Embed Size (px)

Citation preview

Wednesday 25 February 2015

In this Issue

News and Views from the Pinsent Masons Tax teamPM-Tax

© Pinsent Masons LLP 2015

@PM_Tax

Our Comment• PAC report on PwC was a step too far by Heather Self• Revenue & Customs Brief on Skandia case by Darren Mellor-Clark• Permission granted for Judicial Review of APNs by Jason Collins• The SSE and ‘tax dodging’ by Heather Self• Increase in requests by foreign governments for tax information by James Bullock

2

Recent Articles• Ask an expert – COP9 and users of marketed avoidance schemes by Tori Magill • Charity tax reliefs: reasonable and prudent tax planning or tax avoidance? by Janet Hoskin and Chris Thomas• Will your damages be taxable? by Ian Hyde

8

Our perspective on recent casesHMRC v Royal College of Paediatrics and Child Health [2015] UKUT 0038 (TCC)Hutchings v HMRC [2015] UKFTT 0009 (TC)Workstation Farnham Ltd v HMRC [2015] UKFTT 0037 (TC)Eclipse Film Partners No 35 LLP v HMRC [2015] EWCA Civ 95 Investment Trust Companies v HMRC [2015] EWCA Civ 82

14

People 19The next edition of PM-Tax (due out on 11 March) will be a special edition looking at what the next few months have in store for UK corporates.

7722

2

PM-Tax | Wednesday 25 February 2015

PM-Tax | Our Comment>continued from previous page

Heather Self comments on the Public Accounts Committee’s (PAC’s) report on Tax Avoidance and the role of large accountancy firms.

PAC report on PwC was a step too farby Heather Self

Nobody could deny that Margaret Hodge and the PAC have played a major role in putting tax avoidance on the public, and Parliamentary, agenda. But I question whether the most recent report of the PAC, on “Tax Avoidance: the role of large accountancy firms (follow up)” serves a useful purpose. Arguably, it also goes well beyond the scope of the PAC’s role, which is to examine “the accounts showing the appropriation of the sums granted by Parliament to meet the public expenditure, and of such other accounts laid before Parliament as the committee may think fit”.

In November 2014, the International Consortium of Investigative Journalists (ICIJ) published a large number of documents showing that PwC negotiated advance tax rulings in Luxembourg for their clients. These documents are commonly referred to as the “LuxLeaks” documents, and do show that many large companies used complex financing structures involving Luxembourg companies. Some of those arrangements are already being investigated by the EU Competition Commission, to establish whether they constitute State Aid, and the OECD BEPS process is also looking more generally at whether financing structures which result in “double non-taxation” should be curbed.

The PAC’s first complaint is that “the tax arrangements PwC promoted in Luxembourg bear all the characteristics of a mass-marketed tax avoidance scheme.” This is in contrast to their evidence to the PAC in January 2013 that “we are not in the business of selling schemes.” The debate here is mainly one of semantics: PwC’s earlier evidence was in the context of mass-marketed schemes as defined by HMRC for the purposes of the DOTAS (Disclosure of Tax Avoidance Schemes) rules; PwC’s role in obtaining Luxembourg tax rulings is arguably a different matter. The structures shown in the LuxLeaks documents are undeniably complex, and in many cases illustrate how Luxembourg set out to attract international financing business by offering favourable tax treatment: it is hardly surprising that many multinational companies responded to the incentives on offer. Politicians may reasonably want international tax rules to be tightened up, but this is a matter for Parliament – it is also difficult to see how HMRC could “more actively challenge” the advice given, where that advice is in accordance with current international laws.

Recently, disclosures under DOTAS by major firms have fallen, and there are clear signs that many large companies are paying much greater attention to the reputational risk of complex structures which could be labelled as “tax avoidance”. Arguably, the PAC is therefore suggesting a solution to yesterday’s problem.

The PAC goes on to complain that there is no “business of substance” in the countries where multinational companies “shift profits in order to avoid tax”. There is a great deal of technical confusion in this assertion. Firstly, the structures examined are mainly financing structures. UK companies get a tax deduction for interest costs, provided they comply with the arm’s length principle and with anti-avoidance rules such as the unallowable purpose test and the debt cap. It is difficult to see that an interest deduction results in profits being “diverted” from the UK, as the PAC appears to believe. Secondly, the international tax system broadly taxes interest income by reference to its source, rather than looking at the substance of its recipient. So a finance company resident in Luxembourg, with very little substance, would in principle be fully taxable on its interest income. Of course, if the arrangements are wholly artificial and abusive, the UK could deny Treaty relief, but EU cases such as Cadbury Schweppes (C-196/04) have confirmed that it is not necessary to have a full-scale bank in order to be taxable locally on finance income.

Finally, the PAC concludes that “the tax industry has demonstrated very clearly that it cannot be trusted to regulate itself”, and recommends a code of conduct enforced by HMRC. As Patrick Stevens, tax policy director of the CIOT, has pointed out, there is already a code of conduct which is approved by HMRC and is regularly reviewed: it is hard to see what a new code could add, and it would also require HMRC to divert resources away from other activities which are likely to be more profitable – such as monitoring DOTAS disclosures, and strengthening the criteria for disclosure if necessary.

PM-Tax | Our Comment

This comment was published on economia.icaew.com on 11 February 2015

PM-Tax | Wednesday 25 February 2015

PM-Tax | Our Comment

3

7722

>continued from previous page

PAC report on PwC was a step too far (continued)

Let me make it clear that I fully support the OECD BEPS process, and agree that international rules need to be updated so that the tax system is fit for purpose in the 21st century. It is absolutely right that UK politicians, of all parties, should contribute to this process, and should seek to ensure that the economic profits which a company makes in the UK are taxed here. But this is a highly technical area, and I think the PAC is hindering and not helping progress by this report.

Heather Self is a Partner (non-lawyer) with almost 30 years of experience in tax. She has been Group Tax Director at Scottish Power, where she advised on numerous corporate transactions, including the $5bn disposal of the regulated US energy business. She also worked at HMRC on complex disputes with FTSE 100 companies, and was a specialist adviser to the utilities sector, where she was involved in policy issues on energy generation and renewables.

E: [email protected]: +44 (0)161 662 8066

7722

4

PM-Tax | Wednesday 25 February 2015

PM-Tax | Our Comment>continued from previous page PM-Tax | Our Comment

UK film scheme investors issued with ‘accelerated payment notices’ (APNs) demanding payments of disputed tax upfront will be able to challenge the policy in the courts.

Participants in film partnership arrangements set up by Ingenious Media, have been granted permission for a judicial review of HMRC’s new power to require payment of tax upfront, which came into force in July 2014. Pinsent Masons is representing the investors.

Ingenious Media’s film schemes have around 1,300 past and present investors. The tax tribunal is currently considering whether these schemes were run for profit, or whether they were used by individual investors as a means of avoiding tax.

