Embed Size (px)

Citation preview

Head Office:

M1-M2, Mezzanine Floor ,Park Avenue, 24-A, Block 6,PECHS, Shahra-e-Faisal, KarachiTel : 021-34380451-52Fax : 021-34327087E-mail : [email protected]: www.pipfa.org.pk

Lahore Office:

42 Civic Centre, Barkat Market,New Garden Town, Lahore.Tel : 042-35838111, 35866896Fax : 042-35886948E-mail : [email protected]

Faisalabad Office:

Ajmal Centre -1, 289-1,Batala Colony, FaisalabadTel : 041-8500791, 041-8530110E-mail : [email protected]

Publication Committee:

Mr. Jawed Mansha ChairmanMr. Shahzad Ahmad Awan MemberMr. Shahzad Raza Syed MemberMr. Sarmad Ahmad Khan MemberMr. Muhammad Sharif Member

Islamabad Office:

14-K, Firdous Plaza, F-8 Markaz,IslamabadTel : 051-2851572E-mail : [email protected]

PIPFA JOURNAL

Messages:

President, PIPFA................................................................3

Chairman, Publication’s & Seminar Committee ...............3

Articles:Performance Audit; Main Tool Of Measuring

Efficeincy and Ensuring Accountability ............................4

Insurance...........................................................................9

Let’s Play Risk ...................................................................11

IAASB Proposal ................................................................14

Tip of the Quarter .............................................................16

News Updates:

IFAC News ........................................................................17

SECP News .......................................................................18

SBP News..........................................................................19

PIPFA News ....................................................................20

Entitlement to use Designatory letters APFA or FPFA and distinction of membership.

Continuing Professional Development through publications, seminars, workshops etc.

Eligibility for Chief Financial Officer or Company Secretary of listed company.

Entitlement for qualification pay etc. to PIPFA Public Sector Qualified.

Opportunities to inter-act at the national level with elite accounting community.

Exemptions in examination of ICAP, ICMAP, CIMA-UK, ACCA etc.

Professional activities like election of representatives etc.

We are aslo pursuing Higher Education Commission of Pakistan to grant PIPFAqualified / member equal to B.Com Graduate.

Dealing also with Federal Board of Revenue (FBR), Pakistan to allow PIPFA membersfor Tax Practicing.

Why PIPFA?PIPFA’s Membership entails many advantages like:

Salient features of PIPFA Qualifications:On qualifying Final Level, one may apply forthe management level jobs like FinancialAdvisor / Financial Officer.Elevation in Auditor General of Pakistan forBPS -17 is possible after qualifying PIPFA.Students may join audit firms as Audit Traineeor internship in Financial Institutes/Organizations.

VIEWS EXPRESSED HERE DO NOT NECESSARILY REPRESENT THE OFFICIAL POLICY OF THE INSTITUTE

Vol:10, Reg. No. MC-1112 July - September 2013

Celebrating20th Year

of Excellence

Compiled by: Zubair Muhammad

Mr. Jawed ManshaMember

(Nominee of ICMAP)

Pakistan Institute ofPublic Finance Accountants

E X E C U T I V E C O M M I T T E E

Mr. Muhammad Ashraf Shaikh ChairmanMr. Shahzad Ahmad Awan MemberMr. M. Sharif Tabani MemberMian Muhammad Shoaib Member

BOARD OF GOVERNORS STANDING COMMITTEES

B O A R D O F S T U D I E S

Mr. Shahzad Raza Syed ChairmanMr. Jawed Mansha MemberMr. Sajid Hussain MemberMr. M. Sharif Tabani MemberMr. Mohammad Maqbool MemberMr. Sajjad Ahmad Member

E X A M I N A T I O N C O M M I T T E E

Mr. Shahzad Ahmad Awan ChairmanMr. Jawed Mansha MemberMr. Sajid Hussain MemberMr. M. Sharif Tabani MemberMr. Muhammad Sharif MemberMr. Mohammad Maqbool MemberMr. Asif Khan Member

R E G U L A T I O N A N DD I S C I P L I N A R Y C O M M I T T E E

Mr. Mohammad Maqbool ChairmanMr. Sajid Hussain MemberMr. Shahzad Ahmad Awan MemberMr. Asif Khan Member

P U B L I C A T I O N A N D S E M I N A RC O M M I T T E E

Mr. Jawed Mansha ChairmanMr. Shahzad Ahmad Awan MemberMr. Shahzad Raza Syed MemberMr. Sarmad Ahmad Khan MemberMr. Muhammad Sharif Member

Mr. Asif KhanMember

(Nominee of AGP)

Mr. Sarmad Ahmad KhanMember

(Nominee of ICAP)

Mr. Sajid HussainMember(Elected)

Mr. Mohammad MaqboolMember

(Nominee of ICAP)

Mr. Muhammad SharifMember(Elected)

Mr. Sajjad AhmadMember

(Nominee of ICMAP)

Mr. Shahzad Raza SyedMember

(Nominee of AGP)

Mr. Muhammad Ashraf ShaikhPresident

(Nominee of AGP)

Mr. Shahzad Ahmad AwanVice President

(Nominee of ICMAP)

Mr. M. Sharif TabaniSecretary

(Nominee of ICAP)

Mian Muhammad ShoaibTreasurer / Joint Secretary

(Elected)

Celebrating20th Year

of Excellence

PIPFA JOURNALMessages

Respected Members and Dear Students,

I am honored to present 10th edition of PIPFA Journal. PIPFA has achieved a tremendousamount of success over the past years as a result of remarkable participation by its students,members, Board Members and secretarial staff. We have made significant achievementsto celebrate and we want you to be a part of it….every step of the way!

Institute’s events foster education, inspiration, networking and opportunities for learningand mentoring. Participation in PIPFA activities provides you considerable relationshipand limitless learning opportunities.

It is said that tomorrow’s challenges shape today’s education. Never has this statementbeen more relevant than now. Our commitment to preparing our members and students for these challenges is whatdrives Pakistan Institute of Public Finance Accountant’s mission. We are committed to a career-oriented, hands-on education that addresses the multifaceted changes and needs of an emerging global market.

Without question, the human mind is an incredible tool. But this tool often remains locked when we don’t followour passion. This is a challenge we all face as we decide to trust in ourselves and in our abilities. So I encourage youto take full advantage of all that PIPFA is offering and have to offer. The possibilities are exciting. Reach out andunlock your potential.

Accountants drive our global economy - creating wealth, jobs, and meaningful work for billions. Accountantsrevolutionize organizations, and also work inside corporations leveraging new opportunities and creating newsuccesses.

PIPFA has a focused and ambitious plan and an outstanding team that includes members and students from previousyears and talented new ones to achieve its goals. PIPFA looks forward to the active involvement of its members,students and volunteers to strengthen and build the Accountants’ ecosystem. Please join us.

Muhammad Ashraf Shaikh

Let me start by saying I am deeply honored and humbled to present 10th edition of PIPFAJournal. I have a profound respect and passion for this Institute and I’m incredibly motivatedto serve our Institute, our Members and our students.

Our first article provides detailed know how about Performance Audit & its tools, as you knowthat Performance auditing is an area new enough in the history of auditing. Its growth parallelsthe evolution of politics and public administration from one-dimensional focus on control ofinputs (resource) towards broader attention to accountability for outputs and outcomes.

Performance audit is considered to be one of the most effective means for improving performanceand governance. Improvement systems model allows for a wide concept of effectiveness ofauditing, the application of theory to practice which is a frequent object of scientific research,

often a topic of scientific discussions.

Audit, initially created as an accounting oriented function has been transformed into management oriented profession.Nowadays performance audit is an independent profession, which is playing a significant role in the management oforganizations and country’s policy.

Second article is about Insurance and third is about Risk Management, it is fact that Human being, his family and propertiesare always exposed to different kinds of risks. Risk involves the losses. Insurance is a tool which reduces the cost of loss oreffect of loss caused by variety of risk. It accumulates funds to meet individual losses. It is not device to prevent unwantedevent of happening or cause of loss but protects them against that loss by compensating which has lost.

I would like to express my considerable appreciation to all authors of the articles in this issue of the PIPFA Journal. It is theirgenerous contributions of time and effort that made this issue fabulous. At the same time I would like to encourage all ourreaders to consider sharing their special insights with the PIPFA fraternity by submitting an article.

Jawed Mansha

President

Chairman Publication & Seminar Committee

Celebrating20th Year

of Excellence

ARTICLES PIPFA JOURNAL

PERFORMANCE AUDIT;Main Tool Of Measuring Efficeincy AndEnsuring Accountability

By: Muhammad Saeedullah Yousafzai, FPFA

Performance Audit is assessment ofoverall performance of developmentprojects and programs; an instrumentto sharpen the process of accountability.In 1977 the Lima Conference of theInternational Organization of SupremeAudit Institutions (INTOSAI) officerecognized the importance of this typeof auditing. Many countries amendedtheir Audit Acts / Rules and scope ofaudit was expanded to efficiency orvalue of money audit (MuhammadJamil Bhatti, 2002).In traditionalauditing, only financial data is used togive an opinion on financial position ofan entity or project, while inperformance auditing non-financialdata is also taken into consideration.

