Embed Size (px)

Citation preview

Headline PMI 2

Output 5

New orders &

new export orders 7

Backlogs of orders 10

Stocks of finished

goods & major inputs 11

Purchases of inputs 11

Input prices 14

Imports 17

Employment 19

Suppliers’ delivery time 21

Business expectation 22

Helen Chin

Tel: (852) 2300 2471

The Fung Business Intelligence

Centre

10/F, Li Fung Tower,

888 Cheung Sha Wan Road,

Hong Kong

Tel : (852) 2300 2470

Fax : (852) 2635 1598

E-mail : [email protected]

http://www.funggroup.com

IN THIS ISSUE :

PMI Quarterly on China Manufacturing April 2014 Issue 16

FU

NG

BU

SIN

ES

S IN

TE

LL

IGE

NC

E C

EN

TR

E

ww

w.lifu

ng

gro

up

.co

m

PMI points to growth stabilization

Output growth moderated.

New orders index and new export orders index indicate stable

domestic demand and recovering external demand.

Backlogs of orders stayed in the contractionary zone.

Destocking activities continued.

Purchases of inputs decelerated.

Upstream cost pressure eased.

Imports remained weak.

Employment index has fluctuated within a narrow range.

Suppliers’ delivery slowed down.

Chinese manufacturers have become more optimistic.

PMI Quarterly on China Manufacturing

2

April 2014 Issue 16

1. PMI points to growth stabilization

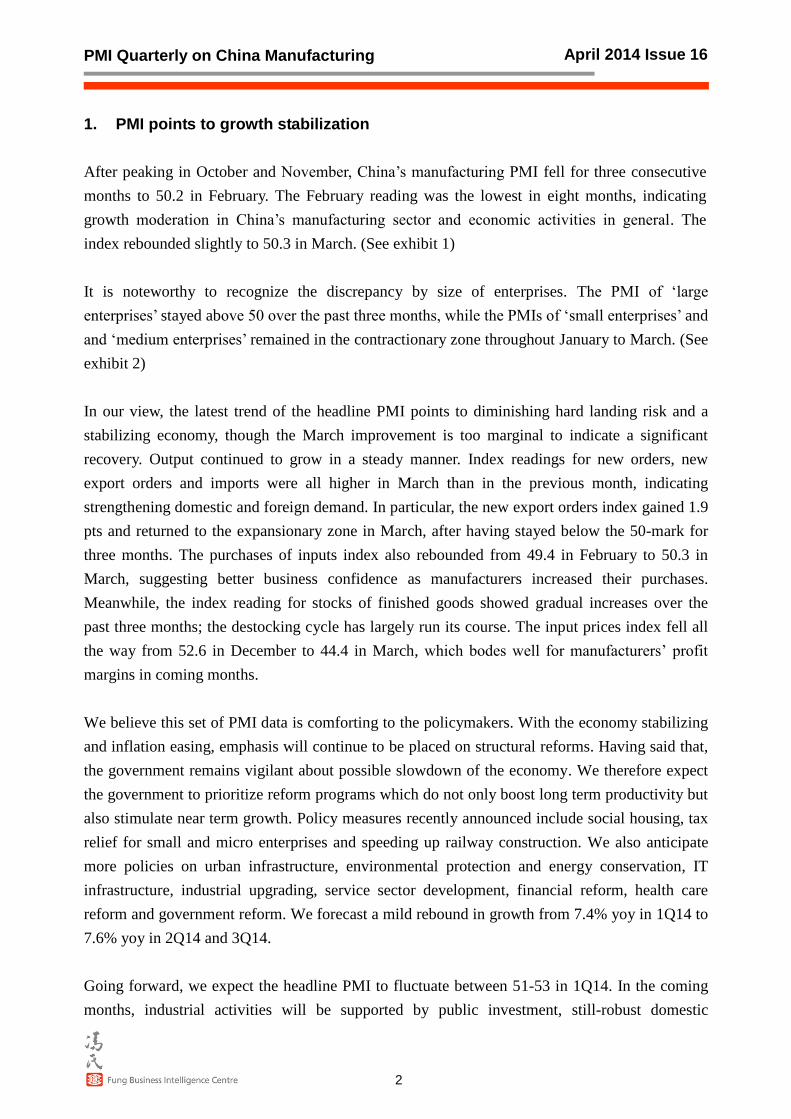

After peaking in October and November, China’s manufacturing PMI fell for three consecutive

months to 50.2 in February. The February reading was the lowest in eight months, indicating

growth moderation in China’s manufacturing sector and economic activities in general. The

index rebounded slightly to 50.3 in March. (See exhibit 1)

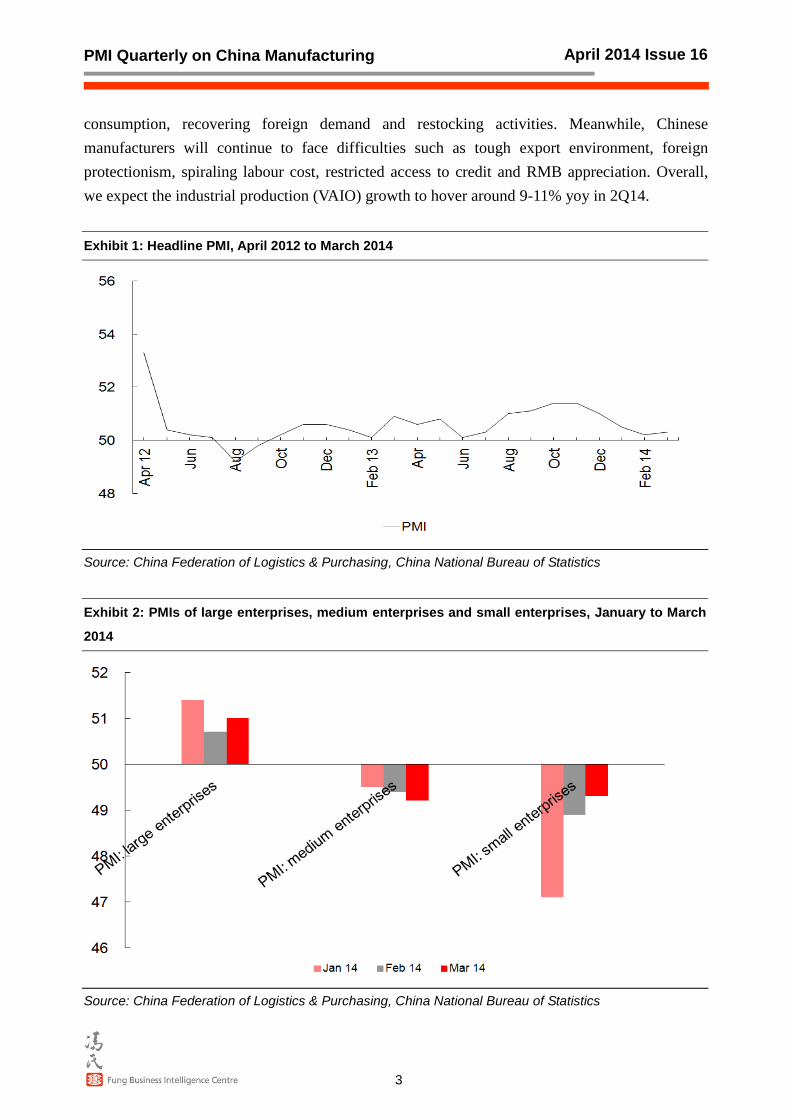

It is noteworthy to recognize the discrepancy by size of enterprises. The PMI of ‘large

enterprises’ stayed above 50 over the past three months, while the PMIs of ‘small enterprises’ and

and ‘medium enterprises’ remained in the contractionary zone throughout January to March. (See

exhibit 2)

In our view, the latest trend of the headline PMI points to diminishing hard landing risk and a

stabilizing economy, though the March improvement is too marginal to indicate a significant

recovery. Output continued to grow in a steady manner. Index readings for new orders, new

export orders and imports were all higher in March than in the previous month, indicating

strengthening domestic and foreign demand. In particular, the new export orders index gained 1.9

pts and returned to the expansionary zone in March, after having stayed below the 50-mark for

three months. The purchases of inputs index also rebounded from 49.4 in February to 50.3 in

March, suggesting better business confidence as manufacturers increased their purchases.

Meanwhile, the index reading for stocks of finished goods showed gradual increases over the

past three months; the destocking cycle has largely run its course. The input prices index fell all

the way from 52.6 in December to 44.4 in March, which bodes well for manufacturers’ profit

margins in coming months.

We believe this set of PMI data is comforting to the policymakers. With the economy stabilizing

and inflation easing, emphasis will continue to be placed on structural reforms. Having said that,

the government remains vigilant about possible slowdown of the economy. We therefore expect

the government to prioritize reform programs which do not only boost long term productivity but

also stimulate near term growth. Policy measures recently announced include social housing, tax

relief for small and micro enterprises and speeding up railway construction. We also anticipate

more policies on urban infrastructure, environmental protection and energy conservation, IT

infrastructure, industrial upgrading, service sector development, financial reform, health care

reform and government reform. We forecast a mild rebound in growth from 7.4% yoy in 1Q14 to

7.6% yoy in 2Q14 and 3Q14.

