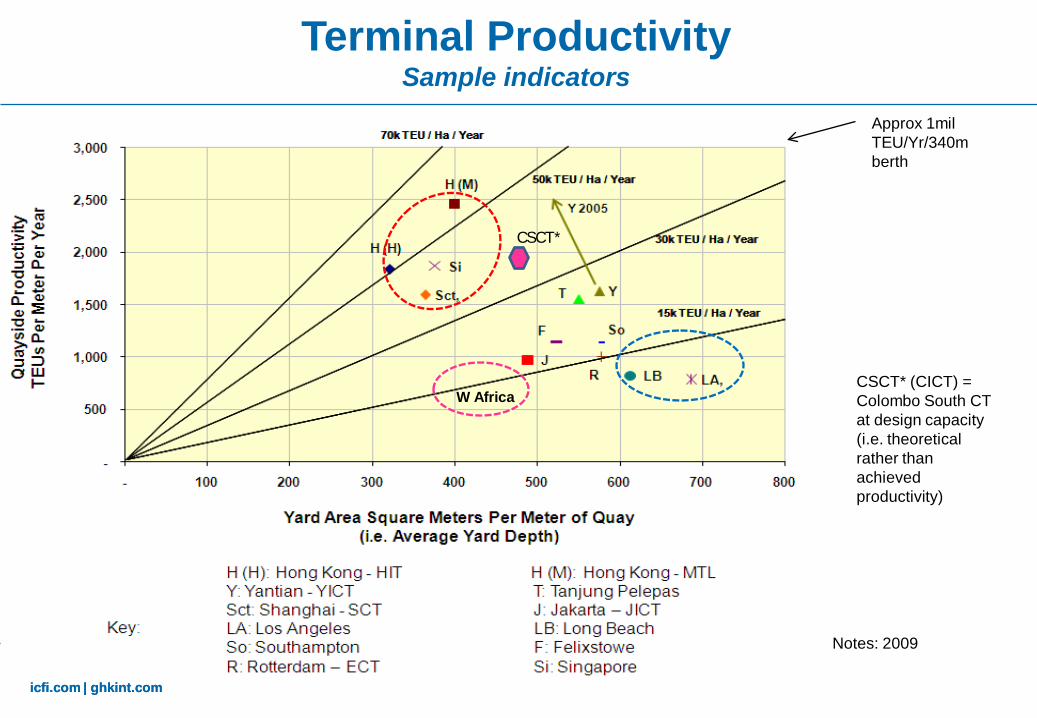

Terminal Productivity Sample indicators

Notes: 2009

Approx 1mil TEU/Yr/340m berth

CSCT*

CSCT* (CICT) = Colombo South CT at design capacity (i.e. theoretical rather than achieved productivity)

W Africa

icfi.com | ghkint.com

Trade & Vessel Mix are Key Port Performance Drivers

icfi.com | ghkint.com icfi.com | ghkint.com

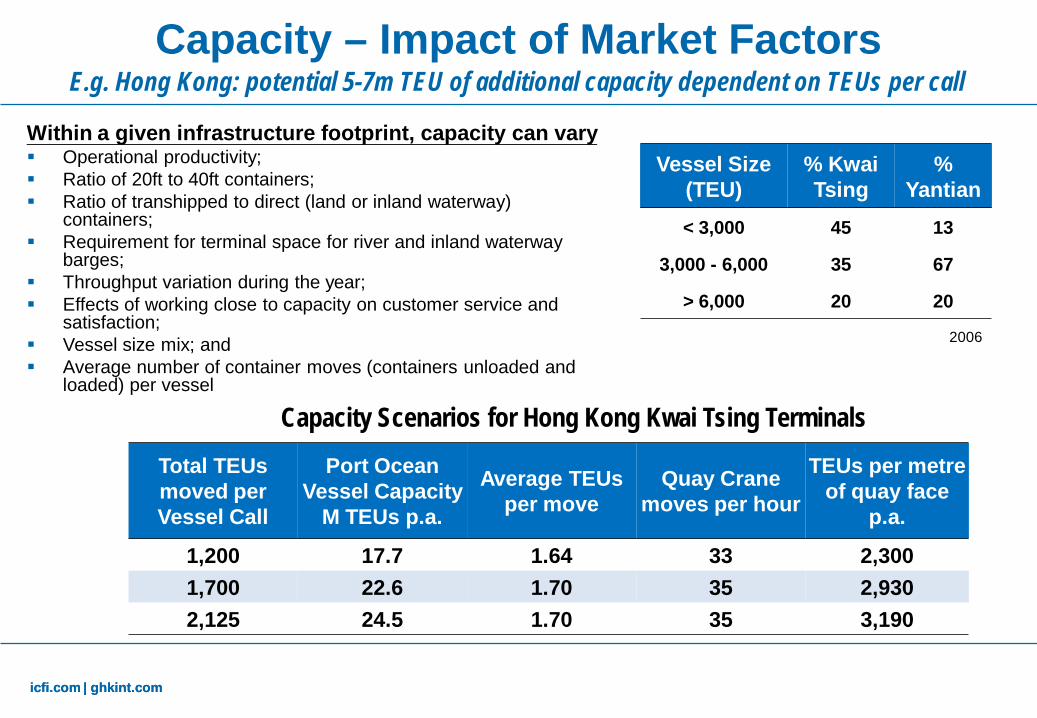

Capacity – Impact of Market Factors

Capacity Scenarios for Hong Kong Kwai Tsing Terminals

E.g. Hong Kong: potential 5-7m TEU of additional capacity dependent on TEUs per call