APNs were introduced in July 2014 and allow HMRC to demand the payment of disputed tax associated with an avoidance scheme up front. APNs can be issued where schemes demonstrate certain ‘avoidance hallmarks’; such as the scheme being subject to disclosure requirements under the Disclosure of Tax Avoidance Schemes (DOTAS) rules or where a general anti-abuse rule (GAAR) counteraction notice has been issued. Previously, HMRC had to win a tribunal case before it could demand disputed tax in these cases. Accelerated payments will be repaid with interest in the event that the scheme is ultimately proved to work.

Where, as in the case of the ingenious schemes, taxpayers are members of a partnership, the notices issued are called Partner Payment Notices (PPNs).

According to HMRC, it has issued APNs and PPNs worth over £1 billion since the new regime came into force. Once a notice is issued, a taxpayer has 90 days to pay the tax unless they successfully make representations to HMRC that the notice should not have been issued. However, representations can only be made on the grounds that the conditions for the notice were not fulfilled – for example that the scheme was not a DOTAS scheme or that the amount of the accelerated payment claimed is incorrect. There is no right of appeal against an APN or a PPN.

In the absence of a right of appeal against an APN or a PPN, judicial review is effectively the only remedy potentially available to the recipient of an APN or PPN. Judicial review is a process through which individuals, businesses and other affected parties with “sufficient standing” can challenge the lawfulness of decisions or actions of public bodies, such as HMRC.

There are several grounds for arguing that the PPNs in these cases were unlawful, including the fact that taxpayers that are issued with one have no right to appeal, which is not compatible with human rights legislation. PPNs could also be challenged on the basis that the legislation is retrospective because it applies to DOTAS schemes which were entered into before the PPN rules came into force.

The Judicial Review will probably be heard by the High Court in the early summer. The court order includes an injunction suspending the claimant’s PPNs until the High Court gives its judgment.

It is possible for other Ingenious Media investors to join the action. Anyone who is interested or has clients who are interested should contact [email protected].

Jason Collins is our Head of Tax. He is one of the leading tax practitioners in the UK specialising in handling any form of complex dispute with HMRC in all aspects of direct tax and VAT, resolving the dispute through structured negotiation and formal mediation. Where necessary, he also handles litigation before the Tax Tribunal and all the way through to the European Court – with a particular expertise in class actions and Group Litigation Orders.

E: [email protected]: +44 (0)20 7054 2727

Permission granted for Judicial Review of APNsby Jason Collins

7722

5

PM-Tax | Wednesday 25 February 2015

>continued from previous page

Last year the CJEU ruled that services supplied by the US headquarters of insurance business, Skandia, to a Swedish branch which was VAT grouped with other local companies were subject to VAT. The court said that because the Swedish branch of Skandia was the member of a VAT group, it could no longer be treated as being the same legal entity as its US head office for VAT purposes. The creation of the VAT group established a new entity, for VAT purposes, which was an amalgam of all its members, it said.

HMRC said it would consider the implication of the decision for UK VAT groups and it has now published Revenue & Customs Brief 2 (2015) which sets out its views.

HMRC says that no changes to the UK’s VAT group provisions are required because the UK’s VAT group rules operate differently to the Swedish rules.

Under the UK’s VAT grouping provisions, a company must have an establishment in the UK to join a UK VAT group. However, unlike in Sweden, the whole body corporate is part of the VAT group, not just the branch or head office which is in the UK. Therefore services provided between an overseas establishment and a UK establishment of the body are not normally supplies for UK VAT purposes, as they are transactions within the same taxable person.

However, HMRC says that there will be implications for UK companies operating through VAT grouped branches in member state that operates similar ‘establishment only’ grouping provisions to Sweden. HMRC says that from 1 January 2016, affected businesses will have to treat intra-entity services provided to or by such establishments as supplies made to or by another taxable person and account for VAT accordingly, even if the entity is within a UK VAT group.

HMRC says that it will confirm the member states that operate similar VAT grouping rules as Sweden as soon as possible.

The changes will have cost implications for banks and insurers operating in the UK and in Sweden, or other EU member states operating similar grouping rules. These businesses cannot recover VAT paid in the same way as businesses in other sectors, as much of their business is VAT exempt.

The impact of the changes does not appear to be as damaging as businesses at first feared, following last year’s CJEU judgment. However, the policy to be implemented by HMRC from the beginning of 2016 will require businesses to undertake specific due diligence concerning the VAT rules around grouping in those member states in which they have branches.

In particular there could be problems for those UK businesses with VAT groups in Germany, the rules for which operate on both a compulsory and ‘German establishment only’ basis.

In addition to the basic legal entity principle, HMRC also confirmed that the impact of the changes would apply to any s43(2A) calculations being performed by the business.

It is probable that the combination of the prospective date of implementation along with the narrowed scope of the changes will lead many businesses to conclude that the news could have been a lot worse. However, it remains the case that a number of businesses may well see profound impact from even this more limited iteration of the VAT group principle.

One must assume that HMRC took legal advice prior to announcing the implementation and so should be reasonably confident of its position. That being said, there will be a sense of watch this space as we await any reaction from the Commission, which has, in the past, disagreed with the UK’s establishment position.

Darren Mellor-Clark is Partner (non-lawyer) in our indirect tax advisory practice and advises clients with regard to key business issues especially within the financial services, commodities and telecoms sectors. In particular he has advised extensively on the indirect tax implications arising from regulatory and commercial change within the FS sector, for example: Recovery and Resolution Planning; Independent Commission on Banking; UCITS IV; and the Retail Distribution Review.

E: [email protected]: +44 (0)20 7054 2743

PM-Tax | Our Comment

Revenue & Customs Brief on Skandia caseby Darren Mellor-Clark

7722

6

PM-Tax | Wednesday 25 February 2015

>continued from previous page

The substantial shareholdings exemption is in danger of being misunderstood.

Some campaigners have begun to campaign for the substantial shareholdings exemption (SSE) to be repealed, and have even described it as “tax-dodging”. I chaired the CIOT Technical Committee during the original consultation process, and have looked back at the documents issued at that time to give a brief historical perspective.

In the mid-90s, the key issue for UK multinationals was surplus ACT: many global companies could not offset their ACT against mainstream tax liabilities, so preferred to receive UK rather than foreign income in order to minimise the surplus. ACT could be offset against tax on capital gains, so the effective tax rate was around 10%.

ACT was, of course, abolished by the incoming Labour Government in 1997 and there was a further upheaval in the changes to the taxation of foreign profits in 2000. That consultation produced a very muted response from business, which preferred the (imperfect) existing system to radical change, and was somewhat shocked at the complexity of the eventual outcome.

So when the first consultation document on what became SSE was published in June 2000, business decided to engage actively. The original proposal was for a deferral, broadly recognising that the tax system imposed a significant difference between sales of assets (where the gain could be rolled over) and sales of shares. By the time the second document was published in November 2000, the possibility of an exemption was being contemplated.