Going forward, we expect the headline PMI to fluctuate between 51-53 in 1Q14. In the coming

months, industrial activities will be supported by public investment, still-robust domestic

PMI Quarterly on China Manufacturing

3

April 2014 Issue 16

consumption, recovering foreign demand and restocking activities. Meanwhile, Chinese

manufacturers will continue to face difficulties such as tough export environment, foreign

protectionism, spiraling labour cost, restricted access to credit and RMB appreciation. Overall,

we expect the industrial production (VAIO) growth to hover around 9-11% yoy in 2Q14.

Exhibit 1: Headline PMI, April 2012 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

Exhibit 2: PMIs of large enterprises, medium enterprises and small enterprises, January to March

2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

PMI Quarterly on China Manufacturing

4

April 2014 Issue 16

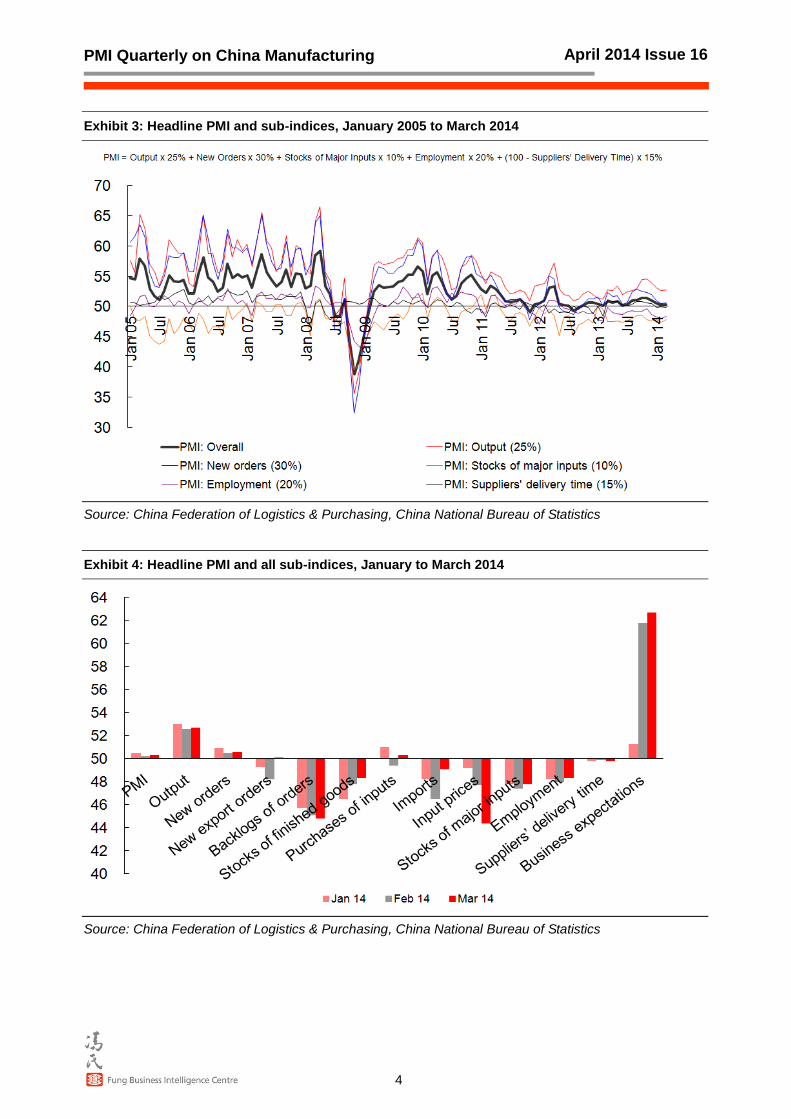

Exhibit 3: Headline PMI and sub-indices, January 2005 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

Exhibit 4: Headline PMI and all sub-indices, January to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

PMI Quarterly on China Manufacturing

5

April 2014 Issue 16

Exhibit 3 shows that the headline PMI moderation over the past three months was mainly

attributed to the marked fall in the new orders index (which weighs 30% in the computation of

the headline PMI) and the output index (weighs 25%). Among the 11 sub-indices (i.e. excluding

the suppliers’ delivery time index), only 3 (output, new orders and business expectations) stayed

in the expansionary zone over the past three months. The indices of backlogs of orders, stocks of

finished goods, stocks of major inputs, imports, input prices and employment remained below 50

throughout the past three months. (See exhibit 4)

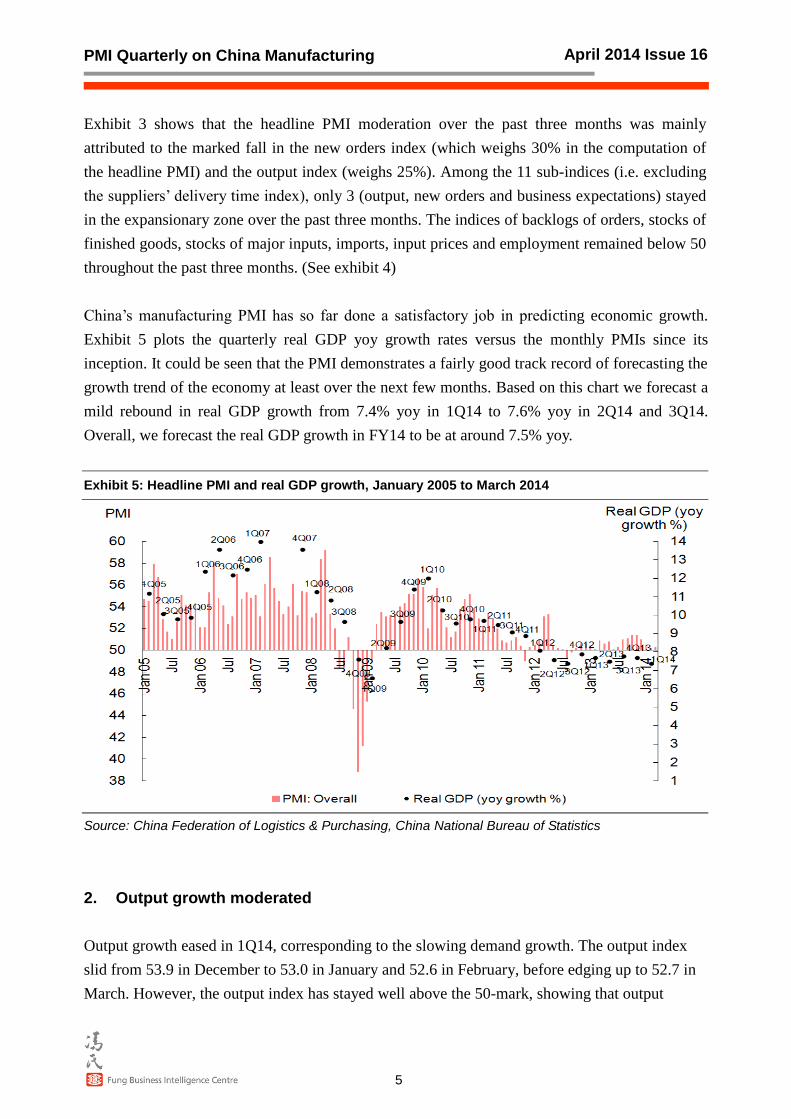

China’s manufacturing PMI has so far done a satisfactory job in predicting economic growth.

Exhibit 5 plots the quarterly real GDP yoy growth rates versus the monthly PMIs since its

inception. It could be seen that the PMI demonstrates a fairly good track record of forecasting the

growth trend of the economy at least over the next few months. Based on this chart we forecast a

mild rebound in real GDP growth from 7.4% yoy in 1Q14 to 7.6% yoy in 2Q14 and 3Q14.

Overall, we forecast the real GDP growth in FY14 to be at around 7.5% yoy.

Exhibit 5: Headline PMI and real GDP growth, January 2005 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

2. Output growth moderated

Output growth eased in 1Q14, corresponding to the slowing demand growth. The output index

slid from 53.9 in December to 53.0 in January and 52.6 in February, before edging up to 52.7 in

March. However, the output index has stayed well above the 50-mark, showing that output

PMI Quarterly on China Manufacturing

6

April 2014 Issue 16

growth was still robust. (See exhibit 6)

Exhibit 7 shows that the deceleration in production growth in the past three months was mainly

attributable to the moderating growth of new orders instead of destocking activities. It is

noteworthy that the stocks of finished goods index has been rising for three consecutive months,

gradually approaching the neutral 50-line. The pace of inventory liquidation has slowed. Output

may grow strongly later when manufacturers have finally run out of their inventories or regained

confidence to restock.

