Embed Size (px)

Citation preview

business

POLYSTYRENE: TOO MUCH, TOO SOON Rapid capacity increase depresses margins; now producers are pushing price hike

Paige Marie Morse C&EN Houston

Polystyrene producers are in the middle of a very poor cycle for the polymer, experiencing severely de

pressed prices in a market that is fraught with overcapacity.

"The polystyrene market continues to be a very difficult one," says David Huntsman, vice president for polymers at Huntsman Corp. "We know this business has peaks and valleys. Obviously, we are in one of the valleys right now and have been for some time."

The problems in this market are not due to a lack of growth, but instead to significant overcapacity that will require, at a minimum, several months for recovery. And many analysts agree that producers have brought this upon themselves.

"With new capacity coming onstream—from Chevron and BASF—there has been a lot of competition to gain and maintain market share," says market analyst Jean Meador of the Houston consulting firm Phillip Townsend Associates. "Producers have been very aggressive, operating at fairly high rates and causing significant softening of the price."

In the December issue of Plastic Mar

ket Monthly, a market analysis newsletter from Townsend, polystyrene prices show a continuing decline throughout 1997. December prices were between 34 and 40 cents per lb for crystal and impact polystyrene, down from 45 to 50 cents in late 1996.

In an attempt to reduce some of the overcapacity in the market, three producers—Nova Chemicals, Huntsman, and BASF—have announced plant closings or capacity reductions in recent months. Although these moves may eventually help the market, they are not expected to offer any short-term relief to producers.

In terms of market growth, polystyrene appears to be quite healthy, according to the Society of the Plastics Industry (SPI). Sales and captive-use figures through October 1997 show an increase of 5.6% over the similar period of the year before. Also, SPI predictions for total 1997 sales and captive use based on the first nine months of the year indicate a 7.6% increase in sales for polystyrene over 1996.

However, SPI statistics also point out the supply-and-demand imbalance that the polystyrene industry is currently experiencing. Production for the first 10 months of 1997 was up 8.2% over the same period in 1996, whereas sales were

BASF recently brought onstream its polystyrene facility in Aitamira, Mexico.

Polystyrene is made in three forms There are three types of polystyrene polymer: crystal, impact, and expandable. Producers generally refer to the polystyrene market as including only crystal and impact grades, also called solid polystyrene. Expandable polystyrene (EPS) is a separate, specialty product that has different market dynamics and is currently priced about two times higher than solid polystyrene.

Crystal polystyrene is a clear, amorphous polymer with good stiffness and electrical insulation properties. It is used primarily in consumer packaging, appliances, and containers.

Impact polystyrene is also known as rubber-modified polystyrene. It contains varying levels of polybuta-diene to improve its toughness. Primary applications include toys, appliances, and consumer packaging.

EPS is a foamed product that is supplied to customers in bead form. It is manufactured by solution polymerization of styrene, forming a lightweight, closed-cell polymer. Its primary markets are construction and packaging.

Data from the Society of the Plastics Industry (SPI) include all three types of polystyrene. SPI sales and captive-use statistics through October 1997 represent 45% impact polystyrene, 40% crystal polystyrene, and 15% EPS.

up only 5.6%. This discrepancy in growth suggests that inventory levels are building, leading to a destabilization of prices.

Stephen Korkmas, polystyrene product manager at Dallas-based Fina, agrees with these observations: "Demand is up, but the fact remains that there is severe overcapacity. At current pricing levels, the industry cannot sustain the resulting margins."

Dow Chemical, North America's largest polystyrene producer, offers a cautious but less dismal view of the market. "We are currently seeing a typical response to new capacity coming onstream," says Clay Dunn, Dow's global business director for polystyrene. "We anticipate some short-term effect on pricing. Long term, we see slow but steady growth in polystyrene demand in North America—about 2.5% per year—over the next 10 years, with balanced supply and demand."

Dow's current estimates of demand for polystyrene are 6 billion lb for the U.S., 6.6 billion lb for North America,

JANUARY 19, 1998 C&EN 19

b u s i n e s s

and 21 billion lb globally. The global annual growth rate is estimated at 4.3% for the next 10 years.