That governments should applythemselves to continuously improvingtheir performance, particularly withrespect to the management of publicfunds and the stewardship ofpublic assets, appears nowto be a generallya c c e p t e dprincipleo f

good governance. Instead of focusingon transaction, it assesses the wholeproject or organization (Geoffrey B.Sprinkle, 2000). Main focus of audit inperformance audit is achievement oftarget. Even if no irregularity has beenmade, but the target is not achievedthat entity / manager is taken to task.Economy, efficiency, effectiveness andenvironmental effects are assessed andaccordingly general recommendationsare made (Rashid Ahmed Saleh, June2002). It is defined as “is an assessmentof the activities of an organization tosee if the resources are beingmanaged with due regardf o r e c o n o m y ,efficiency and

effectiveness and accountability”. Righttime to acquire a resource is also linkedto the need to be fulfilled. The resourceshould be available to satisfy the needwhen it is required. It should neithermake other resources 'wait' nor shouldwait for other resources. Therefore, theauditor reviews procedures to foreseedemand, procurement and availabilityof resources.

Right place for a resource is the onewhere it is needed. The resources maybe available where they are not needed.For example, there may be jobs which

are unmanned and theremay be men who do not

have work. Theauditor reviews the

s y s t e m f o rsignaling the

r e s o u r c eg a p s .

R i g h tCost

July - September 2013

Celebrating20th Year

of Excellence

4

ARTICLES PIPFA JOURNAL

July - September 2013

refers to lowest cost in the life-cycle ofa resource.

Main objective of performance auditare as below:

1. To inform stake holders that howtheir employees / public servantsobtained value for money spent outof firm’s account or publicexchequer and how they ensuredany recovery.

2. To improve governance andencouraging better managementpractices in the organization, basedon self-assessment.

3. Helping managers in making soundjudgments.

Performance audit can be thought of asa set of systematic efforts, initiativesand processes that have a number ofc h a r a c t e r i s t i c s . I t i d e n t i f i e sperformance in terms of results(outputs, outcomes, effects, impacts,etc.). It is assumed that levels ofintended achievement (performancetargets, service standards, etc.) aremeasurable. Traditional audit waschecking of books but in performanceaudit, audit and performance are linked(Chistopher Politt & Hilka Summa,1997).

Approach of Auditors; Inperformance audit main concern isvalue for money and hence an auditorinterviews the executive officers, visits

the field and physically verifies the facts.

Its scope is not limited to examinationof financial statements, waste,extravagance , inef f i c iency orinfectiveness, it goes beyond that andanalyses causes of non-performance aswell. Following are main features ofperformance audit;

• It is not only audit for managers butalso an aid to management.

• Constraints of management ornatural reasons are taken intoconsideration and recommendationsare made on the basis of real lifesituation.

• Findings are quantified in terms ofcash, rupee or dollar, as the casemay be.

• Policies and procedures are assessedand stress is put on objectivity, withno preconceived conclusions.

• Findings andconclusions arem a d e o nverifiable factsa n d i nc o o p e r a t i v erelationship withm a n a g e m e n t( L i a q a t A l iC h a u d h e r y ,2004).

Process of PerformanceAuditPerformance audit is carried out infollowing main stages.

1. Planning: At this stage auditorsprepares for audit, studies the entity,its mandate, organization, budget,main programs, applicable laws andregulations and basic procedures ofthe organization. Issues of potentialsignificance are identified toeconomize on cost of audit.Adequacy or inadequacy of the datalays down the audit criteria andidentifies issues of potentials i g n i f i c a n c e . S o m e t i m e s ,disagreements develop with themanagement regarding theappropriateness of the audit criteria.In such a situation the matter isresolved either by referring to ahigher authority or by allowing theauditor to go ahead independentlyor simply by abandoning theeffectiveness audit restricting itsscope to economy and efficiencyaspects only

2. Execution: The auditor examines alldocuments, visits fields, meetsmanagement employees and collectsdata. The data is analyzed in the lightof rules regulations and goals.Objective, mission statement andpurpose of the project / entity isexamined and it is assessed thatwhether the goal has been obtainedor otherwise or partially. Here comesthe idea of value for money whethervalue has been obtained or not. Cost/ value benefit analysis is carriedvarious test and formulas are used

Celebrating20th Year

of Excellence

5

ARTICLES PIPFA JOURNAL

July - September 2013

and results are obtained. At theexecution stage the auditor reviewsthe adequacy of the management'ss y s t e m o f e f f e c t i v e n e s smeasurement. If no such systemexists then the auditor develops asystem of his own.

3. Reporting: Findings are tabulated,verified through statistical formulasand report preparation is started.The text of audit report gives facts,findings and recommendations. Thefacts relate to the background,financing, executions and operationsof the program / project. Thefindings discuss the extent to whichobjectives have been achievementa n d a t w h a t c o s t , m a j o rachievements and constraints arehighlighted. Recommendations partof the report gives general directionfor actions. It qualifies expecteds a v i n g s o r o t h e r b e n e f i t s(Muhammad Akram Khan, 1988).

Tools ofPerformance AuditIt is an ongoing monitoring andr e p o r t i n g o f p r o g r a m m eaccomplishments, particularly progresstowards pre-established goals. (USGeneral Accounting Office, 1998). It isgives information on what managementdoes and reports based on whatprogrammes are achieving for citizensand at what cost. This implies agreeingon expected outcomes, measuringprogress toward them and using thatinformation to improve performanceand report results (English and

Linquist, 1998).

Performance audit is using performanceinformation effectively and assessingthe requisite or expected outcomes, inthe light of expectations (KPMG, 1998).In performance audit all those tools areused which are commonly availed bymanagement, for decisions making inorganization.These include followings:

1. Audit command language (ACL)

2. Net present value (NPV)

3. Internal rate of return (IRR)

4. Average , Ranges, Regressionanalysis

5. Benefit / Cost Ratio (B/C Ratio)

6. Sensitivity test Ranking etc.

The list is exhaustive and auditor mayuse any tool based on his expertise andnature of the project organization. Hemay also use Bar chat, column chart,line graph or pie chart to show theresults, both actual and expectedvariations may be highlighted throughstatistical tools. The audit report shouldbe based on 5 C’s i.e criteria, condition,cause, conclusion and corrective action(Liaqat Ali Chaudhery, 2004). Criterionexplains as how the auditee action hasbeen measured or what criterion hasbeen involved by the management.Condition will clearly state in thefindings as to what was the actualcondition observed by auditor and howit differed from laid down procedure.The audit findings should identifycauses for the gap between the criterionand condition. Conclusion should bebased on taking into account bothfinancial and non-financial factors. Ifcorrective action by management hasbeen taken then that may be identifiedor otherwise auditor may suggestcorrective action to rectify the situationif possible.

Most notable progress in adoption ofperformance audit is the developmentof non-•'denancial audit approaches byauditors. Non-financial performance( N P I ) i n d i c a t i o n s a r e t h o s eperformance indicators that are notpart of organizations accounting data.NPIs are needed as f inancialinformation does not and cannot coveral l aspects that inf luence an

organization’s performance (FizzaPervez Afzal, 2004). The reinforcement,by the accounting and audit community,of the need for regular, i.e. annual,accountability reporting with a focuson results achieved, related costs,performance indicators, etc., isconsistent with the performancemanagement paradigm. It has driventhe development of internal control andinternal audit functions in governmentwith an emphasis on managementcontrol frameworks, results-basedbudgeting, performance reporting, etc.(Christopher Pollitt and Hilka Summe,1997). A good indication of the extentto which performance audit, and theuse of performance indicators andperformance measures, is increasinglyrooted in the administration ofgovernments, is the evolving role of theexternal/legislative auditor (MichaelBarzelay, 1997). For example, WesternAustralia, New Zealand, Sweden, theUS, England and Wales now carry outaudits of performance indicators andissue opinions instead of stress onregulatory audit (Christopher Pollitt,January 2003).