Exhibit 6: Output index, April 2012 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

Exhibit 7: Output, new orders and stocks of finished goods, January 2005 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

PMI Quarterly on China Manufacturing

7

April 2014 Issue 16

Exhibit 8 demonstrates the correlation (with some lags) between the output index and the yoy

growth of value-added of industrial output (VAIO). The VAIO growth has largely trended

downward since October last year. Looking ahead, we expect the VAIO growth to hover around

9-11% yoy in 2Q14. In the coming months, industrial activities will be supported by public

investment, still-robust domestic consumption, recovering foreign demand and restocking

activities. Meanwhile, Chinese manufacturers will continue to face difficulties such as tough

export environment, foreign protectionism, spiraling labour cost, restricted access to credit and

RMB appreciation.

Exhibit 8: Output index and industrial production growth, January 2005 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

3. New orders index and new export orders index indicate stable domestic

demand and recovering external demand

The new orders index fell to an eight-month low of 50.5 in February, before improving

marginally to 50.6 in March. In any case, the index has stayed in the expansionary zone for

eighteen months, showing that domestic demand has been stable. The new export orders index

had stayed below the 50-mark throughout December to February, before it gained 1.9 pts to

reach 50.1 in March. External demand has stabilized and started to recover.1 (See exhibit 9)

Exhibit 10 shows that the new orders index generally leads industrial production by about 2 to 3

months. The new orders index suggests stable growth of industrial production in coming months.

Again, the projection based on the new orders index is that the VAIO growth is likely to hover

1 We have received a number of enquiries on this point. The ‘new orders index’ covers both domestic orders and export orders. That is to say, the

manufacturers are not asked to differentiate between domestic orders and export orders when filing in the questionnaires.

PMI Quarterly on China Manufacturing

8

April 2014 Issue 16

around 9-11% yoy in 2Q14.

Exhibit 9: New orders index and new export orders index, January 2005 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

Exhibit 10: New orders index and industrial production growth, January 2005 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

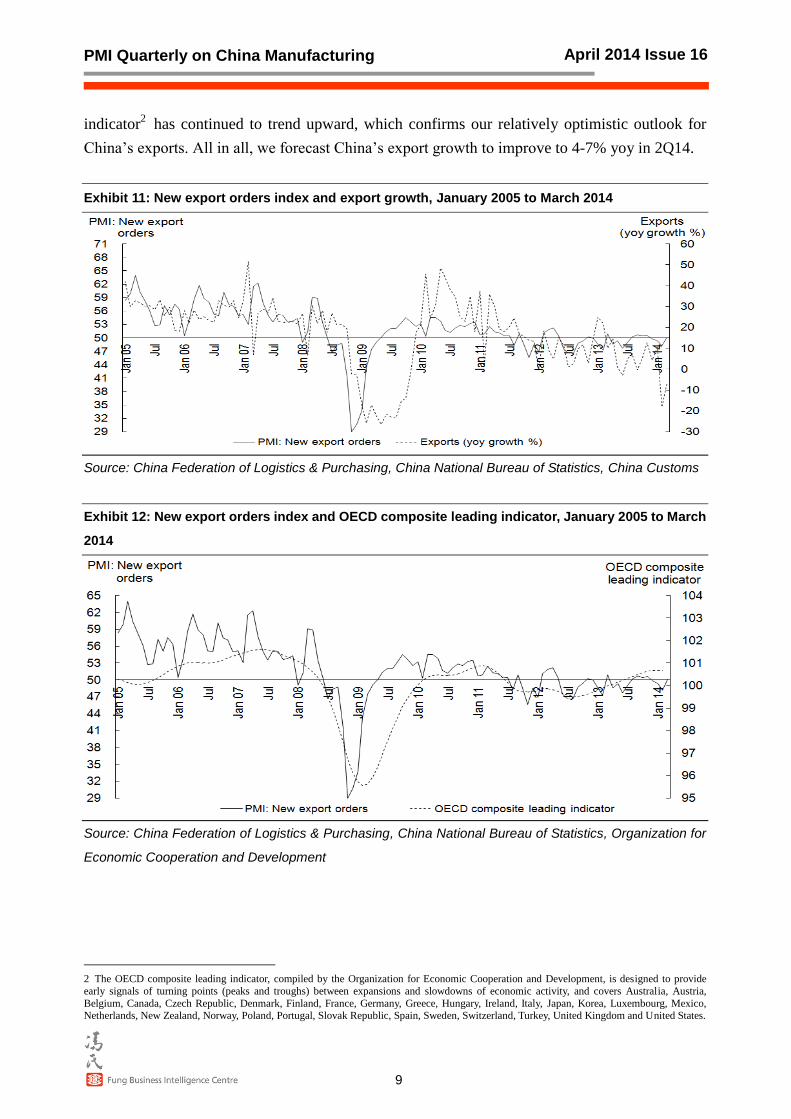

Exhibit 11 plots the new export orders index against the yoy growth rates of China’s exports. The

correlation between the two is fairly high, with the new export orders index leading the export

yoy growth rate by about 3 months (except in early last year, when the export figures were

greatly inflated by fake exports). With the new export orders index rising above the critical

50-mark again, we have become more optimistic over China’s export outlook. Besides, from

exhibit 12 we can see that the new export orders index has been strongly correlated to the

external economies, especially the developed economies. The OECD composite leading

PMI Quarterly on China Manufacturing

9

April 2014 Issue 16

indicator2 has continued to trend upward, which confirms our relatively optimistic outlook for

China’s exports. All in all, we forecast China’s export growth to improve to 4-7% yoy in 2Q14.

Exhibit 11: New export orders index and export growth, January 2005 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics, China Customs

Exhibit 12: New export orders index and OECD composite leading indicator, January 2005 to March

2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics, Organization for

Economic Cooperation and Development

2 The OECD composite leading indicator, compiled by the Organization for Economic Cooperation and Development, is designed to provide

early signals of turning points (peaks and troughs) between expansions and slowdowns of economic activity, and covers Australia, Austria,

Belgium, Canada, Czech Republic, Denmark, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Japan, Korea, Luxembourg, Mexico, Netherlands, New Zealand, Norway, Poland, Portugal, Slovak Republic, Spain, Sweden, Switzerland, Turkey, United Kingdom and United States.

PMI Quarterly on China Manufacturing

10

April 2014 Issue 16

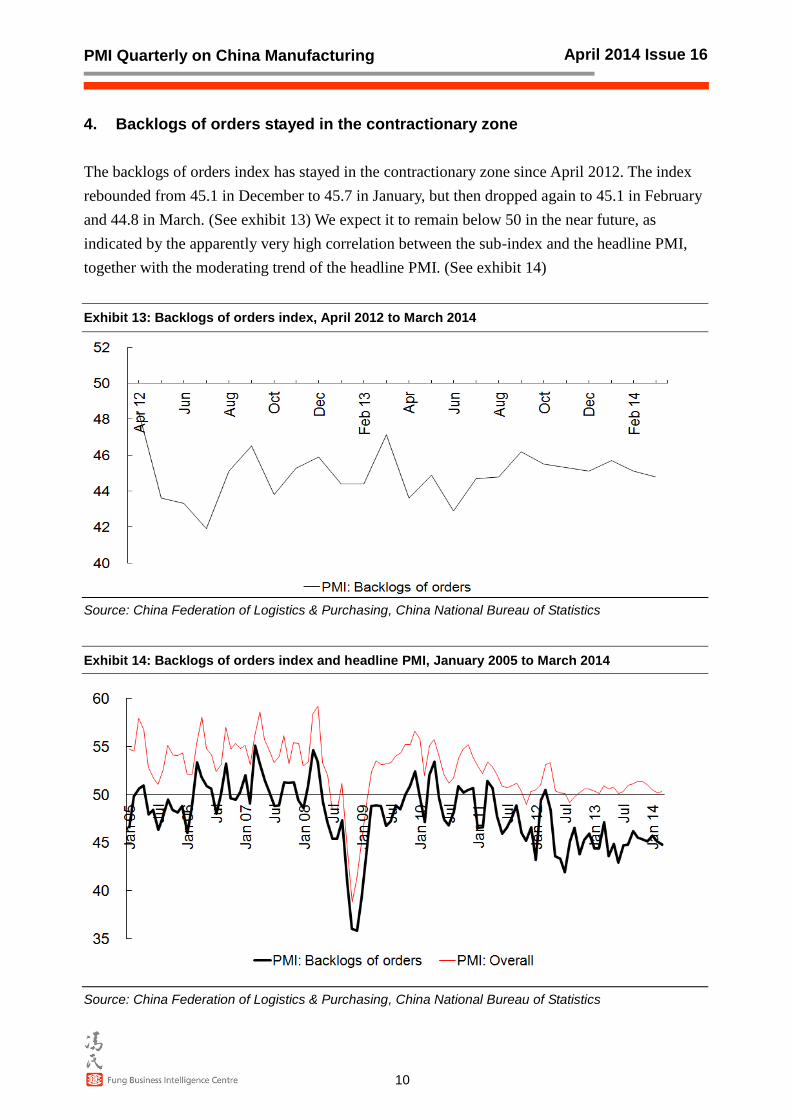

4. Backlogs of orders stayed in the contractionary zone

The backlogs of orders index has stayed in the contractionary zone since April 2012. The index

rebounded from 45.1 in December to 45.7 in January, but then dropped again to 45.1 in February

and 44.8 in March. (See exhibit 13) We expect it to remain below 50 in the near future, as

indicated by the apparently very high correlation between the sub-index and the headline PMI,

together with the moderating trend of the headline PMI. (See exhibit 14)

