Embed Size (px)

Citation preview

PJSC RosneftInvestor Presentation

13.09.2016

August 2016

Important Notice

Information herein has been prepared by the Company. The presented conclusions are based on the general informationcollected as of the date hereof and can be amended without any additional notice. The Company relies on the informationobtained from the sources which it deems credible; however, it does not guarantee its accuracy or completeness.

These materials contain statements about future events and explanations representing a forecast of such events. Anyassertion in these materials that is not a statement of historical fact is a forward-looking statement that involves known andunknown risks, uncertainties and other factors, which may cause our actual results, performance or achievements to bematerially different from any future results, performance or achievements expressed or implied by such forward-lookingstatements. We assume no obligations to update the forward-looking statements contained herein to reflect actual results,changes in assumptions or changes in factors affecting such statements.

This presentation does not constitute an offer to sell, or any solicitation of any offer to subscribe for or purchase anysecurities. It is understood that nothing in this report / presentation provides grounds for any contract or commitmentwhatsoever. The information herein should not for any purpose be deemed complete, accurate or impartial. The informationherein in subject to verification, final formatting and modification. The contents hereof has not been verified by the Company.Accordingly, we did not and do not give on behalf of the Company, its shareholders, directors, officers or employees or anyother person, any representations or warranties, either explicitly expressed or implied, as to the accuracy, completeness orobjectivity of information or opinions contained in it. None of the directors of the Company, its shareholders, officers oremployees or any other persons accepts any liability for any loss of any kind that may arise from any use of this presentationor its contents or otherwise arising in connection therewith.

Information herein has been prepared by the Company. The presented conclusions are based on the general informationcollected as of the date hereof and can be amended without any additional notice. The Company relies on the informationobtained from the sources which it deems credible; however, it does not guarantee its accuracy or completeness.

These materials contain statements about future events and explanations representing a forecast of such events. Anyassertion in these materials that is not a statement of historical fact is a forward-looking statement that involves known andunknown risks, uncertainties and other factors, which may cause our actual results, performance or achievements to bematerially different from any future results, performance or achievements expressed or implied by such forward-lookingstatements. We assume no obligations to update the forward-looking statements contained herein to reflect actual results,changes in assumptions or changes in factors affecting such statements.

This presentation does not constitute an offer to sell, or any solicitation of any offer to subscribe for or purchase anysecurities. It is understood that nothing in this report / presentation provides grounds for any contract or commitmentwhatsoever. The information herein should not for any purpose be deemed complete, accurate or impartial. The informationherein in subject to verification, final formatting and modification. The contents hereof has not been verified by the Company.Accordingly, we did not and do not give on behalf of the Company, its shareholders, directors, officers or employees or anyother person, any representations or warranties, either explicitly expressed or implied, as to the accuracy, completeness orobjectivity of information or opinions contained in it. None of the directors of the Company, its shareholders, officers oremployees or any other persons accepts any liability for any loss of any kind that may arise from any use of this presentationor its contents or otherwise arising in connection therewith.

2

4.1

4.1

5.2

10.3

3.4

2.3

59

83

131

bln boe mmboed $/boe

Hydrocarbon reserves1 Hydrocarbon production2 Lifting costs3

Global Leader in Reserves, Production and Efficiency

2.3

2.5

2.7

3.3

3.6

14.6

13.4

13.0

11.3

10.4

13.09.2016

31

37

38

50

52

Liquids Gas

3Note: (1) Rosneft ABC1+C2 reserves under Russian classification as of Jan 1, 2016, data for other companies is taken from Wood Mackenzie reserve estimates including commercial andsub-commercial reserves; (2) Data for 1H2016; (3) Rosneft, Petrobras, Lukoil , Petrochina data for 1H2016, other competitors – for 2015.

The Company's environmental policy was approved. Itdefines Rosneft’s goals, objectives and principles inenvironmental protection

Program to improve the environmental efficiency by 2025 inplace. Its implementation will help achieving strategic goalsin the environmental protection

International organization BSI confirmed the compliance ofHSE Information System with ISO 14001, highlighting thestrengths of the environmental management system werepointed out

The approved marine ecosystems biodiversity preservationprogram is being implemented in the Rosneft license areaslocated in the Arctic zone of the Russian Federation till 2020

The Company and World Wildlife Fund (WWF) RussianOffice are implementing agreed Road Map of activities for2015-2016

Environmental Protection Activities

The Company's objective in environmental protection is to be the leader inenvironmental safety among oil and gas companies

Key 2015 results The Company's environmental policy was approved. It

defines Rosneft’s goals, objectives and principles inenvironmental protection

Program to improve the environmental efficiency by 2025 inplace. Its implementation will help achieving strategic goalsin the environmental protection

International organization BSI confirmed the compliance ofHSE Information System with ISO 14001, highlighting thestrengths of the environmental management system werepointed out

The approved marine ecosystems biodiversity preservationprogram is being implemented in the Rosneft license areaslocated in the Arctic zone of the Russian Federation till 2020

The Company and World Wildlife Fund (WWF) RussianOffice are implementing agreed Road Map of activities for2015-2016

4

RUB 71.7 bln – environmental protectionexpenses of which

RUB 44.7 bln capital investments aimedat reducing negative impact on the

environment (+65% vs. 2012)

0,282

0,3290,298

0,327

LTIF 2014

LTIF 2015

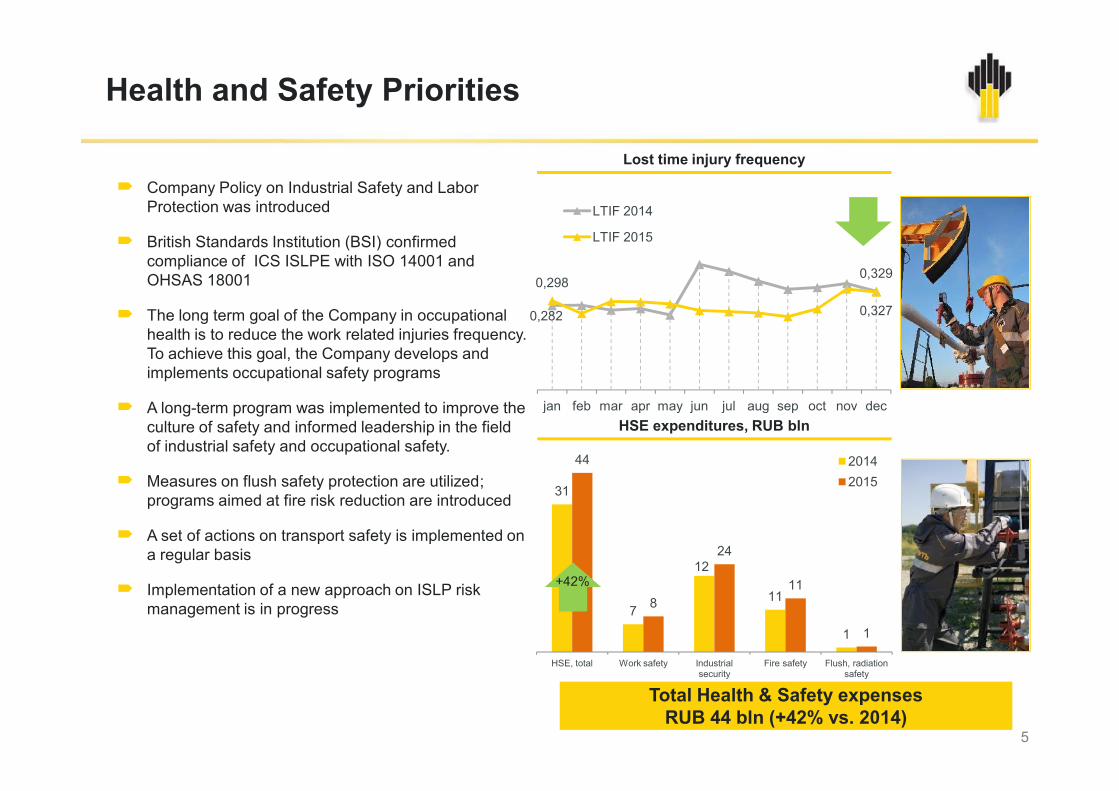

Lost time injury frequency

Health and Safety Priorities

Company Policy on Industrial Safety and LaborProtection was introduced

British Standards Institution (BSI) confirmedcompliance of ICS ISLPE with ISO 14001 andOHSAS 18001

The long term goal of the Company in occupationalhealth is to reduce the work related injuries frequency.To achieve this goal, the Company develops andimplements occupational safety programs

A long-term program was implemented to improve theculture of safety and informed leadership in the fieldof industrial safety and occupational safety.

Measures on flush safety protection are utilized;programs aimed at fire risk reduction are introduced

A set of actions on transport safety is implemented ona regular basis

Implementation of a new approach on ISLP riskmanagement is in progress

jan feb mar apr may jun jul aug sep oct nov dec

31

7

12

11

1

44

8

24

11

1

HSE, total Work safety Industrialsecurity

Fire safety Flush, radiationsafety

20142015

5

HSE expenditures, RUB bln

+42%

Company Policy on Industrial Safety and LaborProtection was introduced

British Standards Institution (BSI) confirmedcompliance of ICS ISLPE with ISO 14001 andOHSAS 18001

The long term goal of the Company in occupationalhealth is to reduce the work related injuries frequency.To achieve this goal, the Company develops andimplements occupational safety programs

A long-term program was implemented to improve theculture of safety and informed leadership in the fieldof industrial safety and occupational safety.

