Embed Size (px)

Citation preview

www.platts.com

The McGraw Hill Companies

PolymerscanVolume 32 / Issue 11 / March 18, 2009

Polymers

Polyvinyl Chloride 3Low Density Polyethylene 4Linear Low Density Polyethylene 5High-Density Polyethylene 6Polypropylene 8Polystyrene 9Acrylonitrile Butadiene Styrene 10Polyethylene Terephthalate 11

Polymer Feedstocks: Olefins

Ethylene 13Ethylene Glycol 14Propylene 15Butadiene 16

Polymer Feedstocks: Aromatics

Paraxylene 18Styrene 18

Polymer Feedstocks: Intermediates

Purified Terephthalic Acid 20Acrylonitrile 20Ethylene Dichloride /Vinyl Chloride Monomer 21

Dimethyl Terephthalate 22

News 22

Americas and Asian Polymer Spot Price Assessments

FAS Houston US Contract FOT Brazil* CFR FE Asia CFR SE Asia CFR South Asia China($/mt) dlvd railcar ($/mt) ($/mt) ($/mt) ($/mt) Domestic

(cts/lb) (Yuan/mt)

PVC SUSP 550-560 40.00-41.00 —- 660-670 660-670 —- —-

LDPE G-P 915-926 46.00-47.00 1180-1190 980-990 980-990 —- 8700-8800LLDPE (Butene) 871-882 43.00-44.00 980-1000 985-995 985-995 1005-1015 8900-9100

HDPE Inj 822-832 43.00-44.00 980-1000 970-980 985-995 960-970 —-Bmldg 810-820 43.00-44.00 970-990 950-960 965-975 950-960 —-Film 926-948 47.00-48.00 970-990 950-960 965-975 970-980 8400-8500Yarn —- —- —- 970-980 985-995 —- —-

PP Homo Inj/Raffia+ 777-799 40.00-41.00 880-890 880-890 890-900 910-920 7900-8000Fiber —- 38.50-39.50 —- —- —- —- —-Copol 826-848 —- 980-990 920-930 920-930 920-930 —-IPP Film 910-920 910-920 950-960 —-BOPP 910-920 920-930 920-930 —-

PS G-P 1065-1075 48.00-49.00 —- 950-960 950-960 —- —-HIPS 1175-1185 53.00-54.00 —- 1060-1070 1060-1070 —- —-

ABS Inj —- 67.00-68.00 —- 1210-1220 1220-1230 —- —-

PET bottle grade 1146-1168# 1213-1235## 934-936 ** 934-936 ** —- —-

Notes: All price assessments reflect spot trades with the exception of US Contract Delivered railcar. * FOT Brazil assessments are for export material via truck to MERCOSUR markets. For AsianPVC, PS, and ABS, FE Asia refers to China. All Asian polymer assessments are basis L/C 0-30 days Credit differentials calculated using 1 month LIBOR +1.5%. + PP Raffia grade reflectsassessments for Asia only. # US PET bottle grade refers to DDP US West Coast. ## US PET contract price is in $/mt. ** Asian PET prices denote FOB North East Asia (South Korea, China) andFOB Southeast Asia (Thailand, Indonesia) respectively.

FOB Middle East Weekly Polymer Netbacks ($/mt)

Thursday Friday Monday Tuesday Wednesday Average

HDPE 914-924 924-934 924-934 934-944 934-944 926.0-936.0LDPE 954-964 964-974 954-964 954-964 964-974 958.0-968.0LLDPE 954-964 964-974 964-974 964-974 969-979 963.0-973.0PP Raffia/Injection 839-849 844-854 849-859 854-864 864-874 850.0-860.0

Notes: FOB Middle East netback denotes CFR Far East Asia assessments minus the prevailing container freight rate from Al-Jubail to Shanghai for a standard 20-foot container.

Daily Polymer Assessments

Thursday Friday Monday Tuesday Wednesday Average

CFR FE Asia ($/mt)

HDPE film 930-940 940-950 940-950 950-960 950-960 942.0-952.0LDPE 970-980 980-990 970-980 970-980 980-990 974.0-984.0LLDPE 970-980 980-990 980-990 980-990 985-995 979.0-989.0PP Homo 855-865 860-870 865-875 870-880 880-890 866.0-876.0

FD NWE (Euro/mt)

LDPE 830-840 830-840 830-840 830-840 830-840 830.0-840.0LLDPE 780-790 780-790 780-790 780-790 780-790 780.0-790.0PP Homo 690-700 690-700 690-700 690-700 690-700 690.0-700.0

FCA Antwerp (Euro/mt)

LDPE 800-810 800-810 800-810 800-810 800-810 800.0-810.0LLDPE 750-760 750-760 750-760 750-760 750-760 750.0-760.0PP Homo 660-670 660-670 660-670 660-670 660-670 660.0-670.0

FAS Houston ($/mt)

LDPE 1025-10471025-1047 992-1014 992-1014 915-926 989.8-1009.6LLDPE 920-930 920-930 910-930 910-930 871-882 906.2-920.4PP Homo 777-799 777-799 777-799 777-799 777-799 777.0-799.0

Notes: The weekly average represents the average of Thursday through Wednesday of the previous week.

Contents

PLATTS POLYMERSCAN VOLUME 32 / ISSUE 11 / MARCH 18, 2009

2 Copyright © 2009, The McGraw Hill Companies

Euro Contract Assessments (Euro/mt)

Germany Holland Italy France Spain Britain* FD NWE CP**

PVC susp 695-715 695-715 680-705 695-715 665-685 620-645 911-938

LDPE G-P 890-900 890-900 890-900 890-900 890-900 820-825 1167-1180

LLDPE C4 (Blown film) 890-900 890-900 890-900 890-900 890-900 810-815 1167-1180

LLDPE C4 (Cast stretch film) 900-910 900-910 900-910 900-910 900-910 819-824 1180-1193

LLDPE C6 (Blown film) 950-960# — — — — — —

LLDPE C6 (Cast stretch film) 950-960# — — — — — —

HDPE Inj 890-900 890-900 890-900 890-900 890-900 805-810 1167-1180

HDPE Bmldg 880-890 880-890 880-890 880-890 880-890 810-815 1154-1167

HDPE Film 860-870 860-870 860-870 860-870 860-870 795-800 1128-1141

HDPE HMW 2-5 900-905 900-905 900-905 900-905 900-905 826-830 1180-1187

HDPE HMW 5-10 895-900 895-900 895-900 895-900 895-900 821-825 1174-1180

PP Homo Inj 800-810 800-810 800-810 800-810 800-810 735-745 1049-1062

PP Copol 840-850 840-850 840-850 840-850 840-850 770-780 1101-1115

GPPP 885-895 885-895 885-895 885-895 885-895 830-839 1161-1174

HIPS 933-943 933-943 933-943 933-943 933-943 875-884 1223-1236

EPS 915-925 915-925 915-925 915-925 915-925 858-868 1200-1213

ABS GP/Nat 1170-1180 — 1170-1180 1170-1180 1170-1180 1097-1107 1534-1547

ABS Ave color 1435-1445 — 1435-1445 1435-1445 1435-1445 1346-1355 1882-1895

ABS Auto black 1220-1230 — 1220-1230 1220-1230 1220-1230 1144-1154 —-

PET bottle grade 1005-1025# — 985-1005 1005-1025 1005-1025 920-940

PET bottle grade — — — — — 981-1002##

APET film grade 975-995#

Notes: *FD Britain = FD UK, with assessments in British Pounds per metric ton. **FD NWE CONTRACT PRICE denotes FD Germany converted into US dollars. # LLDPE C6, PET bottle grade, APETfilm grade assessments are basis FD NWE in Euro/mt. ## PET bottle grade assessments basis FD UK are in Euro/mt. PET assessments refer to regular business at prices negotiated betweenbuyers and sellers on a monthly basis. LLDPE C6 denotes products from Ziegler-Natta catalyst.

Platts European Polymer Spot Price Assessments

FOB NWE FD NWE FCA Antwerp CFR Russia* CFR Turkey** FD UK

($/mt) (Eur/mt) (Eur/mt) (Eur/mt) ($/mt) (GBP/mt)

PVC SUSP 665-675 530-560 — 510-530 700-720 —

LDPE G-P 1025-1035 830-840 800-810 860-870 1050-1060 —

LLDPE (Butene) —- 780-790 750-760 820-830 975-985 —

HDPE Inj 955-965 780-790 760-770 850-860 980-990 —

Bmldg 945-955 810-820 780-790 850-860 970-980 —

Film 985-995 805-815 780-790 850-860 1010-1020 —

PP Homo Inj 815-825 690-700 660-670 530-540 840-850 —

PP Raffia — — — — 840-850 —

PP Copol 905-915 740-750 710-720 580-590 930-940 —

PS G-P 785-795 740-750 — — 810-820 —

HIPS 855-865 788-798 — — 880-890 —

EPS 1165-1175 838-848 — — 1190-1200 —

ABS GP/Nat 1225-1235*** 1018-1028 — — —

PET bottle grade — 850-870 — — — 770-820

PET bottle grade — — — — — 821-874#

Recycled PET — 680-700 — — — 630-670

Recycled PET — — — — — 672-714#

Notes: FOB NWE prices are based on exports of 300mt or more. *CFR Russia denotes CFR St Petersburg; ** CFR Turkey denotes CFR Istanbul; *** ABS GP/Nat denotes CFR NWE in $/mt. #PET bottle grade and Recycled PET assessments for FD UK are in Euro/mt. Recycled PET assessments are for a hot wash flake without food approval.

