Embed Size (px)

Citation preview

Political Visit

Weiwei Cai1 Wenxuan Hou

2

University of Edinburgh Business School, University of Edinburgh, Edinburgh, EH8

9JS, UK

Abstract:

Chinese State leaders (i.e. Politburo Standing Committee Members) often visit firms

in their domestic inspection tours. We argue that political leaders can confer their

reputation and prestige upon visited firms and bring about certain supports from the

government. We document positive market reactions, especially for the president’s

visit. The market reaction is more positive for firms without political connection, far

away from Beijing, and located in places with good institution. Finally, based on the

matched sample after propensity scoring matching, we find that the visit is associated

with higher operating performances, higher effective tax rate, and these firms recruit

more employees and donate less in the future. The results are stronger for the Jingping

Xi Administration.

Keywords: Political visit, political connection, firm performance

1 Contact author: Weiwei Cai Email: [email protected]

2 Wenxuan Hou email: [email protected]

1. Introduction:

Governments can participate in financial market through various methods such as

establishing regulations and policies (e.g. Krueger, 1999; Johnson, 1960), providing

subsidies or directly owning the firms (La Porta, Lopez-de-silanes and Shleifer, 2002).

Political connection is one of the most frequently studied approaches through which

government can assert influences on firms (eg. Faccio, 2006; Claessens, Feijen and

Laeven, 2008). Some recent literature like the paper of Cai, Hou and Rees (2010)

point out that political endorsement (praising firms through state-controlled news

program) is also a method of government to affect the market. However, existing

literature ignore a very common strategy government use to participate in market –

political visit.

To fill this gap, this paper focuses on political visit, a new way that government

uses to influence the financial market. According to Bernhardt (1993), political visit is

defined as “a political device in which a political leader carries out all the functions

and symbolic representations of governing by periodically or constantly traveling

throughout the areas of his domination.” Under financial context, political visit in this

paper is defined as a political device in which a high-level political leader of a country

carries out all the functions and symbolic representations of governing by periodically

visiting firms in their own countries. For instance, in UK, the president David

Cameron visited London Taxi Company on May 2015, which leaded to a so-called

‘hugely exciting day’ for Coventry. For another example, President Obama visited

Apple Pay on 13th

Feb 2015, which is described as a “big win for Apple Pay” by the

CEO of Crone Consulting LLC since political visit brings about huge promotional

value. Political visit is increasing and becomes more important (Cohen & Powell,

2005; Cook, 2002). Political visit is an important opportunity for government to make

key instructions to the market. For example, Obama visited Detroit Auto Show on

January 2016 and made a speech to express government’s idea on the auto industry.

Literature on political connection and helping hand of government imply that

establishing a relationship with government can benefit firms, suggesting the positive

effects of political visit. For example, having intimate relationship with government

can help firms achieve bank loans (Khwaja and Mian, 2005) and outperform other

firms by 160% higher market-to-book ratio (Bunkanwanicha and Wiwattanakantang,

2009). Moreover, the theory of private benefits of control provides theoretical

background for the positive emotional effects of political visit. Based on Yermack

(2010), private benefits of control means people can utilize their position and power

to get not only economic benefits, but also intangible benefits such as prestige and

visibility for themselves. For instance, it is the public visibility and prestige Michelle

Obama gets from her political position as First Lady that makes her influential in

fashion industry (Yermack, 2010). Similarly, in terms of political visit, the visiting

leaders can confer their prestige and visibility they obtained as political leaders upon

the visited firms, thus leading to market reactions.

However, the resource dependence theory and the literature on political

connection also indicate the burden of political visit. According to the resource

dependence theory, firms face high probability to be controlled by the entities with

greater power (Nicholson et al., 2004; Rao et al., 2007). After the firm-government

relationship is established through political visit, government, as the entity with great

power, can control or interfere with the firm in order to reach the political goals. For

instance, government can force firms to recruit more employees. Furthermore, based

on literature on political connection, officers may pursue personal objectives at the

expense of connected firms’ value (Shleifer and Vishny, 1994, 2002). As a result, the

firm-government relationship brought by political visit is not necessarily a good thing

and can cause huge burden for the firms and lead to inferior performance and negative

market reactions.

We hand collect the data of political visit in China from Leader’s Activity

Database from 1st Jan. 2009 to 31st July 2016, covering two governments: the one led

by President Hu (1st Jan.2009 -- 1st March 2013) and the other one led by President

Xi (1st March 2013-- 31st July 2016). The data is basically balanced since there are

almost four years for each government. The results indicate that political visit can lead

to positive market reactions over different time windows, and show that the market

reactions of visit by Xi administration are more significant than those of visit by Hu

administration. When we divide the whole sample according to leaders’ different

rankings of political power, we find that the market reactions of visit by president are

the most significant.

We further investigate the firm and institution heterogeneity. We test whether

market reacts differentially across different types of firms according to the existence

of political connection, firms’ dependence on external financing, geographic

characteristics, and the institutional development level. The results show that political

visit can trigger more significant market reactions for firms without political

connection. Although we assume that the market reactions for the visited firms who

heavily rely on external financing would be larger since political leaders can confer

their credibility and prestige upon these firms and thus help them to solve the

financing problem, we find no difference in market reactions. The third firm trait to

influence the market reactions of political visit is geographic characteristics.

According to Kim, Pantzalis and Park (2012), geographic proximity implies policy

risks and accessibility of resources. We measure the proximity to political power by

using the distances of firms’ headquarters to the capital of China—Beijing. We find

that political visit to firms located far away from Beijing can lead to more significant

market reactions since these firms rarely achieve support from central government.

We also use municipality and autonomous areas to proxy the development levels of

provinces and test whether leaders will take the development levels into account when

they choose places to visit, but we didn’t find supporting evidences for this.

Furthermore, we split samples based on the development of legal institutions,

marketization and the development of banking system. The results demonstrate that

better institutions and marketization can push up the market reactions since good

institutional development can magnify governments’ positive role.

Then we examine what kinds of firms are more likely to be visited. We test a

series of connection-related factors and non-connection-related factors. A lot of

reasons can lead to political visit: it’s possible that leaders prefer to visit connected

firms; it’s also possible that companies bribe officials in return for the visit, especially

in a sole-ruling party like China with heavy corruption; and geographic characteristics

can also influence the political connection, thus influencing the probability of

achieving political visit. All of above possible reasons are connection-related, and the

results show that political connection can increase the possibility to be visited while

no evidence supports that bribery is useful to win the visit. And results reveal that

leaders prefer to visit firms located far away from Beijing and less developed. One

possible reason is that leaders can help those firms to get more social attentions and

improve the development after visiting. Non-connection-related causes include firm

size, age, leverage, and past performance. We find that larger size, younger age, less

leverage and better past performance can increase the probability of being visited.

Finally, we use the significant determining factors mentioned above to match

visited firms with non-visited firms by applying propensity scoring matching and then

test the effects of political visit on firm performance. Results reveal that visit by Xi

administration can help firms to improve future firm performance, no matter which

performance measure is used. In contrast, visit by Hu administration has no impact on

firm performance. We then examine the channel of value creation by testing the

impacts of visit on government support, social burden and firm policies. Results

indicate that visit by Hu administration has no impact on these channels. However,

after being visited by Xi administration, the effective tax rate of firms will increase,

and firms will recruit more employees while donate less. Furthermore, the earnings

management will decrease due to the increased social attention after visiting, and the

shares and salaries of managers will increase as bonus of winning political visit.

This paper contributes to the literature in a number of ways. First, this paper is the

first one to examine the role of political visit in financial market. Existing literature

about political visit or presidential travel is only restricted to politics studies and most

of the studies only focus on the impacts of political visit on leaders themselves. For

example, extant literatures point out that political visit can improve presidents’

popularity (Ostrom and Simon, 1985; Brace and Hinckley, 1992), make power more

tangible (Herbst, 2000; Mitchell, 1991) and get allegiance of local elites (Schatzberg,

2001). This paper is the first one to consider political visit from a different angle by

focusing on the impacts on financial market.

