Embed Size (px)

Citation preview

Please provide via a weekly update or email in advance of our Budget Work Session

scheduled for 1/25/16. What I meant in my question re: the budget proposal, is that I would like to see a more detailed list of

where we are proposing to spend money equal to the amount we spent this year, rather than just having it as one line item and a big "bucket" total in our budget review document. I feel the way it was

presented last year was not detailed enough, and only had us looking at the additional funding we were

requesting, and not allowing for a good look at where we had spent our money in the past, or in general. No need to start from scratch for FY17, but we really need to have a deeper understanding of

where we are spending our money before we approve a budget. We also want to be sure our budget reflects our goals in that we are ensuring that we are investing money in the areas that we have set as

our goals. In the past, your office has provided the Excel files that allow for drilling down to see more detail, which is what I'm requesting of the December financials, and of the proposed budget. There

shouldn't be a lot of staff time involved in pulling this together--just forwarding the document.

Response: The operating budget is presented by specific categories as required by the education article

§ 5-101 to the board. The approved budget is available on our website containing detail budget line-items for each category per the Maryland State Department of Education “Financial Reporting Manual for

Maryland Public Schools” guidelines.

All categories must stay within budget parameters. However, the school system can move funding

(budgets) between categories to cover variances when necessary. If we need to move funds between categories (e.g. Instructional Salaries to Maintenance), it would require both the Board and County

Commissioner approval.

Each month, the school system is required to report the financial status of the school system to the Board

and the county government. In addition, staff has provided, at the request of the Board, provided an excel version of the report to the Board members. In the past, we have not provided a file with drill

down capabilities.

In order for me to approve and support the proposed budget, I would like to have a solid understanding

of answers to the questions I asked regarding the December Financial Reports, as they would provide some clarity for me. Prior to our Board Work Session later this month, please provide answers to all

board members for the following:

For the DECEMBER FINANCIAL REPORT:

1. Why is Equipment and other Fixed Assets over budget by 28%? Will it continue to climb? 2. Why is Special Education Contracted Services over budget by 22%? Will it continue to climb?

3. Why is Student Health Contracted Services over budget by 3%? Will it continue to climb? 4. Why is Capital Outlay Supplies and Materials over budget by 16%? Will it continue to climb?

5. Tuition Reimbursement: We are over by 10%. Are we budgeting for that increase for next year? 6. Category 03 - Instruction. Where will we be pulling the transfer money from to fund equipment and

other fixed assets overrun? Why aren't Supplies and Materials being used on par with the percentage we

are through the school year? What is included in "Other Charges," and why doesn't that have a run-rate consistent with where we are in the school year? What is included in "Transfers"?

7. Category 04 - Special Education - Roughly same questions as for Category 03 above: Where will we pull from to fund contracted services overrun, and what is included in "Other Charges" and "Transfers"?

8. Category 13-Capital Outlay. When is the bill for Contracted Services expected? Right now, we are

only 3% spent. 9. Fixed Charges - We are over budget for teachers' retirement by $791k. How did that happen? Did

we have an unexpected exodus of teachers this year, and don't we know about how much we will be paying out each year?

Response: The monthly financial statements provide a synopsis of the operating budget for both

revenues and expenditures. The report contains information for the current fiscal year (FY 2016) and the prior fiscal year (FY 2015). As a guideline, the percent of budget committed is compared to the percent

of year-end actuals from the same reporting period of the prior fiscal year.

Questions highlighted above refers to the prior year’s (FY 2015) percent of year-end actuals and may not

reflect changes or adjustments made during the second half of the fiscal year. If adjustments are made, compared to the year-end actuals, the percent will be greater than 100.

Audit follow-up question with respect to budget:

1. When the auditors gave their report to us, they recommended that we increase our reserve for funding OPEB as much as possible, with a target percentage of 75%-80%+. Where will we see that

reflected in our budget documents to show this move towards this target number? I believe Paul was to

check out other systems to see what percentages they are using for funding OPEB as we go into the budget cycle.

Response: An analysis was included in the January 16 weekly update to the Board. Please see

attachment 1.

Also, I would like to see the proposed budget from a zero-based budgeting standpoint as well--not just a

"this is what we spent last year and this is what we're asking for in addition to that." I feel I need to have a better grasp on where we spend our money before I approve a budget.