Pitfalls in Performance Audit

Performance audit is a very goodinstrument of accountability and ishelpful in bringing transparency andefficiency, but there are still problems,of which we must take cognizance.Inadequate indicators that do notmeasure what they are intended to, i.e.what evaluators would call ‘poorconstruct validity’. This situation oftenarises when a performance assessmentprocess is implemented hurriedly,under pressure, and indicators arechosen in haste or without sufficientconsideration. This ‘classic’ pitfall isdue typically to a lack of appropriateknowledge and know-how; as well, thelink between activities and outcomes isusually taken for granted by those whocarry out the programme and is treatedas something ‘obvious’. Use ofperformance information to ends forwhich it was not intended. Anotherimportant risk is goal displacement.This phenomenon occurs whenperformance auditor creates incentivesto the detriment of the programme’s

Celebrating20th Year

of Excellence

6

ARTICLES PIPFA JOURNAL

July - September 2013

relevance; and performance indicatorstargets overtake the programme’sraison d’etre. It may fail to achieve thedesired results if insufficient attentionis given to the implementation process;the measurement approach reducesdynamic and complex mult i -dimensional programmes to simplisticformulae and/or mechanistic linearprocesses; the focus of the assessmenteffort is on cosmetics rather thanfundamentals; and, likely the surestway of producing goal displacement,there is failure to involve stakeholdersand obtain buy-in. The problemsassociated with goal displacement canbe exacerbated by what could best becalled ‘perverse incentives’. Forexample, raising the stakes associatedwith management increases thelikelihood that people will ‘work •'derstto the indicators’ and produce bywhatever means the requiredperformance information (Ian C. Davies1999). Low-probability programmetechnologies, i.e. ‘soft’ programmes suchas social interventions, are particularlyvulnerable to lack of attention to whatis really important because it is difficultto measure. What is measured, or evenmeasurable, often bears l itt leresemblance to what is relevant (Perrin,1999). Auditors are in a position to, andshould, draw more on the practice’swide span of knowledge, know-how andresources to address competently boththe methodological and political aspectsand evaluative enterprise, especially int h e c o n t e x t o f p e r f o r m a n c emanagement initiatives (Ian C. Davies,1999). Auditor should make a point oftelling people at the outset of any auditthat he conducts that he follows twosimple principles of fairness: thatmanager is accountable only for thosethings over which he has control, andhe is not expected to do the impossible.Communicating these principles servesas a constructive starting point forcollaborative enterprise (Pollitt,Christopher, et al, 1999). Discussingand agreeing to some rules of the gameis equally important, for example:making sure there is prior agreementon the interpretation of measures andthe uses of performance information;instituting a mechanism to assess the

performance management initiative orprocess itself generating the activeinvolvement and participation ofstakeholders and ensuring transparencyof process. A •'denal lesson learned isthat independent input can beextremely helpful for developing anappropriate and credible performancemanagement approach (Ian C. Davies,1999).

Auditor independence is the mostimportant quality for performanceauditors, as it will affect the results. Inperformance audit, auditors should notbe responsible to develop theorganization’s operation or correct thedefects found during the audit process.Auditors are only responsible formonitoring the feedback that should beimplemented by the organization(Arens, et al, 2005). Auditors have anauthority to implement the feedback orcorrect the defects; it will create biasand reduce auditor’s independence andthe quality of the feedback, particularlyif the auditors will perform audits againin the next period.

Sometimes performance audit maydecrease the performance of a publicorganization. This unintendedconsequence appears where theexpectation of performance is too highor too low (Theil and Leeuw, 2002).Development of the indicator is themost risky process in performanceaudit. Overvaluing or misinterpretingthe performance will bring a negativefeedback for the organization.

The shareholders in a private entityinclude those who have shares in theorganization, while the stakeholders ina public organization have a widerdefinition as voters, tax-payers, society,parliament, and other interest groups.T h i s s h o w s t h a tperformance audit hasmore challenges inpublic organizationthan in private entities(Arens, et al,2005). Inp r i v a t e s e c t o r ,accountabi l i ty i srelatively limited tothe management ororganization and tot h e c l i e n t s o r

customers. Accountability in privatesector is also relatively easy to definebecause the value of goods in privatesector is better measured. On the otherhand, in accountability in public sectoris more complex, because it involvesmultiple stakeholders (Bovens, 2005).

This shows that performance audit inpublic sector is more complex andbroader. Public sector organization alsooften deals with cross cutting issuespolicy (Geoffrey B. Sprinkle, 2000).“Performance measures can be used toevaluate, control, budget, motivate,promote, celebrate, learn, and improvethe organization’s performance” (Behn,2003). Performance audit is acomprehensive audit that audit and allaspect in organization, such aseconomy, efficiency and effectiveness(INTOSAI’s Auditing Standards, 2004).In terms of scope, performance auditmay cover all aspect in organization,but in terms of implementation,performance measurement mayadvance in action and timing. NewPublic Management (NPM) involvesthe transfer of knowledge and principalfrom private to public sector, which hasproved to be more efficient; so that acorporatized public service can also beaudited or measured with the similartool applied in the private sector(Michael Barzelay, July 1997).

Case Study:

Government of Khyber Pakhtunkhwaprovince gave autonomy to four tertiarycare hospitals of the province in 1999.These included Khyber TeachingHospital (1400 beds), Hayat AbadMedical Complex (500beds), LadyReading Hospital (1600 beds), andAyub Teaching Hospital (600 beds).With autonomy these hospitals were

Celebrating20th Year

of Excellence

7

ARTICLES PIPFA JOURNAL

July - September 2013

given one line budget and theirmanagement was run through Boardof Governor (Management Council).Basic purpose of granting autonomywas to improve patient care and bringefficiency. It was assumed that withpassage of time these hospitals wouldmake their own revenue andgovernment would stop budgetingthem.

To asses effects of theautonomy, I undertook performanceaudit of Khyber Teaching Hospital.Following indicators were used.

1. Number of outdoor/indoor patientstreated in a year.

2. Surgery carried out in one ward inone year.

3. Cost reduction of treatment forpatients.

4. Lab tests carried out in a week onyearly basis.

5. Presence / attendance of doctors,paramedics, nurses during dutyhours.

6. Bad occupancy rate of patients.

The data before autonomy and afterautonomy was taken into consideration.Data for twelve years 1998 to 2009 wastabulated and comparison was made.It was observed that with the increaseof population, number of patients hadincreased tremendously, but patientcare had declined. Before autonomyattendance of employee was very goodand it had declined by 30% with passageof time. New machinery had beenpurchased, but patients were lesssatisfied. Most of the tests which weresupposed to be carried out in HospitalLaboratory were referred to privatelaboratories. Patients, who weresupposed to be operated, waited forlonger time. Senior doctors were leastinterested in patient care and they give1-2 hours to the hospital. Number ofdoctors had increased many-folds, butfew were present during duty hours.OPD was mostly manned by traineedoctors. There was no uniformity; insome wards OPD was for 6-days a week,while others had 1 or 2 days a week.Bad occupancy rate had declined to 65%

in 2008 and 66% in 2009. In 2008there were 65565 indoor patients and430313 outdoor patients, but in 2009it was 65572 and 416029 respectively.Cost per patient in 2006 was Rs.512,Rs.545 in 2007, Rs.590 in 2008 andRs.606 in 2009. Administrativeexpenditure had increased but patientcare had declined. Budget was 95%provided by provincial government andthe hospital had failed to generate itsown resources. Its own collectionthrough various sources had increased,but due to increase in salaries it wasjust 5-6% of the total budget. Board ofGovernor (Management Council)consisted of political appointees whowere more interested in promotingwelfare of their voters, rather thanpatients care. Doctors union hadbecome stronger and management wasunable to control them, their everydemand was accepted but no actioncould be taken against them ( Yousafzai,Muhammad Saeedullah , 2010).

It was concluded that Autonomy Act ofProvincial Assembly was not fruitfuland with autonomy, service of thehospital/s had deteriorated. Noimprovement in performance had beenobserved. Due to strong lobby ofdoctors, government could not think ofabolishing autonomy. Many doctorswere scions of parliamentarians, highofficials and therefore no action couldbe taken against them, resultantlypatient care suffered. Autonomy failedto bring economy, efficiency andeffectiveness.

References

Christopher Pollitt (January 2003),Performance audit in Western Europe:trends and choices, Crit icalPerspectives on Accounting, Volume14, Issues 1-2, pp. 157-170.

Christopher Pollitt and Hilka Summe(1997), Performance Audit and PublicManagement, University of Vermont pp. 79.

Theil and Leeuw (2002), Evaluation inPublic Sector Reform: Concepts andPractice in International Perspective,Edward Elgar Publishing.

John English, Evert A. Lindquist (1998),

Performance Management: LinkingResults to Public Debate, Institute ofPublic Administration of Canada.

Fizza Pervez Afzal (July 2004),Essentials about Non-FinancialPerformance Indicators PERFORMITVOL-XXIII, No.3 pp. 85-102.

Geoffrey B. Sprinkle (July 2000), TheEffect of Incentive Contracts onLearning and Performance, THEACCOUNTING REVIEW Vol. 75, No.3 pp. 299-326.

Ian C. Davies (1999), Evaluation andP e r f o r m a n c e M a n a g e m e n t i nGovernment, Sage Publications LondonVol. 5(2) pp.150-159.

