Embed Size (px)

Citation preview

GMR INFRASTRUCTURE LTD BUSINESS OVERVIEW

APRIL 2013

1

Presentation Flow

Key Highlights … 2

Business Structure … 3

Corporate Structure … 4

Airports … 5

Energy … 6

Highways … 13

Financial Summary … 17

Appendix

2

Key Highlights

1 Leading positions across all its operating segments i.e. airports, power and roads

Airports: Largest private developer and operator of airports in India

Power: 5GW of capacity expected to be commissioned by Mar-15 making the company among top 7 power producers

Roads: Mixed portfolio of Annuity and Toll projects with 8 out of 9 projects operational

Leading Infrastructure player – Ideally positioned to capture significant growth opportunities in Infrastructure sector

3 Opportunity from growing investment in infrastructure

India still “building infrastructure for the past”

Significant growth in infrastructure spending expected to help achieve target GDP growth of 9%-10% over the next

decade and to compensate for recent slippages

4 Professional management team with demonstrated track record

Strong management team with extensive experience in successfully developing and managing large-scale infrastructure

projects in India and Overseas

2 Superior quality and scale of assets

Strong execution track record. Delhi Airport was executed in 37 months which is much quicker as compared to other large

international Airports

Delhi Airport ranked 2nd in the world in 25-40 mppa(1) category and Hyderabad Airport ranked 2nd in the world in 5-15

mppa category in Service Quality (ASQ)(2)

Hyderabad Airport adjudged “The Best Cargo Airport & Best Cargo Terminal of the Year” by Air Cargo Association of India

Notes: (1) Million passengers per annum (2) Ranking by Airports Council International (ACI) for 2012

GMR Group is one of India's leading infrastructure companies with business interests across airports, energy, highways and urban infrastructure

5 Evolving Business Strategy

Transformation through consolidation

Equity release and deleverage of balance sheet through divestment of assets at right valuations

Asset Light & Asset Right approach for growth - to follow the principle of “Develop, Build, Create Value, and Divest”

3

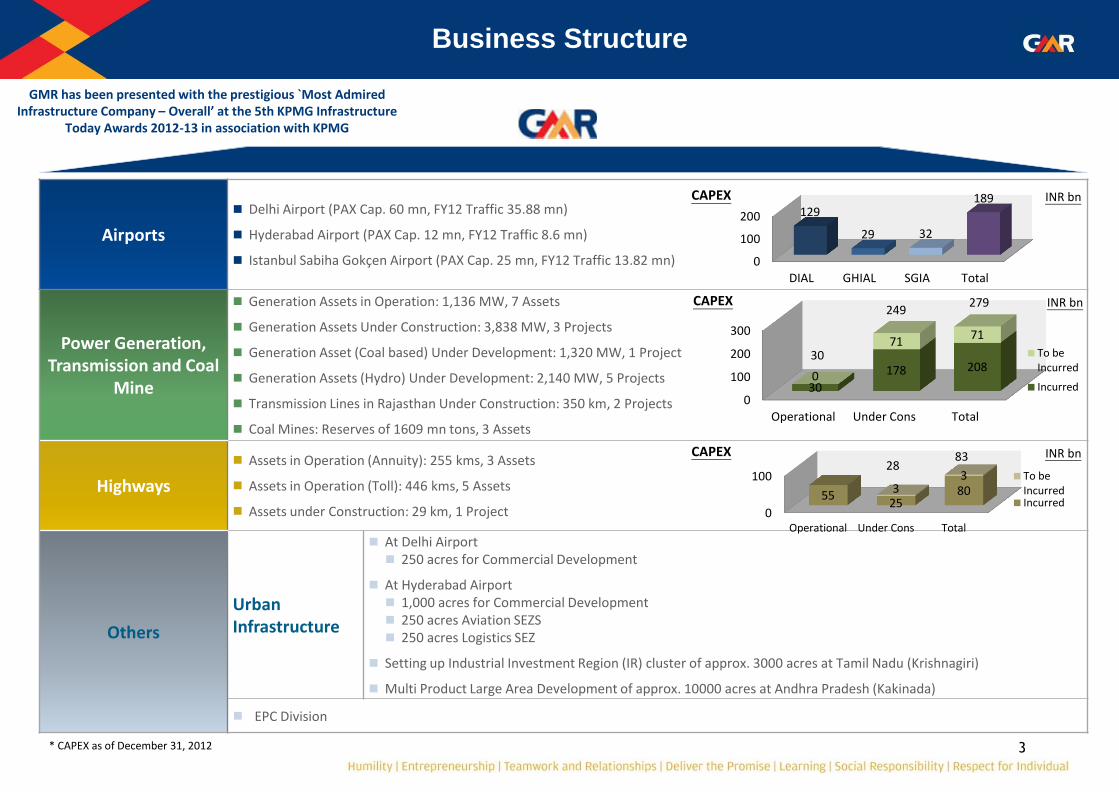

Airports

Delhi Airport (PAX Cap. 60 mn, FY12 Traffic 35.88 mn)

Hyderabad Airport (PAX Cap. 12 mn, FY12 Traffic 8.6 mn)

Istanbul Sabiha Gokçen Airport (PAX Cap. 25 mn, FY12 Traffic 13.82 mn)

Power Generation, Transmission and Coal

Mine

Generation Assets in Operation: 1,136 MW, 7 Assets

Generation Assets Under Construction: 3,838 MW, 3 Projects

Generation Asset (Coal based) Under Development: 1,320 MW, 1 Project

Generation Assets (Hydro) Under Development: 2,140 MW, 5 Projects

Transmission Lines in Rajasthan Under Construction: 350 km, 2 Projects

Coal Mines: Reserves of 1609 mn tons, 3 Assets

Highways

Assets in Operation (Annuity): 255 kms, 3 Assets

Assets in Operation (Toll): 446 kms, 5 Assets

Assets under Construction: 29 km, 1 Project

Others

Urban Infrastructure

At Delhi Airport 250 acres for Commercial Development

At Hyderabad Airport 1,000 acres for Commercial Development 250 acres Aviation SEZS 250 acres Logistics SEZ

Setting up Industrial Investment Region (IR) cluster of approx. 3000 acres at Tamil Nadu (Krishnagiri)

Multi Product Large Area Development of approx. 10000 acres at Andhra Pradesh (Kakinada)

EPC Division

Business Structure

GMR has been presented with the prestigious `Most Admired Infrastructure Company – Overall’ at the 5th KPMG Infrastructure

Today Awards 2012-13 in association with KPMG

0

100

200

300

Operational Under Cons Total

30

178 208 0

71 71

CAPEX

To beIncurred

Incurred

279 249

INR bn

30

0

100

Operational Under Cons Total

55 25

80 3 3

CAPEX

To beIncurredIncurred

83 28

INR bn

0

100

200

DIAL GHIAL SGIA Total

129

29 32

189 CAPEX INR bn

* CAPEX as of December 31, 2012

4

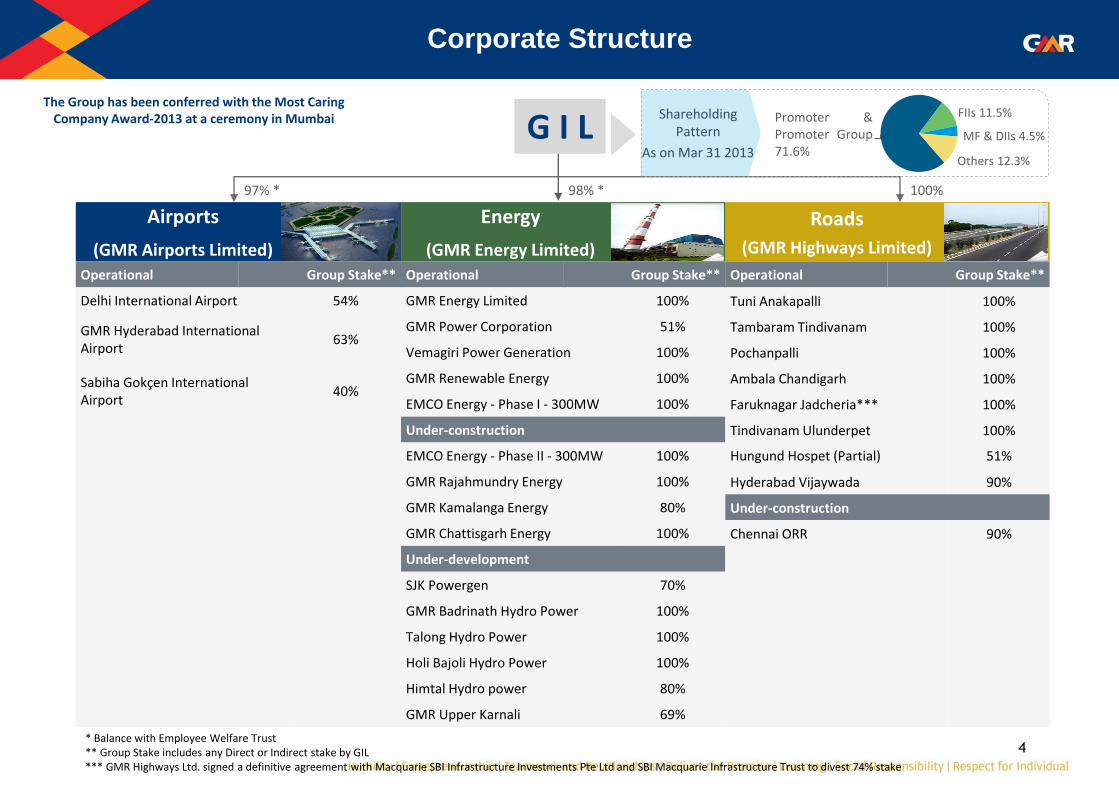

Corporate Structure

Airports

(GMR Airports Limited)

Energy

(GMR Energy Limited)

Roads

(GMR Highways Limited)

Operational Group Stake** Operational Group Stake** Operational Group Stake**

Delhi International Airport 54% GMR Energy Limited 100% Tuni Anakapalli 100%

GMR Hyderabad International Airport

63% GMR Power Corporation 51% Tambaram Tindivanam 100%

Vemagiri Power Generation 100% Pochanpalli 100%

Sabiha Gokçen International Airport

40% GMR Renewable Energy 100% Ambala Chandigarh 100%

EMCO Energy - Phase I - 300MW 100% Faruknagar Jadcheria*** 100%

Under-construction Tindivanam Ulunderpet 100%

EMCO Energy - Phase II - 300MW 100% Hungund Hospet (Partial) 51%

GMR Rajahmundry Energy 100% Hyderabad Vijaywada 90%

GMR Kamalanga Energy 80% Under-construction

GMR Chattisgarh Energy 100% Chennai ORR 90%

Under-development

SJK Powergen 70%

GMR Badrinath Hydro Power 100%

Talong Hydro Power 100%

Holi Bajoli Hydro Power 100%

Himtal Hydro power 80%

GMR Upper Karnali 69%

97% * 98% * 100%

Promoter & Promoter Group 71.6%

FIIs 11.5%

MF & DIIs 4.5%

Others 12.3%

Shareholding Pattern

As on Mar 31 2013

* Balance with Employee Welfare Trust ** Group Stake includes any Direct or Indirect stake by GIL *** GMR Highways Ltd. signed a definitive agreement with Macquarie SBI Infrastructure Investments Pte Ltd and SBI Macquarie Infrastructure Trust to divest 74% stake

The Group has been conferred with the Most Caring Company Award-2013 at a ceremony in Mumbai G I L

5

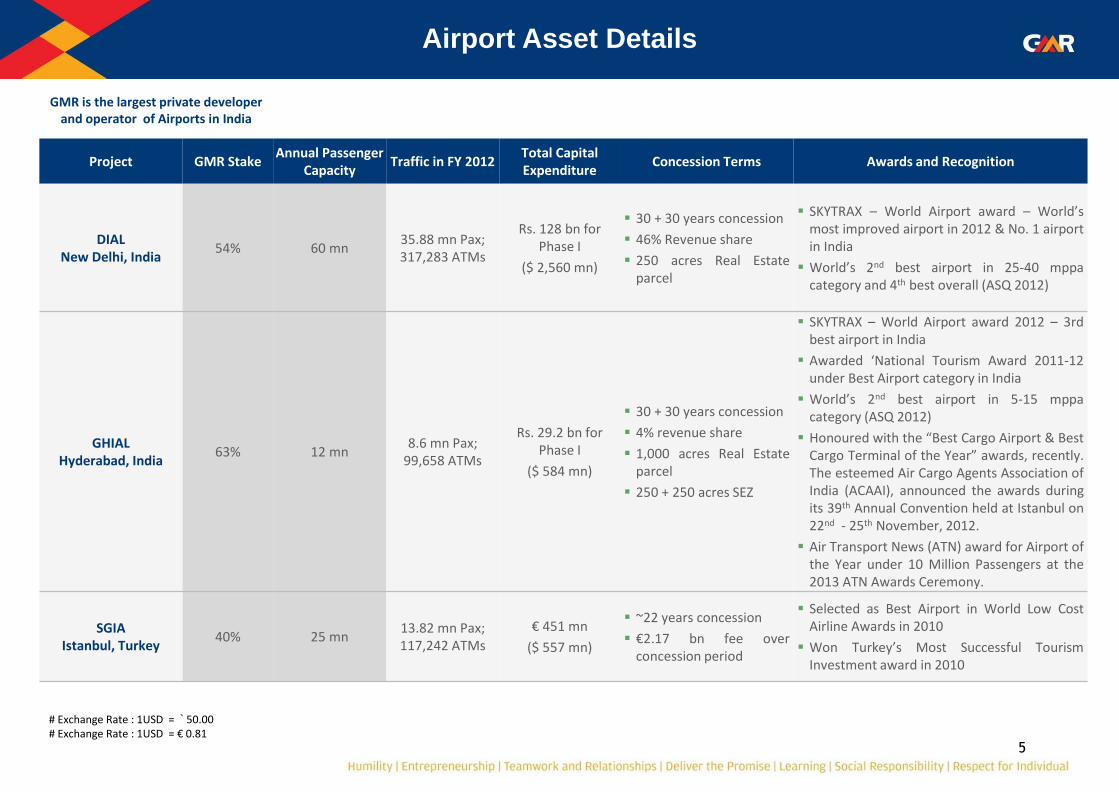

Project GMR Stake Annual Passenger

Capacity Traffic in FY 2012

Total Capital Expenditure

Concession Terms Awards and Recognition

DIAL New Delhi, India

54% 60 mn 35.88 mn Pax; 317,283 ATMs

Rs. 128 bn for Phase I

($ 2,560 mn)

