Embed Size (px)

Citation preview

Policy for Market Failure: Market-based strategies

Price InstrumentsJeffrey Ely and Lam Thuy Vo / NPR

Instrument taxonomy

Market-based instruments

• Advantages of MBI’s over C&C (Stavins, 1998): – cost effectiveness, and – dynamic incentives for technology innovation

• Encourage behavior change through market signals rather than with explicit behavioral requirements.

• Key attribute: MBI’s take advantage of private information that polluters have – RE: means and procedures they could use to reduce

pollution

Price-based policy examples

Fees/taxes/charges to disincentivize activity• User fees (e.g. National Parks)• Congestion fees, road tolls (e.g. London

congestion charge, 8 £)• Emissions fees (e.g. GHG tax)

Subsidies to incentivize activity• Abatement subsidies (reduce “bads”)

– E.g. NC bill to provide $50B to reduce hog farm waste

• Subsidies to encourage “goods”– California Million Solar Roofs Initiative– 2008 Farm Bill

• $14B in subsidies for various crops • $27B to conserve environmentally sensitive

farmland• $23B crop insurance

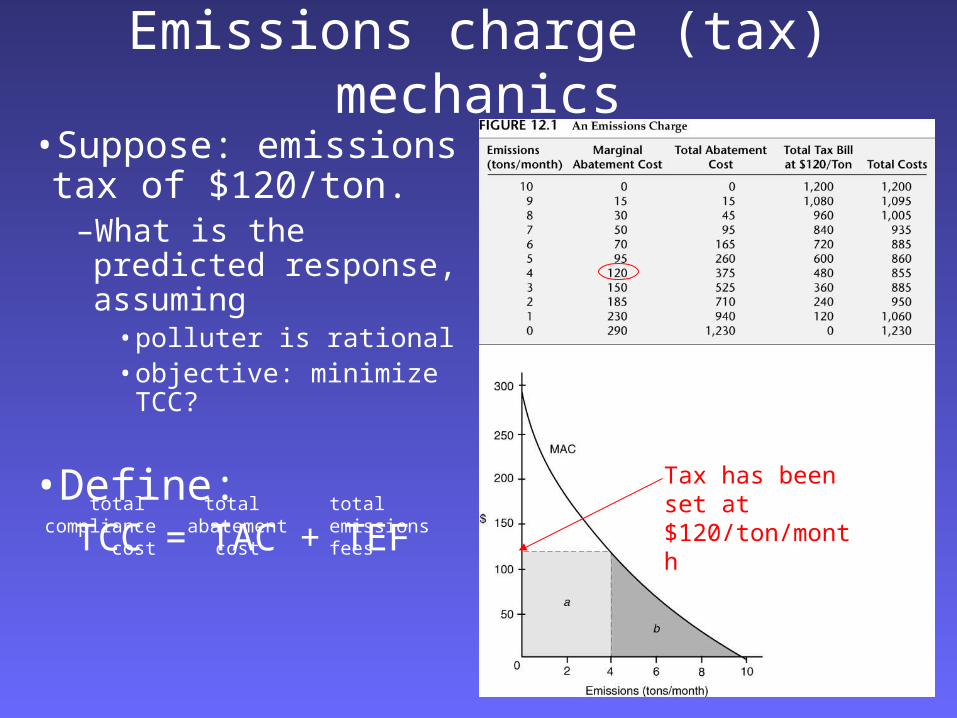

Emissions charge (tax) mechanics

•Suppose: emissions tax of $120/ton.

–What is the predicted response, assuming

• polluter is rational• objective: minimize TCC?

•Define:TCC = TAC + TEF Tax has been set

at $120/ton/monthtotal compliance

cost

total abatement

cost

total emissionsfees

Tax - mechanics

• If the MAC curve shifts down (e.g. MAC’) – does the predicted

level of abatement go up or down (tax unchanged)?

MAC’

Arthur Cecil Pigou“Corresponding to the above investments in which marginal private net product falls short of marginal social net product, there are a number of others, in which, owing to the technical difficulty of enforcing compensation for incidental disservices, marginal private net product is greater than marginal social net product.