Of course, there was a General Election in June 2001, and those of us leading the consultation responses discussed whether we should settle for deferral (which could probably have been implemented before the election) or hold out for the possibility of exemption, which would take longer and might not have been followed up by the new Government. I distinctly remember arguing for the latter, while Edward Troup (now at HMRC, but at the time involved in the consultation from the private sector) advocated the former!

Sure enough, in July 2001, a further Consultation Document was published and Gordon Brown said in the introduction:“We are designing a new relief for corporate capital gains to facilitate the process of restructuring and investment helping business take advantage of emerging global opportunities. We believe that the

proposed exemption approach has substantial attractions, a view shared by business during the initial consultation.”

The logic of the exemption, as I commented in Tax Journal last year, is that the gain on shares in a trading subsidiary broadly represents after tax profits and so should not suffer additional tax on a disposal. To the extent that there is additional value representing goodwill, rollover relief has long been available. The important point is that SSE only applies where the funds remain invested in active trading businesses – once the proceeds are paid out to shareholders, the return is taxable in their hands (as dividend or capital gain). So SSE is, in my view, consistent with the principle that profits should be taxed, but should not be taxed twice.

Without SSE, tax would become a potential distortion in commercial transactions: it is likely that a valuable but non-core business would be retained rather than triggering a tax charge, even if a new owner could derive greater future value by investing in the business. As Gordon Brown himself said in 2001,“The tax system should facilitate decision-making that is driven by commercial factors, rather than by tax considerations.”

It will, of course, be up to a new Government to decide what happens to SSE after May 2015 – but I have yet to hear any coherent argument for its abolition.

Heather Self is a Partner (non-lawyer) with almost 30 years of experience in tax. She has been Group Tax Director at Scottish Power, where she advised on numerous corporate transactions, including the $5bn disposal of the regulated US energy business. She also worked at HMRC on complex disputes with FTSE 100 companies, and was a specialist adviser to the utilities sector, where she was involved in policy issues on energy generation and renewables.

E: [email protected]: +44 (0)161 662 8066

PM-Tax | Our Comment

The SSE and ‘tax dodging’by Heather Self

This comment appeared in Tax Journal on 20 February 2015

7722

7

PM-Tax | Wednesday 25 February 2015

>continued from previous page

The number of requests foreign governments have made to HMRC to help with their own tax evasion investigations rose by 45% in 2013, from 1,701 in 2012 to 2,466 in the year to 31 December 2013 (the latest year for which information is available) as the clampdown on tax evasion by developed economies intensifies.

The largest number of requests came from Norway, which made 690 requests to the UK Government in 2013, a rise of 149 extra requests on the previous year. There were also increases in the number of requests from Ukraine, which stepped up the number of direct requests for information it made by 40% to 88, as well as smaller increases in the number of requests from France (which made 232 requests), Poland (which made 149 requests) and Spain (which made 101 requests).

The rise in the number of requests demonstrates increased activity by foreign tax authorities feeling the pressure from their governments to pursue taxpayers suspected of hiding assets and income offshore. Levels of information exchange are likely to continue to intensify; in October 2014 51 countries signed up to an automatic information exchange agreement coordinated by the OECD.

The UK, particularly London, attracts many HNW foreign nationals that come here to live or invest and this is a key reason for the high volume of requests received by the UK. Some will use the UK as a stable safe haven for their wealth, while others simply see the economy as attractive. Inevitably nearly all of them will have relatively complex tax affairs, and with the cross border exchange of tax information increasing, their chances of coming under the spotlight of their home countries’ tax authorities are growing. Even countries that do not have a desperate need to shore up their public finances are stepping up their fight against tax evasion, because it makes sense to use the new ways to obtain information that are becoming available to them.

Norway, in common with other Scandinavian countries, has long sought to achieve transparency on tax issues, making details of individual taxpayers’ tax payments publicly available. It has recently stepped up its efforts to recover underpaid taxes, introducing a tax amnesty in 2010 which allows those coming forward voluntarily to pay just the taxes and interest due, instead of the normal penalty of 60%.

The higher volume of requests from Ukraine is likely to be associated with that country’s political and economic difficulties. There is expected to be continued interest from the Ukraine authorities into the financial affairs of Ukrainian nationals with assets in London, as the new Government carries out a major anti-corruption drive, with new laws and an Anti-Corruption Bureau both introduced in late 2014. The Ukranian government is likely to use tax information sharing agreements to assist in its anti corruption drive. Much of the information they receive will be about perfectly legitimately acquired assets, but it will also be valuable in helping them to identify any individuals who may have acquired wealth, placed it overseas and be under-declaring it for tax purposes.

James Bullock is Head of our Litigation and Compliance Group. He is one of the UK’s leading tax practitioners and has been recognised as such in the leading legal directories for many years. James has over twenty years of experience advising in relation to large and complex disputes with HMRC for large corporates and high net worth individuals, including in particular leading negotiations and handling tax litigation at all levels from the Tax Tribunal to the Supreme Court and CJEU.

E: [email protected]: +44 (0)20 7054 2726

PM-Tax | Our Comment

Increase in requests by foreign governments for tax informationby James Bullock

7722

8

PM-Tax | Wednesday 25 February 2015

PM-Tax | Recent Articles

My client participated in a marketed avoidance scheme and has received a COP9 notice. He maintains there are no irregularities in his return, and an online accounting forum indicates that a number of participators in the same scheme have also received COP9. He cannot see how the scheme could be ‘fraud’ and wants to take the CDF denial route (he is happy to cooperate with the investigation). However, he is concerned about the impact of one or all of the other scheme users opting for the CDF acceptance route. Is my client more likely to be prosecuted in this scenario?

The issue of COP9 to groups of scheme users reinforces speculation that HMRC is adapting existing tools to tackle marketed avoidance. Treatment of some marketed avoidance schemes as fraudulent at user level is unsurprising when viewed in the context of the current taxscape.

Public opinion that tax avoidance is unacceptable, coupled with the perception that HMRC is ineffective at dealing with those who utilise schemes, perhaps justifies HMRC’s increasingly aggressive approach in which traditional avoidance is reclassified as evasion. But from the perspective of a user, is participation in a scheme really capable of being fraudulent evasion of tax?

Regardless of whether HMRC would be successful at convincing a jury beyond all reasonable doubt that a taxpayer’s actions amount to fraud, there is a considerably lower bar to justify the escalation of a civil fraud investigation to a criminal investigation. Since your client has received COP9, it is clear that HMRC already suspects fraud, and the proposal to issue COP 9 has been considered and approved on the basis that that suspicion is reasonable.

It is therefore critical to consider the potential for escalation from ‘civil fraud’ to criminal investigation in the taxpayer’s individual circumstances.