30 + 30 years concession

46% Revenue share

250 acres Real Estate parcel

SKYTRAX – World Airport award – World’s most improved airport in 2012 & No. 1 airport in India

World’s 2nd best airport in 25-40 mppa category and 4th best overall (ASQ 2012)

GHIAL Hyderabad, India

63% 12 mn 8.6 mn Pax;

99,658 ATMs

Rs. 29.2 bn for Phase I

($ 584 mn)

30 + 30 years concession

4% revenue share

1,000 acres Real Estate parcel

250 + 250 acres SEZ

SKYTRAX – World Airport award 2012 – 3rd best airport in India

Awarded ‘National Tourism Award 2011-12 under Best Airport category in India

World’s 2nd best airport in 5-15 mppa category (ASQ 2012)

Honoured with the “Best Cargo Airport & Best Cargo Terminal of the Year” awards, recently. The esteemed Air Cargo Agents Association of India (ACAAI), announced the awards during its 39th Annual Convention held at Istanbul on 22nd - 25th November, 2012.

Air Transport News (ATN) award for Airport of the Year under 10 Million Passengers at the 2013 ATN Awards Ceremony.

SGIA Istanbul, Turkey

40% 25 mn 13.82 mn Pax; 117,242 ATMs

€ 451 mn

($ 557 mn)

~22 years concession

€2.17 bn fee over concession period

Selected as Best Airport in World Low Cost Airline Awards in 2010

Won Turkey’s Most Successful Tourism Investment award in 2010

Airport Asset Details

# Exchange Rate : 1USD = ` 50.00 # Exchange Rate : 1USD = € 0.81

GMR is the largest private developer and operator of Airports in India

6

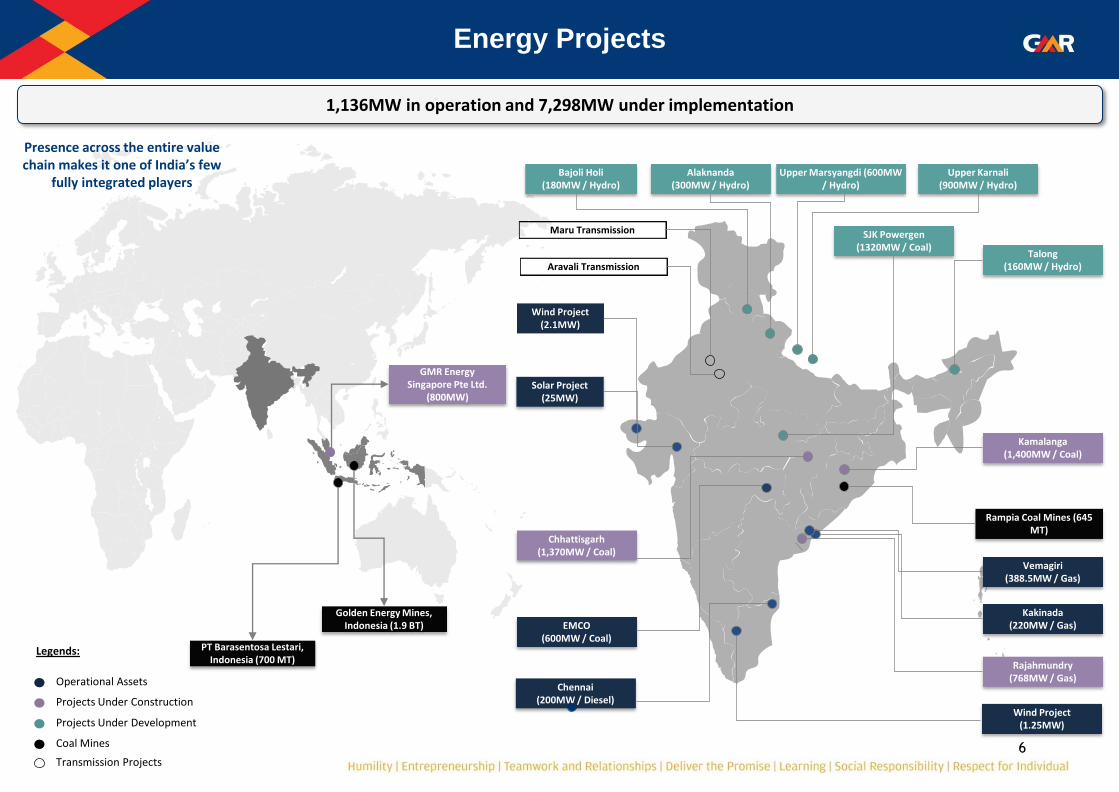

Energy Projects

GMR Energy Singapore Pte Ltd.

(800MW)

PT Barasentosa Lestari, Indonesia (700 MT)

Bajoli Holi (180MW / Hydro)

Alaknanda (300MW / Hydro)

Upper Marsyangdi (600MW / Hydro)

Upper Karnali (900MW / Hydro)

Talong (160MW / Hydro)

Maru Transmission

Aravali Transmission

Wind Project (2.1MW)

Chhattisgarh (1,370MW / Coal)

EMCO (600MW / Coal)

Kakinada (220MW / Gas)

Chennai (200MW / Diesel)

Rajahmundry (768MW / Gas)

Kamalanga (1,400MW / Coal)

Rampia Coal Mines (645 MT)

Vemagiri (388.5MW / Gas)

Solar Project (25MW)

Operational Assets

Projects Under Construction

Projects Under Development

Legends:

Transmission Projects

Coal Mines

1,136MW in operation and 7,298MW under implementation

Wind Project (1.25MW)

Golden Energy Mines, Indonesia (1.9 BT)

SJK Powergen (1320MW / Coal)

Presence across the entire value chain makes it one of India’s few

fully integrated players

7

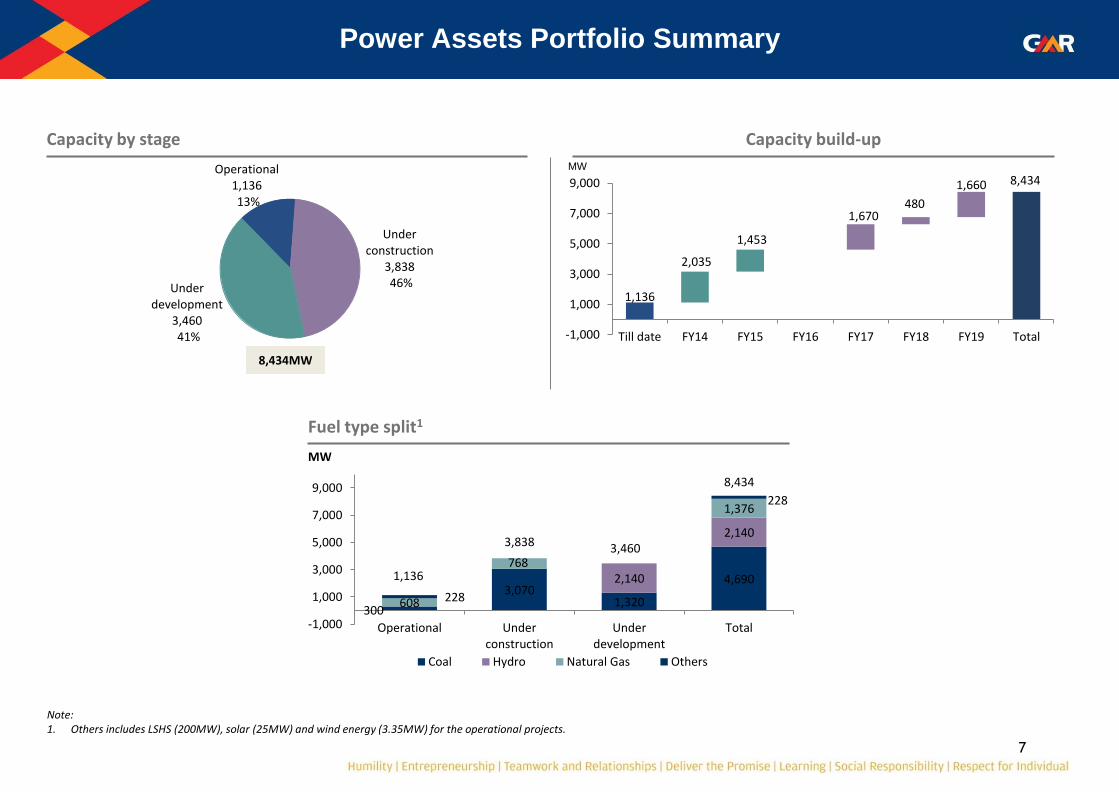

Power Assets Portfolio Summary

Capacity by stage Capacity build-up

Fuel type split1

1,136

8,434

2,035

1,453

1,670 480

1,660

-1,000

1,000

3,000

5,000

7,000

9,000

Till date FY14 FY15 FY16 FY17 FY18 FY19 Total

MW Operational 1,136 13%

Under construction

3,838 46% Under

development 3,460 41%

8,434MW

300

3,070 1,320

4,690 2,140

2,140

608

768

1,376

228

228

1,136

3,838 3,460

8,434

-1,000

1,000

3,000

5,000

7,000

9,000

Operational Underconstruction

Underdevelopment

Total

MW

Coal Hydro Natural Gas Others

Note: 1. Others includes LSHS (200MW), solar (25MW) and wind energy (3.35MW) for the operational projects.

8

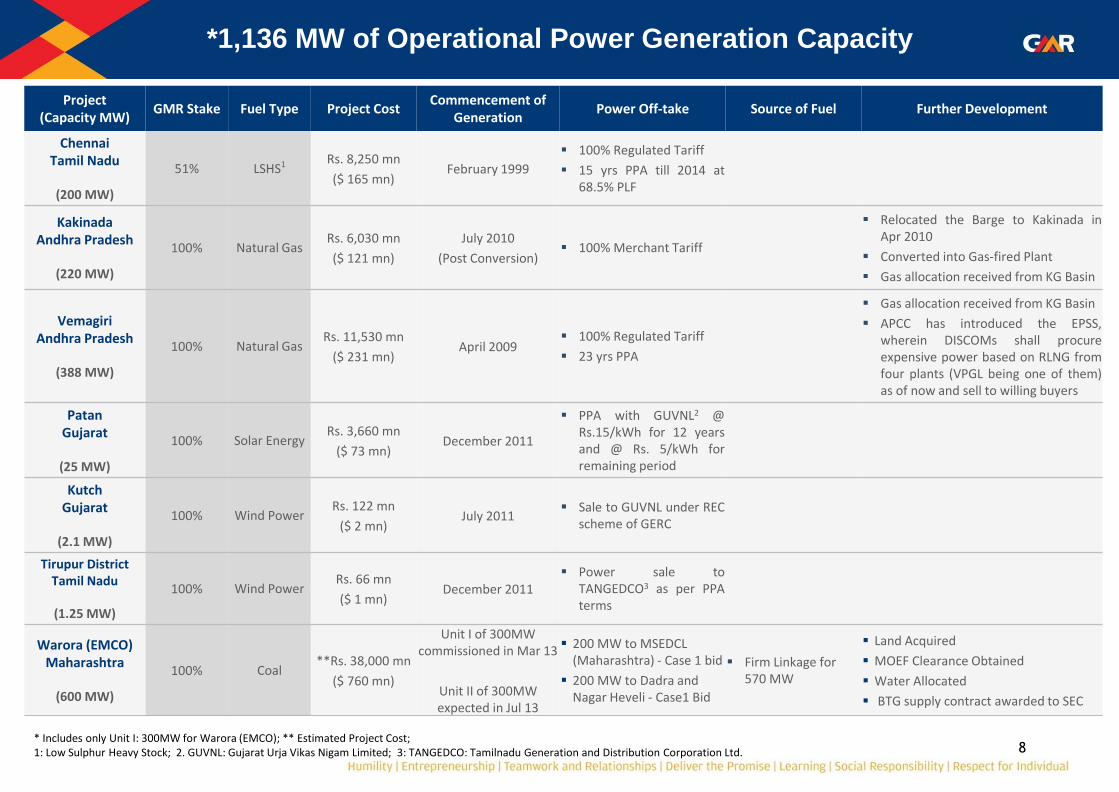

Project (Capacity MW)

GMR Stake Fuel Type Project Cost Commencement of

Generation Power Off-take Source of Fuel Further Development

Chennai Tamil Nadu

(200 MW)

