Embed Size (px)

Citation preview

PLANNING FOR THE NEW TAX LAW

T A X R E F O R M

2

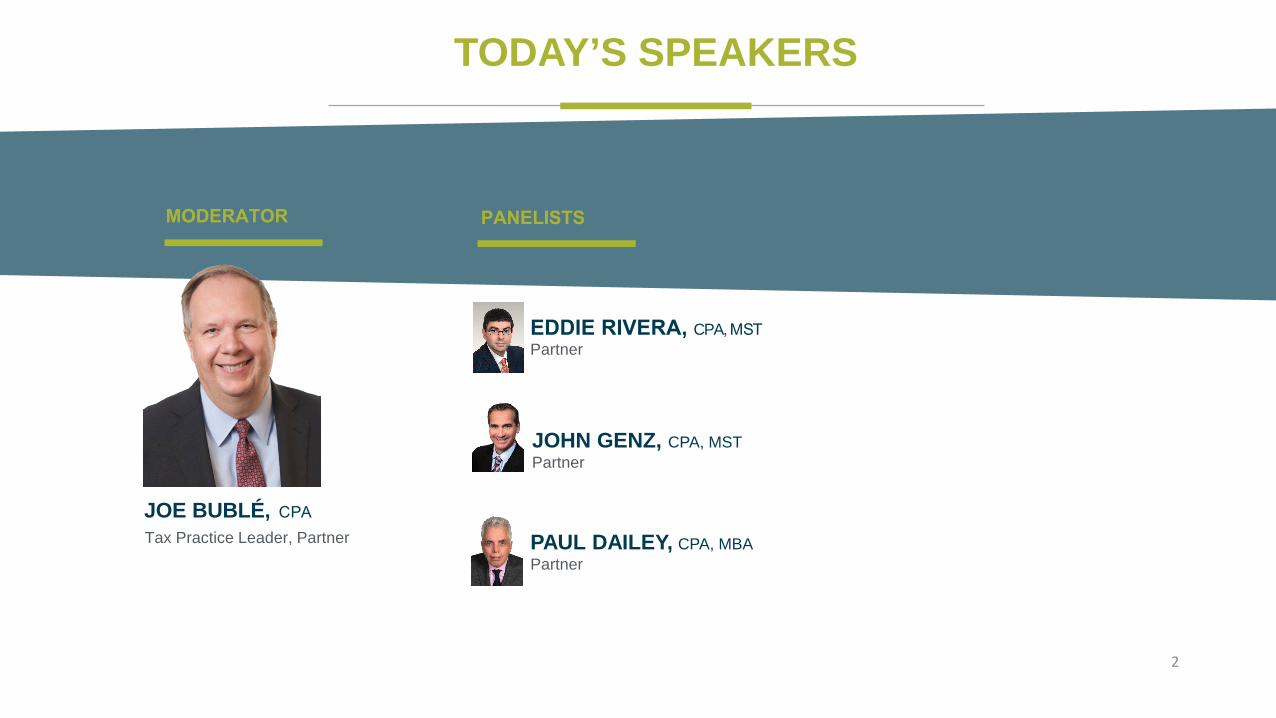

JOE BUBLÉ, C PATax Practice Leader, Partner

MODERATOR PANELISTS

JOHN GENZ, CPA, MSTPartner

PAUL DAILEY, CPA, MBAPartner

EDDIE RIVERA, CPA, MSTPartner

TODAY’S SPEAKERS

BUSINESS

PASS-THROUGH ENTITIES

INTERNATIONAL

TABLE OF CONTENTS

CORPORATE

INDIVIDUALS

BUSINESSPresented by: EDDIE RIVERA

GENERAL BUSINESS PROVISIONS

LIMITATION OF BUSINESS INTEREST DEDUCTIONS:

• Business interest expense limited to:o Business interest income plus 30% of adjusted taxable income for the year ando Floor financing interest of the taxpayer

• Adjusted taxable income is taxable income excluding:o Any income, gain, deduction, or loss not allocated to a trade or business,o Business interest income and interest deductiono NOL deductiono 20% pass-through deduction oro For years before January 1, 2022, depreciation, amortization, and depletion

• Small business exceptiono $25 million gross receiptso Attribution rules apply

• Carry-forward period of disallowed interest is unlimited5

GENERAL BUSINESS PROVISIONS

• Pass-Through Entitieso Applied at entity levelo Carryforwards allocated to owners

• Real estate trade or business opt outo Irrevocable electiono Change in depreciable liveso Bonus depreciation no longer available

6

DEPRECIATION CHANGES

SECTION 179

• Effective for tax years beginning after December 31, 2017

• Increased from $510,000 to $1,000,000

• Phase out increased from $2,030,000 to $2,500,000

• Qualified real property is expanded to include roofs, HVAC property, fire protection,and alarm and security systems.

7

DEPRECIATION CHANGES

BONUS DEPRECIATION

For qualifying assets acquired and placed in service after September 27, 2017 and before January 1, 2023:

• 100% first year deduction for assets with depreciable life of 20 years or less

• Assets can be new or used (cannot be acquired from a related party)