A holistic approachKeep the client’s mind focused on the fact that there is a chance that his scheme involvement may not be the (only) reason that HMRC issued the COP9. Whilst scheme participation may have originally put your client on HMRC’s radar, it may also have obtained information on aspects of tax returns unrelated to the scheme. There are significant risks to a strategy based on second guessing what HMRC knows or suspects. A detailed consideration of the potential problems is without doubt a more productive exercise. If your client is at all unsure about whether there are other irregularities in his tax returns, now is the time for him to tell you.

The mens reaMany taxpayers believe that the term ‘fraud’ is confined to a deliberate act to deprive HMRC of money to which it is entitled. In fact, there are levels of culpability and an omission would suffice. The blanket issue of COP9s to scheme users indicates HMRC’s belief that recklessness is sufficient culpability for fraud. This is where the level of due diligence the taxpayer carried out on the scheme may have a significant impact on whether he should accept or reject the offer of the CDF.

HMRC’s view of the schemeHMRC’s website gives updates on schemes under investigation, litigated and available settlement opportunities. Identifying similar schemes may give an indication of the current thinking, but will not give the complete picture. HMRC’s criminal investigations are excluded, and the information provided on promoter newsletters and public domain forums is often little more than propaganda issued by those with their own interests to protect.

Even if your client does not think the scheme could be considered fraudulent, he should consider whether his opinion is based on independent legal advice, or on the marketing material (and possibly counsel’s opinion) provided by the scheme’s promoters.

If he wishes to reject the offer of the CDF, it may be advisable to explain why he thought that the use of the scheme was efficacious tax planning rather than fraud. Any such explanation should be submitted with the CDF rejection letter, so that that information is available when the case is resubmitted to be considered for criminal investigation suitability. (The removal of the co-operation route for denials does not prevent you from making it clear that your client intends to cooperate and provide supporting information voluntarily. Early submission of relevant information also has a positive impact on penalty mitigation, but bear in mind that any documents submitted may be used by HMRC’s criminal investigators).

PM-Tax | Recent Articles

Ask an expert – COP9 and users of marketed avoidance schemesby Tori Magill

This article was published in Tax Journal on 13 February 2015.

PM-Tax | Wednesday 25 February 2015

PM-Tax | Recent Articles

9

7722

>continued from previous page

Ask an expert – COP9 and users of marketed avoidance schemes (continued)

It is the individual facts of the taxpayer’s case and his behaviours that influence the likelihood of prosecution rather than how everybody else who took part in the scheme responds to the offer of CDF.

Procedural prosecution within COP9Nonetheless it is worth reminding your client that the contractual nature of the CDF means there is a clear audit trail, and documents for HMRC to rely on in a subsequent prosecution. The documents submitted by the recipient may be used in court.

According to the COP9 booklet, the declaration to deny fraud creates a simple document to prosecute in its own right. Equally, failing to disclose a fraud on the disclosure form leaves that offence open to criminal investigation.

The factors beyond your client’s controlHMRC obtains documents from various sources, including other taxpayers. The admissibility of documents obtained under a civil fraud regime in a subsequent criminal prosecution is a matter for the judge and for CDF is a relatively untested area of law.

HMRC contends that information obtained from one scheme user can be used against another, so a challenge on admissibility of information may be an effective strategy. Where the promoters have been under criminal investigation themselves, legal advice on HMRC’s use and admissibility of documents obtained from the promoter may also be advisable.

Whilst it is important to ensure that your client fully understands these issues, the potential impact of what other scheme users do should always be a secondary consideration to the COP9 strategy.

One final aside: You should also consider your own involvement in the client’s decision to purchase the scheme and critically assess your and your firm’s liability. A criminal investigation into the client may result in your premises being subject to warrant, so consider obtaining legal advice if you have any concerns over risk of exposure, reputational damage or a potential conflict of interest.

Tori Magill is a Tax Director specialising in fraud and avoidance investigations, with experience gained in HMRC’s highest profile investigation roles. Tori is a former Group Leader in HMRC’s Specialist Investigations directorate, responsible for HMRC’s most complex fraud and avoidance investigations and litigation. While at HMRC Tori was HMRC’s policy expert for HMRC’s Criminal Investigations and Civil Fraud Investigations for direct tax, indirect tax and Excise duties. She was also responsible for the design and implementation of the Contractual Disclosure Facility for civil fraud investigations, and was the policy owner of HMRC’s Offshore Disclosure facilities.

E: [email protected]: +44 (0)20 7490 6419

7722

10

PM-Tax | Wednesday 25 February 2015

PM-Tax | Recent Articles

HMRC’s hardening stance on tax planning and the current political climate have left many charity trustees treading a fine line between their duty to maximise revenues for the charity’s purposes and being accused of inappropriate tax avoidance. The Charity Commission has recently issued new guidance on this issue – but does it help, and what should trustees be doing in practice?

What are the trustees’ duties in relation to tax?As readers will know, under charity law, charity trustees have a paramount fiduciary duty to act in the best interests of the charity. However, in the murky world of tax mitigation, establishing what that duty entails may not be simple. On the one hand, there is an obvious desire to maximise the charity’s income and exploit any available tax reliefs as a means of doing so. On the other, there is the threat of falling foul of anti-avoidance provisions, risk to charity assets and possible reputational damage which could result in a loss of trust, a reduction in revenue and possibly action by the Charity Commission.

What does the Commission say?It is in this context that the Commission has recently issued its new guidance note ‘Charity tax reliefs: guidance on Charity Commission policy’, which seeks to clarify where the line might be drawn. No doubt this has, in part at least, been motivated by the recent furore over the ‘Cup Trust’ and the consequent pressure from Government and public opinion to ‘get tough’ on perceived avoidance.

Interestingly, the guidance confirms that trustees positively should engage in ‘reasonable and prudent tax planning’, which is stated to include taking advantage of available tax reliefs where this will assist the work of the charity, encourage genuine donations and coincide with the purposes for which these reliefs were created. Trustees may also properly seek to organise their charity’s affairs in a way which minimises the charity’s tax liabilities when entering into transactions or arrangements.

It then goes on to reference HMRC’s definition of ‘tax avoidance’ in outlining what trustees should be wary of when managing a charity’s tax affairs – the emphasis therefore lying on whether the charity’s actions are “operating within the letter but not the spirit of the law”, or which involve artificial transactions whose only aim is to create a tax benefit. In particular trustees are warned against engaging in tax arrangements which serve to benefit private interests, where any benefit to the charity is a by-product of the arrangement rather than the principal aim, and goes on to note that it has “regulatory concern” about “any tax planning arrangements that are imprudent...or could bring the charity or the

charitable sector into disrepute”. These are, perhaps by necessity, very subjective concepts and will sometimes be difficult to apply in practice. Indeed, it seems likely that there quite often will be significant benefit accruing to private interests in one way or another. It is also notable that the Commission has chosen not to focus on existing anti-avoidance legislation such as tainted donations and non-charitable expenditure, but rather to adopt a broader test.

Having established the above concepts, the guidance gives some examples of what, in the Commission’s view, might be reasonable and prudent tax planning, such as encouraging eligible donors to use gift aid when making cash donations, giving advice on structuring legacy gifts in a will so as to attract relief from inheritance tax, or minimising irrecoverable VAT.