Response: The budget is formulated using a variety of concepts which best fit the particular object code.

Zero based budgeting is one of the many tools we use in the budget development process. The chart below provides a summary of the budget development methodology. Please see attachment 2.

G:\Accounting_Confidential\Carole\Special Projects\OPEB BOARD-REPORT-ITEM.docx 1

WEEKLY UPDATE

January 14, 2016

Attachments

WEEKLY ITEM FOR THE BOARD OF EDUCATION

SUBJECT:

GASB 45: Accounting for Other Post-Employment Benefits (OPEB)

OVERVIEW:

Governmental entities follow accounting standards and guidance issued by the

Governmental Accounting Standards Board (GASB). One such standard affecting the

accounting and reporting of Other Post-Employment Benefits (OPEB) offered to retirees

is GASB 45.

GASB 45 requires employers to recognize the true cost of present and future retiree

benefits (including those employees still actively employed) in their financial statements.

The long term costs of OPEB are calculated by certified actuarial accountants and are

influenced by a variety of factors included in our retiree plan and benefit design.

Prior to enacting GASB 45, governmental entities were only required to report the current

year’s cost of retirees’ benefits. These are the premiums the board pays for medical,

dental, and life insurance policies on our retirees for that year. Beginning with fiscal year

2007, GASB 45 required us to not only recognize that cost, but also:

The value of current retiree benefits for future years

The value of retiree benefits for active employees who are not yet retired for the

current and future years

FINANCIAL IMPLICATIONS:

Similar to pension trust funds that provide retirement based on salary and years of

service, the GASB pronouncements require the creation of a trust fund for retiree health

and other benefits. Prior to 2007, all governmental entities simply paid for retiree health

insurance out of the annual operating budget. Recognizing the long term cost of OPEB

has created an enormous liability on the balance sheet, which theoretically, could impact

a county’s credit rating and ability to issue bonds. To reduce this impact, GASB 45

allows an entity to amortize the long term cost of OPEB and report it as a footnote in our

financial statements, provided we fund a portion of the liability each year known as the

Annual Required Contribution (ARC).

The Annual Required Contribution (ARC) is established by the actuarial firm, and is the

amount that should be contributed into the OPEB plan by the board each year. Partial

funding of the ARC can be accomplished through “pay as you go” procedures, meaning

Attachment 1

G:\Accounting_Confidential\Carole\Special Projects\OPEB BOARD-REPORT-ITEM.docx 2

the medical, dental, and life insurance premiums actually paid on behalf of our current

retirees can be counted towards the ARC amount. However; the “pay as you go”

payments are usually not enough to cover the full cost of the ARC. In order to accumulate

enough funds to cover the future liability, governmental entities must establish a separate,

irrevocable trust fund. CCPS is in a consortium with other Maryland school systems, and

contributes to an OPEB trust managed through the Maryland Association of Boards of

Education (MABE). CCPS has made payments to this trust since fiscal year 2008, and

the accumulated amount in our OPEB trust is $26.6 million.

Two important concepts in managing OPEB are the Funded Ratio and the ARC

percentage. The actuarial value of the payments made to the OPEB trust are considered

an asset and are compared to the long term OPEB liability, resulting in a Funded Ratio

percentage1. CCPS’ Funded Ratio was 4.98% as of the June 30, 2015 valuation, which

means we have funded approximately 5% of the long term liability of OPEB.

The ARC percentage is found in the Schedule of Employer Contributions in our financial

statements1. Again, the actual contributions include the premium payments made on

retirees’ benefits during that fiscal year and any additional payments made by the board.

The schedule includes a five year summary of the required annual contribution, our actual

contributions, and the percentage of annual contributions made. CCPS’ ARC percentage

was 47.91% as of June 30, 2015.