Second, this study complements the literature on political economy. Political

economy literature point out that government can participate in market through

different approaches such as issuing policies (Krueger, 1974), establishing political

connections (e.g. Faccio Masulis and McConnell, 2006; You and Du, 2012), directly

owing the firms (La Porta, Lopez-de-silanes and Shleifer, 2002), and providing

political endorsements (Cai, Hou and Rees, 2017). This paper explores a new

approach through which government can participate in the market– political visit.

Different from political connection, both connected and non-connected firms can be

the target of political visit. Additionally, the political leaders who visit the firms are

usually in a position which is much higher than the government officials firms

generally connect with. For example, firms are usually visited by president while

firms rarely have connections with such high level political leaders. And different

from political endorsement, political visit will cause time and money costs for the

leader and his whole team, showing the importance the leaders attach to these firms.

Third, our paper is related to the literature on the certification effects. This stream

of literature point out that reputation can be transferred and bring the firms benefits.

For instance, affiliation with prestigious underwriters (Pollock, Chen and Jackson et

al., 2010; Ramirez, 1995; Carter, Dark and Singh, 1998), venture capitals (Milanov

and Shepherd, 2013), auditors (Beatty, 1989) and authoritative third parties (Doh,

Howton, and Howton S W, et al, 2010; Corbett, Montes-Sancho and Kirsch, 2005;

Bonardo, Paleari and Vismara, 2011) can increase affiliated firms’ reputation and trust.

Affiliating with venture capitals can make firms more credible, lower information

asymmetry and increase the net proceeds of IPO (Megginson and Weiss, 1991;

Pollock et al., 2010; Gulati and Higgins, 2003).While firms have some degree of

freedom to choose which underwriter or venture capital to cooperate with, firms

haven’t the initiative to let high-level political leaders to visit the firm. Therefore,

compared with the certification from financial organizations, achieving visit from

political leaders is rarer and more valuable.

The remaining paper is organized as follows. Section two reviews literature and

hypotheses are developed in section three. Section four provides basic institutional

background and describes the sample. Results about the impacts of political visit on

market reactions and firms performances are detailed in section five and six

respectively. Section seven analyzes the channels of value creation. Finally,

conclusion is articulated in section eight in the paper.

2. Literature review

Government participates in market in both developed and developing countries.

Invisible hand, helping hand and grabbing hand models suggested by Frye and

Shleifer (1996) imply that governments of different countries play an important role

in markets but with different strategies. Invisible-hand governments are

well-organized governments with low corruption, relatively self-restraint and more

benevolent to private sectors, which is more prevalent in Eastern Europe (Sachs,

1994). Helping hand governments, commonly discussed in developing countries like

China, are closely involved in market activities, partial to connected firms but the

corruptions within these countries are still limited (Walder, 1995). In contrast, the

regulatory environment in countries with grabbing hand governments is predatory and

heavily corrupt. The power of government is stronger above law and is used for

rent-seeking (Frye and Shleifer, 1996).

Governments can participate in financial market through various methods such as

establishing regulations and policies, providing subsidies or directly owning the firms.

For example, the very pioneering work of Krueger (1999) in political economy

demonstrates governments’ policies like import restrictions can harm economic

development, showing that establishing policies is a regular approach of government

to exert impacts on market. Abundant researchers like Ramey and Ramey’s (1994),

Bhagwati (1969) and Johnson (1960) also certify that government policies such as

policies on government spending, tariffs and quotas can influence economic growth.

Directly owing firms is another approach for government to participate in market (La

Porta, Lopez-de-silanes and Shleifer, 2002). Comparing with other approaches, direct

government ownership allows governments to have overwhelming power over firms.

Government can also assert impacts on market through political connection.

According to political connection literature, there are a lot of ways to establish

connection, which can be classified as two forms: individual level or firm level.

Individual level connections are consisted of two broad categories: political

experience and political identity. Political experience is defined as top executives’ and

board members’ former occupation in parliaments, government branch, state-owned

banks, and other regulated industries (Hasan et al., 2014; You and Du, 2012; Faccio

Masulis and McConnell, 2006). The executives and board members are considered as

possessing political identity if they are party members (Li et al., 2008), deputies to

National People’s Congress or National Committee (You and Du, 2012), mayors or

deputy mayors (Calomiris Fisman and Wang, 2010), or officers of government or

military (Fan et al., 2007). Additionally, other relatively indirect indicators are also

used to identify the individual level government-firm relationship. For instance, if the

top managers have relatives with the same last name or come from the same family

serving as government officers, Faccio, Masulis and McConnell (2006) and Amore &

Bennedsen (2013) deem such managers as politically connected. Similarly, Siegel

(2007) identifies political connection if the top managers graduated from the same

high school or was born in the same region as government officers. Other indirect

indicators include governmental awards such as the award of “Model worker” (You

and Du, 2012). As to company level connection, literature identify political

connections by exploring whether the firms pay huge campaign contributions

(Claessens, Feijen and Laeven, 2008), whether the headquarters are in the birthplace

of the government officers, or whether the firm is state-owned (Faccio et al., 2006).

Besides political connection, political endorsement is another way through which

government participates in market. Cai, Hou and Rees (2017) define political

endorsement if the state-controlled news program delicate a slot to praise a firm. Such

state-controlled news program is a mouthpiece of government, so the praising from

such program can represent government’s idea. By disseminating their support to

specific firms through state-controlled news program, government can trigger market

reactions, thus participating in and influencing the market.

This paper investigates a new approach government use to participate in the

market activities --- political visit, which is largely ignored by the previous literature.

Political visit, in this paper, is defined as a political device in which a high-level

political leader of a country carries out all the functions and symbolic representations

of governing by periodically visiting firms in their own countries. For example, on

13th

Feb 2015, President Obama visited Apple Pay in Silicon Valley, which is

regarded as a big win for Apply by a lot of consulting companies. Richard Crone,

chief executive officer of Crone Consulting LLC, said. “It makes it look like the

federal government is supporting Apple Pay.” According to Brace and Hinckley

(1992), Cohen & Powell (2005) and Cook (2002), political visiting is becoming

increasingly important. Political visit has multiple objectives, within which making

key instructions to the market and making governments’ will manifest in person are

the most important functions.

3. Hypothesis development

Multiple streams of literature imply the governments’ positive role in market

development, suggesting the positive effects of political visit. Firstly, abundant

literature of helping hand of government and political connection embrace the view

that political connection is a contributing factor of performance improvement and

value enhancement. With an overwhelming advantage compared with most of the

unconnected peers in terms of intimate relationship with government, connected firms

can obtain more favorable treats. As Faccio, Masulis and McConnell (2006) suggested,

once firms belong to the cronies or families of current ruling political parties or

leaders, these connected firms can get preferential resources such as bailouts. Other

preferential treats such as tax reduction (Li, Meng and Wang, 2008; Faccio, 2010;

Bertrand, 2006), tariffs on counterparts (Goldman, Rocholl and So, 2009) and easier

access to loans (Khwaja and Mian, 2005) are common among connected firms. Under

the supporting hand of government, connected firms demonstrate higher value and

generate higher long-term returns for investors (Luo and Liu, 2009). Investors’

positive views on the promising future performances of connected firm push up the

market value. For instance, Bunkanwanicha and Wiwattanakantang (2009) point out

that the market-to-book ratio increase 242.16% after previously non-connected firms

establishing ties with government. The politically connected firms also outperform the

control groups by 160% higher market-to-book ratio. The significant positive

correlation between political connections and superior firm performances are also

testified by researchers like Hillman (2005), Calomiris Fisman, and Wang (2010), and

Siegel (2007).

