Embed Size (px)

Citation preview

Polarcus Limited

SECOND QUARTER REPORT 2011

2 | P o l a r c u s

SECOND QUARTER 2011 REPORT

STEADY ON THE HELM

HIGHLIGHTS

Continued growth with 5 vessels in operation

Revenue of USD 65.8 million, EBITDA of USD 16.7 million and EBIT of USD 2.9 million

Positive net cash flow from operating activities of USD 4.7 million

Solid operational performance following technical improvements in Q1

Polarcus Selma reacquired and financed through a USD 125 million convertible bond issue

Fleet backlog extended well into Q4

New build program for Polarcus Amani and Polarcus Adira on track

USD 410 million bank facility secured at attractive terms

KEY FINANCIALS

Quarter ended Six months ended Year end

30-June-11 30-June-10 30-June-11 30-June-10 2010

USD million

Revenues 65.8 24.8 113.8 35.6 122.7

Vessel operating expenses (40.7) (14.6) (76.3) (23.7) (67.1)

EBITDA 16.7 4.6 21.3 0.8 30.5

EBIT excluding impairment charges (1) 2.9 0.1 (1.9) (6.6) 3.6

Net Financial Income / (Expenses) (11.5) (3.5) (21.5) (11.6) (31.0)

Net profit / (Loss) for the period (8.2) (3.4) (23.4) (18.1) (28.3)

Basic earnings / (Loss) per share (USD) (0.02) (0.01) (0.06) (0.07) 1.00

Net cash flows from operating activities 4.74 (0.37) 4.94 (0.50) 11.7

Total assets (period end) 1,102.6 666.0 1,102.6 666.0 974.1

Total liabilities (period end) 706.8 388.6 706.8 388.6 582.5

Total Equity (period end) 395.8 277.4 395.8 277.4 391.6

Equity Ratio 36% 42% 36% 42% 40%

(1) Q4 2010 impairment of USD 1 million as a result of prepaid slot reservation fees to another shipyard for vessels 7 and

8

3 | P o l a r c u s

FINANCIAL RESULTS

Operating revenue

Revenues were USD 65.8 million in Q2 2011 compared to USD 24.8 million in Q2 2010. The increased revenue is

mainly driven by three additional vessels in operation compared to the same quarter last year. The technical

improvement program initiated and announced in Q1 2011 has led to reduced technical downtime despite

continued operations in harsh weather conditions. Repositioning of several vessels for the strong summer season

in North West Europe has resulted in 25% transit which has negatively impacted the revenues for the quarter.

EBITDA margin of 25.4% in Q2 2011 is up from 18.5% in Q2 2010.

Operating costs

Vessel operating expenses were USD 40.7 million for Q2 2011 compared to USD 14.6 million for Q2 2010. The

increased costs are due to three additional vessels being in operation compared to the same quarter last year. In

addition, operating expenses are net after deferred global transit costs for vessels repositioned during the quarter.

Sales, general and administrative costs were USD 8.4 million in Q2 2011 compared to USD 5.6 million in Q2

2010. Depreciation came to USD 13.8 million compared to USD 4.5 million in Q2 2010. The increases are a

function of expansion of the fleet and of the company.

Financial items

Net financial expenses in Q2 2011 totalled USD 11.1 million compared to USD 3.5 million in Q2 2010. Financial

costs were USD 14.0 million and financial income USD 0.4 million which were related to foreign exchange gains.

Changes to the fair value of financial instruments resulted in a gain of USD 2.6 million. This fair value change is a

non-cash item and relates to the gain on revaluation of the liability for warrants.

Since no income tax expense was recorded, the total loss for the period was USD 8.2 million.

Cash flow and liquidity

Net free cash was reduced by USD 9.3 million to USD 60.8 million during the quarter. Net cash flow from

operating activities contributed USD 4.7 million and cash flow from financing activities amounted to USD 107.8

million. Investing activities amounted to USD 121.9 million.

Net working capital increased by USD 5.8 million as a result of increased current assets of USD 26.3 million and

increased accounts payable of USD 20.9 million during the quarter. The increases are due to two additional vessels

entering into operation during the same period.

The Company raised USD 125 million from financing activities during the quarter of which USD 68.3 million was

recorded as restricted cash at the end of the period. This restricted cash will be released for payments for

equipment and instalments to the shipyard for Polarcus Selma, the sixth vessel in the Polarcus fleet, scheduled to be

delivered in Q3 2011.

Capital expenditure

Capital expenditure incurred

(In USD millions)

Q2 2011 Q2 2010 1H 2011 1H 2010 Year 2010

Seismic vessels and equipment 99.73 64.83 178.73 101.45 278.87

Other 0.04 0.98 0.12 1.15 1.51

Total 99.77 65.80 178.85 102.60 280.39

4 | P o l a r c u s

NEWBUILDING PROGRAM

In November 2010, Polarcus signed shipbuilding contracts with Ulstein Verft AS for two additional high-end 3D

seismic vessels for delivery in March and June 2012 respectively. The two new builds will be constructed to the

ULSTEIN SX134 design. The vessels will be capable of towing up to 14 streamers with 100m lateral separation

between the streamers. The total estimated project capital expenditure based on USD:NOK exchange rate of 6 is

USD 168 million per vessel, including seismic equipment but excluding capitalized interest cost.

