Embed Size (px)

DESCRIPTION

accounting

Citation preview

2011 SUMMER EXAMINATION PERIOD

Module Code: PMC Module Name: Performance Measurement & Control Programme: MSc Finance Exam Date: Summer 2011 Exam Duration: 3 hours writing time No. of Pages (including cover sheet): 6

ALLOWABLE MATERIALS

Open Book Examination

Non-programmable calculator permitted

Statistical Tables are provided with this examination

INSTRUCTIONS TO CANDIDATES

1. SECTION A: Compulsory question.

SECTION B: Answer TWO out of THREE questions.

2. Marks for each question are given in brackets.

3. This exam is worth 50% of the final marks for this module. You are required to achieve a minimum of 40% in this examination to pass the module.

4. All answers must be written in the answer booklet provided.

This paper MUST NOT BE REMOVED from the examination venue. Your mobile telephone must be switched off and in your bag throughout the exam.

SECTION A: Compulsory Question QUESTION ONE

(a) Allwinner Plc is a company which manufactures a range of children’s sports

products, including footballs. These football products require bladders, leather, packaging materials, and labour as direct inputs to the production of the product. Allwinner Plc budget for the month of March 2011 was as follows: Budget for March, 2011

£ £ £ Sales: (6,000 units @ £48 each) 6,000 48.00 288,000

Variable costs:

Bladders (6,000 units @ £3.00 each) 6,000 3.00 18.000

Leather (200 ten-hide bales @ £456) 200 456.00 91,200

Packing materials etc. 7,800

Direct labour (5,000 hours @ £6.00 ph) 5,000 6.00 30,000

Total variable costs (147,000)

Fixed costs:

Administrative expenses 25,434

Salaries 49,566

Total fixed costs (75,000)

Budgeted Net Profit 66,000

Due to an unexpected machine breakdown during March, Alphasport was only able to manufacture 60% of the budgeted production time (5,000 hours) and was unable to sanction any overtime, although the direct labour force was paid in full for the original budgeted hours. Actual costs and output during March were recorded as follows:

Actual for March, 2011 £ £ £ Sales (4000 units at £54 each) 4000 54.00 216,000 Variable costs:

Bladders (4000 units at £4.20 each) 4000 4.20 16,800 Leather (100 ten hide bales at £800 each) 100 800.00 80,000 Sundry and packaging materials 5,200 Direct labor (5000 hours at £6.50 per hour) 5000 6.50 32,500

Total Variable costs 134,500 Fixed Costs

Administrative expenses 26,000

Salaries 49,000

Total Fixed costs 75,000

Actual Net Profit 6,500

Required: (a) Prepare a statement reconciling the budgeted profit with the actual profit and state the variances in the way you consider would be most helpful to management. (18 marks)

(b) Comment briefly on any apparent (i.e. plausible) inter-relationships between variances. (12 marks) (c) Consider the following statement:

“There are more comprehensive models of management control and performance measurement than variance analysis available now such as the balanced score card that tries to incorporate other methods of observing good management practice.”

With reference to the above statement, compare and contrast variance analysis and balanced scorecard approaches as management tools for cost control and performance evaluation. (20 marks) Total 50 marks

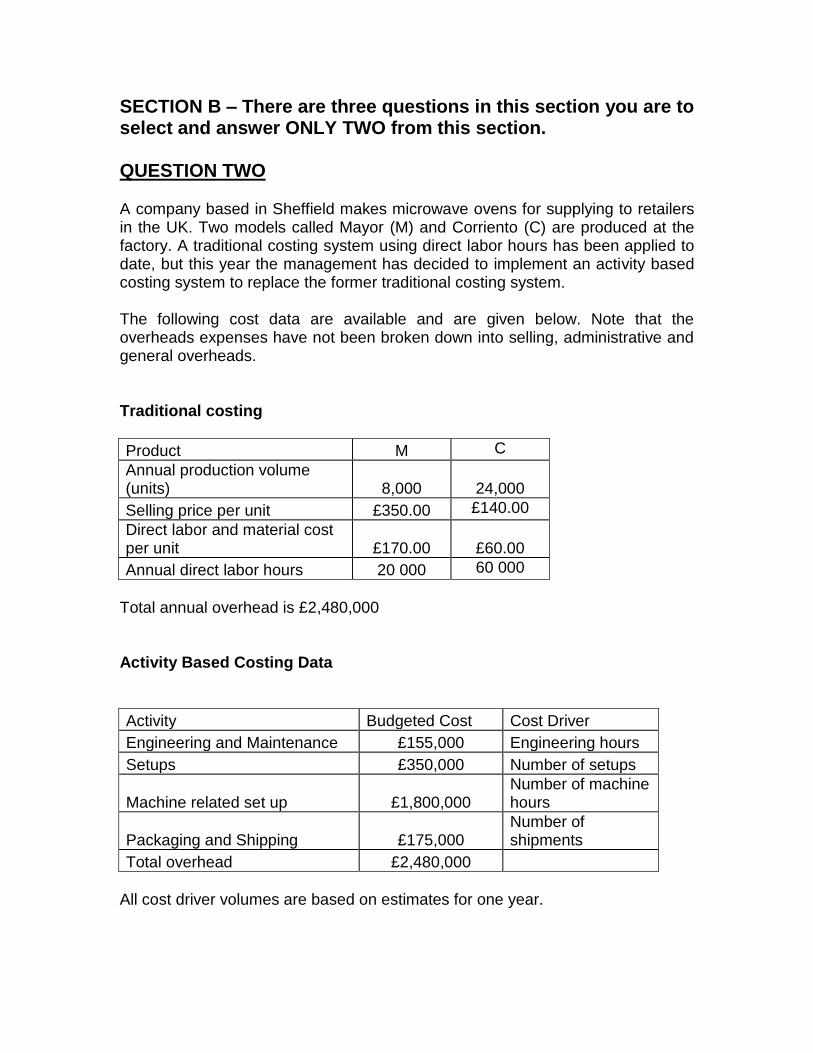

SECTION B – There are three questions in this section you are to select and answer ONLY TWO from this section. QUESTION TWO