Secondly, the theory about private benefits of control provides theoretical

background for the positive emotional effects of political visit. Private benefits of

control means people can get economic gains for themselves by taking advantage of

their position and power. For example, by analyzing NYSE or Amex firms, Barclay

and Holderness (1989) claim that block holders can trade at a premium to the

exchange price and get private benefits by taking advantage of their voting power.

According to Yermack (2010), not merely economic benefits, but also intangible

benefits such as reputation, prestige and public visibility can be obtained through

people’s public position. For instance, the clothing choices of the First Lady, Michelle

Obama, can create significant value for designers and retailers. It is the public

visibility and prestige she obtained from her political position as First Lady that bring

her the power to influence the market. In terms of the political visit, the visiting

political leaders such as presidents can confer their publicity and prestige obtained

from their position upon the visited firms, thus leading to market reactions, which

complies with the theory about private benefits of control.

Thirdly, literature related to presidency also provides supporting evidences for the

positive effects of political visit. Based on McHugo’s experiment (1985), political

leader’s expressive displays can lead to emotional reactions and change public

opinion. And these emotional reactions, in turn, affects vote choice and people’s

attitudes toward the leaders. (Kinder and Abelson, 1981; Abelson et al., 1982). As

mentioned previously, political leaders usually deliver a speech in the visited firm in

order to encourage firms and make key instructions to the market. And these speeches

will be published in the local and central newspapers within next several days to

disseminate government’s ideas. As a result, political visit and leaders’ speech during

the visit can lead to people’s emotional reactions, thus causing market reactions.

Ha: Political visit leads to positive market reactions and favorable future firm

performances.

Resource dependence theory, however, highlights the burden of political visit by

claiming that during the interaction with other entities to obtain resources, firms are

highly likely to be dominated by the entities that control the resources (Nicholson et

al., 2004; Rao et al., 2007), suffer from high costs (Hsu, 2004), experience conflicting

goals with their partners (Froelich, 1999) and face external pressures (Oliver, 1991;

Rowley, 1997). Political visit forms a firm-government relationship, within which

government is the entity with greater power. As a result, government can use their

power to require firms do something harmful to the firm in return for the political visit.

For instance, firms may be required to shoulder more social responsibilities.

Furthermore, literature on political connection also implies that the

firm-government relationship formed through political visit sometimes constrains firm

operations and cause higher costs. First, inefficiency can be caused by the

unreasonable diversion of firm resources and the surrender of autonomy (Shleifer and

Vishny, 2002). For example, under the informal political regulations, connected firms

are forced to invest in government infrastructure projects by using their capital raised

from IPO, and are compelled to pay dividends to release the financial problems of

government (Lawrence, 1999). Second, political officers usually pursue personal

objectives at the expense of connected firms’ value (Shleifer and Vishny, 1994, 2002).

For instance, in order to win the campaign, political officers usually force connected

firms to misallocate capital on campaign contributions, generating economic costs of

higher than 0.2% of GDP (Claessens Feijen and Laeven, 2008). As a result, politically

connected firms are characterized by higher campaign contributions and lower

returns.

Third, connected firms are hampered from adapting to the new competitive

environment due to the heavy “liability to localness” (Uzzi, 1997; Perez-Batres and

Eden, 2008). For example, after foreign banks were allowed by government to enter

the Mexican market, the domestic connected firms suffered from their liability to

government and lost their competitiveness to foreign counterparts (Perez-Batres and

Eden, 2008). Fourth, the political relationship is quite unstable which heavily depend

on political fortunes and are featured as short-term. Consequently, the short-term

relationship encourages opportunistic behaviors such as earnings management (Chen,

Lee and Li, 2008). Therefore, the firm-government relationship formed through

political visit may bring about burden for the firm and lead to negative market

reactions.

Hb: Political visit leads to negative market reactions and harm future firm

performances.

4. Background and Sample

4.1 Background of Political Visit and Politburo Standing Committee

Political visit is becoming increasingly important. According to Brace and Hinckley

(1992) and Hart (1987), presidential travel is an increasingly vital aspect of the public

presidency, with the public presidency being one of the signature developments of

modern presidential leadership. Researchers like Cohen & Powell (2005) and Cook

(2002) also certify that political visiting is increasing.

Political visit has multiple functions. Improving leaders’ popularity (Brace and

Hinckley, 1992) and making power more tangible (Mitchell, 1991) are functions

commonly discussed in the literature of politics. Under finance, one of the most

important objectives of political visit is to make governments’ will manifest in person,

and political visit is an important opportunity for government to make key instructions

to the market. For example, in USA, on 20th

Jan 2016, President Obama visited

Detroit Auto Show to showcase the auto companies his administration helped save.

By delivering the following speech: “……see the progress firsthand that the

automakers have achieved, this attributes to the plan to retool and restructure the

auto industry. I believe that every American should be proud of what our most iconic

industry has done……”, president Obama expressed government’s idea on the auto

industry, demonstrating that political visit is a good opportunity for government to

express the ideas and influence the market. As a result, political visit can be regarded

as a new approach through which government can participate in the market while it

has not been investigated before.

Besides developed countries like U.S. mentioned above, political visit is in

particular a useful device government could use to affect market in countries with

relatively powerful government such as developing countries. For example, on 7th

December 2012, Chinese president Hu visited Guizhou Changzheng Electric CO.,

Ltd., and CLP Zhenhua information Co., Ltd. During the visit, besides inspecting

product lines and management, president Hu expressed government’s will by

delivering a speech to these firms: “……The value of firms lies in innovation. I hope

you can emancipate the mind, reform with keen determination, forge ahead, and

promote the continuous development of enterprises.……” Since Chinese government

is promoting the transform from “made in China” to “created in China”, one key point

of these speech is to encourage firms to improve innovation, showing that political

leaders deem visit as an opportunity to influence the firms and market.

In China, although there is no literature or material clarifies the mechanism of

domestic political visit, we can refer to the mechanism of international political visit

to gain an insight into how it works. During international political visit, some

entrepreneurs or CEOs will be invited to form a delegation to accompany the

president. According to Jifei Wan, the president of China International Chamber of

Commerce, the choice of accompanying entrepreneurs varies from place to place and

time to time, depending on different destinations and different focusing areas of

economic and trade cooperation.

Different chambers of commerce or private trade groups are responsible for

choosing entrepreneurs to form delegation to accompany president during

international political visit according to several principals: First, according to

“Oriental Outlook Weekly”, an official newspaper, the delegation must be formed by

representative entrepreneurs. For example, if the president needs to have a talk with

the leader of the host country about anti-dumping, the CEOs of representative

enterprises in the field of anti-dumping will have a high probability of follow-up.

Second, Xiao Qiang, president of the China Small and Medium Enterprises Research

Institute, said that the decision of choosing firms depends on what the visited

countries need, and what is the purpose of our government during the visit.

Two key words mentioned in international visit can be applied to domestic

political visit: representative and purpose. As to domestic visit, local government is

responsible for recommending representative firms to be visited by the leader. It can

be assumed that big firms are more likely to be visited and this will be tested in the

later section of this paper. Since political visit is an opportunity for government to

make instructions to market, the types of visited firms will change according to the

different purposes of government. For instance, during the National People's Congress

& Chinese People's Political Consultative Conference, Premier Keqiang Li proposed

the concept of “Internet+”, demonstrating that internet is now put on the top agenda to

reach the national strategic level. Correspondingly, more and more entrepreneurs from

the field of internet are chosen as the delegation to accompany president during

international political visit. It can be assumed that internet firms are also more likely

to be chosen as the target of domestic political visit.