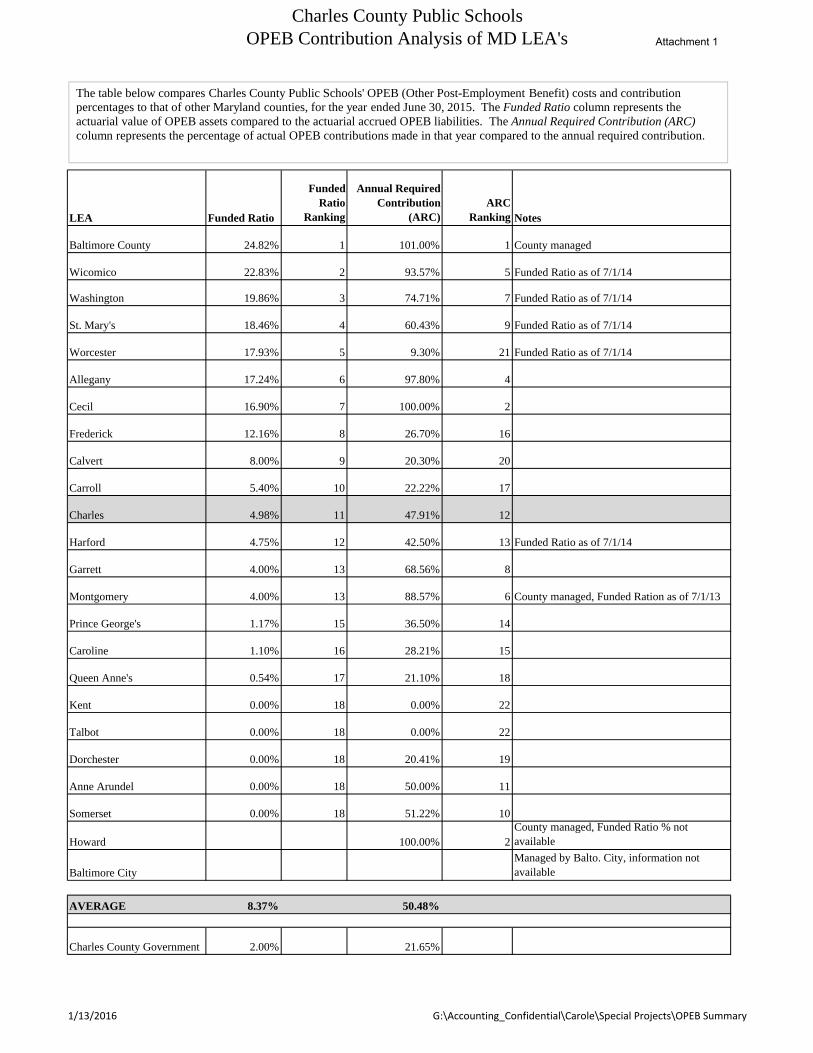

The attached analysis represents a comparison of each Maryland County’s Funded Ratio

and ARC percentage for fiscal year 2015. CCPS’s annual (ARC) funding is consistent

with the state average.

CONCLUSION:

CCPS has taken steps to address GASB 45. While the Funded Ratio remains low, we

have established an annual budget of $4 million to contribute to the OPEB trust. Annual

costs for retiree related health care were $10.6 million for fiscal year 2015 and were paid

from the annual operating budget. Fully funding the ARC in the future will require a

significant financial commitment which is not achievable in the current budget climate.