It also lists a number of arrangements entered into by charities that have previously been considered to be tax avoidance by HMRC. Many of these are obvious examples of avoidance and should probably fail the ‘sniff test’ of any responsible trustee. However, some charities may be concerned by the inclusion on the list of arrangements for obtaining rates relief where “negligible charitable activity subsequently takes place” in the property, and the incorrect categorisation of workers from an employment status perspective – both of which are likely to have occurred on a relatively significant scale.

What does this mean for charities?The Commission’s guidance on where the line should be drawn is helpful to a point. However, as noted above it is inherently subjective and there are widely differing views on what amounts to inappropriate tax planning, which change markedly over time. Take, for example, the Public Accounts Committee’s repeated criticism of the ways in which large corporates minimise their tax bills, which has included presenting the use by corporates of legitimate statutory tax reliefs as a form of tax avoidance. Applying this analysis to the charity sector could potentially mean that even using legitimate reliefs such as gift aid in the intended way could present a risk of criticism.

Charity tax reliefs: reasonable and prudent tax planning or tax avoidance?by Janet Hoskin and Chris Thomas

PM-Tax | Wednesday 25 February 2015

PM-Tax | Recent Articles

11

7722

>continued from previous page

Charity tax reliefs (continued)

This is of course an extreme example and unlikely to be challenged in practice. Nevertheless, it highlights that the Commission might take one view on what amounts to inappropriate tax planning whilst HMRC and indeed the public could take another – one man’s tax efficient structuring is another’s avoidance. There is also the point that tax planning which a few years ago would have been considered quite routine is now held up for public vilification. Perhaps of most concern is the Commission’s (understandable) focus on reputational issues, which presumably requires trustees to take into account the verdict of the court of public opinion, regardless of whether that accurately reflects what the legislation originally intended.

It is, therefore, a question of being alert to risk but managing that risk such that the trustees don’t miss valid and legitimate opportunities to arrange the charity’s affairs in a tax efficient manner or claim legitimate charity reliefs. There is a balance to be struck, and as always obtaining and acting upon independent professional advice will go a long way towards rebutting any suggestion that the trustees may have acted in breach of duty. However, given the potentially serious consequences of perceived avoidance (loss of tax relief, alleged breach of duty, reputational damage etc) and the uncertainties created by the prevailing political climate, many trustees will be concerned that the risks of all but the most ‘plain vanilla’ planning might exceed the benefits, and will want to revisit any existing structures which may be susceptible to criticism.

Janet Hoskin is a tax partner who is head of our charities and commercial trusts practice. Janet has expertise in all aspects of trust law specialising in commercial trust arrangements especially in insurance, banking and pensions arrangements. As part of Janet’s charities practice she specialises in work for universities on governance and the charity law implications of commercial transactions.

E: [email protected] T: +44 (0)113 294 5224

Chris Thomas is a senior associate specialising in trust law, with a particular focus on commercial trust arrangements. He advises a wide range of blue chip clients, including a large number of major insurers and financial institutions, as well as professional trustees. He also provides advice to universities on charity law issues.

E: [email protected] T: +44 (0)121 623 8699

7722

12

PM-Tax | Wednesday 25 February 2015

PM-Tax | Recent Articles

Awards and settlements in commercial disputes can be taxable in the claimant’s hands and the tax treatment needs to be considered at an early stage. The tax treatment of damages which are capital in nature and do not relate to an underlying asset is becoming less favourable.

The tax treatment of damages should be considered at an early stage as this may need to be factored into the amount claimed. Tax also needs to be considered in settlement negotiations to ensure the offer is enough.

Income or capital?The first issue affecting the tax treatment is whether the damages are income or capital in nature for the recipient.

The distinction between income and capital is complex. However, the general rule is that if the damages are to compensate for a loss of income, then the damages are themselves of an income nature, and are therefore taxed as income. However, where the compensation for loss of income relates to the whole structure of the recipient’s trade, it is capital. Where the payment relates to a capital asset (such as a property or shares), it will usually be capital in nature.

Damages which are incomeIf the damages are income in nature they will only be taxable if they fall within one of the categories of taxable income such as receipts of a trade or profession, receipts from a property business, savings income or employment income. There are also some exemptions which are more relevant to individuals, such as personal injury damages.

An example of a trading receipt is debt recovery where goods have been sold or services supplied – although in this case the trading receipt will usually have arisen by reference to when the sale took place and not when payment was made. Damages from a loss of profits claim will usually also be trading receipts.

Damages which are capital Where the damages are capital rather than income in nature the tax position is principally governed by an Extra Statutory Concession, D33. Where the damages relate to an underlying capital asset then the claimant is taxed as if it has sold part of the asset. However, where there is no underlying asset the damages can be tax exempt.

A good example of a claim with no underlying asset would be a professional indemnity claim for misleading tax or financial advice. In contrast, negligent advice on the sale of a property would relate to the ‘underlying asset’ of the property.

The tax exempt treatment where there is no underlying asset is being whittled away by HM Revenue & Customs (HMRC). In January 2014 HMRC amended D33 to limit the exemption to £500,000. Whilst relief can be granted for awards in excess of this £500,000 threshold, it must be claimed from HMRC, and in the case of corporates is unlikely to succeed. The claim can only be made once the size of the payment is known, which may be too late to influence the quantification of the claim or negotiation of the settlement.

Further, HMRC has been consulting again on making further restrictions as part of a review of Extra Statutory Concessions and incorporating them into legislation. The consultation period is now closed, and the outcome of the consultation is not yet known, but if the current proposals are enacted, they will lead to a straight £1 million limit with awards in excess of £1 million being taxable to the extent that they exceed £1 million.

Will your damages be taxable?by Ian Hyde

7722

13

PM-Tax | Wednesday 25 February 2015

PM-Tax | Recent Articles>continued from previous page

Will your damages be taxable? (continued)