8

DEPRECIATION CHANGES

BONUS vs SECTION 179

• State differences

• Trade or business income limitation – section 179

• No limitation on bonus depreciation

• Qualified Improvement Property

9

DEPRECIATION CHANGES

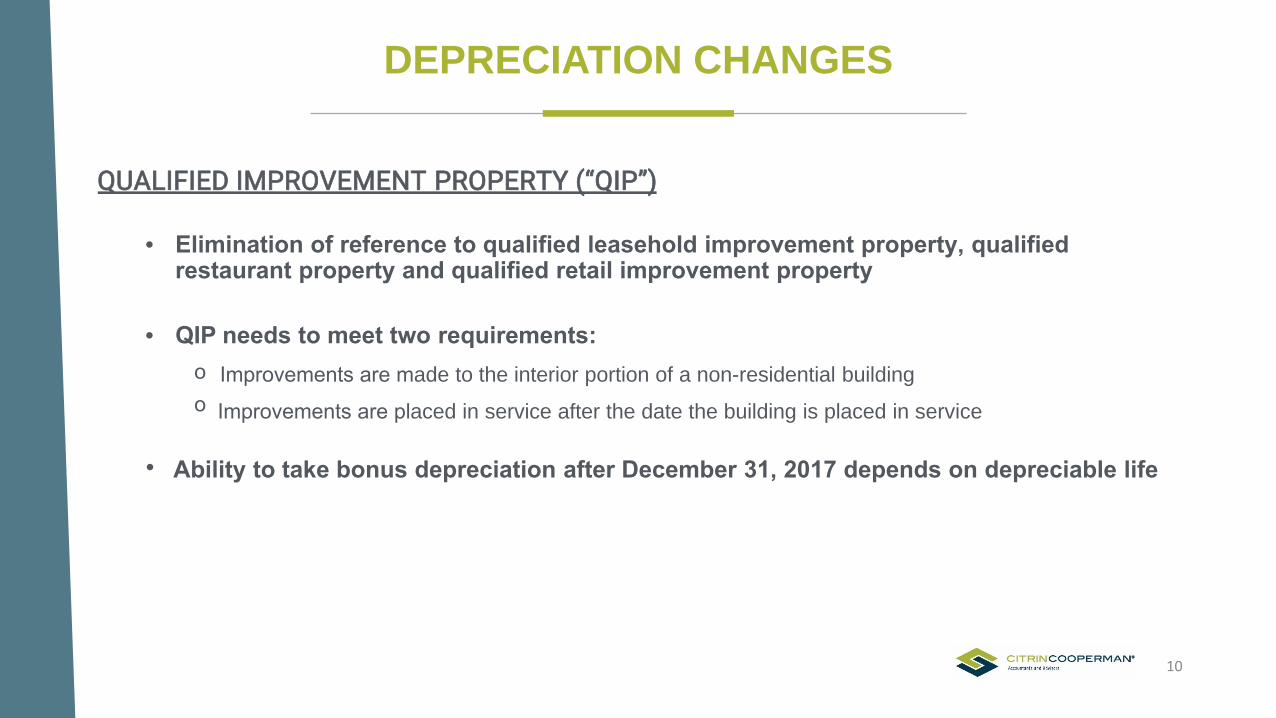

QUALIFIED IMPROVEMENT PROPERTY (“QIP”)

• Elimination of reference to qualified leasehold improvement property, qualifiedrestaurant property and qualified retail improvement property

• QIP needs to meet two requirements:o Improvements are made to the interior portion of a non-residential buildingo Improvements are placed in service after the date the building is placed in service

• Ability to take bonus depreciation after December 31, 2017 depends on depreciable life

10

GENERAL BUSINESS PROVISIONS

• Employer Deduction for Fringe Benefit Expenses limitations

• Exclusion of Entertainment Expense deduction

• Increased gross receipts threshold to $25 million

o Cash method of accountingo Accounting for inventorieso UNICAPo Accounting for small construction contracts

• Like-Kind Exchange limitation

11

QUESTIONS?

Q&A

CORPORATEPresented by: JOHN GENZ

CHANGES TO CORPORATE TAXES

• Corporate tax rates reduced

o Corporate tax rate would generally be a flat 21% rate for tax years beginning in 2018o Some of the larger firms are advising fiscal year filers to prorate the corporate rate for before and after 1/1/2018o The 21% tax rate also applies to Personal Service Corporations

• Dividends received deduction percentages reduced

o If the corporation owned at least 20% of the stock of another corporation, an 80% dividends receiveddeduction was allowed.

• For tax years beginning after Dec. 31, 2017, the 80% dividends received deduction is reduced to 65%o If the corporation owned less than 20% of the stock of another corporation, a 70% dividends received

deduction was allowed.

• For tax years beginning after Dec. 31, 2017, the 70% dividends received deduction is reduced to 50%

14

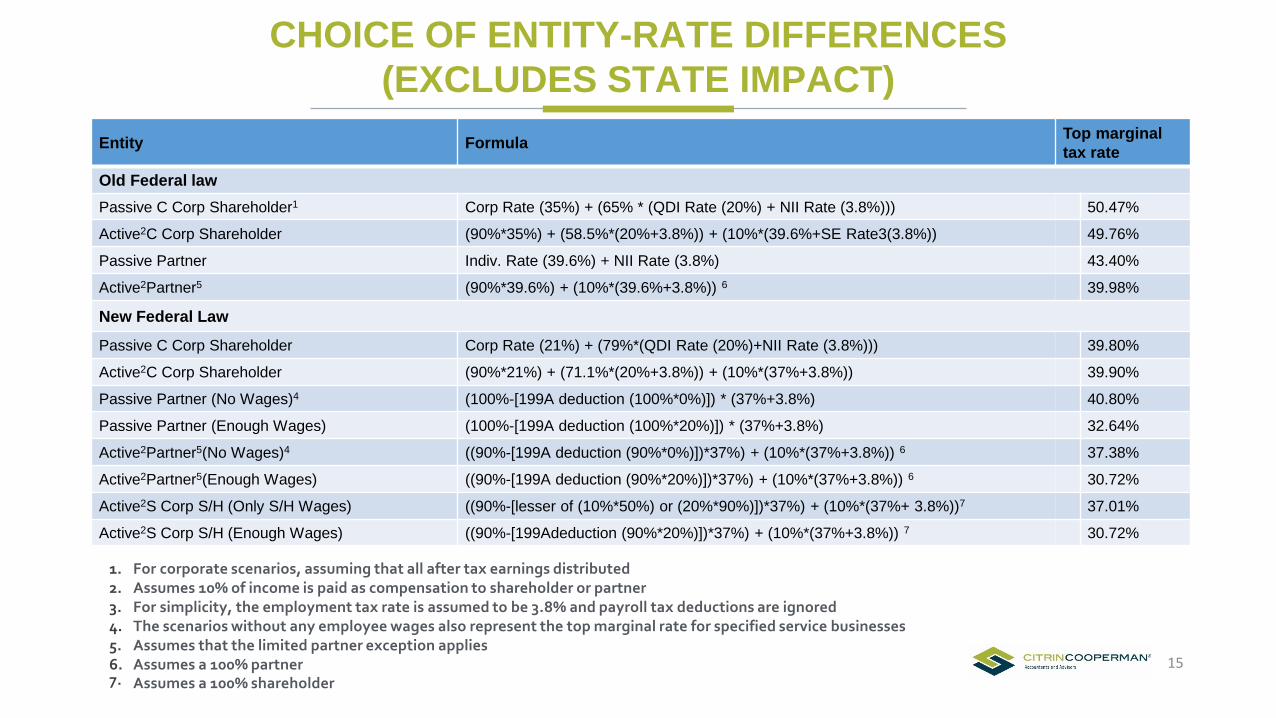

CHOICE OF ENTITY-RATE DIFFERENCES (EXCLUDES STATE IMPACT)

Entity Formula Top marginal tax rate

Old Federal lawPassive C Corp Shareholder1 Corp Rate (35%) + (65% * (QDI Rate (20%) + NII Rate (3.8%))) 50.47%

Active2C Corp Shareholder (90%*35%) + (58.5%*(20%+3.8%)) + (10%*(39.6%+SE Rate3(3.8%)) 49.76%

Passive Partner Indiv. Rate (39.6%) + NII Rate (3.8%) 43.40%

Active2Partner5 (90%*39.6%) + (10%*(39.6%+3.8%)) 6 39.98%

New Federal Law

Passive C Corp Shareholder Corp Rate (21%) + (79%*(QDI Rate (20%)+NII Rate (3.8%))) 39.80%