PLATTS POLYMERSCAN VOLUME 32 / ISSUE 11 / MARCH 18, 2009

3 Copyright © 2009, The McGraw Hill Companies

Polyvinyl Chloride

Europe

The PVC market was seen close to finalising negotiations forthe March contract price. The final price is expected to beclose to a rollover with the upside capped within a range ofEur10-30/mt. Any buyer who has agreed an increase isreported to have had there contract prices brought up inline with other buyers rather than a general increase appliedto all buyers. “Those buyers that were at the bottom of therange for February have been brought up in line with otherbuyers,” a source at one producer noted. Other sourcesnoted that the month started with strong claims fromproducers that they would be looking for increases upwardsof Eur50/mt but the reality has been somewhat different intrying to achieve these increases. The lack of demand acrossEurope has severely undermined the ability for buyers toabsorb any increase in PVC prices. Although demand inMarch was reported to have improved compared withFebruary, the overall level of consumption was still seen asbelow year-ago levels. As producers have been unable toimplement hoped-for increases, they are faced with adifficult situation going forward. In February, feedstocksprices in the form of the monthly ethylene contract priceincreased by Eur95/mt to currently stand at Eur675/mt. Incontrast, PVC prices have fallen from Eur885/mt at the startof 2009 to currently stand at Eur705/mt, a fall of overEur150/mt. The fall in PVC prices combined with the rise infeedstocks costs amounts to a reversal of Eur280/mt for PVCproducers. The net result has been to squeeze margins forproducers of PVC across Europe, but the rise in ethyleneprices is having little impact on PVC buyers, as previouslyethylene prices have been falling while PVC prices havebeen rising. As one distributor commented: “I am buyingPVC not ethylene.” This rise in production costs had ledmany producers to push hard for price rises at the beginningMarch and the inability to achieve any meaningful increaseis a reflection of the poor level of demand. Some marketsources noted the coming spring period may offer somehope of improvement in overall demand, as activity in theconstruction sector would typically see a seasonal upturn.The hoped-for increase in PVC demand would be anincrease compared with January and February levels, but isunlikely to be an increase on year-ago levels, sources said.The level of underlying demand in Germany is particularlyclouded due to government programs aimed at preventingredundancies. The scheme involves the government payingup to 50% of a workers salary in order to prevent job losseswhile a company adjusts to market conditions. There arereports that the scheme is being used by the constructionsector leaving many sources unclear as to what will happenwhen the government support is removed. in the spotmarket prices for FD NWE were assessed unchanged atEur545/mt with offers from Asia reported at this level and

offers from the USA reported at marginally higher levels.CFR Turkey prices were reported to have fallen by as muchas $40/mt again on the back of cheaper priced productsbeing available from Asian markets. While a seasonal upturnmay help to increase volumes, the scale of this upturn maybe insufficient to sustain any increase in PVC prices, sourcessaid Wednesday.

United States

April export values out of the US were talked lower thisweek with prices talked notionally in the $550-560/mt FASHouston range. Even at that level however, sources saidbuyers were hard to find. Sellers were heard to be working tohold offers near $570/mt FAS Houston this week, however,buyers were holding out in an effort to get better deals. Withslowing buy interest in India and China and weak demandin North Africa, Europe, and the US, suppliers were likely toface trouble in selling the same volumes they did inFebruary and March. Sources estimated that India alone saw

Foreign exchange

Eur1 to $ 1.3113 £1 to Eur 1.0662

Polymer Spot Freight Rates ex-Middle East ($/mt)

From: Middle East Middle EastTo: 25-100 mt >100mt

East China 15-20 15-18South China 15-18 10-15India 23-25 20-23Southeast Asia 20-22 18-20NW Europe 80-90 80-90Turkey 100-110 100-110US Gulf 75-80 70-75Latin America 85-90 80-85

Notes: Please refer to the methodology guide for details on port locations.

Metals

Aluminum US Mar 17 cts/lb 63.916Tin US Mar 12 cts/lb 495Tin Europe Mar 13 $/mt 11397-11456

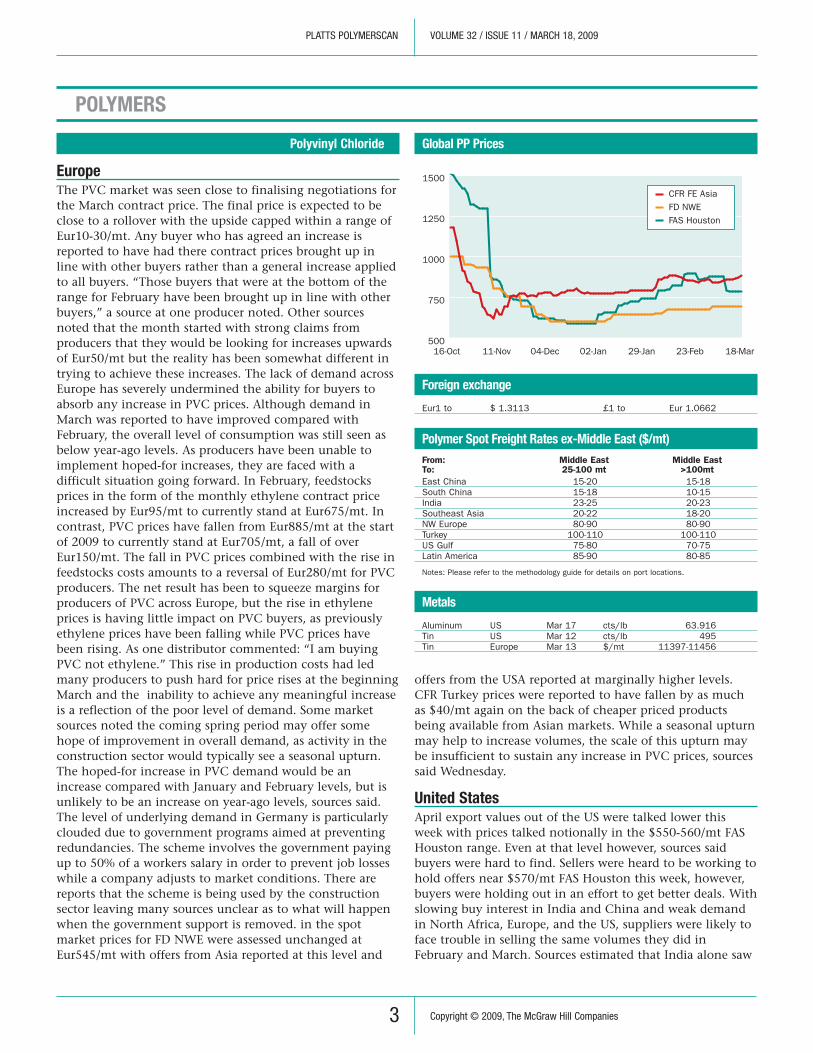

Global PP Prices

($/mt)

500

750

1000

1250

1500

18-Mar 23-Feb 29-Jan 02-Jan 04-Dec 11-Nov 16-Oct

CFR FE AsiaFD NWEFAS Houston

POLYMERS

between 50,000-60,000 mt of PVC land on its shoresbetween February and March. As well, direct producer dealswere attributed with dragging prices lower as one majorproducer was heard to be aggressively pursuing market shareand pricing out traders in the process. Sources reported thatthe producer was offering into Latin America at $610/mtCIF, a number that would produce a netback of near $520-530/mt FAS Houston. “We just cannot compete against thedirect producer deals,” said a participant. Meanwhile, on thedomestic front, producers were still working to pushthrough a 2 cents/lb price hike on domestic contracts.Producers initially announced a 5 cents/lb increase forFebruary, however, ultimately took 3 cents and pushed theremaining 2 cents/lb back to March. Additionally, mostproducers had announced a 3 cents/lb increase for April.Buyers were bearish on the increase, however, givenpersistently weak domestic demand. In production news,Georgia Gulf confirmed that its production at both LakeCharles, Louisiana and Aberdeen, Mississippi was up andrunning. As well, the company has changed the terms ofone if its credit facilities, pushing back covenants with itslenders until March 2010 while increasing and extending itsaccounts receivable securitization until March 2011, thecompany announced earlier this week.

Asia

April Chinese imported PVC prices were flat this week.Offers between $660-700/mt CFR China were reported, anddown to $650/mt CFR China was heard, but unconfirmed.Some buyers were still holding back and looking for anumber below $650/mt CFR China. Deals were reporteddone between $660-690/mt CFR China. A Korean producerreported selling 6,000 mt of PVC at $690/mt CIF China fordelivery end March/early April, and 10,000 mt for deliveryinto Shanghai in April at $690/mt CIF China. An Indiantrader reported selling 200mt at $700/mt CFR China,Indonesian-origin, delivery March. A Taiwanese supplieroffered and traded April-delivery cargoes at $660/mt CFRChina. The difference in traded prices was due toantidumping rates between Taiwan and Korea, for deliveryinto China. Overall demand remained weak into China,with transaction volumes into China below levels for thesame period in 2008. Domestic Chinese prices firmedslightly this week, at around RNB 100-200. Carbide-basedproduction prices were heard between Yuan 6000-6200/mtdelivered China, while ethylene-based production was Yuan6200-6400/mt delivered China. Sources estimated thatcurrent carbide production in China is on average at 45-60% rates. Domestic prices increased following the loss ofbenefits offered by the Chinese government for carbideproduction the first two-and-a-half months of the yearexpired. In India demand remained good, offers fromTaiwan and Korea were heard at $730/mt CFR India. FromEurope the offers were $700/mt CFR India and the offer levelwas below $700/mt CFR India from the US. Meanwhile,Japanese PVC exports were strong in February, rising 2.8%year on the year to 53,961 mt. On a month-on-month basis,

exports rose 7.1%. according to data from Japanese VinylEnvironmental Council officials. On the production side,Shanghai Chlor-Alkali Chemical’s 410,000 mt/year PVCplant in Shanghai will undergo a three-week turnaround inMay. Hanwha’s 225,000 mt/year PVC plant in Yeosu, SouthKorea, will start a one week planned turnaround next week.While, Japan’s Taiyo Vinyl is in the middle of a plannedturnaround at its 310,000 mt/year PVC plant in Yokkaichi.The plant will restart March 24.