Bill Greene, vice president for styrenics at Nova, notes that many producers are "bleeding," but he is more optimistic about market opportunities, citing a 4% market growth rate for North America and 5% globally. "The packaging market is the main growth engine for polystyrene, and it continues to be quite strong."

Another issue affecting several polystyrene producers is that styrene prices are at very low levels. In general, low prices for monomers can benefit polymer producers by reducing their raw material costs. However, most of the major producers-including Dow, Huntsman, Nova, and Chevron—are back-integrated to ethylene and benzene for styrene manufacture, and Fina has access to styrene through a joint venture with General Electric.

"When the polystyrene market is rough, back-integrated producers try to extract value at styrene," says William Kuhlke, president of consultants Kuhlke & Associates in Houston. Right now, these producers cannot get a good price for either product in this chain.

"When looking at the integrated styrene chain, it is unprecedented to see a time when styrene and polystyrene have been as badly depressed as they are right now," says Huntsman.

And styrene raw material costs are also up, notes Fina's Korkmas. "Ethylene is higher than we thought it would be at this time, and benzene has spiked to $1.15 per gal for January." However, he

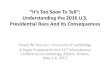

Dow Chemical is the largest North American polystyrene producer

Dow Chemical

Huntsman

BASF

Fina

Nova Chemicals

Chevron

TOTAL

Plant sites

Joliet, III. Midland, Mich. Torrance, Calif. Pevely, Mo. Allyn's Point, Conn. Hanging Rock, Ohio Sarnia, Ontario

Belpre, Ohio Chesapeake, Va. Joliet, III. Peru, III.

Joliet, III. Altamira, Mexico

Carville, La.

Decatur, Ala. Springfield, Mass. Montreal, Quebec

Marietta, Ohio

Annual capacity8

(billion lb)

1.6

. 1 . 2

1.1

1.0

0.8

0.8

6.5

a C&EN estimates for crystal and impact polystyrene, including expansions and closings expected in 1998.

continues, "While styrene margins have been poor, most people thought they would be even lower by this time than they are."

In response to the poor market conditions, Nova, Huntsman, and BASF have announced closures of production facilities,

removing about 6% of North American production capacity.

As of Jan. 1, Nova ended its tolling arrangement with Bayer at Bayer's Addyston, Ohio, facility. In the October 1997 announcement, Greene said this reduction of capacity by 80 million lb will allow Nova's "remaining sites to run near capacity and will improve our cost position."

By the end of this month, Huntsman will complete the shutdown of its Willow Springs, 111., plant and three production lines at its Belpre, Ohio, plant (C&EN, Nov. 10, 1997, page 7), removing 150 million lb of capacity. This marks the first time that this typically aggressive petrochemical and polymer player has closed a production facility because of market conditions.

BASF closed its plant in Hol-yoke, Mass., in November and has accelerated the closure of its Santa Ana, Calif., plant from late 1998 to this summer. Together, these closures remove 155 million lb of annual production.

In its November 1997 announcement, BASF said, "These

actions reflect highly unsatisfactory market conditions and the industry's rapid shift to a manufacturing model characterized by modern large-scale facilities."

At the same time, however, BASF is adding polystyrene capacity at its two remaining manufacturing sites in North Ameri-

ULTRAPURE CUSTOM MANUFACTURING Sachem's Texas manufacturing plant available for ultrapure production. State-of-the-art ultrapure water system and extensive high purity analytical capabilities. ISO 9001.

CIRCLE 38 ON READER SERVICE CARD 2 0 JANUARY 19, 1998 C&EN

SACHEM i n f o @ s a c h e m u s a . c o m

Give us a ca l l a t 5 1 2 - 4 4 4 - 3 6 2 6 or f a x 5 1 2 - 4 4 5 - 5 0 6 6 . 821 East W o o d w a r d A u s t i n , T X 7 8 7 0 4

SACHEM manufactures specialty and fine chemicals at two Reactors up io 8,000 gallon

plants in lexas. 5Α<^Η£Μ has a substantial tracKrecora Cleanroom oackaaina

supplying products to the semiconductor, pharmaceutical SPC trained workforce and other high purity markets. Our success in reliable,

