-

8/2/2019 POB SME Review Update December 2007

1/3

1

PROFESSIONAL OVERSIGHT BOARD

REVIEW OF HOW ACCOUNTANTS SUPPORT THE NEEDS OF SMALL AND

MEDIUM-SIZED

COMPANIES AND THEIR STAKEHOLDERS

UPDATE - DECEMBER 2007

Introduction

The Financial Reporting Council (FRC) aims to strengthen

confidence in corporate reporting and governance.

One way in which the Professional Oversight Board (POB), an

operating body of the FRC, contributes to this aim

is by seeking to increase the extent to which clients of

professionally qualified accountants can rely on them to

act with integrity and competence.

In March 2006, the POB published the findings of its review of

how professional accountants work with small

companies and medium-sized companies and their stakeholders. The

POB decided to undertake the reviewhaving considered the overall

importance of this sector and the significant changes made in

recent years to the

financial accounting and reporting arrangements for these

companies, including the significant take-up of audit

exemptions (see diagram below). The review focused on the extent

to which directors of small companies and

users of their accounts rely on professionally qualified

accountants to act with integrity and competence.

The review was based on research including surveys of the views

of 600 companies and 1,250 accountants and

other business advisers. The POB met with around 25 small

professional accountancy practices nominated by

the bodies, as well as members of the AAT, IFA, and the

Institute of Certified Bookkeepers, and general business

advisers. In addition 350 sets of accounts of small and

medium-sized companies filed at Companies House were

reviewed by the POB together with the professional accountancy

bodies.

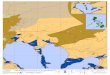

Annual accounts registered at Companies House by type, 2001-02

to 2005-06

0

200

400

600

800

1000

1200

1400

2001-02 2002-03 2003-04 2004-05 2005-06

Annualaccountsregistered

Audited

Not audited

Source: Department of Trade and Industry, Companies in 200506.

Excludes dormant companies.

-

8/2/2019 POB SME Review Update December 2007

2/3

2

Progress in implementing the recommendations

Clarifying the role of professional accountants tousers of

unaudited accountsThe Review found that individuals and

companies

who are considering doing, or are already doing,business with

small companies whose accounts arenot audited are often unclear

over the role ofprofessional accountants in the preparation of

theseaccounts.

Very few sets of accounts on the public recordinclude a report

describing the involvement of theaccountant. Although the

professional accountancybodies provide guidelines to their members

on acompilation service and the use of a compilationreport, the

guidelines vary between the bodies.

Much of the content of these reports is in the formof negative

statements which describe thelimitations of the work undertaken.

Furthermore,some bodies have recommended that the reportsare not

attached to the accounts sent to CompaniesHouse.

To help users of non-audited accounts, the POBrecommended that

the bodies should work togetherto provide a clear explanation of

the extent andrelevance of the involvement of

professionalaccountants in the preparation of accounts. ThePOB

suggested that this should be achievedthrough a cross-profession

report for non-auditedaccounts that includes a very broad

description ofthe scope of engagement of the professionalaccountant

together with a positive description ofthe accountants professional

obligations.

Under their codes of ethics, professionalaccountants are

required not to be associated withaccounts where they believe the

information tocontain a materially false or misleading statementor

statements or information furnished recklessly.They are also

required to maintain their

professional knowledge and skill at the levelrequired to ensure

that clients receive competentprofessional service. These powerful

statements, thePOB noted, could be more clearly communicated tohelp

ensure they are recognised by directors andusers of their

accounts.

The use of the cross-profession report for non-audited accounts

would need to be supported bynew and more secure arrangements for

reportingthe involvement of professional accountants whenaccounts

are filed electronically at Companies

House.

The bodies, through the Consultative Committee ofAccountancy

Bodies (CCAB), set up a workinggroup to consider a cross-profession

report for non-

audited accounts. However, in consulting theirmembers, the

bodies found concerns anduncertainty over the benefits that such a

reportwould deliver to them or their clients. The POB willaccept

invitations to participate in furtherdiscussions with the bodies

and practitioners toexplore these issues and, in association with

otherparts of the FRC, could, if helpful to the bodies,provide more

direct guidance.

The POB considers that further work is needed to explainthe

extent and relevance of the involvement of

professional accountants in non-audited accounts. Theprofession

should not be over-cautious in explaining theeffort taken by its

members as a matter of course to

provide competent professional services and to ensurethat

accounts are of high quality.