Active2C Corp Shareholder (90%*21%) + (71.1%*(20%+3.8%)) + (10%*(37%+3.8%)) 39.90%

Passive Partner (No Wages)4 (100%-[199A deduction (100%*0%)]) * (37%+3.8%) 40.80%

Passive Partner (Enough Wages) (100%-[199A deduction (100%*20%)]) * (37%+3.8%) 32.64%

Active2Partner5(No Wages)4 ((90%-[199A deduction (90%*0%)])*37%) + (10%*(37%+3.8%)) 6 37.38%

Active2Partner5(Enough Wages) ((90%-[199A deduction (90%*20%)])*37%) + (10%*(37%+3.8%)) 6 30.72%

Active2S Corp S/H (Only S/H Wages) ((90%-[lesser of (10%*50%) or (20%*90%)])*37%) + (10%*(37%+ 3.8%))7 37.01%

Active2S Corp S/H (Enough Wages) ((90%-[199Adeduction (90%*20%)])*37%) + (10%*(37%+3.8%)) 7 30.72%

1. For corporate scenarios, assuming that all after tax earnings distributed2. Assumes 10% of income is paid as compensation to shareholder or partner3. For simplicity, the employment tax rate is assumed to be 3.8% and payroll tax deductions are ignored4. The scenarios without any employee wages also represent the top marginal rate for specified service businesses5. Assumes that the limited partner exception applies6. Assumes a 100% partner7. Assumes a 100% shareholder

15

CHANGES TO CORPORATE TAXES

• Corporate Alternative Minimum Tax (“AMT”) repealed

o Under the old law, the corporate AMT was 20% with an exemption amount of $40,000, thatcommenced phasing out at $150,000 of alternative minimum taxable income. Certain smallerbusinesses were exempt from the AMT.

o For tax years beginning after 2017, the AMT is repealed

o However, a prior AMT credit is refundable and can offset regular tax liability in an amount equal to:

• 50% of the excess of the minimum tax credit for the tax year over the amount of the creditallowable for the year against regular tax liability

o This increases to 100% for 2021

16

CHANGES TO CORPORATE TAXES

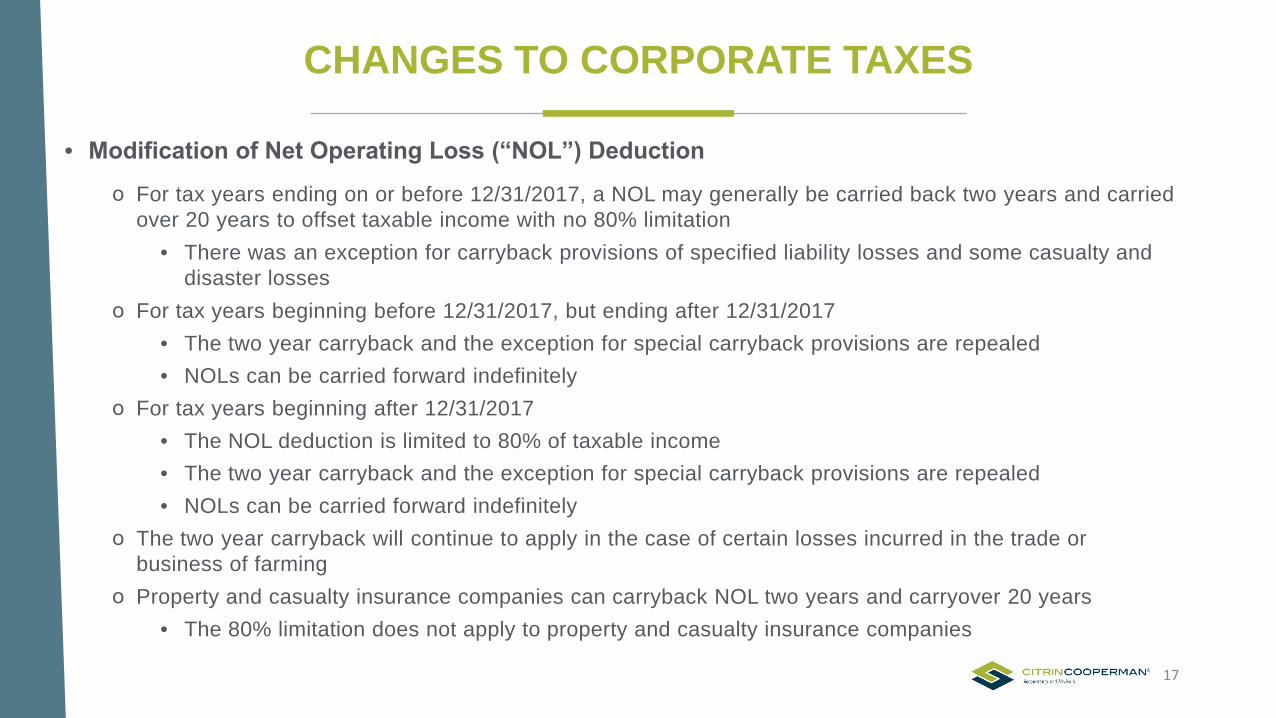

• Modification of Net Operating Loss (“NOL”) Deduction

o For tax years ending on or before 12/31/2017, a NOL may generally be carried back two years and carriedover 20 years to offset taxable income with no 80% limitation

• There was an exception for carryback provisions of specified liability losses and some casualty anddisaster losses

o For tax years beginning before 12/31/2017, but ending after 12/31/2017• The two year carryback and the exception for special carryback provisions are repealed• NOLs can be carried forward indefinitely

o For tax years beginning after 12/31/2017• The NOL deduction is limited to 80% of taxable income• The two year carryback and the exception for special carryback provisions are repealed• NOLs can be carried forward indefinitely

o The two year carryback will continue to apply in the case of certain losses incurred in the trade orbusiness of farming

o Property and casualty insurance companies can carryback NOL two years and carryover 20 years• The 80% limitation does not apply to property and casualty insurance companies

17

CHANGES TO CORPORATE TAXES

• Repeal of Domestic Production Activities Deduction (Section 199)

o Under the old law, taxpayers generally could claim a domestic production activities deduction equal to 9% ofthe lesser of the taxpayer’s qualified production activities income, or the taxpayer’s taxable income for thetax year for property that was manufactured, produced, grown, or extracted within the U.S.

o The domestic production activities deduction is repealed for tax years beginning after December 31, 2017

18

CHANGES TO CORPORATE TAXES

• Five-year write-off of Research & Experimentation (“R&E”) expenseso Under the old law:

• Taxpayers could elect to currently deduct R&E• Forgo a current deduction and amortize over the useful life of the research, but not less than 60 months;• Or elect to recover them over 10 years

o For taxable years beginning after 2021, specified R&E expenses are required to be capitalized andamortized over a 5-year period beginning with the midpoint of the tax year in which the specified R&Eexpenses were paid or incurred

• 15 years in the case of expenditures attributable to research conducted outside the U.S.• Specified R&E expenses subject to capitalization include expenses for software development, but not

expenses for land or for depreciable or depletable property used in connection with the research orexperimentation

• Also excluded are exploration expenses incurred for ore or other minerals (including oil and gas)• In the case of retired, abandoned, or disposed R&E property, any remaining basis must continue to be

amortized over the remaining life

o Prior to 2026, use of this provision is treated as a change in the taxpayer’s accounting methodo R&E credit survives

19

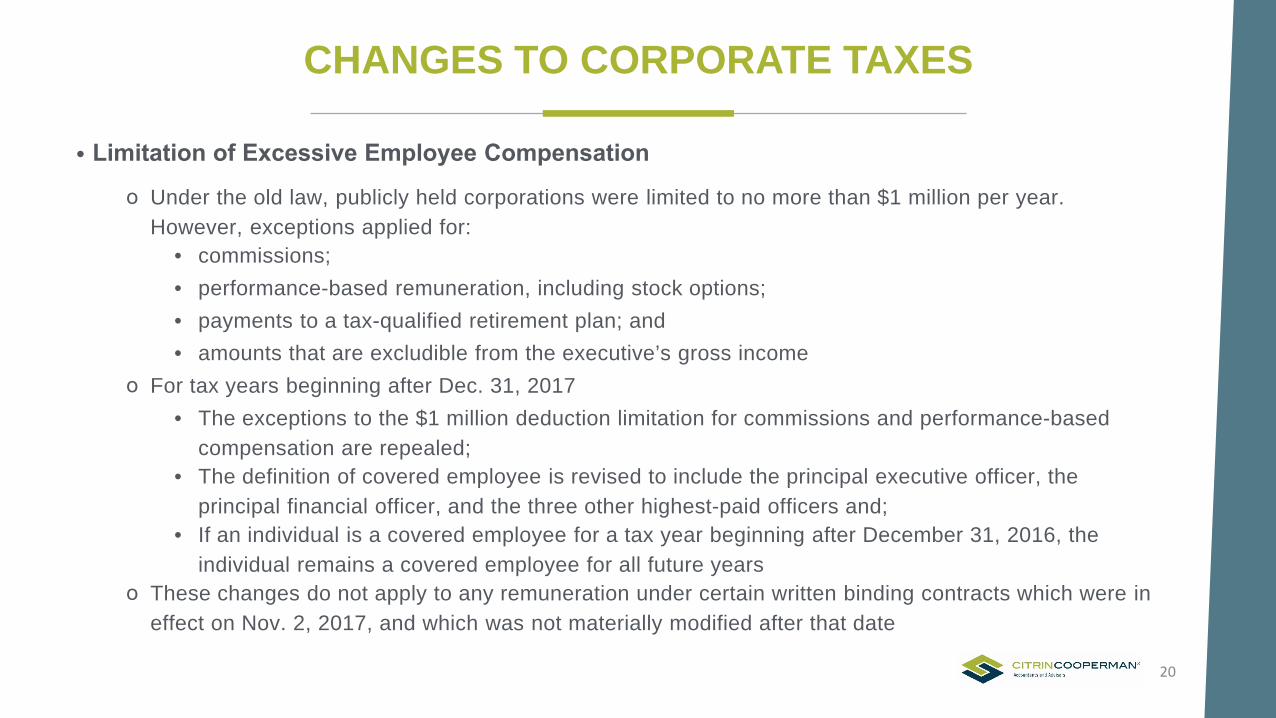

CHANGES TO CORPORATE TAXES

• Limitation of Excessive Employee Compensation

o Under the old law, publicly held corporations were limited to no more than $1 million per year.However, exceptions applied for:

• commissions;• performance-based remuneration, including stock options;• payments to a tax-qualified retirement plan; and• amounts that are excludible from the executive’s gross income

o For tax years beginning after Dec. 31, 2017• The exceptions to the $1 million deduction limitation for commissions and performance-based

compensation are repealed;• The definition of covered employee is revised to include the principal executive officer, the

principal financial officer, and the three other highest-paid officers and;• If an individual is a covered employee for a tax year beginning after December 31, 2016, the

individual remains a covered employee for all future yearso These changes do not apply to any remuneration under certain written binding contracts which were in

effect on Nov. 2, 2017, and which was not materially modified after that date

20

CHANGES TO CORPORATE TAXES

• Impact on Financial Reporting (ASC-740)o The effect of a change in tax laws or rates must be recognized at the date of enactment, December 22, 2017

• Deferred tax assets and liabilities must be adjusted for the effect of the change in tax laws or rates andsuch change may also require a reevaluation of a valuation allowance for deferred tax assets

• The effect must be included in income from continuing operations, including items of deferred tax that wereoriginally accounted for in other comprehensive income, for the period that includes the enactment date

o Since the change was enacted in 2017, an entity with a calendar year-end is required to recognize theeffect in its 2017 financial statements

o A fiscal year-end company must recognize the effect as a discrete item in the interim period of theenactment and must not apportion among interim periods remaining in the current fiscal year throughan adjustment of the annual effective rate

• Companies with deferred tax assets will recognize income tax expense, and companies with deferred taxliabilities will recognize income tax benefit

• The significant components of income tax expense attributable to continuing operations for each yearpresented, including adjustments of a deferred liability or asset for enacted changes in tax laws or rates,must be disclosed in the financial statements or footnote disclosure

o The Securities and Exchange Commission published Staff Accounting Bulletin No. 118 (SAB 118) for publiclytraded companies to ensure timely public disclosures of the accounting impacts of the legislation.

• In SAB 118, the staff addressed certain fact patterns where the accounting for such change is incompleteupon issuance of an entity’s financial statements for the reporting period of enactment

21

QUESTIONS?

Q&A

PASS-THROUGH ENTITIESPresented by: EDDIE RIVERA

SECTION 199A

QUALIFIED BUSINESS INCOME DEFINED:

The term ‘qualified business income’ means, for any taxable year, the net amount of qualified items of income, gain, deduction, and loss with respect to any qualified trade or business of the taxpayer. Such term shall not include any qualified REIT dividends, qualified cooperative dividends, or qualified publicly traded partnership income.

The term ‘qualified items of income, gain, deduction, and loss’ means items of income, gain, deduction, and loss to the extent such items are effectively connected with the conduct of a trade or business within the United States.

**Qualified Business Income does not include guaranteed payments or reasonable S-Corporation compensation.

24

WHAT ARE THE MECHANICS OF THE DEDUCTION?