Low Density Polyethylene

Europe

Demand in the spot market has flattened out further, tradingsources said this week, with spot prices remaining stable atEur830-840/mt FD NWE. Some further attempts to increasespot prices to Eur850-890/mt FD NWE levels had been madeby traders, though with limited success, market sources said.“We have very poor sales and it is very difficult to get pricesto Eur850 and above, as there are still sales done at Eur830-840/mt FD NWE range,” a large-volume trader said. A traderreported a spot deal at Eur825/mt FD Benelux, while anotherreported transacting at Eur850/mt FD Spain. Some tradersnoted early attempts by converters to de-stock as the end-user demand deteriorated in March. Converters reportedprompt-focused business, impacted by short lead times onorders. “It is very difficult to pass the increases to the end-user markets, we are all suffering now. Our chances ofrecovering the increases are close to zero. While ourutilization rates are weak every converter is seekingvolumes—it is very competitive for orders,” one convertersaid. “Every converter is eating in to his own [already verythin] margin...as a result converters are careful with theirstocks, as the orders are very slow,” another converter said.While some converters hoped to see a more favorableenvironment in April, others expected to see another lastrally in prices, before market starts to see new alternativesupplies in the market in May. Producers, on the other hand,were looking to recover dents in their margins further inApril, with one stating “Eur10-20/mt increase in April is notenough, we need another substantial increase in April or wetrim operational rates further. It is better to shut productionthan to lose money on every tonne supplied,” he said. Otherproducers said that if demand eroded in April, they wouldfocus on exports once again in a bid to achieve betternetbacks. “Our customers think that prices will fall, butdemand for us is still relatively strong. April is going to be acrossroad,” another producer said. “We are hardening ourposition now, we had to move more aggressively on theprices for extra volumes requested in the second half ofMarch,” a fourth producer said. Gross values reported thiswere range-bound. Three producers confirmed contractualbusiness at Eur890-900/mt FD NWE, while two producersreported business at Eur900-920/mt FD NWE. Convertersreported a wide range of Eur850-910/mt FD NWE for theirMarch contracts. Gross values remained stable at Eur890-

PLATTS POLYMERSCAN VOLUME 32 / ISSUE 11 / MARCH 18, 2009

4 Copyright © 2009, The McGraw Hill Companies

900/mt FD NWE this week. In production news,LyondellBasell is set to shut its 320,000 mt/year LDPE plantat Aubette, France from March 24 for a week, a companysource said Friday. “We believe that it is important to keep aclose control on stock levels to support a further priceinitiative in April,” the source said. SABIC is set to shut its120,000 mt/year LDPE autoclave unit at Geleen, theNetherlands, a company source said Monday. “The autoclaveproduction is a very expensive and unsustainable processand that is why we have take a decision to shut ourautoclave plant at Geleen,” he said, adding: “We have othersubstitute products available for our customers...The date ofthe closure has not yet been set,” he said. SABIC Europe isalso set to have its first LDPE available out of its new400,000 mt/year tubular plant at Wilton, UK, in May, thesource said, with the plant due to start up at the end of Q12009, he said.

United States

Low density prices decreased steadily over the week by atotal of 5 cents/lb following lower feedstocks. Westlake washeard to have offered low density at 42 cents/lb FASHouston but even at that number some traders said demandwas poor. “I just don’t see much demand for LD right now(in Latin America),” a trader said, despite the lower offer.There also was not much interest in US LD from Asia whereagricultural seasonal demand was absent. Export buyersexpected lower offers going forward considering spotethylene was about 22-23 cents/lb FD USG. Also, producersDow and Westlake were heard to be starting up steamcrackers in the near term that would both put pressure onspot monomer and lengthen LD supply. March supply wasstill somewhat tight, sources said, and for this reason thedomestic 5 cents/lb price increase had not been rescinded.Sources said that while the month’s HDPE increase was mostlikely a failure, for LD and LL the increase still had legs. Ifpart or all of the increase takes hold, backward integrated toethane producers would see margins widen as ethane valueshave fallen 4 cents/gal to 31-31.5 cents/gal from a week ago.

Asia

Asian low density polyethylene prices increased $10/mt on aweek-on-week basis, attributed to constricted supplies fromthe Chinese mainland that saw domestic prices ascendingYuan 300/mt to Yuan 8,700-8,800/mt on an ex-works basis.The market knee-jerked to the shutdown of Shanghai Secco’ssteam cracker and its downstream 650,000 mt/year PE unit,in light of upcoming turnarounds at some of Sinopec’ssubsidary companies in April. LDPE prices were the slowestamong all the PE grades to react to the bullish sentiment,market sources said, and more clearly defined in East Chinathan South China. Industry observers said that SouthChinese end-users were more dependant on actual demandbecause their businesses hinged strongly on re-exports. Thelowest offer heard was placed by QAPCO at $985/mt CFRChina, L/C at sight basis, to which the company sold out itsdaily availability, a company source said. Meanwhile, trades

were concluded broadly within the range of $980-990/mtCFR FEA and SEA, but the majority of producers would onlybegin offering April shipments in the next week thereforediscussions were still a tad quiet.

Latin America

One major Brazilian export to the Mercosur reported loweroffer prices this week matching other suplliers. Buyersconfirmed deals at $1,180/mt FOT for LDPE. In the Mexicandomestic market, LDPE price was heard at 45-48 cents/lbafter the 10% increase reported in the first week of March.The adjustment was realized due to the dollar vs pesoexchange rate and also due to international pricingtendencies. “We have kept sales volumes as programmed forthis month even though we had heard of the existence ofcheaper imported offers. The contracts we have help usmaintain stable prices,” said a source. In the Peruviandomestic market, participants were reselling LDPE at$1,250/mt industrial. Offers from the US to Peru were at$1,160/mt CFR film and industrial, while offers comingfrom Korea were at $1,100/mt CFR film. In the Colombiandomestic market, LDPE was being offered at Pesos 3,396/kgbulk and at Pesos 3,466-3,646/kg bagged. LDPE was beingsold in the Brazilian domestic market at Reals 3,550/mt CIFfor film and industrial grades for medium volumes and atReals 3,600/mt CIF for small volumes.

Linear Low Density Polyethylene

Europe

European spot values for LLDPE C4 have peaked, sometrading source said, adding that they were struggling inimplementing substantially higher prices. “We are trying toachieve Eur810-830/mt FD NWE but it is not easy, especiallywhen we are competing with imports present in themarket,” a large-volume trader said. “The market is quietnow, there is definitely less energy in the market, peopleseem to be sedated,” a second trader said. “Some newplayers have started the pre-marketing now. I would say thatout of all polyethylene grades LLDPE C4 now is most underpressure on the spot market, we are trading at Eur780-800/mt FD NWE now and you can not get higher prices,”another trader said. Some converters have confirmedtrialling pre-marketed product ex-Middle East. “We havesold at Eur770-780/mt FD NWE this week,” a third tradersaid. “We feel that we have already seen the best days of theyear, however having said that oil has been recently movingup and the world as we know it today may reshape itselfvery quickly; we are holding our horses now,” he added.“Some people have started to buy for April now for week 14-15 delivery, maybe prices will have one last rally before theEaster,” the second trader said. In addition, some tradershoped the recent surge in Asian prices would boostEuropean market sentiment. Asian LLDPE prices surged by$15-25/mt this week, impacted by tightening supplies.SABIC will have less PE spot supply after shutting its 890,000

PLATTS POLYMERSCAN VOLUME 32 / ISSUE 11 / MARCH 18, 2009

5 Copyright © 2009, The McGraw Hill Companies

mt/year HDPE/LLDPE PetroKemya plant last week onproduction issues and the start-up of SHARQ’s new 400,000mt/year LLDPE plant at Al Jubail has been delayed to H2 2009.Qatofin has delayed the start-up of its new 450,000 mt/yearLLDPE plant at Masaieed to the fourth quarter of 2009.Meanwhile, in the contract LLDPE C4 market, producersremained content, achieving most of the targets set for March.“We are partially satisfied, the orders are coming through andwe are reaching our targets but our profitability still remainspoor,” a producer said. “Our C4 sales are not going bad, oursales are good. We have very little or no differentiationbetween LDPE and LLDPE C4, while the demand in LLDPE C6has improved even further,” another producer said. Producerscontacted this week confirmed the current published range forLLDPE C4 grades, while converters reported a wide range intheir contracts. Some converters had to accept Eur910/mt FDNWE value with one of their suppliers, who implemented,according to the converters, Eur120/mt increase, which wasnot negotiable. Other converters reported gross values rangingfrom Eur850-890/mt FD NWE. Gross values in C4 and C6grades remained stable this week. Some producers also voicedconcerns about demand developing further into Q2. “We aregoing to react to falling demand, we may adjust production asthere is not point in chasing, grooming and looking after thehorse that makes you lose money by consistently coming lastat the race,” a producer said. Some producers also noted thatApril will be the test for the real demand, as the industry hasrestocked in Q1. While in rotomolding there is good demand,stretch film is slowing down as our customers have thinorders,” a producer said, adding that while seasonalagricultural film business was disappearing, demand for silageapplications were strengthening.

United States

Linear low density prices decreased 2 cents/lb due to lowerethylene costs and weak demand. Offers were talked at 40-40.5 cents/lb FAS Houston but buy interest from LatinAmerica and North Africa were slow. Exporters hoped thatethylene prices would continue to fall and soon producerswould be able to offer low enough to allow for exports toAsia where prices were near $1,000/mt CFR China and hadalready hit that level in South Asia. Compared to HDPE,LLDPE supply was tight which gave support to the March 5cents/lb domestic price increase. While it was unusual tohave a split in PE increases, it would not be the first timeone grade of PE saw an increase when others did not,sources said. Higher prices could be short-lived, however;once Dow, Westlake, and ExxonMobil restart long idledsteam crackers. If producers can lower export offers inApril, they may see more business in South America asBrazil would have trouble following decreases due toexpected higher ethylene costs. Brazil’s ethylene pricefollows US and European contracts at a month lag and theNWE monomer contract for March concluded nearly 15%higher than February’s CP. The US has yet to settle itsMarch ethylene contract but would likely be down due tothe lower spot prices.

Asia

Asian LLDPE prices trekked $15-25/mt higher on the week,buoyed by tightening supplies in the region. The priceincrease and bullish sentiment was most marked in China,where domestic prices leaped Yuan 300-450/mt to Yuan8,900-9,100/mt on an ex-works basis, on the back of theoutage of Shanghai Secco’s steam cracker and its 650,000mt/year PE unit. Secco was heard to be restarting its crackerby March 23, but industry observers surmise PE suppliesfrom Secco would not resume until April. Offers byproducers such as Reliance and Borouge were hiked to$1,000/mt CFR and above, while the majority would onlybegin offering April shipments next week. Qatofin hasdelayed the startup of its new 450,000 mt/year LLDPE plantat Masaieed to the fourth quarter of 2009. SABIC will haveless PE spot supply after shutting its 890,000 mt/yearHDPE/LLDPE PetroKemya plant last week on productionissues and the startup of SHARQ’s new 400,000 mt/yearLLDPE plant at Al Jubail has been delayed to H2 2009. InSouth Asia, offers rose to $1,020/mt CFR.