Khan, Muhammad Akram (1988).Performance auditing-the three 'E's'.Asian Journal of Government Audit.retrieved 13 July 2013, fromhttp://www.asosai.org/journal1988/performance_auditing.htm

Liaqat Ali Chaudhery (2004), AuditingMore Effectively, PERFORMIT Vol-XXIII No.3,pp. 47-71.

Michael Barzelay (July 1997), CentralAudit Institutions and PerformanceAuditing: A Comparative Analysis ofOrganizational Strategies in the OECD,Governance, Volume 10, Issue 3, pp.235-260.

Muhammad Jamil Bhatti,Hand book for performance Audit,AATI Lahore

Pollitt, Christopher,et al (1999),Per formance or Compl iance?Performance Audit and PublicM a n a g e m e n t i n F i v eCountrieshttp://ideas.repec.org/b/oxp/obooks/9780198296003.html#cites

Rashid Ahmed Saleh (June 2002,) TheImpact of Eucalyptus Plantations onthe Environment Under the SocialForestry Project Malakand, Auditreport, published by Auditor Generalof Pakistan.

Yousafzai, Muhammad Saeedullah(2010), Performance Audit Report onAutonomous Health Institutes ofKhyber Pakhtunkhwa, submitted todirector general audit KPK.

8

Celebrating20th Year

of Excellence

ARTICLES PIPFA JOURNAL

July - September 2013

From early days men needs protectionin every aspect of life. The sense ofprotection invents procedures and waysto safeguard the various interestsincluding life and households. Thissense of protection later on developedwith a broad base insurance covers forindustrial and commercial installationsand businesses dealing in millions ofDollars comprising Machinery,Materials and price less prestige livesof persons engaged in performing theirduties in commercial and Industrialoperations.

The need of protection developed anindustry called insurance, whichprovide a broad base of facilities andcovers for every aspect of industrial andcommercial concerns and also provideknowledge of different areas for whichinsurance covers may be obtained andalso the methods and procedures whichto be followed to get maximum coversat lower cost.

In the following lines we will discussthe insurance in brief.

What is Insurance?“Insurance can be defined as a contract(Policy) in which an individual or entityreceives financial protection orreimbursement against losses from aninsurance company. “

The above definition provides that anindividual or entity can make its lossesgood arising out of an accident occurredwhether naturally or otherwise if thesame is covered in insurance contract.

We can classify the major insurancepolicies as under.

General Insurance

General insurance comprises followingmain insurances.

1. Property insurance: It includesinsurance of Building plant andMachinery s tocks bus inessInterruption.

2. Motor Vehicles

3. Electronic Equipment

4. Misc. policies (Cash in safe, Cash intransit, Fidelity Guarantee etc.)

5. Erection /construction All Risk

6. Third party Liability (Property &Human life)

7. Workmen compensation

8. Personal Accident

Stocks and Business Interruptionpolicies can be based on declaratorybasis in which 75% premium is paid oninception values (sum insured) andremaining 25% premium adjustmentwill be made at the end of the year onthe average sum insured calculated onthe basis of actual declaration madeduring the year. In case of return ofpremium 1/3rd or actual refund whichever is lower will be paid.

Marine Insurance

It can be defined as the insurancecovering damages to Hull andmachinery of the vessel, cargo carriedon the vessel and also offers protectionagainst liabilities to shipping andtransport related companies but it alsocovers the transaction made by Roadand Air. Marine insurance can beclassified in two ways.

1. Marine cargo insurance that coversmovement of cargoes through AirRoad and Sea.

2. Marine hull insurance covers shipstructure, it is divided in two policies.Time policy that covers a particular

period for example one year andVoyage policy that covers place toplace for example Karachi toLondon, for a particular voyage.

Agricultural (Crop) Insurance

Pakistan s’ agricultural sectorcontributes a reasonable share incountry s’ GDP. To provide facilitiesInsurance companies took initiative tointroduce Crop Loan insurance. Theduration from crop sowing to harvestis crucial for farmers and they are underthreat of climatic changes. The schemecovers the production loans providedby the banks to the farmers and coverunavoidable losses to crops from flood,Drought, Excessive rain, Hailstorm,Frost, Disease and insect attack.Livestock covers also provided toindemnify the losses against deatharising out due to natural causes,disease, injury and accident.

Following are few insurance companies,which are providing general insuranceservices in Pakistan. However there areother Insurance companies as well.

SR. Sr.# Name of Insurance Comoany Sector

1 Adamjee Insurance Company Ltd. Private

2 Askari General Insurance Company Ltd. Private

3 Central Insurance Company Ltd. Private

4 Century Insurance Company Ltd. Private

5 EFU General Insurance Ltd. PrivateJubilee General Insurance Company Ltd. Private

6 Muslim Insurance Company Ltd. Private

7 National Insurance Company Ltd. Public

9 PICIC insurance Ltd. Private

INSURANCEA Brief Knowledge

By: Syed Yamin Mustafa, APFA

Celebrating20th Year

of Excellence

9

ARTICLES PIPFA JOURNAL

July - September 2013

Health Insurance

It is natural that individuals intent tolive long and enjoy the colors of lifeprovided by Almighty Allah and theyare naturally cautious about theirhealth. Insurance companies capitalizedthis desire and provide health relatedinsurance covers.

It covers Health related risks ofindividual such as hospitalization (Inpatient), Maternity benefit cover, outpatient cover, terrorist cover forinnocent person (Injury due to act ofterrorism) it also provides internationalcover to provide medical facilitiesduring staying at abroad. Some of thecovers are optional. All covers aresubject to certain exclusions (Risk &treatment not covered) and terms andconditions.

Life InsuranceInsurance companies also planned tosecure lives of persons to providefinancial benefits to the individuals andtheir heirs in case of death or bodyinjuries through different covers orpolicies. We will discuss followingcovers in brief.

1. Life

2. Accidental death benefits (ADB)

3. Natural Disabilities (PTD Natural)

4. Accidental Disabi l i ty (PTDAccidental)

5. Loan coverages.

In the case of death financialcompensation equal to sum insured isto be paid. In case of Accidental deathif ADB cover is included in the policyfinancial compensation equal to doubleof sum insured is to be paid. In casesof disability the financial compensation

will be paid according to the ratsspecified in the schedules provided inthe policy.

The following major insurancecompanies provide life insurance inPakistan.

Sr.# Name Of Insurance Company Sector

1 Adamjee Life Insurance Company Ltd. Private

2 American Life Insurance Company (Pak) Ltd. Private

3 EFU Life Assurance Ltd. Private

4 Jubilee Life Insurance Company Ltd. Private

5 State Life insurance Corporation Public

TakafulIn recent years Islamic concept ofinsurance has been introduced underthe name of Takaful. This is an attemptto perform insurance operations, whichare monitored and approved by IslamicLaws. We can define the Takaful asunder.

“Takaful is an Islamic insurance conceptwhich is grounded in Islamic muamalat(banking transactions), observing therules and regulations of Islamic law.Takaful is basically a system of Islamicinsurance based on the principle ofmutual assistance and voluntarycontribution, where the group sharesthe risk collectively. It is operated onthe basis of shared responsibility,brotherhood, solidarity and mutualcooperation or assistance, whichprovides for mutual financial securityand assistance to safeguard participantsagainst a defined risk.”

The word Takaful is derived from theArabic verb Kafala, which means toguarantee; to help; to take care of one’sneeds. This concept has been practisedin various forms for over 1400 years.Muslim jurists acknowledge that thebasis of shared responsibility waspractised between Muslims of Meccaand Medina laid the foundation ofmutual insurance. It is based on theconcept of social solidarity, cooperationand mutual indemnification of lossesof members. It is a pact among a groupof persons who agree to jointlyindemnify the loss or damage that mayinflict upon any of them, out of the fundthey donate collectively.

The following insurance companies areperforming Takaful operations inPakistan.

Sr. # Name Of Insurance Company Sector

1 Dawood Family Takaful Private

2 Pak Kuwait Takaful Company Ltd. Private

3 Pak Qatar General Takaful Ltd. Private

4 Pak Qatar Family Takaful Private

5 Takaful Pakistan Ltd. Private

We have tried to provide basic or initialknowledge about insurance to ourreaders in order to create a overviewregarding insurance and someinsurance companies operated inPakistan and we hope that this initialknowledge will helps to understandinsurance.

I am thankful to EFU General InsuranceLtd, Adamjee Insurance CompanyLimited, State Life InsuranceCorporation and SECP Takaful Guidefor updating my knowledge on thesubject.

Celebrating20th Year

of Excellence

10

ARTICLES PIPFA JOURNAL

July - September 2013

Objective:

The objective of this article is to understand the phenomenon of Risk & its impact inother words “Dealing with Risk” in order to get reasonable assurance to achieve thedesired Vision Mission Strategic Objectives and Goals of an organization.