51% LSHS1 Rs. 8,250 mn

($ 165 mn) February 1999

100% Regulated Tariff

15 yrs PPA till 2014 at 68.5% PLF

Kakinada Andhra Pradesh

(220 MW)

100% Natural Gas Rs. 6,030 mn

($ 121 mn)

July 2010

(Post Conversion) 100% Merchant Tariff

Relocated the Barge to Kakinada in Apr 2010

Converted into Gas-fired Plant

Gas allocation received from KG Basin

Vemagiri Andhra Pradesh

(388 MW)

100% Natural Gas Rs. 11,530 mn

($ 231 mn) April 2009

100% Regulated Tariff

23 yrs PPA

Gas allocation received from KG Basin

APCC has introduced the EPSS, wherein DISCOMs shall procure expensive power based on RLNG from four plants (VPGL being one of them) as of now and sell to willing buyers

Patan Gujarat

(25 MW)

100% Solar Energy Rs. 3,660 mn

($ 73 mn) December 2011

PPA with GUVNL2 @ Rs.15/kWh for 12 years and @ Rs. 5/kWh for remaining period

Kutch Gujarat

(2.1 MW)

100% Wind Power Rs. 122 mn

($ 2 mn) July 2011

Sale to GUVNL under REC scheme of GERC

Tirupur District Tamil Nadu

(1.25 MW)

100% Wind Power Rs. 66 mn

($ 1 mn) December 2011

Power sale to TANGEDCO3 as per PPA terms

Warora (EMCO) Maharashtra

(600 MW)

100% Coal **Rs. 38,000 mn

($ 760 mn)

Unit I of 300MW commissioned in Mar 13

Unit II of 300MW expected in Jul 13

200 MW to MSEDCL (Maharashtra) - Case 1 bid

200 MW to Dadra and Nagar Heveli - Case1 Bid

Firm Linkage for 570 MW

Land Acquired

MOEF Clearance Obtained

Water Allocated

BTG supply contract awarded to SEC

*1,136 MW of Operational Power Generation Capacity

* Includes only Unit I: 300MW for Warora (EMCO); ** Estimated Project Cost; 1: Low Sulphur Heavy Stock; 2. GUVNL: Gujarat Urja Vikas Nigam Limited; 3: TANGEDCO: Tamilnadu Generation and Distribution Corporation Ltd.

9

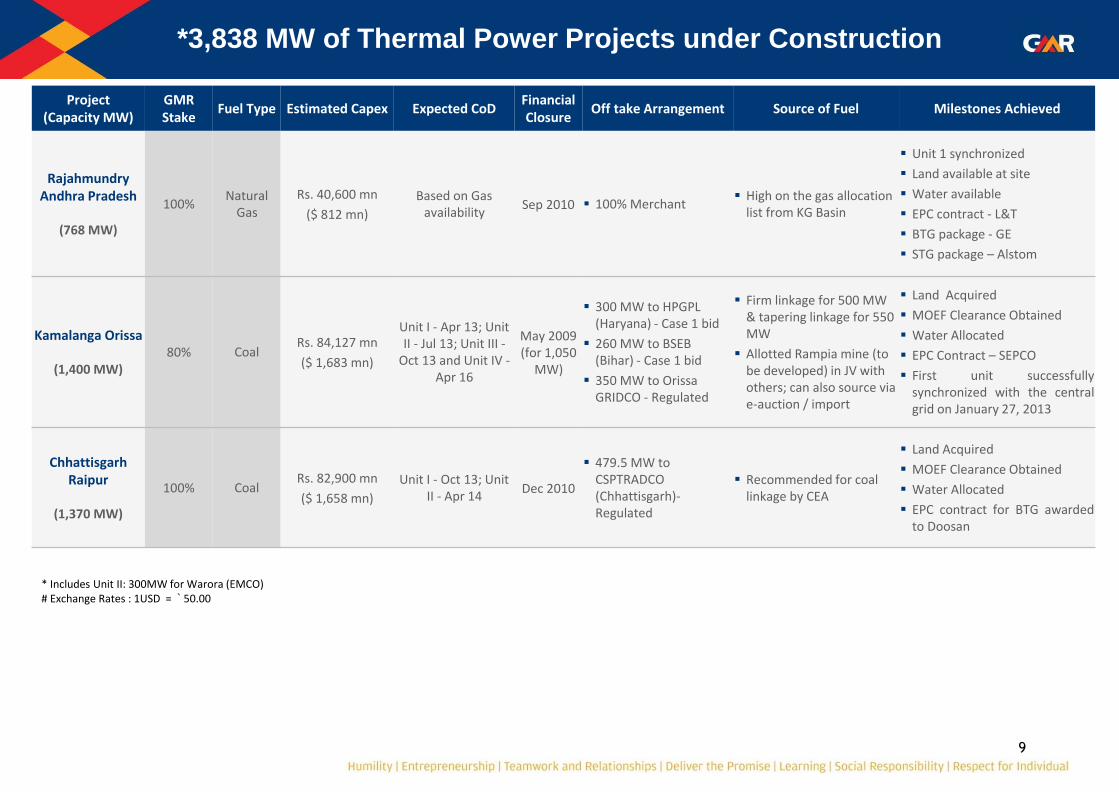

Project (Capacity MW)

GMR Stake

Fuel Type Estimated Capex Expected CoD Financial Closure

Off take Arrangement Source of Fuel Milestones Achieved

Rajahmundry Andhra Pradesh

(768 MW)

100% Natural

Gas

Rs. 40,600 mn

($ 812 mn)

Based on Gas availability

Sep 2010 100% Merchant High on the gas allocation

list from KG Basin

Unit 1 synchronized

Land available at site

Water available

EPC contract - L&T

BTG package - GE

STG package – Alstom

Kamalanga Orissa

(1,400 MW) 80% Coal

Rs. 84,127 mn

($ 1,683 mn)

Unit I - Apr 13; Unit II - Jul 13; Unit III -

Oct 13 and Unit IV - Apr 16

May 2009 (for 1,050

MW)

300 MW to HPGPL (Haryana) - Case 1 bid

260 MW to BSEB (Bihar) - Case 1 bid

350 MW to Orissa GRIDCO - Regulated

Firm linkage for 500 MW & tapering linkage for 550 MW

Allotted Rampia mine (to be developed) in JV with others; can also source via e-auction / import

Land Acquired

MOEF Clearance Obtained

Water Allocated

EPC Contract – SEPCO

First unit successfully synchronized with the central grid on January 27, 2013

Chhattisgarh Raipur

(1,370 MW)

100% Coal Rs. 82,900 mn

($ 1,658 mn)

Unit I - Oct 13; Unit II - Apr 14

Dec 2010

479.5 MW to CSPTRADCO (Chhattisgarh)-Regulated

Recommended for coal linkage by CEA

Land Acquired

MOEF Clearance Obtained

Water Allocated

EPC contract for BTG awarded to Doosan

*3,838 MW of Thermal Power Projects under Construction

* Includes Unit II: 300MW for Warora (EMCO) # Exchange Rates : 1USD = ` 50.00

10

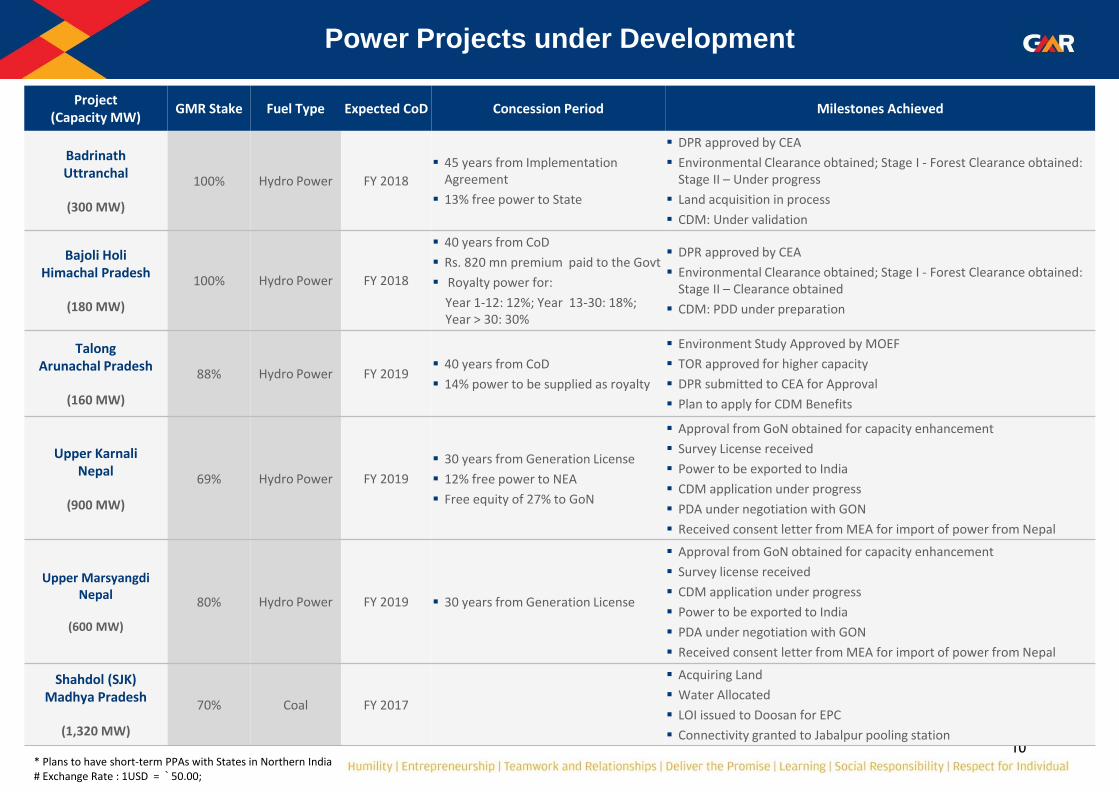

Project (Capacity MW)

GMR Stake Fuel Type Expected CoD Concession Period Milestones Achieved

Badrinath Uttranchal

(300 MW)

100% Hydro Power FY 2018

45 years from Implementation Agreement

13% free power to State

DPR approved by CEA

Environmental Clearance obtained; Stage I - Forest Clearance obtained: Stage II – Under progress

Land acquisition in process

CDM: Under validation

Bajoli Holi Himachal Pradesh

(180 MW)

100% Hydro Power FY 2018

40 years from CoD

Rs. 820 mn premium paid to the Govt

Royalty power for:

Year 1-12: 12%; Year 13-30: 18%; Year > 30: 30%

DPR approved by CEA

Environmental Clearance obtained; Stage I - Forest Clearance obtained: Stage II – Clearance obtained

CDM: PDD under preparation

Talong Arunachal Pradesh

(160 MW)

88% Hydro Power FY 2019 40 years from CoD

14% power to be supplied as royalty

Environment Study Approved by MOEF

TOR approved for higher capacity

DPR submitted to CEA for Approval

Plan to apply for CDM Benefits

Upper Karnali Nepal

(900 MW)

69% Hydro Power FY 2019

30 years from Generation License

12% free power to NEA

Free equity of 27% to GoN

Approval from GoN obtained for capacity enhancement

Survey License received

Power to be exported to India

CDM application under progress

PDA under negotiation with GON

Received consent letter from MEA for import of power from Nepal

Upper Marsyangdi Nepal

(600 MW)

80% Hydro Power FY 2019 30 years from Generation License

Approval from GoN obtained for capacity enhancement

Survey license received

CDM application under progress

Power to be exported to India

PDA under negotiation with GON

Received consent letter from MEA for import of power from Nepal

Shahdol (SJK) Madhya Pradesh

(1,320 MW)

70% Coal FY 2017

Acquiring Land

Water Allocated

LOI issued to Doosan for EPC

Connectivity granted to Jabalpur pooling station

Power Projects under Development

* Plans to have short-term PPAs with States in Northern India # Exchange Rate : 1USD = ` 50.00;