Latin America

Brazilian March export price increases failed to go throughand distributors were heard buying and selling at the sameprice levels in the Mercosur. One buyer in Paraguay confirmedthe $980/mt FOT for LLDPE butene. Paraguayan polyolefindemand firmed up in March due to an expected price increasein April, a local distributor said this week. Deals in Paraguaywere heard at $1,050/mt CIF LLDPE butene and hexane. “Wegenerally sell between 500 and 800 mt of PE per month, butwe were pleasantly surprised with the 1,500mt sold inMarch,” said a source. The main driver behind the demandwas buyers looking to secure resin before a possible $50/mt aprice increase in April, sources said. Brazilian domestic LLDPEwas being offered at Reals 100/mt below end February levels, aproducer reported. Since the start of February, prices droppedReals 200-250/mt. Following the price reduction, resins werebeing offered in the Brazilian domestic market at Reals3,800/mt CIF LLDPE butene and hexene and at Reals3,900/mt CIF octene (prices with pis/cofins).

High-Density Polyethylene

Europe

European traders reported seeing a surge in spotblowmolding and film spot prices in Spain this week, withavailability impacted by a production issue with a majorsupplier. “Film and blowmolding grades definitely have apremium of almost Eur50/mt in Spain,” one trader said.“We can sell spot blowmolding in Spain at Eur900/mt FDNWE now,” another trader said. In other NorthwestEuropean regions, spot market demand has flattened outfurther, trading sources said. Spot values in injection gradeeroded this week as more traders reported trading in a rangeof Eur780-790/mt FD NWE. “We are trying to get Eur800/mtFD NWE but it is very difficult now,” a trader said. One

PLATTS POLYMERSCAN VOLUME 32 / ISSUE 11 / MARCH 18, 2009

6 Copyright © 2009, The McGraw Hill Companies

trader disagreed, saying they were offering to France atEur840/mt FD France and were hoping the market wouldreach that level soon. Spot values in blowmolding grade, onthe contrary, strengthened this week to Eur810-820/mt FDNWE, while film grade strengthened to Eur805-815/mt FDNWE this week. Some traders noted early attempts byconverters to de-stock as the end-user demand deterioratedin March. Converters reported prompt-focused business,impacted by short lead times on orders. “It is very difficultto pass the increases to the end-user markets, we are allsuffering now,” one converter said, continuing: “Thechances of recovering the increases are close to zero. Whileour utilization rates are weak every converter in the marketseeks volumes—it is very competitive.” Another convertersaid: “Every converter is eating in to his own margin, whichis already very thin...[hence] converters are careful with theirstocks, as the orders are very slow.” “We feel that we havealready seen the best days of the year. However, oil has beenrecently moving up and the world as we know it today mayreshape itself very quickly—we are holding our horses now,”a trader said. In addition, some traders hoped that the recentsurge in Asian prices, impacted by tighter materialavailability, would provide a boost to European marketsentiment. SABIC for instance, had shut its 890,000 mt/yearHDPE/LLDPE PetroKemya plant at Al Jubail last week andwould be shutting some of its SHARQ PE units formaintenance on ongoing production issues. As a result, thecompany would have less PE spot availability in April, Asiansources said. Meanwhile, the start-up of its new 400,000mt/year HDPE plant at the SHARQ 3 complex has beendelayed to the second-half of the year. In the Europeancontract market, meanwhile, producers mainly reported agood progression of orders, though some noted a marginalflattening of demand. “We are partially satisfied, the ordersare coming through and we are reaching our targets but ourprofitability still remains poor,” a producer said. While someconverters hoped to see a more favorable environment inApril, others expected to see another the last rally in prices,before market starts to see new alternative supplies in themarket in May. Producers, on the other hand, were lookingto recover dents in their margins further in April, with onestating “Eur10-20/mt increase in April is not enough, weneed another substantial increase in April or we trimoperational rates further,” he said, adding: “It is better toshut production than to loose money on every tonsupplied.” Other producers said that if demand eroded inApril, they would focus on exports once again in a bid toachieve better net-backs. “We are going to react to fallingdemand, we may adjust production as there is not point inchasing, grooming and looking after the horse that makesyou lose money by consistently coming last at the race,” aproducer said. Some producers also noted that April will bethe test for the real demand, as the industry has restocked inQ1. Gross values in injection grade strengthened further toEur890-900/mt FD NWE. Blowmolding grade firmed toEur880-890/mt FD NWE, while film grade strengthened toEur860-870/mt FD NWE.

United States

High density prices dropped across the board as ethylenefell, which allowed offers to decrease and opened exportopportunities to deepsea markets. Spot ethylene has tankednearly 10 cents/lb from early March to just over 22 cents/lbas US ethylene capacities were slowly coming backonstream. Late last week Ineos held a blow molding exportauction that concluded at 34.5 cents/lb delivered in railcarsto Houston (37 cents/lb FAS Houston). The company wasalso heard to have sold injection grade HD at 35 cents/lb inrailcars. These prices worked for export to Latin America andAsia. Film grade had been sold in March at 44 cents/lb FASHouston but traders were waiting for new offers for April ata lower number. The 5 cents/lb domestic price hike washeard to be close to being tabled to April 1 for high density.Weak supply/demand fundamentals coupled with the fall infeedstock costs and lower export prices; all worked againstimplementation of the increase. Ineos was also heard tohave held a domestic market auction for 10 cars of HDinjection where the concluded price was 37.8 cents/lb withan upcharge of 2.5 cents/lb depending where the carswould be delivered.

Asia

The Asian high density polyethylene market leaped $15-20/mt onthe week, lifted by taut supplies, particularly in China. Theshutdown of Shanghai Secco’s cracker and 650,000 mt/year PEunit had a palpable impact on the local market in light ofupcoming maintenance at some Sinopec subsidary companies inApril. The cracker was rumored to be restarting on March 23, andPE supplies from Secco only to resume by April at the earliest.Chinese domestic prices spiked Yuan 300-800/mt across all grades,but most noticeably to Yuan 8,400-8,500/mt for HDPE film andYuan 8,800-9,000/mt for HDPE yarn. Of all the grades, HDPE yarnwas the grade with the stellar increase in the week, leading thepack in terms of demand, sources said. On the deliveredbenchmarks, trades for HDPE yarn was heard concluded byHaldia at $980/mt CFR China, Formosa at $970/mt CFR China,while offers all trekked higher to $990/mt and above. Film gradeHDPE was offered at $950/mt to South China, while the majorityof producers in Asia had sold out their March availability andwere preparing to offer April shipments in the coming week.Bullish sentiment was also buoyed by gains on the western crudebenchmarks in the week and news of certain outages. SABIC forinstance, had shut its 890,000 mt/year HDPE/LLDPE PetroKemyaplant at Al Jubail last week and will be shutting some of itsSHARQ PE units for maintenance on ongoing production issues.As a result, the company would have less PE spot availability inApril. Meanwhile, the startup of its new 400,000 mt/year HDPEplant at the SHARQ 3 complex has been delayed to the second-half of the year. In South Asia, HDPE blow moulding was offeredat $950-960/mt, yarn at $1,020/mt, injection at $960-970/mt, andfilm at $970-980/mt CFR India. The PE market was described asbroadly stable with demand still good. India’s Reliance has alsodelayed the startup of its new 1.1 million mt/year PE unit atJamnagar to sometime between 2010-2011, a company sourcesaid this week.

PLATTS POLYMERSCAN VOLUME 32 / ISSUE 11 / MARCH 18, 2009

7 Copyright © 2009, The McGraw Hill Companies

Latin America

Brazilian HDPE producers expressed concern that a potentialincrease in ethylene prices would result in higherpolyethylene prices and in turn, stifle demand and compressmargins, sources said. Buyer deals in the Mercosur wereheard at the same levels this week and one major Brazilianproducer lower price offer for the resin. March ethyleneprices in Brazil were talked this week at $760/mt FOBhowever a 15% increase in European ethylene values couldpush ethylene prices up despite an expected lower contract.Ethylene prices follow ethylene contract prices in Europeand the US with a month lag. March HDPE was sold in theBrazilian market at Reals 3,900/mt CIF for blow molding andinjection for small volumes, Reals 3,800/mt CIF blowmolding and injection for medium volumes and at Reals3,600-3,700/mt CIF for the same grades for large volumes.

Polypropylene

Europe

Assessed Northwest European polypropylene contract levels heldsteady this week as what was described by sources as anindicative average price of settlements achieved. A number ofsources reported having settled their contracts in the wide rangeof Eur765-830/mt FD NWE for homo-inj grade. The assessedlevel illustrates a Eur30/mt increase versus Platts assessedFebruary contract price levels. One producer said in terms ofcustomers with previously lower priced February contract levelsthere was “absolutely no escape,” implementing a full Eur50/mtincrease to levels of around Eur820-830/mt FD NWE for homo-inj. Other producers said however that they had achievedincreases of Eur20-30/mt with contracts settled so far, one at ahigh end of Eur800/mt FD NWE. A number of sources thoughsaid they had more negotiations to finish by the end of themonth. In Spot business, it was described as another quiet andcalm week, also with levels made in a wide range of Eur690-750/mt FD NWE. One trader said he had heard producer offersof around Eur720/mt FD NWE for homo-inj, but had still notbeen able to achieve anything over Eur700/mt FD NWE with hiscustomers. “Producers are trying to take a firm position (onspot) but it really varies on how balanced they are on particulargrades,” he said. Another trader agreed that there had been littlemovement in spot prices or demand for commodity gradematerial, and had therefore he had been “more active in off-grades.” He said that he was hoping for some improvement indemand in coming weeks, but that “converters are not eager tocommit to increases as they are still waiting to see propyleneprice developments for April.” “We can buy material at Eur630-640/mt FCA Antwerp,” another trader said. Export opportunitiesto Asia were said to be waning still according to sellers thisweek, due to the increase in production costs from March’sEur42/mt increase in propylene and lower prices in Asia thanseen in February. One NWE producer said he was “continuing toship in March for business acquired in February for India andPakistan. Higher costs close the arb window a bit but there areopportunities there for specialty grades where customers are

willing to pay more.” In Russia this week, prices continued tohold steady as sources described demand as stable. One suppliersaid he was did not expect any price increases until around Apriltime, adding that he was still exporting material to Asia, but insmaller lots due to drop in prices and demand seen in Chinarecently in Asia. Prices were pegged at Eur540-550/mt CFR StPetersburg. In the UK, contract prices were assessed steady, asbuyers and sellers said that contract numbers continued to holdparity with European contract prices when applying an averageof the month GBP/Eur exchange rate. In Turkey, demand wasdescribed by sources to still be depressed in general, one tradersaid though he had seen “some good inquiries for small parcelsrecently.” He explained he had seen ex-Turkmenistan offers of$850/mt CPT Istanbul plus 6.5%, equating to $895/mt CFRTurkey. Adding that due to the poor state of demand, anyincrease in offer levels was only driven by recent exports to Asiathat have also gradually reduced in activity.