Background:Risk is used to describe as final outcome may differ from what was expected at the time when the decision was taken,risk and uncertainty plays vital role must be taken into account in strategic planning sometimes these both are to beused interchangeably but there is difference between these too, risk can be quantified based on probabilities anduncertainty can not. Every industry/sector is subject to risk varies from industry to industry being inherent factor “Riskcan never be eliminated but can also be minimized”. An organization might be facing of different risks but most importantneed to carefully deal with are Strategic and Operational risk, might result in serious threat/impact to an organizationas a whole. Strategic risk arises due to strategic decisions taken in light of external environment by directors for persuadingto goals and objectives. Strategic example is in early 1980s IBM reported the largest corporate loss; IBM did not predictthe revolutionary effect that PCs would have on manufacturing and consumers. IBM changed from being predominantly

a hardware manufacturer to consultancy services, and sold its laptop business to Lenovo a china based company.Operational risk arises due to day to day operations in light of internal environment, operational risk example is “Banksurged to adopt strong risk management culture”, There is a pressing need for banks to modify their fragmented approach

LET’S PLAY RISK....By: Bunti Lal , APFA

Celebrating20th Year

of Excellence

11

ARTICLES PIPFA JOURNAL

July - September 2013

of operational risk management infavour of a much more comprehensivegovernance and risk managementframework through clearly defined rolesand responsibilities along withreporting procedures, The State Bankof Pakistan (SBP) Governor dwelt atlength on three main areas, includingoperational risk management - theissues and challenges; treatment ofoperational risk and emergence ofsound principles risk management andregulatory deve lopments andsupervisory expectations to strengthenthe operational risk management withinthe banking sector.

Risk ManagementRISK AVERSION:

Risk aversion depends upon themanagement psychology and behavior,for example management might chooseto invest into a bank account with a lowbut guaranteed interest rate rather thaninto a stock that may have high expectedreturns which also involves a chance oflosing value. However managementmay have different types of attitudestowards risks as follows:

a) A risk seeker is a decision who isinterested in the best outcomeirrespective of small chance ofoccurrence. The perception alwaysalien with the philosophy of highrisk-high return and reward.

b) A risk neutral is a decision makerwho is interested in most likelyoutcome having the greater chanceof occurrence.

c) A risk averse is a decision maker whoalready assumes the worst possibleoutcome even if there is remotechance of occurrence.

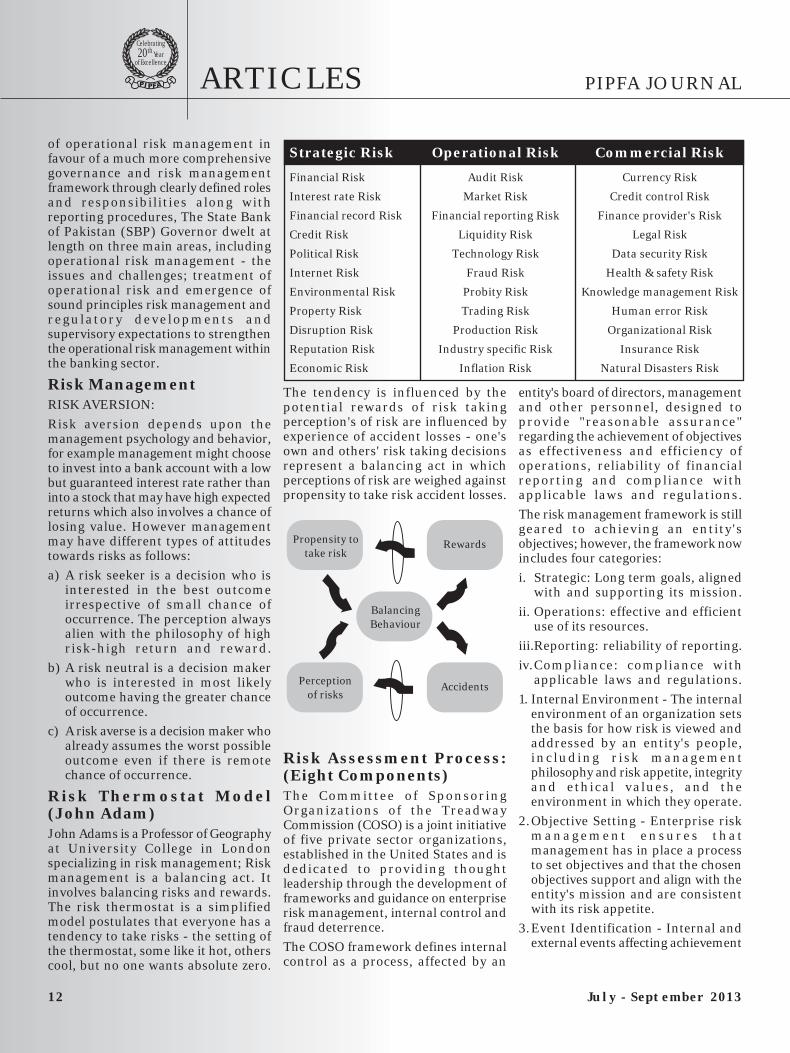

Risk Thermostat Model(John Adam)John Adams is a Professor of Geographyat University College in Londonspecializing in risk management; Riskmanagement is a balancing act. Itinvolves balancing risks and rewards.The risk thermostat is a simplifiedmodel postulates that everyone has atendency to take risks - the setting ofthe thermostat, some like it hot, otherscool, but no one wants absolute zero.

The tendency is influenced by thepotential rewards of risk takingperception's of risk are influenced byexperience of accident losses - one'sown and others' risk taking decisionsrepresent a balancing act in whichperceptions of risk are weighed againstpropensity to take risk accident losses.

Risk Assessment Process:(Eight Components)The Committee of SponsoringOrganizations of the TreadwayCommission (COSO) is a joint initiativeof five private sector organizations,established in the United States and isdedicated to providing thoughtleadership through the development offrameworks and guidance on enterpriserisk management, internal control andfraud deterrence.

The COSO framework defines internalcontrol as a process, affected by an

entity's board of directors, managementand other personnel, designed toprovide "reasonable assurance"regarding the achievement of objectivesas effectiveness and efficiency ofoperations, reliability of financialreporting and compliance withapplicable laws and regulations.

The risk management framework is stillgeared to achieving an entity'sobjectives; however, the framework nowincludes four categories:

i. Strategic: Long term goals, alignedwith and supporting its mission.

ii. Operations: effective and efficientuse of its resources.

iii.Reporting: reliability of reporting.

iv.Compliance: compliance withapplicable laws and regulations.

1. Internal Environment - The internalenvironment of an organization setsthe basis for how risk is viewed andaddressed by an entity's people,inc luding r i sk managementphilosophy and risk appetite, integrityand ethical values, and theenvironment in which they operate.

2.Objective Setting - Enterprise riskm a n a g e m e n t e n s u r e s t h a tmanagement has in place a processto set objectives and that the chosenobjectives support and align with theentity's mission and are consistentwith its risk appetite.

3.Event Identification - Internal andexternal events affecting achievement

Strategic Risk Operational Risk Commercial Risk

Financial Risk Audit Risk Currency Risk

Interest rate Risk Market Risk Credit control Risk

Financial record Risk Financial reporting Risk Finance provider's Risk

Credit Risk Liquidity Risk Legal Risk

Political Risk Technology Risk Data security Risk

Internet Risk Fraud Risk Health & safety Risk

Environmental Risk Probity Risk Knowledge management Risk

Property Risk Trading Risk Human error Risk

Disruption Risk Production Risk Organizational Risk

Reputation Risk Industry specific Risk Insurance Risk

Economic Risk Inflation Risk Natural Disasters Risk

Propensity totake risk

BalancingBehaviour

Rewards

AccidentsPerceptionof risks

Celebrating20th Year

of Excellence

12

ARTICLES PIPFA JOURNAL

July - September 2013

of an entity's objectives must beidentified, distinguishing betweenr i s k s a n d o p p o r t u n i t i e s .Opportunities are channeled back tomanagement's strategy or objective-setting processes.

4.Risk Assessment - Risks areanalyzed, considering likelihood andimpact, as a basis for determininghow they should be managed. Risksare assessed on an inherent and aresidual basis.

5.Risk Response - Management selectsrisk responses - avoiding, accepting,reducing, or sharing risk - developinga set of actions to align risks withthe entity's risk tolerances and riskappetite.

6.Control Activities - Internal Controls,Policies and procedures areestablished and implemented to helpensure the risk responses areeffectively carried out.

7. Information and Communication -Relevant information is identified,captured, and communicated in aform and timeframe that enablep e o p l e t o c a r r y o u t t h e i rr e s p o n s i b i l i t i e s . E f f e c t i v ecommunication also occurs in abroader sense, flowing down, across,and up the entity.

8 Monitoring - The entirety ofenterprise risk management ismonitored and modifications made asnecessary. Monitoring is accomplishedthrough ongoing managementactivities, separate evaluations, or both.