Thus, incidental uncharged disservices are rendered to third parties when the game-preserving activities of one occupier involve the overrunning of a neighbouring occupier's land by rabbits—unless, indeed, the two occupiers stand in the relation of landlord and tenant, so that compensation is given in an adjustment of the rent. ….

Yet again, third parties—this time the public in general—suffer incidental uncharged disservices from resources invested in the running of motor cars that wear out the surface of the roads. The case is similar—the conditions of public taste being assumed—with resources devoted to the production and sale of intoxicants.”

The Economics of Welfare, 1921 h/t Krugman Killer Rabbit of CaerbannogMonty Python and the Holy Grail

Setting an efficient tax

• If the MD function is known then the tax can be set to produce the efficient level of emissions.

• When the tax is set equal to the marginal damage at the efficient level of emissions we call it a “Pigovian tax/fee”

Setting an efficient tax

• Questions: Identify…– Efficient emissions– Given t*:

– TAC: Total abatement cost – TEF: Total emissions fees

(“tax bill”)– TB: Total benefit from

damages averted.

A diversion: • Swiss millionaire (est. wealth: $20M)

• Ferrari Testarossa driver (red)

• a repeat traffic offender“Roland S*”

Source: http://www.blick.ch/news/schweiz/ostschweiz/st-galler-ferrari-raser-ich-bin-diplomat-137378 (Assoc. Press, Jan 7, 2010)

• Caught driving “35 miles an hour faster than the 50-mile-an-hour limit”

• fined $290,000 for speeding (Swiss court in St. Gallen)

– record-breaking fine

• Price instrument in combination with performance standards – tailored to the agent

Equimarginal principle

• Major strength of emissions charges: – IF same tax rate applied to

different sources with different MAC functions

(and each reduces it emissions as predicted such that MAC = tax)

THEN, MAC’s will be equalized across sources.

Cost effectiveness achieved

***Does the regulator have to know the MAC functions for

• a tax to be cost-effective?• a tax to achieve the

socially optimal level of aggregate abatement?

1. look for outcomes in which MACs

are equalized

2. stop when you find the outcome that

achieves the required aggregate abatement

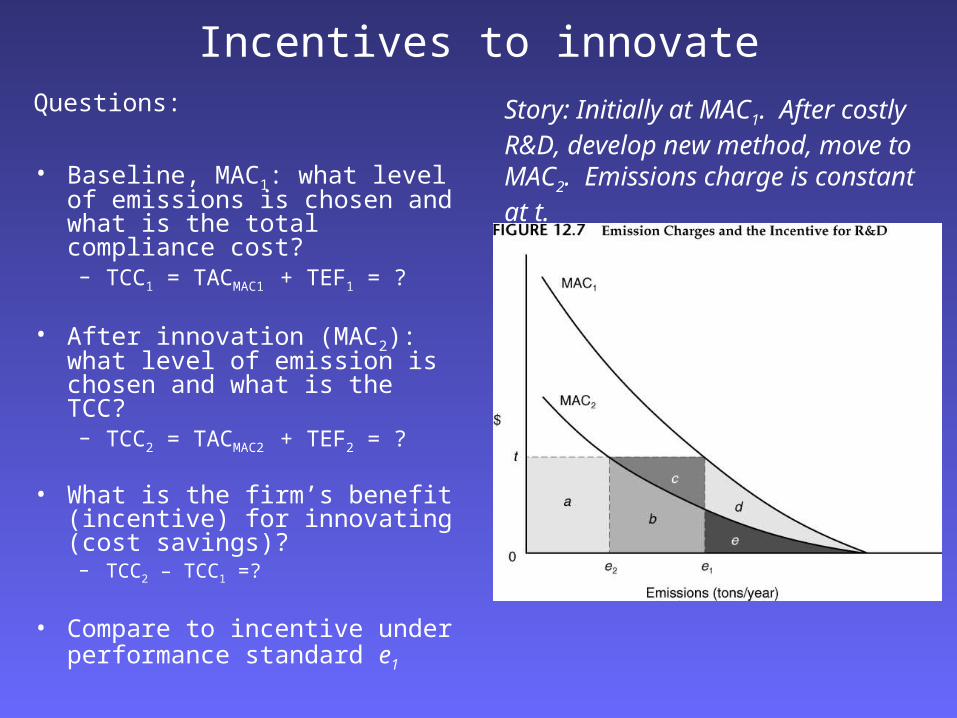

Incentives to innovateQuestions:

• Baseline, MAC1: what level of emissions is chosen and what is the total compliance cost?– TCC1 = TACMAC1 + TEF1 = ?

