Embed Size (px)

Citation preview

Policies and Research on Financial and

Real Estate Markets in Post Crisis

May 20, 2011 NUS-IRES Symposium

Kyung-Hwan Kim Sogang University

Outline of presentation

Introduction

The impact of Global Financial Crisis on housing and housing finance in Korea

Housing asset and rental markets

Mortgage market

Policy issues

Continued expansion of household debt

Mortgage lending and housing price

Regulation of LTV and DTI

Consumer protection

Down-sizing of the housing sector in a rapidly aging society?

Some research questions

2

The impact of the Global Financial Crisis on housing and

housing finance

Impact on housing price : How is this time different?

In neither AFC and GFC, housing was the cause of the crisis.

Mortgage lending and household debt

Steady expansion of mortgage lending and household debt

No significant increase in delinquency or default on mortgages

Low LTV and DTI, low interest rate

HF stopped issuing MBS for four months since September 2008 due to a sudden rise in the MBS spread over the 5 year KTB rate.

Project financing

Not purely project financing

Rapid expansion and high delinquency: a serious concern

Changing market sentiments and rental market

As housing market sentiments turned negative, chonsei is becoming less popular compared with monthly rents with deposit schemes.

3

Korea Purchase

Korea Chonsei

The real rate of change in purchase price and

chonsei deposit index

Housing market conditions one year prior to the AFC and GFC

Dec-96 Dec-07

population ('000) 45954 48297

population growth rate 0.94% 0.33%

share of age 65 and older 6.40% 9.90%

per capita GNI ($) 11205 21695

number of households ('000) 11542 12760

housing supply ratio 92.0% 108.1%

housing stock('000) 10627 13793

unsold units 88867 112254

PIR 4.6 6.6

5 year house price change (%) 0% 23.5%

5 year CPI change (%) 21.8% 11.6%

5 year real house price change(%) -21.8% 11.9%

MDO/GDP 10.0% 33.0%

household loan lending rate 12.30% 6.48%

LTV on KB mortgages 22.7% 35.3%

Source: KB, MLTM, Kim (2011)

The magnitude of house price fall: AFC vs GFC

Korea Seoul

-14

-10

-6

-2

2

6

1 2 3 4 5 6 7 8

Korea house price AFC

Korea house price GFC

-14

-10

-6

-2

2

6

10

1 2 3 4 5 6 7 8

Seoul house price AFC

Seoul house price GFC

Source: KB, Kim (2011)

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

-5

0

5

10

15

20

25

30

35

40

(%)