The CCAB has also met several times withCompanies House and

reports a good level ofagreement on the key areas needing

development.However, since the POB report was published,electronic

filing of accounts has been introduced ina way that shows no

evidence of the involvement of

accountants. This compares to paper filing wherethe name of the

accountant is often provided.

The POB considers that the CCAB should continue towork with

Companies House to find a way of disclosingclearly on the public

record the involvement of

professional accountants in the preparation of

unauditedaccounts, including those filed electronically.

In September 2006, the ICAEW launched aconsultation exercise to

explore the financialinformation requirements and assurance needs

of

businesses that fall below the statutory auditthreshold.

Alongside this, the ICAEW launched anew assurance service that

chartered accountantscan offer clients who would like an

independentreport on their annual accounts.

The POB notes that it is yet to be established whetherthere is a

need for an assurance service in the gapbetween professional

accountants standard accounts

preparation services and audit. Improved clarity over therole of

professional accountants in the preparation ofnon-audited accounts

is necessary before this can be fullyexplored.

-

8/2/2019 POB SME Review Update December 2007

3/3

3

Ensuring that there is substance behind thedescription of the

role of professional accountants

The Review found that a sizeable minority ofaccounts filed on

paper at Companies House,

including those prepared with the involvement ofprofessional

accountants, included technical issues,errors or other evidence of

a lack of care inpreparation. The POB recommended that the

bodiesshould take steps (including those they hadproposed) to help

improve the quality of financialaccounts which have the involvement

of theirmembers. The bodies were asked to report formallyto POB on

the effectiveness of these steps in April2007.

The bodies have taken steps, including publicising

the problems, providing guidance to their membersand assessing

the quality of accounts during qualitycontrol visits. Bodies

reported that more time isneeded before they can measure the

effectiveness ofthese steps.

To help ensure that there is substance behind theexplanation of

the role of professional accountants, thePOB considers that the

professional bodies shouldcontinue their work to improve the

quality of accounts

prepared with their members input. The POB wouldexpect them to

be able to measure the effectiveness of the

measures by Spring 2008.

Helping directors of small companies to assess theirneed for

support from professional accountants

The Review found that some directors of smallcompanies were

unclear over the options availableto them for their financial

reporting and how theycan obtain help with it.

Following the introduction of audit exemption,directors of most

small companies were now free tochoose different types of

accountancy advisers.

Some directors did not know whether their adviserswere

professional accountants or why this might beimportant. This may

reflect a shortage of suitablyqualified bookkeepers, which can

result inprofessional accountants carrying out

routinerecord-keeping work for their clients.

Some company directors were filing abbreviatedaccounts at

Companies House without a fullunderstanding of the commercial

implications of

this choice. Many directors were also unclearwhether they are

filing audited or unauditedaccounts. Some appeared not to be aware

thatcertain user groups, particularly credit managers,may look for

an audit and may be more cautious inthe absence of it.

Some directors appeared not to appreciate the valueof good

financial information. These directors donot look for support in

understanding orinterpreting financial information, often

seeaccounting merely as a regulatory burden and maynot have good

financial information to inform theirdecision making.

The POB recommended that the professional bodieswork together to

explain the role of professionalaccountants to directors of small

companies. ThePOB also recommended that the bodies should

alsoexplain to directors their options in respect of

filingabbreviated or full accounts, having the accountsaudited, and

using accounting information toachieve good financial

management.

The bodies drew attention to their publications and

other initiatives which provide these explanationsto directors

of small companies. One suggested thatgeneral information campaigns

of a scale necessaryto increase awareness amongst company

directorsare beyond the combined budgets of theaccountancy bodies.

Several bodies suggested thatstatutory recognition of the term

accountantwould help directors to better understand the roleof

professional accountants.

The POB considers that the bodies should workcollectively rather

than individually to more effectively

provide information to help directors of small companiesassess

their need for support from professionalaccountants.

The POB appreciates the work of the professional bodies in

implementing the recommendations made in this Review.However, as

set out in this project update, in our view further work is needed

to help ensure that professionalaccountants are able to continue to

meet the needs of directors of small companies and users of their

accounts withintegrity and competence.