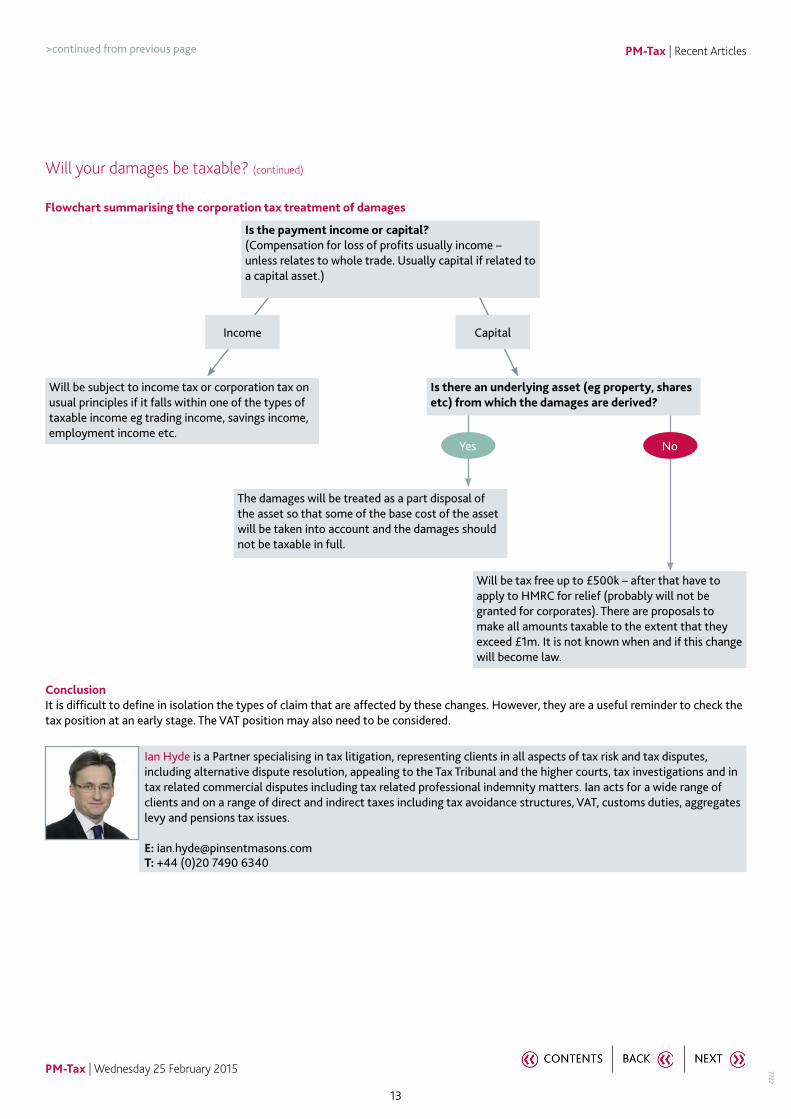

Flowchart summarising the corporation tax treatment of damages

Is the payment income or capital?(Compensation for loss of profits usually income – unless relates to whole trade. Usually capital if related to a capital asset.)

Income

Will be subject to income tax or corporation tax on usual principles if it falls within one of the types of taxable income eg trading income, savings income, employment income etc.

The damages will be treated as a part disposal of the asset so that some of the base cost of the asset will be taken into account and the damages should not be taxable in full.

Will be tax free up to £500k – after that have to apply to HMRC for relief (probably will not be granted for corporates). There are proposals to make all amounts taxable to the extent that they exceed £1m. It is not known when and if this change will become law.

Is there an underlying asset (eg property, shares etc) from which the damages are derived?

Capital

Yes No

ConclusionIt is difficult to define in isolation the types of claim that are affected by these changes. However, they are a useful reminder to check the tax position at an early stage. The VAT position may also need to be considered.

Ian Hyde is a Partner specialising in tax litigation, representing clients in all aspects of tax risk and tax disputes, including alternative dispute resolution, appealing to the Tax Tribunal and the higher courts, tax investigations and in tax related commercial disputes including tax related professional indemnity matters. Ian acts for a wide range of clients and on a range of direct and indirect taxes including tax avoidance structures, VAT, customs duties, aggregates levy and pensions tax issues.

E: [email protected]: +44 (0)20 7490 6340

7722

PM-Tax | Wednesday 25 February 2015

PM-Tax | Our Comment>continued from previous page

14

PM-Tax | Cases

Coleridge sold a building to the Royal College for over £17 million which the parties treated as a transfer of a going concern (TOGC) for VAT purposes so that VAT was not paid. HMRC said that it was not a TOGC and VAT should have been paid. The Royal College appealed and the FTT allowed the appeal. HMRC then appealed to the UT.

Coleridge had opted to waive exemption from VAT when it bought the property. It subsequently refurbished the property. The Royal College let part of its previous premises to two other charities, which wished to move with the College to its new premises.

In an attempt to make the purchase of the property a TOGC, which would not result in VAT that the Royal College would not be able to recover, Coleridge and one of the charities entered into an agreement for a lease for a single room in the property for a premium of £1,000. This lease was conditional upon Coleridge agreeing to sell the property to the Royal College by a certain date and the premium was repayable if the sale did not complete by another date. Later the same day Coleridge and the Royal College exchanged contracts for the sale of the property.

After the property sale had completed, the Royal College granted a 15 year lease to each of the charities for one room in the property.

HMRC argued that the case of Dartford Borough Council that the FTT had relied upon, could be distinguished. Dartford owned some land which they agreed with a developer to develop. The Council and the developer entered a conditional agreement with Sainsbury for buildings to be constructed on the site. However, prior to completion and before any building work or the receipt of rents, the council sold the freehold to a third party (GP), subject to the agreement with Sainsbury. The FTT decided that the sale was a TOGC.

Mr Justice Birss said that the present case was distinguishable from the Dartford case because the charity was already a tenant of the Royal College. He said the agreement for the lease and the sale of the freehold were part and parcel of the same arrangement whereas in Dartford there were two distinct transactions. “Looking at the matter from the point of view of economic activity, in Dartford the economic activity represented by the Council’s agreement with Sainsbury was a pre-existing business which stood separate from the sale of the land to GP. That pre-existing business was transferred, along with the asset (the land), to the purchaser.” he said.

He also dismissed the college’s reliance on HMRC’s guidance that “when you transfer the property to a third party (with the benefit of the prospective tenancy but before a lease has been signed) there is sufficient evidence of intended economic activity for there to be a property rental business capable of being transferred.” He said that this guidance was general guidance which did “not address a transfer of a property which includes the kind of agreement with the kind of prospective tenant as appears in this case”.

However, Mr Justice Birss dismissed HMRC’s appeal against the FTT’s decision that their claim was time barred and so HMRC’s appeal failed.

CommentThis case does not suggest that an agreement for lease with a third party with no previous connection with the buyer would prevent there being a TOGC. What was fatal in this case was the fact that the agreement for lease was with one of the Royal College’s existing tenants – it could not therefore be said that the seller was transferring the letting business to the Royal College – as the Royal College effectively already had that business. TOGC treatment needs to be considered carefully therefore if there is an existing connection between the tenant under a pre-let and the purchaser.

Read the decision

HMRC v Royal College of Paediatrics and Child Health [2015] UKUT 0038 (TCC)

An agreement for lease between the seller and an existing tenant of the purchaser of a building was not sufficient to make the purchase of the building a TOGC for VAT purposes

Cases

7722

PM-Tax | Cases>continued from previous page

Cases (continued)

Mr Hutchings received a gift from his father from an offshore, undeclared bank account less than a year before his father’s death, meaning that, following the death, the gift was subject to inheritance tax. Mr Hutchings did not inform the executors of his receipt of the gift, despite being asked, and paid it into his own offshore and undeclared bank account. HMRC found out about the bank accounts following an anonymous tip off. Mr Hutchings paid inheritance tax on the gift and HMRC also charged Mr Hutchings with a penalty of 50% of the tax due. The penalty was raised on Mr Hutchings as, although it was in respect of an incorrect return filed by the executors, it was attributable to the actions of Mr Hutchings. Mr Hutchings appealed against the penalty.