Political visits in China are usually executed by high-level political leaders like

members of Politburo Standing Committee of Communist Party (PSC). PSC is a

committee consisting of the top leadership of the Communist Party of China with an

officially mandated purpose to conduct policy discussions and make decisions on the

most important political issues. PSC is composed of five to nine members, and

currently Xi administration has seven members. This paper focuses on the political

visits of PSC members, who are prestige enough to transfer their reputation and

popularity to the visited firms.

4.2 Sample and Data

The data on political visit is hand collected from a database called Leader’s Activity

Database. This database integrates reports from different newspapers about political

visits of various leaders. On every report, it would clearly write the starting date and

the reporting date of the visit. In the event study, we use the starting date of the visit

rather than the reporting date as the event day in order to alleviate the information

effects brought by news release. The data is from 1st Jan. 2009 to 31st July 2016,

covering two governments: the one led by President Hu (1st Jan.2009 -- 1st March

2013) and the other one led by President Xi (1st March 2013-- 31st July 2016). The

data is basically balanced since there are almost four years for each government.

The reports in the Leader’s Activity Database reveal information about who are

the visiting leaders, where the leaders visit and what the leaders do. So we record the

places of visit (Province), whether the leader is President (President) and which

Section is the report written on (Section). We also record leaders’ names and rank

them according to their political power. Other financial data such as return on assets

and firm size can be obtained from China Securities Market and Accounting Research

Database (CSMAR), which is developed according to international standards and

focuses on Chinese market. The definitions of variables are shown in table 1.

[Insert table 1 about here]

We collected 482 political visits to firms in total from 1st Jan. 2009 to 31st July

2016. Figure 1 demonstrates the visit frequency in each month. Based on Figure 1,

leaders visit firms more frequently during the midyear, especially in June, July and

August. And it is obvious that the number of political visits decreased dramatically

after 2013 when President Xi assumed office.

[Insert Figure 1 about here]

Table 2 demonstrates the distribution of political visit from 1st March 2009 to

31st July 2016. Panel A is the distribution of provinces. It shows that firms located in

the capital are more likely to be visited by leaders (6.85%). And firms located in

northern areas such as Liaoning (7.88%), Neimenggu (6.02%) and Shandong (7.47%)

also have higher probability of being visited. One possible reason is that northern

areas are relatively less developed, so government is more inclined to visit those

places to stimulate local economic development. Panel B shows the distribution of

leaders. Compared with Xi administration, Hu administration visited firms more

frequently, with 82 and 400 visits respectively. In terms of Xi administration, 19 out

of 82 visits (23.17%) are done by President Xi, while only 28 out of 400 visits (7%)

are done by President Hu during Hu’s administration, showing that the President of Xi

administration visit firms more frequently.

Panel C is the distribution of newspaper sections. Leader’s Activity Database

integrates information about political visit from two resources: People’s Daily and

local newspapers. People’s Daily is an official newspaper of Communist Party and it

is the biggest newspaper group in China. People’s Daily has 24 sections in total,

within which sections 1 to 6 are specialized for the most important news. Based on

Panel C, most of the political visits (81.95%) are reported in the first section, meaning

that political visit is deemed as the most important news. As the official newspaper of

Communist Party, People’s Daily is required to be the mouthpiece of government. By

placing political visits in the first section of the newspaper, People’s Daily can help

government to highlight the instructions leaders made during the visits. Besides

People’s Daily, some political visits may be reported in local newspapers but the

percentage is only 3.32%.

[Insert table 2 about here]

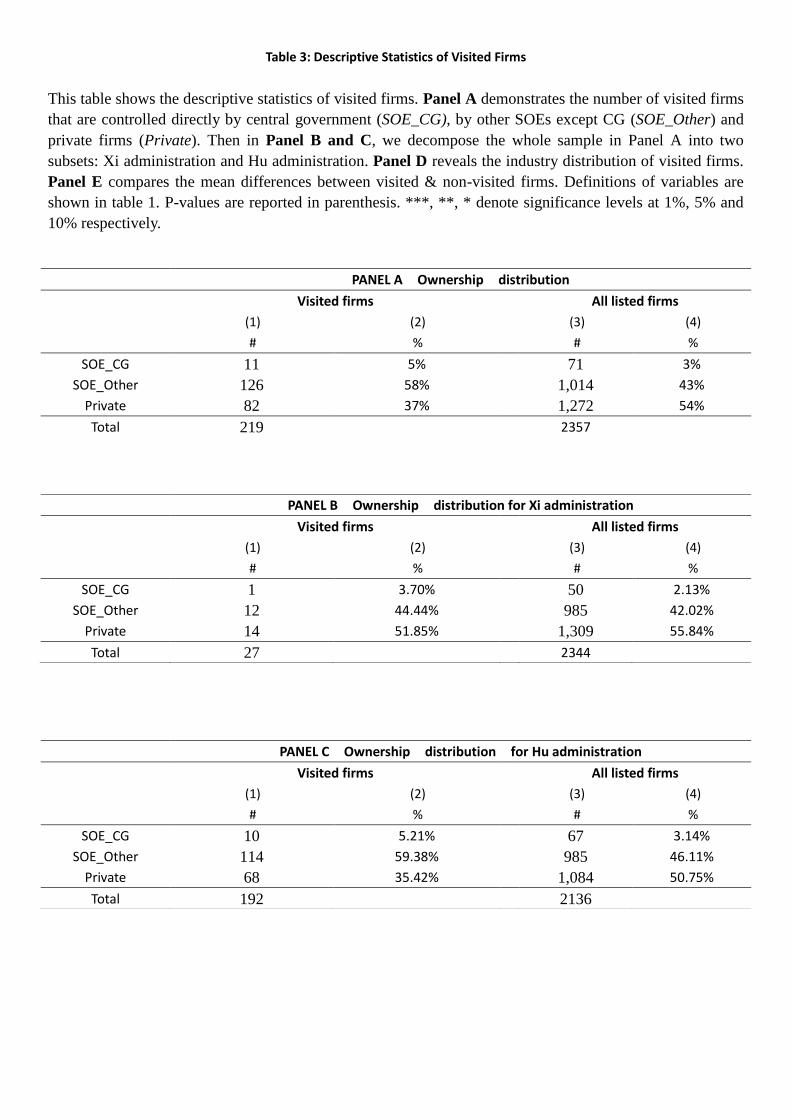

Table 3 shows the descriptive statistics of visited firms. Since firms can be visited

for multiple times, our sample incorporates 482 visits, which incorporate 219 firms.

Panel A compares the distribution of the number of visited firms that are controlled

directly by central government (SOE_CG), by other SOEs except CG (SOE_Other)

and private firms (Private). Compare columns (2) and (4), 5% of visited firms are

directly controlled by central government while only 3% of all listed firms are

controlled by central government. Similarly, the percentage of other SOEs in visited

firms is also higher than that in all listed firms (58% and 43% respectively), meaning

that government is more likely to visit SOEs. Then in Panel B and C, we decompose

the whole sample in Panel A into two subsets: Xi administration and Hu

administration. The results show that both Xi and Hu administrations are more likely

to visit SOEs. However, compared with Hu administration, Xi administration visits

private firms more frequently since the percentage of visits to SOEs versus to private

firms are 64.58% to 35.42% for Hu administration and 48.15% to 51.85% for Xi

administration.

Panel D reveals the industry distribution of visited firms. Some industries such as

energy and information technology have higher probability to be visited. Panel E

compares the mean differences between visited & non-visited firms, showing that

firms with political connection have higher probability to be the target of visiting. For

example, firms controlled by central government or other SOEs and firms with higher

state shares or with directors with political background are more likely to be visited.

Geography also has a say in determining which firms to visit. Based on Panel E, firms

in municipalities or in autonomous areas have higher probability to be visited. In

addition, visited firms also show the following characteristics: larger size, younger

age, less leverage and better past performance.