Measures on flush safety protection are utilized;programs aimed at fire risk reduction are introduced

A set of actions on transport safety is implemented ona regular basis

Implementation of a new approach on ISLP riskmanagement is in progress

Total Health & Safety expensesRUB 44 bln (+42% vs. 2014)

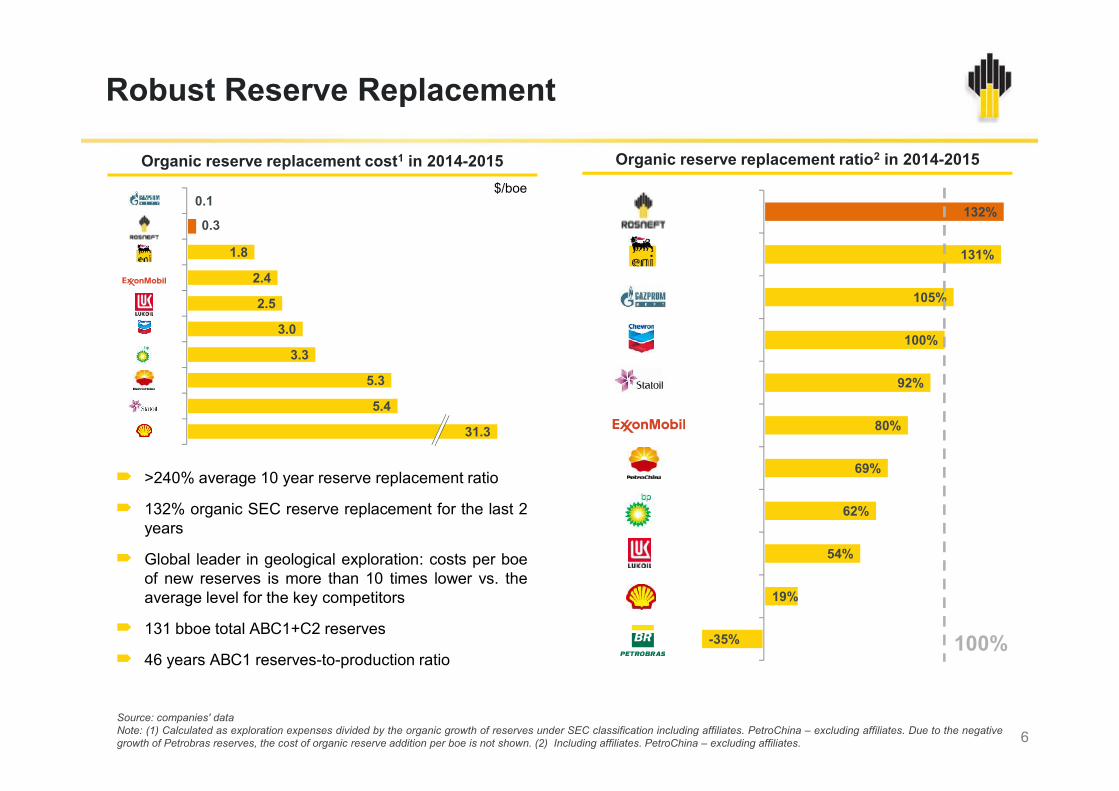

Robust Reserve Replacement

92%

100%

105%

131%

132%

5.3

3.3

3.0

2.5

2.4

1.8

0.3

0.1

Organic reserve replacement cost1 in 2014-2015 Organic reserve replacement ratio2 in 2014-2015

$/boe

6

>240% average 10 year reserve replacement ratio

132% organic SEC reserve replacement for the last 2years

Global leader in geological exploration: costs per boeof new reserves is more than 10 times lower vs. theaverage level for the key competitors

131 bboe total АВС1+С2 reserves

46 years АВС1 reserves-to-production ratio

Source: companies' dataNote: (1) Calculated as exploration expenses divided by the organic growth of reserves under SEC classification including affiliates. PetroChina – excluding affiliates. Due to the negativegrowth of Petrobras reserves, the cost of organic reserve addition per boe is not shown. (2) Including affiliates. PetroChina – excluding affiliates.

-35%

19%

54%

62%

69%

80%31.3

5.4

100%

Gas

Liquid HC

~6.0

2.5

5.2

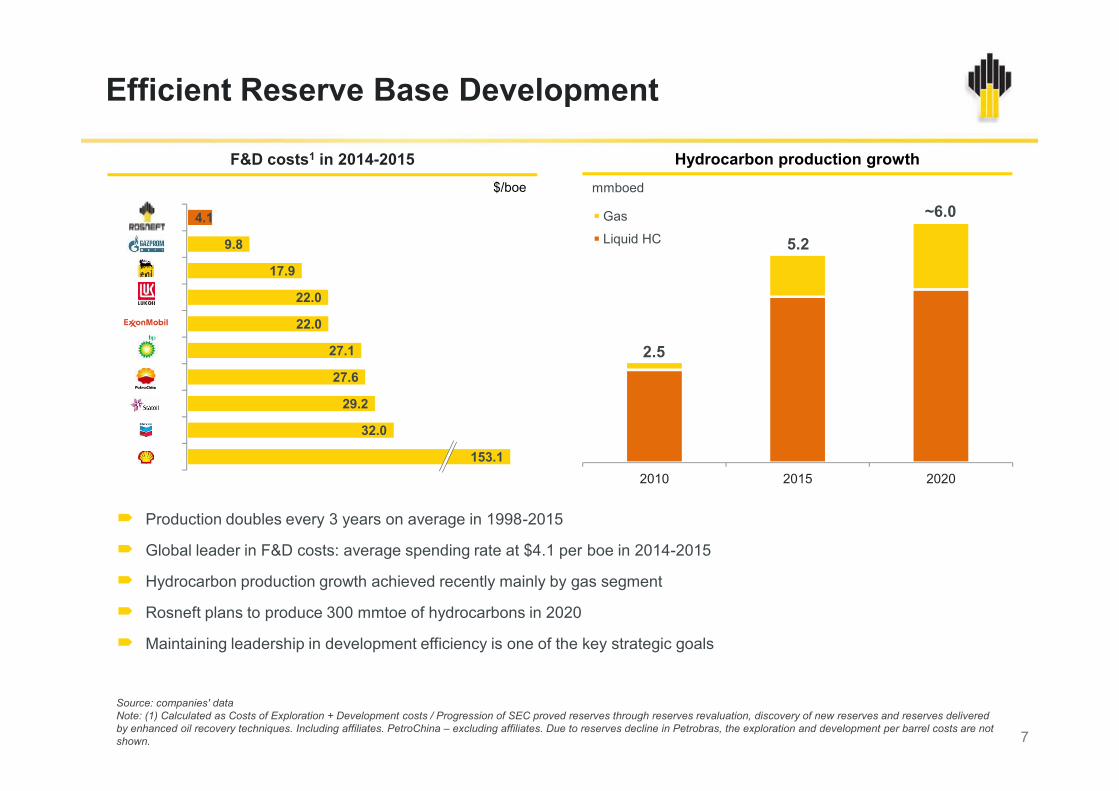

Efficient Reserve Base Development

Hydrocarbon production growthmmboed

29.2

27.6

27.1

22.0

22.0

17.9

9.8

4.1

F&D costs1 in 2014-2015$/boe

7

2010 2015 2020

Production doubles every 3 years on average in 1998-2015

Global leader in F&D costs: average spending rate at $4.1 per boe in 2014-2015

Hydrocarbon production growth achieved recently mainly by gas segment

Rosneft plans to produce 300 mmtoe of hydrocarbons in 2020

Maintaining leadership in development efficiency is one of the key strategic goals

Source: companies' dataNote: (1) Calculated as Costs of Exploration + Development costs / Progression of SEC proved reserves through reserves revaluation, discovery of new reserves and reserves deliveredby enhanced oil recovery techniques. Including affiliates. PetroChina – excluding affiliates. Due to reserves decline in Petrobras, the exploration and development per barrel costs are notshown.