In the case of a taxpayer other than a corporation, there shall be allowed as a deduction for any taxable year an amount equal to the sum of—‘‘(1) the lesser of—

‘‘(A) the combined qualified business income (defined below) amount of the taxpayer, or ‘‘(B) an amount equal to 20 percent of the excess (if any) of—

‘‘(i) the taxable income of the taxpayer for the taxable year, over‘‘(ii) the sum of any net capital gain (as defined in section 1(h)), plus the aggregate amount of the qualified cooperative dividends, of the taxpayer for the tax- able year, plus

‘‘(2) the lesser of—‘‘(A) 20 percent of the aggregate amount of the qualified cooperative dividends of the taxpayer for the taxable year, or‘‘(B) taxable income (reduced by the net capital gain) of the taxpayer for the taxable year.

25

COMBINED QUALIFIED BUINESS INCOME

Combined qualified business income is computed as follows:

1.The SUM OF

The LESSER OF:a. 20% of the taxpayers “qualified business income (defined below)” OR

2. The GREATER OF: (alternative analysis involved when income is above various thresholds)a. 50% of the W-2 wages with respect to the business, ORb. 25% of the W-2 wages with respect to the business PLUS

2.5% of the unadjusted basis of all qualified property

3. PLUS the LESSER OF:a. 20% of qualified cooperative dividends, ORb. Taxable income less net capital gain

The 20% deduction has limitations and phase outs and gets more complex when the taxable income is greater than $315,000 but less than $415,000 when MFJ, and more than $157,500 but less than $207,500 for all other taxpayers.

26

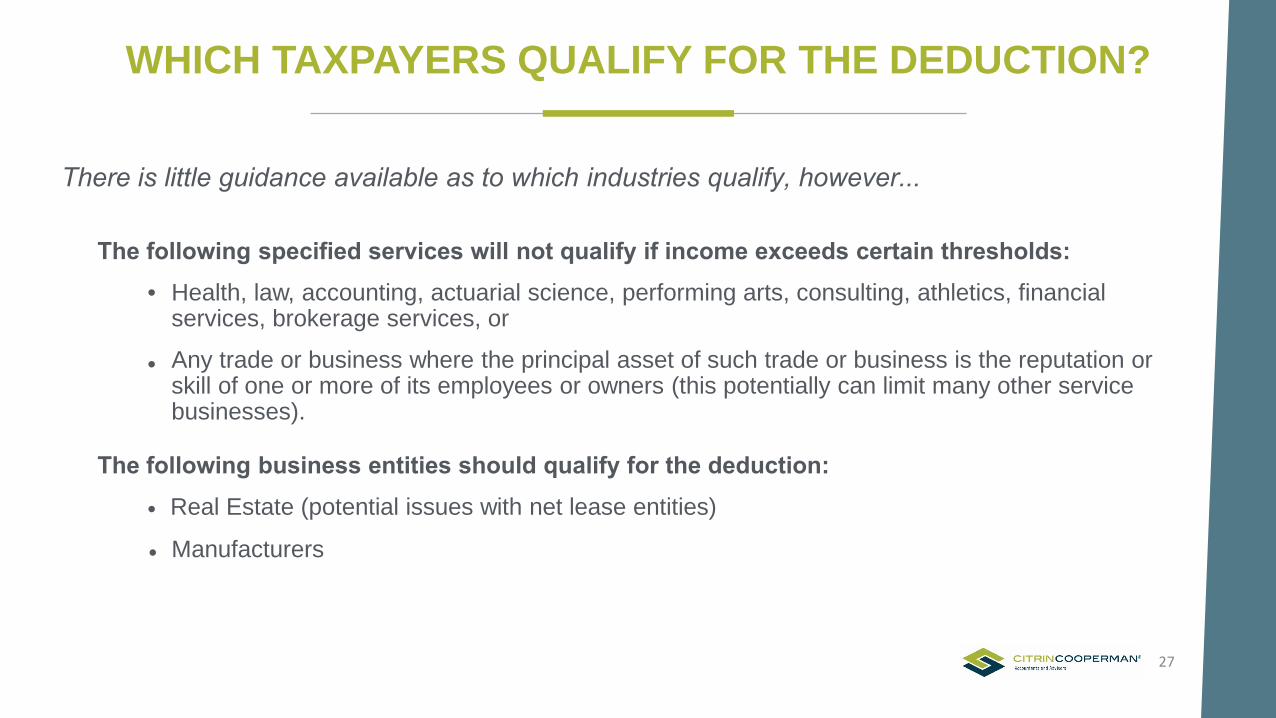

WHICH TAXPAYERS QUALIFY FOR THE DEDUCTION?

There is little guidance available as to which industries qualify, however...

The following specified services will not qualify if income exceeds certain thresholds:• Health, law, accounting, actuarial science, performing arts, consulting, athletics, financial

services, brokerage services, or

• Any trade or business where the principal asset of such trade or business is the reputation orskill of one or more of its employees or owners (this potentially can limit many other servicebusinesses).

The following business entities should qualify for the deduction:

• Real Estate (potential issues with net lease entities)

• Manufacturers

27

QUESTIONS?

Q&A

INTERNATIONALPresented by: PAUL DAILEY

MODIFIED TERRITORIAL TAX REGIME

o Adoption of dividend participation exemption system

o U.S. corporate shareholders of specified foreign corporations (SFC) allowed a full deduction againstthe foreign-source portion of dividends received

• 100% dividends received deduction (DRD)• SFC = 10%-owned foreign corporation (not including a PFIC that is not a CFC)• Applies only to C corporations• Individual and pass-through shareholders continue to be subject to the existing world-wide tax

regimeo U.S. shareholder must hold the stock of the SFC for more than 1 yearo Foreign tax credits disallowed for any dividend to which the DRD applieso Subpart F and Section 956 investment in U.S. property rules continue to apply

o Exception for hybrid dividends• Hybrid dividend = amount received from a CFC for which the CFC received a tax deduction or other

tax benefit

30

Gain recharacterized as a dividend under §1248 upon sale of SFC stock treated as a dividend for DRDo

MODIFIED TERRITORIAL TAX REGIME

• Example: Conversion of ordinary dividends to qualified dividend income (QDI)o A, an individual, owns a 20% interest in UK LTDo A receives a $1,000,000 dividend in 2018o A’s dividend is taxed at a 23.8% rate

o Assume A transferred ownership of UK LTD to NEWCO, a U.S. C corporation

The dividend from UK LTD to NEWCO would not be subject to corporate tax If NEWCO distributes the dividend to A, it would be taxed at the same 23.8% rate that would apply

if A received the dividends directly from UK LTD

o Assume A owns a 20% interest in HK LTD rather than UK LTD

If A owns HK LTD directly, the dividend from HK LTD to A would be taxed at a 37% rate because there is no income tax treaty between HK and the U.S.