Polarcus will after taking delivery of the three vessels currently under construction, increase the company‟s fleet to

eight vessels in 2012. The status of the new building program as of today is:

Vessel

Completion To be delivered Steel

Cut Steel

constructed Overall

construction

Polarcus Selma – 8 streamer vessel 100% 100% 97% Q3 2011

Polarcus Amani – 12-14 streamer vessel 95% 83% 43% Q1 2012

Polarcus Adira – 12-14 streamer vessel 73% 55% 12% Q2 2012

Polarcus Selma is being completed at Drydocks World Dubai with final vessel delivery scheduled for end August

2011. Polarcus Amani and Polarcus Adira are being built at Ulstein Yard and are on schedule and on budget. The

company has a separate site team overseeing the building of the vessels.

Capital investments and financing

In April 2011, Polarcus exercised the option to repurchase Polarcus Selma after raising USD 125 million in a

convertible bond issue with a coupon of 2.875% and a conversion premium of 32.5%. The reference price for the

conversion is USD 1.46.

In July 2011, Polarcus announced that the Company has signed a term sheet for a bank facility of USD 410

million with DnB NOR Bank ASA and DVB Bank SE, Nordic Branch, together with Garanti-instituttet for

Eksportkreditt (GIEK) and Eksportfinans ASA. The fleet financing bank facility will be drawn down in 5 tranches

and used to refinance existing debt related to Polarcus Alima, Polarcus Asima and Polarcus Samur and to finance the

newbuildings Polarcus Amani and Polarcus Adira.

The new financing from Eksportfinans ASA of USD 260 million for long term financing will have a fixed interest

rate of 2.85% in addition to 2.75% guarantee commission to GIEK and the commercial banks. When the bank

facility of USD 410 million is fully drawn, the average interest rate for the Group will be less than 7.5%.

The bank facility is subject to final documentation, expected to be completed by end August 2011. Polarcus Alima

and Polarcus Asima will be refinanced through the new bank facility hence, the new bank facility will be subject to

approval by bondholders in the Polarcus Alima AS USD 80 million senior secured bond issue 2010/2015 (ISIN

NO 0010590300). A summons for a bondholder meeting is expected to be issued in early August 2011.

Polarcus Samur will also be refinanced through the new bank facility. The company therefore expects to call the

Polarcus Limited 08/13 13.0% USD 55 million senior secured bond issue (ISIN NO 0010445935) within Q2/Q3

2012.

5 | P o l a r c u s

OPERATIONS

Backlog

Projects announced in Q2 2011 have extended the average fleet backlog by approximately 11 vessel months,

bringing the average fleet backlog into mid Q4 2011.

Polarcus remains well positioned to take advantage of increased activity in the industry as a result of high oil price

and increased E&P spending.

Vessel utilisation

Utilisation Q2 2011 - Vessel statistics for Q2 2011 include Polarcus Nadia, Polarcus Naila, Polarcus Asima, Polarcus Samur and Polarcus Alima for the whole quarter.

Total fleet

Exclusive seismic contracts 72%

Multi-client seismic 0%

Transit 25%

Yard stays and shakedown 3%

Vessel operations

Polarcus Nadia

Polarcus Nadia continued production in the Falkland Islands until end May and despite continued bad weather the

vessel performance significantly improved from Q1 2011. Upon project completion the vessel transited to the

North Sea where the vessel had a 7 day yard stay, communicated in the Q1 report, to rectify an issue with the

propulsion system. The yard work was successfully completed on schedule and the vessel subsequently mobilized

in the UK sector of the North Sea on 01 July for Polarcus‟ first multi-client survey.

6 | P o l a r c u s

Polarcus Naila

Polarcus Naila continued production in Namibia throughout the quarter, demonstrating excellent performance in

challenging conditions. However, a similar issue with the propulsion system as experienced by her sister vessel,

Polarcus Nadia, has been identified and will be rectified with a short yard stay in Q3 2011. The subject propulsion

system is specific only to Polarcus Nadia and Polarcus Naila.

Polarcus Asima

Polarcus Asima completed her Falkland Island survey in mid-May and transited to the North Sea where the vessel

mobilized for Statoil in mid-June.

Polarcus Samur

Polarcus Samur entered production on 08 April 2011 in Namibia after an extended shakedown due to severe

weather as previously reported in Q1. The vessel departed Namibia on 13 May after completion of 1/3 of the

project in order to meet its follow-on contract commitments in NW Europe. The vessel subsequently mobilized

for a survey campaign offshore Ireland after a brief port call in Las Palmas to resupply and effect some back deck

modifications.

Polarcus Alima

Polarcus Alima was delivered 21 March 2011 to commence operations for Reliance in India. The vessel successfully

completed the survey ahead of the monsoon and then transited to the North Sea where she has mobilized in mid-

July for Spring Energy.

ORGANISATION

During Q2 2011 the Polarcus workforce increased by 105 employees to a total of 495 by the end of the period.

The main increase related to the crewing of Polarcus Selma.

EVENTS AFTER THE QUARTER

On 21 July 2011, the company announced the signature of a term sheet for a bank loan facility of USD 410

million with DnB NOR Bank ASA and DVB Bank SE, Nordic Branch, together with Garanti-instituttet for

Eksportkreditt (GIEK) and Eksportfinans ASA. The facility is offered at attractive terms and significantly

improves the Company‟s financial position and flexibility going forward.