Exhibit 13: Backlogs of orders index, April 2012 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

Exhibit 14: Backlogs of orders index and headline PMI, January 2005 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

PMI Quarterly on China Manufacturing

11

April 2014 Issue 16

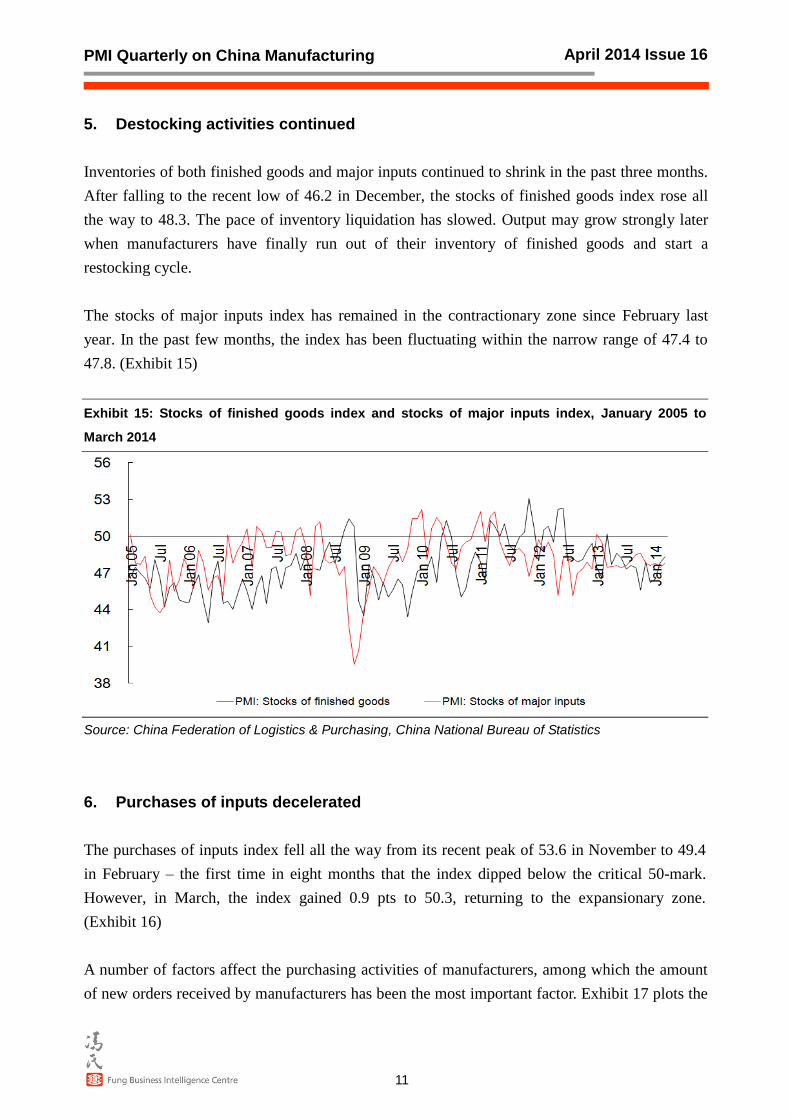

5. Destocking activities continued

Inventories of both finished goods and major inputs continued to shrink in the past three months.

After falling to the recent low of 46.2 in December, the stocks of finished goods index rose all

the way to 48.3. The pace of inventory liquidation has slowed. Output may grow strongly later

when manufacturers have finally run out of their inventory of finished goods and start a

restocking cycle.

The stocks of major inputs index has remained in the contractionary zone since February last

year. In the past few months, the index has been fluctuating within the narrow range of 47.4 to

47.8. (Exhibit 15)

Exhibit 15: Stocks of finished goods index and stocks of major inputs index, January 2005 to

March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

6. Purchases of inputs decelerated

The purchases of inputs index fell all the way from its recent peak of 53.6 in November to 49.4

in February – the first time in eight months that the index dipped below the critical 50-mark.

However, in March, the index gained 0.9 pts to 50.3, returning to the expansionary zone.

(Exhibit 16)

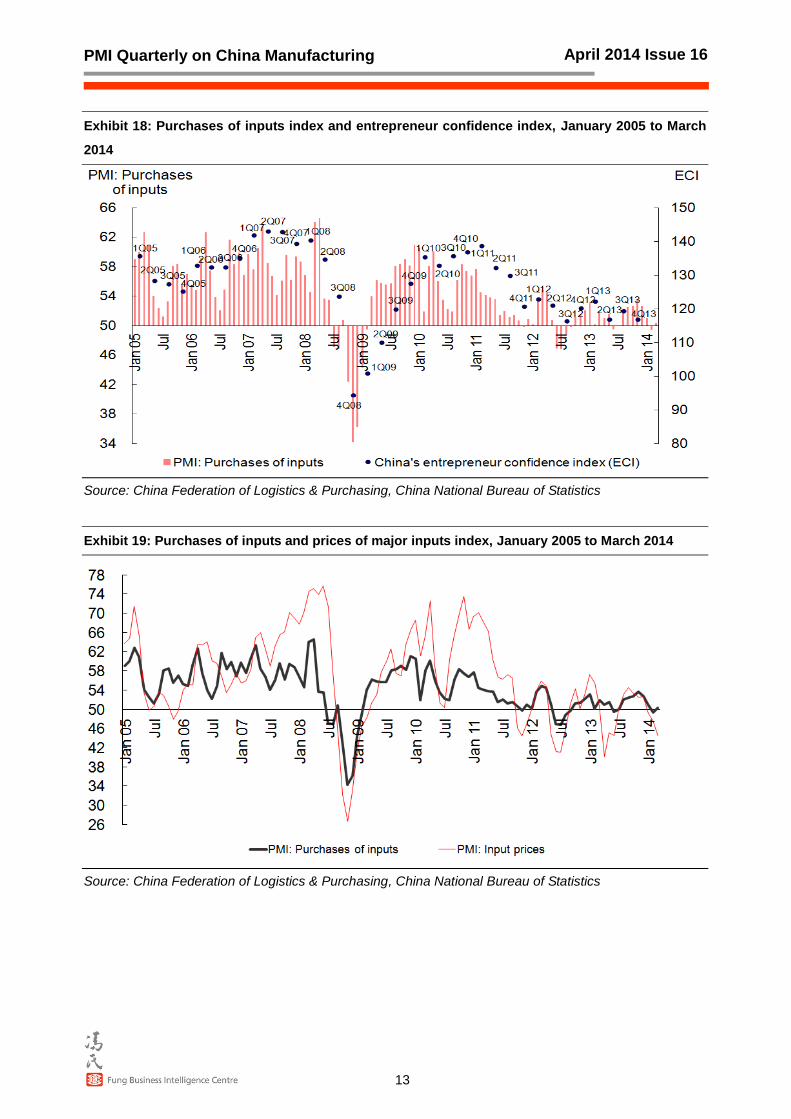

A number of factors affect the purchasing activities of manufacturers, among which the amount

of new orders received by manufacturers has been the most important factor. Exhibit 17 plots the

PMI Quarterly on China Manufacturing

12

April 2014 Issue 16

purchases of inputs index against the new orders index. The correlation between the two

sub-indices is very strong. This is intuitively easy to explain – as manufacturers usually need to

purchase extra inputs to cope with new orders. We expect to see continuous increase in purchases

if the rise in new orders persists. The purchasing activities also reflect business confidence.

Exhibit 18 shows the association between the purchases of inputs index and the entrepreneur

confidence index (ECI). Credit conditions could be another factor. Finally, exhibit 19 shows that

input prices, as well as the expected trend of input prices, are also important considerations when

making purchasing decisions.

