Embed Size (px)

Citation preview

PoolingBasics Spring2017

RecommendedSessionsforPoolingBasicsTrack:ParliamentaryProceduresforPoolBoards,Part1 Monday,March6,9:45-11:00amParliamentaryProceduresforPoolBoards,Part2 Monday,March6,11:15-12:00pmGoverningfortheFuture Monday,March6,1:45-3:00pmTheBoardofDirectorsPipeline Monday,March6,3:15-4:30pmPoolingBasicsSession,Part1 Tuesday,March7,8:45-9:45amPoolingBasicsSession,Part2 Tuesday,March7,10:00-11:15pmPoolingBasicsSession,Part3 Tuesday,March7,11:30-12:30pmPoolingBasicsSession,Part4 Tuesday,March7,2:15-3:00pmPoolingBasicsSession,Part5 Tuesday,March7,3:15-4:15pm

PresentationDescriptionOverthecourseafullday,solidifyyourpoolingbasicsknowledgewithseveralsessionstocomplementAGRiP’sonlinecoursework.BasicssessionswillcoverageUnderwriting,ActuarialScience,theClaimsFunction,FinancialReporting,Auditing,andRiskManagement.Therewillalsobecomplimentarysessions(onMonday),whichwillcovergovernanceandleadershiproles.TherewillbeplentyoftimeforQuestions&AnswersforthePoolingexpertslineduptodispensetheirknowledgeandexperience.

PresentationSoftware[MainPresentation]http://prezi.com/kmedwqqx4eka/?utm_campaign=share&utm_medium=copy&rc=ex0share

[Claims]http://prezi.com/g5vnkt7ffaal/?utm_campaign=share&utm_medium=copy

TableofContentsRecommendedSessionsforPoolingBasicsTrack: 1

PresentationDescription 1

PresentationSoftware 1

Presenters 2

HistoryofInsurancein60seconds 3

PoolingBackground 4

ActuarialScience 8

FinancialReportingandAuditing 9

Claims 12

Underwriting 14

RiskManagement/LossControl 16

TheFutureofPublicEntityPooling 17

Presenters

JoelKress,AGRiPStaff [email protected];603.568.4880JoelKresscurrentlyservesasDirectorofSpecialProjectsforAGRiP.Amongsthisotherprojects,heisupdatingPoolingBasicstobeincludedinaholisticinitiativeknownas‘PoolingAcademy’.Althoughinitsinfancy,PoolingAcademywillwrapupalleducationalinitiativesinthepoolingsector,andstandardizetheeducationalrequirementsforthoseseekingpoolmanagement.

Previously,Mr.KressservedasUnderwritingManagerforGovernmentEntitiesMutual,Inc.PCC,providingreinsuranceunderwritingandactuarialanalyticalservices,aswellascomputerprogrammingfortheclaimsmanagementinformationsystem.PrevioustoGEM,Mr.Kressworkedforanactuarialconsultingfirmfor5years.HehasreceivedtwoBachelorofSciencedegrees(AppliedMathematicsandMathematicalEducation)fromNorthCarolinaStateUniversity,andaMastersdegree(BusinessAdministration)fromSouthernNewHampshireUniversity.HealsoearnedthedesignationAssociateinReinsurance(ARe).

ThomasMeyer,SelectActuarialServices [email protected];(615)269-4469ThomasMeyerhasmorethan17yearsofproperty/casualtyactuarialconsultingexperienceandisoneofthefoundingmembersofSelectActuarialServices.AsaseniorconsultingactuaryheprovidesexpertservicestoawiderangeofSelectclientshelpingthemmaintainanddesignstrongriskmanagementprograms.Alongwithtraditionalproperty/casualtyactuarialwork,Thomasalsohasexperiencewithmorenon-traditionalcoveragessuchastradecreditrisk,managementrisk,pollution,productliability,andhealthinsurancestoploss.Hisexperiencewiththeselinesincludesreserveanalyses,lossforecasting,probabilityanalyses,ratelevelanalyses,largelossmodeling,andcapitaladequacyanalyses.

Mr.MeyerisaFellowoftheCasualtyActuarialSociety,aMemberoftheAmericanAcademyofActuaries,andamemberoftheCasualtyActuarialSocietyExaminationCommittee.HeobtainedaBachelorofScienceinMathematicsfromtheUniversityofNotreDame.

SherylBrandt,Enduris [email protected];509.838.0910SherylBrandthastheprivilegeofpartneringwithover500specialpurposedistrictsintheStateofWashingtoninapplyingriskmanagementtotheirdailyoperations.ForthepastseveralyearsshehasworkedwithPortDistricts,FireDistricts,HealthDistricts,ConventionCenters,WaterandSewerDistricts,etc.focusingonpropertyandliabilitylosses,litigationmanagementandriskmanagement.Shehaspresentedriskmanagementstrategieswithmunicipalities,districtsandassociations,bothstatewideandnationally.Ms.BrandtisagraduateofOregonStateUniversity,activememberofPRIMAandAGRiP,andiscurrentlyonAGRiP'sMembershipPracticesCommittee.CarrieRice,JohnsonLambertLLP [email protected];802.383.4820CarolynRice,CPAisaPartnerthathasover15yearsofexperienceinpublicaccounting.Carolynprimarilyprovidesauditservicestotheinsuranceindustry.Sheisamemberofthefirm’stechnicalcommitteeandmonitorsallGASBpronouncements.Ms.RicejoinedJohnsonLambertin2003,afterhavingworkedfortwolocalCPAfirmswhereshegainedexperienceinanumberofindustries,includingnot-for-profit,manufacturingandgovernmentalsectors.ShealsoservesontheboardofInternationalCenterforCaptiveInsuranceEducation(ICCIE).CarolynisagraduateoftheUniversityofVermont,isalicensedCPAinVermontandHawaii.

MagaliWelch,JohnsonLambertLLP [email protected];802.383.4820MagaliWelch,CPA,CA,AIAFisaPartnerthathasover20yearsofexperienceinpublicaccounting.Magali'smainfocusisprovidingauditservicesinsuranceindustry.Herresponsibilitiesadditionallyincludeco-chairingJohnsonLambert’sTechnicalCommitteewhichhastheresponsibilityforthefirm-widetraining,implementationofnewstandardsandthetechnicalcontentcontainedontheJohnsonLambertwebsite.Shealsooverseesandcoordinatesthefirm'swebinarsandnewsletters.

PriortojoiningJohnsonLambertin1994,Ms.WelchwaswiththeMontrealaccountingfirmofLacroix,Vaillancourt&AssociatesduringwhichtimesheattainedherCharteredAccountingdesignation.Sherecentlycompletedathree-yeartermontheAICPAInsuranceExpertPanel.Ms.WelchhasobtainedanAssociateinAccountingandFinance(AIAF)designationofferedbytheInsuranceInstituteofAmerica.ShealsocompletedtheInternationalFinancialReportingStandards(IFRS)certificationofferedbytheAICPA.

HistoryofInsurancein60seconds(settothemusicofapopularsong)

Lloyd’sofLondon,teatime,cargoships,maritime;BarnbuildingAmish,Franklin’sFireMutuals;Homesteaderstakearisk,farmers’cropstakeahit;Insurancesalesmengetawrap,sellingonebigmoneytrap.

Exclusions,exclusionseverywhere,regulatorsonatear;ActsofGoddon’tyousay,NFIPsavestheday;Asbestos,blacklungdisease,toxicdumpingkillingtrees;UnderwritersoffScot-free,who’llactuallypayforme.