7 | P o l a r c u s

FINANCIAL STATEMENTS

Interim consolidated statement of comprehensive income

Quarter ended

Six months ended

Year ended

30-Jun-11 30-Jun-10

30-Jun-11 30-Jun-10

31-Dec-10

(In thousands of USD) Notes (Unaudited) (Unaudited)

(Unaudited) (Unaudited)

(Audited)

Revenues

Operating revenues

65,792 24,835

113,826 35,603

119,256

Other income

- -

- -

3,478

Total revenues

65,792 24,835

113,826 35,603

122,734

Operating expenses

Vessel operating expenses

(40,692) (14,642)

(76,250) (23,652)

(67,134)

Sales, general and administrative costs

(8,444) (5,642)

(16,313) (11,128)

(25,141)

Depreciation and amortization 10 (13,769) (4,476)

(23,124) (7,395)

(26,849)

Impairment of vessels under construction

- -

- -

(1,000)

Total operating expenses

(62,905) (24,760)

(115,686) (42,175)

(120,124)

Gross profit/(loss)

2,887 75

(1,860) (6,572)

2,610

Financial expenses

Finance costs 11 (14,038) (7,060)

(23,858) (12,798)

(31,983)

Finance income 12 428 443

587 1,984

4,594

Changes in fair value of financial instruments 13 2,551 3,095

1,736 (756)

(3,561)

Net financial expenses

(11,059) (3,522)

(21,535) (11,570)

(30,950)

Profit/(loss) for the period before tax

(8,172) (3,447)

(23,395) (18,142)

(28,340)

Income tax expense

- -

(1) -

-

Total comprehensive income/(loss)

(8,172) (3,447)

(23,396) (18,142)

(28,340)

Profit/(Loss) per share for loss attributable to the equity holders during the period (In USD)

- Basic

(0.020) (0.013)

(0.057) (0.069)

(0.100)

- Diluted

(0.025) (0.023)

(0.058) (0.069)

(0.100)

8 | P o l a r c u s

Interim consolidated balance sheet

30-Jun-11 30-Jun-10

31-Dec-10

(In thousands of USD) Notes (Unaudited) (Unaudited)

(Audited)

ASSETS

Non Current Assets

Property, plant and equipment 3 749,100 315,765

478,544

Vessels under construction 4 107,114 205,661

200,531

Vessels buyback options

- 40,831

19,907

Vessel prepayments 4 28,060 -

28,060

Intangible assets

832 4,288

2,633

Total Non Current Assets

885,105 566,544

729,675

Current Assets

Prepaid expenses

1,500 3,572

2,440

Other current assets

36,707 14,256

26,052

Restricted cash - short term

89,611 33,344

110,749

Cash and bank

60,768 43,266

86,836

Accounts receivable

28,918 5,027

18,357

Total Current Assets

217,504 99,465

244,435

TOTAL ASSETS

1,102,609 666,010

974,110

EQUITY and LIABILITIES

Equity

Issued share capital 5 8,194 5,264

8,194

Share premium

423,737 303,612

423,822

Other reserves

37,040 8,116

9,308

Retained earnings/(loss)

(73,158) (39,564)

(49,762)

Total Equity

395,812 277,428

391,563

Non Current Liabilities

Senior secured bonds 6 131,273 53,665

130,850

Convertible bonds 7 127,977 30,681

31,269

Long-term finance lease 8 183,413 195,564

194,407

Other long-term debt 9 117,235 5,300

72,953

Liability for warrants 5, 13 5,032 3,963

6,768

Employee pension accrual

402 1,104

292

Total Non Current Liabilities

565,332 290,277

436,540

Current Liabilities

Interest payable

9,146 3,950

8,766

Employee accruals and payables

4,102 3,598

6,586

Other accrued expenses

9,279 7,062

7,166

Deferred payments to vendors 14 40,960 29,138

59,874

Long-term finance lease current portion 8 25,348 16,918

22,388

Other long-term debt current portion 9 15,296 4,502

10,936

Accounts payable

37,333 33,138

30,291

Total Current Liabilities

141,465 98,305

146,008

TOTAL EQUITY and LIABILITIES

1,102,609 666,010

974,110

9 | P o l a r c u s

Interim consolidated statement of cash flows

Quarter ended

Six months ended

Year ended

30-Jun-11 30-Jun-10

30-Jun-11 30-Jun-10

31-Dec-10

(In thousands of USD) (Unaudited) (Unaudited)

(Unaudited) (Unaudited)

(Audited)

Cash flows from operating activities

Profit/(loss) for the period before tax (8,172) (3,447)

(23,396) (18,142)

(28,341)

Adjustment for:

Depreciation 13,769 4,476

23,124 7,395

26,849

Impairment of vessels under construction - -

- -

1,000

Changes in fair value of financial instruments (2,551) (3,095)

(1,736) 756

3,561

Stock Options compensation provision 508 516

1,128 861

2,053

Interest expense 6,974 4,475

17,266 11,242

26,844

Interest income (17) (28)

(43) (73)

(157)

Working capital adjustments:

Decrease/(Increase) in current assets (26,251) (9,126)

(20,276) (7,411)

(31,406)

Increase in trade and other payables and accruals 20,477 5,862

8,875 4,877

11,337

Net cash flows from operating activities 4,737 (366)

4,943 (495)

11,741

Cash flows from investing activities

Decrease/(Increase) in restricted cash (73,086) 3,504

21,138 3,181

(74,224)

Purchases of property, plant and equipment (48,770) (36,926)

(188,799) (73,924)

(207,621)

Payments to acquire intangible assets (33) (183)

(115) (211)

(443)

Interest income - 3

- 3

10

Net cash flows used in investing activities (121,888) (33,601)

(167,776) (70,950)

(282,278)

Cash flows from financing activities

Proceeds from the issuance of ordinary shares - -

- -

129,672

Transaction costs on issue of shares - 29

(85) 29

(6,503)

Proceeds from the issuance of senior secured bonds - -

- -

76,929

Proceeds from the issuance of convertible bonds 125,000 -

125,000 -

-

Receipt from sale lease-back fund - -

- 22,255

22,255

Receipt from loans -

53,695

76,081

Repayment of lease liabilities (4,897) (2,967)