153.1

32.0

29.2

2012 2013 2014 2015

Producer price index

In-house service provider

3rd party contractor

+ 22% vs. 2013

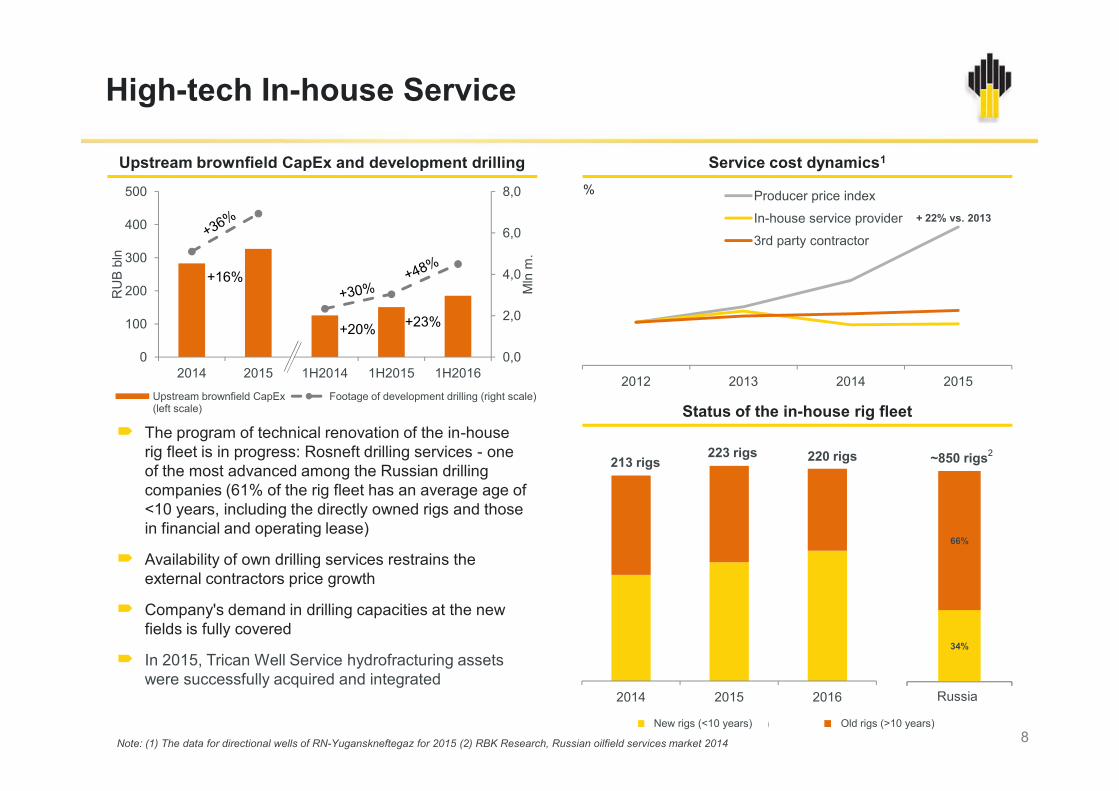

High-tech In-house Service

Upstream brownfield CapEx and development drilling Service cost dynamics1

%

0,0

2,0

4,0

6,0

8,0

0

100

200

300

400

500

2014 2015 1H2014 1H2015 1H2016

Mln

m.

RU

Bbl

n

Upstream brownfield CapEx(left scale)

Footage of development drilling (right scale)

+16%

+20% +23%

8

Status of the in-house rig fleet

2014 2015 2016

Новые БУ (<10 лет) Старые БУ (>10 лет)

34%

66%

РФ

213 rigs223 rigs 220 rigs ~850 rigs2

New rigs (<10 years) Old rigs (>10 years)

The program of technical renovation of the in-houserig fleet is in progress: Rosneft drilling services - oneof the most advanced among the Russian drillingcompanies (61% of the rig fleet has an average age of<10 years, including the directly owned rigs and thosein financial and operating lease)

Availability of own drilling services restrains theexternal contractors price growth

Company's demand in drilling capacities at the newfields is fully covered

In 2015, Trican Well Service hydrofracturing assetswere successfully acquired and integrated

Note: (1) The data for directional wells of RN-Yuganskneftegaz for 2015 (2) RBK Research, Russian oilfield services market 2014

34%

66%

РФRussia

Upstream brownfield CapEx(left scale)

Footage of development drilling (right scale)

2014 2015 2016

Directional wellsHorizontal wells

31%

20% 20%

38%

21%

29%

47%

22%

30%

53%

28% 30%

Gazprom neft Lukoil Rosneft

2013 2014 2015 1H2016

1,8391,594

+15%

Drilling Activity Ramp-up andApplication of Advanced Technologies

Horizontal wells dynamics1 New oil wells completed

Average flow rates in 20152

9

14.3

49.0

9.4

34.0

Average flow rate per oil well Average flow rate per new oil well

Rosneft Russia average

tpd Horizontal wells share growth to 30% across theentire portfolio

Flow rates significantly exceed the sector average

Optimization of well construction technologicalprograms – horizontal wells drilling rate increased by6% vs 2014

Efficient wellwork – horizontal wells with multi-stagehydrofrac increased by ~45%; side-trackingoperations incresed by >44% with incrementalproduction exceeding 2.6 mmt

Yuganskneftegaz: the share of horizontal wells withmultifrac increased to 14% in 1H2016 (13% in 2015,8% in 2014)

Note: (1) CDU TEK data, well performance, constructed wells (rate of horizontal wells in development drilling) (2) CDU TEK data, Rosneft - IFRS

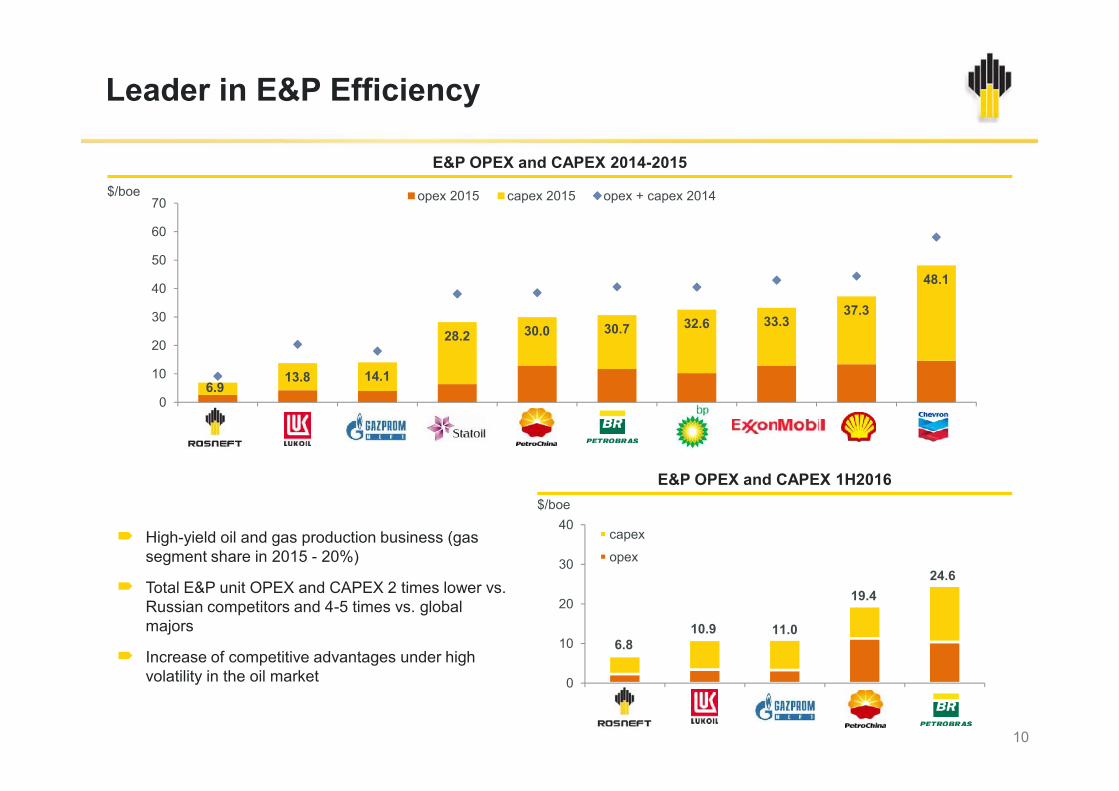

Leader in E&P Efficiency

6.913.8 14.1

28.2 30.0 30.7 32.6 33.337.3

48.1

0

10

20

30

40

50

60

70 opex 2015 capex 2015 opex + capex 2014$/boe

E&P OPEX and CAPEX 2014-2015

10

High-yield oil and gas production business (gassegment share in 2015 - 20%)

Total E&P unit OPEX and CAPEX 2 times lower vs.Russian competitors and 4-5 times vs. globalmajors

Increase of competitive advantages under highvolatility in the oil market

0

E&P OPEX and CAPEX 1H2016

0

10

20

30

40capex

opex

6.810.9 11.0

19.424.6

$/boe

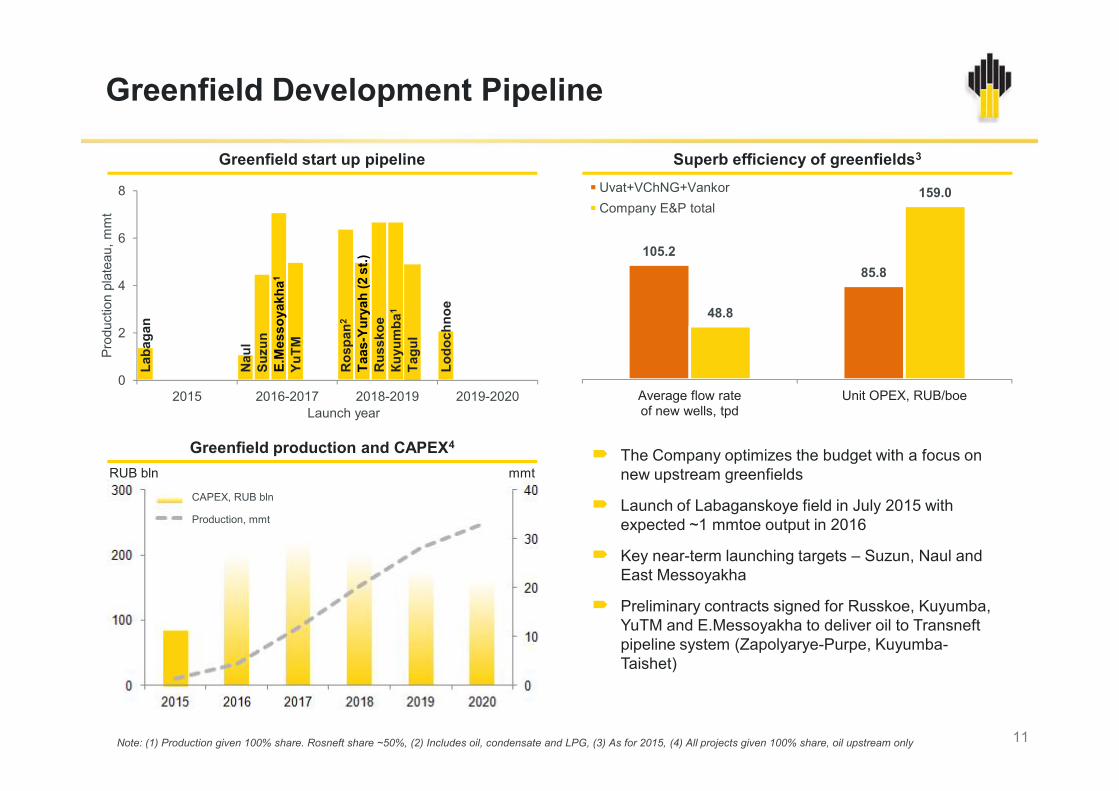

Greenfield Development Pipeline

Greenfield start up pipeline Superb efficiency of greenfields3

105.285.8

48.8

159.0

Average flow rateof new wells, tpd

Unit OPEX, RUB/boe

Uvat+VChNG+VankorCompany E&P total

Laba

gan

Nau

l

Ros

pan2

Lodo

chno

e

Suzu

n

Тааs

-Yur

yah

(2st

.)