Wedidn’tstartthe(insurable)fireItwasalwaysburningSincetheworld’sbeenturningWedidn’tstartthe(insurable)fireNo,wedidn’tlightitButwetriedto(compensate)foritStripSearches,eminentdomain,MirandaRightsaresuchapain;HurricaneAndrew,Northridgeearthquake;EliotSpitzerkillsfinite,contingentcommissionsgoodnight;Medicalandsocialinflationequalspremiumescalation;Katrinarainsdownforaweek,NewOrleansspringsaleak;Lehman,AIGcrashes,GreatRecessionlashes;InvestorseyeInsuranceprofit,softmarketbeyondalllogic;UnderwritersoffScot-free,who’llactuallypayforme;Wedidn’tstartthe(insurable)fireItwasalwaysburningSincetheworld’sbeenturningWedidn’tstartthe(insurable)fireNo,wedidn’tlightitButwetriedto(compensate)forit

PoolingBackground

PoolingBasics–FillingthePool

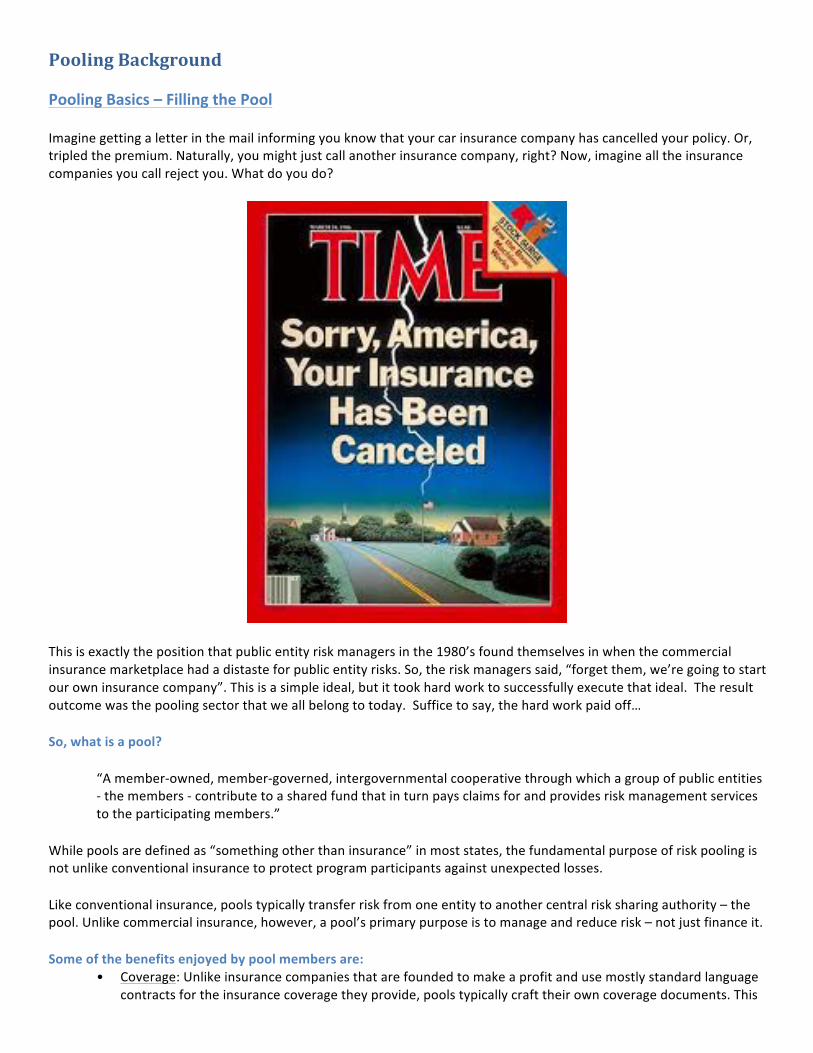

Imaginegettingaletterinthemailinformingyouknowthatyourcarinsurancecompanyhascancelledyourpolicy.Or,tripledthepremium.Naturally,youmightjustcallanotherinsurancecompany,right?Now,imaginealltheinsurancecompaniesyoucallrejectyou.Whatdoyoudo?

Thisisexactlythepositionthatpublicentityriskmanagersinthe1980’sfoundthemselvesinwhenthecommercialinsurancemarketplacehadadistasteforpublicentityrisks.So,theriskmanagerssaid,“forgetthem,we’regoingtostartourowninsurancecompany”.Thisisasimpleideal,butittookhardworktosuccessfullyexecutethatideal.Theresultoutcomewasthepoolingsectorthatweallbelongtotoday.Sufficetosay,thehardworkpaidoff…

So,whatisapool?

“Amember-owned,member-governed,intergovernmentalcooperativethroughwhichagroupofpublicentities-themembers-contributetoasharedfundthatinturnpaysclaimsforandprovidesriskmanagementservicestotheparticipatingmembers.”

Whilepoolsaredefinedas“somethingotherthaninsurance”inmoststates,thefundamentalpurposeofriskpoolingisnotunlikeconventionalinsurancetoprotectprogramparticipantsagainstunexpectedlosses.

Likeconventionalinsurance,poolstypicallytransferriskfromoneentitytoanothercentralrisksharingauthority–thepool.Unlikecommercialinsurance,however,apool’sprimarypurposeistomanageandreducerisk–notjustfinanceit.

Someofthebenefitsenjoyedbypoolmembersare:• Coverage:Unlikeinsurancecompaniesthatarefoundedtomakeaprofitandusemostlystandardlanguage

contractsfortheinsurancecoveragetheyprovide,poolstypicallycrafttheirowncoveragedocuments.This

providesthememberswiththeavailabilityofcoverage,terms,andlimitswhicharebestsuitedtoaddresstherisksofthemembers.

• Services:Riskmanagementistypicallyseenasadetractionfromaninsurancecompany’sbottomline.Thepoolingcommunityhascommittedmuchmorelaborandcapitaltoreduce,mitigate,andpreventlossesfromhappening.Thesecustomizedriskmanagementservicesareprovidedtomeetyourmembers’riskmanagementandadministrationneeds.

• Financialsavings:Reducedlosses,loweroverhead,leverageinthepurchaseofcatastropheinsurance(or“reinsurance”),andinvestmentincomethataccruestothemember-owners,allallowapooltoofferlowercostsoverthelongrunthancommercialinsurance.

• Budgetarystability:Thefinancialadvantages,togetherwithprudentfundingandmembercommitment,hasprovidedgreaterbudgetarystabilitytomembers.Thecommercialinsurancemarket,however,vacillatesgreatlydependingonanumberofinternalandexternalfinancialconditions.

Formations

Poolsareorganizeddifferentlyineachstate–afunctionofstatelaw.Theinitialformationanditsincorporatingdocumentsdeterminehowyourpoolinteractswithitsmembershipandregulators,andgenerallydoesnotallowforinterstatemembership.

Dependingwhereyoulivearoundthecountry,poolsmightbecalledJointPowersAuthorities,InterlocalAgreements,Trusts,Reciprocals,Funds,RiskRetentionGroups,andevenMutualInsuranceCompaniesandCaptiveInsuranceCompanies.Alloftheseareslightlydifferentinorganizationandregulatoryrequirements,butgenerallytheyallfunctionsimilarlytoyourownpool.

FoundationDocuments

Regardlessofpoolformationtype,youshouldhavemanyofthesamecorelegaldocuments.Thosearethepool’s‘Bylaws’andits‘MembershipAgreement’,whichsetforththeresponsibilitiesandrelationshipbetweenthepoolandeachmember.

Amongallthosegoverningdocuments,therecontainsprovisionswhichshouldaddressatleastthefollowing:• Membershipeligibilitycriteria• Obligationsofmembers• Membershiptermination• Powersanddutiesofgoverningbodies• Ownershipanduseanddistributionofassets• Assessments• Professionalcertifications(includingactuarialreviewsandfinancialaudits)• Governancepoliciesprovidingaframeworkforoperationalissue(i.e.targetsurplus,fundingcriteria,etc.)

Regulations

Themethodofpoolingregulationvariesfromstatetostate.Eachstatehastheauthoritytoregulatemunicipalinsuranceandriskpooling,mostoftendisparatelyso.Accordingly,it’scrucialtoknowyourstate’sregulationstoensurecomplianceandtheabilitytocontinueoperations.Evenlargely“unregulated”poolsneedtounderstandtheauthorityunderwhichtheyoperate,andbeawarethat,whileastatemaynotexercisemuchregulatoryoversighttoday,thatconveniencecouldchangetomorrow.