[Insert table 3 about here]

5. Political Visit and Market Reaction

5.1 Market reactions

To examine the value of political visit, we first use event study to examine cumulative

abnormal return (CAR). Abnormal return is calculated as the excess return over

market return. The reports about political visit from Leader’s Activity Database

clearly write the starting date and the reporting date of the visit. In the event study, we

use the starting date of the visit rather than the reporting date as the event day in order

to alleviate the information effects brought by news release. Figure 2 shows the

significant market reactions of political visit, which almost reaches 2.5%. The market

starts to react 10 days before, which is caused by the information leakage since

leaders’ visiting plans are determined in advance and the local government will be

informed about the visit in advance in order to let them have enough time to prepare

for the visit.

[Insert Figure 2 about here]

Figure 3 decomposes political visits into two parts: visits by Hu administration

and visits by Xi administration. According to Figure 3, the market reactions of Xi

administration are much greater, which approaches 7%. One plausible reason is that

compared with Hu administration, the Xi administration is more powerful. For

instance, after a key four-day meeting of top-level party officials in Beijing,

Communist Party has elevated Xi Jinping to the "core" of its leadership. "The core of

the Chinese Communist party” is not just a new title but very symbolic in China and

implies the power of President Xi. Moreover, after Xi launched the anti-corruption

campaign, his reputation and prestige becomes more and more impressive. As a result,

people make more dramatic market reactions to the visit of the government led by

President Xi for its power and reputation. Another possible reason for the significant

market reactions is that Xi administration visits firms less frequently (82 times) if

compared with the visits of Hu administration (400 times).

[Insert Figure 3 about here]

Table 4 shows the significance of market reactions over different time windows.

Row (1) of Panel A demonstrates that political visit can trigger significant positive

market reactions over all windows. In row (2), we divide political visit into the visit of

Hu administration and the visit of Xi administration. The results show that the market

reactions of visit by Xi administration are more significant than those of visit by Hu

administration, which is consistent with figure 3. Row (3) divides the whole sample

according to leaders’ different rankings of political power. We code the rankings

according to the rankings listed on Leader’s Activity Database and rank 1 refers to

president. The results show that the market reactions of visit by president are the most

significant. This is also supported by the results in row (4) when we divide sample

into president and other positions. Panel B of table 4 demonstrates the market

reactions of political visits reported in different newspaper sections. The results

indicate that the market reactions of the visit reported on the first section of People’s

Daily are the most significant.

[Insert Table 4 about here]

5.2 Firm Heterogeneity

To address challenges and limitations of previous results, we take firm heterogeneity

into account to explore whether visit differentially affects market reactions across

different types of firms in a manner that is consistent with particular theories. We split

sample according to the existence of political connection, the dependence on external

financing, and the geographic proximity to address two interpretational and analytical

weaknesses of previous results. Firstly, through splitting samples according to firm

characteristics, we can evaluate the precision of different theoretical predictions about

whether existence of political connections, distance to political power and dependence

on external financing will influence the impacts of visit on market reactions. Secondly,

concerns about omitted variable bias can be reduced by differentiating among various

types of firms to focus on how market reacts differently to political visit across

different firms.

The first firm trait that can influence the market reactions of political visit is the

existence of political connections, which implies the existence of political supports.

Political visit, as a new kind of political support, can trigger different market reactions

for firms with and without connections. One hypothesis is that political support has

diminishing marginal effects, meaning that the effects of political visit for firms

already with political connection is not as large as the effects for firms without

connections. Consequently, market reactions for non-connected firms are higher.

Competing hypothesis is that firms already with connections can utilize their political

network to get more material preferential resources once they achieve political visit

from central government. As a result, visit for connected firms are deemed as more

valuable in the eyes of investors. To test this, we split samples according to five

proxies of political connection: (1) whether the directors of the firm has a political

background; (2)whether the firm is SOE; (3) whether the firm is CG; (4) number of

state shares; (5) the corruption level of the firm. Corruption is the ratio of

entertainment cost to the sales. Firms with higher ratio are more likely to spend

money to bribe government in return for political connection. The results of mean

tests are shown in table 5. Panel A tests the difference in CAR(-7,90), and we also test

the difference in CAR(-7,180) in panel B to make our results more robust. Rows (1)

to (5) of both panels demonstrate that the market reactions of firms without or with

relatively low connections are significantly higher, which is consistent with our first

hypothesis.

The second firm trait that the market reactions of visit are contingent on is the

dependence on external financing. The impacts of political visit on firms who heavily

rely on external financing are assumed to be larger since these firms can get easier

access to external funds after achieving more social attentions and reputation through

political visit. However, although the difference is significant in Panel A, the

significant results disappear when we extend the window in panel B.

The third firm trait to influence the market reactions are geographic

characteristics: (7) the distance of the visited firms to Beijing; (8) whether the firm is

located in municipality; and (9) whether the firm is located in autonomous areas.

According to Kim, Pantzalis and Park (2012), proximity to political power can reflect

firms’ exposure to political resources and policy risks. This paper then examines

whether the influences of political visit vary if proximity to political power changes.

We measure the proximity to political power by using the distances of firms’

headquarters to the capital of China—Beijing. One hypothesis is that firms far away

from Beijing can rarely get support from central government or at least the supports

are not as strong as those for the firms who are close to the political center. As a result,

political visits to firms far away from Beijing can lead to more dramatic market

reactions. The competing hypothesis is that firms close to political center can get

more material government supports once they are visited by taking advantage of the

close geographic distances. Row (7) of table 5 panel A and B shows that visit to firms

located far away from Beijing can trigger more significant market reactions. We also

split sample according to municipality and autonomous areas to test whether the

impacts of visit vary if the development level of cities change. Municipality refers to

four relatively developed cities: Beijing, Shanghai, Tianjin and Chongqing.

Autonomous areas are the places with a lot of minorities and relatively less developed.

The results in row (8) and (9) of table 5 indicate that there is no difference in the

market reactions.

[Insert Table 5 about here]

5.3 Institution Heterogeneity

Institution development level, like firm characteristics, can influence the market

reactions of political visit. Shleifer and Vishny (1994, 1998) and Hellman, Jones, and

Kaufmann (2000) suggest that politicians’ interventions in business activities are more

severe when institutional constraints are weak. In other words, when institutional

development is weak, the negative role of government may exceed its positive role

due to the heavy interventions. In contrast, the good institutional development can

magnify governments’ positive role.

We split samples according to the development of legal institution, marketization

and banking system in table 5. These indexes are obtained from a survey of Fan

(2011). Two proxies are used to measure the development of legal institution: (1)

Government efficiency refers to the days spent with government and (2) Helping hand

of government index. Following Fan’s (2011) method, we use the proportion of

non-state sales to proxy the marketization. The results in row (1) to (3) of panel A

table 5 indicate that visit to the firms located in provinces with better institution and

marketization can lead to higher market reactions. Panel A tests the difference in

CAR(-7,90), and we also test the difference in CAR(-7,180) in panel B to make our

results more robust. The results in panel B are consistent with panel A.

[Insert Table 6 about here]

6 Political visit and firm performance

6.1 Determinants of political visit

Since table 3 indicates that SOEs are visited more frequently, we then investigate

what types of firms are more likely to be visited. We first test 3 different

connection-related determining factors of political visit. The first one is political

connection. It’s possible that connected firms have higher possibility to be visited by

the government. Three proxies are used to measure political connection: (1) whether

the controlling shareholders of the visited firms are central government (SOE_CG) or

other SOEs (SOE_other). (2) Whether the directors of the visited firms have political

background (PB). (3) Number of state shares (State shares). The dependent variable

of Table 8 is P(visit), meaning the probability to be visited, which equals 1 if the firm

is visited by political leaders. The results shown in column (1) and (3) of table 7

demonstrate that political connection is a significant determinant of political visit.

However, the results in column (2) indicate that individual-level connections like the

political background of directors are not significant determinants.