11

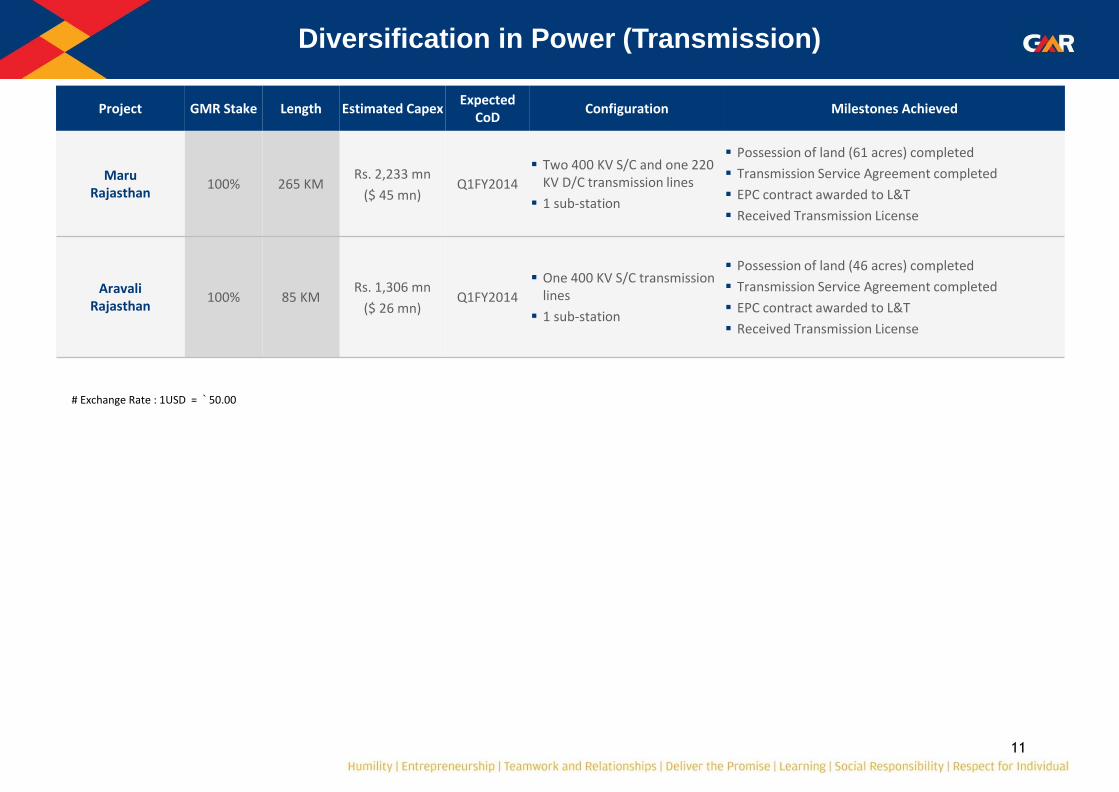

Project GMR Stake Length Estimated Capex Expected

CoD Configuration Milestones Achieved

Maru Rajasthan

100% 265 KM Rs. 2,233 mn

($ 45 mn) Q1FY2014

Two 400 KV S/C and one 220 KV D/C transmission lines

1 sub-station

Possession of land (61 acres) completed

Transmission Service Agreement completed

EPC contract awarded to L&T

Received Transmission License

Aravali Rajasthan

100% 85 KM Rs. 1,306 mn

($ 26 mn) Q1FY2014

One 400 KV S/C transmission lines

1 sub-station

Possession of land (46 acres) completed

Transmission Service Agreement completed

EPC contract awarded to L&T

Received Transmission License

Diversification in Power (Transmission)

# Exchange Rate : 1USD = ` 50.00

12

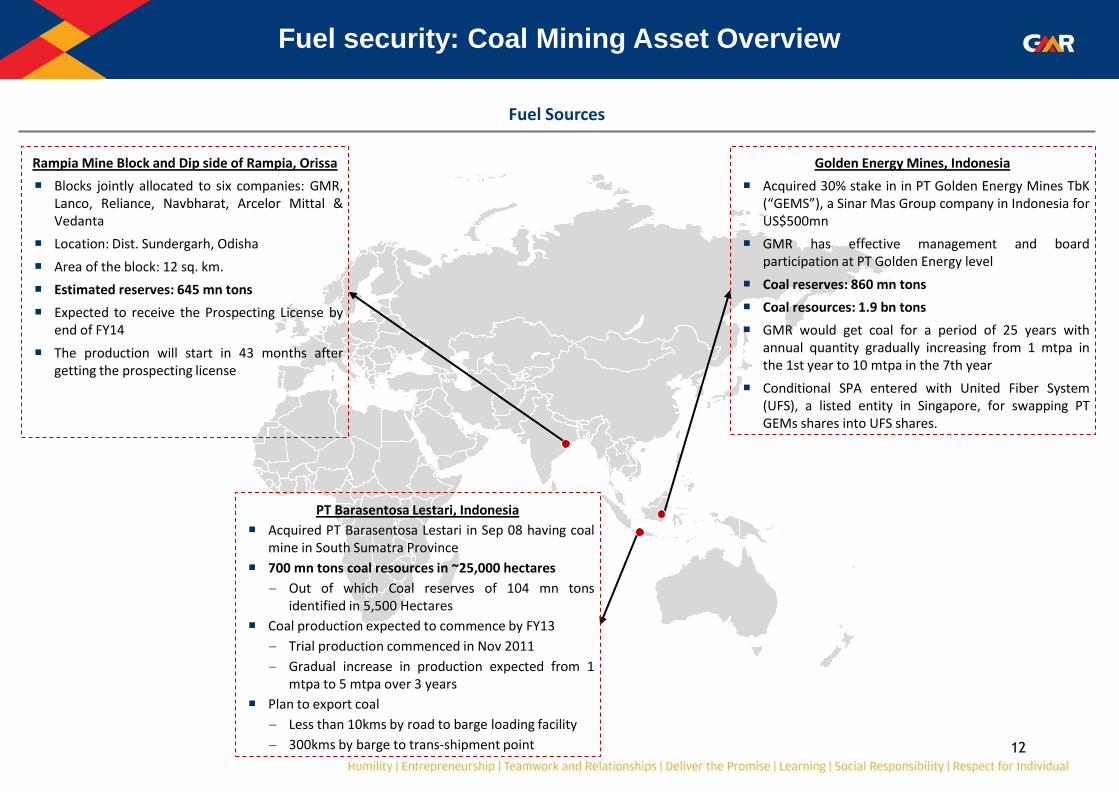

Fuel security: Coal Mining Asset Overview

Rampia Mine Block and Dip side of Rampia, Orissa

Blocks jointly allocated to six companies: GMR, Lanco, Reliance, Navbharat, Arcelor Mittal & Vedanta

Location: Dist. Sundergarh, Odisha

Area of the block: 12 sq. km.

Estimated reserves: 645 mn tons

Expected to receive the Prospecting License by end of FY14

The production will start in 43 months after getting the prospecting license

PT Barasentosa Lestari, Indonesia

Acquired PT Barasentosa Lestari in Sep 08 having coal mine in South Sumatra Province

700 mn tons coal resources in ~25,000 hectares

Out of which Coal reserves of 104 mn tons identified in 5,500 Hectares

Coal production expected to commence by FY13

Trial production commenced in Nov 2011

Gradual increase in production expected from 1 mtpa to 5 mtpa over 3 years

Plan to export coal

Less than 10kms by road to barge loading facility

300kms by barge to trans-shipment point

Golden Energy Mines, Indonesia

Acquired 30% stake in in PT Golden Energy Mines TbK (“GEMS”), a Sinar Mas Group company in Indonesia for US$500mn

GMR has effective management and board participation at PT Golden Energy level

Coal reserves: 860 mn tons

Coal resources: 1.9 bn tons

GMR would get coal for a period of 25 years with annual quantity gradually increasing from 1 mtpa in the 1st year to 10 mtpa in the 7th year

Conditional SPA entered with United Fiber System (UFS), a listed entity in Singapore, for swapping PT GEMs shares into UFS shares.

Fuel Sources

13

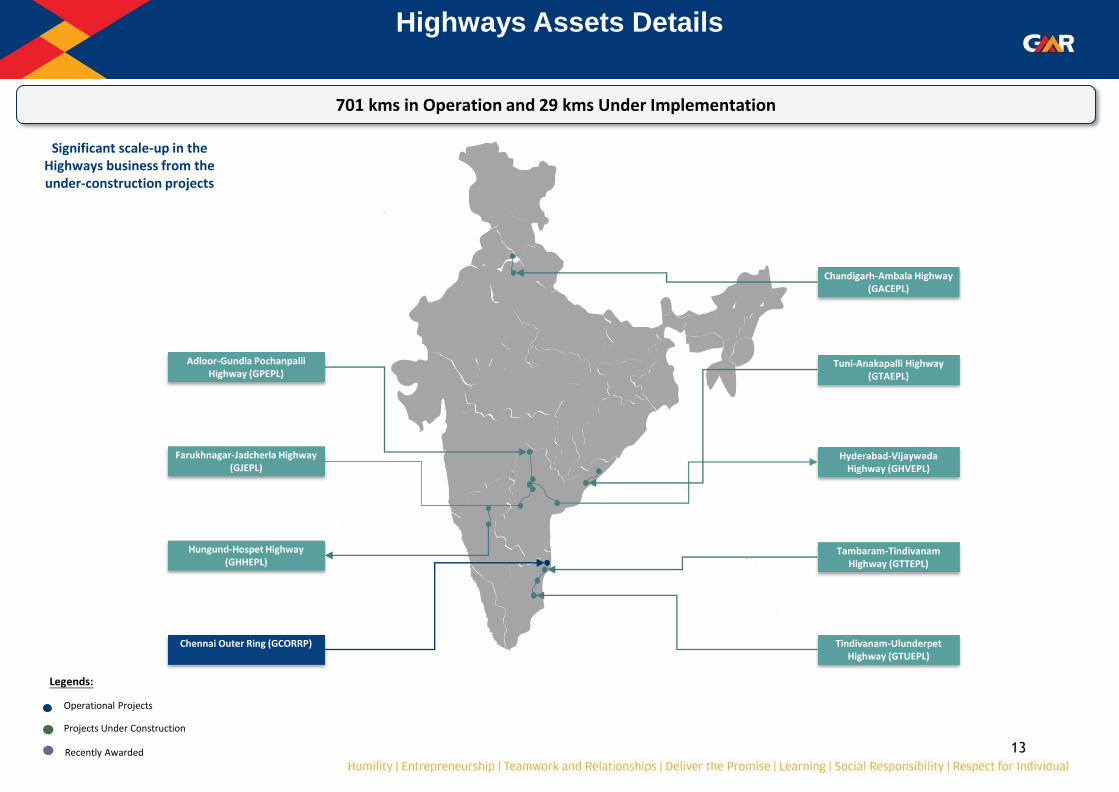

Hyderabad

Chandigarh-Ambala Highway (GACEPL)

Tambaram-Tindivanam Highway (GTTEPL)

Tindivanam-Ulunderpet Highway (GTUEPL)

Tuni-Anakapalli Highway (GTAEPL)

Adloor-Gundla Pochanpalli Highway (GPEPL)

Farukhnagar-Jadcherla Highway (GJEPL)

Hyderabad-Vijaywada Highway (GHVEPL)

Chennai Outer Ring (GCORRP)

Hungund-Hospet Highway (GHHEPL)

Projects Under Construction

Operational Projects

Legends:

Highways Assets Details

701 kms in Operation and 29 kms Under Implementation

Recently Awarded

Significant scale-up in the Highways business from the under-construction projects

14

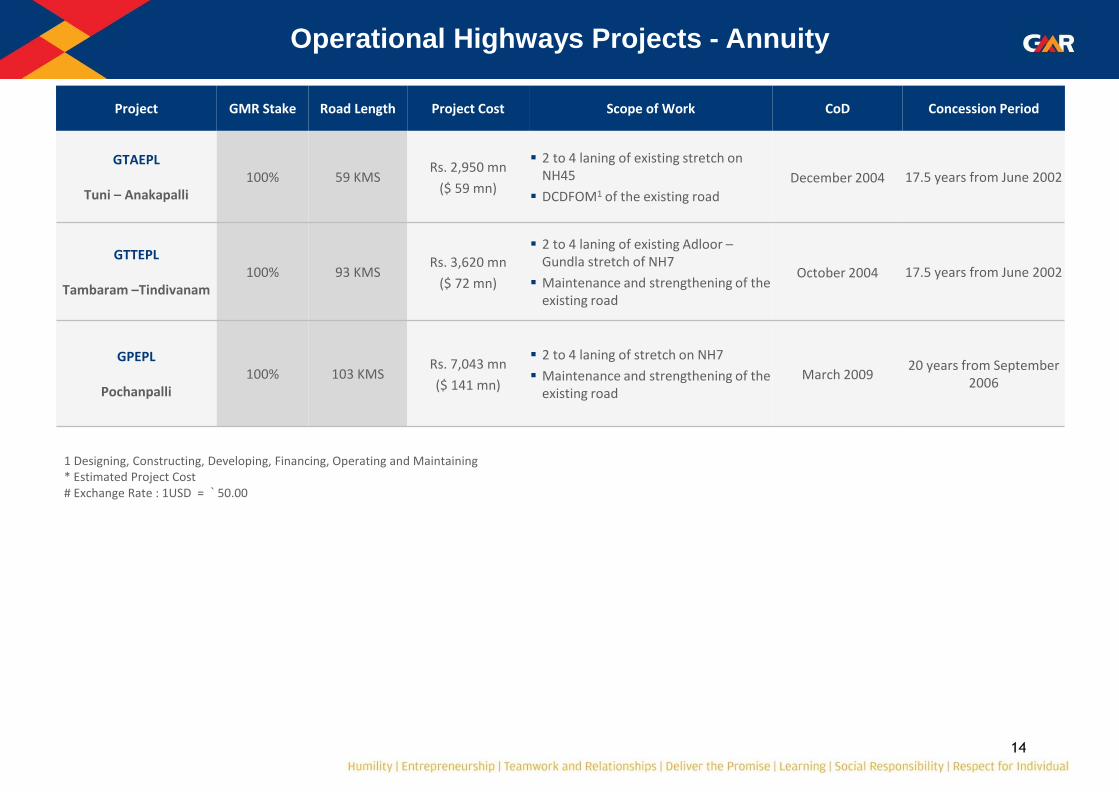

Project GMR Stake Road Length Project Cost Scope of Work CoD Concession Period

GTAEPL

Tuni – Anakapalli 100% 59 KMS

Rs. 2,950 mn

($ 59 mn)

2 to 4 laning of existing stretch on NH45

DCDFOM1 of the existing road

December 2004 17.5 years from June 2002

GTTEPL

Tambaram –Tindivanam 100% 93 KMS

Rs. 3,620 mn

($ 72 mn)