Rate of change in Seoul apartment price and delinquency

on housing loans

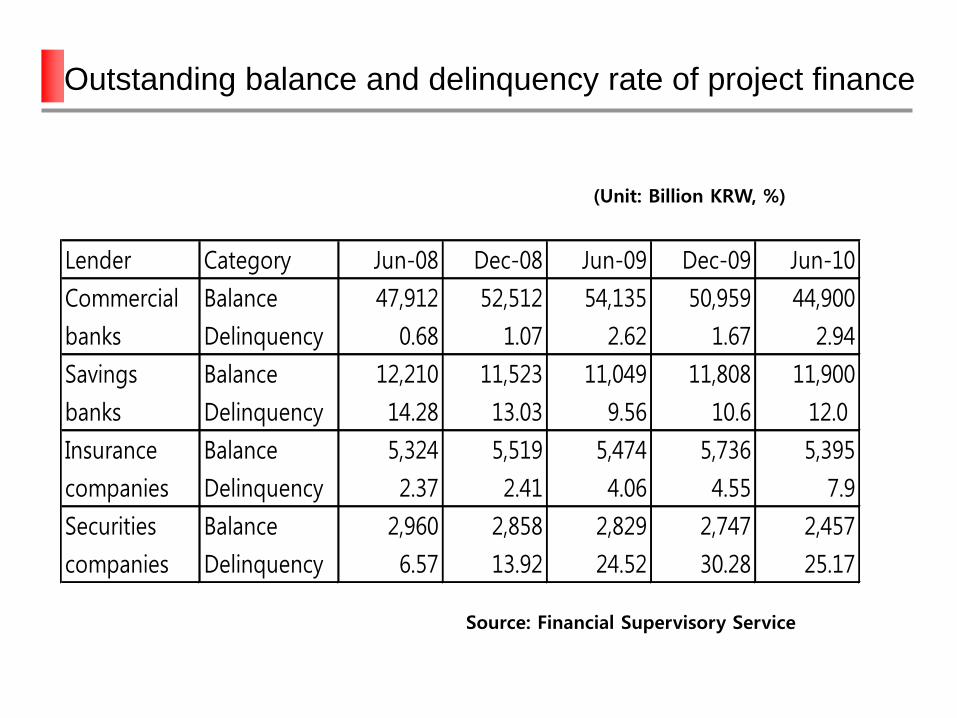

Outstanding balance and delinquency rate of project finance

Lender Category Jun-08 Dec-08 Jun-09 Dec-09 Jun-10

Commercial Balance 47,912 52,512 54,135 50,959 44,900

banks Delinquency 0.68 1.07 2.62 1.67 2.94

Savings Balance 12,210 11,523 11,049 11,808 11,900

banks Delinquency 14.28 13.03 9.56 10.6 12.0

Insurance Balance 5,324 5,519 5,474 5,736 5,395

companies Delinquency 2.37 2.41 4.06 4.55 7.9

Securities Balance 2,960 2,858 2,829 2,747 2,457

companies Delinquency 6.57 13.92 24.52 30.28 25.17

(Unit: Billion KRW, %)

Source: Financial Supervisory Service

Trend of unsold units

9

Unsold houses have become a problem in recent years.

Year 1995-1998

1999-2002

2003 2004 2005 2006 2007 2008 2009 2010

Korea 113380 46464 38261 69133 57215 73772 112254 165599 123297 88,706

Seoul 1927 1914 735 612 574 529 454 2486 1803 2,729

Incheon 4197 957 467 1770 1196 426 527 1647 4539 4,265

Gyeonggi 18511 10002 6168 13076 10472 3769 13643 22795 19325 22,418

SCR 24635 12873 7370 15458 12242 4724 14624 26928 25667 29,412

Rekindling fear of bubble?

A short-lived up-turn

House price appreciation in 2009

Government intervened to cool the housing market

Reversal of the pattern of house price increases

Emergence of gloomy forecast for house prices

Demographic changes, but weren’t they expected?

Implications of lowered expectations

Demand for home ownership fell

Demand for chonsei increased

Emergence of monthly-rental contracts

Why has the suffering been less severe this time?

Macroeconomic factors

GDP growth suffered, but not so much in general, and bottomed out

sooner.

Interest rate remained low.

Financial sector has gotten bigger and stronger (much smaller non-

performing loans)

Government stimulus package was large, comprehensive and prompt.

Housing market factors

Housing price appreciation was smaller than in Europe and US.

Household sector is more resilient

Market expectations recovered soon (learning from the previous crisis?)

Government pre-emptive intervention to stabilize housing demand.

Policy issues going forward

Managing household debt

Strengthening the mortgage market

Macroprudential regulations

Down-sizing of housing sector?

The future of chonsei

Will it phase out?

12

Rapid growth in household debt

13

Mortgage debt currently comprises 65% of banks’ household debt.

Household’s financial liabilities to disposable income ratio rose to 142.7%.

There is a concern that household debt could be a potential risk having an adverse effect on the financial system and the recovery of economy, in case its increasing trend persists.