United States

Domestic prices increased this week for homo polymerpolypropylene, as ranges were reportedly in the 40’s cents/lb,a buyer said. Despite the increase in pricing, demandremained poor. “There has been a 44% decline in sales,” saida PP buyer. “Supply is long, there is no demand and no oneis buying.” Still producers were heard to be slashingoperating rates in an effort to minimize inventory levels andbolster pricing, participants said. In the export market, offspec material was pegged in the range of 33-38 cents/lb,delivered rail car, for homo polymer utility grade. Demandwas also reportedly stagnant for the export PP homo polymermarket, given the auto and housing industries have seensignificant declines in sales. Producers, however, werereportedly offering higher levels in an attempt to raise theprice, despite the lack of buyer interest. Upstream, oneproducer confirmed settling March PGP contracts up 1cent/lb at 29 cents/lb. “It’s likely a split settlement at 1-2cents up,” said one participant. Spot propylene prices moveddown as activity continued to be slow this week. Arbitrageopportunities to Europe and Asia were closed and domesticappetite for material thinned, sources said.

Asia

Asian polypropylene prices spiked $25-60/mt higher in theweek, an increase led by gains in the Chinese domesticmarket. Local retail offers for homo leaped Yuan 300-700/mtto Yuan 7,900-8,100/mt, Yuan 7,800-7,900/mt for inj/yarnand Yuan 8,700/mt for block copol, all on an ex-works basis.Shanghai Secco has shut its cracker and its 250,000 mt/yearPP plant. The company was heard to be planning a restartthem on March 23. Inventory levels in China among localproducers were heard to be lower than normal, with Sinopecand Petrochina operating their PP units at an average 80%capacity, industry observers said. Short supply becameapparent to Chinese buyers this week. In addition, SABIC saidit would have less PP spot material to offer in April due toongoing production issues at its plants, without giving furtherdetails. Indian producers sold raffia/inj in a broad range of

PLATTS POLYMERSCAN VOLUME 32 / ISSUE 11 / MARCH 18, 2009

8 Copyright © 2009, The McGraw Hill Companies

$870-880/mt CFR, $900-910/mt for IPP film, but had hikedoffers to $900/mt and above levels by Wednesday. Koreanproducers reported selling $900/mt for homo/injection, $930-940/mt for block copol, $910-920/mt for BOPP, and currentoffers were $10-20/mt higher from deal done levels. Taiwaneseproducers sold PP homo at $900/mt, $930-950/mt for IPP film,$935/mt for BOPP and around $930/mt for block copol.According to sources, BOPP, injection and block copol wereseeing the best demand. BOPP because of high operations atdownstream factories, injection buoyed by strong demand inSouth China and block copol on short supply. Southeast Asianprices were lifted in tandem with China, but price indicationswere few and far between as Southeast Asian producers hadsold out of March material and were offering April shipmentsonly in the coming week. In South Asia, trade was thin asparticipants were expecting product from Reliance’s newJamnagar plant to be available in the market soon in April.

Latin America

Prices failed to move this week as distributors in theMercosur reported buying and selling at static levels, beforeApril announcements. Buyers confirmed prices at $990/mtfor co-polymer and at $890/mt for homo. Domestic PPprices in Argentina were set to rise following a $30/mt,March price increase announcement by one producer. It wasnot immediately clear whether other producers wouldfollow. “We expected a better demand for March butprobably we are going to be with the same volumes we sawlast month,” said the souce. Following the increase, PP wasbeing offered in the domestic Argentinean market at $1,050-1,080/mt CIF raffia, $1,060-1,090/mt CIF injection, $1,030-1,100/mt CIF random, $1,100/mt CIF co-polymer impactand at $1,300-1,400/mt CIF special resins. Meanwhile, in theBrazilian domestic market, PP prices for March were downReals 200/mt compared to the previous month, sources said.

Polystyrene

Europe

Two producers said this week they expected to settle theiraverage March contracts at a rise of between Eur30-40/mt aboveMarch contract prices. One converter said that he expected tosettle its monthly intake volumes at a rise of Eur30/mt, leavingthe gross CP below Eur900/mt FD NWE. Most producers nowadmit their original indications of around 60/mt wereunachievable, given poor demand, which was expected to persistwell into the second quarter. If confirmed this implied producershad been able to recover some margin lost in February. However,producers argued that with the combined February-March SM CPdelta of around Eur81/mt, a recovery of no more than Eur10/mtwould be considered a disappointment. Sources were not hopefulfor an improvement in April demand, and hence expected thatunless further production cuts were announced then there waslittle scope for further margin recovery. “Demand in Europe hasbeen less than expected [this year], no worse than February,” aproducer said. “If demand from industry was the same or even a

slight increase, I think prices could fall further. [But] if there arefurther PS production cuts, it could be [possible] to see anincrease in prices,” the converter said. Most producers saidpegged the GPPS-HIPS spread at no less than Eur50/mt, whileanother said that pressure from polybutadiene prices had led tosome spreads agreed as low as Eur40/mt. Polystyrene productioncapacity was oversupplied by around 700,000 mt/year, a numberof producers and converters agreed. Sources point to industry2008 production estimates of around 2.5-3 million mt/year,while actual demand was thought to be around 2.2-2.3 million,including exports, sources said. One producer pointed to “arecession factor of 250,000 mt/year”. This was the amount ofcapacity cut due to the economic downturn. Last week Total saidit would permanently shut one of its two lines at its Gonfreville,France site. Although the company would not comment on thespecific capacity to be shut or the total site capacity, one sourceestimated the high impact PS line was producing around 60,000mt/year, from a total production at the site of around 120,000mt/year. Both producers and converters agreed that capacitiesneeded to be cut or a degree of consolidation would be on thecards. “The European market needs more consolidation. There isa constant innovation in these sectors, meaning less plastics (insome applications),” a producer said. “More capacity shutdownsare coming and this has to be done [to aid recovery].” Sourcessaid that the smaller units should disappear due to theirinefficiency. “Closures are all that’s left. A 60,000 mt plant is notworld scale, and they will continue to underperform,” a producersaid. In EPS, a producer said it expected to settle its Marchcontracts at a rollover but was still pushing for an increase ofaround Eur10-20/mt in March. Sentiment continued to beweighed by lackluster demand and still little improvement inconstruction. In production news, BASF started up a new 90,000mt/year expandable PS unit at its Ludwigshafen, Germany unitlast week, the company said. Also, Sunpor last week shut downits 70,000 mt/year unit in Polten, Austria, for a scheduledturnaround, company sources said.

United States

Producers and consumers reported a 3 cent hike on PScontracts in March, with two sellers delaying the remaining 2cents via temporary voluntary allowance. The initialnomination was for 5 cents/lb in mid-February. However,producers pushed the hike to March 1. Accordingly, the assessmentthis week moved up to 48-49 cents/lb delivered rail car for generalpurpose while HIPS was pegged at 53-54 cents/lb delivered rail car.Buyers were still unhappy with the settlement as they complainedof weak demand that could not support the increase. Further, backin February when benzene contracts settled up 34 cents higher to135 cents/gal, PS producers could have easily pushed through a 2cent hike, one end-user commented. With a lower March CP of 129cents/gal, there was no justification, he added. In production, onePS supplier was reportedly experiencing mechanical issues inCalifornia, but one buyer said the issue was being resolved.Confirmation from the producer was unavailable by time of press.Meanwhile, the market was balanced with manufacturers matchingproduction with demand. In feeds, spot styrene was flat from lastweek at 35.50-36 cents/lb FOB USG.

PLATTS POLYMERSCAN VOLUME 32 / ISSUE 11 / MARCH 18, 2009

9 Copyright © 2009, The McGraw Hill Companies

Asia

Asian general purpose polystyrene prices spiked $60/mt on theCFR China benchmark this week in a bid to keep up withrecent sharp gains seen in feedstock styrene monomer prices.SM prices shot up last week as worries remained over short-term supplies. A steam cracker outage at China’s ShanghaiSecco caused the company to delay its March SM contractsupplies. Operations at its 500,0000 mt/year SM and 300,000mt/year polystyrene plant are low at the moment, a companysource said Wednesday. Secco is planning to restart its troubledsteam cracker around March 23, ending what would then be atwo-week unplanned outage due to mechanical problems,sources close to the company said Wednesday. The cost pushwas reflected in the PS retail market in Hong Kong, which waspricing general purpose polystyrene at $950-990/mt. Someproducers had raised offers this week, but most were still torevise their earlier offers. “We have stopped offeringGPPS/HIPS to the market since we were taken aback by thetrend in SM prices last week. At this point, we do not plant tosell below $1,000/mt,” a major US producer said Wednesday.Ex-Taiwan offers were left unrevised at $910-940/mt, buttraders expected these offers to be increased this week. Anotherproducer in Taiwan already raised offers to $980/mt CIF HK forend-March shipment. A Japanese producer said he lastconcluded GPPS March cargoes at $920/mt late last week,however, new offers would be placed at $960-980/mt CIF basisto Hong Kong market this week. Ex-Thailand offers to HongKong/China market were not seen this week. Thailand’s IRPChas restarted its SM, PS units, however, demand in the SEAsian market was not looking good, a company source said.The company had not made any new offers this week, and wastrying to meet some delayed PS commitments. In the domesticmarket, the situation remained one of “shortage,” sources said.Deal price of GPPS was at Yuan 7,800-8,500/mt (deliveredbasis) while that of high impact polystyrene was at Yuan8,500-9,500/mt (delivered basis). The outlook for the marketfor GPPS looked better in the short-term, with areas that sawdemand include extruded polystyrene and CD casing.However, concerns remained on the volatile behaviour of SMprices. SM prices showed signs of weakness this week, as short-term bullishness on supply was replaced by concerns ondownstream ability to absorb the cost.