(10,306) (5,652)

(14,904)

Repayment of other long-term debt (1,159) (1,069)

(5,422) (1,775)

(3,981)

Interest paid (11,141) (4,475)

(26,159) (15,543)

(37,660)

Interest income 17 28

43 73

157

Net cash flows from financing activities 107,820 (8,453)

136,765 (613)

242,049

Net increase/(decrease) in cash and cash equivalents

(9,331) (42,420)

(26,068) (72,058)

(28,487)

Cash and cash equivalents at the beginning of the period

70,100 85,686

86,836 115,323

115,323

Cash and cash equivalents at the end of the period

60,768 43,266

60,768 43,266

86,836

10 | P o l a r c u s

Interim consolidated statement of changes in equity

(In thousands of USD except for number of shares)

Number of Shares

Issued Share capital

Share Premium

Other Reserves

Retained Earnings/

(Loss)

Total Equity

Balance as at 31 December 2009 263,174,820 5,264 303,583 7,255 (21,422) 294,680

Total comprehensive income/(loss) for the period

- - - (28,340) (28,340)

Employee stock options provision

- - 2,053 - 2,053

Issue of share capital

19 October 2010 at NOK 5.15 (USD 0.90) per share 67,421,359 1,348 59,063 - - 60,411

24 November 2010 at NOK 5.30 (USD 0.93) per share 73,400,000 1,468 62,876 - - 64,344

21 December 2010 at NOK 5.15 (USD 0.86) per share 5,700,000 114 4,803 - - 4,917

Transaction costs on issue of shares

- (6,503) - - (6,503)

Balance as at 31 December 2010 409,696,179 8,194 423,822 9,308 (49,762) 391,563

Total comprehensive income/(loss) for the period

- - - (23,396) (23,396)

Transaction costs on issue of shares

- (85) - - (85)

Issue of convertible bonds

- - 26,604 - 26,604

Employee stock options provision

- - 1,128 - 1,128

Balance as at 30 June 2011 409,696,179 8,194 423,737 37,040 (73,158) 395,812

11 | P o l a r c u s

Notes to the interim consolidated financial statements

1. General information

The interim condensed consolidated financial statements of Polarcus Limited (the “Company”) and its subsidiaries

(together the “Group”) for the half year ended 30 June 2011 were authorized for issue in accordance with a

resolution of the Board of Directors on 25 July 2011.

Polarcus Limited is a pure play marine geophysical company with a pioneering environmental agenda, specializing

in high-end towed streamer data acquisition from Pole to Pole.

Polarcus Limited was incorporated on 17 December 2007 in the Cayman Islands with its registered office at

Walker House, 87 Mary Street, George Town, Grand Cayman, Cayman Islands. The Group has its main

administration office in Dubai, United Arab Emirates which is the domicile of the Group.

The Group has five high end 3D vessels, Polarcus Nadia, Polarcus Naila, Polarcus Asima, Polarcus Samur and Polarcus

Alima that are currently operational. A sixth vessel Polarcus Selma is expected to be delivered in Q3 2011.

Shipbuilding contracts have been signed for a further two vessels, Polarcus Amani and Polarcus Adira, with delivery

in the first half of 2012.

1.1 Financing

Due to global economic conditions at the time, the Company in July 2009 carried out a restructuring of the

Group. Under the restructuring the Company sold two of its vessel owning subsidiaries, Polarcus 4 owning the

vessel Polarcus Selma and Polarcus 6 owning the vessel Polarcus Alima to Zickerman Holding Limited and

Zickerman Group Limited (together “ZL”) for a consideration of USD 1 each per vessel. ZL carried, after the

transaction, all financial obligations related to Polarcus 4 and Polarcus 6. The Group had an option to repurchase

each of Polarcus Selma and Polarcus Alima at a price equal to the remaining cost of completing each vessel.

In October 2010, Polarcus exercised the option to repurchase Polarcus Alima after raising USD 200 million in new

capital comprising USD 65 million in equity, placed at NOK 5.15 (USD 0.90), a USD 80 million bond with a

coupon of 12.50% and a USD 55 million bank loan facility with an average interest rate of approximately 5%.

In April 2011, Polarcus exercised the option to repurchase Polarcus Selma after raising USD 125 million in a

convertible bond with a coupon of 2.875% and a conversion premium of 32.5%. The reference price for the

conversion is USD 1.46.

In November 2010 Polarcus signed shipbuilding contracts for two additional high-end 3D seismic vessels for

delivery in the first half of 2012. To partly finance the new vessels' total estimated project capital expenditure of

USD 168 million per vessel the company raised USD 65 million of equity at NOK 5.30 (USD 0.93) in a private

placement.

In July 2011 Polarcus announced that the Company has signed a term sheet for a bank facility of USD 410 million

with DnB NOR Bank ASA and DVB Bank SE, Nordic Branch, together with Garanti-instituttet for

Eksportkreditt (GIEK) and Eksportfinans ASA. The fleet financing bank facility will be drawn down in 5 tranches

and used to refinance existing debt related to Polarcus Alima, Polarcus Asima and Polarcus Samur and to finance the

newbuildings Polarcus Amani and Polarcus Adira.

The Company will take advantage of the USD 260 million proposals from Eksportfinans ASA for long term

financing of Polarcus Amani and Polarcus Adira at a fixed interest rate of 2.85% in addition to 2.75% guarantee

commission to GIEK and the commercial banks. When the bank facility of USD 410 million is fully drawn, the

average total interest rate for the eight vessel fleet will be less than 7.5%.