Source : BOK, NSO

Mortgage Debt Outstanding

Source : BOK, NSO

Household’s financial liabilities to disposable income

0

2

4

6

8

10

12

14

16

18

0

50

100

150

200

250

300

350

400

450

01 02 03 04 05 06 07 08 09

Bank's Household loan (L)Bank's Mortgage loan (L)Mortgage Debt per Household(R)

House

hold

&

Mort

gage loan (

KRW

in t

rillio

ns)

Mo

rtgag

e D

eb

t per H

ou

seh

old

1

1.05

1.1

1.15

1.2

1.25

1.3

1.35

1.4

1.45

1.5

400

450

500

550

600

650

700

750

800

850

900

02 03 04 05 06 07 08 09

Household's liabilities(L) Household's liabilities/Disposable income(R)

(KR

W in

tri

llio

ns)

13 Source: HF

Improving the mortgage system

Problems with the ARM-dominated market

Non-amortizing bullet mortgages

How to promote FRM?

Developments in the U.K. since Miles report (2004)

Funding FRM

MBS vs covered bonds

Going down markets

The credit-constrained and underserved

Mortgage insurance?

Consumer protection

Rollover risk, interest rate adjustment with no cap, prepayment penalty

Provision of information about the risk of loan products

Composition of mortgage products by interest

variability

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Denm

ark

Nethe

rland

s

Cana

da US

Germ

any

Japa

n UK

Spain

Ireland

Australia

Korea

ARM

ST Fixed

MedT Fixed

LT Fixed

FRM marketsARM markets

Source: Lea (2010), HF (2010)

15

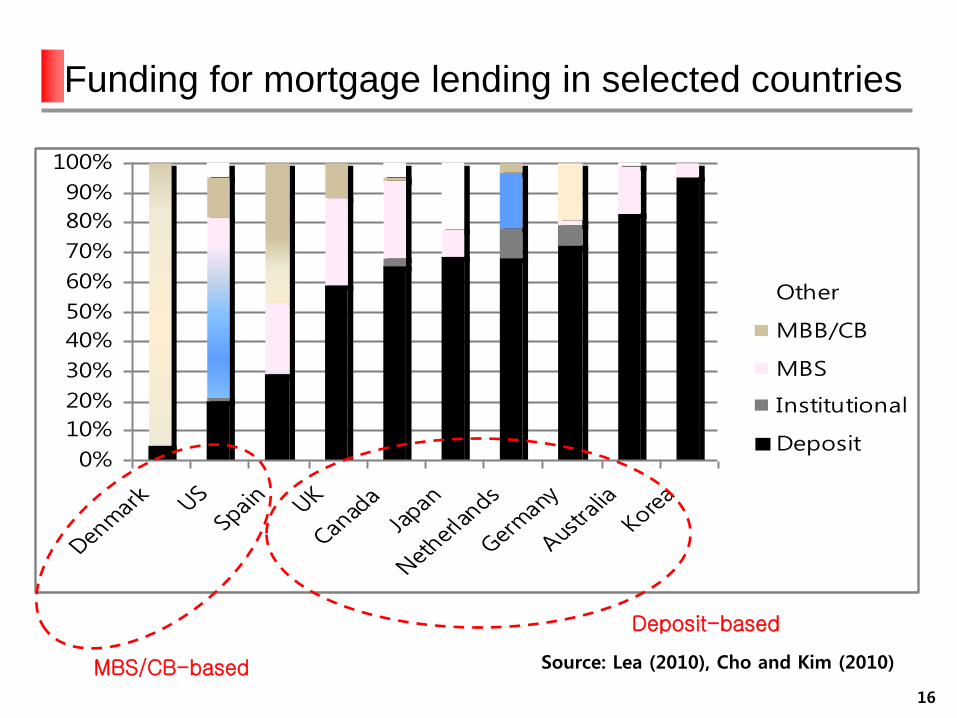

Funding for mortgage lending in selected countries

16

Source: Lea (2010), Cho and Kim (2010)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Denmark US

Spain UK

Cana

da

Japa

n

Nethe

rland

s

German

y

Austra

lia

Korea

Other

MBB/CB

MBS

Institutional

Deposit

MBS/CB-based

Deposit-based

Macroprudential regulations

What is a macroprudential regulation?