Vessel Size (TEU)

% Kwai Tsing

% Yantian

< 3,000 45 13

3,000 - 6,000 35 67

> 6,000 20 20

Total TEUs moved per Vessel Call

Port Ocean Vessel Capacity

M TEUs p.a.

Average TEUs per move

Quay Crane moves per hour

TEUs per metre of quay face

p.a.

1,200 17.7 1.64 33 2,300 1,700 22.6 1.70 35 2,930 2,125 24.5 1.70 35 3,190

Within a given infrastructure footprint, capacity can vary Operational productivity; Ratio of 20ft to 40ft containers; Ratio of transhipped to direct (land or inland waterway)

containers; Requirement for terminal space for river and inland waterway

barges; Throughput variation during the year; Effects of working close to capacity on customer service and

satisfaction; Vessel size mix; and Average number of container moves (containers unloaded and

loaded) per vessel

2006

icfi.com | ghkint.com icfi.com | ghkint.com

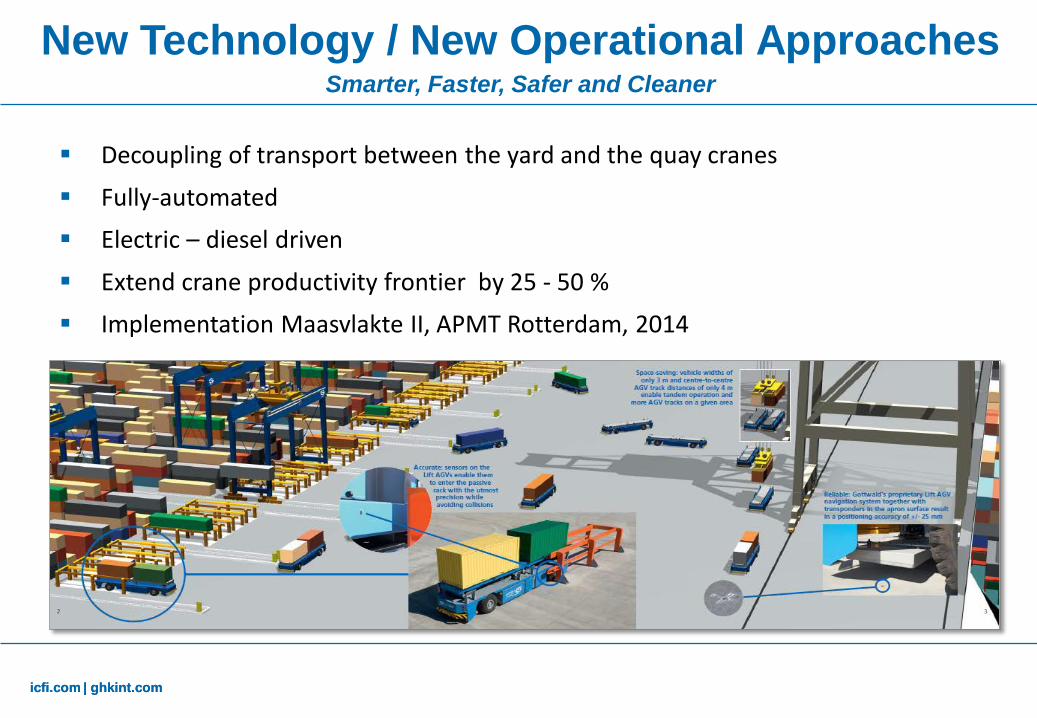

New Technology / New Operational Approaches Smarter, Faster, Safer and Cleaner

Decoupling of transport between the yard and the quay cranes

Fully-automated

Electric – diesel driven

Extend crane productivity frontier by 25 - 50 %

Implementation Maasvlakte II, APMT Rotterdam, 2014

Productivity – squeezing the most from what

you have − Port reform − What to measure − Impact of market forces

Meeting carrier requirements − Infrastructure & service requirements − Transhipment markets

Financing expansion: adapting to uncertainty & risk − Focus on efficiency and competition − New sources of finance − Securing the hinterland