Mr Hutchings claimed that the executors were at fault as they should have informed him of the need to declare the gift as part of his father’s taxable estate. However, the FTT found as fact that the trustees had informed Mr Hutchings of the need to declare but that Mr Hutchings had not responded to their letter. The FTT held that Mr Hutchings had deliberately withheld information regarding the gift in an attempt to evade paying tax on it. As Mr Hutchings had deliberately failed to inform the trustees of the offshore gift, with the intention of evading tax, the FTT held that this action meant that the error in the IHT 400 tax return was attributable to Mr Hutchings and the penalty was upheld.

CommentThis case highlights that penalties can be charged on taxpayers who receive previously undisclosed offshore assets and continue along the path of non-disclosure. This is particularly relevant given that HMRC will soon have more information than ever before through the automatic exchange of information regimes of FATCA and then the Common Reporting Standard. In addition, anyone who has undeclared assets, inherited or otherwise, should be aware that access to the favourable offshore tax disclosure facilities will shortly close.

Read the decision

Hutchings v HMRC [2015] UKFTT 0009 (TC)

Taxpayer’s failure to disclose an offshore gift resulted in penalty for incorrect inheritance tax return

15

PM-Tax | Wednesday 25 February 2015

7722

PM-Tax | Cases>continued from previous page

Cases (continued)

The taxpayer appealed against a default surcharge of £752.32 imposed (at the 10% rate for a fourth default) for late payment of VAT in respect of VAT accounting period 11/13. HMRC cancelled the surcharge liability notice issued in respect of the first default in the cycle because it found a time to pay agreement had been in force. The result was that the default for period 11/13 became subject to default surcharge at the rate applicable to a third default (i.e. 5%). This meant the size of the surcharge reduced to £376.16 and HMRC confirmed they would not be seeking to collect it, under their general administrative practice of not enforcing default surcharges of less than £400 arising at the 2% or 5% rates for second and third defaults.

Although the taxpayer was not being charged with a default surcharge for period 11/13, Judge Kevin Poole said that the taxpayer was strictly liable to a surcharge for that period and therefore he could appeal against that liability. The judge pointed out that if the taxpayer did not appeal against the surcharge for 11/13, but committed a further default in the current cycle of defaults (leading to the imposition of a further surcharge) the Tribunal would have no jurisdiction, in the context of an appeal against the later surcharge, to consider whether there was a reasonable excuse for the 11/13 default.

In this case the judge considered that the default surcharge for 11/13 was justifiable and the taxpayer’s appeal was dismissed.

CommentThe case highlights the difficulty HMRC’s administrative relaxation in not collecting small surcharges can cause if a surcharge that is not collected by HMRC is not appealed at the time and there is a later default. The judge said “Until the legislation is changed to correct this deficiency, the only safe course for taxpayers who receive surcharge liability extension notices which have benefited from the £400 administrative relaxation is to appeal against their issue where the taxpayer considers there is a reasonable excuse for the default, even though there is no immediate financial penalty at stake. He said that although “the Tribunal is likely to be sympathetic to applications for late appeals in relation to earlier surcharge liability notices where the taxpayer is prevented by this legislative bear trap from raising any ‘reasonable excuse’ argument in relation to those earlier defaults in the context of a later default surcharge appeal” – that could not be guaranteed.

Read the decision

Workstation Farnham Ltd v HMRC [2015] UKFTT 0037 (TC)

Default surcharge could be appealed even though HMRC was not collecting the liability and if it was not appealed at the time it arose, it could not strictly be appealed at the time the taxpayer had a further default.

16

PM-Tax | Wednesday 25 February 2015

7722

>continued from previous page PM-Tax | Our Cases

Cases (continued)

Eclipse Film Partners No 35 LLP v HMRC [2015] EWCA Civ 95

Activities of film partnership did not amount to a trade.

Eclipse 35 and its members entered into a complex series of transactions in relation to the acquisition, distribution and marketing of film rights in relation to two films produced by the Disney group. Members of Eclipse 35 contributed a total of £840 million capital to Eclipse 35, much of which was funded by borrowing. They paid approximately £293 million in interest but could only claim tax relief in respect of that interest if Eclipse 35 was carrying on a trade and if the borrowed money was used wholly for the purpose of that trade.

Eclipse claimed that it carried on the trade of acquiring and exploiting film rights. HMRC said that Eclipse 35 never carried on a trade but had merely organised a sophisticated financial model involving licensing and distribution rights in respect of two Disney films designed to give a series of pre-determined cash flows and with the ultimate object of giving rise to interest payments by the members on borrowings for which they can claim tax relief to set against other income they have which is otherwise taxable.

The FTT decided that what Eclipse 35 actually did was not a trading transaction. The UT dismissed Eclipse’s appeal on the trading point and Eclipse appealed to the Court of Appeal.

The Court of Appeal said that after analysing the evidence in detail the FTT had concluded on the facts that the substantial reality was that Disney produced the films; let the rights in them to Eclipse 35, and immediately took them back again; Disney personnel created marketing plans and implemented them; and they reported back to Eclipse 35 what Disney was doing. The Court of Appeal said “Against that background the FTT’s conclusion that Eclipse 35 was not in reality carrying on a trade was justified and indeed correct. Eclipse 35 did not discharge the evidential burden of showing that it was engaged in trade in any realistic or meaningful way.”

The Court of Appeal agreed with the FTT that the fact that there was a small chance of Eclipse receiving extra payments referred to as ‘contingent receipts’ did not give the business of Eclipse 35, looking at it as a whole, a trading character. The Court said that having regard to the business as a whole, the right to contingent receipts was no more than a potential additional return on a fixed term investment.

Eclipse 35’s appeal was dismissed.

CommentThe effect of the decision is that the Eclipse 35 investors are not able to claim tax relief for the sizeable interest payments they made, but are taxed on the income received as part of the arrangements.

Read the decision

17

PM-Tax | Wednesday 25 February 2015

7722

>continued from previous page PM-Tax | Our Cases

Cases (continued)

This case concerns a number of closed-end investment trusts which obtained investment management services from management companies upon which they paid VAT. In June 2007, the ECJ ruled in Claverhouse that the exemption from VAT for the “management of special investment funds” was capable of including closed-end investment funds. In November 2007 HMRC announced that fund management services supplied to investment trust companies would be treated as exempt supplies and Items 9 and 10 of Group 5 in Schedule 9 VATA 1994 were amended. Therefore between 1 January 1990 and 1 October 2008 the UK had failed properly to transpose Article 13B(d)(6) into national legislation and managers who had supplied the services and accounted for the output tax on them were entitled to make claims for repayment under s.80 VATA 1994.