The bank facility is subject to final documentation, expected to be completed before the end of August 2011. As

Polarcus Alima and Polarcus Asima will be included in the fleet security structure, the new bank facility will be

subject to approval by bondholders in the Polarcus Alima AS USD 80 million senior secured bond issue

2010/2015 (ISIN NO 0010590300). A summons for bondholder meeting is expected to be issued early August

2011.

12 | P o l a r c u s

As Polarcus Samur will be included in the bank facility the Company expects to call the Polarcus Limited 08/13

13% USD 55 million senior secured bond issue (ISIN NO 0010445935) within Q2/Q3 2012.

The going concern assumption

These interim condensed consolidated financial statements are presented based on the going concern assumption

under International Financial Reporting Standards.

2. Significant Accounting Policies

These interim condensed consolidated financial statements for the period ended 30 June 2011 have been prepared

in accordance with IAS 34 Interim Financial Reporting. They do not include all the information required for full

annual financial statements and should be read in conjunction with the audited consolidated financial statements

of the Group for the year ended 31 December 2010.

The accounting policies applied by the Group in these interim condensed consolidated financial statements are

consistent with those applied in the audited consolidated financial statements for the year ended 31 December

2010 unless otherwise stated. Refer to Note 2 Summary of Significant Accounting Policies to the Consolidated Financial

Statements in the 2010 Annual Report for information on the Company‟s accounting policies.

3. Property, Plant and Equipment

(In thousands of USD)

Seismic vessels and equipment

Furniture and fixtures

Office and IT equipment

Total

Costs

Balance as of 1 January 2011 496,967 1,636 708 499,311

Additional capital expenditures 291,942 4 - 291,946

Assets under finance leases 1,519 - - 1,519

Disposals (1,451) (1) - (1,452)

Balance as of 30 June 2011 788,976 1,639 708 791,323

Depreciation and impairment losses

Balance as of 1 January 2011 20,085 376 306 20,767

Depreciation for the period 21,364 194 72 21,629

Disposals (173) - - (173)

Balance as of 30 June 2011 41,276 569 379 42,223

Carrying amounts

As of 1 January 2011 476,882 1,260 402 478,544

As of 30 June 2011 747,700 1,070 329 749,100

Carrying amounts held under finance lease as of 30 June 2011

265,942 - - 265,942

On 3 March 2011, the Group took delivery of Polarcus Samur. The cost of the vessel incurred up to delivery was

USD 133.08 million. Polarcus Samur is pledged as security for a 13% interest bearing senior secured bond and

interest accrued thereon. Also refer to Note 4 Vessels under construction and Note 6 Senior secured bonds.

On 21 March 2011, the Group took delivery Polarcus Alima. The cost of the vessel incurred up to delivery was

USD 140.03 million. Polarcus Alima has been pledged as a 1st priority security towards a USD 80 million loan

facility and a USD 55 million loan facility together with Polarcus Asima.

13 | P o l a r c u s

Polarcus Alima and Polarcus Asima are pledged as a 2nd priority security for a 12.5% interest bearing senior secured

bond and interest accrued thereon. Also refer to Note 4 Vessels under construction and Note 6 Senior secured bonds.

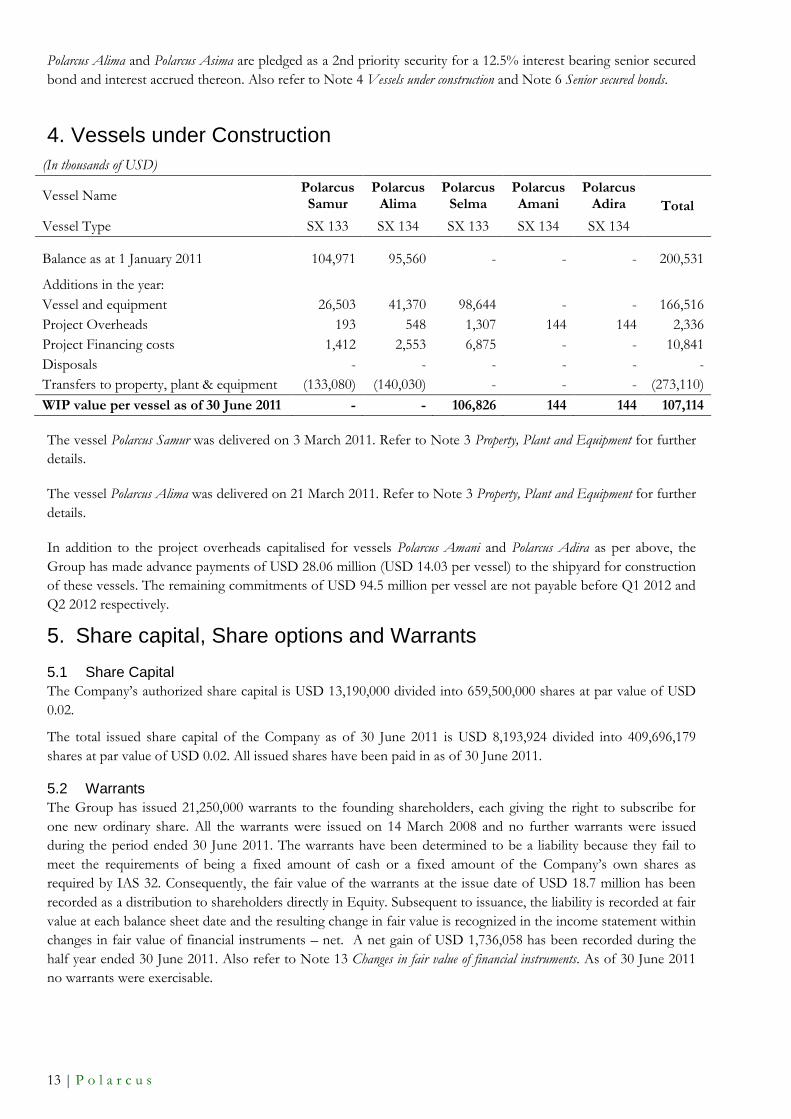

4. Vessels under Construction

(In thousands of USD)