Context

icfi.com | ghkint.com icfi.com | ghkint.com

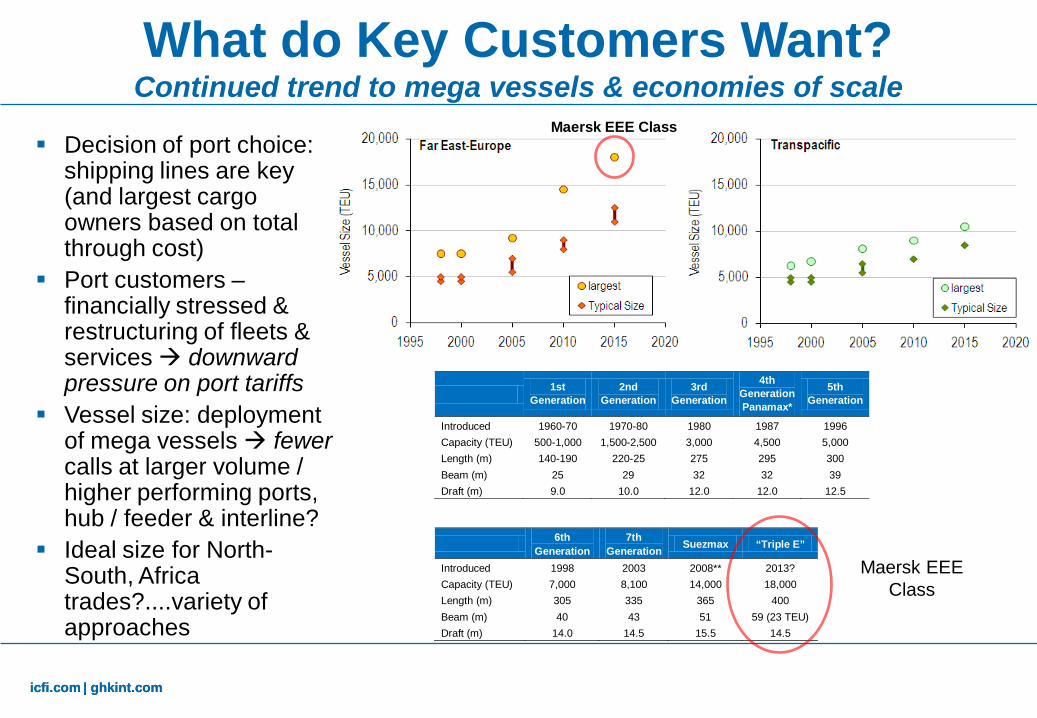

1st Generation

2nd Generation

3rd Generation

4th GenerationPanamax*

5th Generation

Introduced 1960-70 1970-80 1980 1987 1996 Capacity (TEU) 500-1,000 1,500-2,500 3,000 4,500 5,000 Length (m) 140-190 220-25 275 295 300 Beam (m) 25 29 32 32 39 Draft (m) 9.0 10.0 12.0 12.0 12.5

6th Generation

7th Generation Suezmax “Triple E”

Introduced 1998 2003 2008** 2013? Capacity (TEU) 7,000 8,100 14,000 18,000 Length (m) 305 335 365 400 Beam (m) 40 43 51 59 (23 TEU) Draft (m) 14.0 14.5 15.5 14.5

Decision of port choice: shipping lines are key (and largest cargo owners based on total through cost)

Port customers – financially stressed & restructuring of fleets & services downward pressure on port tariffs

Vessel size: deployment of mega vessels fewer calls at larger volume / higher performing ports, hub / feeder & interline?

Ideal size for North-South, Africa trades?....variety of approaches

Maersk EEE Class

Maersk EEE Class

What do Key Customers Want? Continued trend to mega vessels & economies of scale

icfi.com | ghkint.com

To Play the Game You Must Invest “Build it and they will come?”…but no guarantees biggest vessels will call

• Major shipping lines demand performance gains – 30+ moves per crane hour: 200 moves/ship hr @ berth for larger vessels – Reliable berth windows and turnaround time

• CAPEX for mega-vessels – 16-17m water depth – long straight quays (1,200 – 2,000 m) – outreach for 24 across – land (25ha/400m berth) – inland connectivity (for gateway ports)

• Major hub (and some gateway) ports must efficiently accommodate a variety of vessels sizes (e.g. from feeder / barges to mother vessels) - flexibility in design