Acrylonitrile Butadiene Styrene

Europe

Sentiment was mixed in the ABS market this week, with therealization that demand was still sluggish. Whereas at thebeginning of the month, producers were upbeat about ademand improvement, sources admitted that the much-hoped-for improvement in weather, that would enableconstruction projects to be undertaken, was still yet tomaterialize. Auto industry figures still showed that demandremained at low levels, and the housing market was stilldeemed to be dire. Last week, producers were hopeful to hitincreases as high as Eur50/mt, but others have since scaled

back this expectation in the wake of the continued poordemand scenario. One producer said that it could agreesome of its contracts at a rollover, but it was still hopeful ofachieving an increase of around Eur10-20/mt in othercontract business. “We will try to increase business, theproducer said. “Negotiations have been poor this year andmarket consumption not great,” the producer added.However, the same source was upbeat about the stimuluspackage offered in Germany at the start of February tosubsidize new car sales. He said that this was good news andwould help the ABS market. In the butadiene market,producers reported an unwillingness or need to sell anyvolumes due to their systems being in balance. “We arebalanced and we don’t have to or need to go to into themarket,” a producer said. However, prices remained underpressure due to persistent long supply in the crude C-4chain. Free delivered NWE prices were assessed at aroundEur345/mt, while FOB Rotterdam prices were assessed at$305/mt, as per Platts data March 13.

United States

January, February and March were successively stronger, oneproducer said Wednesday. “It’s a trend we want to see,” heexplained, but there were still questions about whether demandwill peak in April as it typically does. Spot prices this week weretalked at 67-72 cents/lb delivered railcar for injection grade, andthe assessment was steady Wednesday. In industry news, SABICInnovative Plastics has selected Ashland Distribution as anauthorized distributor to select customers in North America.The announcement included all SABIC resin products includingABS and polycarbonate, a spokeswoman for SABIC confirmed.The agreement would be finalized in the coming weeks andwas expected to take effect in mid-April. In feedstocks, balancemonth styrene was flat from last week at 35.50-36 cents/lb FOBUSG. March butadiene contracts settled at 25 cents/lb. Inacrylonitrile, domestic spot was at 33-34 cents/lb delivered.

Asia

Asian acrylonitrile-butadiene-styrene prices maintainedstrength this week gaining $10-20/mt on the CFR China/SEAsia benchmark. Gains were seen both due to rising feedstockcosts — especially SM prices surging to $880-885/mt at the endof last week, as well as strength in demand that was able toabsorb higher prices. Ex-Taiwan, ABS offers that were revisedthis week were at $1,220/mt CIF Hong Kong. Taiwan’s majorChi Mei Corp. did not announce a new offer (the old offerannounced last week was $1,210/mt CIF Hong Kong for Marchshipment) this week. A source said the company was waitingto determine if recent SM gains were sustainable. That lookedunlikely this week, as SM prices retreated, falling $20/mt to$865/mt CFR China in Wednesday’s trade. Short termbullishness last week on SM supply shortage was replaced byconcerns on downstream ability to absorb the cost. Ex-KoreaABS offers were few, with producers targeting ABS price of$1,250-1,260/mt CIF Hong Kong/China for April shipment.Dealers were already quoting higher prices in the Hong Kongmarket, with retail prices heard at $1,250-1,260/mt. Prices in

PLATTS POLYMERSCAN VOLUME 32 / ISSUE 11 / MARCH 18, 2009

10 Copyright © 2009, The McGraw Hill Companies

the domestic market in China shot up Yuan 500/mt more on theweek to Yuan 10,800-11,500/mt ex-works (for low- to high-endmaterial). The supply situation for March was still one of“shortage,” a producer in Ningbo said. ABS plants in China wereworking overtime to meet domestic requirements. “We hopethere are no plant outages, since we will not be able to meet theadditional requirements of the market,” a producer said. Demandfrom the home appliance sector was good, while demand fromthe electronics and automobile sector was lagging behind, sourcessaid. In market news, BASF’s SM unit in Ulsan, South Korea, is stilloffline, while its polystyrene and ABS units also at Ulsan wereoperating normally, estimated around 80-100%. Japan’s Technopolymer is currently running its ABS unit at 70% of its nameplatecapacity of 250,000 mt/year, a company source said Friday.

Polyethylene Terephthalate

Europe

In southern Europe an increase of Eur80/mt was reported on theMarch contract price, short of the Eur100/mt increase sought byproducers, but above the estimate pass through cost of higherfeedstock prices. There was still no clear settlement on theNorthwest European monoethylene glycol March contract. Theinitial settlement for MEG of Eur495/mt FD NWE, which isEur15/mt higher than the February CP of Eur480/mt. Theincrease in paraxylene and prices and MEG contract prices wouldequate to an increase of approximately Eur54/mt in PET prices. Ifboth second initial settlements for PX and MEG were to befollowed, at increases of Eur85/mt and Eur15/mt respectively andthus officially settled, this would equate to around a Eur54/mtincrease in PET terms. Spanish producers reported an increase ofEur80-85/mt on the March CPs. Demand in Spain was reportedto be relatively healthy in January and February, with oneproducer reporting demand for February as being as good as2008 levels. The better than expected demand in the early part ofthe year, combined with a reduction in production rates, helpedproducers to manage supply and demand and pass through anincrease. Other producers have reported similar increases in CPsfor March although one producer reported settling his Marchcontract at Eur890-900/mt. Looking forward, to negotiations forApril, the likelihood of another increase would be difficult toimplement according to one producer. “On the one hand wehave rising feedstock prices, but on the other side volumes forMarch were not good-no a lot of products was drawn down, so itwould be difficult to pass through another increase,” a source at aproducer said. Stock levels at some producers were also reportedto be high relatively high in anticipation of an upturn indemand relative to January and February. Other factors thatcould erode margins for PET producers are higher PTA prices. PTAwas looking increasingly tight due to the continuing problems atArtenius’ PTA production plant at Wilton, Northeast England,which is still shutdown. There were further reports that Arteniuscould extend the force majeure beyond March, athough acompany source declined to comment. On the positive side theshutdown of the PTA plant would mean there should be anincrease in PX availability. One trader estimated that there could

be an additional 20-30kt more PX hitting the spot market in amonth. In the spot PET market values were reported to havefallen to Eur850-870/mt FD NWE on the back of cheaper pricedimports from Asia. The availability of cheaper imports was alsoreported to be limiting any upside in contract negotiations.

US

PET contracts were talked up 2 cents/lb for March but were notyet completely settled. The increase would be a far cry fromthe initial 7 cents/lb nomination but would still allow for amargin increase for producers. Costs were down about 0.3cents/lb following the lower PX CP and rollover of MEGcontracts. A 2 cents/lb price hike would put prices just over 55cents/lb. Demand had not taken off as it typically does beforethe summer beverage season, sources said. There were no Aprilincreases issued yet but a producer said if March finishes up 2cents/lb, the other 5 cents/lb would be pushed to April toguard against any sudden jump in feedstock prices. MEGcontracts are already slated to drop about 3 cents/lb in Aprilbut spot PX values have held steady. The import market hadslowed considerably, traders said. “I haven’t even gotten anyoffers from Asia lately,” an importer said. Duty-free resin washeard sold at 53 cents/lb delivered to West Coast customers forApril arrival. From China and Korea, offers were at a similarlevel but deals were few. The import offer was under thedomestic price but many buyers did not want to take thechance on imports as domestic prices could easily decrease inApril or May to at, or under current import offers. “Demand isso poor, it would not surprise me to see April prices decreasedomestically,” a supplier said.

Asia

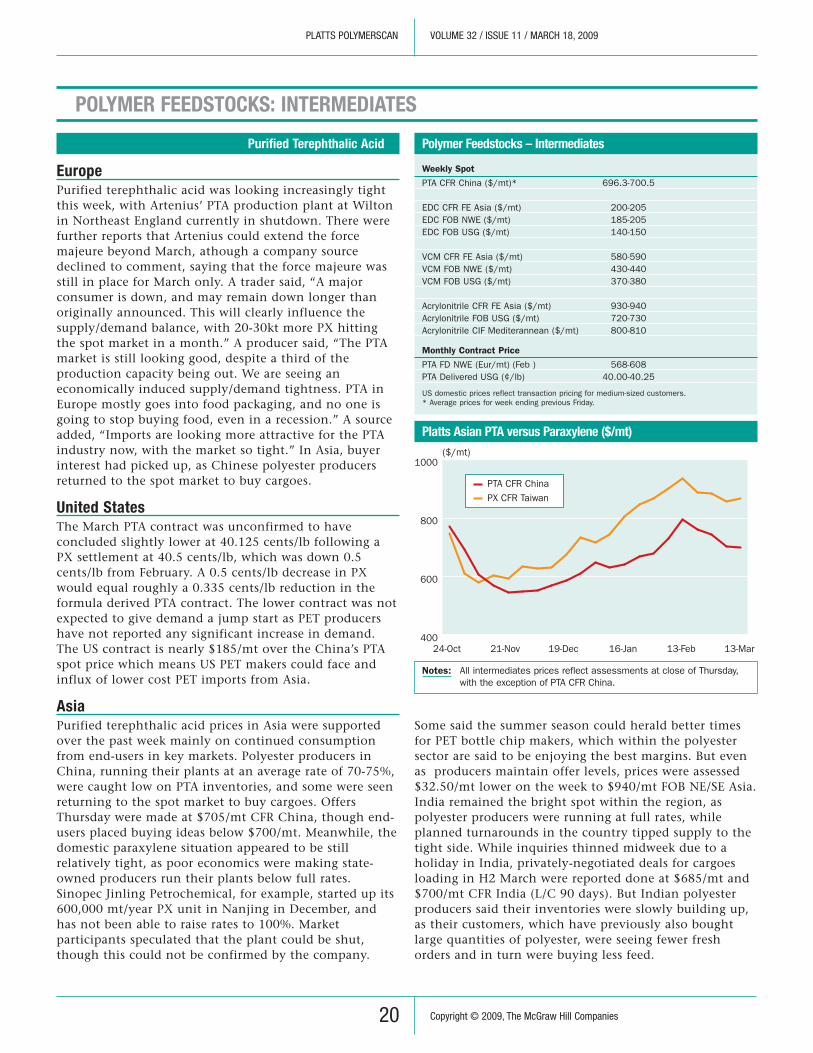

Bottle grade polyethylene terephthalate continued toweaken this week, despite feedstock purified terephthalicacid surging. PET was assessed $5 lower to $935/mt FOBNortheast Asia/Southeast Asia going into the second monthof its peak demand season in the northern hemisphere.Exports to Eastern Europe, the EU and Russia have fallen,and some PET manufacturers are seeing their orders beingslashed by half compared to the same time last year.“Demand in Eastern Europe and Russia is down sharplybecause their currencies have weakened against the USdollar,” an industry source said. “These countries also havedifficulties opening letters of credit.” Bids from LatinAmerica were said to be only around $860/mt FOB as theregion was still holding quite a lot of inventory. A tradersaid his exports to the EU for March were lower than forJanuary and February — a sign that the global economy isdeepening, despite what politicians are saying to the contrary.For the week, PTA rose $27.50 since Thursday to $730/mt CFRChina on Wednesday. Traders said the surge is because oftight supply as many producers are building inventory inpreparation for a shutdown by a few South Korean producersin April. Monoethylene glycol, however, has been relativelystable, at $442/mt CFR China due to excess supply. A PETproducer said: “There’s lots of MEG sitting around in Chinathat no one is buying. There’s just too much MEG.”