Protect the financial system as a whole

Capital requirements as a key tool to control pro-cyclical leverage

Relationship with monetary policy

LTV or DTI ceilings as macroprudential regulation?

Devised as a tool for containing house price hike?

Direct control of lending criteria vs. indirect regulation via banking

supervision

More flexible system relying on individual lenders

17

Housing prices and household loans, 2000-2010

18

Source: Kim and Kim 2010

Positive correlation

Regulations on mortgage origination

LTV

DTI

First Introduced in Sep. 2002

Now applicable to all mortgage origination

Max. LTV ratio differently set by considering

Loan Maturity, House Price, House Type

Location (Speculation Zone, Metropolitan Region)

Lender (Bank vs. Non-banking)

Introduced in 2004 as a requirement for allowing Max.

70% of LTV ratio to FRMs

Expanded its application to mortgages originated

in Speculation Zone in 2006

Application of DTI, decided by Location & House Type

Max. DTI ratio differently set by considering

House Price, Loan Amount, Property Size

Lender (bank vs. Non-banking)

19

MAX. LTV

ratio

MAX. LTV

ratio

70%

Raised to 70%

(More >=10 yrs &

less than 1yr of interest-only payments)

70%

60% All

properties 60%

50% Reduced to

50%

( M=< 3yrs)

Set the LTV ceiling as 50% for

nonbank financial institutions

(M=<10yrs &

more than 600m Won)

Reduced to 50%

(More than 600m Won

in metropolitan area)

50%

40% Reduced to 40%

( M=< 10yrs)

Reduced to 40%

( M=< 10yrs &

more than 600m

Won)

40%

Extended to Nonbank financial Institutions

Removed speculative zones

except 3 Gangnam districts in 2008

Expand the LTV regulations to

all financial institutions for the metropolitan

area in 2009

Introduced the LTV ratio

ceiling of 60% in 2002

Apartment price change

Delinquency Ratio

(%)

History of LTV regulation

MAX. DTI

ratio

MAX. DTI

ratio 70%

Extended to nonbanking institutions as

40~70% of DTI ceiling

70%

60%

Set DTI as

40~60%

for

=<600m

Won

Other

metropolitan

area

60% 50%

40%

Introduced

DTI ceiling

as 40%

>=600m

Won

(speculative

zones)

Non-speculative

zones 50%

3 Gangnam

districts 40%

Apartment price change

Delinquency Ratio

(%)

Extended to overheated

speculative zones

Give exemption to debtors

owning less than 2 houses

until March 2011

History of DTI regulation

Down-sizing the housing sector?

Prospects of shrinking demand

A Mankiw-Weil thesis?

Income growth and cohort effect

Need to overhaul the supply system?

How to upgrade the existing stock?

Demand-supply mismatch?

Spatial

Size and quality

Coping with a rapidly aging population

Reverse mortgages in an early stage of development

Lower the portion of housing asset?

Some research questions

Explaining volatility in housing markets

price and quantity volatility

Narrowing the gap between macroeconomics and real estate economics

Macroeconomists need to appreciate the heterogeneity in real estate markets

Rear estate economists need to understand the macro-real estate linkages

Housing finance after GFC

The end of originate to distribute model?

How to secure internationally comparable data on real estate?

Availability and limitations of price indexes and quantity data

How can we explain the persistence of chonsei system in Korea?

Chonsei as a unique lease and financing mechanism

23

Explaining volatility in housing markets

Supply elasticity and volatility

Price volatility vs quantity volatility

Price stability with an elastic regime vs hangover of overbuilding

during a boom driven by irrational expectations

Market sentiments and dynamics

Predicting turning points

Mean reversion?