• Risk/reward: investment requirements are higher but in the absence of significant Import/Export (I/E) cargo, incentives for largest vessels to call may be insufficient – challenge for transhipment hubs

icfi.com | ghkint.com icfi.com | ghkint.com

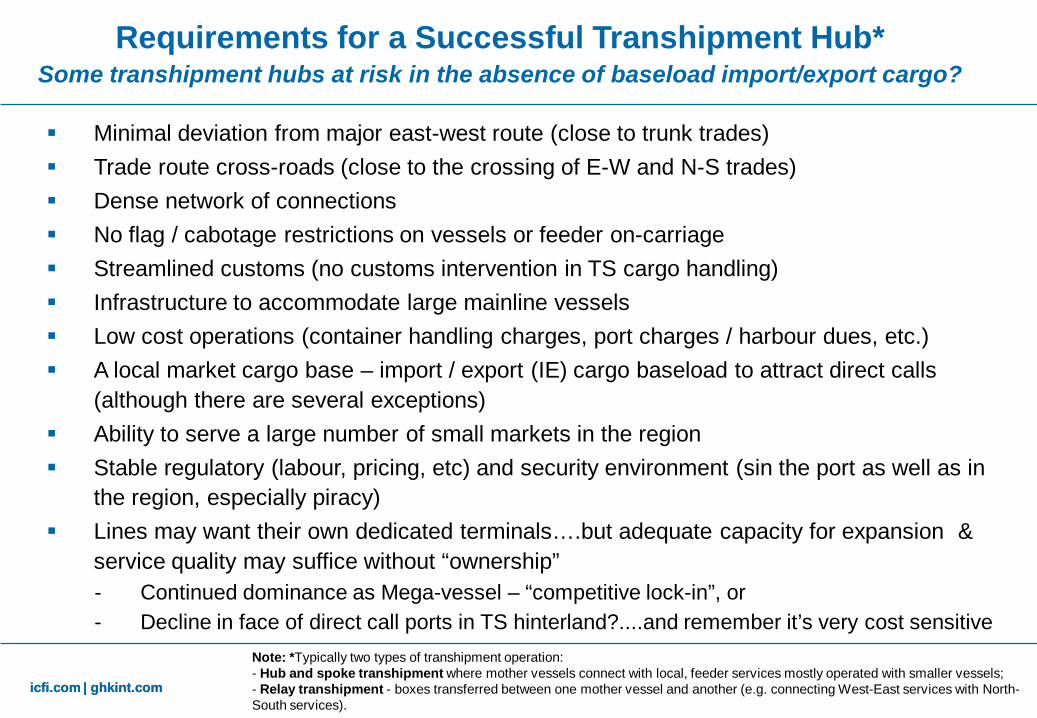

Requirements for a Successful Transhipment Hub* Some transhipment hubs at risk in the absence of baseload import/export cargo?

Note: *Typically two types of transhipment operation: - Hub and spoke transhipment where mother vessels connect with local, feeder services mostly operated with smaller vessels; - Relay transhipment - boxes transferred between one mother vessel and another (e.g. connecting West-East services with North-South services).

Minimal deviation from major east-west route (close to trunk trades) Trade route cross-roads (close to the crossing of E-W and N-S trades) Dense network of connections No flag / cabotage restrictions on vessels or feeder on-carriage Streamlined customs (no customs intervention in TS cargo handling) Infrastructure to accommodate large mainline vessels Low cost operations (container handling charges, port charges / harbour dues, etc.) A local market cargo base – import / export (IE) cargo baseload to attract direct calls

(although there are several exceptions) Ability to serve a large number of small markets in the region Stable regulatory (labour, pricing, etc) and security environment (sin the port as well as in

the region, especially piracy) Lines may want their own dedicated terminals….but adequate capacity for expansion &

service quality may suffice without “ownership” - Continued dominance as Mega-vessel – “competitive lock-in”, or - Decline in face of direct call ports in TS hinterland?....and remember it’s very cost sensitive