The managers made s.80 claims for refunds in respect of periods ending before 4 December 1996. HMRC repaid to the managers the amounts that the managers had paid to HMRC net of input tax deductions and the managers passed on these net amounts to the investment trusts. The example was used of £100 of VAT paid by the investment trusts to the managers, £25 input tax incurred by the managers and £75 as the net amount accounted for to HMRC by the managers.

The three-year limitation period applied to s.80 claims in respect of periods after 4 December 1996. There were therefore periods after 4 December 1996 for which the managers could not bring s.80 claims because of the three year limit. The investment trusts themselves therefore claimed directly from HMRC the difference between the VAT paid to the managers and the amount reimbursed to them (£25) and the VAT paid to the managers during the dead period, for which the managers could not bring section 80 claims

(£75). The claims were mistake-based restitutionary claims on the basis that HMRC was unjustly enriched at the investment trusts’ expense by the amount of the overpaid tax. In the alternative they said they had a direct right of recovery on the San Giorgio basis for charges levied in breach of EU law. HMRC refused these claims and the investment trusts appealed to the High Court.

The High Court held that no domestic law restitution was available as section 80(7) applied to the investment trusts as well as the managers. However, it decided that EU law required the investment trusts to be given a direct remedy to recover the whole £100 unlawfully levied VAT from HMRC because it had proved impossible or excessively difficult for the investment trusts to recover the VAT from the managers.

The CA said that “in the context of VAT the final consumer who pays the tax has a sufficient economic connection with HMRC to be able to say that they have been enriched at his expense when the tax ought never to have been imposed on the services which were supplied”. It decided that section 80(7) did not prevent claims by the investment trusts. The CA said it limited any claim for the recovery of the tax by the accounting party (the managers) to one under section 80 but did not limit claims by the investment trusts which were never accountable for the tax and did not pay it to HMRC. The CA said they could recover the £75 but not the £25 as HMRC was only unjustly enriched by the £75.

Under EU law the High Court had said that the full £100 was recoverable. The CA said that only the £75 was recoverable from HMRC. It said “Our provisional view is that there is much to be said for the view that the same principles should govern the position under EU law as determine the extent of the unjust enrichment under domestic law. In both cases the Court should have regard to the position not only at the time when the tax was paid but also having regard to the consequences of reversing the tax position. On this basis the end consumer can have no greater right of recovery against HMRC than the accounting party itself. The £25 is therefore recoverable against the managers alone. This is consistent with the principle that the repayment of the overpaid tax is to be effected through the machinery provided by the Member State which must include its own application of the VAT rules.”

CommentThis is an important decision confirming that end users can rely on UK law restitutionary rights, as well as EU law, to recover VAT that has been improperly charged.

Read the decision

18

PM-Tax | Wednesday 25 February 2015

Investment Trust Companies v HMRC [2015] EWCA Civ 82

End users can recover unlawfully charged VAT direct from HMRC to the extent that the supplier has not recovered input tax.

PM-Tax | Wednesday 25 February 2015

This note does not constitute legal advice. Specific legal advice should be taken before acting on any of the topics covered.Pinsent Masons LLP is a limited liability partnership registered in England & Wales (registered number: OC333653) authorised and regulated by the Solicitors Regulation Authority and the appropriate regulatory body in the other jurisdictions in which it operates. The word ‘partner’, used in relation to the LLP, refers to a member of the LLP or an employee or consultant of the

LLP or any affiliated firm of equivalent standing. A list of the members of the LLP, and of those non-members who are designated as partners, is displayed at the LLP’s registered office: 30 Crown Place, London EC2A 4ES, United Kingdom. We use ‘Pinsent Masons’ to refer to Pinsent Masons LLP, its subsidiaries and any affiliates which it or its partners operate as separate

businesses for regulatory or other reasons. Reference to ‘Pinsent Masons’ is to Pinsent Masons LLP and/or one or more of those subsidiaries or affiliates as the context requires. © Pinsent Masons LLP 2015.

For a full list of our locations around the globe please visit our website: www.pinsentmasons.com

Tell us what you thinkWe welcome comments on the newsletter, and suggestions for future content.

Please send any comments, queries or suggestions to: [email protected]

We tweet regularly on tax developments. Follow us at: @PM_Tax

7722

PM-Tax | PeoplePM-Tax | People

People

Our People Out and About

Jason Collins and Ian Anderson (our new senior consultant in Doha) spoke on US and UK FATCA to STEP’s Arabia branch in Dubai on 2 February.

Jason Collins also spoke to the Hong Kong Trustees’ Association on FATCA on 5 February. He has also recently appeared on Newsnight and Sky News to talk about evasion and avoidance involving offshore accounts.

James Bullock appeared on the BBC News Channel talking about HMRC and the Public Accounts Committee and also offshore bank accounts. James also spoke at a client dinner in Dubai (along with Singapore Regulatory Partner Neil McInnes) in relation to the tax–related issues in relation to enquiries and investigations into corrupt activities.

Fiona Fernie appeared on BBC News Channel and Radio 5 Live Wake up to Money discussing HMRC’s response to the disclosures concerning offshore accounts.

Heather Self spoke on diverted profits tax at the University of Oxford ‘s Centre for Business Taxation conference on 13 January. The recording of her session can be accessed here. She has also recorded a podcast on diverted profits tax for MBL seminars. Heather has also appeared on the BBC News channel recently talking about the PAC and on avoidance/evasion. Heather is also appearing in a webinar for LexisNexis on 10 March, on tax inversions.

Eloise Walker has been speaking to James Hayward of Treasury Today on points to watch out for on the Chinese GAAR. You can read a copy of her published comments here.

Members of the Share Plans Team, led by Matthew Findley and Lynette Jacobs, presented on hot topics from the world of share plans and directors’ pay including malus and clawback, post-vesting holding periods, directors’ remuneration in the 2015 AGM season and HMRC and international developments at the January Share Plans Studies Group meetings in our London, Birmingham, Edinburgh, Leeds and Manchester offices.

Matthew Findley, Lynette Jacobs and Barbara Onuonga will be presenting at the Global Equity Organisation’s Annual Conference in London in April 2015. Matthew is giving two presentations, the first, entitled “Tick tock Tick tock.....Employees aren’t saving enough – the role of reward, employee stock plans and pensions in defusing the savings time bomb” together with Carolyn Saunders of the Pinsent Masons’ Pensions Team and Peter Newhouse of Unilever and the second, “Share Ownership Guidelines – How to Handle this Global Shareholder Alignment & Governance Golden Child”, alongside Geoff Hamel of ISP; Robert Head of Pearson and Jonmichael Day of Lincoln Financial. Lynette and Barbara will be presenting on “Lessons Learned Late Night: Effective Management and Communication of Equity Awards in a Corporate Transaction”, submitted alongside one of the team’s clients, in relation to an acquisition the client made in 2014.