HOWEVER, if A owns HK LTD through NEWCO, there would be no corporate level tax on the dividend and A would be subject to the QDI rate of 23.8% upon a dividend distribution from NEWCO

31

MANDATORY REPATRIATION TAX

• One-time toll tax on undistributed nonpreviously taxed foreign earnings and profits (E&P)• Pre-2018 accumulated deferred E&P MUST be included as Subpart F income

o E&P does not include previously taxed income (PTI) or effectively connected income (ECI)• Income inclusion for 2017 tax year for calendar year SFCs

o Payment of tax due with 2017 tax return, without regard to extensions

o Although no current guidance, taxpayers should consider basing their estimated tax payments on110%of their 2016 tax liability

• Applies to ALL U.S. shareholders of a SFC that is also a deferred foreign incomecorporation (DFIC)

o In contrast to the DRD, which is available only to corporate U.S. shareholders, the toll tax appliesto all U.S. shareholders (individuals, partnerships/LLCs, S-corporations and trusts)

o Deferral allowed for S-corporations until a triggering event occurs S-corporation shareholder must make the deferral election on a timely filed tax return for the tax

year in which there is a mandatory inclusion (i.e., for calendar year taxpayers, due date of 2017tax returns)

32

MANDATORY REPATRIATION TAX

• U.S. shareholder = U.S. person owning 10% of the vote of a DFIC• DFIC = any SFC of a U.S. shareholder that has accumulated post-1986 deferred foreign

income greater than zero• E&P measurement date greater of E&P on Nov. 2, 2017 or Dec. 31, 2017

o Accruals after November 2 will not be taken into account in computation of E&P – e.g., foreign taxesaccrue at year-end, so they will reduce E&P only at December 31 measurement date

• Allocation of E&P deficits permittedo E&P deficits of SFCs are allocated pro rata among the DFICs based upon the ratio of each DFIC’s

positive E&P over total positive E&P Allocation will impact which DFIC’s deemed paid foreign tax credits can offset the toll tax

• Election to pay over 8 yearso No interesto 8% for first 5 years, then 15%, 20% and 25% for years 6 through 8, respectivelyo Election must be made by the due date of the income tax return (2017 tax return for calendar year

taxpayers)

33

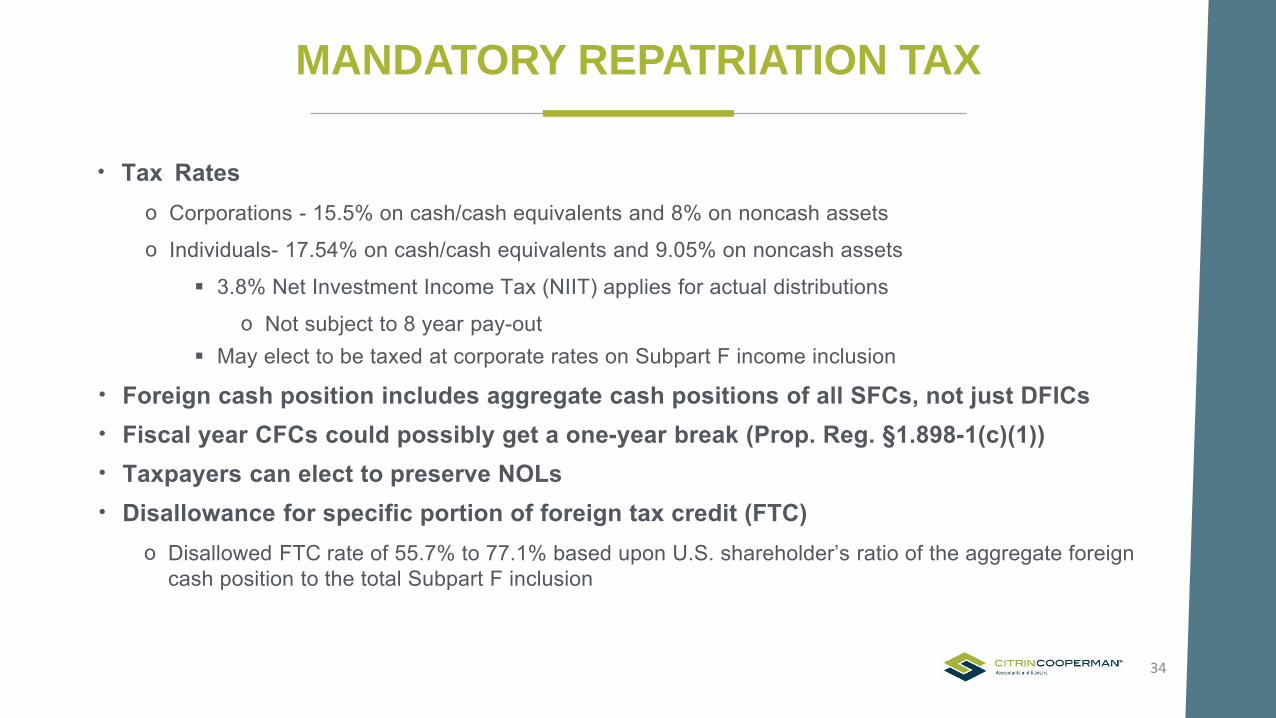

MANDATORY REPATRIATION TAX

• Tax Rateso Corporations - 15.5% on cash/cash equivalents and 8% on noncash assets

o Individuals- 17.54% on cash/cash equivalents and 9.05% on noncash assets

3.8% Net Investment Income Tax (NIIT) applies for actual distributions

Not subject to 8 year pay-out May elect to be taxed at corporate rates on Subpart F income inclusion

• Foreign cash position includes aggregate cash positions of all SFCs, not just DFICs• Fiscal year CFCs could possibly get a one-year break (Prop. Reg. §1.898-1(c)(1))• Taxpayers can elect to preserve NOLs• Disallowance for specific portion of foreign tax credit (FTC)

o Disallowed FTC rate of 55.7% to 77.1% based upon U.S. shareholder’s ratio of the aggregate foreigncash position to the total Subpart F inclusion