2 to 4 laning of existing Adloor – Gundla stretch of NH7

Maintenance and strengthening of the existing road

October 2004 17.5 years from June 2002

GPEPL

Pochanpalli 100% 103 KMS

Rs. 7,043 mn

($ 141 mn)

2 to 4 laning of stretch on NH7

Maintenance and strengthening of the existing road

March 2009 20 years from September

2006

Operational Highways Projects - Annuity

1 Designing, Constructing, Developing, Financing, Operating and Maintaining * Estimated Project Cost # Exchange Rate : 1USD = ` 50.00

15

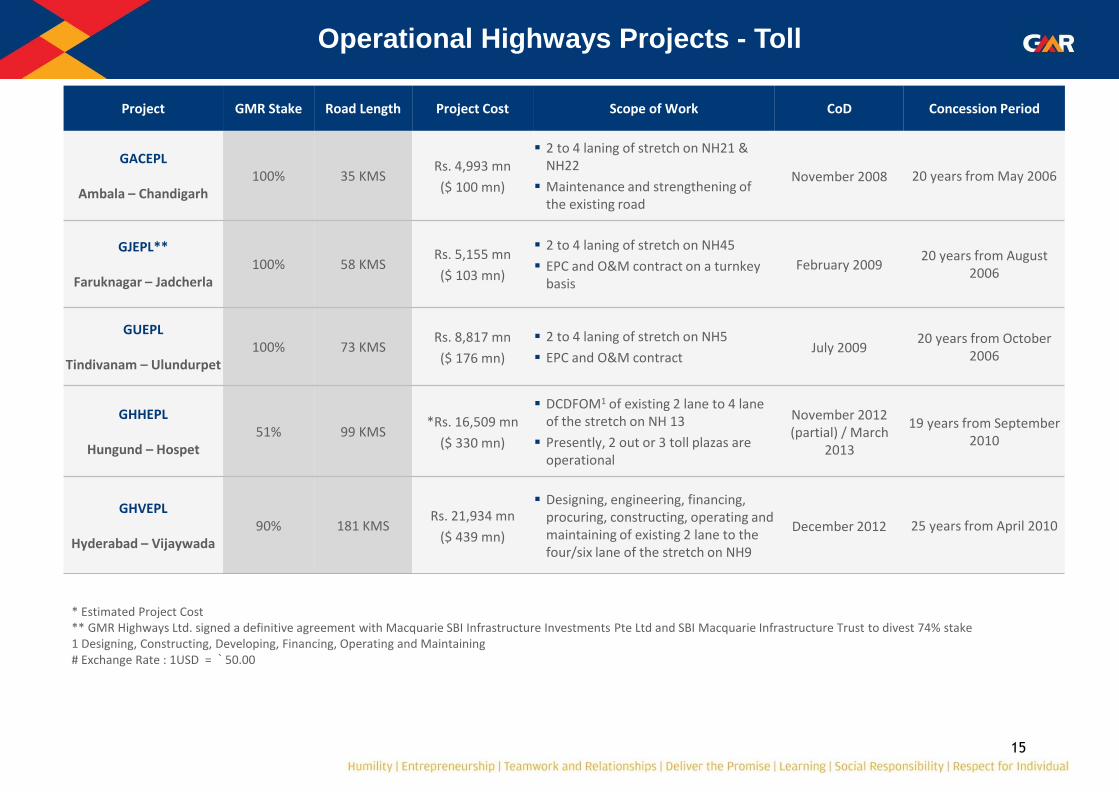

Project GMR Stake Road Length Project Cost Scope of Work CoD Concession Period

GACEPL

Ambala – Chandigarh 100% 35 KMS

Rs. 4,993 mn

($ 100 mn)

2 to 4 laning of stretch on NH21 & NH22

Maintenance and strengthening of the existing road

November 2008 20 years from May 2006

GJEPL**

Faruknagar – Jadcherla 100% 58 KMS

Rs. 5,155 mn

($ 103 mn)

2 to 4 laning of stretch on NH45

EPC and O&M contract on a turnkey basis

February 2009 20 years from August

2006

GUEPL

Tindivanam – Ulundurpet 100% 73 KMS

Rs. 8,817 mn

($ 176 mn)

2 to 4 laning of stretch on NH5

EPC and O&M contract July 2009

20 years from October 2006

GHHEPL

Hungund – Hospet 51% 99 KMS

*Rs. 16,509 mn

($ 330 mn)

DCDFOM1 of existing 2 lane to 4 lane of the stretch on NH 13

Presently, 2 out or 3 toll plazas are operational

November 2012 (partial) / March

2013

19 years from September 2010

GHVEPL

Hyderabad – Vijaywada 90% 181 KMS

Rs. 21,934 mn

($ 439 mn)

Designing, engineering, financing, procuring, constructing, operating and maintaining of existing 2 lane to the four/six lane of the stretch on NH9

December 2012 25 years from April 2010

Operational Highways Projects - Toll

* Estimated Project Cost ** GMR Highways Ltd. signed a definitive agreement with Macquarie SBI Infrastructure Investments Pte Ltd and SBI Macquarie Infrastructure Trust to divest 74% stake 1 Designing, Constructing, Developing, Financing, Operating and Maintaining # Exchange Rate : 1USD = ` 50.00

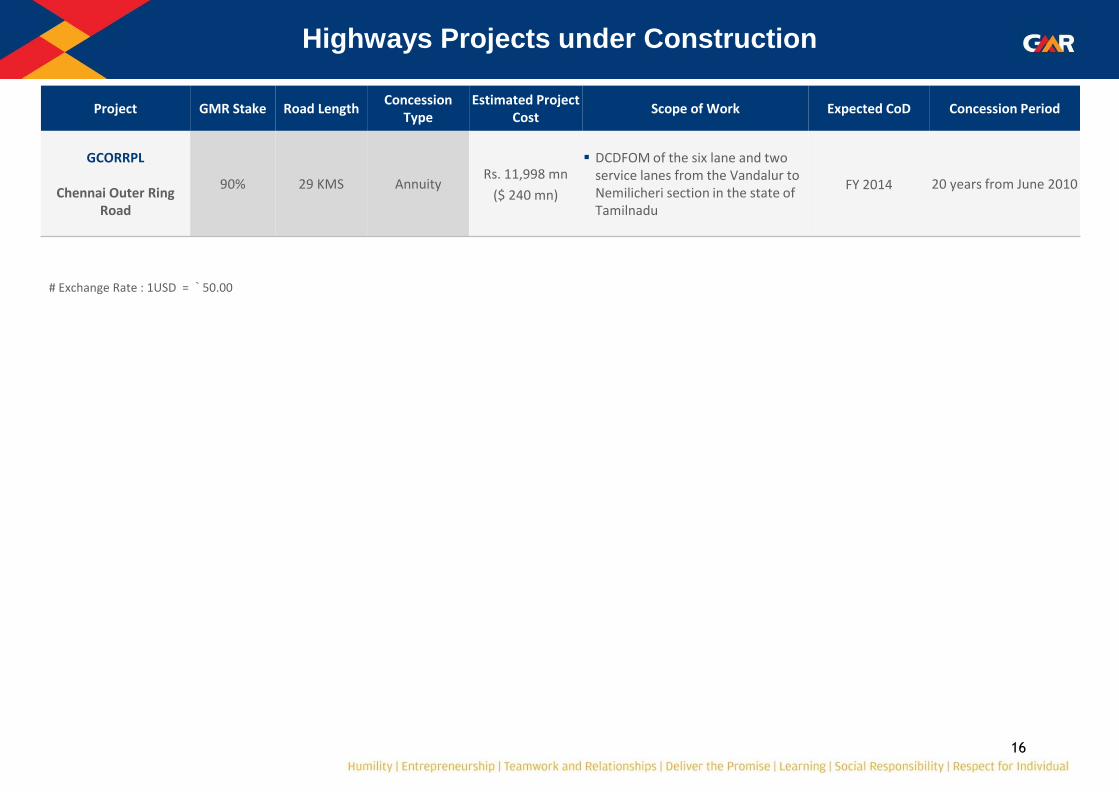

16

Project GMR Stake Road Length Concession

Type Estimated Project

Cost Scope of Work Expected CoD Concession Period

GCORRPL

Chennai Outer Ring Road

90% 29 KMS Annuity Rs. 11,998 mn

($ 240 mn)

DCDFOM of the six lane and two service lanes from the Vandalur to Nemilicheri section in the state of Tamilnadu

FY 2014 20 years from June 2010

Highways Projects under Construction

# Exchange Rate : 1USD = ` 50.00

17

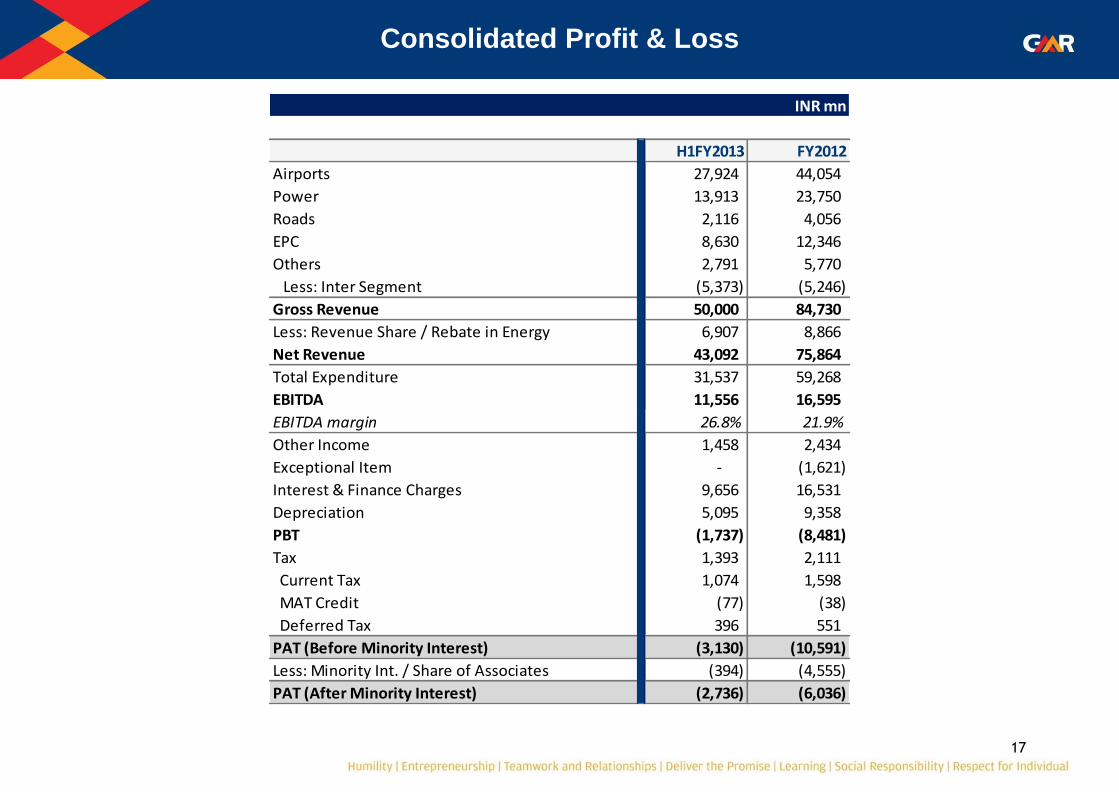

Consolidated Profit & Loss

H1FY2013 FY2012

Airports 27,924 44,054

Power 13,913 23,750

Roads 2,116 4,056

EPC 8,630 12,346

Others 2,791 5,770

Less: Inter Segment (5,373) (5,246)

Gross Revenue 50,000 84,730

Less: Revenue Share / Rebate in Energy 6,907 8,866

Net Revenue 43,092 75,864

Total Expenditure 31,537 59,268

EBITDA 11,556 16,595

EBITDA margin 26.8% 21.9%

Other Income 1,458 2,434

Exceptional Item - (1,621)

Interest & Finance Charges 9,656 16,531

Depreciation 5,095 9,358

PBT (1,737) (8,481)

Tax 1,393 2,111

Current Tax 1,074 1,598

MAT Credit (77) (38)

Deferred Tax 396 551

PAT (Before Minority Interest) (3,130) (10,591)

Less: Minority Int. / Share of Associates (394) (4,555)

PAT (After Minority Interest) (2,736) (6,036)