18 meaaohm ultraoure water detail-oriented manufacturing can mean success for you in

60 acre North Texas niant site transferring your ultrapure production to a convenient

PPT analytical capabilities Central U.S. location. ί>Αϋ1Η^Μ will give a prompt,

ISO 9001 registered thorough review of your project. We are flexible in

Responsible Care customizing our plant to suit your individual needs.

ca—Joliet, HI., and Altamira, Mexico. The Joliet site will be expanded from 520 million to 760 million lb per year in third-quarter 1998. The plant in Altamira began production in July 1997, adding 315 million lb of annual capacity in North America. BASF notes that the product from this plant is for both the North and South American markets.

BASF's switch from smaller production sites to large-capacity lines reflects a change in the polystyrene production dynamics that is also occurring in other plastics industries. A difference for polystyrene is that its market cannot handle the capacity as well.

"The polystyrene market is slower growing and smaller overall than other polymers such as polyethylene and polypropylene," says Huntsman. "The technology that is available today allows a single line to make 250 million to 300 million lb of product, which has a major impact on a market that only grows at 3% per year."

The advantages of large-scale production versus smaller plants are still debated in the industry, primarily because the market is intermediate in size yet has steady but slow growth rates.

Huntsman Corp. operates multiple plants located close to end-use markets and customers. "Our reduced transportation costs more than offset some of the scale differences of the larger lines," says Huntsman. "There is a trade-off between having the efficiencies of scale at one location and having a smaller scale but multiple locations closer to your customer base."

In contrast, Korkmas at Fina maintains that its four-line, single production site with an annual capacity of 1 billion lb provides significant operating efficiencies that keep costs low.

Dow is an intermediate case—its proprietary manufacturing technology provides incremental capacity expansion with rninimal capital investment. This allows the company to keep pace with the slow growth expected in North America, according to Dunn.

Regardless of specific production size, producers are hoping that these closures will help stabilize prices and possibly support the 3-cent-per-lb price increase that was announced last month for Jan. 1.

"The announced rationalization is a positive first step toward restoring the balance to the polystyrene market," says Huntsman. "It also supports what we have been telling our customers all along about the seriousness of the financial situation of the market."

Both Fina's Korkmas and Nova's Greene

Fifty years of Styrofoam This year marks the 50th anniversary of Dow Chemical's Styrofoam brand, the world's first extruded polystyrene foam product. Styrofoam has been manufactured continuously since the late 1940s, and it remains the leading product of its type in the world.

Styrofoam was introduced as an insulation material for the construction industry, which continues to be the dominant application today. Other uses that take advantage of the product's rigidity and high thermal and water resistance include marine applications, low-temperature warehouses, and floral arrangements.

"While the basic characteristics have remained," remarks John Somerville, Dow's commercial director of North American building materials, "we have invested 50 years of research, development, and marketplace input to continually come up with new technologies, applications, and variations."

Currently, there are hundreds of Styrofoam products in use—varying in size, strength, edge treatment, facing options,

Styrofoam Brand Products

He Otut Orvmvi: C«'«>*'^

and densities. Styrofoam is made from crystal polystyrene using hydrochlo-rofluorocarbons as blowing agents.

Dow is celebrating this anniversary with the launch of a new logo for Styrofoam brand insulation. The logo retains the familiar blue color of the original and incorporates a skyline of commercial and residential buildings that depicts its primary market.

Also in 1998, Dow will begin a four-year program as the exclusive supplier of rigid foam insulation to Habitat for Humanity, International. In addition, the Dow Chemical Co. Foundation will donate $1 million to Habitat affiliates in each year of this program.

Time is money in product development. If you're involved in product development you can have many constraints to deal with; getting your hot new compound to market first isn't enough anymore. You need it done right, and on budget too. Whatever the scale, we're geared to it. We have extensive experience in process scale-up and the resources to get it done right. We have established many individual product drug master files and offer cGMP facilities for every step of the way When time counts, count on us. Request information.