CoverageDocumentandLinesofBusiness

Intheinsuranceindustry,organizationssuchastheISO(“InsuranceServicesOffices”)promulgatestandardizedcoveragelanguagethat,intheory,helpsregulatorswiththeapprovalprocess,andleadstowardmoreconsistentcoverageinterpretations.Nevertheless,disputesarise,andwhentheydo,thereisahugebodyofcourtcaselawtofallbackon.

Sincemostpoolsaren’ttechnicallyinsurers,theircoveragedocumentsarenot“insurancedocuments”;theyaremanuscriptcontractsbetweenthepoolandthemember,andgenerallyinterpretedunderContractLaw,ratherthanInsuranceLaw.Mostpoolsrefertotheircoveragedocumentsasthe“MemorandumofCoverage”,oran“MOC”.

WhetherISOformsormanuscriptcontracts,MOC’sshouldincludecertainsectionsthatallowforconsistentunderstandingandinterpretation.Theseinclude:

• Declarations:Also,referredtoasthe“DEC”page,thisusuallysinglepagequicklyoutlinesthespecificcoverage,limitdeductibles,andendorsementsthateachparticularmemberhaspurchased.

• Definitions:Identifiesandclearlydefineskeytermsforpurposesofthatparticularcoverage.• CoverageAgreement:Thebodyoftheagreementthatexplainswhattheexactcoverageasitisintended.• Conditions:Requirementsofthememberintheeventofaclaim,suchascooperatingwiththeinvestigation,

andtakingstepstominimizetheloss.• Exclusions:Clearlyexpressedrestrictionstotheintendedcoverage,someofwhichmaybequitestandard

(suchasasbestos,orlossescausedbywar),andsomewhichmaybespecifictothatpool(suchassubsidence,forapoolwithcoastalexposure).

• Endorsements:Standardormanuscript,theseareaddedtoanindividualmember’sMOCtochange,add,ordetractcoverage.Endorsementsarenegotiatedandagreeduponbyboththememberandthepool.

Ingeneral,thereareeighttypesofcoveragepoolsmightoffer:• Property• Boiler&Machinery(or,EquipmentBreakdown)• Crime&Fidelity• Liability• AutoLiability• Workers’Compensation• HealthorEmployeeBenefits• UnemploymentInsurance

WhataretheBasicDutiesofaPoolBoardMember?

Thelegalstructureofthepoolanditsboard–whetherdirectorsortrustees–presentslegalnuancesintherolesandresponsibilitiesofboardmembersthatarepool-specific.Thereare,however,somegeneralcharacteristicsthathelpensuretheboardpromotesthecooperativeculturethatisinstrumentaltoapool’ssuccess:

• Asamemberoftheboard,yourdutyistothepool–NOTtothememberyourepresent• Youarenotexpectedtobeatechnicalexpert,butyouareexpectedtoengagetechnicalexpertisewhen

needed,andtoalwaysactingoodfaith• Youareexpectedtodeliberateanddebatewithyourcolleaguesontheboard,butonceactionistaken,you

mustsupportthataction.Inotherwords,“TheBoardspeakswithonevoice.”

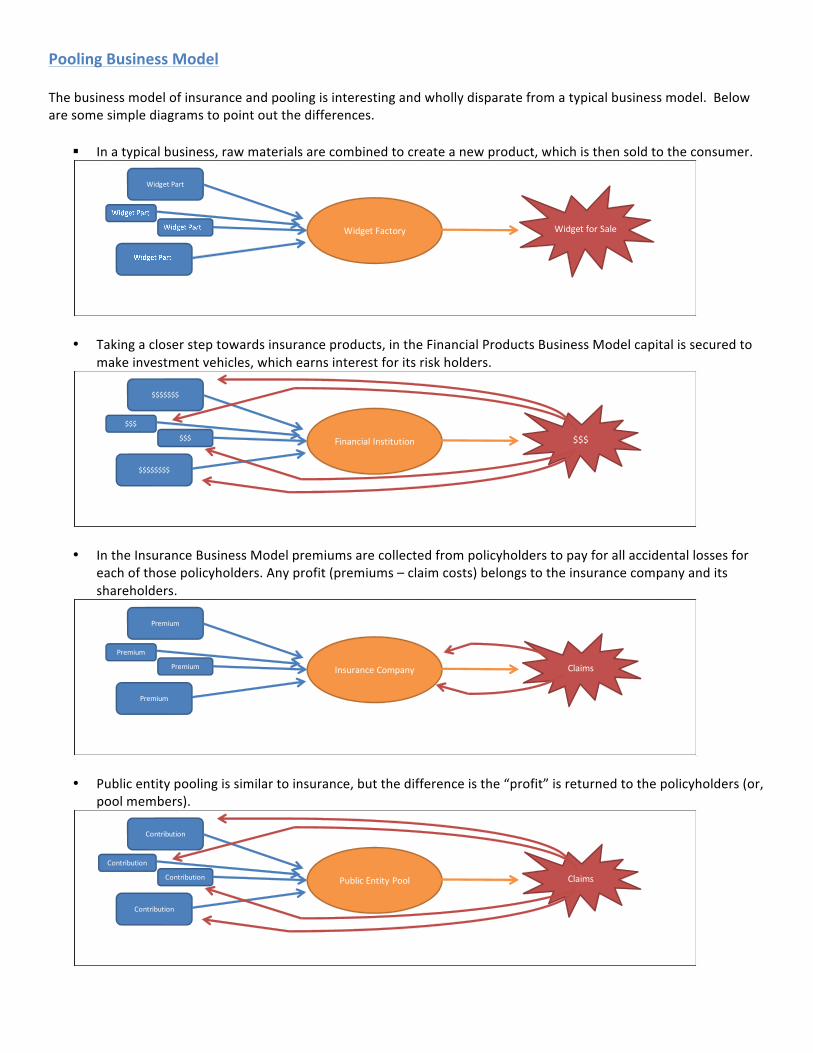

PoolingBusinessModel

Thebusinessmodelofinsuranceandpoolingisinterestingandwhollydisparatefromatypicalbusinessmodel.Belowaresomesimplediagramstopointoutthedifferences.

§ Inatypicalbusiness,rawmaterialsarecombinedtocreateanewproduct,whichisthensoldtotheconsumer.

• Takingaclosersteptowardsinsuranceproducts,intheFinancialProductsBusinessModelcapitalissecuredtomakeinvestmentvehicles,whichearnsinterestforitsriskholders.

• IntheInsuranceBusinessModelpremiumsarecollectedfrompolicyholderstopayforallaccidentallossesforeachofthosepolicyholders.Anyprofit(premiums–claimcosts)belongstotheinsurancecompanyanditsshareholders.

• Publicentitypoolingissimilartoinsurance,butthedifferenceisthe“profit”isreturnedtothepolicyholders(or,poolmembers).

WidgetPart

WidgetFactory WidgetforSale

$$$$$$$

$$$

$$$

$$$$$$$$

Financial Institution $$$

Premium

Premium

Premium

Premium

Insurance Company Claims

Contribution

Contribution

Contribution

Contribution

Public EntityPool Claims

Additionally,therearesomeinterestingaspectstothebusinessmodelofinsurancecompaniesandpublicentitypoolsversusthetraditionalbusinessmodel.Inmostbusinesses,youmakeaproductsuchasawidget.Thecostofmakingthatwidgetisknown,becauseyouhavetospendalmostallofthecostofmakingthatwidgetbeforeyousellittoaconsumer.Whenyousellthewidget,youaddupallthecoststomakeit,putinalittleprofit,andchargethecustomerthatprice.