Since it’s possible that companies bribe officials in return for the visit, especially

in a sole-ruling party like China with heavy corruption, the second possible

connection-related determinant is corruption. Firm-level corruption data is hard to

collect since firms are reluctant to disclose such unethical information, so we follow

World Bank’s method to calculate Corruption as the ratio of entertainment cost to

sales. As shown in column (4) of table 5, corruption is not a significant determinant of

political visit.

Geographic characteristics can also influence the probability of achieving

political visit. The first two geographic characteristics we test are: municipality and

autonomous areas. Municipality refers to four relatively developed cities: Beijing,

Shanghai, Tianjin and Chongqing. Autonomous areas are the places with a lot of

minorities and relatively less developed. These two geographic characteristics can

help us to investigate whether provincial development level will be taken into account

when leaders choose firms to visit. Municipality is negatively significant while

autonomous area is positively significant as shown in column (5) and (6) respectively,

meaning that government is more inclined to visit less developed areas in order to

confer credibility and attention upon those firms and regions. The third geographic

characteristic we test is the distance to the political power. We measure the proximity

to political power by using the distances of firms’ headquarters to the capital of

China—Beijing. Since the previous results show that leaders tend to visit less

developed autonomous regions more frequently, and relatively less developed regions

are usually far away from the capital, we assume that firms far away from capital is

more likely to achieve political visit. Results in column (7) provide supporting

evidences for this assumption.

We then test several non-connection-related determinants of political visit. Firstly,

government may consider the political visit as a method to win over people’s support

(Faccio, Masulis and McConnell, 2006). As a result, the more employees one firm has,

the more likely the government visits that firm. So in column (8) of Table 7, we want

to test whether logarithm of employee number (Employee) can significantly predict

the probability of political visit. The results show that the government is partial to

firms with more employees in order to draw more support.

Secondly, we test whether other common firm features at play here, including

firm size, age, leverage, and past performance. Size is defined as the logarithm of

market value, which is consistent with the method used by other researchers like

Hasan et al. (2014). Since size is certified to be the determinant of political connection

(Hasan et al., 2014), the determinant of obtaining political bailouts (Faccio, Masulis

and McConnell, 2006), and one of the determining factors of achieving third-party

endorsement (Adams, 1999), it can be assumed that firm size can influence the

probability of being visited. Since the younger the firm is, the more likely firm

pursues political visit in order to adapt to market and achieve trust from consumers,

age is included in models. Furthermore, leverage, as a proxy for solvency, and firm

past performances can also affect the probability of visit because government has

preference to visit representative firms with good financial and managerial status. All

of these possible influential firm characteristics are included in model (1) to (8), and

the results indicate that larger size, younger age, less leverage and better past

performance can increase the probability of being visited. Finally, the model in

column (9) incorporates all possible determinants mentioned above. As shown in

column (9), the number of state shares can still increase the probability of political

visit while the proxies for geographic characteristics are no longer significant, and the

results of most of the basic firm features like size and age are consistent with previous

results.

[Insert Table 7 about here]

6.2 Firm Performance

Before testing the impact of political visit on future firm performance, we use the

significant determinants of political visit shown in section 6.1 and a series of firm

basic characteristics like leverage and age to match visited firms with non-visited

firms by applying propensity scoring matching (PSM). According to table 8, most of

the differences between the variables of treatment and control group are no longer

significant after one-to-one matching.

[Insert Table 8 about here]

The matched sample has 706 observations, namely 353 pairs of visited and

non-visited firms. The same firm can be visited repeatedly in different years, so one

firm can be visited for several times by the same or different political leaders during

the eight years. In table 9, we use the matched sample to test the effects of political

visit on firm future performance. The dependent variable is firm performance and

performance is forwarded one year in order to give firms enough time to take

advantage of the political visit. We use four different measurements of performance in

order to make the results more robust: operating margin (OM), ROA, ROE and ROS.

In column (1), (4), (7) and (10), we treat all visits as a whole and test the impacts on

one-year forwarded performance. While political visit can help firms to improve

future ROA and ROE, it has no impact on OM and ROS. Then we test the influence

of political visits by different governments separately. Column (2), (5), (8) and (11)

focus on the impacts of visit by Xi administration while column (3), (6), (9) and (12)

investigate the visit by Hu administration. The results present that visit by Xi

administration can significantly improve firm performance, no matter which

performance measures are used. In contrast, visits by Hu administration have no

impact on firm performance.

[Insert Table 9 about here]

7. Chanel of Value Creation

Then we test the impacts of political visit on the government support firms can obtain

and the social burden firms need to shoulder in the future, and also on the changes of

firm policies. Matched sample is used here. According to the researchers like Hearn

(2012) and Faccio, Masulis and McConnell (2006), companies are able to get more

favorable resources after establishing relationship with government. Therefore, we

test whether government will give visited firms more supports like reduction in

effective tax rates. However, the results in panel A table 10 show that there is no

impact on the one year forwarded effective tax rate (ETR_F) or the change of

effective tax rate (δETR), and the firms are even expected to pay more tax after being

visited by Xi administration.

Based on Raff and Siming (2016), after the reintroduction of knighthoods and

damehoods of CEO, firms employ more employees in order to shoulder social

responsibility. So in our study, it can be supposed that after being visited by political

leaders and attract more attentions from the society, the visited firms need to shoulder

more social responsibilities by contributing more donations or employing more

employees. Results in panel A demonstrate that firms visited by Xi administration

need to shoulder more social responsibilities after being visited but donate less.

We further explore the impacts of political visit on corporate policies: earnings

management (EM_F orδEM), management shares (Managershares_F) and

management salaries (Salary_F). According to panel B of table 10, earnings

management decreased significantly due to the increased social attention after being

visited by Xi administration. Management shares and salaries are supposed to increase

after political visit as a bonus of winning leaders’ visiting, and the results support this

assumption. Table 10 also indicate that visit by Xi administration can influence

government support, social burden and firm policies while visit by Hu administration

almost has no impacts on firms.

[Insert Table 10 about here]

8. Conclusions:

Existing literatures investigate how government participates in market through

various approaches, but ignore a common strategy government use to influence the

market – political visit. Political visit is a pervasive phenomenon across different

countries and has traditionally been studied only in literature on politics. To fill these

gaps, political visit is introduced in this paper as a new way that government can use

to participate in the market. Political visit, under this paper, is defined as a political

device in which a high-level political leader of a country carries out all the functions

and symbolic representations of governing by periodically visiting firms in their own

countries.

The results demonstrate that political visit can lead to positive market reactions

over different time windows, especially when the firms are visited by Xi

administration or president. We also test whether market reacts differentially across

different types of firms and under different institution development level. The visit to

firms without political connection, far away from Beijing, and located in a place with

good institution can lead to higher market reactions. Moreover, results show that

government is more inclined to visit firms with connections. But political connection

is only one of the reasons for firms to achieve political visit. Firms with larger size,

younger age, less leverage, more employees, better past performance, located far

away from Beijing are also more likely to achieve political endorsements. After

matching sample through PSM, results indicate that being visited by Xi administration

can improve firm performance while being visited by Hu administration has no

impact on performance. Results also point out that after being visited by Xi

administration, the effective tax rate of firms will increase, and firms will recruit more

employees while donate less. Furthermore, the earnings management will decrease

due to the increased social attention after visiting, and the shares and salary of

managers will increase as bonus of winning political visit. However, being visited by

Hu administration has no impact on these channels.

This paper is the first one to examine the role of political visit in financial market.