Vessel Name Polarcus Samur

Polarcus Alima

Polarcus Selma

Polarcus Amani

Polarcus Adira Total

Vessel Type SX 133 SX 134 SX 133 SX 134 SX 134

Balance as at 1 January 2011 104,971 95,560 - - - 200,531

Additions in the year:

Vessel and equipment 26,503 41,370 98,644 - - 166,516

Project Overheads 193 548 1,307 144 144 2,336

Project Financing costs 1,412 2,553 6,875 - - 10,841

Disposals - - - - - -

Transfers to property, plant & equipment (133,080) (140,030) - - - (273,110)

WIP value per vessel as of 30 June 2011 - - 106,826 144 144 107,114

The vessel Polarcus Samur was delivered on 3 March 2011. Refer to Note 3 Property, Plant and Equipment for further

details.

The vessel Polarcus Alima was delivered on 21 March 2011. Refer to Note 3 Property, Plant and Equipment for further

details.

In addition to the project overheads capitalised for vessels Polarcus Amani and Polarcus Adira as per above, the

Group has made advance payments of USD 28.06 million (USD 14.03 per vessel) to the shipyard for construction

of these vessels. The remaining commitments of USD 94.5 million per vessel are not payable before Q1 2012 and

Q2 2012 respectively.

5. Share capital, Share options and Warrants

5.1 Share Capital

The Company‟s authorized share capital is USD 13,190,000 divided into 659,500,000 shares at par value of USD

0.02.

The total issued share capital of the Company as of 30 June 2011 is USD 8,193,924 divided into 409,696,179

shares at par value of USD 0.02. All issued shares have been paid in as of 30 June 2011.

5.2 Warrants

The Group has issued 21,250,000 warrants to the founding shareholders, each giving the right to subscribe for

one new ordinary share. All the warrants were issued on 14 March 2008 and no further warrants were issued

during the period ended 30 June 2011. The warrants have been determined to be a liability because they fail to

meet the requirements of being a fixed amount of cash or a fixed amount of the Company‟s own shares as

required by IAS 32. Consequently, the fair value of the warrants at the issue date of USD 18.7 million has been

recorded as a distribution to shareholders directly in Equity. Subsequent to issuance, the liability is recorded at fair

value at each balance sheet date and the resulting change in fair value is recognized in the income statement within

changes in fair value of financial instruments – net. A net gain of USD 1,736,058 has been recorded during the

half year ended 30 June 2011. Also refer to Note 13 Changes in fair value of financial instruments. As of 30 June 2011

no warrants were exercisable.

14 | P o l a r c u s

5.3 Stock Options

The Group has granted share options to executive management and other selected employees. As of 30 June 2011

the Group has issued 13,700,000 options of which 3,041,000 were issued during the half year ended 30 June 2011.

The total fair value of options granted up to 30 June 2011 is USD 9.30 million calculated using the Black-Scholes

model, assuming all options will be exercised. During the half year ended 30 June 2011, the Group has expensed

USD 1,127,800 towards stock options granted as employee compensation. Number of options exercisable as of 30

June 2011 were 4,942,133 however none of them were exercised.

6. Senior Secured Bonds

On 30 July 2008, the Company issued 550 senior secured callable bonds at par value of USD 100,000 each,

totalling USD 55 million, bearing interest of 13% per annum. The net proceeds of the issue were employed to

part-finance the construction of the vessel Polarcus Samur through the vessel owning company Polarcus Samur Ltd

(formerly known as Polarcus 3 Ltd). The interest for this loan is payable semi-annually in arrears on 30 January

and 30 July each year. The bonds will mature five years from the date of issue at their nominal value. On the date

of the issue, net proceeds of USD 53,075,000 have been accounted under Non-current liabilities.

On 27 October 2010, the Group issued 800 senior secured callable bonds at par value of USD 100,000 each,

totalling USD 80 million, bearing an interest of 12.5% per annum. The net proceeds of the issue were employed to

part-finance the construction of the vessel Polarcus Alima through the vessel owning company Polarcus 6 Ltd. The

interest for this loan is payable semi-annually in arrears on 29 April and 29 October each year. The bonds will

mature five years from the date of issue at their nominal value. On the date of issue, net proceeds of USD

76,929,481 were accounted under Non-current liabilities.

The balance sheet value of the above two loans are as below;

(In thousands of USD) 30-Jun-11 30-Jun-10

31-Dec-10

13% Senior secured callable bonds 54,039 53,665

53,846

12.5% Senior secured callable bonds 77,234 -

77,004

Total 131,273 53,665

130,850

15 | P o l a r c u s

7. Convertible Bonds

On 30 July 2008 the Company had issued 350 subordinated unsecured callable convertible bonds at a par value of

USD 100,000 each totalling USD 35 million, bearing 8.5% interest per annum. The interest is payable semi-

annually in arrears on 30 January and 30 July each year. The bonds mature five years from issue date at their

nominal value of USD 35 million or can be converted into a total of 10,802,470 shares at the holders‟ option at a

conversion price of USD 3.24 per share. The conversion price is subject to adjustment upon certain changes of

the Company‟s share capital and in case of mergers and de-mergers.