E.M

esso

yakh

а1

Rus

skoe

YuТМ

Кuyu

mba

1

Tagu

l

0

2

4

6

8

2015 2016-2017 2018-2019 2019-2020

Prod

uctio

n pl

atea

u,m

mt

11

Average flow rateof new wells, tpd

Unit OPEX, RUB/boe

The Company optimizes the budget with a focus onnew upstream greenfields

Launch of Labaganskoye field in July 2015 withexpected ~1 mmtoe output in 2016

Key near-term launching targets – Suzun, Naul andEast Messoyakha

Preliminary contracts signed for Russkoe, Kuyumba,YuTM and E.Messoyakha to deliver oil to Transneftpipeline system (Zapolyarye-Purpe, Kuyumba-Taishet)

Greenfield production and CAPEX4

Note: (1) Production given 100% share. Rosneft share ~50%, (2) Includes oil, condensate and LPG, (3) As for 2015, (4) All projects given 100% share, oil upstream only

2015 2016-2017 2018-2019 2019-2020Launch year

CAPEX, RUB bln

Production, mmt

mmtRUB bln

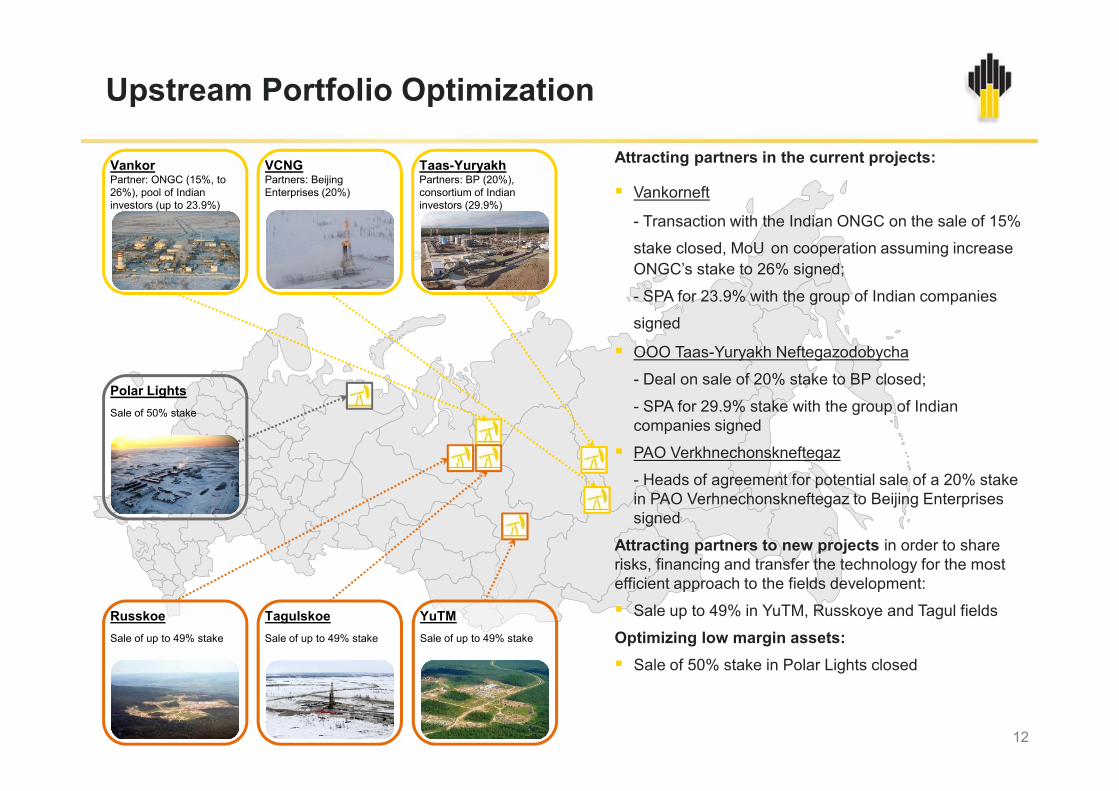

Upstream Portfolio Optimization

VankorPartner: ONGC (15%, to26%), pool of Indianinvestors (up to 23.9%)

Taas-YuryakhPartners: BP (20%),consortium of Indianinvestors (29.9%)

Polar LightsSale of 50% stake

Attracting partners in the current projects:

Vankorneft

- Transaction with the Indian ONGC on the sale of 15%

stake closed, MoU on cooperation assuming increaseONGC’s stake to 26% signed;

- SPA for 23.9% with the group of Indian companies

signed

OOO Taas-Yuryakh Neftegazodobycha

- Deal on sale of 20% stake to BP closed;

- SPA for 29.9% stake with the group of Indiancompanies signed

PAO Verkhnechonskneftegaz

- Heads of agreement for potential sale of a 20% stakein PAO Verhnechonskneftegaz to Beijing Enterprisessigned

Attracting partners to new projects in order to sharerisks, financing and transfer the technology for the mostefficient approach to the fields development:

Sale up to 49% in YuTM, Russkoye and Tagul fields

Optimizing low margin assets: Sale of 50% stake in Polar Lights closed

VCNGPartners: BeijingEnterprises (20%)

RusskoeSale of up to 49% stake

TagulskoeSale of up to 49% stake

YuTMSale of up to 49% stake

Polar LightsSale of 50% stake

Attracting partners in the current projects:

Vankorneft

- Transaction with the Indian ONGC on the sale of 15%

stake closed, MoU on cooperation assuming increaseONGC’s stake to 26% signed;

- SPA for 23.9% with the group of Indian companies

signed

OOO Taas-Yuryakh Neftegazodobycha

- Deal on sale of 20% stake to BP closed;

- SPA for 29.9% stake with the group of Indiancompanies signed

PAO Verkhnechonskneftegaz

- Heads of agreement for potential sale of a 20% stakein PAO Verhnechonskneftegaz to Beijing Enterprisessigned

Attracting partners to new projects in order to sharerisks, financing and transfer the technology for the mostefficient approach to the fields development:

Sale up to 49% in YuTM, Russkoye and Tagul fields

Optimizing low margin assets: Sale of 50% stake in Polar Lights closed

12

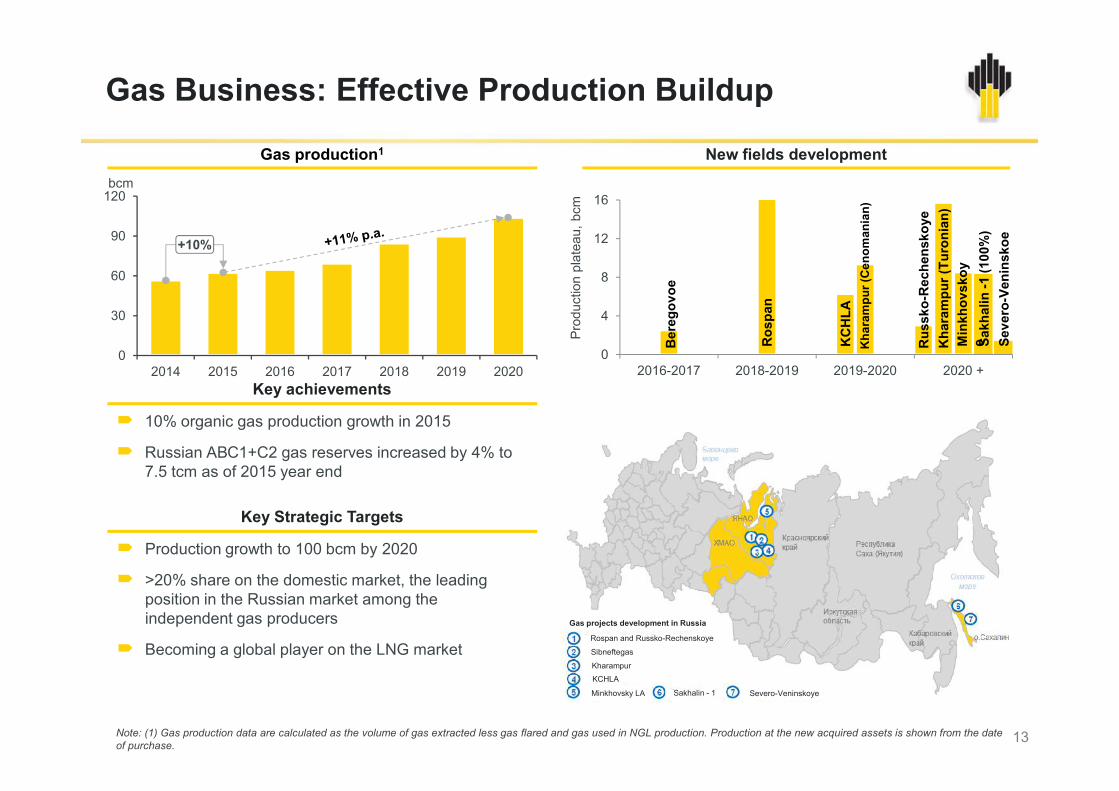

Gas Business: Effective Production Buildup

Key achievements

Gas production1

bcm

0

30

60

90

120

2014 2015 2016 2017 2018 2019 20200

4

8

12

16

2016-2017 2018-2019 2019-2020 2020 +

Prod

uctio

n pl

atea

u, b

cm

Ber

egov

oe

Ros

pan

KC

HLA

Kha

ram

pur (

Cen

oman

ian)