Existing literature about political visit or presidential travel is only restricted to

politics studies and most of the studies only focus on the impacts of political visit on

leaders themselves while this paper visits from a different angle by focusing on the

impacts of political visit on financial market. And this study supplements the literature

on political economy by introducing political visit as a new approach that government

can use to influence the market. Different from political connection, both connected

and non-connected firms can be the target of political visit, and the political leaders to

visit firms usually have a higher-level position than the officials firms normally

connected with. And different from political endorsement, the money and time costs

for the leader and his whole team by doing political visit demonstrate the importance

the leaders attach to these firms. Furthermore, this paper is also related to the

literature on certification effects. Compared with general certification from financial

organizations, achieving visit from political leaders of central government is rarer and

more valuable.

References:

Amore, M. D., & Bennedsen, M. (2013). The value of local political connections in a

low-corruption environment. Journal of Financial Economics,110(2), 387-402.

Barclay M J, Holderness C G. Private benefits from control of public corporations[J].

Journal of financial Economics, 1989, 25(2): 371-395.

Bertrand, M., Kramarz, F., Schoar, A., & Thesmar, D. (2006). Politicians, firms and

the political business cycle: evidence from France. Unpublished working paper.

University of Chicago.

Bhagwati, "On the Equivalence of Tariffs and Quotas," in his Trade, Tariffs and

Growth, London 1969.

Brace, P., & Hinckley, B. (1992). Follow the leader: Opinion polls and the modern

presidents. New York: HarperCollins

Bunkanwanicha, P., & Wiwattanakantang, Y. (2009). Big business owners in

politics. Review of Financial Studies, 22(6), 2133-2168.

Calomiris, C. W., Fisman, R., & Wang, Y. (2010). Profiting from government stakes in

a command economy: Evidence from Chinese asset sales. Journal of Financial

Economics, 96(3), 399-412.

Claessens, S., Feijen, E., & Laeven, L. (2008). Political connections and preferential

access to finance: The role of campaign contributions. Journal of Financial

Economics, 88(3), 554-580.

Cohen J E, Powell R J. Building Public Support from the Grassroots Up: The Impact

of Presidential Travel on State ‐ Level Approval[J]. Presidential Studies

Quarterly, 2005, 35(1): 11-27.

Cook, C. (2002). The permanence of the “permanent campaign”: George W. Bush’s

public presidency. Presidential Studies Quarterly, 32, 753-764.

Faccio M. Politically connected firms[J]. The American economic review, 2006, 96(1):

369-386.

Faccio, M. (2010). Differences between Politically Connected and Nonconnected

Firms: A Cross‐Country Analysis. Financial Management,39(3), 905-928.

Faccio, M., Masulis, R. W., & McConnell, J. (2006). Political connections and

corporate bailouts. The Journal of Finance, 61(6), 2597-2635.

Fan, J. P., Wong, T. J., & Zhang, T. (2007). Politically connected CEOs, corporate

governance, and Post-IPO performance of China's newly partially privatized

firms. Journal of financial economics, 84(2), 330-357.

Frye T, Shleifer A. The invisible hand and the grabbing hand[R]. National Bureau of

Economic Research, 1996.

Goldman, E., Rocholl, J., & So, J. (2009). Do politically connected boards affect firm

value?. Review of Financial Studies, 22(6), 2331-2360.

H. G. Johnson, "The Cost of Protection and the Scientific Tariff," J. Polit. Econ., Aug.

1960, 68, 327-45.

Hart, R. P. (1987). The sound of leadership: Presidential communication in the

modern age. Chicago: University of Chicago Press.

Hasan, I., Jackowicz, K., Kowalewski, O., & Kozlowski, L. (2014). Politically

connected firms in Poland and their access to bank financing (No. 2/2014). Bank

of Finland, Institute for Economies in Transition.

Hillman, A. J. (2005). Politicians on the board of directors: do connections affect the

bottom line?. Journal of Management, 31(3), 464-481.

Jeffrey Herbst, States and Power in Africa: Comparative Lessons in Authority and

Control (Princeton: Princeton University Press, 2000), pp. 97-136.

John W. Bernhardt, Itinerant Kingship and Royal Monasteries in Early Medieval

Germany, c. 936-1075 (Cambridge: Cambridge University Press, 1993)

Khwaja, A. I., & Mian, A. (2005). Do lenders favor politically connected firms? Rent

provision in an emerging financial market. The Quarterly Journal of Economics,

1371-1411.

Krueger, Anne O. "The Political Economy of the Rent-Seeking Society." American

La Porta R, Lopez‐de‐Silanes F, Shleifer A. Government ownership of banks[J].

The Journal of Finance, 2002, 57(1): 265-301.

Lawrence, S. (1999). Too many mothers-in-law. Far Eastern Economic Review, 19(2),

12-13.

Li, H., Meng, L., Wang, Q., & Zhou, L. A. (2008). Political connections, financing

and firm performance: Evidence from Chinese private firms. Journal of

development economics, 87(2), 283-299.

Li, J. J., Poppo, L., & Zhou, K. Z. (2008). Do managerial ties in China always

produce value? Competition, uncertainty, and domestic vs. foreign firms.

Strategic Management Journal, 29(4), 383-400.

Luo, D., & Liu, X. (2009). Political relationship, entry barriers, and firm

performance. Management World, (5), 97-106.

Michael Schatzberg, Political Legitimacy in Middle Africa: Father, Family, Food

(Bloomington: Indiana University Press, 2001).

Mitchell T. The limits of the state: beyond statist approaches and their critics[J].

American political science review, 1991, 85(01): 77-96.

Ostrom, C. W., & Simon, D. M. (1985). Promise and performance: A dynamic model

of presidential popularity. American Political Science Review, 79, 334-358.

Sachs, Jeffrey. Poland's jump to a market economy. Cambridge, MA: MIT Press,

1994.

Siegel, J. (2007). Contingent political capital and international alliances: Evidence

from South Korea. Administrative Science Quarterly, 52(4), 621-666.

Walder, Andrew. "China's Transitional Econ- omy: Interpreting its Significance."

China Quarterly, December 1995, (144), pp. 963-79.

Yermack D. The Michelle Markup: The First Lady’s Impact on Stock Prices of

Fashion Companies[J]. Available at SSRN 1596803, 2011.

You, J., & Du, G. (2012). Are political connections a blessing or a curse? Evidence

from CEO turnover in China. Corporate Governance: An International

Review, 20(2), 179-194.

Table 1 Definition of Variables

Variables

Visit Dummy variable, equals one if the firm is visited by a political leader.

Xi administration Dummy variable, equals one if the firm is visited by Xi administration. Xi administration refers to the

government led by president Xi. Our sample covers 1st March 2013-- 31st July 2016.

Hu administration Dummy variable, equals one if the firm is visited by Hu administration. Hu administration refers to the

government led by president Hu. Our sample covers 1st Jan.2009 -- 1st March 2013.

SOE_CG If actual controller is central government, equals one.

SOE_Other If actual controller is other SOEs except central government, equals one.

Private If actual controller is private company or individuals, equals one.

PB PB refers to political background. If the director of a firm also works as a government official, equals

one.

State share The logarithm of number of shares owned by the state.

Corruption Equals the ratio of the entertainment costs of managers or the hospitality fees to sales. Firm-level data.

Municipality If the firm is located in municipalities (Beijing, Shanghai, Tianjin and Chongqing), equals 1.

Autonomous Autonomous equals one if that area is classified as autonomous area by government since there are a lot

of minorities

Distance Distance, as a measurement of the proximity to political power, refers to the distances of firms’

headquarters to the political center of China—Beijing.

Size Ln( Market value), where the value of non-tradable shares are calculated by using net asset value.

Age The age of the firm since established.

Leverage Total equity/total liability

Employee The logarithm of employee number

Employee_F The logarithm of employee number, forwarded one year.

ROA_F Return on asset, forwarded one year.

Return on Asset (ROA) =Net income/Ave. of beginning and ending total assets

Past performance (ROA_P) (ROA𝑡−1 + ROA𝑡−2)/2

ROS_F Return on sakes, forwarded one year.