Forinsuranceandpoolingcontracts,youchargethecustomerfirstintheformofpremiumsorcontributions,andthenyearsanddecadeslateryoufindouthowmuchthatproductcosts.Thatunknowncostforallthoseyearsanddecadesisreserves,whichareestimatedbytheclaimsstaffandanactuary.Likeallpredictions,theestimatesareneverassumedtobeentirelycorrect.Thoseunknownestimateshavetobebookedonourbalancesheetandincomestatement.Fortunately(quiteliterally),thereisabenefittothisbusinessmodel.Allthosebookedreservessittingonyourbalancesheetcanbeinvestedtogenerateinvestmentincome.Thisinvestmentincomecanusedtoeithergarneradditional“profit”ortolowerthecostofpremiums/contributions.

ActuarialScience

TheProbabilitiesandStatisticsofPredictingtheFutureActuariesplayavitalroleintheoperationandsuccessofpoolsbyprovidinganalysiscrucialtothefinancialviabilityofpools.Quitesimply,whenapooloffersitsproduct–indemnificationcoverage–itcannotknowforsurewhatitsfinalcostfortheproduct–theclaimsitwillpay,andwhenitwillpaythem–willbe.Thatiswhereactuariescomein.Actuariesaretrainedintriedandprovenstatisticalmethodsofmakingfuture“guesses”asaccurateaspossible.Thepool’sactuaryshouldalsobeinvolvedinestablishingthefundingrequirementsfortheupcomingyear,orthe“rates”thepoolwillchargemembers.Thisinvolvesprojectionsoffuturelosses,basedonpastexperienceandwhetherotherchangesareoccurring(suchaschangesincoverages,thelitigationenvironment,orbenefitslevelsinworkers'compensation)andaddingothercosts,suchasadministrativeexpensesandreinsurancecosts.Actuariesusemathematics,statistics,economics,andfinancetoanalyzethefinancialconsequencesofrisk.Inthiscase,therisksanalyzedarerelatedtothecoveragesor“riskscovered”bypools.FundingStudiesSo,howdoyoufundforalossthathasyettooccur?Or,inbusinessterms,howdoyoupriceaproductyouaresellingtoday,whenyoudon’tknowtheultimateproductioncostsformanyyears(orevendecades)?Anactuaryconductsalossprojectionanalysis,whichisanestimateoftheretainedlossesthatwilloccurduringaspecifictimeperiodinthefuture,basedonthecoverageprovidedbythepooltoitsmembers.Inordertoprojectthelossesforthecomingperiod,anactuarywillreviewthehistoricallossesandexposuresassociatedwithpreviousperiods.Heorshewillalsoaskforinputfrommanagementonwhatmightbedifferentnextyear,intermsofchangingmembershiporcoverages,forexample.Anactuarywillfirstestimatetheultimatelossesforeachofthepreviousperiodsbasedonseveralactuarialmethods.Theincurredandpaidlossdevelopmentmethodsarethemostcommonandbasicmethodsused.ReserveStudiesAnactuarialreserveanalysisestimatesapool’soutstandingliabilitiesresultingfromtherisktransfercontractstheyhavewritteninthepast.Oneuniquecharacteristicofrisktransferproductsisthattheproductsarepricedbeforethepolicyiswritten,butthefinalcostmaynotbeknownforsometimesdecadeslater.Forpropertyrisks,itmayonlybefiveyears–yourbuildingburnsdown,youbuildanotherone.But,forworkers’compensation,aninjuredworkermighthavealifetimeofbenefits.

Theliabilitiestobefundedconsistoftwocomponents:1.Casereservesarethereserveamountsshownonthelossrun.Theyaretypicallyestimatedbyaclaim

adjuster,lawyer,orotherinsuranceprofessional.Theyrepresenttheamountofmoneyestimatedforfuturepaymentsrelatedtoaparticularclaim.

2.IBNRreservescanbethoughtofascomposedoftwofurtherparts–PureIBNRreservesandreservesfordevelopmentonknownclaims.

• PureIBNRreservesaretheestimatedamountneededforclaimsthathavehappenedbuthavenotbeenreportedtothepoolyet.

• Reservesfordevelopmentonknownclaimsareestimatedadditionalamountsneededtoultimatelysettleknownclaimsinadditiontothecurrentcasereserves.

FinancialReportingandAuditing

BalanceSheetandIncomeStatementBasics

Animportantpartofanyorganizationisitsfinancialhealth.Twokeycomponentsofassessingandreportingfinancialhealtharebalancesheetsandincomestatements.Wewillexplainthebasicsofeachandhowtheyinterrelate.

ABalanceSheet(BS)isastatementofacompany’sfinancialpositionataparticularmomentintime.Thisfinancialreportshowsthetwosidesofacompany’sfinancialsituation:whatitownsandwhatitowes.Whatthecompanyowns,calledits"assets,"isalwaysequaltothecombinedvalueofwhatthecompanyowes,calledits"liabilities,"andthevalueofitsshareholders’equity.

Assets=Liabilities+ShareholderEquity

Thisiswhyitiscalleda"balancesheet",asthetwosidesmustbeequal.Youmayalsohearthisas"theleftequalingtheright."Ifthecompanyweretodissolve,thenitsdebtswouldbepaid,andanyassetsthatremainedwouldbedistributedtotheshareholdersastheirequity.Bankruptcyoccursinsituationswhereshareholderequityiszero,andthecompanyowesmoreliabilitiesthanitownsassets.

AnIncomeStatement(IS)showstherevenuesfrombusinessoperations,expensesofoperatingthebusiness,andtheresultingnetprofit(orloss)ofacompanyoveraspecificperiodoftime.Weusuallyseethisreportedquarterlyandannually.

BSandISastheyapplytoPools

Thepool’sbalancesheetlookverysimilar,excepttherearetwotopicswearegoingtospendsomemoretimeonlaterinthiscourse:InvestmentandReserves.Theseareuniqueitemstopoolsandinsurancecompanies.Poolsandinsurancecompaniesarerequiredtoretainhugeamountofcapitalasreservesforfutureclaimpayments(CaseReservesareforknownfuturepaymentsandIBNRReservesareforunknownfuturepayments).Thisextracapitalsitsinaninvestmentportfolioforyearsandyear,so‘Investments’isalargeticketitemforpoolsandinsurancecompaniestomonitor.