A company based in Sheffield makes microwave ovens for supplying to retailers in the UK. Two models called Mayor (M) and Corriento (C) are produced at the factory. A traditional costing system using direct labor hours has been applied to date, but this year the management has decided to implement an activity based costing system to replace the former traditional costing system. The following cost data are available and are given below. Note that the overheads expenses have not been broken down into selling, administrative and general overheads. Traditional costing

Product M C

Annual production volume (units) 8,000

24,000

Selling price per unit £350.00 £140.00

Direct labor and material cost per unit £170.00

£60.00

Annual direct labor hours 20 000 60 000

Total annual overhead is £2,480,000 Activity Based Costing Data

Activity Budgeted Cost Cost Driver

Engineering and Maintenance £155,000 Engineering hours

Setups £350,000 Number of setups

Machine related set up £1,800,000 Number of machine hours

Packaging and Shipping £175,000 Number of shipments

Total overhead £2,480,000

All cost driver volumes are based on estimates for one year.

Cost driver M C

Engineering hours 6,000 8 000

Number of Setups 300 50

Machine hours 80,000 80 000

Number of shipments 7 000 9 000

Required:

(a) Calculate the unit cost for the two models, M and C, based on the data available for the traditional costing system. (6 marks)

(b) Calculate the unit costs for the M and C models based on the data

available for the activity based costing system. (10 marks)

(c) Using the data available measure and discuss the most significant differences between the traditional costing system and the activity based costing system in cost allocations for products M and C.

(9 marks) Total 25 marks

QUESTION THREE A company which makes sophisticated financial calculators has designed a new casing for its product which requires a different finish to the previous casing because the material type is a recently developed synthetic material and much stronger and more scratch-resistant than the previous plastic material used for the product casing. It is the first time the workforce will have to work with this new synthetic material. The design department selected a team of experienced workers to manufacture a trial batch of 10 calculators using the new material. After due consideration, management has decided to assume an 80% learning curve for production of the product, which is given below:

X ( batches of 100

units)

Y(%) X (continued) Y(%) (continued)

1 100 8 51.2

2 80 9 49.3

3 70.2 10 47.7

4 64.0 12 44.9

5 59.6 14 42.8

6 56.2 20 38.1

7 53.4 40 30.5

Also, a task analysis of the processes used to produce this first batch of calculators indicated the following direct inputs and average costs per calculator: Direct material £300 Direct labor £200 Each direct labor hour costs £90

Required:

(a) Estimate how many direct labor hours will be required to produce the fourth batch of calculators.

(5 marks) (b) What is the prime cost per calculator for the fourth batch?

(2 marks)

(c) Assume after completing and selling the first 4 batches, the company receives an order from a wholesaler for a batch of 100 calculators. How many direct labor hours will be required to produce this batch of calculators?

(4 marks) (d) If the company uses a cost plus margin approach to price its products,

what is the price per calculator for the batch in part (c) if the company, in addition to material and labor costs also incurs variable overheads which are 75% of direct labor cost. (4 marks)

(e) Critically assess some of the typical purposes for which learning curve

estimations may be used by the management accounting department. (10 marks)

Total marks 25

QUESTION FOUR (a) Explain the difference between a “push” and “pull” manufacturing system as it related to the “Just-In-Time” (JIT) inventory system. (9 marks) (b) Suppose a company operates a just-in-time (JIT) inventory system and has a dedicated set of production facilities for component X. The JIT system in place is designed in such a way that no stock of materials or finished goods is held. At start of period 1 the planned information relating to production of component X through the dedicated facilities is as follows:

Each unit of X has input materials: 3 units of material A at £18 per unit and 2 units of material B at £9 per unit.

Variable cost per unit of component X (excluding materials) is £15 per unit worked on.

Fixed costs of the dedicated facilities for the period are £162,000.

It is anticipated that 5% of the units X worked on in the process will be defective and will be scrapped.

It is estimated that customers will require, free of charge, replacement of faulty units of X at a rate of 2% of the quantity invoiced to them in fulfilment of orders. The company is pursuing a total quality management (TQM) philosophy. As a consequence of this philosophy, all losses will be treated as abnormal in recognition of a zero-defects policy and will be valued at variable cost of production. Actual statistics for period 1 are given below: Period 1 Invoiced to customers (units) 54,000 WIP (units) 61,200 Total costs: (£) Materials A & B 4,406,400 Other Variable cost of production 918,000 Fixed costs 1,620,000 Required:

(i) Prepare an analysis to show that the period 1 actual results were

achieved at the planned level in respect of: quantities and losses and unit cost levels for materials and variable costs.

(10 marks)

(ii) Use your analysis from (i) above to calculate the value of the planned level of each of the internal and external failure costs for period 1 and comment on your results.

(6 marks)

Total marks 25

END OF QUESTION PAPER