Risk assessment involves identifying,analyzing, profiling, quantifying andconsolidating risk, risk appetite refersto strength and level of risk anorganization can bear varies fromorganization to organization. The Ernst& Young report managing risk acrossenterprise emphasis that r iskassessment should into a consistent,embedded activity rather than becarried out as a significant stand aloneprocess. In 2005 British Petroleum(BP) launched a code of conductregarding what BP has expectationsand wants to ensure that all employeeswill comply with legal requirements,company standards, safety, workplace

behaviour, bribery, corruption andfinancial integrity.

There is a saying by John Paul Jones“It seems to be law of nature, inflexibleand inexorable, that those who will notrisk cannot win”. By virtue of naturerisk can be controllable and beyondthe control of an organization( U n c o n t r o l l a b l e ) e x a m p l e o funcontrollable risk is the plandeveloped by the National DisasterManagement Authority (NDMA) incol laborat ion with the JapanInternational Co-operation Agency(JICA), NDMA commission hasapproved a “Disaster Risk ReductionPolicy” to create capacity for earlywarning system and for identifying andmonitoring vulnerability and hazardtrend.

“To know about all possiblerisks and understanding

potential impact is an art”

C o n t r o l L i m i t a t i o n s :Internal control, no matter how welldesigned and operated, can provideonly reasonable assurance tomanagement and the board ofdirectors regarding achievement of anentity's objectives. The likelihood ofachievement is affected by limitationsinherent in all internal control systems.These include the realities that humanjudgment in decision-making can befaulty, and that breakdowns can occurbecause of such human failures assimple error or mistake. Additionally,controls can be circumvented by thecollusion of two or more people, andmanagement has the ability to overridethe internal control system. Anotherlimiting factor is the need to considercontrols' relative costs and benefits.

RISK MITIGATING STRATEGIES:

Once risks have been identified andassessed, all techniques to manage therisk fall into one or more of these fourmajor categories. First Avoidance(eliminate, withdraw from or notbecome involved), second Reduction(optimize - mitigate), third Sharing(transfer - outsource or insure) andfinally Retention (accept and budget).Ideal use of these strategies may not

be possible. Some of them may involvetrade-offs that are not acceptable tothe organization or person making therisk management decisions.

Responsibility….?The Executive Management, Riskmanagement committee, Internalauditor, External auditor, Managersand staff but it won't be wrong to saythat everyone working in theorganization is responsible, HoweverBoard has the overall responsibilityof risk management as being part oft h e C o r p o r a t e G o v e r n a n c eresponsibilities.

“ Y o u c a n m e a s u r eopportunity with the sameyardstick that measure therisk involved. They go togather”Effective communication also mustoccur in a broader sense, flowing down,across and up the organization. Allpersonnel must receive a clear messagefrom top management that controlresponsibilities must be takenseriously. They must understand theirown role in the internal control system,as well as how individual activitiesrelate to the work of others. They musthave a means of communicatingsignificant information upstream.There also needs to be effectivecommunication with external parties,such as customers, suppliers,regulators and shareholders. This isaccomplished through ongoingmonitoring activities, separateevaluations or a combination of thetwo. Ongoing monitoring occurs in thecourse of operations. It includesregular management and supervisoryactivities, and other actions personneltake in performing their duties. Thescope and frequency of separateevaluations will depend primarily onan assessment of risks and theeffectiveness of ongoing monitoringp r o c e d u r e s . I n t e r n a l c o n t r o ldeficiencies should be reportedupstream, with serious mattersreported to top management and theboard.

Celebrating20th Year

of Excellence

13

ARTICLES PIPFA JOURNAL

July - September 2013

IntroductionThe International Auditing andAssurance Standards Board (IAASB)has released proposals that couldfundamentally transform the auditor'sreport , great ly enhancing i tscommunicative value. The ExposureDraft (ED) proposes a new standard,International Standard on Auditing(ISA) 701, Communicating Key AuditMatters in the Independent Auditor'sReport, and a number of revisions toexisting standards, including ISA 700,Forming an Opinion and Reportingon Financial Statements (see IAASBpress release). While the proposalsstand to significantly change the shapeof auditor reporting for listed entities,the impact on unlisted entities is likelyto be much smaller. Nevertheless,there are proposed requirements thatapply to all audits. These are intendedto help demonstrate the value of theaudit and, furthermore, may improveservice and promote engagementefficiency.

This article summarizes this impact andsuggests how small- and medium-sizedpractices (SMPs) and small- andmedium-sized entities (SMEs) can getinvolved to help ensure the best possibleoutcome.

ProposalsThe proposed new and revisedstandards deal mainly with reportingconsiderations, which typically involvedecisions by the auditor toward the endof the audit process. There are, however,aspects that may have implications forwhat the auditor does at or near thebeginning of the audit, such as agreeingthe terms of and planning theengagement, as well as communicatingwith those charged with governance.The most significant implications forthe audits of unlisted entities aredescribed below.

Content of the Auditor'sReportThe centerpiece of the proposals isproposed ISA 701. This completely newstandard establishes requirements andg u i d a n c e f o r t h e a u d i t o r ' sdetermination and communication ofkey audit matters in the auditor's report.Key audit matters, which are selectedfrom matters communicated with thosecharged with governance, are requiredto be communicated in the auditor'sreport for listed entities. Auditors offinancial statements of unlisted entitiesmay also be required, or may decide, tocommunicate key audit matters in theauditor's report.

For example, law, regulation, ornational auditing standards may requireauditors of unlisted entities in aparticular jurisdiction to communicatekey audit matters. Moreover, theauditors of other unlisted entities maywish to use the new mechanism of keyaudit matters on a voluntary basis.Where key audit matters arecommunicated for audits of financialstatements of unlisted entities (eithervoluntarily or when required by law orregulation) then such matters shouldbe determined and communicated inthe same manner as for listed entities(see paragraph 4 of proposed ISA 701and paragraphs 30 and A30-A31 ofproposed ISA 700 [Revised]).

ISA 700 has been revised to establishnew required reporting elements,including a requirement for the auditorto include an explicit statement ofauditor independence and disclose thes o u r c e ( s ) o f r e l e v a n t e t h i c srequirements, for all audits includingthose of unlisted entities. Similarly, ISA570, Going Concern, has been amendedto establish auditor reportingrequirements applicable to all audits.The IAASB believes it is in the publicinterest for this to have universal

application.

Agreeing the terms of theEngagementIn light of the possibility of auditors ofunlisted entities communicating keyaudit matters in the auditor's report, orbeing requested by management orthose charged with governance to doso, the IAASB has proposed limitedamendments to other ISAs, includingISA 210, Agreeing the Terms of AuditEngagements. Specifically, if the auditoris not required to communicate keyaudit matters but intends to do so, anew requirement has been establishedfor the auditor to include a statementin the audit engagement letter regardingsuch intent. This will provide anadditional opportunity for the auditorto communicate with management andthose charged with governance toensure there's a clear understanding asto the nature of the key audit mattersto be disclosed.

Communicating with thoseCharged with GovernanceIn light of proposed ISA 701,amendments are proposed to therequired auditor communications withthose charged with governance for allaudits. The most significant proposedchange to ISA 260 relates to the existingrequirement for the auditor tocommunicate an overview of theplanned scope and timing of the auditwith those charged with governance.Proposed ISA 260 (Revised) ,Communication with Those Chargedwith Governance, expands thisrequirement to include communicatingabout the significant risks identified bythe auditor (see paragraph 15 ofproposed ISA 260 [Revised]).

Communication with those chargedwith governance about significant risksis likely already occurring in manyaudits, including those of SMEs, as ISAs

IAASB ProposalsFor Enhancing The Auditor's Report:Potential Impact on Audits of Unlisted Entities

By Brian Bluhm,Deputy Chair, & Phil CowoperthwaiteMember, IFAC SMP Committee

Celebrating20th Year

of Excellence

14

ARTICLES PIPFA JOURNAL

July - September 2013,

demand a risk-based approach to theaudit. But the IAASB believes auditquality could benefit from explicitlyrequiring such communication in everyaudit. The proposed requirement wouldprovide those charged with governancewith insight into those areas for whichthe auditor determined special auditconsideration was necessary and, in sodoing, help those charged withgovernance to fulfill their responsibilityto oversee the financial reportingprocess. This will also provide theauditor with an opportunity to garneradditional insights into significant risksfrom those charged with governanceand, thereby, help ensure the auditprogram is appropriately focused.

The IAASB believes it is in the publicinterest to establish this requirementfor audits of financial statements of allentities, not only for listed entities.Communicating with those chargedwith governance about significant risksis not expected to result in a significantburden on auditors who are notrequired to communicate key auditmatters in the auditor's report (e.g.,auditors of unlisted entities), asproposed ISA 260 (Revised) remainsflexible for such communication to be

made orally. In addition, the IAASBproposes requiring the auditor toc o m m u n i c a t e , a s p a r t o fcommunicating the significant findingsfrom the audit, circumstances thatrequire significant modification of theauditor's planned approach to the audit,to align with the factors the auditorconsiders in determining key auditmatters (see paragraph 16(c) ofproposed ISA 260 [Revised]). This willprovide further opportunity for dialoguewith those charged with governance tohelp ensure all responsible parties havea full understanding of areas ofs igni f icant auditor at tent ion.