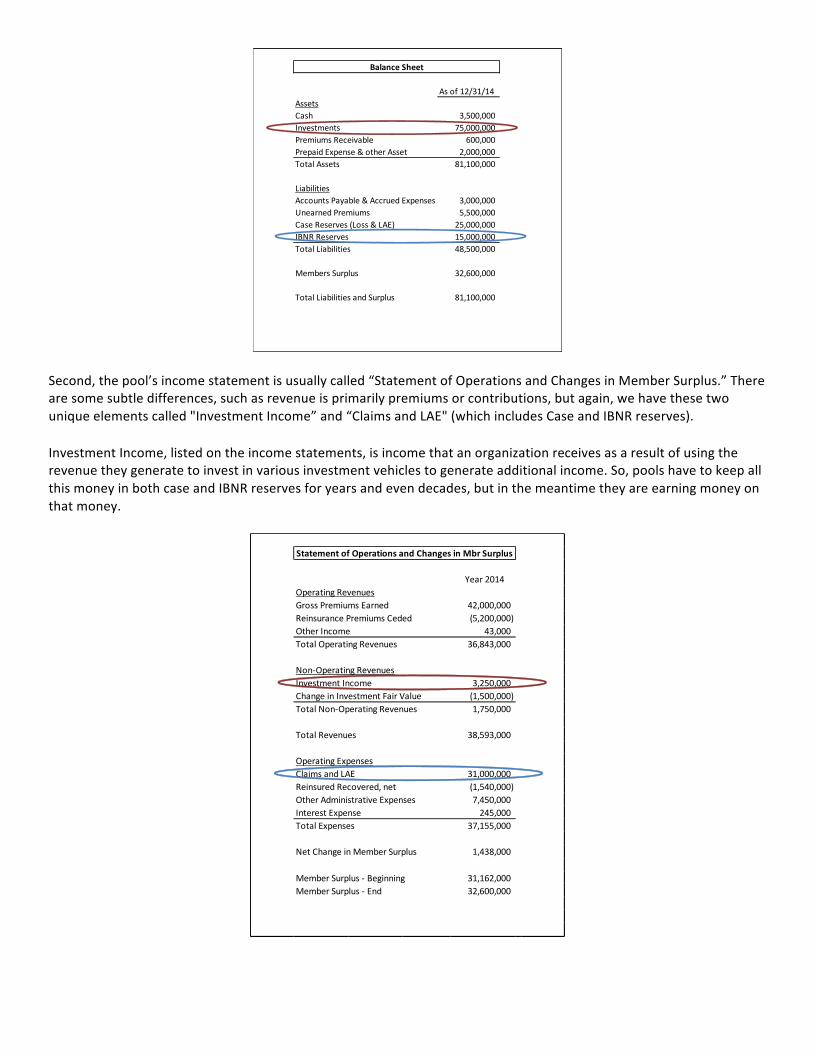

Second,thepool’sincomestatementisusuallycalled“StatementofOperationsandChangesinMemberSurplus.”Therearesomesubtledifferences,suchasrevenueisprimarilypremiumsorcontributions,butagain,wehavethesetwouniqueelementscalled"InvestmentIncome”and“ClaimsandLAE"(whichincludesCaseandIBNRreserves).

InvestmentIncome,listedontheincomestatements,isincomethatanorganizationreceivesasaresultofusingtherevenuetheygeneratetoinvestinvariousinvestmentvehiclestogenerateadditionalincome.So,poolshavetokeepallthismoneyinbothcaseandIBNRreservesforyearsandevendecades,butinthemeantimetheyareearningmoneyonthatmoney.

Asof12/31/14AssetsCash 3,500,000Investments 75,000,000PremiumsReceivable 600,000PrepaidExpense&otherAsset 2,000,000TotalAssets 81,100,000

LiabilitiesAccountsPayable&AccruedExpenses 3,000,000UnearnedPremiums 5,500,000CaseReserves(Loss&LAE) 25,000,000IBNRReserves 15,000,000TotalLiabilities 48,500,000

MembersSurplus 32,600,000

TotalLiabilitiesandSurplus 81,100,000

BalanceSheet

Year2014OperatingRevenuesGrossPremiumsEarned 42,000,000ReinsurancePremiumsCeded (5,200,000)OtherIncome 43,000TotalOperatingRevenues 36,843,000

Non-OperatingRevenuesInvestmentIncome 3,250,000ChangeinInvestmentFairValue (1,500,000)TotalNon-OperatingRevenues 1,750,000

TotalRevenues 38,593,000

OperatingExpensesClaimsandLAE 31,000,000ReinsuredRecovered,net (1,540,000)OtherAdministrativeExpenses 7,450,000InterestExpense 245,000TotalExpenses 37,155,000

NetChangeinMemberSurplus 1,438,000

MemberSurplus-Beginning 31,162,000MemberSurplus-End 32,600,000

StatementofOperationsandChangesinMbrSurplus

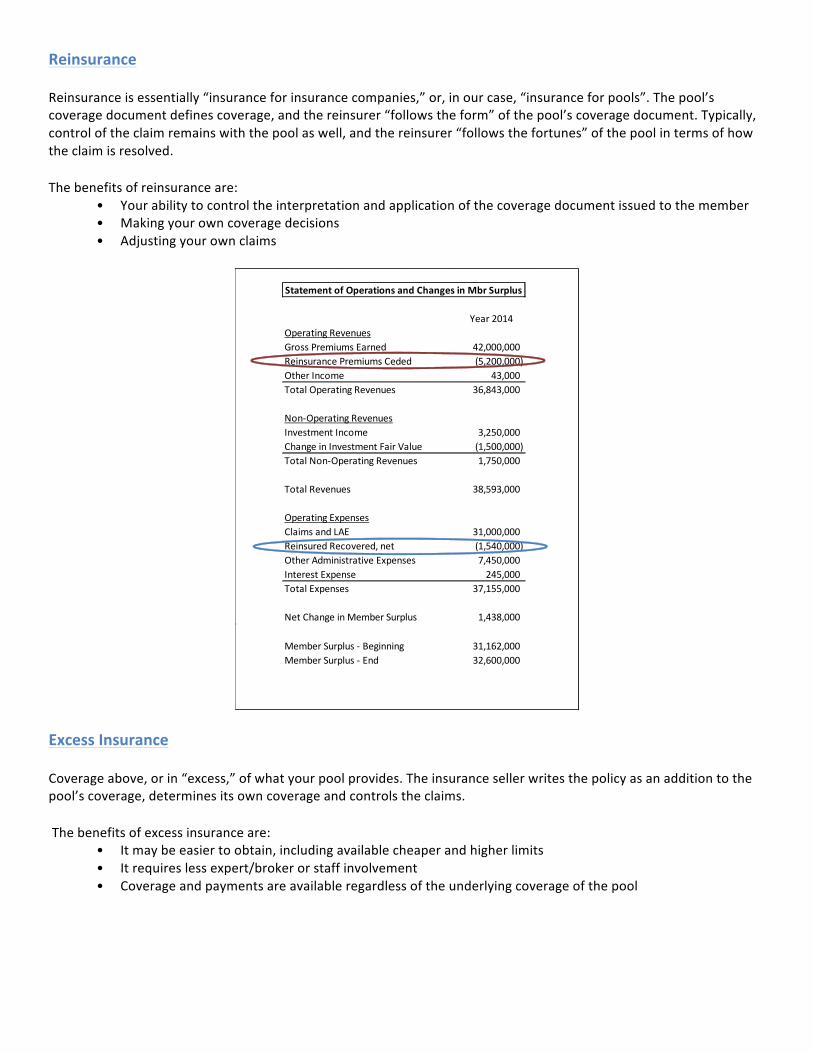

Reinsurance

Reinsuranceisessentially“insuranceforinsurancecompanies,”or,inourcase,“insuranceforpools”.Thepool’scoveragedocumentdefinescoverage,andthereinsurer“followstheform”ofthepool’scoveragedocument.Typically,controloftheclaimremainswiththepoolaswell,andthereinsurer“followsthefortunes”ofthepoolintermsofhowtheclaimisresolved.

Thebenefitsofreinsuranceare:• Yourabilitytocontroltheinterpretationandapplicationofthecoveragedocumentissuedtothemember• Makingyourowncoveragedecisions• Adjustingyourownclaims

ExcessInsurance

Coverageabove,orin“excess,”ofwhatyourpoolprovides.Theinsurancesellerwritesthepolicyasanadditiontothepool’scoverage,determinesitsowncoverageandcontrolstheclaims.