icfi.com | ghkint.com icfi.com | ghkint.com

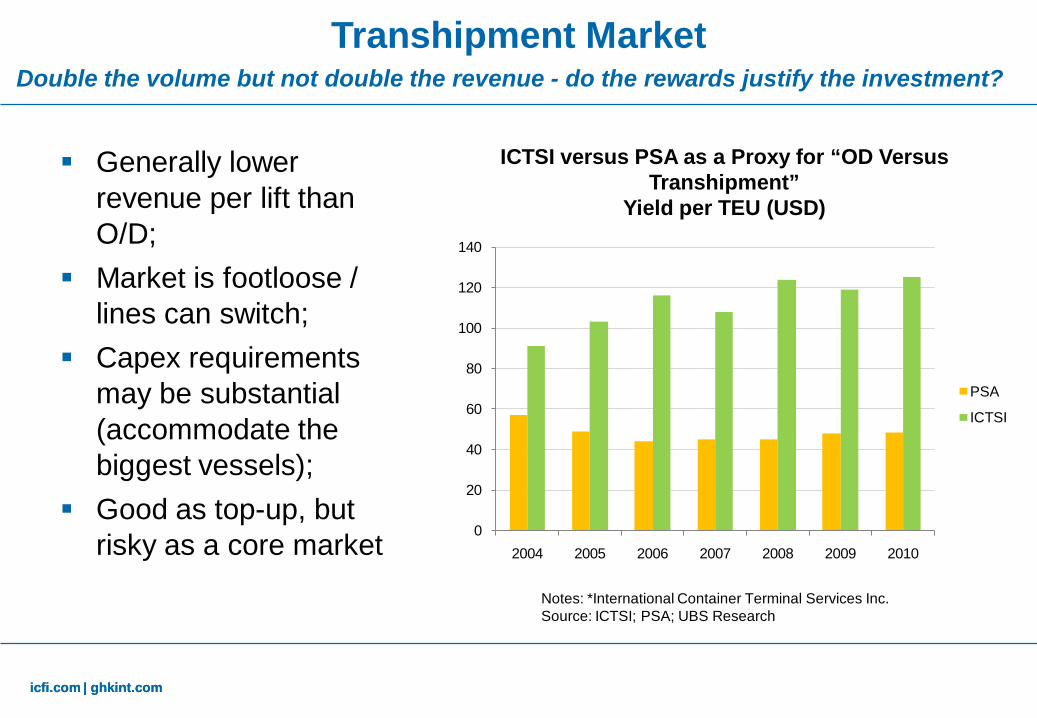

Transhipment Market Double the volume but not double the revenue - do the rewards justify the investment?

Generally lower revenue per lift than O/D;

Market is footloose / lines can switch;

Capex requirements may be substantial (accommodate the biggest vessels);

Good as top-up, but risky as a core market Notes: *International Container Terminal Services Inc.

Source: ICTSI; PSA; UBS Research

ICTSI versus PSA as a Proxy for “OD Versus Transhipment”

Yield per TEU (USD)

0

20

40

60

80

100

120

140

2004 2005 2006 2007 2008 2009 2010

PSA

ICTSI

Productivity – squeezing the most from what

you have − Port reform − What to measure − Impact of market forces

Meeting carrier requirements − Infrastructure & service requirements − Transhipment markets

Financing expansion: adapting to uncertainty & risk − Focus on efficiency and competition − New sources of finance − Securing the hinterland

Context

icfi.com | ghkint.com icfi.com | ghkint.com

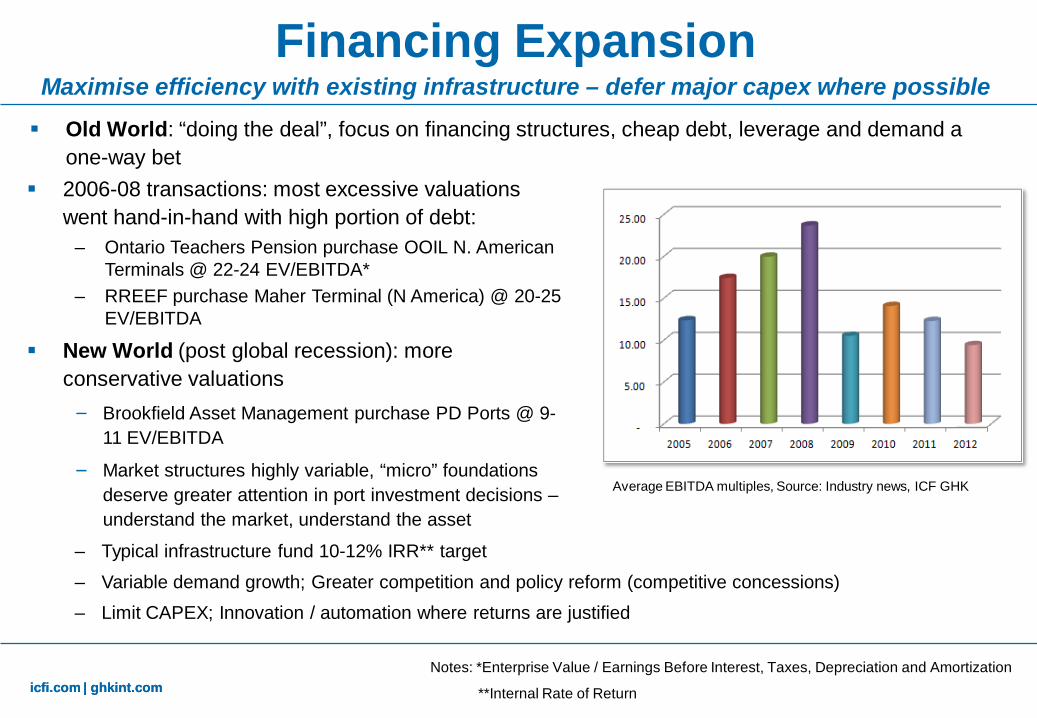

Financing Expansion Maximise efficiency with existing infrastructure – defer major capex where possible Old World: “doing the deal”, focus on financing structures, cheap debt, leverage and demand a

one-way bet

Notes: *Enterprise Value / Earnings Before Interest, Taxes, Depreciation and Amortization

**Internal Rate of Return

2006-08 transactions: most excessive valuations went hand-in-hand with high portion of debt:

– Ontario Teachers Pension purchase OOIL N. American Terminals @ 22-24 EV/EBITDA*