34

o

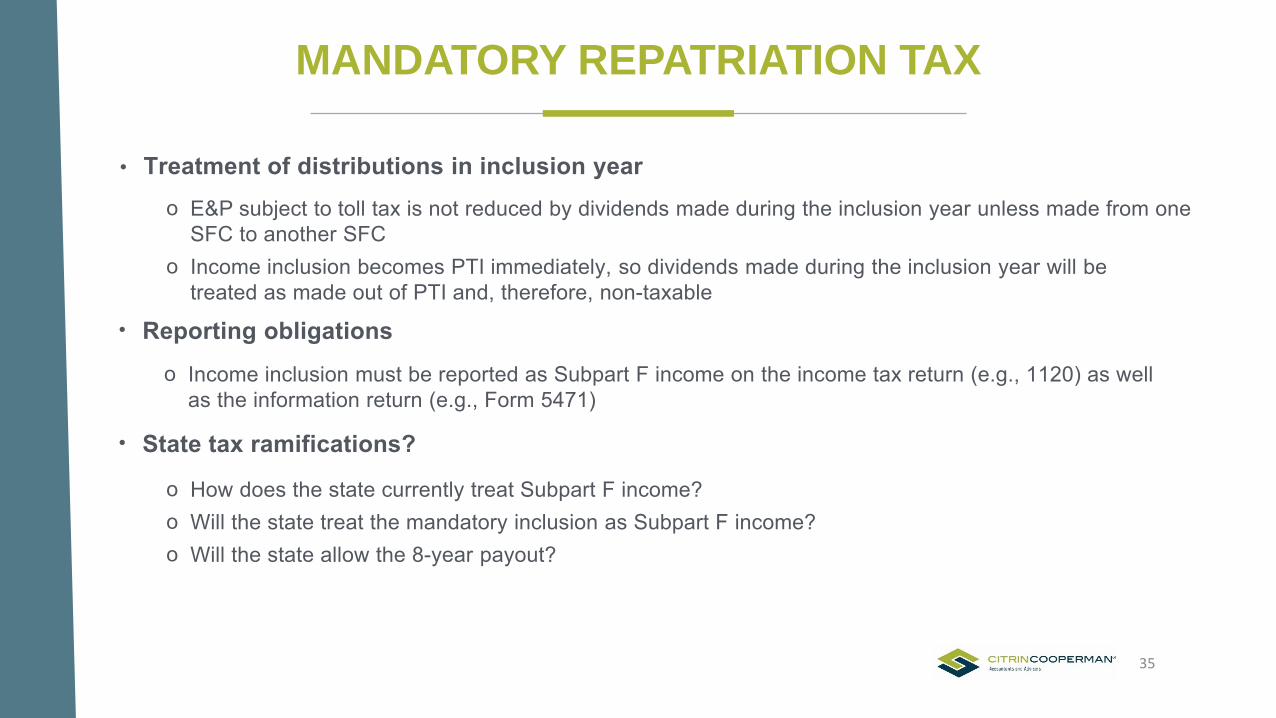

MANDATORY REPATRIATION TAX

• Treatment of distributions in inclusion yearo E&P subject to toll tax is not reduced by dividends made during the inclusion year unless made from one

SFC to another SFCo Income inclusion becomes PTI immediately, so dividends made during the inclusion year will be

treated as made out of PTI and, therefore, non-taxable

• Reporting obligations

o Income inclusion must be reported as Subpart F income on the income tax return (e.g., 1120) as wellas the information return (e.g., Form 5471)

• State tax ramifications?

o How does the state currently treat Subpart F income?o Will the state treat the mandatory inclusion as Subpart F income?o Will the state allow the 8-year payout?

35

MODIFICATIONS TO SUBPART F REGIME

• Expansion of U.S. Shareholder definition to include value as well as vote

o Effective for tax years of foreign corporations beginning after December 31, 2017o Example:

A, a U.S. person, owns 9% of the voting power of FC and 60% of the value B, a U.S. person, owns 50% of the voting power of FC C, a nonresident alien (NRA) owns 41% of the voting power of FC and 40% of the value Under prior law, FC was not a CFC, HOWEVER, beginning in 2018, FC is a CFC

• Downward attribution from foreign persons to related U.S. personso Effective for tax years of foreign corporations beginning before January 1, 2018

Expands the scope of entities (and entity owners) subject to the toll taxo For purposes of determining CFC status, a U.S. corporation, partnership, estate, or trust can be attributed

ownership of a foreign corporation from a foreign shareholder, partner, or beneficiaryo Subpart F and Section 956 income inclusions continue to be limited to U.S. shareholder’s stock held

directly, or indirectly through foreign entities

36

MODIFICATIONS TO SUBPART F REGIME

o Notice 2018-13 – Form 5471 Instructions will be amended to provide an exception from Category 5filing (CFC filing requirement) if no U.S. shareholder owns stock directly, or indirectly through foreignentities and the foreign corporation is a CFC solely because of this new downward attribution rule

o Example:

Foreign shareholders own 100% of FC FC owns 100% of DC and 80% of FC1, and DC owns the remaining 20% of FC1 Under prior law, FC1 was not a CFC, HOWEVER, DC now owns 100% of FC1 (20%directly

and 80% through attribution from FC) and, therefore, FC1 is a CFCDC is still only required to report 20% of any Subpart F income

• Repeal of 30-day minimum holding period

o Effective for tax years of foreign corporations beginning after December 31, 2017o Subpart F income inclusion required if foreign corporation is a CFC at any time during the tax year

o

37

GLOBAL INTANGIBLE LOW-TAXED INCOME (GILTI)

• Aimed at counteracting incentive created by the participation exemption to shift profits offshore• Applies to U.S. shareholders of CFCs

New foreign to U.S. downward entity attribution rule expands scope of entitiesExpanded definition of U.S. shareholder to include value broadens the scope of U.S. persons

• Treated similar to Subpart F income (NOT really Subpart F income)• Refers to shareholder’s net CFC tested income over net deemed tangible income return

o In general, GILTI is equal to gross income in excess of extraordinary returns from tangibledepreciable assets excluding ECI, Subpart F income, high-taxed income, and related party dividends

o Foreign-derived intangible income (FDII) is equal to the foreign-source portion of deemedintangible income

o

o

38

GLOBAL INTANGIBLE LOW-TAXED INCOME

• 80% deemed paid foreign tax credit is availableo Separate foreign tax credit basket applies

• U.S. corporate shareholders allowed a deduction for 37.5% of its FDII and 50% of its GILTI

GILTI deduction generally results in an effective tax rate of 10.5% for domestic corporationsFDII deduction generally results in an effective tax rate of 13.125% for domestic corporations

• Susceptible to EU assertions that it is an illegal export subsidy in violation of the WTO Agreement

oo

39

BASE EROSION ANTI-ABUSE TAX (BEAT)

• Aimed at preventing companies from stripping out U.S. earnings via deductible payments toforeign affiliates

o Targets companies that significantly reduce their U.S. tax liability with base eroding payments toforeign related parties

• Applies to C corporations with average annual gross receipts of at least $500,000,000 for thethree preceding tax years and a “base erosion percentage” of at least 3%

o Domestic corporations and foreign corporations generating ECI

• BEAT is equivalent to the excess of 10% ( 5% for 2018) of “modified taxable income” (generally,regular taxable income plus the base eroding payments such as interest and royalties) over itsregular tax liability as reduced by credits