• After innovation (MAC2): what level of emission is chosen and what is the TCC?– TCC2 = TACMAC2 + TEF2 = ?

• What is the firm’s benefit (incentive) for innovating (cost savings)?

– TCC2 – TCC1 =?

• Compare to incentive under performance standard e1

Story: Initially at MAC1. After costly R&D, develop new method, move to MAC2. Emissions charge is constant at t.

Incentives to innovate are greater under emissions charges than standards

• R&D efforts will lead to a bigger reduction in compliance costs for firms (abatement plus taxes) under a tax compared to a standard.

• Under a tax: a firm will automatically reduce its emissions as it finds ways to shift its MAC function downward – Same incentive not present under standards.

Subsidy policies

• Payments to reduce pollution (less of a bad)

• Price supports (e.g. agriculture) (more of a “good”).

• Deposit-refund systems– Subsidy is the refund (deposit funds the subsidy

payment).

• Subsidy removal

Subsidies• Pollution context: polluter paid per unit of

reduction below some benchmark level– generates an incentive: opportunity cost for polluting

• emitting a given unit of pollution means forgoing the subsidy payment.

• Subsidies to reduce pollution are not common. Why?– Violates “polluter pays” principle– Can potentially lead to more pollution:

Subsidies decrease firm pollution increase industry profits encourage

new entrants more production more pollution

Environmental Law Institute, 2009

Federal energy subsidies, 2002-2008

• “Worried about an impending public health crisis, government officials are considering offering financial incentives to the pharmaceutical industry, like tax breaks and patent extensions, to spur the development of vitally needed antibiotics.

• …bacteria (have) steadily become resistant to virtually all existing drugs at the same time that a considerable number of pharmaceutical giants have abandoned this field in search of more lucrative medicines.”

“Antibiotics Research Subsidies Weighed by U.S.” (A. Pollack, NYT, 11/5/10)

“Antibiotics Research Subsidies Weighed by U.S.” (NYT, 11/5/10)

• “While the notion of directly subsidizing drug companies may be politically unpopular in many quarters, proponents say it is necessary to bridge the gap between the high value that new antibiotics have for society and the low returns they provide to drug companies.

• `There is a market failure,’ said Representative Henry A. Waxman, a California Democrat and the chairman of the House Energy and Commerce Committee, who said he was considering introducing legislation. `We need to look at ways to spur development of this market.’”

• Alternative approach: Generating Antibiotic Incentives Now bill: “provide certain antibiotics with five extra years of protection from generic competition” <What type of approach is that?>

Subsidy removal example: Below-cost timber sales

• Moving timber from U.S. public lands into the marketplace frequently costs the Federal government more than it gets in return implicit subsidy– Common form: credits to private lumber companies for road

building– 1964 Forest Roads and Trails Act

• companies deduct road construction expenses (credits) directly from the amount they pay the Forest Service for the timber they extract.

• Removal of these subsidies could foster environmental protection and save taxpayers up to (an estimated) $1.2 billion over five years.

(Stavins, 1998)

Optional additional material

Ian W.H. Parry. (2011). Reforming the Tax System to Promote Environmental Objectives: An Application to Mauritius. IMF working paper 11/124.

OECD countries

Enforcement costs

• Non-point-source (NPS) pollution: “a form of pollution in which neither the source nor the size of specific emissions can be observed with sufficient accuracy” (Xepapadeas, 2011)

• Most non-point sources of pollution cannot be regulated through emissions charges

– Too costly to monitor• E.g. pollutants in street runoff, agricultural

runoff.