On 27 April 2011 the Company issued 1250 senior secured convertible bonds at par value of USD 100,000 each

totalling USD 125 million, bearing 2.875% interest per annum. The interest is payable semi-annually in arrears on

27 April and 27 October each year. The bonds mature five years from issue date at their nominal value of USD

125 million or can be converted into a total of 64,616,180 shares at the holders‟ option at a conversion price of

USD 1.9345 per share. The conversion price is subject to adjustment upon certain changes of the Company‟s

share capital and in case of mergers and de-mergers.

The convertible bonds have been accounted for in separate components – the value of the liability component has been recognized at its fair value and the remaining part as equity. In measuring fair value of the liability component, an estimated market rate for a similar debt without a conversion right has been used in discounting the cash flow under the loan agreement. The estimated market rate was based on valuations of the interest rate for a non-convertible bond at the date of drawing the loan. There will be no re-measuring of the fair value of the liability and equity components.

At the issue dates, the following amounts were recognized in the financial statements for each of the above bond loans;

(In thousands of USD)

8.5% Unsecured bonds 2.875% Secured bonds

Fair value of liability component 28,751 95,271

Fair value of equity component 5,024 26,604

Net proceeds on the issue dates 33,775 121,875

The equity component of convertible bonds as per above are included in the „Other reserves‟ in the balance sheet. The liability component of the above two loans are as below;

(In thousands of USD) 30-Jun-11 30-Jun-10

31-Dec-10

8.5% Subordinated unsecured convertible bonds 31,897 30,681

31,269

2.875% Senior secured convertible bonds 96,080 -

-

Total 127,977 30,681

31,269

16 | P o l a r c u s

8. Long-term Finance Lease

Upon delivery from the shipyard, the vessels Polarcus Nadia and Polarcus Naila were sold to GSH2 Seismic Carrier I

AS (the „lessor‟) according to the sale and lease-back financing arrangement entered into on 30 June 2008 as

amended on 29 July 2009. The purchase price of USD 90 million each per vessel (total USD 180 million) is fully

paid by the lessor to the Group in instalments throughout the vessel construction period. Immediately upon the

sale of the vessels, the Group leased back the vessels from the lessor at a fixed charter rate of USD 35,000 per day,

payable in arrears throughout the duration of the charter period. This arrangement falls under the category of

finance lease as described under IAS 17. Accordingly at the inception of the lease USD 180 million has been

recorded as a liability.

The Company has entered into lease agreements with Sercel Inc, Houston to acquire marine acquisition

equipment (the “streamer systems”). The duration of each lease is 30 months and the Company has an option to

purchase the streamer systems at any time during the lease period. As of 30 June 2011, streamer systems worth

USD 56,166,181 were leased under this arrangement.

The outstanding liability under the above mentioned arrangements are disclosed in the Group‟s balance sheet as

„Long-term finance lease‟ which is further classified into long-term and short-term portions as below;

(In thousands of USD) 30-Jun-11 30-Jun-10

31-Dec-10

Lease payments due after 12 months from the balance sheet date 183,413 195,564

194,407

Lease payments due within 12 months from the balance sheet date 25,348 16,918

22,388

Total 208,761 212,482

216,795

9. Other Long-term Debt

The Group on 14 September 2009 entered into a facility agreement with Eksportfinans ASA and DVB Bank SE

for a USD 80 million loan facility. The Eksportfinans tranche of the facility (USD 55 million) relates to financing

of Norwegian equipment on-board the vessels Polarcus Samur and Polarcus Asima. This has been guaranteed by the

Norwegian Guarantee Institute for Export Credits (GIEK). The DVB Bank tranche (USD 25 million) relates to

financing of the vessel Polarcus Asima. The vessel Polarcus Asima was pledged as security for this loan facility. The

facility was drawn on 31 August 2010 post delivery of the vessel Polarcus Asima from the shipyard. As of 30 June

2011 the Group has repaid USD 3,125,000 against liability under this loan facility.

A similar loan facility of USD 55 million was entered into in January 2011 and was drawn on 21 March 2011 post

delivery of Polarcus Alima. The Eksportfinans tranche of the facility (USD 33 million) relates to financing of

Norwegian equipment on-board the vessels Polarcus Alima which has been guaranteed by the Norwegian

Guarantee Institute for Export Credits (GIEK). The DVB Bank tranche (USD 22 million) relates to financing of

the vessel Polarcus Alima. The vessels Polarcus Asima and Polarcus Alima have been pledged as security for this loan

facility.

The Company has acquired some of its streamer systems from Sercel Inc, Houston by way of a 40% down

payment. The remaining 60% of the purchase price is payable through 36 monthly instalments including interest

at 8% per annum. The affected streamer system has been pledged as security for this arrangement. The total value

of equipment acquired under this arrangement is USD 22,631,523. As of 30 June 2011, the Company has paid

USD 17,331,977 against its liability under this arrangement. The net outstanding liability at the period end is USD

5,299,546.