INR mn

18

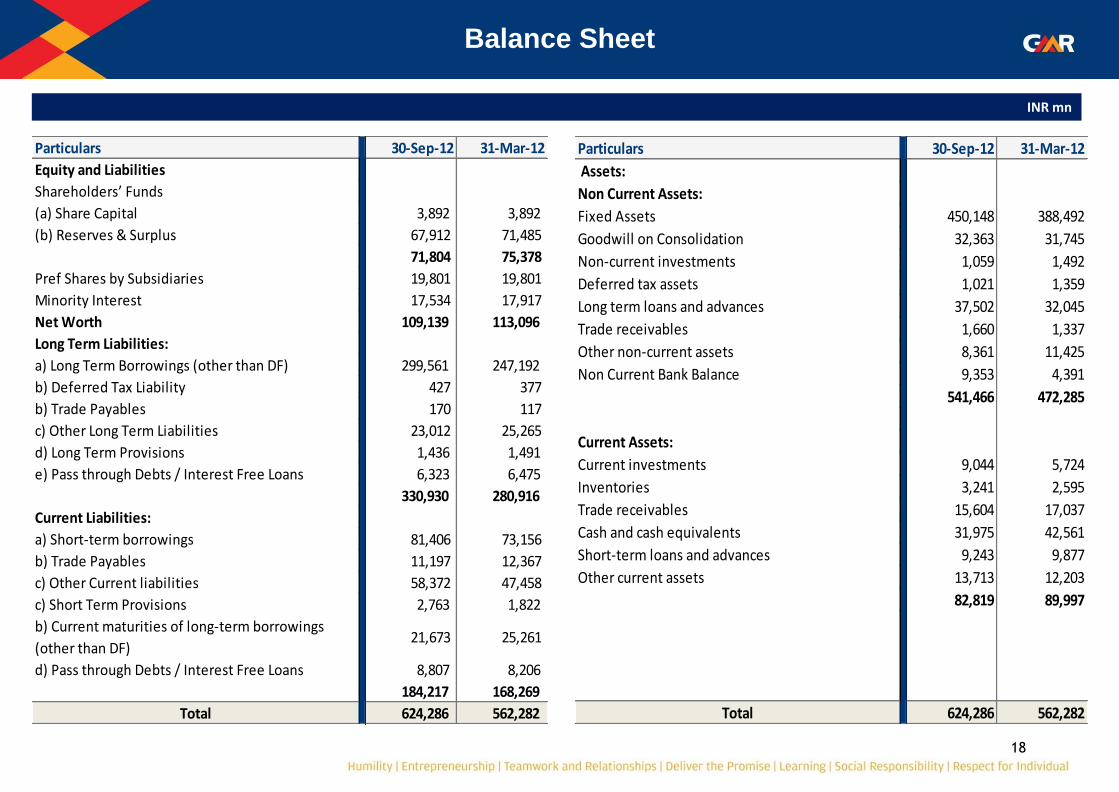

Balance Sheet

Particulars 30-Sep-12 31-Mar-12

Assets:

Non Current Assets:

Fixed Assets 450,148 388,492

Goodwill on Consolidation 32,363 31,745

Non-current investments 1,059 1,492

Deferred tax assets 1,021 1,359

Long term loans and advances 37,502 32,045

Trade receivables 1,660 1,337

Other non-current assets 8,361 11,425

Non Current Bank Balance 9,353 4,391

541,466 472,285

Current Assets:

Current investments 9,044 5,724

Inventories 3,241 2,595

Trade receivables 15,604 17,037

Cash and cash equivalents 31,975 42,561

Short-term loans and advances 9,243 9,877

Other current assets 13,713 12,203

82,819 89,997

Total 624,286 562,282

Particulars 30-Sep-12 31-Mar-12

Equity and Liabilities

Shareholders’ Funds

(a) Share Capital 3,892 3,892

(b) Reserves & Surplus 67,912 71,485

71,804 75,378

Pref Shares by Subsidiaries 19,801 19,801

Minority Interest 17,534 17,917

Net Worth 109,139 113,096

Long Term Liabilities:

a) Long Term Borrowings (other than DF) 299,561 247,192

b) Deferred Tax Liability 427 377

b) Trade Payables 170 117

c) Other Long Term Liabilities 23,012 25,265

d) Long Term Provisions 1,436 1,491

e) Pass through Debts / Interest Free Loans 6,323 6,475

330,930 280,916

Current Liabilities:

a) Short-term borrowings 81,406 73,156

b) Trade Payables 11,197 12,367

c) Other Current liabilities 58,372 47,458

c) Short Term Provisions 2,763 1,822

b) Current maturities of long-term borrowings

(other than DF) 21,673 25,261

d) Pass through Debts / Interest Free Loans 8,807 8,206

184,217 168,269

Total 624,286 562,282

INR mn

19

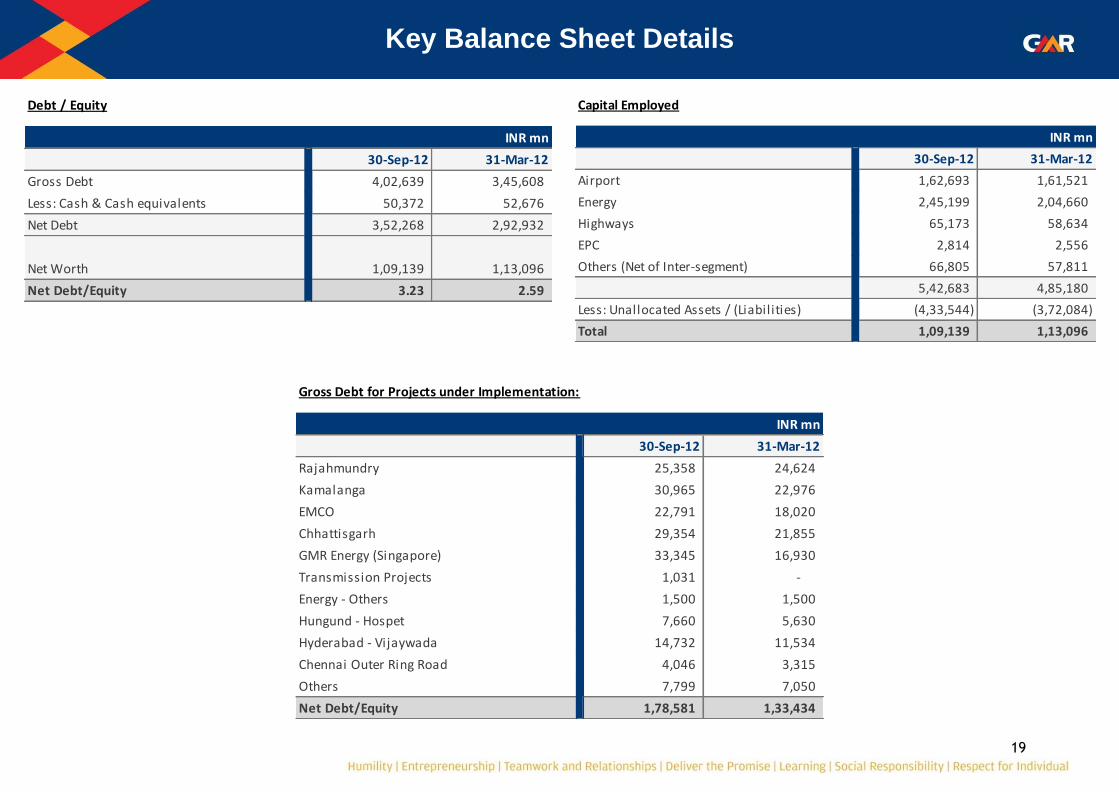

Key Balance Sheet Details

Debt / Equity

30-Sep-12 31-Mar-12

Gross Debt 4,02,639 3,45,608

Less: Cash & Cash equivalents 50,372 52,676

Net Debt 3,52,268 2,92,932

Net Worth 1,09,139 1,13,096

Net Debt/Equity 3.23 2.59

INR mn

Gross Debt for Projects under Implementation:

30-Sep-12 31-Mar-12

Rajahmundry 25,358 24,624

Kamalanga 30,965 22,976

EMCO 22,791 18,020

Chhattisgarh 29,354 21,855

GMR Energy (Singapore) 33,345 16,930

Transmission Projects 1,031 -

Energy - Others 1,500 1,500

Hungund - Hospet 7,660 5,630

Hyderabad - Vijaywada 14,732 11,534

Chennai Outer Ring Road 4,046 3,315

Others 7,799 7,050

Net Debt/Equity 1,78,581 1,33,434

INR mn

Capital Employed

30-Sep-12 31-Mar-12

Airport 1,62,693 1,61,521

Energy 2,45,199 2,04,660

Highways 65,173 58,634

EPC 2,814 2,556

Others (Net of Inter-segment) 66,805 57,811

5,42,683 4,85,180

Less: Unallocated Assets / (Liabilities) (4,33,544) (3,72,084)

Total 1,09,139 1,13,096

INR mn

20

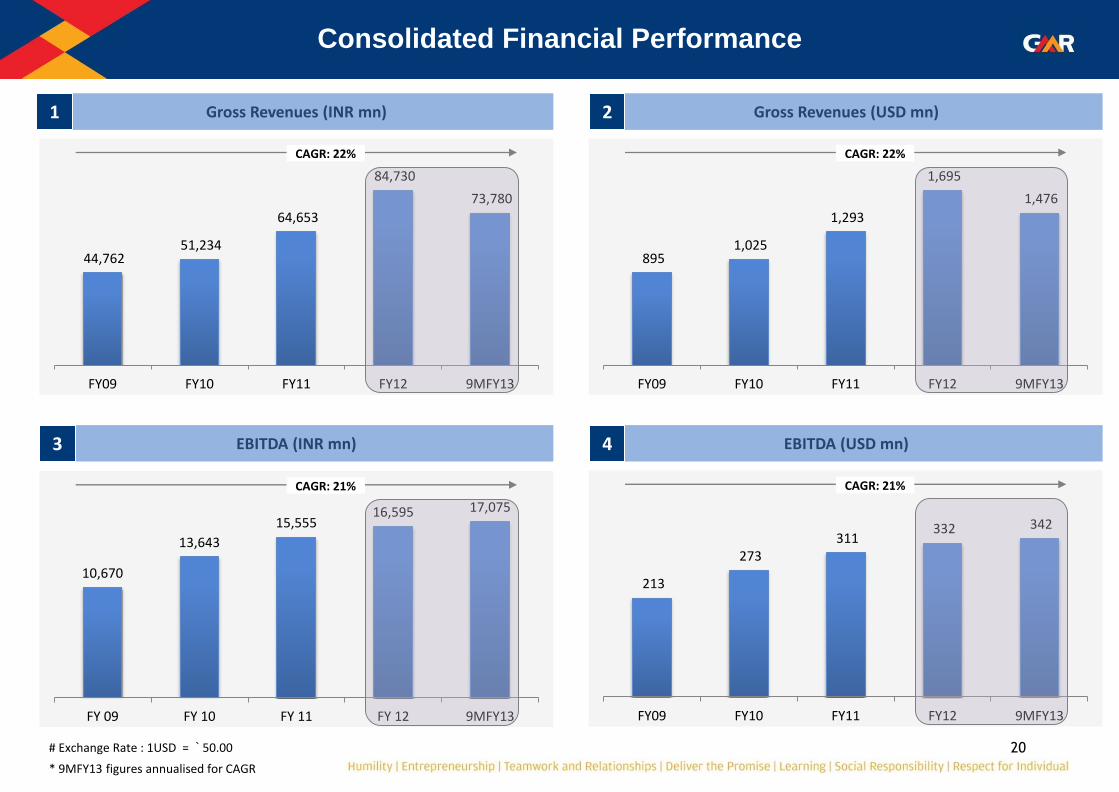

Consolidated Financial Performance

EBITDA (INR mn) 3

Gross Revenues (INR mn) 1

EBITDA (USD mn) 4

Gross Revenues (USD mn) 2

# Exchange Rate : 1USD = ` 50.00

* 9MFY13 figures annualised for CAGR

44,762 51,234

64,653

84,730

73,780

FY09 FY10 FY11 FY12 9MFY13

CAGR: 22%

895 1,025

1,293

1,695

1,476

FY09 FY10 FY11 FY12 9MFY13

CAGR: 22%

10,670

13,643

15,555 16,595 17,075

FY 09 FY 10 FY 11 FY 12 9MFY13

CAGR: 21%

213

273 311

332 342

FY09 FY10 FY11 FY12 9MFY13

CAGR: 21%

Appendix

22

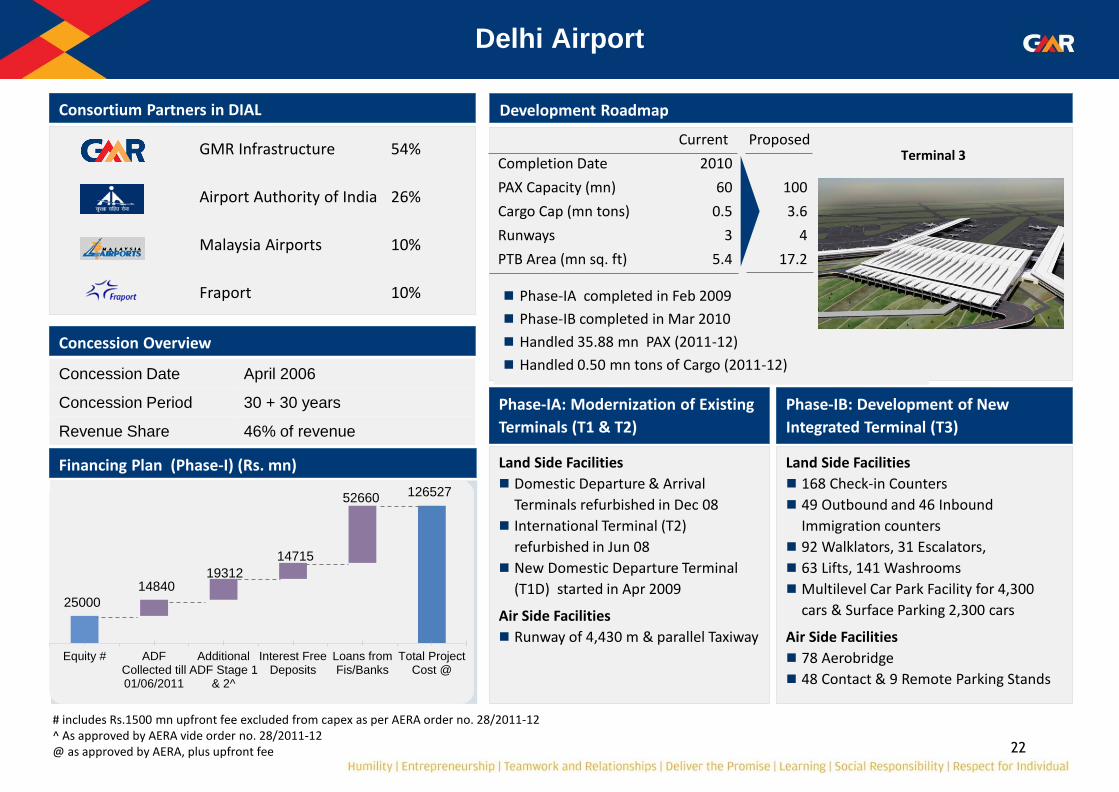

Current Proposed

Completion Date 2010

PAX Capacity (mn) 60 100

Cargo Cap (mn tons) 0.5 3.6

Runways 3 4

PTB Area (mn sq. ft) 5.4 17.2

GMR Infrastructure 54%

Airport Authority of India 26%

Malaysia Airports 10%

Fraport 10%

Delhi Airport

Consortium Partners in DIAL

Financing Plan (Phase-I) (Rs. mn)