Rus

sko-

Rec

hens

koye

Kha

ram

pur (

Turo

nian

)M

inkh

ovsk

oye Sa

khal

in-1

(100

%)

Seve

ro-V

enin

skoe

New fields development

+10%

13

10% organic gas production growth in 2015

Russian АВС1+С2 gas reserves increased by 4% to7.5 tcm as of 2015 year end

Key achievements

Key Strategic Targets

Production growth to 100 bcm by 2020

>20% share on the domestic market, the leadingposition in the Russian market among theindependent gas producers

Becoming a global player on the LNG market

Note: (1) Gas production data are calculated as the volume of gas extracted less gas flared and gas used in NGL production. Production at the new acquired assets is shown from the dateof purchase.

Rospan and Russko-Rechenskoye

Sibneftegas

Kharampur

KCHLA

Gas projects development in Russia

Sakhalin - 1 Severo-VeninskoyeMinkhovsky LA

less than 5 bcmmore than 5 bcm

KhMAO

KaliningradRegion

Bashkortostan

Perm Kray

SverdlovskRegion

MoscowRegion

KrasnodarRegion

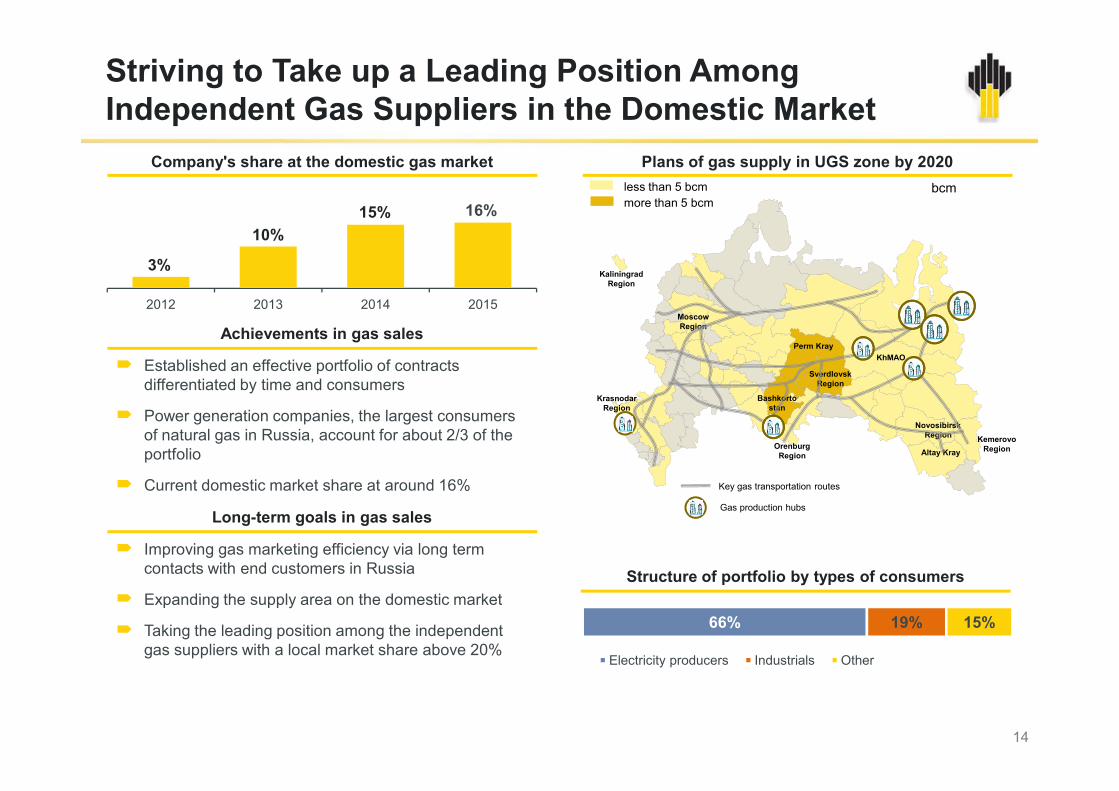

Company's share at the domestic gas market

2012 2013 2014 2015

3%

10%15% 16%

Plans of gas supply in UGS zone by 2020

Achievements in gas sales

Established an effective portfolio of contractsdifferentiated by time and consumers

Power generation companies, the largest consumersof natural gas in Russia, account for about 2/3 of theportfolio

Current domestic market share at around 16%

bcm

Striving to Take up a Leading Position AmongIndependent Gas Suppliers in the Domestic Market

14

Key gas transportation routes

Gas production hubs

66% 19% 15%

Electricity producers Industrials Other

KemerovoRegion

Bashkortostan

KrasnodarRegion

NovosibirskRegion

Altay KrayOrenburg

Region

Long-term goals in gas sales

Established an effective portfolio of contractsdifferentiated by time and consumers

Power generation companies, the largest consumersof natural gas in Russia, account for about 2/3 of theportfolio

Current domestic market share at around 16%

Improving gas marketing efficiency via long termcontacts with end customers in Russia

Expanding the supply area on the domestic market

Taking the leading position among the independentgas suppliers with a local market share above 20%

Structure of portfolio by types of consumers

85 87 8588

9451%

59%

80% 81%

100%

54%

55% 55% 55%

69%

0%

20%

40%

60%

80%

100%

0

16

31

47

63

79

94

2013 2014 2015 2017 Modernizationcompletion

Key achievements for 2015

Light product yield improved from 54.8% to 55.3%,refining depth increased from 65.3% to 66.5%

Full transition to Euro-5 motor fuels production for theRussian market in accordance with TechnicalRegulations requirements

Commissioning of isomerization units at Kuibyshevrefinery, at Novokuybyshev refinery and at Ryazanrefinery and launching MTBE in Angarskpetrochemical company

Reconstruction of catalytic reforming unit at Syzranand Kuybyshev refineries completed

Processing and production of motor fuel1

Rosneft Continues the Refining Modernization in Russia

46%

49%

51%

55%

56%

60%

60%

63%

Ryazan Refinery

Achinsk Refinery

Angarsk PCC

Komsomolsk Refinery

Novokuybyshev Refinery

Syzran Refinery

Tuapse Refinery

Kuybyshev Refinery

2013 2014 2015 2017 ModernizationcompletionRefinery thoughput in Russia, mmt

Gasoline and diesel Euro-4/5 production share,%Light product yield,%

15

Progress in refineries upgrade program

Light product yield improved from 54.8% to 55.3%,refining depth increased from 65.3% to 66.5%

Full transition to Euro-5 motor fuels production for theRussian market in accordance with TechnicalRegulations requirements

Commissioning of isomerization units at Kuibyshevrefinery, at Novokuybyshev refinery and at Ryazanrefinery and launching MTBE in Angarskpetrochemical company

Reconstruction of catalytic reforming unit at Syzranand Kuybyshev refineries completed

Note: (1) W/o FEPCO project; share of motor fuel and diesel fuel – w/o mini refineries

Plans for 2016

Increased production of high-margin petroleumproducts by reducing the production of fuel oil

Implementation of the import substitution program inthe area of chemicals, catalysts and additives to motorfuels