Exhibit 16: Purchases of inputs index, April 2012 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

Exhibit 17: Purchases of inputs and new orders, January 2005 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

PMI Quarterly on China Manufacturing

13

April 2014 Issue 16

Exhibit 18: Purchases of inputs index and entrepreneur confidence index, January 2005 to March

2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

Exhibit 19: Purchases of inputs and prices of major inputs index, January 2005 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

PMI Quarterly on China Manufacturing

14

April 2014 Issue 16

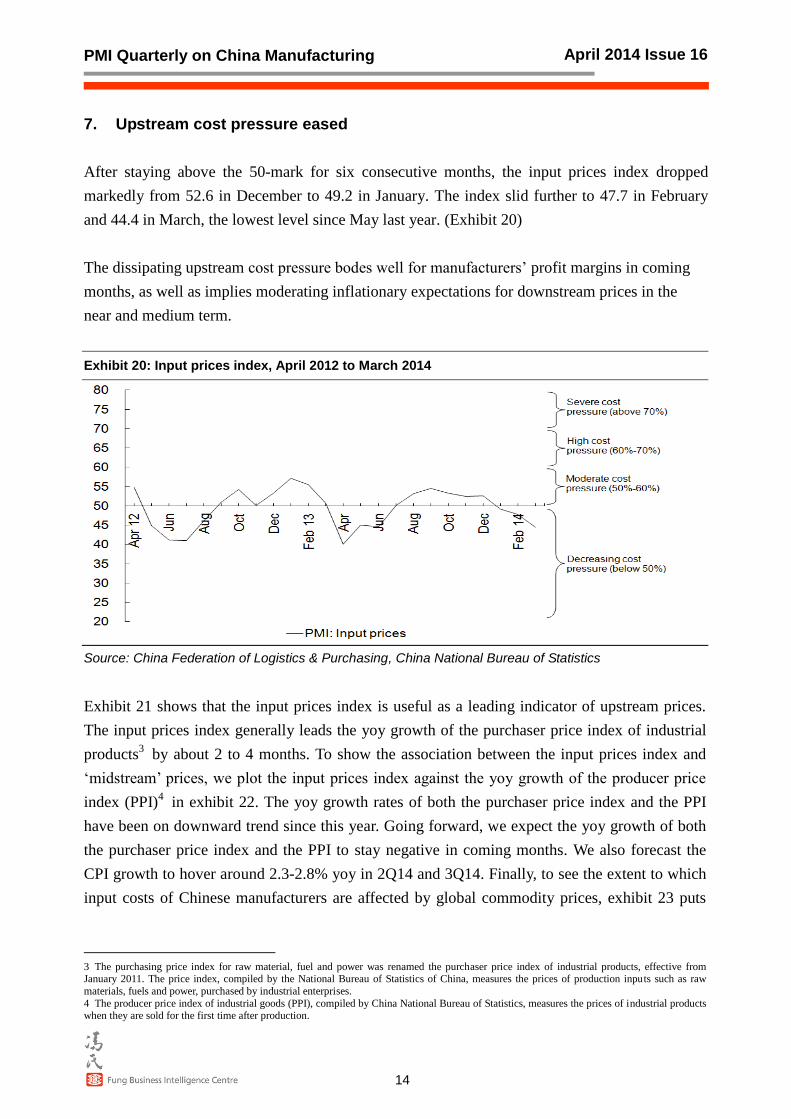

7. Upstream cost pressure eased

After staying above the 50-mark for six consecutive months, the input prices index dropped

markedly from 52.6 in December to 49.2 in January. The index slid further to 47.7 in February

and 44.4 in March, the lowest level since May last year. (Exhibit 20)

The dissipating upstream cost pressure bodes well for manufacturers’ profit margins in coming

months, as well as implies moderating inflationary expectations for downstream prices in the

near and medium term.

Exhibit 20: Input prices index, April 2012 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

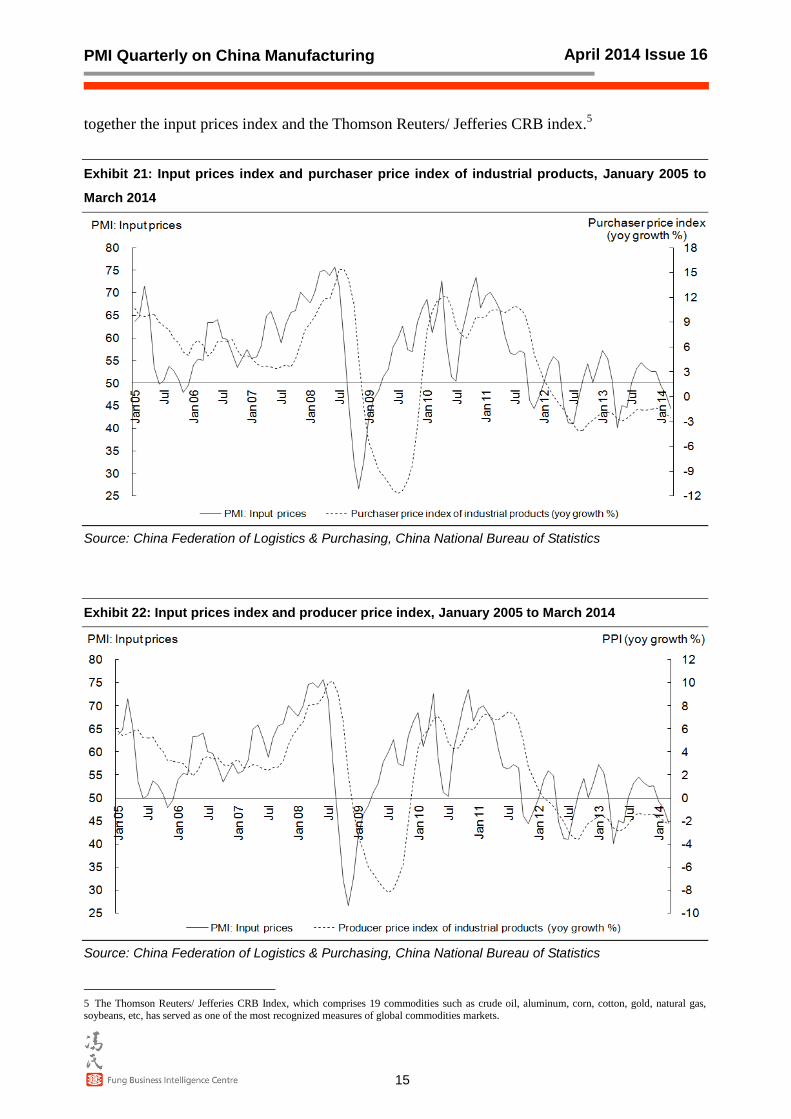

Exhibit 21 shows that the input prices index is useful as a leading indicator of upstream prices.

The input prices index generally leads the yoy growth of the purchaser price index of industrial

products3 by about 2 to 4 months. To show the association between the input prices index and

‘midstream’ prices, we plot the input prices index against the yoy growth of the producer price

index (PPI)4 in exhibit 22. The yoy growth rates of both the purchaser price index and the PPI

have been on downward trend since this year. Going forward, we expect the yoy growth of both

the purchaser price index and the PPI to stay negative in coming months. We also forecast the

CPI growth to hover around 2.3-2.8% yoy in 2Q14 and 3Q14. Finally, to see the extent to which

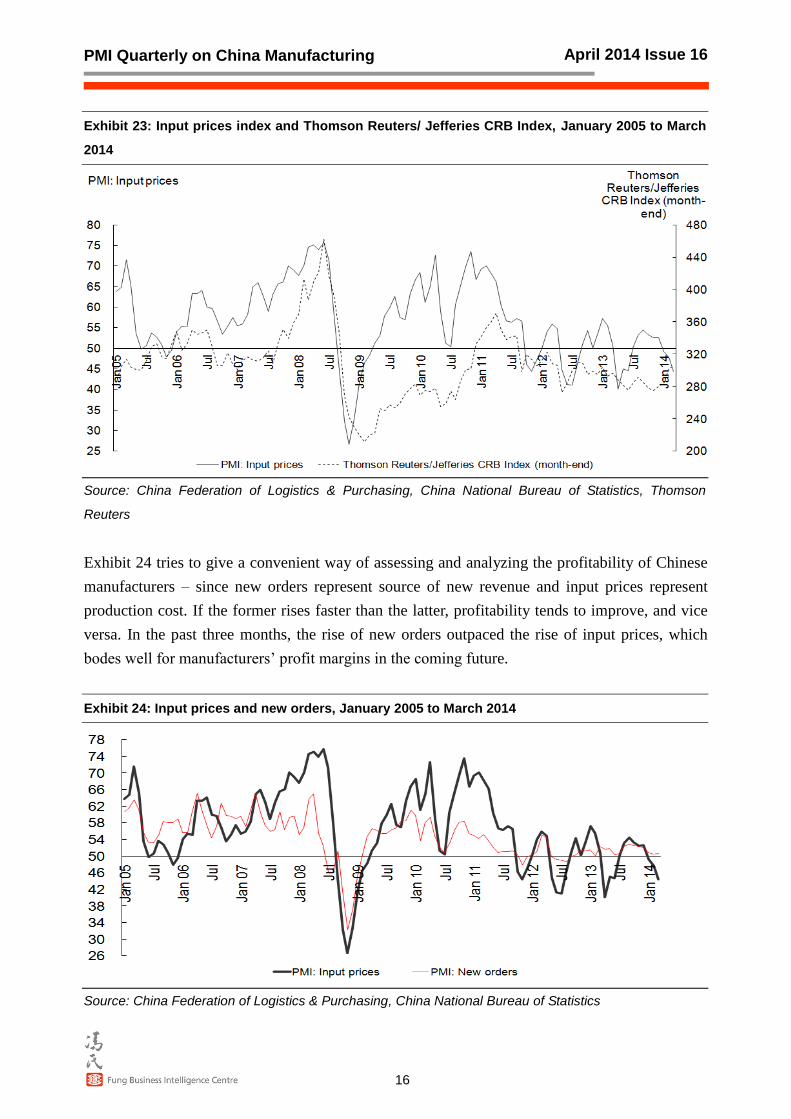

input costs of Chinese manufacturers are affected by global commodity prices, exhibit 23 puts

3 The purchasing price index for raw material, fuel and power was renamed the purchaser price index of industrial products, effective from January 2011. The price index, compiled by the National Bureau of Statistics of China, measures the prices of production inputs such as raw

materials, fuels and power, purchased by industrial enterprises.