Development Roadmap

Concession Overview

Phase-IB: Development of New

Integrated Terminal (T3)

Phase-IA: Modernization of Existing

Terminals (T1 & T2)

Land Side Facilities

168 Check-in Counters

49 Outbound and 46 Inbound

Immigration counters

92 Walklators, 31 Escalators,

63 Lifts, 141 Washrooms

Multilevel Car Park Facility for 4,300

cars & Surface Parking 2,300 cars

Air Side Facilities

78 Aerobridge

48 Contact & 9 Remote Parking Stands

Land Side Facilities

Domestic Departure & Arrival

Terminals refurbished in Dec 08

International Terminal (T2)

refurbished in Jun 08

New Domestic Departure Terminal

(T1D) started in Apr 2009

Air Side Facilities

Runway of 4,430 m & parallel Taxiway

Terminal 3

Phase-IA completed in Feb 2009

Phase-IB completed in Mar 2010

Handled 35.88 mn PAX (2011-12)

Handled 0.50 mn tons of Cargo (2011-12) Concession Date April 2006

Concession Period 30 + 30 years

Revenue Share 46% of revenue

25000

14840 19312

14715

52660 126527

Equity # ADFCollected till01/06/2011

AdditionalADF Stage 1

& 2^

Interest FreeDeposits

Loans fromFis/Banks

Total ProjectCost @

# includes Rs.1500 mn upfront fee excluded from capex as per AERA order no. 28/2011-12 ^ As approved by AERA vide order no. 28/2011-12 @ as approved by AERA, plus upfront fee

23

Delhi Airport: Annual Operational Performance

Cargo handled (in ‘000s of Tonnes)

Air Traffic Movements (ATMs in ‘000s) Passenger Traffic (in millions)

3

2

includes non billable domestic cargo.

Revenue growth (in Rs millions) 4

157.9 185.8 201.2

240.4

59.5 63.4

74.8

76.9

FY 09 FY 10 FY11 FY12

109.9 165.0 136.0 135.2

287.2

334.5 390.9 367.6

FY 09 FY 10 FY11 FY12

Domestic International Non aero revenue also includes cargo and CPD income

3,420 4,221 4,648 4,829

6,055 7,311

7,784 10,097

FY 09 FY 10 FY11 FY12

Aero Non-aero

15.1 17.8 20.7 25.1

7.8 8.3

9.3

10.8

FY 09 FY 10 FY11 FY12

1

24

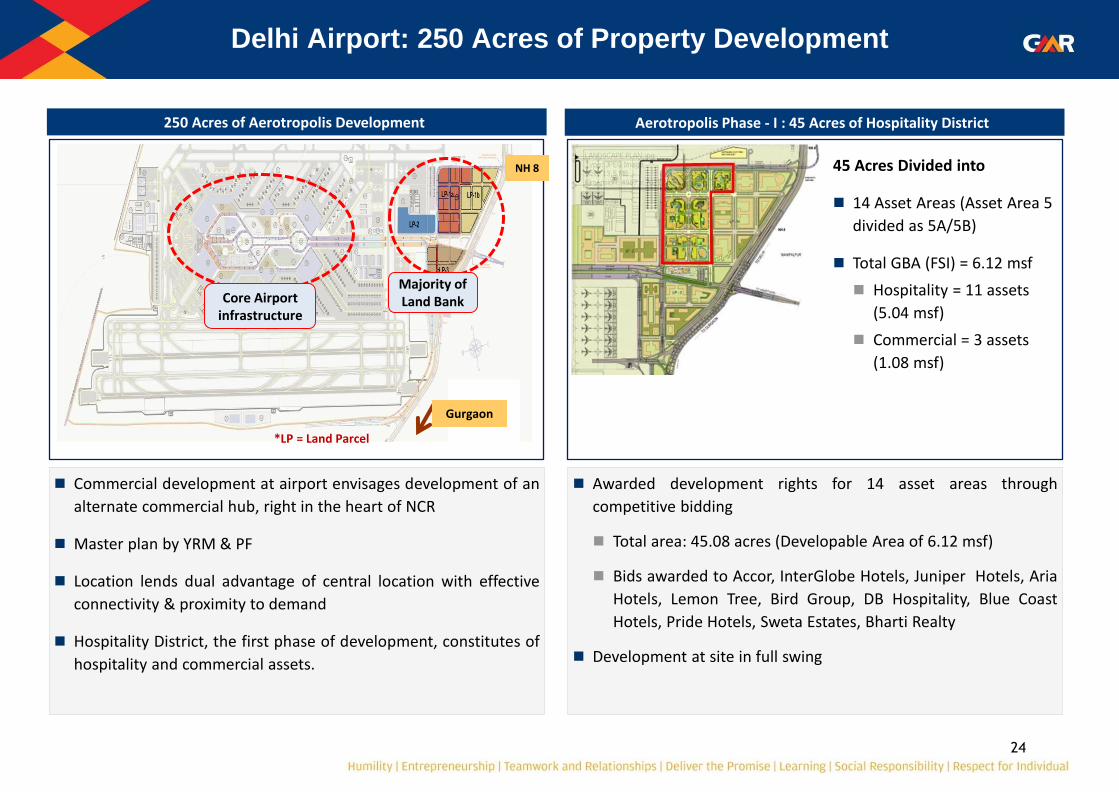

Delhi Airport: 250 Acres of Property Development

250 Acres of Aerotropolis Development Aerotropolis Phase - I : 45 Acres of Hospitality District

45 Acres Divided into

14 Asset Areas (Asset Area 5

divided as 5A/5B)

Total GBA (FSI) = 6.12 msf

Hospitality = 11 assets

(5.04 msf)

Commercial = 3 assets

(1.08 msf)

Commercial development at airport envisages development of an

alternate commercial hub, right in the heart of NCR

Master plan by YRM & PF

Location lends dual advantage of central location with effective

connectivity & proximity to demand

Hospitality District, the first phase of development, constitutes of

hospitality and commercial assets.

Awarded development rights for 14 asset areas through

competitive bidding

Total area: 45.08 acres (Developable Area of 6.12 msf)

Bids awarded to Accor, InterGlobe Hotels, Juniper Hotels, Aria

Hotels, Lemon Tree, Bird Group, DB Hospitality, Blue Coast

Hotels, Pride Hotels, Sweta Estates, Bharti Realty

Development at site in full swing

Majority of Land Bank Core Airport

infrastructure

NH 8

Gurgaon

*LP = Land Parcel

25

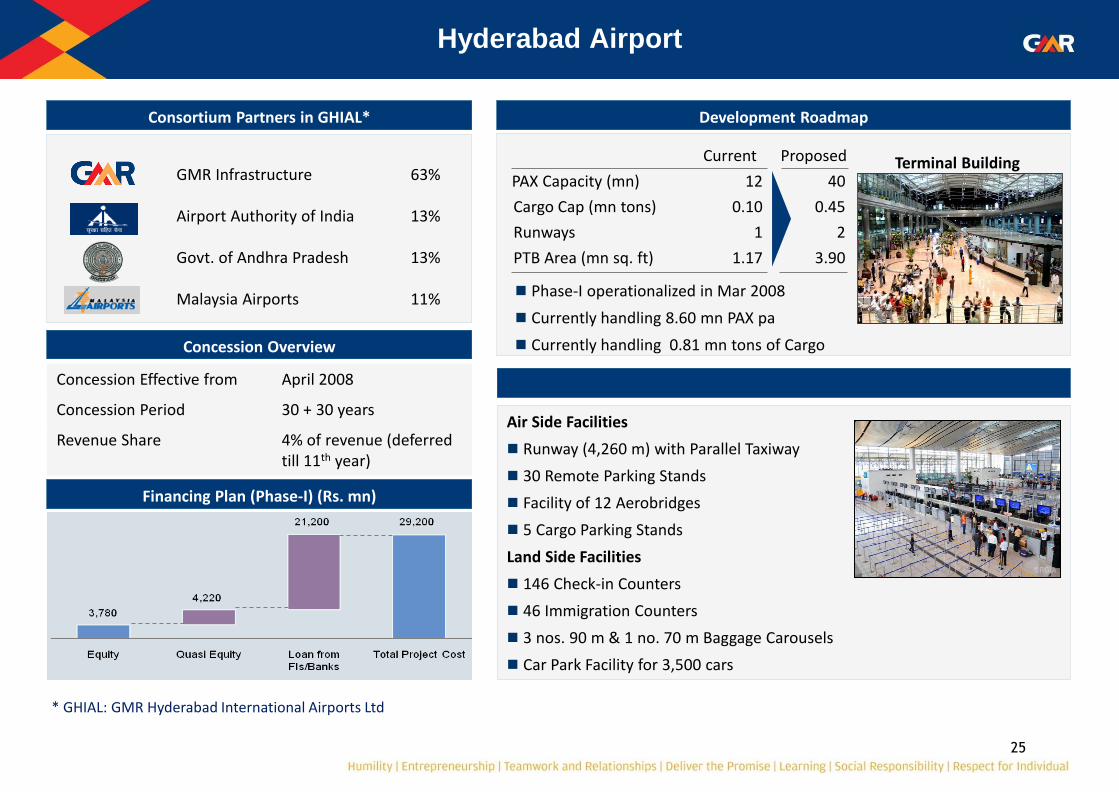

Concession Effective from April 2008

Concession Period 30 + 30 years

Revenue Share 4% of revenue (deferred till 11th year)

Hyderabad Airport

Consortium Partners in GHIAL*

Air Side Facilities

Runway (4,260 m) with Parallel Taxiway

30 Remote Parking Stands

Facility of 12 Aerobridges

5 Cargo Parking Stands

Land Side Facilities

146 Check-in Counters

46 Immigration Counters

3 nos. 90 m & 1 no. 70 m Baggage Carousels

Car Park Facility for 3,500 cars

Financing Plan (Phase-I) (Rs. mn)

Development Roadmap

Terminal Building

Phase-I operationalized in Mar 2008

Currently handling 8.60 mn PAX pa

Currently handling 0.81 mn tons of Cargo Concession Overview

Current Proposed

PAX Capacity (mn) 12 40

Cargo Cap (mn tons) 0.10 0.45

Runways 1 2

PTB Area (mn sq. ft) 1.17 3.90

GMR Infrastructure 63%

Airport Authority of India 13%

Govt. of Andhra Pradesh 13%

Malaysia Airports 11%

* GHIAL: GMR Hyderabad International Airports Ltd

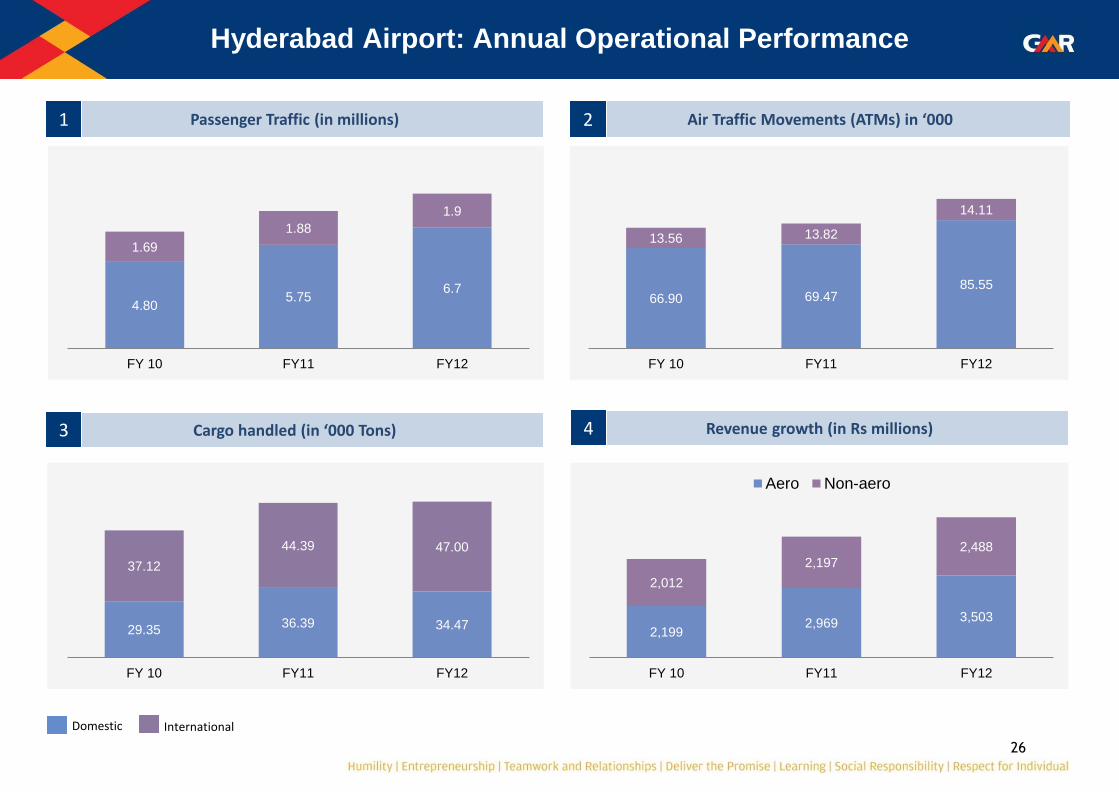

26

Hyderabad Airport: Annual Operational Performance

Cargo handled (in ‘000 Tons)