Further construction of facilities within the refinerymodernization program

Implementation of the program for efficiencyimprovement and maintaining assets

26.6 20.1

3.14.9

23.8 30.8

5.37.611.1

14.8High-octanegasoline

Naphta

Diesel

Jet fuel

Fuel oil11689 74

457

Maintenance

Development

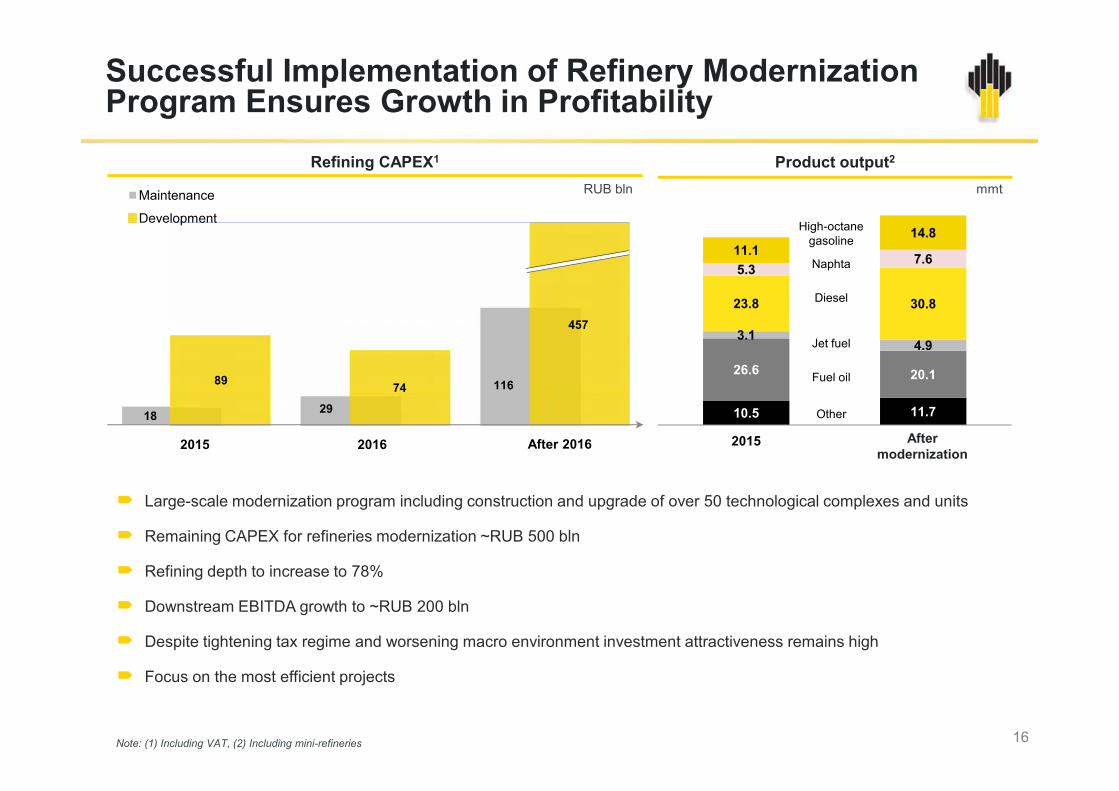

Refining CAPEX1 Product output2

RUB bln mmt

Successful Implementation of Refinery ModernizationProgram Ensures Growth in Profitability

10.5 11.7

2015 После модернизации

Other

Large-scale modernization program including construction and upgrade of over 50 technological complexes and units

Remaining CAPEX for refineries modernization ~RUB 500 bln

Refining depth to increase to 78%

Downstream EBITDA growth to ~RUB 200 bln

Despite tightening tax regime and worsening macro environment investment attractiveness remains high

Focus on the most efficient projects

18 29

2016 After 20162015

Note: (1) Including VAT, (2) Including mini-refineries 16

Aftermodernization

Refinery Modernization Effect

Modernization effect+7.5 $/bbl

Average refining margin growth1

2.6

10.1

4.0

Tax maneuver effect-1.4 $/bbl

$/bbl

Rosneft (2014) Rosneft without modernization Rosneft with modernization

17Note: (1) Refining margins calculated assuming the following macro parameters: crude oil price of $55 per bbl of Brent and exchange rate of RUB 62,5 per USD

2.64.0

Following the modernization at Russian refineries refining depth will increase to >78%, light product yield will reach ~67%,production of motor fuels conforming technical regulations will grow to 50 mtpa

Refinery modernization and upgrade CAPEX will total c. RUB 1.1 trln (incl. VAT) of which >RUB 700 bln already financed

Worsening macro and refining margins decline following tax maneuver reduced financial options for capital-intensemodernization program. However the Company preserved almost all projects in its portfolio and continued theirimplementation within existing financial constraints

Refineries primaryrefining

vacuumblock

isomerization

catcracking

hydrotreatment

reforming alkylation coking1 hydrocra

cking MTBE

Ryazan

Angarsky

Novokuibyshevsky

Syzransky

Refinery Modernization Roadmap

Note: (1) Delayed coking or flexicoking

Kuibyshevsky

Komsomolsk

Touapsinskiy

Achinsk

Saratov

Effect Throughput Refiningdepth

Euro-5gasoline

Lightproduct

yield

Euro-5motorfuels

Euro-5gasoline

Euro-5gasoline

Refiningdepth

Lightproduct

yield

Euro-5gasoline

Construction completed Completion in 2017+ UpgradeCompletion in 2016

unit capacity 18

Crude oil sales channels

20%

70%

9% 1%

AsiaEurope and otherCIS

200835%

52%

8% 5%

Efficient Oil Marketing

Focus on optimizing logistics and maximizing netbacks

Supplies to Asian market up 120% for last 4 years; recordhigh volumes at 39.7 mmt in 2015

Further increase in supply expected to 49.5 mmt by 2020(42% of total crude oil export)

Current portfolio of LT supply contracts offers sustainablehigh-margin realization channels at the market pricingterms ensuring highly profitable resources monetization

35%

52%

8% 5%

1H 2016

19

CISDomestic

$ bln

Prepayments under LT crude oil supply contractsLong term crude oil supply contracts1

Direction Partner Average annualvolumes (mmt)² Duration

China CNPC, Transneft up to 40³ 10-27 years

Novorossiysk/Primorsk/Ust-Luga

Glencore, Vitol,Trafigura, BP 13 5 years

Germany Totsa, RTSA 11 2-3 years

Poland Orlen, GrupaLOTOS S.A. 12 3-7 years

Czech Orlen 2 3 years

Domestic market Afipsky Refinery 2 3 years

Note: (1) The list of contracts in force as of March 2016 including duration (2) Volumes for a given year may differ from average volumes (3) The number assumes potential increase ofannual supplies from 7 to 10 mmtpa

14.8

29.7

42.5 40.9

received 2013 received 2014 received 2015 repaid 2Q2016

CAPEX and HC production

Flexible Investment Program

23.8

22.3

21.8

20.3

19.0

17.0

10.1

9.5

4.3

2015 Upstream Capex: benchmarking$/boe

0

1 400

2 800

4 200

5 600

0

300

600

900

RUB bln kboed

595533

308

Note: (1) Including international and off-shore projects

Flexible investment program: quick response to changes inmacro environment

Stability of strategic objectives:

production increase with a focus on the most efficientprojects,

meeting the license and inter-governmental obligationsincluding the provision of oil and petroleum productsupplies,

preserving the market share

2016-17 Capex: new Upstream projects1 ~ RUB 620 bln,Downstream development projects ~ RUB 160 bln.

Sustaining leadership in E&P unit CAPEX

20

0

250

500

750

1000

2014 2015 2016-2017 range

Upstream (brownfields) Upstream (greenfields)Downstream (existing) Downstream (new)Other

595

CAPEXRUB bln

533

1

33.5

23.8002014 2015 H1 2016

Upstream Downtream Other HC Production

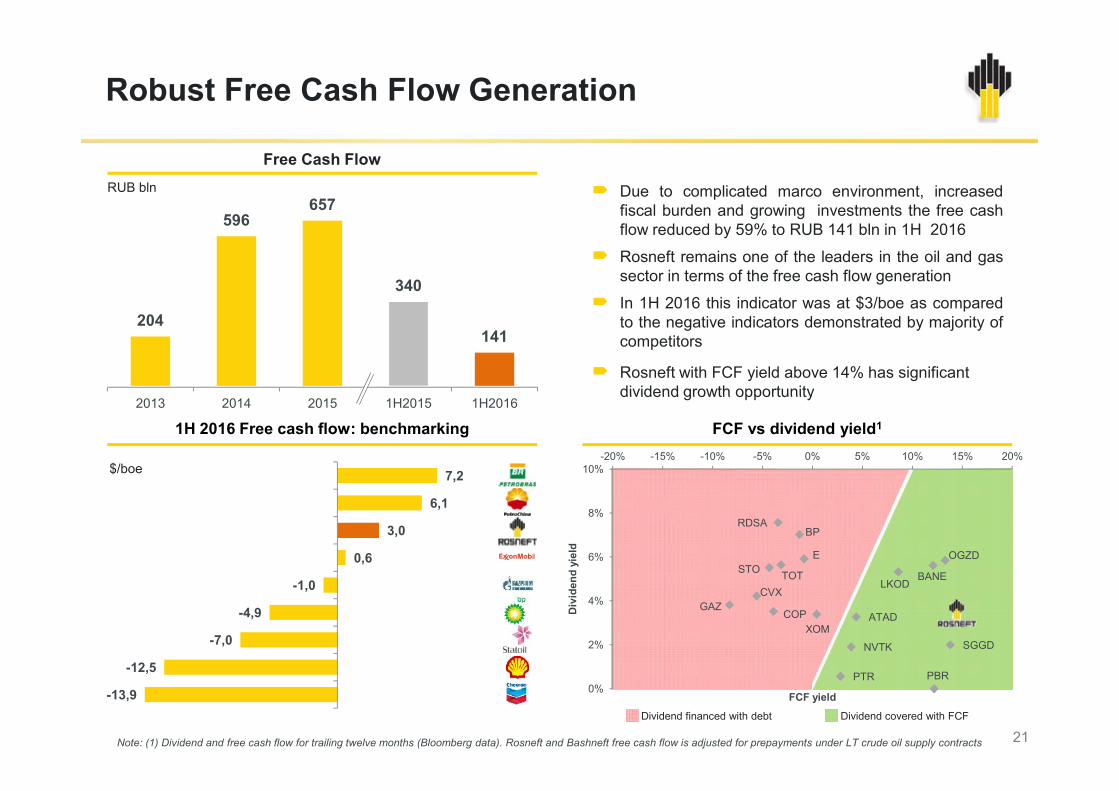

204

596657

340

141

Due to complicated marco environment, increasedfiscal burden and growing investments the free cashflow reduced by 59% to RUB 141 bln in 1H 2016