– RREEF purchase Maher Terminal (N America) @ 20-25 EV/EBITDA

New World (post global recession): more conservative valuations − Brookfield Asset Management purchase PD Ports @ 9-

11 EV/EBITDA

− Market structures highly variable, “micro” foundations deserve greater attention in port investment decisions – understand the market, understand the asset

– Typical infrastructure fund 10-12% IRR** target

– Variable demand growth; Greater competition and policy reform (competitive concessions) – Limit CAPEX; Innovation / automation where returns are justified

Average EBITDA multiples, Source: Industry news, ICF GHK

icfi.com | ghkint.com icfi.com | ghkint.com

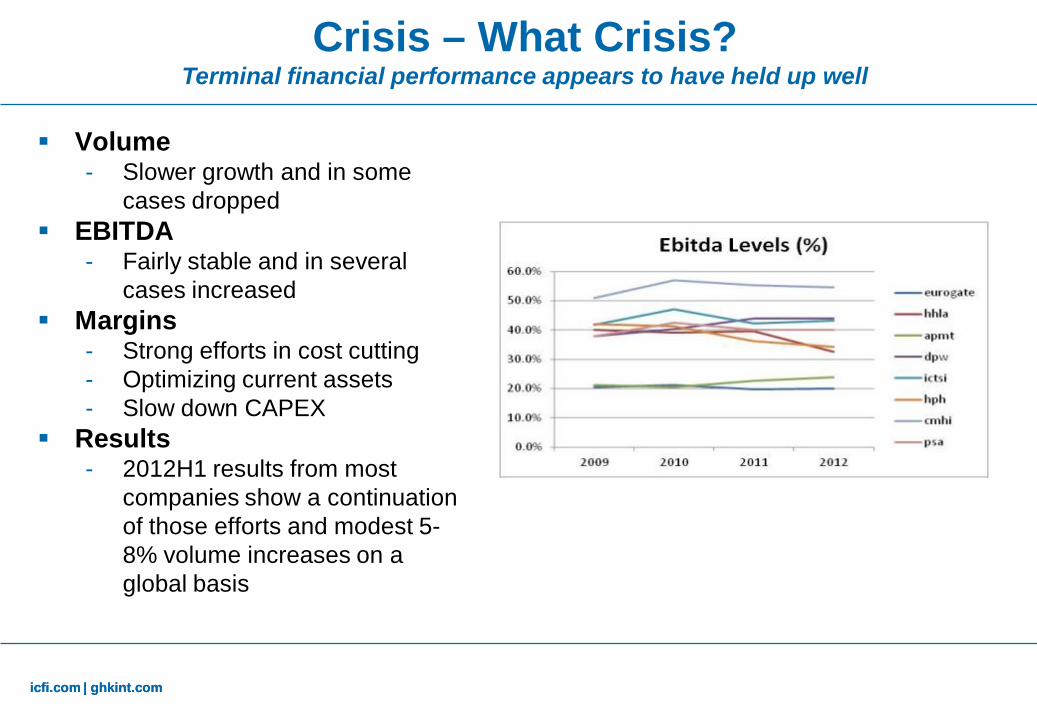

Crisis – What Crisis? Terminal financial performance appears to have held up well

Volume - Slower growth and in some

cases dropped EBITDA

- Fairly stable and in several cases increased

Margins - Strong efforts in cost cutting - Optimizing current assets - Slow down CAPEX

Results - 2012H1 results from most

companies show a continuation of those efforts and modest 5-8% volume increases on a global basis

icfi.com | ghkint.com icfi.com | ghkint.com

New Sources of Finance Pension funds / asset managers: e.g. Ontario Teachers Pension Fund, Brookfield Asset

Management, Sovereign Wealth Funds, etc. Long investment horizons – pensions seeking less volatility, inflation protection &

diversification: infrastructure should be favoured…. but still an immature asset class Institutional investors (including pension) 2009 alternative investment allocations*

– Hedge funds, real estate & private equity 86% – Infrastructure 2% – Infrastructure by 2012 plan to increase to 6%

Source: *Russell Investments’ 2010 Global Survey on Alternative Investing

*Weisdorf: Infrastructure will be as big as real estate The managing director and chief executive of JPMorgan Asset Management’s Infrastructure Investments Group says he believes infrastructure is the ‘Holy Grail’ for institutional investors and could represent as large a slice of investor portfolios as real estate within 10 to 15 years. (Infrastructure Investor, October 2011)

Full / majority investment or minority investors partnering world class operators?

N American funds most proactive in infrastructure, but geographical focus on N America, EU and Latin America – Asia, Gulf barely touched.