4 The producer price index of industrial goods (PPI), compiled by China National Bureau of Statistics, measures the prices of industrial products when they are sold for the first time after production.

PMI Quarterly on China Manufacturing

15

April 2014 Issue 16

together the input prices index and the Thomson Reuters/ Jefferies CRB index.5

Exhibit 21: Input prices index and purchaser price index of industrial products, January 2005 to

March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

Exhibit 22: Input prices index and producer price index, January 2005 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

5 The Thomson Reuters/ Jefferies CRB Index, which comprises 19 commodities such as crude oil, aluminum, corn, cotton, gold, natural gas, soybeans, etc, has served as one of the most recognized measures of global commodities markets.

PMI Quarterly on China Manufacturing

16

April 2014 Issue 16

Exhibit 23: Input prices index and Thomson Reuters/ Jefferies CRB Index, January 2005 to March

2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics, Thomson

Reuters

Exhibit 24 tries to give a convenient way of assessing and analyzing the profitability of Chinese

manufacturers – since new orders represent source of new revenue and input prices represent

production cost. If the former rises faster than the latter, profitability tends to improve, and vice

versa. In the past three months, the rise of new orders outpaced the rise of input prices, which

bodes well for manufacturers’ profit margins in the coming future.

Exhibit 24: Input prices and new orders, January 2005 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

PMI Quarterly on China Manufacturing

17

April 2014 Issue 16

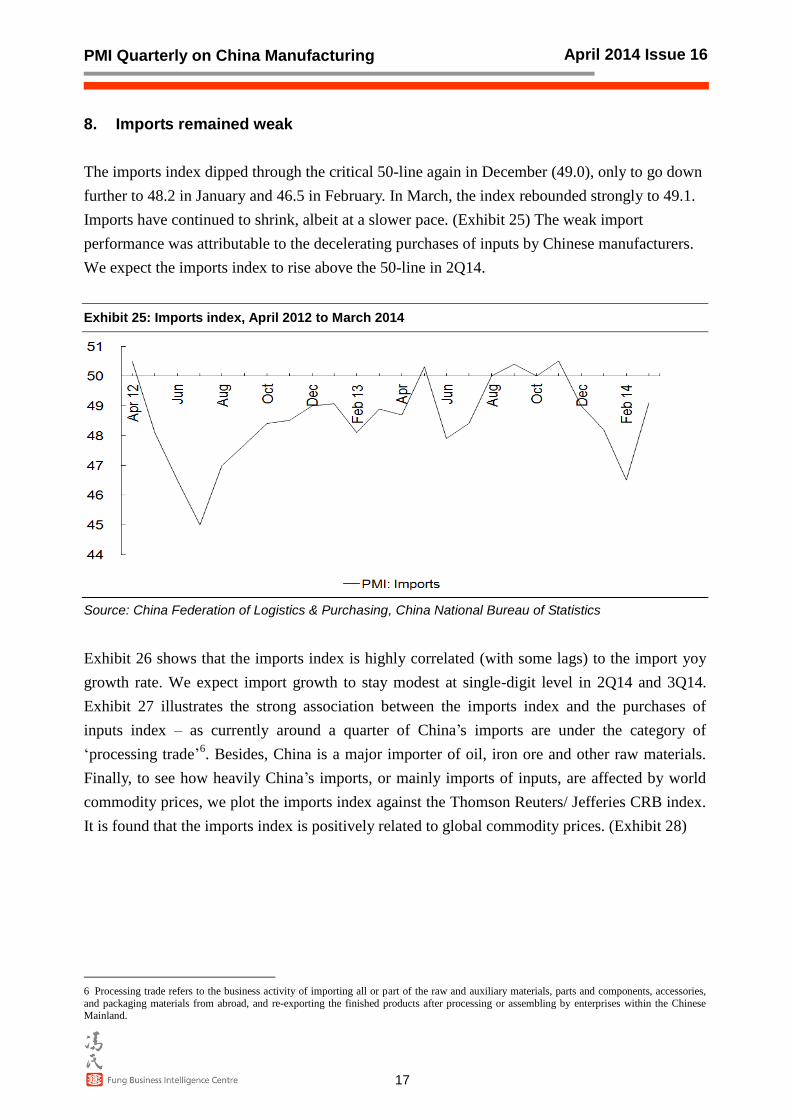

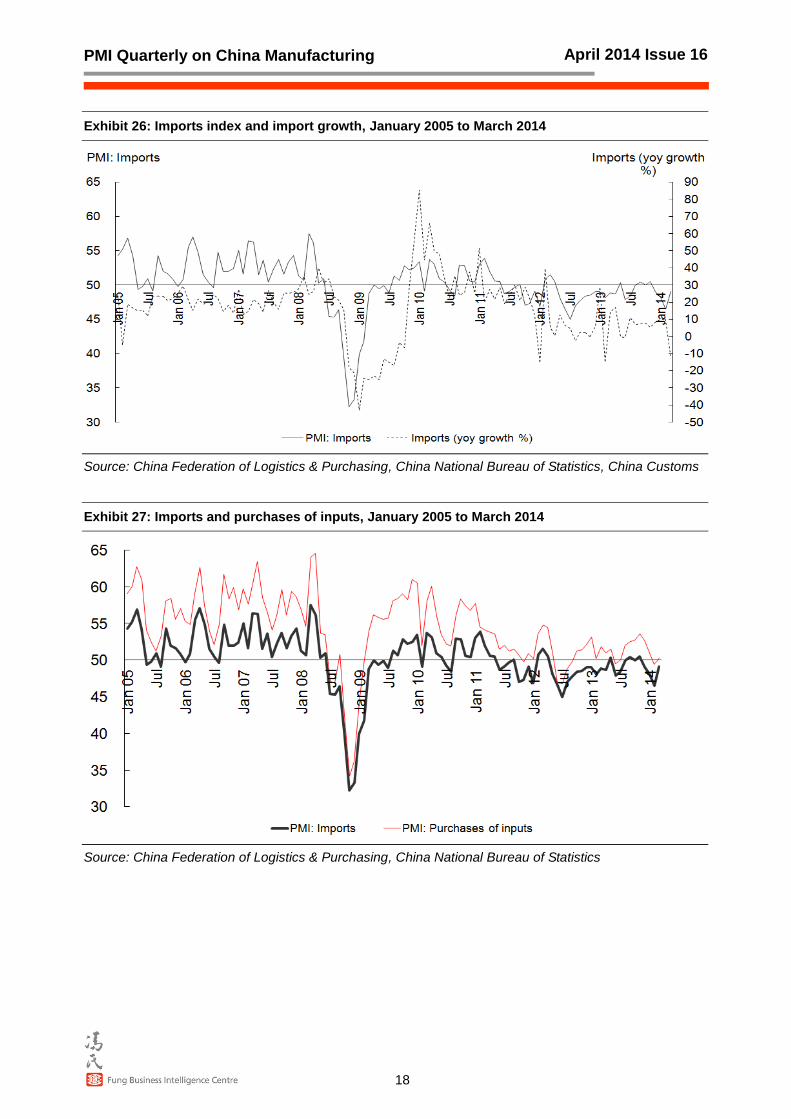

8. Imports remained weak

The imports index dipped through the critical 50-line again in December (49.0), only to go down

further to 48.2 in January and 46.5 in February. In March, the index rebounded strongly to 49.1.

Imports have continued to shrink, albeit at a slower pace. (Exhibit 25) The weak import

performance was attributable to the decelerating purchases of inputs by Chinese manufacturers.

We expect the imports index to rise above the 50-line in 2Q14.

Exhibit 25: Imports index, April 2012 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

Exhibit 26 shows that the imports index is highly correlated (with some lags) to the import yoy

growth rate. We expect import growth to stay modest at single-digit level in 2Q14 and 3Q14.

Exhibit 27 illustrates the strong association between the imports index and the purchases of

inputs index – as currently around a quarter of China’s imports are under the category of

‘processing trade’6. Besides, China is a major importer of oil, iron ore and other raw materials.