Rosneft remains one of the leaders in the oil and gassector in terms of the free cash flow generation

In 1H 2016 this indicator was at $3/boe as comparedto the negative indicators demonstrated by majority ofcompetitors

Rosneft with FCF yield above 14% has significantdividend growth opportunity

RUB bln

Free Cash Flow

Robust Free Cash Flow Generation

2013 2014 2015 1H2015 1H2016

Due to complicated marco environment, increasedfiscal burden and growing investments the free cashflow reduced by 59% to RUB 141 bln in 1H 2016

Rosneft remains one of the leaders in the oil and gassector in terms of the free cash flow generation

In 1H 2016 this indicator was at $3/boe as comparedto the negative indicators demonstrated by majority ofcompetitors

Rosneft with FCF yield above 14% has significantdividend growth opportunity

21

FCF vs dividend yield1

Dividend financed with debt Dividend covered with FCF

$/boe

1H 2016 Free cash flow: benchmarking

-13,9

-12,5

-7,0

-4,9

-1,0

0,6

3,0

6,1

7,2

SGGD

OGZD

PBR

BANELKOD

ATAD

NVTK

PTR

XOM

E

BP

TOT

RDSA

COP

STO

CVXGAZ

0%

2%

4%

6%

8%

10%-20% -15% -10% -5% 0% 5% 10% 15% 20%

Div

iden

d yi

eld

FCF yield

Note: (1) Dividend and free cash flow for trailing twelve months (Bloomberg data). Rosneft and Bashneft free cash flow is adjusted for prepayments under LT crude oil supply contracts

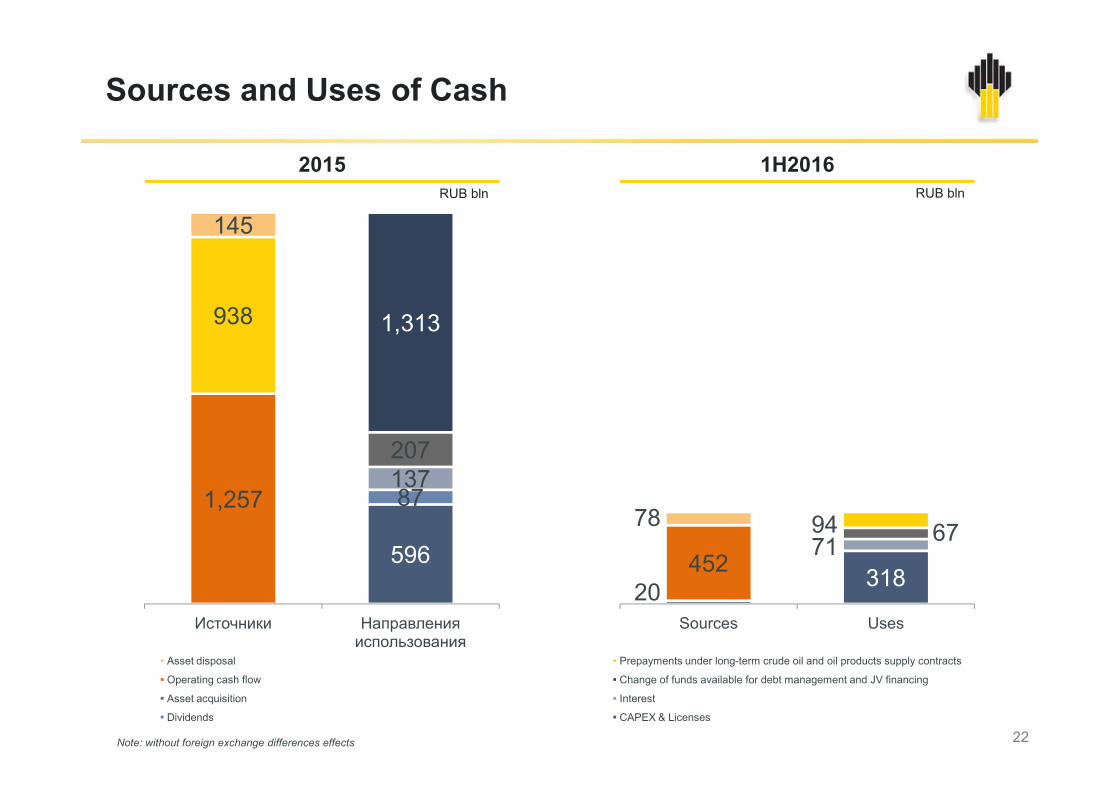

1,313938

145RUB bln

2015 1H2016RUB bln

Sources and Uses of Cash

596

87137207

1,257

Источники Направленияиспользования

Asset disposal Prepayments under long-term crude oil and oil products supply contracts

Operating cash flow Change of funds available for debt management and JV financing

Asset acquisition Interest

Dividends CAPEX & Licenses

31871 67

20452

9478

Sources Uses

22Note: without foreign exchange differences effects

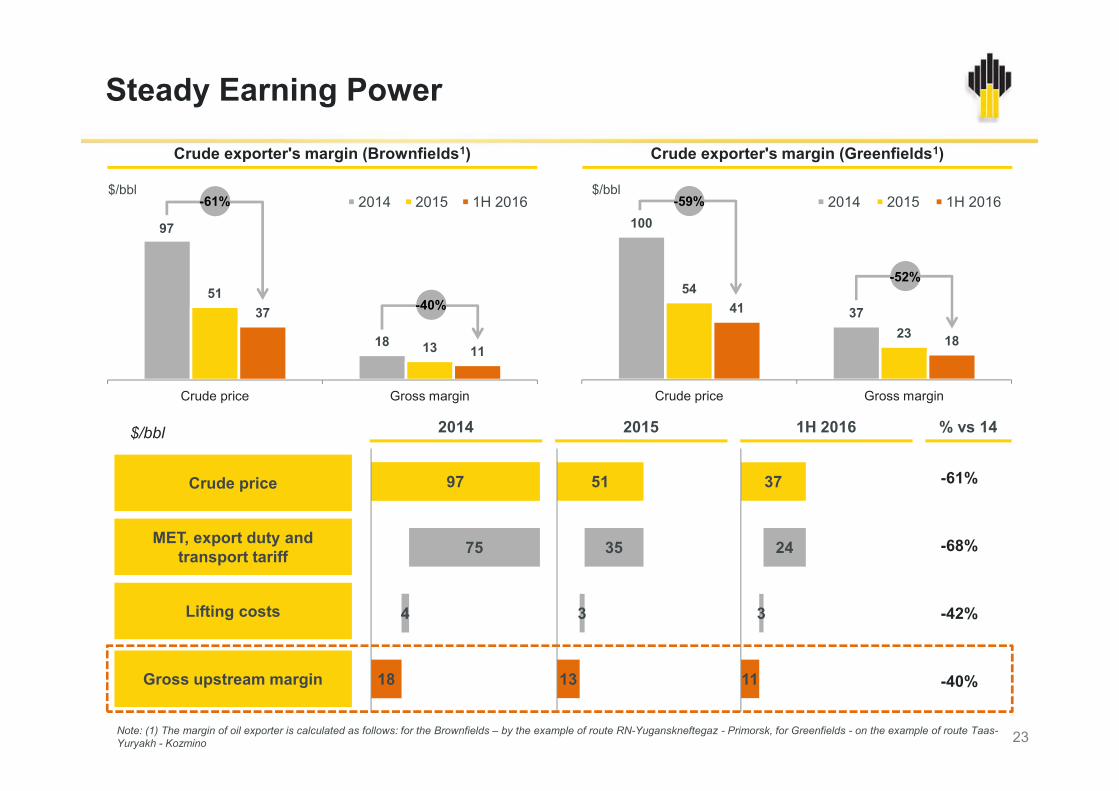

Crude exporter's margin (Brownfields1) Crude exporter's margin (Greenfields1)

$/bbl $/bbl

Steady Earning Power

100

37

54

23

41

18

Crude price Gross margin

2014 2015 1H 2016

18

51

13

37

11

Crude price Gross margin

2014 2015 1H 2016

97

-61%

-40%

-59%

-52%

23

$/bbl

Crude price

MET, export duty andtransport tariff

Lifting costs

Gross upstream margin

Note: (1) The margin of oil exporter is calculated as follows: for the Brownfields – by the example of route RN-Yuganskneftegaz - Primorsk, for Greenfields - on the example of route Taas-Yuryakh - Kozmino