PLATTS POLYMERSCAN VOLUME 32 / ISSUE 11 / MARCH 18, 2009

11 Copyright © 2009, The McGraw Hill Companies

Platts Global Ethylene Prices ($/mt)

PLATTS POLYMERSCAN VOLUME 32 / ISSUE 11 / MARCH 18, 2009

12 Copyright © 2009, The McGraw Hill Companies

($/mt)

200

390

580

770

960

1150

18-Mar 23-Feb 29-Jan 02-Jan 04-Dec 11-Nov 16-Oct

CFR NE AsiaCIF NWE EthyleneSpot Ethylene FD USGC

US (¢/lb)

Spot Friday

FOB USG A/F* 22.00-22.50

Fiber Grade Monthly Contract Price (Mar ): 23.50-24.50 FOB USG

Asia ($/mt)

Spot Friday Weekly Average

CFR China 439-441 439.0-441.2CFR Taiwan 439-441 –CFR SE Asia 439-441 (1) –

Average Monthly Contract Price (Apr) – CFR Asia:613MEG CP Nomination (Mar) – CFR Asia: 560-560

(1) CFR SE Asia = CFR Indonesia.Note: *A/F denotes anti-freeze grade Asian ethylene glycolassessments are basis L/C 90 days.

Polymer Feedstocks – Butadiene

Europe

Spot Friday

FD NWE (Eur/mt) 343-347FOB Rdam ($/mt) 302-307

Quaterly Contract Price (Q1) 600-600 (Eur/mt)Ineos Olefins Monthly Contract Price Ex-Works:425-425 (Eur/mt)

US (¢/lb)

Spot Friday

CIF USG 15.00-17.00

Monthly Contract Price (Apr ) 25-25

Asia ($/mt)

Spot Friday

FOB Korea 495-505CFR Taiwan 525-535CFR SE Asia 560-570 (1)FOB Japan 475-485CFR China 530-540

(1) CFR SE Asia = CFR Indonesia. *A/F denotes anti-freeze grade.

Polymer Feedstocks – Ethylene Glycol Assessments (cont...)

Notes: All olefin prices reflect assessments at close of previous Friday.

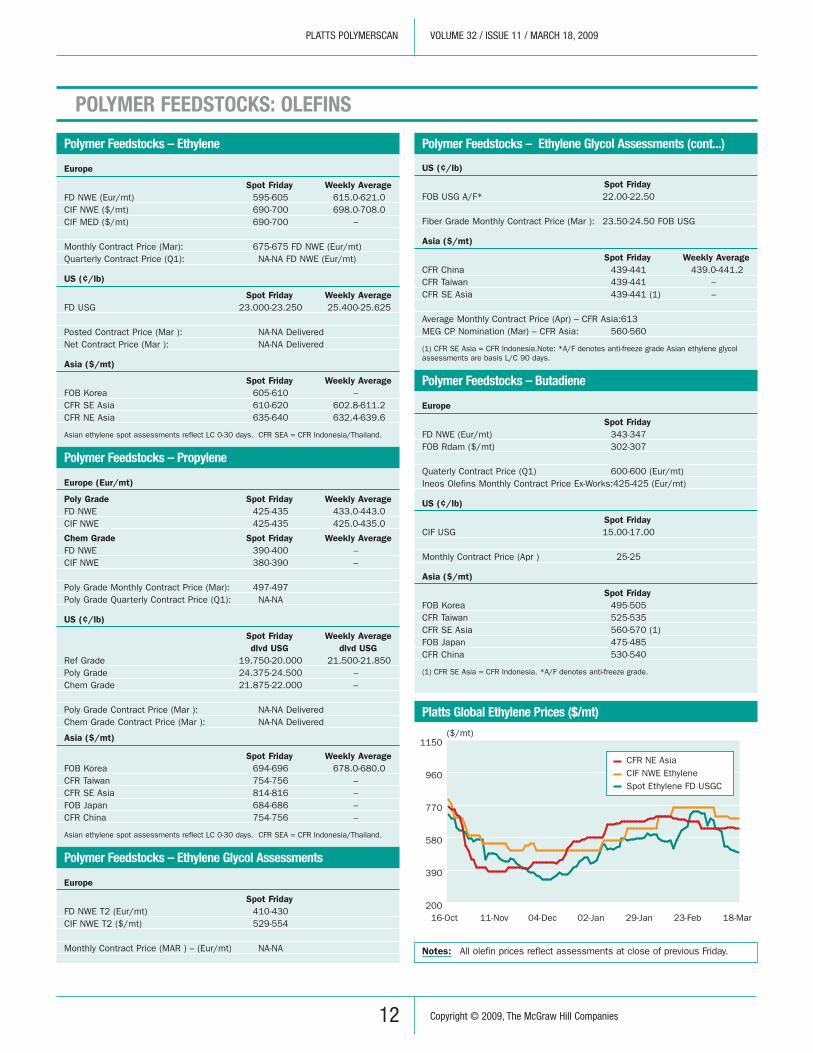

Polymer Feedstocks – Ethylene

Europe

Spot Friday Weekly Average

FD NWE (Eur/mt) 595-605 615.0-621.0CIF NWE ($/mt) 690-700 698.0-708.0CIF MED ($/mt) 690-700 –

Monthly Contract Price (Mar): 675-675 FD NWE (Eur/mt)Quarterly Contract Price (Q1): NA-NA FD NWE (Eur/mt)

US (¢/lb)

Spot Friday Weekly Average

FD USG 23.000-23.250 25.400-25.625

Posted Contract Price (Mar ): NA-NA DeliveredNet Contract Price (Mar ): NA-NA Delivered

Asia ($/mt)

Spot Friday Weekly Average

FOB Korea 605-610 –CFR SE Asia 610-620 602.8-611.2CFR NE Asia 635-640 632.4-639.6

Asian ethylene spot assessments reflect LC 0-30 days. CFR SEA = CFR Indonesia/Thailand.

Polymer Feedstocks – Propylene

Europe (Eur/mt)

Poly Grade Spot Friday Weekly Average

FD NWE 425-435 433.0-443.0CIF NWE 425-435 425.0-435.0

Chem Grade Spot Friday Weekly Average

FD NWE 390-400 –CIF NWE 380-390 –

Poly Grade Monthly Contract Price (Mar): 497-497Poly Grade Quarterly Contract Price (Q1): NA-NA

US (¢/lb)

Spot Friday Weekly Average

dlvd USG dlvd USG

Ref Grade 19.750-20.000 21.500-21.850Poly Grade 24.375-24.500 –Chem Grade 21.875-22.000 –

Poly Grade Contract Price (Mar ): NA-NA DeliveredChem Grade Contract Price (Mar ): NA-NA Delivered

Asia ($/mt)

Spot Friday Weekly Average

FOB Korea 694-696 678.0-680.0CFR Taiwan 754-756 –CFR SE Asia 814-816 –FOB Japan 684-686 –CFR China 754-756 –

Asian ethylene spot assessments reflect LC 0-30 days. CFR SEA = CFR Indonesia/Thailand.

Polymer Feedstocks – Ethylene Glycol Assessments

Europe

Spot Friday

FD NWE T2 (Eur/mt) 410-430CIF NWE T2 ($/mt) 529-554

Monthly Contract Price (MAR ) – (Eur/mt) NA-NA

POLYMER FEEDSTOCKS: OLEFINS

PLATTS POLYMERSCAN VOLUME 32 / ISSUE 11 / MARCH 18, 2009

13 Copyright © 2009, The McGraw Hill Companies

Ethylene

Europe

European ethylene spot values softened this week on improvedmaterial availability and more pronounced selling interest,market sources said. Buying interest was seen at Eur575-590/mtFD NWE, while selling interest was seen at Eur610/mt FD NWE,resulting in a spot assessment at Eur595-605/mt FD NWEFriday. No spot deals were reported this week, though moreliquidity on the spot market was seen possible as marginalderivative sales and marginal ethylene tons were looking lessdisconnected in the spot market. “Now I am consideringbuying as spot ethylene starts to approach more marginallycompetitive polyethylene sales,” an integrated marketparticipant said. While seeing more length emerging, ethyleneproducers said that it was “manageable” and was not requiringa reconsideration of ongoing operational rates at crackers yet.With moderate ethylene length incrementally emerging theconfidence in demand from some derivatives, such as PVC andglycols was somewhat eroding, some ethylene producers andconsumers said. “The PVC market is suffering now as theycould not pass the ethylene increase through,” an ethyleneproducer said. “There is no demand—it is a buyers’ market,” aPVC producer said. “While demand remains uncertain forsecond-half March and April, the signals are worryingly bearish.Ethylene is already showing signs of length and capacity isexpected to return to the market in April. Additionalpolyethylene on stream in second-quarter [non-NWE] will alsoadd price pressure to the chain,” an integrated player said,adding: “Discipline will be key for Europe and operating ratescould be effected.” With cracker co-products performance stilldisappointing, ethylene continued to be the most bankable,giving the highest returns, some producers said. Some addedthat despite some bearish tones emerging in the market, therewas no imminent credible downward pressure on the product.Northwest European polyethylene prices continued tostrengthen, as PE producers remained firm on their pricepolicies. With the current published LDPE price at Eur890-900/mt FD NWE or Eur811/mt FD NWE net, using a typicaldiscount of 8%, only Eur12/mt margin could be made as PEproducers needed to have Eur811/mt FD NWE net level as abreak even with March ethylene contract price. In HDPEblowmolding grade PE producers need Eur831/mt net as abreak even level, however at the current published gross valueof Eur870-880/mt or Eur796/mt net, they were in a red byEur35/mt. “Some of our customers expect better conditions inApril. However, regardless of what happens to ethylene we willstill be seeking to improve our margins...there is still nointegrated margin to talk about,” one PE producer said. “A lackof visibility does impact our customers’ purchasing patterns,who continue to buy only what they need. However, to thosewho expect lower prices in April, we say that for PE producersto engage in a price war and start competing for volume therehas to be a substantial wedge margin. And there is no suchmargin,” another PE producer said. LyondellBasell is set to shutits 320,000 mt/year LDPE plant at Aubette, from March 24 for aweek, a company source said. “We believe that it is important

to keep a close control on stock levels to support a further priceinitiative in April,” the source said.