Shipping lines returning to the fray (e.g. Cosco)… long-term commitment? Chinese operators going global: Shanghai International Port Group, China Merchants Smaller international operators, e.g. ICTSI, Gulftainer

icfi.com | ghkint.com

You’re only as good as the weakest link

…and terminal operators do not control all the supply chain links

OPERATIONS NEAR PORT ‘PUBLIC-PRIVATE PARTNERSHIP’ OPERATIONS AT PORT

‘CUSTOMER FOCUS’

Quay Yard

IT

• Road • Inland shipping • shortsea feeder • International

trans-shipment • (Pipelines)

OPERATIONS AWAY FROM PORT

‘SECURING THE HINTERLAND’

Support facilities • Customs • Bank, Insurance, Legal • Freight forwarders, etc.

Infrastructure • Logistics parks • River-road centre • Rail-road centre, etc.

Maritime • Navigation channels • Piloting / towage • Ship repair, etc.

‘SEAMLESS CARGO MOVEMENT’

GOVERNMENT PARTNERSHIP

LOCAL REGIONAL NATIONAL

icfi.com | ghkint.com icfi.com | ghkint.com

Hamburg - HHLA direct involvement in rail services to large part

of the hinterland own trucking services network of inland depots

Rotterdam – ECT large inland depot network (focus on barges

and rail connectivity) Cargo acceptance at the depots Direct investments Operational involvement no rail investments (but service agreements)

Strategy: Reaching Out

icfi.com | ghkint.com icfi.com | ghkint.com

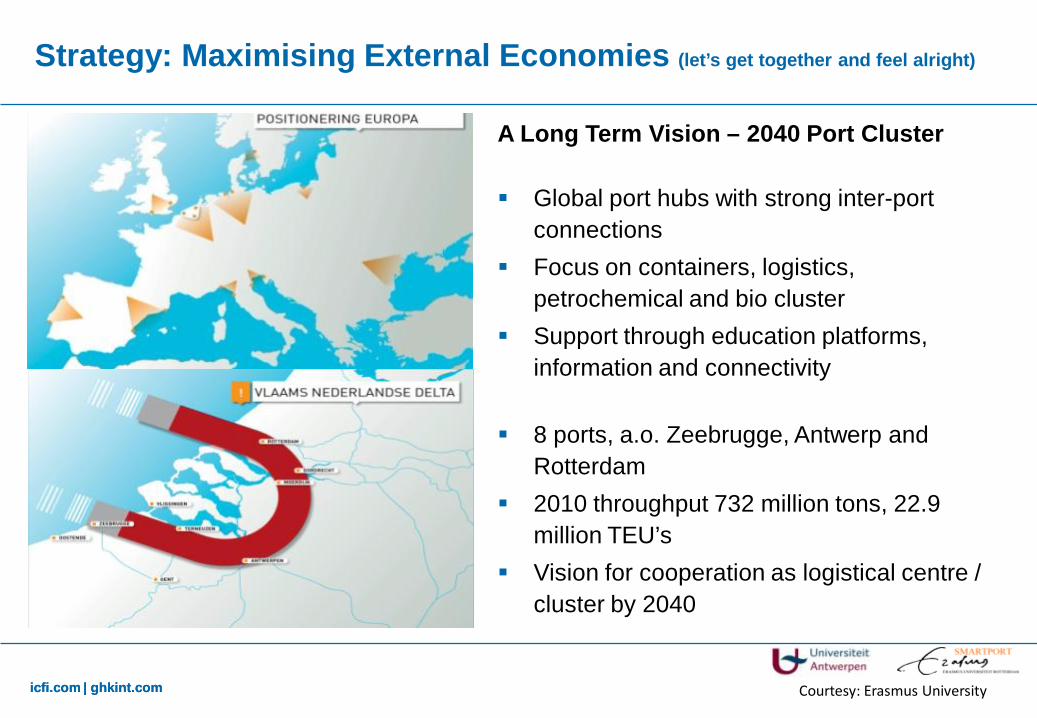

A Long Term Vision – 2040 Port Cluster Global port hubs with strong inter-port

connections Focus on containers, logistics,

petrochemical and bio cluster Support through education platforms,

information and connectivity 8 ports, a.o. Zeebrugge, Antwerp and

Rotterdam 2010 throughput 732 million tons, 22.9

million TEU’s Vision for cooperation as logistical centre /

cluster by 2040

Strategy: Maximising External Economies (let’s get together and feel alright)