Crude price Gross marginCrude price Gross margin

51

35

3

13

97

75

4

18

2014 2015 % vs 14

-61%

-68%

-42%

-40%

1H 2016

37

24

3

11

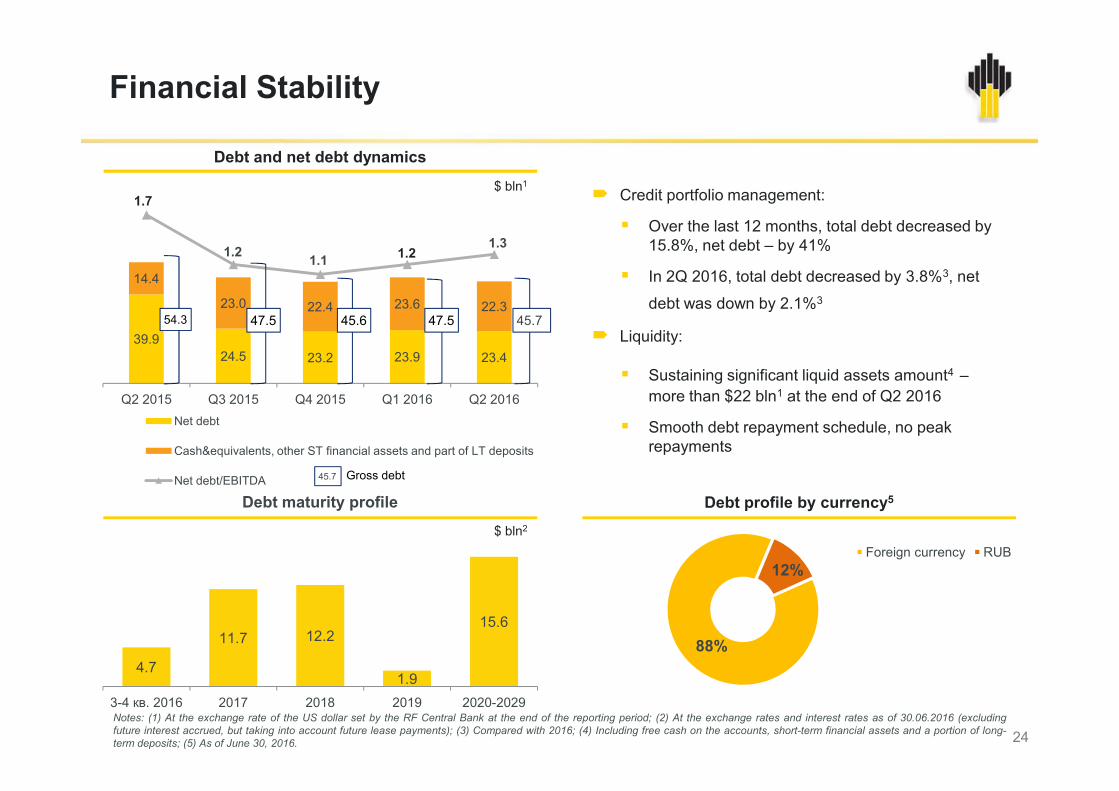

Financial Stability

39.924.5 23.2 23.9 23.4

14.4

23.0 22.4 23.6 22.3

1.7

1.2 1.1 1.21.3

0,00,20,40,60,81,01,21,41,61,8

0

10

20

30

40

50

60

70

80

Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016

54.3 47.5 45.6 47.5 45.7

Debt and net debt dynamics

$ bln1 Credit portfolio management:

Over the last 12 months, total debt decreased by15.8%, net debt – by 41%

In 2Q 2016, total debt decreased by 3.8%3, net

debt was down by 2.1%3

Liquidity:

Sustaining significant liquid assets amount4 –more than $22 bln1 at the end of Q2 2016

Smooth debt repayment schedule, no peakrepayments

24

Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016Net debt

Cash&equivalents, other ST financial assets and part of LT deposits

Net debt/EBITDA 45.7 Gross debt

Notes: (1) At the exchange rate of the US dollar set by the RF Central Bank at the end of the reporting period; (2) At the exchange rates and interest rates as of 30.06.2016 (excludingfuture interest accrued, but taking into account future lease payments); (3) Compared with 2016; (4) Including free cash on the accounts, short-term financial assets and a portion of long-term deposits; (5) As of June 30, 2016.

88%

12%Foreign currency RUB

Debt profile by currency5Debt maturity profile

4.7

11.7 12.2

1.9

15.6

3-4 кв. 2016 2017 2018 2019 2020-2029

$ bln2

Credit portfolio management:

Over the last 12 months, total debt decreased by15.8%, net debt – by 41%

In 2Q 2016, total debt decreased by 3.8%3, net

debt was down by 2.1%3

Liquidity:

Sustaining significant liquid assets amount4 –more than $22 bln1 at the end of Q2 2016

Smooth debt repayment schedule, no peakrepayments

Dividend payments and oil prices

Sustainable Dividend Payments / High Yields

Dividends paid since the IPO totaled ~ RUB 615 bln

DPS CAGR since the IPO >25%

Dividend payout ratio of no less than 25% of IFRS netincome starting 2011

RUB 11.75 per share (RUB 124.5 bln, 35% of IFRS netprofit) – dividend for 2015,+43% YoY

1,3 1,6 1,9 2,3 2,87,5 8,1

9.2*8,2

11.8

61,7

111,3 108,7

0,000,501,001,502,002,503,003,504,004,505,005,506,006,507,007,508,008,509,009,5010,0010,5011,0011,5012,0012,5013,0013,5014,0014,5015,0015,5016,0016,5017,0017,5018,0018,5019,0019,5020,0020,5021,0021,5022,0022,5023,0023,5024,0024,5025,0025,5026,0026,5027,0027,5028,0028,5029,0029,5030,0030,5031,0031,5032,0032,5033,0033,5034,0034,5035,0035,5036,0036,5037,0037,5038,0038,5039,0039,5040,0040,5041,0041,5042,0042,5043,0043,5044,0044,5045,0045,5046,0046,5047,0047,5048,0048,5049,0049,5050,0050,5051,0051,5052,0052,5053,0053,5054,0054,5055,0055,5056,0056,5057,0057,5058,0058,5059,0059,5060,0060,5061,0061,5062,0062,5063,0063,5064,0064,5065,0065,5066,0066,5067,0067,5068,0068,5069,0069,5070,0070,5071,0071,5072,0072,5073,0073,5074,0074,5075,0075,5076,0076,5077,0077,5078,0078,5079,0079,5080,0080,5081,0081,5082,0082,5083,0083,5084,0084,5085,0085,5086,0086,5087,0087,5088,0088,5089,0089,5090,0090,5091,0091,5092,0092,5093,0093,5094,0094,5095,0095,5096,0096,5097,0097,5098,0098,5099,0099,50100,00100,50101,00101,50102,00102,50103,00103,50104,00104,50105,00105,50106,00106,50107,00107,50108,00108,50109,00109,50110,00110,50111,00111,50112,00112,50113,00113,50114,00114,50115,00115,50116,00116,50117,00117,50118,00118,50119,00119,50120,00

0

2

4

6

8

10

12

14

16

18

20DPS, RUB

Brent, $/bbl

3.7

12.9

25

19.75%

69.50%

10.75%

RussianFederation

Free float BP

Rosneft shareholders2Benchmarking free cash flow yield1

*Adjusted for RUB 167 bln revaluation effect of acquired TNK-BP assetsNote: (1) Calculated using LTM free cash flow, (2) As of June 1, 2016

1,3 1,6 1,9 0,000,501,001,502,002,503,003,504,004,505,005,500

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

13% 12%8% 5% 5% 4%

-11%

• OPEX control• Managing SGA and production costsBelow inflation

• CAPEX control• Review current project portfolio to increase profitabilityOptimization Optimization of investment portfolio, supplier relationship management

Control over manageable operating expenses

Financial Priorities

• Free cash flowPositive

• Dividend payoutNot less than 25%of IFRS net profit

• Preserving financial leverage near current levels~1.3-1.4x Optimal mix of external and internal financing

Provide consistently high shareholder returns

Generate free cash flow sufficient to fulfill all obligations

26

AppendixAppendix

Indicator 2015 2014 % 1H2016 %

EBITDA, RUB bln 1,245 1,057 17.8% 621 (7.3)%

Net income, RUB blnattributable to Rosneft shareholders

355 348 2.0% 103 (45.8)%

Adjusted net income1, RUB blnattributable to Rosneft shareholders

479 395 21.0% 248 (8.8)%

Adjusted operating cash flow2, RUB bln 1,252 1,129 10.9% 449 (26.3)%

Capital expenditures, RUB bln 595 533 11.6% 308 14.5%

Key Financial Indicators

Adjusted free cash flow2, RUB bln 657 596 10.2% 141 (58.5)%

EBITDA, $ bln 20.8 29.0 (28.3)% 9.0 (23.7)%

Net income, $ blnattributable to Rosneft shareholders 6.1 9.3 (34.4)% 1.6 (54.3)%

Adjusted net income1, RUB blnattributable to Rosneft shareholders 7.9 10.3 (24,0)% 3.5 (27.1)%

Adjusted operating cash flow2, $ bln 21.9 29.7 (26.3)% 7.2 (36.8)%

Capital expenditures, $ bln 9.7 13.9 (30.2)% 4.4 (6.4)%

Adjusted free cash flow2, $ bln 12.2 15.8 (22.8)% 2.8 (58.2)%

Urals,th. RUB/bbl

3.14 3.75 (16.3)% 2,67 (18.9)%

28Note: (1) Adjusted for foreign exchange differences and other one-off effects; (2) Adjusted for prepayments under long-term oil supply contracts and operations with trading securities.

Countries of operation

Canada

Gulf of Mexico

RussiaUkraine

Belarus

Germany

Italy

China

Norway Mongolia

Turkmenistan

VNKhK

Tianjinrefinery

Upstream assets

Refineries

India

Kyrgyzstan

Geography of Operations

Armenia

Georgia

Venezuela

Italy

Brazil

VietnamAlgeria

Upstream and downstream projects in 23 countries

821 licenses for hydrocarbons production in Russia and abroad1

Largest subsoil user in Russia: oil and condensate resources of 23 bln t, gas resources of 22.8 tcm2

11 refineries in Russia and stakes in 7 refineries abroad

A wide network of retail sites: 2,557 retail sites3

Note: (1) As of 2015 year end, (2) Including foreign projects, (3) As of Dec 31, 2015, including own and leased sites

CubaIndia

Egypt

IndonesiaMozambique

29