FeedbackThe IAASB believes that the proposedISAs can be implemented in a mannerproportionate to the size and complexityof an entity and welcomes the views ofboth preparers and auditors of financialstatements of unlisted entities, includingSMEs, in this regard. The IAASB alsoinvites respondents to comment on areaswhere additional guidance may behelpful to illustrate how the proposedISAs can be implemented in aproportionate manner. The IFAC SMPCommittee has been providing regular

and robust input to the IAASBthroughout the ED's development,starting with a response letter to theInvitation to Comment. Please tell us (inthe IFAC SMP Community on LinkedIn)and the IAASB (click on SubmitComment) what you think about the EDand consider field testing ISA 701 onunlisted entities.

ResourcesFor a summary of the proposals, seethe At a Glance.

For a detailed explanation of theproposals, see the ExplanatoryMemorandum.

For the proposed new and revised ISAs,see the ED.

For related resources for SMPs fromIFAC, its members, and others, seeImplementation in the SMP area of theIFAC website (www.ifac.org/SMP) orthe SMP Committee's Delicious page.

Copyright © August 2013 by theInternational Federation of Accountants(IFAC). All rights reserved. Used withpermiss ion of IFAC. [email protected] for permissionto reproduce, store, or transmit thisdocument.

Without education it is complete darkness and witheducation it is light. Education is a matter of life anddeath to our nation. The world is moving so fast that ifyou do not educate yourselves you will be not onlycompletely left behind, but will be finished up. The HolyProphet (PBUH) had enjoined his followers to go even toChina in the pursuit of knowledge. If that was thecommandment in those days when communications weredifficult, then, truly, Muslims as the true followers of theglorious heritage of Islam, should surely utilize all availableopportunities. No sacrifice of time or personal comfortshould be regarded too great for the advancement of thecause of education.Quaid-e-Azam Muhammad Ali Jinnah

I have learned silence from the talkative, toleration fromthe intolerant, and kindness from the unkind; yet, strange,I am ungrateful to those teachers.Khalil Gibran

I don't measure a man's success by how high he climbs

but how high he bounces when he hits bottom.George S. Patton

Optimism is the faith that leads to achievement. Nothingcan be done without hope and confidence.Helen Keller

Success is not final, failure is not fatal: it is the courageto continue that counts.Winston Churchill

Take up one idea. Make that one idea your life - think ofit, dream of it, live on that idea. Let the brain, muscles,nerves, every part of your body, be full of that idea, andjust leave every other idea alone. This is the way to success.Swami Vivekananda

“Don't worry about failures, worry about the chances youmiss when you don't even try.”Jack Canfield

“The best revenge is massive success.” - Frank Sinatra

Quotes

Celebrating20th Year

of Excellence

15

Tip of the Quarter PIPFA JOURNAL

July - September 2013

W e c a n n o t t o u c h a n d f e e l“leadership,” though we can see andoften hear the results of it when it iseffective or ineffective, of goodcharacter or poor ethics. There areliterally hundreds of leadershipprograms available for executives,mid-level managers and new leaders.Many of these address developingthe abilities of leaders in the areas ofstrategic and critical thinking,enhancing relationships, negotiating,managing risks, people, change,conflicts and financials, making theright decisions, managing work-lifebalance -- all of which are no lessdifficult to transact than the technicalskills required in any strategicleadership function.

But beyond fundamental academic ortechnical skills, people need to learnhow to identify their strengths andcombine those with their passions inways that empower them to establishand achieve a vision for their lives.They need to learn how to managetheir time and to set, pursue andsystematically reassess their progresstoward achieving goals that empowerthem to realize their potential.Equipping people with the tools theyneed to seize control of their futuresis a powerful step toward securing astrong future for these individuals,and also our nations as a whole. Thebest solution to our countries’problems lies in helping people,especially our future leaders, to learnto live reflective, purposeful lives.

Helping our leaders to learn andunderstand who they are is important.Through their triumphs and trials,they will have the processes and toolsto know how to draw from innerstrength and act with discipline. Thisunderstanding will help them copewith the pressures of addressing thei s s u e s a n d o p p o r t u n i t i e s o fglobalization and consolidation, thechanging go-to-market strategies, theexplosion of available information ormore sophisticated, knowledgeableclients and customers. And, for those

just trying to survive each day, theymust have th is s trength andunderstanding to develop the meansto access fundamental necessities ofliving, and to persevere beyond theircircumstances.

The earlier we initiate this process ofself-discovery, the better. Our newhires often become the leaders ofc o r p o r a t i o n s , o r g a n i z a t i o n s ,communities and government. Inserving as executives and managers,these leaders are expected to serve ascommunity influencers and corporaterepresentatives who heed the needs ofthose experiencing poverty, healthcrises or lack of education, all the whilea s s e s s i n g a n y p o l i t i c a l a n dgovernmenta l d iscr iminat ion ,criminality or other implications.Giving them self-knowledge and avision at the outset of their careersgives them the freedom to choose thedirection they desire and theenvironments in which they want towork and live. It helps them fromstumbling into the quicksand of life’sdisappointments.

To be successful, people must have avision of what success looks like forthem. With a well-understood, deepmotivation for their personal andprofessional pursuits, their prioritieswill come into focus. They will not bethinking about procrastinating, takinga detour from their calling, orsabotaging their success. When peopleare truly focused and engaged, theybecome the masters of their destinies.They are truly free.

Gaining self-awareness—and then doingsomething about it—is not a taskeveryone is willing to take on. Manypeople are content with things the waythey are. People may desire greatersuccess, but they don’t want to exertthe effort to improve themselves. Onepossible reason for this is they don’teven realize they have the power to dosomething about it if they wanted to. Ifyou’re not aware there’s a problem, oryou don’t think you have the ability tochange your circumstances, you will

stay where you are. The good news isthat by the act of looking inward to seekour true selves, we are takingresponsibility and moving toward self-actualization. You can only start tomaximize your potential once you knowexactly who you are, and what isimportant to you.

L e a d e r s h i p a b i l i t i e s a n dcharacter is t ics must be wel l -developed in order to lead effectively.Yet, there is a fundamental dimensionmissing from this equation. Itencompasses leaders discovering thecore of who they are -- and who theycan become. There is a constant inleadership. It is the freedom of theindividual to know precisely who heis and what drives him, and on thisplatform become clear on how hemust lead, exercise his abilities,display his character, make his choicesa n d s e r v e h i s c o n s t i t u e n t s .Exceptional leaders are able to adaptto new tasks, to new roles, to newenvironments, and still be productive.T h e y r e a l i z e t h a t w i t h t h emanagement and growth of their“internal strength,” they can and mustpositively respond to the externalenvironment, which is often outsideof individual control.

A leader’s depth of internal knowledgeand strength stands the test of time,congruently, consistently, and nom a t t e r t h e n a t u r e o f t h ecircumstances. This leadershipfoundation can be one of the mostelusive to discover, unless the processand tools for doing so are madeaccessible. Once accessed, the ensuingdiscoveries are keys to opening doorsfor developing new abilities andcharacteristics, as well as creating orrecognizing new opportunities.

Leadership is everything, whether youare leading a life, a community, anorganization or a business, or you arein school. If you want ownership ofyour life, business and its privilegest h e n p r o g r e s s a n dtransformation should begin with you.

Source: www.success.com

Career Success Begins with LeadershipLeadership begins with self-discovery

Celebrating20th Year

of Excellence

16

News PIPFA JOURNAL

July - September 2013

IFAC NewsI A A S B P r o p o s e sStandards to FundamentallyTransform the Auditor'sR e p o r t ; F o c u s e s o nCommunicative Valueto UsersThe International Auditing andAssurance Standards Board (IAASB)released proposals to enhance the futureauditor's report. The IAASB's ExposureDraft, Reporting on Audited FinancialStatements: Proposed New and RevisedInternational Standards on Auditing(ISAs), responds to calls from investors,analysts, and other users of auditedfinancial statements in the wake of theglobal financial crisis for the auditor toprovide more relevant information inthe auditor's report based on the auditthat was performed.

“We expect the proposed new andrevised standards will result insubstantive changes to how auditorsc o n t e m p l a t e a n d a p p r o a c hcommunication to users of their reports-the beneficiaries of a financial statementaudit,” explained Prof. Arnold Schilder,IAASB Chairman. “These changes arecritical to the perceived value of thefinancial statement audit and thus to thecontinued relevance of the auditingprofession.”