Momentum traders and the price-volume correlation

Pre-sale and the behavior of developers

24

Observational equivalence: Supply becoming more elastic

vs shifting inelastic supply curve

25

P2

P1

D1

S2A

S1A

Q0 Q1 Q2

P0

P

D2

S0A

Do

SB

Q

Supply elasticity and the U.S. housing bubble

The expected rate of appreciation in house prices is very sensitive to

the assumed supply elasticity.

Speculation has driven house prices well above levels that can be

justified by economic fundamentals in less than half of the cities

examined.

Establishing ‘‘30% over the expected increase” as a housing bubble

threshold, only 25 of the 84 metropolitan areas with significantly positive

supply elasticities exceed this threshold.

With the exception of Las Vegas, every single one of these areas is

either within 75 miles of the Atlantic coast or California’s Pacific coast,

suggesting that extreme speculative activity, so prominently publicized,

was extraordinarily localized.

26 Source: Goodman and Thibodeau JHE 2008

House price gain since 2000 to peak and fall from

peak

27

Source: SPCS, A year in review 2009

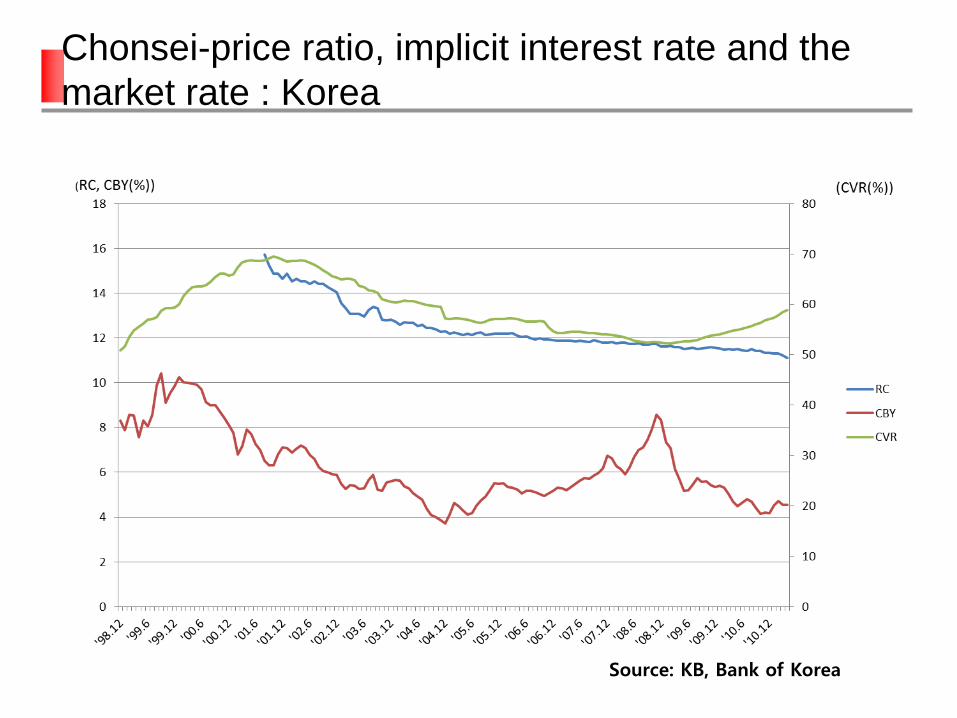

Chonsei as informal housing finance

The mechanism

The tenant pays a lump sum deposit to the landlord up front

The deposit is fully refunded at the termination of lease

It is a rental contract and a financing device at the same time.

The deposit level

The ratio between the deposit and the house value varies over time and

across locations.

The ratio is affected by the supply conditions as well as expectations about

capital gains.

A spectrum of deposit and monthly rents

Pure monthly rental contracts are rare.

Various combinations of deposit and monthly rents are available.

The implicit interest rate is much higher than market rate.

The future of chonsei? 28

Chonsei-price ratio, implicit interest rate and the

market rate : Korea

Source: KB, Bank of Korea