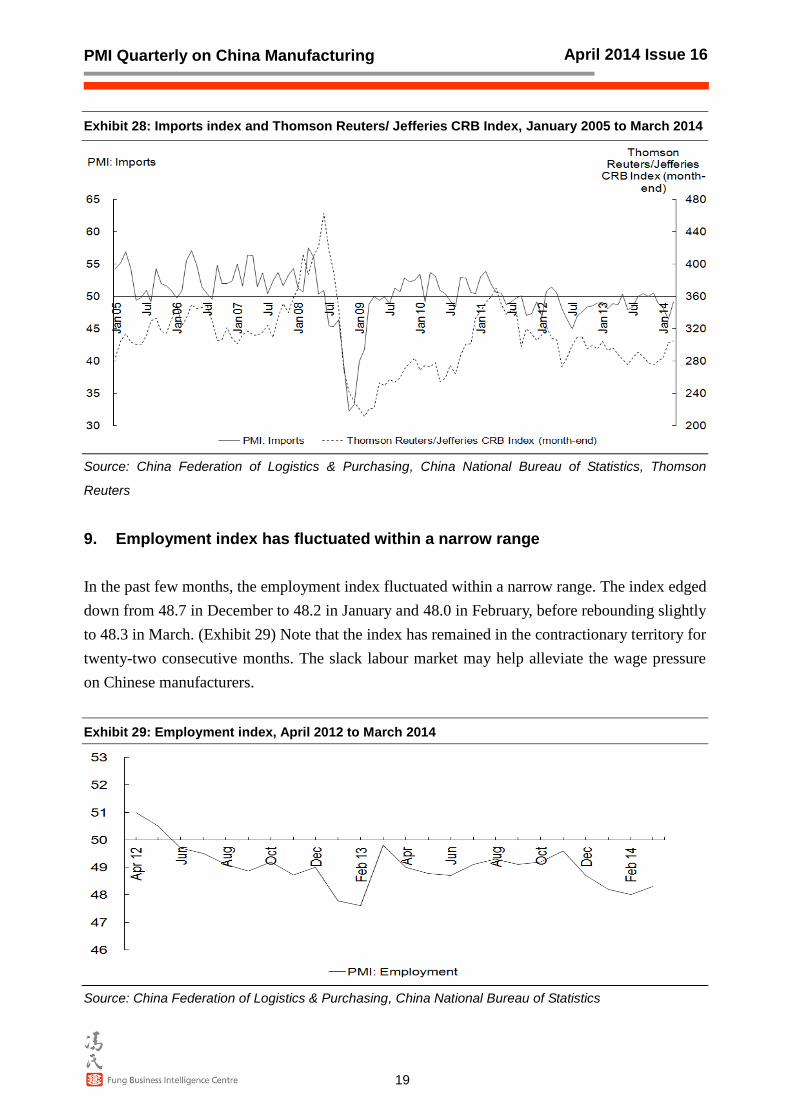

Finally, to see how heavily China’s imports, or mainly imports of inputs, are affected by world

commodity prices, we plot the imports index against the Thomson Reuters/ Jefferies CRB index.

It is found that the imports index is positively related to global commodity prices. (Exhibit 28)

6 Processing trade refers to the business activity of importing all or part of the raw and auxiliary materials, parts and components, accessories,

and packaging materials from abroad, and re-exporting the finished products after processing or assembling by enterprises within the Chinese Mainland.

PMI Quarterly on China Manufacturing

18

April 2014 Issue 16

Exhibit 26: Imports index and import growth, January 2005 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics, China Customs

Exhibit 27: Imports and purchases of inputs, January 2005 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

PMI Quarterly on China Manufacturing

19

April 2014 Issue 16

Exhibit 28: Imports index and Thomson Reuters/ Jefferies CRB Index, January 2005 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics, Thomson

Reuters

9. Employment index has fluctuated within a narrow range

In the past few months, the employment index fluctuated within a narrow range. The index edged

down from 48.7 in December to 48.2 in January and 48.0 in February, before rebounding slightly

to 48.3 in March. (Exhibit 29) Note that the index has remained in the contractionary territory for

twenty-two consecutive months. The slack labour market may help alleviate the wage pressure

on Chinese manufacturers.

Exhibit 29: Employment index, April 2012 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

PMI Quarterly on China Manufacturing

20

April 2014 Issue 16

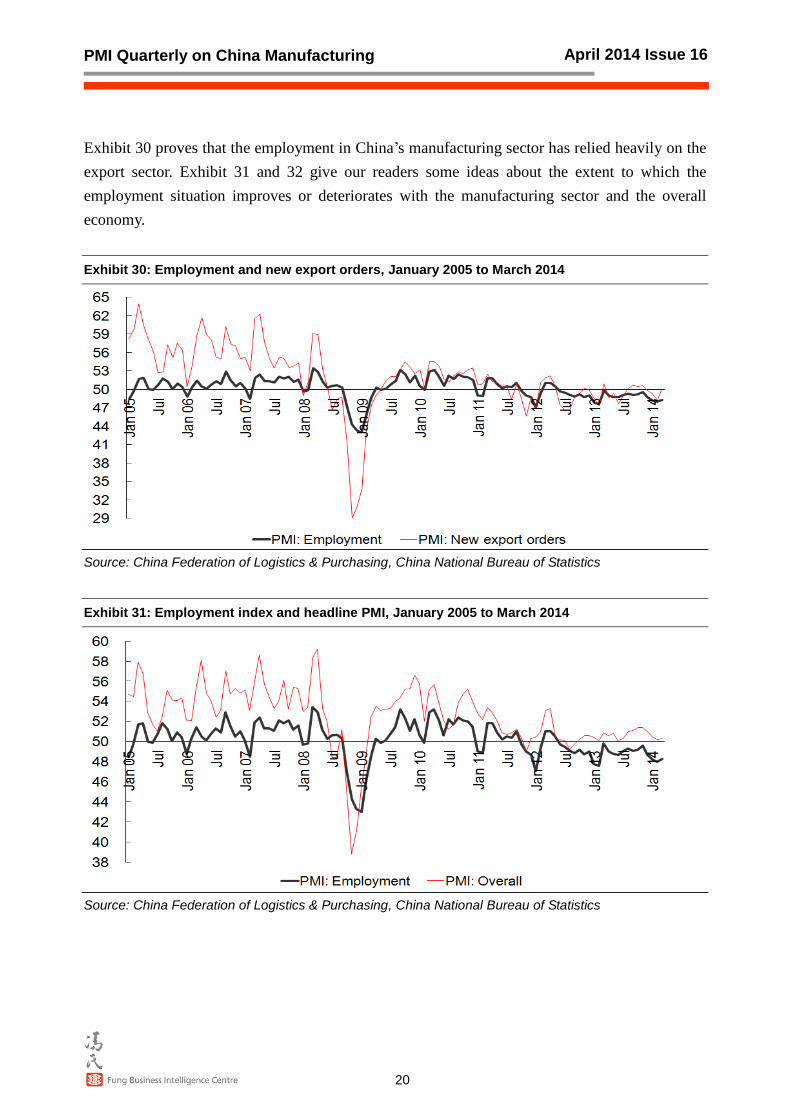

Exhibit 30 proves that the employment in China’s manufacturing sector has relied heavily on the

export sector. Exhibit 31 and 32 give our readers some ideas about the extent to which the

employment situation improves or deteriorates with the manufacturing sector and the overall

economy.

Exhibit 30: Employment and new export orders, January 2005 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

Exhibit 31: Employment index and headline PMI, January 2005 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