Thebenefitsofexcessinsuranceare:• Itmaybeeasiertoobtain,includingavailablecheaperandhigherlimits• Itrequireslessexpert/brokerorstaffinvolvement• Coverageandpaymentsareavailableregardlessoftheunderlyingcoverageofthepool

Year2014OperatingRevenuesGrossPremiumsEarned 42,000,000ReinsurancePremiumsCeded (5,200,000)OtherIncome 43,000TotalOperatingRevenues 36,843,000

Non-OperatingRevenuesInvestmentIncome 3,250,000ChangeinInvestmentFairValue (1,500,000)TotalNon-OperatingRevenues 1,750,000

TotalRevenues 38,593,000

OperatingExpensesClaimsandLAE 31,000,000ReinsuredRecovered,net (1,540,000)OtherAdministrativeExpenses 7,450,000InterestExpense 245,000TotalExpenses 37,155,000

NetChangeinMemberSurplus 1,438,000

MemberSurplus-Beginning 31,162,000MemberSurplus-End 32,600,000

StatementofOperationsandChangesinMbrSurplus

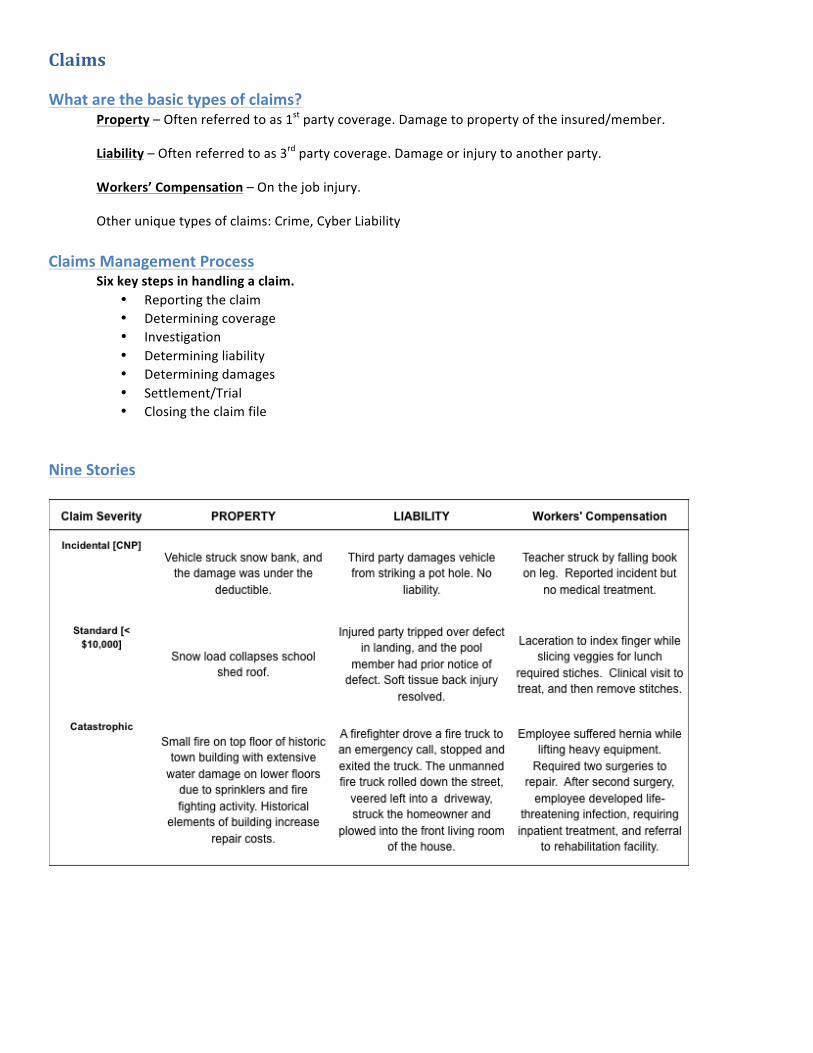

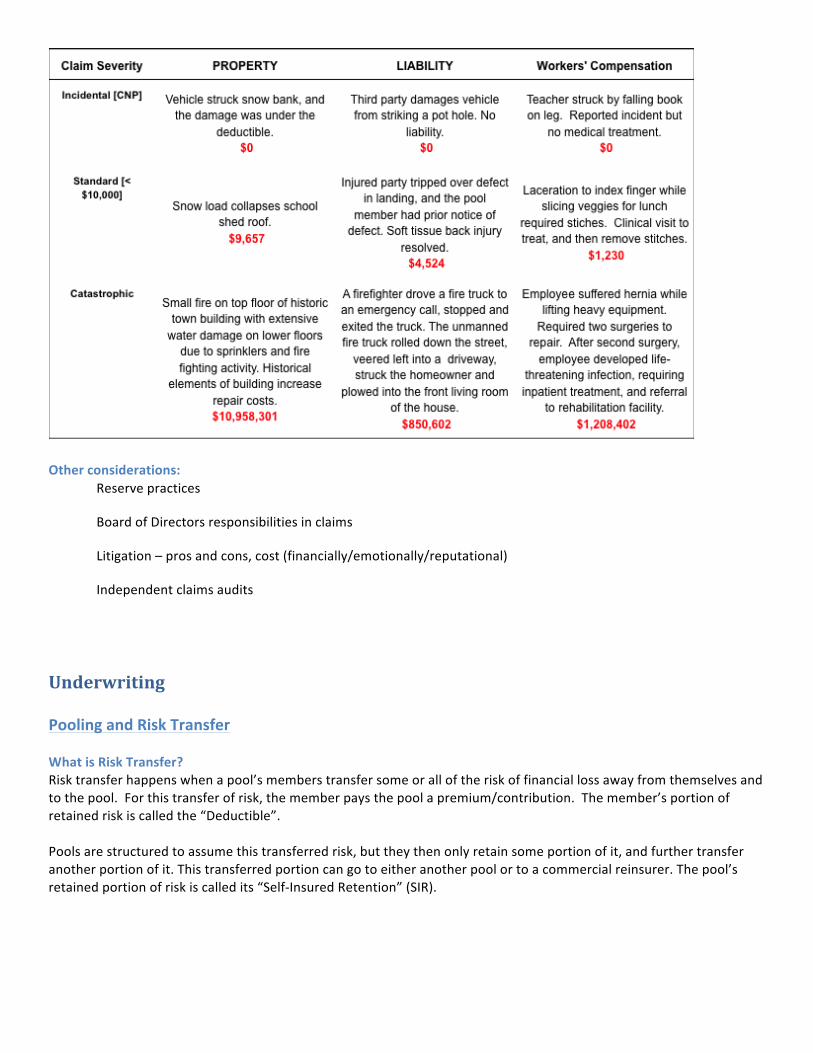

Claims

Whatarethebasictypesofclaims?Property–Oftenreferredtoas1stpartycoverage.Damagetopropertyoftheinsured/member.

Liability–Oftenreferredtoas3rdpartycoverage.Damageorinjurytoanotherparty.

Workers’Compensation–Onthejobinjury.

Otheruniquetypesofclaims:Crime,CyberLiability

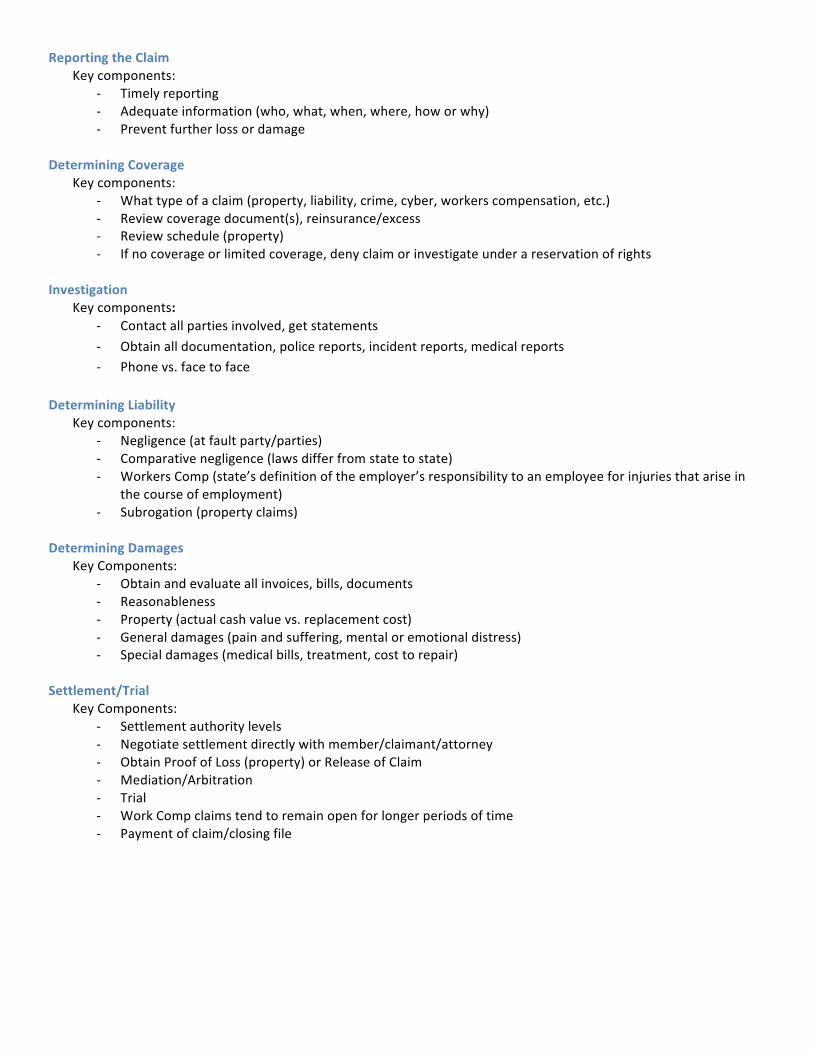

ClaimsManagementProcessSixkeystepsinhandlingaclaim.