PFANSTIEHL LABORATORIES, INC. The source for carbohydrate chemistry 1219 Glen Rock Avenue / Waukegan, IL 60085-0439 I 847/623-0370 •Toll Free: 1-800/383-0126 • FAX:847/623-9173 International: Pfanstiehl (Europe) Ltd. +44 (0) 1606.331825 • FAX: +44 (0) 1606.331826 http://www.pfanstiehl.com e-mail: [email protected]

MAKING THINGS WORK CIRCLE 22 ON READER SERVICE CARD

JANUARY 19, 1998 C&EN 21

PFANSTIEHL

New From Grant Chemical

PCI2

e Phosphonous

Intermediate

Volume TSCA Registered

ental Quantities

FERRO CORPORATION Grant Chemical Division, Sales Group 111 West Irene Road Zachary, Louisiana 70791 Telephone: (504) 654-6801 Fax: (504) 654-3268 Visit us online at vwvw.ferro.com

ft @ Responsible Care iso 9002/Q92 A Public Commitment Certificate QSR-314

® FERRO. CIRCLE 53 ON READER SERVICE CARD

Organo functional silicones measure up to your projects

Toll/Custom Manufacturing

With over forty years

experience in :

• development

• production

• handling of

organopolysiloxanes

• chemical hazard management

• effluent treatment

• quality (ISO 9001

Rhodia Silicones offers you

the wealth of its experience to

partner your developments that

incorporate functional silicones

(Rhodia

Contacts : e-mail : [email protected]

North America Europe Asia/Pacific

Rhodia Inc. Rhodia Silicones Rhodia Asia/Pacific

CN7500 17/19 Av. G.Pompidou 18/F Mamlife Tower

Cranburry, NJ 08512 69486 Lyon Cedex 03 169 Electric rd.

7500 USA France North Point, Hong Kong

Tel. (1)609 860 3581 Tel. : (33) 472 73 76 71 Tel. : (852) 2807 53 65

Fax: (1)609 860 0139 Fax : (33) 472 73 66 07 Fax:(852)2979 02 41

Silicones

CIRCLE 42 ON READER SERVICE CARD

22 JANUARY 19, 1998 C&EN

b u s i n e s s

add that recently announced price increases for styrene may help to bolster support for the polystyrene increases. However, Greene says, "there is some push back from customers on this. Some customers are questioning the timing around the increase, because they may not be able to pass it along to their customers."

Consultant Meador is less optimistic about the price increase, noting a failed attempt last summer. "The 4-cent-per-lb increase nominated in June 1997 was pushed back, and finally it just disappeared because the supply-and-demand fundamentals were against the hike. I do not have much optimism about the full 3-cent-per-lb January increase. Producers will have to wait until the curtailed production from the closures removes some of the excess product from the market."

Meador also reports that December contract prices continue to show some erosion, and prices for off-grade product—often a leading indicator for prime material—declined 1.7 cents per lb from November to December.

Another issue that concerns polystyrene producers is the uncertainty of the export market. This has become an increasingly important market for polystyrene, with SPI estimates showing a 15% increase from 1996 to 1997 to 8.6% of the sales and captive-use market.

In addition, the recent Asia-Pacific financial crisis was not fully considered in many industry estimates of exports, and the extent of its impact is unclear (C&EN, Dec. 15, 1997, page 18). The export market was stagnant in the fourth quarter, according to Meador, and few producers expect much improvement in 1998.

Market analyst Kuhlke strongly cautions that the export market will be poor in 1998. He notes that differences in end-of-year prices between the U.S. and Asia, which he estimates at 35 cents per lb in the U.S. and 30 cents per lb in Asia, will reduce most of the overseas opportunities.

"Shipping product to Asia will be very tough in 1998," says Kuhlke. "I expect exports to take a dive in 1998. Then where will producers move that extra product, especially if the U.S. market slows?"

It looks like 1998 will be a difficult year for polystyrene producers, but they are in control of their own fate.

"A price increase will be an uphill battle for producers," says Meador. "It will be interesting to see how disciplined producers will be and whether they will actually walk away from business if they cannot get the price they seek."4

ARYL PHOSPHINE

CALL OR WRITE FOR MORE INFORMATION OR SAMPLES