Air Traffic Movements (ATMs) in ‘000 Passenger Traffic (in millions)

3

2 1

Domestic International

Revenue growth (in Rs millions) 4

4.80 5.75

6.7

1.69

1.88

1.9

FY 10 FY11 FY12

66.90 69.47 85.55

13.56 13.82

14.11

FY 10 FY11 FY12

29.35 36.39 34.47

37.12

44.39 47.00

FY 10 FY11 FY12

2,199 2,969

3,503

2,012

2,197

2,488

FY 10 FY11 FY12

Aero Non-aero

27

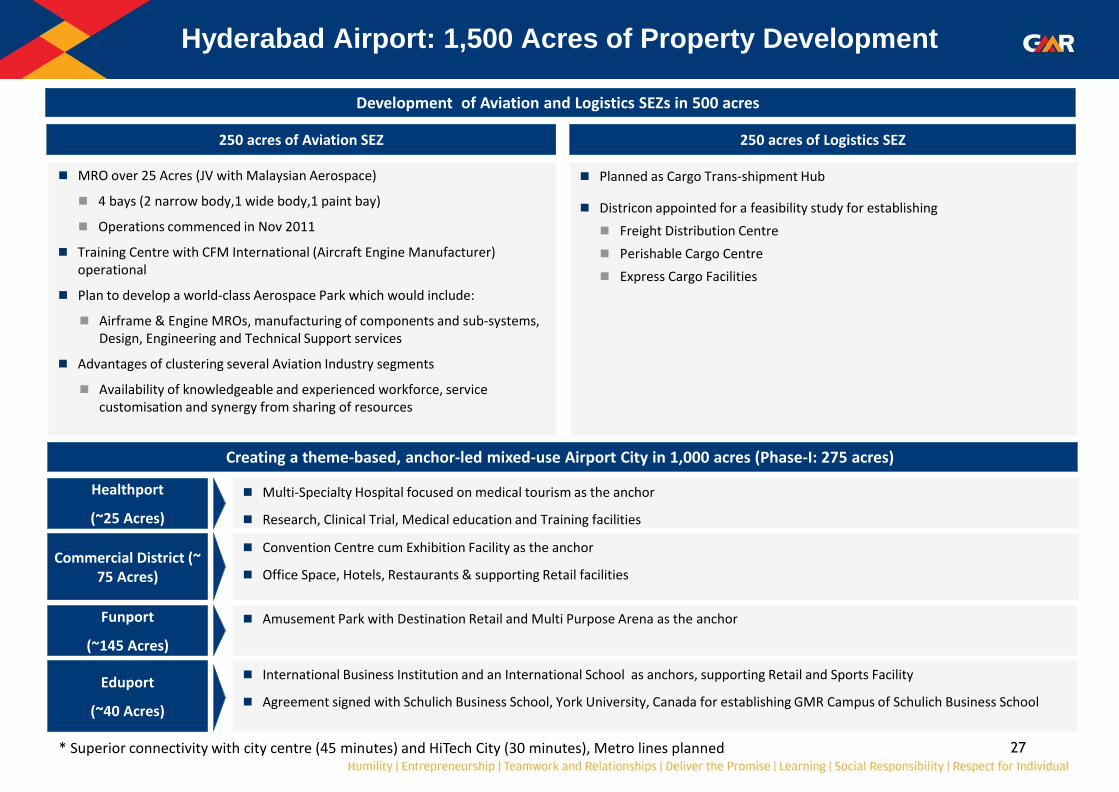

Hyderabad Airport: 1,500 Acres of Property Development

* Superior connectivity with city centre (45 minutes) and HiTech City (30 minutes), Metro lines planned

Healthport

(~25 Acres)

Multi-Specialty Hospital focused on medical tourism as the anchor

Research, Clinical Trial, Medical education and Training facilities

Funport

(~145 Acres)

Amusement Park with Destination Retail and Multi Purpose Arena as the anchor

Commercial District (~ 75 Acres)

Convention Centre cum Exhibition Facility as the anchor

Office Space, Hotels, Restaurants & supporting Retail facilities

Eduport

(~40 Acres)

International Business Institution and an International School as anchors, supporting Retail and Sports Facility

Agreement signed with Schulich Business School, York University, Canada for establishing GMR Campus of Schulich Business School

Creating a theme-based, anchor-led mixed-use Airport City in 1,000 acres (Phase-I: 275 acres)

Development of Aviation and Logistics SEZs in 500 acres

250 acres of Aviation SEZ

MRO over 25 Acres (JV with Malaysian Aerospace)

4 bays (2 narrow body,1 wide body,1 paint bay)

Operations commenced in Nov 2011

Training Centre with CFM International (Aircraft Engine Manufacturer) operational

Plan to develop a world-class Aerospace Park which would include:

Airframe & Engine MROs, manufacturing of components and sub-systems, Design, Engineering and Technical Support services

Advantages of clustering several Aviation Industry segments

Availability of knowledgeable and experienced workforce, service customisation and synergy from sharing of resources

250 acres of Logistics SEZ

Planned as Cargo Trans-shipment Hub

Districon appointed for a feasibility study for establishing

Freight Distribution Centre

Perishable Cargo Centre

Express Cargo Facilities

28

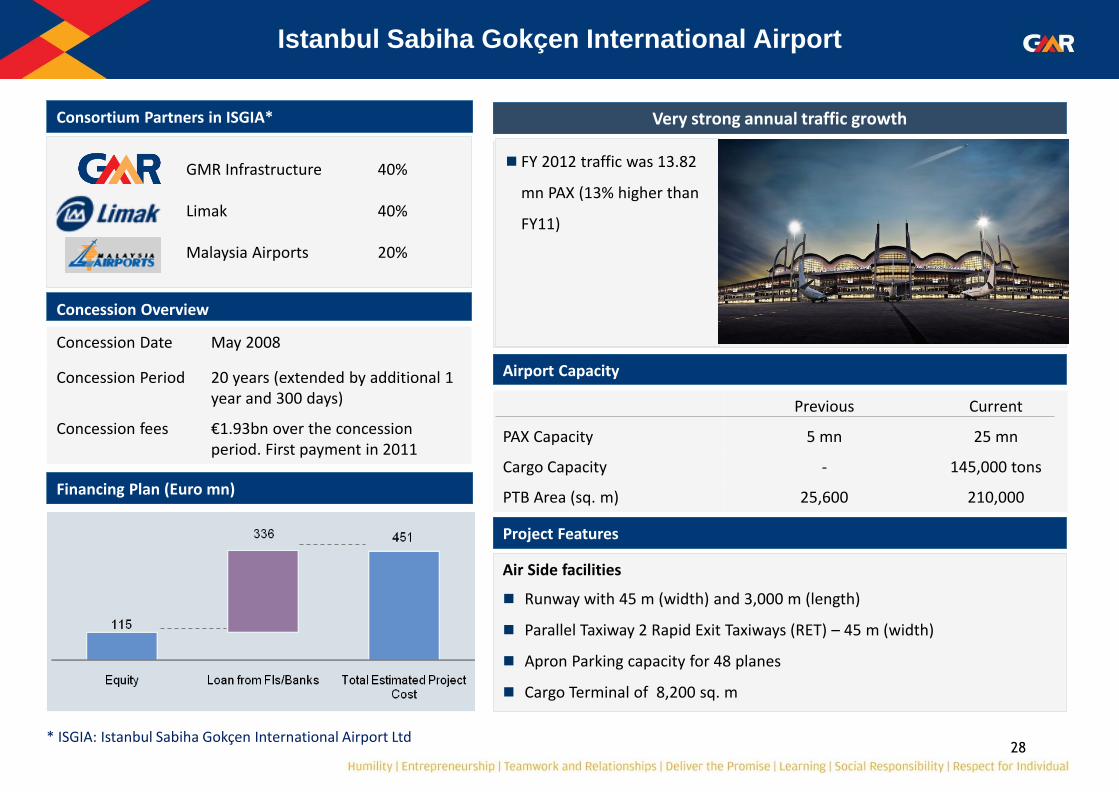

Airport Capacity

Project Features

Air Side facilities

Runway with 45 m (width) and 3,000 m (length)

Parallel Taxiway 2 Rapid Exit Taxiways (RET) – 45 m (width)

Apron Parking capacity for 48 planes

Cargo Terminal of 8,200 sq. m

Istanbul Sabiha Gokçen International Airport

Financing Plan (Euro mn)

Very strong annual traffic growth

FY 2012 traffic was 13.82

mn PAX (13% higher than

FY11)

Consortium Partners in ISGIA*

Concession Overview

GMR Infrastructure 40%

Limak 40%

Malaysia Airports 20%

* ISGIA: Istanbul Sabiha Gokçen International Airport Ltd

Concession Date May 2008

Concession Period 20 years (extended by additional 1 year and 300 days)

Concession fees €1.93bn over the concession period. First payment in 2011

Previous Current

PAX Capacity 5 mn 25 mn

Cargo Capacity - 145,000 tons

PTB Area (sq. m) 25,600 210,000

29

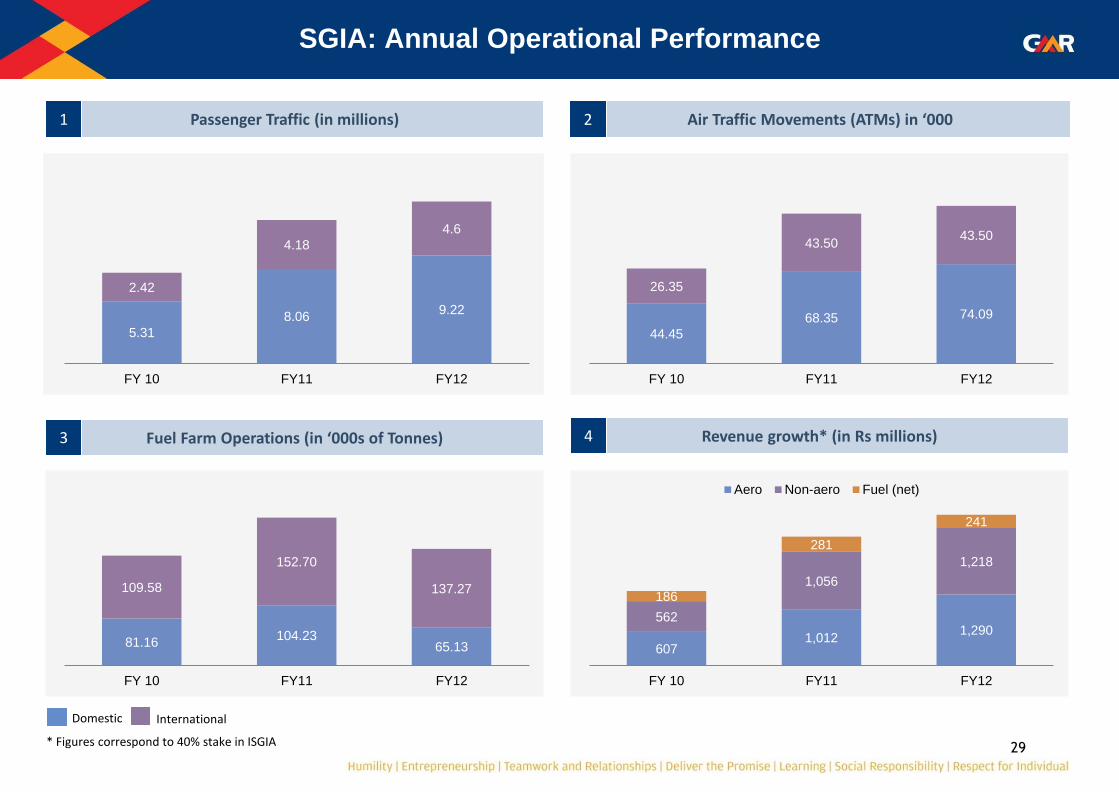

SGIA: Annual Operational Performance

Fuel Farm Operations (in ‘000s of Tonnes)

Air Traffic Movements (ATMs) in ‘000 Passenger Traffic (in millions)

3

2 1

Revenue growth* (in Rs millions) 4

607 1,012

1,290 562

1,056

1,218

186

281

241

FY 10 FY11 FY12

Aero Non-aero Fuel (net)

5.31

8.06 9.22

2.42

4.18

4.6

FY 10 FY11 FY12

44.45

68.35 74.09

26.35

43.50 43.50

FY 10 FY11 FY12

81.16 104.23

65.13

109.58

152.70

137.27

FY 10 FY11 FY12

Domestic International

* Figures correspond to 40% stake in ISGIA