Return on Sales (ROS) =Net income/sales

OM_F Operating margin, forwarded one year.

Operating Margin (OM)= EBIT/Sales

ROE_F Return on equity, forwarded one year.

Return on Equity (ROE) =Net income/Ave. of beginning and ending total equity

Subsidy_F Government subsidy, forwarded one year.

δETR Following Feng, Johansson and Zhang’s (2013) method, δETR represents the change in tax

burden, equaling to the difference between the annual effective tax rate before and after the

political endorsements. ETR is defined as (tax expense-deferred tax expense)/EBIT.

ETR_F Effective tax rate, forwarded one year. ETR is defined as (tax expense-deferred tax

expense)/EBIT.

Management share_F Logarithm of management shareholdings, forwarded one year.

Salary_F Logarithm of management salaries, forwarded one year.

Donation_F Donation_F means the donation, representing corporates’ social responsibilities.

Self-dealing_F Logarithm of related-party transfer.

EM_F Ratio of non-operating income relative to revenue, forwarded one year.

δEM Change in earnings management.

Government efficiency Days spent with government, obtained from a survey of Fan (2001)

Helping hand of government Obtained from a survey of Fan (2001). The survey question is : how helpful is the government during

M&A?

Marketization index Proportion of non-state sales to total sales, obtained from a survey of Fan (2001)

Table 2 Descriptive Statistics of Visit

This table shows the descriptive statistics of political visits. Panel A demonstrates the distribution of the visited provinces.

Panel B demonstrates the distribution of leaders who visit firms. Panel C is the distribution of newspaper sections which

report political visit. Leader’s Activity Database integrates information about political visit from two resources: People’s

Daily and local newspapers. People’s Daily is an official newspaper of Communist Party and it is the biggest newspaper

group in China. People’s Daily has 24 sections in total, within which sections 1 to 6 are specialized for most important

news.

Panel A Distribution of Province

Province name Freq. Percent

Anhui 19 3.940

Beijing 33 6.850

Fujian 9 1.870

Gansu 16 3.320

Guangdong 23 4.770

Guangxi 14 2.900

Guizhou 5 1.040

Hainan 4 0.830

Hebei 14 2.900

Henan 18 3.730

Heilongjiang 9 1.870

Hubei 20 4.150

Hunan 25 5.190

Jilin 18 3.730

Jiangsu 32 6.640

Jaingxi 7 1.450

Liaoning 38 7.880

Neimenggu 29 6.020

Ningxixa 12 2.490

Qinghai 2 0.410

Shandong 36 7.470

Shanxi 13 2.700

Shannxi 7 1.450

Shanghai 13 2.700

Sichuan 15 3.110

Tianjin 10 2.070

Xinjiang 18 3.730

Yunnan 6 1.240

Zhejiang 7 1.450

Chongqing 10 2.070

Total 482 100

Table 2 Descriptive Statistics of Visit (Cont.)

This table shows the descriptive statistics of political visits. Panel A demonstrates the distribution of the visited provinces.

Panel B demonstrates the distribution of leaders who visit firms. Panel C is the distribution of newspaper sections which

report political visit. Leader’s Activity Database integrates information about political visit from two resources: People’s

Daily and local newspapers. People’s Daily is an official newspaper of Communist Party and it is the biggest newspaper

group in China. People’s Daily has 24 sections in total, within which sections 1 to 6 are specialized for most important

news.

Panel B Distribution of leaders during visiting

Xi administration Hu administration

Leader name Freq. Percent Leader name Freq. Percent

Jinping Xi 19 23.17 Jintao Hu 28 7

Keqiang Li 23 28.05 Jinping Xi 35 8.750

Yunshan Liu 10 12.20 Qinglin Jia 69 17.25

Zhengsheng Yu 7 8.540 Changchun Li 75 18.75

Dejiang Zhang 8 9.760 Keqiang Li 49 12.25

Gaoli Zhang 15 18.29 Jiabao Wen 67 16.75

Bangguo Wu 29 7.250

Guoqiang He 48 12

Total 82 100 Total 400 100

Panel C Distribution of Sections

Sections Freq. Percent

People’s Daily section 1 395 81.95

People’s Daily section 2 7 1.450

People’s Daily section 3 41 8.510

People’s Daily section 4 23 4.770

Local Newspaper 16 3.320

Total 482 100

Table 3: Descriptive Statistics of Visited Firms

This table shows the descriptive statistics of visited firms. Panel A demonstrates the number of visited firms

that are controlled directly by central government (SOE_CG), by other SOEs except CG (SOE_Other) and

private firms (Private). Then in Panel B and C, we decompose the whole sample in Panel A into two

subsets: Xi administration and Hu administration. Panel D reveals the industry distribution of visited firms.

Panel E compares the mean differences between visited & non-visited firms. Definitions of variables are

shown in table 1. P-values are reported in parenthesis. ***, **, * denote significance levels at 1%, 5% and

10% respectively.

PANEL A Ownership distribution

Visited firms All listed firms

(1) (2) (3) (4)

# % # %

SOE_CG 11 5% 71 3%

SOE_Other 126 58% 1,014 43%

Private 82 37% 1,272 54%

Total 219 2357

PANEL B Ownership distribution for Xi administration

Visited firms All listed firms

(1) (2) (3) (4)

# % # %

SOE_CG 1 3.70% 50 2.13%

SOE_Other 12 44.44% 985 42.02%

Private 14 51.85% 1,309 55.84%

Total 27 2344

PANEL C Ownership distribution for Hu administration

Visited firms All listed firms

(1) (2) (3) (4)

# % # %

SOE_CG 10 5.21% 67 3.14%

SOE_Other 114 59.38% 985 46.11%

Private 68 35.42% 1,084 50.75%

Total 192 2136

Table 3: Descriptive Statistics of Visited Firms (Cont.)

This table shows the descriptive statistics of visited firms. Panel A demonstrates the number of visited firms that are controlled directly by central government

(SOE_CG), by other SOEs except CG (SOE_Other) and private firms (Private). Then in Panel B and C, we decompose the whole sample in Panel A into two

subsets: Xi administration and Hu administration. Panel D reveals the industry distribution of visited firms. Panel E compares the mean differences between

visited & non-visited firms. Definitions of variables are shown in table 1. P-values are reported in parenthesis. ***, **, * denote significance levels at 1%, 5% and 10%

respectively.

PANEL D industry distribution

GICs industry ALL Visited Firms Xi administration Hu administration All listed firms

(1) (2) (3) (4) (5) (6) (7) (8)

# % # % # % # %

10 Energy 9 4.170 2 8.00 7 3.66 57 2.74

15 Materials 39 18.06 4 16.00 35 18.32 401 19.30

20 Industrials 59 27.31 5 20.00 54 28.27 484 23.29

25 Consumer Discretionary 36 16.67 6 24.00 30 15.71 379 18.24

30 Consumer Staples 9 4.170 0 0.00 9 4.71 148 7.12

35 Health Care 13 6.020 2 8.00 11 5.76 131 6.30

40 Financials 9 4.170 2 8.00 7 3.66 171 8.23

45 Information Technology 33 15.28 4 16.00 29 15.18 230 11.07

50 Telecommunication Services 1 0.460 0 0.00 1 0.52 5 0.24

55 Utilities 8 3.700 0 0.00 8 4.19 72 3.46

Table 3: Descriptive Statistics of Visited Firms (Cont.)

This table shows the descriptive statistics of visited firms. Panel A demonstrates the number of visited firms

that are controlled directly by central government (SOE_CG), by other SOEs except CG (SOE_Other) and

private firms (Private). Then in Panel B and C, we decompose the whole sample in Panel A into two

subsets: Xi administration and Hu administration. Panel D reveals the industry distribution of visited firms.

Panel E compares the mean differences between visited & non-visited firms. Definitions of variables are