The IAASB's deliberations on theproposed new and revised ISAs wereinformed by international research, twopublic consultations, stakeholderoutreach including three publicroundtables held in 2012, and the 165responses to the June 2012 Invitationto Comment: Improving the Auditor'sReport. “The signals from these inputswere clear: Change is essential. There issupport for the IAASB's direction, andfor a global solution. Challenges exist,but they can be overcome,” added Prof.Schilder.

The Exposure Draft includes a newproposed ISA titled Communicating KeyAudit Matters in the IndependentAuditor's Report. This proposed ISAdirects auditors of financial statementsof listed entities to communicate in their

report those matters that, in the auditor'sprofessional judgment, were of mostsignificance in the audit of the financialstatements. “The intended outcome ofthis proposal is more informative auditreports, with information about the auditof the financial statements that is uniqueand more specific to the entity that hasbeen audited,” noted James Gunn,IAASB Technical Director.

Among other enhancements, the IAASBis also proposing requirements forauditors to include specific statementsabout going concern in their reports, tomake an explicit statement about theauditor's independence from the auditedentity and, for listed entities, to disclosethe name of the engagement partner inthe auditor's report. The Exposure Draftincludes example reports that illustratethe application of the proposed new andrevised ISAs in various circumstances.

How to Comment

The IAASB invites all stakeholders torespond to this Exposure Draft, whichincludes specific questions forrespondents on key aspects of theproposals and highlights areas of focusfor various stakeholders in respondingto the Exposure Draft. To access theExposure Draft and submit a comment,v i s i t t h e I A A S B ' s w e b s i t eatwww.iaasb.org. Comments on theExposure Draft are requested byNovember 22, 2013.

IESBA Clarifies Definition of"Those Charged WithGovernance"The International Ethics StandardsBoard for Accountants (IESBA, theEthics Board) released final changes tothe definition of “those charged withgovernance” in its Code of Ethics forProfessional Accountants (the Code).

The changes are intended to more closelyalign the definition of “those chargedwith governance” in the Code with thatin the International Auditing andAssurance Standards Board (IAASB)'sInternational Standard on Auditing(ISA) 260, Communication with ThoseCharged with Governance, therebyeliminating any potential confusion. The

Ethics Board does not expect anychanges will be necessary to accountingfirms' systems and methodologies orcommon practice.

The changes clarify that a subgroup ofthose charged with governance of anentity, such as an audit committee, mayassist the governing body in meeting itsresponsibilities. In those cases, if aprofessional accountant or firmcommunicates with such a subgroup,the Code requires the professionalaccountant or firm to determine whethercommunication with all of those chargedwith governance is also necessary so thatthey are adequately informed.

“The changes to the definition reflect theEthics Board's ongoing commitment toeliminate unnecessary differences withthe IAASB's standards, which serves toenhance our shared stakeholders'understanding of our standards andguidance,” said Jörgen Holmquist, chairof the IESBA. “Furthermore, byclarifying the definition, the Ethics Boardaims to promote more consistentapplication of the Code, which is criticalto its mission to ultimately foster aconsistent and high level of ethicalbehavior by professional accountantsaround the world.”

As with all revisions to the Code, thechanges have been approved followingconfirmation by the Public InterestOversight Board that due process indeveloping the changes was followed.The changes, effective on July 1, 2014,will be printed in the 2014 Handbook ofthe Code of Ethics for ProfessionalAccountants. The 2013 Handbook iscurrently available to download orpurchase.

IPSASB Publishes FirstRecommended PracticeGuideline on the Long-TermSustainability of PublicFinancesThe International Public SectorAccounting Standards Board (IPSASB)has issued Recommended PracticeGuideline 1 (RPG 1), Reporting on theLong-Term Sustainability of an Entity'sFinances. RPG 1 provide guidance on

Celebrating20th Year

of Excellence

17

News PIPFA JOURNAL

July - September 2013

reporting on the long-term sustainabilityof a public sector entity's finances overa specified time horizon in accordancewith stated assumptions on policy anddemographic and economic variables.RPGs are a new type of publication thatprovides guidance on the broader aspectsof financial reporting that are outsidethe financial statements.

The sovereign debt crisis brought intosharp focus the importance of the fiscalcondition of governments and otherpublic sector entities to the globaleconomy. Concerns persist about theability of governments to meet debtservicing obligations. The extent to whichgovernments can maintain their currentlevels and quality of service delivery andmeet social benefit program obligations-without raising taxes and contributionsor increasing debt to unsustainablelevels-is a major economic and socialissue.

Although such concerns have generallyexisted in nations with well-establishedsocial programs, there is a growingrealization that they also extend to fast-developing nations that have recentlyestablished such programs.

Policies and decisions current as of thereporting date have a long-term impacton future inflows and outflows ofresources. Information on theconsequences of such policies anddecisions supplements information onliabilities, expenses, assets, and revenuein the financial statements. Flows thatare captured by long-term fiscalsustainability reporting include:

• F u t u r e t a x r e c e i p t s a n dintergovernmental transfers that donot meet the definition of an asset

• Obligations relating to social benefitsprograms that do not meet thedefinition of a liability

“RPG 1 provides straightforwardguidance on presenting informationabout the capacity of an entity to providesocial benefits at existing levels, tomaintain existing taxation revenues andto meet its financial commitments,” saidIPSASB Chair Andreas Bergmann. “Bydeveloping guidance on reportinginformation about the long-termsustainability of an entity's finances,

RPG 1 reflects the IPSASB ConceptualFramework's position that, in order tomeet users' needs, the scope of financialreporting is more comprehensive thanthe financial statements.”

The development and finalization of theRPG benefited greatly from the oversightof a task force with a wide membership,including representatives of (a) standardsetters with involvement in developingguidance for reporting on fiscalcondition, (b) governments that havemany years' experience reporting onlong-term fiscal sustainability, and (c)supranational organizations such as theInternational Monetary Fund, theOrganisation for Economic Co-operationand Development, and Eurostat, thestatistical agency of the European Union.

SECP NEWSSECP to amend Single-Member Companies RulesIn order to facilitate the corporate sector,especially entrepreneurs, the Securitiesand Exchange Commission of Pakistan(SECP) has proposed amendments tothe 2003 Single-Member Companies(SMCs) Rules.

At the moment, 1,672 single-membercompanies are registered with the SECP,which represent a mere 2.6% of the totalcorporate portfolio. The concept of SMCwas introduced in 2003 to encouragetransformation of sole proprietorshipsinto corporate entities. An SMC can beformed with just one-member comparedwith the requirement to have at leasttwo members for a private limitedcompany and a minimum of threemembers in case of a public limitedcompany.

In view of relatively slow growth ofSMCs, the SMCs Rules have beenreviewed and certain amendments havebeen proposed to further simplify therequirements especially relating to thenominee and alternate nomineedirectors. At present, the SMCs have toreport particulars of nominee andalternative nominee directors to theregistrar along with their consent to actas such. This mechanism is proposed tobe revamped for promoting the SMC

concept. An explicit provision regardingnominee of single member has beenproposed in the rules in place of anominee director. Also, a clarificationhas been made regarding nominee to bea natural person only. Further, througha provision, the role of nominee has beendefined in case of death of singlemember, by defining an elaboratesuccession mechanism.

Besides, these amendments also allowa body corporate to be a subscriber ofan SMC. Earlier, only natural personcould form an SMC. The amendmentsalso introduce the concept of “non-member” director for SMCs who hasbeen defined as a director nominated bya body corporate, government,institution or an authority, which is amember of the SMC.

The SMC Rules amendment notificationhas been vetted by the Law Ministry,and it has been published in the officialgazette. The draft amendments have alsobeen placed at the SECP web discussionf o r u m a t :http://forum.secp.gov.pk/forum.php toelicit public opinion. It is envisaged thatthe proposed amendments to the rulesshall not only simplify the regulatorymechanism, but also pave the wayt o w a r d s c o r p o r a t i z a t i o n a n ddocumentation of the SME sector.

SECP revising NBF sectorregulatory framework

Keeping in view the inherent risks in thepresent composition of financial sector,the Securi t ies and ExchangeCommission of Pakistan (SECP) is theprocess of revising the NBF sector toreform the entire financial sector.

Mr. Imtiaz Haider, the SECPCommissioner for Special izedCompanies Division, has said that theroadmap was rolled out in the form of areport in March 2013. In the said report,the SECP suggested to develop analternative financial system by way ofpromoting non-bank financial (NBF)sector to diversify the inherent systemicrisk and provide different asset classesto promote savings as well as meet thespecific needs of participants. Otherrecommendations included some macro-

Celebrating20th Year

of Excellence

18

News PIPFA JOURNAL

July - September 2013

level suggestions regarding taxationregime, encouraging long-term savingsand channeling these savings to under-served segments.

Mr. Imtiaz Haider further said that agood number of market professionals,industry participants and financialinstitutions provided comments on thereport. Moreover, some new ideas werealso received. The SECP has analyzedthe feedback given by the public on thesuggested reforms.