Courtesy: Erasmus University

icfi.com | ghkint.com

Wrap: Improving Efficiency – “win-win” Ports are lumpy investments; significant environmental foot-print Emerging economies require substantial new-build, but must also focus on

improved efficiency within and outside terminal: “win-win” in terms of commercial and environmental performance – Enhancing terminal productivity: systems and operations – labour & regulatory

regime is critical – Enhancing efficiency of inland connectivity: trucking, barging….and rail (long-tem) – Regulatory – streamline labour, customs & trade regulations; stable & transparent

operational regime – Full allocation of costs to private sector wherever possible – Level playing field – terminal operators to compete / no collusion on price – Supplement with higher environmental standards: e.g. higher quality bunker fuel,

electrification of yard equipment, etc. Finance for acquisition / expansion increasingly focused on efficiency and better

appreciation of market risks Remember the primary objective for gateway ports: reduce costs for importers &

exporters

icfi.com | ghkint.com icfi.com | ghkint.com

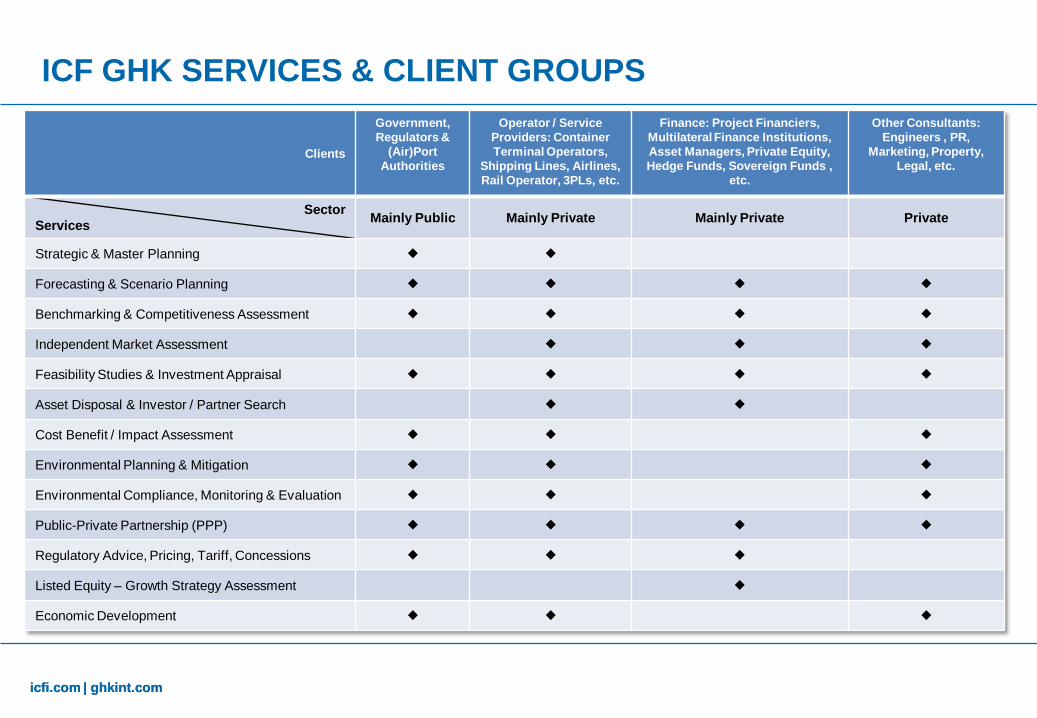

Clients

Government, Regulators &

(Air)Port Authorities

Operator / Service Providers: Container Terminal Operators,

Shipping Lines, Airlines, Rail Operator, 3PLs, etc.

Finance: Project Financiers, Multilateral Finance Institutions, Asset Managers, Private Equity, Hedge Funds, Sovereign Funds ,

etc.

Other Consultants: Engineers , PR,

Marketing, Property, Legal, etc.

Sector Services Mainly Public Mainly Private Mainly Private Private

Strategic & Master Planning

Forecasting & Scenario Planning

Benchmarking & Competitiveness Assessment

Independent Market Assessment

Feasibility Studies & Investment Appraisal

Asset Disposal & Investor / Partner Search

Cost Benefit / Impact Assessment

Environmental Planning & Mitigation

Environmental Compliance, Monitoring & Evaluation

Public-Private Partnership (PPP)

Regulatory Advice, Pricing, Tariff, Concessions

Listed Equity – Growth Strategy Assessment

Economic Development

ICF GHK SERVICES & CLIENT GROUPS

icfi.com | ghkint.com

ICF GHK - Selected Clients

Tiger Global Management, LLC

ICF GHK - Selected Clients

icfi.com | ghkint.com

Thank You – Any Questions?

Hong Kong 19th Floor Heng Shan Centre

145 Queen's Road East Wanchai, Hong Kong

T +852 2868 6980 F +852 2530 4302

London Clerkenwell House

67 Clerkenwell Road London, EC1R 5BL

T +44 (0)20 7611 1100 F +44 (0)20 7368 6960

Beijing China Overseas Plaza, Central Tower

20th Floor, Suite 2001 No. 8 Guanghua Dongli

Chaoyang District Beijing, China 100020 CN

T +86 10 6562 8300 F +86 10 6562 8301

Boston One Main Street

Cambridge, MA 02142 T + 1 617 218 3540 F + 1 617 218 3600

Delhi M-66 GK II 2nd Floor Near M Block Market

New Delhi 110048, India T + 91 11 2696 9553 F + 91 11 2696 6478