40

SALE OF U.S. PARTNERSHIP INTEREST BY U.S. NON-RESIDENTS

• Rev. Rul. 91-32 position codified in response to taxpayer-friendly Tax Court decision inGrecian Mining case ( currently under Appeal by the IRS)

• Nonresidents selling an interest in a U.S. partnership will be taxable on the gain as deemedattributable to ECI

• Hypothetical sale mandated as if the U.S. partnership sold all of its assetso 10% WHT imposed on gross proceeds

• FIRPTA rules continue to apply to gain from the sale of real estate held by a U.S. partnership• Effective for sales after Nov. 26, 2017, however, WHT requirement only applies to

dispositions after Dec.31, 2017• Notice 2018-08 - Withholding on disposition of interest in publicly traded partnerships suspended

until additional guidance is issued (no current guidance regarding non-publicly tradedpartnership interests)

o Reduced tax rate should apply as based upon actual gain on disposition

41

SOURCING OF INCOME FROM INVENTORY SALES

• Under prior law, inventory sales were typically sourced under the 50/50 method

• Under new law, income from inventory sales is sourced solely on the basis of productionactivities with respect to the property

o If property is solely produced in the U.S., the income from the sale of the property is treated as U.S. sourceo If all production activities are conducted abroad, the sales income is treated as foreign sourceo Location where title passes is irrelevant

• Effective for tax years ending after December 31, 2017

42

SEPARATE FOREIGN TAX CREDIT BASKET FOR FOREIGN BRANCH INCOME

• Foreign branch income is required to be allocated to a separate foreign tax credit basket

o Foreign branch income = business profits attributable to qualified business units (QBUs)o Foreign branch income does not include passive income

• Effective for tax years beginning after December 31, 2017

43

PLANNING CONSIDERATIONS

• Conversion to C corporations for DRD eligibility• Section 962 election to minimize toll tax• Incorporation of foreign branches• Restructuring to avoid applicability of Subpart F regime (e.g., check-the-box planning)• Leveraged blocker structures for real estate investments – still viable under new law?

o Must be eligible for portfolio interest exemption under Section 871(h)o Should be able to claim real property trade or business exemption under new Section 163(j) 30%

EBDA limitation Trade-off is mandatory ADS depreciation

o $25M gross receipts limitation determined based upon aggregation rules Foreign sales of foreign related parties are considered

Section 448(c)(2) reduces at least 80% threshold of Section 1563(a) to at least 50%o

44

PLANNING CONSIDERATIONS

o

Estate tax considerations still exist

Differential between capital gains tax rate and corporate tax rate is now only 1%Benefit could lean towards corporate structure to the extent Section 1250 recapture rate of 25%applies

o

State tax considerationsWhile corporate structure could bear a heavier tax burden, income taxes are deductible for Federal purposes as compared to practical disallowance at the individual level

Even if Section 163(j) applies, still an effective means of repatriation

45

•

•

•

•

QUESTIONS?

Q&A

INDIVIDUALS

Presented by: JOE BUBLÉ

TAX RATE CHANGES

2018 Post Reform Tax Rate Tables

Rate Married Rate Married

10%

Single

$0 - $18,650 10%

Single

$0 - $19,050

15% $9,326 -$37,950 $18,651-$75,900 12% $9,526 - $38,700 $19,051 - $77,400

25% $37,950 - $91,900 $75,901-$153,100 22% $38,701 - $82,500 $77,401 - $165,000

28% $91,900 - $191,650 $153,101-$233,350 24% $82,501 - $157,500 $165,001 - $315,000

33% $191,651 - $416,700 $233,351-$416,700 32% $157,501 - $200,000 $315,001 - $400,000

35% $416,701 - $418,400 $416,700 - $470,700 35% $200,001 - $500,000 $400,000 - $600,000

39.6% $418,401 up $470,700 up 37% $500,000 up $600,000 up

2017 Pre-Reform Tax Rate Tables

$0 - $9,325 $0 - $9,525

48

THINGS THAT ARE GONE

• Personal Exemptions• State and Local Income and Property Tax - $10,000 exception• Miscellaneous Itemized Deductions

o Tax Preparation Feeso Investment Advisory Feeso Employee Business Expenseso Entertainment Expenses (not Meals)

• Personal Casualty Losses• Moving Expenses• Shared Responsibility Payment (2019)• Alimony Taxability and Deduction (2019 Agreements)• Gambling expenses in excess of net winnings

49

THINGS THAT HAVE CHANGED

• Interest Expenseo Mortgages

• Home Mortgages In Existence on December 15, 2017—no changes• Post 12/15/17 home acquisition interest deduction limited to principal amounts of

$750,000. Second homes continue to qualify.• Refinances post 12/15/17 grandfathered at $1 million ONLY up to debt level at date of

refinance. (No cashing out of equity).

o Home Equity Line of Credit• Interest allowed on HELOC only to extent proceeds were used to acquire, construct or

substantially renovate property.

• EXAMPLE-$200,000 HELOC used in 2016 to buy $100,000 car and $100,000 to repair andreplace roof on home. In 2018 interest on roof repair only deductible.

50

THINGS THAT HAVE CHANGED

• Medical Expenses deductible to extent they exceed 7.5% of Adjusted Gross Income, down from 10%

• Charitable Contributions to Public charities limit increased from 50% of AGI to 60% of AGI

• Standard Deduction almost doubled to $24,000 for married couple.o Timing of Deductions

• Child Credit Increased to $2,000 per child and $500 per non child dependento Credit fully available until AGI reaches $400,000. ($200,000 single).o Up to $1,400 refundable if tax liability is zero.

• Stock Option Income recognition from grants by private companies can be deferred for five years• Business losses limited to $500,000 per year. Any excess carried forward as Net Operating Loss.• Net Operating Losses cannot be carried back. Can be carried forward indefinitely

o Use of losses limited to 80% of taxable income for post 2017 losses.

51

ALTERNATIVE MINIMUM TAX

• An alternative tax system that disallows many deductions and taxes income at alower rate (For 2017: 28% vs 39.6%).

• Taxpayer pays the higher of the two computations.

• Currently (2017 and prior) the largest disallowed expenses for AMT are state and localincome and real estate taxes and miscellaneous itemized deductions.

52

ALTERNATIVE MINIMUM TAX – 2018 VERSION

• For 2018 28% vs 37%

• AMT exemption increased

• With state and local taxes and miscellaneous itemized deductions repealed, the largestcause of AMT eliminated

• Anticipation is that many who were hit with AMT in the past will no longer be so.

53

QUESTIONS?

Q&A

CONTACT US

JOHN GENZ

(347) [email protected]

PAUL DAILEY(347) [email protected]

JOE BUBLÈ

(646) [email protected]

EDDIE RIVERA

55

(973) [email protected]

THANK YOU