The outstanding liability under the above mentioned arrangements is disclosed in the Group‟s balance sheet as

„Other long-term debt‟ which is further classified in to long-term and short-term portions as per below;

(In thousands of USD) 30-Jun-11 30-Jun-10

31-Dec-10

Installments due after 12 months from the balance sheet date 117,235 5,300

72,953

Installments due within 12 months from the balance sheet date 15,296 4,502

10,936

Total 132,531 9,802

83,889

17 | P o l a r c u s

18 | P o l a r c u s

10. Depreciation and Amortization

(In thousands of USD)

Quarter ended

Six months ended

Year ended

30-Jun-11 30-Jun-10

30-Jun-11 30-Jun-10

31-Dec-10

Depreciation of seismic vessels and equipment 12,762 4,269

21,364 7,085

22,317

Depreciation of office equipment 132 64

265 125

368

Amortization of intangible assets 108 87

216 128

314

Disposal of office equipment - 57

- 57

57

Disposal of seismic equipment 767 -

1,278 -

3,793

Total 13,769 4476

23,124 7395

26,849

11. Finance Costs (In thousands of USD)

Quarter ended

Six months ended

Year ended

30-Jun-11 30-Jun-10

30-Jun-11 30-Jun-10

31-Dec-10

Interest expenses on senior secured bond 4,503 1,873

8,998 3,744

9,235

Interest expenses on convertible bond 2,469 1,022

3,523 2,038

4,114

Interest expenses on deferred payments to the shipyard

312 508

329 985

3,773

Interest expenses on lease arrangements 6,034 6,509

12,101 11,887

22,629

Other interest expenses 2,031 1,282

4,019 1,866

7,348

Interest expenses capitalized to vessels under construction

(1,720) (4,467)

(6,050) (8,724)

(18,651)

Net interest expenses 13,629 6,727

22,920 11,796

28,447

Realized currency exchange loss 409 43

891 385

1,373

Unrealized currency exchange loss - 290

47 617

1,587

Other financial losses - -

- -

576

Total 14,038 7,060

23,858 12,798

31,983

12. Finance Income (In thousands of USD)

Quarter ended

Six months ended

Year ended

30-Jun-11 30-Jun-10

30-Jun-11 30-Jun-10

31-Dec-10

Interest income from deposit with banks 18 31

43 76

167

Interest income offset against capitalized interest expenses

- (3)

- (3)

(10)

Net interest income 18 28

43 73

157

Realized exchange gain 228 386

248 1,838

2,669

Unrealized exchange gain 172 29

286 73

1,768

Other financial income 10 -

10 -

-

Total 428 443

587 1,984

4,594

The realized currency gain or loss represents the effect of foreign currency payments made and the unrealized

currency gain or loss represents the effect of revaluation of foreign currency financial assets other than those

treated as cash flow hedging instruments.

19 | P o l a r c u s

13. Changes in Fair value of Financial Instruments

The changes in fair value of financial instruments represent the profit or loss on revaluation of liabilities on

warrants issued. Also refer to Note 5.2 Warrants. The fair value of the warrant liability at each balance sheet date

and the profit or loss on revaluation for the periods reported are as per below;

(In thousands of USD)

Quarter ended

Six months ended

Year ended

30-Jun-11 30-Jun-10

30-Jun-11 30-Jun-10

31-Dec-10

Warrant liability at fair value on the balance sheet dates

5,032 3,963

5,032 3,963

6,768

Profit/(loss) on revaluation of the fair value of warrant liability

2,551 3,095

1,736 (756)

(3,561)

14. Transactions with Related Parties

Zickerman Holding Limited and Zickerman Group Limited (together “ZL”) hold 13.61% of the paid-in share

capital of the Company as of 30 June 2011. In April 2011, the Company exercised the option of repurchasing

Polarcus Selma from ZL. The Company paid USD 3.5 million to ZL towards the purchase price of shares in

Polarcus Selma Ltd (formerly known as „Polarcus 4 Ltd‟), owning the rights to vessel Polarcus Selma. Also refer to

Note 1.1 Financing.

Drydocks World Dubai (“DWD”) holds 9.15% of the paid-in share capital of the Company as of 30 June 2011.

Below is a summary of major transactions between DWD and the Group during the half year ended 30 June 2011;

(In thousands of USD)

Payments made under ship building contracts 29,960

Payments made under the deferred payment arrangement 81,012

Financing costs paid 6,710

Total payments made during the half year ended 30 June 2011 117,681

Payments due as of 30 June 2011 included in Accounts payable 4,535

Payments due under the deferred payment arrangement 40,960

Total payments due as of 30 June 2011 45,495

There were no major transactions with other related parties during the half year ended 30 June 2011.

15. Subsequent Events

On 21 July 2011, the company announced the signature of a term sheet for a bank loan facility of USD 410

million with DnB NOR Bank ASA and DVB Bank SE, Nordic Branch, together with Garanti-instituttet for

Eksportkreditt (GIEK) and Eksportfinans ASA. The facility is offered at attractive terms and significantly

improves the Company‟s financial position and flexibility going forward.

20 | P o l a r c u s

Statement pursuant to Section 5-6 of the Securities Trading Act

We confirm that, to the best of our knowledge, the condensed set of financial statements for the first half of 2011

which has been prepared in accordance with IAS 34 Interim Financial Reporting gives a true and fair view of the

Company‟s consolidated assets, liabilities, financial position and results of operations, and that the interim report

includes a fair review of the information under the Norwegian Securities Trading Act section 5–6 fourth

paragraph.

To the best of our knowledge, this report gives:

a true and fair overview of important events that occurred during the accounting period and their impact on the half-yearly financial statements

(together with Note 3. Financial Risk Management and the Board of Directors Report section 8. Risk, both in the Group‟s 2010 Annual Report) a true and fair description of the principal risks and uncertainties facing the Group over the next accounting period and

a true and fair description of major transactions with related parties

Dubai, 25 July 2011

The Board of Directors of Polarcus Limited

Peter Martin Rigg Tore Karlsson

Chairman Vice-Chairman

(Sign.)

Ali A. bin Towaih Al Suwaidi Hege Sjo Carl Gustav Zickerman

(Sign.)

Katherine (Martin) Hall Mohammad Rizal Bin Abdullah Jogeir Romestrand

Carl Peter Zickerman

Rolf Ronningen

Chief Executive Officer

Tom Henrik Sundby

Chief Financial Officer