PMI Quarterly on China Manufacturing

21

April 2014 Issue 16

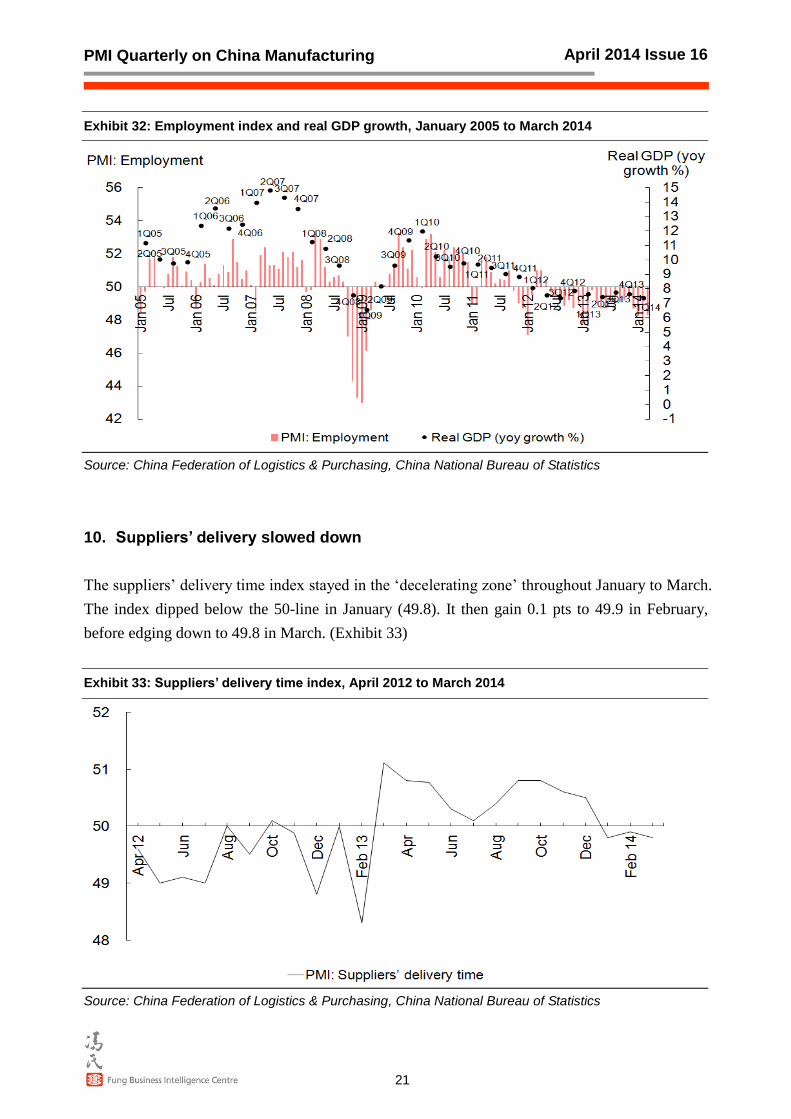

Exhibit 32: Employment index and real GDP growth, January 2005 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

10. Suppliers’ delivery slowed down

The suppliers’ delivery time index stayed in the ‘decelerating zone’ throughout January to March.

The index dipped below the 50-line in January (49.8). It then gain 0.1 pts to 49.9 in February,

before edging down to 49.8 in March. (Exhibit 33)

Exhibit 33: Suppliers’ delivery time index, April 2012 to March 2014

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

PMI Quarterly on China Manufacturing

22

April 2014 Issue 16

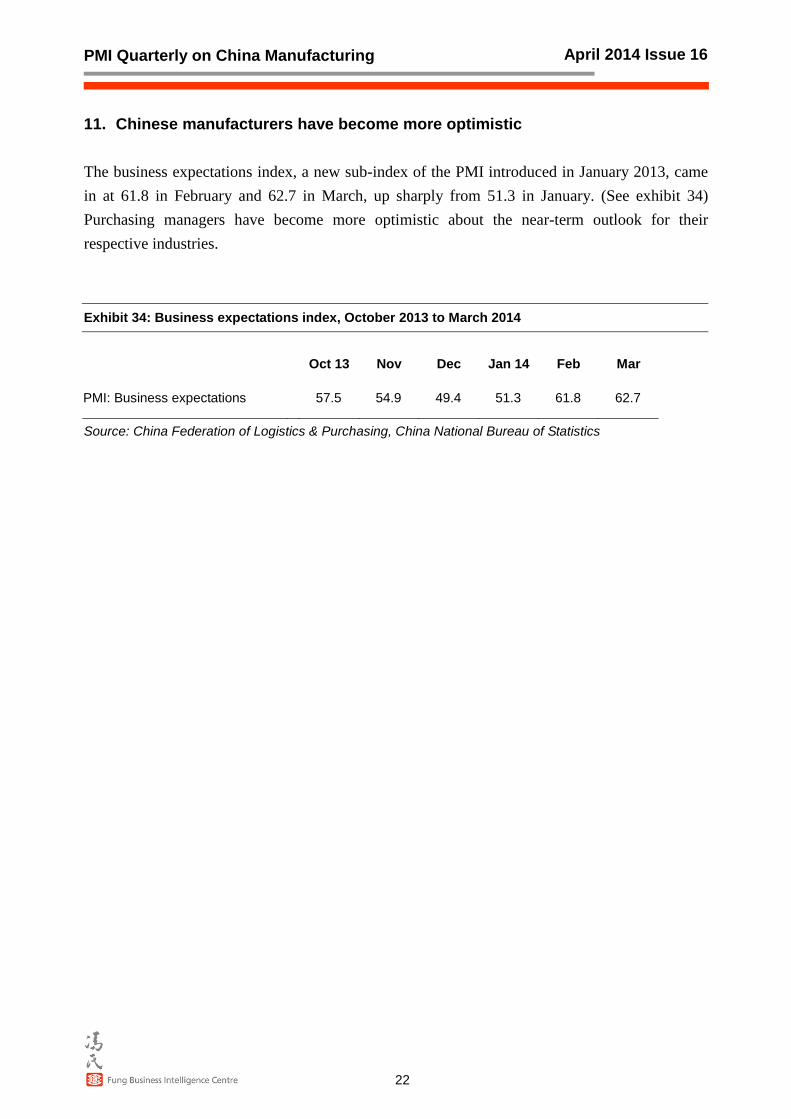

11. Chinese manufacturers have become more optimistic

The business expectations index, a new sub-index of the PMI introduced in January 2013, came

in at 61.8 in February and 62.7 in March, up sharply from 51.3 in January. (See exhibit 34)

Purchasing managers have become more optimistic about the near-term outlook for their

respective industries.

Exhibit 34: Business expectations index, October 2013 to March 2014

Oct 13 Nov Dec Jan 14 Feb Mar

PMI: Business expectations

57.5 54.9 49.4 51.3 61.8 62.7

Source: China Federation of Logistics & Purchasing, China National Bureau of Statistics

PMI Quarterly on China Manufacturing

23

April 2014 Issue 16

About China Manufacturing PMI:

China Manufacturing Purchasing Managers’ Index (PMI) provides an early indication each month of

economic activities in the Chinese manufacturing sector. It is jointly published by China Federation of

Logistics & Purchasing (CFLP) and the National Bureau of Statistics (NBS). The Fung Business

Intelligence Centre is responsible for drafting and disseminating the English PMI report.

Every month questionnaires are sent to 3,000 manufacturing enterprises all over China. The data

presented herein is compiled from the enterprises’ responses about their purchasing activities and supply

situations. CFLP makes no representation regarding the data collection procedures, nor does it disclose

any data of individual enterprises. The PMI should be compared to other economic data sources when

used in decision-making.

3,000 manufacturing enterprises in 21 industries from Eastern, Northeastern, Central and Western China

are surveyed. The sampling of the enterprises involves the use of Probability Proportional to Size

Sampling (PPS), which means the selection of enterprises surveyed is largely based on each industry’s

contribution to GDP, and the representation of each geographical region.

Survey responses reflect the change of each indicator, if any, in the current month compared to the

previous month. There are 12 indicators in the survey: Output, New Orders, New Export Orders, Backlogs

of Orders, Stocks of Finished Goods, Purchases of Inputs, Imports, Input Prices, Stocks of Major Inputs,

Employment, Suppliers’ Delivery Time and Business Expectations. For each of the indicators, this report

shows the percentage of enterprises reporting each response, the difference between the percentage of

responses in the positive economic direction and the negative economic direction, and the diffusion index.

The diffusion index is the sum of the positive responses plus a half of those responding ‘the same’.

Diffusion indices have the properties of leading indicators and are convenient summary measures showing

the prevailing direction of change and the scope of change. An index reading above 50 indicates an overall

positive change in that variable; below 50, an overall negative change.

The PMI is a composite index based on the seasonally adjusted diffusion indices for five of the indicators

with varying weights: New Orders—30%; Output—25%; Employment—20%; Suppliers’ Delivery

Time—15%; and Stocks of Major Inputs—10%. A PMI reading above 50 indicates an overall expansion in

the manufacturing sector; below 50, an overall contraction.

Currently there are 22 countries and regions conducting the PMI survey and compilation, based on an

internationally standardized methodology.

PMI Quarterly on China Manufacturing

24

April 2014 Issue 16

The Fung Group is a privately held multinational group of companies headquartered in Hong Kong whose core businesses are trading, logistics, distribution and retailing. The Fung Group employs over 43,000 people across 40 economies worldwide, generating total revenue of more than US$21.9 billion in 2012. Fung Holdings (1937) Limited, a privately held business entity headquartered in Hong Kong, is the major shareholder of the Fung group of companies. Please visit www.funggroup.com for more about the Fung Group. Through exceptional relationships and deep networks, the Fung Business Intelligence Centre (formerly known as the Li & Fung Research Centre) collects and analyses market data on China's economy, with special reference to sourcing, supply chains, distribution and retail. It also produces reports on sourcing and trading in other Asian countries. Serving as a knowledge bank for the Fung Group, the Centre makes its market data and analysis available to businesses, scholars and governments around the world. It has become an impartial thought leader on issues shaping the future of manufacturing, distribution, logistics and retailing in China, and regularly provides advice and consultancy services to internal and external clients.

© Copyright 2014 The Fung Business Intelligence Centre. All rights reserved.

Though the Fung Business Intelligence Centre endeavours to ensure the information provided in this publication is accurate and updated, no legal liability can be attached as to the contents hereof. Reproduction or redistribution of this material without prior written consent of the Fung Business Intelligence Centre is prohibited.