• Reportingtheclaim• Determiningcoverage• Investigation• Determiningliability• Determiningdamages• Settlement/Trial• Closingtheclaimfile

NineStories

ReportingtheClaimKeycomponents:

- Timelyreporting- Adequateinformation(who,what,when,where,howorwhy)- Preventfurtherlossordamage

DeterminingCoverage

Keycomponents:- Whattypeofaclaim(property,liability,crime,cyber,workerscompensation,etc.)- Reviewcoveragedocument(s),reinsurance/excess- Reviewschedule(property)- Ifnocoverageorlimitedcoverage,denyclaimorinvestigateunderareservationofrights

Investigation

Keycomponents:- Contactallpartiesinvolved,getstatements- Obtainalldocumentation,policereports,incidentreports,medicalreports- Phonevs.facetoface

DeterminingLiability

Keycomponents:- Negligence(atfaultparty/parties)- Comparativenegligence(lawsdifferfromstatetostate)- WorkersComp(state’sdefinitionoftheemployer’sresponsibilitytoanemployeeforinjuriesthatarisein

thecourseofemployment)- Subrogation(propertyclaims)

DeterminingDamages

KeyComponents:- Obtainandevaluateallinvoices,bills,documents- Reasonableness- Property(actualcashvaluevs.replacementcost)- Generaldamages(painandsuffering,mentaloremotionaldistress)- Specialdamages(medicalbills,treatment,costtorepair)

Settlement/Trial

KeyComponents:- Settlementauthoritylevels- Negotiatesettlementdirectlywithmember/claimant/attorney- ObtainProofofLoss(property)orReleaseofClaim- Mediation/Arbitration- Trial- WorkCompclaimstendtoremainopenforlongerperiodsoftime- Paymentofclaim/closingfile

Otherconsiderations:Reservepractices

BoardofDirectorsresponsibilitiesinclaims

Litigation–prosandcons,cost(financially/emotionally/reputational)

Independentclaimsaudits

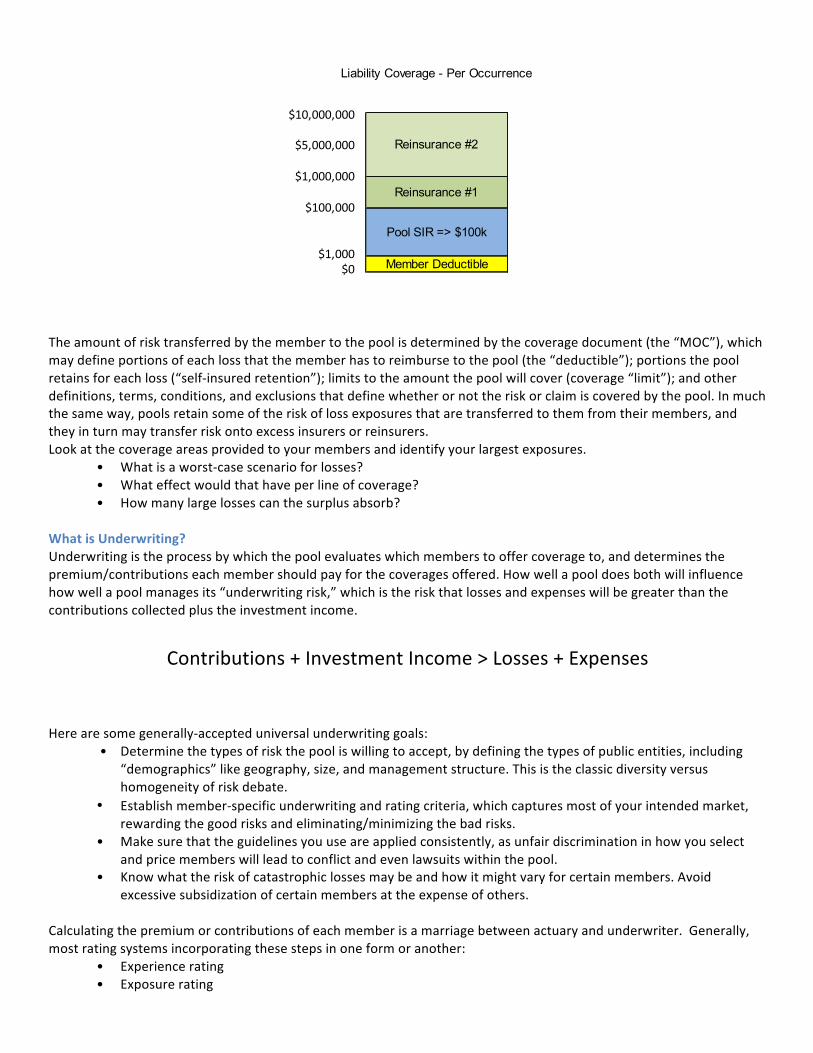

UnderwritingPoolingandRiskTransferWhatisRiskTransfer?Risktransferhappenswhenapool’smemberstransfersomeoralloftheriskoffinanciallossawayfromthemselvesandtothepool.Forthistransferofrisk,thememberpaysthepoolapremium/contribution.Themember’sportionofretainedriskiscalledthe“Deductible”.Poolsarestructuredtoassumethistransferredrisk,buttheythenonlyretainsomeportionofit,andfurthertransferanotherportionofit.Thistransferredportioncangotoeitheranotherpoolortoacommercialreinsurer.Thepool’sretainedportionofriskiscalledits“Self-InsuredRetention”(SIR).

Theamountofrisktransferredbythemembertothepoolisdeterminedbythecoveragedocument(the“MOC”),whichmaydefineportionsofeachlossthatthememberhastoreimbursetothepool(the“deductible”);portionsthepoolretainsforeachloss(“self-insuredretention”);limitstotheamountthepoolwillcover(coverage“limit”);andotherdefinitions,terms,conditions,andexclusionsthatdefinewhetherornottheriskorclaimiscoveredbythepool.Inmuchthesameway,poolsretainsomeoftheriskoflossexposuresthataretransferredtothemfromtheirmembers,andtheyinturnmaytransferriskontoexcessinsurersorreinsurers.Lookatthecoverageareasprovidedtoyourmembersandidentifyyourlargestexposures.

• Whatisaworst-casescenarioforlosses?• Whateffectwouldthathaveperlineofcoverage?• Howmanylargelossescanthesurplusabsorb?

WhatisUnderwriting?Underwritingistheprocessbywhichthepoolevaluateswhichmemberstooffercoverageto,anddeterminesthepremium/contributionseachmembershouldpayforthecoveragesoffered.Howwellapooldoesbothwillinfluencehowwellapoolmanagesits“underwritingrisk,”whichistheriskthatlossesandexpenseswillbegreaterthanthecontributionscollectedplustheinvestmentincome.

Contributions+InvestmentIncome>Losses+Expenses

Herearesomegenerally-accepteduniversalunderwritinggoals:

• Determinethetypesofriskthepooliswillingtoaccept,bydefiningthetypesofpublicentities,including“demographics”likegeography,size,andmanagementstructure.Thisistheclassicdiversityversushomogeneityofriskdebate.