1 Annual Financial Report, June 30, 2015, Retiree Health Plan Trust, page 63

Attachment 1

Charles County Public SchoolsOPEB Contribution Analysis of MD LEA's

LEA Funded Ratio

Funded Ratio

Ranking

Annual Required Contribution

(ARC) ARC

Ranking Notes

Baltimore County 24.82% 1 101.00% 1 County managed

Wicomico 22.83% 2 93.57% 5 Funded Ratio as of 7/1/14

Washington 19.86% 3 74.71% 7 Funded Ratio as of 7/1/14

St. Mary's 18.46% 4 60.43% 9 Funded Ratio as of 7/1/14

Worcester 17.93% 5 9.30% 21 Funded Ratio as of 7/1/14

Allegany 17.24% 6 97.80% 4

Cecil 16.90% 7 100.00% 2

Frederick 12.16% 8 26.70% 16

Calvert 8.00% 9 20.30% 20

Carroll 5.40% 10 22.22% 17

Charles 4.98% 11 47.91% 12

Harford 4.75% 12 42.50% 13 Funded Ratio as of 7/1/14

Garrett 4.00% 13 68.56% 8

Montgomery 4.00% 13 88.57% 6 County managed, Funded Ration as of 7/1/13

Prince George's 1.17% 15 36.50% 14

Caroline 1.10% 16 28.21% 15

Queen Anne's 0.54% 17 21.10% 18

Kent 0.00% 18 0.00% 22

Talbot 0.00% 18 0.00% 22

Dorchester 0.00% 18 20.41% 19

Anne Arundel 0.00% 18 50.00% 11

Somerset 0.00% 18 51.22% 10

Howard 100.00% 2County managed, Funded Ratio % not available

Baltimore CityManaged by Balto. City, information not available

AVERAGE 8.37% 50.48%

Charles County Government 2.00% 21.65%

The table below compares Charles County Public Schools' OPEB (Other Post-Employment Benefit) costs and contribution percentages to that of other Maryland counties, for the year ended June 30, 2015. The Funded Ratio column represents the actuarial value of OPEB assets compared to the actuarial accrued OPEB liabilities. The Annual Required Contribution (ARC) column represents the percentage of actual OPEB contributions made in that year compared to the annual required contribution.

1/13/2016 G:\Accounting_Confidential\Carole\Special Projects\OPEB Summary

Attachment 1

1/21/2016

Description FY 2016 Base Budget

Percent of

Total Methodology

71 - SALARIES & WAGES

PART-TIME WAGES

7116 - TEACHER-SUBSTITUTE 5,401,217 1.6% Incremental Based

7119 - STIPEND-STAFF DEVELOPMENT 553,319 0.2% Program Based

7135 - EXTRA DUTY PAY 1,780,890 0.5% Contract Based

7187 - TEMPORARY EMPLOYEE 980,523 0.3% Incremental Based

7192 - OTHER EARNINGS 924,635 0.3% Contract Based

7195 - EXTENDED DAY 374,411 0.1% Program Based

7198 - OVERTIME 833,389 0.2% Incremental Based

TOTAL PART-TIME WAGES 10,848,384 3.2%

FULL-TIME SALARIES 190,162,806 56.9% Zero / Formula /Program Based - Class Size and Program Needs.

71 - SALARIES & WAGES Total 201,011,189 60.2%

72 - CONTRACTED SERVICES

7204 - BUS OPERATIONS-TO & FROM 23,795,070 7.1%

Contract /Formula Based - Per Vehicle Allotment, # Capacity Transported, Distance, Time, State Mandate Of

Limited Vehicle Life Cycle.

7229 - REPAIRS-BUILDING/GROUNDS 3,469,082 1.0% Zero Based - Fund Balance Projects And On-Going Maintenance Project Reserves

7247 - NURSING SERVICES 3,122,600 0.9% Contract Based - Health Department Of Charles County

7299 - OTHER CONTRACTED SERVICE 3,050,694 0.9% Contract Based / Incremental Based Maintenance Projects, Athletics, School Reserve

7246 - SOFTWARE MAINTENANCE 1,126,523 0.3% Contract Based - Throughout The School System

7219 - COPIER LEASE/CONTRACT 949,436 0.3% Contract /Formula Based - Xerox Copier Lease Program

7207 - CONTRACTED INSTRUCTION 727,700 0.2% Contract Based - Tri-County Youth Services Program, Space Foundation Program

7266 - SURVAILLANCE SERVICE 412,087 0.1% Contract Based - Honeywell Hvac Monitoring

7245 - HARDWARE MAINTENANCE 402,400 0.1% Contract Based - Computer Maintenance Program

7226 - REFUSE DISPOSAL 331,100 0.1% Contract Based - Refuse Removal

7214 - GAME OFFICIALS 289,622 0.1% Incremental Based - Athletic Game Officials

7241 - MAINTENANCE CONTRACT 217,920 0.1% Contract Based - Building Elevators

7217 - LEGAL FEES 205,000 0.1% Incremental Based - Legal Consultaing Fees For Court Cases

7232 - SNOW REMOVAL 200,000 0.1% Incremental Based - Based On Independent Contractors

7202 - AUDITING 197,400 0.1% Contract Based - External Audit

Miscellaneous 1,201,136 0.4% Contract Based

72 - CONTRACTED SERVICES Total 39,697,770 11.9%

73 - SUPPLIES & MATERIALS

7323 - MATERIALS OF INSTRUCTION 3,619,408 1.1% Formula Based - Based On Student Enrollment