United States

Spot ethylene values in the US shed roughly 5.5 cents/lb weekon week as oversupply concerns persisted. Early week saw awide bid/offer spread with buyers holding out in expectation oflower prices. March offers were heard Monday at 33 cents/lbMtB Wms against bids heard at 26 cents/lb MtB Wms. Aprilpricing remained backwardated to March with a tighter rangeas offers were heard at 28 cents/lb MtB Wms against bids at 25cents/lb MtB Wms. Participants failed to converge, however,and no trades were heard done. Tuesday sellers lowered offers acouple cents and March was heard offered at 31 cents/lb. Stillbuyers saw looming steam cracker restarts and weak derivativedemand and held bids near 26 cents/lb. March offers fellfurther mid-week and were heard at 27 cents/lb MtB Wms. Bidshowever fell as well and were seen at 21.25 cents/lb MtB Wms.March formula offers were heard at ethane x .422 plus 12.5cents/lb against bids at ethane x .422 plus 9 cents/lb. April wasslightly discounted to March with offers heard at 26 cents/lbagainst bids at 21 cents/lb at both MtB Wms and Equ. May wasflat to April while Q2 offers were at 25.75 with no bids heard.Q2 formula offers were heard early in the day at ethane x .422plus 10 cents/lb and later moved lower to plus 9.5 cents/lb.March offers opened Thursday at 21 cents/lb MtB pipe againstbids seen at 17 cents/lb MtB pipe. Meanwhile, ethylene buyerscontinued to hold out in hope of lower prices. March bids heldsteady at 21 cents/lb MtB Wms while March offers opened theday at 27 cents/lb MtB Wms. Participants began to convergelater in the day and March bids were heard at 23 cents/lbagainst offers at 25.50 cents/lb. Q2 was offered at 26.50 cents/lbat both MtB Wms and Equ. April formula bids were seen atethane x .422 plus 5.5 cents/lb against offers at ethane x .422plus 9.5 cents/lb. After close of assessment, March traded twiceat 23 cents/lb MtB Wms. Friday saw the bid offer spread tightenwith March heard bid at 22.50 cents/lb MtB Wms against offersat 24 cents/lb MtB Wms. April bids were seen at 21 cents/lbMtB Equ with no corresponding offers heard. Q2 formula offerswere seen at ethane x .422 + 9.25 cents/lb against bids seen atethane x .422 + 5.5 cents/lb. June ethylene was offered atethane x .422 plus 9.5 cents/lb at both MtB Wms and Equ. Noconfirmed trades were reported and the assessment closed at23-23.50 cts/lb. In production, CP Chem had shut down itsethylene unit at Sweeney, Texas following a malfunction at afurnace at the facility. A source familiar with operations saidthat the unit is up and running again. “We’re back in thepipeline. Just an unexpected outage for a day or two.”

Latin America

Ethylene prices in the Mexican domestic market werereported for March at $635/mt FOB contract which was adownward variance of 1.97% over last month. In localcurrency, the price was Pesos 9,245/mt FOB which reflects anincrease of 4.34%. In the spot market, ethylene Mexican domesticprices were at $777/mt FOB and remained stable from last month,while in local currency the price was Pesos 11,311/mt FOB which

was in increase of 5% over February and caused by a monetaryexchange fluctuation. PEMEX was preparing the next ethyleneexport for the 21st of March for a total of 4,500 metric tons,probably to Asia. “Our biggest ethylene client that wouldnormally buy 3,500 metric tons per month closed down, andnow we will begin trying to export this excess product everymonth,” said a source. PEMEX’s plants were reported to beworking at 80% capacity this month with the Cangrejera andMorelos plants producing 1,650 tons of ethylene daily, while thePajaritos plant was producing 380 tons per day. Ethylene contractprices in the Brazilian domestic market were reported with anincrease of 10% for March over last month’s prices. Prices wereheard at $760/mt FOB and in local currency at Reals 1,800/mtFOB. Ethylene prices in the Brazilian domestic market follows theinternational movements on monthly ethylene contract prices inEurope and the US with a month lag.

Asia

NEA: An unplanned naphtha-fed steam cracker outage at ShanghaiSeccoprompted buying of FOB Korea spot ethylene cargoes bytraders, which pushed the FOB Korea benchmark values up by$12.5/mt on the week. Secco's 900,000 mt/year sole cracker wasshut over last weekend due to a technical problem, triggeringsupply crunch concerns in the region for prompt end-Marchloading. Two spot ethylene cargoes were reported to have been soldbetween $600-610/mt FOB Korea for end-March loading. A bid fora spot cargo was heard at $600/mt FOB Korea for end-Marchloading, Korean producers countered at $620-630/mt FOB Korea,but such demand was for prompt loading only, with April-loadingbids widely lower at $570-580/mt FOB Korea. On the other hand,the week-on-week price increase on a CFR NEA basis was ratherlimited at $2.5/mt. End-users buying appetite for April delivery wasstill weak in the region, with bids widely reported between $620-630/mt CFR Taiwan/China for April delivery. An offer at $650/mtCFR Taiwan for April was widely rejected this week. End-users werestill reluctant to build their ethylene inventories this week,following a successful restart of Formosa's 600,000 mt/year No. 1cracker late Thursday. SEA: Prices basis CFR SE Asia rose $10/mt,reflecting tight supplies in the region. Regional supplies have beentight, while the influx from the Middle East was also limited. Thisweek, two cargoes (total quantity 4,500 mt) were offered from Iran,the first offer from the country in March. The two cargoes werereported to have been sold this week between $610-620/mt CFRThailand for end-March/H1-April delivery. End-users in Indonesia,however, did not chase the prices, with buying indications for H2-April delivery maintained at or below $600/mt CFR Indonesia.Indonesia's main spot ethylene buyers were vinyls producers, whowere not in hurry to buy spot cargoes as their plants have beenrunning below full capacity. Selling indications were reported at$630/mt CFR SE Asia for any-April delivery.

Ethylene Glycol

Europe

There was no finalization on the Northwest Europeanmonoethylene glycol March contract price this week despite

two initial settlements being done. A second initialsettlement was confirmed done at Eur495/mt FD NWEWednesday, a source from the involved producer said. Theprice is Eur35/mt lower than the first initial settlement ofEur530/mt done at the end of February, and Eur15/mthigher than the February CP of Eur480/mt. For a NWE MEGcontract to be officially settled, four independent partiesmust agree over the price. While buyers were eager to followthe second settlement, producers were unwilling to settle atsuch a reduced price, as one producer said: “I will notfollow. The price is too low and is not at all representative ofthe current market conditions.” The converse was true ofthe first settlemen, with buyers unwilling to settle at ahigher price. With the back end of March quicklyapproaching, buyers suggested if neither settlements wasfollowed by end-of next week a combined March/Aprilsettlement could arise. “While I would immediately followthe second settlement, I don’t believe it will be followed asthe other producers are very reluctant to settle at such alower price. What I see happening is a combined settlementfor March and April as there is such a big gap between bothinitial settlements,” a buyer said, with another calling such asettlement “a definite possibility”. However, a March CPsettlement was not completely lost, with some sellers furthersuggesting both parties meet midway and settle at Eur510-515/mt FD NWE. Direction from Asia pointed to adownward slope in CPs for April, with the first nominationsannounced $50/mt lower at $560/mt CFR Asia. Asia wascontinuing to play an important role in the European Marchcontract negotiations, with buyers pointing out Asia settlingat a rollover for March contracts and also the recent pricedrops in the Asian spot market. In further news, producerswere unfazed by Saudi Arabia’s Rabigh Refining andPetrochemical Co’s (PetroRabigh), recent announcement itwould sell all its MEG in Asia and Europe based on termcontracts. “It’s difficult to say exactly how it will affect theEuropean contract market but I think everyone, regardless ofwhether they are based in Europe or not, has to sell at themarket price,” a producer said. PetroRabigh, a joint venturebetween state-owned Saudi Aramco and Japan’s SumitomoChemical, was scheduled to make its first deliveries of MEGfrom its 600,000 mt/year plant at Rabigh at the end ofMarch. But due to the delay of the start up its ethane-basedsteam cracker, the start up of its MEG plant has been pushedback to the first week of April. Meanwhile, on the spotmarket prices truck prices remained relatively stable thisweek with the higher end edging up just Eur5/mt. Whiledeals were reported done as high as Eur450-470/mt FD NWEand Antwerp for March delivery, trades were again alsoreported at lower levels of Eur410/mt FD NWE, Marchdelivery. In bulk, the market was subdued this week with noreported bulk business done. However, sources suggestedprices were likely to fall next week as cheaper Iranianmaterial was scheduled to hit Europe. “While the market hasbeen very, very quiet this week and over the last three weeksin fact, let me just say this is about to change as there willbe some large import volumes coming into the market next

PLATTS POLYMERSCAN VOLUME 32 / ISSUE 11 / MARCH 18, 2009

14 Copyright © 2009, The McGraw Hill Companies

week,” a source said. According to Platts data, the last timeIranian material was sold in Europe—at the beginning ofJanuary—bulk spot prices fell by over $65/mt.

United States