• Establishmember-specificunderwritingandratingcriteria,whichcapturesmostofyourintendedmarket,rewardingthegoodrisksandeliminating/minimizingthebadrisks.

• Makesurethattheguidelinesyouuseareappliedconsistently,asunfairdiscriminationinhowyouselectandpricememberswillleadtoconflictandevenlawsuitswithinthepool.

• Knowwhattheriskofcatastrophiclossesmaybeandhowitmightvaryforcertainmembers.Avoidexcessivesubsidizationofcertainmembersattheexpenseofothers.

Calculatingthepremiumorcontributionsofeachmemberisamarriagebetweenactuaryandunderwriter.Generally,mostratingsystemsincorporatingthesestepsinoneformoranother:

• Experiencerating• Exposurerating

Liability Coverage - Per Occurrence

Reinsurance #2

Reinsurance #1

Pool SIR => $100k

Member Deductible

$10,000,000

$5,000,000

$1,000,000

$100,000

$1,000$0

• Premiumallocation• Schedulerating

DifferencesofInsuranceandPoolingUnderwritingWhileinsuranceandpoolingunderwritingaresimilar,theydohavethreedistinctdifferences.Theseare:

• Communityrating• Useofdataanalytics• Howtheyacceptorrejectrisk

UnderwritingBiasItisimpossibletoremovebiasfromourlives,andthisistrueforunderwriters.Therearemanybiasestoavoid(https://en.wikipedia.org/wiki/List_of_cognitive_biases)tobecomecompletelyobjective,asnobleasthatgoalis.Relatedtobiasesistheconceptofdiscrimination,andbystatelawtherearecertaindiscriminationswecannotusewhileunderwriting(gender,race,religion,etc).But,essentially,thejoboftheunderwriteristofindadiscriminatorybasisamongthepolicyholderstowardsrisk.Ifyouhavetwoschoolsthatyouareunderwriting,andoneschoolisthoughttobetwiceasriskyastheother.Intuitively,youshouldchargethefirstschooltwiceasmuchcontributionasthesecond,right?But,whatbasisareyoumakingthatdeterminationof“twicetherisk”,absentanylossdata.Ifthefirstschoolhadtwiceasmanystudents,thenyoucouldmakearationalargumentthatitwouldbetwiceasrisky.But,ifyouweretoassesstherisklevelagainstaprotectedclass(forinstance,thefirstschoolisAllBoysandthesecondschoolisAllGirls),thenthatisillegal.So,underwritersneedtomakeasobjectiveselectorstoriskaspossible.Onecommonbiasis‘IngroupBias’,whichisthetendencytogivepreferentialtreatmenttootherstheyperceivetobemembersoftheirowngroup.So,backtotheschoolexample,perhapsevenwithtwiceasmanystudentsthefirstschoolgetsthesamepremiumasthesecondschool,merelybecauseitresidesinthesametownastheunderwriterlives.

RiskManagement/LossControlRiskManagementinthePoolingContext"Riskmanagement"isacorefunction–somewouldsayTHEcorefunction–ofpools.Mostdefinitionsofriskmanagementinvolvetheprocessoftheidentification,assessment,andtreatmentofrisk,where"risk"isuncertaintyandusuallyviewedasnegative,asinthepossibilityofloss,damage,orharm.Youwillhearreferencestoanumberofprograms,activitiesorfunctions,allofwhichareformsofriskmanagement.Someofthemorecommoninclude:

• Lossprevention:Referringtoeffortstokeepbadoutcomesfromhappeninginthefirstplace,oftenthroughbettertrainingofemployeestoavoidinjurytothemselvesorothers;adoptionandenforcementofgoodpoliciesforpublicofficialstofollow;wellnessprogramstoimproveemployeehealth;anduseofpreventivemaintenanceprogramsforpropertiesandpublicinfrastructure.

• Losscontrol:Referringtoeffortstoreducethesizeofanylossthatdoesoccur,throughpromptreporting,proactiveclaimmanagement,andpostincidentoraccidentreview.

• Safety:Mostcommonlyassociatedwithemployeeon-the-jobinjuryprevention,butalsoapplicabletocreatingandassuringsafeenvironmentsforthepublic,orsafeoperationofvehiclesorequipment.

• Training:Agrowingareaofactivityforpools,especiallyusingnewtechnologyforefficiency,andoftentoincludecomplianceissues.

Oneofthemostimportant,yetchallenging,aspectsofriskmanagementisdetermininghowmuchtoinvestinriskmanagementprogramsandservices(i.e.measuringtheireffectiveness).Howdoyouknowifthespecificinvestmentsactuallyhadanimpactonthelosscosts?Maybethereductionwouldhavehappenednomatterwhat.Maybeitisjustgoodluck.CreatingaCultureofRiskManagementPerformanceimprovementprotocols:Toencouragetherightbehavior–andforthebenefitoftherestofthemembership–poolsadoptprogramsthatrequirememberstomakechangesinordertostayinthepool,andevenrefuserenewal,ifnecessary.Thismightalsotaketheformofincentivizedpricingforthosemembersofthepoolsthatadheretostrictsafetypracticesorrecommendedchangestoexistingpolicies.Casestudies:Sharingthepositiveresultsofonememberwithothers,andleveragingpilotprogramsacrossthewholepoolmembership,isanaturalwayforpoolstoimprovetheirriskmanagementculture.Dataanalysis:Poolsnowhave20to40yearsofdata,andtoolstobetteranalyzethedata,tounderstandwhatworks,andwhatdoesn't,thatcanhelpthepoolengageitsmembersinthevalueofriskmanagement.

TheFutureofPublicEntityPoolingWhatdoesthefuturehold?That’satoughquestion,butAGRiPhastakenthestepstoensurewestartthinkingaboutthefutureinadisciplinedway.ThroughourResidentFuturistRebeccaRyan,wecanbrieflytalkaboutfoursegmentsofthefuturethatwillaffectpooling(and,notinsignificantly,therestofourlives,aswell).GenerationalShiftsAstheBabyBoomergenerationmovestowardsretirement,theoriginalfoundersofthepoolingmovementwillbetakingalltheirinstitutionalknowledgewiththiswhentheyleavethepool.Additionally,anationwideshortageofGenerationX’erstoreplacethemwillleadanemployee’smarketforemployment.Poolswillhavetoremaincompetitivetoretainthebeststaffing,andcontinuetoinnovatetointerestyoungerworkers.TechnologyThereisnodoubtthattechnologyhasandwillcontinuetochangeourlivesandourbusinessmodels.But,howso?Whocouldhavepredicted20yearsagohowtheInternetandsocialmediawouldfundamentallychangebusinessmodelscenturiesold?So,whatisnext?Noonecansayforcertain,butit’sagoodbettogoaskyourinternwhatheorshethinks…LeadershipChangesAsthepoolingstaffturnsoverinfavorofayounger,moretechnologicallymindedemployee,poolmanagementneedstocontinuetoengagenotonlythem,butthepoolmemberrepresentatives,aswell.On-sitemeetings,mailedflyers,andphysicallocationsarenolongerimportant.Newmanagersmustintegratenewmethodstoengagenewemployeesandconstituencies.Newmanagersmustharnessthepowerofinformationanddisseminateittoeveryoneseamlesslyandconstantly.CatastrophicWeatherIrregardlessofwhocausedit,thereislittledoubtthatweatherpatternsarechangingfromhistoricaldata.Patternsarebecomingmoreerraticandsevere,andcatastrophicweatherisplaguingareaswherepreviouslytherewasnone.Aspoolsgrapplewiththeseenormouslossevents,riskmanagersandunderwritershavetore-doubletheireffortsandre-thinkwhatwaspreviouslyimprobable.Moregenerally,poolsneedtoleadthechargeofinfluencingpublicentitiestore-thinktheirinfrastructure,maintainedproperties,andsocialservices.