7321 - REPAIR MATERIALS-BUILDING 856,380 0.3% Zero Based - Building Maintenance

7305 - CUSTODIAL SUPPLIES 684,389 0.2% Formula Based - Square Footage Allocation

7341 - TEXTBOOKS 576,590 0.2% Program Based - Textbook Reserve, Textbook Allocations Based On Enrollment

7328 - OFFICE SUPPLIES 406,703 0.1% Formula Based - Office Supply Reserve And Allocations Based On Enrollment

7315 - LIBRARY BOOKS 382,081 0.1% Formula Based - Library Reserves And Enrollment Allocation

7342 - VEHICLE FUEL 262,017 0.1% Incremental Based - Fuel For Ccps Vehicle Fleet

7308 - DUPLICATING SUPPLIES 195,803 0.1% Incremental Based - Print Shop Duplicating Supplies

7320 - REPAIR MATERIALS-EQUIP 175,974 0.1% Zero Based - Capital Projects

7340 - TESTING-OTHER 151,830 0.0% Formula Based - Student Testing

Miscellaneous 1,104,836 0.3% Incremental Based

73 - SUPPLIES & MATERIALS Total 8,416,011 2.5%

74 - OTHER CHARGES

7431 - UTILITIES-ELECTRICITY 6,128,000 1.8% Incremental Baseds - Based On Kilowatt Usage

7432 - UTILITIES-OIL 1,389,700 0.4% Incremental Baseds - Based On Usage Of Gallons

7450 - REAL & PERSONAL PROPERTY 621,600 0.2% Formula Based

7451 - VEHICLE & CASUALTY 497,412 0.1% Formula Based

7433 - UTILITIES-WATER & SEWAGE 448,000 0.1% Incremental Based - Gallon Usage At All Buildings

7430 - COMMUNICATIONS 434,200 0.1% Incremental Based - Telephone

7438 - PROFESSIONAL DEVELOPMENT 357,587 0.1% Program Based - Staff Development Opportunities

7437 - EMPLOYEE TRANSPORTATION 258,572 0.1% Incremental Based - Staff Mileage Reimbursement

7420 - STUDENT COMPETITIONS 178,450 0.1% Program Based - National Student Competition

Miscellaneous 392,325 0.1% Incremental Based

74 - OTHER CHARGES Total 10,705,846 3.2%

75 - EQUIPMENT

75 - EQUIPMENT Total 3,306,808 1.0% Zero Based

78 - FIXED CHARGES

7814 - INSURANCE-HOSPITALIZATION 32,335,126 9.7% Incremental Based -Claims, Enrollments, Trends

7826 - SOCIAL SECURITY 16,081,579 4.8% Formula Based

7827 - TEACHERS RETIREMENT 7,953,500 2.4% Formula Based

7842 - OPEB RESERVE 4,000,000 1.2% Zero Based

7806 - EMPLOYEE RETIREMENT 3,601,690 1.1% Formula Based

7836 - WORKER'S COMPENSATION 1,500,000 0.4% Formula Based - Claims, Enrollments, Trends

7813 - INSURANCE-LIFE 715,000 0.2% Formula Based

7828 - TUITION REIMBURSEMENT 700,000 0.2% Contract Based

7843 - ACA PAYMENTS 637,000 0.2% Formula Based - Number Of Employees

7819 - UNEMPLOYMENT COMPENSATION 200,000 0.1% Formula Based - Number Of Employees

Miscellaneous 105,000 0.0% Incremental Based

78 - FIXED CHARGES Total 67,828,895 20.3%

79 - TRANSFERS

79 - TRANSFERS Total 3,210,294 1.0% Formula Based - Tuition For Special Needs Student Placed In A Non-Public Facility

Grand Total 334,176,813 100.0%

Summary Amount $ Percent

Zero Based 201,971,050 60%

Incremental Based 50,963,330 15%

Formula Based 40,262,564 12%

Contract Based 38,939,531 12%

Program Based 2,040,356 1%

Total 334,176,831 100%

G:\Budget\FY2017\BOOK\PROPOSED\KELLY CHART.xlsxSheet1 1 of 1

Attachment 2